Embed Size (px)

Citation preview

• Administrative– Quiz #2 due today– Quiz #3 due Wednesday 2/18– Midterm 2 Monday 2/23

• Cash and Receivables (ch. 7)

AgendaAgenda

Cash & Cash Equivalents

• Cash: Currency and coins held, checks & money orders received, bank account balances

• Cash Equivalents are short-term, highly liquid investments that are:1. Readily convertible into known amounts of cash2. So near maturity that there is no risk of change in valuation from

fluctuating interest rates (original maturities of no longer than 3 months)

– E.G., T-bills, commercial paper, money market funds

Cash Equivalents – cash is grouped together with cash equivalents and reported as the most liquid current asset on the balance sheet

• Restricted Cash (i.e., cash restricted or “earmarked” for a specific purpose, such as a loan contract that requires the firm to maintain a certain cash balance) is disclosed as a long-term asset if it relates to long-term items (such as payment of L/T debt)

• Bank Overdraft – disclosed as a current liability unless there are other positive-balance cash accounts at the same bank that it can be netted against– IFRS vs. US GAAP

• US GAAP: Does NOT offset bank overdrafts against the cash account (unless cash available in another account in the same bank)

• IFRS: Includes bank overdrafts in cash and cash equivalents if repayable on demand and form a part of an entity’s cash management

Reporting of CashReporting of Cash

• Since cash is the most liquid asset, internal control of cash is imperative.• Controls must prevent unauthorized use of cash.• Management must have necessary information for proper use of cash. • Three Key Controls:

– Management oversight and authorization• Especially useful in small organizations where the owner can

monitor activities (and where there are limited resources to have separation of duties)

– Separation of duties: i.e., separate the responsibilities of physical control over cash and record keeping for cash

• E.g., have one employee prepare the deposit slip and make the entry, and another employee will actually make the deposit

– The bank reconciliation

Controls and CashControls and Cash

Accounts receivable – oral promises to pay for goods and services sold.

Receivable topics:• Trade and Cash Discounts• A/R valuation• Notes receivable – written promises to pay amount at a

specified future date. Arise from a variety of transactions (i.e. not just trade) and may be short-term or long-term

• A/R transfers

ReceivablesReceivables

• Trade Discounts – reduction in list price for differential volume

• Cash discounts – reduction in amount paid if paid within a specified period. Two accounting methods for recording cash discounts:

1. Gross method records discounts when taken by customers (most commonly used)

2. Net method records discounts not taken by customers.

Recognition of Accounts Recognition of Accounts ReceivableReceivable

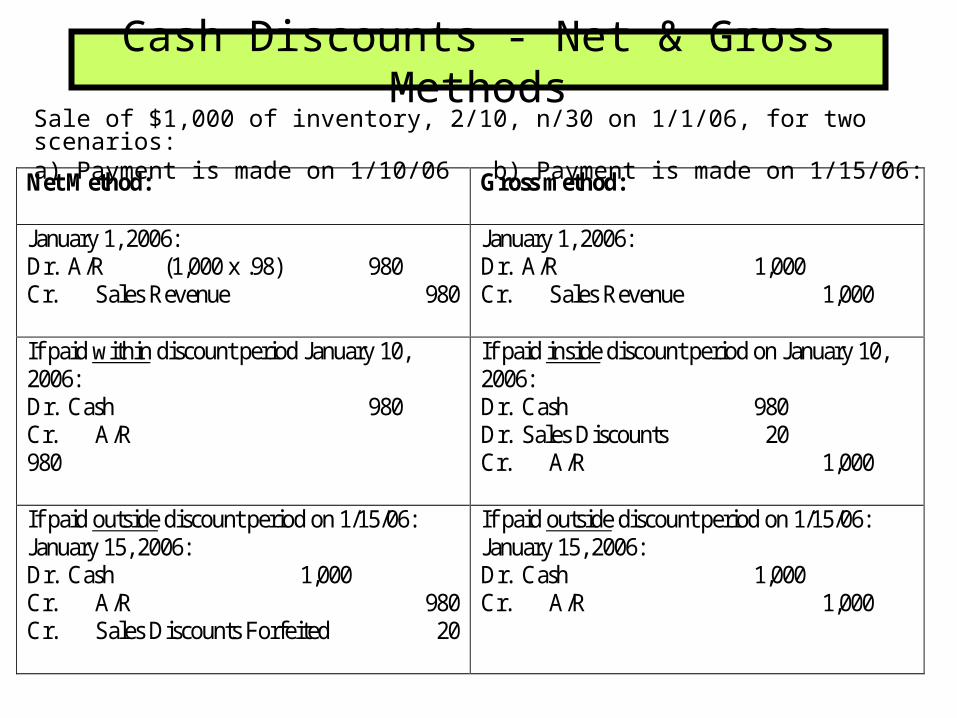

Cash Discounts - Net & Gross Methods

Sale of $1,000 of inventory, 2/10, n/30 on 1/1/06, for two scenarios: a) Payment is made on 1/10/06 b) Payment is made on 1/15/06:

Net Method:

Gross method:

January 1, 2006: Dr. A/R (1,000 x .98) 980 Cr. Sales Revenue 980

January 1, 2006: Dr. A/R 1,000 Cr. Sales Revenue 1,000

If paid within discount period January 10, 2006: Dr. Cash 980 Cr. A/R 980

If paid inside discount period on January 10, 2006: Dr. Cash 980 Dr. Sales Discounts 20 Cr. A/R 1,000

If paid outside discount period on 1/15/06: January 15, 2006: Dr. Cash 1,000 Cr. A/R 980 Cr. Sales Discounts Forfeited 20

If paid outside discount period on 1/15/06: January 15, 2006: Dr. Cash 1,000 Cr. A/R 1,000

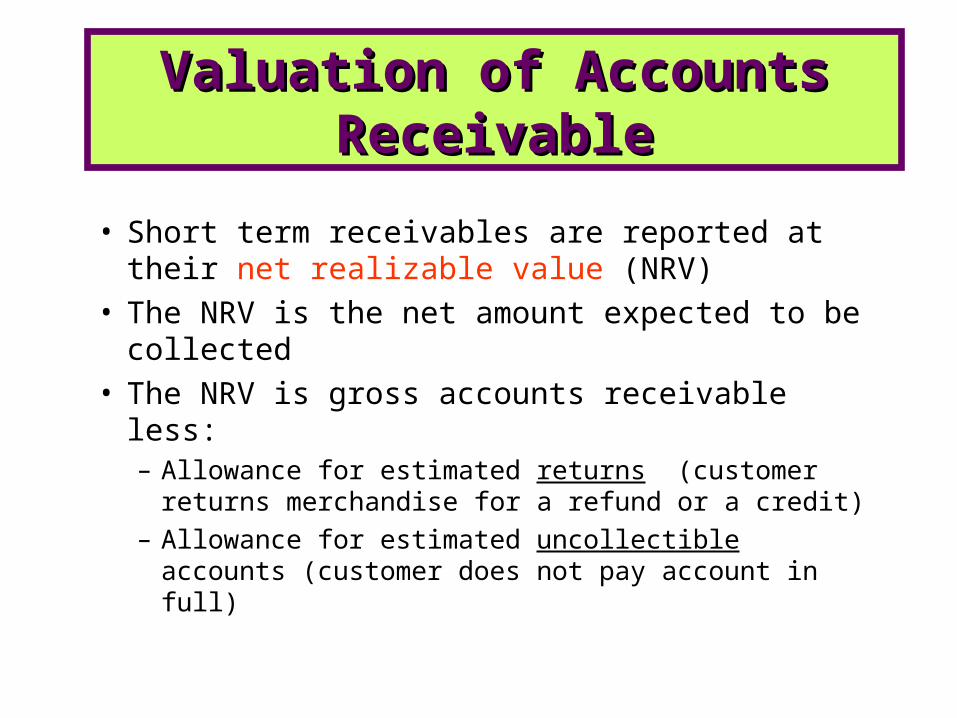

• Short term receivables are reported at their net realizable value (NRV)

• The NRV is the net amount expected to be collected

• The NRV is gross accounts receivable less:– Allowance for estimated returns (customer

returns merchandise for a refund or a credit)– Allowance for estimated uncollectible accounts

(customer does not pay account in full)

