Embed Size (px)

Citation preview

ADVANCES AND NPA

PREPARED BY :

C.A. D. G. KURUNDWADKARM.COM., LL.B(GEN), FCA, FCS, AICWA

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

Advances:

a) Credit Appraisala) Sanctioning / Disbursementb) Documentationc) Review / Monitoring /

Supervision

Documentation

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

Highly significant as the very safety & security of the advances depends on documentation.

Proper documentation, effective supervision & monitoring and efficient early warning system is a hallmark of audit of advances.

Documentation must be:-Complete-Valid-Enforceable

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

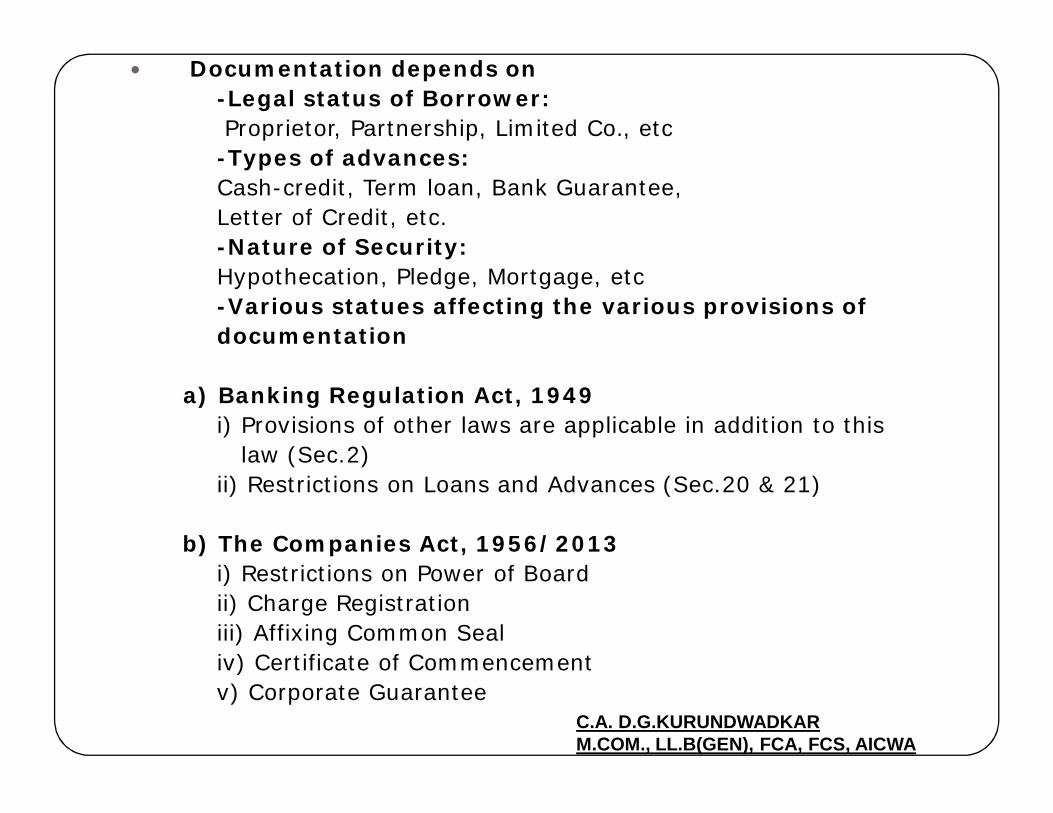

Documentation depends on -Legal status of Borrower:Proprietor, Partnership, Limited Co., etc-Types of advances:Cash-credit, Term loan, Bank Guarantee,Letter of Credit, etc.-Nature of Security:Hypothecation, Pledge, Mortgage, etc-Various statues affecting the various provisions of documentation

a) Banking Regulation Act, 1949i) Provisions of other laws are applicable in addition to this

law (Sec.2) ii) Restrictions on Loans and Advances (Sec.20 & 21)

b) The Companies Act, 1956/2013i) Restrictions on Power of Board ii) Charge Registration iii) Affixing Common Sealiv) Certificate of Commencementv) Corporate Guarantee

