Embed Size (px)

Citation preview

1

AES

GENER

HIGHLIGHTS

2

Highlights 2013

3

• Subordinated bond with 60 years tenor

• Prepayment of $147 million Senior Bond

due in March 2014

VENTANAS IV

• Start-up of commercial

operations in March 2013

COCHRANE PROJECT

• Financial close and start of

construction in March 2013

CAPITAL INCREASE

ALTO MAIPO PROJECT

• Financial close and start of principal

construction works in December 2013

• Alto Maipo project awarded Latin

America Power Deal of the Year by

Project Finance International magazine

ISSUE OF $450 MILLION

CORPORATE BONDS

• Shareholders approved capital

increase of up to US$450 million

• Expect to issue between US$150 -

$200 million in 1H 2014

2nd Phase of Expansion Progress

Making progress in 2nd Phase of Expansion

Projects under Construction Medium term Projects

Alto Maipo Cochrane

Guacolda V Tunjita

Retrofits

Andes Solar Angamos Desalinization

Interconnection SING – SADI

Financing Sources

Project Finance Capital Increase Corporate Debt

4

AES

GENER

AES

GENER OVERVIEW

5

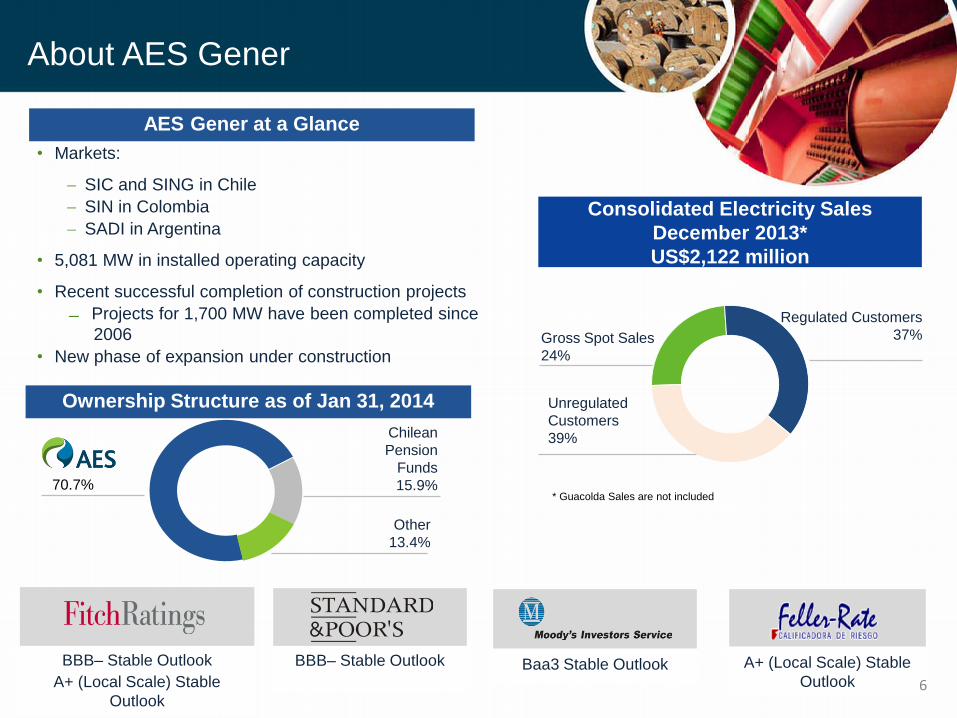

Ownership Structure as of Jan 31, 2014

AES Gener at a Glance

A+ (Local Scale) Stable

Outlook

BBB– Stable Outlook

A+ (Local Scale) Stable

Outlook

70.7%

Chilean

Pension

Funds

15.9%

Other

13.4%

BBB– Stable Outlook Baa3 Stable Outlook

Consolidated Electricity Sales

December 2013*

US$2,122 million

Gross Spot Sales

24%

Unregulated

Customers

39%

Regulated Customers

37%

* Guacolda Sales are not included

6

About AES Gener

• Markets:

SIC and SING in Chile

SIN in Colombia

SADI in Argentina

• 5,081 MW in installed operating capacity

• Recent successful completion of construction projects

Projects for 1,700 MW have been completed since

2006

• New phase of expansion under construction

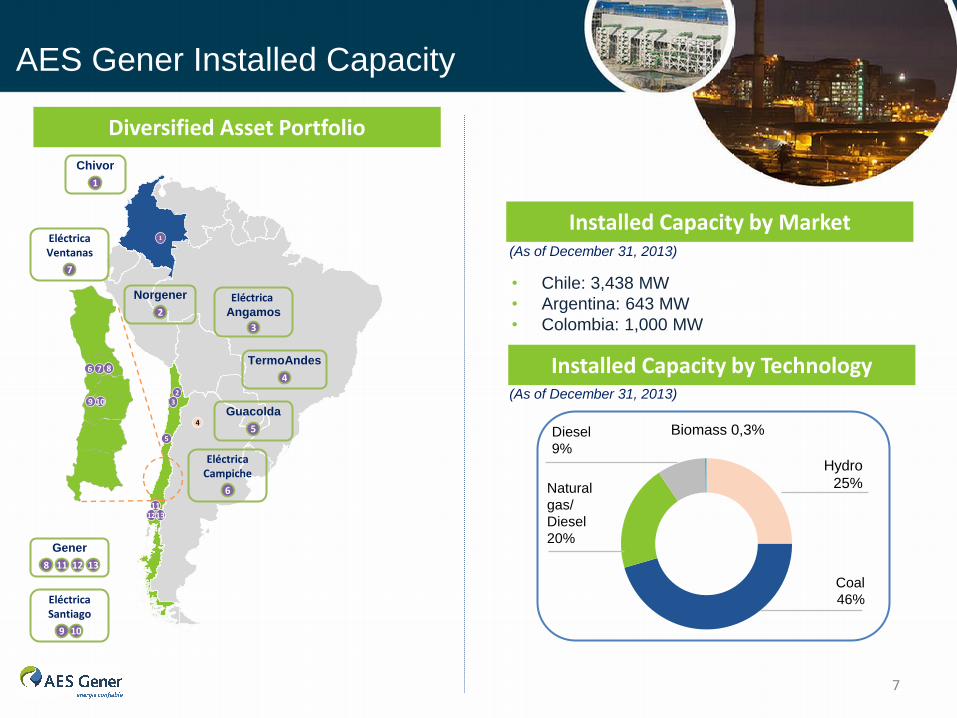

AES Gener Installed Capacity

1

2 3

4

5

6 7 8

9 10

11 12 13

Chivor

1

Norgener

2

TermoAndes

4

Eléctrica Angamos

3

Guacolda

5

Eléctrica Campiche

6

Eléctrica Ventanas

7

Gener

8 11 12 13

Eléctrica Santiago

9 10

(As of December 31, 2013)

Hydro

25%

Coal

46%

Diesel

9%

Biomass 0,3%

Natural

gas/

Diesel

20%

• Chile: 3,438 MW

• Argentina: 643 MW

• Colombia: 1,000 MW

Diversified Asset Portfolio

Installed Capacity by Market

Installed Capacity by Technology

7

(As of December 31, 2013)

MARKETS

AES

GENER

8

2%

7%

9%

12%

15% 15%

40%

TermoAndes S.A.

Pampa Energía S.A.

