Embed Size (px)

Citation preview

Chapter 1: Estimation TheoryAdvanced Econometrics - HEC Lausanne

Christophe Hurlin

University of Orléans

November 20, 2013

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 1 / 147

Section 1

Introduction

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 2 / 147

1. Introduction

Estimation problem

Let us consider a continuous random variable Y characterized by amarginal probability density function fY (y ; θ) for y 2 R and θ 2 Θ.The parameter θ is unknown.

Let fY1, ..,YNg a random sample of i .i .d . random variables that havethe same distribution as Y .

We have one realisation fy1, .., yNg of this sample.

How to estimate the parameter θ?

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 3 / 147

1. Introduction

Remarks

1 The estimation problem can be extended to the case of aneconometric model. In this case we consider two variables Y and Xand a conditional pdf fY jX=x (y ; θ) that depends on a parameter or avector of unknown parameters θ.

2 In this chapter, we dont derive the estimators (for the estimationmethods, see next chapters). We admit that we have an estimator bθfor θ whatever the estimation method used and we study its nitesample and large sample properties.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 4 / 147

1. Introduction

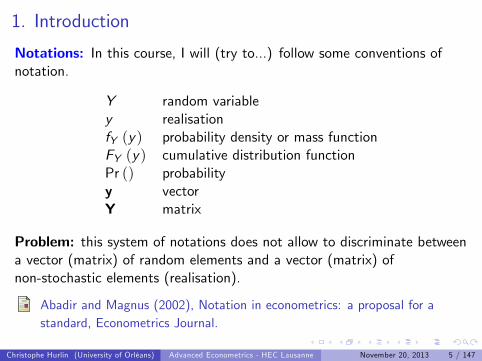

Notations: In this course, I will (try to...) follow some conventions ofnotation.

Y random variabley realisationfY (y) probability density or mass functionFY (y) cumulative distribution functionPr () probabilityy vectorY matrix

Problem: this system of notations does not allow to discriminate betweena vector (matrix) of random elements and a vector (matrix) ofnon-stochastic elements (realisation).

Abadir and Magnus (2002), Notation in econometrics: a proposal for astandard, Econometrics Journal.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 5 / 147

1. Introduction

The outline of this chapter is the following:

Section 2: What is an estimator?

Section 3: Finite sample properties

Section 4: Large sample properties

Subsection 4.1: Almost sure convergence

Subsection 4.2: Convergence in probability

Subsection 4.3: Convergence in mean square

Subsection 4.4: Convergence in distribution

Subsection 4.5: Asymptotic distributions

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 6 / 147

Section 2

What is an Estimator?

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 7 / 147

2. What is an Estimator?

Objectives

1 Dene the concept of estimator.

2 Dene the concept of estimate.

3 Sampling distribution.

4 Discussion about the notion of "good "estimator.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 8 / 147

2. What is an Estimator?

Denition (Point estimator)

A point estimator is any function T (Y1,Y2, ..,YN ) of a sample. Anystatistic is a point estimator.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 9 / 147

What is an estimator?

Example (Sample mean)

Assume that Y1,Y2, ..,YN are i .i .d . Nm, σ2

random variables. The

sample mean (or average)

Y N =1N

N

∑i=1Yi

is a point estimator (or an estimator) of m.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 10 / 147

2. What is an Estimator?

Example (Sample variance)

Assume that Y1,Y2, ..,YN are i .i .d . Nm, σ2

random variables. The

sample variance

S2N =1

N 1N

∑i=1

Yi Y N

2is a point estimator (or an estimator) of σ2.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 11 / 147

2. What is an Estimator?

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 12 / 147

2. What is an Estimator?

Fact

An estimator bθ is a random variable.

Consequence: bθ has a (marginal or conditional) probability distribution.This sampling distribution is caracterized by a probability densityfunction (pdf) fbθ (u)

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 13 / 147

2. What is an Estimator?

Denition (Sampling Distribution)

The probability distribution of an estimator (or a statistic) is called thesampling distribution.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 14 / 147

2. What is an Estimator?

Fact

An estimator bθ is a random variable.

Consequence: The sampling distribution of bθ is caracterized bymoments such that the expectation E

bθ , the variance Vbθ and more

generally the k th central moment dened by:

E

bθ Ebθk = Z

u µbθk fbθ (u) du 8k 2 N

µbθ = Ebθ = Z

u fbθ (u) du

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 15 / 147

2. What is an Estimator?

Denition (Point estimate)

A (point) estimateis the realized value of an estimator (i.e. a number)that is obtained when a sample is actually taken. For an estimator bθ it canbe denoted by bθ (y) .

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 16 / 147

2. What is an Estimator?

Example (Point estimate)For instance yN is an estimate of m.

yN =1N

N

∑i=1yi

If N = 3 and fy1, y2, y3g = f3,1, 2g then yN = 1.333.If N = 3 and fy1, y2, y3g = f4,8, 1g then yN = 1.etc..

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 17 / 147

2. What is an Estimator?

Question: What constitues a good estimator?

1 The search for good estimators constitutes much of econometrics.

2 An estimator is a rule or strategy for using the data to estimatethe parameter. It is dened before the data are drawn.

3 Our objective is to use the sample data to infer the value of aparameter or set of parameters, which we denote θ.

4 Sampling distributions are used to make inferences about thepopulation. The issue is to know if the sampling distribution of theestimator bθ is informative about the value of θ....

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 18 / 147

2. What is an Estimator?

Question (contd): What constitues a good estimator?

1 Obviously, some estimators are better than others.

1 To take a simple example, your intuition should convince you that thesample mean would be a better estimator of the population mean thanthe sample minimum; the minimum is almost certain to underestimatethe mean.

2 Nonetheless, the minimum is not entirely without virtue; it is easy tocompute, which is occasionally a relevant criterion.

2 The idea is to study the properties of the sampling distributionand especially its moments such as E

bθ (for the bias), Vbθ (for

the precision), etc..

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 19 / 147

2. What is an Estimator?

Question (contd): What constitues a good estimator?

Estimators are compared on the basis of a variety of attributes.

1 Finite sample properties (or nite sample distribution) of estimatorsare those attributes that can be compared regardless of the samplesize (SECTION 3).

2 Some estimation problems involve characteristics that are unknown innite samples. In these cases, estimators are compared on the basison their large sample, or asymptotic properties (SECTION 4).

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 20 / 147

2. What is an Estimator?

Key Concepts Section 2

1 Point estimator2 Point estimate3 Sampling distribution

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 21 / 147

Section 3

Finite Sample Properties

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 22 / 147

3. Finite Sample Properties

Objectives

1 Dene the concept of nite sample distribution.

2 Finite sample properties => What is a good estimator?

3 Unbiased estimator.

4 Comparison of two unbiased estimators.

5 FDCR or Cramer Rao bound.

6 Best Linear Unbiased Estimator (BLUE).

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 23 / 147

3. Finite Sample Properties

Denition (Finite sample properties and nite sample distribution)

The nite sample properties of an estimator bθ correspond to the propertiesof its nite sample distribution (or exact distribution) dened for anysample size N 2 N.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 24 / 147

3. Finite Sample Properties

Two cases:

1 In some particular cases, the nite sample distribution of theestimator is known. It corresponds to the distribution of the randomvariable bθ for any sample size N.

