Embed Size (px)

Citation preview

AGRICULTURAL SECTOR SKILLS PLAN

2011-2016:

Prepared on behalf of the Sector by AgriSETA

for submission to the Department of Higher Education and Training

AGRICULTURAL SECTOR STRATEGIC SKILLS PLAN August 2015

2

Table of Contents

Table of Contents .................................................................................................. 2 List of Acronyms ................................................................................................... 6 List of Tables ......................................................................................................... 7 List of Figures ........................................................................................................ 7 Chapter 1: SECTOR PROFILE ................................................................................ 8

1.1 Introduction ................................................................................................................. 8 1.2 Scope of coverage ........................................................................................................ 8 1.3 Key role players ......................................................................................................... 11

1.3.1 National government departments ................................................................... 11 1.3.2 Sector representatives ....................................................................................... 14

1.4 Economic performance.............................................................................................. 14 1.4.1 Overview of structure of the sector ................................................................... 14 1.4.2 GDP Contribution ............................................................................................... 15 1.4.3 Exports ................................................................................................................ 17 1.4.4 Revenue from Skills Development Levies .......................................................... 17

1.5 Employer profile ........................................................................................................ 17 1.6 Labour market profile ................................................................................................ 19

1.6.1 Occupational categories ..................................................................................... 21 1.6.2 Employee profile and trends .............................................................................. 23

1.7 Conclusion ................................................................................................................. 26 Chapter 2: KEY SKILLS ISSUES............................................................................ 27

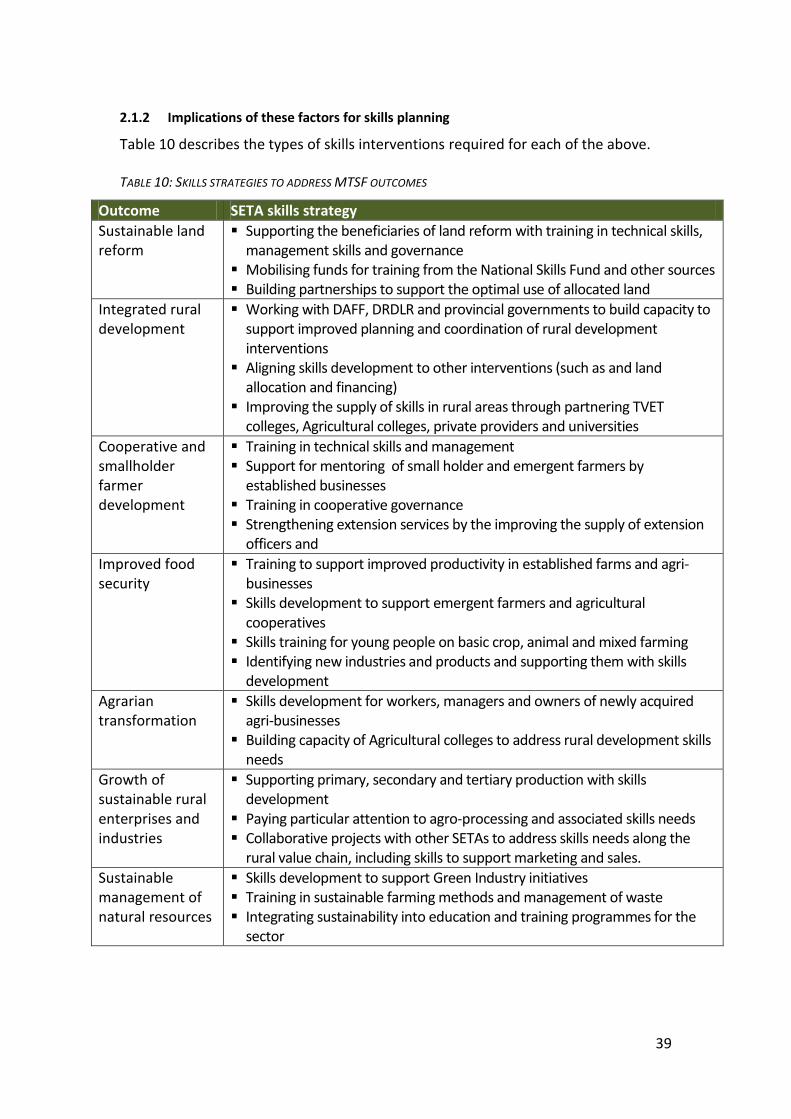

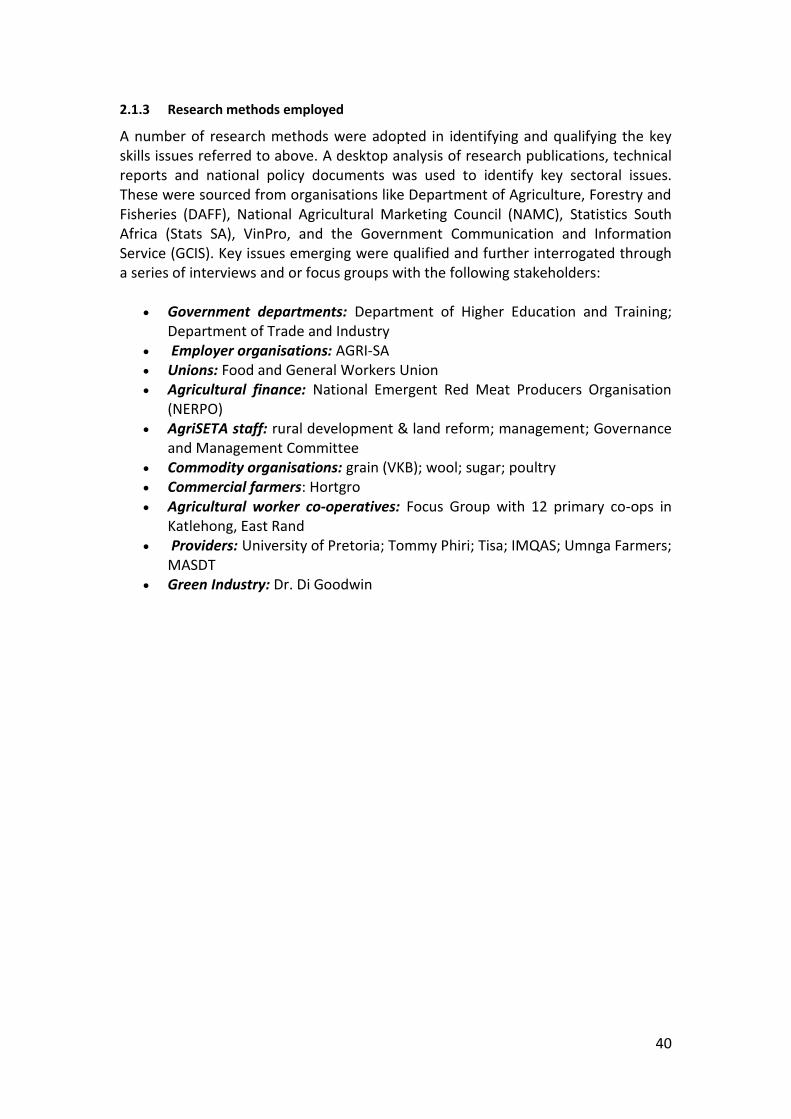

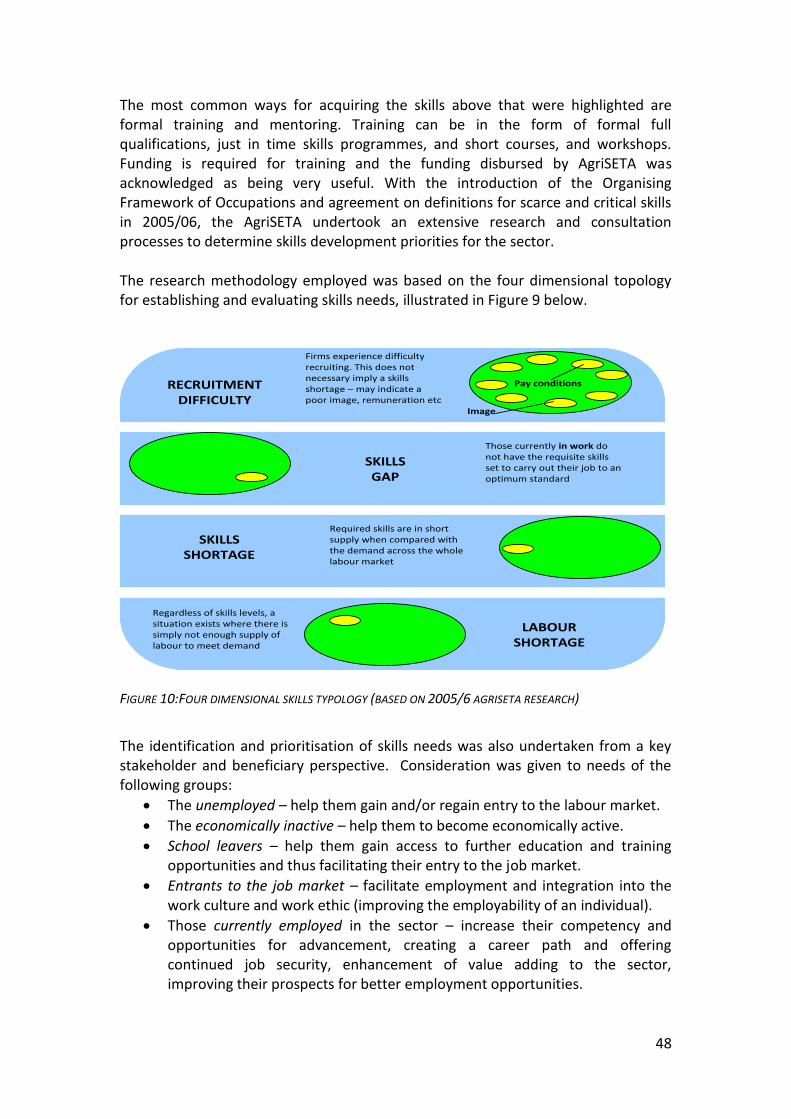

2.1 Change Drivers ........................................................................................................... 27 2.1.1 Factors impacting on skills demand and supply ................................................. 27 2.1.2 Implications of these factors for skills planning ................................................. 39 2.1.3 Research methods employed ............................................................................. 40

2.2 Alignment with national strategies and plans ........................................................... 41 2.3 Implementing national strategies and plans ............................................................. 45 2.4 Conclusion ................................................................................................................. 46

Chapter 3: SKILLS MISMATCH ........................................................................... 47 3.1 Extent of skills demand .............................................................................................. 47

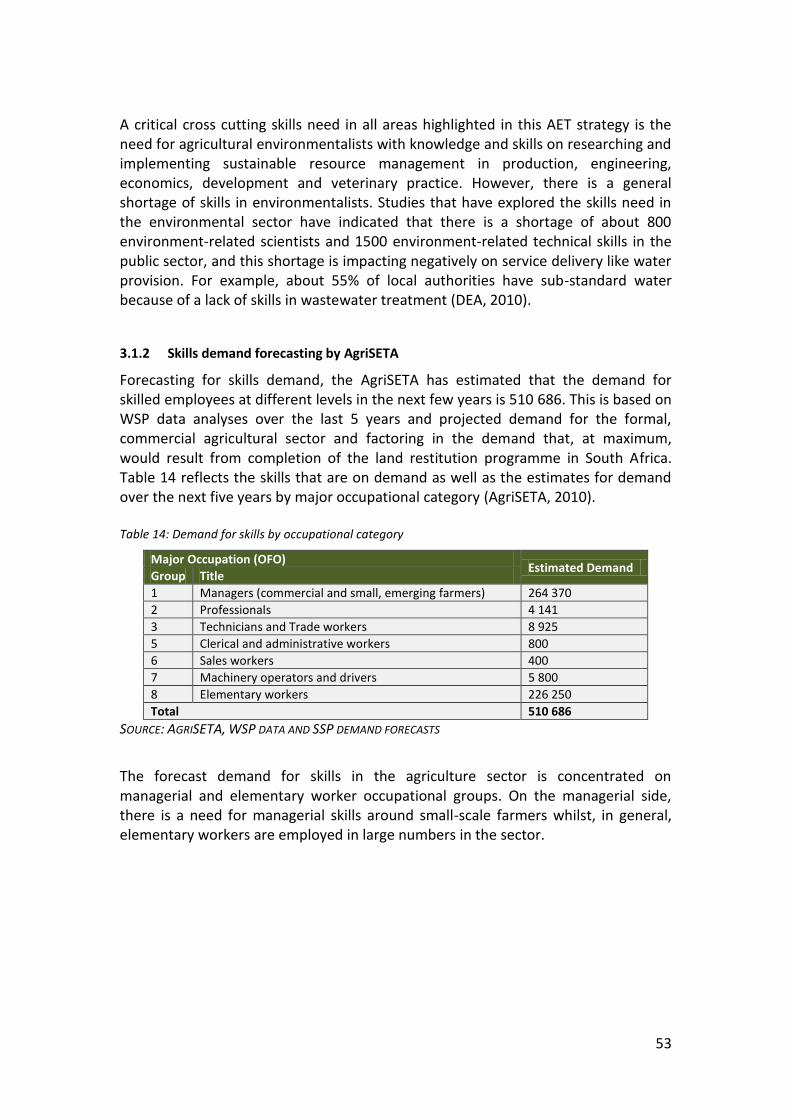

3.1.1 The National Education and Training Strategy for Agriculture (AET Strategy) .. 52 3.1.2 Skills demand forecasting by AgriSETA .............................................................. 53

3.2 Extent of skills supply ................................................................................................ 54 3.2.1 Colleges of agriculture ........................................................................................ 54 3.2.2 The role of AgriSETA in skills supply ................................................................... 56 3.2.3 Training Provider Perspectives ........................................................................... 56 3.2.4 Training Conducted ............................................................................................ 57

3.3 Scarce Skills and Skills Gaps ....................................................................................... 59 3.3.1 Top 10 Scarce Skills ............................................................................................ 59 3.3.2 Skills Gaps Overview ........................................................................................... 60

3.4 Conclusion ................................................................................................................. 62 Chapter 4: SECTOR PARTNERSHIPS ................................................................... 64

4.1 Current partnerships ................................................................................................. 64 4.1.1 Department of Rural Development and Land Reform (DRDLR) ......................... 64 4.1.2 Youth .................................................................................................................. 64 4.1.3 Department of Agriculture, Forestry and Fisheries (DAFF) ................................ 64 4.1.4 KZN Department of Agriculture.......................................................................... 65 4.1.5 Gert Sibande TVET College ................................................................................. 65

3

4.2 Planned Partnerships ................................................................................................. 65 4.2.1 Agricultural and TVET colleges ........................................................................... 65 4.2.2 Mentoring partnerships ..................................................................................... 66 4.2.3 SETA partnerships .............................................................................................. 67 4.2.4 Green Industry Partnership ................................................................................ 67

4.3 Partnership-related challenges .................................................................................. 68 4.4 Conclusion ................................................................................................................. 68

Chapter 5: Skills Priority Actions ....................................................................... 69 5.1 Introduction ............................................................................................................... 69 5.2 Key findings from previous chapters ......................................................................... 69 5.3 Key priority actions .................................................................................................... 70

5.3.1 Priority 1: Supporting skills development along the rural supply chain ............ 70 5.3.2 Priority 2: Skills to support equity in the sector ................................................. 70 5.3.3 Priority 3: skills to support enterprise development ......................................... 71 5.3.4 Priority 4: Improving the supply of quality education and training to the sector 72 5.3.5 Priority 5: skills for sustainability ....................................................................... 72 5.3.6 Priority 6: Building the capacity of government to support rural development 73

References .......................................................................................................... 74

4

Foreword This Final Draft of the Sector Skills Plan is submitted in fulfilment of the requirements of the Department of Higher Education and Training (DHET). It has been prepared for the period 2011 to 2016 in accordance with the Skills Development Act (Chapter 3; Section 10) and within the framework of the National Skills Development Strategy (NSDS) III. It has been developed in alignment with several National Policies. The policies include the: National Development Plan, New Growth Path, Human Resource Strategy for South Africa, Integrated Growth and Development Plan, National Policy on Food and Nutrition Security and, the White Paper on Post School education and training. The objective of this Sector Skills Plan is to provide information on the Agricultural Sector profile, identify scarce and critical skills in this sector and provide for measures the SETA has taken or is to take to address those scarcities.

---------------------------------------------------------- Prof G Mayende Chairperson: AgriSETA Accounting Official Sign-Off

5

Endorsement It is hereby certified that this Sector Skills Plan:

Was developed by the management of the AgriSETA under the guidance of the AgriSETA Accounting Authority.

It takes into account all the relevant policies, legislation and other mandates for which the AgriSETA is responsible.

Accurately reflects the strategic outcome orientated goals and objectives which the AgriSETA will endeavour to achieve over the period 2011 to 2016.

---------------------------------------------------------- Mr P Xaba Skills Planning Manager ---------------------------------------------------------- Mr J S Madiba CEO: AgriSETA

6

List of Acronyms

ADEP Aquaculture Development and Enhancement Programme

AET Strategy The National Education and Training Strategy for Agriculture

ATIs Agricultural Training Institutes

BFAP Bureau for Food and Agricultural Policy

CPI Consumer Price Index

DAFF Department of Agriculture, Forestry and Fisheries

DHET Department of Higher Education and Training

DRDLR Department of Rural Development and Land Reform

DTI Department of Trade and Industry

FGWU Food and general Workers Union

FMP Fibre Processing and Manufacturing

GDP Gross Domestic Product

HSRC Human Sciences Research Council

IDGP Integrated Growth and Development Plan

IDP Integrated Development Plan

IPAP Industrial Policy Action Plan

KZN KwaZulu-Natal

MAFISA Micro Agricultural Financial Institution of South Africa

MTSF Medium Term Strategic Framework

NAFU National African Farmers Union of South Africa

NDP National Development Plan

NERPO National Emergent Red Meat Producers Organisation

NGP New Growth Path

NEETS Not in Employment Education or Training

NSDS III National Skills Development Strategy III

NSFAS National Student Financial Aid Scheme

QLFS Qualterly Labour Force Survey

RADP Recapitalisation and Development Programme

RPL Recognition of Prior Learning

SACAU Southern African Confederation of Agricultural Unions

SADC Southern African Development Community

SAIVECET Vocational and Continuing Education and Training

SDA Skills Development Act

SIP Strategic Integrated Project

SIZA Sustainability Initiative of South Africa

StatsSA Statistics South Africa

UIF Unemployment Insurance Fund

WSP Workplace Skills Plan

WTO World Trade Organisation

7

List of Tables

Table 1: Activities within the agricultural sector by international SIC code .................. 8 Table 2: Government department roles in relation to agriculture.............................. 11 Table 3: Commercial farming enterprises 2013 .......................................................... 15 Table 4: Distribution of employers by size and province ............................................ 18 Table 5: Distribution of employers by sebsector ......................................................... 19 Table 6: Employment in the agriculture, forestry and fisheries sector ....................... 20 Table 7: StatsSA gender distribution: agriculture, forestry and fisheries ................... 20 Table 8: Average weighted labour cost for the pome and stone fruit industries ....... 22 Table 9: Labour costs at different wine farms in the Western Cape ........................... 23 Table 11: National policy and skills development implications table ......................... 41 Table 12: Interview Analysis of Skills Demanded ........................................................ 47 Table 13: Skills demand by employer category ........................................................... 50 Table 14: Demand for skills by occupational category ................................................ 53 Table 15: Colleges of agriculture ................................................................................. 55 Table 16: AgriSETA approved training providers ......................................................... 56 Table 17: Employee trained by occupational category and gender ............................ 58 Table Table 19: StatsSA gender distribution: agriculture, forestry and fisheries ........ 61

List of Figures

Figure 1: Gross value of products, 2013/2014 ............................................................ 16 Figure 2: Sector contribution to nominal GDP (1st quarter 2015) .............................. 16 Figure 3: Provincial distribution of employers ............................................................. 17 Figure 4: Distribution of employers by size ................................................................. 18 Figure 5: Employment categories within large organisations ..................................... 22 Figure 6: Gender profile of employees ........................................................................ 23 Figure 7: Employees per subsector .............................................................................. 25 Figure 8:Age profile of employees ............................................................................... 25 Figure 9:Employees by race in the agricultural sector ................................................ 26 Figure 10:Four dimensional skills typology (based on 2005/6 agriseta research) ...... 48 Figure 11:Skills Development Interventions ................................................................ 58

8

Chapter 1: SECTOR PROFILE

1.1 Introduction

The purpose of this chapter is to provide an overview of the agricultural sector in South Africa by describing the sector, to enable an understanding of:

Scope of coverage,

Key role players,

How the sector contributes to the broader South African economy,

The employer profile

The number of people employed in the sector and their demographics. This sector profile provides the context that will inform the strategic planning required of skills planning.

1.2 Scope of coverage

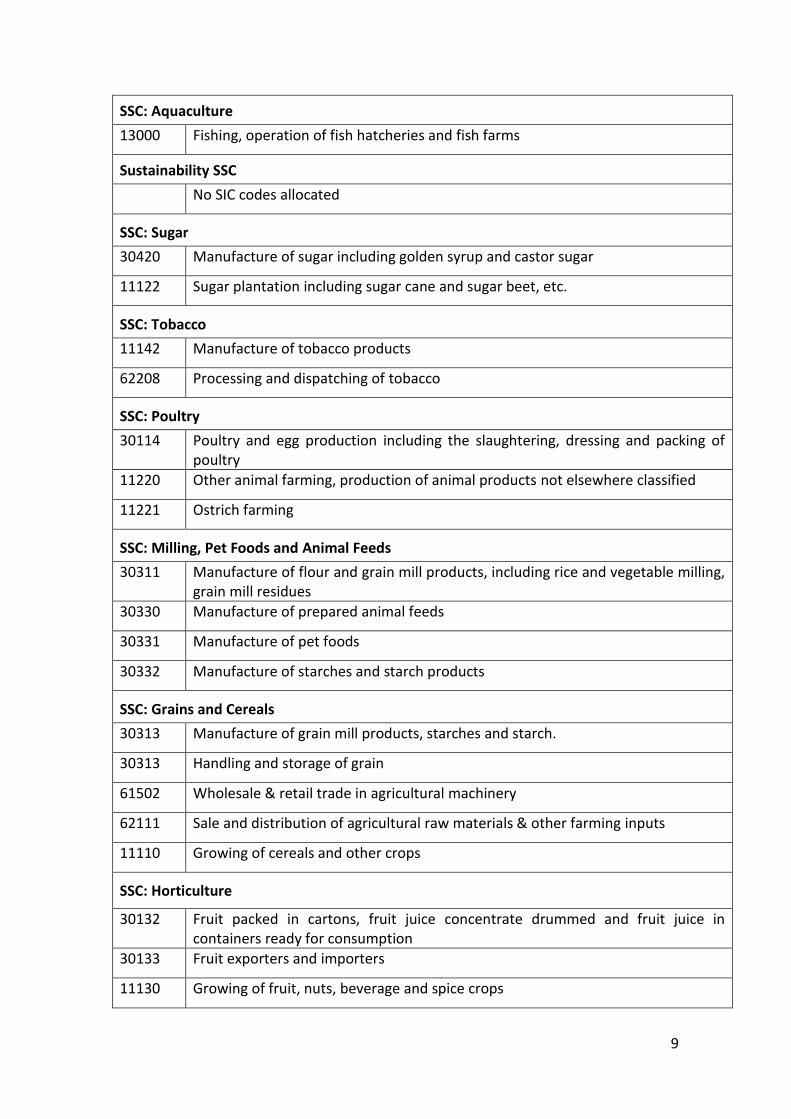

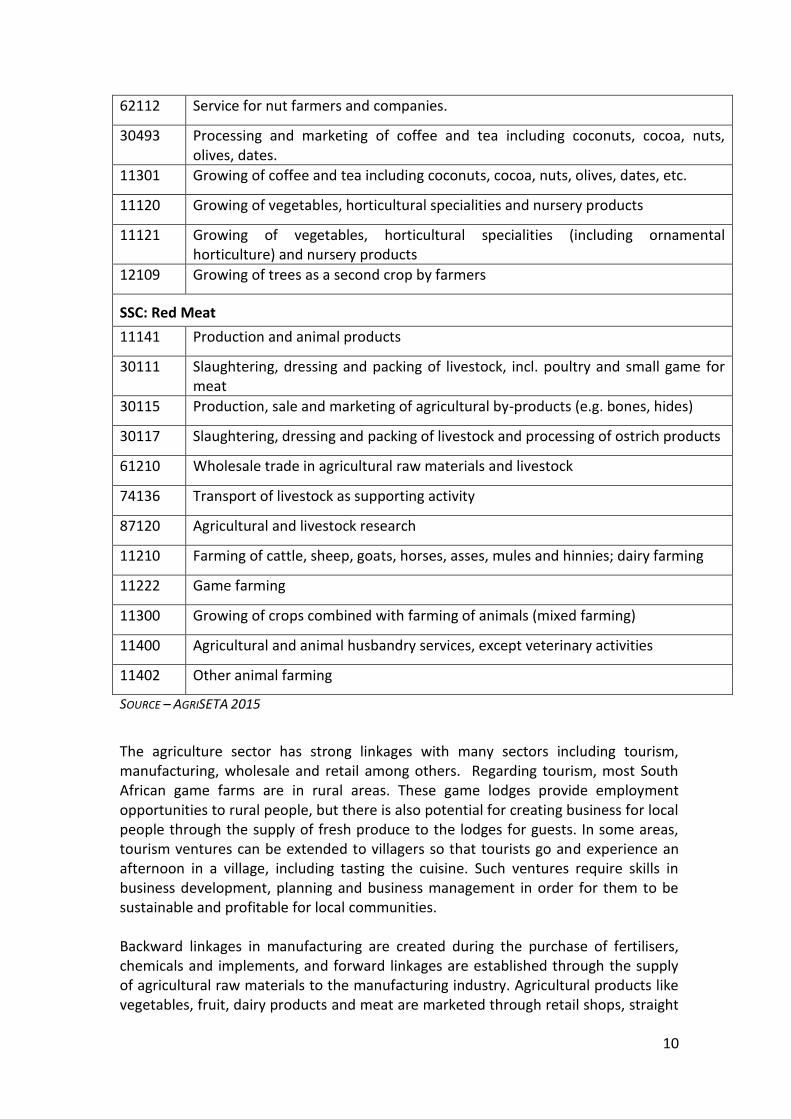

The agriculture sector in the context of skills development is based only on agricultural activity concerned with production and some primary processing of food, aquaculture and growing of trees as a secondary activity. As per the scope of coverage as determined by the Minister (AgriSETA Constitution, 2011), the agricultural sector in South Africa is divided into 41 Standard Industrial Classification (SIC) Codes that are classified according to agricultural and economic focus. The sector encompasses both primary (resource production) and secondary (primary processing) activities. Out of these 41 industries, AgriSETA has constituted twelve sub-sector committees. Table 1 below illustrates the allocation of the 41 industries into 12 sub-sectors, their codes, as well as their area of focus. These 12 sub-sector committees are as follows: Seed; Pest Control; Fibre; Aquaculture; Sustainability; Sugar; Tobacco; Poultry; Milling Pet Foods and Animal Feeds; Grains and Cereals; Horticulture; and Red Meat. Table 1: Activities within the agricultural sector by international SIC code

SIC Code Scope of Coverage / Description

SSC: Seed

11140 Seed production and marketing

SSC: Pest Control

99003 Pest control

SSC: Fibre

30118 Grading, ginning and packing of wool and cotton raw material.

9

SSC: Aquaculture

13000 Fishing, operation of fish hatcheries and fish farms

Sustainability SSC

No SIC codes allocated

SSC: Sugar

30420 Manufacture of sugar including golden syrup and castor sugar

11122 Sugar plantation including sugar cane and sugar beet, etc.

SSC: Tobacco

11142 Manufacture of tobacco products

62208 Processing and dispatching of tobacco

SSC: Poultry

30114 Poultry and egg production including the slaughtering, dressing and packing of poultry

11220 Other animal farming, production of animal products not elsewhere classified

11221 Ostrich farming

SSC: Milling, Pet Foods and Animal Feeds

30311 Manufacture of flour and grain mill products, including rice and vegetable milling, grain mill residues

30330 Manufacture of prepared animal feeds

30331 Manufacture of pet foods

30332 Manufacture of starches and starch products

SSC: Grains and Cereals

30313 Manufacture of grain mill products, starches and starch.

30313 Handling and storage of grain

61502 Wholesale & retail trade in agricultural machinery

62111 Sale and distribution of agricultural raw materials & other farming inputs

11110 Growing of cereals and other crops

SSC: Horticulture

30132 Fruit packed in cartons, fruit juice concentrate drummed and fruit juice in containers ready for consumption

30133 Fruit exporters and importers

11130 Growing of fruit, nuts, beverage and spice crops

10

62112 Service for nut farmers and companies.

30493 Processing and marketing of coffee and tea including coconuts, cocoa, nuts, olives, dates.

11301 Growing of coffee and tea including coconuts, cocoa, nuts, olives, dates, etc.

11120 Growing of vegetables, horticultural specialities and nursery products

11121 Growing of vegetables, horticultural specialities (including ornamental horticulture) and nursery products

12109 Growing of trees as a second crop by farmers

SSC: Red Meat

11141 Production and animal products

30111 Slaughtering, dressing and packing of livestock, incl. poultry and small game for meat

30115 Production, sale and marketing of agricultural by-products (e.g. bones, hides)

30117 Slaughtering, dressing and packing of livestock and processing of ostrich products

61210 Wholesale trade in agricultural raw materials and livestock

74136 Transport of livestock as supporting activity

87120 Agricultural and livestock research

11210 Farming of cattle, sheep, goats, horses, asses, mules and hinnies; dairy farming

11222 Game farming

11300 Growing of crops combined with farming of animals (mixed farming)

11400 Agricultural and animal husbandry services, except veterinary activities

11402 Other animal farming

SOURCE – AGRISETA 2015

The agriculture sector has strong linkages with many sectors including tourism, manufacturing, wholesale and retail among others. Regarding tourism, most South African game farms are in rural areas. These game lodges provide employment opportunities to rural people, but there is also potential for creating business for local people through the supply of fresh produce to the lodges for guests. In some areas, tourism ventures can be extended to villagers so that tourists go and experience an afternoon in a village, including tasting the cuisine. Such ventures require skills in business development, planning and business management in order for them to be sustainable and profitable for local communities. Backward linkages in manufacturing are created during the purchase of fertilisers, chemicals and implements, and forward linkages are established through the supply of agricultural raw materials to the manufacturing industry. Agricultural products like vegetables, fruit, dairy products and meat are marketed through retail shops, straight

11

from the farm. The agricultural sector therefore directly and indirectly creates employment for a significant number of people.

1.3 Key role players

1.3.1 National government departments

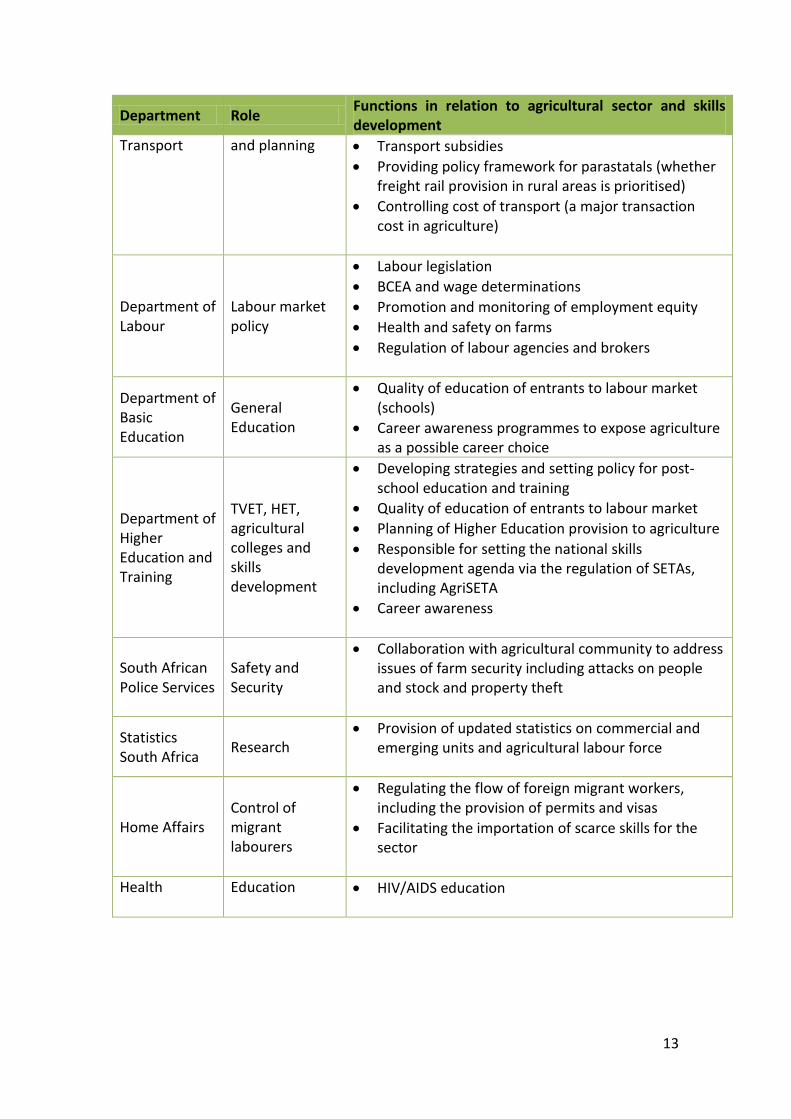

There are a number of government departments, nationally and in provinces as well as local municipalities involved in the agricultural sector. The following table sets out the broad contribution that each department makes to the agricultural sector. Table 2: Government department roles in relation to agriculture

Department Role Functions in relation to agricultural sector and skills development

Department of Agriculture, Forestry and Fisheries

Agricultural policy and support

Sector regulatory framework

Sector strategy and leadership

Organisation of support to farmers (extension services)

Sector BEE charter

Funding of development interventions in support of agriculture including provision of bursaries for scarce skills

Department of Rural Development and Land Reform

Land Reform and land claims settlements

Settling claims

Ensuring that farms remain functional pending the settlement of claims

Identifying claimants who wish to develop agricultural enterprises

Partnering with AgriSETA in mobilising funds for capacity building of claimants

Making land available for renting or purchase for farming

Custodians of the Recapitalisation and Development Programme implemented in 2009. Since then this has been revised in alignment with the National Development Plan, providing the enabling mechanism for land reform in the country.

Department of Economic Development

Economic planning

Sector economic strategies

Identification of economic policy levers and interventions and motivation of these in cabinet

National Treasury and SARS

Macro-economic policy

Financial planning

Financial incentives

Accountability of Land Bank

Regulations relating to credit

VAT, PAYE and company tax

12

Department Role Functions in relation to agricultural sector and skills development

National Planning Commission

Planning

Macro strategy in relation to land reform and rural development

Identification of inter-departmental overlaps and gaps

Department of Cooperative Governance and Traditional Affairs (and municipalities)

Municipal capacity development and coordination

Linking agricultural and rural development to IDPs and LED

Infrastructure and services to agricultural enterprises

Land and industrial zone management (making suitable space available for enterprises)

Department of Environmental Affairs

Environmental planning and natural resource management

Policy and guidelines on environment protection and natural resource management

Partner in environmental education

Department of Trade and Industry (and provincial departments of economic development)

Industrial strategy

IPAP 2

BEE codes

Identification of growth areas

Identification and promotion of export opportunities

Trade policies and international agreements on access to markets (WTO, GATT. DOHA)

SMME and cooperative registration (CIPRO)

SEDA services to SMMEs and Cooperatives

Provincial development agencies and banks (Wesgro, Ithala, etc.) who provide funds and advice on marketing and trade etc.

Has a sector desk focussing on agro-processing and agricultural strategy and policy implementation.

Informal unit within the Enterprise Development Unit also focuses on informal sector development in agriculture.

Department of Water Affairs

The management of water supply

Water supply

Boreholes

Regulation and management of water and prevention of waste/excess use. Responsible for Water Boards that manage local irrigation schemes

Department of Energy

Energy supply Strategy in relation to electricity supply to rural areas

Cost of power (Eskom)

Department of Transport policy Planning for transport needs in rural areas

13

Department Role Functions in relation to agricultural sector and skills development

Transport and planning Transport subsidies

Providing policy framework for parastatals (whether freight rail provision in rural areas is prioritised)

Controlling cost of transport (a major transaction cost in agriculture)

Department of Labour

Labour market policy

Labour legislation

BCEA and wage determinations

Promotion and monitoring of employment equity

Health and safety on farms

Regulation of labour agencies and brokers

Department of Basic Education

General Education

Quality of education of entrants to labour market (schools)

Career awareness programmes to expose agriculture as a possible career choice

Department of Higher Education and Training

TVET, HET, agricultural colleges and skills development

Developing strategies and setting policy for post-school education and training

Quality of education of entrants to labour market

Planning of Higher Education provision to agriculture

Responsible for setting the national skills development agenda via the regulation of SETAs, including AgriSETA

Career awareness

South African Police Services

Safety and Security

Collaboration with agricultural community to address issues of farm security including attacks on people and stock and property theft

Statistics South Africa

Research Provision of updated statistics on commercial and

emerging units and agricultural labour force

Home Affairs Control of migrant labourers

Regulating the flow of foreign migrant workers, including the provision of permits and visas

Facilitating the importation of scarce skills for the sector

Health Education HIV/AIDS education

14

1.3.2 Sector representatives

There are two major umbrella organisations representing the interests of farmers, AgriSA and the National African Farmers Union of South Africa (NAFU). AgriSA represents both commercial farmers and cooperatives’ interests through its engagement at national (has structures in all the provinces, except Limpopo) and international level. AgriSA is a member of the Southern African Confederation of Agricultural Unions (SACAU), a regional farmers’ union for farmers in Southern Africa. NAFU is a union for predominantly previously historically disadvantaged smallholder farmers with a membership base including farmers, agribusinesses, farmers’ organisations, corporations and individuals who support their goals. Different unions in all provinces represent NAFU. There are other employer organisations who are not affiliated to AgriSA and NAFU including:

Agricultural Industrial and Medium Employers Organisation

Agricultural, Mining and Industrial Chemical Manufacturers’ Association

Agrilabour Employers’ Organisation

Algoa Meat Traders Association

East Coast Poultry Producers Employers’ Association

East London and District Meat Traders Association

Fertiliser Industry Employers’ Organisation

Landbou Werkgewers organisasie

Red Meat Producers’ Association

1.4 Economic performance

1.4.1 Overview of structure of the sector

South Africa has a dual agricultural economy comprising a well-developed commercial sector (also referred to as formal) and a predominantly subsistence-oriented sector (also known as informal) in the rural areas (GCIS, 2012). In recent years, the commercial sector has been slowly transforming from a predominantly white owned sector and now includes what are referred to as ‘emerging’ or ‘new’ farmers, who have acquired agricultural land as part of government’s effort to transform the agricultural sector. Using data from the Stats SA 2007 commercial agriculture census and data from other multiple sources, Kirsten1 estimates the number of commercial farms in South Africa in 2013 to be 69 996, comprising 39 966 farms registered for value added tax (VAT) and another 30 000 that are not registered for VAT. Of the VAT registered farms, the sector is dominated by farms with an income of less than R500 000 as highlighted in Table 3.

1Personal email communication. The figures in this table were presented by Prof Johann Kirsten at an Agri

meeting in the Free State in July 2013.

15

Table 3: Commercial farming enterprises 2013

SOURCE: PROF JOHANN KIRSTEN, 2013

There is uncertainty about the number of smallholder farmers in South Africa and figures vary between 160 000 to 2.4 million, depending on the source (Pienaar, 2013). Subsistence farming for supplementing income and food reserves is also a feature of the agricultural sector. In 2013, 18.9% (up from 18.1% in 2012) of 25 330 South African households surveyed were involved in agricultural production, with 14,2% (up from 10.8% in 2012) cultivating farmland and 87.8% (down from 90,2%, in 2012) working on backyard gardens. There is scope for AgriSETA to provide skills development interventions to the subsistence sector, which receives very limited training.2 Useful training would be on livestock and crop production, as well as marketing for those who are farming to supplement their income. Skills would improve the efficiency and effectiveness of subsistence activities, which could contribute significantly to the national basket if subsistence farmers are linked up with markets.

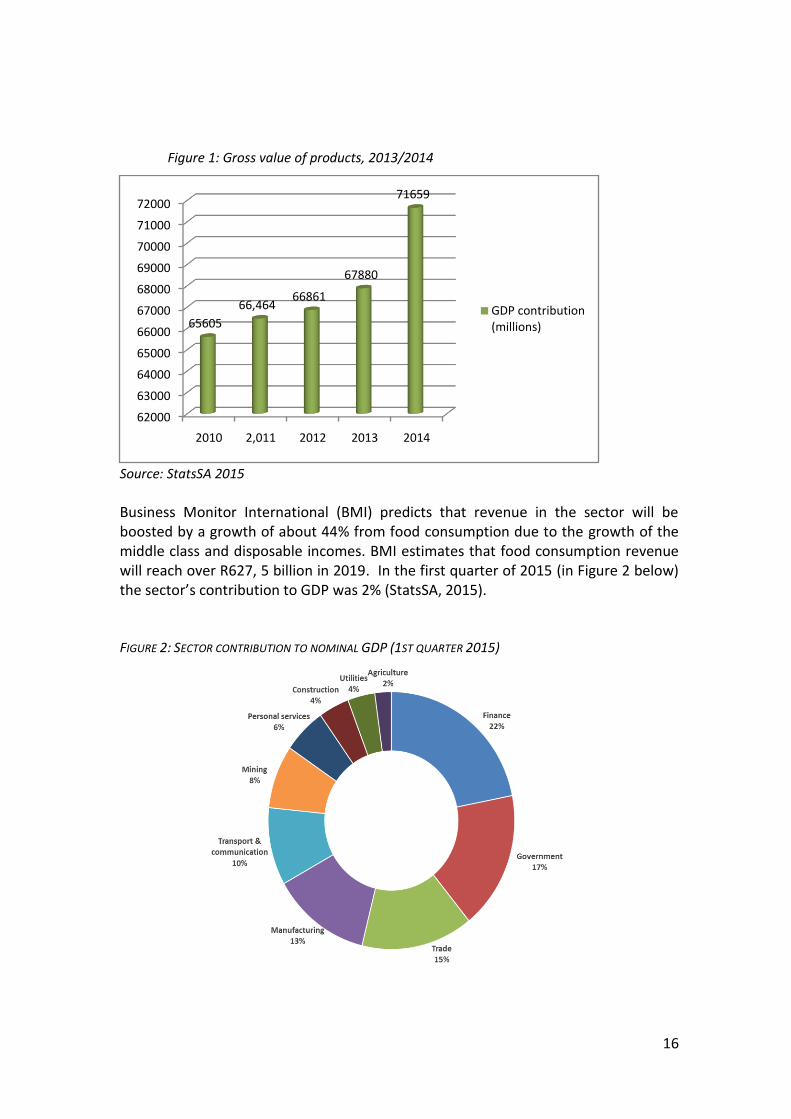

1.4.2 GDP Contribution

The gross domestic product (GDP) contribution of primary commercial agriculture to South Africa’s economy is about 3%, and reaches 12% when the whole agricultural value chain is considered. 3 Over the past five years, the contribution of the agriculture, forestry and fisheries sector to the GDP has seen a steady increase as reflected in Figure 1.

2 Less than 3% of households surveyed indicated they received any training

3South Africa Yearbook 2013/2014, p.31

Category (Gross Farm Income) Number of farming units

Share of commercial farming units

R5 million and more 2 927 4.1%

R3 million to R5 million 2 172 3.1%

R500 000 to R3 million 12 290 17.57%

Less than R500 000 22 577 32.27%

Total (VAT registered famers) 39 966 57.12%

Other commercial farmers (not registered for VAT) (Census 2011)

30 000 42.88%

Total commercial farmers 69 966 100%

16

Figure 1: Gross value of products, 2013/2014

Source: StatsSA 2015

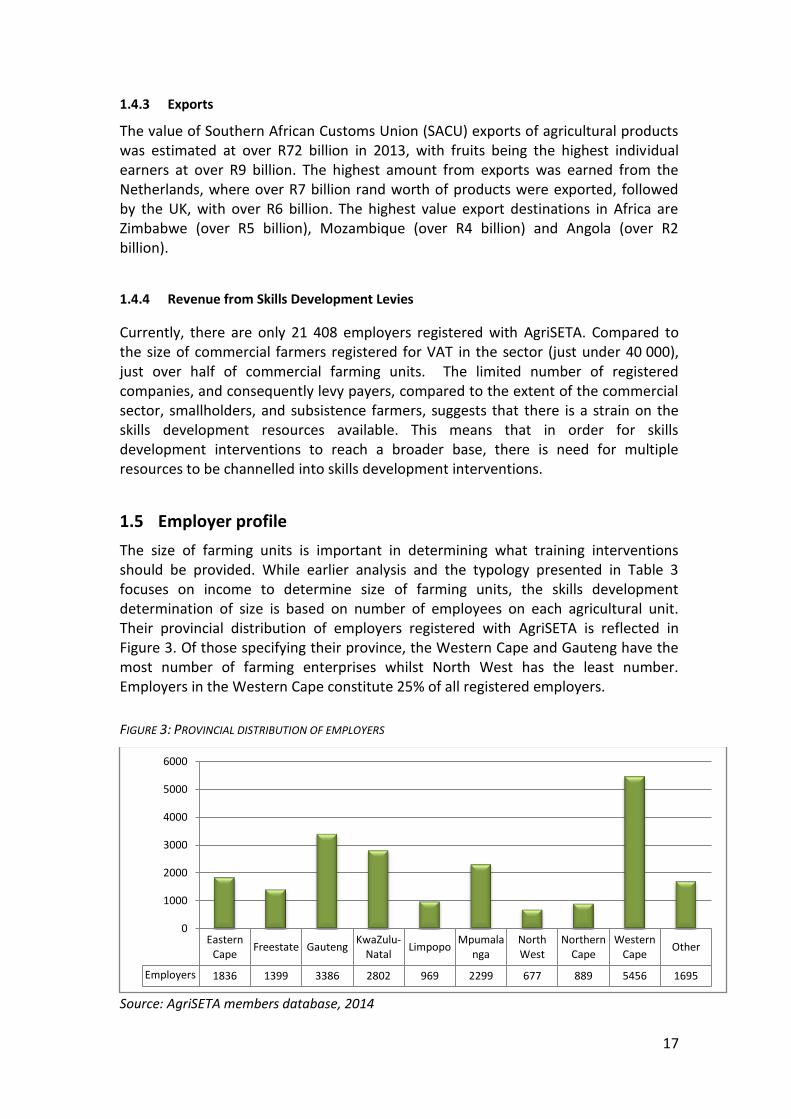

Business Monitor International (BMI) predicts that revenue in the sector will be boosted by a growth of about 44% from food consumption due to the growth of the middle class and disposable incomes. BMI estimates that food consumption revenue will reach over R627, 5 billion in 2019. In the first quarter of 2015 (in Figure 2 below) the sector’s contribution to GDP was 2% (StatsSA, 2015). FIGURE 2: SECTOR CONTRIBUTION TO NOMINAL GDP (1ST QUARTER 2015)

62000

63000

64000

65000

66000

67000

68000

69000

70000

71000

72000

2010 2,011 2012 2013 2014

65605

66,46466861

67880

71659

GDP contribution (millions)

17

1.4.3 Exports

The value of Southern African Customs Union (SACU) exports of agricultural products was estimated at over R72 billion in 2013, with fruits being the highest individual earners at over R9 billion. The highest amount from exports was earned from the Netherlands, where over R7 billion rand worth of products were exported, followed by the UK, with over R6 billion. The highest value export destinations in Africa are Zimbabwe (over R5 billion), Mozambique (over R4 billion) and Angola (over R2 billion).

1.4.4 Revenue from Skills Development Levies

Currently, there are only 21 408 employers registered with AgriSETA. Compared to the size of commercial farmers registered for VAT in the sector (just under 40 000), just over half of commercial farming units. The limited number of registered companies, and consequently levy payers, compared to the extent of the commercial sector, smallholders, and subsistence farmers, suggests that there is a strain on the skills development resources available. This means that in order for skills development interventions to reach a broader base, there is need for multiple resources to be channelled into skills development interventions.

1.5 Employer profile

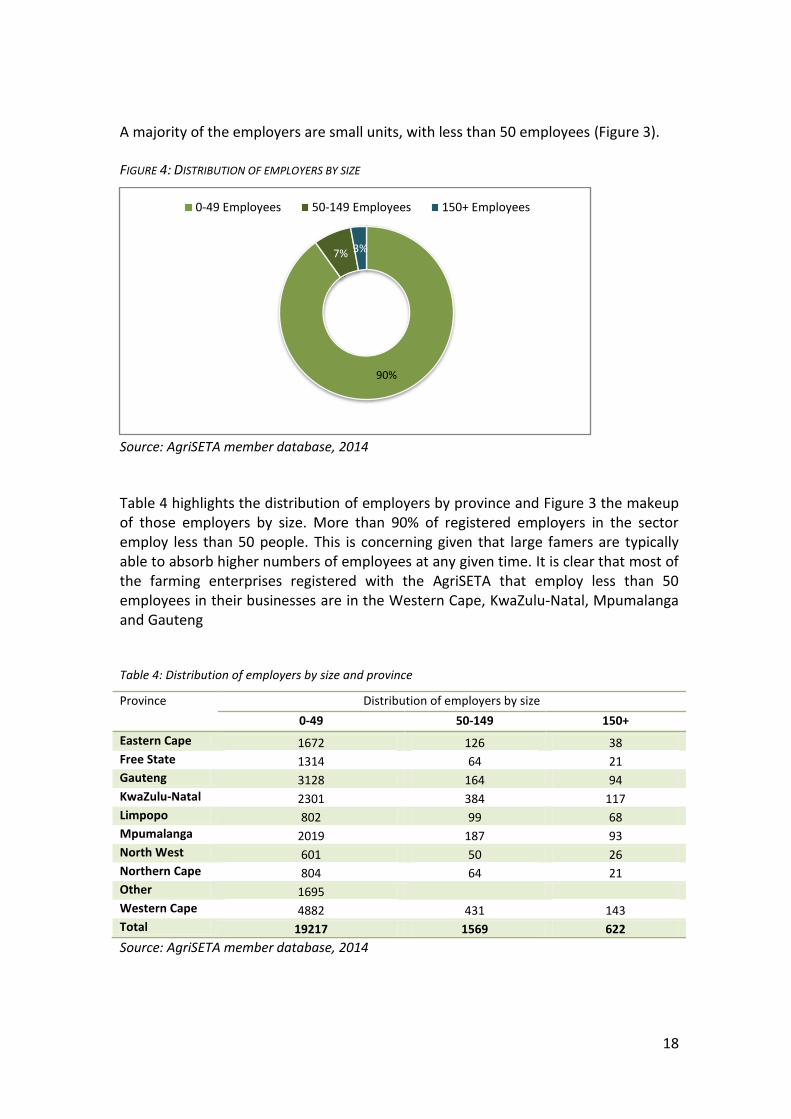

The size of farming units is important in determining what training interventions should be provided. While earlier analysis and the typology presented in Table 3 focuses on income to determine size of farming units, the skills development determination of size is based on number of employees on each agricultural unit. Their provincial distribution of employers registered with AgriSETA is reflected in Figure 3. Of those specifying their province, the Western Cape and Gauteng have the most number of farming enterprises whilst North West has the least number. Employers in the Western Cape constitute 25% of all registered employers.

FIGURE 3: PROVINCIAL DISTRIBUTION OF EMPLOYERS

Source: AgriSETA members database, 2014

Eastern Cape

Freestate GautengKwaZulu-

NatalLimpopo

Mpumalanga

North West

Northern Cape

Western Cape

Other

Employers 1836 1399 3386 2802 969 2299 677 889 5456 1695

0

1000

2000

3000

4000

5000

6000

18

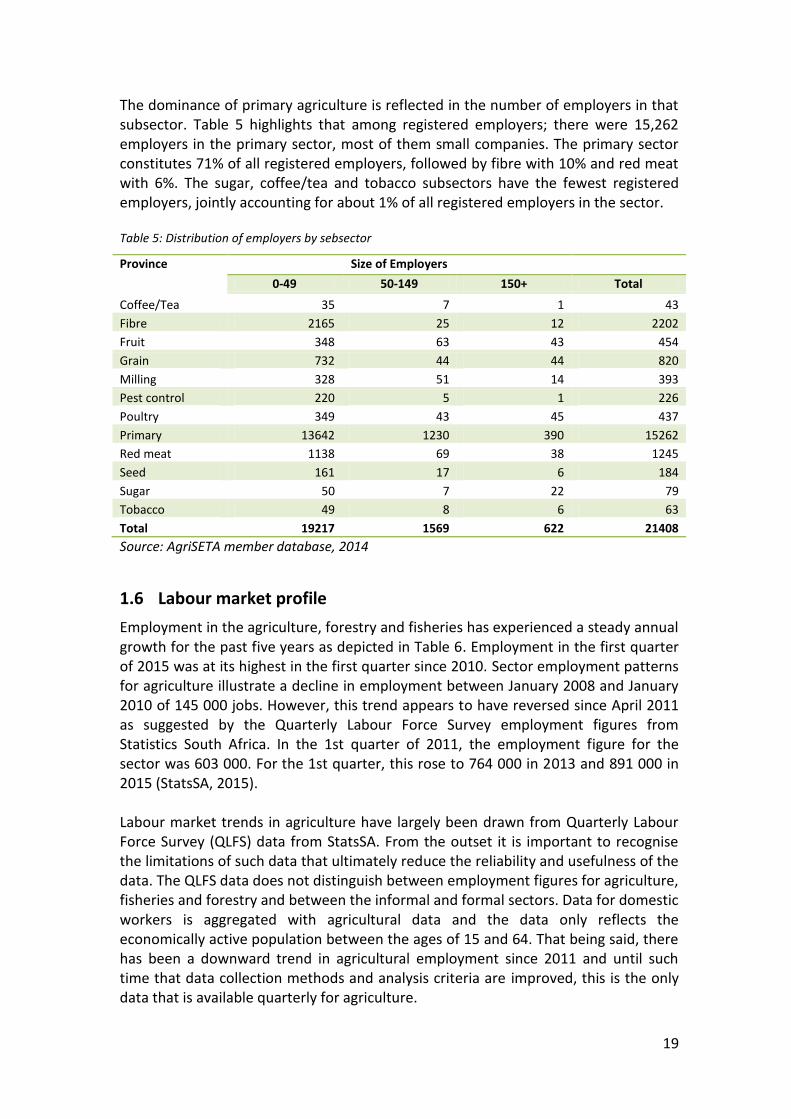

A majority of the employers are small units, with less than 50 employees (Figure 3). FIGURE 4: DISTRIBUTION OF EMPLOYERS BY SIZE

Source: AgriSETA member database, 2014

Table 4 highlights the distribution of employers by province and Figure 3 the makeup of those employers by size. More than 90% of registered employers in the sector employ less than 50 people. This is concerning given that large famers are typically able to absorb higher numbers of employees at any given time. It is clear that most of the farming enterprises registered with the AgriSETA that employ less than 50 employees in their businesses are in the Western Cape, KwaZulu-Natal, Mpumalanga and Gauteng Table 4: Distribution of employers by size and province

Province Distribution of employers by size

0-49 50-149 150+

Eastern Cape 1672 126 38 Free State 1314 64 21 Gauteng 3128 164 94 KwaZulu-Natal 2301 384 117 Limpopo 802 99 68 Mpumalanga 2019 187 93 North West 601 50 26 Northern Cape 804 64 21 Other 1695

Western Cape 4882 431 143 Total 19217 1569 622

Source: AgriSETA member database, 2014

90%

7% 3%

0-49 Employees 50-149 Employees 150+ Employees

19

The dominance of primary agriculture is reflected in the number of employers in that subsector. Table 5 highlights that among registered employers; there were 15,262 employers in the primary sector, most of them small companies. The primary sector constitutes 71% of all registered employers, followed by fibre with 10% and red meat with 6%. The sugar, coffee/tea and tobacco subsectors have the fewest registered employers, jointly accounting for about 1% of all registered employers in the sector. Table 5: Distribution of employers by sebsector

Province Size of Employers

0-49 50-149 150+ Total

Coffee/Tea 35 7 1 43

Fibre 2165 25 12 2202

Fruit 348 63 43 454

Grain 732 44 44 820

Milling 328 51 14 393

Pest control 220 5 1 226

Poultry 349 43 45 437

Primary 13642 1230 390 15262

Red meat 1138 69 38 1245

Seed 161 17 6 184

Sugar 50 7 22 79

Tobacco 49 8 6 63

Total 19217 1569 622 21408

Source: AgriSETA member database, 2014

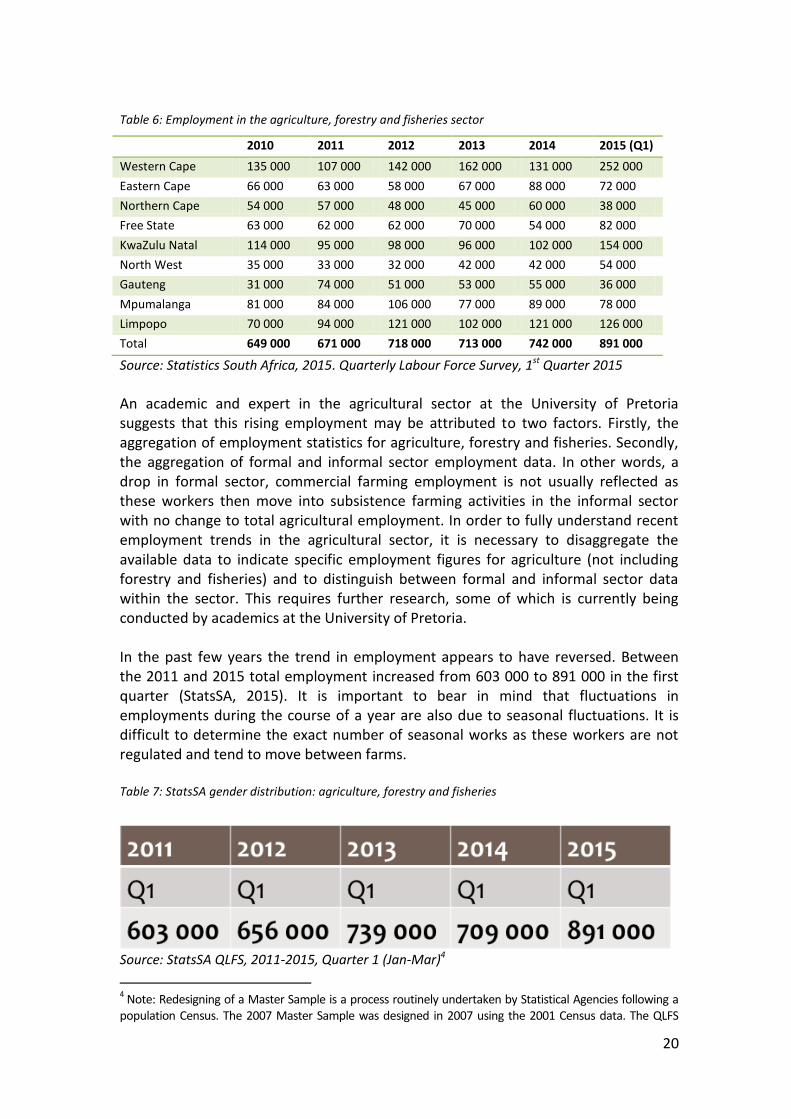

1.6 Labour market profile

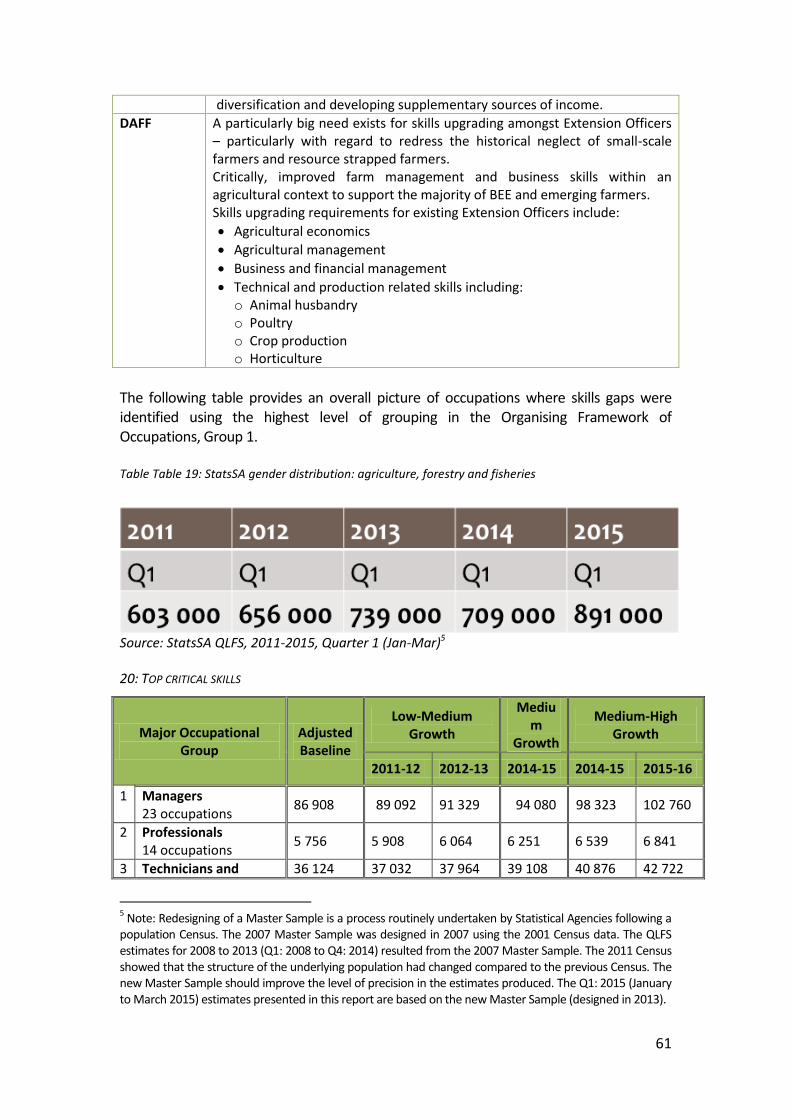

Employment in the agriculture, forestry and fisheries has experienced a steady annual growth for the past five years as depicted in Table 6. Employment in the first quarter of 2015 was at its highest in the first quarter since 2010. Sector employment patterns for agriculture illustrate a decline in employment between January 2008 and January 2010 of 145 000 jobs. However, this trend appears to have reversed since April 2011 as suggested by the Quarterly Labour Force Survey employment figures from Statistics South Africa. In the 1st quarter of 2011, the employment figure for the sector was 603 000. For the 1st quarter, this rose to 764 000 in 2013 and 891 000 in 2015 (StatsSA, 2015). Labour market trends in agriculture have largely been drawn from Quarterly Labour Force Survey (QLFS) data from StatsSA. From the outset it is important to recognise the limitations of such data that ultimately reduce the reliability and usefulness of the data. The QLFS data does not distinguish between employment figures for agriculture, fisheries and forestry and between the informal and formal sectors. Data for domestic workers is aggregated with agricultural data and the data only reflects the economically active population between the ages of 15 and 64. That being said, there has been a downward trend in agricultural employment since 2011 and until such time that data collection methods and analysis criteria are improved, this is the only data that is available quarterly for agriculture.

20

Table 6: Employment in the agriculture, forestry and fisheries sector

2010 2011 2012 2013 2014 2015 (Q1)

Western Cape 135 000 107 000 142 000 162 000 131 000 252 000

Eastern Cape 66 000 63 000 58 000 67 000 88 000 72 000

Northern Cape 54 000 57 000 48 000 45 000 60 000 38 000

Free State 63 000 62 000 62 000 70 000 54 000 82 000

KwaZulu Natal 114 000 95 000 98 000 96 000 102 000 154 000

North West 35 000 33 000 32 000 42 000 42 000 54 000

Gauteng 31 000 74 000 51 000 53 000 55 000 36 000

Mpumalanga 81 000 84 000 106 000 77 000 89 000 78 000

Limpopo 70 000 94 000 121 000 102 000 121 000 126 000

Total 649 000 671 000 718 000 713 000 742 000 891 000

Source: Statistics South Africa, 2015. Quarterly Labour Force Survey, 1st Quarter 2015

An academic and expert in the agricultural sector at the University of Pretoria suggests that this rising employment may be attributed to two factors. Firstly, the aggregation of employment statistics for agriculture, forestry and fisheries. Secondly, the aggregation of formal and informal sector employment data. In other words, a drop in formal sector, commercial farming employment is not usually reflected as these workers then move into subsistence farming activities in the informal sector with no change to total agricultural employment. In order to fully understand recent employment trends in the agricultural sector, it is necessary to disaggregate the available data to indicate specific employment figures for agriculture (not including forestry and fisheries) and to distinguish between formal and informal sector data within the sector. This requires further research, some of which is currently being conducted by academics at the University of Pretoria. In the past few years the trend in employment appears to have reversed. Between the 2011 and 2015 total employment increased from 603 000 to 891 000 in the first quarter (StatsSA, 2015). It is important to bear in mind that fluctuations in employments during the course of a year are also due to seasonal fluctuations. It is difficult to determine the exact number of seasonal works as these workers are not regulated and tend to move between farms. Table 7: StatsSA gender distribution: agriculture, forestry and fisheries

Source: StatsSA QLFS, 2011-2015, Quarter 1 (Jan-Mar)4

4 Note: Redesigning of a Master Sample is a process routinely undertaken by Statistical Agencies following a

population Census. The 2007 Master Sample was designed in 2007 using the 2001 Census data. The QLFS

21

South Africa recorded an unemployment rate of 26,4% (StatsSA, 2015) in the first quarter of 2014 (narrow definition). South Africa now has a NEET (not in employment, education or training) youth population of approximately 3,4 million people. The sheer scale of the crisis demands each and every sector’s involvement in addressing it. Although employment has decreased overall in the sector, employment trends have varied by sub-sector. Because of increased productivity, the wool growing sub-sector has experienced an increase in employment. Currently there are 35 000 farm workers involved in wool farming. There has been an additional 2 000 emerging farmers over the past few years, with close to 20 000 emerging farmers farming in wool. In the sugar sub-sector, there has also been an increase in employment because of land restitution and redistribution programmes which have led to a demand for seasonal and permanent workers. Sugar cane farming is labour intensive. While some employment growth has been experienced at sub-sector level, some companies that have expanded have also realised employment growth, for example, one of the interviewed grain companies has realised a 40% increase in employment from value adding services like abattoirs and feed mills. Elsewhere in the grain sub-sector employment has been stable in the last five years. Influence of weather conditions is big in the sub-sector so there has been fluctuating production. The sub-sector is not labour intensive in most of the functions, so output can increase without added human resource requirements (stakeholder interviews: 2014).

1.6.1 Occupational categories

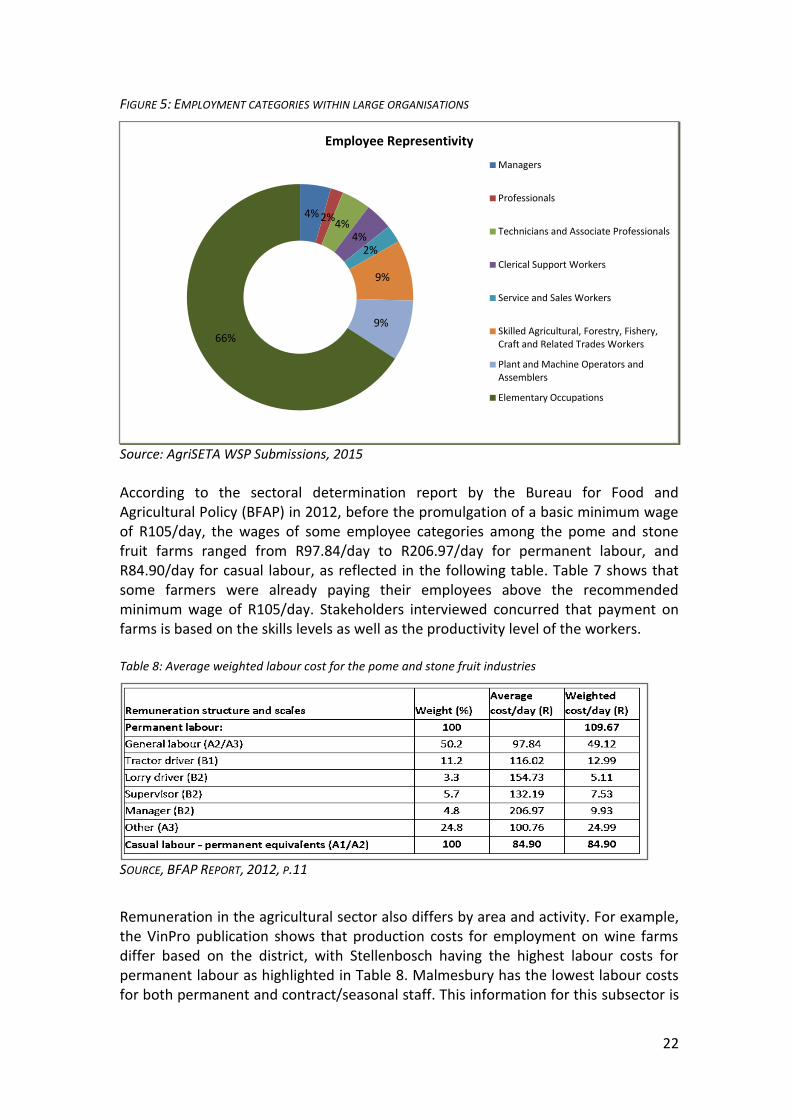

The skills requirements for agricultural units vary from highly skilled managerial and professional occupations to fairly low level skills for elementary occupations. An analysis of WSPs submitted by large employers in 2015 shows that the majority of employees (66%) are engaged in elementary occupations followed by Skilled Agricultural, Forestry, Fishery, Craft and Related Trades Workers (9%) and Plant and Machine Operators and Assemblers (9%). Professionals and the Service and Sales Workers have the lowest representivity at 1.8% and 2.5% respectively (Figure 5).

estimates for 2008 to 2013 (Q1: 2008 to Q4: 2014) resulted from the 2007 Master Sample. The 2011 Census showed that the structure of the underlying population had changed compared to the previous Census. The new Master Sample should improve the level of precision in the estimates produced. The Q1: 2015 (January to March 2015) estimates presented in this report are based on the new Master Sample (designed in 2013).

22

FIGURE 5: EMPLOYMENT CATEGORIES WITHIN LARGE ORGANISATIONS

Source: AgriSETA WSP Submissions, 2015

According to the sectoral determination report by the Bureau for Food and Agricultural Policy (BFAP) in 2012, before the promulgation of a basic minimum wage of R105/day, the wages of some employee categories among the pome and stone fruit farms ranged from R97.84/day to R206.97/day for permanent labour, and R84.90/day for casual labour, as reflected in the following table. Table 7 shows that some farmers were already paying their employees above the recommended minimum wage of R105/day. Stakeholders interviewed concurred that payment on farms is based on the skills levels as well as the productivity level of the workers. Table 8: Average weighted labour cost for the pome and stone fruit industries

SOURCE, BFAP REPORT, 2012, P.11

Remuneration in the agricultural sector also differs by area and activity. For example, the VinPro publication shows that production costs for employment on wine farms differ based on the district, with Stellenbosch having the highest labour costs for permanent labour as highlighted in Table 8. Malmesbury has the lowest labour costs for both permanent and contract/seasonal staff. This information for this subsector is

4% 2%4%

4%2%

9%

9%

66%

Employee Representivity

Managers

Professionals

Technicians and Associate Professionals

Clerical Support Workers

Service and Sales Workers

Skilled Agricultural, Forestry, Fishery, Craft and Related Trades Workers

Plant and Machine Operators and Assemblers

Elementary Occupations

23

useful in determining the interventions on skills. Data on salaries for top end agriculture professionals is not easily available, as no surveys have been done on this information. However, Quantec data shows that in 2014, compensation to employees constituted 27.69% of farming costs. Table 9: Labour costs at different wine farms in the Western Cape

Source: Vinpro Cost Guide 2013/2014, p. 15

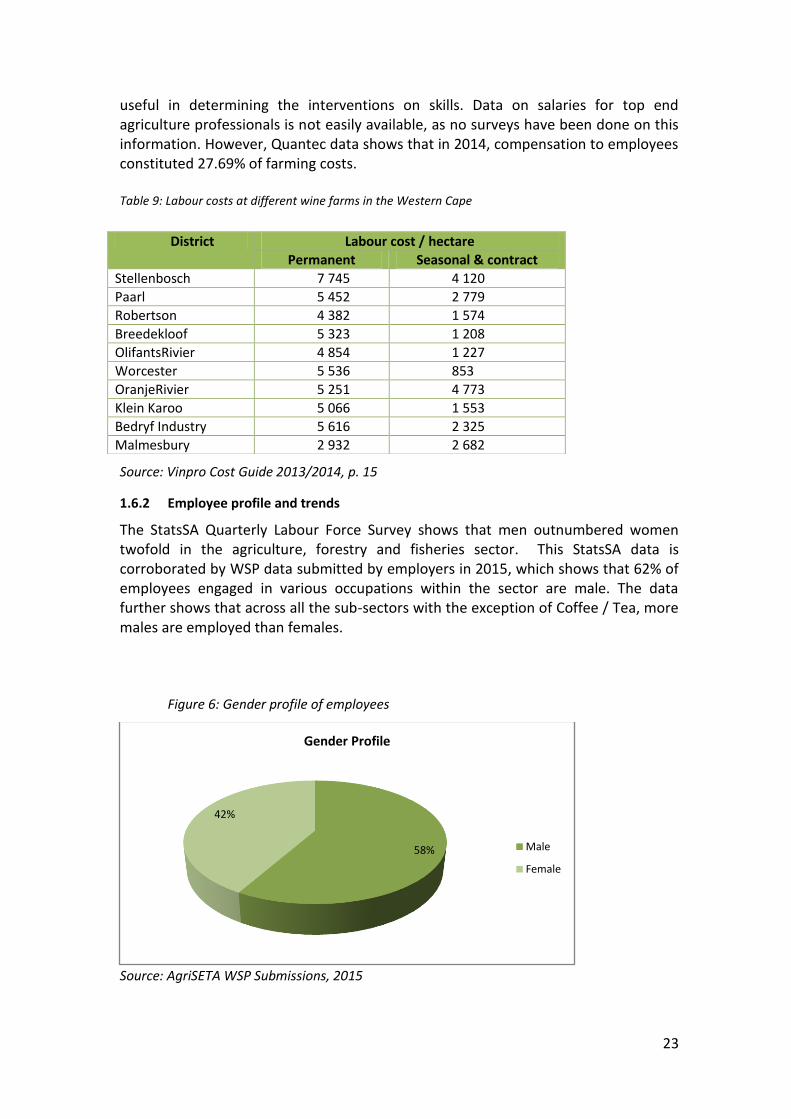

1.6.2 Employee profile and trends

The StatsSA Quarterly Labour Force Survey shows that men outnumbered women twofold in the agriculture, forestry and fisheries sector. This StatsSA data is corroborated by WSP data submitted by employers in 2015, which shows that 62% of employees engaged in various occupations within the sector are male. The data further shows that across all the sub-sectors with the exception of Coffee / Tea, more males are employed than females.

Figure 6: Gender profile of employees

Source: AgriSETA WSP Submissions, 2015

58%

42%

Gender Profile

Male

Female

District Labour cost / hectare

Permanent Seasonal & contract

Stellenbosch 7 745 4 120

Paarl 5 452 2 779

Robertson 4 382 1 574

Breedekloof 5 323 1 208

OlifantsRivier 4 854 1 227

Worcester 5 536 853

OranjeRivier 5 251 4 773

Klein Karoo 5 066 1 553

Bedryf Industry 5 616 2 325

Malmesbury 2 932 2 682

24

Analysis of WSP submissions by employers in 2014 shows that the majority of employees are in the primary sub-sector (57%) followed by grain and poultry at 11% each. Coffee / Tea sub-sector has the least representivity of workers with 0.4% of the workforce (Figure 6).

25

Figure 7: Employees per subsector

Source: AgriSETA WSP Submissions

Half of the people employed in the sector amongst the employers submitting WSPs are in the ages 35 to 55. Young people below the age of 35 constitute 42% of people employed whilst 8% are above the age of 55. All in all, over 90% of the workers are below the age of 55 (Figure 7). Due to a high number of people between the age 35 and 55 it may be important to understand amongst those, which ones are approaching the age of 55, which makes people eligible for early retirement.

Figure 8:Age profile of employees

Source: AgriSETA WSP Submissions, 2015

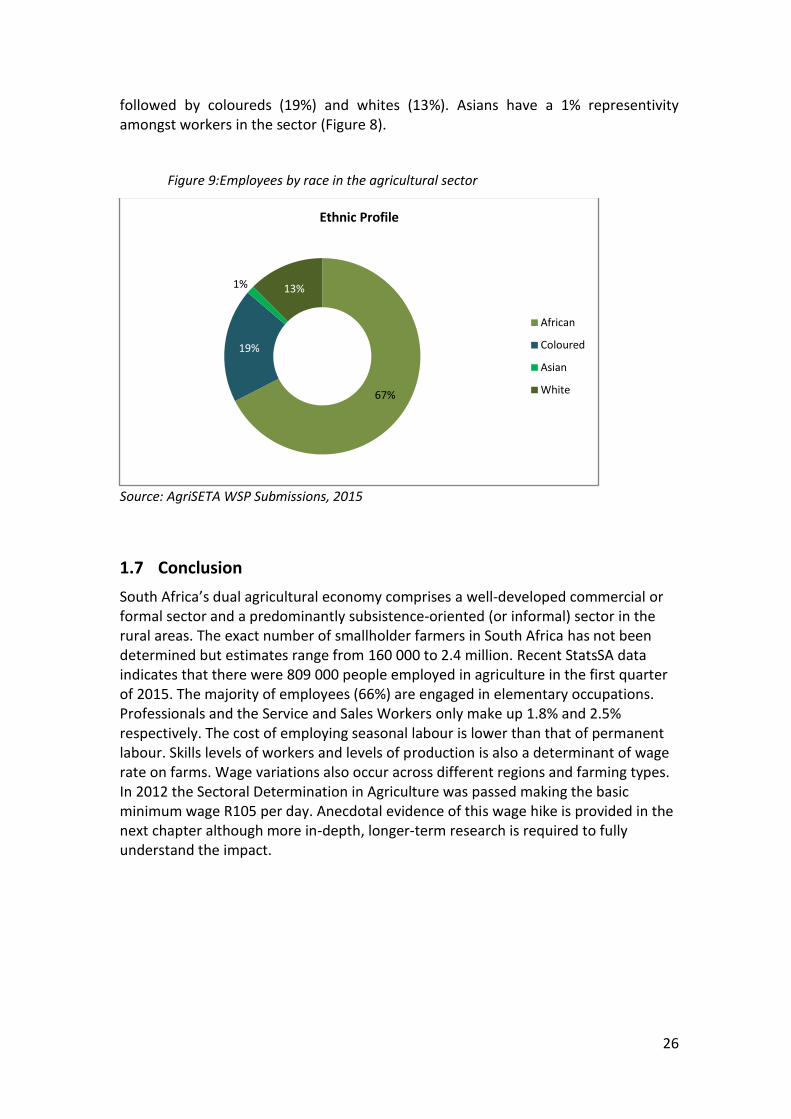

There are more Africans employed in the sector than any other race. The WSP data shows that about 67% of workers engaged by employers in the sector are Africans

0% 2%

7%11% 2%

0%

11%

57%

6% 1% 2% 1%

Employees per Subsector

Coffee / Tea

Fibre

Fruit

Grain

Milling

Pest control

Poultry

Primary

Red meat

Seed

Sugar

Tobacco

42%

50%

8%

Employee Age Profile

Age Group - Less than 35

Age Group - 35 to 55

Age Group - Greater than 55

26

followed by coloureds (19%) and whites (13%). Asians have a 1% representivity amongst workers in the sector (Figure 8).

Figure 9:Employees by race in the agricultural sector

Source: AgriSETA WSP Submissions, 2015

1.7 Conclusion

South Africa’s dual agricultural economy comprises a well-developed commercial or formal sector and a predominantly subsistence-oriented (or informal) sector in the rural areas. The exact number of smallholder farmers in South Africa has not been determined but estimates range from 160 000 to 2.4 million. Recent StatsSA data indicates that there were 809 000 people employed in agriculture in the first quarter of 2015. The majority of employees (66%) are engaged in elementary occupations. Professionals and the Service and Sales Workers only make up 1.8% and 2.5% respectively. The cost of employing seasonal labour is lower than that of permanent labour. Skills levels of workers and levels of production is also a determinant of wage rate on farms. Wage variations also occur across different regions and farming types. In 2012 the Sectoral Determination in Agriculture was passed making the basic minimum wage R105 per day. Anecdotal evidence of this wage hike is provided in the next chapter although more in-depth, longer-term research is required to fully understand the impact.

67%

19%

1% 13%

Ethnic Profile

African

Coloured

Asian

White

27

Chapter 2: KEY SKILLS ISSUES

This chapter identifies key factors that are driving change and impacting skills demand and supply within the agricultural sector. Particular attention is paid to the following: sustainable land reform, cooperative and smallholder farmer development, improvements in food security, mechanisation, sustainable farming, integrated rural development and, the creation of viable and sustainable rural enterprises and industry. Each of these issues is placed within a broader agrarian transformation agenda.

2.1 Change Drivers

2.1.1 Factors impacting on skills demand and supply

i. Land reform

Land reform has a significant bearing on food security and agriculture’s contribution to GDP. The objective of the land reform programme is to transfer 30% of agricultural land to black ownership by 2025 to ensure more equitable access to land by historically disadvantaged people and to increase their participation in agricultural activities (Xingwana, 2008). The MTSF target is for 20% or 16.2 million hectares by 2019. Four processes have informed land reform (Centre for Development Enterprise, 2008):

Land restitution, involving returning land or providing financial compensation to those whose land was dispossessed during apartheid;

Land redistribution, transferring more land to the historically disadvantaged;

Tenure reform, modernising land tenure rules and access to land ownership; and

Providing financial support for the development of emerging farmers. Between 1994 and 2010, 7,4 million hectares of land were transferred or redistributed to previously disadvantaged persons via the Land Reform Programme. This included agricultural land as well as land used for other activities. For agricultural land redistributed, the programme resulted neither in rising production nor increased economic growth as many of its beneficiaries lacked the necessary skills and knowledge to farm effectively. In 2010 the Department of Rural Development and Land Reform (DRDLR) introduced a Recapitalisation and Development Programme (RADP) for distressed farms that were redistributed since 1994. The aim of this programme is sustainable rural land reform and targets some 1807 farms over the current MTEF period. The use of mentors and strategic partners from the farming sector is central within the programme. Mentors and partners are expected to assist land reform beneficiaries with, “access to markets, farm production, skills development, packaging of projects, access to additional finance, coaching mentorship and advocacy” (DRDLR, 2012, 21). The programme has undergone numerous challenges. Emergent farmers face difficulties in accessing adequate financing, marketing their products and, accessing higher levels of the

28

value chain. Also, the pool of emergent farmers need extensive skills development and is ageing. Emergent farmers may access agricultural infrastructure finance via The Land Bank of South Africa. The Micro Agricultural Financial Institutions of South Africa (MAFISA) financial scheme provides soft loans at lower, fixed interest rates (currently 8 per cent) and is made available to livestock farmers. Pre-training is a prerequisite for accessing the MAFISA loan. The scheme provides state-subsidised loans but is often interpreted as providing grants, amongst those accessing them. Record keeping of agricultural input costs is poor making it difficult to measure output. There is a lack of general financial management skills. Many of the businesses applying for finance are built around one person and this is problematic for sustainability (SSP stakeholder interview, 2014). The proposed draft policy on strengthening the relative rights of people working the land by the Ministry of Rural Development and Land Reform has caused increased tensions in the sector. The main thrust of the policy is the development and implementation of a system of equity sharing on commercial farms whereby the commercial farmer retains 50% ownership of their farm, and cedes 50% ownership to workers in the form of equity shares based on length of time that they have worked on the farm (Hall, 2014). Challenges linked to the proposed ownership model are: the high cost to the State of acquiring the 50% equity on behalf of the workers, increased retrenchments of workers that have worked less than 10 years and departmental capacity needed to manage the 50% equity fund. Hall, a critic of current land reform processes, cautions that “the model can work if it is accompanied by carefully designed interventions in organizational development, worker empowerment and so on. The best share equity schemes in the wine industry (Stellar Organics, Thandi, and Solms Delta to mention some well-known examples) spent millions of Rands on this. If done well, it can lead to many workers bettering their position within the organization of the farm and entering into middle management; and it can increase vocational and educational opportunities for their children. But this requires careful design and lots of money. The handful of successes involved very substantial private investment alongside public funds” (Hall, 2014). Another critical view expressed suggests that many farm workers are not so much concerned with equity shareholding (a key focus of current policy) but are rather seeking land tenure security, better wages and working conditions and improved access to land for their own use through land redistribution programmes (Hall, 2014). In other words the intended beneficiaries and expected drivers of reform may not always seek to benefit in the manner set out in policy. The Department of Rural Development and Land Reform in conjunction with the Department of Agriculture, Forestry and Fisheries (DAFF) must find ways of addressing such challenges if the 2025 land redistribution target is to be met. There is a collective determination in the sector that in the process of engaging in land reform there should be retention of current skills, the development of new skills and

29

skills transfer during the period when land is changing hands, and as far as possible maintaining and expanding food production during after the transfer of land and/or equity. This is a major concern as of the 7 million hectares of land that has changed hand, some 4.3 million are viewed as underutilised. The MTSF sets a target of reducing this figure to 3 million by 2019. Many commodity organisations interviewed have an empowerment arm aimed at addressing empowerment issues for the sub-sector. There is a strong belief that empowerment will only be successful if a multi-pronged approach is adopted, focusing on enabling legislation, skills development, resource mobilisation, and education about the importance of land restitution and redistribution. Such a multi-pronged approach is envisaged in the NTSF. Many organisations are doing work to support land reform programmes through skills development interventions. Hortgro facilitates and supports land reform projects focussing on farmers becoming successful and commercially viable. Hortgro works with farmers who already own some land. To date, Hortgro has supported 47 projects in the Western Cape and 15 in the Eastern Cape. This translates to 4 973 beneficiaries in the Western Cape and 1 135 in the Eastern Cape. Similarly, the Wool Growers Association is assisting wool growers in rural areas to improve their productivity. The South African Sugar Association supports land restitution programmes by ensuring that no cane field lies fallow and that sugar cane becomes sustainable for small scale farmers. Mobile Agri Skills Development and Training trains small scale farmers in enterprise development (stakeholder interviews, 2014). There are many projects driven by different stakeholders and funded from various sources such as DAFF and the National Treasury Jobs Fund. AgriSA provides social skills programmes such as those aimed at the upliftment of women in rural areas and HIV/AIDS awareness as well as and management skills for emerging farmers. AgriSA has developed a partnership in the wool sub-sector targeted at the development of local skills in sheep shearing. Currently the industry mainly uses workers from Lesotho. Apart from in a certain industries such as poultry farming, on-site training is viewed as the most impactful form of training for emerging farmers because:

Training can be done in a manner that is practical and accessible to farm workers.

Training is conducted in the local language using appropriate methodologies

Training accommodates the farmer’s working schedule and does not affect productivity.

ii. Agricultural Co-operatives

The interview process for the SSP included a focus group discussion with twelve, primary agricultural co-operatives held in Katlehong in the East Rand of Johannesburg. All the co-operatives had been engaged for between 3 and 7 years in planting and growing crops (mainly vegetables) and selling these locally, mainly via

30

street vendors. All have aspirations to expand production and markets and feel that with more reliable water supply, access to better quality land, better implements and some machinery, as well as skills training, they could be much more effective. There are currently some 450 cooperatives and other small and emergent enterprises (generally governed by Community Property Associations (CPAs) that are receiving support from AgriSETA, some funded by the SETA, some by DAFF and some by funds obtained from the National Skills Fund. Although no formal evaluation of this work has been conducted a number of lessons have been learned and inform current strategy. Key challenges amongst the co-ops include:

Difficulties in accessing resources e.g. water & land. Co-ops make use of land provided by various land owners, including private land, schools, police stations, municipalities. These are often governed by short term leases or by way of an informal arrangement. Land access and greater security of leases is a key challenge as well as inadequate tools & equipment.

Lack of transport from home to the farm, and for produce – transporting it to the point of sale.

Lack of production skills: technical skills training is badly needed by all those engaging in cooperative farming.

Governance and management. Many worker cooperatives find it very difficult to manage cash flow, develop a sound business model and address governance issues such as the setting of viable pay levels, and putting in place financial and other controls.

Lack of other skills along the value chain: financial, negotiating with municipalities that own the land, marketing.

Cooperatives (an emergent farming entities in general) tend to be formed by more elderly workers, with few young people being attracted into the industry.