Valuation of Accounts Valuation of Accounts ReceivableReceivable

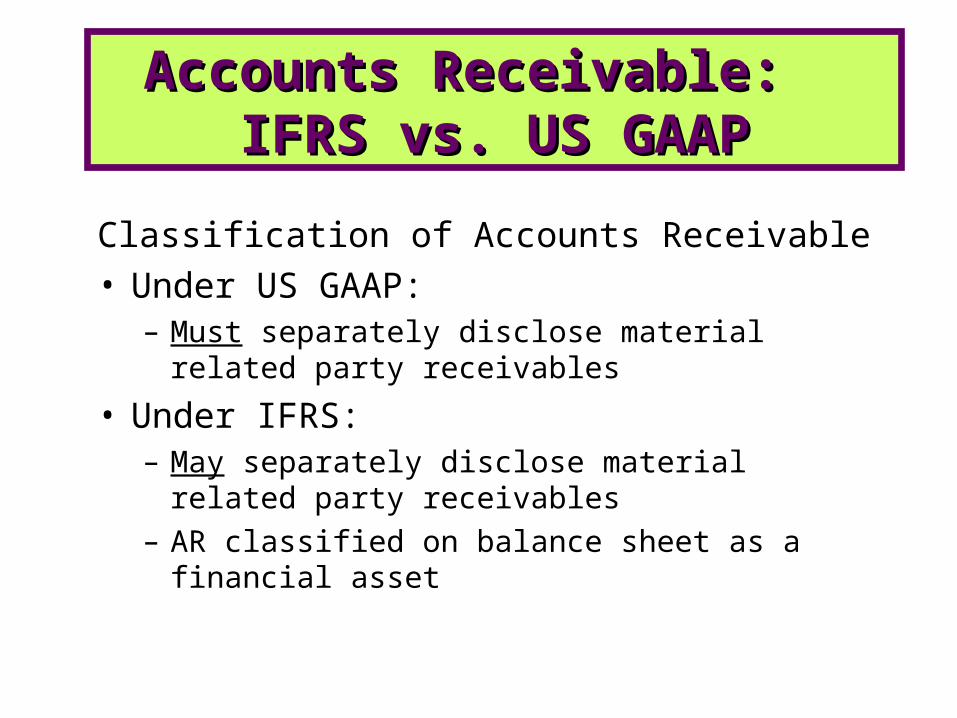

Classification of Accounts Receivable• Under US GAAP:

– Must separately disclose material related party receivables

• Under IFRS:– May separately disclose material related

party receivables– AR classified on balance sheet as a

financial asset

Accounts Receivable: Accounts Receivable: IFRS vs. US GAAPIFRS vs. US GAAP

Methods

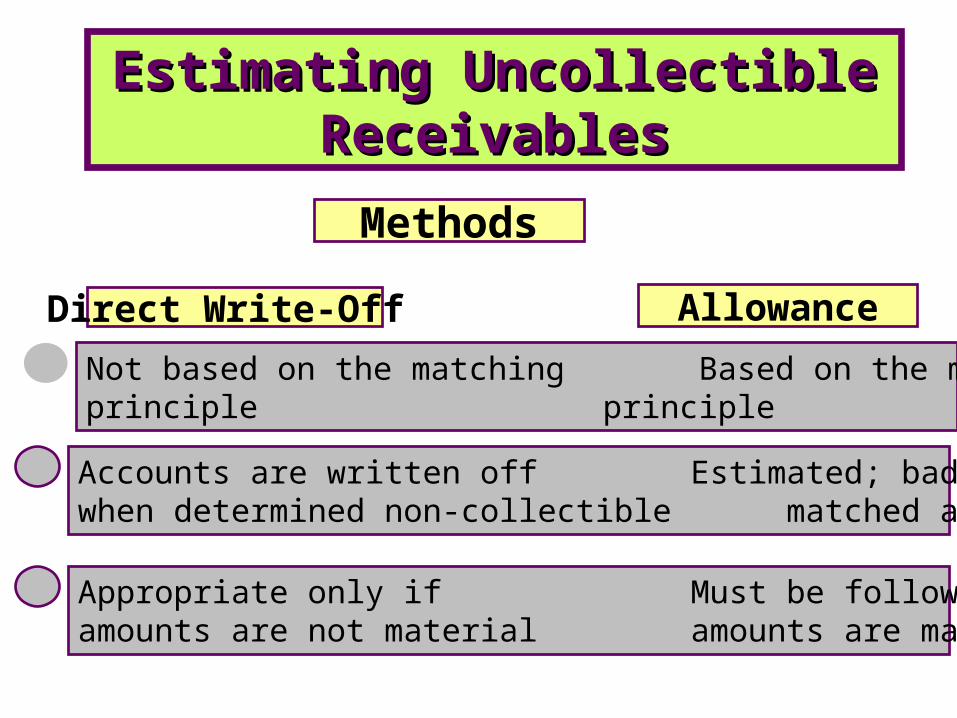

Direct Write-Off Allowance

Not based on the matching Based on the matchingprinciple principle

Appropriate only if Must be followed ifamounts are not material amounts are material

Accounts are written off Estimated; bad debts arewhen determined non-collectible matched against revenue

Estimating Uncollectible Estimating Uncollectible ReceivablesReceivables

Accounts Receivable

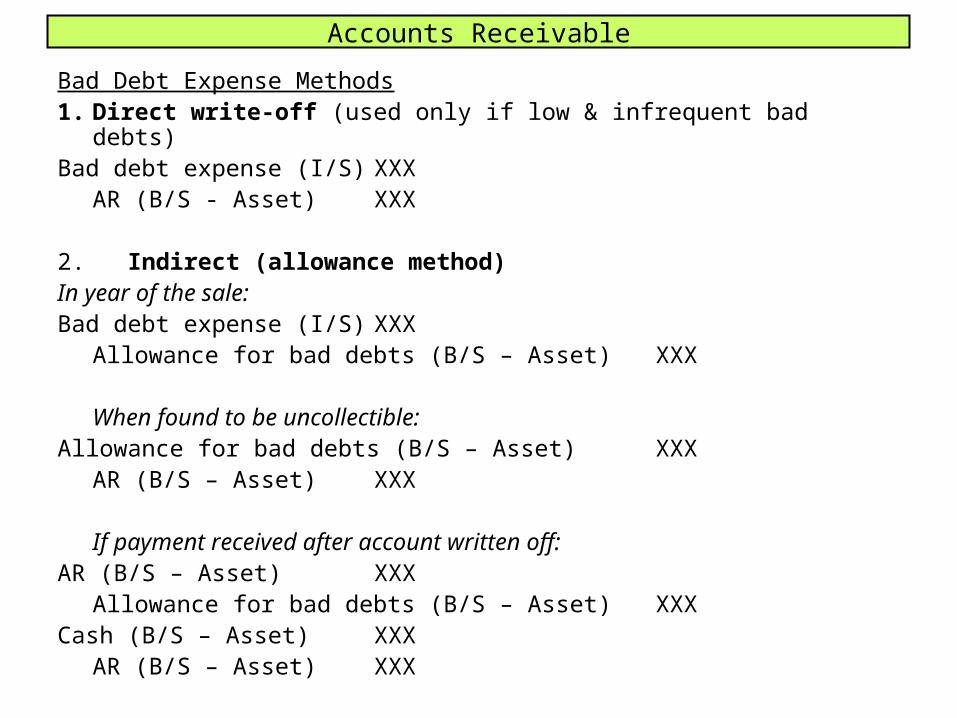

Bad Debt Expense Methods1. Direct write-off (used only if low & infrequent bad debts)Bad debt expense (I/S) XXX

AR (B/S - Asset) XXX

2. Indirect (allowance method)In year of the sale:Bad debt expense (I/S) XXX

Allowance for bad debts (B/S – Asset) XXX

When found to be uncollectible:Allowance for bad debts (B/S – Asset) XXX

AR (B/S – Asset) XXX

If payment received after account written off:AR (B/S – Asset) XXX

Allowance for bad debts (B/S – Asset) XXXCash (B/S – Asset) XXX

AR (B/S – Asset) XXX

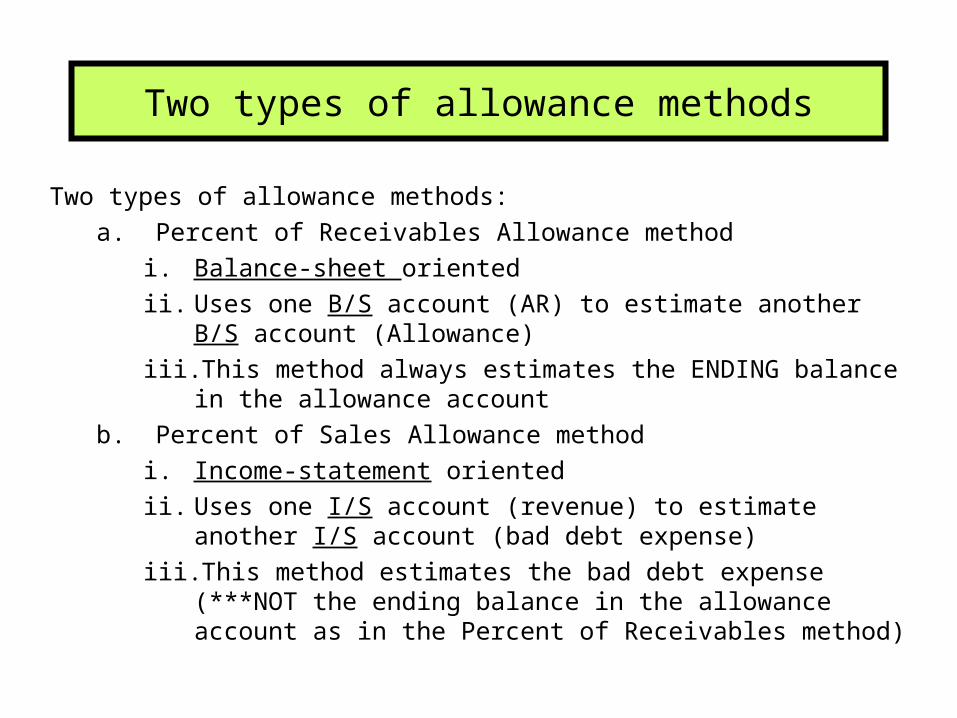

Two types of allowance methods

Two types of allowance methods:a. Percent of Receivables Allowance method

i. Balance-sheet orientedii. Uses one B/S account (AR) to estimate another B/S

account (Allowance)iii. This method always estimates the ENDING balance in

the allowance accountb. Percent of Sales Allowance method

i. Income-statement orientedii. Uses one I/S account (revenue) to estimate another I/S

account (bad debt expense)iii. This method estimates the bad debt expense (***NOT

the ending balance in the allowance account as in the Percent of Receivables method)

