Embed Size (px)

Citation preview

www.harriswilliams.de

Harris Williams & Co. Ltd is a private limited company incorporated under English law having its registered office at 5th Floor, 6 St. Andrew Street, London EC4A 3AE, UK, registered withthe Registrar of Companies for England and Wales under company number 7078852. Directors: Mr. Christopher Williams, Mr. Ned Valentine, Mr. Paul Poggi and Mr. Thierry Monjauze,authorised and regulated by the Financial Conduct Authority.

Harris Williams & Co. Ltd Niederlassung Frankfurt (German branch) is registered in the Commercial Register (Handelsregister) of the Local Court (Amtsgericht) of Frankfurt am Main,Germany, under registration number HRB 96687, having its business address at Bockenheimer Landstrasse 33-35, 60325 Frankfurt am Main, Germany. Permanent Representative(Ständiger Vertreter) of the Branch Niederlassung: Mr. Jeffery H. Perkins.

AEROSPACE, DEFENSE & GOVERNMENT SERVICES

INDUSTRY UPDATE │ OCTOBER 2015

0

PAGE |

HARRIS WILLIAMS & CO. ADG UPDATE

CONTENTS

ADG Group Insights:Government Services

Market Updates:

• Aerospace

• Defense

• Government Services

ADG CONTACTS

Jon NemoManaging [email protected]+1 (267) 675-5911

Chris RogersManaging [email protected]+1 (804) 915-0188

Doug KinardVice [email protected]+1 (804) 915-0127

Chris SmithVice [email protected]+1 (804) 932-1383

+1 (804) 887-6014

David [email protected]

+1 (804) 887-6079

AEROSPACE, DEFENSE & GOVERNMENT SERVICES

INDUSTRY UPDATE │ OCTOBER 2015

1

www.harriswilliams.de

Harris Williams & Co. is pleased to present our Aerospace, Defense & Government

Services (ADG) update for October 2015.

In this update, we revisit our June 2015 article on the near-term opportunity in

government services for private equity buyers and offer updated perspectives

underpinned by sector activity over the last four months.

As always, we hope you enjoy the content of this month’s reader and look forward

to hearing your thoughts and opinions.

Regards,

Industry Sectors

Aerospace

• Aircraft Interiors

• Airframe and Engine Components

• Avionics & Electronics

• Electromechanical and Power

• Fixed Base Operations

• Maintenance, Repair & Overhaul

• Software and Information

Services

• Specialty Materials & Metals

• Supply Chain Management &

Distribution

Defense

• Air, Land, and Sea Platforms and

Subsystems

• C4ISR Systems & Sensors

• Defense Electronics

• Satellite Equipment

• Homeland Security Technologies

• Supply Chain Management and

Distribution

• Tactical Products & Accessories

• Unmanned Systems

• Weapon Systems & Munitions

Government Services

• Cybersecurity

• Intelligence Services

• Simulation and Training

• Platform Maintenance &

Modernization

• Software and Information Services

• Systems Engineering &

Technical Assistance (SETA)

• Technical, Operations, and

Logistics Support Services

• Technology and Professional

Services

ADG Group Overview

Chris Rogers

Managing Director

Jon Nemo

Managing Director

Harris Williams & Co.’s Aerospace, Defense & Government Services (ADG) Group

combines deep industry knowledge and relationships with the best M&A advisory

services in the middle market. As a pure-play advisor with no conflicts of interest,

our ADG Group offers differentiated strategic advice and seamless execution to a

global base of leading aerospace, defense, and government services clients.

PAGE |

Sponsor Target Investment Thesis

Opportunity to better capitalize and accelerate the

growth trajectory of a leading engineering

services provider

Opportunity to unlock the value of a strategically

compelling merger of equals

Opportunity to capitalize on the accelerating importance

of big data and advanced analytics to both national

security and commercial markets

ADG GROUP INSIGHTS: GOVERNMENT SERVICES

AEROSPACE, DEFENSE & GOVERNMENT SERVICES

INDUSTRY UPDATE │ OCTOBER 2015

2

$2.1B$1.8B

Sponsor-Led Strategic-Led

EXHIBIT 1: GOV’T SERVICES M&A DEALS (ENTERPRISE VALUE > $100M)