2 In most of cases, the nite sample distribution is unknown, but wecan study some specic moments (mean, variance, etc..) of thisdistribution (nite sample properties).

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 25 / 147

3. Finite Sample Properties

Example (Sample mean and nite sample distribution)

Assume that Y1,Y2, ..,YN are N .i .d .m, σ2

random variables. The

estimator bm = Y N (sample mean) has also a normal distribution:bm = 1

N

N

∑i=1Yi N

m,

σ2

N

8N 2 N

Consequence: the nite sample distribution of bm for any N 2 N is fullycharacterized by m and σ2 (parameters that can be estimated). Example:if N = 3, then bm N

m, σ2/3, if N = 10, then bm N

m, σ2/10,

etc..

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 26 / 147

3. Finite Sample Properties

Proof: The sum of independent normal variables has a normal distributionwith:

E (bm) = 1N

N

∑i=1

E (Yi ) =NmN= m

V (bm) = V

1N

N

∑i=1Yi

!=

1N2

N

∑i=1

V (Yi ) =Nσ2

N2=

σ2

N

since the variables Yi are

independent (then cov (Yi ,Yj ) = 0)identically distributed (then E (Yi ) = m and V (Yi ) = σ2,8i 2 [1, ..,N ]).

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 27 / 147

3. Finite Sample Properties

Remarks

1 Except in very particular cases (normally distributed samples), theexact distribution of the estimator is very di¢ cult to calculate.

2 Sometimes, it is possible to derive the exact distribution of atransformed variable g

bθ , where g (.) is a continuous function.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 28 / 147

3. Finite Sample Properties

Example (Sample variance and nite sample distribution)

Assume that Y1,Y2, ..,YN are N .i .d .m, σ2

random variables. The

sample variance

S2N =1

N 1N

∑i=1

Yi Y N

2is an estimator of σ2. The transformed variable (N 1) S2N/σ2 has aChi-squared (exact / nite sample) distribution with N 1 degrees offreedom:

(N 1)σ2

S2N χ2 (N 1) 8N 2 N

Proof: see Chapter 4.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 29 / 147

3. Finite Sample Properties

FactIn most of cases, it is impossible to derive the exact / nite sampledistribution for the estimator (or a transformed variable).

Two reasons:

1 In some cases, the exact distribution of Y1,Y2..YN is known, but thefunction T (.) is too complicated to derive the distribution of bθ :

bθ = T (Y1, ..YN ) ??? 8N 2 N

2 In most of cases, the distribution of the sample variables Y1,Y2..YN isunknown... bθ = T (Y1, ..YN ) ??? 8N 2 N

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 30 / 147

3. Finite Sample Properties

Question: how to evaluate the nite sample properties of the estimator bθwhen its nite sample distribution is unknow?

bθ ??? 8N 2 N

Solution: We will focus on some specic moments of this (unknown)nite sample (sampling) distribution in order to study some properties ofthe estimator bθ and determine if it is a "good" estimator or not.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 31 / 147

3. Finite Sample Properties

Denition (Unbiased estimator)

An estimator bθ of a parameter θ is unbiased if the mean of its samplingdistribution is θ:

Ebθ = θ

orEbθ θ

= Bias

bθ θ= 0

implies that bθ is unbiased. If θ is a vector of parameters, then theestimator is unbiased if the expected value of every element of bθ equalsthe corresponding element of θ.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 32 / 147

3. Finite Sample Properties

Source: Greene (2007), Econometrics

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 33 / 147

3. Finite Sample Properties

Example (Bernouilli distribution)Let Y1,Y2, ..,YN be a random sampling from a Bernoulli distribution witha success probability p. An unbiased estimator of p is

bp = 1N

N

∑i=1Yi

Proof: Since the Yi are i .i .d . with E (Yi ) = p, then we have:

E (bp) = 1N

N

∑i=1

E (Yi ) =pNN= p

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 34 / 147

3. Finite Sample Properties

Example (Uniform distribution)Let Y1,Y2, ..,YN be a random sampling from a uniform distribution U[0,θ].An unbiased estimator of θ is

bθ = 2N

N

∑i=1Yi

Proof: Since the Yi are i .i .d . with E (Yi ) = (θ + 0) /2 = θ/2, then wehave:

Ebθ = E

2N

N

∑i=1Yi

!=2N

N

∑i=1

E (Yi ) =2N Nθ

2= θ

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 35 / 147

3. Finite Sample Properties

Example (Multiple linear regression model)Consider the model

y = Xβ+ µ

where y 2 RN , X 2 MNK is a nonrandom matrix, β 2 RK is a vector ofparameters, E (µ) = 0N1 and V (µ) = σ2IN . The OLS estimator

bβ = X>X1 X>yis an unbiased estimator of β.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 36 / 147

3. Finite Sample Properties

Proof: Since y = Xβ+ µ, X 2 MNK is a nonrandom matrix andE (µ) = 0, we have

E (y) = Xβ

As a consequence:

Ebβ =

X>X

1X>E (y)

=X>X

1X>Xβ

= β

The estimator bβ is unbiased.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 37 / 147

3. Finite Sample Properties

Remark:

Even it is not relevant in the section devoted to the nite sampleproperties of estimators, we can introduce here the notion ofasymptotically unbiased estimator (which can be considered as a largesample property..).

Here we assume that the estimator bθ = bθN depends on the samplesize N.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 38 / 147

3. Finite Sample Properties

Denition (Asymptotically unbiased estimator)

The sequence of estimators bθN (with N 2 N) is asymptotically unbiased if

limN!∞

EbθN = θ

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 39 / 147

3. Finite Sample Properties

Example (Sample variance)

Assume that Y1,Y2, ..,YN are N .i .d .m, σ2

random variables. The

uncorrected sample variance dened by

eS2N = 1N

N

∑i=1

Yi Y N

2is a biased estimator of σ2 but is asymptotically unbiased.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 40 / 147

3. Finite Sample Properties

Proof: We known that:

S2N =1

N 1N

∑i=1

Yi Y N

2(N 1)

σ2S2N χ2 (N 1) 8N 2 N

Since, we have a relationship between S2N and eS2N , such that:eS2N = 1

N

N

∑i=1

Yi Y N

2=

N 1N

S2N

then we get:Nσ2eS2N χ2 (N 1) 8N 2 N

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 41 / 147

3. Finite Sample Properties

Proof (contd):

Nσ2eS2N χ2 (N 1) 8N 2 N

Reminder: If X χ2 (v) , then E (X ) = v and V (X ) = 2v . By denition:

E

Nσ2eS2N = N 1

or equivalently:

EeS2N = N 1N

σ2 6= σ2

So, eS2N = (1/N)∑Ni=1

Yi Y N

2is a biased estimator of σ2.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 42 / 147

3. Finite Sample Properties

Proof (contd): But eS2N = (1/N)∑Ni=1

Yi Y N

2is asymptotically

unbiased since:

limN!∞

EeS2N = lim

N!∞

N 1N

σ2 = σ2

Remark: Even in a more general framework (non-normal), the samplevariance (with a correction for small sample) is an unbiased estimator of σ2

S2N = (N 1)1| z correction for small sample

N

∑i=1

Yi Y N

2ES2N= σ2

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 43 / 147

3. Finite Sample Properties

Unbiasedness is interesting per se but not so much!

