Embed Size (px)

Citation preview

AGRICULTURE RESEARCH PROJECT

Waterloo Wellington December 2015

Agriculture Research Project - December 2015

TABLE OF CONTENTSExecutive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Project Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Key Industry and Employment Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Farm Jobs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Waterloo Region . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Key Growth Industries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Change in Number of Businesses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Key Declining Industries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Wellington County . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Key Growth Industries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Change in Number of Businesses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Survey/Key Informant Feedback . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Why Do People Get Into Farming? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Size of Farms (Land and Workers) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

New Products/Markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Key Considerations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Appendix A – Waterloo Region . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Appendix B – Wellington County . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Appendix C – Survey Responses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

Appendix D – Industry Consultation Feedback . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

Appendix E – Consultation Participant List (December 2, 2015) . . . . . . . . . . . . . . 31

This report was compiled by Carol Simpson, Executive Director, Workforce Planning Board of Waterloo Wellington Dufferin (WPB).The material contained in this report is drawn from a variety of sources considered to be reliable. We make no representation or warranty,

express or implied, as to its accuracy or completeness. In providing this material, WPB does not assume any responsibility or liability.

This Employment Ontario Project is funded by the Government of Ontario The views expressed in this document do not necessarily reflect those of Employment Ontario.

We would like to express our thanks to all those who contributed to this research project.

Agriculture Research Project - December 2015 1

EXECUTIVE SUMMARYOver the past 2-3 years, we have seen surprising and dramatic changes in the make-up of Waterloo Wellington’s Agriculture sector . An increase in the total number of Agricultural and Agricultural-related businesses in Waterloo Wellington is bucking the trend compared to what is happening across Ontario (where the trend is decline not growth) .

The research confirmed that new products and markets are being developed and that these can provide both economic and employment opportunities for both existing and new Agriculture businesses . There is evidence of specialization into niche products which is providing additional opportunities, not just in on-farm Agriculture but also in Agriculture Supports . Understanding where these opportunities are is key if we are to be able to provide encouragement and the appropriate supports to maintain, retain and grow these businesses in Waterloo Wellington .

Although business growth is not equal in all subsectors, overall the region is well positioned to continue to provide traditional and non-traditional opportunities for both long-standing and new farmers . Planning for future land use will require collaborative efforts from many different key stakeholders if we are to meet the needs of current and future Agriculture businesses, while recognizing that population growth is critical to the survival of rural communities .

PROJECT OVERVIEWThe goal of this research was to:

- Identify key growth sectors at the highest possible level of detail

- Investigate whether immigration is a factor

• New product development

• New markets/customer demand

- Determine whether this area is an incubator

• Not a lot of land here for purchase

• Are renters starting out here then moving to buy Ag land and grow

• Are we attracting new farmers from the larger urban areas

Through a variety of activities, including data analysis, literature reviews, surveys and key stakeholder interviews we hoped to determine where and why this growth is occurring and share that knowledge with our communities . This knowledge will help to identify what can be done to encourage and support these businesses and how to retain them and help them grow .

The following organizations committed to be project partners:

- Ontario Agricultural College (University of Guelph)

- Farm Start

- Township of Woolwich

- Ontario Agri-Food Education

- County of Wellington

Partners formed an advisory group for the project . The committee first met in June 2015 to direct the Researcher to relevant data/information and key stakeholder contacts .

In December 2015, a consultation session was held to provide broader industry stakeholders an opportunity to review the findings and comment on some key ideas put forward for consideration . Their feedback is provided in Appendix D .