June – October 2015Source: Public Information and Harris Williams &Co Estimates

5 Deals 1 Deal

Government Services: Revisiting the Near-Term Opportunity for Private Equity

When we last shared our observations on the government services market back in early June, we discussed

reasons to expect increased deal-making from private equity, reasons to expect a more shallow landscape

of aggressive strategic acquirers (at least for the near-term), and the growing importance of the equity

capital markets to pure-play federal services platforms. What has followed since our last post was a very

active four months of sector M&A and notable strategic announcements. With this in mind, a brief recap of

recent developments seems timely -- and also valuable context for our latest outlook for the remainder of

2015 and beyond.

As we predicted, financial sponsors

have led the sector’s most recent run of

M&A activity. As illustrated in Exhibit 1,the aggregate transaction value of

government services deals of $100M or

more over the last four months was $2.1B

for sponsor-led transactions, in

comparison with $1.8B for strategic-led

transactions. However, the most

important context for this comparison is

the footnote that the $1.8B for strategics

represents a single deal -- CSGov’s

pending acquisition of Providence Equity

backed SRA International.

This is in contrast to five sizeable sponsor-led deals – which involved nine different private equity groups.

Bolstered by an abundance of low cost debt financing, select sponsors have clearly demonstrated

conviction behind a variety of different investment theses (see Exhibit 2) and have done so in a window of

time during which most of the sector’s largest strategics are either digesting, divesting, or distracted.

Along these lines, strategic buyers do continue to actively shop, but the shifting and yet unsettled sector

landscape is limiting the near-term boldness of their deal-making. Despite the resurgence in sponsor-led

deals, strategic buyers have by no means left the M&A field -- as evidenced by SAIC’s $790M acquisition of

Scitor earlier this year, the pending CSGov/SRA combination, a string of smaller technology-oriented

transactions, and our expectation that another large strategic-led services deal will likely be announced in

the near term.

EXHIBIT 2: SELECT RECENT SPONSOR-LED TRANSACTIONS

PAGE |

ADG GROUP INSIGHTS: GOVERNMENT SERVICES

AEROSPACE, DEFENSE & GOVERNMENT SERVICES

INDUSTRY UPDATE │ OCTOBER 2015

EXHIBIT 3: PENDING DIVESTITURES / SPIN-OUTS (ENTERPRISE VALUE > $100M)

Source: Public Information and Harris Williams &Co Estimates

$6.2B

$4.7B

$1.7B

$10.9B

Sponsor-Led Strategic-Led

That said, the current buyer universe for services

deals has been decidedly less strategic than in

years past. A key driver of this shift is the

competitive landscape disruption that is being

effected by multiple, large spin-outs and the

decision by many of the defense primes to exit

all or large segments of their services businesses.

Reference Exhibit 3, which highlights our

estimated enterprise values of large government

services assets that are currently in the process of

being spun-out or divested. This totals $12.6B

and includes $1.7B of sponsor-owned platforms

and $4.7B of major strategic divestitures (a figure

which excludes the pending spin-out of CSGov)

– most of whom under their current ownership

had historically been heavyweight impact

players within government services M&A.

Once the dust settles and these large pending services transactions are acquired or otherwise recapitalized,

the universe of strategic buyers for core middle market government services transactions will take on

materially greater breadth and depth.

As we discussed back in June, the equity capital markets also remain well positioned to play a much more

prominent role within the future federal services landscape. While the planned IPOs of Alion and SRA that

were in the works earlier this year have since resulted in M&A deals, several other sponsor-owned platforms

(and strategic divestitures) are already, or should be, considering future public offerings (or spin-outs) for their

government services businesses. As we highlighted in our last article, a number of factors have markedly

increased the appetite and sentiment in recent months within the public equity markets for pure-play

government services companies, which have outperformed the S&P by 6.5% since June 30th. As illustrated in

Exhibit 4, the current universe of public pure-play government services companies is both larger, more diverse,

and more highly valued in early October 2015 than it was five years ago.

