Embed Size (px)

Citation preview

Agents, Brokers and Navigators:Agents, Brokers and Navigators:Issues to Consider When Creating A Issues to Consider When Creating A

State-Based Health Insurance State-Based Health Insurance ExchangeExchange

Julian LagoPast FAHU President / Exchange liaison

National Association of Health Underwriters

The Starting Point

PPACA requires every state to have an exchange as a health insurance purchasing option for individual consumers and small employers.

Exchanges will be a purchasing portal for subsidized and unsubsidized qualified health plans, as well as an enrollment point for Medicaid, CHIP and other state public health assistance programs.

PPACA requires every exchange to have a Navigator program to facilitate health plan enrollment.

Agents and brokers are specifically listed by the law as one of the groups that may be Navigators, but the law also stipulates a compensation/financing method that conflicts with traditional agent compensation structures.

PPACA specifically provides for state health insurance exchanges to choose to utilize the services of agents and brokers beyond the navigator program to help exchange customers both with enrollment in qualified plans and also with the premium tax credits.

Existing laws in every state provide for licensed health insurance producers to sell and service all health plans offered in the state.

Issues to Address

• The use of agents and brokers in an exchange, both as navigators and/or through traditional means

• Funding of navigator program• Compensation of agents and brokers

and individuals performing navigator functions

• Regulation of navigators, agents and brokers

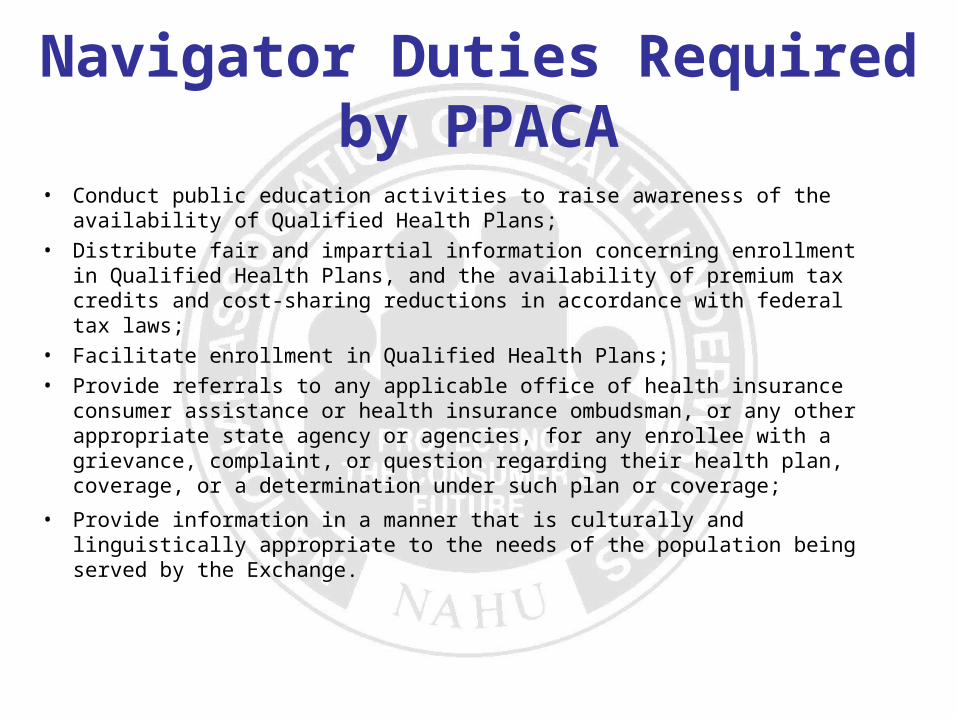

Navigator Duties Required by PPACA

• Conduct public education activities to raise awareness of the availability of Qualified Health Plans;

• Distribute fair and impartial information concerning enrollment in Qualified Health Plans, and the availability of premium tax credits and cost-sharing reductions in accordance with federal tax laws;

• Facilitate enrollment in Qualified Health Plans;• Provide referrals to any applicable office of health insurance

consumer assistance or health insurance ombudsman, or any other appropriate state agency or agencies, for any enrollee with a grievance, complaint, or question regarding their health plan, coverage, or a determination under such plan or coverage;

• Provide information in a manner that is culturally and linguistically appropriate to the needs of the population being served by the Exchange.

Precedent for Traditional Agent Involvement

•Utah Exchange•Massachusetts Connector•Existing State-Level Private Health Insurance Exchanges•Previous State-Level Purchasing Pool Experiments•State-Level High Risk Pools•State-Level Subsidy Programs•Long-Term Care Partnerships•Federal Preexisting Condition Insurance Plan

Licensure Issues To Address• Will navigators be individuals or entities?

– If entities, should that entity be appropriately licensed/regulated by the state?