AES Argentina

SADESA

ENDESA

Estado Nacional Argentina

Otros

Electricity System Overview

21%

45%

24%

10% AES Gener

E-CL

Endesa

Others

SIC SING

Colombia Argentina

17%

40%21%

22%AES Gener

Endesa

Colbun

Others

• Energy Sales: 70% Regulated Customers

• Generation by Type: 58% Hydro and 41% Thermo

Main Players: Installed Capacity Main Players: Installed Capacity

13,585 MW 3,963 MW

• Energy Sales: 88% Unregulated Customers

• Generation by Type: 99% Thermo

Main Players: Installed Capacity Main Players: Installed Capacity

7%12%

20%

22%8%

15%

16%AES Chivor

Celsia

Endesa

EPM

Gecelca

Isagen

Others 14,533 MW

• Energy Sales: 67% Regulated

• Generation by Type: 80% Hydro

31,138 MW

• Energy Sales: 46% Industrial and 39% Residential

• Generation by Type: 66% Thermo and 29% Hydro

Source: CDEC-SIC Source: CDEC-SING. TermoAndes is not included

Source: XM Source: CAMESSA 9

As of December 31, 2012

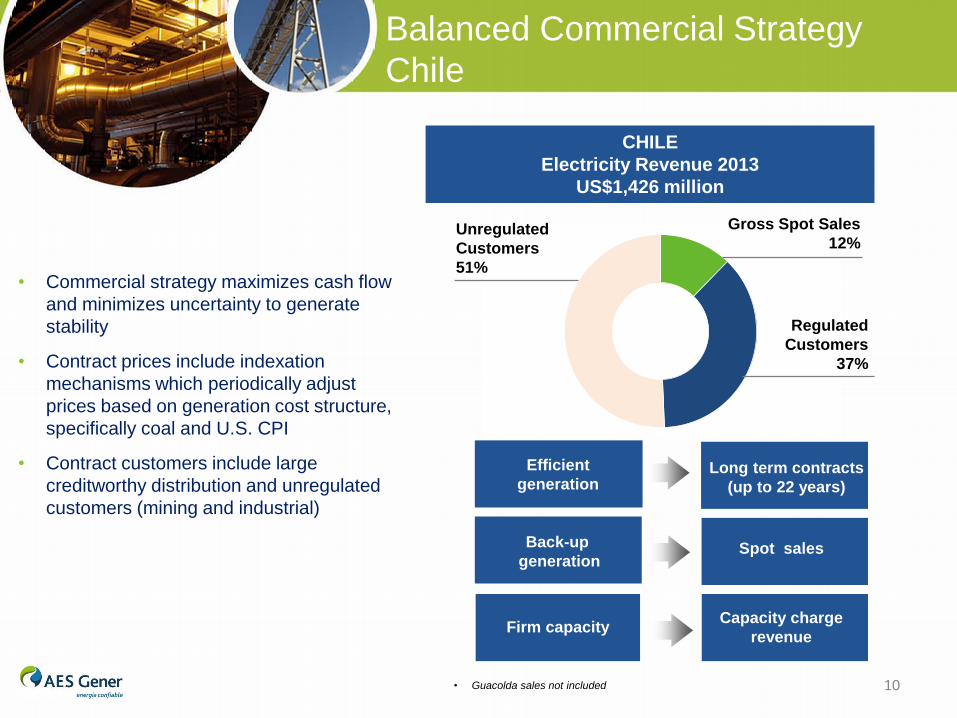

Balanced Commercial Strategy

Chile

Gross Spot Sales

12%

Regulated

Customers

37%

CHILE

Electricity Revenue 2013

US$1,426 million

Unregulated

Customers

51% • Commercial strategy maximizes cash flow

and minimizes uncertainty to generate

stability

• Contract prices include indexation

mechanisms which periodically adjust

prices based on generation cost structure,

specifically coal and U.S. CPI

• Contract customers include large

creditworthy distribution and unregulated

customers (mining and industrial)

• Guacolda sales not included 10

Efficient

generation Long term contracts

(up to 22 years)