9.7x

Median TEV / CY15E EBITDA

EXHIBIT 4: PUBLIC PURE-PLAY PUBLIC GOVERNMENT SERVICES (TOTAL ENTERPRISE VALUE)

($ in billions)

$14.8

$16.7

$1.9

$11.2 $11.2

$27.9

12/31/2010 Existing Pure-Plays New Pure-Plays 10/15/2015

Net TEV increase includes impact of Six3 Systems, Scitor, and 15+

Other M&A Deals

3

6.9x

Median TEV / CY10 EBITDA

October 2015 TEV of Public Pure-Play Government

Services Companies Nearly 2x that of Five Years Ago

PAGE |

ADG GROUP INSIGHTS: GOVERNMENT SERVICES

AEROSPACE, DEFENSE & GOVERNMENT SERVICES

INDUSTRY UPDATE │ OCTOBER 2015

So what does all this mean for future government services M&A? It means conditions that point to multiplestructural drivers for sustained high levels of middle market deal-making – and near-term windows of

opportunity, in particular for private equity. Based on our assessment of the current market, a few specific

observations:

First, as the most prominent upper middle market deals (meaning >$500M) of the past two years are

fully integrated and balance sheets are de-levered, several key strategic acquirers will eventually be

back more meaningfully in the M&A market. And they will be back in the market targeting “move the

needle” transactions in terms of both differentiated capabilities and size.

Second, most of the $12.6B of pending government services deals now or soon to be in the market

should have new homes within the next six to twelve months. This means newly acquired or

independent entities seeking to redefine growth strategies and competitively differentiate themselves –

strategies for which M&A will no doubt play a prominent role.

Finally, the transformation of the services landscape that is now underway is structurally dramatic by

any historical standard – in terms of its scope, its scale, and the market influence of its participants. As a

result, it will eventually force M&A action upon even those who, as of late, have been less active -- or

more disciplined, depending on your perspective. Organic growth and internal initiatives alone will

prove insufficient to consistently compete and win in today’s government services market – a market

that simultaneously values scale efficiencies, accelerating rates of technology adoption, and constant

agility in delivering more operational capability.

We’ll thus close with a prediction that we can deliver with conviction. The government services landscape of

early fall 2015 is going to look starkly different in five years. Opportunity is always present amidst times of

significant change -- and for this reason we are looking forward to a very dynamic near-term M&A market

within services as we prepare to close out 2015 and enter 2016.

When Considering Strategic Alternatives, Engage Specialist Advisors with No Conflicts of Interest

For government services platforms now considering a range of strategic alternatives, thoughtfully navigating

this process requires specialized expertise, relationships, and access. Harris Williams & Co. and Solebury

Capital, both subsidiaries of The PNC Financial Services Group, Inc. (NYSE: PNC), have complementary and

rigorously independent business models. We provide a singularly unique combination of capabilities for clients

who are now considering this range of strategic alternatives.

Solebury Capital (www.solecap.com) is the largest equity capital markets advisory

firm in the United States, advising on over 40% of all private equity backed company

IPOs in each of the last two years. Solebury’s unparalleled activity level translates into

To learn more about our firms’ individual and combined capabilities, contact:

Chris RogersManaging Director, ADG GroupHarris Williams & [email protected]+1 (804) 915-0188

Jon NemoManaging Director, ADG GroupHarris Williams & [email protected]+1 (267) 675-5911

a powerful information hub for clients, that when combined with the firm’s no conflicts model and Street

relationships, provides a meaningful advantage to clients as they contemplate the public markets.

Harris Williams & Co. (www.harriswilliams.com) is a leader in middle market M&A

advisory services and is one of the largest sources of deal flow to the most relevant

private equity buyers of large government services platforms. Our track record of

exceptional client outcomes can be attributed to the firm’s strategic focus, dedicated industry groups, and

pure-play, no conflicts model – with over 98% of our revenue from sell-side M&A advisory. Our firm’s extensive

market intelligence and the specialized industry expertise and relationships of our dedicated Aerospace,

Defense & Government Services (ADG) Group provide unique advantages to our clients.