• How will the state ensure legitimacy and accountability?• Should entities be responsible for the conduct of their

employees and/or volunteers? Or should these individuals be held personally accountable/licensed as well?

• What liability will navigators have?• How will potential complaints and/or grievances be

addressed?• How should individual performing navigator functions be

regulated and held accountable?– Producer Licensure?– Exchange-specific Certification?

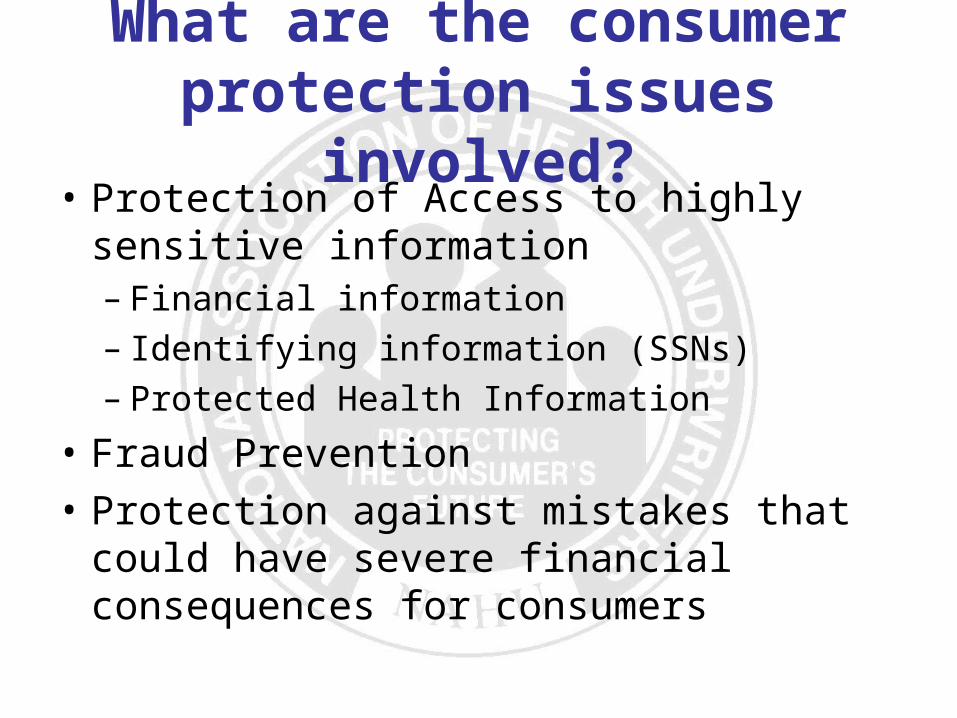

What are the consumer protection issues involved?

• Protection of Access to highly sensitive information– Financial information– Identifying information (SSNs)– Protected Health Information

• Fraud Prevention• Protection against mistakes that could

have severe financial consequences for consumers

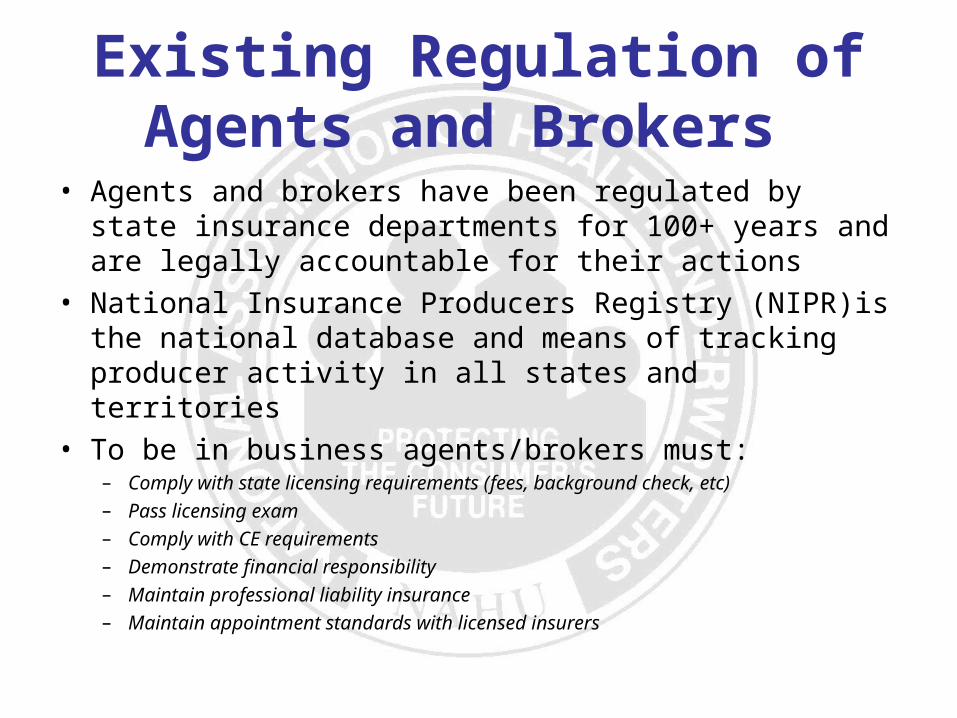

Existing Regulation of Agents and Brokers

• Agents and brokers have been regulated by state insurance departments for 100+ years and are legally accountable for their actions

