Embed Size (px)

Citation preview

A f f o r d a b l e H o u s i n g

C o m p l i a n c e B e s t

P r a c t i c e s M a n u a l

A Leas ing Consul tant ’s Guide to

Compl iance Monitor ing Requirements of

Af fordab le Hous ing Programs

By : J o s é Apon t e , HCCP , NCP - E , SHCM

Reproductions are not permitted without the expressed

written permission of Preferred Compliance Solutions, LLC.

© 2020 Preferred Compliance Solutions, LLC. All Rights Reserved

595 S. 80 E. Suite 415 Logan, Utah 84321

Website: www.preferredcompliance.com

Purpose of this Manual

This manual is intended to be a resource for Preferred Compliance Solutions, LLC. clients

that have been given the responsibility of managing and maintaining compliance.

This manual is a training and reference guide. It is designed to answer the most frequently

asked questions regarding the program procedures, rules, and regulations, as interpreted

and adhered as policy and procedures. It should be a useful resource to on-site

management personnel.

Although state agencies and their contractors monitor program compliance, most times

their compliance requirements invite more lenient procedures than those which are set

forth by the regulations as the most reliable. These also do not take into consideration a

lender or syndicator’s interpretation of compliance, and the owner’s requirement to adhere

to these when more stringent than those set by the state.

Here at Preferred Compliance Solutions, LLC. we believe compliance practices can be

labeled as:

a) Good b) Better c) Best

Policies and procedures in this manual have been set by management for your community

and Preferred Compliance Solutions, LLC. to ensure we protect the owner’s interest with

the BEST compliance program possible.

Property staff must contact management prior to making any exceptions to any of these

policies and/or procedures.

A F F O R D A B L E H O U S I N G C O M P L I A N C E M A N U A L

i

C H A P T E R 1 P A G E

Introduction To Compliance

1.0 Introduction to Compliance 1

1.1 How Does This Affect Your Community? 1

1.2 LIHTC Program Organization Chart 2

1.3 Compliance Timetable 3

1.4 Our Policy 4

1.5 Compliance Involvement With Applications 4

1.6 Managing a Tax Credit Property 7

1.7 Key Stages 8

1.8 Basic Requirements 9

1.9 State Audit Timelines (Annual Management

Review) 10

1.10 The Day of the Audit 10

1.11 After the Audit 11

1.12 Common Non-Compliance 12

1.13 Non-Correctible Non-Compliance 12

1.14 Non-optional vs optional Fees 13

1.15 Overcharged Rent 14

1.16 Rent in Units with Rental Assistance 15

C H A P T E R 2 P A G E

Interviewing an Applicant

2.0 Welcome Card 16

2.1 Four Steps to Pre-Qualifying Applicants 16

2.2 The Application 16

2.3 Identification Needed 18

2.4 Household and Family Size 18

2.5 Absentee Spouses 20

2.6 Underage Household Members Not Members

of the Family 21

2.7 Live In Aide 22

2.8 Full Time Student Applicant 23

2.9 HOME and section 8 Student Rule 24

2.10 Student Exemptions: 25

2.11 Demographic Requirements 26

2.12 Demographic Definitions 27

C H A P T E R 3 P A G E

Anticipated Gross Annual Income

3.0 Types of Income That Must be Included in

the Income Calculation 31

3.1 Types of Income That are NOT Included in

the Income Calculation 44

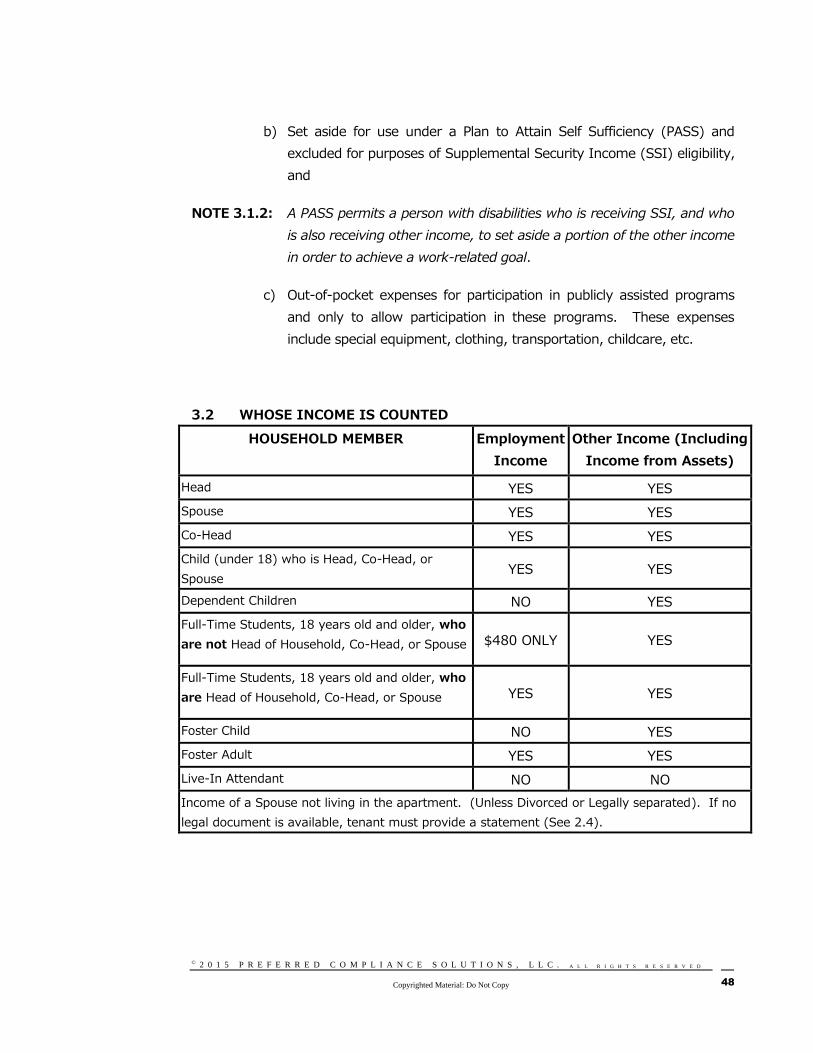

3.2 Whose Income is Counted 48

C H A P T E R 4 P A G E

Verifying and Documenting Income

4.0 Methods of Income Verification 49

4.1 Reviewing Reported Income Verification 49

4.2 Acceptable Income Verification 51

4.3 Acceptable Forms of Income Verification 58

C H A P T E R 5 P A G E

Calculating Total Gross Annual Income

5.0 Calculating Anticipated Gross Income 65

5.1 Hourly Full Time Employment 65

5.2 Weekly Full-Time Employment 66

5.3 Bi-Weekly Full-Time Employment 66

5.4 Bi-Monthly Full-Time Employment 66

5.5 When Calculating Seasonal or Part-Time

Employment 67

5.6 Year-to-Date Calculation 67

5.7 Pay Increase Calculation 68

5.8 Calculating Income from Educational

Assistance 71

5.9 Annual Income Quick Reference Chart 72

C H A P T E R 6 P A G E

Unemployed Applicants & Applicants Receiving

Rental Assistance (i.e. Section 8)

