Embed Size (px)

DESCRIPTION

For 31 years, Advocate magazine has served attorneys who represent plaintiffs in Southern California

Citation preview

Journal of Consumer AttorneysAssociations for Southern California

June 2013

“OPEN, Sesame!”Is there is a magic word to open up the insurer’s policy limits?

INSURANCEFrom brokers and agents to the bad-faith trial

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:56 PM Page 1

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 2

©20

13 M

arc

Frie

dlan

d/C

reat

ive

Inte

llige

nce,

Inc.

/LA

-NY

THE LAW FIRM YOU’VE BEEN ABLE TO TRUST WITH YOUR CASE FOR OVER 35 YEARS

If you’re referring your clients for litigation, don’t settle for

To explore Joint Venture and Referral Relationships, please or

WWW.GREENE-BROILLET.COM

Named Top Tier Los Angeles Law Firm for personal injury, product liability and professional malpractice law by U.S. News–Best Lawyers®

Named the Top Listed Personal Injury Law Firm in California by Best Lawyers®

Named one of the “Top Plaintiff’s Law Firms in America” by the National Law Journal

Named as Top 10 Super Lawyers by Southern California Super Lawyers® Magazine

The only plaintiff’s firm with 4 of the top 100 Southern California Super Lawyers® for 2013

Multiple Lawyers of the Year winners by U.S. News – Best Lawyers

2 of the Top 10 impact verdicts of 2012 by Daily Journal

Multiple Trial Lawyer of the Year award winners by Consumer Attorneys Association of Los Angeles

NAMED TOP TIER LAW FIRM NATIONWIDE BY U.S. NEWS — BEST LAWYERS® IN PRODUCT LIABILITY

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 1

©20

13 M

arc

Frie

dlan

d/C

reat

ive

Inte

llige

nce,

Inc.

/LA

-NY

THE LAW FIRM YOU’VE BEEN ABLE TO TRUST WITH YOUR CASE FOR OVER 35 YEARS

If you’re referring your clients for litigation, don’t settle for

To explore Joint Venture and Referral Relationships, please or

WWW.GREENE-BROILLET.COM

Named Top Tier Los Angeles Law Firm for personal injury, product liability and professional malpractice law by U.S. News–Best Lawyers®

Named the Top Listed Personal Injury Law Firm in California by Best Lawyers®

Named one of the “Top Plaintiff’s Law Firms in America” by the National Law Journal

Named as Top 10 Super Lawyers by Southern California Super Lawyers® Magazine

The only plaintiff’s firm with 4 of the top 100 Southern California Super Lawyers® for 2013

Multiple Lawyers of the Year winners by U.S. News – Best Lawyers

2 of the Top 10 impact verdicts of 2012 by Daily Journal

Multiple Trial Lawyer of the Year award winners by Consumer Attorneys Association of Los Angeles

NAMED TOP TIER LAW FIRM NATIONWIDE BY U.S. NEWS — BEST LAWYERS® IN PRODUCT LIABILITY

Advocate Jun13 issue2_Advocate template 2007.qxd 5/22/2013 1:24 PM Page 2

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 3

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 7:04 PM Page 4

JUNE 2013 The Advocate Magazine — 5

� � � � � � � � � � � � � � � � � � � � �

One of Nevada’s largest and highestrated personal injury law � rms

© 2013 RHLF

� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

“Rick is one of the best lawyers in the country. I call him every time I have any issue in Nevada and would not hesitate to refer him any type of case of any size. We recently settled a Nevada case for multi-seven � gures after two days of mediation. Rick was masterful in dealing with the retired judge mediator, the defense team, and our clients, and he

maximized the recovery. Whenever I need anything in Nevada, the Richard Harris Law Firm is there for me.”

~ C. Michael Alder, Esq., CAALA Past President,CAALA Trial Lawyer of the Year 2004

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 5

6 — The Advocate Magazine JUNE 2013

ContentsContentsFeatures:

Advertising Sales: Neubauer & Associates, Inc. Chris Neubauer - Sales Manager. 760-721-2500 Fax: 760-721-0294e-mail: [email protected] Rate card available online at www.theadvocatemagazine.com

Submitting articles for publication: Check the annual editorial calendar at www.theadvocatemagazine.com to see when yourlegal topic would be most appropriate. Articles on time sensitive matters are welcome throughout the year, as are opinion columns,humor pieces, human-interest stories, lifestyle and personality features. Send your article as a WordPerfect or Word documentattachment to e-mail: [email protected]. Please check the website for complete editorial requirements.

Reprint permission: E-mail written request to Managing Editor Cindy Cantu: [email protected]

14

24

36

50

74

80

62

85

What do we do with Du?Have the courts resolved whether insurers must make settlement offers,or just respond to offers?Sharon Arkin

The overlooked benefits of Coverage “P” in generalliability policiesCoverage “P” affords coverage beyond physical injury and property damage,including privacy and disparagement claims.Kirk Pasich

HMO bad faith Using legislative history to take on Martin v. PacifiCare.Carolina Rose and Jeffrey Ehrlich

California’s ban on discretionary clauses indisability and life insuranceCalifornia Insurance Code section 10110.6: When it applies and how it standsup to ERISA preemption.Brent Brehm and Corrine Chandler

Winning punitive damages for insurance bad faithYour guide to the bad-faith trial from voir dire through closing statement.Ricardo Echeverria

“OPEN, Sesame!”Is there a magic word to open up the insurer’s policy limits? The authorsexplore the nuances of litigation that can result in the lid being taken off thepolicy.Mark Algorri and Carolyn Tan

Insurance agent or insurance broker – what’sin a name? Why it’s a distinction with a difference.Robert S. Gianelli and Jully C. Pae

Should California provide drivers’ licensesregardless of immigration status? The author suggests that driving privilege cards and provisional licenses,along with buying plenty of Uninsured Motorist Coverage, are the onlylogical methods of improving public safety. Barry P. Goldberg

Volume 40, Number 6, JUNE 2013

Editor-in-ChiefJeffrey EhrlichAssociate EditorsJoseph Barrett, Mary Bennett, Joan Kessler, James Kristy,Beverly Pine, Norman Pine, Rahul Ravipudi, Linda Rice,Ibiere Seck, Geraldine WeissEditors-in-Chief EmeritiKevin Meenan, William Daniels, Steven Stevens, Christine Spagnoli, Thomas StolpmanManaging EditorCindy [email protected] EditorEileen Goss

Consumer Attorneys Association of Los AngelesPresidentLisa MakiPresident-ElectGeoffrey WellsFirst Vice PresidentJoseph BarrettSecond Vice PresidentDavid Ring

Board of GovernorsMartin Aarons, Mike Armitage, Shehnaz Bhujwala, ToddBloomfield, John Blumberg, Michael Cohen, Scott Corwin,Jeffrey Ehrlich, Mayra Fornos, Stuart Fraenkel, ScottGlovsky, Steve Goldberg, Jeff Greenman, Christa Haggai-Ramey, Genie Harrison, Arash Homampour, Neville Johnson,Bill Karns, Aimee Kirby, James Kristy, Lawrence Lallande,Anthony Luti, Shawn McCann, Minh Nguyen, Linda FermoyleRice, David Rosen, Jeffrey Rudman, Ibiere Seck, DouglasSilverstein, Armen Tashjian, Kathryn Trepinski, GeraldineWeiss, Jeff Westerman, Ronnivashti Whitehead, AndrewWright, Dan Zohar

Orange County Trial Lawyers AssociationPresidentScott CooperPresident-ElectCasey JohnsonFirst Vice PresidentTed WackerSecond Vice PresidentVincent HowardThird Vice PresidentH. Shaina Colover

Board of DirectorsMelinda S. Bell, Gregory G. Brown, Anthony W. Burton,Brent W. Caldwell, Cynthia A. Craig, Jerry N. Gans, RobertB. Gibson, Paul E. Lee, Kevin G. Liebeck, Christopher E.Purcell, Solange E. Ritchie, Sarah C. Serpa, Adina T. Stern,Douglas B. Vanderpool, Janice M. Vinci, Atticus N. Wegman

Periodicals postage paid at Los Angeles, California.Copyright © 2013 by the Consumer Attorneys Association of Los Angeles. All rights reserved. Reproduction in whole or in part without written permission is prohibited.

ADVOCATE (ISSN 0199-1876) is published monthly at thesubscription rate of $50 for 12 issues per year by theConsumer Attorneys Association of Los Angeles,800 West Sixth Street, #700, Los Angeles, CA 90017(213) 487-1212 Fax (213) 487-1224 www.caala.org

POSTMASTER:Send address changes to ADVOCATEc/o Neubauer & Associates, Inc.P.O. Box 2239Oceanside, CA 92051

TreasurerRicardo EcheverriaSecretaryMichael AriasImmediate Past PresidentMichael AlderExecutive DirectorStuart Zanville

PublisherRichard [email protected]

SecretaryGeraldine LyTreasurerB. James PantoneParliamentarianJonathan DworkImmediate Past PresidentDouglas SchroederExecutive DirectorJanet Thornton

Art DirectorDavid Knopf

88

90

8

99

12

105

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 6

JUNE 2013 The Advocate Magazine — 7

On the cover:Main Image: Opening the Vault | iStockphoto | www.thinkstockphotos.com

“Open, Sesame” was the magic phrase used by Ali Baba in the story Ali Baba and the Forty Thieves.The words opened the cave in which the forty thieves had hidden a treasure.

88

90

Independent Cumis counsel: The second prongWhen the insured is given the right to choose counsel and control its owndefense.Kim Collins

Insurance strategies for mediationA look at the fundamental insurance issues that arise at mediation.Edward Susolik

Departments:

8

99

12

105

ABOUT THIS ISSUEInsurance: Coverage and bad faithGuidance from some of the best plaintffs’insurance lawyers in Southern California.Jeffrey Isaac Ehrlich

FROM THE EXECUTIVE DIRECTORConsumer Attorneys Association of Los AngelesThe Court funding crisisShocking numbers and wordsthat will make a difference.Stuart Zanville

Appellate Reports and cases in briefRecent cases of interest to members of theplaintiffs’ bar.Jeffrey Isaac Ehrlich

FROM THE PRESIDENTOrange County Trial Lawyers AssociationJoin in the fight against MICRA.Support “38 is too late”Scott Cooper

DIRECTORY OF ADVERTISERSCALENDAR OF EVENTS

CAALA RESOURCE CENTERCAALA Webinar Library –Resources FREE for membersFree educational Webinarsare now available for FREEon demand at caala.org

FROM THE PRESIDENTConsumer Attorneys Association of Los AngelesA message for petand animal loversShare your stories aboutspecial pets in the CAALA community.Lisa Maki

106107

108

Advocate Jun13 issue2_Advocate template 2007.qxd 5/22/2013 12:18 PM Page 7

This year we have a great insuranceissue. In fact, we have so many articlesthat space is at a premium, so I have tokeep this “about this issue” column veryshort. My brevity should not be seen asan absence of gratitude to each of theauthors for sharing their wisdom. KirkPasich once again contributed an article,this year on advertising-injury coverage.This is one of the least-understood kindsof insurance coverage, but as Kirk pointsout, it can be critical. His article is agreat place to start.