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

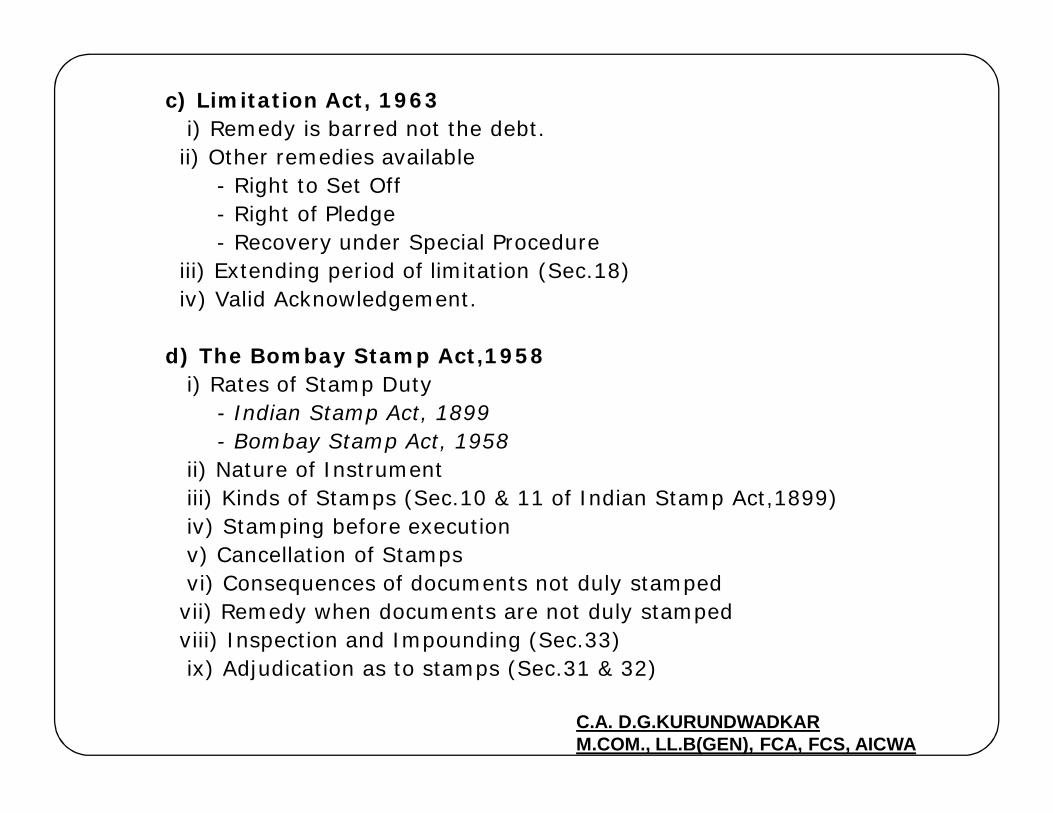

c) Limitation Act, 1963i) Remedy is barred not the debt.ii) Other remedies available

- Right to Set Off- Right of Pledge- Recovery under Special Procedure

iii) Extending period of limitation (Sec.18)iv) Valid Acknowledgement.

d) The Bombay Stamp Act,1958i) Rates of Stamp Duty

- Indian Stamp Act, 1899- Bombay Stamp Act, 1958

ii) Nature of Instrumentiii) Kinds of Stamps (Sec.10 & 11 of Indian Stamp Act,1899)iv) Stamping before executionv) Cancellation of Stampsvi) Consequences of documents not duly stampedvii) Remedy when documents are not duly stampedviii) Inspection and Impounding (Sec.33)ix) Adjudication as to stamps (Sec.31 & 32)

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

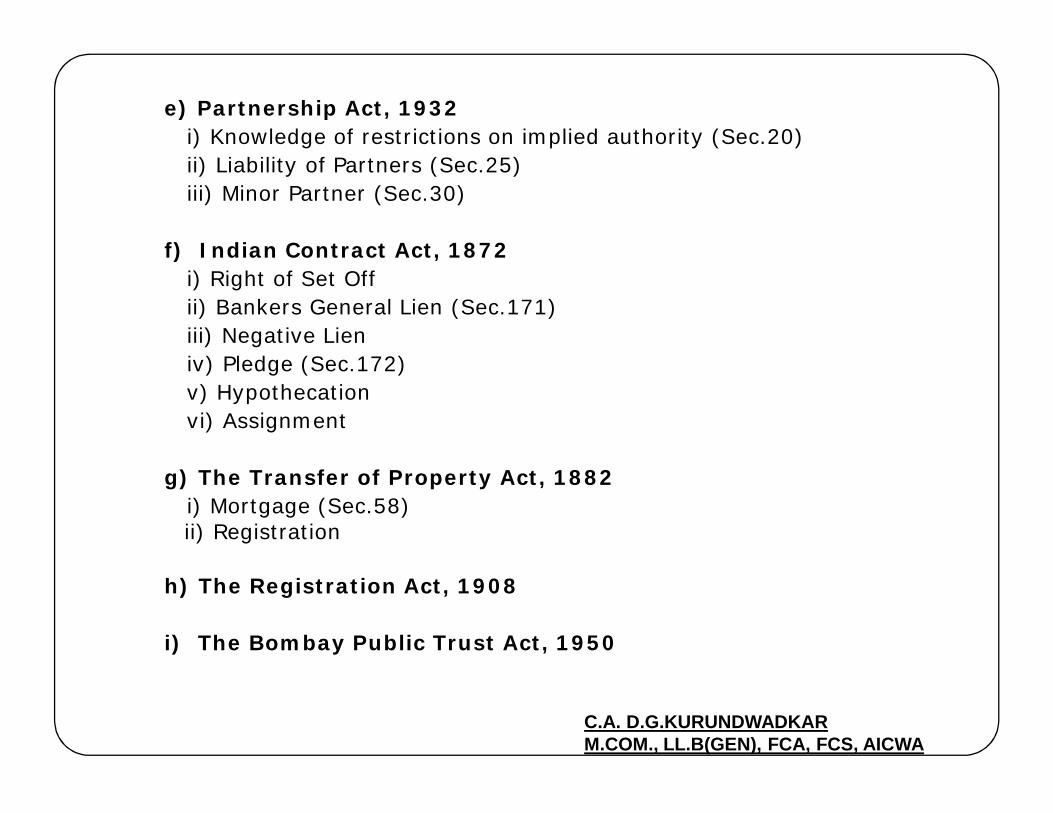

e) Partnership Act, 1932i) Knowledge of restrictions on implied authority (Sec.20)ii) Liability of Partners (Sec.25)iii) Minor Partner (Sec.30)

f) Indian Contract Act, 1872i) Right of Set Offii) Bankers General Lien (Sec.171)iii) Negative Lieniv) Pledge (Sec.172)v) Hypothecationvi) Assignment

g) The Transfer of Property Act, 1882i) Mortgage (Sec.58)ii) Registration

h) The Registration Act, 1908

i) The Bombay Public Trust Act, 1950

Guidelines of the Reserve Bank of India on:

Income Recognition, Asset Classification,

Provisioning and

other related matters.

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

Highlights

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

Committee on Financial system set up under Chairmanship of M. Narasimham by RBI which submitted its report in 1992.

Policy of Income Recognition made objective based on record of recovery rather than subjective consideration.

‘Prudential Norms/Guidelines’ for Income Recognition, Asset Classification & Provision.

