Embed Size (px)

Citation preview

After-Tax Analysis

October 24, 2014

Summary of Last Lecture

Our business has to pay taxes.

We can deal with this either by doing a pretax analysisand increasing our MARR to take account of the fact that some of our profits will go in tax

Or by doing an after-tax analysis, which is more work but more realistic.

In BC, ``small’’ means less than $400 000 taxable annual income

Province or territory Small bus. Higher rateNewfoundland and Labrador 4% 14%Nova Scotia 3.5% 16%Prince Edward Island 4.5% 16%New Brunswick 4.5% 12%Ontario 4.5% 11.5%Manitoba 0% 12%Saskatchewan 2% 12%British Columbia 2.5% 11%Yukon 4% 15%Northwest Territories 4% 11.5%Nunavut 4% 12%Alberta 3% 10%Quebec 8% 11.9%

Pre-TaxAnalysis

After-TaxAnalysis

After-Tax Analysis

Same as pre-tax analysis, except we use the after-tax MARR and adjust the cash flows to take account of the effects of taxation.

Taxation has two main effects:

Operating costs and incomes are affected by the tax rate (simple)

Capital costs are affected by the tax rate anddepreciation allowances (a bit complicated)

Details depend on the country we’re in.

Capital Cost Allowance

When a company buys a capital asset, it can’t deduct the cost of the purchase from its income.

But it can deduct the subsequent annual depreciationof the asset from its income.

The rules for how and how fast things depreciatevary from one country to another.

For an after-tax analysis, we reduce the initial cost ofa capital acquisition by the present value of the taxes saved by depreciating it.

The government groups all possible capital acquisitionsinto a small number of classes, and sets rules for howfast the assets in a given class can depreciate.

You begin each year with a certain amount in each assetclass – the `Undepreciated Capital Cost’, or `UCC’ – anddepreciate it by the Capital Cost Allowance, or `CCA’.

Algorithm for Calculating Deductions in a CCA Class

1. Start with the undepreciated capital cost UCCn-1

2. Subtract proceeds from assets sold during the year

3. Add 50% of the cost of asset additions

4. Carry forward the 50% balance from any assets added last year

5. Subtract government assistance payments or tax credits

6. Calculate the CCA for this asset class from the total at step 5:

CCA = UCCn-1 * d

7. UCCn = UCCn-1 - CCA

CCA Recapture

You buy an asset for $P. It is the only asset in its class, and it depreciates over n years. At the beginning of year n, its book value is UCC(n)

If we now sell it for $S, then:

1. If S < UCC(n), no tax is owed.

2. If P > S > UCC(n), you owe tax on S-UCC(n)

3. If S > P, you owe tax on P – UCC(n), and

S-P is a capital gain.

(Taxed at 50% of the corporate tax rate)

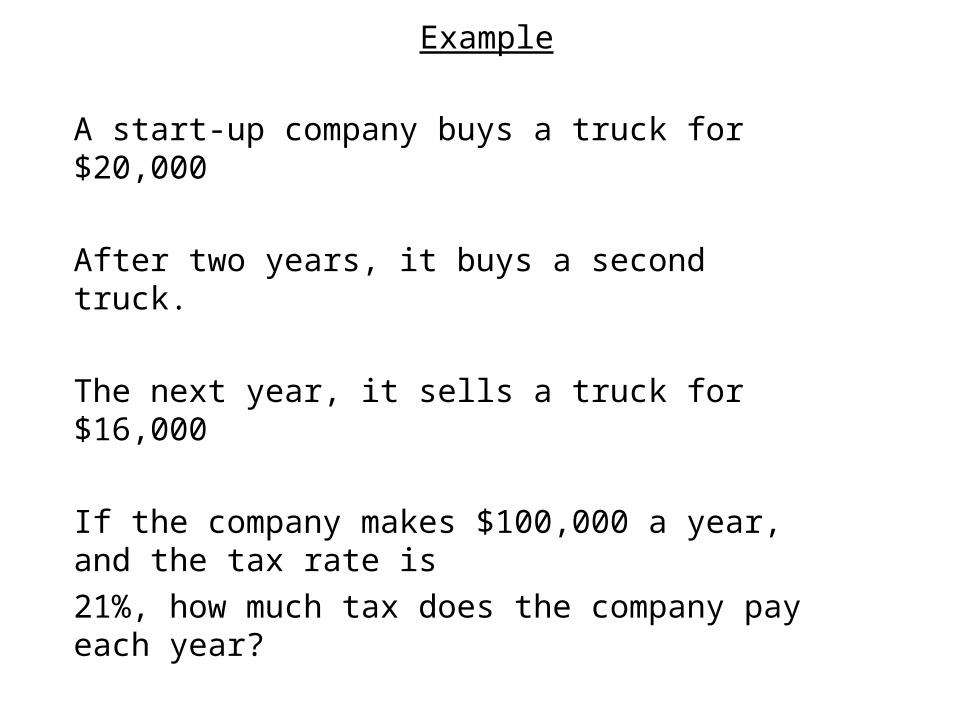

Example

A start-up company buys a truck for $20,000

After two years, it buys a second truck.