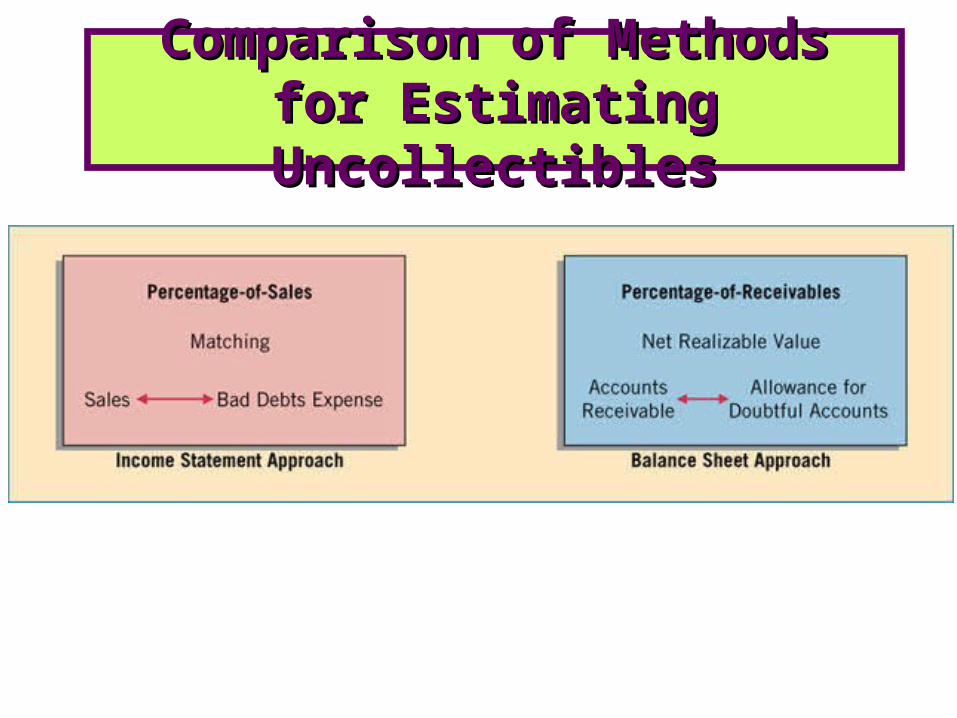

Comparison of Methods Comparison of Methods for Estimating for Estimating UncollectiblesUncollectibles

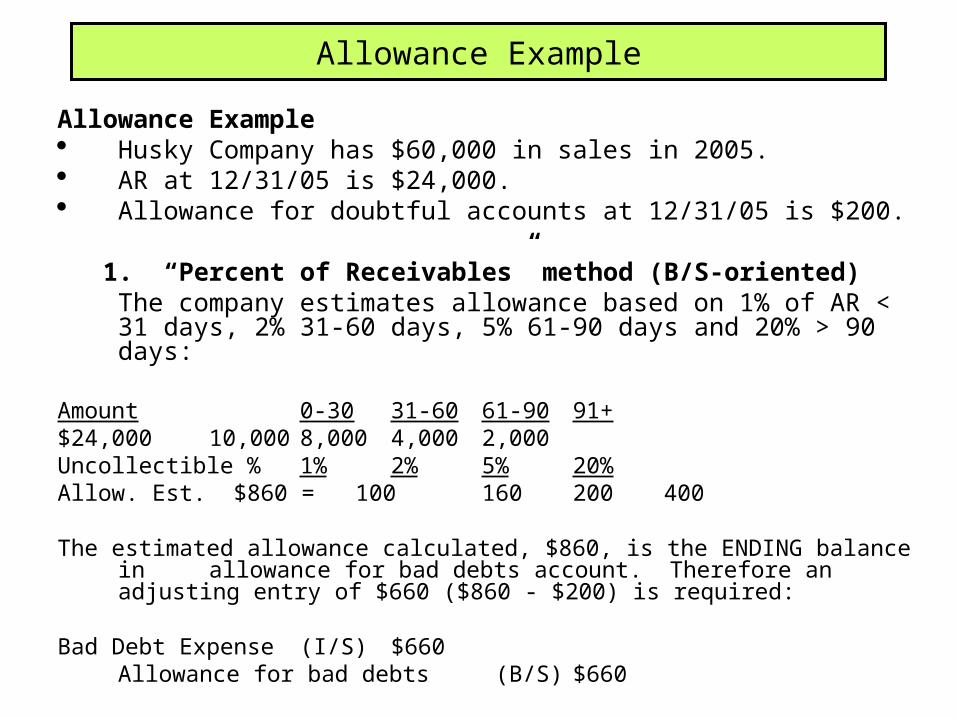

Allowance Example

Allowance Example Husky Company has $60,000 in sales in 2005. AR at 12/31/05 is $24,000. Allowance for doubtful accounts at 12/31/05 is $200.

1. “Percent of Receivables” method (B/S-oriented)The company estimates allowance based on 1% of AR

< 31 days, 2% 31-60 days, 5% 61-90 days and 20% > 90 days:

Amount 0-30 31-60 61-90 91+$24,000 10,000 8,000 4,000 2,000Uncollectible % 1% 2% 5% 20%Allow. Est. $860 = 100 160 200 400

The estimated allowance calculated, $860, is the ENDING balance in allowance for bad debts account. Therefore an adjusting

entry of $660 ($860 - $200) is required:

Bad Debt Expense (I/S) $660Allowance for bad debts (B/S) $660

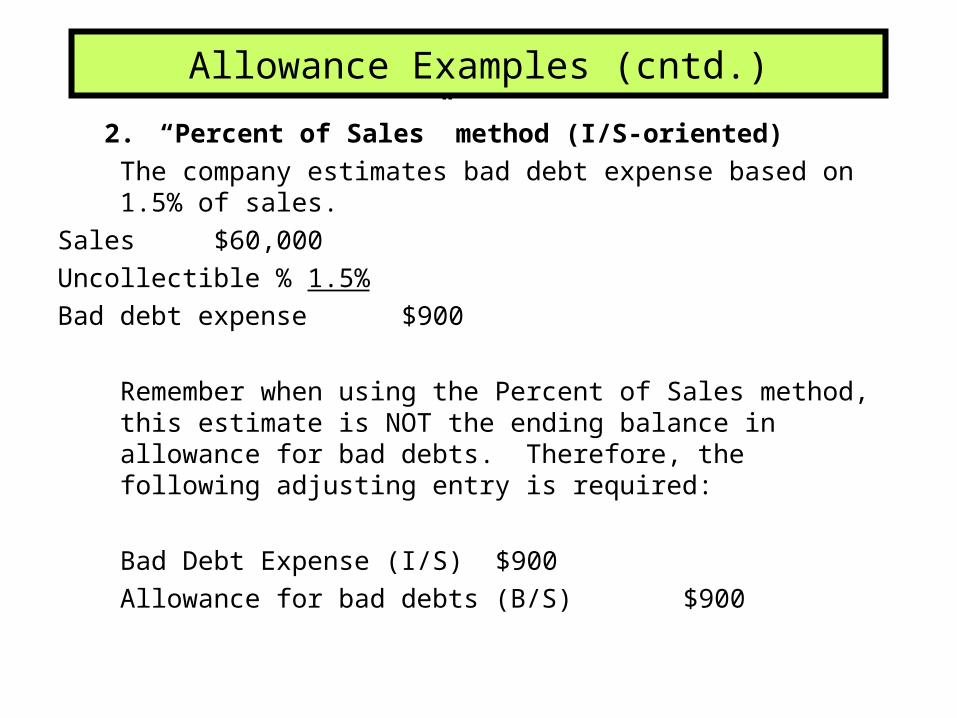

Allowance Examples (cntd.)