6.0 Unemployed Applicants 73

6.1 Applicants Participating in Rental Assistance

Programs 73

TABLE OF CONTEN TS

A F F O R D A B L E H O U S I N G C O M P L I A N C E M A N U A L

ii

C H A P T E R 7 P A G E

Included and Excluded Assets

7.0 Assets 76

7.1 Included Assets 76

7.2 Excluded Assets 79

C H A P T E R 8 P A G E

Documenting and Calculating Assets

8.0 Asset verification 81

8.1 Determining the Value of Assets 81

8.2 Checking and Savings Accounts 82

8.3 Real Estate 84

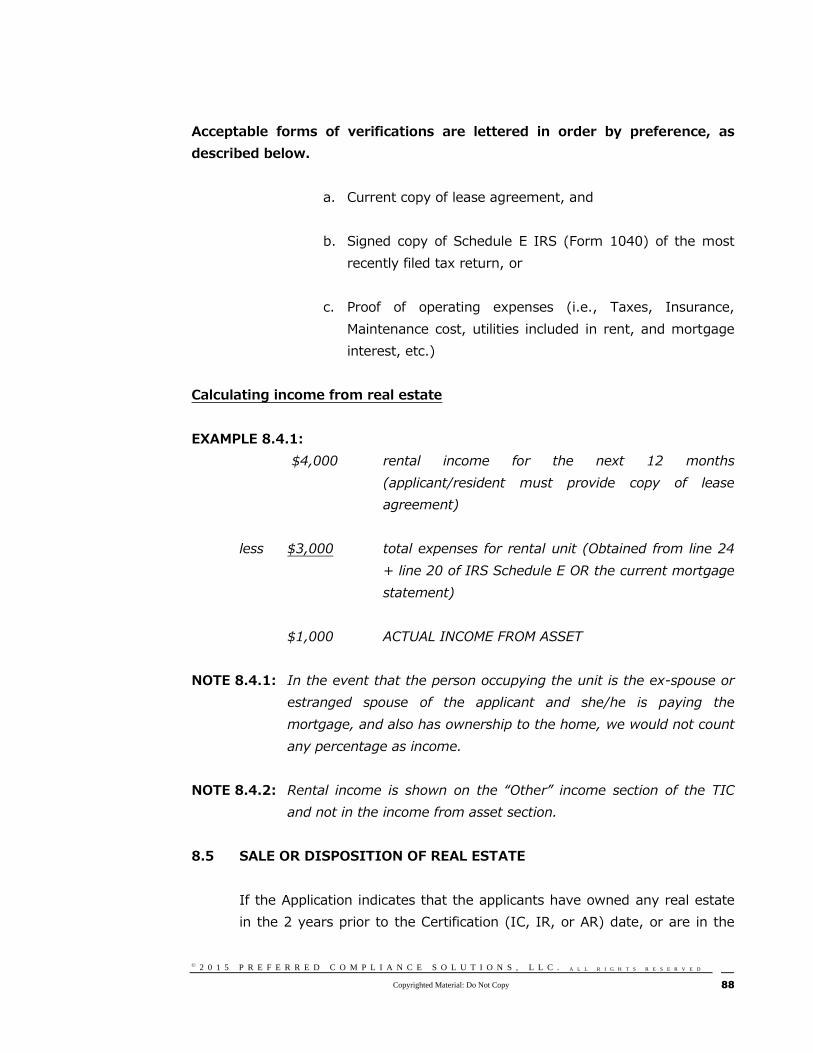

8.4 Rental Income From Real Estate 87

8.5 Sale or Disposition of Real Estate 88

8.6 Disposal of Assets for Less than Fair Market

Value 89

8.7 Documenting CDs, Money Market Accounts

or Treasury Bills 91

8.8 Documenting Stocks or Securities 92

8.9 Documenting Trust Funds 93

8.10 Documenting Bonds 98

8.11 Documenting 401K and retirement accounts99

8.12 Documenting IRAs, Keogh or Other

Retirement Savings Accounts 100

8.13 Annuities 101

C H A P T E R 9 P A G E

Tenant Income Certification

9.0 Tenant Income Certification (TIC) 104

9.1 Line-By-Line Instructions 105

C H A P T E R 1 0 P A G E

Change in Status After Move In

10.0 Changes in Family Size 113

10.1 Family Size Decrease 113

10.2 Family Size Increase 114

10.3 Unit Transfers 115

C H A P T E R 1 1 P A G E

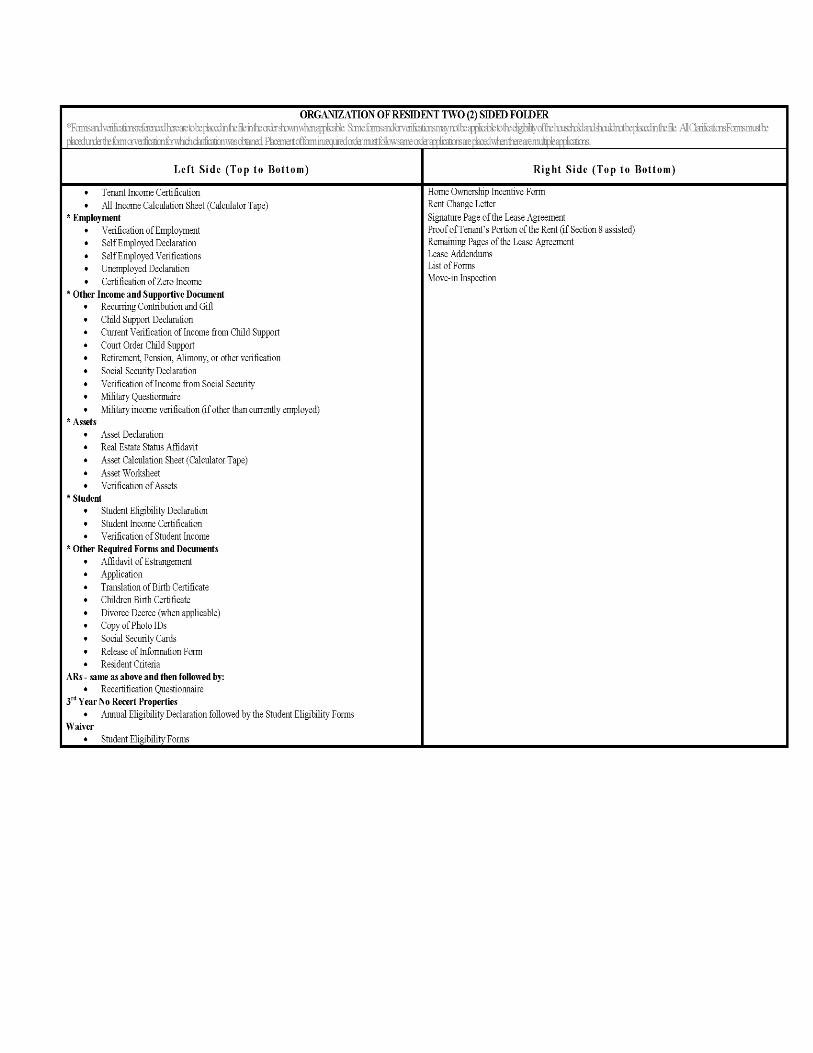

Resident Files

11.0 Resident Files 116

11.1 Correspondance File Set-Up 117

11.2 File Dividers 117

11.3 Compliance File Set-Up 117

11.4 Recommended File Set-Up 118

11.5 Employee Resident File 120

C H A P T E R 1 2 P A G E

Record Keeping

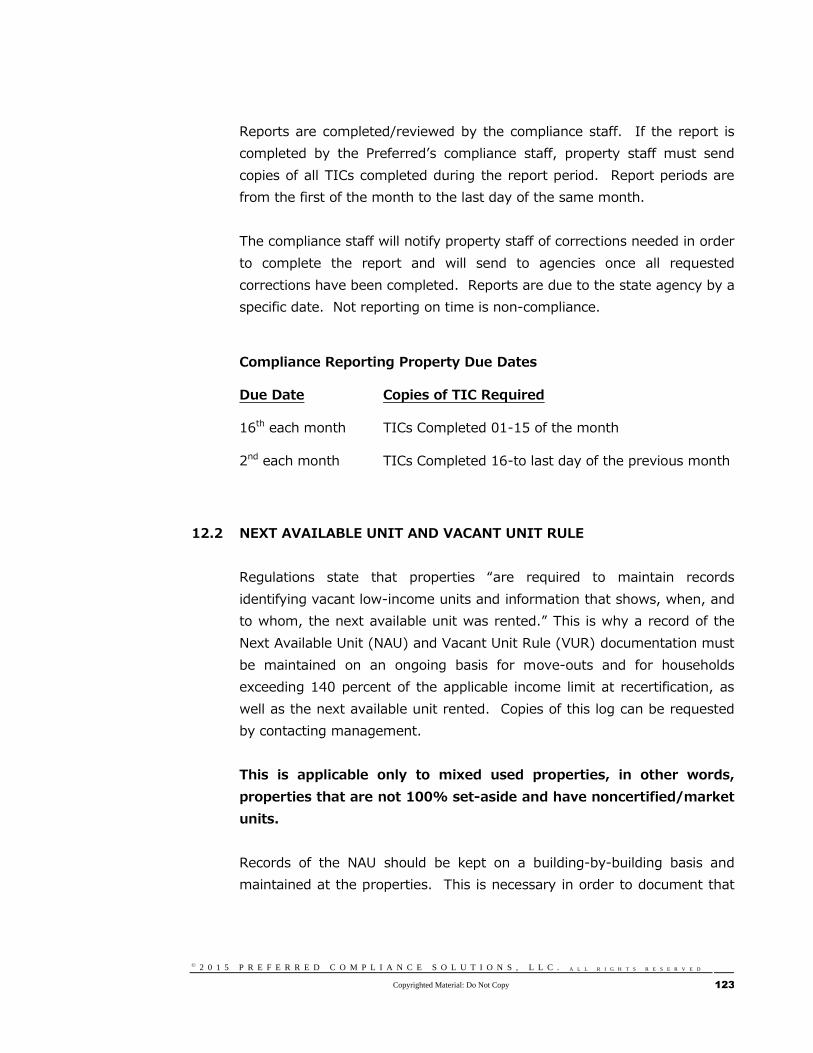

12.0 Reporting Requirements 122

12.1 Program Report 122

12.2 Next available unit and vacant unit rule 123

12.3 Line-By-Line Instructions (Preferred’s NAU

Log) 127

C H A P T E R 1 3 P A G E

Lease Agreement vs. Annual Recertification

13.0 Lease Agreement 130

13.1 Lease Agreement vs. Annual Recertification

(AR) 130

13.2 Annual Recertification (AR) 131

13.3 AR Notice Schedule 132

C H A P T E R 1 4 P A G E

Resident Programs (Tenant Services)

14.0 Resident Programs 134

14.1 Frequency 135

14.2 Record Keeping 135

14.3 Compliance Involvement 136

C H A P T E R 1 5 P A G E

Forms

15.0 Compliance Forms 137

A F F O R D A B L E H O U S I N G C O M P L I A N C E M A N U A L

iii

C H A P T E R 1 6 P A G E

Maintenance Staff Compliance Policies And

Procedures

16.0 Maintenance Staff And State Audits 138

16.1 Preparing for a Physical Inspection 139

16.2 Major Areas of Focus 142

C H A P T E R 1 7 P A G E

Las políticas y procedimientos de cumplimiento del

personal de mantenimiento

17.0 El personal de mantenimiento y las

auditorias del estado 145

17.1 Preparamiento para una inspección física. 146

17.2 Áreas Principales de Atención 149

C H A P T E R 1 8 P A G E

Acquisition and Rehabilitation

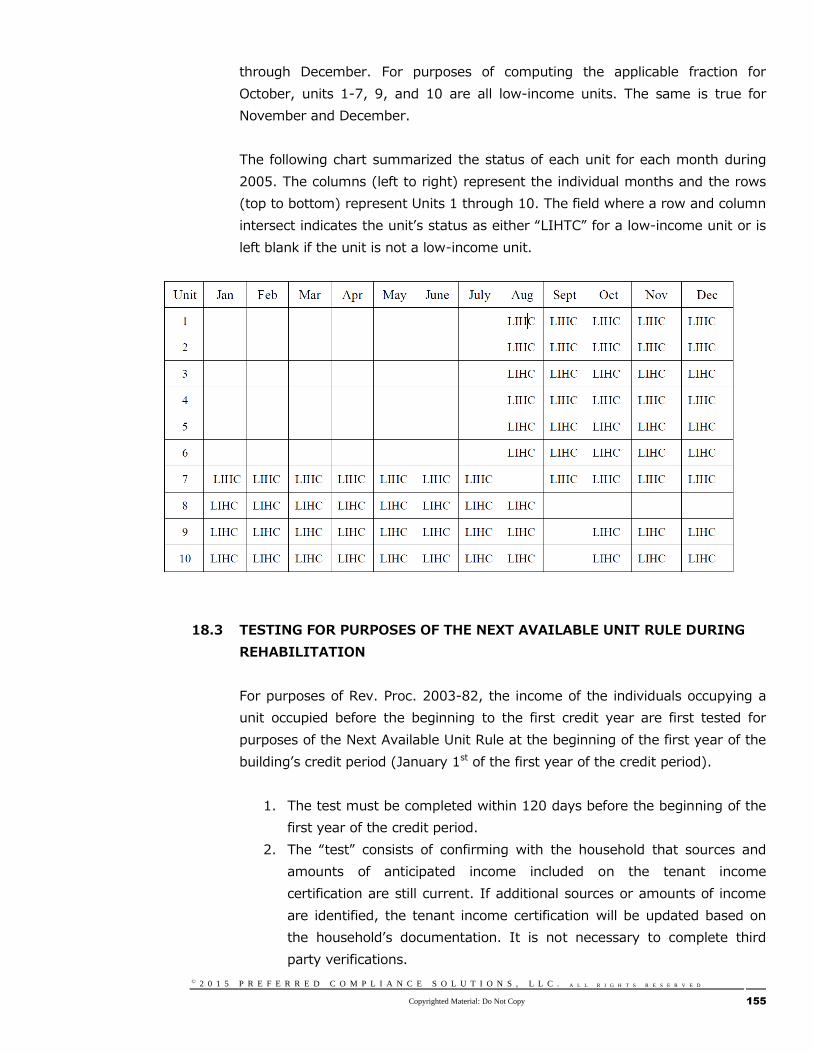

18.0 Acquisition and Rehabilitation 152

18.1 Applicable Fraction 153

18.2 Tracking the Applicable Fraction During the

First Year of the Credit Period 153

18.3 Testing for Purposes of the Next Available

Unit Rule During Rehabilitation 155

INTRODUCTION TO COMPLIANCE

1.0 INTRODUCTION TO COMPLIANCE

In order to know how to comply, one must first understand the meaning of

compliance. Let us look at the definition of compliance. Compliance is the

act of yielding to a wish, request, or demand; acquiescence. In other

words, to do as you are directed, to follow the rules or demands of another.

How Does COMPLIANCE Pertain to Us?

Some of the communities that our company manages participate in federal

income tax credit, and other programs instituted by Congress, to provide

eligible households quality and affordable home living. To ensure the

integrity of the programs, the IRS and HUD have state and local agencies

oversee compliance with their regulations.

1.1 HOW DOES THIS AFFECT YOUR COMMUNITY?

Whenever you have a valuable item such as tax credits and other affordable

housing programs the demand is usually greater than the supply. Whoever

meets and maintains compliance (adheres to the requirements of the IRS, HUD

and the state) may utilize the assistance; whoever does not comply, (ignores

these requirements) will be found to be in NON-COMPLIANCE and could be

eliminated from using the programs. Our business is based on managing

communities that have secured these tax credits. If we do not adhere to the

rules, and are found to be in NON-COMPLIANCE, the community could lose

the assistance, and subsequently we could lose the management. The bright

Chapter

1

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 2

side is, if you follow the guidelines as set forth in this chapter, compliance is

easy!

This chapter outlines the compliance issues relevant to the Low Income

Housing Tax Credit Program (LIHTC), Bonds, and HOME as set forth in Section

42 of the Internal Revenue Code, HUD Handbook 4350.3, and state

Compliance Guidebook. State agencies administer the Programs and conduct

routine audits of the resident files by visiting the communities on a regular

basis. This is to ensure that the community and owners adhere to the program

rules. They also require submission of reports on a regular basis, documenting

the demographics and income of the residents. All of the units at your

community are regulated by the Internal Revenue Service and monitored by

your particular state agency.

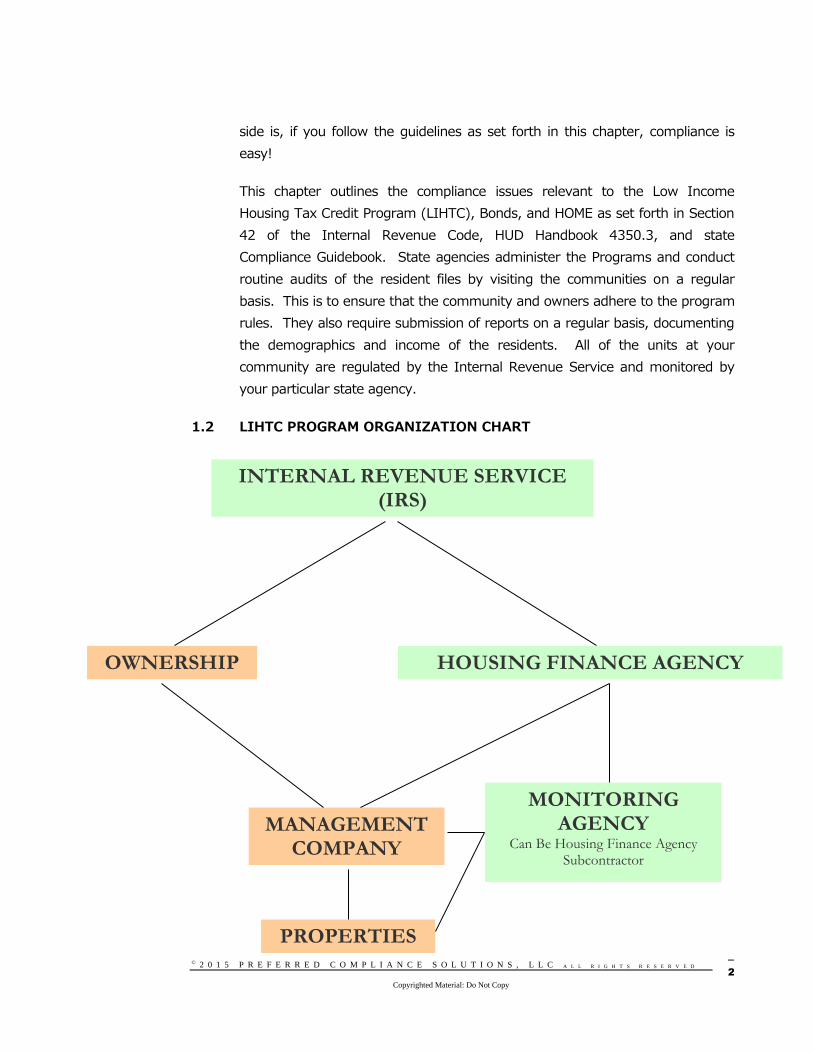

1.2 LIHTC PROGRAM ORGANIZATION CHART

OWNERSHIP

PROPERTIES

HOUSING FINANCE AGENCY

MONITORING AGENCY

Can Be Housing Finance Agency Subcontractor

INTERNAL REVENUE SERVICE (IRS)