Poor organisation of co-ops. No secondary structures to rally on behalf of primary co-ops – for example to negotiate better leases and access to water. It is becoming clear that there is a need to focus more on the structures that can purchase and sell products on behalf of producers.

A number of conclusions emerged via the discussions with the co-ops. There was consensus over the need for some type of secondary co-op structure that is skilled in areas other than basic crop production, such as: business, marketing, communication & negotiation, machinery maintenance etc. All of the co-ops highlighted the need for better collaboration and agreement within co-ops amongst their members in terms of what to produce, how etc. In relation the type of training needed, co-op interviewees were in favour of longer-term (12 month) training programmes that lead to qualifications and that have a combination of practical, production-related training and business skills.

iii. Food security

South Africa currently produces enough food to meet the needs of its population. Despite this, many people continue to go hungry. According to FoodBank SA, 11

31

million people are food insecure in the country whilst a further 14 million are vulnerable to food insecurity (GCIS, 2012). Similarly, the results of the National Health and Nutrition Survey released in August 2013 indicate that only 45,6% of our population are food secure, 28,3% is at risk of hunger and 26% experienced hunger and were food insecure (HSRC, 2014). There is increasing evidence that food security can become a cause for concern. In a document produced by the Bureau for Food and Agricultural Policy (BFAP) in 2012, reference is made to the increasing impact of mining on agriculture in Mpumalanga Province. A pilot study has been initiated to evaluate the effects on coal mining on maize farming, in the Delmas, Ogies and Leandra areas. “At the current rate of coal mining in Mpumalanga, it was calculated that approximately 12% of South Africa’s total high potential arable land will be transformed, while a further 13.6% is currently being prospected by the mines in Mpumalanga. Current mining and new prospects for mining could soon have devastating effects on agricultural production as well as long term food security implications for the entire country” (BFAP, 2012). BFAP estimates that at current maize farming yields, 447 581 tons of maize will be taken out of production as the result of current and prospective mining operations. This will result in a 10% rise in the price of maize with huge repercussion for South Africa and particularly the poor and vulnerable sectors of our population. Despite government increases in the levels of social grants and in the number of persons receiving these grants to almost 16 million in February 2014 (StatsSA, 2014), rising unemployment, increased food prices, reduced agricultural yields, HIV and AIDS, poor environmental conditions and generally high levels of poverty all contribute to food insecurity, particularly amongst the poor and in rural areas. Whilst food is available it is often not accessible to families. The result has been a concerted effort on the part of government to prioritise the issue of food security in South Africa and this is reflected in multiple policy and strategic documents at the national, departmental and sectoral levels. The National Development Plan highlights food security as both a cause and effect of poverty and inequality. The NDP outlines several strategies aimed at improving levels of food security including: improved irrigation, secure land tenure (particularly amongst women) and better nutrition education (SA Presidency, 2011). This is the platform on which the national policy on food and nutrition security has recently been developed by the Department of Social Development and the Department of Agriculture, Forestry and Fisheries. The policy adopts a multi-faceted approach towards food and nutrition security that integrates existing strategies and programmes affiliated to health, education, environmental protection, agrarian reform and agricultural development across multiple departments and sectors. The policy defines food and nutrition security as: “Access to and control over the physical, social and economic means to ensure sufficient, safe and nutritious food at all times, for all South Africans, in order to meet the dietary requirements for a healthy life” (DSD, 2013, 8). Five key pillars make up the food security policy and are as follows:

32

Improved availability of nutritional safety nets including government, private sector, NGO and CBO nutrition and feeding programmes as well as emergency food relief.

Improved nutrition education so that people are better informed about nutrition choices.

Aligning agricultural investment to local economic development needs especially in rural areas. Here there is a focus on the provision and subsidization of agricultural inputs and services as well as better food storage and distribution networks. This is intended to reduce food wastage and improve the accessibility of food.

Improvements to the market participation of emerging farmers via public-private partnerships, the implementation of a government food purchase programme targeted at smallholder farmers as well as the implementation of the AgriBEE Charter whereby agro-processing industries are expected to incorporate emerging farmers as suppliers of agricultural produce.

Risk management linked to protecting prime agricultural land from other activities such as mining, game farming and property development that result in reduced food production. This also involves expanded investments in research and technology to better understand food production vulnerabilities associated with climate change and bioenergy demands (DSD, 2013).

iv. Mechanisation in agriculture

A prominent trend within the agricultural sector is that, “as agriculture becomes more mechanized, the unskilled labour force is replaced by a significantly smaller skilled labour force” (South African Ministry of Labour, 2013, 14). That being said, increases to the agricultural labour wage will not, “automatically result in increased mechanisation,” (South African Ministry of Labour, 2013, 16) as technologies are not always available and for certain types of agriculture such as intensive fruit farming, mechanized harvesting techniques are not appropriate for meeting the high quality standards required for the exporting of such produce. The rate at which mechanisation displaces labour in agriculture is dependent on the availability of technology, the cost of labour and capital and existing economic conditions. What has become noticeable in recent years is that demand for artisans (mechanics for example) has increased in the sector. As mechanisation occurs it is likely that this trend will continue with demand reducing for general labouring or less skilled workers and demand increasing for artisans and technically qualified workers.

v. Sustainable agricultural development

There has been an increasing focus on the use of environmentally sustainable farming practices across the agricultural sector. In some policy documents such as the National Development Plan and the New Growth Path this is referred to as green economy practices. However, within the agricultural sector “green economy” industries are often associated with such enterprises as ornamental horticulture, organic nurseries and farms and landscaping. Thus, for the purpose of this SSP, the

33

term sustainable farming is preferred as this better describes sustainable practices associated within the broader “green economy.” The United Nations Environment Programme (UNEP, 2013, 9) describes the green economy as “an economy that results in improved human well-being and social equity, while significantly reducing environmental risks and ecological scarcities”. A green economy operates in a manner whereby economic growth and development including employment creation follows a path in which carbon emissions are reduced, energy and resource efficiency is promoted and environmental degradation is lessoned. Sustainable farming is recognised as important as conveyed through industry-specific training interventions across different subsectors. In horticulture, training focuses on green issues in fruit farming. In wool growing, green issues are important in predator management. The sugar cane sub-sector is using waste fibre to generate energy; most of the mills are running their energy from fibre. There is investigation on how to transfer excess energy to Eskom, and research around biofuels is taking place. In poultry, environmental impact assessments (EIA) are needed to start farming with 5000 birds. This is costly and difficult for emerging farmers (SSP stakeholder interviews, 2014). The skills system needs to respond to a new set of knowledge and skills requirements (largely at a higher level) for sustainable farming. Research and development on the role of green industries in the agricultural sector should expand. Capacity development for developing and implementing green technologies is needed as is the upskilling of farm workers in energy-efficient methods, resource sustainability, agro-processing and other green technologies. Sustainable agricultural development has been closely aligned to what is termed “ethical farming,” the foundation of what Alan Wright refers to as the “new farming movement” (Wright, 2013). Ethics ultimately drive practice. In agriculture, increasing consumer demand for inexpensive food and need to maximise profit based on neoliberal economic thinking have formed the basis of underlying ethics within the sector and this in turn has encouraged industrial farming practices. Such practices have resulted in an increase in the use of chemicals, irrigation methods that are wasteful, climate change, the destruction of our oceans and other aquatic systems, rapid top soil loss leading to desertification and the implementation of poor worker health and safety conditions (Wright, 2013). Wright explains that historically, ethics and good practice were often passed down between the generations but that in today’s world this is not the case as many farmers are new to the sector and are in fact what he calls, “agricultural orphans” (Ibid, 2013). Many emergent farmers in South Africa may be classified as “agricultural orphans.” Despite the weaknesses of such as position, it does present us with an opportunity to develop new agricultural ethics that will shape sustainable and ecologically friendly farming practice that are tied to existing realities such as high levels of mechanisation and our scientific understanding. The development of new agricultural ethics, according to Wright, requires a number of things. Firstly, clear goals need to be set as these will guide the

34

development of our ethics and limit the number of possibilities. “If our goals are to grow food without toxic residues on the fruiting bodies, than we can no longer believe in spraying for mid-season pests” (Wright, 2013). The second step is to use science to better understand our physical and natural environment. Thirdly, we must observe the cause and effect of our farming practices on our natural environment carefully and where it appears to not be working we must change such practices. Fourthly, on-going sustainable agriculture is dependent on our ability to continuously reassess and evaluate our existing practice. Wright emphasises that we must not be fearful of abandoning standard farming practices simply because we fear failure. We must be prepared to listen and learn from others who are using innovative farming practice that is ecologically ethical. There has been a lot of research conducted in these areas and we must draw on this and the experience of these individuals. Finally, Wright warns that we should not restrict ourselves to a particular growing practice or style (e.g. deep organic) but that we should develop a blend of different practices that are suited to specific regional, climatic and other needs (Ibid, 2013). A view often expressed by farm employers is that current labour legislation makes dismissing workers difficult and so securing labour without entering into contracts of employment is an attractive alternative. Organised Labour is seeking to restrict these opportunities through either regulating or eliminating labour brokers, and efforts are being made to regulate the use of foreign labour. However for the foreseeable future, the trend is for formally employed people to reduce in number and contracted in and casual or agency work to increase. The Sustainability Initiative of South Africa, familiarly known as the SIZA programme, was initiated in 2008 by Fruit South Africa in an attempt to promote ongoing ethical labour practices on fruit farms and pack houses in South Africa (Fruit SA, 2012). The programme has developed a standard of ethical practice and audit methodology for monitoring such practice known as the SIZA Standard. This is based on local labour legislation as well as international standards. The Standard refers to a number of key labour issues including: wages and employment benefits; living conditions; occupational health and safety; the use of child labour; discrimination, harassment and abuse; freedom of association and collective bargaining; the right to terminate labour by workers and, the development of business policy on fair labour practices (Ibid, 2012). It was partly developed as the result of increased global pressure linked to the need for more ethical labour practices on farms (Ibid, 2012). Although it was developed by the fruit industry it may be adopted across other agricultural subsectors. This requires capacity building and increased awareness linked to implementing the SIZA standard. There is reference to the need for skills development opportunities to be provided to all agricultural workers, seasonal and permanent. Although targeted at growers, the SIZA standard also requires growers to sign a service level agreement with labour service providers to ensure that these providers are adhering to applicable legislation in terms of the workers that they supply. Furthermore, the Standard requires all non-permanent workers (including seasonal

35

workers) to sign a formal contract of employment with the employer and that the contracting of non-permanent workers “should not be used to avoid obligations that would normally accrue to permanent workers” (Fruit SA, 2012, 73). In addition, the Standard expects that all “non-permanent workers that leave and return to the same place of work shall accrue all leave and other benefits due to them by law” (Fruit SA, 2012, 74).

vi. Transformation in agriculture – wages and skills

The existence of a very large pool of largely unskilled unemployed workers has an impact on the farming sector. It drives wages down and creates opportunities for casualisation and the expansion of labour contract agencies and brokers. In addition there are significant numbers of foreign nationals, mainly from Zimbabwe and Mozambique, who are seeking work and often finding it on farms and in primary processing and packaging plants. There are benefits to the sector with skilled and semi-skilled workers coming into the labour market, being absorbed into the workforce and helping raise productivity levels. However at the lower skilled end of the market the existence of this pool brings further casualisation and downward pressure on wages. Tensions are likely to increase, and further protests either in the form of xenophobic outbreaks or actions against farmers are likely to increase. Indicative of this is the 2013 labour unrest amongst fruit farm workers in the De Doorns area in the Western Cape. Such unrest has caused government to relook the issue of farm worker wages, particularly with respect to casual labour. One of the outcomes of these protests was Sectoral Determination 13 that deals with employment conditions for farm workers in South Africa. One of the main changes adopted in Sectoral Determination 13 is in relation to the minimum wage for farm workers. As of the 1st March 2013, this minimum wage was increased from R69 per day to R105 per day. Although it is still early days to fully comprehend the real effects of the wage increase on both farmers and farm workers, there are indications that farmers are responding by down-scaling their operations and/or reducing the number of permanent farm workers employed (as suggested by the employment data over the past year). A previous study conducted Bhorat, Kanbur and Stanwix on the impact of the 2003 wage hike in the agricultural sector over a four year period indicates that this did result in a drop in employment on farms (Bhorat et al., 2013). However, it must be cautioned at this stage that an in-depth economic analysis that considers a range of factors, over a much longer period of time, is necessary to reach an accurate conclusion with respect to the 2013 wage hike. That being said, there is some anecdotal evidence to suggest that farmers are not really paying higher wages as they have responded to the wage hike by reducing the number of hours worked per day from nine to eight hours as well as reducing the number of seasonal and permanent workers employed. The decline the employment figure of 55 000 jobs as indicated in the Labour Force Survey for this year may be indicative of this. Generally higher earnings are accompanied by increased productivity and so it can be expected that these sorts of adjustments will happen. According to the CEO of Agriwes-Kaap, “wages have always been associated with productivity. On some farms some people

36