2 Agriculture Research Project - December 2015

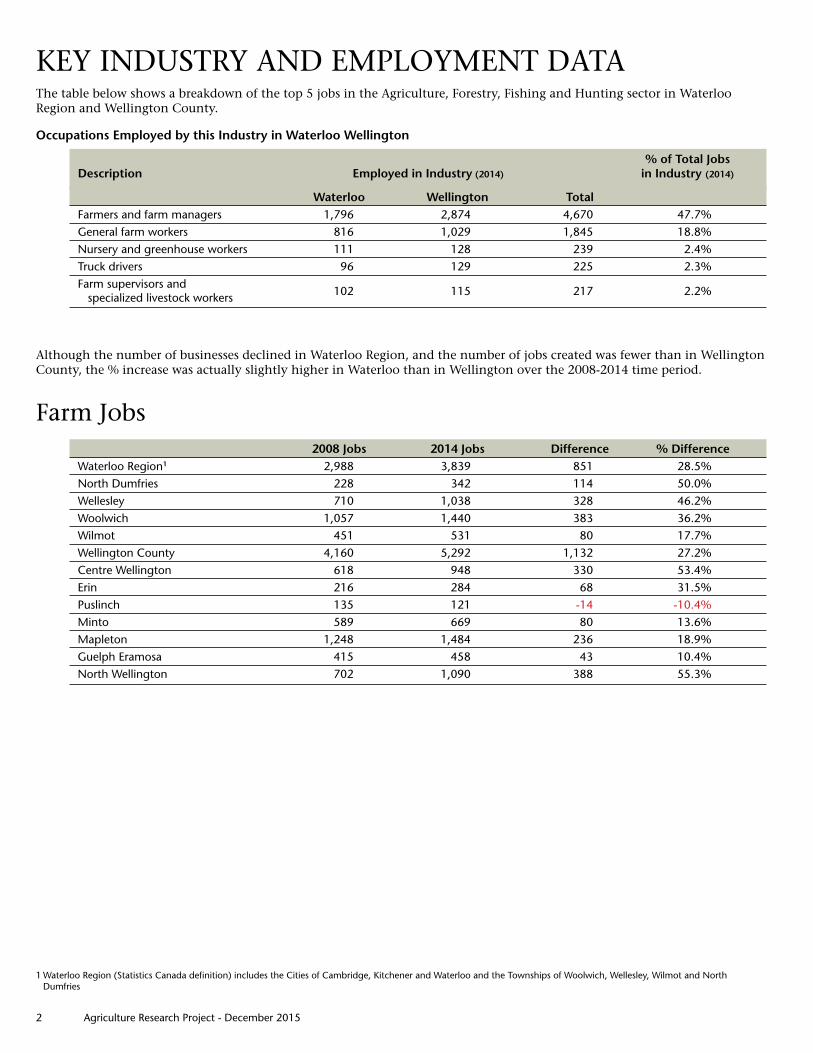

KEY INDUSTRY AND EMPLOYMENT DATAThe table below shows a breakdown of the top 5 jobs in the Agriculture, Forestry, Fishing and Hunting sector in Waterloo Region and Wellington County .

Occupations Employed by this Industry in Waterloo Wellington

% of Total Jobs Description Employed in Industry (2014) in Industry (2014)

Waterloo Wellington Total Farmers and farm managers 1,796 2,874 4,670 47.7%General farm workers 816 1,029 1,845 18.8%Nursery and greenhouse workers 111 128 239 2.4%Truck drivers 96 129 225 2.3%Farm supervisors and specialized livestock workers 102 115 217 2.2%

Although the number of businesses declined in Waterloo Region, and the number of jobs created was fewer than in Wellington County, the % increase was actually slightly higher in Waterloo than in Wellington over the 2008-2014 time period .

Farm Jobs 2008 Jobs 2014 Jobs Difference % DifferenceWaterloo Region1 2,988 3,839 851 28.5%North Dumfries 228 342 114 50.0%Wellesley 710 1,038 328 46.2%Woolwich 1,057 1,440 383 36.2%Wilmot 451 531 80 17.7%Wellington County 4,160 5,292 1,132 27.2%Centre Wellington 618 948 330 53.4%Erin 216 284 68 31.5%Puslinch 135 121 -14 -10.4%Minto 589 669 80 13.6%Mapleton 1,248 1,484 236 18.9%Guelph Eramosa 415 458 43 10.4%North Wellington 702 1,090 388 55.3%

1 Waterloo Region (Statistics Canada definition) includes the Cities of Cambridge, Kitchener and Waterloo and the Townships of Woolwich, Wellesley, Wilmot and North Dumfries

Agriculture Research Project - December 2015 3

WATERLOO REGIONIn Waterloo Region, from June 2012 to June 2014, Agriculture’s share of total businesses declined slightly from 5% of all businesses to 4% . There was a decline of 316 businesses with most losses in Dairy cattle and milk production . Animal combination farming lost 280 businesses however some of these businesses are likely now being recorded in other sub-industries .

Although the urban municipalities of Cambridge, Kitchener and City of Waterloo do all have direct Agriculture and Support businesses, their numbers are small enough to not impact this study . It is noted however that Cambridge’s share of Ag businesses actually increased from 1% to 2% in the 2-year period used for this study .

% of Agriculture Businesses of all Businesses

June 2012 June 2014

Waterloo Wellington 7% 7%Waterloo Region 5% 4%North Dumfries 12% 12%Wellesley 40% 27%Woolwich 18% 18%Wilmot 12% 11%

Key Growth IndustriesFrom June 2012 to June 2014, the number of sheep farms rose from 1 to 12 and goat farming rose from 4 farms to 10 farms . The largest growth in both these industries was in Woolwich . One sheep farm in Woolwich reported having 10-19 employees in June 2014 while all other sheep and goat farms in the municipality reported no employees .

Corn farming rose from 18 businesses to 63 however there was a decline in the larger farms and business growth was among the indeterminate2 group from 83% to 87% of total businesses . Most growth in this industry was seen in Wilmot and Woolwich .

In Soybean farming, there were 18 new businesses and the number of indeterminate businesses rose from 70% to 82% however there was also slight growth in the 5-9 employee range . Woolwich had the largest increase in this industry with 7 new businesses .

Support activities rose in all categories; crop production, animal production and forestry with 28 new businesses .

2 Indeterminate businesses may or may not have workers however they do not report having payroll employees. They may be self-employed or have family members or contractors working for them but no payroll staff.