I have new authors this year. MarkAlgorri and Carolyn Tan have written anarticle on the various ways that an insurermay “open up” a liability policy by failingto settle within policy limits. This can bethe difference between a $15,000 recoveryand multi-million dollar for your client.Also Kim Collins, a career defense lawyer,explains some of the finer points aboutwhen insurers must provide independentcounsel for their insured because theylack a financial interest in the outcome ofthe underlying case.

If you were to ask experienced plain-tiffs (or defense) lawyers to name the

plaintiffs’ lawyers with the most knowledgeabout insurance, that list would likelyinclude the following names: Rob Gianelli,Ed Susolik, Ricardo Echeverria, andSharon Arkin. I have articles from each ofthem in this issue. Robert S. Gianelli andJully C. Pae have written an article thatcanvasses California law on the often-con-fusing area of broker/agent liability. SharonArkin has written on the Ninth Circuit’sdecisions in Du v. Allstate. Du I createdsomething of a firestorm of controversyabout whether an insurer had an affirma-tive duty to settle a case. Du II somewhatsidestepped the issue, but Sharon showswhy you need to know about both deci-sions. Ricardo has written at what he isparticularly adept – trying an insurancebad-faith case. His article is the next-bestthing to second-chairing a trial with him.And Ed Susolik has written on what maybe the most important issue of all to theplaintiff ’s practice – how to use insuranceissues to leverage settlement in mediation.

These articles would make for a goodissue, but as they say on TV, “But wait,there is more.” Brent Brehm and CorinneChandler have explained how California

law now forbids the use of “discretionary”clauses in life, disability, health, and acci-dental-death insurance policies, and howERISA is likely to impact that legislation.

Carolina Rose, an expert on Californialegislative history, has co-written an articlewith me concerning Health & Safety Codesection 1371.25, which courts have con-strued to abolish vicarious liability forclaims against HMOs. Carolina shows how,properly evaluated, the legislative historyfor that statute shows that the courts aregetting it wrong.

Finally, Barry Goldberg has written avery topical article on whether — fromthe standpoint of public safety and unin-sured-motorist coverage — Californiashould provide drivers licenses to undoc-umented immigrants.”

My thanks go to each author.Writing good articles is hard work. So,too, is putting an issue of this magazinetogether. And every month Cindy Cantu,David Knopf, Eileen Goss, and oftenRich Neubauer make it happen. I get thesexy title – “Editor in Chief.” And theydo the hard work of making a bunch ofarticles into a magazine.

8 — The Advocate Magazine JUNE 2013

Maximizing Results.MATTHEW MCNICHOLAS JOHN MCNICHOLAS PATRICK MCNICHOLAS

Rewarding relationships.McNicholas & McNicholas has worked with lawyers throughout Los Angeles, California, and the country on a wide variety of cases including: massive personal injury, wrongful death, employment, civil rights, train and trucking accidents, aviation accidents, and sexual abuse. The firm’s partners have been listed in Super Lawyers for eight consecutive years, recognized by the Daily Journal as Top 100 Lawyers in California, The American Board of Trial Advocates, The American College of Trial Lawyers, and the International Academy of Trial Lawyers. The firm realizes the importance of referrals and the benefit clients receive when successful lawyers

work together to reach a common goal—winning.

�ree generations of lawyers, one law �rm, a united purpose. Yours.

HIGH SEVEN FIGURES2011 referral and joint-venture fees

NEAR 10 FIGURES results for clients in the last decade

HIGH EIGHT FIGURES 2011 client awards

LOS ANGELES, CA | www.mcnicholaslaw.com | 866-664-3055

Jeffrey Isaac EhrlichEditor-in-Chief

From theEditor

Jeffrey Isaac EhrlichEditor-in-Chief

By Jeffrey Isaac EhrlichEditor-in-Chief

Aboutthis Issue

Jeffrey Isaac Ehrlich

Aboutthis Issue

Book Review

Insurance: Coverage and bad faithGuidance from the best plaintiffs' insurance lawyers in Southern California

Cut Costs and Save Timewith Deposition Summaries by 4 CORNERS

Look for us in CAALA Vegas 2013, Booth 228

�Quality service

�5 business days or fewer turnaround

�Standard 2 column with Headers and TOC

�Ability to handle large volume jobs

1.888.460.7444www.4cornersdepo.com

Cut Costs and Save Timewith Deposition Summaries by 4 CORNERS

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 8

Maximizing Results.MATTHEW MCNICHOLAS JOHN MCNICHOLAS PATRICK MCNICHOLAS

Rewarding relationships.McNicholas & McNicholas has worked with lawyers throughout Los Angeles, California, and the country on a wide variety of cases including: massive personal injury, wrongful death, employment, civil rights, train and trucking accidents, aviation accidents, and sexual abuse. The firm’s partners have been listed in Super Lawyers for eight consecutive years, recognized by the Daily Journal as Top 100 Lawyers in California, The American Board of Trial Advocates, The American College of Trial Lawyers, and the International Academy of Trial Lawyers. The firm realizes the importance of referrals and the benefit clients receive when successful lawyers

work together to reach a common goal—winning.

�ree generations of lawyers, one law �rm, a united purpose. Yours.

HIGH SEVEN FIGURES2011 referral and joint-venture fees

NEAR 10 FIGURES results for clients in the last decade

HIGH EIGHT FIGURES 2011 client awards

LOS ANGELES, CA | www.mcnicholaslaw.com | 866-664-3055

Insurance: Coverage and bad faithGuidance from the best plaintiffs' insurance lawyers in Southern California

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 9

10 — The Advocate Magazine JUNE 2013

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 10

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 11

I am not a numbers person, I preferwords. Maybe it’s because I was nevergood at math (it took me three tries topass high school algebra), and I’ve alwayspreferred verbal communication over sta-tistics.

But when it comes to the CaliforniaCourt funding crisis, there are somenumbers I want to share with you: • $1.1 billion (Amount cut from theCalifornia’s Court budget since 2007)• $161 million (Amount cut from theL.A. County Superior Court budget since2010)• 60 (Courthouses closed in California)• 10 (Courthouses closed in L.A. County)• 31 (California counties that havereduced the hours their Courts’ publicwindows are open)• 38 (California counties that havereduced their Courts’ self-help services)• 16 (California counties that have closedtraffic court locations)• 4 (L.A. County courthouses that nowhear landlord-tenant disputes)• 5 (L.A. County courthouses that nowhear small claims cases)

These are shocking numbers to any-one who believes in the Constitution andits guarantees of access to justice for all,not just the rich and powerful.

Justice delayedAs the Court changes that were man-

dated by the budget cuts begin to takeeffect, one unavoidable and highly dam-aging consequence is delay. Justicedelayed is justice denied and these days,a lot of justice is being denied inCalifornia.

California Supreme Court JusticeGordon Liu recently said, “Civil suits arethe bread and butter of our daily livesand delays will force people to find otherways to settle disputes.”

In June of last year L.A. SuperiorCourt Judge Mary Ann Murphy wrote in

this magazine, “Further budget cuts mayusher a return to master calendar, thecalendar congestion of the 1970’s, 1980’sand early 1990’s and five years to trial.”

She quoted from a Rand Institutefor Civil Justice study that the long waitto trial caused a “profound crisis” thatimpeded access to justice in the LosAngeles Superior Court. “Frustrated liti-gants may accept a settlement ratherthan wait for an open courtroom andmay lose faith in the court’s ability toresolve disputes.”

Judge Murphy surmised, “Furtherbudget cuts may cause the unthinkable –a return to the master calendar. Mastercalendar is a highly inefficient utilizationof court resources that would likely causea return to five years to trial.”

Unfortunately, in the year since thatarticle appeared and through no fault ofthe Court, Judge Murphy’s worst-casescenario has become the new normal.

A recent report from the Trial CourtPresiding Judges Advisory Committeequoted a representative of the L.A.Superior Court with powerful wordsabout the impact of the delays that willbe caused by the budget cuts:

Delay is pernicious. It takes holdincrementally. There will be no catas-trophe, only a slow and inexorabledecline. Delay allows everyone to con-tinue to pretend there is access to jus-tice. Only after months or years ofwaiting will one litigant at a time real-ize how the system has failed.Courthouse doors are being closed

and no amount of teeth-gnashing, hand-wringing or finger-pointing will changethe reality that our Courts are in gravedanger.

The power of wordsWhat will make a difference are

words. Words that must be spoken byConsumer Attorneys on behalf of the

people you stand up for every day. Wordsthat must be heard by California’s law-makers to better understand the impor-tance of the Courts and the serviceConsumer Attorneys perform forCalifornians of all creeds, colors, reli-gions and socioeconomic circumstances.

Whether you are talking to yourelected officials or to your friends andneighbors, educate them about what youdo each day to create a safer California,and that public safety is at risk withoutCourts that are accessible.

Explain that closing Courts hitsespecially hard at our state’s most vulner-able citizens; the less fortunate, the poor,veterans and the disabled.

Be clear that this is not about thelawyers. The Courts and the civil justicesystem protect people from unsafe prod-ucts, unsafe medicine, unfair businesspractices and negligent corporate con-duct.

Individuals, including corporateinterests, must be held accountable whenthey do something wrong, harmful orillegal and the civil justice system levelsthe legal playing field and guaranteesthat ordinary people get a fair shake incourt.

As California’s revenues increase, thestate has the money to repair the exten-sive damage done to our judicial systemas a result of years of budget cuts.

