Embed Size (px)

Citation preview

ANNUAL REPORT 2014

The brands displayed throughout our 2014 annual report are some of the well know consumer and industrial brands marketed by our various subsidiaries.

Registered Offi ce: 18 Victoria Avenue,

P.O. Box 191, Port of Spain, Trinidad, West Indies

Phone: (868) 623-4871Fax: (868) 623-1966

www.agostinislimited.com

ANNUAL REPORT 2014

Agostini Cover 3.indd 1 12/11/14 1:04 PM

1AnnuAl RepoRt 2014

Agostini Interiors Lighting

2 Agostini’s LiMited

Contents

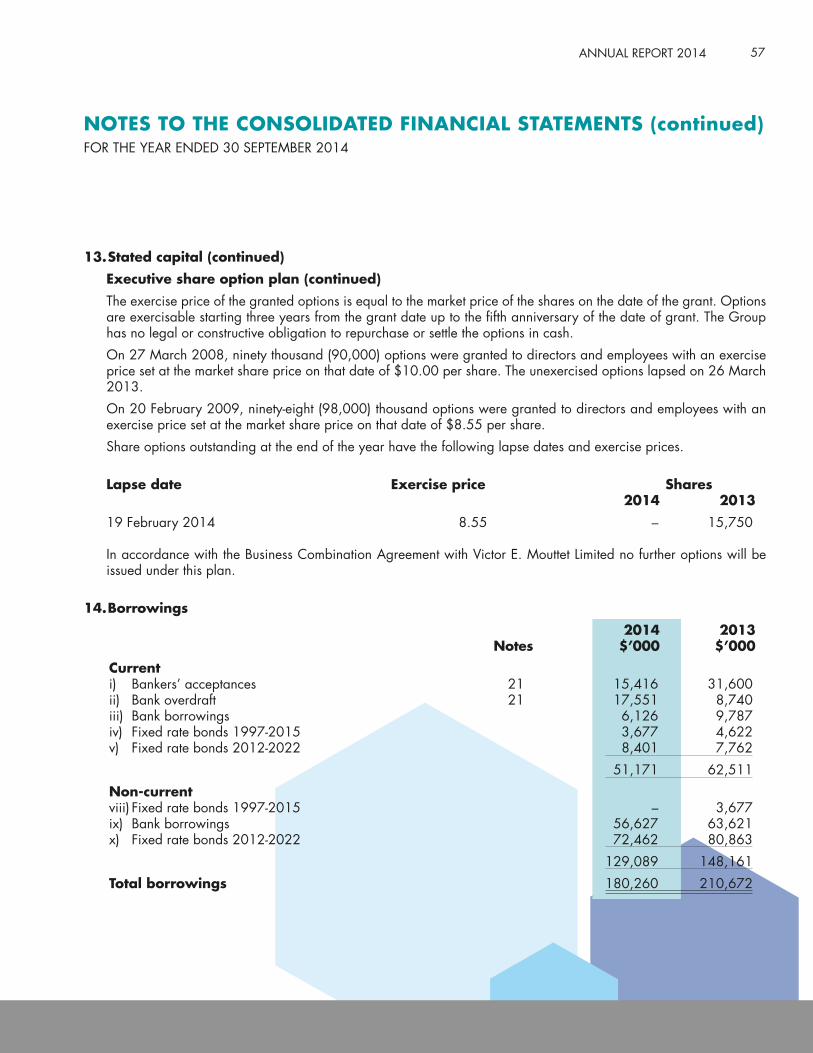

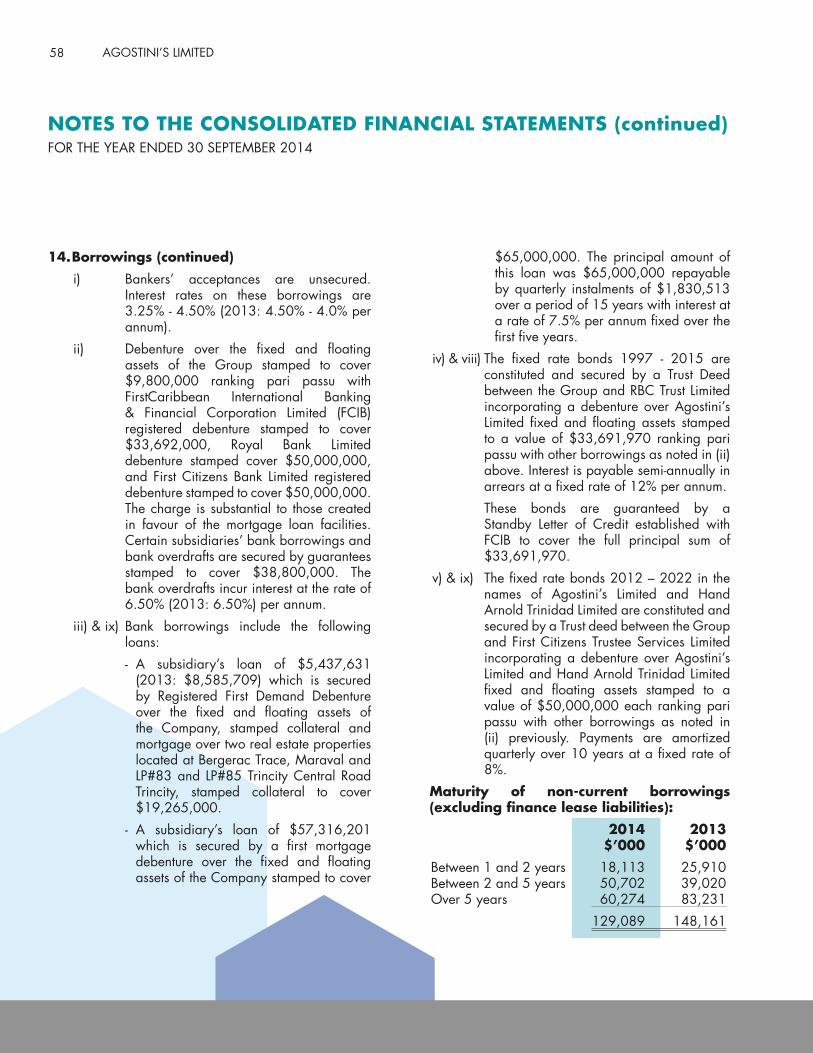

Notice of Meeting 3

History of the Agostini’s Limited Group 4

Subsidiaries 6

Board of Directors 8

Corporate Governance 10

Chairman’s Remarks 14

Management Discussion & Analysis 16

Report of the Directors 22

Independent Auditor’s Report 23

Consolidated Statement of Financial Position 24

Consolidated Income Statement 26

Consolidated Statement of Comprehensive Income 27

Consolidated Statement of Changes In Equity 28

Consolidated Statement of Cash Flows 29

Notes to the Consolidated Financial Statements 30

Directors’ & Senior Officers’ Interest & 11 Largest Shareholders 67

Our Group’s Products:

SuperPharm Limited 68

Smith Robertson & Company Limited 69

Hand Arnold Trinidad Limited 70

Agostini Marketing 72

Rosco Petroavance Limited 75

Company of the Year 78

Proxy Form 79

Management Proxy Circular 80

Corporate Information Inside back cover

All figures in this report are quoted in TT$. The exchange rate was US$1.00=TT$6.3733 as at 30 September 2014.

Novartis Consumer Health

3AnnuAl RepoRt 2014

notiCe of meeting

Notice is hereby given that the Seventy-First Annual Shareholders’ Meeting of Agostini’s Limited will be held at the Marriott Hotel, Invaders Bay, Port of Spain on Monday, January 26, 2015 at 9:30 a.m. for the following purposes:

1. To receive and consider the Group’s Financial Statements for the year ended September 30, 2014 and the Reports of the Directors and Auditors thereon.

2. To re-elect the following Director retiring by rotation:

Ms. Amalia Maharaj

3. To appoint Auditors and to authorise the Directors to fix their remuneration.

4. To transact any other ordinary business of the Company.

By Order of the Board

R. Rajkumarsingh

Secretary

December 8, 2014

Documents available for inspection

No Service Contracts have been entered into between the Company and any of the Directors.

Vitamin C from Bayer

Pain Management from GSK

4 Agostini’s LiMited

4 Annual Report 2013

History of tHe Agostini’s Limited group

1925

19331943

19501965

19701982

19841986

1993

Hilti W.L. Yearwood is acquired, later to become Agostini’s Fastening Systems (now a division of Agostini Marketing).

Agostini Industries Limited is established to manufacture diapers and feminine napkins (assets divested in 2004).

Gordon Grant Trading, a distribution company specialising in pharmaceutical distribution, is acquired. Agostini Marketing’s pharmaceutical lines are merged into this company, which is renamed Agostini Pharmaceutical Limited.

Agostini’s acquires a majority shareholding in Rosco Sales Limited, an oilfield supply company founded in 1950.

1995 The Group expands into low-cost housing and townhouse construction, and constructs 30 townhouses and over 300 low-cost single family homes (assets divested in 2010).

20002007

20082010

2011 2012

Petroavance Trinidad Limited, an oilfield supply company, is acquired and merged with Rosco Sales to become Rosco Petroavance Limited.

Agostini’s acquires a majority interest in Mobern Lighting in Maryland, USA, as a sister operation to Agos Manufacturing (assets divested in 2010).

Hand Arnold Trinidad Limited, a large diversified consumer products distributor established in 1920, is acquired.

Victor E. Mouttet Limited acquires a controlling interest in Agostini’s Limited with its sale of Smith Robertson & Co. Limited, a major pharmaceutical distributor founded in 1894, and the acquisition of SuperPharm Limited, a major retail pharmacy chain, which began operations in 2005.