4 Agriculture Research Project - December 2015

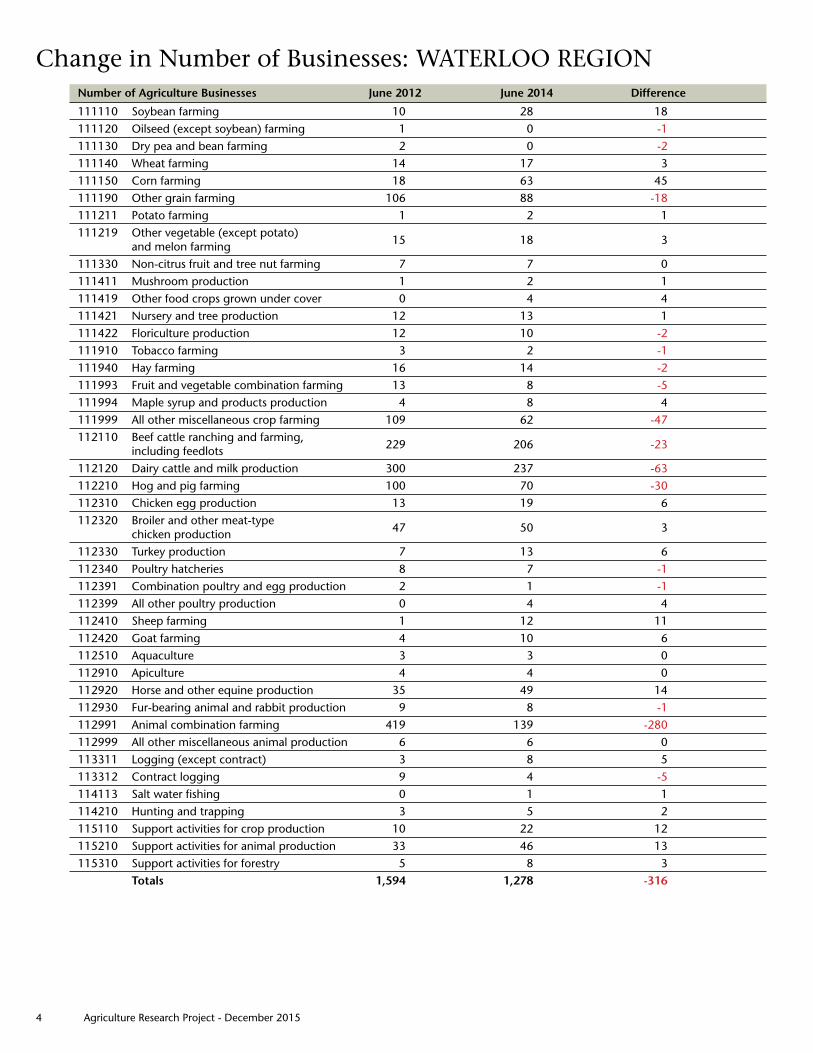

Change in Number of Businesses: WATERLOO REGIONNumber of Agriculture Businesses June 2012 June 2014 Difference

111110 Soybean farming 10 28 18111120 Oilseed (except soybean) farming 1 0 -1111130 Dry pea and bean farming 2 0 -2111140 Wheat farming 14 17 3111150 Corn farming 18 63 45111190 Other grain farming 106 88 -18111211 Potato farming 1 2 1111219 Other vegetable (except potato) and melon farming 15 18 3

111330 Non-citrus fruit and tree nut farming 7 7 0111411 Mushroom production 1 2 1111419 Other food crops grown under cover 0 4 4111421 Nursery and tree production 12 13 1111422 Floriculture production 12 10 -2111910 Tobacco farming 3 2 -1111940 Hay farming 16 14 -2111993 Fruit and vegetable combination farming 13 8 -5111994 Maple syrup and products production 4 8 4111999 All other miscellaneous crop farming 109 62 -47112110 Beef cattle ranching and farming, including feedlots 229 206 -23

112120 Dairy cattle and milk production 300 237 -63112210 Hog and pig farming 100 70 -30112310 Chicken egg production 13 19 6112320 Broiler and other meat-type chicken production 47 50 3

112330 Turkey production 7 13 6112340 Poultry hatcheries 8 7 -1112391 Combination poultry and egg production 2 1 -1112399 All other poultry production 0 4 4112410 Sheep farming 1 12 11112420 Goat farming 4 10 6112510 Aquaculture 3 3 0112910 Apiculture 4 4 0112920 Horse and other equine production 35 49 14112930 Fur-bearing animal and rabbit production 9 8 -1112991 Animal combination farming 419 139 -280112999 All other miscellaneous animal production 6 6 0113311 Logging (except contract) 3 8 5113312 Contract logging 9 4 -5114113 Salt water fishing 0 1 1114210 Hunting and trapping 3 5 2115110 Support activities for crop production 10 22 12115210 Support activities for animal production 33 46 13115310 Support activities for forestry 5 8 3 Totals 1,594 1,278 -316