Two months ago the U.S. Congresspassed emergency legislation that fixeddelays at the nation’s airports caused bythe sequestration furlough of air trafficcontrollers. The bill was passed in a mat-ter of days after legislators were besiegedwith complaints from their constituents.

The time for California’s legislatureto act to address the impact of delays inthe Courts is now, and now is the timefor your voice to be heard. Contact me [email protected]. �

The Court funding crisisShocking numbers and words that will make a difference

Stuart ZanvilleConsumer Attorneys Association of Los Angeles

From theExecutive Director

12 — The Advocate Magazine JUNE 2013

Advocate Jun13 issue2_Advocate template 2007.qxd 5/22/2013 11:28 AM Page 12

AcupuncturistAnesthesiologistCardiologistChiropractorDentistGeneral SurgeonImaging CenterPM&R

Physical TherapistPlastic SurgeonPodiatristPrimary CarePsychiatristPsychologistPulmonologistNeurologist

NeuropsychiatristNeuropsychologistOphthalmologistMedical LabOrthopedistOtolaryngologistPain ManagementPharmacy

Advocate Jun13 issue2_Advocate template 2007.qxd 5/22/2013 11:28 AM Page 13

In June 2012, the initial publisheddecision issued by the Ninth CircuitCourt of Appeals in Du v. Allstate Ins. Co.(9th Cir. 2012) 681 F.3d 1118 (“Du I”)created a firestorm in the insuranceindustry. The decision issued after denialof rehearing in October 2012 (Du v.Allstate Ins. Co. (9th Cir. 2012) 697 F.3d753 [“Du II”] spread the fire to the plain-tiffs’ insurance bad-faith bar.

The “central legal issue” the NinthCircuit purported to address in Du I –and which it neatly dodged in Du II –was this: “Does an insurer have a duty,after liability of the insured has becomereasonably clear, to attempt to effectuatea settlement in the absence of a demandfrom the claimant?” (Du I, at 1122.)

In Du I, the court first discussed thegeneral duty of good faith and fair deal-ing of an insurer to settle a third-partyliability claim against its insured “withinpolicy limits ‘when there is substantiallikelihood of a recovery in excess of thoselimits,’” citing Kransco v. American EmpireSurplus Lines Ins. Co. (2000) 23 Cal.4th390. But, as the court went on to pointout, the duty to settle has been common-ly applied “to situations in which theinsurer unreasonably rejects a settlementoffer within policy limits. “ (Id., at 1123.)The Du I court, however, concluded thatthe duty applies more broadly andrequires “an insurer to effectuate settle-ment when liability is reasonably clear,even in the absence of a settlementdemand.” (Ibid.)

Ultimately, despite its conclusionthat such a duty existed, the Du I courtheld that the evidence in the trial courtdid not support giving the jury aninstruction to that effect.

Not surprisingly, the insurer soughtrehearing of the decision. “Within daysof the Ninth Circuit’s June 11, 2012opinion, the court received dozens ofamicus letters and briefs urging the court

to grant rehearing or certify the case tothe California Supreme Court.”(DiMugno & Glad, California InsuranceLaw Handbook, § 11:196, Comment.)

In its October 2012 amended deci-sion, the court noted that Du’s appealraised the issue of whether the duty ofgood faith and fair dealing can bebreached in the absence of a settlementdemand by the third party, and brieflysummarized the cases and arguments oneither side of the issue. Ultimately, how-ever, the court declined to resolve thatlegal question because it was unnecessaryto do so in light of the fact that theinsured did not present adequate evi-dence to support that claim in any event.

So what do we do with Du?In both Du I and Du II, the Ninth

Circuit identified a hotly contested issuein insurance bad-faith law: Does a liabili-ty insurance company have an affirmativeduty to attempt to settle a third-partyclaim against its policyholder without asettlement demand from the third party?

Du II does not give us a definitiveanswer. So, what do we do with that?

Well, the first thing we don’t do iscite Du I. That decision was supersededby Du II and it is therefore unciteable.But that doesn’t mean that – as policy-holders’ counsel – we can’t adapt theanalysis applied by the Ninth Circuit inDu I. We can – and should.

Think before you leapOne caveat before going through the

analysis: Make sure you have a strongcase on the facts before you try to makethis argument and especially before youtry to appeal it. The old law-schoolmaxim that “bad facts make bad law” istrue – especially in the insurance bad-faith context. Even when you have agreat case on the facts, the insurancecompany will do its level best (meaning it

will do its worst) to argue that the com-pany was “set up” and that the bad faithwas all on the part of the policyholderand/or the third party. Making bad lawfor everyone else just to promote yourown marginal case is a grave disservice toevery other injured third party and, inthe long run won’t help your client any-way. So think before you leap.

Obviously, the best way to deal withthe issue is to avoid it altogether. If you arecounsel for the injured third party, provideall the relevant documentation and infor-mation the insurance company reasonablyneeds to assess its insured’s liability andyour client’s damages and make a reason-able settlement offer. You can do it “early”in the case so long as you have a strong lia-bility case and damages clearly in excess ofthe policy limits. Yes, by making a settle-ment offer, you take the risk that the insur-ance company will accept the offer andyour client will not be able to “blow the lidon the policy.” But if you don’t provide therelevant information, you and your clientare at far greater risk that the bad-faithcase will go south on you and you will beleft with nothing but the bill for the costspaid and the loss of months of litigationtime on a case-to-nowhere that could havebeen spent on more productive litigation.

If you are bad-faith counsel, youpretty much have to take the facts as theyare and work with what you have. Butthat doesn’t mean you should take a runat every case. The trial and appellatecourts – especially in these days of severebudget cuts – are looking for ways to getrid of cases and will not tolerate over-reaching. Be smart with your time andthe court’s resources and leave the mar-ginal cases alone.

How do you make the argument?The California Supreme Court has

unequivocally established that the

14 — The Advocate Magazine JUNE 2013

What do we do with Du?Are insurers required to offer settlements before the claimant asks?

Sharon J. Arkin

Du continues

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 14

What do we do with Du?Are insurers required to offer settlements before the claimant asks?

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 15

Du — continued

implied covenant of good faith and fairdealing in an insurance policy “obligatesthe insurance company, among otherthings, to make reasonable efforts to set-tle a third party’s lawsuit against theinsured.” (PPG Industries, Inc. v.Transamerica Ins. Co. (1999) 20 Cal.4th310, 312.) One of the primary reasonsfor the imposition of this duty on aninsurer is the inherent conflict created bythe circumstances: The policyholderwants the claim to settle within the policylimits in order to avoid personal liability;and the company wants to settle theclaim for as little as possible. Without theduty of good faith as an incentive to set-tle within the policy limits, it would be inthe company’s best interest to simply letthe case go to trial and let the policy-

holder take the risk of an excess judg-ment, knowing that it would never paymore than the policy limit no matterwhat. (Merritt v Reserve Ins. Co. (1973) 34Cal.App.4th 858, 874.) Thus, the insur-ance carrier “must conscientiously try tostrike a balance between conflicting inter-ests” and must assess the claim “bothfrom its own point of view and from thatof the assured.” (Ibid.)

There is no question that the goodfaith duty to settle applies when a reason-able settlement demand within policylimits is made by the third party.(Johansen v. California State Auto. Ass’ninter-Ins. Bureau (1975) 15 Cal.3d 9, 16;Blue Ridge ins. Co. v. Jacobsen (2001) 25Cal.4th 489, 498; Merritt, supra.) Butmerely responding to a settlement

demand from the third party, rather thaninitiating settlement efforts, ignoresimportant statutory, regulatory and pub-lic policy obligations on the part of aninsurance company to make affirmativeefforts to resolve the litigation against itspolicyholder.

First, nothing in the controllingSupreme Court decisions even impliedlyjustifies conditioning the duty to settle onreceipt of a settlement demand from thethird party. (Comunale v. Traders &General Ins. Co. (1958) 50 Cal.2d 654,659-661; Crisci v. Security Ins. Co. of NewHaven, Conn. (1967) 66 Cal.2d 425, 429;Johansen, at 16-17.) And that makessense: While a settlement demand maycrystallize the existence of the conflict in

16 — The Advocate Magazine JUNE 2013

Victims of car crashes, slip & falls and other accidents often present foot, ankleand lower extremity injuries as a result of their trauma. We specialize in evaluating,diagnosing and treating personal injury patients to return them to their previousway of life. Call us today to see what we can do to help your client.

FOOT AND ANKLE SURGERIES ON LIEN

GLENDALE311 N. Verdugo Rd.Glendale, CA 91206

NORTH HOLLYWOOD 12626 Riverside Dr., Suite #510North Hollywood, CA 91607

BEVERLY HILLS6221 Wilshire Blvd., Suite #607Los Angeles, CA 90048

3 Convenient Southern California Locations

(818)409-9912www.drallenmassihi.com

We’ll get your clients back on their feetWe’ll get your clients back on their feet

Du continues

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 16

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 17

Du — continued

the mind of the company, the conflictitself manifestly exists irrespective ofwhether there is an actual demand. Inassessing the policyholder’s risk, theinsurer “must conduct itself as though italone were liable for the entire amountof the judgment” (Johansen, at 16) and, asa practical reality “no rational defendantwould sit back and allow a high exposurecase to go to trial without at leastattempting to settle simply because theplaintiff shows no interest in settling.”(DiMugno & Glad, California InsuranceLaw Handbook, § 11:196.)

Second, statutory provisions alsosupport the conclusion that a carrier can-not simply sit back and await a settle-ment demand. Insurance Code section790.03(h)(5) expressly provides that acarrier has a duty to attempt in “good

faith to effectuate prompt, fair and equi-table settlements of claims in which lia-bility has become reasonably clear.” Athird-party claimant cannot base a claimon violation of that statutory mandate.But the violation of that statutory man-date is evidence of the insurance compa-ny’s unreasonable conduct in an actionfor breach of the duty of good faith bythe policyholder or the policyholder’sassignee. (Jordan v. Allstate Ins. Co. (2007)148 Cal.App.4th 1062, 1078; Rattan v.United Services Auto. Association (2000) 84Cal.App.4th 715, 724.) Thus, the factthat the insurer failed to make any effortto attempt to settle the case in theabsence of a specific settlement demandmay be evidence of its breach of the duty ofgood faith. And that this is a justifiablebasis for imposition of liability is supported

by the fact that the Judicial Council hascrafted an approved jury instructionbased on violations of section 790.03(h)to be used in bad-faith cases. (CACI2337.)