1 The absence of bias is not a su¢ cient criterion to discriminate amongcompetitive estimators.

2 It may exist many unbiased estimators for the same parameter(vector) of interest.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 44 / 147

3. Finite Sample Properties

Example (Estimators)

Assume that Y1,Y2, ..,YN are i .i .d . with E (Yi ) = m, the statistics

bm1 = 1N

N

∑i=1Yi

bm2 = Y1are unbiased estimators of m.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 45 / 147

3. Finite Sample Properties

Proof: Since the Yi are i .i .d . with E (Yi ) = m, then we have:

E (bm1) = 1N

N

∑i=1

E (Yi ) =NmN= m

E (bm2) = E (Y1) = m

Both estimators bm1 and bm2 of the parameter m are unbiased.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 46 / 147

3. Finite Sample Properties

How to compare two unbiased estimators?

When two (or more) estimators are unbiased, the best one is the moreprecise,.i.e. the estimator with the minimum variance.

Comparing two (or more) unbiased estimates becomes equivalent tocomparing their variance-covariance matrices.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 47 / 147

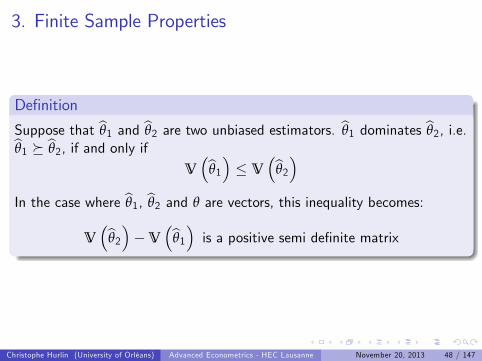

3. Finite Sample Properties

Denition

Suppose that bθ1 and bθ2 are two unbiased estimators. bθ1 dominates bθ2, i.e.bθ1 bθ2, if and only ifVbθ1 V

bθ2In the case where bθ1, bθ2 and θ are vectors, this inequality becomes:

Vbθ2V

bθ1 is a positive semi denite matrix

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 48 / 147

3. Finite Sample Properties

0 0.5 1 1.5 2 2.5 3 3.5 40

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

θ

Estimator 1Estimator 2

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 49 / 147

3. Finite Sample Properties

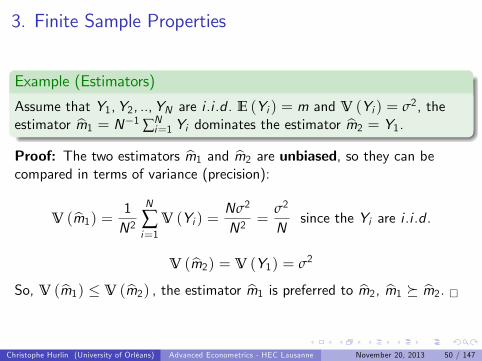

Example (Estimators)

Assume that Y1,Y2, ..,YN are i .i .d . E (Yi ) = m and V (Yi ) = σ2, theestimator bm1 = N1 ∑N

i=1 Yi dominates the estimator bm2 = Y1.Proof: The two estimators bm1 and bm2 are unbiased, so they can becompared in terms of variance (precision):

V (bm1) = 1N2

N

∑i=1

V (Yi ) =Nσ2

N2=

σ2

Nsince the Yi are i .i .d .

V (bm2) = V (Y1) = σ2

So, V (bm1) V (bm2) , the estimator bm1 is preferred to bm2, bm1 bm2. Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 50 / 147

3. Finite Sample Properties

Question: is there a bound for the variance of the unbiased estimators?

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 51 / 147

3. Finite Sample Properties

Denition (Cramer-Rao or FDCR bound)

Let X1, ..,XN be an i .i .d . sample with pdf fX (θ; x). Let bθ be an unbiasedestimator of θ; i.e., Eθ(bθ) = θ. If fX (θ; x) is regular then

Vθ

bθ I1N (θ0) = FDCR or Cramer-Rao bound

where IN (θ0) denotes the Fisher information number for the sampleevaluated at the true value θ0. If θ is a vector then this inequality meansthat Vθ

bθI1N (θ0) is positive semi-denite.

FDCR: Frechet - Darnois - Cramer and RaoRemark: we will dene the Fisher information matrix (or number) inChapter 2 (Maximum Likelihood Estimation).

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 52 / 147

3. Finite Sample Properties

Denition (E¢ ciency)

An estimator is e¢ cient if its variance attains the FDCR (Frechet -Darnois - Cramer - Rao) or Cramer-Rao bound:

Vθ

bθ = I1N (θ0)

where IN (θ0) denotes the Fisher information matrix associated to thesample evaluated at the true value θ0.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 53 / 147

3. Finite Sample Properties

Finally, note that in some cases we further restrict the set of estimators tolinear functions of the data.

Denition (Estimator BLUE)An estimator is the minimum variance linear unbiased estimator or bestlinear unbiased estimator (BLUE) if it is a linear function of the data andhas minimum variance among linear unbiased estimators

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 54 / 147

3. Finite Sample Properties

Remark: the term "linear" means that the estimator bθ is a linear functionof the data Yi : bθj = N

∑i=1

ωijYi

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 55 / 147

3. Finite Sample Properties

Key Concepts Section 3

1 Finite sample distribution2 Finite sample properties3 Bias and unbiased estimator4 Comparison of unbiased estimators5 Cramer-Rao or FDCR bound6 E¢ cient estimator7 Linear estimator8 Estimateur BLUE

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 56 / 147

Section 4

Asymptotic Properties

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 57 / 147

4. Asymptotic Properties

Problem:

1 Let us consider an i .i .d . sample Y1,Y2..,YN , where Y has a pdffY (y ; θ) and θ is an unknown parameter.

2 We assume that fY (y ; θ) is also unknown (we do not know thedistribution of Yi ).

3 We consider an estimator bθ (also denoted bθN to show that it dependson N) such that bθ = T (Y1,Y2, ..,YN ) bθN

4 The nite sample distribution of bθN is unknown....bθN ??? 8N 2 N

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 58 / 147

4. Asymptotic Properties

Question: what is the behavior of the random variable bθN when thesample size N tends to innity?

