Embed Size (px)

Citation preview

AFRICAN DEVELOPMENT BANK

Reference No.: Language : English Distribution: Original : French Financial Sector Development Support Programme Country : Kingdom of Morocco APPRAISAL REPORT October 2009 Appraisal

Team E

Team Leader Team Members : Sector Director : Country Director: Division Manager:

Mr. E. DIARRA, Principal Economist OSGE Mr. A. BA, Principal Economist ORNB W. RAIS, Financial Analyst MAFO and Consultants (Macro-Economist and Financial Sector Specialists) Mr. G. NEGATU, Director, OSGE Mr. I. LOBE NDOUMBE, Director ORNB Mrs. M. KANGA, Division Manager, OSGE.2

Peer Reviewers E

I. KOUSSOUBE, Lead Economist, ORWB A. BENBARKA, Principal Investment Officer OPSM.2 H.A.KOUASSI, Principal Economist, OSGE.2 L. PICARD Principal Investment Officer OPSM.4

Table of Contents Page LIST OF TABLES-LIST OF BOXES-LIST OF FIGURES, LIST OF ANNEXES, (i-viii) LIST OF TECHNICAL ANNEXES, FISCAL YEAR-CURRENCY EQUIVALENTS, ACRONYMS AND ABBREVIATIONS, LOAN INFORMATION, SUMMARY OF THE PROGRAMME, PROGRAMME MATRIX I – THE PROPOSAL 1 II – COUNTRY AND PROGRAMME CONTEXT 1

2.1 Governmental Development Strategy and Medium-Term Reform Priorities 1 2.2 Recent Economic Developments, Outlook and Constraints 2 2.3 Status of Bank Portfolio 6

III – JUSTIFICATION, KEY DESIGN AND SUSTAINABILITY ISSUES 6

3.1 Linkage with CSP, Analytical Works used in preparing the Programme and Prerequisites 6 3.2 Collaboration and Coordination with other Donors 7 3.3 Results and Lessons from Similar Previous Operations 7 3.4 Relations with Other Bank Operations 8 3.5 Comparative Advantages of the Bank 8 3.6 Application of Good Practice Principles as regards Conditionality 8

IV – PROGRAMME PROPOSAL 8

4.1 Programme Objectives 8 4.2 Programme Pillars and Components and Expected Outcomes 9 4.3 Financing Requirements and Arrangements 17 4.4 Programme Beneficiaries 17 4.5 Impact on Gender 18 4.6 Environmental Impact 18 4.7 Impact on Business Environment 18

V – IMPLEMENTATION, MONITORING AND EVALUATION 18

5.1 Implementation Arrangements 18 5.2 Monitoring and Evaluation Arrangements 18

VI – LEGAL DOCUMENTS AND LEGAL AUTHORITY 19

6.1 Legal Documents 19 6.2 Conditions Precedent to Bank Group Intervention 19 6.3 Compliance with Bank Group Policies 20

VII – RISK MANAGEMENT 20 VIII – RECOMMENDATION 20 ____________________________________________________________________________________ This report has been prepared by Mr. E. DIARRA, Principal Economist OSGE.2, following joint missions with the World Bank to Rabat in June and September 2009. It also includes inputs from five Consultants, comprising a Macro-Economist and four Financial Sector Specialists, as well as discussions with World Bank Economists. All questions should be referred to Mr. G. Negatu, Director, OSGE (Extension 2077) and Mrs. M. Kanga, Division Manager, OSGE.2 (Extension 2251).

i

List of Tables

List of Boxes

Box 1 : Impact of the Global Financial Crisis and Mitigation Measures taken by the Government Box 2 : Measures precedent to the presentation of PADESFI to the Boards of Directors

List of Annexes

List of Technical Annexes

Fiscal Year January- December

Currency Equivalents

(In October 2009)

UA 1 = Moroccan Dirhams (DHM) 12.41

UA 1 = Euro (EUR) 1.08 UA 1 = US Dollar (USD) 1.58

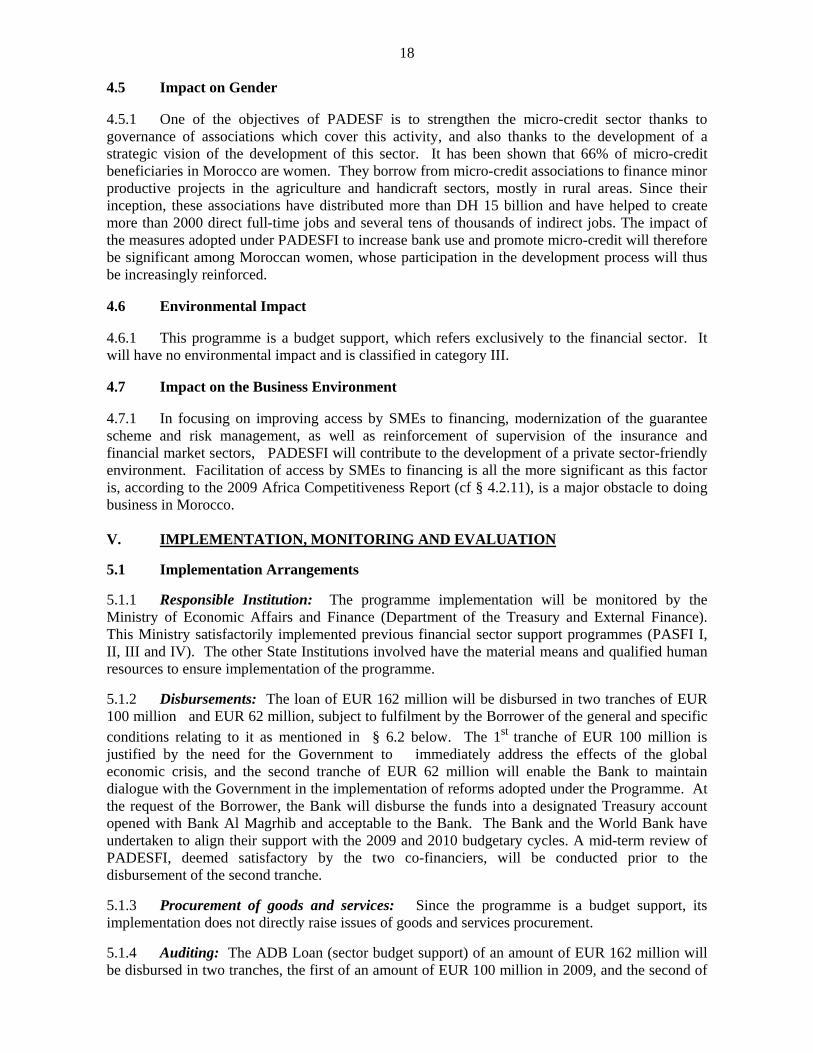

Table 1 Budget Balance and Financing Requirements

Annex 1 Financial Sector Development Policy Letter Annex 2 Matrix of Programme Measures Annex 3 Notes on Relations with IMF Annex 4 Trend of Key Macro-economic and Financial Indicators Annex 5 Conditions precedent to budget support

Annex 1 Presentation of Morocco’s Financial Sector Annex 2 List of Analytical Works Annex 3 Technical Note on Extension of Banking Services in Morocco Annex 4 Microcredit Sector in Morocco Annex 5 National Guarantee System in Morocco Annex 6 Public-Private Investment Fund Establishment Project (FPPI) Annex 7 Presentation of the Securities Ethics Board (CDVM) Annex 8 Insurance and Reinsurance in Morocco Annex 9 Presentation of the Financial Information Processing Unit Annex 10 Note on the Futures Market Annex 11 Presentation of Maroclear, the Central Custodian Annex 12 Presentation of the Casablanca Stock Exchange

ii

Acronyms and Abbreviations

ADB African Development Bank AMC Micro-Credit Association BAM Bank Al Maghrib (Central Bank of Morocco) BCP Banque Centrale Populaire BNDE National Bank for Economic Development CIF Cost, Insurance and Freight CAM Crédit Agricole du Maroc CDG Deposit and Management Fund CDVM Securities Ethics Board CEC Credit Institutions Committee CIH Housing and Hotel Credit Fund CIM Interbank Credit Card Centre CNCA National Agricultural Credit Fund DAPS Department of Insurance and Social Security DH Dirham EU European Union FDI Foreign Direct Investments GDP Gross Domestic Product GFCF Gross Fixed Capital Formation IGF General Inspectorate of Finance IMF International Monetary Fund IVT Treasury Bond Intermediary MAROCLEAR Central Custodian MF Mutual Fund PASFI Financial Sector Support Programme PFI Public Financial Institutions SBVC Casablanca Stock Exchange Company SGB Stock Exchange Management Company SICAV Open-end Investment Company SME Small and Medium-Sized Enterprises UA Unit of Account VAT Value Added Tax VC Venture Capital VSE Very Small Enterprise

iii

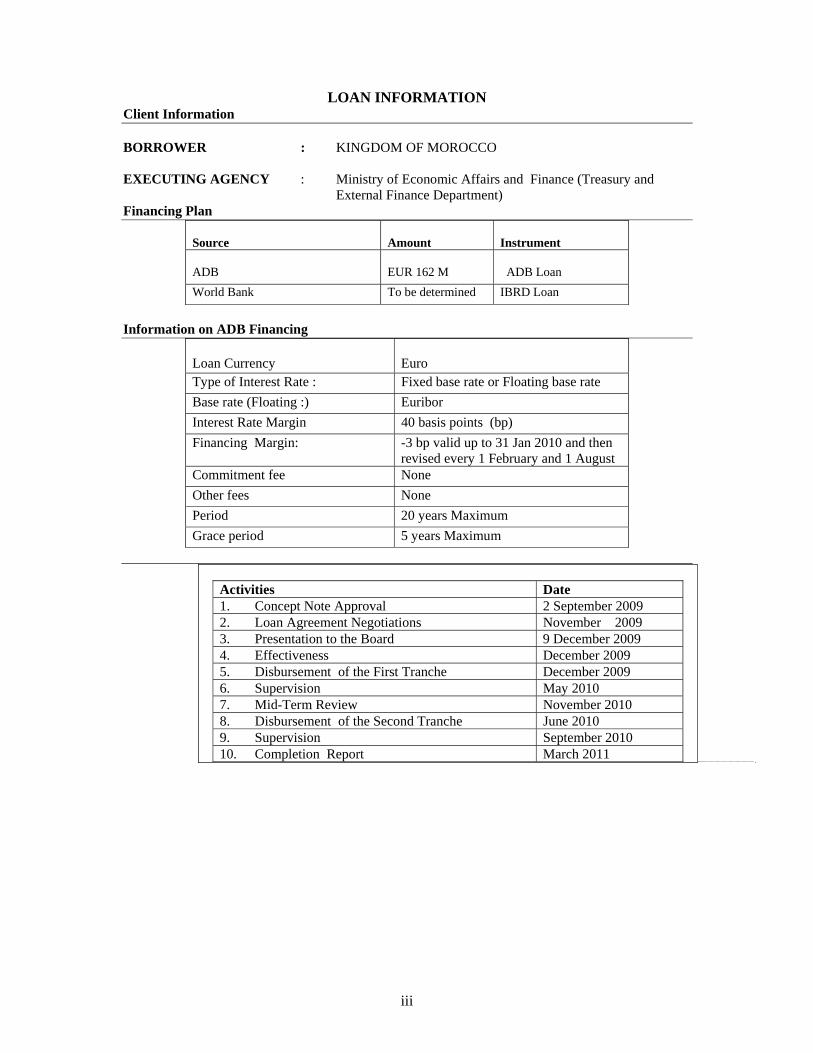

LOAN INFORMATION Client Information BORROWER : KINGDOM OF MOROCCO EXECUTING AGENCY : Ministry of Economic Affairs and Finance (Treasury and

External Finance Department) Financing Plan

Source

Amount

Instrument

ADB

EUR 162 M

ADB Loan

World Bank To be determined IBRD Loan

Information on ADB Financing

Loan Currency

Euro

Type of Interest Rate : Fixed base rate or Floating base rate Base rate (Floating :) Euribor Interest Rate Margin 40 basis points (bp) Financing Margin: -3 bp valid up to 31 Jan 2010 and then

revised every 1 February and 1 August Commitment fee None Other fees None Period 20 years Maximum Grace period 5 years Maximum

Activities Date 1. Concept Note Approval 2 September 2009 2. Loan Agreement Negotiations November 2009 3. Presentation to the Board 9 December 2009 4. Effectiveness December 2009 5. Disbursement of the First Tranche December 2009 6. Supervision May 2010 7. Mid-Term Review November 2010 8. Disbursement of the Second Tranche June 2010 9. Supervision September 2010 10. Completion Report March 2011

iv

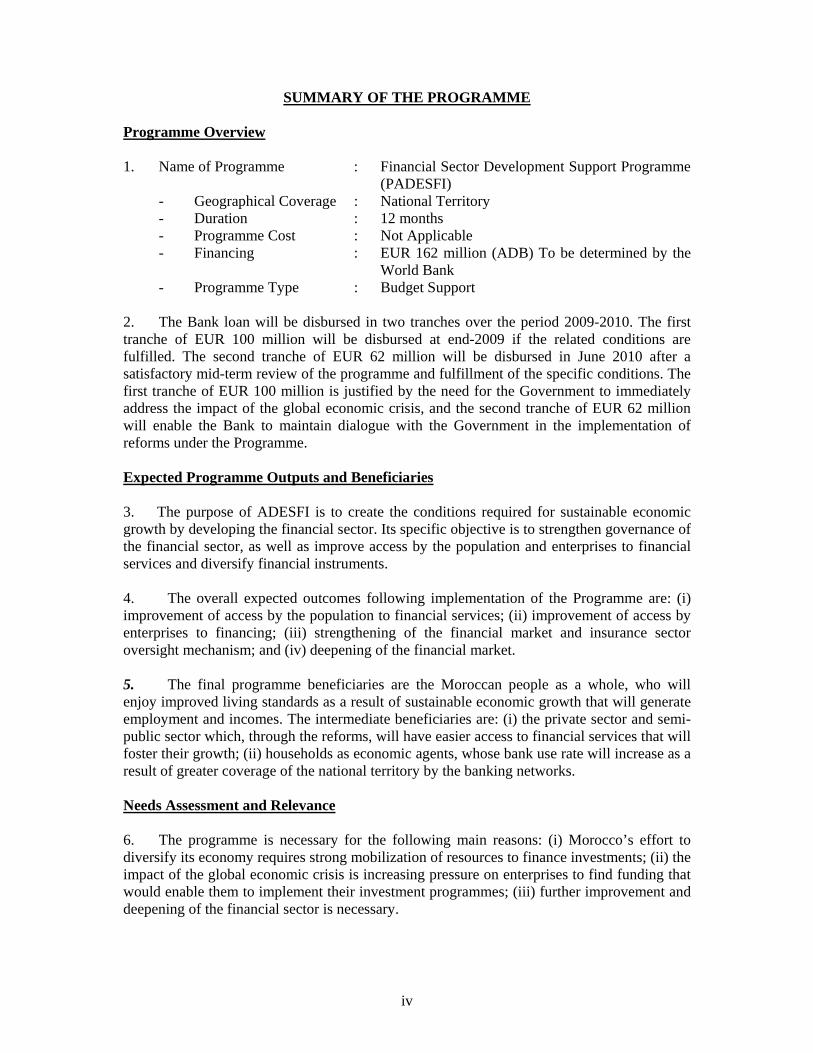

SUMMARY OF THE PROGRAMME Programme Overview 1. Name of Programme : Financial Sector Development Support Programme

(PADESFI) - Geographical Coverage : National Territory - Duration : 12 months - Programme Cost : Not Applicable - Financing : EUR 162 million (ADB) To be determined by the

World Bank - Programme Type : Budget Support 2. The Bank loan will be disbursed in two tranches over the period 2009-2010. The first tranche of EUR 100 million will be disbursed at end-2009 if the related conditions are fulfilled. The second tranche of EUR 62 million will be disbursed in June 2010 after a satisfactory mid-term review of the programme and fulfillment of the specific conditions. The first tranche of EUR 100 million is justified by the need for the Government to immediately address the impact of the global economic crisis, and the second tranche of EUR 62 million will enable the Bank to maintain dialogue with the Government in the implementation of reforms under the Programme. Expected Programme Outputs and Beneficiaries 3. The purpose of ADESFI is to create the conditions required for sustainable economic growth by developing the financial sector. Its specific objective is to strengthen governance of the financial sector, as well as improve access by the population and enterprises to financial services and diversify financial instruments. 4. The overall expected outcomes following implementation of the Programme are: (i) improvement of access by the population to financial services; (ii) improvement of access by enterprises to financing; (iii) strengthening of the financial market and insurance sector oversight mechanism; and (iv) deepening of the financial market. 5. The final programme beneficiaries are the Moroccan people as a whole, who will enjoy improved living standards as a result of sustainable economic growth that will generate employment and incomes. The intermediate beneficiaries are: (i) the private sector and semi-public sector which, through the reforms, will have easier access to financial services that will foster their growth; (ii) households as economic agents, whose bank use rate will increase as a result of greater coverage of the national territory by the banking networks. Needs Assessment and Relevance 6. The programme is necessary for the following main reasons: (i) Morocco’s effort to diversify its economy requires strong mobilization of resources to finance investments; (ii) the impact of the global economic crisis is increasing pressure on enterprises to find funding that would enable them to implement their investment programmes; (iii) further improvement and deepening of the financial sector is necessary.

v

7. The programme addresses the challenges arising from the recent global economic crisis, which the Government intends to meet, as soon as possible, with the coordinated support of the Bank and the World Bank, so as to consolidate and expand the achievements of the previous four financial sector adjustment programmes (PASFI I to PASFI IV). 8. The programme adopted is relevant: The main conditions of success of the programme have been fulfilled: proper ownership of the programme by the country; close coordination and risk sharing with the co-financier ; fulfillment of the general and technical prerequisites for this type of programme ; compliance with good practices in terms of conditionalities including the implementation of measures precedent to submission of the programme to the Board of Directors ; and design of a results-based monitoring and evaluation mechanism. The area of intervention of PADESFI, namely the financial sector, is relevant to the priorities of the Government’s Programme as reflected in the Development Policy Letter, and to those of the CSP 2007 – 2011 of Morocco. Bank’s Value Added 9. With about ten years of experience in financial sector reforms in Morocco following the series of four financial sector adjustment programmes, the Bank has drawn relevant lessons which have been shared with the co-financier and used in the formulation of this programme. During preparation and appraisal missions, the Bank helped to improve the original programme design by proposing that the Government should add other reform areas in risk coverage by insurance (natural disasters) and deepening of the financial market. Institution Building and Knowledge Development 10. PADESFI will contribute to institution building of the public administration and private sector, including associations. The analytical works, as well as the various draft texts examined for the formulation of the programme, contribute to knowledge development. The same applies to the sharing of experience acquired in other countries.

vi

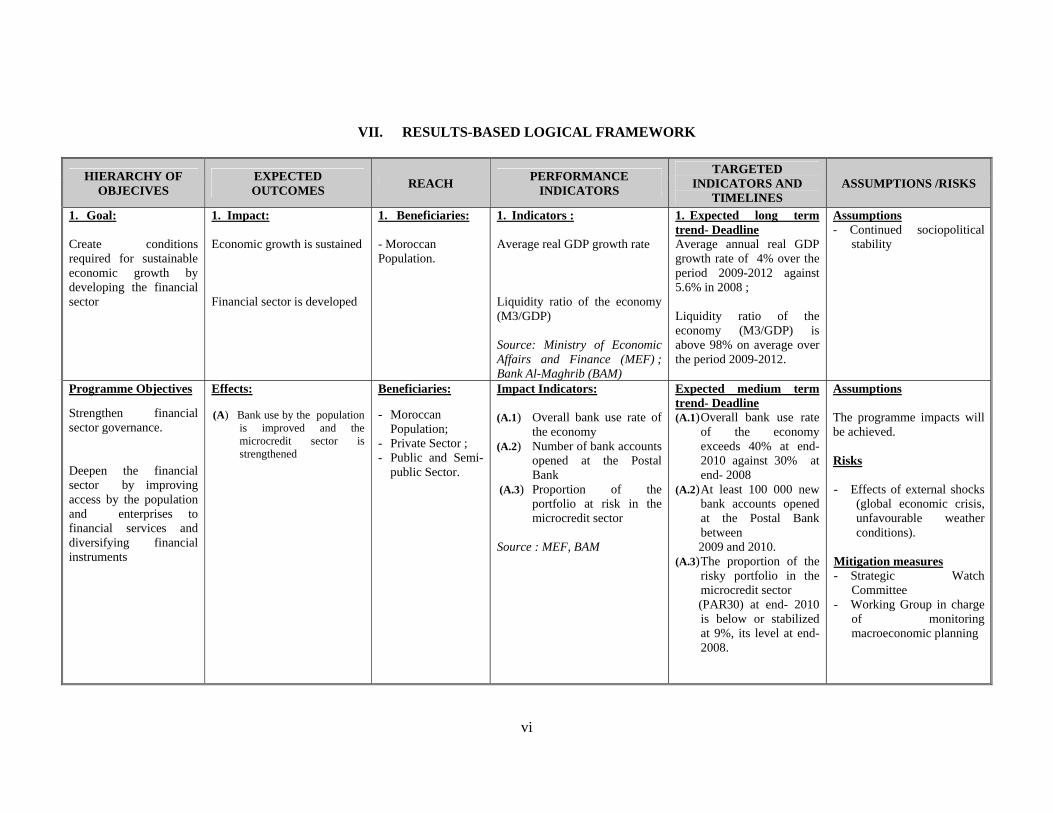

VII. RESULTS-BASED LOGICAL FRAMEWORK

HIERARCHY OF OBJECIVES

EXPECTED OUTCOMES REACH PERFORMANCE

INDICATORS

TARGETED INDICATORS AND

TIMELINES ASSUMPTIONS /RISKS

1. Goal: Create conditions required for sustainable economic growth by developing the financial sector

1. Impact: Economic growth is sustained Financial sector is developed

1. Beneficiaries: - Moroccan Population.

1. Indicators : Average real GDP growth rate Liquidity ratio of the economy (M3/GDP) Source: Ministry of Economic Affairs and Finance (MEF) ; Bank Al-Maghrib (BAM)

1. Expected long term trend- Deadline Average annual real GDP growth rate of 4% over the period 2009-2012 against 5.6% in 2008 ; Liquidity ratio of the economy (M3/GDP) is above 98% on average over the period 2009-2012.

Assumptions - Continued sociopolitical

stability

Programme Objectives Strengthen financial sector governance. Deepen the financial sector by improving access by the population and enterprises to financial services and diversifying financial instruments

Effects: (A) Bank use by the population

is improved and the microcredit sector is strengthened

Beneficiaries: - Moroccan Population; - Private Sector ; - Public and Semi-

public Sector.

Impact Indicators: (A.1) Overall bank use rate of

the economy (A.2) Number of bank accounts

opened at the Postal Bank

(A.3) Proportion of the portfolio at risk in the microcredit sector

Source : MEF, BAM

Expected medium term trend- Deadline (A.1) Overall bank use rate

of the economy exceeds 40% at end- 2010 against 30% at end- 2008

(A.2) At least 100 000 new bank accounts opened at the Postal Bank between

2009 and 2010. (A.3) The proportion of the

risky portfolio in the microcredit sector

(PAR30) at end- 2010 is below or stabilized at 9%, its level at end- 2008.

Assumptions The programme impacts will be achieved. Risks - Effects of external shocks

(global economic crisis, unfavourable weather conditions).

Mitigation measures - Strategic Watch

Committee - Working Group in charge

of monitoring macroeconomic planning

vii

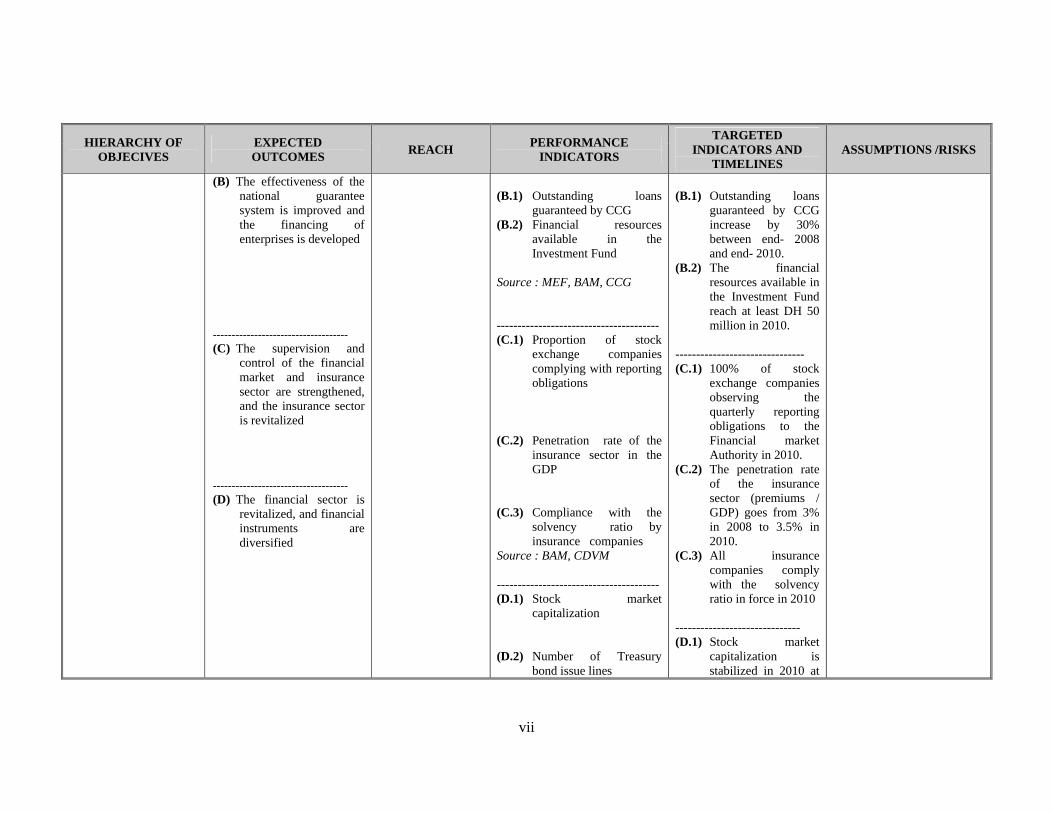

HIERARCHY OF OBJECIVES

EXPECTED OUTCOMES REACH PERFORMANCE

INDICATORS

TARGETED INDICATORS AND

TIMELINES ASSUMPTIONS /RISKS

(B) The effectiveness of the national guarantee system is improved and the financing of enterprises is developed

------------------------------------ (C) The supervision and

control of the financial market and insurance sector are strengthened, and the insurance sector is revitalized

------------------------------------ (D) The financial sector is

revitalized, and financial instruments are diversified

(B.1) Outstanding loans

guaranteed by CCG (B.2) Financial resources

available in the Investment Fund

Source : MEF, BAM, CCG --------------------------------------- (C.1) Proportion of stock

exchange companies complying with reporting obligations

(C.2) Penetration rate of the

insurance sector in the GDP

(C.3) Compliance with the

solvency ratio by insurance companies

Source : BAM, CDVM --------------------------------------- (D.1) Stock market

capitalization (D.2) Number of Treasury

bond issue lines

(B.1) Outstanding loans

guaranteed by CCG increase by 30% between end- 2008 and end- 2010.

(B.2) The financial resources available in the Investment Fund reach at least DH 50 million in 2010.

------------------------------- (C.1) 100% of stock

exchange companies observing the quarterly reporting obligations to the Financial market Authority in 2010.

(C.2) The penetration rate of the insurance sector (premiums / GDP) goes from 3% in 2008 to 3.5% in 2010.

(C.3) All insurance companies comply with the solvency ratio in force in 2010

------------------------------ (D.1) Stock market

capitalization is stabilized in 2010 at

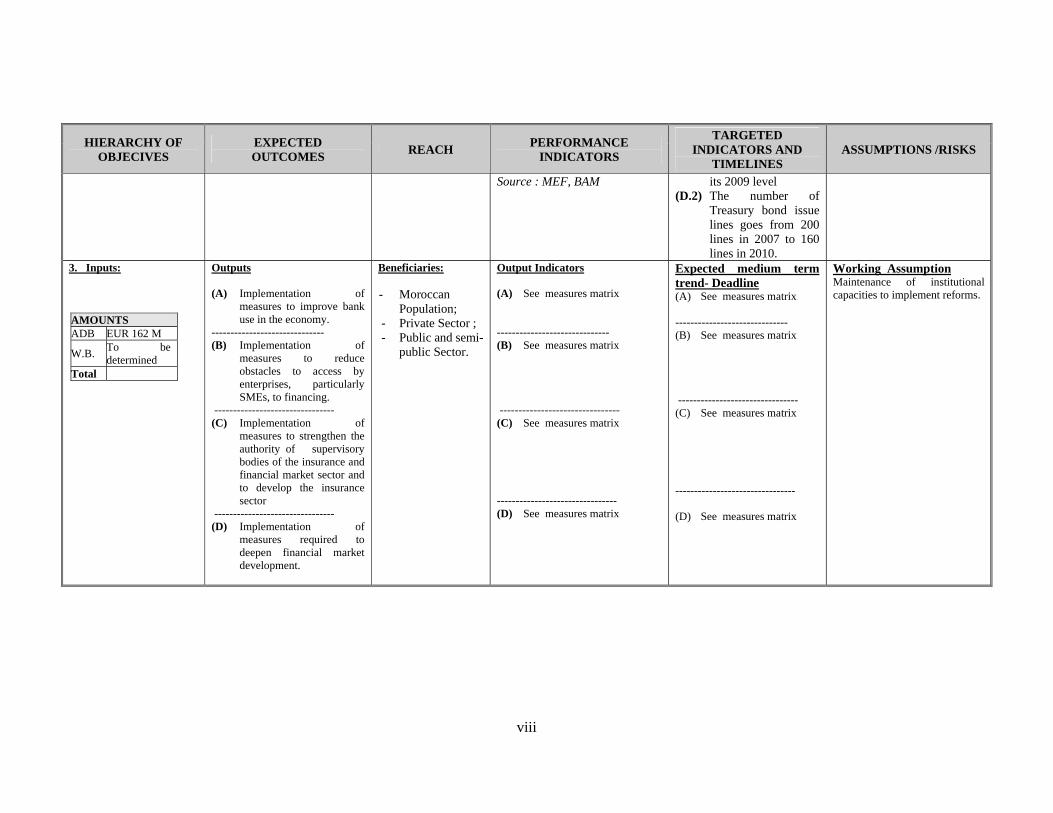

viii

HIERARCHY OF OBJECIVES

EXPECTED OUTCOMES REACH PERFORMANCE

INDICATORS

TARGETED INDICATORS AND

TIMELINES ASSUMPTIONS /RISKS

Source : MEF, BAM its 2009 level (D.2) The number of

Treasury bond issue lines goes from 200 lines in 2007 to 160 lines in 2010.

3. Inputs: AMOUNTS ADB EUR 162 M

W.B. To be determined

Total

Outputs (A) Implementation of

measures to improve bank use in the economy.

------------------------------ (B) Implementation of

measures to reduce obstacles to access by enterprises, particularly SMEs, to financing.

-------------------------------- (C) Implementation of

measures to strengthen the authority of supervisory bodies of the insurance and financial market sector and to develop the insurance sector

-------------------------------- (D) Implementation of

measures required to deepen financial market development.

Beneficiaries: - Moroccan Population; - Private Sector ; - Public and semi-

public Sector.

Output Indicators (A) See measures matrix ------------------------------ (B) See measures matrix -------------------------------- (C) See measures matrix -------------------------------- (D) See measures matrix

Expected medium term trend- Deadline (A) See measures matrix ------------------------------ (B) See measures matrix -------------------------------- (C) See measures matrix -------------------------------- (D) See measures matrix

Working Assumption Maintenance of institutional capacities to implement reforms.

REPORT AND RECOMMENDATION OF THE MANAGEMENT OF THE AFRICAN DEVELOPMENT BANK TO THE BOARD OF DIRECTORS

CONCERNING A PROPOSAL FOR A LOAN TO THE KINGDOM OF MOROCCO FOR THE FINANCIAL SECTOR DEVELOPMENT SUPPORT PROGRAMME

I THE PROPOSAL 1.1 I submit the following report and recommendation relating to a loan of EUR 162 million to the Kingdom of Morocco to finance the Financial Sector Development Support Program (PADESFI) in Morocco. It is a sector budget support to be implemented as from December 2009 for a 12-month period ending on 31 December 2010. It is in response to a request submitted to the Bank in July 2009 by the Government, and is a continuation of the series of four financial sector adjustment programmes that have been supported by the Bank and other multilateral donors, particularly the World Bank and European Union. The programme is based on the strategic orientations of the Government’s medium-term development programme. The design of PADESFI has taken into account the principles of the Paris Declaration on aid effectiveness and those of good practices as regards conditionality. It complies with the guidelines of the Bank’s mid-term review of the 2009-2011 Country Strategy Paper, the 1st pillar of which concerns improved governance and the second pillar, enterprise development. It also seeks to achieve one of the expected outcomes of the implementation of the CSP, namely increased investments through easier access of SMEs to financing. 1.2 The preparation of the Programme in June and its appraisal in September 2009 were carried out in close collaboration with the World Bank, which is the co-financier. Its purpose is to create conditions required for sustainable economic growth by developing the financial sector, and its specific objective is to reinforce governance of the financial sector and deepen it by improving access of the population and enterprises to financial services and the diversification of financial instruments. The expected outcomes of its implementation are: (i) improved bank use among the population; (ii) strengthening of the micro-credit sector; (iii) improved effectiveness of the national guarantee system; (iv) improved risk information and management in credit operations; (v) development of venture capital activity for the benefit of enterprises; (vi) strengthening of financial market supervision and control; (vii) strengthening of supervision and control, as well as revitalization, of the insurance sector; (viii) diversification of financial instruments; and (ix) revitalization of the financial market. PADESFI is a new phase in the implementation of major financial sector reforms in Morocco. II. COUNTRY AND PROGRAM CONTEXT 2.1 Government’s Development Strategy and Medium-Term Priorities 2.1.1 The Government’s medium-term economic and social programme for the period 2007-2012 aims at deepening macro-economic and sectoral reforms so as to boost economic growth and enhance the economy’s capacity to resist external shocks. It is divided into three key strategic areas of focus namely: (i) improvement of governance and the business climate; (ii) strengthening of competitiveness and regional integration by upgrading infrastructure; and (iii) human development and strengthening of the social sectors so as to improve the living conditions of the population. These general strategic orientations are supplemented by a series of detailed sectoral medium and long term strategies which aim at providing investors and various operators with the required visibility in terms of the potential and development prospects of the sectors concerned (energy, agriculture, water, industry, phosphates, tourism, handicraft, sea fishing, offshoring, domestic trade, and logistics).

2

2.1.2 The medium-term reform priorities regarding governance in particular concern enhancing public administration efficiency in terms of public resources management through its modernization, improvement of the business environment, deepening of financial sector reforms, strengthening of the independence of the judiciary and its efficiency, development and extension of decentralization, devolution, regionalization and the fight against corruption. 2.1.3 In the financial sector in particular, the Government aims to: (i) facilitate access of SMEs to sources of finance; (ii) reform the insurance system; (iii) develop venture capital; (iv) shorten the time taken by the State to pay debts owed enterprises, and (v) encourage micro-credit as well as promote the creation of small enterprises by adapting the "Moukawalati" programme to the environment and needs of the national economic fabric. PADESFI, by virtue of its objectives and components, will address these concerns of the Government. The development policy letter in Annex 1 of this Report provides further details on these priorities.

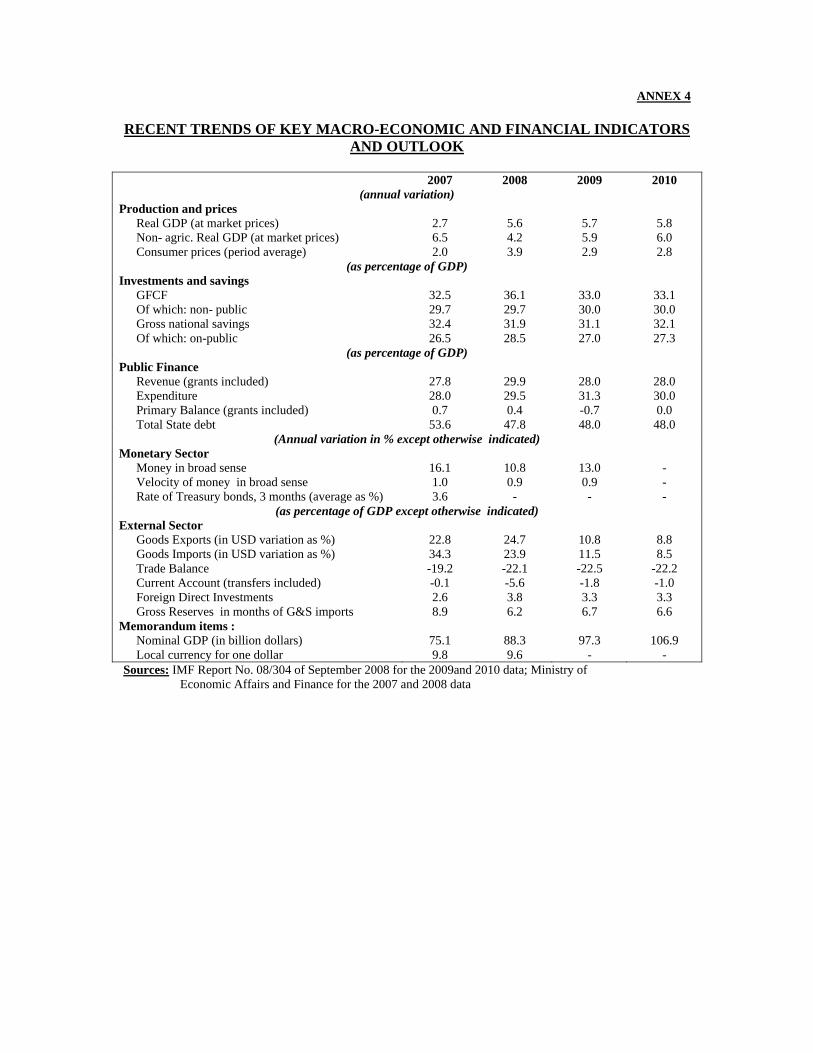

2.2 Recent Economic and Social Developments, Outlook, Constraints and Challenges Recent macro-economic and social trends 2.2.1 At the macro-economic level, Morocco recorded, up until 2008 encouraging results, marked by gradual diversification of the productive base of its economy with the emergence of new activities in the services sector. In 2008, GDP growth stood at 5.6% against 2.7% in 2007 thanks in particular to a very satisfactory crop year resulting from good rainfall. However, as from the 4th

quarter of 2008 and the 1st half of 2009, tangible signs of the effects of the global crisis appeared, particularly in the decline of activities of exporting industries (textile, phosphates, automobile and leather) following a 4% drop in foreign demand for Moroccan products. Accordingly and despite the adjustment measures taken by the Government to cope with the crisis, the growth rate expected at end-2009 should not exceed 5.3%, with 3.9% for the non-agricultural sector. Regarding the inflation rate, it reached 3.9% in 2008 against 2% in 2007 due to pressure from the prices of food and imported energy products, and also to the rise in private transport tariffs. However, a slowdown in world oil market demand leading to a drop in prices (USD 60.5 per barrel in 2009 against USD 97 in 20081) should, in 2009, reduce inflation to around 2.5%. 2.2.2 Public finance: The budgetary position, which had improved up to 2008 thanks to the increased effectiveness of the tax policy as well as measures to streamline the management of State resources as part of Public administration reforms (MTEF, lumping of credits, wage bill reduction, etc.) deteriorated in 2009 as a result of the crisis. Thus, from a surplus position (0.7% of GDP in 2007 and 0.4% of GDP in 2008) the budget in 2009 will show a deficit of around 3.5% of GDP due to a lower level of activity in the key exporting industries and the drop in domestic demand. This will result in increased resource requirements to enable the Government to pursue implementation of its public investments policy. 2.2.3 Money and credit: The monetary situation was marked by a substantial expansion of credit up to 2007 with an annual variation of 23.4% before witnessing a slight decline of 4 growth points in 2008. Considering the contraction of foreign exchange reserves in 2008, which continued into 2009, and the decline in Public Treasury debt to the banking system, the increase in the money supply was limited, from 16.1% in 2007 to 10.8% in 2008 and, probably, 8% in 2009. This helped to mitigate the risk of inflation due to monetary causes. In 2008, the inter-bank rate, which reflects fluctuations in the short-term interest rate of Banks, stood at 3.37% on average compared to its 2007 level, while interest on bank deposits was 3.80% in 2008 against 3.57% in 2006 and 2007. This situation reflects the long term resource requirements of the banking system. 1 Source : World Economic outlook, IMF, World Bank – Commodity prices data

3

2.2.4 Country’s external position: In 2008, the worsening of the trade deficit due to the high increase in imports, particularly of oil products (36.2% against 16.8% in 2007) and exports stagnation coupled with the 3.4% drop in remittances from Moroccans residing abroad and also a 5.6% fall in receipts from tourism, led to a current transactions deficit of -5.2% of GDP. This poor performance marked a disruption in the series of surplus results recorded during the previous six years. Despite net capital inflows, the overall balance of payments deficit amounted to -3.4% of GDP due to the decline in 2008 of foreign direct investments which reduced foreign exchange reserves from 9 months in 2007 to 7 months of goods and services imports in 2008. In 2009, the exchange reserves should not exceed 6.9 months of goods and services imports due to a drop in the current account transactions of the balance of payments to -6% of GDP against -5.4% of GDP in 2008. 2.2.5 Public debt: Outstanding foreign debt has reduced progressively from 46.7% of GDP ten years ago to 19.4% of GDP in 2008. However, domestic debt, which represented 34.1% in 1998, rose to 37.3% of GDP in 2008. This trend should be gradually reversed on account of the appearance, due to the crisis, of current account transactions deficits of the balance of payments; hence the need for external resources to finance the economy. 2.2.6 At the social level: Although the progress recorded in recent years is real and encouraging, much remains to be done to improve the social indicators sustainably. Indeed, the implementation of the National Human Development Initiative (INDH), launched in 2005, has produced positive results in terms of poverty reduction. The poverty rate, for instance, dropped by more than 40% between 2001 and 2008, from 15.3% to 9%. However, the social indicators remain relatively weak compared to those of countries with a comparable level of income: (i) the illiteracy rate among the population aged 10 years and above is 40% against 33.2% on average in Africa, that is approximately 12 million people, and in rural areas can exceed 60% and 75% among women.; (ii) infant mortality is 40 per thousand, while maternal mortality stands at to 227 per 100 000 live births, which rates are considered to be among the highest in the region. In terms of precariousness and social exclusion, there are still more than 933 shantytowns and more than 400 under-developed districts throughout the country.

Box 1: Impacts of the global financial crisis and mitigation measures taken

by the Government 1. Impact of the crisis: (i) 4% drop in foreign demand for Moroccan exports; (ii) 3.4% drop

in remittances from Moroccans residing abroad (9% of GDP) due to unemployment following the decline in activity of the building construction and automobile sectors in the host countries where they are employed; (iii) 5.6% contraction of tourism receipts; (iv) 28.6% drop in foreign direct investments (FDI); (v) worsening of unemployment at 9.6% in 2009 against 9.1% at the same period in 2008, which reduces the domestic demand of households.

2. Crisis mitigation measures taken by the Government: (i) In February 2009, establishment

of a public-private Strategic Watch Committee, aimed at strengthening the consultation and response mechanisms by taking appropriate measures to mitigate the effects of the crisis. It is within this framework that specific measures were taken for enterprises exposed to the collapse of foreign demand, targeting tax measures, as well as for households by subsidizing the prices of basic commodities such as sugar, flour, cooking gas, etc; (ii) the measures to support enterprises are divided into three aspects, namely : (a) the labour aspect : aimed at maintaining employment and skills through the reimbursement by the State for a period of six months renewable, of the employer contributions of the enterprises concerned; (b) commercial aspect: by providing better conditions of access to export insurance and financial assistance to assist the exporting companies in their prospecting programmes. In this case, it concerns: (a) the reduction from 3% to 1% of the trade fair and marketing

4

insurance premium; (b) increase in the percentage of cover from 50% to 80% for trade fair insurance and marketing insurance; (c) reduction of the commercial credit insurance premium to 0.3%, (d) launching of targeted communication campaigns, and financing by the State of 80% of promotion expenses within the limit of a ceiling of DH 100 000 per mission and company; (iii) financial aspect: through the putting in place of guarantee mechanisms, managed by the Central Guarantee Fund, to enable exporting companies of the sectors concerned to benefit from the advantageous conditions for financing their revolving fund requirements and soft terms granted by the banks. In concrete terms, this means: (a) granting of a guarantee within the framework of the product " Damane Exploitation" of 65% of the credit for financing the revolving fund requirement with a guarantee ceiling of DH 9 M per company, (b) granting within the framework of the " Moratorium" product of 65% to cover the deferment of the principals of medium and long term credits due in 2009 with a ceiling of DH 2 M per company. All these efforts by the Government to assist enterprises coupled with the subsidies of basic commodities have resulted in an increase in the “compensation” aspect of the State Budget whose amount represented 4.6% of GDP in 2008 against 2.3% and 2.7% of GDP respectively in 2006 and 2007.

Outlook, constraints and challenges 2.2.7 The resilience of the Moroccan economy within this context of global economic crisis and the adjustment measures taken by the authorities have helped to mitigate its impacts. However, they have proved insufficient to provide a lasting solution to the weaknesses of the economy, such as the limited budgetary sustainability, the competitiveness of the economy, and the productivity of the agricultural sector, which is still dependent on the vagaries of the weather. According to initial estimates of the authorities, the economic outlook in 2010 will be marked by a growth rate of about 3.5%, a budget deficit representing 4% of GDP despite the stability of the operating expenditures at its 2009 level, and inflation contained at 2%. 2.2.8 In this light, the Government intends to embark more strongly on the diversification of its economy and strengthening of its competitiveness. In this regard, it will in 2010 pursue and intensify the budget policy of economic recovery initiated in 2009 and marked by tax reduction to sustain the purchasing power of households and a 20.4% increase in public investments to reinforce domestic demand. Morocco will indeed have to deal with the scope of financing requirements from both the private sector and the public sector. In 2008, private sector operations showed financing requirements of approximately DHM 28 billion against a financing capacity of DHM 6.4 billion in 2007. To do so, the country will need a healthy and dynamic financial sector, ready to mobilize adequate resources (particularly long-term) to finance productive investments. Under these circumstances, the problems of financing becomes a major issue, especially in light of the recent substantial increase in private sector financing requirements and the persistent problems of guarantees constraining the access of companies to financing. Financial Sector : Current Situation and Challenges (cf Technical Annex 1) 2.2.9 Morocco’s financial sector comprises the banking sector and the non-banking financial sector, including the insurance sector, the mortgage sector, the money market and other financial services such as leasing and venture capital/investment capital. The micro-credit institutions also belong to the financial sector. The latter plays a paramount role in the financing of the productive fabric and in Morocco’s private sector promotion. In the non-banking financial sector, insurance companies and pension funds mobilized more resources (DH 31.3 billion against DH 20.3 in 2007) and they have tripled their subscriptions for the issue of bonds (DH 13.3 billion against DH 4.8 billion in 2007). Regarding the banking environment, the overall balance sheet of banks stood at 763 billion in 2008, representing 90% of GDP. Similarly, the banks have been able to improve

5

their balance sheets of outstanding credits, since the latter represent only 6% of overall outstanding claims in 2008. This has further strengthened the solidity of banks in Morocco. 2.2.10 Despite the progress achieved thus far in the Moroccan financial sector reform, there are still major challenges which must be addressed for the sector to play its role in financing the country’s development. Indeed, the banking sector is showing signs of exhaustion, particularly with (i) significant reduction (more half) of credit growth with a rate of 23% between 2007 and 2008 against 69% over period 2006-2007, (ii) an increase in deposits that has remained lower than that of credits, with a drop in sight deposits (55%) to the benefit of term deposits (31%) thus leading to a tightening of the liquidity of banks, which have increasingly been refinanced by BAM, (iii) a significant moderation (of more than one third) of the increase in bank resources of 7% in 2008 against 26% in 2007. As for the stock market, it is showing limits in its role of long-term financing of companies. Indeed, there was a deterioration in its key indicators in 2008, particularly with: (i) continued interruption of the upward trend over the last three last years with a depreciation of the MADEX index by more than 13%, (ii) the 9.3% fall in stock market capitalization against a 40.6% rise in 2007, (iii) contraction of the volume of trade on the central market of approximately 25% and (iv) the 32.1% drop in overall turnover. 2.2.11 The Financial Sector Evaluation Programme (PESF) implemented in 2008 by the World Bank and the IMF, records significant progress achieved by the financial sector in Morocco, in particular: (i) the State’s divestiture from the financial sector and modernization of some public institutions that remain active, (ii) reinforcement of banking supervision so as to align it with international standards, (iii) improvement of the financial infrastructure, particularly with the putting in place of modern systems of payments and progress in the project of creation of a credit bureau, (iv) adoption of a law to combat money laundering and financing of terrorism (cf Technical Annex 9). The report concludes that the banks in Morocco are stable, profitable, adequately capitalized, and show greater resilience to external shocks. Thanks to its solidity and its limited exposure to external financial markets, the Moroccan financial system was only slightly affected by the crisis. However, there are still challenges to be addressed in order to improve the contribution of the financial sector to economic development. This appraisal recommends in particular: (i) further reinforcement, improvement, deepening and supervision of the financial sector, (ii) better preparation of financial institutions for risk management due to major potential variations of exchange rates and interest rates. 2.2.12 In light of this appraisal, the deepening of the long-term financial market features among the major challenges facing the financial sector. It is expected that this will be addressed by introducing new products such as long-term instruments and options, the negotiation of margins, and the securitization and negotiation of the indexed bonds. However, the introduction of more sophisticated and complex products on the market requires that the reform of the legal and control framework, just as the capacities of CDVM as an institution in charge of regulating the market, need to be enhanced. PADESFI will help to address these challenges by consolidating the gains of PASFI completed in 2004 and extending its effects in a context of global economic crisis. PADESFI will in particular allow for: (i) improved governance through the reinforcement of transparency and independence of the regulatory and control authorities; (ii) deepening of the financial sector by improving the access of companies to financing. Through this financing, the Bank will also be honouring its commitment as regards supporting Member States to face the global economic crisis.

6

2.3 Status of Bank Portfolio 2.3.1 At 30 September 2009, the Bank portfolio in Morocco comprises 18 active operations for a total amount of UA 1 129.40 million. The sector distribution of the portfolio shows dominance of the infrastructure sector (energy, transport, water and sanitation) representing more than 80% of ongoing commitments and confirms the significant role of the Bank in the financing of these sectors in Morocco. With the start of activities of MAFO, the performance of the portfolio improved significantly, with the disbursement rate (excluding operations not yet effective) increasing from 37% to 53% from 2006 to 2009. This performance is all the more significant as the mean age of the portfolio reduced from 3.7 to 2.1 years. III. JUSTIFICATION, KEY DESIGN AND SUSTAINABILITY ELEMENTS 3.1 Linkages with the CSP, assessment of country readiness and underlying analytical

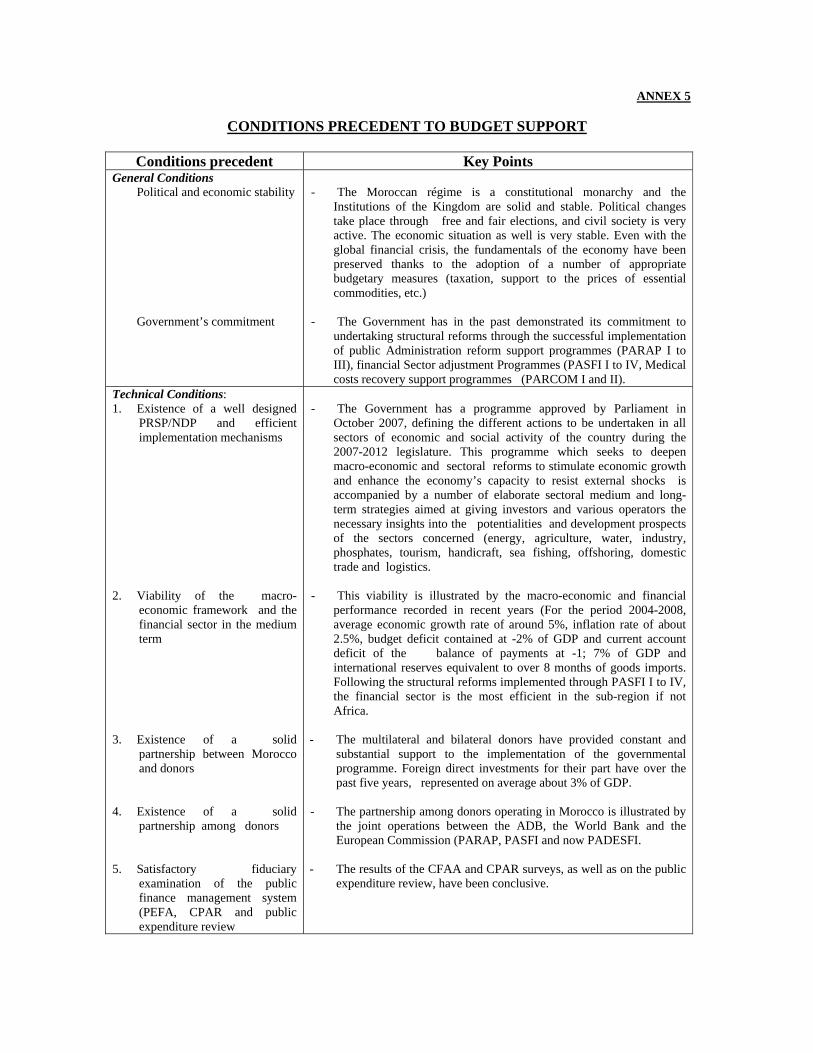

elements 3.1.1 Linkages with the CSP: PADESFI is in conformity with the guidelines of the mid-term review of the country strategy 2009-2011, which underscore reinforcement of the governance system and upgrading of economic and corporate infrastructure. By supporting the Government’s efforts in these fields, the Bank is fostering improvement of the business climate, thus contributing to the creation of an environment more conducive to the development of private sector activities and reinforcement of corporate competitiveness. 3.1.2 Conditions precedent to the implementation of budget support: Morocco had a CPIA rating of 4.2 in 2008, and it also meets the required preconditions both at the general and technical levels. Generally, the country enjoys political and economic stability and the Government’s commitment to carrying out the reforms is constantly demonstrated. At the economic level, Morocco’s performance has been remarkable over the past few years, thus reflecting ongoing efforts to improve the macroeconomic framework and implement reforms centred on the strengthening of competitiveness and diversification of the productive base of the economy. At the technical level, Morocco also satisfies the required fundamentals concerning the existence of a medium-term programme, the public finance management system and institutional capacities. 3.1.3 At the fiduciary level, the structural reforms undertaken in Morocco, particularly under various phases of the Bank-financed Public Administration Reform Support Programme (PARAP) have contributed to the improvement of budgetary control and effectiveness of public spending. The reliability of the financial management marked by a low level of risk was confirmed in 2007, following the review by the World Bank of the progress made in the implementation of the recommendations of the Country Financial Assessment and Accountability (CFAA) Report for 2007. However, the Moroccan authorities were urged to make efforts to reduce the time-frame for accounts submission and actively promote the control function. The Country Procurement Analysis Review (CPAR 2008), which is an update of the 2005 report, concluded that overall risk remains low as regards public procurement. The exercise concluded that the ongoing reforms undertaken as regards: (i) results-based budgetary control, (ii) medium-term expenditure framework (MTEF), (iii) budgetary deconcentration, (iv) expenditure control, and (v) strengthening of the procurement system, etc), in spite of their simultaneity, have been implemented at a steady pace and have reinforced the efficiency and reliability of the country’s budgetary and accounting system. Furthermore, the international ratings agency, Fitch Ratings, on 15 September 2009 confirmed the "Investment rank" granted to Morocco with a stable outlook, thus reflecting the progress made by the country at both the economic and political levels. The foreign currency debt and the local currency debt are thus rated BBB- and BBB respectively.

7

3.1.4 Institutional capacities: The Government has in previous programmes shown its capacity to mobilize development partners on programmes over which it has a thorough grasp, thus showing proof of a capacity of ownership and coordination of such programmes. For the management and implementation of investments and reform programmes, the Moroccan administration has human capacities of a satisfactory level of qualification and a well-structured administrative mechanism to carry out its public service missions in an overall satisfactory manner. The Ministry of Economic Affairs and Finance, which is in charge of managing this programme, has the high-level technical skills required to carry out the planned reforms satisfactorily. However, on account of the complexity of some of these reforms, such as the deepening of the financial market and improvement of risk management, Morocco will need external technical assistance to provide the required supplementary expertise. 3.1.6 Analytical works: The design of the programme benefited from the results of the analytical works undertaken recently by the Bank and the country itself and other external organizations and partners. These include the mid-term review of the country strategy 2009-2011, the study on the national guarantee system conducted by the Government, and the report of the Financial Sector Assessment Programme of the IMF and the World Bank in 2008 (cf §2.2.13). The detailed list of the analytical works is featured in Technical Annex 2. 3.2 Collaboration and coordination with other donors 3.2.1 Collaboration and coordination with the World Bank, the co-financier of PADESFI, are in conformity with the guidelines of the Paris Declaration on aid effectiveness (joint identification, preparation and appraisal missions and joint preparation of the reforms matrix). The programme review and supervision will be carried out jointly. Similarly, the programme design conforms to the other Paris Declaration guidelines, such as: alignment of assistance with national priorities; use of country systems, namely allocating resources directly to the national budget and designation of the Ministry of Economic Affairs and Finance (Treasury and External Finance Department) as the programme coordination agency; and improvement of the predictability of aid through the commitment of partners to supporting the medium-term programme, as well as the commitment of the Government to implementing the reforms adopted. 3.3 Results and lessons learnt from similar operations 3.3.1 The Bank has financed several budget support programmes in Morocco, including 4 financial sector support programmes (PASFI I to IV), the public administration reform support programme (phases I, II, III), the medical coverage support programme (phases I and II) and more recently the education system emergency plan support programme. The completion reports prepared for most of these programmes showed the country’s good performance in the implementation of the said programmes. 3.3.2 Lessons have been learnt from the implementation of the various Bank-financed programmes in Morocco, in particular taking into account of difficulties encountered in fulfilling the disbursement conditions concerning the approval of legal instruments. It is also important for the Government and partners in the programme to better coordinate monitoring of the implementation of the measures and conditions during the programme implementation. The design of PADESFI has taken into account these key lessons by underscoring the reduction and practicality of disbursement conditions, whose formulation was consensually agreed between the Government and the Bank and the World Bank.

8

3.4 Relations with the other Bank operations 3.4.1 The Bank has in the past financed four operations relating to Morocco’s financial sector, namely PASFI I to IV which were all aimed at implementing structural reforms to improve the sector. PADESFI is also consistent with the other ongoing operations of the Bank in Morocco, which contribute to the reinforcement of corporate competitiveness and private sector development through the upgrading of economic infrastructure and support of the Government’s structural reform programmes. Bank operations in these two domains represent more than 80% of its portfolio. Furthermore, PADESFI, whose objective is to reinforce governance in the financial sector and deepen it, constitutes an appropriate framework for creating an environment conducive to the improvement of the business climate. As such, its impact will consolidate the gains of the Bank-supported Public Administration Reform Support Programme (PARAP), which has enabled Morocco to make substantial progress in administrative, economic and financial governance. 3.5 Comparative advantages of the Bank 3.5.1 With ten years of experience in financial sector reforms in Morocco, following the series of the four financial sector adjustment programmes, the Bank has been able to draw relevant lessons which were shared with the co-financier and used for formulating this programme. During preparation and appraisal missions, the Bank contributed to improving the initial design of the programme, and proposed to the Government to add other areas of reform, namely risk coverage by insurance (natural disasters) and deepening of the financial market. This experience in the sector thus confers on the Bank a comparative advantage, which has enabled it to prepare and appraise PADESFI within a short time-frame, thus responding to the urgency expressed by the Government and thereby honouring the commitments made by the Bank to rapidly respond to its Member States confronted with the effects of the global economic crisis. 3.6 Application of good practice principles as regards conditionalities 3.6.1 Good practice principles as regards conditionalities, particularly those related to ownership, the coordinated accountability framework, adaptation of this framework to the context, the choice of disbursement conditions for results, and the predictability of financial support were taken into account in the design and formulation of PADESFI. 3.6.2 The Bank and the World Bank, which support PADESFI, had sustained consultations during the various preparation missions of the programme so as to strengthen synergy and coherence of their respective interventions. An accountability framework, namely a common measures and performance indicators matrix, has been put in place in a coordinated manner by the Government, the Bank and the World Bank in order to harmonize the disbursement conditions and the procedures for assessing the progress made under the programme. These consultation efforts are supported by the strong ownership of the programme by the country marked by the Government’s commitment to meeting the financial sector challenges. IV. THE PROPOSED PROGRAMME

4.1 Programme Goal and Objectives 4.1.1 The purpose of PADESFI is to create conditions required for sustainable economic growth through the development of the financial sector. Within the current context of a global economic crisis, the targeted average annual GDP growth rate is 4% over the period 2009-2012, and the targeted average liquidity ratio of the economy (M3/GDP) is 98% over the same period. Its specific objective is to strengthen the governance of the financial sector and deepen it by improving access of the population and enterprises to financial services, and diversifying financial instruments.

9

4.2 Programme Components, Objectives and Expected Outcomes 4.2.1 Since the early 90s, Morocco has made substantial efforts to modernize its financial sector, whose principal beneficiaries have been the Moroccan population, the private sector, and the semi-public sector. This programme falls within the framework of deepening of the reforms already undertaken for the benefit the same beneficiaries, and it has four major objectives: (i) to improve access of the population to financial services, (ii) to improve access of enterprises to financing, (iii) to reinforce the control mechanism of the financial market and insurance sector, and (iv) to deepen the financial market. COMPONENT 1 : IMPROVEMENT OF ACCESS OF THE POPULATION TO

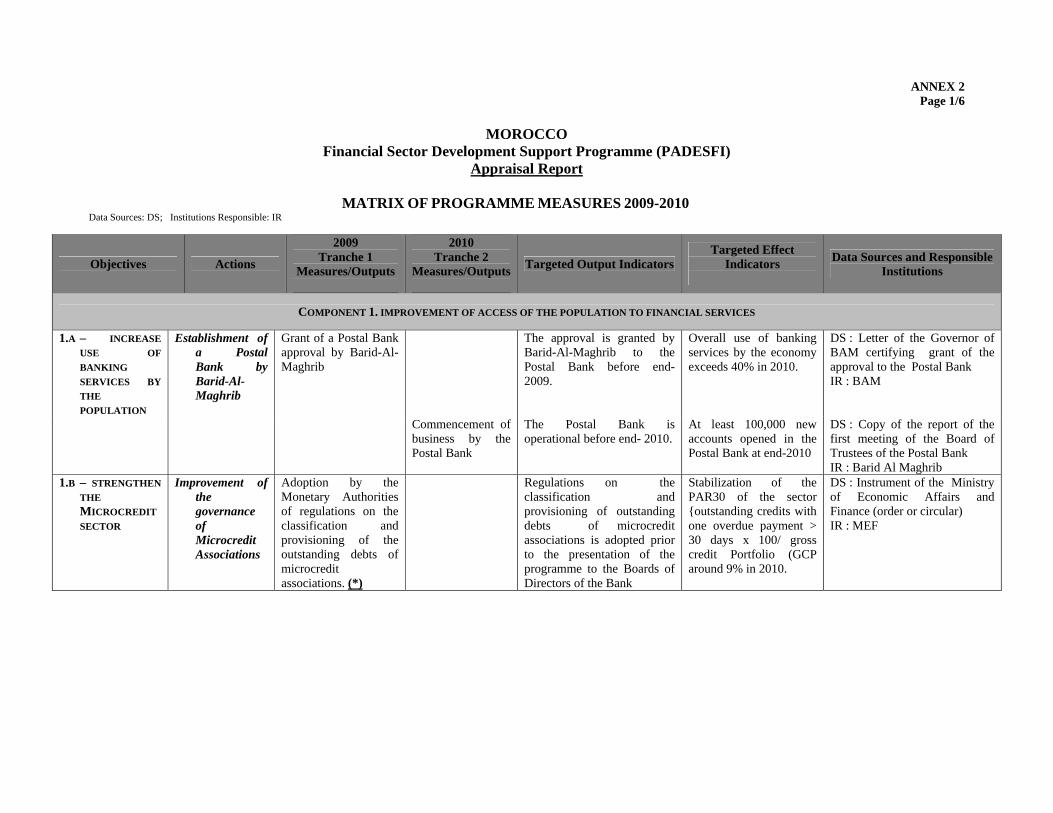

FINANCIAL SERVICES 4.2.2 As part of the fight against banking exclusion, the reforms of PADESFI aim to: (i) improve mass banking where households’ outreach financial services needs are far from being met, particularly in rural areas, and (ii) reinforce the micro-credit sector. Access of the population to financial services will be improved mainly through the professionalization of the financial services of the Post office, which will be operated through the creation of the Postal Bank. This bank will manage the postal cheques accounts held mainly by small savers with a business plan, which envisages its extension to the hinterland, particularly in rural areas. This reform, along with those aimed at micro-credit sector reinforcement, will result mainly in an increased rate of use of banking services. Sub-component 1a : Improvement of Bank use by the Population 4.2.3 Context and challenges: The bank use rate in Morocco is estimated at 30% in 2008 (cf Technical Annex 3). This rate actually conceals very significant disparities between rural areas and urban zones where it is around 60%. To offset the inadequate presence of banks in rural and peri-urban areas, Poste Maroc with its extensive network of 1200 offices and its 4 million postal cheques accounts provides an opportunity to extend access of the population to financial services on most of the territory. To play this role fully, Poste Maroc must first professionalize its financial services. 4.2.4 Recent actions: To address the challenge of professionalizing its financial services, the institutional and organizational framework of Poste Maroc has been revised through the implementation of two major actions. Initially, Poste Maroc was transformed into a limited liability company “Poste Maroc SA” whose capital is held entirely by the State. Thereafter, in its set-up, there was a clear separation between the universal mail service and the financial services. To this end, Poste Maroc was authorized by Decree No 2-08-258 of 5 June 2008 to create a banking subsidiary company known as Bank Al Barid, which will be charged with the development of the financial services provided by Poste Maroc SA. This will allow for the development of specific skills in the management of postal accounts and cheques, and avoidance of cross subsidies between potentially profitable banking activities and the universal mail service potentially in deficit. 4.2.5 Programme Measures: To promote access of the population to financial services, particularly in rural and peri- urban areas, the measures envisaged are: (i) granting of approval to the postal bank, Bank Al-Barid in 2009 by Bank-Al Maghrib and (ii) commencement of activities of this new bank during the year 2010.

10

4.2.6 Expected outcomes: The implementation of these measures should lead to the following outcomes before end- 2010 : (i) at least 100 000 new accounts opened at Bank Al-Barid, and (ii) a bank use rate of over 40% Sub-component 1b : Strengthening of the micro-credit sector 4.2.7 Context and challenges: With and outstanding credit of DHM 5.6 billion in 2008 representing 45% of the overall debts in the entire Arab world, Morocco’s micro-credit sector is fairly dynamic but also highly exposed (cf Technical Annex 4). It is marked by high concentration, given that of a dozen associations present in the sector, five hold 95% of the overall outstanding credit. Similarly, the services offered are undiversified. They are limited mainly to the granting of credits capped at DHM 50 000 for purposes of financing income-generating activities. Recent trends in the sector show a strong deterioration of the portfolio quality with an increase in the portfolio at risk (PAR 30) of 1.1% in 2007 to 9% at the end of June 2009 in a context of proliferation of cross indebtedness, debt overhang of the beneficiaries and degradation of the governance of associations. One of the major challenges currently facing this sector is thus that of improving the AMC portfolio quality. 4.2.8 Recent actions: The existing regulation was amended in 2004 to enable AMCs to broaden their range of financial services by authorizing them to finance social housing and connection to the electrical supply network and drinking water. In 2008, the Jaïda fund was launched, with a capital allocation of DH 200 million, to reinforce the financial base of AMCs. A study on the institutional transformation of the AMC was ordered by the Moroccan Government; its conclusions are expected in 2010. To reinforce the method of governance in the micro-credit sector, it was decided in 2006 that thenceforth AMCs would be subject to the control and supervision of the BAM by enshrining the principle of documentary and on– the- spot controls. Furthermore, to contain the phenomenon of crossed indebtedness, the five biggest associations agreed to share, among them, information relating to customers. Similarly, BAM invited associations to sign an agreement formalizing their membership of the recently created Bureau de Crédit. 4.2.9 Programme Measures: To reinforce the micro-credit sector, the Moroccan Government intends to focus on the improvement of governance of micro-credit associations through implementation of the following actions: (i) adoption by the monetary authorities, in 2009, of regulations on the classification and replenishment of outstanding debts of micro-credit associations; (ii) putting in place by the monetary authorities, in 2010, of regulations on the governance, risk management and internal auditing of micro-credit associations. 4.2.10 Expected outcomes: The new measures envisaged under this Programme, coupled with those under way, should reduce cross-indebtedness and debt overhang of households. In particular, these reforms should help to improve risk management and clean up the portfolio, the main expected outcome being the stabilization of PAR 30 at around 9% in 2010, unless it falls. COMPONENT 2 : IMPROVING ACCESS OF ENTERPRISES TO FINANCING 4.2.11 Access of enterprises to financing is a persistent constraint in Morocco even if the country has gained 10 places (from the 141st position to the 131st among 181 countries) in the 2010 ranking of the Doing Business report. In particular, the problem of guarantee remains a serious constraint on access to resources and, in this regard according to the 2009 Africa Competitiveness Report, Morocco comes at the bottom of the rankings (% of collateral compared to the loan amount is 169% whereas it is on average 109% for the region and 103% for countries with similar incomes). Faced with this situation, the reforms considered are aimed at: (i) improving the efficiency of the

11

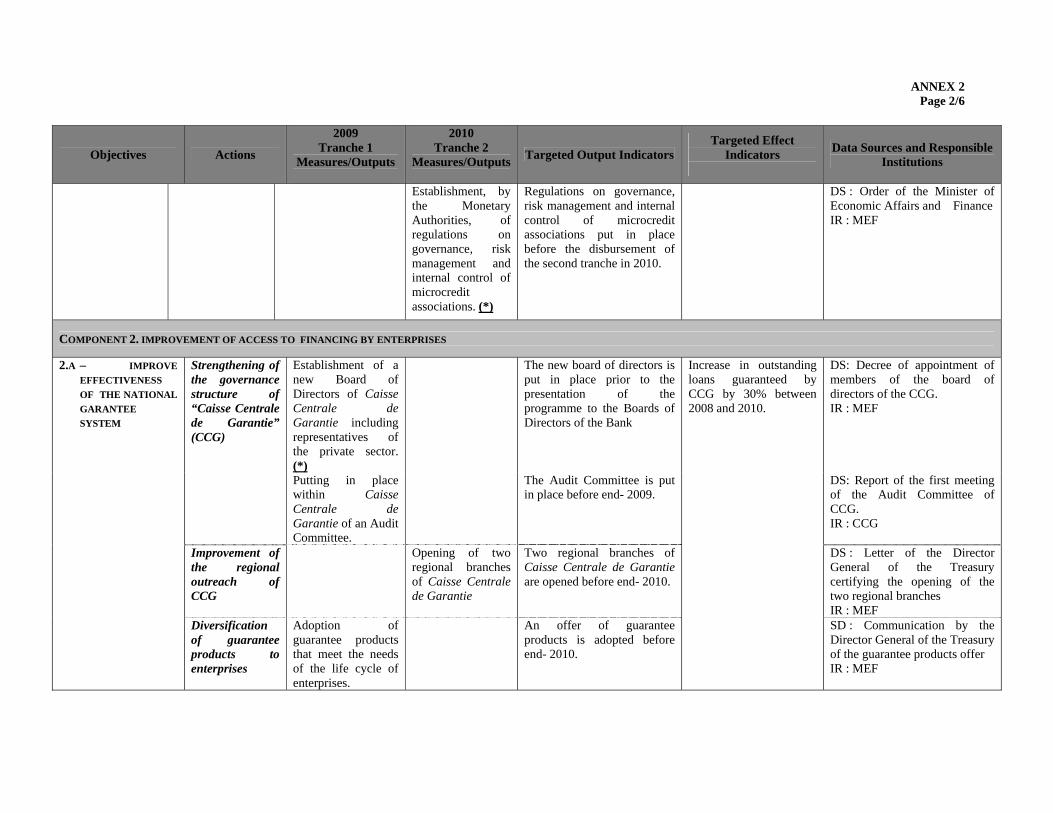

national guarantee system, (ii) improving risk information and management in credit operations, and (iii) developing venture capital activity for the benefit of enterprises. Sub-component 2a : Improvement of effectiveness of the national guarantee system 4.2.12 Context and challenges: The Moroccan Government deemed it necessary, by exercising national solidarity through sovereign guarantee, to support SMEs by providing them access to bank loans although they are unable to present security interests. The national guarantees mechanism (cf Technical Annex 5) was based mainly on three organizations: (i) the Caisse Centrale de Garantie (CCG), a public financial institution, comparable to a credit institution and thus subject to the supervision of BAM and whose mission consisted in managing public guarantee and co-financing funds, while itself providing guarantees on equity fund investments, (ii) Dar AD-Damane, a limited liability company created by the banks which, like the CCG, were managing both public and private guarantee funds; and, to a lesser extent, (iii) the Caisse Marocaine de Marché, which provided guarantee in pawn for public contracts. This mechanism required sectoral assistance according to the strategies of the Government. Indeed, 14 guarantee funds (textile, upgrading, tourism, enterprise creation) were managed by the two main guarantee institutions. These mechanisms were governed by different implementing instruments, leading to a compounding of granting procedures and to a confusion of the missions of the various actors and thus under-use of the guarantee lines put in place. In 2008, CCG commitments in the SME sector stood at DH 658 million (a 10% increase compared to 2007) for a total of 905 files. However, to be able to pursue its mission to serve SMEs in a sustainable manner, the CCG structures must be reinforced and the institution must be able to manage its risks efficiently. 4.2.13 Recent actions: The Government has conducted a strategic study to: (i) clarify the objectives of the national guarantee system, as well as the role of the institutions in such a system, (ii) have a more structured products offer the better meets corporate needs, and finally (iii) review the entire process of management and relations of the CCG with banks (define a new vision). Since the presence of two institutions complicated the visibility of the mechanism among the banks, it was decided that only one institution was to manage the system and the CCG was best placed to do so. To reinforce its role in the financing of SMEs, the Caisse Centrale de Garantie adopted a Development Plan for the period 2009-2012, which is centred on the following main thrusts: (i) products matching the corporate life cycle, (ii) streamlined procedures: celerity, responsiveness, delegation of guarantee decisions, and (iii) regional redeployment for better outreach to banks and enterprises through the creation of business districts in the major cities of the Kingdom. The CCG also concluded with the banks co-operation agreements on the use of guarantee and co-financing products. In addition, the State intends to support the national guarantee system by providing it with an annual subsidy of DHM 150 million over a period of 4 years 4.2.14 Programme Measures: To improve the efficiency of the national guarantee system, the Government intends to implement three essential actions. First of all, the governance structure of the CCG will be reinforced by putting in place in 2009: (i) a new Board of Directors with representatives of the private sector, and (ii) an audit committee. Secondly, improving the regional outreach of CCG will be promoted through the opening of two regional branches of the CCG in 2010. The third and final action to be implemented will be the diversification of guarantee products to companies through the adoption in 2009 of guarantee products that meet the needs of the corporate life cycle. 4.2.15 Expected outcomes: The implementation of this package of reforms should lead to a 30% increase in outstanding credits to SMEs benefiting from the guarantee of the CCG.

12

Sub-component 2b : Improvement of risk information and management in credit operations

4.2.16 Context and challenges: The financial infrastructure concerning the collection, accessibility, scope, disclosure and quality of information on credit is already fairly well developed in Morocco. In this regard, the 2010 Doing Business report grants Morocco a score of 5 on a scale of 6, which places the country above the average of OECD countries (score 4.1) and of the MENA region (score 3.3). The information disseminated may be positive (credit amount and repayment schedule), or negative (late payments, number and amount of repayment defaults). The creation and launching of the activities of a credit bureau can only consolidate this performance, which will ultimately allow for better control of credit risks and costs. 4.2.17 Recent actions: In February 2008, an agreement was signed between BAM and a private structure "Experian Maroc, Crédit Bureau International", under which BAM delegates to "Experian Maroc" the responsibility to reinforce and modernize the financial infrastructure dedicated to risk management by guaranteeing complete and comprehensive information. It is an approval with delegated management by BAM, the communicated data transiting through BAM before being sent to the credit bureau. The creation of a credit bureau will help to improve financial information relating to bank customers, not only the large enterprises but also SMEs, very small enterprises, private individuals and the customers benefiting from micro-credits, by putting in place: (i) a database that is more comprehensive and precise on the levels of indebtedness and solvency of the customers of the banking system and the AMC; (ii) a system for consolidating, processing and analyzing all the descriptive and financial data concerning the debt of the customers of credit institutions. 4.2.18 Programme Measures: The Government has agreed that the credit bureau should start operating in 2010. By then, reporting tests will be conducted, including one in 2009 to ensure the reliability of the system and enable the various actors to study the system. 4.2.19 Expected outcomes: Once the credit bureau goes operational, one should expect: (i) an improved rate of access to bank financing and a reduction of credit charges thanks to a drop in risk premium, (ii) wider access of operators to quality, reliable, comprehensive, complete and standardized information throughout the banking system (iii) access of customers hitherto excluded from the banking system thanks to improved risk assessment; (iv) reduction of outstanding credits and better protection the rights of borrowers. At the end of this programme, the main expected outcome should be a reduction of the share of non-performing bank loans in overall outstanding bank loans from 6% in 2008 to 5% in 2010. Sub-component 2c : Development of the venture capital business for enterprises 4.2.20 Context and challenges: The venture capital business is governed by Law No. 41-05 of February 2006 relating to Venture Capital Placement Organizations (OPCR). According to this law, the OPCR must invest at least 50% of their funds in SMEs as defined in the 2002 SME Charter. The venture capital sector consists of about fifteen enterprises, which manage 20 investment funds (13 general and 7 specialized practitioners) with an overall target volume of DH 10 billion in 2008. The importance of this sector in the Moroccan economy remains limited (0.03 of GDP) considering the following main factors: (i) weak interest of SMEs to be financed through this instrument, and (ii) rigorous conditions of eligibility. It is necessary to support the development of VC within the framework of a public/private partnership as in certain developed countries 4.2.21 Recent actions: As part of the revision of the national guarantee system, it was decided that the CCG should provide its guarantee to the equity or quasi-equity fund contributions realized by venture capital companies in eligible enterprises. A system of tax incentives for the OPCR was

13

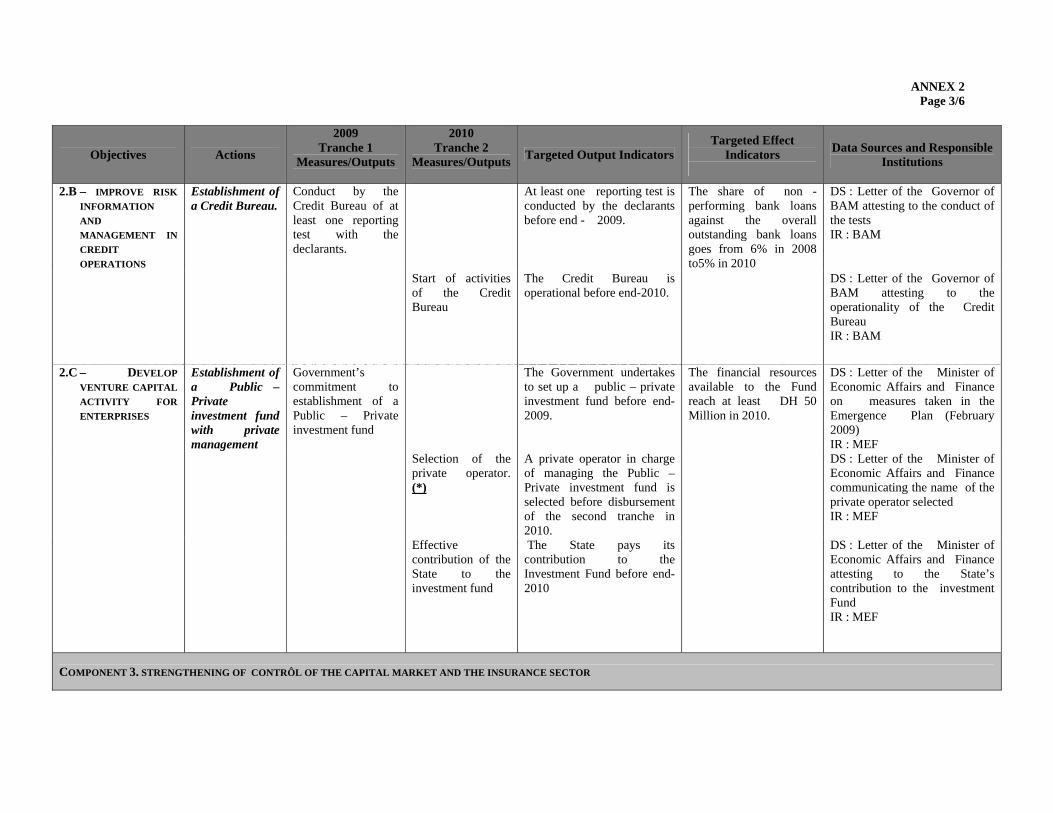

adopted by the finance law of 2006, including exemptions on the dividends obtained by the OPCR. To benefit from the exemption provided by the law, the OPCR must hold in their securities portfolio at least 50% of shares of unlisted Moroccan companies whose turnover, excluding value-added tax, is lower than 50 million dirhams. Under the Emergency Programme concluded between the State and the Private Sector, there is provision for the creation of public-private investment funds to promote the venture capital business and, through this, foster the financial inclusion of companies, particularly SMEs (cf Technical Annex 6). Within this framework, the Government intends to rely on the CCG to support the development of venture capital activities. The budgetary resources allocated to these Funds will be DHM 350 million spread out over the period 2009-2012. The Funds will be managed by one or more private operators. The funds will target starting, development and transmission. The idea at this point is that the public and the private will carry out the investments on an equal basis. Similarly, there are incentives mechanisms for private stakeholders (different conditions of remuneration between public shares and private shares, public shares repurchase terms and conditions, etc...). 4.2.22 Programme Measures: The measures envisaged under the programme concern: (i) Government’s commitment to setting up a public-private investment fund in 2009: (ii) selection of the private operator, and (iii) effective State contribution to the investment fund. 4.2.23 Expected Outcomes: In the long term, the implementation of the reforms envisaged by the Government should lead to an increase in the outstanding credit of OPCR. At the end of this programme, the main expected outcomes are: (i) lifting of the obstacle to capitalization currently penalizing many companies, thanks to the availability of the financial resources for the fund worth at least DHM 50 million in 2010; (ii) fostering of equity capital investments in the new enterprises. COMPONENT 3 : STRENGTHENING OF THE FINANCIAL MARKET AND

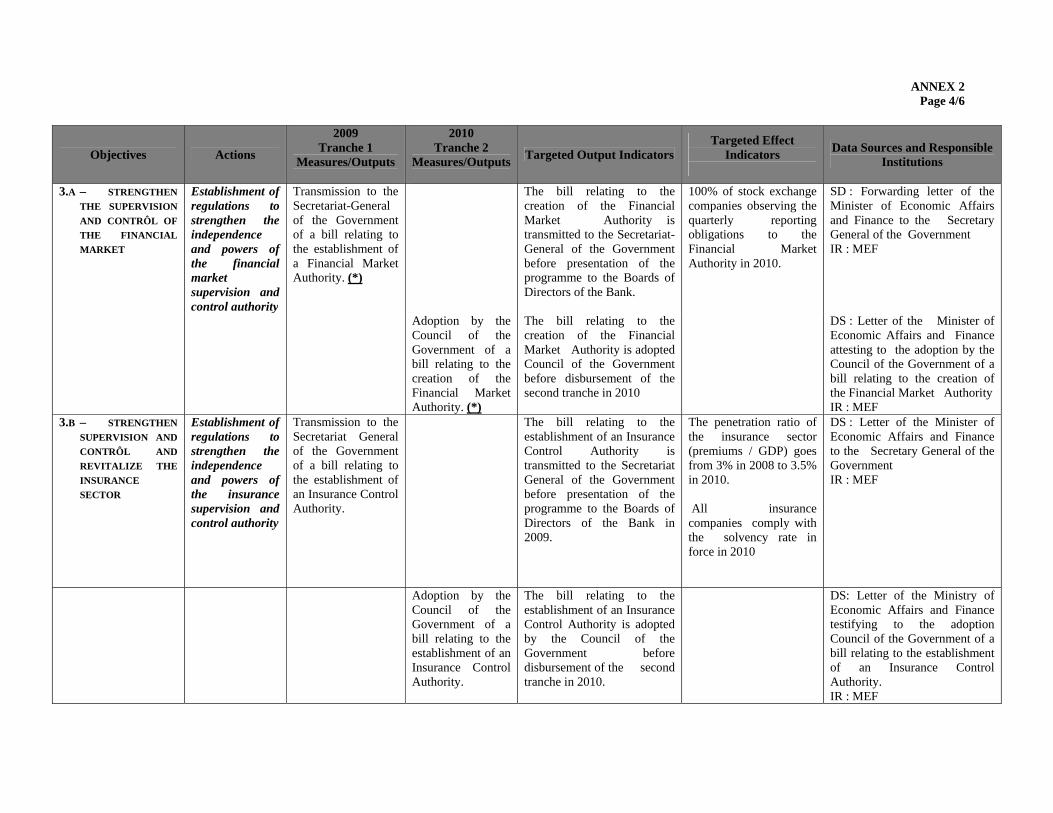

INSURANCE SECTOR CONTROL MECHANISM 4.2.24 The reform actions envisaged by PADESFI aim to: (i) reinforce supervision and control of the financial market, (ii) reinforce supervision and control and boost the insurances sector. Sub-component 3a : Strengthening of supervision and control of the financial market 4.2.25 Context and challenges: Created by the Dahir on Law No 1-93-212 of 21 September 1993, the Securities Ethics Board (CDVM) is responsible for protecting the savings invested in transferable securities (cf Technical Annex 7). As such, it: (i) supervises market stakeholders, (ii) monitors the availability and quality of information required by issuers, (iii) supervises the market, and (iv) assists the development of the market. The Board of Directors of the CDVM is chaired by the Minister of Economic Affairs and Finance. Considering the Government’s ambitions to make Casablanca a money market of international stature, the CDVM should, by virtue of its independence and its capacity to ensure transparency of the market, gain the full confidence of investors. 4.2.26 Recent actions: This challenge is all the more pressing as the CDVM became a member of the International Organization of Securities Commissions (OSCO) in 2008. 4.2.27 Programme Measures: To strengthen supervision and control of the financial market, the Government intends to put in place a legal framework enhancing the independence and capacities of the authority charged with supervision and control of the financial market, the authority being currently represented by CDVM. In this regard, the measures envisaged in the programme are: (i) transmission in 2009 to the Secretariat-General of the Government of a bill relating to the creation, through transformation of the CDVM, of a Financial Market Authority; and

14

(ii) adoption by the Cabinet meeting, in 2010, of the bill relating to the creation of the Financial Market Authority. The objective of this new instrument is to establish the independence of the control body from the Executive and to ensure that its decisions are collegial for more objectivity in its sanctioning process. Thus, the new Authority will be provided with a sanctions mechanism independent of the Minister of Economic Affairs and Finance which, in addition, will play only an observer role on the Board of Directors of the supervisory body. 4.2.28 Expected outcomes: At the end of the programme, the main expected outcome is that all the stock market companies will fulfil their obligations of quarterly reporting to the Financial Market Authority in 2010.

Sub-component 3.b : Strengthening of supervision and control, and revitalization of the

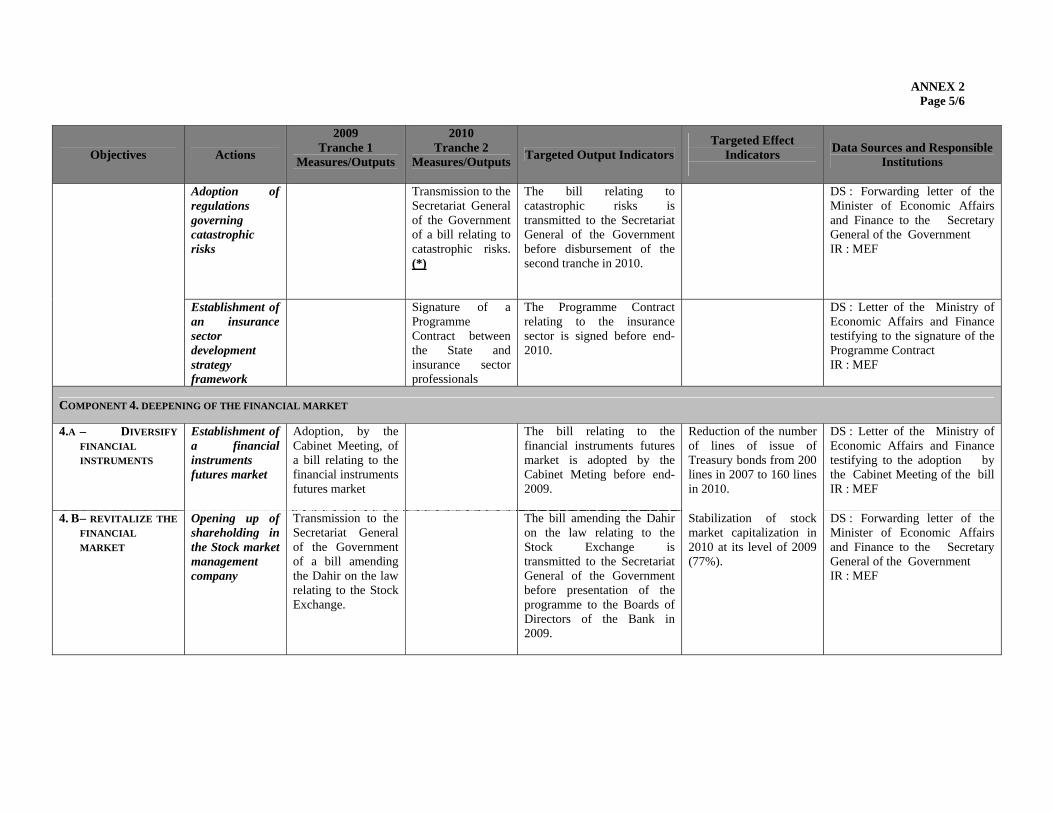

insurance sector 4.2.29 Context and challenges: The Moroccan market, which comprises sixteen insurance and mutual insurance companies and one reinsurance company, is the leading in the Maghreb and the second of the African continent. With a turnover exceeding DH Bln 19.75 in 2008 (an increase of 11.43% compared to 2007), the industry relies mainly on the dynamism of the following branches: Life (33.21%), land borne motor vehicles (30.34%) and Casualty Accidents-sickness-maternity (12.47%). With a loss ratio of 86% in 2008, the profitability of the sector results from the net financial proceeds generated by investments based mainly on transferable securities (90%), real estate (4%), and cash investments (6%). The assets of Moroccan institutional investors are generally placed in medium-term financial instruments, as long-term interest rates are not very competitive. This leads to inconsistency between the duration of their assets and that of their liabilities. The Department of Insurance and Social Protection (DAPS) of the Ministry of Economic Affairs and Finance is the authority charged with supervision and control of the insurance sector (cf Technical Annex 8). For better supervision of the sector, it is necessary to strengthen the independence of this authority. 4.2.30 Recent actions: Following the publication of a new Insurance Code in 2002, prudential regulations were reinforced in 2004 and 2005 to raise them to international standards, and a new accounting plan was adopted. These new provisions officialized bank insurance, which accounts for the rapid development of life insurance. New laws passed between 2006 and 2008 institute mandatory insurance (car, industrial accidents and disease). With regard to insurance contracts, the rules of suspension were clarified and contracts in Units of Account were introduced into the Life branch by taking into account their risk levels. Finally, the new Insurance Code establishes the separation of the Life and Non-Life branches. Tariffs have been progressively raised in all branches, leading to complete liberalization in 2006. The Moroccan Government also commissioned from two international firms (Oliver Wymann and Actuaria), a diagnostic study of the insurance sector. This study recommends 75 improvement measures designed to serve as basis for the vision of all the stakeholders of the sector in the coming years within the framework of a programme contract. 4.2.31 Programme Measures: Through its programme of reforms, the Moroccan Government intends to improve the supervision of insurance and reinsurance companies, social insurance funds, the organization of the sector, governance of the actors, and transparency of activities. For this reason, it will set up an independent authority for control and supervision of the insurance sector. Besides monitoring and control of application of the rules enacted by the Insurance Code and the respective legal instruments governing the various pension funds, this Authority will have powers to sanction and define prudential and control rules for the insurance sector. The granting and withdrawal of approvals will remain solely the competence of the Minister of Finance upon approval by the Authority. The intermediaries will be approved by the Authority. It has been

15

decided that: (i) the Ministry of Finance will transmit to the Secretariat-General of the Government, before submission to the Council, the bill relating to the creation of an independent Insurance Sector Control Authority; (ii) this instrument must be adopted by the Cabinet Meeting in 2010. To improve the protection of individual and collective assets in a country exposed to environmental hazards and terrorism, the Moroccan Government has prepared a legal framework relating to catastrophic risks which will enable insurance and reinsurance sector operators to effectively cover protection of communities and individuals. The bill relating to catastrophic risks will be transmitted to the Secretariat-General of the Government in 2010. Lastly, the Government intends to put in place a strategic framework for insurance sector development. To reach a common vision, the Moroccan Government will undertake broad consultations with the various insurance sector stakeholders that should lead to the signature in 2010 of a Programme Contract defining the commitments of the public and private sectors for sustainable development of the sector. 4.2.32 Expected outcomes: At the end of the programme: (i) the rate of penetration of the insurance sector should increase from 3% in 2008 to 3.5% in 2010, and (ii) all the Moroccan insurance companies will comply with the solvency ratio in force. COMPONENT 4 : DEEPENING OF THE FINANCIAL MARKET 4.2.33 The deepening of the financial market aims to: (i) diversify the financial instruments, and (ii) boost the financial market. It is in line with reforms initiated some twenty years ago and aimed at making Morocco a world-class money market with credible governance institutions and where the appropriate financial instruments circulate. Sub-component 4a : Diversification of financial instruments 4.2.34 Context and challenges: Admittedly, many financial instruments (shares, bonds, Treasury bonds, short-term negotiable debt securities, etc.) already circulate on Morocco’s financial market (cf Technical Annex 10). However, in a context of volatility of prices, interest rates, and exchange rates, the holders of such securities remain exposed to the various risks, hence the need to put at their disposal instruments of coverage as exist on major money markets. In this regard, the existence of a long-term financial instruments market (Futures and Options) offers holders of securities (particularly banks, insurance companies, retirement funds, various mutual fund management companies), the possibility of protecting themselves, at a certain cost, against risks of expiry rates and, in general, against the risks of asset price fluctuations. In Morocco, there is officially no organized long-term instruments market. Nevertheless, certain operations already being carried out in private are akin to long-term operations. Furthermore, for long-rate coverage instruments, there must first of all be sufficient underlying assets and a reliable and non-volatile rates curve, directly linked to the issue of long-term Treasury bonds. The establishment of a formal framework of a long- term financial instruments market, as well as the existence of sufficient underlying assets, are challenges to be met. 4.2.35 Recent actions: The Government has embarked on a process of establishment of an organized market in the long term, the first stage being the development of the regulatory framework of the market, which will allow for investment in products providing better coverage for financial market risks. Conscious of the need to have a reliable rates curve, the Government is striving to prepare a programme that in the long term will help to reactivate the issue of long-term treasury bonds before effective start of the futures market.

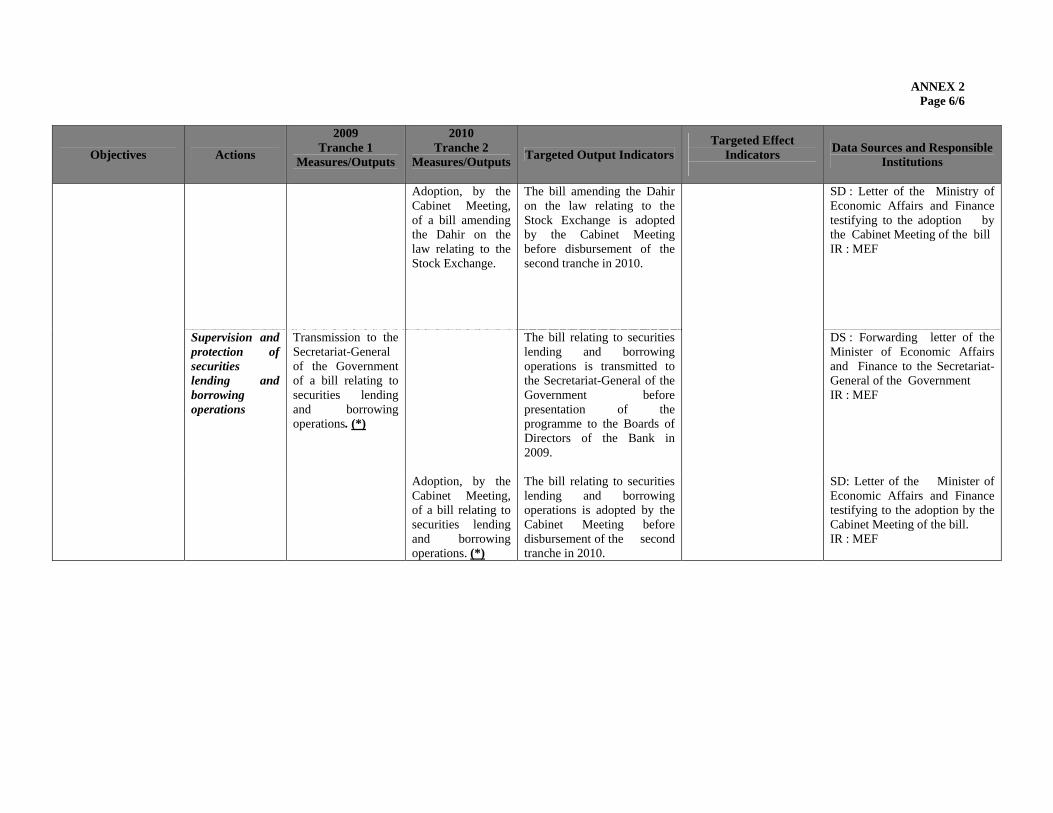

16

4.2.36 Programme Measures: The Government intends to open a financial instruments futures market. To that end, it has been decided that in 2009, the Cabinet Meeting will adopt a bill relating to the financial instruments futures market. 4.2.37 Expected Outcomes: Pending the effective start of the financial instruments futures market, there are plans to reduce the number of lines of issue of Treasury bonds from 200 lines in 2007 to 160 lines in 2010 so as to increase the volume of securities per line and thus consolidate the size underlying assets. Sub-component 4b : Revitalization of the financial market 4.2.38 Context and challenges: The financial market is organized around the Casablanca Stock Market, a limited liability company whose capital is held in equal shares by 17 stock market companies (cf. Technical Annex 12). The market performed poorly in 2008 with, in particular (i) a decline in two indices, namely MASI and MADEX of 13.43% and 13.41% respectively; (ii) a 9.31% drop in stock exchange capitalization, and (iii) 32% reduction in transactions, particularly in the central stock market, which recorded a 64% drop while the block shares market dropped by 19%. In addition to such recent poor performance, the Casablanca Stock Exchange is structurally in search of fresh breath that should enable it to substantially increase the number of companies listed, as well as that of stock exchange transactions. Furthermore, the current practice of carrying out lending and borrowing transactions outside any legal framework hampers transparency and efficiency of the market. 4.2.39 Recent Actions: Casablanca Stock Exchange has started identifying companies that can access the stock market. Similarly, it conducts information and sensitization campaigns to popularize and promote the stock exchange institution, and is currently developing a vision to go international. 4.2.40 Programme Measures: The Government intends to open up the shares of the company managing the Casablanca Stock Exchange (CSE) so as to improve the governance of the stock exchange institution. In this way, the CSE can benefit from transfer of competence as a result of the subscription of major shareholders to its capital. To that end, a bill amending the Dahir on the law relating to the Stock Market will be transmitted to the Secretariat-General of the Government in 2009, and adopted in 2010. In addition, the Government intends to supervise and protect securities lending and borrowing transactions by putting in place a legal framework that would ensure transparency in these operations, and thereby revitalize them. Hence, the Government intends: (i) in 2009, to transmit to the Secretariat-General of the Government a bill relating to securities lending and borrowing transactions, and (ii) in 2010, to have the said bill adopted by the Cabinet Meeting. 4.2.41 Expected Outcomes: At the end of the programme in 2010, it is expected that the stock exchange capitalization will at least be stabilized at its 2009 level. 4.2.42 Status of implementation of the programme reforms: Following dialogue with the Government, the latter has undertaken to put in place the following measures prior to presentation of the programme to the Boards of Directors of the Bank Group:

17

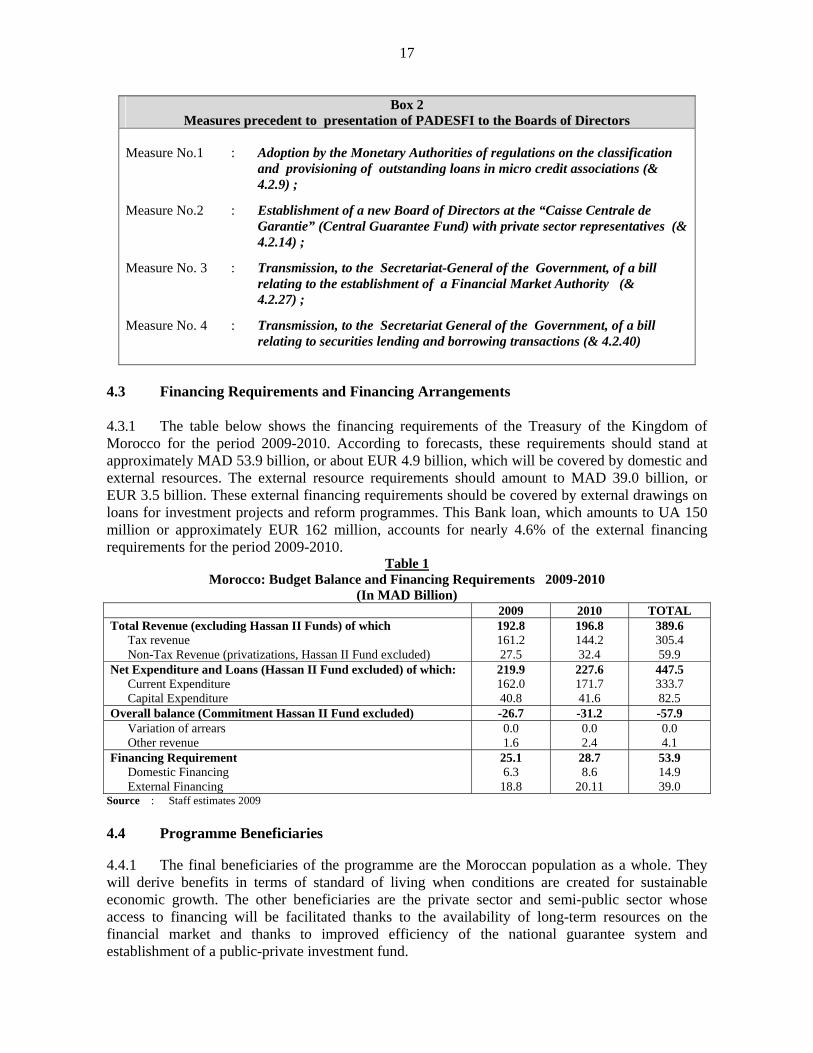

Box 2

Measures precedent to presentation of PADESFI to the Boards of Directors Measure No.1 : Adoption by the Monetary Authorities of regulations on the classification