In July 2011, Agostini Pharmaceutical is amalgamated into Smith Robertson & Company Limited.

Agostini’s Limited re-branded “Every Business a Benchmark”

Johnnie Agostini begins operations as a commission indent business.

Agostini Brothers changes its name to Agostini’s Limited and becomes a public company listed on the Trinidad and Tobago Stock Exchange.

Victor Agostini joins and Agostini Brothers partnership is formed. In 1941 another brother, Frank, joins the Firm.

Agostini Brothers transitions from a commission indent business to a distribution company with the addition of major pharmaceutical, food and hardware products.

Agos Manufacturing established to manufacture fluorescent light fixtures and incandescent light bulbs (assets divested in 2009).

H istor y of the Agost in i ’s L imited Group

Agostini Brothers becomes a limited liability company.

Interior contracting services are added as a new business.

5AnnuAl RepoRt 2014

5

Luxury Tissue Products

1925

19331943

19501965

19701982

19841986

1993

Hilti W.L. Yearwood is acquired, later to become Agostini’s Fastening Systems (now a division of Agostini Marketing).

Agostini Industries Limited is established to manufacture diapers and feminine napkins (assets divested in 2004).

Gordon Grant Trading, a distribution company specialising in pharmaceutical distribution, is acquired. Agostini Marketing’s pharmaceutical lines are merged into this company, which is renamed Agostini Pharmaceutical Limited.

Agostini’s acquires a majority shareholding in Rosco Sales Limited, an oilfield supply company founded in 1950.

1995 The Group expands into low-cost housing and townhouse construction, and constructs 30 townhouses and over 300 low-cost single family homes (assets divested in 2010).

20002007

20082010

2011 2012

Petroavance Trinidad Limited, an oilfield supply company, is acquired and merged with Rosco Sales to become Rosco Petroavance Limited.

Agostini’s acquires a majority interest in Mobern Lighting in Maryland, USA, as a sister operation to Agos Manufacturing (assets divested in 2010).

Hand Arnold Trinidad Limited, a large diversified consumer products distributor established in 1920, is acquired.

Victor E. Mouttet Limited acquires a controlling interest in Agostini’s Limited with its sale of Smith Robertson & Co. Limited, a major pharmaceutical distributor founded in 1894, and the acquisition of SuperPharm Limited, a major retail pharmacy chain, which began operations in 2005.

In July 2011, Agostini Pharmaceutical is amalgamated into Smith Robertson & Company Limited.

Agostini’s Limited re-branded “Every Business a Benchmark”

Johnnie Agostini begins operations as a commission indent business.

Agostini Brothers changes its name to Agostini’s Limited and becomes a public company listed on the Trinidad and Tobago Stock Exchange.

Victor Agostini joins and Agostini Brothers partnership is formed. In 1941 another brother, Frank, joins the Firm.

Agostini Brothers transitions from a commission indent business to a distribution company with the addition of major pharmaceutical, food and hardware products.

Agos Manufacturing established to manufacture fluorescent light fixtures and incandescent light bulbs (assets divested in 2009).

H istor y of the Agost in i ’s L imited Group

Agostini Brothers becomes a limited liability company.

Interior contracting services are added as a new business.

Hand Arnold’s Double Duty Household Range

6 Agostini’s LiMited

subsidiAries

A.J. Agostini - Chairman

A.B. Pashley - CEO / Director

C.G. Bernard - Director

R.A. Rodriguez - Director

G.M. Agostini - Non-Exec Director

T.K. Austin - Non-Exec Director

R.A. Farah - Non-Exec Director

A.J. Agostini - Chairman

S.A. Gunness-Balkissoon - CEO/ Director

S.K. Malzar - Finance Director/ Company Secretary

S.J. Montano - Director

L.M. Mackenzie - Non-Exec Director

Suppliers of building materials, interior

contracting services, medical and printing

supplies

Distributors of grocery, food and beverage

products.

100% owned

100% owned

Richport Food Range- Keeping you healthy

Progress Growing Up Milk from Aspen

Cheekies Diapers

7AnnuAl RepoRt 2014

C.E.Mouttet - Chairman

G. Maharaj - Managing Director

S.T.Pariag - Director

J.M.Aboud - Non-Exec Director

L.M.Mackenzie - Non-Exec Director

J.J.Rahael - Non-Exec Director

M. Gonsalves Suite - Company Secretary

A.J. Agostini - Chairman

Walter Bernard - Deputy Chairman

Wayne Bernard - CEO/Director

J.P. Rostant - Director

C.G. Bernard - Non-Exec Director

R.A. Rodriguez - Non-Exec Director

V.Balroop - Company Secretary

C.E. Mouttet - Chairman

R.A. Farah - CEO/Director

I. Maharaj - Director

M. Stagg - Director

N.R. Ramjohn - Finance Director / Secretary

A.J. Agostini - Non-Exec Director

Retail pharmacy and convenience store

Suppliers of industrial, hydraulic and oilfield products and services.

Distributors of pharmaceutical

and personal care products

100% owned

92% owned

100% owned

Vitamins and Minerals from Pfizer

8 Agostini’s LiMited

Non-Executive DirectorCEO / Director of Victor E. Mouttet LtdChairman of Prestige Holdings Ltd Director since 2010Chairman of the Corporate Governance and Nomination Committee and Member of the Human Resources & Compensation Committee

Non-Executive Director CEO/Director of Smith Robertson & Company LtdDirector of Vemco LtdDirector since 2010

Managing Director of Agostini’s LtdDirector of Caribbean Finance Company LtdDirector since 1990

Chairman of Agostini’s LtdDirector of Prestige Holdings Ltd, Grace Kennedy Ltd and Arthur Lok Jack Graduate School of BusinessDirector since 2004Member of the Human Resources & Compensation Committee and Corporate Governance and Nomination Committee

Non-Executive Independent DirectorPartner of Pollonais, Blanc, De la Bastide & JacelonDirector of Heroes FoundationDirector since 2011Member of the Audit & Risk Committee

boArd of direCtors

JOSEPH ESAU

ANTHONY J. AGOSTINI

ROGER A. FARAH

AMALIA L. MAHARAJ

CHRISTIAN E. MOUTTET

9AnnuAl RepoRt 2014

Non-Executive Independent DirectorManagement ConsultantDirector since 2009Member of the Human Resources & Compensation Committee and Audit & Risk Committee

Non-Executive Independent DirectorCEO of Cerca TechnologyDirector/Owner of Secret Bay (Dominica)Executive Chairman of Fort Young Hotel (Dominica)President of the Dominica Hotel & Tourism AssociationDirector since 2012

Chief Financial Officer & Company Secretary of Agostini’s LtdDirector of First Citizens Holdings Ltd.Company Secretary since 2014

Non-Executive Independent DirectorFinancial Controller of Atlantic LNG Company of Trinidad & TobagoDirector since 2007Chairman of the Audit & Risk Committee and Member of the Corporate Governance and Nomination Committee

Non-Executive DirectorFinance Director of Access and Security Solutions Ltd.Director of Scotiabank Trinidad & Tobago Ltd and Scotialife Trinidad & Tobago LtdDirector since 2004

Non-Executive Director Chairman of Caribbean Finance Company Ltd Director of Southern Sales & Service Co Ltd and Best Auto Ltd.Director since 1996Committees: Chairman of Human Resources & Compensation Committee

LISA M. MACKENzIE

GREGORNASSIEF

RAJESH RAJKUMARSINGH

REYAz W. AHAMAD

E. GILLIAN WARNER-HUDSON

BARRY A. DAVIS

10 Agostini’s LiMited

CorporAte governAnCe

boArd reportThe Board of the Company had four quarterly board meetings and a strategic review / planning and budget meeting.

The average number of attendees at board meetings were 9.5 out of 10 members.

boArd Committees & mAndAtes Corporate Governance & Nomination Committee

The Committee makes appropriate recommendations to the Board and its scope includes the following:

• Tomonitorbestpracticesforgovernanceworldwideand review the Company’s governance practices to ensure they continue to exemplify appropriately high standards of corporate governance.

• To recommend to theBoard for considerationandadoption:

- The membership and mandates of Board Committees.

- The size and composition of the Board.

- Suitable candidates for nomination as Non- Executive Directors.

- Appointments to the Boards of Subsidiary, Affiliate and Associate Companies.

- The communication process between the Board and Management.

- Approval of the appointments of Executives to the Boards of companies outside the Agostini’s Limited Group.

• To establish/review policies and procedures withrespect to transactions between the Company, its subsidiaries and affiliates and Related Parties, Executive Officers and Directors.

• TomonitortheCompany’sCodeofConduct.

• To review themandatesandcompositionofBoardCommittees annually.

• To review the performance of the Board and theDirectors annually.

• To establish/monitor an appropriate proceduregoverning the trading in the Company’s securities by Directors and Officers.

This Committee met twice during the year and in addition, conducted an evaluation of the Board and individual members. This process involved a methodical feedback from, and meetings with, individual Directors, and was carried out by a sub-committee comprised of the Chairs of the Board and of the Corporate Governance & Nomination Committee, with the other member of the Committee comprising the two member panel as required.

Corporate Governance & Nomination Committee

Christian Mouttet (Chairman)Joseph EsauBarry Davis

Lea & Perrins - the original Worcestershire Sauce

Deworming from GSK

11AnnuAl RepoRt 2014

The Company is in compliance with the Trinidad & Tobago Corporate Governance Code.