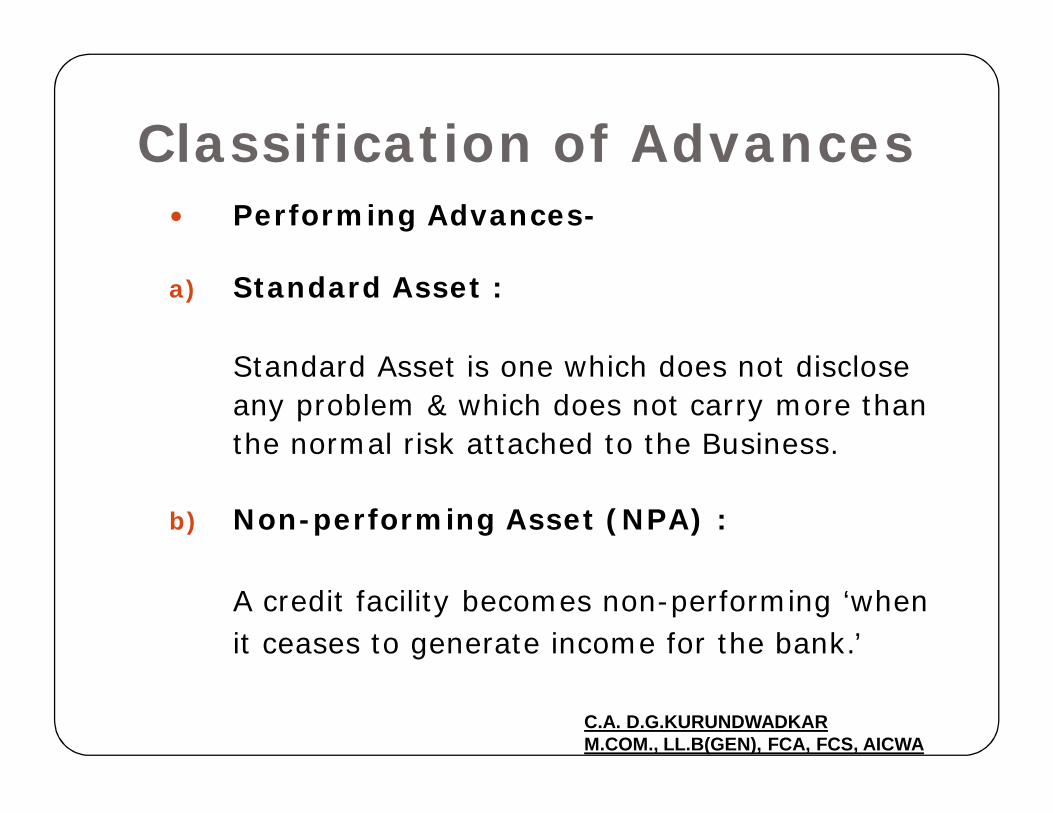

Classification of Advances

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

Performing Advances-

a) Standard Asset :

Standard Asset is one which does not disclose any problem & which does not carry more than the normal risk attached to the Business.

b) Non-performing Asset (NPA) :

A credit facility becomes non-performing ‘when it ceases to generate income for the bank.’

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

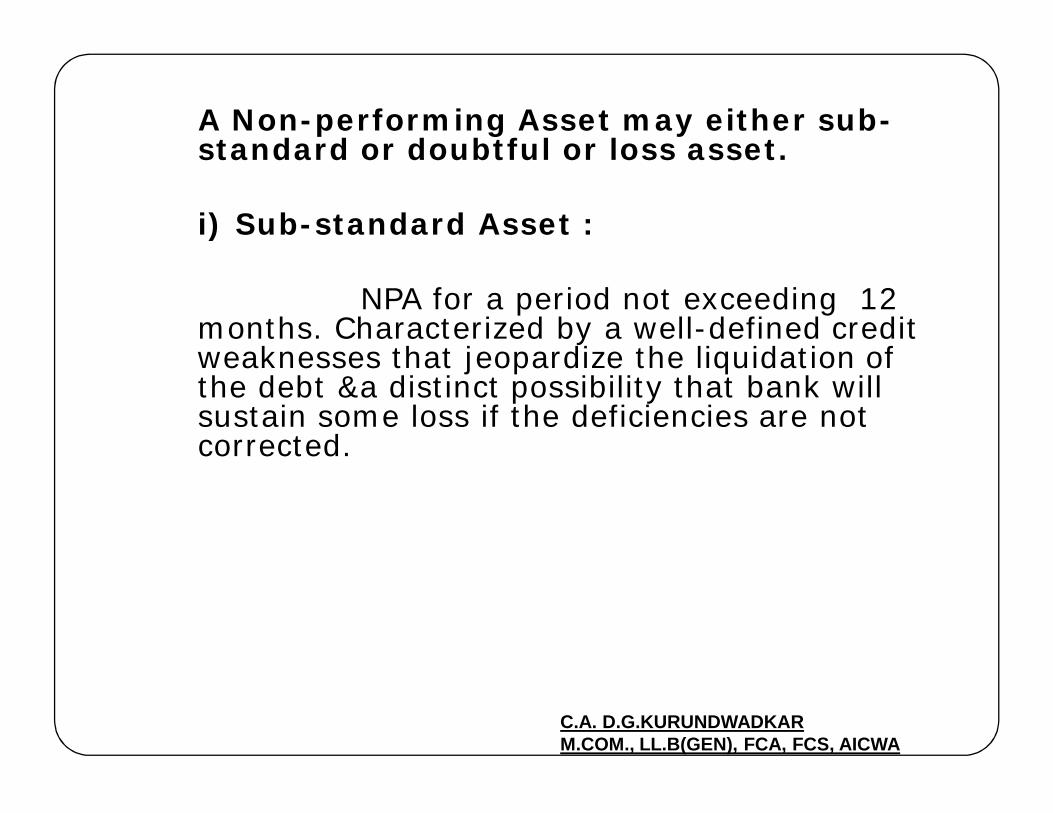

A Non-performing Asset may either sub-standard or doubtful or loss asset.

i) Sub-standard Asset :

NPA for a period not exceeding 12 months. Characterized by a well-defined credit weaknesses that jeopardize the liquidation of the debt &a distinct possibility that bank will sustain some loss if the deficiencies are not corrected.