MANAGEMENT COMPANY

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 3

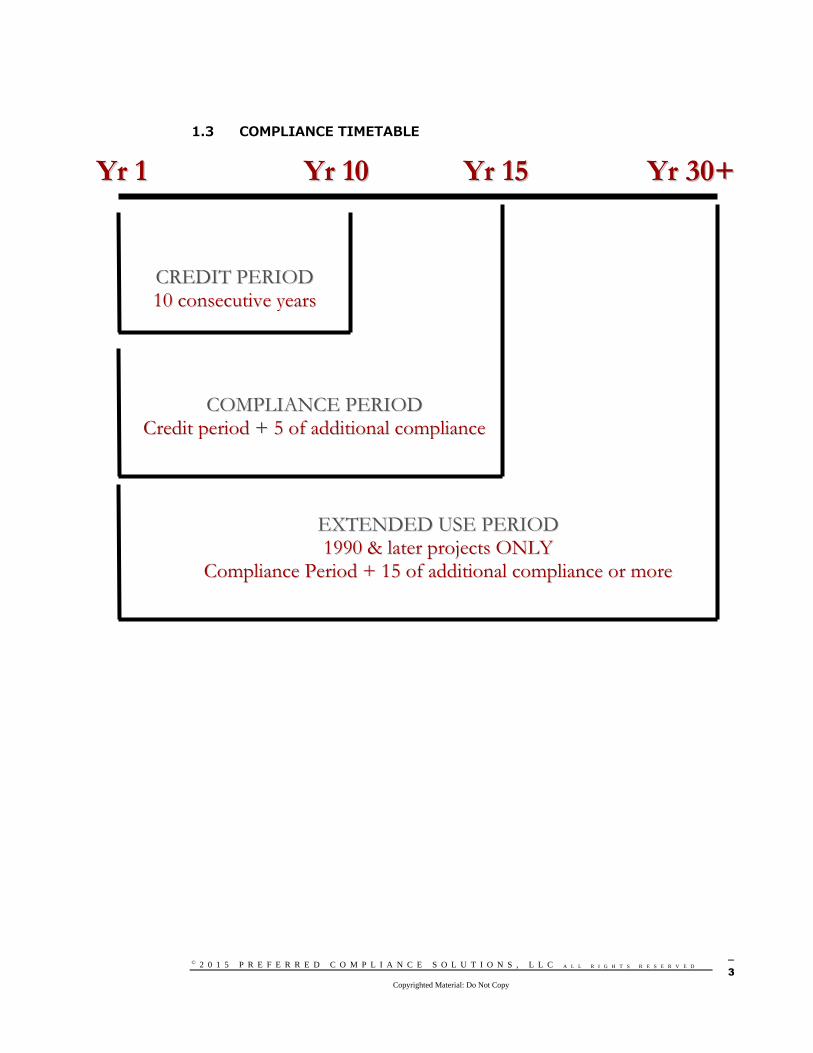

1.3 COMPLIANCE TIMETABLE

CCRREEDDIITT PPEERRIIOODD

1100 ccoonnsseeccuuttiivvee yyeeaarrss

CCOOMMPPLLIIAANNCCEE PPEERRIIOODD

CCrreeddiitt ppeerriioodd ++ 55 ooff aaddddiittiioonnaall ccoommpplliiaannccee

YYrr 11 YYrr 1100 YYrr 1155 YYrr 3300++

EEXXTTEENNDDEEDD UUSSEE PPEERRIIOODD

11999900 && llaatteerr pprroojjeeccttss OONNLLYY

CCoommpplliiaannccee PPeerriioodd ++ 1155 ooff aaddddiittiioonnaall ccoommpplliiaannccee oorr mmoorree

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 4

1.4 OUR POLICY

For your protection, all compliance related correspondence, reports and

questions must be directed to management or Preferred Compliance Solutions

staff. All outgoing reports will be reviewed by this department, prior to

forwarding to a State, local or Federal Agency. On site staff must never

contact State, local or Federal Agencies. Any calls initiated by State, local or

Federal Agencies or their monitoring agents must be forwarded to the

compliance department as well. There are no exceptions to this policy.

1.5 COMPLIANCE INVOLVEMENT WITH APPLICATIONS

Management and/or, when applicable, Preferred Compliance Solutions

MUST review and approve all applications for residency prior to move

in, and recertifications immediately upon completion. At no time

should anyone move-in to your community without written final approval.

Compliance Approval

Immediately after all documentation needed in order to qualify a household

with program requirements have been received, the manager must review

all documents prior to sending for approval. No household should move in

unless written approval (“Final Results”) has been received.

Although, Preferred Compliance Solutions reviews all initial certifications on

the same day these are received, final result/approval might take more

than a day due to corrections needed for the file. Therefore, proactively,

an applicant’s move-in date should be scheduled accordingly (no less than

3 business days from the time sent for review and approval). In order to

review application(s), you must send the following information. Note that

not ensuring all documentation is submitted for review may cause a delay

in receiving a final result:

❖ Compliance Application Coversheet

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 5

❖ Fully Completed Application

❖ Verification(s) of Income and Supporting Documentation

❖ Asset Affidavit and Supporting Documentation

❖ Student Eligibility Affidavit, Student Verification Form and Student

Income Certification (when applicable)

❖ Birth Certificates that show parent’s name for all minors

❖ Clarification Forms & Statements completed (when applicable)

❖ Any other verification of documentation needed to properly qualify

household

Corrections and/or Clarifications Request

Once compliance reviews the documents listed above, when applicable,

they will issue a “Correction Request” that will list any unclear or non-

compliance findings that will need to be corrected and/or clarified by the

community staff.

Once resolved, corrections and/or clarifications must be sent to compliance.

Once received, compliance staff will review these corrections and/or

clarifications and determine if the “Additional Steps Needed” can be issued.

Additional Steps Needed

Once a file is ready for approval, Preferred Compliance will issue an

“Additional Steps Needed” template indicating the certification can be

completed. This will require a signed lease and TIC be sent to compliance

for final review and “Final Approval”.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 6

Final Approval

Final results will be issued in the form of a “Final Results” template which

will detail if application is approved or denied, with the reason. “Final

Results” will be posted to Preferred Compliance Solutions, LLC NextGen

eFile system. When a correction or result is posted, those able to upload

files to the NextGen eFile system for your property will receive an email

notification. Therefore, it is critical that a current email is listed in their

NextGen eFile account. However, in the absence of a proper email, results

can still be accessed by logging into the NextGen eFile Access system.

It is critical to the eligibility of the household that all corrections

made during the file review process leading to a final result make it

into the final tenant file. Not doing so could cause the unit to be in

non-compliance.

NextGen eFile Access

“NextGen eFile Access” section is a free file sharing solution provided by

Preferred Compliance Solutions, LLC. This solution allows properties the

convenience of uploading applications and corrections that will be reviewed

by compliance professionals. It allows the properties to view the

information before it is submitted, therefore ensuring that all documents

are uploaded. It also gives the properties the immediate confirmation that

documents have been received by our system.

In addition, when using “NextGen eFile Access” your properties are able to

view and print a record of the date and time an application was received

and printed in our office. Because of non-compliance findings, correction

requests and approvals are also uploaded to this section, this also serves as

a solution to our compliance professionals in delivering correction requests

and final results of compliance status.

Best of all it saves everyone time and money, no storage space, no copies

to make, and no boxes with copies of files to ship.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 7

1.6 MANAGING A TAX CREDIT PROPERTY

NOTE 1.6.1: Remember, if you have more than one program on your property, you

should always use the most restrictive guideline.

To successfully manage a tax credit property, you must always have the

following information on hand. This can be found in the Land Use Restriction

Agreement (LURA) for your property:

❖ The number of units set aside for tax credit compliance

requirements

❖ The applicable maximum income for each family size

❖ The maximum allowable gross rents

❖ The utility allowance for each unit size

❖ Resident services promised on the Land Use Restriction Agreement

(LURA) and/or Extended Use Agreement (EUA)

The following information needs to be posted where all residents and

prospective residents can see it:

❖ Income Limits and Rents

❖ Utility Allowance Chart

❖ Resident Selection Policy

❖ Late Charge Policy

❖ Fair Housing Poster (English and Spanish)

❖ Office Hours

❖ Emergency Phone Numbers

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 8

1.7 KEY STAGES

There are four key stages in the life of a Tax Credit project.

A. DEVELO PMENT PERIOD

The development period for a project begins when commitment of LIHTCs or

other Affordable Housing program(s) are made by the state and lasts until the

owner places the project in service. A building is determined to be “placed in

service” when the first unit is ready for occupancy (certified for occupancy). In

general, the owner must place the project in service before the end of the 2nd

calendar year in which the project receives its LIHTC or other Affordable

Housing program commitment.

B. LEASE-UP PERIOD

The lease-up period starts once a project has been placed in service and lasts

until the owner begins to claim the project’s Tax Credits. Owners can start

claiming a project’s Tax Credits at the end of the tax year following the project

being placed in service.

During this period, owner/managers need to qualify all of the units they will

count as set-aside.

C. COMPLIANCE PERIOD (SEE SECTION 1 .3)

The compliance period begins with the first tax year in which the owner claims

Tax Credits for the project and lasts for 15 consecutive years.

D. EXTENDED USE PERIOD (SEE SECTION 1.3)

Once the 15-year compliance period ends, projects enter the extended use

period. Owners/managers of these projects are required to maintain the

property’s low-income occupancy for an additional 15 years beyond the end of

the compliance period – the remaining life of the extended use agreement for

the project. In some cases longer, for example, most of our communities

require a 50-year extended use period.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 9

1.8 BASIC REQUIREMENTS

For a unit to be counted as a Tax Credit unit, the following six conditions

must be met:

❖ All units in the same building identification number must be certified

by qualified households.

❖ The resident’s income may not exceed the applicable income limit

for your community (at time of move-in).

❖ The rent paid by the resident plus allowance for resident-paid

utilities may not exceed the maximum allowable rent for that unit.

❖ The physical condition of that unit must meet local health, safety

and building codes.

❖ Management must execute a lease of no less than seven months

with the resident.

❖ Management must list the unit as an eligible unit on reports

submitted to the state or local agencies.

❖ In most states and in mixed used properties, property staff must re-

examine the resident’s eligibility annually and maintain rents at or

below applicable rent limits.

As mentioned before, here at Preferred Compliance Solutions, LLC. we believe

compliance practices can be labeled as:

a) Good b) Better c) Best

Policies and procedures in this manual have been set by management for your

community and Preferred Compliance Solutions to ensure we protect these

basic requirements with the BEST compliance program possible.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 10

1.9 STATE AUDIT TIMELINES (ANNUAL MANAGEMENT REVIEW)

The State or local agency will write or call your office, management and/or

owner telling them the date they will be doing an on-site audit of your property.