Audit & Risk Committee

This Committee’s duties include:

Financial Reporting

To review, and challenge where necessary, the actions and judgements of Management, in relation to the Company’s financial statements, operating and financial review, interim reports, preliminary announcements and related formal statements before submission to, and approval by, the Board, and before clearance by auditors. Its scope covers:

• Critical accounting policies and practices, theconsistency of their application and any changes in them.

• Decisions requiring a significant element ofjudgement.

• The extent to which the financial statements areaffected by any unusual transactions in the year and how they are disclosed.

• Theclarityofdisclosures.

• Significantadjustmentsresultingfromtheaudit.

• Thegoingconcernassumption.

• Compliancewithaccountingstandards.

• Compliance with stock exchange and other legalrequirements.

• Thereviewoftheannualfinancialstatementsofthepension funds and tri-annual actuarial valuations.

Internal Audit

• Monitoring and reviewing the effectiveness of theCompany’s Internal Audit function in the context of the Company’s overall risk management system.

• Approving theappointmentof theheadof internalaudit.

• The scope and rescourcing of the internal auditfunction and ensuring it has adequate resources and appropriate access to information to enable it to perform its function effectively and in accordance with the relevant professional standards.

• Reviewingandassessing theannual internal auditplan.

• Reviewingallinternalauditreports.

• Reviewing and monitoring management’sresponsiveness to the findings and recommendations of the internal auditor.

External Audit

• Overseeing the Company’s relations with theexternal auditor.

• Recommending to the Board the appointment,reappointment and removal of the external auditor.

• Approving the terms of engagement and theremuneration of the external auditor.

• Assessingthequalification,expertiseandresources,effectiveness and independence of the external auditors annually.

Whiskas and Fresh Step Cat Products

Ozon - the Power of Clean

12 Agostini’s LiMited

• Reviewingandmonitoringthecontentoftheexternalauditor’s management letter and the responsiveness thereto.

• Developing for the Board’s consideration theCompany’s policy in relation to the provision of non-audit services by the auditor and ensuring that the provision of such services does not impair the external auditor’s independence or objectivity.

Internal Control

• Reviewing the effectiveness of the Company’sprocedures for whistleblowing and for detecting fraud;

• Reviewingmanagement’sreportsoftheeffectivenessof the systems for internal financial control and financial reporting;

• Monitoring the integrity of theCompany’s internalfinancial controls;

• Assessingtheeffectivenessofthesystemsestablishedby Management to identify, manage and monitor both financial and non financial risks.

Risk

• Consideringanymattersrelatingtotheidentification,assessment, monitoring and management of risks associated with the operations of the Group.

• Compliance by the Group with its Risk AppetiteStatement.

• ReportingtotheBoardonanymaterialchangestothe risk profile of the Group.

• Monitoring any instances involving materialbreaches or potential breaches of the Group’s Risk Appetite Statement.

• Reviewing the annual insurance coverage andensuring all insurable risks are adequately covered.

The Audit & Risk Committee met four times during the year.

Audit & Risk Committee

Barry Davis (Chairman)Gillian Warner Hudson

Amalia Maharaj

Human Resources & Compensation Committee

This Committee is responsible for all matters relating to the compensation policies of the Group. It reviews, approves or recommends to the Board of Directors suitable Compensation Policies, the compensation structure and programmes.

The Committee’s primary responsibilities include the following:

• The review and recommendation to the Board ofDirectors, for adoption, of all Human Resource and Compensation Policies of the Agostini’s Limited Group.

• The review and recommendation to the Board ofDirectors, for adoption, the compensation structure and incentive programmes for the Group Managing Director and other Executives.

• Proposing, within the guidelines set out in theCompany’s compensation structure, for approval of the Board, annual bonus and other incentive-based awards, to Executives and other qualifying employees.

• Reviewing the compensation paid to Non-Executive Directors and recommending appropriate adjustments from time to time.

• Reviewingandapprovingmanagement successionplans for Executive Officers.

• Review with the Group Managing Director andrecommend to the Board, appointments of senior management positions throughout the Agostini’s Limited Group.

• Monitoringcompliancewith theExecutiveMedicalExamination Policy and process.

This Committee met once during the year.

Human Resources & Compensation Committee

Reyaz Ahamad (Chairman)Joseph Esau

Christian MouttetGillian Warner-Hudson

13AnnuAl RepoRt 2014

Hershey’s Chocolates ... make every special moment even sweeter

With a name like Smuckers it has to be good

Harbison Fischer sucker rods

14 Agostini’s LiMited

CHAirmAn’s remArksConsoLidAted resuLts And finAnCiAL positionGroup sales and profit for the year ended September 30, 2014, attributable to shareholders, amounted to $ 1.36 billion and $ 79.9 million, compared with $1.31 billion and $61.9 million in the previous year, respectively. Earnings per share was $1.36 compared with $1.06 in 2013, an improvement of 28% over prior year.

The Group ended the year with an improved debt to equity ratio of 21:79 compared with 27:73 in 2013, a strong financial position, which will facilitate expansion of the activities.

operAtions revieW And segment AnALysisPharmaceutical & Personal Care Distribution

Smith Robertson, our Pharmaceutical and Personal Care distribution Company, produced record results, and continues to be a significant contributor to the Group’s performance.

SuperPharm, with seven locations in full operation during the year, and an eighth unit recently opened in Diego Martin, showed good growth in sales and profitability, and is well placed to continue its expansion drive and improved profitability.

JOSEPH ESAU

It has to be Heinz.

0

5

10

15

20

2010 2011 2012 2013 2014Year

$9.80

$12.57

$15.37

$17.60 $17.25

sHAre priCe At yeAr end(tt$)

15AnnuAl RepoRt 2014

Food, Construction & Other Trading

Hand Arnold, our food and grocery product distribution business, had a good year, with many of our key product lines experiencing double digit growth.

Agostini Marketing, our building products and services business, did not perform to expectations, as the construction environment remained difficult throughout the year. With new contracts already in place for the current year, we expect this division to show improved results in the coming year.

Rosco Petroavance, our oilfield, industrial and hydraulic products business, performed reasonably well in an environment where oil prices were under pressure in the latter part of the financial year, causing a slowdown in projects and purchases from several of our customers.

outLookThe Group is at an advanced stage of investment negotiations which we expect to be announce over the coming months. These, together with our existing operations which are performing well, will facilitate continued growth, and we expect improved results in 2015.

dividendsYour Board has approved a final dividend of 33 cents per share. This brings the total dividend for the year to 55 cents compared with 46 cents in 2013. This dividend will be paid on February 2, 2015 to shareholders whose names appear on the register of members on January 7, 2015. The Company’s register of members will be closed on January 8 and 9, 2015.

subseQuent eventOn October 2, 2014, Agostini’s Limited refinanced its debt portfolio, with Scotiabank Trinidad & Tobago Limited. This new financing of $275 million comprised of $170 million seven (7) year fixed rate facility and $105 million in working capital facilities. This refinancing is expected to reduce the Group’s borrowing costs in 2015, by approximately $5 million.

ACknoWLedgementsWe thank our employees for their hard work and dedication over the past year. We are also grateful to our many customers and suppliers that continue to support us, and I thank my fellow Directors for their guidance and committed service.

Joseph P. Esau

Chairman

November 24, 2014Made from fresh, never from powder.

0

10

20

30

40

50

60

20

4244

46

55

Year2010 2011 2012 2013 2014

dividends per sHAre(tt¢)

16 Agostini’s LiMited

mAnAgement disCussion And AnALysis

The financial year 2014 was a successful one for most of our subsidiaries. After 3 years of relatively flat results, our investment in owned brands and technology, as well as our focus on product rationalisation, cost control and strengthening of the Company’s balance sheet, have started to benefit the Group’s operating profit.

Sales grew by 3.5%, while earnings per share increased 28%. The Group generated $80 million in cash from operating activities, of which $23 million was reinvested in the business, $23 million was used to repay debt and $28 million was returned to shareholders through dividends.

Management has worked extensively this past year to create opportunities for growth and diversification, and we look forward to sharing these with you as they come to fruition in the coming months.

ANTHONYAGOSTINI

Glad. Bag it. Store it.

0

300

600

900

1200

1500

857

1,256 1,294 1,3131,359

Year2010 2011 2012 2013 2014

turnover (tt$ miLLion)

0

2

4

6

8

10

12

14

16

6.75%

15.24%14.56%

12.63%

14.5%

Year2010 2011 2012 2013 2014

return on eQuity (%)

17AnnuAl RepoRt 2014

Clorox - Cleaner World, Healthier Lives

finAnCiAL HigHLigHts Restated 2014 2013 % Increase $’000 $’000 Gross Sales 1,410,639 1,363,011 3.49 Sales to Third Parties 1,359,383 1,312,703 3.56 Operating Profit 123,696 103,767 19.21 Profit before Tax 107,145 87,156 22.93 Profit for the Year 80,546 62,580 28.71 Profit attributable to Shareholders 79,932 61,946 29.03 Stock Units In Issue (‘000) 58,704 58,704 - Earnings per Share $1.36 $1.06 28.30 Total Dividends 32,287 26,984 19.65 Total Assets 955,373 889,717 7.38 Stockholders’ Equity 554,058 494,513 12.04

informAtion by segment Restated Restated 2014 2013 2014 2013 $’000 $’000 $’000 $’000 Third Party Turnover Operating Profit Pharmaceutical and Personal Care Distribution 853,134 815,877 92,498 78,477 Food, Construction Related and Other Trading 506,249 496,826 31,198 25,290

1,359,383 1,312,703 123,696 103,767 Group Assets Employees Employed at Year End 2014 2013 Pharmaceutical and Personal Care Distribution 465,535 424,655 561 599 Food, Construction Related and Other Trading 489,838 465,062 407 426

955,373 889,717 968 1,025

18 Agostini’s LiMited

Chloraseptic Sore Throat Spray and Lozenges from Prestige

Allergies, Cough and Cold Relief from Carlisle

Agostini InteriorsPratt & Lambert Paint Systems

19AnnuAl RepoRt 2014

Lactacyd Intimate Liquid Soap

Stayfree / Carefree Feminine Protection

PHARMACEUTICAL AND PERSONAL CARE DISTRIBUTION

DISTRIBUTION

Our pharmaceutical distribution company, Smith Robertson, had another good year. This subsidiary continues to be the leading supplier of both Ethical and OTC drugs to both the Government and the Private sectors. While there was some reduction in purchasing by the Government’s central buying facility, this was offset by an increase in sales to the private trade. We continue to look for avenues to diversify the business in related products and services, and expand our Personal Care offering. The acquisition of the property that houses the central administration office and distribution warehouse, has also added value to the business in the current financial year.