Agriculture Research Project - December 2015 5

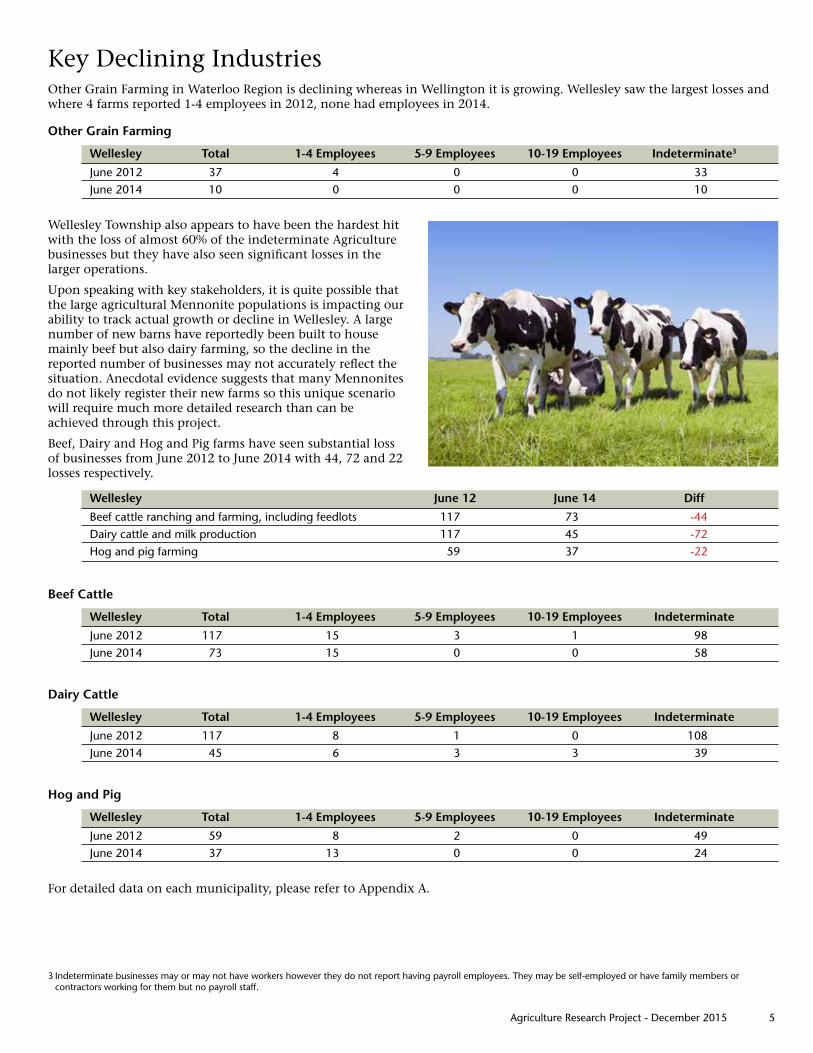

Key Declining IndustriesOther Grain Farming in Waterloo Region is declining whereas in Wellington it is growing . Wellesley saw the largest losses and where 4 farms reported 1-4 employees in 2012, none had employees in 2014 .

Other Grain Farming

Wellesley Total 1-4 Employees 5-9 Employees 10-19 Employees Indeterminate3

June 2012 37 4 0 0 33June 2014 10 0 0 0 10

Wellesley Township also appears to have been the hardest hit with the loss of almost 60% of the indeterminate Agriculture businesses but they have also seen significant losses in the larger operations .

Upon speaking with key stakeholders, it is quite possible that the large agricultural Mennonite populations is impacting our ability to track actual growth or decline in Wellesley . A large number of new barns have reportedly been built to house mainly beef but also dairy farming, so the decline in the reported number of businesses may not accurately reflect the situation . Anecdotal evidence suggests that many Mennonites do not likely register their new farms so this unique scenario will require much more detailed research than can be achieved through this project .

Beef, Dairy and Hog and Pig farms have seen substantial loss of businesses from June 2012 to June 2014 with 44, 72 and 22 losses respectively .

Wellesley June 12 June 14 Diff

Beef cattle ranching and farming, including feedlots 117 73 -44Dairy cattle and milk production 117 45 -72Hog and pig farming 59 37 -22

Beef Cattle

Wellesley Total 1-4 Employees 5-9 Employees 10-19 Employees Indeterminate

June 2012 117 15 3 1 98June 2014 73 15 0 0 58

Dairy Cattle

Wellesley Total 1-4 Employees 5-9 Employees 10-19 Employees Indeterminate

June 2012 117 8 1 0 108June 2014 45 6 3 3 39

Hog and Pig

Wellesley Total 1-4 Employees 5-9 Employees 10-19 Employees Indeterminate

June 2012 59 8 2 0 49June 2014 37 13 0 0 24

For detailed data on each municipality, please refer to Appendix A .

3 Indeterminate businesses may or may not have workers however they do not report having payroll employees. They may be self-employed or have family members or contractors working for them but no payroll staff.

6 Agriculture Research Project - December 2015

WELLINGTON COUNTYIn Wellington County4, from June 2012 to June 2014, Agriculture’s share of total businesses grew from 12% to 14% with an additional 516 businesses .

Although the urban municipality of Guelph does have over 100 direct Agriculture and Support businesses, the numbers are small enough to not impact this study (only 1% of all businesses) .