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

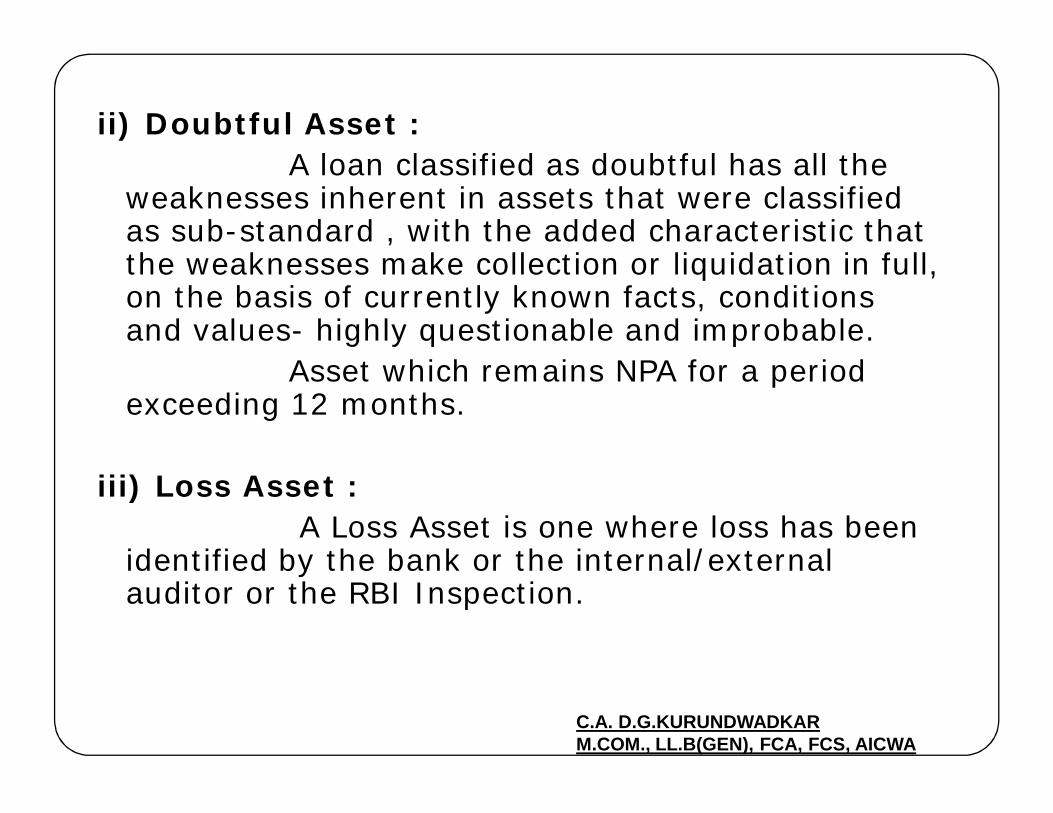

ii) Doubtful Asset : A loan classified as doubtful has all the

weaknesses inherent in assets that were classified as sub-standard , with the added characteristic that the weaknesses make collection or liquidation in full, on the basis of currently known facts, conditions and values- highly questionable and improbable.

Asset which remains NPA for a period exceeding 12 months.

iii) Loss Asset :A Loss Asset is one where loss has been

identified by the bank or the internal/external auditor or the RBI Inspection.

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

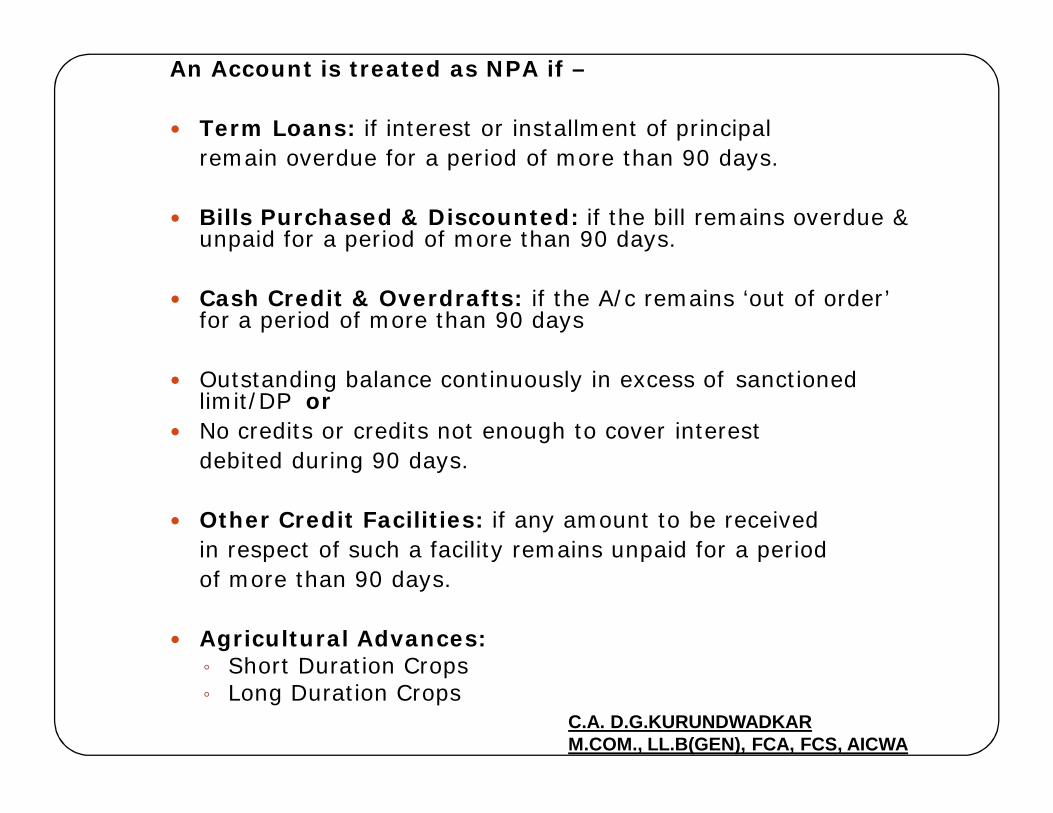

An Account is treated as NPA if –

Term Loans: if interest or installment of principalremain overdue for a period of more than 90 days.

Bills Purchased & Discounted: if the bill remains overdue & unpaid for a period of more than 90 days.

Cash Credit & Overdrafts: if the A/c remains ‘out of order’ for a period of more than 90 days

Outstanding balance continuously in excess of sanctioned limit/DP or

No credits or credits not enough to cover interestdebited during 90 days.