Denition (Asymptotic theory)Asymptotic or large sample theory consists in the study of thedistribution of the estimator when the sample size is su¢ ciently large.

The asymptotic theory is fundamentally based on the notion ofconvergence...

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 59 / 147

4. Asymptotic Properties

We are mainly concerned with four modes of convergence:

1 Almost sure convergence

2 Convergence in probability

3 Convergence in quadratic mean

4 Convergence in distribution.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 60 / 147

4. Asymptotic Properties

We are mainly concerned with four modes of convergence:

1 Almost sure convergence

2 Convergence in probability

3 Convergence in quadratic mean

4 Convergence in distribution.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 61 / 147

Section 4

Asymptotic Properties

4.1. Almost Sure Convergence

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 62 / 147

4. Asymptotic Properties4.1. Almost sur convergence

Denition (Almost sure convergence)Let XN be a sequence random variable indexed by the sample size. XNconverges almost surely (or with probability 1 or strongly) to a constantc , if, for every ε > 0,

Pr limN!∞

XN c < ε

= 1

or equivalently if:

PrlimN!∞

XN = c= 1

It is writtenXN

a.s .! c

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 63 / 147

4. Asymptotic Properties4.1. Almost sur convergence

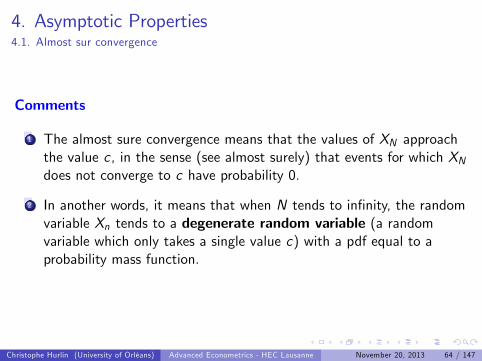

Comments

1 The almost sure convergence means that the values of XN approachthe value c , in the sense (see almost surely) that events for which XNdoes not converge to c have probability 0.

2 In another words, it means that when N tends to innity, the randomvariable Xn tends to a degenerate random variable (a randomvariable which only takes a single value c) with a pdf equal to aprobability mass function.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 64 / 147

4. Asymptotic Properties4.1. Almost sur convergence

0 0.5 1 1.5 2 2.5 3 3.5 40

0.2

0.4

0.6

0.8

1

1.2

c=2

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 65 / 147

4. Asymptotic Properties4.1. Almost sur convergence

Denition (Strong consistency)

A point estimator bθN of θ is strongly consistent if:

bθN a.s .! θ

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 66 / 147

4. Asymptotic Properties4.1. Almost sur convergence

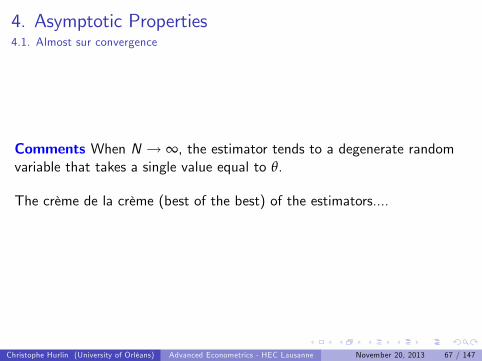

Comments When N ! ∞, the estimator tends to a degenerate randomvariable that takes a single value equal to θ.

The crème de la crème (best of the best) of the estimators....

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 67 / 147

4. Asymptotic Properties

We are mainly concerned with four modes of convergence:

1 Almost sure convergence

2 Convergence in probability

3 Convergence in quadratic mean

4 Convergence in distribution.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 68 / 147

4. Asymptotic Properties

We are mainly concerned with four modes of convergence:

1 Almost sure convergence

2 Convergence in probability

3 Convergence in quadratic mean

4 Convergence in distribution.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 69 / 147

Section 4

Asymptotic Properties

4.2. Convergence in Probability

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 70 / 147

4. Asymptotic Properties4.2. Convergence in probability

Denition (Convergence in probability)Let XN be a sequence random variable indexed by the sample size. XNconverges in probability to a constant c , if, for any ε > 0,

limN!∞

Pr (jXN c j > ε) = 0

It is writtenXN

p! c or plim XN = c

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 71 / 147

4. Asymptotic Properties4.2. Convergence in probability

XNp! c if lim

N!∞Pr (jXN c j > ε) = 0

0 0.5 1 1.5 2 2.5 3 3.5 40

0.5

1

1.5

2

2.5

3

3.5

4

4.5

c=2

cε c+ε

This area tends to 0

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 72 / 147

4. Asymptotic Properties4.2. Convergence in probability

XNp! c if lim

N!∞Pr (jXN c j > ε) = 0 for a very small ε...

0 0.5 1 1.5 2 2.5 3 3.5 40

50

100

150

200

250

300

350

400

c=2

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 73 / 147

4. Asymptotic Properties4.2. Convergence in probability

Comments

1 The general idea is the same than for the a.s. convergence: XN tendsto a degenerate random variable (even if it is not exactly the case)equal to c ..

2 But when XN is very likely to be close to c for large N, what aboutthe location of the remaining small probability mass which is not closeto c?...

3 Convergence in probability allows more erratic behavior in theconverging sequence than almost sure convergence.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 74 / 147

4. Asymptotic Properties4.2. Convergence in probability

Remark The notationXN

p! X

where X is a random element (scalar, vector, matrix) means that thevariable XN X converges to c = 0.

XN Xp! 0

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 75 / 147

4. Asymptotic Properties4.2. Convergence in probability

Denition (Weak consistency)

A point estimator bθN of θ is (weakly) consistent if:

bθN p! θ

Remark: In econometrics, in most of cases, we only consider the weakconsistency. When we say that an estimator is "consistent", it generallyrefers to the convergence in probability.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 76 / 147

4. Asymptotic Properties4.2. Convergence in probability

Lemma (Convergence in probability)Let XN be a sequence random variable indexed by the sample size and c aconstant. If

limN!∞

E (XN ) = c

limN!∞

V (XN ) = 0

Then, XN converges in probability to c as N ! ∞ :

XNp! c

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 77 / 147

4. Asymptotic Properties4.2. Convergence in probability

Example (Consistent estimator)

Assume that Y1,Y2, ..,YN are i .i .d . with E (Yi ) = m and V (Yi ) = σ2,where σ2 is known and m is unknow. The estimator bm, dened by,

bm = 1N

N

∑i=1Yi

is a consistenty estimator of m.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 78 / 147

4. Asymptotic Properties4.2. Convergence in probability

Proof: Since Y1,Y2, ..,YN are i .i .d . with E (Yi ) = m and V (Yi ) = σ2,we have :

E (bm) = 1N

N

∑i=1

E (Yi ) = m

limN!∞

V (bm) = limN!∞

1N2

N

∑i=1

V (Yi ) = limN!∞

σ2

N= 0

The estimator bm is (weakly) consistent:

bm p! m

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 79 / 147

4. Asymptotic Properties4.2. Convergence in probability

Example (Consistent estimator)