If you receive a letter or a call, please notify the compliance department and

your supervisor immediately. Please note in many instances, notice of an audit

is received only days before the audit.

NOTE 1.9.1: The date of the Audit is set by the State or local agency and is

always changing. There are no set dates.

NOTE 1.9.2: Prior to the date of the audit

❖ Send a notice to all residents advising them of the date of

the audit, and that apartments will be randomly picked for a

physical inspection.

❖ Do a complete inventory of files.

1.10 THE DAY OF THE AUDIT

❖ Have a folder prepared with current copies of

a. Questionnaire (State or their monitoring agency will mail with audit

notification)

b. Copies of your last advertising

c. Last three months Newsletters

d. Rent Roll (printed the day of the audit)

e. Updated copy of Utility Allowance (if using PHA chart, dated within

90 days)

f. Latest Income Limits and Rent Schedule Chart

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 11

g. Updated Next Available Unit Log (Properties with market units only)

h. Updated State’s program compliance reports including summary

pages

i. Copies of resident services sign-in logs and other applicable

information needed to prove that it was provided (when applicable)

❖ Have a quiet area with plenty of workspace for the auditor(s)

❖ Have refreshments on hand (i.e. soda, chips, etc.)

❖ Check on auditor(s) periodically to see if they need anything

A representative from management may be present to furnish all

information and answer the Auditor’s questions. This will free you to

work and keep you from getting into a situation in which you may

feel unsure. Be polite but look to the representative for guidance. If

you happen to be in a position that your representative is not present

during the audit, you are to be polite, but ask the Auditor to refer

questions to the representative. The representative is there to take the

pressure off of you and to protect you from any miscommunication.

1.11 AFTER THE AUDIT

After the audit has been completed, you will receive a review letter. This takes

an average of 2 to 4 weeks. When the review letter is received, you will be

informed of the outcome.

Any time you receive a letter from the State or local agency, call

management and send a copy immediately.

Do not answer questions about your audit either in person or by phone if the

State or local agency contacts you. Instead, politely offer to take their name,

phone number, and inform them that someone from management will contact

them as soon as possible. You must immediately contact the compliance

department. We may already have the answer for the caller, and they

may just be confused about whom to call.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 12

1.12 COMMON NON-COMPLIANCE

a. Units not ready for immediate occupancy – IRS has instructed state

agencies to issue 8823s for vacant units that are not available for

rent because the units are not prepared for immediate occupancy

b. Not complying with the time requirements of forms required by the

monitoring agency

c. Not having the resident file information such as application,

certification and/or lease

d. Health and life safety issues such as smoke detectors

e. Not completing required annual income certifications in a timely

manner

f. Not calculating assets correctly

g. Not calculating income correctly

h. Using incorrect Income Limits – not updating yearly in a timely

manner

i. Not updating Utility Allowance figures annually as required

j. Exceeding Maximum Allowable Rent as a result of using incorrect

AGMI or Utility Allowances

k. Failure to make the next unit available to a Housing Credit qualified

household when an existing HC household’s income exceeds 140%

of the maximum allowable income.

1.13 NON-CORRECTIBLE NON-COMPLIANCE

a. Ineligible household

b. Improper transfers

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 13

c. Ineligible students

d. Not reporting in a timely manner

e. Overcharged rent

1.14 NON-OPTIONAL VS OPTIONAL FEES

Typical non-compliance may involve converting common areas to

commercial property or charging fees for facilities (such as a swimming

pool and clubhouse), the cost of which were included in the Eligible Basis.

Fees may not be charged for common areas that have been included

as part of the Eligible Basis. Prior to charging a fee, property staff

must confirm with management that such fee is allowed under

program regulations.

Units may be residential rental property notwithstanding the fact that

services other than housing are provided. However, any charges to low-

income tenants for services that are not optional generally must be

included in gross rent calculation. A service is optional when the service is

not a condition of occupancy and there is a reasonable alternative.

PET, LAUNDRY ROOM, AND OTHER FEES

Charges for non-optional services such as a washer and/or dryer hookup

fee and built-in/on storage sheds (paid month-to-month or a single

payment) would always be included within gross rent. No separate fees

should be charged for tenant facilities (i.e., pools, parking, recreational

facilities) if the costs of the facilities are included in eligible basis. Assuming

they are optional, charges such as pet fees, laundry room fees, garage, and

storage fees may be charged in addition to the rent; i.e., they are not

included in the rent computation. All required costs or fees, i.e.,

redecorating fees, which are not refundable, are included in the rent

computation and therefore could result in overcharged rent.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 14

APPLICATION FEE

Unless otherwise approved by the State Agency, application fees may be

charged to cover the actual cost of checking a prospective tenant’s income,

credit history, and landlord references. The fee is limited to recovery of the

actual out-of-pocket costs. No amount may be charged in excess of the

average expected out-of-pocket costs of checking tenant qualifications at

the project. It is also acceptable for the applicant to pay the fee directly to

the third party actually providing the applicant’s rental history.

1.15 OVERCHARGED RENT

Gross rent includes any utility allowance. Tenant rent is the portion of the

Total Tenant Payment the tenant pays each month to the property for rent.

Tenant rent is calculated by subtracting the utility allowance from the Total

Tenant Payment.

Because HUD determines a tenant’s rent on a monthly basis, state

agencies must determine whether the property is in compliance with

the gross rent limits each month of the owner’s current tax year.

The worst noncompliance possible is over charged rent. Once a unit is

determined to have been noncompliant with the rent limits, the unit ceases

to be a low-income unit for the remainder of the owner’s tax year. The unit

is back in compliance on the first day of the next tax year if the rent

charged on a monthly basis does not exceed the limit. An owner cannot

avoid the disallowance of the tax credits by rebating excess rent or fees to

the affected tenants.

EXAMPLE 1.15.0:

The owner of a 100% LIHC building leased all the units to eligible

tenants during 2007, the third year of the credit period. However,

management inadvertently overcharged rent to tenants occupying 3

bedroom apartments. The error impacted 15 out of 75 units. The

owner is a calendar year taxpayer.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 15

The Applicable Fraction for 2007 is 60/75, which equals 80 percent,

rather than the required 75/75, which is equals to 100 percent.

Therefore, the owner has lost 20 percent credits for the calendar

year. The unit is back in compliance on January 1, 2008 if the owner

correctly limits the rent for all units.

EXAMPLE 1.15.1:

Overcharged Rent Impacted Minimum Set-Aside

The owner leased the rental units in a 100% LIHC building to

eligible tenants by the end of the first year of the credit period.

However, management overcharged rent for all the units and, as a

result, failed to meet the minimum set-aside for the first year of the

credit period.

The building does not qualify for LIHC.

1.16 RENT IN UNITS WITH RENTAL ASSISTANCE

As long as the household is receiving Federal rental assistance, their portion

of the rent, according to the Section 8 calculations, can be more than the

maximum allowable rent applicable to the unit, if permitted by your state

agency. However, USC Title 26 Section 42(g)(2)E states that if their

income rises to a point where it maxes out under Section 8, so that no

rental assistance payment is being received, they are no longer considered

a Section 8 household, and the HC rent restrictions “kick-in” and the

household’s rent would have to be reduced.

EXAMPLE 1.16.1:

At initial certification Sallie is receiving rental assistance. Her tenant

paid portion, as calculated by Section 8, is $695; this exceeds the

maximum allowable rent of $690. As long as she continues to receive

Federal rental assistance, the tenant portion of the rent plus utility

allowance can be more than the maximum allowable rent of $690.

However, if Sallie were to stop receiving Section 8 rental assistance, her

rent must be reduced to applicable limits of $690.

INTERVIEWING AN APPLICANT

2.0 WELCOME CARD

The welcome card is a tool designed by management to determine the

eligibility of prospective applicants. Use this form to assist in the initial

interview with the prospective applicant.

2.1 FOUR STEPS TO PRE-QUALIFYING APPLICANTS

❖ Determine Household Size

❖ Compute Annual Gross Income

❖ Compare Income to Maximum Allowable Income Limits

❖ Verify Income Information

❖ Determine all household members student status (see section 2.8)

2.2 THE APPLICATION

The applicant must always complete the application with the assistance of a

leasing consultant. The application may never be given to anyone to be

completed outside of the leasing office.

It is important that all sections of the application are fully and clearly

completed and signed by all adults. N/A is NOT an acceptable answer to any

question on the application. Answer “No” or “None” instead.

Chapter

2

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 17

Multiple applicants (other than spouse) must fill out separate applications.

The application should include:

❖ The name and correct age of each person who will occupy the unit

(legal name should be given just as it will appear on the Lease and

Tenant Income Certifications).

❖ All sources and amounts of current and anticipated annual income

expected to be earned during the twelve (12) month certification

period (including total assets and asset income).

❖ The signature of the applicant(s) and the date the application was

completed. (You should explain to the applicant that all the

information they provide is considered confidential and will be

handled accordingly.)

❖ Student Status including full and part-time.

When the application reflects anticipated income less than what the income

verified by the employer states (by a difference of $1,000 or more), the

applicant must clarify with a written statement explaining the reason for the

difference. If the applicant anticipates significantly more than what the verified

income reflects (by $1,000 or more), to best document eligibility, applicant

must write a very detailed self-affidavit that includes explanation as to why

there are such large differences. Certification must not be completed until

eligibility has been fully documented.

If an area of the application needs to be revised, the applicant should draw a

single line through the incorrect information and list the correct information

above or beside. All changes must be initialed by the applicant.