Third, several cases have confirmedthe carrier’s duty to affirmativelyattempt to settle a claim in which liabil-ity is reasonably clear, even in theabsence of a settlement demand. InPray v. Foremost Ins. Co. (9th Cir. 1985)767 F.2d 1329, 1330, the Ninth Circuitspecifically found that “[i]t is reasonablyclear that California courts will inter-pret the California statute as imposingupon an insurance company the dutyactively to investigate and attempt tosettle a claim by making, and by accept-ing, reasonable settlement offers once

18 — The Advocate Magazine JUNE 2013

Du continues

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 18

JUNE 2013 The Advocate Magazine — 19

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 19

Du — continued

liability has become reasonably clear.”(Emphasis added.) Although the directenforceability of the mandates of sec-tion 790.03(h) is now precluded byMoradi-Shalal v. Fireman’s Fund Ins. Cos.(1988) 46 Cal.3d 287, such a violationis, as noted above, evidence of an insur-er’s breach of the duty of good faith.More importantly, Pray supports theconstruction and interpretation of sec-tion 790.03(h)(5) as requiring an affir-mative effort on the part of the carrierto make a settlement offer once liabilityis reasonably clear.

Boicourt v. Amex Assurance Co.Boicourt v. Amex Assurance Co. (2000)

78 Cal.App.4th 1390 provides powerfulsupport for the conclusion that a carrierhas a duty to take affirmative action tosettle a claim. In Boicourt, the injuredthird party requested disclosure from thecarrier of its policyholder’s policy limitsbefore filing suit. The carrier refused todisclose the limits, or even to contact itspolicyholder for permission to disclosethe limits. Five months into the litigation,the carrier offered the $100,000 policylimits – which the third party refused. Inthe subsequent bad-faith case, the trialcourt granted summary judgment infavor of the carrier, ruling that becausethe injured third party never made a for-mal settlement offer, the carrier did notbreach the covenant of good faith. The

appellate court rejected that conclusionand reversed the summary judgment.

In discussing the issue, Boicourt tiedits analysis to the fact by refusing to dis-close the policy limits, the carrier ham-pered the ability of the third-partyclaimant to even make a reasonable set-tlement offer and the carrier’s blanketpolicy could be evidence of bad faitheven in the absence of a settlement offerby the injured third party. The courtexpressly limited its holding by statingthat the decision was not intended to“explore the degree to which the impliedcovenant of good faith and fair dealingimposes on a liability insurer a duty to be‘proactive’ in settling cases.” (Id., at1400.)

But one thing the Boicourt opiniondoes is very strongly reject reliance onthe decision in Merritt v. Reserve Ins. Co.(1973) 34 Cal.App.3d 858, 877 for theproposition that a carrier can be in badfaith “only” if a reasonable settlementoffer is made by the third party claimantand unreasonably rejected by the carrier.As Boicourt extensively demonstrates,Merritt’s discussion of the issue is dicta –and nothing more. (Boicourt, at 1395-1397.) Among other considerations in itsrejection of Merritt’s dicta, Boicourt point-ed out that Merritt “did not reject thisbasis of liability on the legal ground thatan insurer need never ‘initiate settlementovertures,’ but on the particular facts of

the case before the court: There was noevidence at all to support the conjecturethat ‘overtures’ might have been fruitful.”(Boicourt, at 1396, fn. 3; emphasis inoriginal.)

Thus, Boicourt provides strong sup-port for the argument that Merritt – thecase usually relied on by carriers to arguethat they have no duty to make an offer –does not answer the question.

ConclusionThe simple reality is that this ques-

tion will not be resolved unless and untilthe Supreme Court actually decides it. Inthe meantime, it’s a valid argument tomake in the right factual setting. But,again, the best course of action is alwaysto make a reasonable settlement offerwithin policy limits as early in the case aspossible consistent with the availability ofinformation needed by the carrier tomake a reasonable determination.

Sharon J. Arkin is the principal of The Arkin Law Firm. She has been certifiedby the California State Bar, Board of LegalSpecialization as an appellate specialist since 2001. In 2011 Ms. Arkin received theCLAY award from California Lawyer magazine as an Appellate Attorney of the Yearand in 2012 was named one of the Top 50Women Attorneys in Southern Californiaby Los Angeles Magazine. E-mail:[email protected].

20 — The Advocate Magazine JUNE 2013

DARRYL H. GRAVER, ESQ.

818.884.8474fax 818.884.8388

EXPERIENCEDARBITRATOR/MEDIATOR

“Have Gavel Will Travel”Over 3,000 successful conclusions

TM

DARRYL H. GRAVER, ESQ.

818.884.8474fax 818.884.8388

To Schedule, call Judicate West 800.488.8805

EXPERT WITNESSLEGAL MALPRACTICE

Any underlying case/transaction,fee disputes, ethics, 45 years

Phillip Feldman, BS, MBA, JD, AV Preeminent (PEER Rated)

Bd. Cert. Legal Malpractice ABPLA & ABAAlso State Bar Defense

(818) 986-9890

www.LegalMalpracticeExperts.comE-mails: [email protected]

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 20

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 21

Advocate Jun13 issue2_Advocate template 2007.qxd 5/22/2013 12:18 PM Page 22

Mid S e v e n F i g u r e s ( a r m ampu t a t i o n )

M i d S e v e n F i g u r e s ( t r a uma t i c b r a i n i n j u r y )

M i d S e v e n F i g u r e s ( t r a uma t i c b r a i n i n j u r y )

L ow S e v e n F i g u r e s ( n e c k s u r g e r y )

L ow S e v e n F i g u r e s ( n e c k s u r g e r y )

L ow S e v e n F i g u r e s ( n e c k & b a c k s u r g e r y )

L ow S e v e n F i g u r e s ( l e g f r a c t u r e & p u n c t u r e d l u n g )

L ow S e v e n F i g u r e s ( l e g f r a c t u r e )

L ow S e v e n F i g u r e s ( b a c k s u r g e r y )

L ow S e v e n F i g u r e s ( t r a uma t i c b r a i n i n j u r y )

L ow S e v e n F i g u r e s ( n e c k s u r g e r y )

L ow S e v e n F i g u r e s ( a r m f r a c t u r e )

L ow S e v e n F i g u r e s ( a r m f r a c t u r e )

L ow S e v e n F i g u r e s ( n e c k & b a c k s u r g e r y )

L ow S e v e n F i g u r e s ( n e c k f r a c t u r e )

O v e r S e v e n F i g u r e s p a i d i n A s s o c i a t i o n F e e s i n 2 0 1 2

P e r s o n a l I n j u r y W r o n g f u l D e a t h M a s s To r t s

O u r V e r d i c t s & S e t t l e m e n t s

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:46 PM Page 23

24 — The Advocate Magazine JUNE 2013

In 1966, Coverage “P” was intro-duced as a standard form endorsementfor general liability insurance policies,adding coverage for claims alleging “per-sonal injury.” (Farbstein & Stillman,Insurance for the Commission of IntentionalTorts (1969) 20 Hastings L.J. 1219 (here-after “Farbstein”).) Before then, personalinjury coverage was not provided on astandard form basis. As one insuranceindustry publication explained:

Coverage of liability for libel, slan-der, false arrest, detention, maliciousprosecution, invasion of privacy, etc.has been written for many years under

non-standard forms. . . . [D]ifferencesin coverage and policy provisions arebecoming less common. These latterendorsements have even establishedthe quasi-official title of ‘PersonalInjury Liability’ insurance for this typeof coverage.

(Fire Casualty & Surety Bulletin, PersonalInjury Liability Coverage (second print-ing, May 1968) Public Liability, p.i-1.)

The Personal Injury endorsement wasadopted so that coverage would no longerbe “confined to those damages resultingfrom ‘bodily injury or property damage.’”(Farbstein, at 1238.) When introduced, the

endorsement extended coverage to injuryarising out of listed “offenses” beyondbodily injury and property damage.

The two most important features ofthe endorsement are the unrestricteduse of the term “injury” and the absenceof any requirement that the loss be“caused by an occurrence.” Thus, cover-age is afforded for any injury arising outof one of the scheduled torts, undoubt-edly extending to all forms of generaland special damages normally recover-able in actions predicated on these torts.

(Id. at 1239.)

The overlooked benefits of Coverage “P” in general liability policiesCoverage “P” affords coverage beyond physical injuryand property damage, including privacy and disparagement claims

Kirk A. Pasich

Overlooked continues

To

Advocate Jun13 issue2_Advocate template 2007.qxd 5/22/2013 11:28 AM Page 24

Makarem & AssociatesT O P L E G A L M A L P R A C T I C E L I T I G A T O R S

California State Bar Certified - Legal Malpractice Specialist

Daily Journal “Top 20 Under 40” Attorney in CA (2007)

SuperLawyer (2010, 2011, 2012)

We cooperate with referral fees and co-counsel relationshipsunder Rule 2-200 of the CA Rule of Professional Conduct.

C L I E N T - AT T O R N E Y F E E D I S P U T E S | E X P E R T W I T N E S S S E R V I C E S | AT T O R N E Y F I D U C I A R Y D U T I E S

3 1 0 . 3 1 2 . 0 2 9 9www.makaremlaw.com

11601 Wilshire Blvd., Suite 2440Los Angeles, CA 90025-1760 RON MAKAREM

We fight to uphold our legal profession

We litigatelegal malpractice.

Congratulations Ron!

Top 100 SuperLawyer — CA 2013

Advocate Jun13 issue2_Advocate template 2007.qxd 5/22/2013 11:28 AM Page 25

Overlooked — continued

Over the years, the coverage mor-phed, becoming part of the standard ISOCGL form rather than an endorsement.Later versions of the policy began com-bining personal injury and advertisinginjury coverage into a single form.

“Personal and advertising injury”coverage now typically obligates insurersto defend and indemnify their insuredsagainst claims alleging injury arising outof specified “offenses.” These offensestypically include the “[o]ral or writtenpublication, in any manner, of materialthat slanders or libels a person or organi-zation or disparages a person’s or organi-zation’s goods, products or services,” orthat “violates a person’s right of privacy,”or “[i]infring[es] upon another’s copy-right, trade dress or slogan” in an adver-tisement. (Commercial General LiabilityCoverage Form (ISO Properties, Inc.2006) § V.14.) This coverage extends to awide range of claims.