Other Credit Facilities: if any amount to be receivedin respect of such a facility remains unpaid for a periodof more than 90 days.

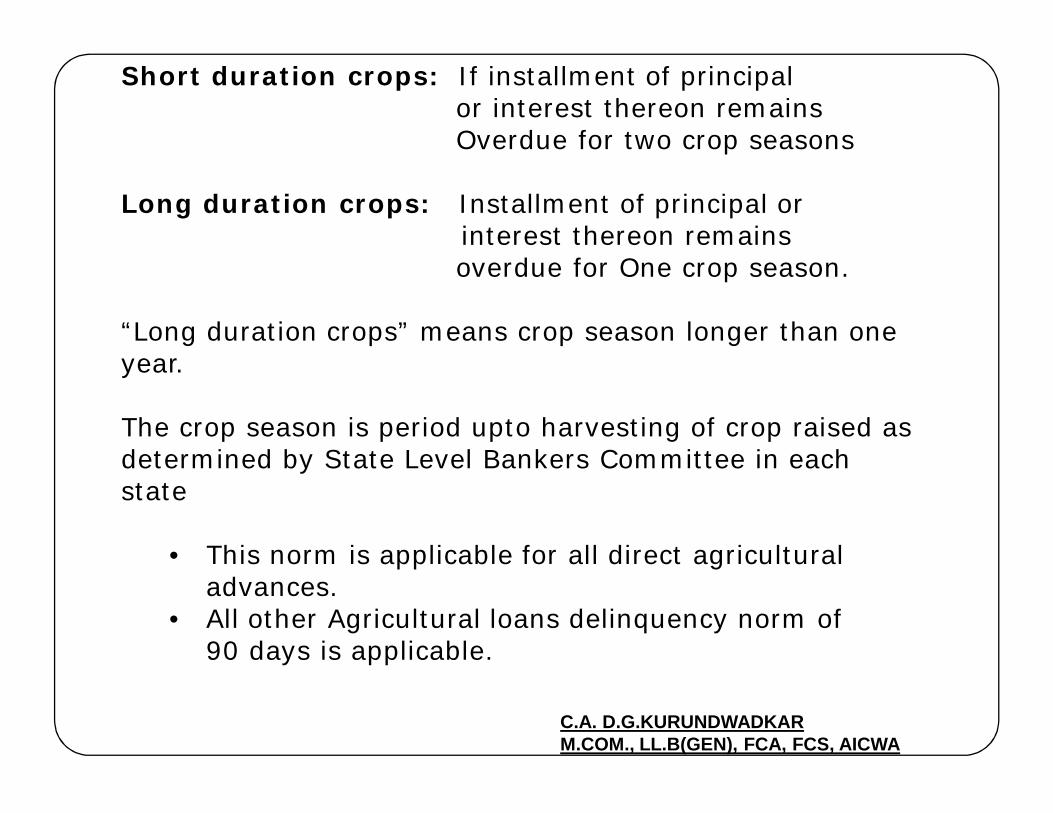

Agricultural Advances:◦ Short Duration Crops◦ Long Duration Crops

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

Short duration crops: If installment of principalor interest thereon remains Overdue for two crop seasons

Long duration crops: Installment of principal or interest thereon remainsoverdue for One crop season.

“Long duration crops” means crop season longer than one year.

The crop season is period upto harvesting of crop raised as determined by State Level Bankers Committee in each state

• This norm is applicable for all direct agriculturaladvances.

• All other Agricultural loans delinquency norm of90 days is applicable.

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

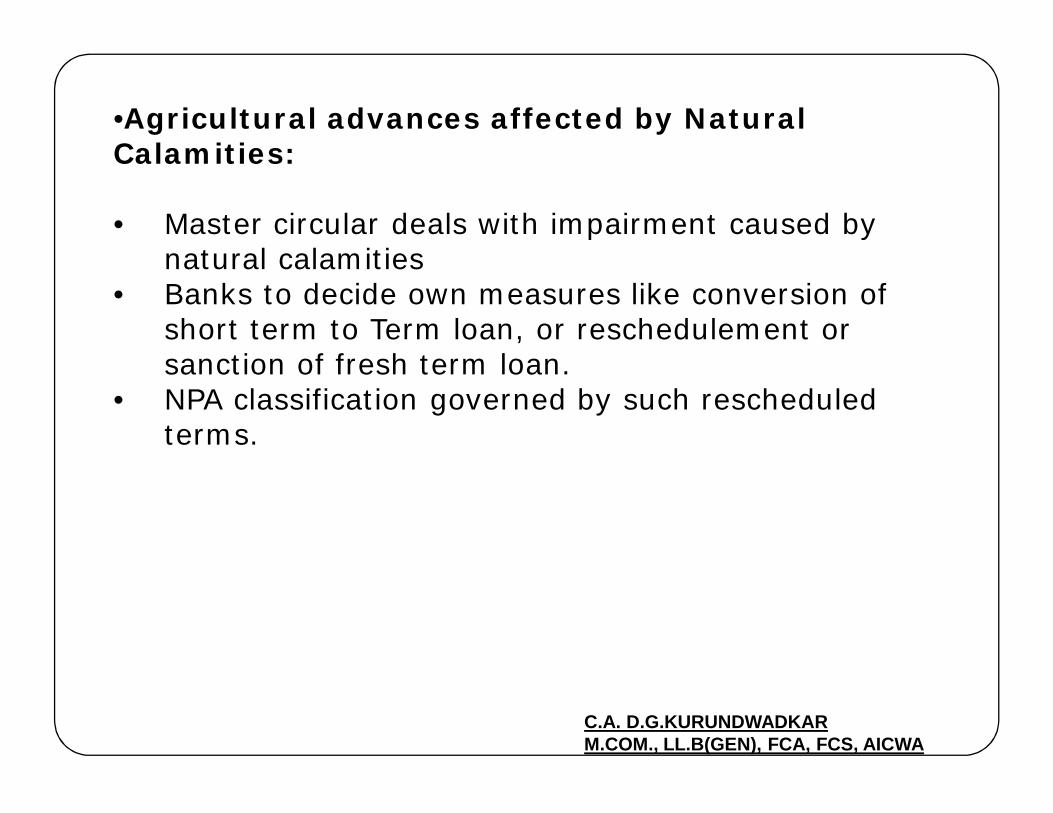

•Agricultural advances affected by Natural Calamities:

• Master circular deals with impairment caused by natural calamities

• Banks to decide own measures like conversion ofshort term to Term loan, or reschedulement orsanction of fresh term loan.