% of Agriculture Businesses of all Businesses

June 2012 June 2014

Waterloo Wellington 7% 7%Wellington County 12% 14%Centre Wellington 11% 14%Erin 8% 7%Puslinch 8% 10%Minto 42% 43%Mapleton 44% 53%Guelph Eramosa 13% 13%Wellington North 40% 37%

Key Growth IndustriesDespite a decline in Beef cattle ranching and farming, including feedlots in Waterloo Region, the industry is growing immensely in Wellington County with 151 new businesses since June 2012 . 78% of that growth is located in Mapleton with another 18% in Wellington North and 9% in Centre Wellington .

Mapleton Growth of Beef cattle ranching and farming, including feedlots

Total 1-4 employees 5-9 employees Indeterminate

June 2012 34 4 0 30June 2014 152 10 3 139

Another sub-industry that is growing in Wellington, but in decline in Waterloo, is Dairy cattle and milk production however, this growth is not consistent across the County . Wellington North lost 30 businesses (22% decline), Guelph Eramosa lost 3 businesses (11% decline) and Erin lost 1 business (33% decline) . Centre Wellington saw slight growth with 4 new businesses (9% increase), while Minto had 14 new businesses (19% increase) . Again the highest growth in this sub-industry is in Mapleton with 91 new businesses, almost double that from June 2012 .

Mapleton Growth of Dairy cattle and milk production

Total 1-4 5-9 10-19 20-49 Indeterminate Employees Employees Employees Employees

June 2012 95 14 3 0 1 77June 2014 186 24 2 3 1 156

4 Wellington County includes the City of Guelph, Towns of Minto and Erin and Townships of Centre Wellington, Wellington North, Mapleton, Puslinch, Guelph Eramosa

Agriculture Research Project - December 2015 7

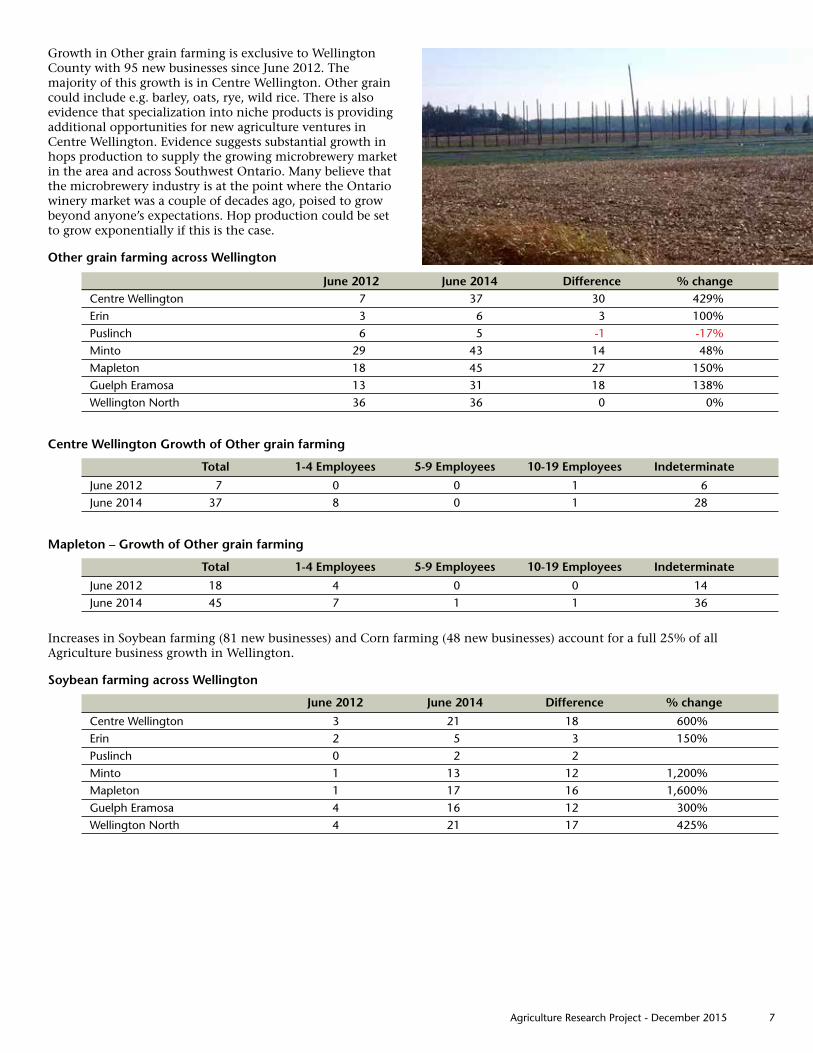

Growth in Other grain farming is exclusive to Wellington County with 95 new businesses since June 2012 . The majority of this growth is in Centre Wellington . Other grain could include e .g . barley, oats, rye, wild rice . There is also evidence that specialization into niche products is providing additional opportunities for new agriculture ventures in Centre Wellington . Evidence suggests substantial growth in hops production to supply the growing microbrewery market in the area and across Southwest Ontario . Many believe that the microbrewery industry is at the point where the Ontario winery market was a couple of decades ago, poised to grow beyond anyone’s expectations . Hop production could be set to grow exponentially if this is the case .