RETAIL

We have experienced top line and profitability growth in many of our stores in this financial year. Investment in our newer stores at Trinicity and Marabella has met profitability expectations in the current year, and we will continue to upgrade our more mature stores to maximise their performance.

In November 2014, we opened our newest SuperPharm outlet in Diego Martin. The store has been well received by customers, and we expect this unit to be another positive contributor to this subsidiary’s results.

The start of construction of another store at Mausica, Arima, has had a number of setbacks, but our landlord

is due to begin building works in January 2015. We continue to look for suitable sites to expand our footprint, for further market share, economies of scale and improved profitability.

FOOD, CONSTRUCTION RELATED & OTHER TRADING

FOOD, BEVERAGE & GROCERY DISTRIBUTION

Hand Arnold experienced growth in both sales and profitability in the past year. The strategy has been to focus on the strengthening of profitable brands, rationalisation of the product portfolio, and improvement of our ordering and delivery efficiencies through technology and better execution. Sales of our “Moo!” dairy products continue to grow, and the brand is holding its place in the market after two years since its launch, despite strong competitive responses from established players

CONSTRUCTION PRODUCTS & SERVICES

Agostini Marketing: 2014 was another year of slow construction activity in Trinidad & Tobago. There were few new major projects, but we were able to maintain profitability through the many smaller jobs that we secured. Going into the new financial year, we have been awarded several more substantial contracts which should result in increased profitability in 2015.

We continue to pursue arbitration proceedings with the Housing Development Corporation on the Wellington Road, Debe housing project and we expect a favourable outcome in the current year.

20 Agostini’s LiMited

TEN YEAR FINANCIAL REVIEW

Restated Restated 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005 $’000 $’000 $’000 $’000 $’000 $’000 $’000 $’000 $’000 $’000

Group Turnover 1,359,383 1,312,703 1,293,887 1,255,743 856,702 719,765 547,410 449,296 384,740 322,661

Profit Before Taxation 107,145 87,156 90,242 87,434 57,354 52,339 46,063 37,685 29,347 31,867

Profit for the Year 80,546 62,580 64,707 61,523 40,371 36,373 33,855 27,977 21,992 24,517

Net Profit Attributable to Agostini’s Limited Shareholders 79,932 61,946 64,260 61,275 24,780 791 30,201 27,779 21,818 24,404

Dividend Amount 32,287 26,984 25,811 24,611 10,241 1,453 11,899 11,833 9,407 8,858

Times covered 2.48 2.30 2.51 2.49 2.4 - 2.5 2.4 2.3 2.8

Issued Stock Units (‘000) 58,704 58,704 58,662 58,608 58,583 29,057 27,029 26,897 26,887 26,843

Stockholders’ Equity 554,058 494,513 458,182 402,773 358,933 216,992 210,008 182,775 169,429 151,848

Dividend per Stock Unit 55¢ 46¢ 44¢ 42¢ 20¢ 5¢ 42¢ 44¢ 35¢ 33¢

Earnings per Stock Unit 136.2¢ 105.5¢ 110.3¢ 104.9¢ 74.7¢ 2.7¢ 111.9¢ 103.3¢ 81.3¢ 90.9¢

Net Assets 698,792 660,025 570,930 485,668 443,646 300,592 298,802 216,554 197,878 177,418 Notes: 1 The 2012 and 2013 figures have been adjusted in accordance with IAS 19, Pension Benefits.

2 The 2008 and 2009 figures have been adjusted in accordance with IFRS 5 Non current assets held for sale and discontinued operations.

3 The stockholders equity figure for 2007 has been adjusted to reflect the adoption of IAS 12 p61 (a).

4 The 2005 figures have been adjusted to reflect adoption of IFRS 2 Share Based Payments.

Johnson & Johnson Consumer Products

21AnnuAl RepoRt 2014

ENERGY & INDUSTRIAL PRODUCTS & SERVICES

Rosco Petroavance’s performance was flat for the first time in a number of years, due to a slowdown of activity in the oilfield sector. Our testing tower stand, which is the only one of its kind in the country and which allows us to provide additional testing services to our larger energy customers, was commissioned during the year. Construction has recently begun on the company’s new office building to be completed in mid 2015, which will provide much needed additional space for storage and service activities.

PROPERTY RATIONALISATIONWe have recently vacated our Nelson Street property, the home of our head office and several operations for the last 44 years, and expect to finalise lease agreements with tenants in the second quarter of the current year.

STRATEGIC INTENTAll the companies in the Group have continued their commitment to managing, developing and becoming “Benchmark” businesses, and have strived to achieve our initiatives on the platforms of Financial Strength, Employee Excellence, Innovation and Exceeding Customer Expectations.

In May 2014, the Group’s top 55 directors, managers and unit leaders, came together to discuss new ways to deliver value within their organisations, and across the Group. The focus of the workshops was on challenging the way we look at our current business models, to assess their sustainability in today’s business environment. The sessions were facilitated by two USA based leaders in Innovation.

The output of the workshops was the reengineering of the business models within our business units, to ensure they are driven by innovation. This was the underlying goal in our 2014-2015 Strategic Planning process, and we have started to introduce new ways to transform how we deliver value to our customers. The Management has also committed to creating an Innovation Council in our Group, and testing at least one innovation project in the ensuing year.

FINANCIAL STRENGTHAt the end of the financial year, the Group’s debt to equity ratio stood at 21:79. This position gives us the capacity to finance acquisitions and growth as required. In October 2014 the Group finalised a refinancing of the Group’s total debt with Scotiabank T&T Ltd. These new facilities of $275 million are expected to save the Group in excess of $5 million in the current year, net of refinancing costs.

CORPORATE SOCIAL RESPONSIBILITYThe Group continues to support and donate to numerous charities and worthy causes, in our community. We are in the final stages of establishing a wider Group Charitable Foundation, which should be fully operational in the current year.

Anthony Agostini

Managing Director

December 8, 2014

Novartis Consumer Health

Sensodyne - No. 1 Dentist Recommended for Sensitive Teeth

22 Agostini’s LiMited

Your Directors have pleasure in presenting their report for the year ended September 30, 2014.

Financial Results $’000

Income for the year before taxation 107,145 Less Taxation (26,599)

Profit for the Year 80,546 Less: Attributable to Minority Interest (614)

Net Income for the year after taxation 79,932 Dividends - Interim (12,914)

- Final (19,373)

Profit Retained for the year 47,645

Dividend

Based on the Group’s results, the Directors have approved a final dividend of 33¢, resulting in a total dividend of 55¢ for the year.

Directors

The Director retiring by rotation under the bye laws, Ms. Amalia Maharaj, being eligible, offers herself for re-election.

Auditors

The Auditors, Ernst & Young, retire and being eligible, offer themselves for reappointment.

The Directors are satisfied that the audited Financial Statements published in this Report comply with applicable financial reporting standards, and present fairly in all material respects, the financial affairs of the Group.

By Order of the Board

R. Rajkumarsingh

Secretary

December 8, 2014

report of tHe direCtors

Ribena and Lucozade - fuelling the good times

23AnnuAl RepoRt 2014

Independent audItor’s report

to the shareholders of agostini’s Limited

report on the consolidated financial statements We have audited the accompanying consolidated financial statements of Agostini’s Limited and its subsidiaries (the Group) which comprise the consolidated statement of financial position as of 30 September 2014 and the consolidated income statement, consolidated statement of comprehensive income, consolidated statement of changes in equity and consolidated statement of cash flows for the year then ended and a summary of significant accounting policies and other explanatory information.

Management’s responsibility for the financial statementsManagement is responsible for the preparation and the fair presentation of these consolidated financial statements in accordance with International Financial Reporting Standards, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

auditor’s responsibilityOur responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

opinionIn our opinion, the consolidated financial statements present fairly, in all material respects the financial position of the Group as of 30 September 2014, and its financial performance and cash flows for the year then ended in accordance with International Financial Reporting Standards.