2. “Percent of Sales” method (I/S-oriented)The company estimates bad debt expense based on

1.5% of sales.Sales $60,000Uncollectible % 1.5%Bad debt expense $900

Remember when using the Percent of Sales method, this estimate is NOT the ending balance in allowance for bad debts. Therefore, the following adjusting entry is required:

Bad Debt Expense (I/S) $900Allowance for bad debts (B/S) $900

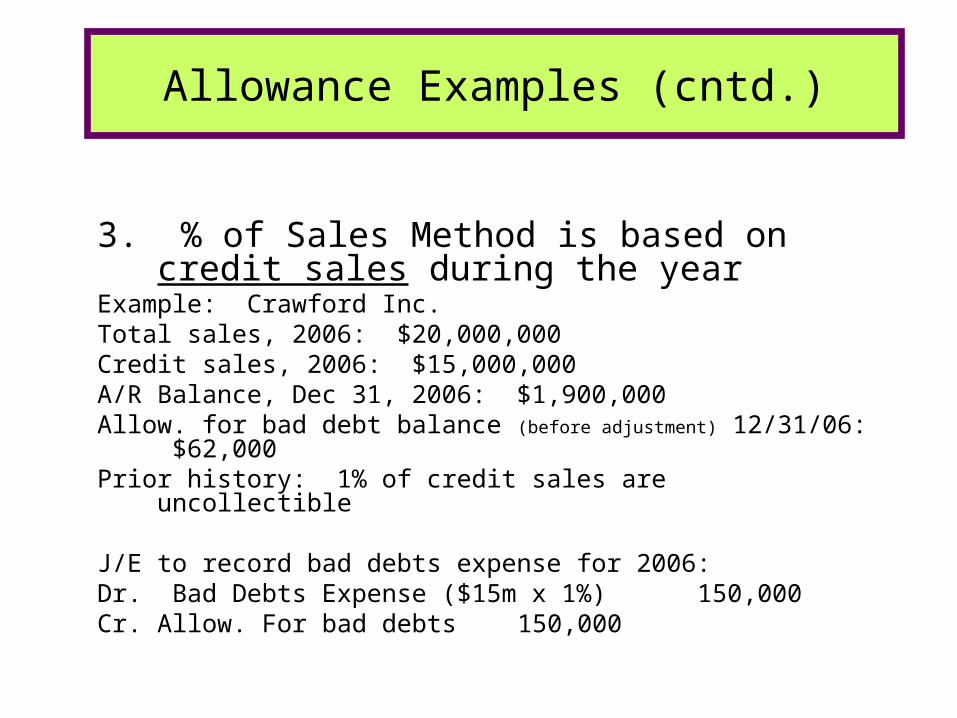

3. % of Sales Method is based on credit sales during the year

Example: Crawford Inc.Total sales, 2006: $20,000,000Credit sales, 2006: $15,000,000A/R Balance, Dec 31, 2006: $1,900,000Allow. for bad debt balance (before adjustment) 12/31/06:

$62,000Prior history: 1% of credit sales are uncollectible

J/E to record bad debts expense for 2006:Dr. Bad Debts Expense ($15m x 1%) 150,000Cr. Allow. For bad debts 150,000

Allowance Examples (cntd.)

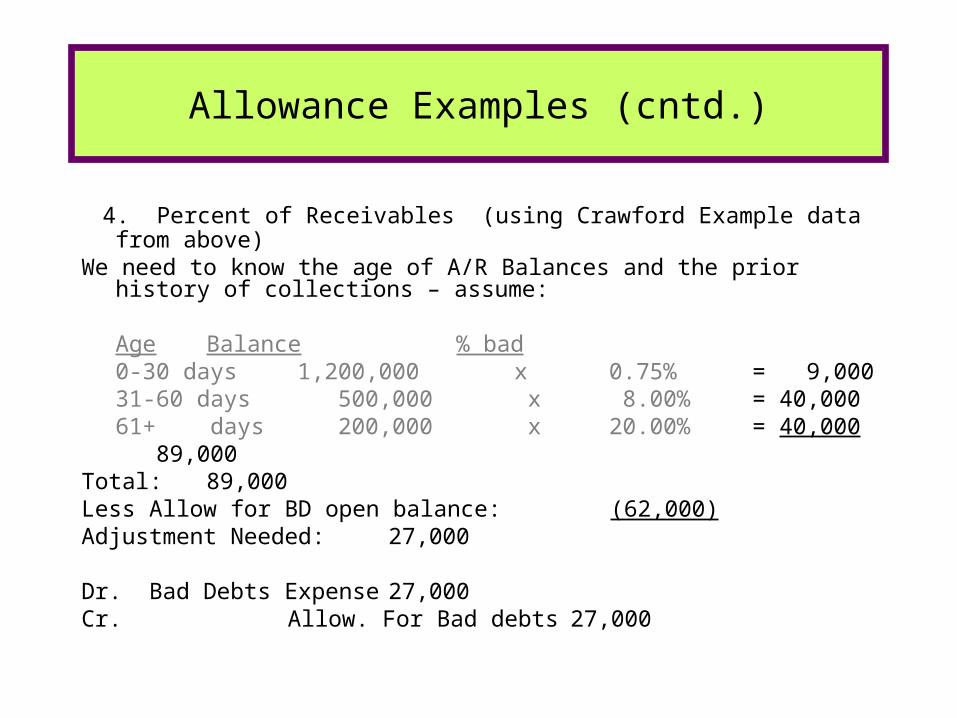

4. Percent of Receivables (using Crawford Example data from above)

We need to know the age of A/R Balances and the prior history of collections – assume: Age Balance % bad0-30 days 1,200,000 x 0.75% = 9,00031-60 days 500,000 x 8.00% = 40,00061+ days 200,000 x 20.00% = 40,000

89,000Total: 89,000Less Allow for BD open balance: (62,000)Adjustment Needed: 27,000

Dr. Bad Debts Expense 27,000Cr. Allow. For Bad debts 27,000

Allowance Examples (cntd.)

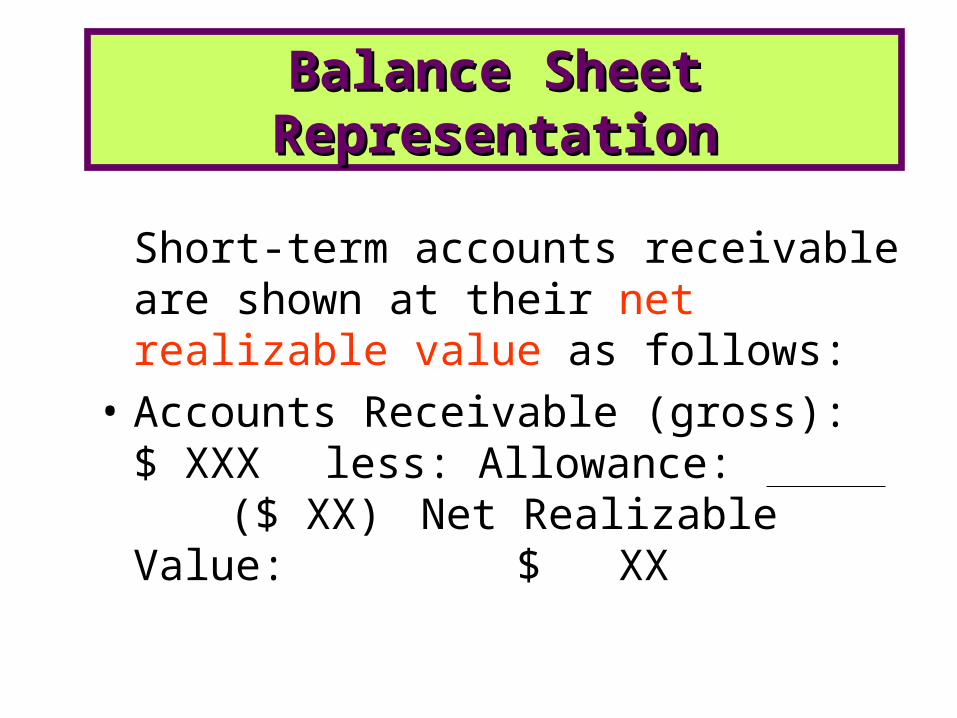

Short-term accounts receivable are shown at their net realizable value as follows:

• Accounts Receivable (gross): $ XXX less: Allowance: ($ XX) Net Realizable Value: $ XX