Other grain farming across Wellington

June 2012 June 2014 Difference % changeCentre Wellington 7 37 30 429%Erin 3 6 3 100%Puslinch 6 5 -1 -17%Minto 29 43 14 48%Mapleton 18 45 27 150%Guelph Eramosa 13 31 18 138%Wellington North 36 36 0 0%

Centre Wellington Growth of Other grain farming

Total 1-4 Employees 5-9 Employees 10-19 Employees Indeterminate

June 2012 7 0 0 1 6June 2014 37 8 0 1 28

Mapleton – Growth of Other grain farming

Total 1-4 Employees 5-9 Employees 10-19 Employees Indeterminate

June 2012 18 4 0 0 14June 2014 45 7 1 1 36

Increases in Soybean farming (81 new businesses) and Corn farming (48 new businesses) account for a full 25% of all Agriculture business growth in Wellington .

Soybean farming across Wellington

June 2012 June 2014 Difference % change

Centre Wellington 3 21 18 600%Erin 2 5 3 150%Puslinch 0 2 2 Minto 1 13 12 1,200%Mapleton 1 17 16 1,600%Guelph Eramosa 4 16 12 300%Wellington North 4 21 17 425%

8 Agriculture Research Project - December 2015

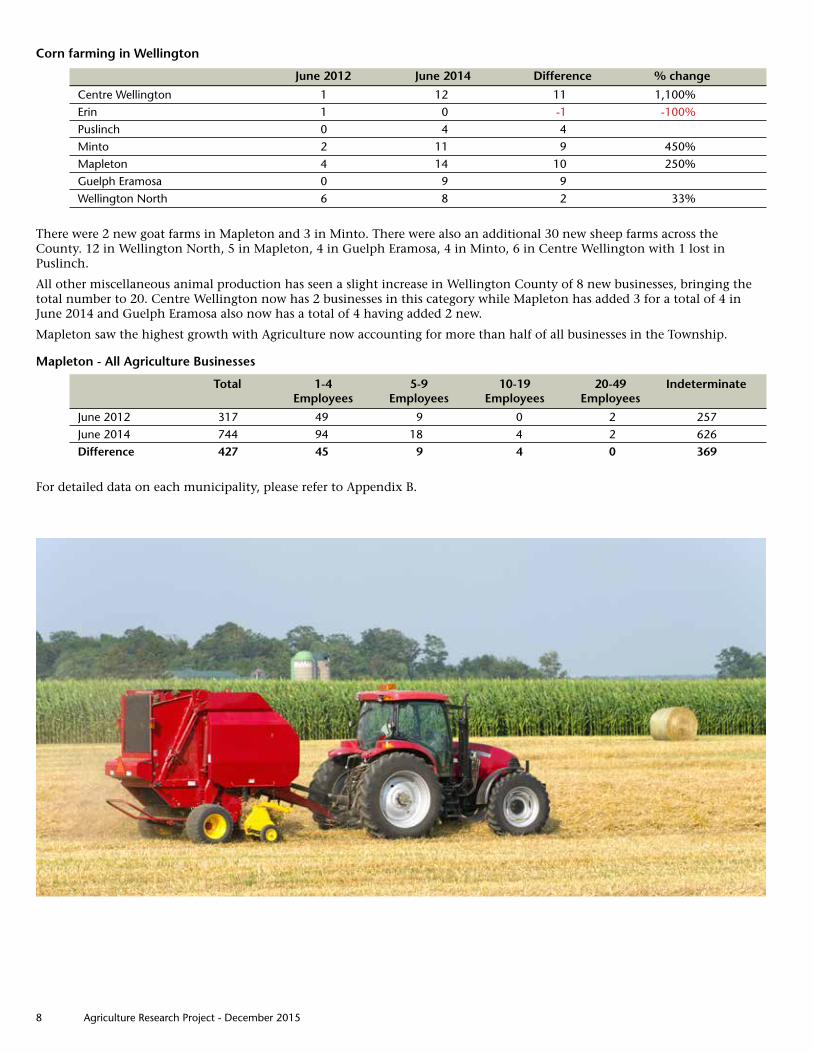

Corn farming in Wellington

June 2012 June 2014 Difference % change

Centre Wellington 1 12 11 1,100%Erin 1 0 -1 -100%Puslinch 0 4 4 Minto 2 11 9 450%Mapleton 4 14 10 250%Guelph Eramosa 0 9 9 Wellington North 6 8 2 33%

There were 2 new goat farms in Mapleton and 3 in Minto . There were also an additional 30 new sheep farms across the County . 12 in Wellington North, 5 in Mapleton, 4 in Guelph Eramosa, 4 in Minto, 6 in Centre Wellington with 1 lost in Puslinch .

All other miscellaneous animal production has seen a slight increase in Wellington County of 8 new businesses, bringing the total number to 20 . Centre Wellington now has 2 businesses in this category while Mapleton has added 3 for a total of 4 in June 2014 and Guelph Eramosa also now has a total of 4 having added 2 new .

Mapleton saw the highest growth with Agriculture now accounting for more than half of all businesses in the Township .