• National Insurance Producers Registry (NIPR)is the national database and means of tracking producer activity in all states and territories

• To be in business agents/brokers must:– Comply with state licensing requirements (fees, background check, etc)– Pass licensing exam– Comply with CE requirements– Demonstrate financial responsibility– Maintain professional liability insurance– Maintain appointment standards with licensed insurers

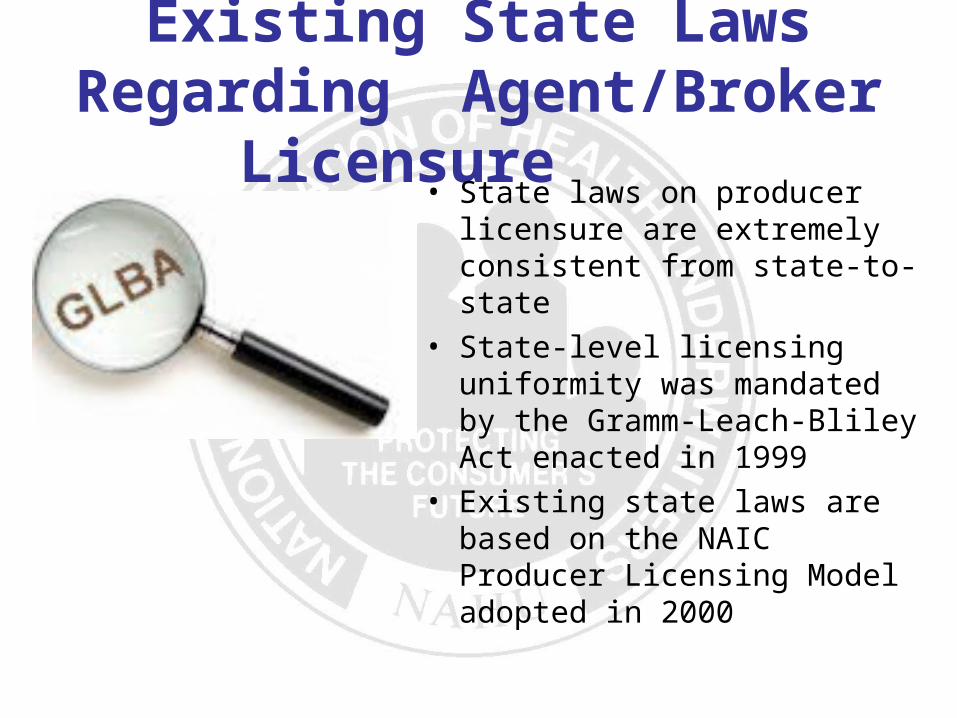

Existing State Laws Regarding Agent/Broker Licensure

• State laws on producer licensure are extremely consistent from state-to-state

• State-level licensing uniformity was mandated by the Gramm-Leach-Bliley Act enacted in 1999