“WHITE OUT” may never be used. The use of “White Out” on any document

voids the signed document. It is your company’s policy that there be no white

out allowed at the properties.

It is management’s responsibility to obtain sufficient information on all

applicants at the time of application so that verification forms can be

completed.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 18

2.3 IDENTIFICATION NEEDED

NOTE 2.3.1: To properly qualify a household, verifications must always include

picture ID, social security card for everyone and birth certificates for all

occupants under 18. In Senior (Elderly) properties, a government

issued ID is required for household members that will qualify the unit as

“Elderly,”

Applicants with no social security card must provide copies of legal work

permit, green card or other legal document permitting them to work in the

United States. Please be sure to check your resident selection criteria to

see if management has alternate requirements.

BIRTH CERTIFICATES

The importance of birth certificates: Eligibility for low-income housing is

based on an income limit, which is based on the number of people in the

household. We need to determine if the occupants, particularly minors, are

members of the household. Although not required by regulation, the best

way to determine this is to request a Vital Statistics birth certificates. When

there is an absent parent there is a possibility that the household receives

child support. (see sections 2.4, 2.5 and 4.3 for additional guidance)

NOTE 2.3.2: The only exception to this is foster children. In this case, the

resident must provide proof of foster parenthood and we do not

count income paid to the resident for foster care (see section 3.1(E)

for additional guidance) when such income is made through the

official foster care agency.

2.4 HOUSEHOLD AND FAMILY SIZE

As a general rule, a “household” consists of all individuals (or tenants)

residing in a unit. To determine the household income limit, all applicable

income standards are adjusted for family size. For LIHTC purposes, all

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 19

occupants of a unit are considered in the determination of family size

except the following:

1. Live-in aides. A person who resides with one or more elderly

persons, near-elderly persons, or persons with disabilities, and who

is determined to be essential to the care and well-being of the

person(s); is not obligated for the support of the person(s); and

would not be living in the unit except to provide the necessary

supportive services. While a relative may be considered to be a live-

in aide/attendant, they must meet the above requirements. The

income of live-in aides is not included in the household’s income.

2. Guests. A visitor temporarily staying in the unit with the consent of

the tenant or another member of the household who has expressed

or implied authority to consent on behalf of the tenant.

INCLUDED IN HOUSEHOLD SIZE

When determining family size for income limits, you must include the following

individuals who are not living in the unit:

1. Children temporarily absent due to placement in a foster home;

2. Children in joint custody arrangements who are present in the

household 50% or more of the time. If disputed, determine which

parent claimed the children as dependents for purposes of filing a

federal income tax return.

3. Children who are away at school but who live with the family during

school recesses;

4. Unborn children of pregnant women (as self-certified by the

woman);

5. Children who are in the process of being adopted;

6. Foster children that are in the legal guardianship or custody of a

State, county, or private adoption or foster care agency, yet are

cared for by foster parents in their own homes under some kind of

foster care arrangement with the custodial agency.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 20

7. Foster adult is usually an adult with a disability who is unrelated to

the tenant family and who is unable to live alone.

8. Temporarily absent family members who are still considered family

members if approved to live in the unit. For example, the property

may consider a family member who is working in another state on

assignment to be temporarily absent;

9. Family members in the hospital, or a rehabilitation facility, for

periods of limited or fixed duration are considered a family member.

These persons are temporarily absent;

10. Persons permanently confined to a hospital or nursing home. The

family decides if such persons are included when determining family

size for income limits. If the family chooses to include the

permanently confined person as a member of the household,

property staff must include income received by the confined person

in calculating family income.

2.5 ABSENTEE SPOUSES

There are several questions that must be answered when dealing with an

absentee spouse. They are the following:

• Is the absentee spouse a household member?

• Why is the absentee spouse not going to be residing in the apartment?

• For how long is the absentee spouse not going to be residing in the

apartment?

• Is the absentee spouse providing any financial support to the

household?

In the event it is anticipated that the absentee spouse is a household member

and/or will be residing in the unit in the twelve months following the

certification (certification period), his/her income must be documented and

counted towards the maximum allowable income.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 21

The policy and procedure set is; all applicants 18 years and older, or in the case

of emancipation, must sign an “Affidavit of Estrangement” if their spouse will

not be residing in the unit and will not be counted as a household member.

This is not to be confused with an absent spouse who will be counted as a

household member (i.e., away on military leave, temporarily absent, etc.) and

whose income will be counted.

When the spouse will be absent and is, or will, no longer be a household

member for the twelve months following the certification (certification period),

applicant(s) must:

1. Sign an “Affidavit of Estrangement or Absent Spouse” form.

When it is determined that a spouse will be absent due to not being able to

enter the country, and therefore not anticipated to be a household member in

the twelve months following the certification, he/she is not included in the

certification. The applicant should sign an “Affidavit of Estrangement or Absent

Spouse” form and provide supporting documentation as applicable. Any

income he/she contributes to the household is counted as a recurring gift or

contribution.

2.6 UNDERAGE HOUSEHOLD MEMBERS NOT MEMBERS OF THE FAMILY

In order to be considered a household member, a minor must be shown to live

in the household at least 50% of the time, but is not required to be a “family”

member. Applicants are allowed to decide what constitutes their “family.” For

example, if an applicant wants to include his nephew as part of the “family” or

“household,” it is required that the minor be determined part of the household

by how much time the minor will be in the unit.

At time of application, it might be determined by looking at the birth certificate

(See section 2.3) that a parent or both parents are missing from the household.

If at least one parent is in the unit, it could be assumed the child will be in the

unit at least 50% of the time, unless a divorce decree, child support order, or

other documents placed in the file state otherwise.

In the event that both parents are not part of the household, documentation

that the minor is indeed part of the household must be obtained from an

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 22

independent source (guidance counselor, clergy, social worker, school where

the minor is attending, etc.). Documentation must show at least one adult

household member as guardian for the minor.

NOTE 2.6.1: A letter from either the minor’s parent or legal guardian is NOT

sufficient proof. This policy was set to avoid fraudulent letters in an

effort to increase household size in order to increase applicable income

limits.

2.7 LIVE-IN AIDE

A live-in aide is an individual who resides with one or more elderly persons,

near-elderly persons, or persons with disabilities and who:

1. Is determined to be essential to the care and well-being of the

persons;

2. Is not responsible for the support of the persons; and

3. Would not be living in the unit except to provide the necessary

supportive services (24 CFR 5.403).

While a relative may be considered to be a live-in aide, they shall

meet the above requirements, especially the last. The live-in aide

qualifies for occupancy only when the individual needing supportive

services qualifies and shall not qualify for continued occupancy as a

remaining family member. A spouse can never be a live-in aide.

Verification that the live-in aid is needed, must be obtained from the

person’s physician, psychiatrist or other medical practitioner or health care

provider. The property may not require applicant or tenants to provide

access to confidential medical records or to submit to a physical

examination.

Once established that an individual is a Live-in Aide his or her income is not

included in determining household eligibility.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 23

2.8 FULL TIME STUDENT APPLICANT

In general, occupants of a unit should not be considered qualified, if

all of the occupants are full-time students, unless they meet certain

exceptions listed in section 2.9. This is the same at time of annual

recertification as it is at time of initial certification.

The IRS has defined full-time students as follow:

Student Definition: Those attending or who will attend an

educational organization for five months

during the calendar year in which the

certification will be effective (months need not

be consecutive).

Educational Organization: One that normally maintains a regular faculty

and curriculum, and normally has an enrolled

body of pupils or students in the attendance

at the place where its educational activities

are regularly carried on. The term

“educational organization” includes

elementary schools, junior and senior high

schools, colleges, universities, and technical,

trade, and mechanical schools. It does not

include on-the-job training courses.

Determining Status: The determination of student status as full or

part-time is based on the criteria used by the

educational institution the student is

attending. Such is documented by the

institution on the “Student Verification” form.

In order to qualify to reside in a low-income unit when the household is

determined to be composed of all full-time students, they must meet one of

the student exemptions listed in section 2.9.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 24

It must also be noted that in the event a household member is determined

to be a student, full-time or part-time, and the household receives HUD

Section 8 assistance, all income received or anticipated to be received as

educational assistance must be counted in determining the household’s

income eligibility. For additional guidance on this, please see Chapter

3.1(I).

2.9 HOME AND SECTION 8 STUDENT RULE

Effective August 23, 2013 the HOME program adopts the Section 8 Housing

Choice Voucher (HCV) program restrictions on student participation found

at 24 CFR 5.612, which exclude any student that:

1. Is enrolled in a higher education institution

2. Is under age 24

3. Is not a veteran of the U.S. military

4. Is not married

5. Does not have a dependent child(ren)

6. Is not a person with disabilities

7. Is not otherwise individually eligible, or has parents who,

individually or jointly, are not eligible on the basis of income.

All of the above are prohibited from receiving any type of HOME assistance,

including renting HOME-assisted rental units, receiving HOME tenant-based

rental assistance, or otherwise participating in the HOME program

independent of their low- or very low-income families.

What triggers the student rule?

LIHTC/MMRB When ALL household members are students

HOME When ANY member is a student

HOME AND SECTION 8 STUDENT ELIGIBILITY

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 25

A student enrolled in an Institute of Higher Education as defined by the

Higher Education Act of 1965-Amended 1998 will be deemed eligible for

assistance if the student meets all other eligibility requirements, passes

screening criteria and is:

1. Living with parents/guardian or

2. 24 or older or

3. A veteran of the United States armed services or

4. Married or

5. Has a dependent child or

6. Can prove independence of parents including

a. The parents did not claim the student on the most recent tax

return and

b. The student has lived independent of the parents for at least

one year or meets the Department of Education’s definition

of an independent student

c. Can legally sign a lease

7. Is disabled and was receiving assistance as of November 30, 2005

or

8. Has parents who are income eligible for the Section 8 program

2.10 STUDENT EXEMPTIONS:

The following list of exemptions includes those for HOME properties

committed before August 23, 2013. See section 2.9 for a list of those who do

not qualify under the current student rules of the HOME program.

MMRB, LIHTC, SAIL, and HOME properties only:

• At least one household member will be residing in the unit who is NOT a

full-time student.

Must List all such household members on the application: (Part-time

students must include verification from school documenting this

status)

• Applicants are full-time students, married AND file a joint tax return

APPLICANT MUST PROVIDE: A copy of marriage license.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 26

LIHTC / MMRB / SAIL properties only:

• Applicant is currently receiving assistance under Title IV of the Social

Security Act (i.e., AFDC or TANF)

APPLICANT MUST PROVIDE: A third-party verification of AFDC or

TANF award required

• Applicant is a full-time student that is a single parent and his/her children

are also full-time students and are not dependents on another individual’s

tax return other than a parent of such children.

APPLICANT MUST PROVIDE: A signed copy of most recent tax

return

• Applicant is a full-time student that is enrolled in the Job Training

Partnership Act (JTPA) or under similar Federal, State, or local laws.

APPLICANT MUST PROVIDE: A verification of enrollment &

mission statement of the program if not JTPA

• Applicant is a full-time student who previously was under the care and

placement of a foster care program. She/he must be currently

transitioning into independent living.

APPLICANT MUST PROVIDE: Third party verification is the only

acceptable form of verification of foster care.

SAIL properties only:

• Applicant is full-time student participating in an educational or training

program approved by the state (i.e. Soldiers for Scholars)

APPLICANT MUST PROVIDE: A verification of enrollment &

mission statement of the program

NOTE 2.10.1: Remember, if you have more than one program on your

property, you should always use the most restrictive guidelines.

2.11 DEMOGRAPHIC REQUIREMENTS

Demographic requirements (a.k.a. Special Set Aside) are the occupancy

requirements, or restrictions to serve commercial fishing worker, the elderly,

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 27

farmworkers, homeless, and other communities. Set-aside housing for these

groups might have been promised by the developer in order to serve the needs

of these demographic. Regulatory Agreements describes the requirements

when applicable to the property.

2.12 DEMOGRAPHIC DEFINITIONS

Elderly Household In order to be considered an elderly household,

in an 80/20 set-aside property, at least one of

the occupants must be 55 years or older.

Pursuant to the Federal Fair Housing Act, when

the property has an 80/20 set-aside, no more

than 20% of the units can be rented to families,

and at no time, less than 80% of the units must

be rented to the elderly. Other than in a

federally funded property, occupants under the

age of 18 are not required to be allowed.

In order to be considered an elderly household

in a property which has 100% of units set-aside

for the elderly, all household members must be

62 years or older. Other than in a federally

funded property, occupants under the age of 18

are not required to be allowed to live there.

Homeless An individual or family who lacks a fixed,

regular, and adequate nighttime residence or

an individual or family who has a primary

nighttime residence that is:

1. A supervised publicly or privately

operated shelter designed to

provide temporary living

accommodations, including welfare

hotels, congregate shelters, and

transitional housing; or

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 28

2. An institution that provides a

temporary residence for individuals

intended to be institutionalized; or

3. A public or private place not

designed for, or ordinarily used as,

a regular sleeping accommodation

for human beings.

The term does not refer to any individuals

imprisoned or otherwise detained pursuant to

state or Federal law.

Commercial Fishing Household A household of one or more persons wherein

at least one member of the household is a

Commercial Fishing Worker at time of initial

occupancy.

A laborer who is employed on a seasonal,

temporary, or permanent basis in fishing in

saltwater or freshwater and who derived at

least 50% of their income in the immediately

preceding 12 calendar months from such

employment.

The definition includes a person who has

retired as a laborer due to age, disability, or

illness.

1. In order to be considered retired

from commercial fishing work due

to age, a person shall be 50 years

of age or older and shall have been

employed for a minimum of five

(5) years as a fishing worker

immediately preceding retirement.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 29

2. In order to be considered retired

from commercial fishing work due

to disability or illness, a person

must be:

a. Medically established that

the person is unable to be

employed as a fishing

worker due to such

disability or illness.

Farmworker Household Unless specified in the Regulatory Agreement,

a household of one or more persons wherein

at least one member of the household is a

Farmworker at time of initial occupancy.

A farmworker is any laborer who is employed

on a seasonal, temporary or permanent basis

in the planting, cultivating harvesting or

processing of agricultural or aqua cultural

products, and who has derived at least 50%

of their income in the immediate preceding 12

calendar months from such employment.

The definition includes a person who has

retired as a laborer due to age, disability, or

illness.

1. In order to be considered retired

from farm work due to age, a

person shall be 50 years of age or

older and shall have been

employed for a minimum of five

(5) years as a farmworker

immediately preceding retirement.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 30

2. In order to be considered retired

from farm work due to disability or

illness, a person must be:

a. Medically established

that the person is

unable to be employed

as a Farmworker due to

such disability or illness.

"Aquaculture" means the cultivation of aquatic

organisms. "Aqua cultural producers" means

those persons engaging in the production of

aqua cultural products are certified.

"Aquaculture products" means the aquatic

organisms and any product derived from

aquatic organisms that are owned and

propagated, grown, or produced under

controlled conditions. Such products do not

include organisms harvested from the wild for

depuration, wet storage, or relay for

purification. Most State’s Statutes require

that any person engaging in aquaculture shall

be certified by the State Department of

Agriculture and Consumer Services.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 31

ANTICIPATED GROSS ANNUAL INCOME

3.0 TYPES OF INCOME THAT MUST BE INCLUDED IN THE INCOME

CALCULATION

Household income is defined as the gross income (with no adjustments or

deductions) the household anticipates it will receive in the 12-month period

following the effective date of the household’s certification of income. If the

household’s income cannot be determined based on current information

because the household reports little to zero income, or income fluctuates,

income may be determined based on actual income received or earned

within the last twelve months before the determination.

Income includes, but is not limited to, earned and unearned income from

all household members age 18 and older (adults, including foster adults),

unearned income of minor children and foster children under the age of 18,

and income from assets. Emancipated minors, persons under the age of 18

who have entered into a lease under state law, are treated as adults.

Income of Adults and Dependents

Adults

Count the annual earned and unearned income of the head, spouse or co-

head, and other adult members of the family, including foster adults. In

addition, persons under the age of 18 who have entered into a lease under

state law are treated as adults, and their annual income must also be

counted. These persons will be either the head, spouse, or co-head; they

are sometimes referred to as emancipated minors.

Chapter

3

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 32

NOTE 3.0.1: If an emancipated minor is residing with a family as a member other

than the head, spouse, or co-head, the individual would be

considered a dependent and his or her income is not counted.

Dependents

A dependent is a family member who is under 18 years of age, is disabled,

or is a full-time student. The head of the family, spouse, co-head, foster

child, or live-in aide are never dependents. Some income received on

behalf of family dependents is counted and some is not.

Earned income of minors (family members under 18) is not counted.

However, unearned annual income is counted, including that of foster

children.

Because households’ certifications are based on a “snap shot” of the

household’s income at time of initial certification, earned income of minors

that will turn 18 years old during the twelve months following the effective

date of the certification is not required to be counted.

NOTE 3.0.2: Benefits or other unearned income of minors is counted.

Employment Income

Employment income includes (but is not limited to) hourly wages, salaries,

overtime pay, tips, bonuses, and commissions before any payroll

deductions. Payments in lieu of employment income are also included; e.g.,

workers compensation, severance pay, unemployment and disability

compensation. Earned income from employment of children (including

foster children) is excluded.

Any household member that receives tip income or works in a

position/industry that would normally receive tips, must complete a

“Declaration of Tip Income.” The household member’s signature on the

declaration must be witnessed by property management representative.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 33

Maximum benefits and annualized payments should not be used unless the

source of funds is expected to continue throughout the certification period

or for an indeterminable length of time. For example, if the third party does

not indicate the length of time for which the tenant will be receiving a

certain income, then the income should be annualized. In the event that

the family cannot provide documentation that access to a specific source of

income is for a limited and determinable time period, the benefits should be

considered to be available for an indefinite time period and annualized.

EXAMPLE 3.0.0: Benefits for Indefinite Time Period

John works as a telemarketer for $9.00 an hour, 40 hours a

week. He does not work overtime, has no other source of

income, and is not planning to leave his job. His anticipated

income is computed as:

($9.00/hour) x (40 hours/week) x (52 weeks/year) = $18,720/year

EXAMPLE 3.0.1: Benefits for Definite Time Period

A teacher’s assistant works nine months annually and

receives $1,300 per month. During the summer recess, the

teacher’s assistant works for the Parks and Recreation

Department for $600 a month. The teacher’s assistant’s

anticipated income is computed as:

($1,300 x 9 months) + ($600 x 3 months) = $13,500

If information is available on changes in income expected to occur during

the year, use that information to determine the total anticipated income

from all know sources during the year.

EXAMPLE 3.0.2: Anticipated Changes in Income

In May 2004, an unemployed plumber applies for LIHTC

housing. At that time, the plumber is receiving

unemployment benefits of $250.00 per month and will

qualify for benefits for 4 more months. Documentation that

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 34

such is the case is available. Beginning in October, the

plumber will be employed at $1,000 per month. The

plumber’s anticipated income is computed for the period

from May to September 2004 plus the income for October

2004 through May 2005.

($250.00 x 5 months) + ($1,000 x 7 months) = $8,250

Property staff are expected to make reasonable judgments regarding the

most reliable method for estimating the income a household will receive

during the year. If the tenant’s income cannot be determined using current

information, the property staff may include actual income received or

earned within the 12-month period before the determination of annual

income.

EXAMPLE 3.0.3: Sporadic Employment

Justine is disabled and not always able to work full-time. She

has income from disability insurance and a family trust, and

also works as a typist with a temporary agency when she is

well. Last year she worked nearly six months, but at the time

she applies for an LIHTC apartment, she has more medical

problems and does not know when or how much she will be

able to work.

Because Justine is not working at the time of the certification

and actual income from her sporadic employment as a typist

cannot be reasonably determined, the income earned during

the six-month period in the prior year should be included in

the income certification.

Management staff must make a reasonable judgment. The

prior year’s income should not be used to estimate Justine’s

future income if she can provide sufficient documentation

that her earning capabilities have changed; e.g., her contract

with the temporary agency has been terminated.

Military Income

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 35

Military employment may include (but is not limited to) base and longevity

pay, proficiency pay, sea and foreign duty pay, hazardous duty pay,

subsistence and clothing allowances. All these are includable in income.

Hostile fire pay, however, is excluded from income. Note: a temporarily

absent individual on active military duty must be removed from the family

and his or her income must not be included in the computation of

household income, unless (1) that person is the head of the family, spouse,

or co-head or (2), the spouse or a dependent of the person on active

military duty resides in the unit.

Military Basic Housing Allowance

Military basic housing allowances are also included in income.

Student Income

The treatment of a student’s income is dependent on the age of the

student, the type of income, and the status of the student within the

household. It doesn’t matter whether the student is living with the

household or is away at school.

1. If the full-time student is 18 years of age or older and is the head of

the family, spouse or co-head, all income is included.

2. If the full-time student is 18 years of age or older and a dependent,

only the lesser of actual earned income or $480 is included, along

with unearned income and income from assets. Documentation

that the full-time student is a dependent of a household member

and verification of full-time student status, must be placed in the

file. When such documentation is not available, we must count all

earned incomes.

3. If the full-time student is a minor (under the age of 18), then only

unearned income and income from assets is included. No income

from employment is counted.

The treatment of educational scholarships and grants is discussed later

in this chapter.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 36

NOTE 3.0.3: The income of full-time students 18 years of age or older who are

members of the household but away at school is counted the same as

the income for other full-time students. The income of minors who are

members of the household but away at school is counted the same as

the income for other minors.

Foster Care Payments

Payment received by the family for the care of foster children or foster adults is

not counted. This rule applies only to payments made through the official

foster care relationships with local welfare agencies.

Adoption Assistance Payment

Adoption assistance payments in excess of $480 per child per year are not

counted.

Income of Temporarily Absent Family Members

You must count all income of family members approved to reside in the

unit, even if some members are temporarily absent, unless the absent

individual is on active military duty.

A temporarily absent individual on active military duty must be removed

from the family, and his or her income must not be counted unless that

person is the head of the family, spouse, or co-head. However, if the

spouse or a dependent of the person on active military duty resides in the

unit, that person’s income must be counted in full, even if the military

member is not the head, or spouse of the head of the family. The income

of the head, spouse, or co-head will be counted even if that person is

temporarily absent for active military duty.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 37

Examples – Income of Temporarily Absent Family Members

• John Chouse works as an accountant. However, he suffers from a disability that

periodically requires lengthy stays at a rehabilitation center. When he is confined to

the rehabilitation center, he receives disability payments equaling 80% of his usual

income.

During the time he is not in the unit, he will continue to be considered a family

member. Even though he is not currently in the unit, his total disability income will

be counted as part of the family’s annual income. Properties with Section 8 are

required to conduct an interim recertification.

• Mirna Martinez accepts temporary employment in another location and needs a

portion of her income to cover living expenses in the temporary/new location. The

full amount of the income must be included in annual income.

• Charlotte Paul is on active military duty. Her permanent residence is her parents'

assisted unit where her husband and children live. Charlotte is not currently exposed

to hostile fire. Therefore, because her spouse and children are in the assisted unit,

her military pay must be included in annual income. (If her dependents or spouse

were not in the unit, she would not be considered a family member and her income

would not be included in annual income.)

Income of Permanently Confined Family Members

An individual permanently confined to a nursing home or hospital may not

be named as family head, spouse, or co-head but may continue to count as

a family member at the family’s discretion. The family’s decision on

whether or not to include the permanently confined family member as a

family member determines if that person’s income will be counted.

Include If the permanently confined individual is counted as a

family member, his/her income is counted.

Exclude If the permanently confined individual is excluded as a

family member the income is not counted.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 38

If the family elects to include the permanently confined member, the

individual is listed on the TIC as an adult who is not the head, spouse, or

co-head, even when the permanently confined family member is married to

the person who is or will become the head of the family.

Educational Scholarships or Grants

All forms of student financial assistance (grants, scholarships, educational

entitlements, work study programs, and financial aid packages) are

excluded from annual income but must be included when the household

receives Section 8 assistance. This is true whether the assistance is paid

to the student or directly to the educational institution. This is also true if

the student is part time or full time.

For students receiving Section 8 assistance, all financial assistance a

student receives (1) under the Higher Education Act of 1965, (2) from

private sources, or (3) from an institution of higher education that is in

excess of amounts received for tuition is included in annual income except if

the student is over the age of 23 with dependent children or the student is

living with his or her parents who are receiving Section 8 assistance. See

sections 2.6 and 5.8 for further information.

Alimony or Child Support

Alimony or child support amounts awarded by the court are counted, unless

the applicant certifies that payments are not being made and he or she

provides documentation of having taken all reasonable legal actions to

collect amounts due, including filing with the appropriate courts or agencies

responsible for enforcing payment and provides a current payment history

showing no payments received. See Note 4.3.2 for further guidance in

regard to child support.

Regular Cash Contributions and Gifts

Any regular contributions and gifts from persons not living in the unit must

be counted as income. These sources may include rent and utility

payments paid on behalf of the family and other cash or noncash

contributions provided on a regular basis.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 39

Examples – Regular Cash Contributions

• The father of a young single parent pays her monthly

utility bills. On average he provides $100 each month.

The $100 per month must be included in the family’s

annual income.

• The daughter of an elderly tenant pays her mother’s

$175 share of rent each month. The $175 value must

be included in the tenant’s annual income.

NOTE 3.0.4: Groceries and/or contributions paid directly to the childcare provider

by persons not living in the unit are excluded from annual income.

NOTE 3.0.5: Temporary, nonrecurring, or sporadic income (including gifts) is not

counted.

Temporary, Nonrecurring, or Sporadic Income

Irregular, nonrecurring monetary gifts, or contribution to resident are not

included in income.

Income from a Business

When calculating annual income, you must include the net income from

the operation of a business or profession, including self-employment

income. Net income is the gross income less business expenses, interest

on loans, and depreciation computed on a straight-line basis. If the net

income from a business is negative, it must be counted as zero income. A

negative amount must not be used to offset other family income.

NOTE 3.0.6: In addition to net income, you must count any salaries or other

amounts distributed to family members from the business, and cash

or assets withdrawn by family members, except when the

withdrawal is a reimbursement of cash or assets invested in the

business.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 40

NOTE 3.0.7: When calculating net income, you must not deduct principal

payments on loans, interest on loans for business expansion or

capital improvements, other expenses for business expansion, or

outlays for capital improvements.

NOTE 3.0.8: A low-income tenant may use a portion of a low-income unit

exclusively and on a regular basis as a principle place of business,

and claim the associated expenses as tax deductions, as long as the

unit is the tenant’s primary residence. If the tenant is providing

daycare services, the tenant must have applied for (and not have

been rejected), be granted (and still have in effect), or be exempt

from having a license, certification, registration, or approval as a

daycare facility or home under state law.

Periodic Social Security Payments

Count the gross amount, before deductions for Medicare, etc., of periodic

Social Security payments. Include payments received by adults on behalf of

individuals under the age of 18 or by individuals under the age of 18 for

their own support.

Adjustments for Prior Overpayment of Benefits

If an agency is reducing a family's benefits to adjust for a prior

overpayment (e.g., social security, SSI, TANF, or unemployment benefits),

count the amount that is actually provided after the adjustment.

© 2 0 1 5 P R E F E R R E D C O M P L I A N C E S O L U T I O N S , L L C . A L L R I G H T S R E S E R V E D

Copyrighted Material: Do Not Copy 41

Example – Adjustment for Prior Overpayment of Benefits

Lee Park’s social security payment of $250 per month is being

reduced by $25 per month for a period of six months to make up

for a prior overpayment. Count his social security income as

$225 per month for the next six months and as $250 per month

for the remaining six months.

Periodic Payments from Long-Term Care Insurance, Pensions,

Annuities, and Disability or Death Benefits

The full amount of periodic payments from annuities, insurance policies,