Mapleton - All Agriculture Businesses

Total 1-4 5-9 10-19 20-49 Indeterminate Employees Employees Employees Employees

June 2012 317 49 9 0 2 257June 2014 744 94 18 4 2 626Difference 427 45 9 4 0 369

For detailed data on each municipality, please refer to Appendix B .

Agriculture Research Project - December 2015 9

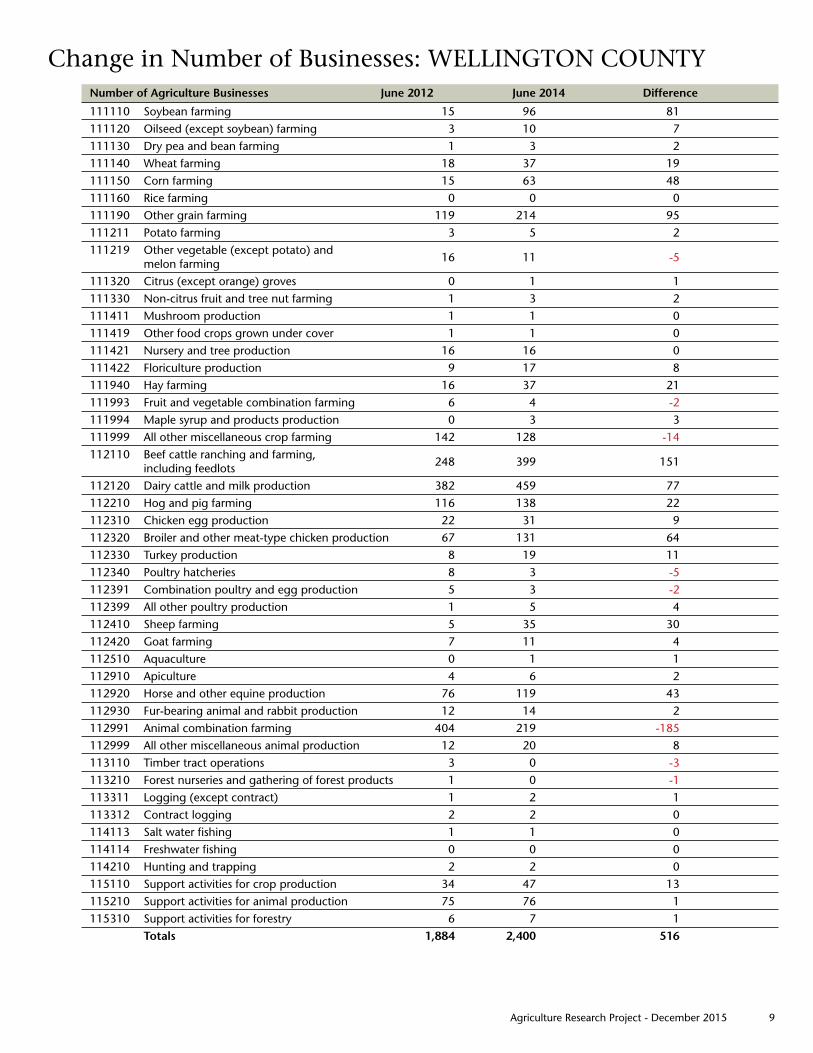

Change in Number of Businesses: WELLINGTON COUNTYNumber of Agriculture Businesses June 2012 June 2014 Difference

111110 Soybean farming 15 96 81111120 Oilseed (except soybean) farming 3 10 7111130 Dry pea and bean farming 1 3 2111140 Wheat farming 18 37 19111150 Corn farming 15 63 48111160 Rice farming 0 0 0111190 Other grain farming 119 214 95111211 Potato farming 3 5 2111219 Other vegetable (except potato) and melon farming 16 11 -5

111320 Citrus (except orange) groves 0 1 1111330 Non-citrus fruit and tree nut farming 1 3 2111411 Mushroom production 1 1 0111419 Other food crops grown under cover 1 1 0111421 Nursery and tree production 16 16 0111422 Floriculture production 9 17 8111940 Hay farming 16 37 21111993 Fruit and vegetable combination farming 6 4 -2111994 Maple syrup and products production 0 3 3111999 All other miscellaneous crop farming 142 128 -14112110 Beef cattle ranching and farming, including feedlots 248 399 151

112120 Dairy cattle and milk production 382 459 77112210 Hog and pig farming 116 138 22112310 Chicken egg production 22 31 9112320 Broiler and other meat-type chicken production 67 131 64112330 Turkey production 8 19 11112340 Poultry hatcheries 8 3 -5112391 Combination poultry and egg production 5 3 -2112399 All other poultry production 1 5 4112410 Sheep farming 5 35 30112420 Goat farming 7 11 4112510 Aquaculture 0 1 1112910 Apiculture 4 6 2112920 Horse and other equine production 76 119 43112930 Fur-bearing animal and rabbit production 12 14 2112991 Animal combination farming 404 219 -185112999 All other miscellaneous animal production 12 20 8113110 Timber tract operations 3 0 -3113210 Forest nurseries and gathering of forest products 1 0 -1113311 Logging (except contract) 1 2 1113312 Contract logging 2 2 0114113 Salt water fishing 1 1 0114114 Freshwater fishing 0 0 0114210 Hunting and trapping 2 2 0115110 Support activities for crop production 34 47 13115210 Support activities for animal production 75 76 1115310 Support activities for forestry 6 7 1 Totals 1,884 2,400 516