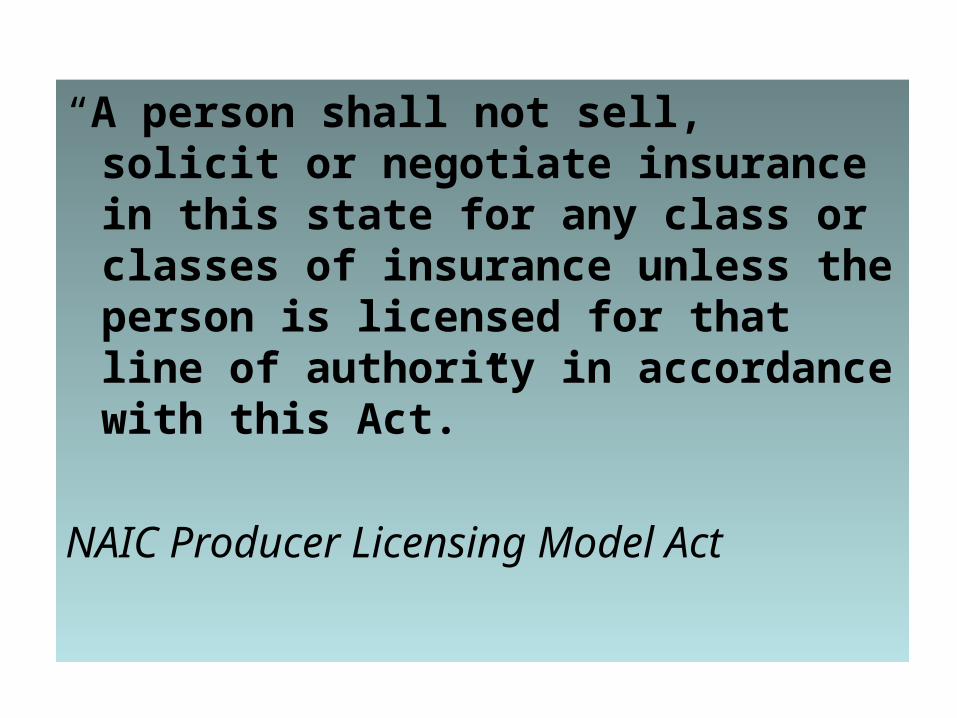

• Existing state laws are based on the NAIC Producer Licensing Model adopted in 2000

“A person shall not sell, solicit or negotiate insurance in this state for any class or classes of insurance unless the person is licensed for that line of authority in accordance with this Act.”

NAIC Producer Licensing Model Act

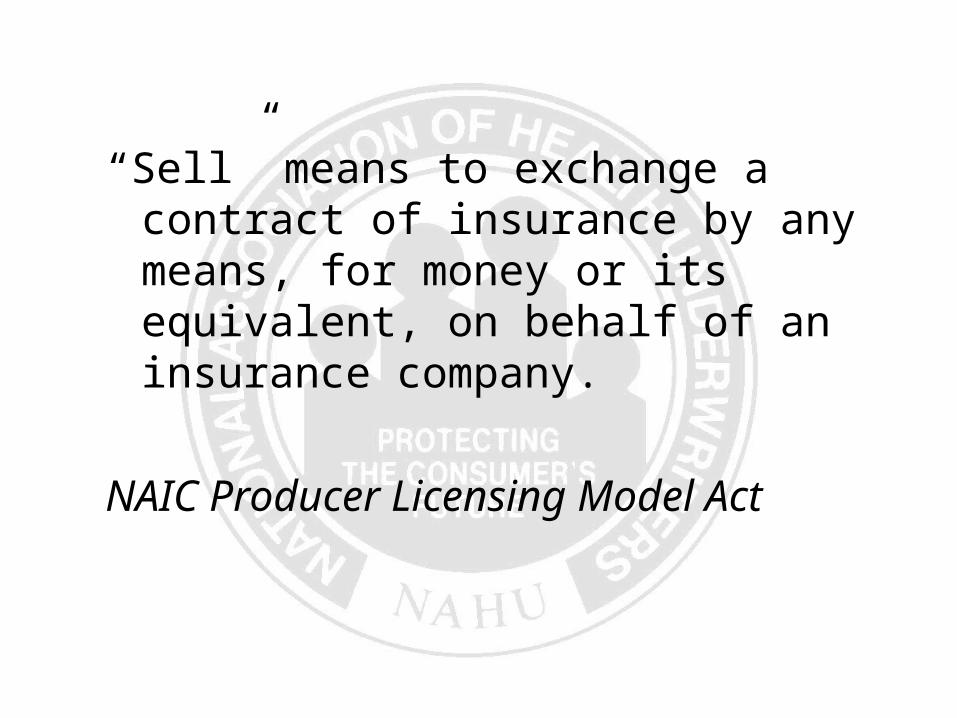

“Sell” means to exchange a contract of insurance by any means, for money or its equivalent, on behalf of an insurance company.