Generació

n de

respaldo Generación de

respaldo

Spot sales

Firm capacity Capacity charge

revenue

Back-up

generation

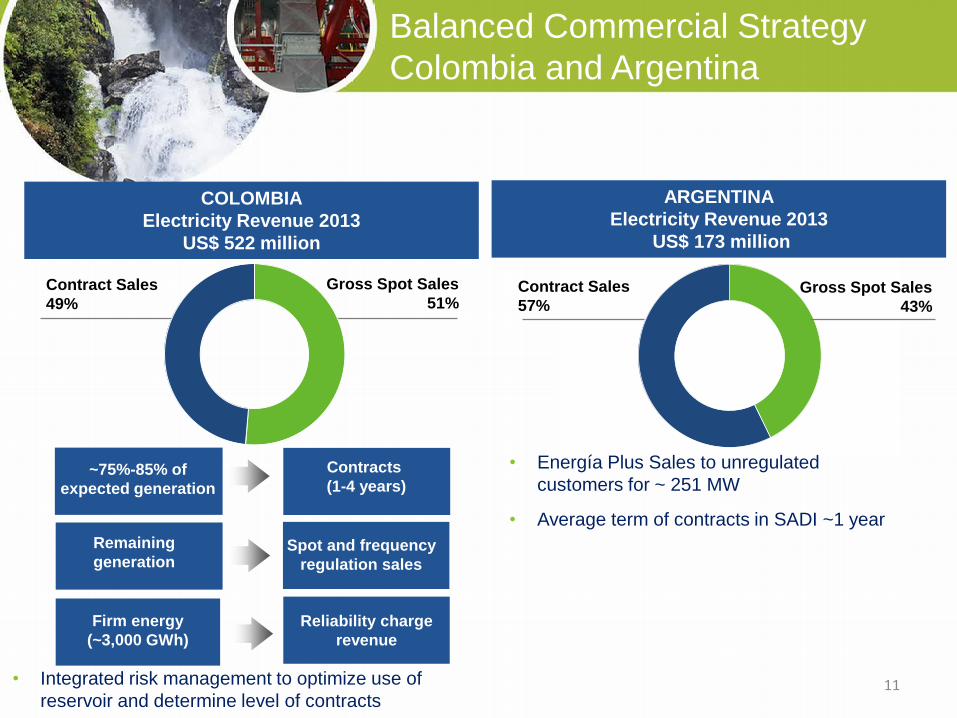

Balanced Commercial Strategy

Colombia and Argentina

~75%-85% of

expected generation

Spot and frequency

regulation sales

Firm energy

(~3,000 GWh)

Remaining

generation

Reliability charge

revenue

Gross Spot Sales

51% Contract Sales

49%

COLOMBIA

Electricity Revenue 2013

US$ 522 million

ARGENTINA

Electricity Revenue 2013

US$ 173 million

• Energía Plus Sales to unregulated

customers for ~ 251 MW

• Average term of contracts in SADI ~1 year

Gross Spot Sales

43%

Contract Sales

57%

Contracts

(1-4 years)