• NPA classification governed by such rescheduledterms.

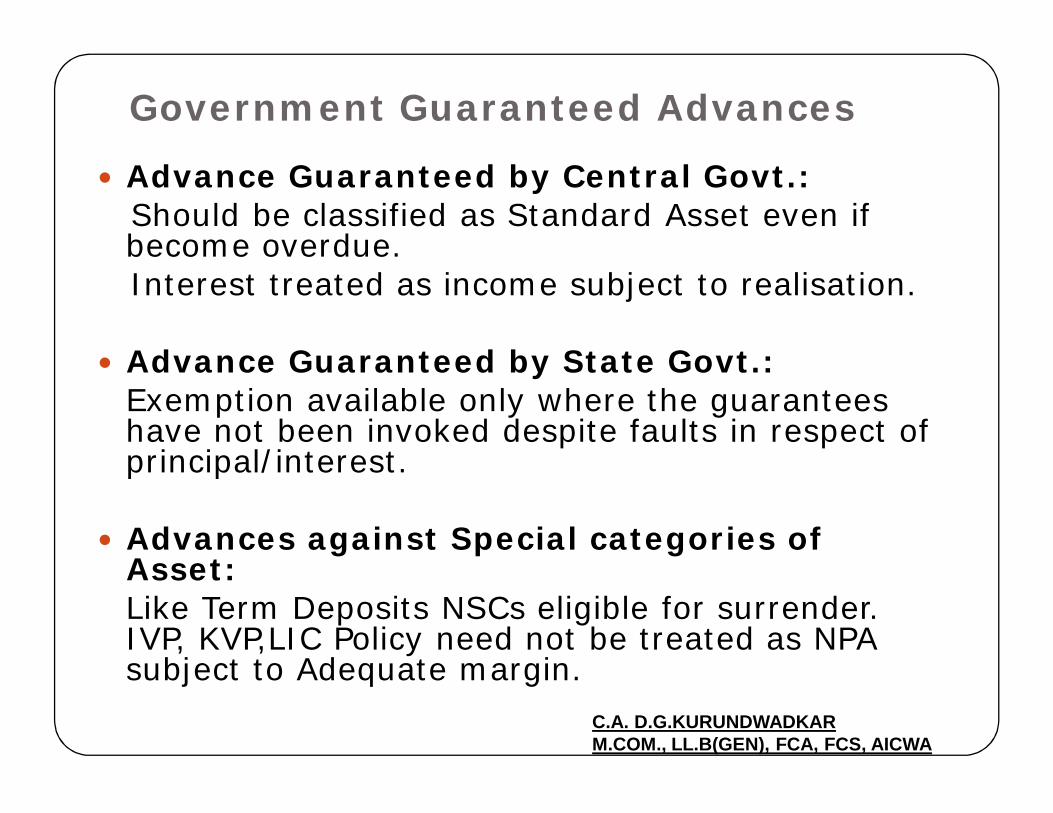

Government Guaranteed Advances

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

Advance Guaranteed by Central Govt.:Should be classified as Standard Asset even if become overdue.Interest treated as income subject to realisation.

Advance Guaranteed by State Govt.: Exemption available only where the guarantees have not been invoked despite faults in respect of principal/interest.

Advances against Special categories of Asset:Like Term Deposits NSCs eligible for surrender. IVP, KVP,LIC Policy need not be treated as NPA subject to Adequate margin.

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

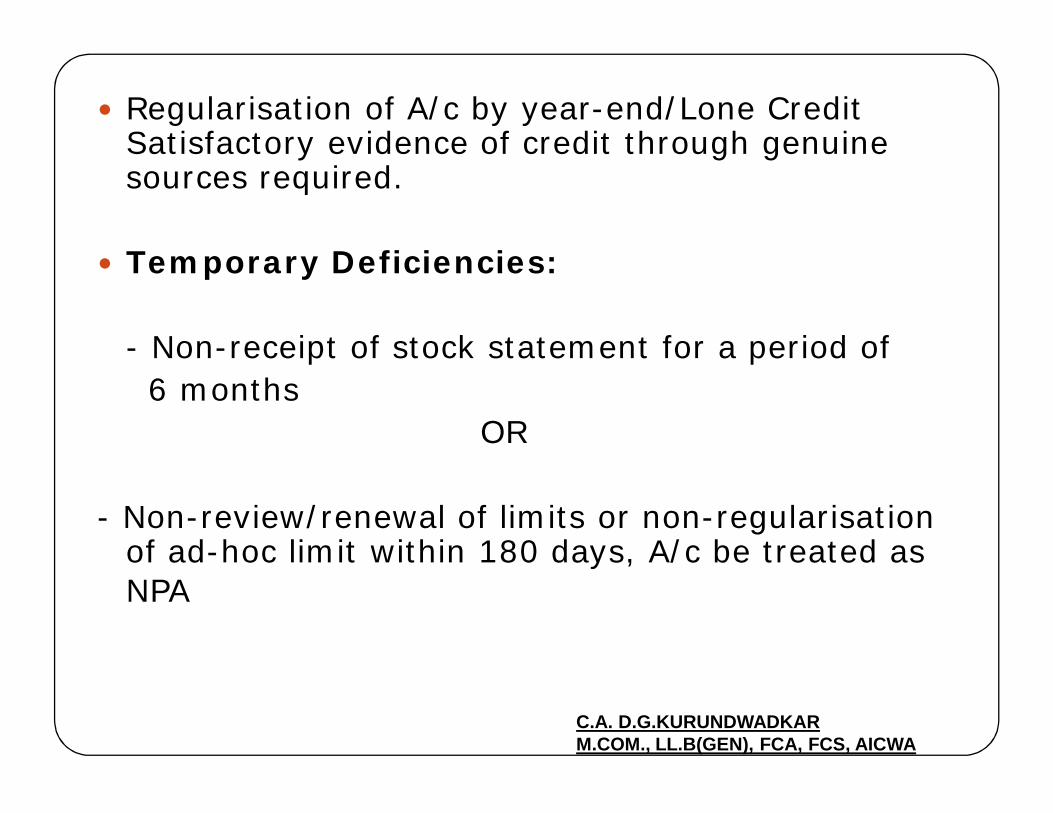

Regularisation of A/c by year-end/Lone Credit Satisfactory evidence of credit through genuine sources required.

Temporary Deficiencies:

- Non-receipt of stock statement for a period of6 months

OR

- Non-review/renewal of limits or non-regularisation of ad-hoc limit within 180 days, A/c be treated as NPA

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

Net Worth of Borrower/Guarantor or Availability of Security not deciding factors for NPA status

Determination of NPA : Borrower-wise, Not Facility wiseDevolvement of letters of credit or invoked guarantees credited to separate A/c are to be considered for applicationof Prudential Norms.

Project Finance under Moratorium Period :A/c become overdue after due date of payment ofinstallment or interest

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

Advances to Staff : Interest Portion to beconsidered as overdue as per the terms of sanction letter only.

Consortium Advances : Classification of borrowalA/c according to own record of recovery of the concerned bank.

Apportioned Limits & Transfer of A/cs from otherBranches

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

Threat to recovery :

In case of potential threat to recovery, on account of erosion in value of security, non-availability of security or fraud committed by borrower :

Realizable value of security is less than 50% -can be classified as a doubtful asset

Realizable value less than 10% - can be directly classified as Loss Asset.

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

Provisioning on performing & non-performing Assets :

a) Provision is required to be made in respect of allthe A/cs categories as “Standard ,Sub-standard, Doubtful & Loss”

b) Provision to be made as under:

i) Loss Assets:

The entire amount should be written off. If the assets are permitted to remain in the books for any reason, 100 percent of the outstanding should be provided for.

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

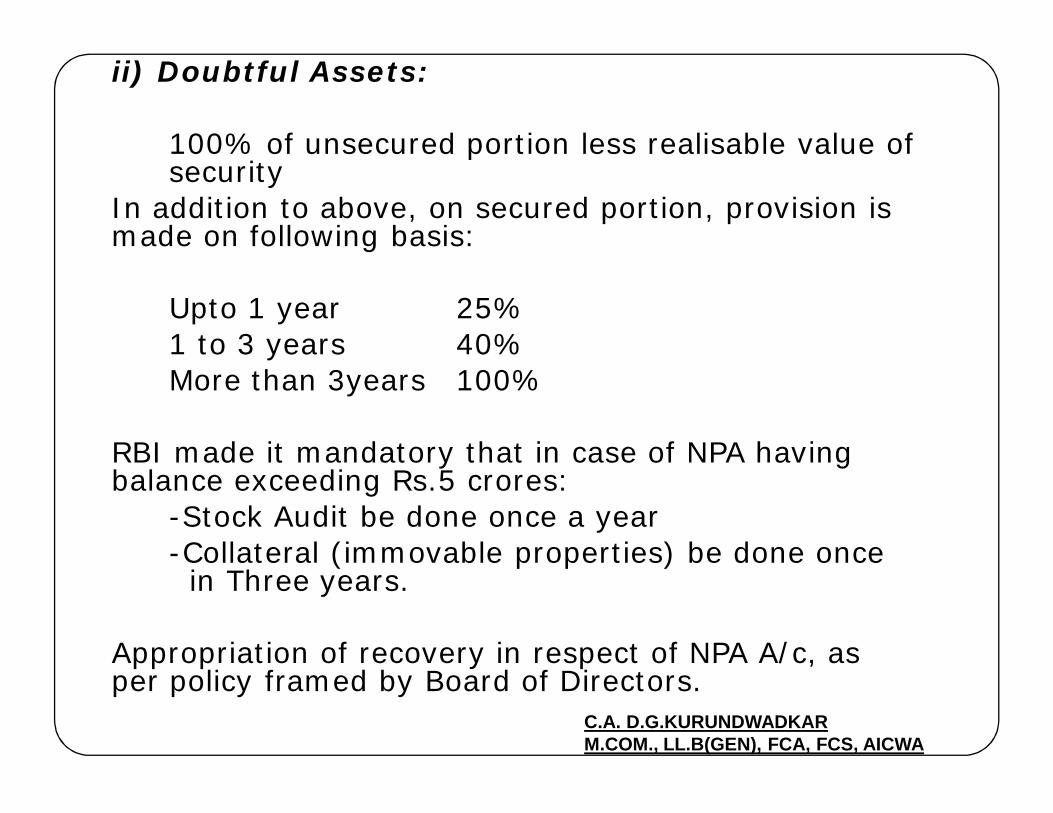

ii) Doubtful Assets:

100% of unsecured portion less realisable value of security

In addition to above, on secured portion, provision is made on following basis:

Upto 1 year 25%1 to 3 years 40%More than 3years 100%

RBI made it mandatory that in case of NPA having balance exceeding Rs.5 crores:

-Stock Audit be done once a year-Collateral (immovable properties) be done once in Three years.

Appropriation of recovery in respect of NPA A/c, as per policy framed by Board of Directors.