NAIC Producer Licensing Model Act

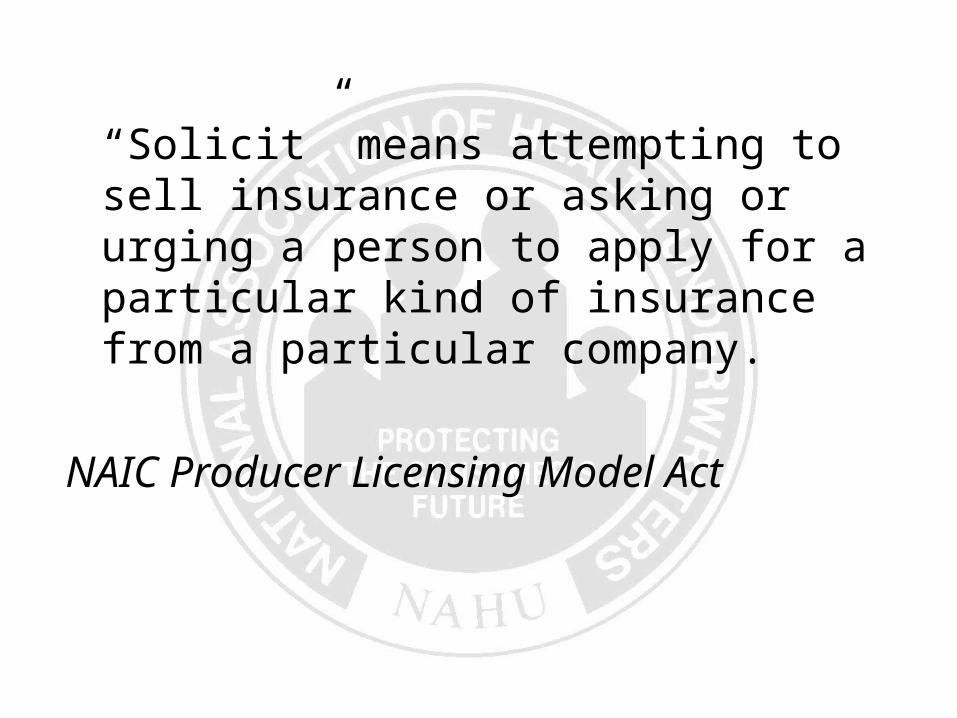

“Solicit” means attempting to sell insurance or asking or urging a person to apply for a particular kind of insurance from a particular company.

NAIC Producer Licensing Model Act

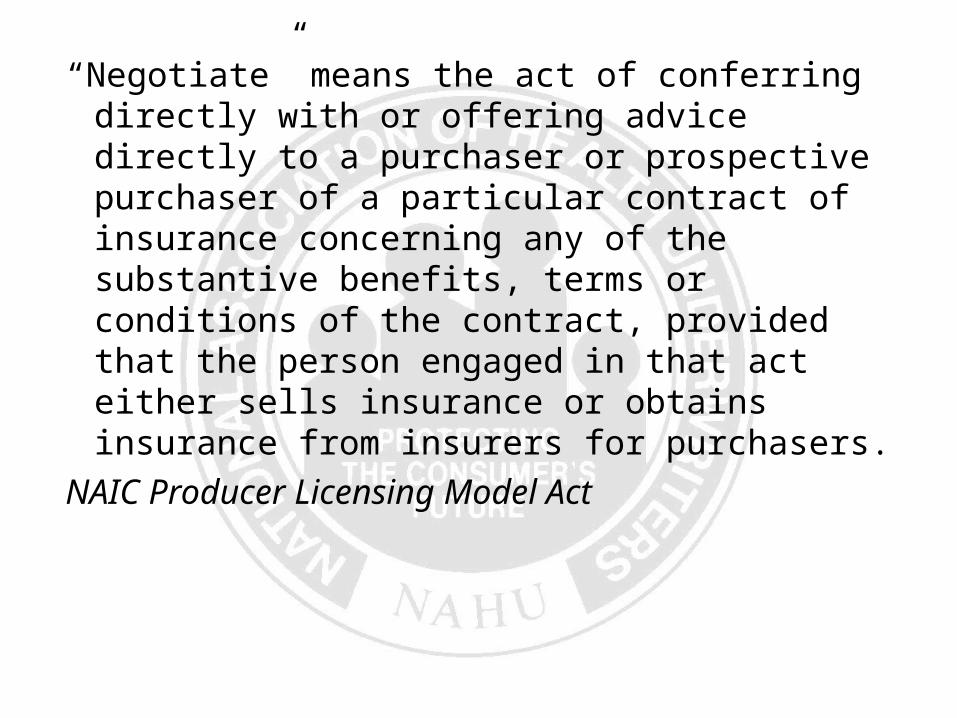

“Negotiate” means the act of conferring directly with or offering advice directly to a purchaser or prospective purchaser of a particular contract of insurance concerning any of the substantive benefits, terms or conditions of the contract, provided that the person engaged in that act either sells insurance or obtains insurance from insurers for purchasers.