4

PAGE |

13.3x

9.6x

7.7x

7.2x

16.8x

15.3x

14.3x

13.5x

13.3x

12.7x

12.4x

12.2x

12.0x

11.7x

11.0x

10.8x

10.4x

10.1x

10.0x

9.8x

9.7x

9.7x

9.5x

9.2x

9.0x

8.5x

8.4x

8.4x

7.5x

7.3x

6.6x

6.1x

13.8x

10.9x

9.5x

9.3x

8.8x

8.2x

8.2x

8.1x

7.9x

EMBR3

BA

BBD.B

AIR

TDG

ROLL

BEAV

PCP

ZC

MGGT

HXL

HEI

AIR

HRX

COL

WAI R

BBA

SAF

SNR

TGI

WWD

ESL

LMIA

MAL

B

ATRO

KAMN

MOG.A

DCO

KLXI

SPR

GKN

AME

HON

CW

ETN

TXT

RR.

CR

UTX

PH

GE

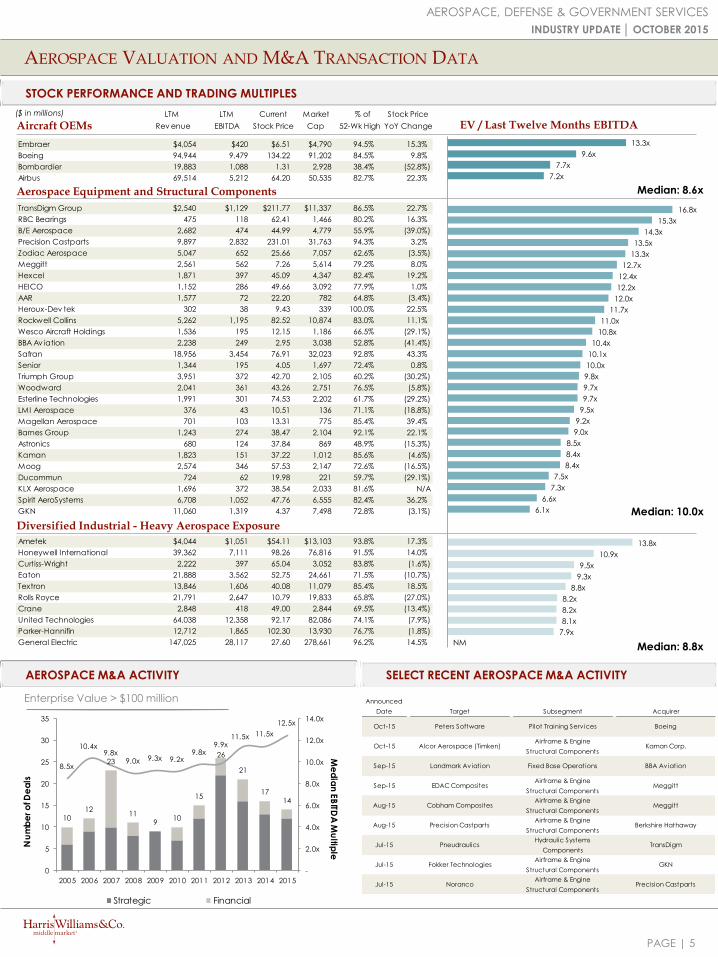

LTM LTM Current Market % of Stock Price

Rev enue EBITDA Stock Price Cap 52-Wk High YoY Change

Embraer $4,054 $420 $6.51 $4,790 94.5% 15.3%

Boeing 94,944 9,479 134.22 91,202 84.5% 9.8%

Bombardier 19,883 1,088 1.31 2,928 38.4% (52.8%)

Airbus 69,514 5,212 64.20 50,535 82.7% 22.3%

TransDigm Group $2,540 $1,129 $211.77 $11,337 86.5% 22.7%

RBC Bearings 475 118 62.41 1,466 80.2% 16.3%

B/E Aerospace 2,682 474 44.99 4,779 55.9% (39.0%)

Precision Castparts 9,897 2,832 231.01 31,763 94.3% 3.2%

Zodiac Aerospace 5,047 652 25.66 7,057 62.6% (3.5%)

Meggitt 2,561 562 7.26 5,614 79.2% 8.0%

Hexcel 1,871 397 45.09 4,347 82.4% 19.2%

HEICO 1,152 286 49.66 3,092 77.9% 1.0%

AAR 1,577 72 22.20 782 64.8% (3.4%)