Port of SpainTRINIDAD24 November 2014

24 Agostini’s LiMited

ConsoLIdated stateMent oF FInanCIaL posItIonFOR THE YEAR ENDED 30 SEPTEMBER 2014

restated restated 2014 2013 2012 notes $’000 $’000 $’000

assetsnon-current assets Property, plant and equipment 6 247,985 248,221 178,778 Investment property 7 57,259 54,408 15,025 Intangible asset 8 78,017 79,042 77,263 Retirement benefit assets 9 25,783 19,333 16,574 Deferred tax asset 15 14,376 18,843 18,763

423,420 419,847 306,403Current assets Inventories 10 279,113 245,968 244,798 Construction contract work-in-progress 11 275 82 209 Trade and other receivables 12 218,079 186,748 212,652 Taxation recoverable 2,952 4,156 4,623 Cash at bank and in hand 21 31,534 32,916 80,199

531,953 469,870 542,481

total assets 955,373 889,717 848,884

eQuItYCapital and reserves Stated capital 13 187,404 187,404 187,012 Capital reserve 2,652 2,652 2,652 Revaluation reserve 28,422 28,497 23,025 Retained earnings 335,580 275,960 241,349

554,058 494,513 454,038 Non-controlling interests 1,247 1,069 845

total equity 555,305 495,582 454,883

25AnnuAl RepoRt 2014

ConsoLIdated stateMent oF FInanCIaL posItIon (continued)FOR THE YEAR ENDED 30 SEPTEMBER 2014

restated restated 2014 2013 2012 notes $’000 $’000 $’000

LIaBILItIesnon-current liabilities Borrowings 14 129,089 148,161 105,508 Retirement benefit liability 9 – 3,552 – Deferred tax liability 15 14,398 12,730 10,539

143,487 164,443 116,047Current liabilities Trade and other payables 16 200,116 160,991 188,583 Taxation payable 5,294 6,190 12,641 Borrowings 14 51,171 62,511 76,730

256,581 229,692 277,954

total liabilities 400,068 394,135 394,001

total equity and liabilities 955,373 889,717 848,884

The accompanying notes form an integral part of these financial statements.

On November 24, 2014 the Board of Directors of Agostini’s Limited authorised these financial statements for issue.

_________________________________ Director _________________________________ Director

26 Agostini’s LiMited

restated 2014 2013 notes $’000 $’000turnover 1,359,383 1,312,703

Cost of sales (1,035,534) (1,003,571)

Gross profit 323,849 309,132

other operating income 28,080 25,328

351,929 334,460expenses Other operating (132,518) (125,303) Administration (60,661) (64,507) Marketing and distribution (35,054) (40,883)

(228,233) (230,693)

operating profit 123,696 103,767

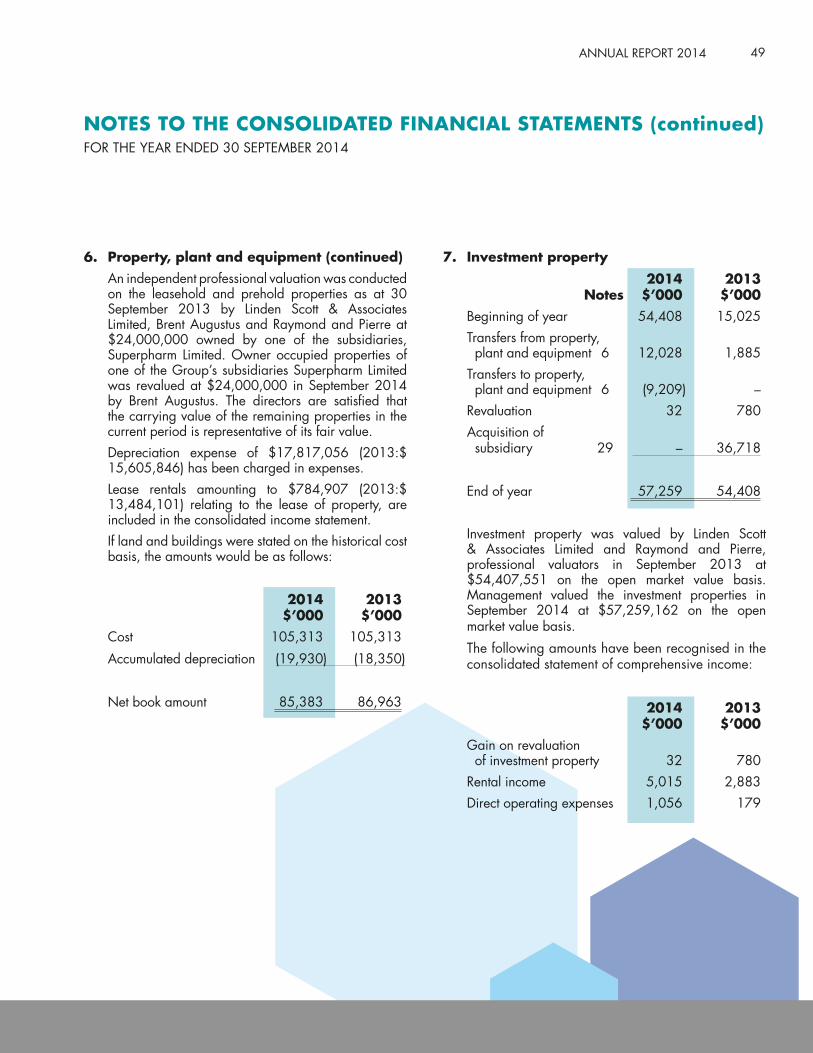

Gain on revaluation of investment property 7 32 780

Finance costs - net 18 (16,583) (17,391)

profit before taxation 107,145 87,156taxation 19 (26,599) (24,576)

profit for the year 80,546 62,580

attributable to: Owners of the parent 79,932 61,946 Non-controlling interests 614 634 80,546 62,580

earnings per share for profit attributable to shareholders - Basic 20 1.36 1.06

- Diluted 20 1.36 1.06

The accompanying notes form an integral part of these financial statements.

ConsoLIdated InCoMe stateMentFOR THE YEAR ENDED 30 SEPTEMBER 2014

27AnnuAl RepoRt 2014

ConsoLIdated stateMent oF CoMpreHensIVe InCoMeFOR THE YEAR ENDED 30 SEPTEMBER 2014

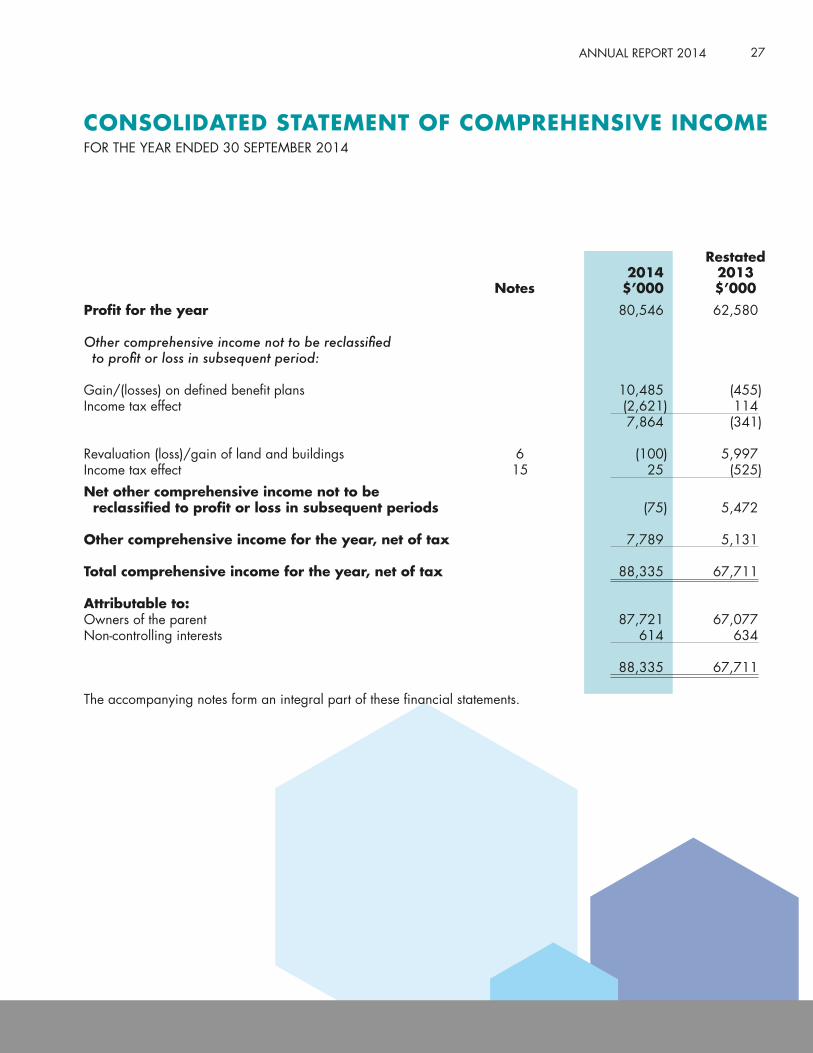

restated 2014 2013 notes $’000 $’000profit for the year 80,546 62,580

Other comprehensive income not to be reclassified to profit or loss in subsequent period:

Gain/(losses) on defined benefit plans 10,485 (455)Income tax effect (2,621) 114 7,864 (341)

Revaluation (loss)/gain of land and buildings 6 (100) 5,997Income tax effect 15 25 (525)net other comprehensive income not to be reclassified to profit or loss in subsequent periods (75) 5,472

other comprehensive income for the year, net of tax 7,789 5,131

total comprehensive income for the year, net of tax 88,335 67,711

attributable to:Owners of the parent 87,721 67,077Non-controlling interests 614 634

88,335 67,711

The accompanying notes form an integral part of these financial statements.