NAIC Producer Licensing Model Act

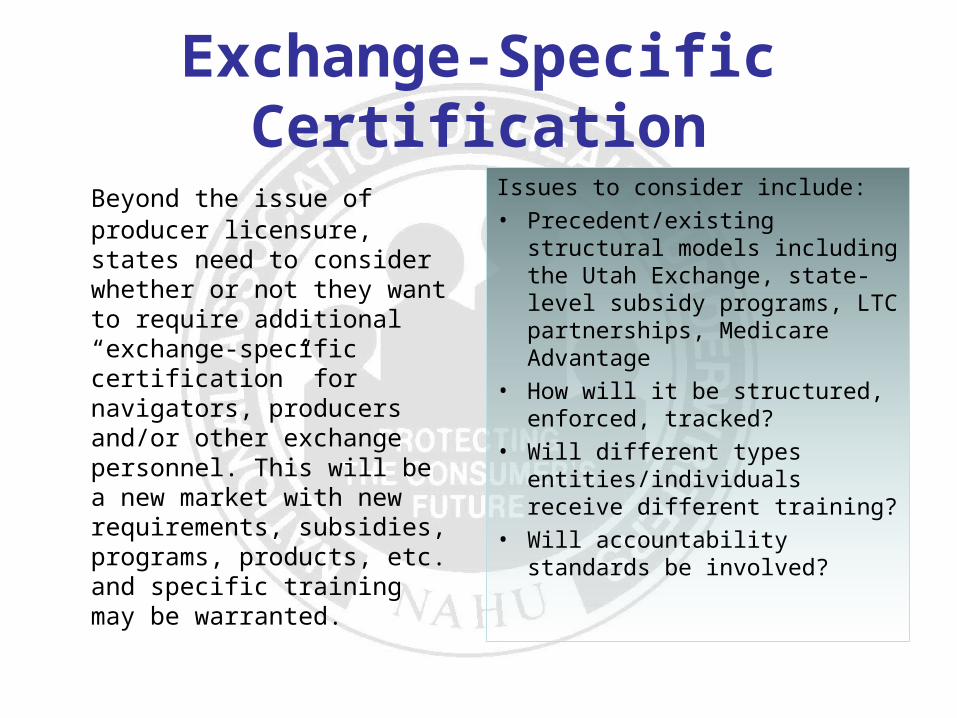

Exchange-Specific Certification

Beyond the issue of producer licensure, states need to consider whether or not they want to require additional “exchange-specific certification” for navigators, producers and/or other exchange personnel. This will be a new market with new requirements, subsidies, programs, products, etc. and specific training may be warranted.

Issues to consider include:• Precedent/existing

structural models including the Utah Exchange, state-level subsidy programs, LTC partnerships, Medicare Advantage

• How will it be structured, enforced, tracked?

• Will different types entities/individuals receive different training?

• Will accountability standards be involved?

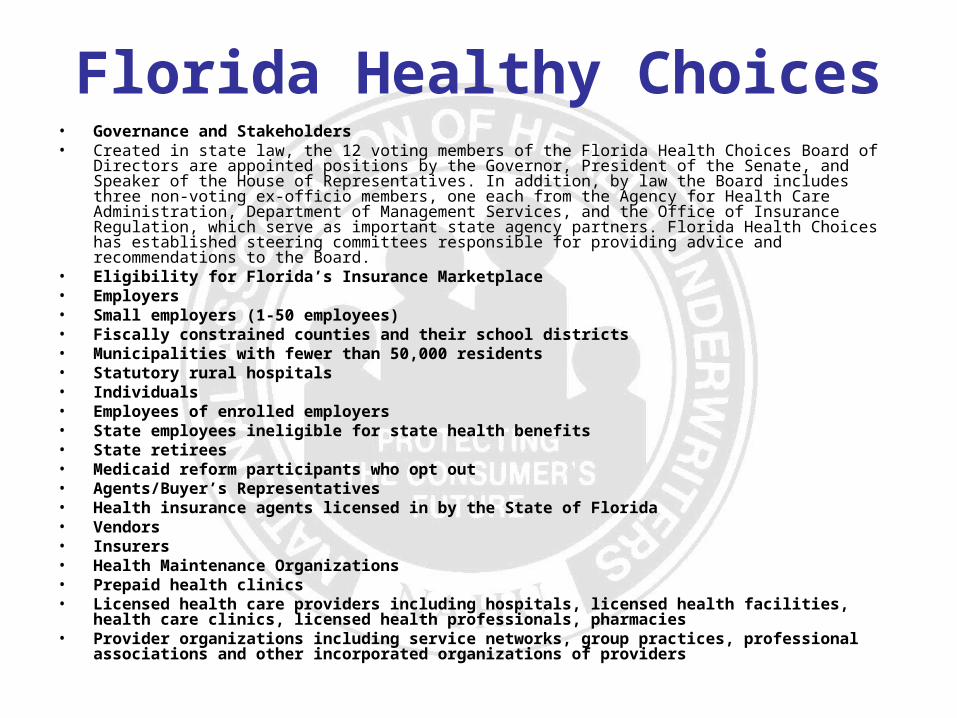

Florida Healthy Choices• Governance and Stakeholders• Created in state law, the 12 voting members of the Florida Health Choices Board of Directors are

appointed positions by the Governor, President of the Senate, and Speaker of the House of Representatives. In addition, by law the Board includes three non-voting ex-officio members, one each from the Agency for Health Care Administration, Department of Management Services, and the Office of Insurance Regulation, which serve as important state agency partners. Florida Health Choices has established steering committees responsible for providing advice and recommendations to the Board.

