Embed Size (px)

Citation preview

The Fiber of NationsDECEMBER, 2008

A d v e rt i s i N G F e At U r e

Little did he realize it at the time, but Adam Smith, the eminent Scottish economist, wrote a book pertinent to fiber deploy-ment and policy in 1776 — more than 150 years before the exist-ence of fiber optics. In his work titled An Inquiry into the Nature and Causes of the Wealth of Nations, Smith describes the notion of an "invisible hand", referencing the ability of mar-kets to correct themselves with minimal intervention on the part of government or other organizations.

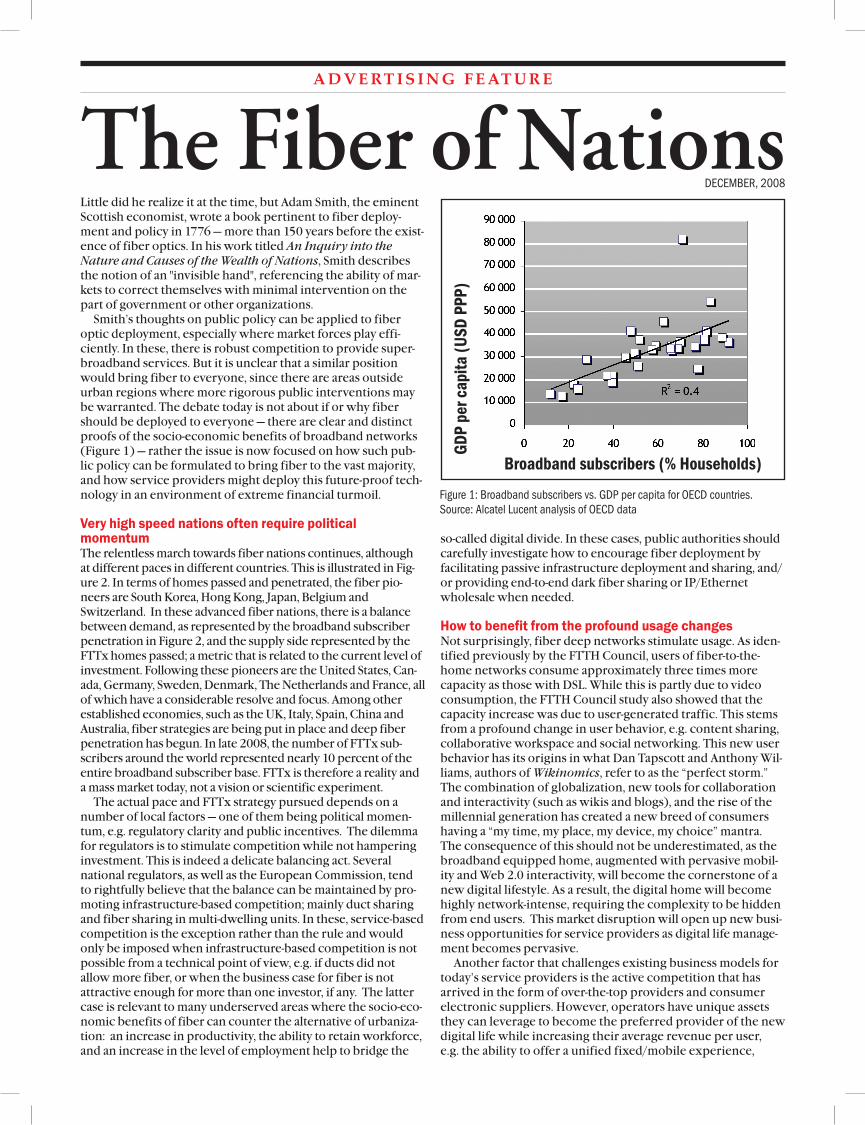

Smith’s thoughts on public policy can be applied to fiber optic deployment, especially where market forces play effi-ciently. In these, there is robust competition to provide super-broadband services. But it is unclear that a similar position would bring fiber to everyone, since there are areas outside urban regions where more rigorous public interventions may be warranted. The debate today is not about if or why fiber should be deployed to everyone — there are clear and distinct proofs of the socio-economic benefits of broadband networks (Figure 1) — rather the issue is now focused on how such pub-lic policy can be formulated to bring fiber to the vast majority, and how service providers might deploy this future-proof tech-nology in an environment of extreme financial turmoil.