• Integrated risk management to optimize use of

reservoir and determine level of contracts 11

FINANCIAL

REVIEW

AES

GENER

12

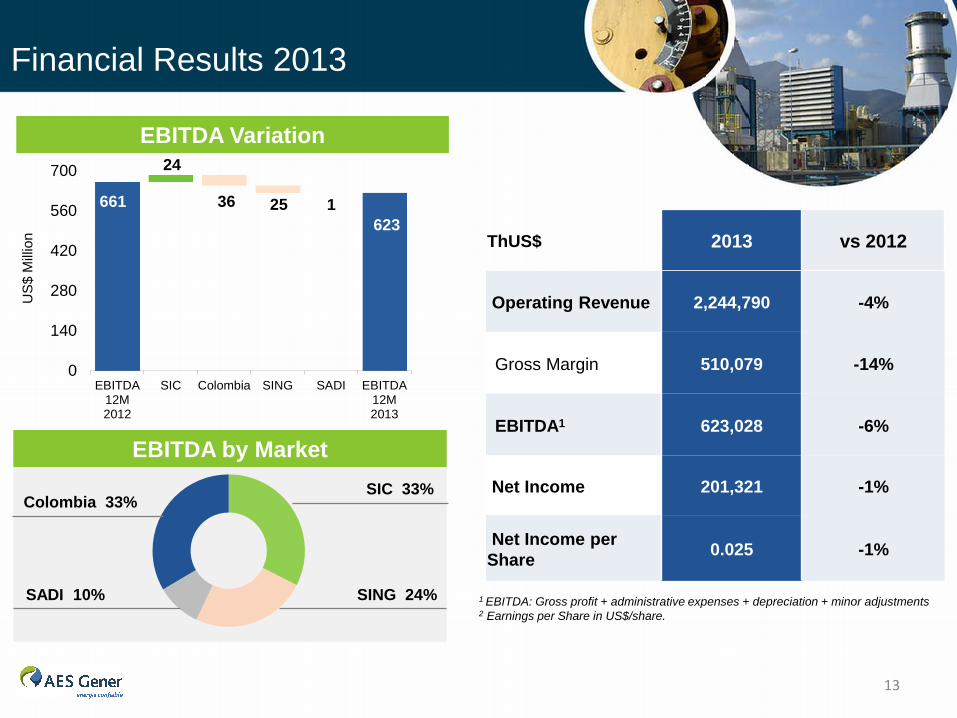

Financial Results 2013

ThUS$ 2013 vs 2012

Operating Revenue 2,244,790 -4%

Gross Margin 510,079 -14%

EBITDA1 623,028 -6%

Net Income 201,321 -1%

Net Income per

Share 0.025 -1%

1 EBITDA: Gross profit + administrative expenses + depreciation + minor adjustments 2 Earnings per Share in US$/share.

EBITDA Variation

661

623

24

36 25 1

0

140

280

420

560

700

EBITDA12M2012

SIC Colombia SING SADI EBITDA12M2013

US

$ M

illio

n

EBITDA by Market

SIC 33%

SING 24% SADI 10%

Colombia 33%

13

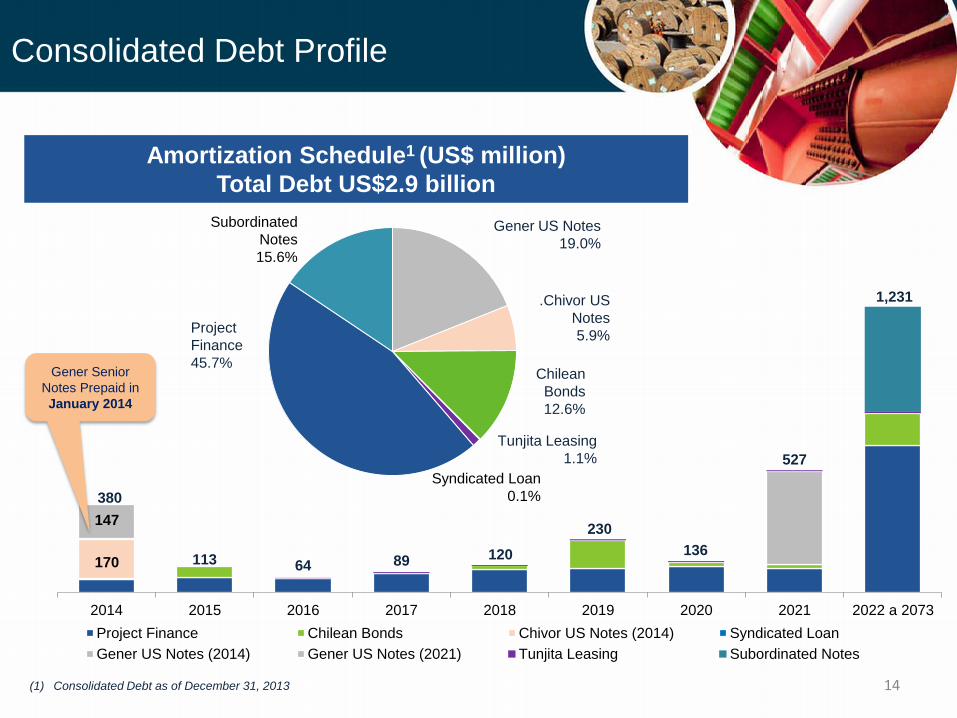

2014 2015 2016 2017 2018 2019 2020 2021 2022 a 2073

Project Finance Chilean Bonds Chivor US Notes (2014) Syndicated Loan

Gener US Notes (2014) Gener US Notes (2021) Tunjita Leasing Subordinated Notes

Consolidated Debt Profile

Amortization Schedule1 (US$ million)