Heroux-Dev tek 302 38 9.43 339 100.0% 22.5%

Rockwell Collins 5,262 1,195 82.52 10,874 83.0% 11.1%

Wesco Aircraft Holdings 1,536 195 12.15 1,186 66.5% (29.1%)

BBA Av iation 2,238 249 2.95 3,038 52.8% (41.4%)

Safran 18,956 3,454 76.91 32,023 92.8% 43.3%

Senior 1,344 195 4.05 1,697 72.4% 0.8%

Triumph Group 3,951 372 42.70 2,105 60.2% (30.2%)

Woodward 2,041 361 43.26 2,751 76.5% (5.8%)

Esterline Technologies 1,991 301 74.53 2,202 61.7% (29.2%)

LMI Aerospace 376 43 10.51 136 71.1% (18.8%)

Magellan Aerospace 701 103 13.31 775 85.4% 39.4%

Barnes Group 1,243 274 38.47 2,104 92.1% 22.1%

Astronics 680 124 37.84 869 48.9% (15.3%)

Kaman 1,823 151 37.22 1,012 85.6% (4.6%)

Moog 2,574 346 57.53 2,147 72.6% (16.5%)

Ducommun 724 62 19.98 221 59.7% (29.1%)

KLX Aerospace 1,696 372 38.54 2,033 81.6% N/A

Spirit AeroSystems 6,708 1,052 47.76 6,555 82.4% 36.2%

GKN 11,060 1,319 4.37 7,498 72.8% (3.1%)

Ametek $4,044 $1,051 $54.11 $13,103 93.8% 17.3%

Honeywell International 39,362 7,111 98.26 76,816 91.5% 14.0%

Curtiss-Wright 2,222 397 65.04 3,052 83.8% (1.6%)

Eaton 21,888 3,562 52.75 24,661 71.5% (10.7%)

Textron 13,846 1,606 40.08 11,079 85.4% 18.5%

Rolls Royce 21,791 2,647 10.79 19,833 65.8% (27.0%)

Crane 2,848 418 49.00 2,844 69.5% (13.4%)

United Technologies 64,038 12,358 92.17 82,086 74.1% (7.9%)

Parker-Hannifin 12,712 1,865 102.30 13,930 76.7% (1.8%)

General Electric 147,025 28,117 27.60 278,661 96.2% 14.5%

AEROSPACE VALUATION AND M&A TRANSACTION DATA

STOCK PERFORMANCE AND TRADING MULTIPLES

AEROSPACE M&A ACTIVITY

AEROSPACE, DEFENSE & GOVERNMENT SERVICES

INDUSTRY UPDATE │ OCTOBER 2015

Enterprise Value > $100 million

Aircraft OEMs

Aerospace Equipment and Structural Components

Diversified Industrial - Heavy Aerospace Exposure

SELECT RECENT AEROSPACE M&A ACTIVITY

EV / Last Twelve Months EBITDA

5

Median: 8.6x

Median: 10.0x

Median: 8.8x

($ in millions)

NM

1012

23

119

10

15

26

21

1714

8.5x

10.4x9.8x

9.0x 9.3x 9.2x9.8x

9.9x11.5x 11.5x

12.5x

-

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

0

5

10

15

20

25

30

35

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Me

dia

n E

BITD

A M

ultip

le

Nu

mb

er o

f De

als

Strategic Financial

Announced

Date Target Subsegment Acquirer

Oct-15 Peters Software Pilot Training Serv ices Boeing

Oct-15 Alcor Aerospace (Timken)Airframe & Engine

Structural ComponentsKaman Corp.

Sep-15 Landmark Aviation Fixed Base Operations BBA Aviation

Sep-15 EDAC CompositesAirframe & Engine

Structural ComponentsMeggitt

Aug-15 Cobham CompositesAirframe & Engine

Structural ComponentsMeggitt

Aug-15 Precision CastpartsAirframe & Engine

Structural ComponentsBerkshire Hathaway

Jul-15 PneudraulicsHydraulic Systems

ComponentsTransDigm

Jul-15 Fokker TechnologiesAirframe & Engine

Structural ComponentsGKN

Jul-15 NorancoAirframe & Engine

Structural ComponentsPrecision Castparts

PAGE |

11.0x

10.9x

10.1x

9.8x

9.7x

9.6x

9.6x

7.4x

7.2x

5.5x

16.8x

13.5x

13.3x

12.7x

12.4x

11.8x

10.8x

10.4x

10.1x

9.7x

9.0x

RTN

LMT

NOC

BA.