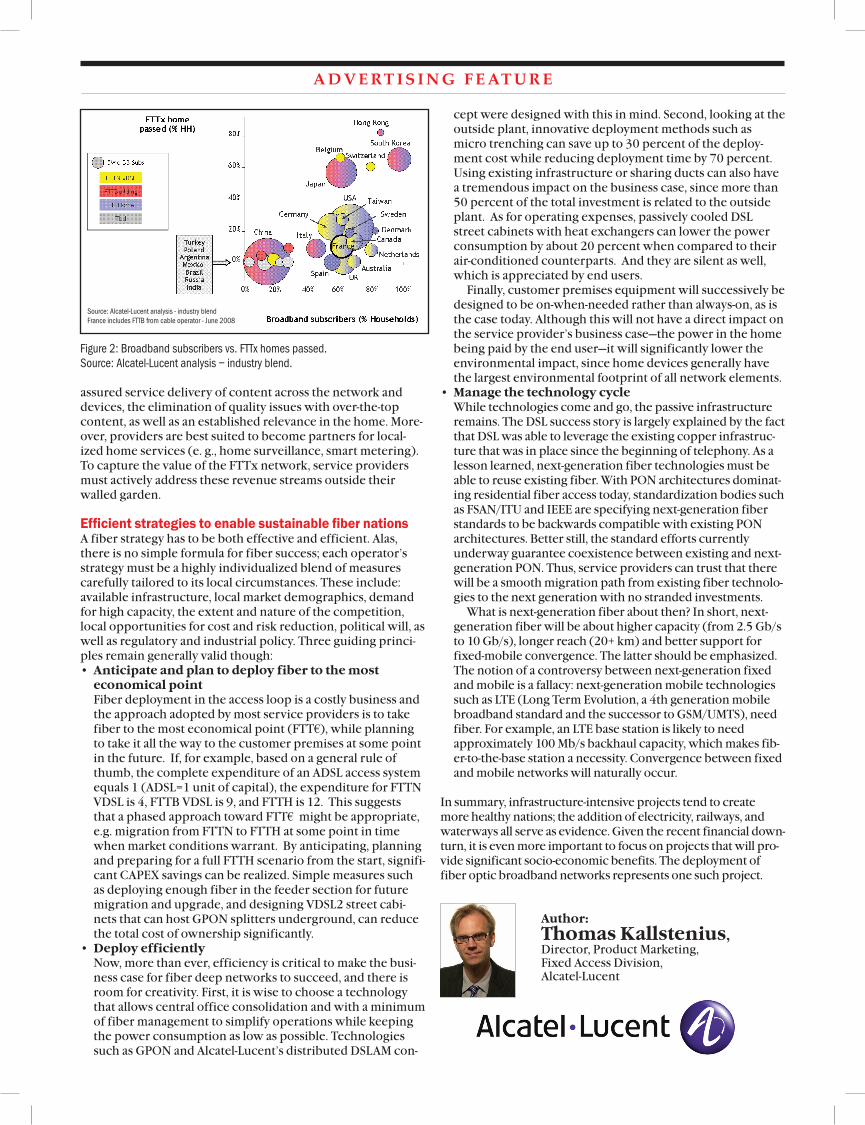

Very high speed nations often require political momentumThe relentless march towards fiber nations continues, although at different paces in different countries. This is illustrated in Fig-ure 2. In terms of homes passed and penetrated, the fiber pio-neers are South Korea, Hong Kong, Japan, Belgium and Switzerland. In these advanced fiber nations, there is a balance between demand, as represented by the broadband subscriber penetration in Figure 2, and the supply side represented by the FTTx homes passed; a metric that is related to the current level of investment. Following these pioneers are the United States, Can-ada, Germany, Sweden, Denmark, The Netherlands and France, all of which have a considerable resolve and focus. Among other established economies, such as the UK, Italy, Spain, China and Australia, fiber strategies are being put in place and deep fiber penetration has begun. In late 2008, the number of FTTx sub-scribers around the world represented nearly 10 percent of the entire broadband subscriber base. FTTx is therefore a reality and a mass market today, not a vision or scientific experiment.