For example, courts have recognizedthat personal-injury provisions afford cov-erage for privacy claims. In St. Paul Fire &Marine Insurance Co. v. Green Tree FinancialCorp. (5th Cir. 2001) 249 F.3d 389, thecourt addressed coverage for claims thatdebt collectors contacted plaintiffs severaltimes per week and threatened to inform

their employers of their delinquency. Theinsurer argued that it had no duty todefend because there was no specific alle-gation of an invasion of privacy and thatthe claim was for “unfair debt collectionpractices.” The court held that the insur-er had a duty to defend, noting that thefactual allegations “clearly support acause of action for invasion of privacy.”(Id. at 394.) It explained that “becausefactual allegations may favor one cause ofaction over another does not alleviate aninsurer’s duty to defend if the facts poten-tially state a cause of action coveredunder the policy.” (Ibid.)

Disparagement claimsPersonal-injury coverage also pro-

vides broad protection for claims involv-ing disparagement. Commentators havelong said that personal-injury coveragefor disparaging statements “appears tocreate coverage for a wide range of eco-nomic injuries,” including “interferencewith a prospective advantage,” “inducinga third person to breach a contract [and]. . . stealing his customers . . . or tradesecrets, all [of which] may involve defam-atory or disparaging utterances or thepublication of private information.”(Farbstein, at 1240.)

For example, in Propis v. Fireman’sFund Insurance Co. (1985) 492 N.Y.S.2d228, the court considered allegations thatthe insured had interfered with theclaimant’s business activities by “contact-ing and communicating with others” andthat the insured maliciously interferedwith the claimant’s new contract andinduced a third party to discharge theclaimant. The court held that the person-al injury provisions provided coverage,stating:

We note that the material publishedor uttered need not, to be the basis ofa covered claim under [the personalinjury provision], constitute a libel orslander or be legally defamatory oreven allegedly false . . . [T]he defini-tion of ‘Personal Injury’ lists the cov-ered publications or utterances in thedisjunctive, i.e., ‘of a libel and slanderor of other disparaging or defamingmaterial’ . . . It is enough if theinsured has published or uttered ‘dis-paraging material’ – material which isderogatory or belittling. . . .

(Id. at 737-38.)In Atlantic Mutual Insurance Co. v. J.

Lamb, Inc. (2002) 100 Cal.App.4th 1017, the issue was whether certain

26 — The Advocate Magazine JUNE 2013

When myclients needfinancialassistanceprior tosettlementto cover theirexpenses,I trust myfriends atFund CapitalAmericato help.

Gary A. Dordick, Esq.Gary A. Dordick, Esq.Trial AttorneyLaw Offices of Gary A. Dordick

Complete Settlement SolutionsA client-centered team to preserve settlements and protect your clients• Security: Annuity and U.S. Treasury Bond Funded Structured Settlements• Protection: Special Needs Trust Services with Nationwide Network of

Trust Officers and Trust Attorneys• Growth: Asset Management• Medicare Compliance in Liability Cases• Medicare Set Aside Accounts with Professional and Self Administration• Coordination of Public Benefits with a Qualified Settlement Fund

WE ARE EXPERIENCED IN MASS TORTS NATIONWIDE

800-315-3335 • [email protected]

Jane Riley-Pugh

Overlooked continues

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:47 PM Page 26

When myclients needfinancialassistanceprior tosettlementto cover theirexpenses,I trust myfriends atFund CapitalAmericato help.

Gary A. Dordick, Esq.Gary A. Dordick, Esq.Trial AttorneyLaw Offices of Gary A. Dordick

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:47 PM Page 27

Overlooked — continued

communications with customers of a com-petitor fell within personal injury cover-age, thus triggering a duty to defend.The underlying complaint alleged that

the insured intentionally communicatedwith another company, falsely stating thatthe other company was selling productsthat were subject to the insured’s patent

claim. The court of appeal held that theallegations in the underlying complaint“clearly allege a disparagement of [theother company] as well as its products.”(See also Sentex Sys., Inc. v. HartfordAccident & Indem. Co. (C.D. Cal. 1995) 882F.Supp. 930 [allegation that insured madefalse or misleading statement about com-petitor or its products triggers duty todefend for claim of disparagement].)

Personal-injury coverage also hasbeen held to obligate insurers to defendantitrust lawsuits based on unsubstantiat-ed allegations in otherwise uncoveredclaims. As the Ninth Circuit Court ofAppeals explained:

[In] Ruder & Finn v. Seaboard Sur.(1981) 52 N.Y.2d 663, 439 N.Y.S.2d858, 422 N.E.2d 518 , . . . a New Yorkcourt determined that an insurancecompany had a duty to defend itsinsured against an antitrust action thatincluded an allegation of “false dispar-agement.” . . . The court rejected theinsurer’s argument that “two solitary,unsubstantiated words” buried within a“completely unrelated federal antitrustcause of action, which was, itself,undisputedly not covered” could nottrigger the duty to defend.

(Pension Trust Fund for Operating Eng’rs v.Fed. Ins. Co. (9th Cir. 2002) 307 F.3d 944,951 n.4.)

Thus, even if the focus of the lawsuitappears to be on allegations or claimsthat are not covered, this does not meanthat an insurer is excused from its dutiesto its insured. (See Horace Mann Ins. Co.v. Barbara B. (1993) 4 Cal.4th 1076, 1084 [duty to defend even if uncoveredclaim “is the ‘dominant factor’ in [the]case”].)

Another Ninth Circuit decision pro-vides an example of how the duty todefend is triggered based on a similarnotion of “two solitary, unsubstantiatedwords” buried in a complaint. InManzarek v. St. Paul Fire & Insurance Co.(9th Cir. 2008) 519 F.3d 1025, 1031,Robby Krieger and Ray Manzarek, two ofthe founding members of The Doors,had been sued by John Densmore, thedrummer of The Doors. Densmore

28 — The Advocate Magazine JUNE 2013

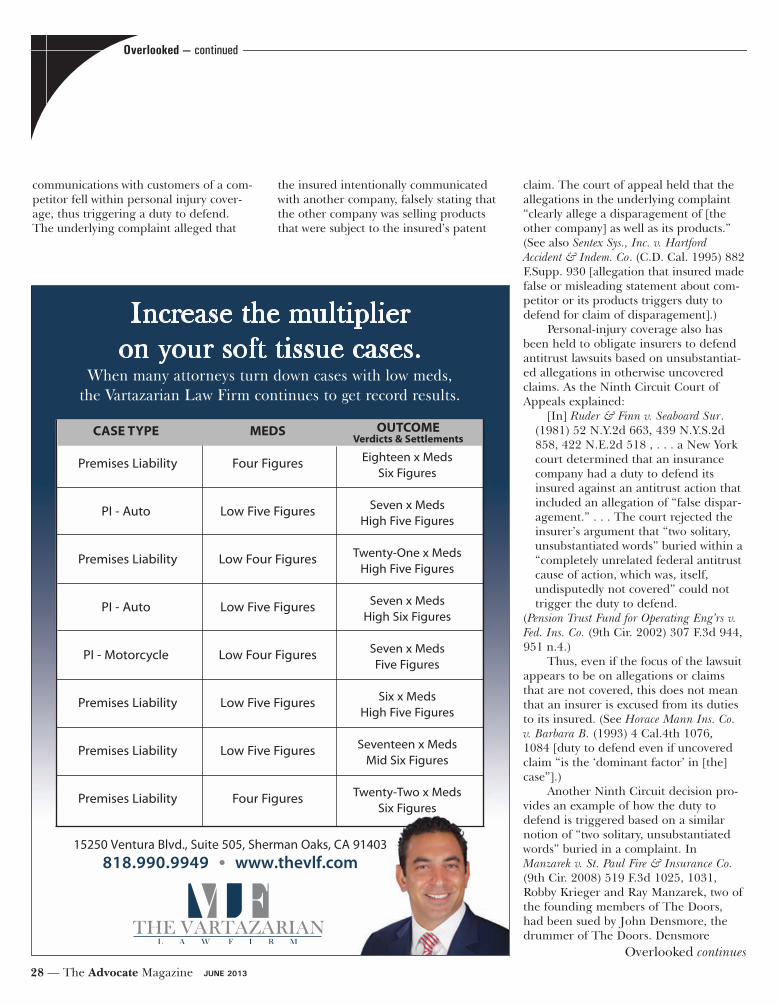

Increase the multiplieron your soft tissue cases.

When many attorneys turn down cases with low meds,the Vartazarian Law Firm continues to get record results.

Eighteen x MedsSix Figures

Seven x MedsHigh Five Figures

Twenty-One x MedsHigh Five Figures

Seven x MedsHigh Six Figures

Seven x MedsFive Figures

Six x MedsHigh Five Figures

Seventeen x MedsMid Six Figures

Twenty-Two x MedsSix Figures

Premises Liability Four Figures

PI - Auto Low Five Figures

Premises Liability Low Four Figures

PI - Auto Low Five Figures

PI - Motorcycle Low Four Figures

Premises Liability Low Five Figures

Premises Liability Low Five Figures

Premises Liability Four Figures

CASE TYPE MEDS

15250 Ventura Blvd., Suite 505, Sherman Oaks, CA 91403818.990.9949 • www.thevlf.com

OUTCOMEVerdicts & Settlements

Overlooked continues

Advocate Jun13 issue2_Advocate template 2007.qxd 5/22/2013 11:28 AM Page 28

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:47 PM Page 29

Overlooked — continued

alleged that Krieger and Manzarek, whowere touring as members of the band“The Doors of the 21st Century,” andtheir touring company, Doors Touring,Inc., were liable for infringing on TheDoors name, trademark, and logo inconjunction with tours and marketing.Densmore also alleged, in a single para-graph in his 68-paragraph complaint,that he had suffered damage to his “rep-utation and stature” because the infringe-ment caused people to believe “that hewas not, and is not, an integral andrespected part of The Doors band, or isone member who easily can be replacedby another drummer.” (Id. at 1033.)

Advertising injuryManzarek and Doors Touring noti-

fied their insurer, seeking coverage for

“advertising injury” (which includedlibel, slander, and disparagement) and“bodily injury” (which included mentalanguish and emotional distress). Theinsurer denied coverage. It first contend-ed that there was no coverage for thecopyright infringement and relatedclaims because the policy had an exclu-sion for claims arising in the “field ofentertainment,” which applied to thepublication and advertising of productsand materials in media. (Id. at 1032.)The insurer next claimed that Densmorehad not alleged “bodily injury.”