Assume that Y1,Y2, ..,YN are N .i .d .m, σ2

random variables. The

sample variance dened by

S2N =1

N 1N

∑i=1

Yi Y N

2is a (weakly) consistent estimator of σ2.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 80 / 147

3. Finite Sample Properties4.2. Convergence in probability

Proof: We known that for normal sample:

(N 1)σ2

S2N χ2 (N 1) 8N 2 N

E

(N 1)

σ2S2N

= N 1 V

(N 1)

σ2S2N

= 2 (N 1)

We get immediately:ES2N= σ2

limN!∞

VS2N= lim

N!∞

2σ4

N 1

= 0

The estimator S2N is (weakly) consistent : S2N

p! σ2.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 81 / 147

4. Asymptotic Properties4.2. Convergence in probability

Lemma (Chain of implication)The almost sure convergence implies the convergence in probability:

a.s .! =) p!

where the symbol "=) " means implies". The converse is not true

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 82 / 147

4. Asymptotic Properties4.2. Convergence in probability

Comments

1 One of the main applications of the convergence in probability andthe almost sure convergence is the law of large numbers.

2 The law of large numbers tells you that the sample mean converges inprobability (weak law of large numbers) or almost surely (stronglaw of large numbers) to the population mean:

XN =1N

N

∑i=1Xi !

N!∞E (Xi )

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 83 / 147

4. Asymptotic Properties4.2. Convergence in probability

Theorem (Weak law of large numbers, Khinchine)

If fXig , for i = 1, ..,N is a sequence of independently and identicallydistributed (i.i.d.) random variables with nite mean E (Xi ) = µ (<∞),then the sample mean XN converges in probability to µ:

XN =1N

N

∑i=1Xi

p! E (Xi ) = µ

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 84 / 147

4. Asymptotic Properties4.2. Convergence in probability

Theorem (Strong law of large numbers, Kolmogorov)

If fXig , for i = 1, ..,N is a sequence of independently and identicallydistributed (i.i.d.) random variables such that E (Xi ) = µ (< ∞) andE (jXi j) < ∞, then the sample mean XN converges almost surely to µ:

XN =1N

N

∑i=1Xi

a.s .! E (Xi ) = µ

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 85 / 147

4. Asymptotic Properties4.2. Convergence in probability

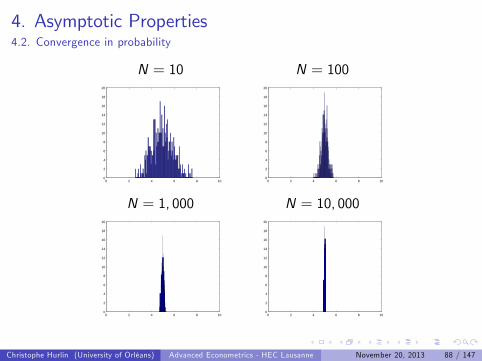

Illustration:

1 Let us consider a random variable Xi U[0,10] and draw an i .i .dsample fxigNi=1

2 Compute the sample mean xN = N1 ∑Ni=1 xi .

3 Repeat this procedure 500 times. We get 500 realisations of thesample mean xN .

4 Build an histogram of these 500 realisations.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 86 / 147

4. Asymptotic Properties4.2. Convergence in probability

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 87 / 147

4. Asymptotic Properties4.2. Convergence in probability

N = 10 N = 100

0 2 4 6 8 100

2

4

6

8

10

12

14

16

18

20

0 2 4 6 8 100

2

4

6

8

10

12

14

16

18

20

N = 1, 000 N = 10, 000

0 2 4 6 8 100

2

4

6

8

10

12

14

16

18

20

0 2 4 6 8 100

2

4

6

8

10

12

14

16

18

20

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 88 / 147

4. Asymptotic Properties4.2. Convergence in probability

An animation is worth 1,000,000 words...

Click me!

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 89 / 147

4. Asymptotic Properties4.2. Convergence in probability

Proof: There are many proofs of the law of large numbers. Most of themuse the additional assumption of nite variance V (Xi ) = σ2 and theChebyshevs inequality.

Theorem (Chebyshevs inequality)Let X be a random variable with nite expected value µ and nitenon-zero variance σ2. Then for any real number k > 0,

Pr (jX µj kσ) 1k2

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 90 / 147

4. Asymptotic Properties4.2. Convergence in probability

Proof (contd): Under the assumpition of i .i .d .µ, σ2

, we have that:

EXN= µ V

XN=

σ2

N

Given the Chebyshevs inequality, we get for k > 0:

PrXN µ

k σpN

1k2

Let us dene ε > 0 such that

ε =kσpN() k =

εpN

σ

Then we get for any ε > 0:

PrXN µ

ε σ2

ε2N

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 91 / 147

4. Asymptotic Properties4.2. Convergence in probability

Proof (contd): for any ε > 0:

PrXN µ

ε σ2

ε2N

So, when N ! ∞ this probability is necessarily equal to 0 (since 0means = 0)

PrlimN!∞

XN µ ε

= 0 8ε > 0

Since PrXN µ

< ε= 1 P

XN µ ε

, we have:

PrlimN!∞

XN µ < ε

= 1 8ε > 0

XNa.s .! µ (SLLN) =) XN

p! µ (WLLN)

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 92 / 147

4. Asymptotic Properties4.2. Convergence in probability

Remarks

1 These two theorems consider a sequence of independently andidentically distributed (i.i.d.) random variables (as a consequencewith the same mean E (Xi ) = µ, 8i = 1, ..,N.

2 There are alternative versions of the law of large numbers forindependent random variables not identically (heterogeneously)distributed with E (Xi ) = µi (cf. Greene, 2007).

1 Chebychevs Weak Law of Large Numbers.

2 Markovs Strong Law of Large Numbers.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 93 / 147

4. Asymptotic Properties4.2. Convergence in probability

Theorem (Slutskys theorem)

Let XN and YN be two sequences of random variables where XNp! X and

YNp! c, where c 6= 0, then:

XN + YNp! X + c

XNYNp! cX

XNYN

p! Xc

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 94 / 147

4. Asymptotic Properties4.2. Convergence in probability

Remark: This also holds for sequences of random matrices. The laststatement reads: if XN

p! X and YNp! Ω then

Y1N XNp! Ω1X

provided that Ω1 exists.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 95 / 147

4. Asymptotic Properties4.2. Convergence in probability

ExampleLet us consider the multiple linear regression model

yi = x>i β+ µi

where xi = (xi1..xiK )> is K 1 vector of random variables,

β = (β1...βK )> is K 1 vector of parmeters, and where the error term µi

satises E (µi ) = 0 and E (µi j xij ) = 0 8j = 1, ..K . Question: show thatthe OLS estimator dened by

bβ = N

∑i=1xix>i

!1 N

∑i=1xiyi

!

is a consistent estimator of β.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 96 / 147

4. Asymptotic Properties4.2. Convergence in probability

Proof: let us rewritte the OLS estimator as:

bβ =

N

∑i=1xix>i

!1 N

∑i=1xiyi

!