GD

HO

BA

FNC

AIR

HII

AVAV

CHG

MRCY

COB

HRS

OA

ULE

FLIR

LLL

ESLT

TDY

CUB

CMTL

KTOS

DEFENSE VALUATION AND M&A TRANSACTION DATA

STOCK PERFORMANCE AND TRADING MULTIPLES

AEROSPACE, DEFENSE & GOVERNMENT SERVICES

INDUSTRY UPDATE │ OCTOBER 2015

Defense Prime

Contractors

Defense Technologies

DEFENSE M&A ACTIVITY SELECT RECENT DEFENSE M&A ACTIVITY

Enterprise Value > $50 million

EV / Last Twelve Months EBITDA

6

Median: 9.6x

Median: 12.1x

38.0x

($ in millions)

30

27

30

2019

29

25

16

18

11

13

12.4x

11.9x

13.4x

12.0x

10.5x 10.5x

8.6x 8.4x

9.9x

8.5x 8.1x

-

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

0

5

10

15

20

25

30

35

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Me

dia

n E

BITD

A M

ultip

le

Nu

mb

er o

f De

als

Strategic Financial

Announced

Date Target Subsegment Acquirer

Sep-15 GE Embedded Systems Defense Electronics Veritas Capital

Jul-15 Sikorsky Helicopter OEM Lockheed Martin

Jun-15 VievuTactical and Protection

Equipment The Safariland Group

Jun-15 Point Blank EnterprisesTactical and Protection

Equipment JLL Partners

Jun-15Kratos Electronic

Products Div ision (Herley)Defense Electronics Ultra Electronics

Apr-15 Kutta Technologies Unmanned Systems Sierra Nevada Corp.

Apr-15Inmet and Weinschel

Assets (Cobham)Defense Electronics API

Apr-15Semtech Corp (Defense

and Microwave Business)Defense Electronics Jariet Technologies

Apr-15Hunter Technology

CorporationDefense Electronics Sparton Corp.

LTM LTM Current Market % of Stock Price

Rev enue EBITDA Stock Price Cap 52-Wk High YoY Change

Raytheon $22,753 $3,336 $112.89 $34,268 99.3% 15.8%

Lockheed Martin 45,398 6,146 210.64 65,411 97.4% 19.5%

Northrop Grumman 23,945 3,585 174.58 32,715 98.1% 40.3%

BAE Systems 25,647 2,493 6.98 22,080 82.1% (2.2%)

General Dynamics 31,779 4,632 141.25 45,585 91.9% 16.9%

Thales 15,177 1,553 70.52 14,685 95.5% 43.9%

Boeing 94,944 9,479 138.42 94,056 87.1% 12.3%

Finmeccanica 16,784 1,692 13.44 7,770 87.0% 54.3%

Airbus 69,514 5,212 62.74 49,387 81.6% 12.0%

Huntington Ingalls 6,959 1,067 104.63 5,003 72.7% 10.9%

AeroVironment $255 $7 $21.50 $505 69.4% (23.8%)

Mercury Systems 547 54 3.51 679 91.5% (4.1%)

Cobham 235 35 16.59 571 94.3% 39.2%

Harris Corporation 3,249 556 4.50 5,090 83.2% 3.2%

Orbital ATK 5,083 1,102 75.33 9,313 88.9% N/A

Ultra Electronics Holdings 3,590 492 77.65 4,589 95.8% 0.0%

FLIR Systems 1,108 183 27.56 1,925 93.0% 0.2%

L-3 Communications Holdings 1,547 351 27.65 3,878 80.2% (4.8%)

Elbit Systems 11,654 1,188 109.93 8,831 82.7% (0.6%)

Teledyne Technologies 3,029 360 76.31 3,260 90.0% 24.7%

Cubic 2,366 389 83.47 2,954 74.7% (10.6%)

Comtech Telecommunications 1,401 121 43.62 1,173 78.3% (5.1%)

Chemring Group 307 47 23.49 379 57.7% (32.8%)