28 Agostini’s LiMited

ConsoLIdated stateMent oF CHanGes In eQuItYFOR THE YEAR ENDED 30 SEPTEMBER 2014

attributable to equity holders of the parent non stated Capital revaluation retained controlling capital reserve reserve earnings total interests total notes $’000 $’000 $’000 $’000 $’000 $’000 $’000

Year ended 30 september 2014Balance at 1 October 2013 (Restated) 187,404 2,652 28,497 275,960 494,513 1,069 495,582Profit for the year – – – 79,932 79,932 614 80,546Other comprehensive income – – (75) 7,864 7,789 – 7,789Total comprehensive income – – (75) 87,796 87,721 614 88,335Dividend paid – 2014 (48¢ per share) 27 – – – (28,176) (28,176) (436) (28,612)Balance at 30 September 2014 187,404 2,652 28,422 335,580 554,058 1,247 555,305

Year ended 30 september 2013Balance at 1 October 2012 as previously stated 187,012 2,652 23,025 234,275 446,964 845 447,809Restatement - Employee Benefits 5 – – – 7,074 7,074 – 7,074Balance at 1 October 2012 (restated) 187,012 2,652 23,025 241,349 454,038 845 454,883Profit for the year (restated) – – – 61,946 61,946 634 62,580Other comprehensive income (restated) – – 5,472 (341) 5,131 – 5,131Total comprehensive income (restated) – – 5,472 61,605 67,077 634 67,711Dividend paid - 2013 (46¢ per share) 27 – – – (26,994) (26,994) (410) (27,404)Executive share option: - Shares issued 13 392 – – – 392 – 392Balance at 30 September 2013 (restated) 187,404 2,652 28,497 275,960 494,513 1,069 495,582

The accompanying notes form an integral part of these financial statements.

29AnnuAl RepoRt 2014

ConsoLIdated stateMent oF CasH FLoWsFOR THE YEAR ENDED 30 SEPTEMBER 2014

restated 2014 2013 notes $’000 $’000operating activitiesProfit before taxation 107,145 87,156Adjustments for:

Depreciation of property, plant and equipment 6 18,546 15,606Amortization of intangible assets 8 1,058 639Gain on sale of plant and equipment (7) (162)Gain on acquisition 29 – (980)Net retirement benefit expense 9 483 338Gain on revaluation of investment property 7 (32) (780)Property, plant and equipment write off 1,567 –

Operating profit before changes in working capital 128,760 101,817Changes in working capital

Increase in inventories (33,145) (1,170)(Increase)/Decrease in work-in-progress (193) 127(Increase)/Decrease in trade and other receivables (31,330) 26,752

Increase/(Decrease) in trade and other payables 39,123 (28,048)Cash flows from operating activities 103,215 99,478Taxation paid (22,997) (29,715)net cash flows from operating activities 80,218 69,763Investing activities

Purchase of property, plant and equipment 6 (22,654) (20,573)Proceeds from sale of plant and equipment 130 283Purchase of intangible assets 8 (51) (2,418)Purchase of subsidiary 29 – (34,468)

Proceeds from subsidiary 29 – 36net cash flows used in investing activities (22,575) (57,140)Financing activities

Share issue 13 – 392Net repayment on loans (23,040) (61,634)Dividends paid 27 (28,176) (26,994)Dividends paid to minority interests (436) (410)

net cash flows used in financing activities (51,652) (88,646)Cash increase/(decrease) during the year 5,991 (76,023)Cash and cash equivalents, at 1 october (7,424) 68,599Cash and cash equivalents, at 30 september 21 (1,433) (7,424)

The accompanying notes form an integral part of these financial statements.

30 Agostini’s LiMited

1. General informationThe Company is a limited liability company, incorporated and domiciled in the Republic of Trinidad and Tobago and the address of its registered office is 18 Victoria Avenue, Port of Spain. The Group is principally engaged in trading and distribution and interior building contracting.The shares of the Parent Company are listed on the Trinidad and Tobago Stock Exchange. The majority shareholder is Victor E. Mouttet Limited (VEML), which owns 50.3% of the shares.

2. summary of significant accounting policiesThe principal accounting policies applied in the preparation of these consolidated financial statements are set out below. These policies have been consistently applied to all the years presented, unless otherwise stated.

(a) Basis of preparationThe consolidated financial statements of the Group are prepared under the historical cost convention.The consolidated financial statements provide comparative information in respect of the previous period. In addition, the Group presents an additional consolidated statement of financial position at the beginning of the earliest period presented when there is a retrospective application of an accounting policy, a retrospective restatement, or a reclassification of items in the consolidated financial statements. An additional consolidated statement of financial position as at 1 October 2012 is presented in these consolidated financial statements due to retrospective application of a change in accounting policy relative to IAS 19-Employee Benefits (Revised 2011).

notes to tHe ConsoLIdated FInanCIaL stateMentsFOR THE YEAR ENDED 30 SEPTEMBER 2014

i) Statement of complianceThese consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB).

ii) Principles of consolidationThe consolidated financial statements of the Group include the accounts of the parent and its subsidiary companies. All intra-group balances, transactions, and income and expenses have been eliminated in full.Non-controlling interests represent the portion of profit or loss and net assets not held by the Group and are presented separately in the consolidated statement of comprehensive income and within equity in the consolidated statement of financial position, separately from parent shareholders’ equity.

iii) Changes in accounting policies and disclosuresa) New accounting policies adopted

The accounting policies adopted are consistent with those of the previous financial year except that the Group has adopted the following new and amended IFRS and IFRIC (International Financial Reporting Interpretations Committee) interpretations as of 1 October 2013:•IAS 19 Employee Benefits (Revised

2011)•IFRS13FairValueMeasurement•IAS 1 Presentation of Items of Other

Comprehensive Income – Amendments to IAS 1

•IAS1Clarificationoftherequirementforcomparative information (Amendment)

31AnnuAl RepoRt 2014

2. summary of significant accounting policies (continued)(a) Basis of preparation (continued)

iii) Changes in accounting policies and disclosures (continued)a) New accounting policies adopted

(continued)•IFRS 10 Consolidated financial

statements•IFRS11Jointarrangements•IFRS12Disclosuresofinterestsinother

entities

Ias 19 employee Benefits (revised 2011) The Group applied IAS 19 (Revised 2011) retrospectively in the current period in accordance with the transitional provisions set out in the revised standard. The opening consolidated statement of financial position of the earliest comparative period presented (1 October 2013) and the comparative figures have been accordingly restated. IAS 19 (Revised 2011) changes the accounting for defined benefit plans and termination benefits. The most significant change relates to the accounting for changes in defined benefit obligations and plan assets. The amendments require the recognition of changes in defined benefit obligations and in the fair value of plan assets when they occur, and hence eliminate the ‘corridor approach’ permitted under the previous version of

IAS 19 and accelerate the recognition of past service costs. The amendments require all actuarial gains and losses to be recognised immediately through other comprehensive income in order for the net pension asset or liability recognised in the consolidated statement of financial position to reflect the full value of the plan deficit or surplus.Furthermore, the interest cost and expected return on plan assets used in the previous version of IAS 19 are replaced with a ‘net interest’ amount under IAS 19 (Revised 2011), which is calculated by applying the discount rate to the net defined benefit liability or asset. These changes have had an impact on the amounts recognised in the consolidated income statement and other comprehensive income in prior years (see the tables below for details). In addition, IAS 19 (Revised 2011) introduces certain changes in the presentation of the defined benefit cost including more extensive disclosures.Specific transitional provisions are applicable to first-time application of IAS 19 (Revised 2011). The Group has applied the relevant transitional provisions and restated the comparative amounts on a retrospective basis (see the tables below for details).The impact of the adoption of IAS 19 (revised) on the previously reported year ended 30 September 2013 and current year ended 30 September 2014 is illustrated below:

notes to tHe ConsoLIdated FInanCIaL stateMents (continued)FOR THE YEAR ENDED 30 SEPTEMBER 2014

32 Agostini’s LiMited

notes to tHe ConsoLIdated FInanCIaL stateMents (continued)FOR THE YEAR ENDED 30 SEPTEMBER 2014

2. summary of significant accounting policies (continued)(a) Basis of preparation (continued)

iii) Changes in accounting policies and disclosures (continued)a) New accounting policies adopted (continued)

Ias 19 employee Benefits (revised 2011 - restatement) (continued) 2014 2013Impact on profit or loss for the year: $’000 $’000(Increase)/decrease in administrative expense (483) 1,616Decrease/(increase) in income tax expenses 120 (404)(Decrease)/increase in profit for the year (363) 1,212

2014 2013Impact on other comprehensive income for the year: $’000 $’000Net increase/(decrease) in re-measurement of defined benefit asset 10,485 (455)(Increase)/decrease in income tax relating to othercomprehensive income (2,621) 114Increase/(decrease) in other comprehensive income for the year 7,864 (341)Increase in total comprehensive income for the year 7,501 871

as at as at 30 september 1 october 2014 2013 2013Impact on equity net assets/for the year: $’000 $’000 $’000

Increase in pension plan asset 10,002 4,313 9,434

Total non-current assets 10,002 4,313 9,434

(Increase)/decrease in deferred tax liability (3,105) (290) (2,360)

(Increase) in pension plan liability – (3,552) –

Total non-current liabilities (3,105) (3,842) (2,360)

Net input on equity 6,897 471 7,074

33AnnuAl RepoRt 2014

notes to tHe ConsoLIdated FInanCIaL stateMents (continued)FOR THE YEAR ENDED 30 SEPTEMBER 2014

2. summary of significant accounting policies (continued)(a) Basis of preparation (continued)

iii) Changes in accounting policies and disclosures (continued)a) New accounting policies adopted

(continued)IFrs 13 Fair Value MeasurementIFRS 13 establishes a single source of guidance under IFRS for all fair value measurements. IFRS 13 does not change when an entity is required to use fair value, but rather provides guidance on how to measure fair value under IFRS. IFRS 13 defines fair value as an exit price. There was no effect on the Group’s recognition of its assets and liabilities.IAS 1 Presentation of Items of Other Comprehensive Income (OCI) – Amendments to IAS 1The amendments to IAS 1 introduce a grouping of items presented in OCI. Items that will be reclassified (‘recycled’) to profit or loss at a future point in time have to be presented separately from items that will not be reclassified. The amendments affect presentation only and have no impact on the Group’s financial position or performance. The required disclosure is included in the consolidated statement of comprehensive income.

Ias 1 Clarification of the requirement for comparative information (amendment)These amendments clarify the difference between voluntary additional comparative information and the minimum required

comparative information. An entity must include comparative information in the related notes to the financial statements when it voluntarily provides comparative information beyond the minimum required comparative period. The amendments clarify that the opening statement of financial position (as at 1 October 2013 in the case of the Group), presented as a result of retrospective restatement or reclassification of items in financial statements does not have to be accompanied by comparative information in the related notes.As a result, the Group has not included comparative information in its notes in respect of the opening consolidated statement of financial position as at 1 October 2013. The amendments affect presentation only and have no impact on the Group’s consolidated financial position or performance.

IFrs 10 Consolidated financial statementsIFRS 10 builds on existing principles by identifying the concept of control as the determining factor in whether an entity should be included within the consolidated financial statements of the parent company. The standard provides additional guidance to assist in the determination of control where this is difficult to assess. The adoption of this standard did not impact the consolidated financial statements.

34 Agostini’s LiMited

notes to tHe ConsoLIdated FInanCIaL stateMents (continued)FOR THE YEAR ENDED 30 SEPTEMBER 2014

2. summary of significant accounting policies (continued)(a) Basis of preparation (continued)

iii) Changes in accounting policies and disclosures (continued)a) New accounting policies adopted

(continued)IFrs 11 Joint arrangementsIFRS11Jointarrangementsfocusesontherights and obligations of the parties to the arrangement rather than its legal form. There are two types of joint arrangements: jointoperationsand jointventures. Jointoperations arise where the investors have rights to the assets and obligations for the liabilities of an arrangement. A joint operator accounts for its share of the assets, liabilities, revenues and expenses. Joint ventures arise where the investorshave rights to the net assets of the arrangement; joint ventures are accounted for under the equity method. Proportional consolidation of joint arrangements is no longer permitted. The Group does not have any joint arrangements.

IFrs 12 disclosures of Interests in other entitiesIFRS 12 sets out the requirements for disclosures relating to an entity’s interests in subsidiaries, joint arrangements, associates and structured entities. The requirements in IFRS 12 are more comprehensive than the previously existing disclosure requirements for subsidiaries. While the Group has subsidiaries with material non-controlling interests, there are no unconsolidated structured entities.

b) New accounting policies not adoptedThe Group has not adopted early the following new and revised IFRS’s and IFRIC interpretations that have been issued but are not yet effective or not relevant to the Group’s operations: • Investment Entities (Amendments

to IFRS 10, IFRS 12 and IAS 27) - Effective1January2014

• IFRS9FinancialInstruments–Effective1January2014

• IAS32OffsettingFinancialAssetsandFinancial Liabilities – Amendments to IAS32–Effective1January2014

• IFRIC Interpretation 21 Levies (IFRIC21)–Effective1January2014

• IAS39Novation of Derivatives andContinuation of Hedge Accounting – Amendments to IAS 39 – Effective 1 January2014

• IFRS 14 – Interim standard onregulatory deferral accounts.

These standards, interpretations and amendments are not expected to impact the Group.

(b) Consolidationi) Subsidiaries

Subsidiaries, which are those companies in which the Group, directly or indirectly, has an interest of more than one half of the voting rights or otherwise has power to govern the financial and operating policies are consolidated. Subsidiaries are consolidated from the date on which control is transferred to the Group and are no longer consolidated from the date that control ceases.

35AnnuAl RepoRt 2014

notes to tHe ConsoLIdated FInanCIaL stateMents (continued)FOR THE YEAR ENDED 30 SEPTEMBER 2014

2. summary of significant accounting policies (continued)(b) Consolidation (continued)

i) Subsidiaries (continued)All significant inter-company transactions, balances and unrealised gains on transactions between Group companies are eliminated; unrealised losses are also eliminated unless the cost cannot be recovered. Where necessary, accounting policies of subsidiaries have been changed to ensure consistency with the policies adopted by the Group.The purchase method of accounting is used to account for the acquisition of subsidiaries by the Group. The cost of an acquisition is measured at the fair value of the assets given, equity instruments issued and liabilities incurred or assumed at the date of exchange, plus costs directly attributable to the acquisition. Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are measured initially at their fair values at the acquisition date, irrespective of the extent of any minority interest. The excess of the cost of acquisition over the fair value of the Group’s share of the identifiable net assets acquired is recorded as goodwill. If the cost of acquisition is less than the fair value of the net assets of the subsidiary acquired, the difference is recognised directly in the consolidated income statement.

ii) Transactions and minority interestsThe Group applies a policy of treating transactions with minority interests as transactions with parties external to the Group.A listing of the Group’s subsidiaries is set out in Note 23.

(c) segment reportingAn operating segment is a group of assets, liabilities and operations which are included in the measures that are used by the chief operating decision maker.

(d) Foreign currency translationi) Functional and presentation currency

Items included in the financial statements of each of the Group’s entities are measured using the currency of the primary economic environment in which the entity operates (‘the functional currency’). The consolidated financial statements are presented in Trinidad and Tobago dollars, which is the Group’s functional and presentation currency.

ii) Transactions and balancesForeign currency transactions are translated into the functional currency using the exchange rates prevailing at the dates of the transactions. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation at year end exchange rates of monetary assets and liabilities denominated in foreign currencies, are recognised in the consolidated income statement.

36 Agostini’s LiMited

2. summary of significant accounting policies (continued)(e) property, plant and equipment

Freehold properties comprise mainly warehouses, retail outlets and offices occupied by the Group and are shown at fair value, based on valuations by external independent appraisers, less subsequent depreciation for buildings. Any accumulated depreciation at the date of revaluation is eliminated against the gross carrying amount of the asset, and the net amount is restated to the revalued amount of the asset. All other property, plant and equipment are stated at historical cost less depreciation. Historical cost includes expenditure that is directly attributable to the acquisition of the items.Subsequent costs are included in the asset’s carrying amount or recognised as a separate asset, as appropriate, only when it is probable that future economic benefits associated with the item will flow to the Group and the cost of the item can be measured reliably. All other repairs and maintenance are charged to the consolidated income statement during the financial period in which they are incurred.Increases in the carrying amount arising on revaluation of land and buildings are credited to the revaluation reserve included in the equity section of the consolidated statement of financial position. Decreases that offset previous increases of the same asset are charged against revaluation reserve directly in equity; all other decreases are charged to the consolidated income statement.

The freehold buildings are depreciated on a straight line basis at 1.5% - 2% per annum on the valuation. Leasehold improvements are amortised over the lives of the leases which include options to renew for further terms ranging from 6 years to 10 years which the Group intend to exercise. Land and capital work-in-progress are not depreciated. Depreciation is provided on plant and other assets on the straight line basis at rates as follows:Machinery and equipment - 10% - 331/3% per annumMotor vehicles - 121/2% - 25% per annumFurniture and office equipment - 10% - 25% per annumThe estimated useful lives of property, plant and equipment is reviewed and adjusted if appropriate, at each financial year end.An asset’s carrying amount is written down immediately to its recoverable amount if the asset’s carrying amount is greater than its estimated recoverable amount.Gains and losses on disposals are determined by comparing proceeds with carrying amounts. These are included in the consolidated income statement. When revalued assets are sold, the amounts included in the revaluation surplus account are transferred to retained earnings.

(f) Investment propertyInvestment property principally comprising freehold land and buildings are held for long-term rental yields and are not occupied by the Group. Investment properties are carried at fair value, representing the open market value determined annually by independent professional valuers.

notes to tHe ConsoLIdated FInanCIaL stateMents (continued)FOR THE YEAR ENDED 30 SEPTEMBER 2014

37AnnuAl RepoRt 2014

notes to tHe ConsoLIdated FInanCIaL stateMents (continued)FOR THE YEAR ENDED 30 SEPTEMBER 2014

2. summary of significant accounting policies (continued)(f) Investment property (continued)

Fair value is based on active market prices, adjusted, if necessary, for any difference in the nature, location or condition of the specific asset. Investment properties are not subject to depreciation. Changes in fair value are recorded in the consolidated income statement.If an investment property becomes owner - occupied, it is reclassified as property, plant and equipment, and its fair value at the date of reclassification becomes its cost for subsequent accounting purposes.If an item of property, plant and equipment becomes an investment property because its use has changed, any difference arising between the carrying amount and the fair value of this item at the date of transfer is recognised in equity as a revaluation of property, plant and equipment. However, if a fair value gain reverses a previous impairment loss, the gain is recognised in the consolidated income statement. Upon the disposal of such investment property, any surplus previously recorded in the revaluation surplus account is transferred to retained earnings. The transfer is not made through the consolidated income statement.

(g) Intangible assetGoodwillGoodwill represents the excess of the cost of an acquisition over the fair value of the Group’s share of the net identifiable assets of the acquired subsidiary/associate at the date of acquisition. Goodwill on acquisition of subsidiaries is included in intangible assets. Goodwill on acquisition of associates is included in investments in associates and is tested for impairment as part of the overall balance. Separately recognised

goodwill is tested annually for impairment and carried at cost less accumulated impairment losses. Impairment losses on goodwill are not reversed. Gains and losses on the disposal of an entity include the carrying amount of goodwill relating to the entity sold.Goodwill is allocated to cash-generating units for the purpose of impairment testing. The allocation is made of those cash-generating units or groups of cash-generating units that are expected to benefit from the business combination in which the goodwill arose.