=

N

∑i=1xix>i

!1 N

∑i=1xix>i β+ µi

!

=

N

∑i=1xix>i

!1 N

∑i=1xix>i

!β+

N

∑i=1xix>i

!1 N

∑i=1xiµi

!

= β+

N

∑i=1xix>i

!1 N

∑i=1xiµi

!

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 97 / 147

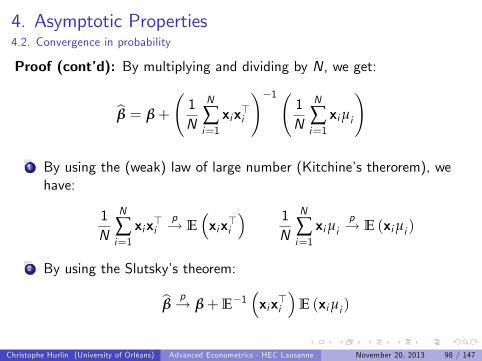

4. Asymptotic Properties4.2. Convergence in probability

Proof (contd): By multiplying and dividing by N, we get:

bβ = β+

1N

N

∑i=1xix>i

!1 1N

N

∑i=1xiµi

!

1 By using the (weak) law of large number (Kitchines therorem), wehave:

1N

N

∑i=1xix>i

p! Exix>i

1N

N

∑i=1xiµi

p! E (xiµi )

2 By using the Slutskys theorem:

bβ p! β+E1xix>i

E (xiµi )

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 98 / 147

4. Asymptotic Properties4.2. Convergence in probability

Reminder: If X and Y are two random variables, then

E (X jY ) = 0 =) E (X Y ) = 0

The reverse is not true.

E (X jY ) = 0 =)(cov (X ,Y ) = E (XY ) E (X )E (Y ) = 0

E (X ) = 0

E (X jY ) = 0 =) E (XY ) = 0

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 99 / 147

4. Asymptotic Properties4.2. Convergence in probability

Proof (contd): bβ p! β+E1xix>i

E (xiµi )

SinceE (µi j xij ) = 0 8j = 1, ..K ) E (µixi ) = 0K1

We have bβ p! β

The OLS estimator bβ is (weakly) consistent.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 100 / 147

4. Asymptotic Properties

We are mainly concerned with four modes of convergence:

1 Almost sure convergence

2 Convergence in probability

3 Convergence in quadratic mean

4 Convergence in distribution.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 101 / 147

4. Asymptotic Properties

We are mainly concerned with four modes of convergence:

1 Almost sure convergence

2 Convergence in probability

3 Convergence in quadratic mean

4 Convergence in distribution.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 102 / 147

Section 4

Asymptotic Properties

4.3. Convergence in Mean Square

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 103 / 147

4. Asymptotic Properties4.3. Convergence in mean square

Denition (Convergence in mean square)

Let fXig for i = 1, ..,N be a sequence of real-valued random variables

such that EjXN j2

< ∞. XN converges in mean square to a constant c ,

if:limN!∞

EjXN c j2

= 0

It is writtenXN

m.s .! c

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 104 / 147

4. Asymptotic Properties4.3. Convergence in mean square

Remark: It is the less usefull notion of convergence.. except for thedemonstrations of the convergence in probability.

Lemma (Chain of implication)The convergence in mean square implies the convergence in probability:

m.s .! =) p!

where the symbol "=) " means implies". The converse is not true.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 105 / 147

4. Asymptotic Properties

We are mainly concerned with four modes of convergence:

1 Almost sure convergence

2 Convergence in probability

3 Convergence in quadratic mean

4 Convergence in distribution

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 106 / 147

4. Asymptotic Properties

We are mainly concerned with four modes of convergence:

1 Almost sure convergence

2 Convergence in probability

3 Convergence in quadratic mean

4 Convergence in distribution

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 107 / 147

Section 4

Asymptotic Properties

4.4. Convergence in Distribution

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 108 / 147

4. Asymptotic Properties4.4. Convergence in distribution

Denition (Convergence in distribution)Let XN be a sequence random variable indexed by the sample size with acdf FN (.). XN converges in distribution to a random variable X withcdf F (.) if

limN!∞

FN (x) = F (x) 8x

It is written:XN

d! X

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 109 / 147

4. Asymptotic Properties4.4. Convergence in distribution

Comment: In general, we have:

XN|zrandom var.

d! X|zrandom var.

XN|zrandom var.

p! c|zconstant

In the case, where

XN|zrandom var.

p! X|zrandom var.

it means XN X| z random var.

p! 0|zconstant

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 110 / 147

4. Asymptotic Properties4.4. Convergence in distribution

Lemma (Chain of implication)The convergence in probability implies the convergence in distribution:

p! =) d!

where the symbol "=) " means implies". The converse is not true.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 111 / 147

4. Asymptotic Properties4.4. Convergence in distribution

Denition (Asymptotic distribution)

If XN converges in distribution to X , where FN (.) is the cdf of XN , thenF (.) is the cdf of the limiting or asymptotic distribution of XN .

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 112 / 147

4. Asymptotic Properties4.4. Convergence in distribution

Consequence: Generally, we denote:

XN|zrandom var.

d! L|zasy. distribution

It means XN converges in distribution to a random variable X that has adsitribution L.Example

XNd! N (0, 1)

means that XN converges to a random variable X normally distributed orthat XN has an asymptotic standard normal distribution.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 113 / 147

4. Asymptotic Properties4.4. Convergence in distribution

Denition (Asymptotic mean and variance)The asymptotic mean and variance of a random variable XN are themean and variance of the asymptotic or limiting distribution, assumingthat the limiting distribution and its moments exist. These moments aredenoted by

Easy (XN ) Vasy (XN )

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 114 / 147

4. Asymptotic Properties4.4. Convergence in distribution

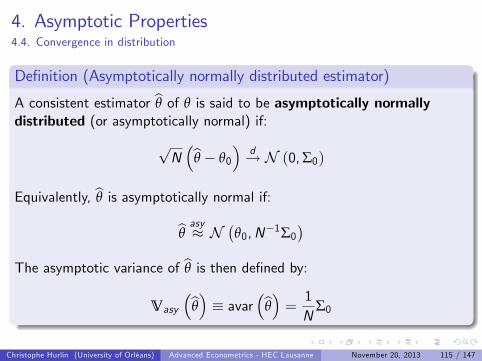

Denition (Asymptotically normally distributed estimator)

A consistent estimator bθ of θ is said to be asymptotically normallydistributed (or asymptotically normal) if:

pNbθ θ0

d! N (0,Σ0)

Equivalently, bθ is asymptotically normal if:bθ asy N

θ0,N1Σ0

The asymptotic variance of bθ is then dened by:

Vasy

bθ avarbθ = 1N

Σ0

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 115 / 147

Section 4

Asymptotic Properties

4.5. Asymptotic Distributions

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 116 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Lets go back to our estimation problem

We consider a (strongly) consistent estimator bθN of the trueparameter θ0. bθN a.s .! θ0 =) bθN p! θ0

This estimator has a degenerated asymptotic distribution(point-mass distribution), since when N ! ∞,

limN!∞

fbθN (x) = f (x)where fbθN (.) is the pdf of bθN and f (x) is dened by:

f (x) =10

if x = θ00 otherwise

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 117 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

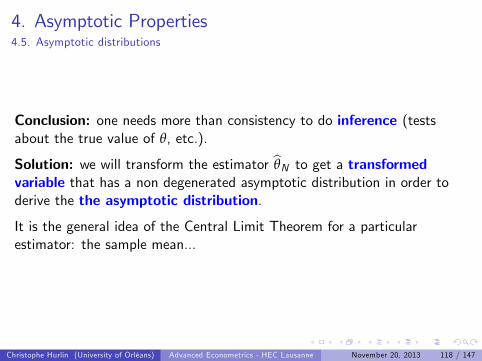

Conclusion: one needs more than consistency to do inference (testsabout the true value of θ, etc.).

Solution: we will transform the estimator bθN to get a transformedvariable that has a non degenerated asymptotic distribution in order toderive the the asymptotic distribution.

It is the general idea of the Central Limit Theorem for a particularestimator: the sample mean...

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 118 / 147

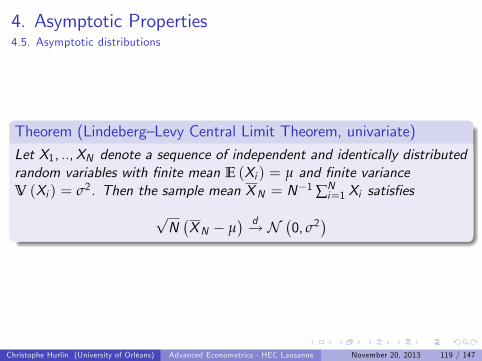

4. Asymptotic Properties4.5. Asymptotic distributions

Theorem (LindebergLevy Central Limit Theorem, univariate)Let X1, ..,XN denote a sequence of independent and identically distributedrandom variables with nite mean E (Xi ) = µ and nite varianceV (Xi ) = σ2. Then the sample mean XN = N1 ∑N

i=1 Xi satises

pNXN µ

d! N0, σ2

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 119 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Comment:

1 The result is quite remarkable as it holds regardless of the form of theparent distribution (the distribution of Xi ).

2 The central limit theorem requires virtually no assumptions (otherthan independence and nite variances) to end up with normality:normality is inherited from the sums of small independentdisturbances with nite variance.

Proof: Rao (1973).

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 120 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Illustration:

1 Let us consider a random variable Xi χ2 (2) , such that E (Xi ) = 2and V (Xi ) = 4 and draw an i .i .d sample fxigNi=1

2 Compute the sample mean xN = N1 ∑Ni=1 xi and the transformed

variablepN (xN 2) /2

3 Repeat this procedure 5,000 times. We get 5,000 realisations of thistransformed variable.

4 Build an histogram (and a non parametric kernel estimate of f X N (.))of these 5,000 realisations and compare it to the normal pdf.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 121 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 122 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

N = 10 N = 100

4 2 0 2 4 60

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45RealisationsS tandard normal pdfK ernel estimate

5 0 50

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45RealisationsS tandard normal pdfK ernel estimate

N = 1, 000 N = 10, 000

6 4 2 0 2 4 60

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4RealisationsS tandard normal pdfK ernel estimate

5 0 50

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4RealisationsS tandard normal pdfK ernel estimate

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 123 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Click me!

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 124 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

DenitionThe convergence result (CLT)

pNXN µ

d! N0, σ2

can be understood as:

XNasy N

µ,

σ2

N

where the symbol

asy means "asymptotically distributed as". The

asymptotic mean and variance of the sample mean are then dened by:

EasyXN= µ Vasy

XN=

σ2

N

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 125 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Speed of convergence: why studyingpNXN in the TCL?

1 For simplicity, let us assume that µ = E (Xi ) = 0 and let us study theasymptotic behavior of NαXN

VNαXN

= N2αV

XN= N2α σ2

N= N2α1σ2

2 If we assume that α > 1/2, then 2α 1 > 0, the asymptotic varianceof NαXN is innite:

limN!∞

VNαXN

= +∞

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 126 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

1 If we assume that α < 1/2, then 2α 1 < 0, the NαXN has adegenerated distribution:

limN!∞

VNαXN

= 0

2 As a consequence α = 1/2 is the only choice to get a nite andpositive variance

Vp

NXN= σ2

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 127 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Summary: Let X1, ..,XN denote a sequence of independent andidentically distributed random variables with nite mean E (Xi ) = µ andnite variance V

X 2i= σ2. Then, the sample mean

XN =1N

∑Ni=1 Xi

satisesWLLN: XN

p! µ

CLT:pNXN µ

d! N0, σ2

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 128 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

The central limit theorem does not assert that the sample meantends to normality. It is the transformation of the sample mean thathas this property

WLLN: XNp! µ

CLT:pNXN µ

d! N0, σ2

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 129 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Theorem (LindebergLevy Central Limit Theorem, multivariate)Let x1, .., xN denote a sequence of independent and identically distributedrandom K 1 vectors with nite mean E (xi ) = µ and nite variancecovariance K K matrix V (xi ) = Σ. Then the sample meanxN = N1 ∑N

i=1 xi satises

pN(xN µ)| z

K1

d! N

0@ 0|zK1

, Σ|zKK

1A

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 130 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Remark: there exist other versions of the CLT, especially for independentbut not identically (heterogeneously) distributed variables

1 LindebergFeller Central Limit Theorem for unequal variances.

2 Liapounov Central Limit Theorem for unequal means and variances.

For more details, see:

Greene W. (2007), Econometric Analysis, sixth edition, PearsonPrentice Hill.

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 131 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Question: from the CLT (univariate or multivariate), and the asymptoticdistribution of XN , how to derive the asymptotic distribution of anestimator bθ that depends on the sample mean?

bθ = g XN asy ???

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 132 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Theorem (Continouous mapping theorem)

Let fXig for i = 1, ..,N be a sequence of real-valued random variables andg (.) a continous function:

if XNa.s! X then g (XN )

a.s! g (X )

if XNp! X then g (XN )

p! g (X )

if XNd! X then g (XN )

d! g (X )

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 133 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Example (multiple linear regression model)Let us consider the multiple linear regression model

yi = x>i β+ µi

where xi = (xi1..xiK )> is K 1 vector of random variables,

β = (β1...βK )> is K 1 vector of parameters, and where the error term

µi satises E (µi ) = 0, V (µi ) = σ2 and E (µi j xij ) = 0, 8j = 1, ..KQuestion: show that the OLS estimator satises

pNbβ β0

d! N

0, σ2E1

x>i xi

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 134 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Proof:

1 Rewritte the OLS estimator as:

bβ = N

∑i=1xix>i

!1 N

∑i=1xiyi

!= β0 +

N

∑i=1xix>i

!1 N

∑i=1xiµi

!

2 Normalize the vector bβ β0

pNbβ β0

=

1N

N

∑i=1xix>i

!1 pN1N

N

∑i=1xiµi

!

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 135 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Reminder: if x is a vector of random variables and Y is a scalar (randomvariable) such that E (xY ) = 0, then

V (xY ) = Ex E (Y j x) x>

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 136 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Proof (contd):

3. Using the WLLN and the CMP: 1N

N

∑i=1xix>i

!1p! E1

xix>i

4. Using the CLT:

pN

1N

N

∑i=1xiµi E (xiµi )

!d! N (0,V (xiµi ))

with E (µi j xik ) = 0, 8k = 1, ..K =) E (xiµi ) = 0 and

V (xiµi ) = Exiµiµix

>i

= E

Exiµiµix

>i

xi= E

xiV (µi j xi ) x>i

= σ2E

xix>i

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 137 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Proof (contd): we have 1N

N

∑i=1xix>i

!1p! E1

xix>i

pN

1N

N

∑i=1xiµi

!d! N

0, σ2E

xix>i

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 138 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Theorem (Slutskys theorem for convergence in distribution)

Let XN and YN be two sequences of random variables where XNd! X and

YNp! c, where c 6= 0, then:

XN + YNd! X + c

XNYNd! cX

XNYN

d! Xc

If YN and XN are matrices/vectors, then Y 1N XNd! c1X with

Vc1X

= c1Vc1>

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 139 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Proof (contd): By using the Sluskys theorem (for a convergence indistribution), we have:

pNbβ β0

=

1N

N

∑i=1xix>i

!1 pN1N

N

∑i=1xiµi

!d! N (Π,Ω)

withΠ = E1

xix>i

0 = 0

Ω = E1xix>i

σ2E

xix>i

E1

xix>i

= σ2E1

xix>i

Finally, we have:

pNbβ β0

d! N

0, σ2E1

xix>i

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 140 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

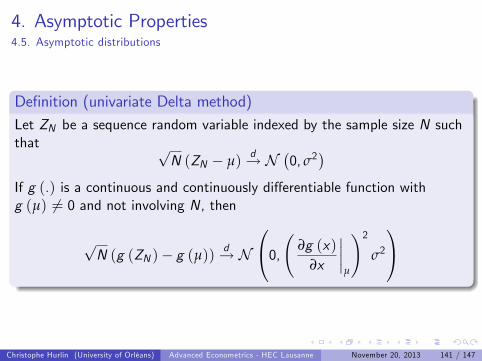

Denition (univariate Delta method)Let ZN be a sequence random variable indexed by the sample size N suchthat p

N (ZN µ)d! N

0, σ2

If g (.) is a continuous and continuously di¤erentiable function withg (µ) 6= 0 and not involving N, then

pN (g (ZN ) g (µ))

d! N

0@0, ∂g (x)∂x

µ

!2σ2

1A

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 141 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

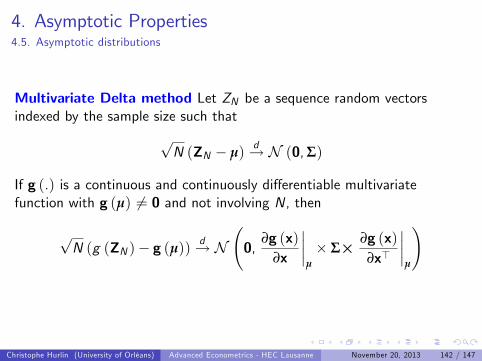

Multivariate Delta method Let ZN be a sequence random vectorsindexed by the sample size such that

pN (ZN µ)

d! N (0,Σ)

If g (.) is a continuous and continuously di¤erentiable multivariatefunction with g (µ) 6= 0 and not involving N, then

pN (g (ZN ) g (µ))

d! N 0,

∂g (x)∂x

µ

Σ ∂g (x)∂x>

µ

!

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 142 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

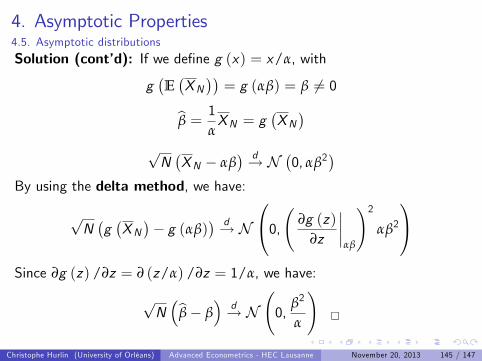

Example (Gamma distribution)Let X1, ..,XN denote a sequence of independent and identically distributedrandom variables. We assume that Xi Γ (α, β) (gamma distribution)with E (X ) = αβ and V (X ) = αβ2, α > 0, β > 0 and a pdf dened by:

fX (x ; α, β) =xα1 exp

x

β

Γ (α) βα , useless in this exercice, but for your culture

for 8x 2 [0,+∞[ , where Γ (α) =R ∞0 t

α1 exp (t) dt denotes theGamma function. We assume that α is known. Question: What is theasymptotic distribution of the estimator bβ dened by:

bβ = 1αN

N

∑i=1Xi

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 143 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Solution: The estimator bβ is dened by:bβ = 1

αN

N

∑i=1Xi

Since X1, ..,XN are i .i .d . with E (X ) = αβ and V (X ) = αβ2, we canapply the LindebergLevy CLT, and we get immediately:

pNXN αβ

d! N0, αβ2

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 144 / 147

4. Asymptotic Properties4.5. Asymptotic distributions

Solution (contd): If we dene g (x) = x/α, with

gEXN= g (αβ) = β 6= 0

bβ = 1αXN = g

XN

pNXN αβ

d! N0, αβ2

By using the delta method, we have:

pNgXN g (αβ)

d! N

0@0, ∂g (z)∂z

αβ

!2αβ2

1ASince ∂g (z) /∂z = ∂ (z/α) /∂z = 1/α, we have:

pNbβ β

d! N

0,

β2

α

!

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 145 / 147

4. Asymptotic Properties

Key Concepts Section 4

1 Almost sure convergence2 Convergence in probability3 Law of large numbers: Khinchines and Kolmogorovs theorems4 Weakly and strongly consistent estimator5 Slutskys theorem6 Convergence in mean square7 Convergence in distribution8 Asymptotic distribution and asymptotic variance9 Lindeberg-Levy Central Limite Theorem (univariate and multivariate)10 Continuous mapping theorem11 Delta method

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 146 / 147

End of Chapter 1

Christophe Hurlin (University of Orléans)

Christophe Hurlin (University of Orléans) Advanced Econometrics - HEC Lausanne November 20, 2013 147 / 147