Kratos 807 48 4.11 243 57.7% (35.7%) NM

NM

PAGE |

14.4x

10.7x

10.3x

9.8x

9.4x

8.5x

7.8x

7.8x

7.7x

11.7x

9.4x

9.4x

9.1x

9.0x

6.1x

4.3x

LTM LTM Current Market % of Stock Price

Rev enue EBITDA Stock Price Cap 52-Wk High YoY Change

Engility $1,643 $151 $27.58 $1,015 56.3% (21.0%)

Booz Allen Hamilton 5,304 507 26.93 3,945 86.0% 8.0%

SAIC 4,064 320 42.22 1,943 75.4% (8.3%)

CACI International 3,313 299 80.87 1,960 87.7% 15.1%

Leidos 5,063 418 44.36 3,197 94.0% 27.8%

ManTech International 1,613 122 27.04 1,015 76.7% 1.5%

NCI, Inc 317 25 13.19 172 78.7% 54.6%

VSE Corporation 449 63 42.96 231 51.1% (16.0%)

Vectrus 1,157 43 22.60 239 66.9% N/A

KEYW 303 1 7.08 273 56.2% (27.6%)

Babcock International $5,938 $752 $15.03 $7,578 80.6% (7.9%)

CGI 8,163 1,404 36.82 11,315 82.9% 25.0%

AECOM 15,829 856 29.21 4,410 82.5% 3.9%

ICF 1,104 105 30.73 595 70.3% (6.0%)

CSC 11,697 1,015 64.33 8,899 87.8% 14.3%

Jacobs 12,216 840 40.65 5,032 81.5% (13.0%)

Fluor 20,254 1,348 46.72 6,772 67.0% (24.1%)

Serco 5,847 (990) 1.62 1,762 32.7% (62.9%)

KBR 5,891 (133) 18.88 2,725 90.9% 7.5%

GOVERNMENT SERVICES VALUATION AND M&A TRANSACTION DATA

STOCK PERFORMANCE AND TRADING MULTIPLES

AEROSPACE, DEFENSE & GOVERNMENT SERVICES

INDUSTRY UPDATE │ OCTOBER 2015

Government Services

Providers

GOVERNMENT SERVICES M&A ACTIVITY SELECT RECENT GOVERNMENT SERVICES M&A ACTIVITY

Enterprise Value > $50 million

Median: 9.4x

EV / Last Twelve Months EBITDA

7

Diversified Services – Heavy Government Exposure

Median: 9.1x

($ in millions)

NM

14

18

2223

15

2624

18

7

19

13

15.3x

9.9x

12.2x 11.9x

10.5x10.0x 11.1x

7.6x9.4x

10.0x

11.0x

-

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

18.0x

0

5

10

15

20

25

30

35

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Me

dia

n E

BITD

A M

ultip

le

Nu

mb

er o

f De

als

Strategic Financial

Announced

Date Target Subsegment Acquirer

Oct-15 AxiosIntelligence and Cyber

Security Serv icesLGS Innovations

Aug-15 SRA InternationalTechnology and Professional

Serv icesCSC

Aug-15 Novetta SoltutionsIntelligence and Cyber

Security Serv icesThe Carlyle Group

Aug-15 Salient Federal SolutionsTechnology and Professional

Serv icesCRGT

1

Jul-15 AlionTechnology and Professional

Serv icesVeritas Capital

Jul-15ManTech Cyber

Solutions International

Intelligence and Cyber

Security Serv icesCounterTack

Jun-15 Knowledge Consulting GroupIntelligence and Cyber

Security Serv icesManTech

Jun-15 STG GroupTechnology and Professional

Serv ices

Global Defense and National

Security Systems

May-15 Creative Computing SolutionsSoftware Information and

Serv ices

Triple-I

(DFW Capital Partners)

(1) Merger

NM

NM

Aerospace, Defense & Government

Services

PAGE |

HARRIS WILLIAMS & CO. OFFICE LOCATIONS

UNITED STATES EUROPE

BostonTwo International Place24th FloorBoston, Massachusetts 02110Phone: +1 (617) 482-7501

Cleveland1900 East 9th Street20th FloorCleveland, Ohio 44114Phone: +1 (216) 689-2400