• Eligibility for Florida’s Insurance Marketplace• Employers• Small employers (1-50 employees) • Fiscally constrained counties and their school districts • Municipalities with fewer than 50,000 residents • Statutory rural hospitals• Individuals• Employees of enrolled employers • State employees ineligible for state health benefits • State retirees • Medicaid reform participants who opt out• Agents/Buyer’s Representatives• Health insurance agents licensed in by the State of Florida• Vendors• Insurers • Health Maintenance Organizations • Prepaid health clinics • Licensed health care providers including hospitals, licensed health facilities, health care

clinics, licensed health professionals, pharmacies • Provider organizations including service networks, group practices, professional

associations and other incorporated organizations of providers

• Florida’s Insurance Marketplace• Over an 18 month period, Florida’s Insurance Marketplace will be

launched in three distinct phases – Quick Start, Mid-term Phase, and Long-Term Phase. As the program progresses over time, the Marketplace will evolve and grow to include more vendors, products and web-based functionality.

• Currently, the major components of the Marketplace include:• Web-based portals specifically designed for employers,

employees and agents • Shop-and-compare functionality to facilitate choice • Online calculator to compute monthly costs • Ability to find an agent • Back-office product, service and financial support • Customer contact center located in St. Petersburg, Florida• Initially, Florida’s Insurance Marketplace will include health

insurance policies and health maintenance contracts. As the program matures, additional options will include:

• Limited benefit plans • Prepaid clinic services • Service contracts • Arrangements for specific amounts and types of health

services and treatment • Flexible spending accounts

• Funding• Start-up funding to design and launch the program was

provided by the State of Florida in the form of a one-time lump sum appropriation of $1.5 million. The Marketplace must become financially self-sustaining through the use of a minimal surcharge on the products it sells which cannot exceed 2.5 percent.

• How is Florida’s Insurance Marketplace different from an Insurance Exchange under National Health Care Reform?

• While both programs are web-based and allow for choice among available products and programs, there are some essential differences in how they work. For instance, participation in Florida’s Insurance Marketplace is purely voluntary for employers, employees and individual consumers. It was designed by the State of Florida to serve Florida’s unique insurance market, and it will connect consumers with the insurance agents and health benefit providers they are seeking. A wider range of service providers, insurance options, benefit levels, and a greater number of consumer choices are planned for Florida’s Insurance Marketplace.

Exchange Developments• New Proposed Rules Released will Impact ExchangesAugust 15th the administration released three proposed rules:

1. Exchange eligibility and employer standards (HHS)2. Medicaid eligibility increase and the proposed enrollment system (HHS)3. Guidance on premium subsidies for coverage accessed through the exchange (IRS)

NAHU Staff and Exchange Working Group continues to analyze all recent regulationsQuestions remain surrounding the foundation of a federal fall-back exchange

• HHS launches Exchange Listening TourKick-off regional exchange listening session took place on Aug. 23 in Portland, ORAdditional listening sessions scheduled for Atlanta, Chicago, Denver, New York and Sacramento over the coming weeks

• State Exchange Activity Remains Busy

• Scoreboard:Signed-13 (CA, CO, CT, HI, IL, MD, ND, NV, OR, VA, VT, WA, WVOn Hold-9 (DC, ME, MN, NE, NC, NH, NY, PA, TX)Dead/Vetoed-11 (AK, AZ, AR, IN, MO, MT, NE, NM, OK, RI, SC)Work Arounds-8 (AL, GA, IN, IA, KS, MS, OH, WI)