SoftwareSoftware assets which have been acquired directly are recorded initially at cost. On acquisition the useful life of the asset is estimated and the cost amortised over its life and tested for impairment when there is evidence of same. The current estimated useful life of the software asset is 3 years.The amortisation period and the amortisation method for these intangible assets are reviewed at least at the end of each reporting period. Changes in the expected useful life or the expected pattern of consumption of future economic benefits embodied in the asset are considered to modify the amortisation period or method, as appropriate, and are treated as changes in accounting estimates. The amortisation expense on these intangible assets is recognised in the consolidated income statement as the expense category that is consistent with the function of the intangible assets.

38 Agostini’s LiMited

notes to tHe ConsoLIdated FInanCIaL stateMents (continued)FOR THE YEAR ENDED 30 SEPTEMBER 2014

2. summary of significant accounting policies (continued)(h) offsetting financial instruments

Financial assets and liabilities are offset and the net amount reported in the consolidated statement of financial position, only where there is a legally enforceable right to offset the recognised amounts and there is an intention to settle on a net basis, or to realise the asset and settle the liability simultaneously.

(i) InventoriesInventories are stated at the lower of cost and net realisable value, cost being landed value determined on the weighted average basis. The cost of finished goods and work-in-progress comprises raw materials, direct labour, other direct costs and related production expenses. Net realisable value is the estimate of the selling price in the ordinary course of business, less the cost of completion and selling expenses.

(j) Construction contractsA construction contract is a contract specifically negotiated for the construction of an asset or a combination of assets that are closely interrelated or interdependent in terms of their design, technology and functions or their ultimate purpose or use.When the outcome of a construction contract cannot be estimated reliably, contract revenue is recognised to the extent of contract costs incurred where it is probable those costs will be recoverable. Contract costs are recognised when incurred.

When the outcome of a construction contract can be estimated reliably, contract revenue and contract costs are recognised by using the ‘percentage of completion method’. The stage of completion is determined by internal valuations. When it is probable that total contract costs will exceed total contract revenue, the expected loss is recognised as an expense immediately.Costs incurred in the year in connection with future activity on a contract are excluded and shown as contract work-in-progress. The aggregate of the costs incurred and the profit/(loss) recognised on each contract is compared against the progress billings up to the year end. Where costs incurred and recognised profits (less recognised losses) exceed progress billings, the balance is shown as due from customers on construction contracts, under receivables and prepayments. Where progress billings exceed costs incurred plus recognised profits (less recognised losses), the balance is shown as due to customers on construction contracts, under trade and other payables.

(k) Financial assetsInitial recognition and measurementThe Group’s financial assets include cash and bank, trade and other receivables and available-for-sale investment. The Group determines the classification of its financial assets at initial recognition. All financial assets are recognised initially at fair value.

39AnnuAl RepoRt 2014

notes to tHe ConsoLIdated FInanCIaL stateMents (continued)FOR THE YEAR ENDED 30 SEPTEMBER 2014

2. summary of significant accounting policies (continued)(k) Financial assets (continued)

Subsequent measurementThe subsequent measurement of financial assets depends on their classification as follows:

Cash and cash equivalentsCash and cash equivalents comprise cash in hand and at banks, deposits held at call with banks, bank overdrafts and short-term borrowings. Bank overdrafts and short-term borrowings are included within borrowings in current liabilities on the consolidated statement of financial position.

available-for-sale financial investmentsAvailable for sale financial investments are securities intended to be held for an indefinite period of time, but may be sold in response to needs for liquidity or changes in interest rates, exchange rates, or equity prices. After initial recognition, available for sale financial assets are measured at fair value, based on quoted market prices.Unrealised gains and losses are reported within equity until the investment is derecognised or the investment is determined to be impaired, net of deferred tax. On derecognition or impairment, the cumulative gain or loss previously reported in equity is transferred to the consolidated statement of comprehensive income.

trade and other receivablesTrade receivables, which generally have 30-90 day terms, are recognised at original invoice amount less an allowance for any uncollectible amounts. An estimate for doubtful debts is established when there is objective evidence that the amount will not be collected according to the original terms of the invoice. When a trade

receivable is uncollectible, it is written off against the allowance accounts for trade receivables.

Impairment of financial assetsThe Group assesses at each reporting date whether there is any objective evidence that a financial asset or group of financial assets is impaired. A financial asset or a group of financial assets is deemed to be impaired if, and only if, there is objective evidence of impairment as a result of one or more events that has occurred after the initial recognition of the asset (an incurred ‘loss event’) and that loss event has an impact on the estimated future cash flows of the financial asset or group of financial assets that can be reliably estimated. Evidence of impairment may include indications that the debtors or a group of debtors is experiencing significant financial difficulty, default or delinquency in interest or principal payments, the probability that they will enter bankruptcy or other financial reorganisation and where observable data indicate that there is a measurable decrease in the estimated future cash flows, such as changes in arrears or economic conditions that correlate with defaults.In the case of equity investments classified as available-for-sale, objective evidence would include a significant or prolonged decline in the fair value of the investment below its cost. ‘Significant’ is to be evaluated against the original cost of the investment and ‘prolonged’ against the period in which the fair value has been below it original cost. Where there is evidence of impairment, the cumulative loss-measured as the difference between the acquisition cost and the consolidated value, less any impairment loss on that investment previously recognised in the consolidated statement of comprehensive income is removed from other comprehensive income and recognised in the consolidated statement of comprehensive income.

40 Agostini’s LiMited

2. summary of significant accounting policies (continued)(k) Financial assets (continued)

Impairment of financial assets (continued)In relation to trade receivables the carrying amount of the receivable is reduced through use of an allowance account when there is doubt about the collectability of the amounts due under the original terms of the invoice. Impaired debts are derecognized when they are assessed as uncollectible.

(l) Financial liabilitiesInitial recognition and measurement All financial liabilities are recognised initially at fair value and in the case of loans and borrowings, plus directly attributable transaction costs. The Group’s financial liabilities include accounts payable and accruals and are recognised initially at fair value.

Subsequent measurementThe measurement of financial liabilities depends on their classification as follows:

Loans and borrowingsAfter initial recognition, interest bearing loans and borrowings are subsequently measured at amortised cost using the effective interest rate (EIR) method. Gains and losses are recognised in the consolidated income statement when the liabilities are derecognised as well as through the EIR amortisation process.Amortised cost is calculated by taking into account any discount or premium on acquisition

notes to tHe ConsoLIdated FInanCIaL stateMents (continued)FOR THE YEAR ENDED 30 SEPTEMBER 2014

and fee or costs that are an integral part of the EIR. The EIR amortisation is included in finance cost in the consolidated statement of comprehensive income.

trade and other payablesLiabilities for trade and other accounts payable which are normally settled on 30 day terms are carried at cost which is the fair value of the consideration to be paid in the future goods and services received, whether or not billed to the Group.

De-recognitionA financial liability is derecognised when the obligation under the liability is discharged or cancelled or expires.When an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as a de-recognition of the original liability and the recognition of a new liability, and the difference in the respective carrying amounts is recognised in the consolidated income statement.

(m) stated capitalShares are classified as equity. Incremental costs directly attributable to the issue of shares are shown in equity as a deduction from the proceeds.

41AnnuAl RepoRt 2014

notes to tHe ConsoLIdated FInanCIaL stateMents (continued)FOR THE YEAR ENDED 30 SEPTEMBER 2014

2. summary of significant accounting policies (continued)(n) Current and deferred income taxes

The tax expense for the period comprises current and deferred tax. Tax is recognised in the consolidated income statement, except to the extent that it relates to items recognised directly in equity.The current income tax assets and liabilities for the current and prior periods are measured at the amount expected to be recovered from or paid to the taxation authorities. The tax rates and tax laws used to compute the amount are those that are enacted or substantively enacted at the consolidated statement of financial position date.Deferred income tax is provided using the liability method, on temporary differences arising between the tax bases of assets and liabilities and their carrying amounts in the financial statements. Deferred income tax is determined using tax rates and tax laws that have been enacted or substantially enacted by the consolidated statement of financial position date and are expected to apply when the related income tax asset is realised or the deferred income tax liability is settled.Deferred tax assets relating to carry forward of unused tax losses are recognised to the extent that it is probable that future taxable profit will be available against which the unused tax losses can be utilised.

(o) employee benefitsPensionRetirement benefits for Group’s employees, are provided by various defined benefit plans. These plans are funded by contributions from the Group and qualified employees. Payments are made to pension trusts, which is financially separate from the Group, in accordance with periodic calculations by actuaries.For the Hand Arnold Trinidad Limited and Agostini’s Limited defined benefit plans, the pension accounting costs are assessed using the projected unit credit method. Under this method, the cost of providing pensions is charged to the consolidated income statement so as to spread the regular cost over the service lives of employees in accordance with the advice of independent actuaries who carry out a full valuation of the plans every three years. The pension obligation is measured as the present value of the estimated future cash outflows. All actuarial gains and losses to be recognised are spread forward over the average remaining service lives of employees.The employees of Smith Robertson & Company Limited are members of the Victor E. Mouttet Limited defined benefit plan, the assets of which are held in separate trustee administered funds. The pension plan is funded by payments from employees and by the Company taking account of the recommendations of independent qualified actuaries.The Company’s contributions are included in the employee benefit expense of these consolidated financial statements. Any assets and liabilities in relation to this defined benefit plan in accordance with International Accounting Standard 19 - Employee Benefits are recorded by the Victor E. Mouttet Limited.

42 Agostini’s LiMited

notes to tHe ConsoLIdated FInanCIaL stateMents (continued)FOR THE YEAR ENDED 30 SEPTEMBER 2014

2. summary of significant accounting policies (continued)(o) employee benefits (continued)