Total Debt US$2.9 billion

Project

Finance

45.7%

Gener US Notes

19.0%

.Chivor US

Notes

5.9%

Tunjita Leasing

1.1%

Chilean

Bonds

12.6%

Syndicated Loan

0.1%

Subordinated

Notes

15.6%

Gener Senior

Notes Prepaid in

January 2014

1,231

380

113 64 89 120

230

136

527

147

170

(1) Consolidated Debt as of December 31, 2013 14

847 1,049 1,110 1,114 1,156 1,487

309

740 1,010 1,154 1,126

1,298

2008 2009 2010 2011 2012 2013

Deuda Project Finance Deuda CorporativaCorporate Debt Project Finance Debt

EBITDA* since 2008 Debt increase associated with projects

EBITDA by market (US$ Million) Total debt (US$ Million)

Stable Net Debt/EBITDA* Total Capex

Net Debt/ EBITDA (times) CAPEX (US$ Million)

2008 2009 2010 2011 2012 2013

Solid Financial Indicators

2008 2009 2010 2011 2012 2013

2,268 2,282

1,156

1,789

2,120 528

472

737 661 623

2,785

2.8x 2.5x

3.2x

2.3x

2.8x

3.3x

657

865

511

395 419

532

397

36% 32%

18%

33% 27% 33%

43%

38%

39%

32%

27% 24%

3%

1%

4%

9% 10% 20%

27%

27%

30%

37% 33%

2008 2009 2010 2011 2012 2013

SIN SADI SING SIC

* Note:: EBITDA means adjusted EBITDA. Adjusted; EBITDA = Gross Profit + Administrative Expenses + Depreciation + Minor Adjustments

15

GROWTH

PROJECTS

AES

GENER

16

1,022

17

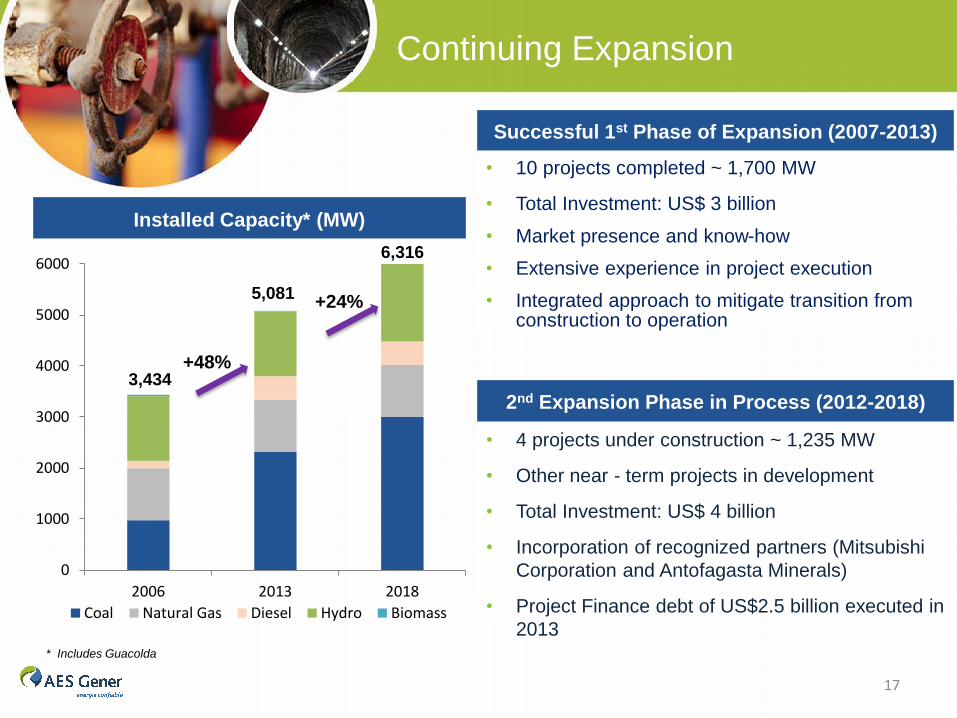

Continuing Expansion

Installed Capacity* (MW)