The Ninth Circuit disagreed. Itbegan by analyzing the duty to defend. Itemphasized that, “‘Any doubt as towhether the facts establish the existenceof the defense duty must be resolved inthe insured’s favor.’” (Id. at 1031.) The

court held that the field of entertainmentexclusion did not apply. It pointed outthat the exclusion would not apply, forexample, if Manzarek and Doors Touring“began distributing ‘The Door’s Own’ lineof salad dressing . . . because [they]would not necessarily publicize, distrib-ute, exploit, exhibit, or advertise inmedia such as motion pictures.” (Id. at1032-33.) It further noted that the exclu-sion also would not bar all coverage ifthey “began marketing a line of t-shirtsor electric guitars with The Doors logo or[Jim] Morrison’s likeness on them.” (Id.at 1033.) It then held that the insurerhad a duty to defend because the under-lying complaint was “silent about whattype of products and merchandise thatManzarek and [Doors Touring] produced

www.imeobservers.com 888.876.1483

Now offering Nurse Observers at a fraction of the cost

www.imeobservers.com 888.876.1483

Now offering Nurse Observers at a fraction of the costSERVING ALL OF SOUTHERN CALIFORNIA

We will send aDoctor to observe

your clients’ next DME!

Don’t let theDefense MedicalExam Ruinyour P.I. Case

We will send aDoctor to observe

your clients’ next DME!• DME Observation Services• DME Audio Recording• Medical Record Review• Expert Testimony• Discounts for CAALA Members

30 — The Advocate Magazine JUNE 2013

Overlooked continues

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:47 PM Page 30

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:47 PM Page 31

and marketed.” (Ibid.) This sufficed totrigger the defense duty.

The Ninth Circuit next turned to thequestion of whether the policy’s “bodilyinjury” coverage obligated the insurer todefend. It rejected the insurer’s argu-ment that there was no potential for“personal injury” coverage. It held thatthe allegations that Densmore’s “reputa-tion and stature” had been damagedwere “sufficient to raise the potential ofan award of mental anguish or emotionaldistress damages,” even though the com-plaint contained no emotional distresscause of action and did not refer to emo-tional distress.

A California Court of Appeal recentlyheld that the alleged disparaging state-ment may be implied from the allegationstriggering the duty to defend. (Travelers

Prop. & Cas. Co. of Am. v. Charlotte RusseHolding, Inc. (2012) 207 Cal.App.4th 969,978 [“[t]he underlying claims may triggera duty to defend if the conduct for whichthe policies provide coverage is chargedby implication, as well as by direct accusa-tion”].) Moreover, no cause of action fordisparagement or trade libel is needed totrigger coverage. “In order to trigger per-sonal injury coverage it is not essentialthat the underlying claims must beexpressly phrased in terms of ‘disparage-ment’ or trade libel.” (Ibid.)

In Travelers, the plaintiff alleged thatthe insured had damaged its brand by itssale of products at severely discountedprices. The insured sought coverageunder the advertising injury provisions ofthe policy, which included coverage for“[o]ral, written, or electronic publication

of material that slanders or libels a per-son or organization or disparages a per-son’s or organization’s goods.” (Id. at974.) Even though the complaint did notcontain a single allegation regarding anystatement by the insured, the court heldthat the insurer had a duty to defend. (Id.at 981.) In doing so, the court explainedthat the potential for coverage existedunder the policy’s definition of “advertis-ing injury” even though the plaintiff hadneither asserted a cause of action fortrade libel nor pled all of the elements oflibel or defamation. (Id. at 979-80.) Forcoverage purposes, the alleged disparag-ing statement was implied in the allega-tion that the insured’s conduct hadcaused damage to the plaintiff ’s brandand the marketability and saleability of itsproducts. As the court explained:

[T]he allegation of disparagementmay be implied. The question here, . . .therefore is not whether the underlyingclaims expressly allege that the [insured]parties disparaged [the claimant’s] prod-ucts, but whether the allegations may beunderstood to accuse the [insured] par-ties of statements and conduct “thatslanders or libels a person or organiza-tion or disparages a person’s or organi-zation’s goods, products or services . . . .

(Id. at 978-79.) The court also confirmed that it did

not matter whether the underlying law-suits involved a cause of action for tradelibel. It acknowledged that even if theclaim against the insureds

...could not be viable without alleg-ing all of the elements of a trade libelcause of action, . . . [t]he insurer’s dutyto defend is not conditioned on thesufficiency of the underlying pleading’sallegations of a cause of action; that isan issue for which the policy entitledthe [insured parties] to an insurer-funded defense.

(Id. at 979.) Finally, the court noted that con-

sumers might be confused as to the ori-gin, quality, and affiliation of theinsureds’ products:

[W]e cannot rule out the possibilitythat [the] pleadings could be understood

Overlooked — continued

OFFICES LOCATED NEXT TO THE TARMAC IN SANTA MONICA

310.392.5000www.baileypartners.com32 — The Advocate Magazine JUNE 2013

Overlooked continues

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:47 PM Page 32

Trust your referral to the team with proven resultsRecent Verdicts and Settlements

OFFICES LOCATED NEXT TO THE TARMAC IN SANTA MONICA

310.392.5000www.baileypartners.com

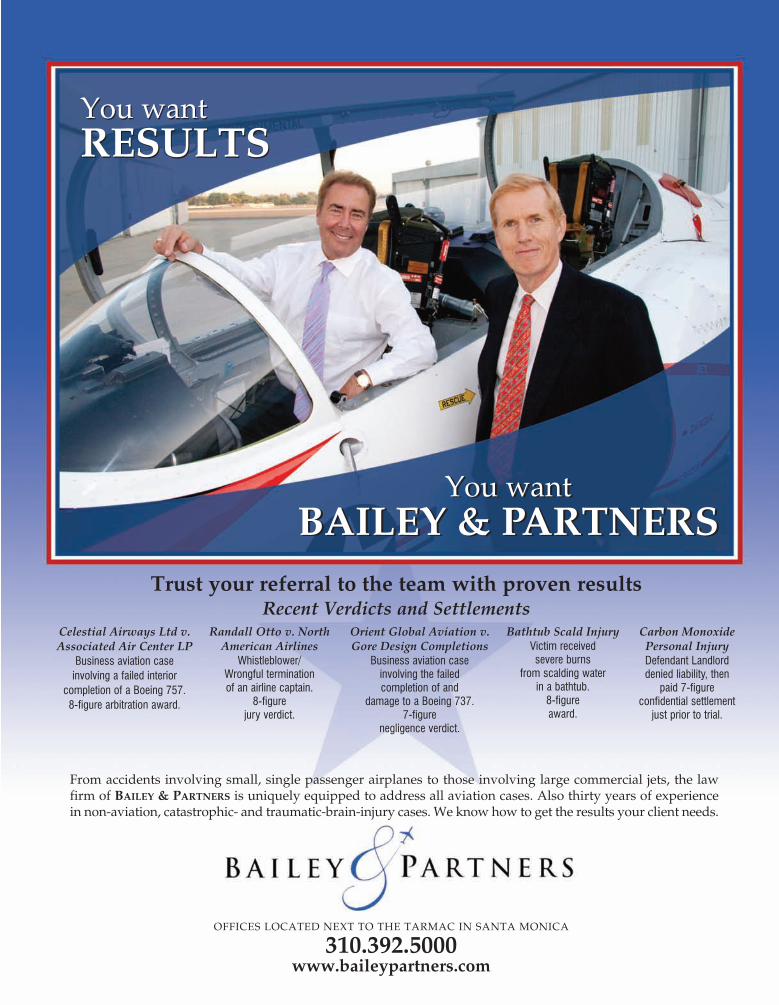

From accidents involving small, single passenger airplanes to those involving large commercial jets, the lawfirm of BAILEY & PARTNERS is uniquely equipped to address all aviation cases. Also thirty years of experiencein non-aviation, catastrophic- and traumatic-brain-injury cases. We know how to get the results your client needs.

You wantBAILEY & PARTNERS

You wantRESULTS

You wantBAILEY & PARTNERS

Bathtub Scald InjuryVictim receivedsevere burns

from scalding waterin a bathtub.

8-figureaward.

Randall Otto v. NorthAmerican Airlines

Whistleblower/Wrongful terminationof an airline captain.

8-figurejury verdict.

Celestial Airways Ltd v.Associated Air Center LP

Business aviation caseinvolving a failed interior

completion of a Boeing 757.8-figure arbitration award.

Orient Global Aviation v.Gore Design Completions

Business aviation caseinvolving the failedcompletion of and

damage to a Boeing 737.7-figure

negligence verdict.

Carbon MonoxidePersonal InjuryDefendant Landlorddenied liability, then

paid 7-figureconfidential settlement

just prior to trial.

You wantRESULTS

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:47 PM Page 33

Overlooked — continued

34 — The Advocate Magazine JUNE 2013

Proud Members Since 1999

Enter your client’s ZIP code on our Web site to be directed to the nearest location

Six Convenient LA County Locations

Submit

GR ANADA HILLS 818.363.8450

Same Day AppointmentMultilingual Doctors & Sta�

www.PVchiroinc.com818.834.6966

Colossus Related ReportsPrompt Reports & Billing

PATRICK PAREHJAN, D.C., I.D.E.

ARTIN KHODADADI, D.C.

VICTOR CALDERON, D.C.

ROBERT VARTZAR, D.C., Q.M.E.

RODRIK KHOSROVIAN, D.C.

STEPHEN PORTILLO, D.C.

GLENDALE 818.553.1790

PACOIMA 818.834.6966

MID WILSHIRE 213.381.0075

EAST LOS ANGELES 323.266.7800

HUNTINGTON PARK 323.588.4770

CAALA Affiliate Vendor

PACOIMA(818) 834-6966

GRANADA HILLS(818) 363-8450

HUNTINGTON PARK(323) 588-4770

EAST LOS ANGELES(323) 266-7800

MID WILSHIRE(213) 381-0075

GLENDALE(818) 553-1790

to charge that the dramatic discountsat which the . . . products were beingsold communicated to potential cus-tomers the implication — false, accord-ing to [the claimant] — that the prod-ucts were not (or that the [insured]parties did not believe them to be) pre-mium, high-end goods.