The actual pace and FTTx strategy pursued depends on a number of local factors — one of them being political momen-tum, e.g. regulatory clarity and public incentives. The dilemma for regulators is to stimulate competition while not hampering investment. This is indeed a delicate balancing act. Several national regulators, as well as the European Commission, tend to rightfully believe that the balance can be maintained by pro-moting infrastructure-based competition; mainly duct sharing and fiber sharing in multi-dwelling units. In these, service-based competition is the exception rather than the rule and would only be imposed when infrastructure-based competition is not possible from a technical point of view, e.g. if ducts did not allow more fiber, or when the business case for fiber is not attractive enough for more than one investor, if any. The latter case is relevant to many underserved areas where the socio-eco-nomic benefits of fiber can counter the alternative of urbaniza-tion: an increase in productivity, the ability to retain workforce, and an increase in the level of employment help to bridge the

so-called digital divide. In these cases, public authorities should carefully investigate how to encourage fiber deployment by facilitating passive infrastructure deployment and sharing, and/or providing end-to-end dark fiber sharing or IP/Ethernet wholesale when needed.

How to benefit from the profound usage changesNot surprisingly, fiber deep networks stimulate usage. As iden-tified previously by the FTTH Council, users of fiber-to-the-home networks consume approximately three times more capacity as those with DSL. While this is partly due to video consumption, the FTTH Council study also showed that the capacity increase was due to user-generated traffic. This stems from a profound change in user behavior, e.g. content sharing, collaborative workspace and social networking. This new user behavior has its origins in what Dan Tapscott and Anthony Wil-liams, authors of Wikinomics, refer to as the “perfect storm.” The combination of globalization, new tools for collaboration and interactivity (such as wikis and blogs), and the rise of the millennial generation has created a new breed of consumers having a “my time, my place, my device, my choice” mantra. The consequence of this should not be underestimated, as the broadband equipped home, augmented with pervasive mobil-ity and Web 2.0 interactivity, will become the cornerstone of a new digital lifestyle. As a result, the digital home will become highly network-intense, requiring the complexity to be hidden from end users. This market disruption will open up new busi-ness opportunities for service providers as digital life manage-ment becomes pervasive.

Another factor that challenges existing business models for today’s service providers is the active competition that has arrived in the form of over-the-top providers and consumer electronic suppliers. However, operators have unique assets they can leverage to become the preferred provider of the new digital life while increasing their average revenue per user, e.g. the ability to offer a unified fixed/mobile experience,

Figure 1: Broadband subscribers vs. GDP per capita for OECD countries. Source: Alcatel Lucent analysis of OECD data

GDP

per c

apita

(USD

PPP

)Broadband subscribers (% Households)

A d v e rt i s i N G F e At U r e

assured service delivery of content across the network and devices, the elimination of quality issues with over-the-top content, as well as an established relevance in the home. More-over, providers are best suited to become partners for local-ized home services (e. g., home surveillance, smart metering). To capture the value of the FTTx network, service providers must actively address these revenue streams outside their walled garden.