The next year, it sells a truck for $16,000

If the company makes $100,000 a year, and the tax rate is

21%, how much tax does the company pay each year?

(Trucks are in Asset Class 10, with a CCA rate of 30%)

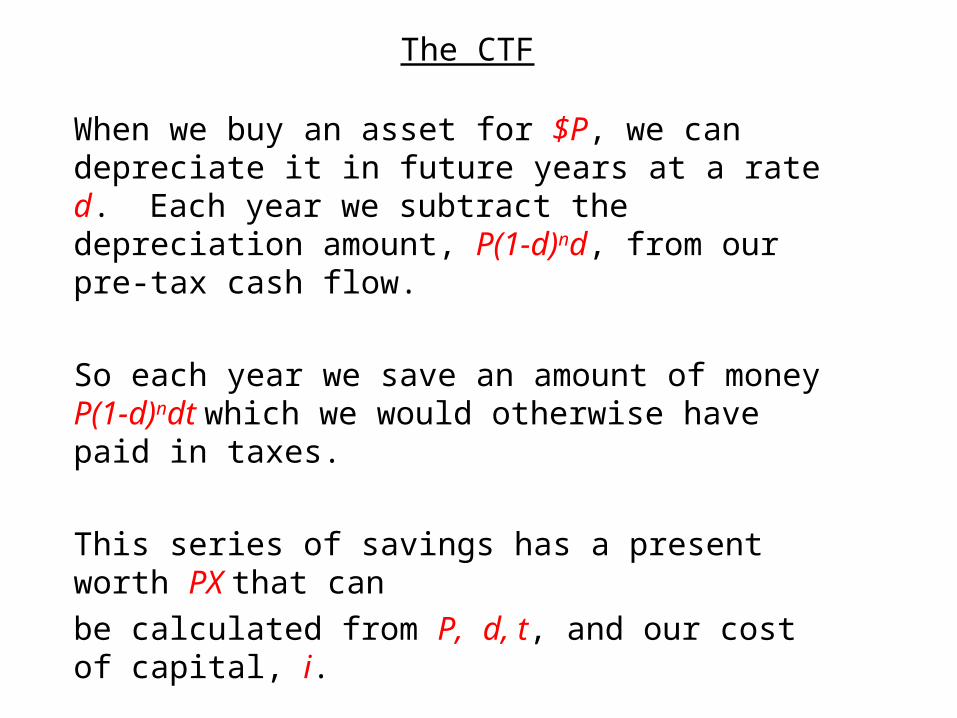

The CTF

When we buy an asset for $P, we can depreciate it in future years at a rate d. Each year we subtract the depreciation amount, P(1-d)nd, from our pre-tax cash flow.

So each year we save an amount of money P(1-d)ndt which we would otherwise have paid in taxes.

This series of savings has a present worth PX that can

be calculated from P, d, t, and our cost of capital, i.

So the effective present cost, in an after-tax analysis, is

P – PX, or P (1-X). The factor (1-X) is called the CTF

Suppose you are an engineer trying to persuadeyour boss to buy a spectrum analyser.

It will be easier to make the case for its purchaseif the CTF is

a)Higher (closer to 1)

b)Lower (closer to 0)

The CTF

If we ignore the first-year rule, the CTF is:

CTF = 1 – td/(i+d)

Including the first-year rule, the CTF is:

CTF = 1 -

(On no account should you memorise these.)

The CTF

As the tax rate, t, increases, does the CTF get bigger or smaller?

The CTF

As the tax rate, t, increases, does the CTF get bigger or smaller?

As depreciation, d, increases, does the CTF get bigger or smaller?

The CTF

As the tax rate, t, increases, does the CTF get bigger or smaller?

As depreciation, d, increases, does the CTF get bigger or smaller?

As the MARR, i, increases, does the CTF get bigger or smaller?

Possible confusion

The tax relief resulting from the depreciation of a capital assetreduces its effective purchase price by the amount P(1-CTF)

The tax relief resulting from the depreciation of a capital assetreduces its effective purchase price by the factor CTF