Balance Sheet Balance Sheet RepresentationRepresentation

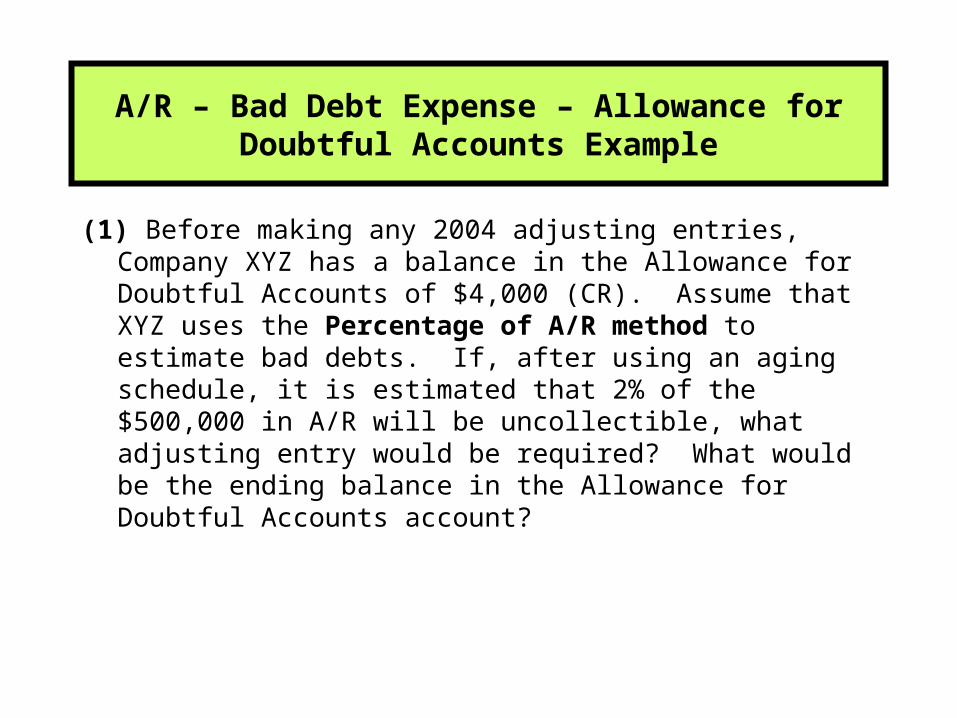

A/R – Bad Debt Expense – Allowance for Doubtful Accounts Example

(1) Before making any 2004 adjusting entries, Company XYZ has a balance in the Allowance for Doubtful Accounts of $4,000 (CR). Assume that XYZ uses the Percentage of A/R method to estimate bad debts. If, after using an aging schedule, it is estimated that 2% of the $500,000 in A/R will be uncollectible, what adjusting entry would be required? What would be the ending balance in the Allowance for Doubtful Accounts account?

A/R – Bad Debt Expense – Allowance for Doubtful Accounts Example

(2) Before making any 2004 adjusting entries, Company XYZ has a balance in the Allowance for Doubtful Accounts of $4,000 (CR). Assume that XYZ uses the Percentage of Sales method to estimate bad debts. If XYZ estimates that 5% of total credit sales for 2004 will ultimately prove uncollectible, what adjusting entry would be required if credit sales for 2004 totaled $100,000? What would be the ending balance in the Allowance for Doubtful Accounts account?

A/R – Bad Debt Expense – Allowance for Doubtful Accounts Example

(3) At the beginning of 2004, the balance in the Allowance account was $11,000 (CR). During the year, $8,000 of delinquent accounts were written off. Then, $2,000 of these delinquent accounts was ultimately determined to be collectible, and these accounts were collected. Additionally, the 2004 ending balance in A/R was $150,000. If XYZ uses the Percentage of A/R method to estimate bad debts, and 5% of A/R is estimated to be uncollectible, what adjusting entry would be made to account for the bad debts? What would be the ending balance in the

Allowance for Doubtful Accounts account?

A/R – Bad Debt Expense – Allowance for Doubtful Accounts Example

(4) At the beginning of 2004, the balance in the Allowance account was $11,000 (CR). During the year, $8,000 of delinquent accounts was written off. Then, $2,000 of these delinquent accounts was ultimately determined to be collectible, and these accounts were collected. Additionally, assume that total credit sales for the year were $200,000. If XYZ uses the Percentage of Sales method to estimate bad debts, and 5% of credit sales are estimated to be uncollectible, what adjusting entry would be made to account for the bad debts? What would be the ending balance in the Allowance for Doubtful Accounts account?

NR are written promises that will receive certain sum(s) of money at specified future date(s)

• Record NR at the PV of future cash flows using the effective interest rate– Notes receivable are issued at face value when the stated rate of interest is

the same as the effective (market) rate.– If the stated rate is less than the effective rate then a discount results.– If the stated rate is greater than the effective rate then a premium results.– The discount or premium is amortized to interest revenue by the effective

interest method.

• Record interest revenue each period using the effective interest method

Recognition of Notes Recognition of Notes ReceivableReceivable

Issues NOT at face value

Non-interest bearing Interest bearing

1. Determine issue price on notes receivable at implicit rate of interest2. The discount/premium is amortized to interest revenue by the effective interest method

1. Determine issue price on notes receivable at the effective rate of interest.2. The discount/premium is amortized to interest revenue by the effective interest method

Recognition of Notes Recognition of Notes ReceivableReceivable

Club Soda Inc. purchases a machine from Fruit Juice Ltd. with a list price of $10,000 on January 1, 2006, and Club Soda accepts, in return, a note for $10,000, non-interest bearing, due on December 31, 2007. The fair value of the machine on January 1 is $7,972.

Prepare journal entries to record the Fruit Juice’s sale, any adjusting entries, and the entry to record the payment on December 31, 2007.

Notes Receivable – Non-Interest Notes Receivable – Non-Interest BearingBearing

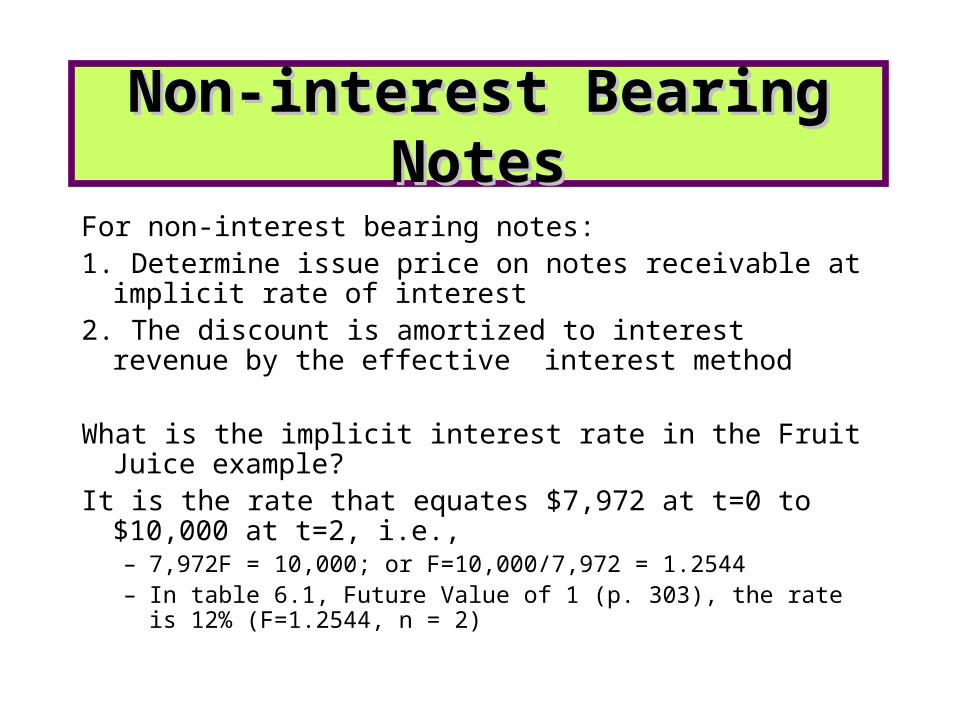

For non-interest bearing notes:1. Determine issue price on notes receivable at implicit rate

of interest2. The discount is amortized to interest revenue by the

effective interest method

What is the implicit interest rate in the Fruit Juice example?It is the rate that equates $7,972 at t=0 to $10,000 at t=2, i.e.,

– 7,972F = 10,000; or F=10,000/7,972 = 1.2544– In table 6.1, Future Value of 1 (p. 303), the rate is 12% (F=1.2544,

n = 2)