Efficient strategies to enable sustainable fiber nationsA fiber strategy has to be both effective and efficient. Alas, there is no simple formula for fiber success; each operator’s strategy must be a highly individualized blend of measures carefully tailored to its local circumstances. These include: available infrastructure, local market demographics, demand for high capacity, the extent and nature of the competition, local opportunities for cost and risk reduction, political will, as well as regulatory and industrial policy. Three guiding princi-ples remain generally valid though:

Anticipate and plan to deploy fiber to the most •economical pointFiber deployment in the access loop is a costly business and the approach adopted by most service providers is to take fiber to the most economical point (FTT€), while planning to take it all the way to the customer premises at some point in the future. If, for example, based on a general rule of thumb, the complete expenditure of an ADSL access system equals 1 (ADSL=1 unit of capital), the expenditure for FTTN VDSL is 4, FTTB VDSL is 9, and FTTH is 12. This suggests that a phased approach toward FTT€€ might be appropriate, e.g. migration from FTTN to FTTH at some point in time when market conditions warrant. By anticipating, planning and preparing for a full FTTH scenario from the start, signifi-cant CAPEX savings can be realized. Simple measures such as deploying enough fiber in the feeder section for future migration and upgrade, and designing VDSL2 street cabi-nets that can host GPON splitters underground, can reduce the total cost of ownership significantly. Deploy efficiently•Now, more than ever, efficiency is critical to make the busi-ness case for fiber deep networks to succeed, and there is room for creativity. First, it is wise to choose a technology that allows central office consolidation and with a minimum of fiber management to simplify operations while keeping the power consumption as low as possible. Technologies such as GPON and Alcatel-Lucent’s distributed DSLAM con-

cept were designed with this in mind. Second, looking at the outside plant, innovative deployment methods such as micro trenching can save up to 30 percent of the deploy-ment cost while reducing deployment time by 70 percent. Using existing infrastructure or sharing ducts can also have a tremendous impact on the business case, since more than 50 percent of the total investment is related to the outside plant. As for operating expenses, passively cooled DSL street cabinets with heat exchangers can lower the power consumption by about 20 percent when compared to their air-conditioned counterparts. And they are silent as well, which is appreciated by end users.

Finally, customer premises equipment will successively be designed to be on-when-needed rather than always-on, as is the case today. Although this will not have a direct impact on the service provider’s business case—the power in the home being paid by the end user—it will significantly lower the environmental impact, since home devices generally have the largest environmental footprint of all network elements. Manage the technology cycle•While technologies come and go, the passive infrastructure remains. The DSL success story is largely explained by the fact that DSL was able to leverage the existing copper infrastruc-ture that was in place since the beginning of telephony. As a lesson learned, next-generation fiber technologies must be able to reuse existing fiber. With PON architectures dominat-ing residential fiber access today, standardization bodies such as FSAN/ITU and IEEE are specifying next-generation fiber standards to be backwards compatible with existing PON architectures. Better still, the standard efforts currently underway guarantee coexistence between existing and next-generation PON. Thus, service providers can trust that there will be a smooth migration path from existing fiber technolo-gies to the next generation with no stranded investments.

What is next-generation fiber about then? In short, next-generation fiber will be about higher capacity (from 2.5 Gb/s to 10 Gb/s), longer reach (20+ km) and better support for fixed-mobile convergence. The latter should be emphasized. The notion of a controversy between next-generation fixed and mobile is a fallacy: next-generation mobile technologies such as LTE (Long Term Evolution, a 4th generation mobile broadband standard and the successor to GSM/UMTS), need fiber. For example, an LTE base station is likely to need approximately 100 Mb/s backhaul capacity, which makes fib-er-to-the-base station a necessity. Convergence between fixed and mobile networks will naturally occur.

In summary, infrastructure-intensive projects tend to create more healthy nations; the addition of electricity, railways, and waterways all serve as evidence. Given the recent financial down-turn, it is even more important to focus on projects that will pro-vide significant socio-economic benefits. The deployment of fiber optic broadband networks represents one such project.

Source: Alcatel-Lucent analysis - industry blend France includes FTTB from cable operator - June 2008

Author: Thomas Kallstenius, Director, Product Marketing, Fixed Access Division, Alcatel-Lucent

Figure 2: Broadband subscribers vs. FTTx homes passed. Source: Alcatel-Lucent analysis – industry blend.