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

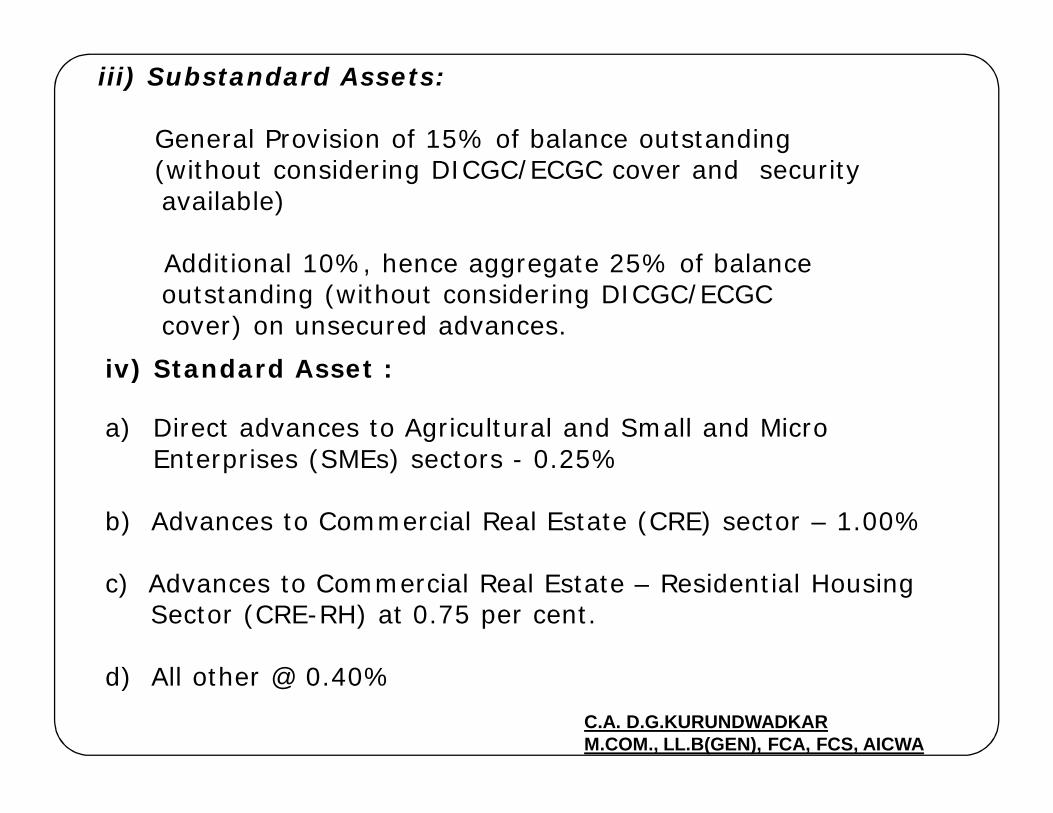

iii) Substandard Assets:

General Provision of 15% of balance outstanding(without considering DICGC/ECGC cover and security available)

Additional 10%, hence aggregate 25% of balance outstanding (without considering DICGC/ECGCcover) on unsecured advances.

iv) Standard Asset :

a) Direct advances to Agricultural and Small and MicroEnterprises (SMEs) sectors - 0.25%

b) Advances to Commercial Real Estate (CRE) sector – 1.00%

c) Advances to Commercial Real Estate – Residential HousingSector (CRE-RH) at 0.75 per cent.

d) All other @ 0.40%

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

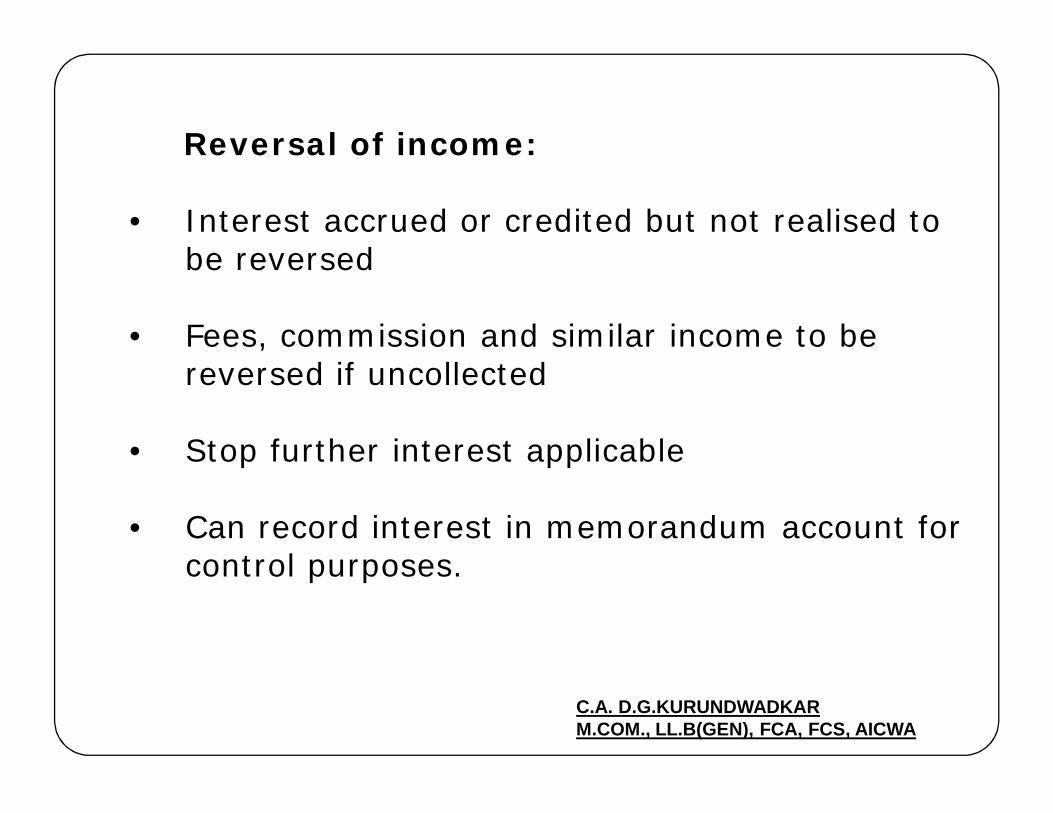

Reversal of income:

• Interest accrued or credited but not realised tobe reversed

• Fees, commission and similar income to be reversed if uncollected

• Stop further interest applicable

• Can record interest in memorandum account forcontrol purposes.

C.A. D.G.KURUNDWADKAR M.COM., LL.B(GEN), FCA, FCS, AICWA

THANK YOU