(Id. at 980.) Therefore, the court concluded that

an allegation of a disparaging statementwas implied based on the underlyingplaintiff ’s allegations regarding damageto its brand and the marketability of itsproducts.

Courts also have found that person-al-injury coverage applies to a variety ofclaims alleging interference with interestsattending to the possession or enjoymentof real property. (See, e.g., Fragomeno v.Ins. Co. of the West (1989) 207 Cal.App.3d

822, 828 [term “personal injury” obli-gates insurer to defend and indemnifyfor “any act constituting an invasion ofthe right of private occupancy whichincurs tort liability”].) Indeed, courtshave found coverage in a broad range ofcircumstances:• Battery made possible by trespass.(Hartford Accident & Indemnity Co. v.Krekeler (8th Cir. 1974) 491 F.2d 884.)• Conversion when repossession alleged-ly was accomplished by insured’s techni-cally deficient entry onto premises.(Cincinnati Insurance. Co. v. Davis (1980)265 S.E.2d 102.) • Enactment of zoning amendment limit-ing development. (Town of Stoddard v.Northern Security Insurance Co. (D.N.H.1989) 718 F.Supp. 1062.) • Interference with quiet enjoyment anduse of home from loud noise and unduly

bright night lighting. (Titan HoldingsSyndicate, Inc. v. City of Keene (1st Cir.1990) 898 F.2d 265.)• Race discrimination. (Gardner v.Romano (E.D. Wisc. 1988) 688 F.Supp.489; Clinton v. Aetna Life & Casualty Co.(Conn. Super. Ct. 1991) 594 A.2d 1046.)• Trespass, nuisance, and CERCLAclaims. (Martin-Marietta Corp. v. SuperiorCourt (1995) 40 Cal.App.4th 1113.)

Overlooking personal-injury cover-age can result in insureds not obtaining adefense paid for by their insurers forclaims that otherwise would be covered,and in less insurance money being avail-able for possible settlements of claims.

Kirk Pasich is a partner in the LosAngeles office of Dickstein Shapiro LLP. He is the Client Strategy Leader for the firm’sInsurance Coverage Group.

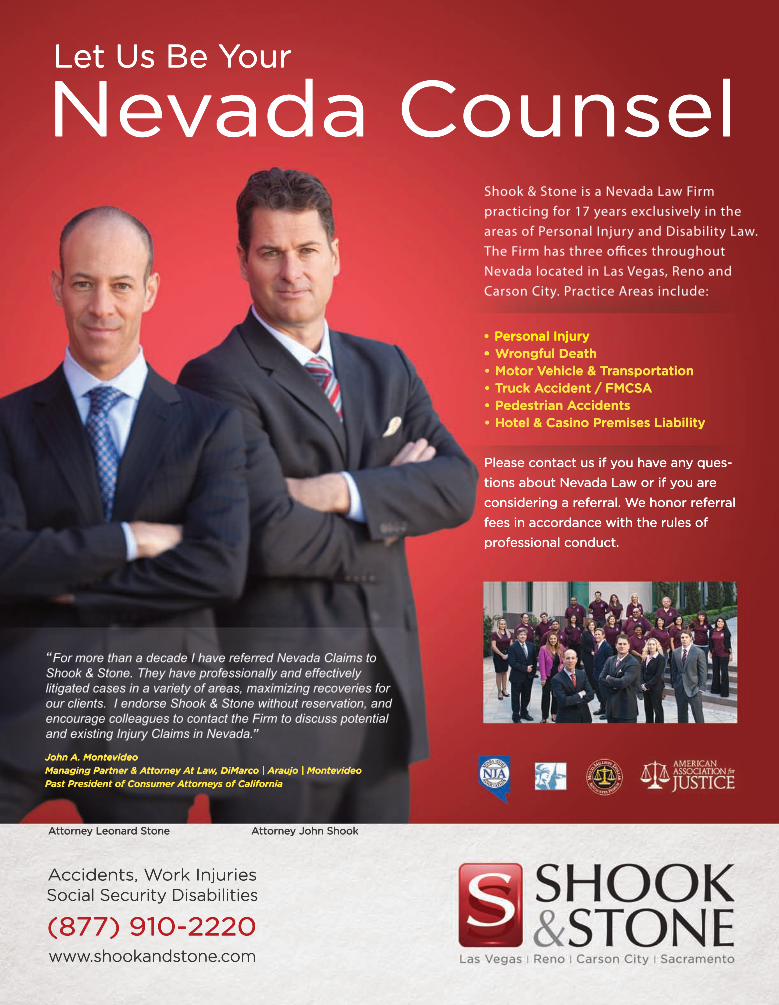

Shook & Stone is a Nevada Law Firmpracticing for 17 years exclusively in theareas of Personal Injury and Disability Law.The Firm has three o�ces throughoutNevada located in Las Vegas, Reno andCarson City. Practice Areas include:

�

�

For more than a decade I have referred Nevada Claims to Shook & Stone. They have professionally and effectively litigated cases in a variety of areas, maximizing recoveries for our clients. I endorse Shook & Stone without reservation, and encourage colleagues to contact the Firm to discuss potential and existing Injury Claims in Nevada.

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:47 PM Page 34

Shook & Stone is a Nevada Law Firmpracticing for 17 years exclusively in theareas of Personal Injury and Disability Law.The Firm has three o�ces throughoutNevada located in Las Vegas, Reno andCarson City. Practice Areas include:

“

”

For more than a decade I have referred Nevada Claims to Shook & Stone. They have professionally and effectively litigated cases in a variety of areas, maximizing recoveries for our clients. I endorse Shook & Stone without reservation, and encourage colleagues to contact the Firm to discuss potential and existing Injury Claims in Nevada.

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:47 PM Page 35

In 1995, the Legislature enactedHealth and Safety Code section 1371.25,at the behest of the CaliforniaPsychological Association (“CPA”). Thestated purpose of the bill was to preventhealth care service plans (HMOs), fromincluding draconian “hold harmless”provisions in their contracts with the pro-fessionals who provide medical services

to the HMOs’ subscribers (“providers”),forcing the providers to indemnify theHMOs for the HMOs’ wrongful denial ofservices.

The statutory language is brief – onlythree sentences. Section 1371.25 says:

A plan, any entity contracting with aplan, and providers are each responsi-ble for their own acts or omissions, and

are not liable for the acts or omissionsof, or the costs of defending, others.Any provision to the contrary in a con-tract with providers is void and unen-forceable. Nothing in this section shallpreclude a finding of liability on thepart of a plan, any entity contractingwith a plan, or a provider, based on the

36 — The Advocate Magazine JUNE 2013

HMO bad faith Using legislative history to take on Martin v. PacifiCare

Jeffrey Isaac Ehrlich Carolina Rose

HMO continues

GERALD P. HAWKINS©

Advocate Jun13 issue2_Advocate template 2007.qxd 5/22/2013 12:18 PM Page 36

HMO bad faith Using legislative history to take on Martin v. PacifiCare

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:47 PM Page 37

HMO — continued

doctrines of equitable indemnity, com-parative negligence, contribution, orother statutory or common law basesfor liability.

For many years, the statute appearedto serve its stated purpose and to do littleelse. But over time, HMOs began to relyon it as a virtual immunity shield against

bad-faith claims against them. TheHMOs argued that the statute eliminatedall claims against them based on vicari-ous liability for the conduct of theirproviders. They claimed that if an entitythey hired to make utilization-reviewdecisions wrongfully refused to providecoverage, and a subscriber sufferedinjury, that subscriber had no claimagainst the HMO itself – only a claimagainst the provider. The only situationwhere HMOs claimed they could be heldliable was if the subscriber appealed theproviders’ decision to the HMO, and theHMO affirmed it.

Plaintiffs argued that this approachstood the concept of insurance bad faithon its head. After all, it was the HMOs –not their contracted providers – whostood in contractual privity with the sub-scribers. California law was settled thatthe tort of bad faith followed the line ofcontractual privity. As a result, when aninsurer denied a claim and was sued forbad faith, the claim had to be maintainedagainst the insurer; not against theadjuster who the insurer hired to adjustthe claim. This was the holding ofGruenberg v. Aetna Ins. Co. (1973) 9 Cal.3d566. And it was also well established thatan insurer’s duty of good faith and fairdealing was non-delegable. (Hughes v.Blue Cross of Northern California (1989)215 Cal.App.3d 832.)

Plaintiffs argued that the purpose ofsection 1371.25 was to outlaw the type ofhold-harmless provisions that the CPAcomplained about, and the Legislatureachieved that goal in an inelegant, buteffective way. The first sentence of thestatute, standing alone, did abolish theconcept of vicarious liability for HMOs.The second sentence – which was the keyprovision – then outlawed all contractswith HMOs that were inconsistent withthe principle. And then the third sen-tence operated as a saving clause, essen-tially re-establishing the basic principlesof common-law liability: “Nothing in thissentence shall preclude a finding of liabil-ity on the part of a plan . . . based on thedoctrines of equitable indemnity, compar-ative negligence, contribution, or otherstatutory or common law bases for liability.”

38 — The Advocate Magazine JUNE 2013

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:47 PM Page 38

The first published opinion to con-sider the issue was Watanabe v. CaliforniaPhysicians’ Service (2008) 169 Cal.App.4th56.) The Watanabe court adopted theHMO’s view, finding that it was nonsensi-cal to interpret the third sentence as re-establishing the liability that the first sen-tence abolished. But the Watanabe courtrefused to review the statute’s legislativehistory, finding that the statutory mean-ing was so clear on its face that there wasno need to do so.

In Martin v. PacifiCare of Cal. (2011)198 Cal.App.4th 1390, the court didconsider the statute’s legislative history,and it decided that it supported theWatanabe court’s construction of thestatute. As a result, it affirmed a nonsuitin a bad-faith lawsuit and wrongful-deathagainst PacifiCare arising out of thedenial by its contracted provider, BrightMedical Group (“Bright”). The claimalleged that Bright refused to authorizethe treatment that its subscriber, ElsieMartin, needed to treat a cerebralaneurysm. She had been referred to spe-cialists at USC for care that Bright’s owndoctors could not provide, but Brightneedlessly sent her to those doctors any-way, delaying her care for months. Elsie’saneurysm burst before she got the treat-ment she needed.