Non-interest Bearing Non-interest Bearing NotesNotes

Non-interest Bearing Non-interest Bearing NotesNotes

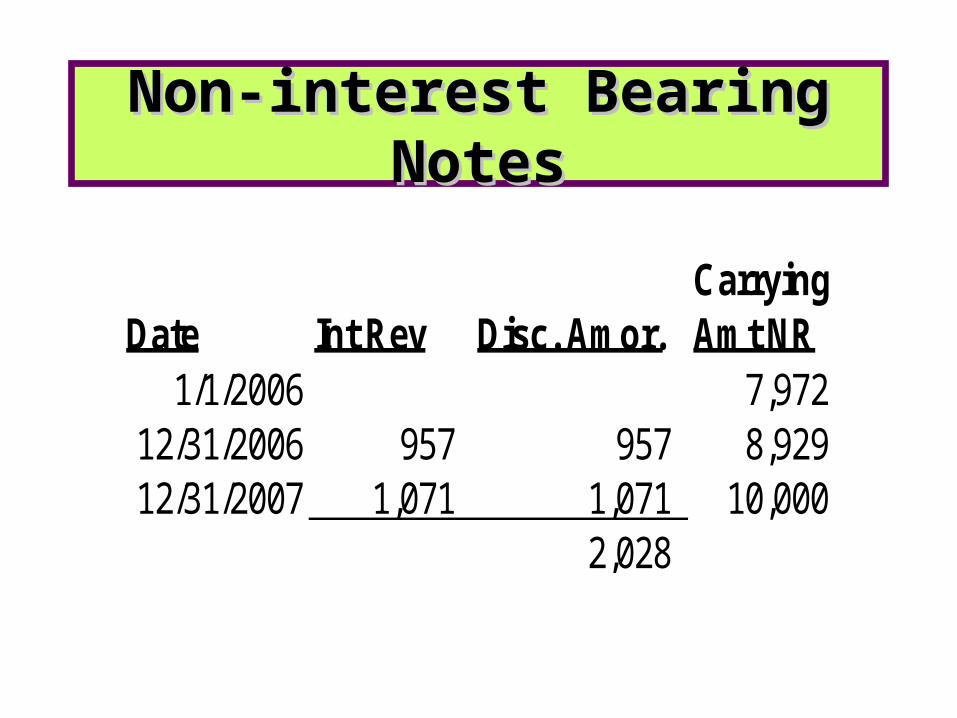

Carrying Date Int Rev Disc. Amor. Amt NR

1/1/2006 7,972 12/31/2006 957 957 8,929 12/31/2007 1,071 1,071 10,000

2,028

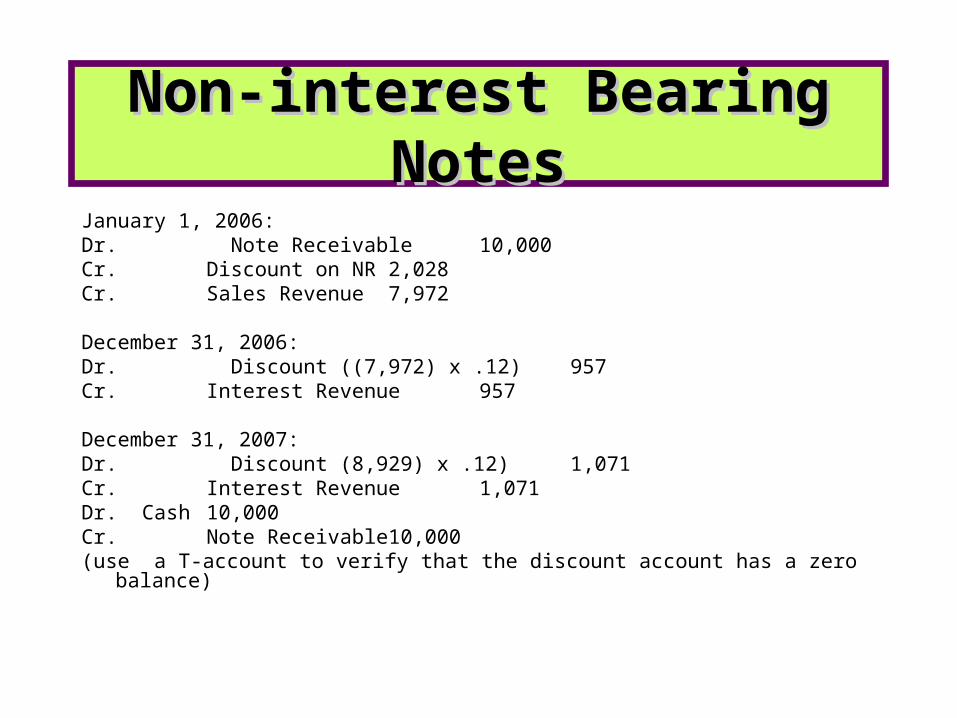

January 1, 2006:Dr. Note Receivable 10,000Cr. Discount on NR 2,028Cr. Sales Revenue 7,972

December 31, 2006:Dr. Discount ((7,972) x .12) 957Cr. Interest Revenue 957

December 31, 2007:Dr. Discount (8,929) x .12) 1,071Cr. Interest Revenue 1,071Dr. Cash 10,000Cr. Note Receivable 10,000(use a T-account to verify that the discount account has a zero balance)

Non-interest Bearing Non-interest Bearing NotesNotes

• The non-interest bearing example is a special case of the situation where the stated interest rate is different from the market rate

• What if an interest rate is given, but the market rate is different?

Notes Where Stated Rate Notes Where Stated Rate is Different from Market is Different from Market

RateRate

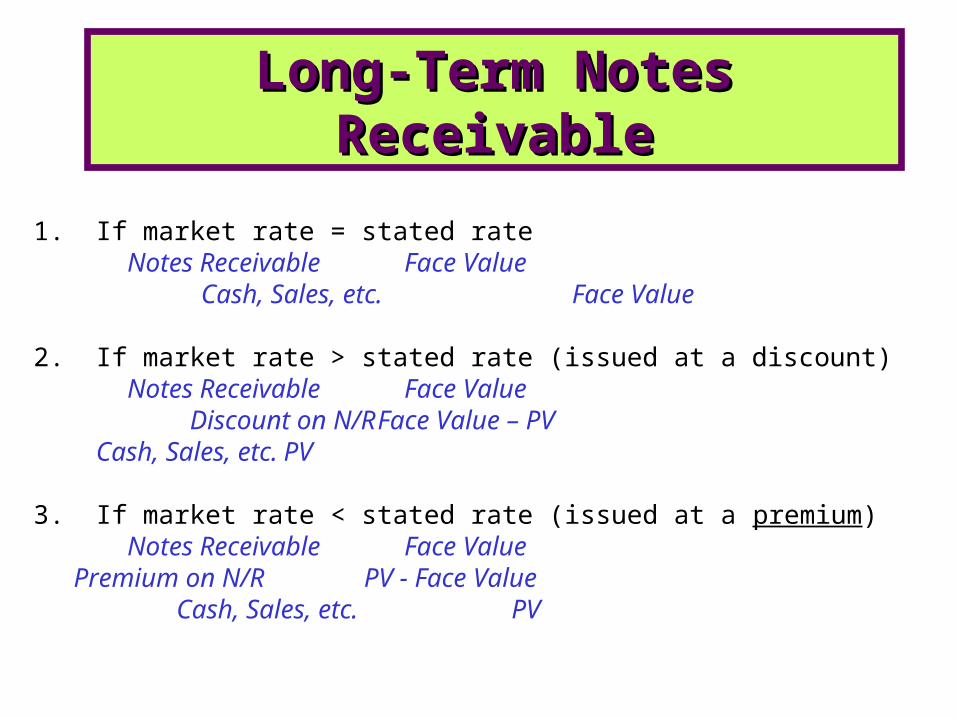

1. If market rate = stated rate Notes Receivable Face Value Cash, Sales, etc. Face Value

2. If market rate > stated rate (issued at a discount) Notes Receivable Face Value

Discount on N/R Face Value – PVCash, Sales, etc. PV

3. If market rate < stated rate (issued at a premium) Notes Receivable Face Value Premium on N/R PV - Face Value

Cash, Sales, etc. PV

Long-Term Notes Long-Term Notes ReceivableReceivable

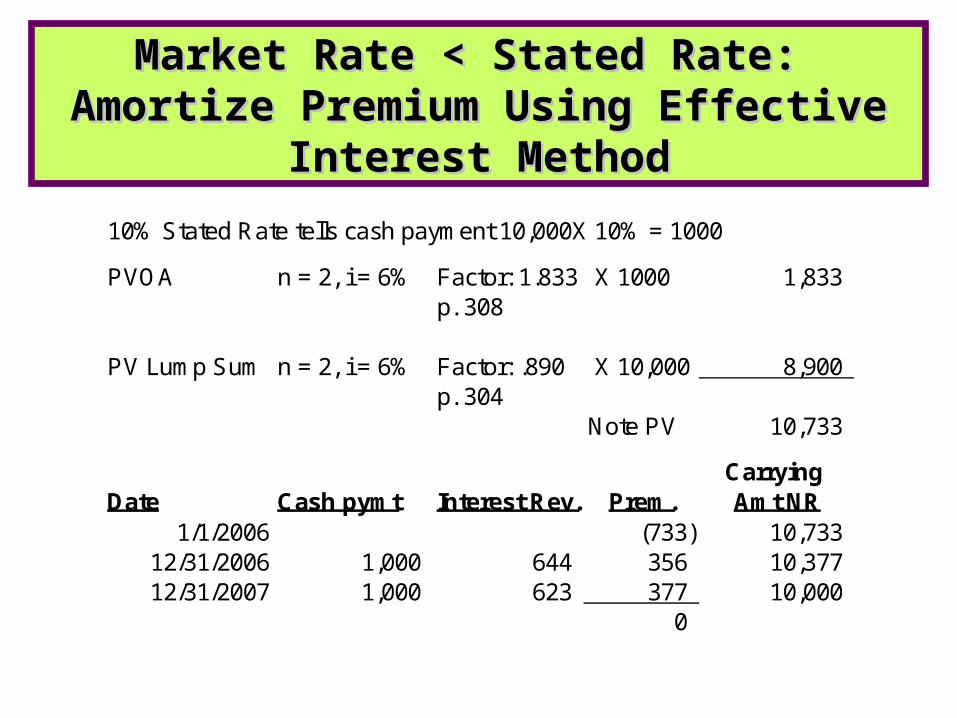

Assume the data in the non-interest bearing note example, but now the note pays interest at 10% (stated rate) and the appropriate market rate for Fruit Juice Ltd. is 6%. Here the market rate < the stated rate, so there will be a premium.

Determine PV of this note:• 1st: calculate the PV of the Annuity: (10,000 x

10%) = 1,000 for 2 years at 6%: 1,000 x 1.833 = 1,833[PV of an Annuity, Table 6-4, p. 308 (n=2; i = market 6%)]

• 2nd: calculate the PV of the principal payment in 2 years: 10,000 x .8900 = 8,900[PV of 1, Table 6-2, p. 304 (n = 2; i = market 6%)]

• So PV of note on January 1, 2006 is 10,733 (1833 + 8900) (i.e., a premium)

Example where Stated Rate and Example where Stated Rate and Market Rate DifferMarket Rate Differ

Market Rate < Stated Rate: Market Rate < Stated Rate: Amortize Premium Using Effective Amortize Premium Using Effective

Interest MethodInterest Method

10% Stated Rate tells cash payment 10,000X 10% = 1000

PVOA n = 2, i = 6% Factor: 1.833 X 1000 1,833 p. 308

PV Lump Sum n = 2, i = 6% Factor: .890 X 10,000 8,900 p. 304

Note PV 10,733

Carrying Date Cash pymt Interest Rev. Prem. Amt NR

1/1/2006 (733) 10,733 12/31/2006 1,000 644 356 10,377 12/31/2007 1,000 623 377 10,000

0

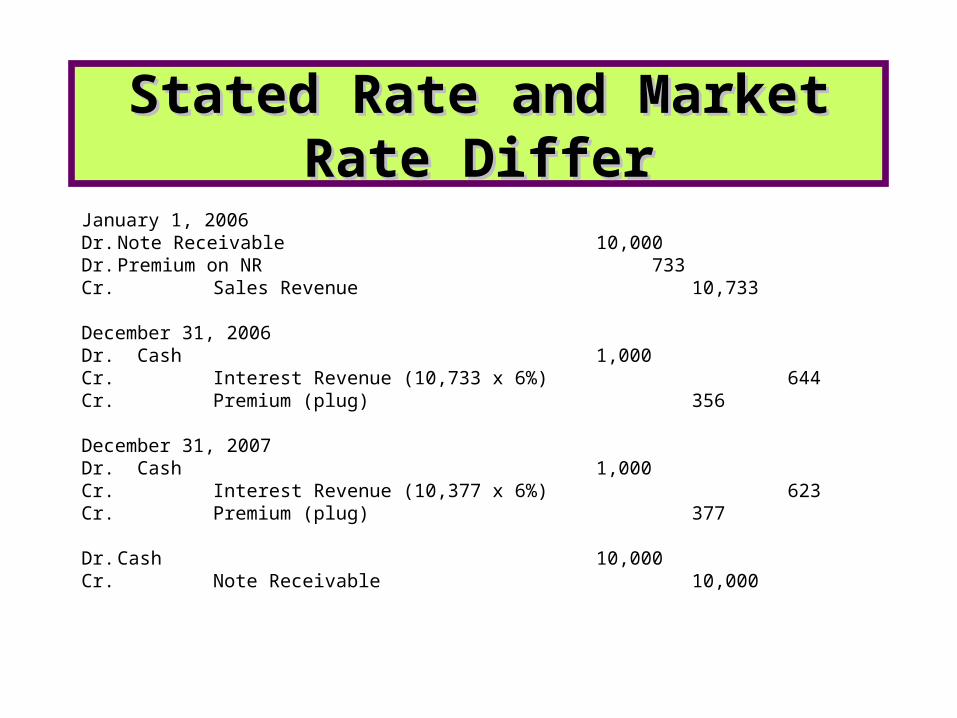

January 1, 2006Dr. Note Receivable 10,000Dr. Premium on NR 733Cr. Sales Revenue 10,733

December 31, 2006Dr. Cash 1,000Cr. Interest Revenue (10,733 x 6%) 644Cr. Premium (plug) 356

December 31, 2007Dr. Cash 1,000Cr. Interest Revenue (10,377 x 6%) 623Cr. Premium (plug) 377

Dr. Cash 10,000Cr. Note Receivable 10,000

Stated Rate and Market Stated Rate and Market Rate DifferRate Differ

• The holder of accounts or notes receivable may transfer them for cash.

• The transfer may be either:1. A secured borrowing (i.e., the “seller” is

really borrowing from the transferee)– The original holder retains ownership of

receivables in a secured borrowing transaction.

2. A sale of receivables– Holder transfers ownership of receivables

in a sale (transfers risks of collection).

Disposition of Accounts Disposition of Accounts and Notes Receivableand Notes Receivable

• Overall - Receivables remain on the books of the company borrowing money (i.e. – no sale) (and continue to treat A/R as usual (collections, write-off, etc.)

• Transferor:– Records liability– Records a finance charge.– Collects accounts receivable.– Records sales returns and sales discounts.– Absorbs bad debts expense.– Records interest expense on notes payable.– Pays on the note periodically from collections.

Secured Borrowing – the Secured Borrowing – the BasicsBasics

• Factor records the (transferred) accounts as assets in its books.

• Transferor:– Transfers ownership of receivables to factor.– Records any amount retained by transferee as “due

from factor.”• This is an amount held back to protect the transferee

in case of non-payment by customer– Records loss on sale of receivables.– Records any component liability (when appropriate

– i.e. if the sale is on a “with recourse” basis) • i.e., any estimated future liability that the transferor

will need to pay if customers do not pay (and if the amount held back by the factor is insufficient)

SaleSale of Receivables – the of Receivables – the BasicsBasics

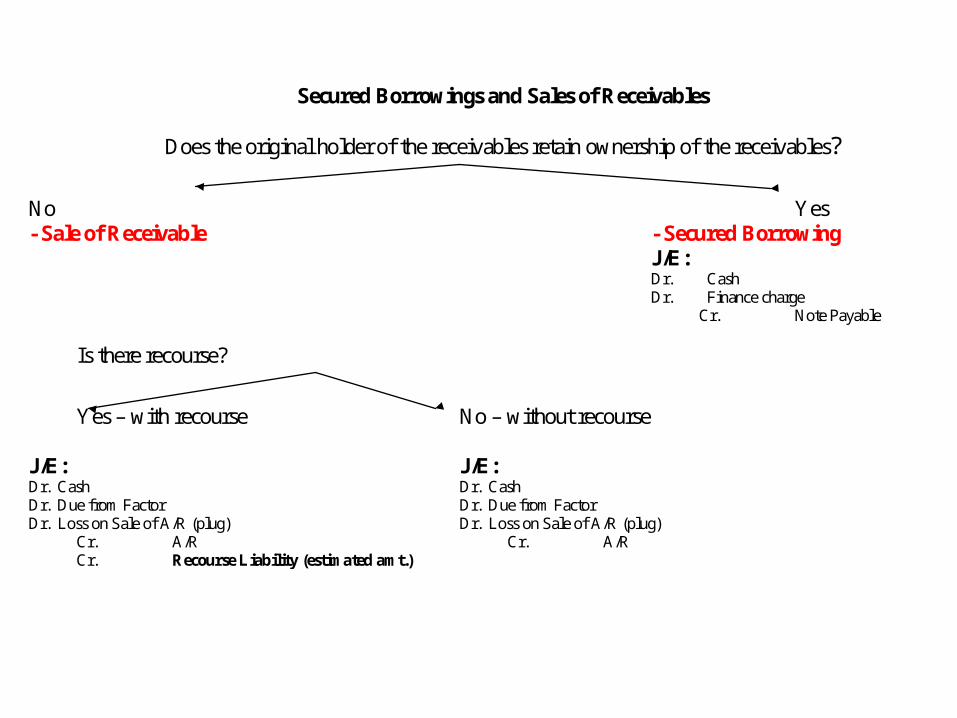

Secured Borrowings and Sales of Receivables

Does the original holder of the receivables retain ownership of the receivables?

No Yes - Sale of Receivable - Secured Borrowing J/E: Dr. Cash Dr. Finance charge Cr. Note Payable

Is there recourse?

Yes – with recourse No – without recourse J/E: J/E: Dr. Cash Dr. Cash Dr. Due from Factor Dr. Due from Factor Dr. Loss on Sale of A/R (plug) Dr. Loss on Sale of A/R (plug)

Cr. A/R Cr. A/R Cr. Recourse Liability (estimated amt.)

Transferred Assets Isolated from Transferor

Isolated = put beyond the reach of transferor– So the transferor no longer has any rights over the A/R

– This includes creditors of the transferor, if it goes bankrupt

• This is not different from any other type of sale– If you “buy” a car from a dealership but must return the

car if the dealership wants, and must turn the car over to the dealership’s creditors if it goes bankrupt, then you really don’t own it.