Minneapolis222 South 9th StreetSuite 3350Minneapolis, Minnesota 55402Phone: +1 (612) 359-2700

Richmond (Headquarters)1001 Haxall Point9th FloorRichmond, Virginia 23219Phone: +1 (804) 648-0072

San Francisco575 Market Street31st FloorSan Francisco, California 94105Phone: +1 (415) 288-4260

FrankfurtBockenheimer Landstrasse 33-3560325 FrankfurtGermanyPhone: +49 069 3650638 00

London63 Brook StreetLondon W1K 4HS, EnglandPhone: +44 (0) 20 7518 8900

NETWORK OFFICES

Beijing

Hong Kong

Mumbai

New Delhi

Shanghai

Energy, Power & Infrastructure

IndustrialsHealthcare & Life Sciences

Transportation & Logistics

Business Services

Building Products & Materials

Technology, Media & Telecom

Specialty Distribution

ConsumerAerospace, Defense & Government

Services

Harris Williams & Co. has a broad range of industry expertise, which creates powerful opportunities.Our clients benefit from our deep-sector experience, integrated industry intelligence andcollaboration across the firm, and our commitment to learning what makes them unique. For moreinformation, visit our website.

OUR FIRM

AEROSPACE, DEFENSE & GOVERNMENT SERVICES

INDUSTRY UPDATE │ OCTOBER 2015

8

PAGE |

HARRIS WILLIAMS & CO.

AEROSPACE, DEFENSE & GOVERNMENT SERVICES

INDUSTRY UPDATE │ OCTOBER 2015

DISCLOSURES

9

Harris Williams & Co. (www.harriswilliams.com and www.harriswilliams.de) is a preeminent middle market investment bank focused on the advisoryneeds of clients worldwide. The firm has deep industry knowledge, global transaction expertise, and an unwavering commitment to excellence. HarrisWilliams & Co. provides sell-side and acquisition advisory, restructuring advisory, board advisory, private placements, and capital markets advisoryservices.

Harris Williams & Co. Ltd is a private limited company incorporated under English law having its registered office at 5th Floor, 6 St. Andrew Street,London EC4A 3AE, UK, registered with the Registrar of Companies for England and Wales under company number 7078852. Directors: Mr. ChristopherWilliams, Mr. Ned Valentine, Mr. Paul Poggi and Mr. Thierry Monjauze, authorised and regulated by the Financial Conduct Authority.

Harris Williams & Co. Ltd Niederlassung Frankfurt (German branch) is registered in the Commercial Register (Handelsregister) of the Local Court(Amtsgericht) of Frankfurt am Main, Germany, under registration number HRB 96687, having its business address at Bockenheimer Landstrasse 33-35,60325 Frankfurt am Main, Germany. Permanent Representative (Ständiger Vertreter) of the Branch Niederlassung: Mr. Jeffery H. Perkins.

The information and views contained in this report were prepared by Harris Williams & Co. (“Harris Williams”). It is not a research report, as such term isdefined by applicable law and regulations, and is provided for informational purposes only. It is not to be construed as an offer to buy or sell or asolicitation of an offer to buy or sell any financial instruments or to participate in any particular trading strategy. The information contained herein isbelieved by Harris Williams to be reliable, but Harris Williams makes no representation as to the accuracy or completeness of such information. HarrisWilliams and/or its affiliates may be market makers or specialists in, act as advisers or lenders to, have positions in and effect transactions in securitiesof companies mentioned herein and also may provide, may have provided, or may seek to provide investment banking services for thosecompanies. In addition, Harris Williams and/or its affiliates or their respective officers, directors and employees may hold long or short positions in thesecurities, options thereon or other related financial products of companies discussed herein. Opinions, estimates and projections in this reportconstitute Harris Williams’ judgment and are subject to change without notice. The financial instruments discussed in this report may not be suitable forall investors, and investors must make their own investment decisions using their own independent advisors as they believe necessary and based upontheir specific financial situations and investment objectives. Also, past performance is not necessarily indicative of future results. No part of this materialmay be copied or duplicated in any form or by any means, or redistributed, without Harris Williams’ prior written consent.

Copyright© 2015 Harris Williams & Co., all rights reserved.