0

1000

2000

3000

4000

5000

6000

2006 2013 2018

Coal Natural Gas Diesel Hydro Biomass

3,434

5,081

* Includes Guacolda

+48%

6,316

+24%

2nd Expansion Phase in Process (2012-2018)

• 4 projects under construction ~ 1,235 MW

• Other near - term projects in development

• Total Investment: US$ 4 billion

• Incorporation of recognized partners (Mitsubishi

Corporation and Antofagasta Minerals)

• Project Finance debt of US$2.5 billion executed in

2013

Successful 1st Phase of Expansion (2007-2013)

• 10 projects completed ~ 1,700 MW

• Total Investment: US$ 3 billion

• Market presence and know-how

• Extensive experience in project execution

• Integrated approach to mitigate transition from construction to operation

Financing Plan:

2nd Expansion Phase

18

Project Level Debt (Project Finance)

• Cochrane Project: US$ 1,000 million

• Alto Maipo Project: US$ 1,217 million

• Guacolda V Project: US$ 318 million

• Tunjita Project: US$ 63 million

Equity Contribution

• Partners (Mitsubishi Corporation & Antofagasta Minerals)

• Junior Subordinated Notes: US$ 300 million

• Capital Increase:

• Approximately US$150 – US$200 million

• AES Corp has indicated intention to participate

Total Investment

~ US$ 4 billion

Attractive projects portfolio under

construction

Cochrane - 532 MW Coal

Non-recourse project

finance of US$1,000 million

Mitsubishi Corp:40% partner

Investment: US$ 1.35 billion

Estimated operation date:

2016

27% progress

2

2

4

Use of flows from Tunjita

river deviation

Investment: US$68 million

Estimated operation date:

2H 2014

71% progress

Tunjita – 20MW Hydro (run-of-river) 1

1 Santiago

Bogotá

Non-recourse project

finance of US$318 million

Investment: US$450

million

Estimated operation date:

2015

50% progress

Guacolda V – 152 MW Carbón 4

3

Non-recourse project

finance of US$ 1,217

million

AMSA: 40% partner

Investment: US$ 2.05

billion

Estimated operation date:

2018

Alto Maipo – 531 MW Hydro (run-of.river) 3

Installation in Units I and

II of Ventanas and

Norgener plants

Investment as of

December 2013:

~ US$84 million Norgener

~ US$72 million Ventanas

Installation in Units I, II

and IV of Guacolda

Emission Control Equipment 5

Antofagasta

19

220 MW – (First stage of 20

MW)

Environmental approval

obtained in 2012

Adjacent to Los Andes

substation

Santiago

Antofagasta

6

7

Solar Project Andes - SING

750 MW – coal (2 units)

Located close to Constitución,

VII region

Environmental approval

obtained in 2008

Los Robles - SIC 6

Other Projects

Angamos Desalinization Plant

SING – SADI Interconnection

Existing water rights (hydro)

Battery Energy Storage (BESS)

8

7

20

Other Development Projects

AES

GENER

KEY TAKEAWAYS

21

Key Takeaways

• Dry and variable hydrology in Colombia

• Lower spot prices and higher withdrawal costs in SING

• Maintenance at Ventanas Complex (Units I and III) and Norgener Complex (Units I and II) in Q3 and Q4

• Major maintenance at Nueva Renca from May-September

• Higher coal generation due to start-up of Ventanas IV in March

• Partnerships executed for Cochrane and Alto Maipo projects

• Execution of project finance debt for ~ US$2.5 billion

• Issue of Subordinated Bond for $450 million

• Capital Increase of approximately US$150 - US$200 million in 2Q 2014

Balanced Financial Structure

Achievement of Important Milestones

Challenging 2013 But Same Solid Fundamentals

• Completion of construction and start-up of commercial operations of Ventanas IV

• Initiation of construction of Cochrane and Alto Maipo projects

22

23

www.aesgener.com