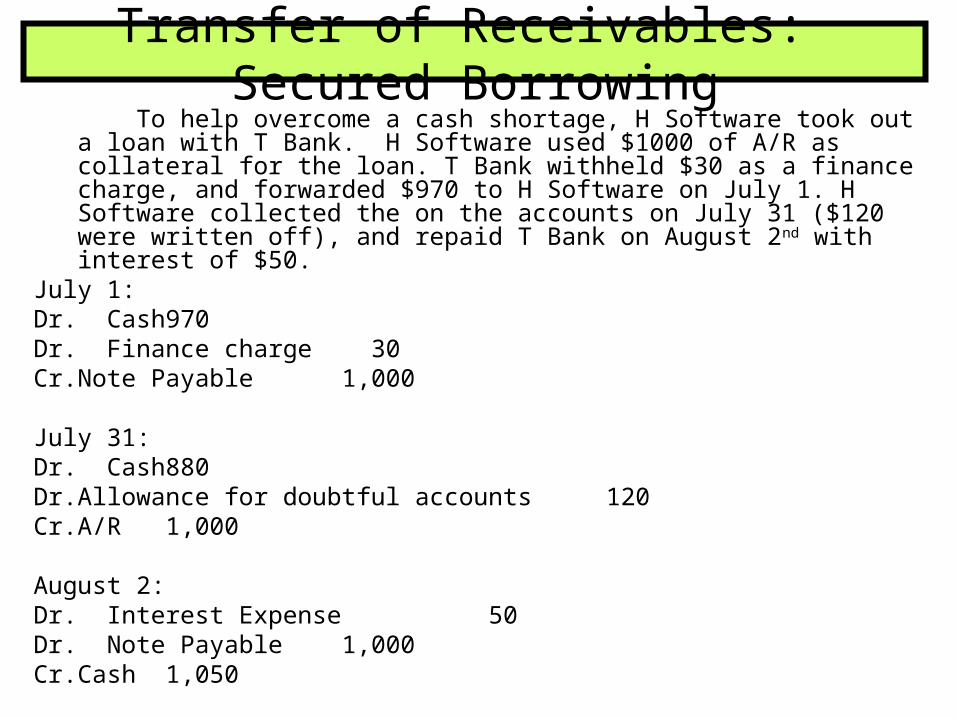

Transfer of Receivables: Secured Borrowing

To help overcome a cash shortage, H Software took out a loan with T Bank. H Software used $1000 of A/R as collateral for the loan. T Bank withheld $30 as a finance charge, and forwarded $970 to H Software on July 1. H Software collected the on the accounts on July 31 ($120 were written off), and repaid T Bank on August 2nd with interest of $50.

July 1:Dr. Cash 970Dr. Finance charge 30Cr. Note Payable 1,000

July 31:Dr. Cash 880Dr. Allowance for doubtful accounts 120Cr. A/R 1,000

August 2:Dr. Interest Expense 50Dr. Note Payable 1,000Cr. Cash 1,050

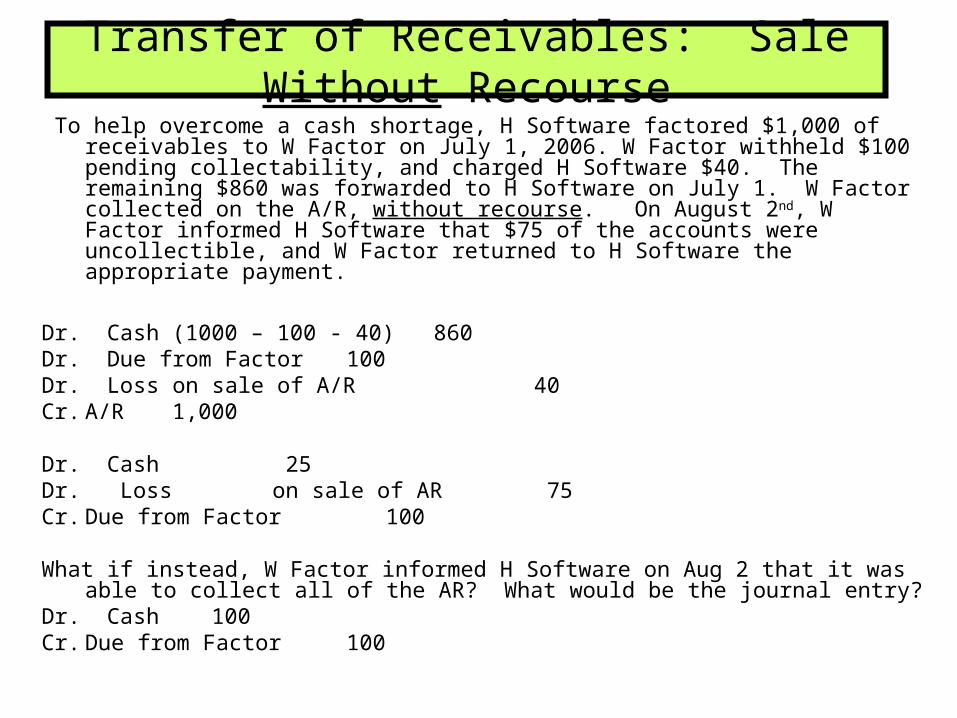

Transfer of Receivables: Sale Without Recourse

To help overcome a cash shortage, H Software factored $1,000 of receivables to W Factor on July 1, 2006. W Factor withheld $100 pending collectability, and charged H Software $40. The remaining $860 was forwarded to H Software on July 1. W Factor collected on the A/R, without recourse. On August 2nd, W Factor informed H Software that $75 of the accounts were uncollectible, and W Factor returned to H Software the appropriate payment.

Dr. Cash (1000 – 100 - 40) 860Dr. Due from Factor 100Dr. Loss on sale of A/R 40Cr. A/R 1,000

Dr. Cash 25Dr. Loss on sale of AR 75Cr. Due from Factor 100

What if instead, W Factor informed H Software on Aug 2 that it was able to collect all of the AR? What would be the journal entry?

Dr. Cash 100Cr. Due from Factor 100

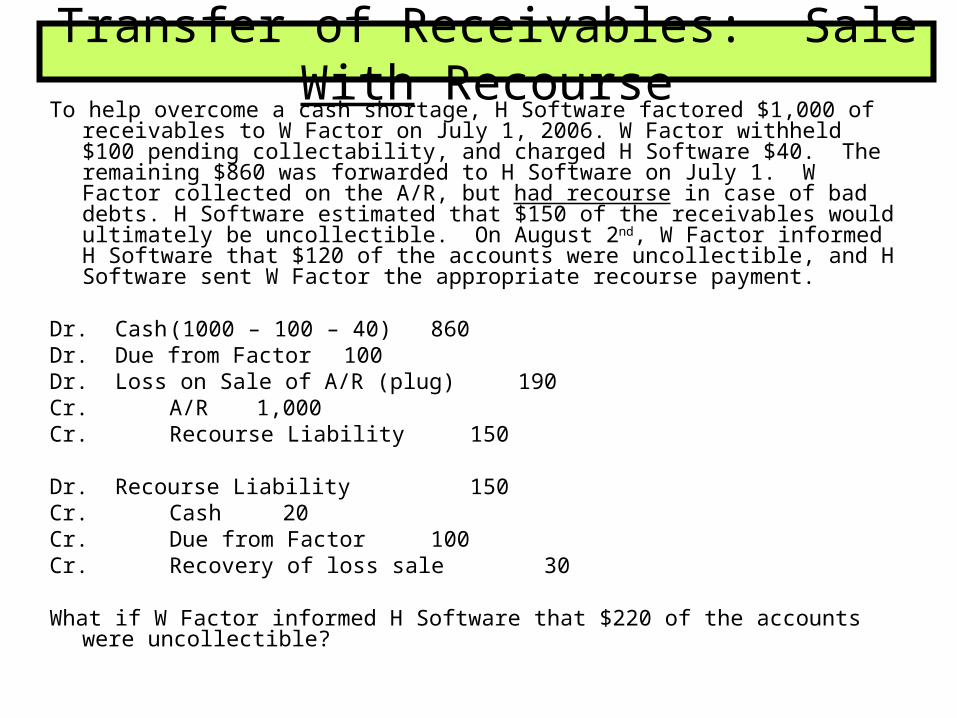

Transfer of Receivables: Sale With Recourse

To help overcome a cash shortage, H Software factored $1,000 of receivables to W Factor on July 1, 2006. W Factor withheld $100 pending collectability, and charged H Software $40. The remaining $860 was forwarded to H Software on July 1. W Factor collected on the A/R, but had recourse in case of bad debts. H Software estimated that $150 of the receivables would ultimately be uncollectible. On August 2nd, W Factor informed H Software that $120 of the accounts were uncollectible, and H Software sent W Factor the appropriate recourse payment.

Dr. Cash (1000 – 100 – 40) 860Dr. Due from Factor 100Dr. Loss on Sale of A/R (plug) 190Cr. A/R 1,000Cr. Recourse Liability 150

Dr. Recourse Liability 150Cr. Cash 20Cr. Due from Factor 100Cr. Recovery of loss sale 30

What if W Factor informed H Software that $220 of the accounts were uncollectible?