Relying on Watanabe, the trial courtgranted nonsuit in favor of PacifiCare,finding that the only claim available toElsie’s family was against Bright itself, notPacifiCare. (Full disclosure, one of the co-authors of this article, Jeff Ehrlich, wasappellate counsel for the Martin family.)In this article, legislative history expertCarolina Rose has reviewed the Martincourt’s legislative-history analysis, andconcludes that the Martin court got itwrong. I will let Carolina take it from here.

The Martin Court The Martin court did not correctly

apply the legislative history and intent ofHealth and Safety Code section 1371.25as added by Stats. 1995, Chapter 774,Sec. 2, Assembly Bill (AB) 1840(Figueroa) when it reached this decision:

We agree with Watanabe that section1371.25’s plain language prevents a

health care service plan from being heldvicariously liable for a medical provider’sacts or omissions. Our examination of section 1371.25’s legislative history fur-ther supports that conclusion.

[Emphasis added. Martin, 198Cal.App.4th at p.1392.]

It is a confusing reality that an entitythat is authorized under the Knox-Keeneact to be a “provider” of medical healthcare services to patients can also contractwith the health care service insuranceplan to serve in a separate, strictlyadministrative manner as the plan’s con-tract agent to determine if medical serv-ices requested by one of the “provider’s”roster of licensed medical professionalsmade on behalf of an insured patient aremedically necessary and should thereforebe covered by the plan.

Such gatekeepers of insurance cover-age are known as medical utilizationreview (UR) contractors or agents. (URservices can also be provided by the planitself or another entity who does not alsoprovide medical health care services tothe plan.)

In Martin, Bright, the licensed“provider” of health care services forPacifiCare, was also PacifiCare’s URagent. PacifiCare paid Bright extra just todo the UR. The patient harm at issuewas caused by Bright in its capacity as theplan’s UR agent – not in its capacity asPacifiCare’s “provider” of medical healthcare services. Unfortunately, the Martincourt attributed Bright’s UR decision toits “provider” status.

As the court saw it, the applicationof 1371.25 was simple: (1) Bright was alicensed “provider” of medical services.(2) Bright’s UR decision to deny servicesto the patient caused the patient harm atissue. (3) Under a plain reading of sec-tion 1371.25, as supported by the legisla-tive history, only Bright, the “provider,”was responsible for the harm caused byits UR “acts or omissions” – not the plan,PacifiCare.

The legislative history of AB 1840does not support this outcome. A detailedreview of the extensive record reveals thatthe terms “providers … acts or omissions”adopted in the first sentence of section

1371.25 were only intended to apply toproviders’ negligence or malpractice inthe delivery of health care services. Thehistory does not reveal that the 1995Legislature intended to insulate plans,such as PacifiCare, from vicarious liabilityfor harm caused by their UR agents, suchas Bright, who also happen to be theplans’ medical service “provider.”

Unfortunately, a detailed review of the key legislative records docu-menting these findings is not possiblegiven the space constraints imposed forthis article. Feel free to contact me formy unedited analysis. What follows is abrief outline of some of the major find-ings.PART 1. Key findings from the legisla-tive history which contradict Martin.• The definition of “provider” inHealth and Safety Code Section 1345(i)’s harmonizes with the use of thatterm in section 1371.25. It only encom-passes acts related to patient care, notUR acts.

Strictly speaking, a “provider” ofmedical services is only obligated to acton behalf of a patient’s interests. Asdefined under Health and Safety Codesection 1345 (i), a “provider” is “licensedby the state to deliver or furnish health careservices” (emphasis added). In contrast, aplan’s UR contract agent is only obligat-ed to act on behalf of a plan’s financialand insurance coverage interests. SuchUR services are not embraced within thedefinition of “provider” under section1345(i). Significantly, this definition wasin existence in 1995 when section1371.25 was added. The 1995Legislature was aware of it under theprincipal of statutory construction thatthe Legislature is presumed to act in cog-nizance of existing law. (SutherlandStatutory Construction, Statutes and StatutoryConstruction (7th Ed. 2007) Vol. 2A,s.45:12 at pages 115-119.)

Both the Watanabe and Martin courtsfailed to consider that the term“providers” in section 1371.25 wasintended to harmonize with the defini-tion of “provider” in 1345 (i). In effect,the “providers… acts or omissions”addressed in section 1371.25 were only

JUNE 2013 The Advocate Magazine — 39

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:47 PM Page 39

HMO — continued

intended to apply to those occurring inthe delivery of health care services forpatients – not in the delivery of UR

services for the plan. As summarizedbelow, this understanding is supported inthe legislative history.

• The sole purpose of section 1371.25is to stop plans from shifting liabilityfor harm caused by their UR decisionsto their “providers” of medical servicesthrough insidious “hold harmless”agreements. Watanabe and Martincompletely undermined this purpose.

Martin acknowledged that the original purpose of section 1371.25 was to stop HMOs from forcing their“providers” of medical services to acceptinsidious “hold harmless” provisions intheir contracts, thereby shifting theplans’ liability to their “providers” forharm caused by the plans’ UR decisionsto delay or deny health care coverage.But the court found that this purpose was“broadened” during the amendmentprocess to eliminate vicarious liability.(Martin, 198 Cal.App.4th at pp. 1403-1404.)

Not true. The legislative historyactually shows that the amendmentswere merely technical clarifications toassure that plans would not be liable for“providers… acts or omissions” relatingto negligence or malpractice in thedelivery of health care services. The his-tory does not document an intent toinsulate a plan from vicarious liabilityfor harm caused by its UR agents,including agents who also happened tobe the plan’s provider of medical servic-es. 1. The Assembly Committee on Health’searly analysis set the tone at page 3 intwo ways. (1) It incorporated the spon-sor’s intent to require plans to be respon-sible for their acts, just as providers areresponsible for their negligence or mal-practice in the delivery of health careservices. (2) It also pointed to the possi-bility of future amendments to clarifythat intent.

This bill would prohibit plans fromincluding hold harmless provisionsprotecting the plans in contracts withproviders. The sponsors feel that plansshould be responsible for adverse results oftheir actions in the same manner asproviders. Generally, there seems to beagreement with the intent of this provision

40 — The Advocate Magazine JUNE 2013

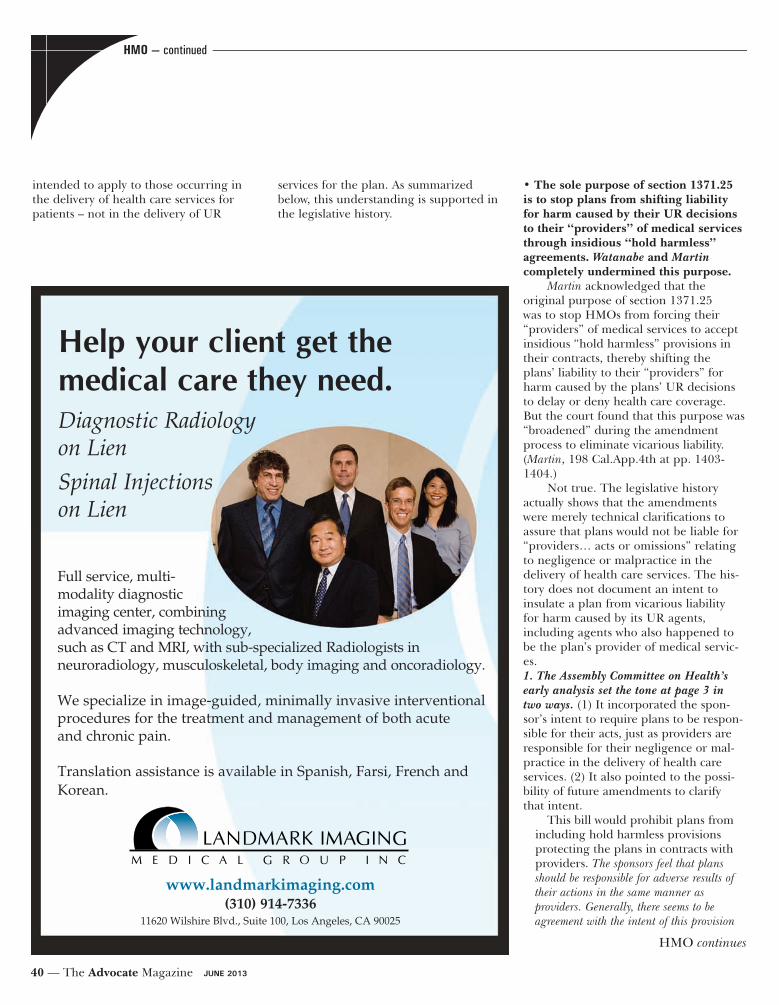

Full service, multi-modality diagnosticimaging center, combiningadvanced imaging technology,such as CT and MRI, with sub-specialized Radiologists inneuroradiology, musculoskeletal, body imaging and oncoradiology.

We specialize in image-guided, minimally invasive interventionalprocedures for the treatment and management of both acuteand chronic pain.

Translation assistance is available in Spanish, Farsi, French andKorean.

Help your client get themedical care they need.Diagnostic Radiologyon LienSpinal Injectionson Lien

www.landmarkimaging.com(310) 914-7336

11620 Wilshire Blvd., Suite 100, Los Angeles, CA 90025

HMO continues

Advocate Jun13 issue2_Advocate template 2007.qxd 5/22/2013 11:28 AM Page 40

Advocate Jun13 issue2_Advocate template 2007.qxd 5/21/2013 6:47 PM Page 41

but disputes remain on the specific wording.In addition, a concern has been raised toinsure that such language covering circum-stances where the provider, not the plan,has denied services or otherwise committedwrongful acts.

[Emphasis added.] 2. HMO concerns trigger amendmentsaddressed in Martin. An “expansion” ofthe original purpose was not intended.Rather, concerns raised by Health Net,the California Association of HMOs(CAHMO) and Kaiser Permanente(“Kaiser”) ultimately resulted in amend-ments to assure that plans would not bevicariously liable for their providers’ neg-ligence or malpractice in the delivery ofhealth care services. This intent wasembodied in the final version of 1371.25that the Martin court misconstrued. • Health Net’s letter dated April 27,1995, lobbies for a targeted amend-ment. It was aimed at making sure thatplans would only be liable for harmcaused by plans or their UR “agents” intheir decisions to deny services. HealthNet did not want to be liable for harmcaused by providers’ negligence or mal-practice in the delivery of health careservices: