Embed Size (px)

Citation preview

AFTER-SCHOOL ALL-STARS

FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2011

TABLE OF CONTENTS

Page

INDEPENDENT AUDITORS' REPORT 1

FINANCIAL STATEMENTS

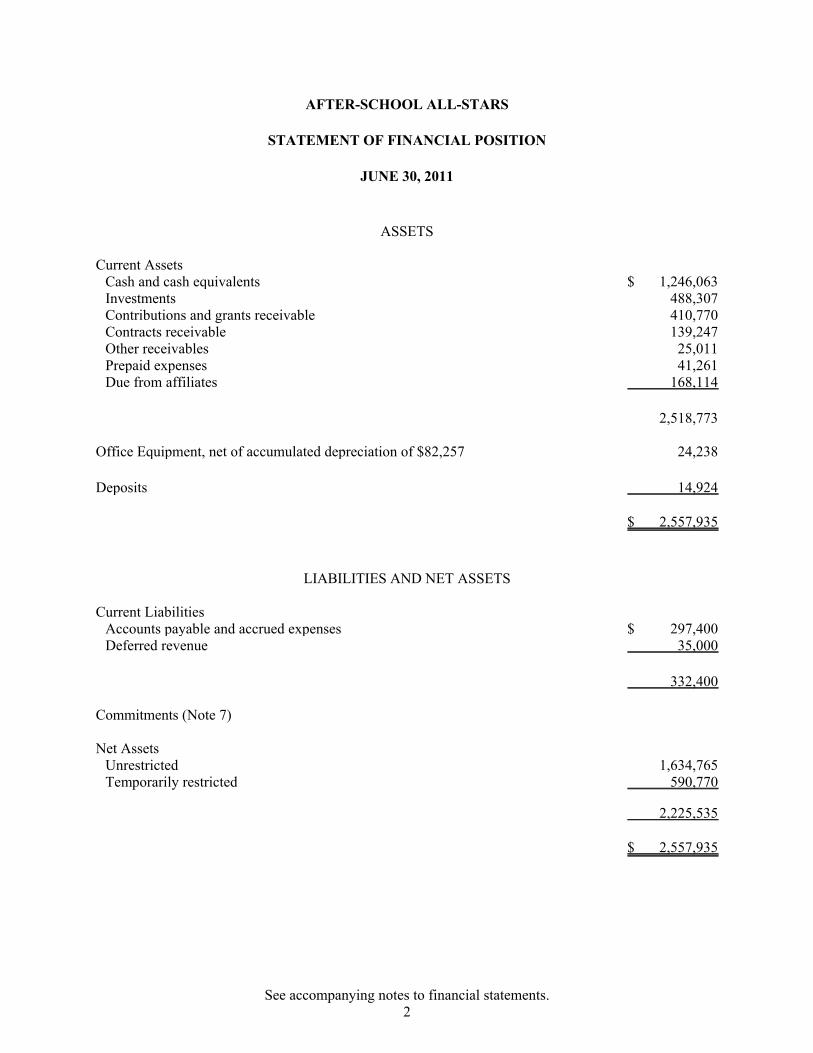

Statement of Financial Position 2

Statement of Activities 3

Statement of Functional Expenses 4

Statement of Cash Flows 5

NOTES TO FINANCIAL STATEMENTS 6 - 12

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTINGAND ON COMPLIANCE AND OTHER MATTERS BASED ON ANAUDIT OF FINANCIAL STATEMENTS PERFORMED INACCORDANCE WITH GOVERNMENT AUDITING STANDARDS 13 - 14

AFTER-SCHOOL ALL-STARS

STATEMENT OF FINANCIAL POSITION

JUNE 30, 2011

ASSETS

Current AssetsCash and cash equivalents $ 1,246,063Investments 488,307Contributions and grants receivable 410,770Contracts receivable 139,247Other receivables 25,011Prepaid expenses 41,261Due from affiliates 168,114

2,518,773

Office Equipment, net of accumulated depreciation of $82,257 24,238

Deposits 14,924

$ 2,557,935

LIABILITIES AND NET ASSETS

Current LiabilitiesAccounts payable and accrued expenses $ 297,400Deferred revenue 35,000

332,400

Commitments (Note 7)

Net AssetsUnrestricted 1,634,765Temporarily restricted 590,770

2,225,535

$ 2,557,935

See accompanying notes to financial statements.2

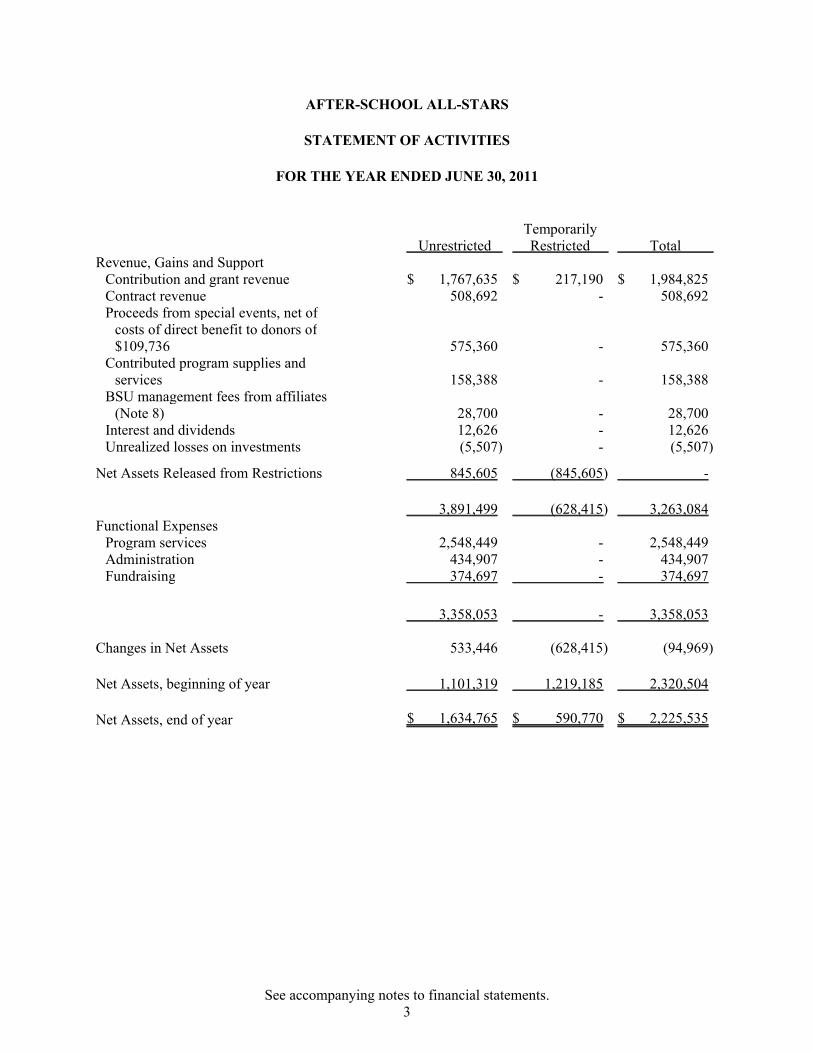

AFTER-SCHOOL ALL-STARS

STATEMENT OF ACTIVITIES

FOR THE YEAR ENDED JUNE 30, 2011

UnrestrictedTemporarilyRestricted Total

Revenue, Gains and SupportContribution and grant revenue $ 1,767,635 $ 217,190 $ 1,984,825Contract revenue 508,692 - 508,692Proceeds from special events, net of

costs of direct benefit to donors of$109,736 575,360 - 575,360

Contributed program supplies andservices 158,388 - 158,388

BSU management fees from affiliates(Note 8) 28,700 - 28,700

Interest and dividends 12,626 - 12,626Unrealized losses on investments (5,507) - (5,507)

Net Assets Released from Restrictions 845,605 (845,605) -

3,891,499 (628,415) 3,263,084Functional Expenses

Program services 2,548,449 - 2,548,449Administration 434,907 - 434,907Fundraising 374,697 - 374,697

3,358,053 - 3,358,053

Changes in Net Assets 533,446 (628,415) (94,969)

Net Assets, beginning of year 1,101,319 1,219,185 2,320,504

Net Assets, end of year $ 1,634,765 $ 590,770 $ 2,225,535

See accompanying notes to financial statements.3

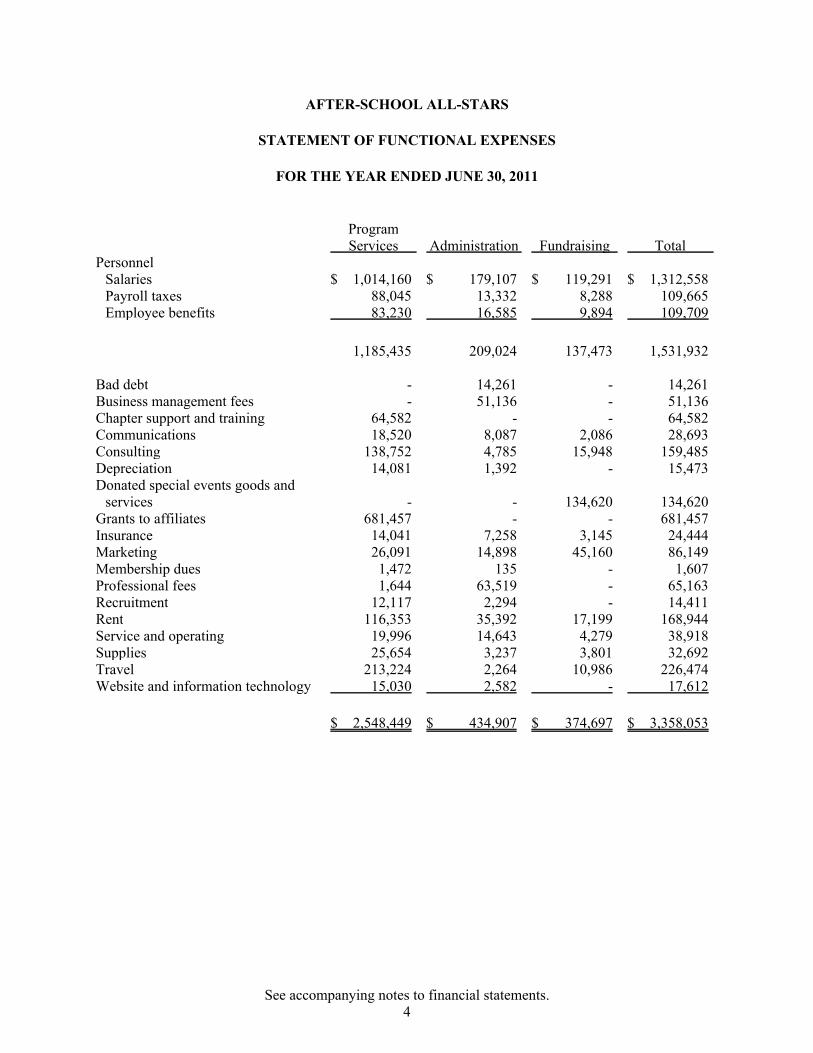

AFTER-SCHOOL ALL-STARS

STATEMENT OF FUNCTIONAL EXPENSES

FOR THE YEAR ENDED JUNE 30, 2011

ProgramServices Administration Fundraising Total

PersonnelSalaries $ 1,014,160 $ 179,107 $ 119,291 $ 1,312,558Payroll taxes 88,045 13,332 8,288 109,665Employee benefits 83,230 16,585 9,894 109,709

1,185,435 209,024 137,473 1,531,932

Bad debt - 14,261 - 14,261Business management fees - 51,136 - 51,136Chapter support and training 64,582 - - 64,582Communications 18,520 8,087 2,086 28,693Consulting 138,752 4,785 15,948 159,485Depreciation 14,081 1,392 - 15,473Donated special events goods and

services - - 134,620 134,620Grants to affiliates 681,457 - - 681,457Insurance 14,041 7,258 3,145 24,444Marketing 26,091 14,898 45,160 86,149Membership dues 1,472 135 - 1,607Professional fees 1,644 63,519 - 65,163Recruitment 12,117 2,294 - 14,411Rent 116,353 35,392 17,199 168,944Service and operating 19,996 14,643 4,279 38,918Supplies 25,654 3,237 3,801 32,692Travel 213,224 2,264 10,986 226,474Website and information technology 15,030 2,582 - 17,612

$ 2,548,449 $ 434,907 $ 374,697 $ 3,358,053

See accompanying notes to financial statements.4

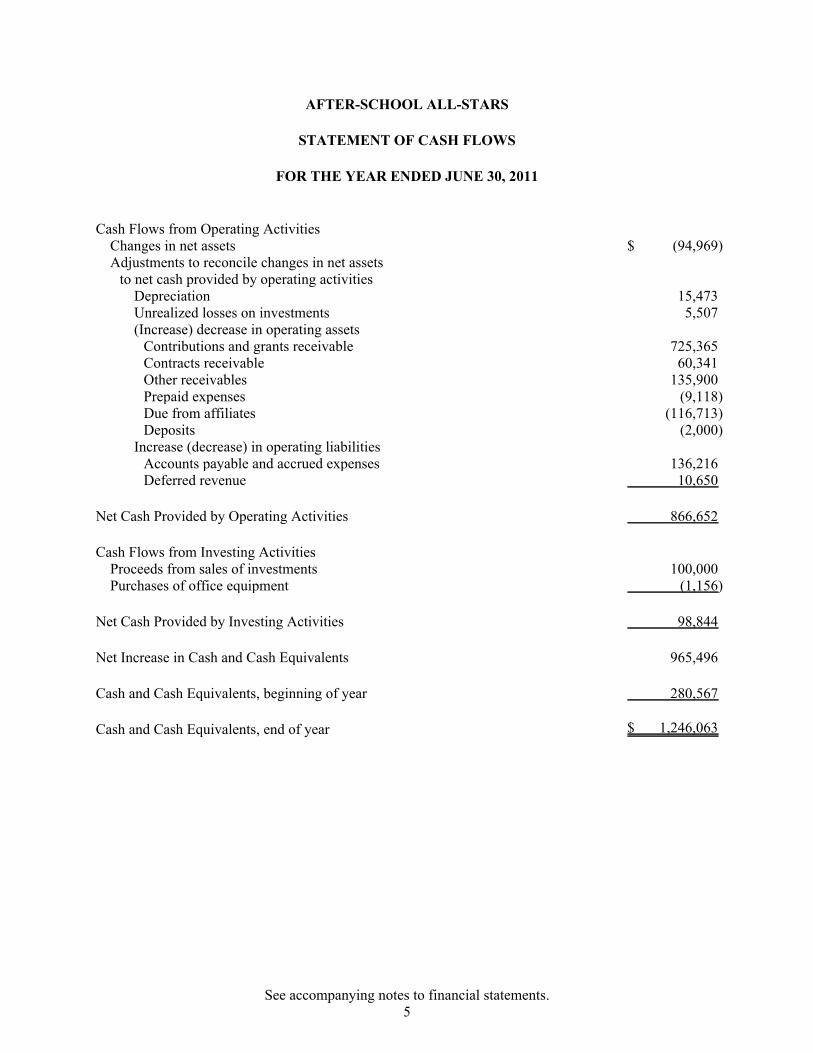

AFTER-SCHOOL ALL-STARS

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED JUNE 30, 2011

Cash Flows from Operating ActivitiesChanges in net assets $ (94,969)Adjustments to reconcile changes in net assets

to net cash provided by operating activitiesDepreciation 15,473Unrealized losses on investments 5,507(Increase) decrease in operating assets

Contributions and grants receivable 725,365Contracts receivable 60,341Other receivables 135,900Prepaid expenses (9,118)Due from affiliates (116,713)Deposits (2,000)

Increase (decrease) in operating liabilitiesAccounts payable and accrued expenses 136,216Deferred revenue 10,650

Net Cash Provided by Operating Activities 866,652

Cash Flows from Investing ActivitiesProceeds from sales of investments 100,000Purchases of office equipment (1,156)

Net Cash Provided by Investing Activities 98,844

Net Increase in Cash and Cash Equivalents 965,496

Cash and Cash Equivalents, beginning of year 280,567

Cash and Cash Equivalents, end of year $ 1,246,063

See accompanying notes to financial statements.5

AFTER-SCHOOL ALL-STARS

NOTES TO FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2011

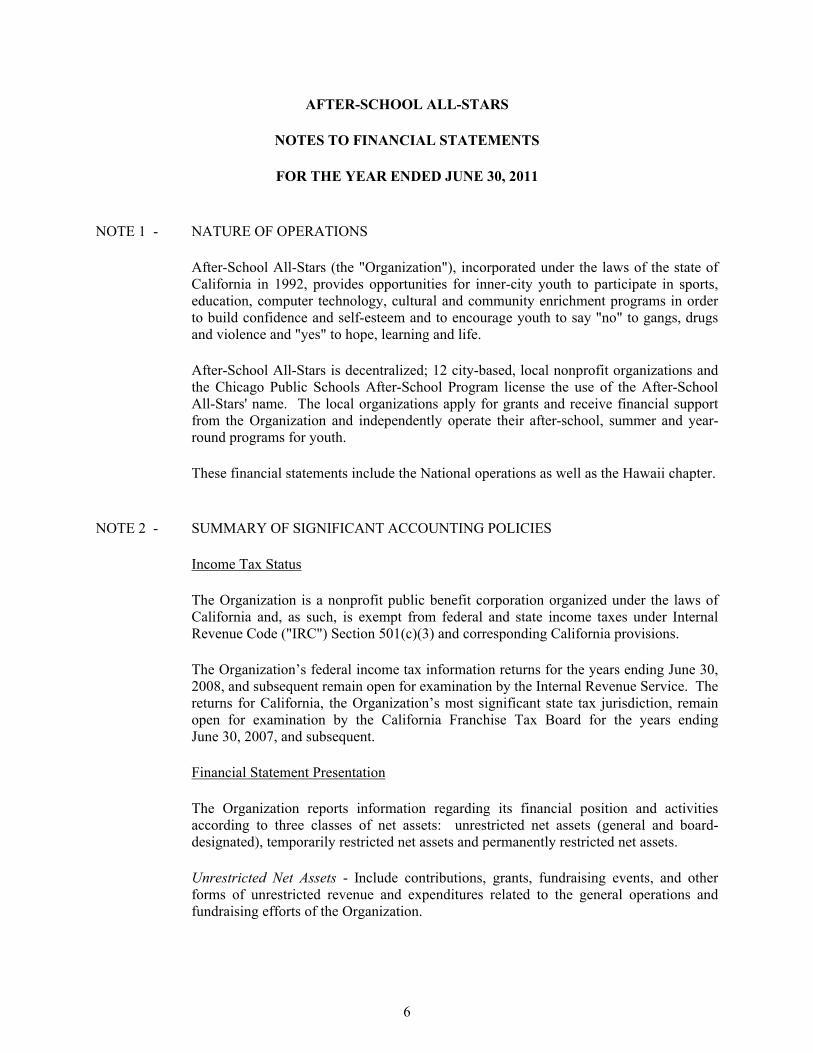

NOTE 1 - NATURE OF OPERATIONS

After-School All-Stars (the "Organization"), incorporated under the laws of the state ofCalifornia in 1992, provides opportunities for inner-city youth to participate in sports,education, computer technology, cultural and community enrichment programs in orderto build confidence and self-esteem and to encourage youth to say "no" to gangs, drugsand violence and "yes" to hope, learning and life.

After-School All-Stars is decentralized; 12 city-based, local nonprofit organizations andthe Chicago Public Schools After-School Program license the use of the After-SchoolAll-Stars' name. The local organizations apply for grants and receive financial supportfrom the Organization and independently operate their after-school, summer and year-round programs for youth.

These financial statements include the National operations as well as the Hawaii chapter.

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Income Tax Status

The Organization is a nonprofit public benefit corporation organized under the laws ofCalifornia and, as such, is exempt from federal and state income taxes under InternalRevenue Code ("IRC") Section 501(c)(3) and corresponding California provisions.

The Organization’s federal income tax information returns for the years ending June 30,2008, and subsequent remain open for examination by the Internal Revenue Service. Thereturns for California, the Organization’s most significant state tax jurisdiction, remainopen for examination by the California Franchise Tax Board for the years endingJune 30, 2007, and subsequent.

Financial Statement Presentation

The Organization reports information regarding its financial position and activitiesaccording to three classes of net assets: unrestricted net assets (general and board-designated), temporarily restricted net assets and permanently restricted net assets.

Unrestricted Net Assets - Include contributions, grants, fundraising events, and otherforms of unrestricted revenue and expenditures related to the general operations andfundraising efforts of the Organization.

6

AFTER-SCHOOL ALL-STARS

NOTES TO FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2011

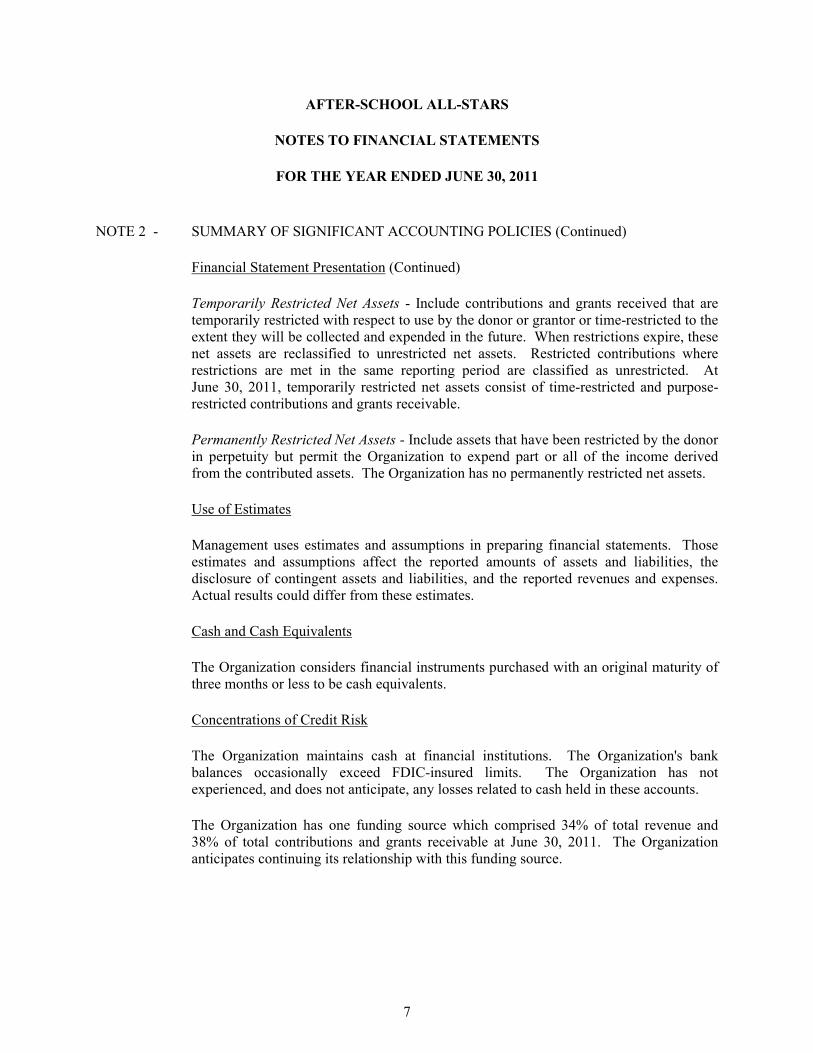

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Financial Statement Presentation (Continued)

Temporarily Restricted Net Assets - Include contributions and grants received that aretemporarily restricted with respect to use by the donor or grantor or time-restricted to theextent they will be collected and expended in the future. When restrictions expire, thesenet assets are reclassified to unrestricted net assets. Restricted contributions whererestrictions are met in the same reporting period are classified as unrestricted. AtJune 30, 2011, temporarily restricted net assets consist of time-restricted and purpose-restricted contributions and grants receivable.

Permanently Restricted Net Assets - Include assets that have been restricted by the donorin perpetuity but permit the Organization to expend part or all of the income derivedfrom the contributed assets. The Organization has no permanently restricted net assets.

Use of Estimates

Management uses estimates and assumptions in preparing financial statements. Thoseestimates and assumptions affect the reported amounts of assets and liabilities, thedisclosure of contingent assets and liabilities, and the reported revenues and expenses.Actual results could differ from these estimates.

Cash and Cash Equivalents

The Organization considers financial instruments purchased with an original maturity ofthree months or less to be cash equivalents.

Concentrations of Credit Risk

The Organization maintains cash at financial institutions. The Organization's bankbalances occasionally exceed FDIC-insured limits. The Organization has notexperienced, and does not anticipate, any losses related to cash held in these accounts.

The Organization has one funding source which comprised 34% of total revenue and38% of total contributions and grants receivable at June 30, 2011. The Organizationanticipates continuing its relationship with this funding source.

7

AFTER-SCHOOL ALL-STARS

NOTES TO FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2011

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

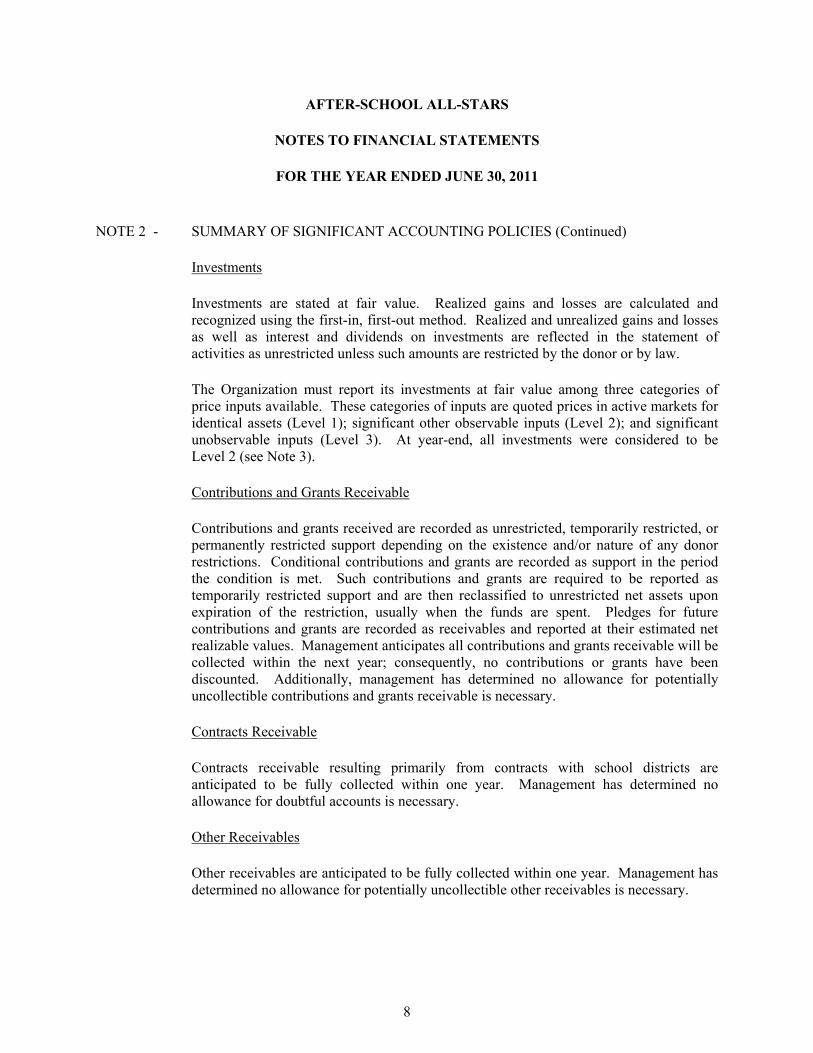

Investments

Investments are stated at fair value. Realized gains and losses are calculated andrecognized using the first-in, first-out method. Realized and unrealized gains and lossesas well as interest and dividends on investments are reflected in the statement ofactivities as unrestricted unless such amounts are restricted by the donor or by law.

The Organization must report its investments at fair value among three categories ofprice inputs available. These categories of inputs are quoted prices in active markets foridentical assets (Level 1); significant other observable inputs (Level 2); and significantunobservable inputs (Level 3). At year-end, all investments were considered to beLevel 2 (see Note 3).

Contributions and Grants Receivable

Contributions and grants received are recorded as unrestricted, temporarily restricted, orpermanently restricted support depending on the existence and/or nature of any donorrestrictions. Conditional contributions and grants are recorded as support in the periodthe condition is met. Such contributions and grants are required to be reported astemporarily restricted support and are then reclassified to unrestricted net assets uponexpiration of the restriction, usually when the funds are spent. Pledges for futurecontributions and grants are recorded as receivables and reported at their estimated netrealizable values. Management anticipates all contributions and grants receivable will becollected within the next year; consequently, no contributions or grants have beendiscounted. Additionally, management has determined no allowance for potentiallyuncollectible contributions and grants receivable is necessary.

Contracts Receivable

Contracts receivable resulting primarily from contracts with school districts areanticipated to be fully collected within one year. Management has determined noallowance for doubtful accounts is necessary.

Other Receivables

Other receivables are anticipated to be fully collected within one year. Management hasdetermined no allowance for potentially uncollectible other receivables is necessary.

8

AFTER-SCHOOL ALL-STARS

NOTES TO FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2011

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

Office Equipment

Purchases of office equipment are recorded at cost. Donated items are recorded atestimated fair value when received. Depreciation both purchased and donated officeequipment are computed using the straight-line basis over the estimated useful lives,generally five years.

Normal repairs and maintenance are expensed as incurred, whereas significant chargeswhich materially increase values or extend useful lives are capitalized and depreciatedover the estimated useful lives of the related assets.

Impairment of Long-Lived Assets

Management reviews each asset or asset group for impairment whenever events orcircumstances indicate that the carrying value of an asset or asset group may not berecoverable, but at least annually. The review of recoverability is based onmanagement's estimate of the undiscounted future cash flows that are expected to resultfrom the asset's use and eventual disposition. These cash flows consider factors such asexpected future operating income, trends and prospects, as well as the effects ofcompetition and other factors. If an impairment event exists due to the projectedinability to recover the carrying value of an asset or asset group, an impairment loss isrecognized to the extent that the carrying value exceeds estimated fair value. Noimpairment provision was recorded by the Organization during the year.

Deferred Revenue

Cash collected in advance for a special event which occurred in August 2011 has beenreported as deferred revenue.

Functional Allocation of Expenses

The Organization allocates its expenses on a functional basis among its various programand support services. Expenses that can be identified with a specific program or supportservice are allocated directly according to their natural expense classification. Otherexpenses that are common to several functions are allocated accordingly.

9

AFTER-SCHOOL ALL-STARS

NOTES TO FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2011

NOTE 2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

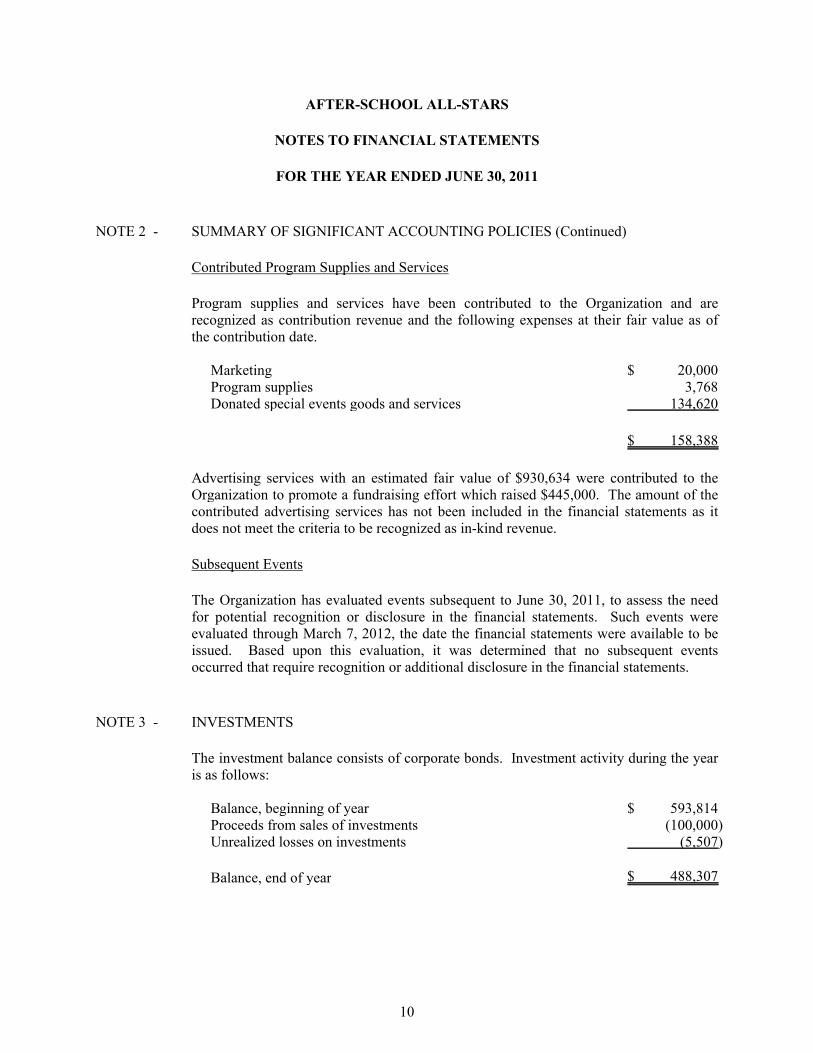

Contributed Program Supplies and Services

Program supplies and services have been contributed to the Organization and arerecognized as contribution revenue and the following expenses at their fair value as ofthe contribution date.

Marketing $ 20,000Program supplies 3,768Donated special events goods and services 134,620

$ 158,388

Advertising services with an estimated fair value of $930,634 were contributed to theOrganization to promote a fundraising effort which raised $445,000. The amount of thecontributed advertising services has not been included in the financial statements as itdoes not meet the criteria to be recognized as in-kind revenue.

Subsequent Events

The Organization has evaluated events subsequent to June 30, 2011, to assess the needfor potential recognition or disclosure in the financial statements. Such events wereevaluated through March 7, 2012, the date the financial statements were available to beissued. Based upon this evaluation, it was determined that no subsequent eventsoccurred that require recognition or additional disclosure in the financial statements.

NOTE 3 - INVESTMENTS

The investment balance consists of corporate bonds. Investment activity during the yearis as follows:

Balance, beginning of year $ 593,814Proceeds from sales of investments (100,000)Unrealized losses on investments (5,507)

Balance, end of year $ 488,307

10

AFTER-SCHOOL ALL-STARS

NOTES TO FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2011

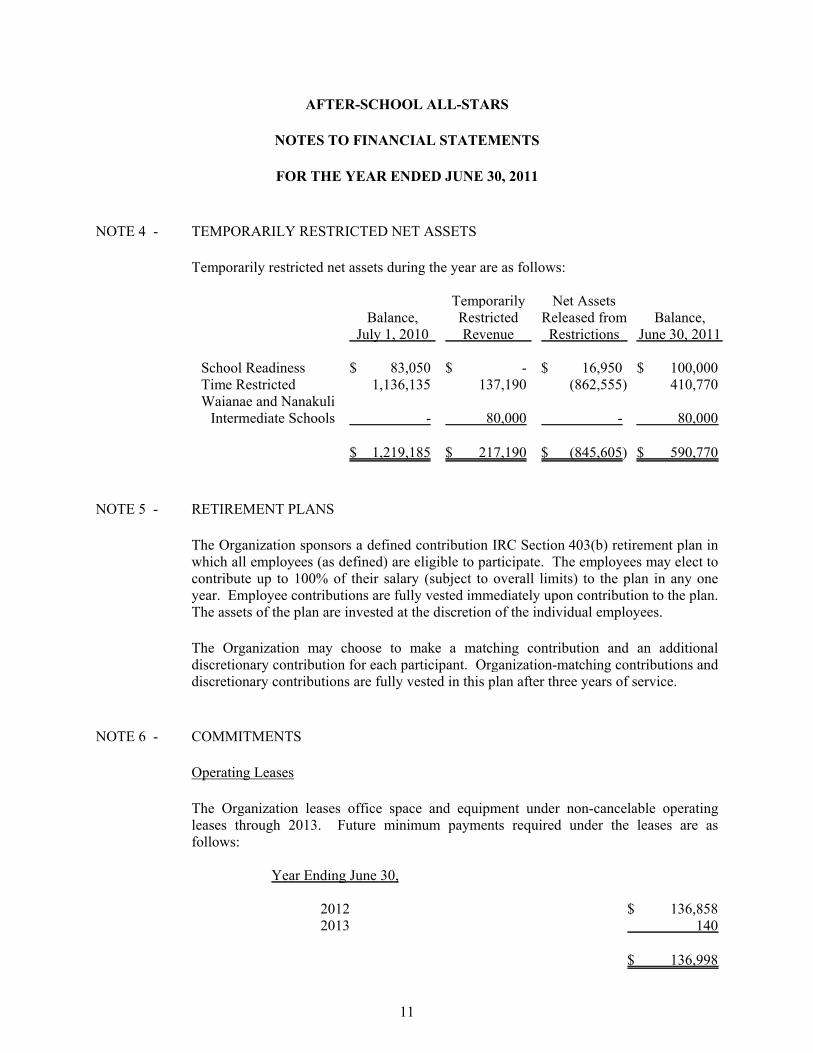

NOTE 4 - TEMPORARILY RESTRICTED NET ASSETS

Temporarily restricted net assets during the year are as follows:

Balance,July 1, 2010

TemporarilyRestrictedRevenue

Net AssetsReleased fromRestrictions

Balance,June 30, 2011

School Readiness $ 83,050 $ - $ 16,950 $ 100,000Time Restricted 1,136,135 137,190 (862,555) 410,770Waianae and Nanakuli

Intermediate Schools - 80,000 - 80,000

$ 1,219,185 $ 217,190 $ (845,605) $ 590,770

NOTE 5 - RETIREMENT PLANS

The Organization sponsors a defined contribution IRC Section 403(b) retirement plan inwhich all employees (as defined) are eligible to participate. The employees may elect tocontribute up to 100% of their salary (subject to overall limits) to the plan in any oneyear. Employee contributions are fully vested immediately upon contribution to the plan.The assets of the plan are invested at the discretion of the individual employees.

The Organization may choose to make a matching contribution and an additionaldiscretionary contribution for each participant. Organization-matching contributions anddiscretionary contributions are fully vested in this plan after three years of service.

NOTE 6 - COMMITMENTS

Operating Leases

The Organization leases office space and equipment under non-cancelable operatingleases through 2013. Future minimum payments required under the leases are asfollows:

Year Ending June 30,

2012 $ 136,8582013 140

$ 136,998

11

AFTER-SCHOOL ALL-STARS

NOTES TO FINANCIAL STATEMENTS

FOR THE YEAR ENDED JUNE 30, 2011

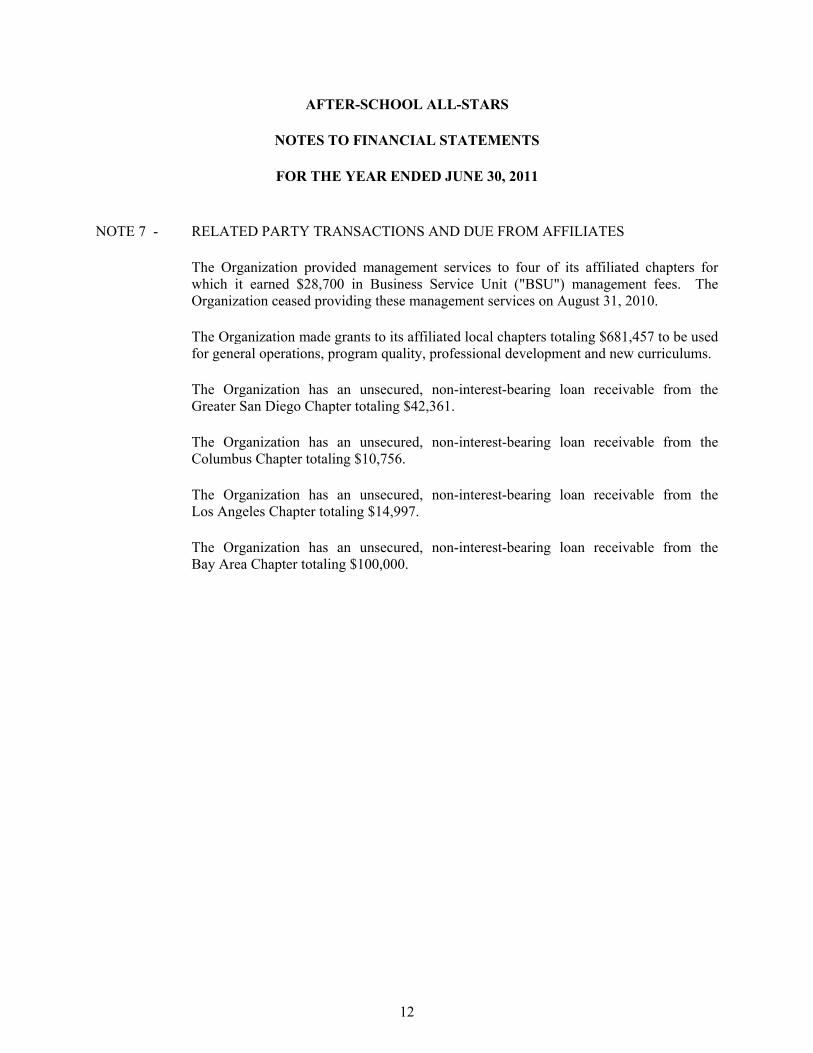

NOTE 7 - RELATED PARTY TRANSACTIONS AND DUE FROM AFFILIATES

The Organization provided management services to four of its affiliated chapters forwhich it earned $28,700 in Business Service Unit ("BSU") management fees. TheOrganization ceased providing these management services on August 31, 2010.

The Organization made grants to its affiliated local chapters totaling $681,457 to be usedfor general operations, program quality, professional development and new curriculums.

The Organization has an unsecured, non-interest-bearing loan receivable from theGreater San Diego Chapter totaling $42,361.

The Organization has an unsecured, non-interest-bearing loan receivable from theColumbus Chapter totaling $10,756.

The Organization has an unsecured, non-interest-bearing loan receivable from theLos Angeles Chapter totaling $14,997.

The Organization has an unsecured, non-interest-bearing loan receivable from theBay Area Chapter totaling $100,000.

12