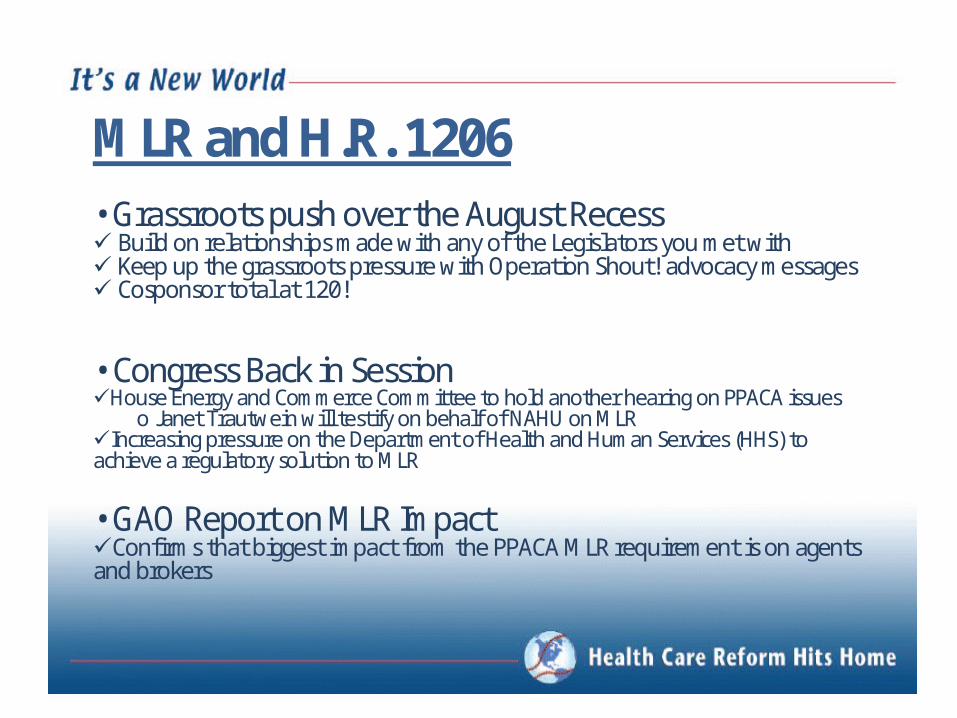

MLR and H.R. 1206• Grassroots push over the August Recess Build on relationships made with any of the Legislators you met with Keep up the grassroots pressure with Operation Shout! advocacy messages Cosponsor total at 120!

• Congress Back in SessionHouse Energy and Commerce Committee to hold another hearing on PPACA issues

o Janet Trautwein will testify on behalf of NAHU on MLRIncreasing pressure on the Department of Health and Human Services (HHS) to achieve a regulatory solution to MLR

• GAO Report on MLR ImpactConfirms that biggest impact from the PPACA MLR requirement is on agents and brokers

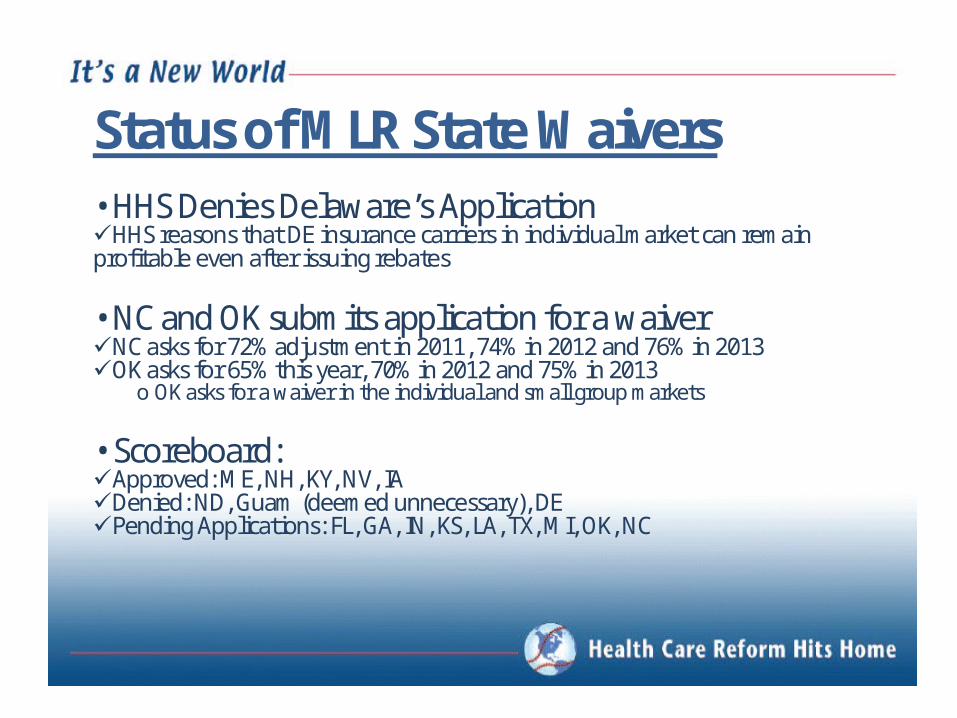

Status of MLR State Waivers• HHS Denies Delaware’s ApplicationHHS reasons that DE insurance carriers in individual market can remain profitable even after issuing rebates

• NC and OK submits application for a waiverNC asks for 72% adjustment in 2011, 74% in 2012 and 76% in 2013OK asks for 65% this year, 70% in 2012 and 75% in 2013

o OK asks for a waiver in the individual and small group markets

• Scoreboard:Approved: ME, NH, KY, NV, IADenied: ND, Guam (deemed unnecessary), DEPending Applications: FL, GA, IN, KS, LA, TX, MI, OK, NC

• HHS Tells States: Come “Partner” With Us on Exchanges

• The Department of Health and Human Services (HHS) released details yesterday as to how it plans to “partner” with states on exchange development. Called the Affordable Insurance Exchange “Partnership Options” Opportunities initiative, the administration’s plan is that it will give states new choices to consider as they plan their exchanges for 2014. HHS believes that while some states may choose to fully operate their own exchange, others might wish to perform some functions and let the federal government perform others for them.

For More Information

Julian E. LagoPlastridge Agency

Palm Beach Gardens FL561-630-4955