10 Agriculture Research Project - December 2015

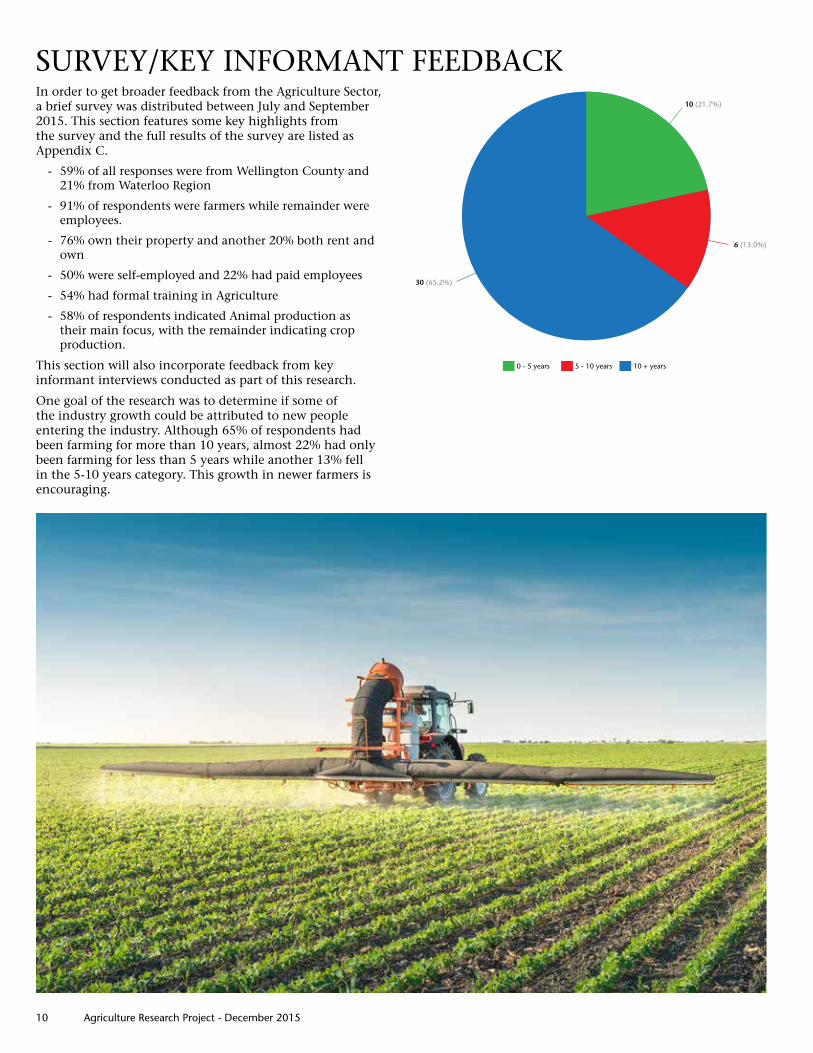

In order to get broader feedback from the Agriculture Sector, a brief survey was distributed between July and September 2015 . This section features some key highlights from the survey and the full results of the survey are listed as Appendix C .

- 59% of all responses were from Wellington County and 21% from Waterloo Region

- 91% of respondents were farmers while remainder were employees .

- 76% own their property and another 20% both rent and own

- 50% were self-employed and 22% had paid employees

- 54% had formal training in Agriculture

- 58% of respondents indicated Animal production as their main focus, with the remainder indicating crop production .

This section will also incorporate feedback from key informant interviews conducted as part of this research .

One goal of the research was to determine if some of the industry growth could be attributed to new people entering the industry . Although 65% of respondents had been farming for more than 10 years, almost 22% had only been farming for less than 5 years while another 13% fell in the 5-10 years category . This growth in newer farmers is encouraging .

SURVEY/KEY INFORMANT FEEDBACK

Agriculture Research Project - December 2015 11

Why do people get into farming?When we considered why people had gotten into farming, we anticipated that the majority would be family farm operations . Although 48% of all survey respondents fell into this category, another 41% indicated that they were not from a farm background . Almost half of those were entrepreneurs seeking new business opportunities .

When we looked at those who had been farming for less than 5 years, the outcomes were even more surprising with only 30% from farm operations and a full 60% from entrepreneurship and rural lifestyle/move from urban centres . This certainly would indicate that the newer farmers are entering for less traditional reasons than farmers who have been farming for more than 10 years . 80% of those new farmers indicated that they were based in Wellington County with the remainder in Waterloo Region .

Key informant interviews would tend to lend credence to these findings in that several people referred to younger people moving away from urban centres to farm in Wellington County . Younger people who are entering the sector appear more likely to be producing niche-style product e .g . wool/fibre, artisanal cheeses, organic, etc .

12 Agriculture Research Project - December 2015

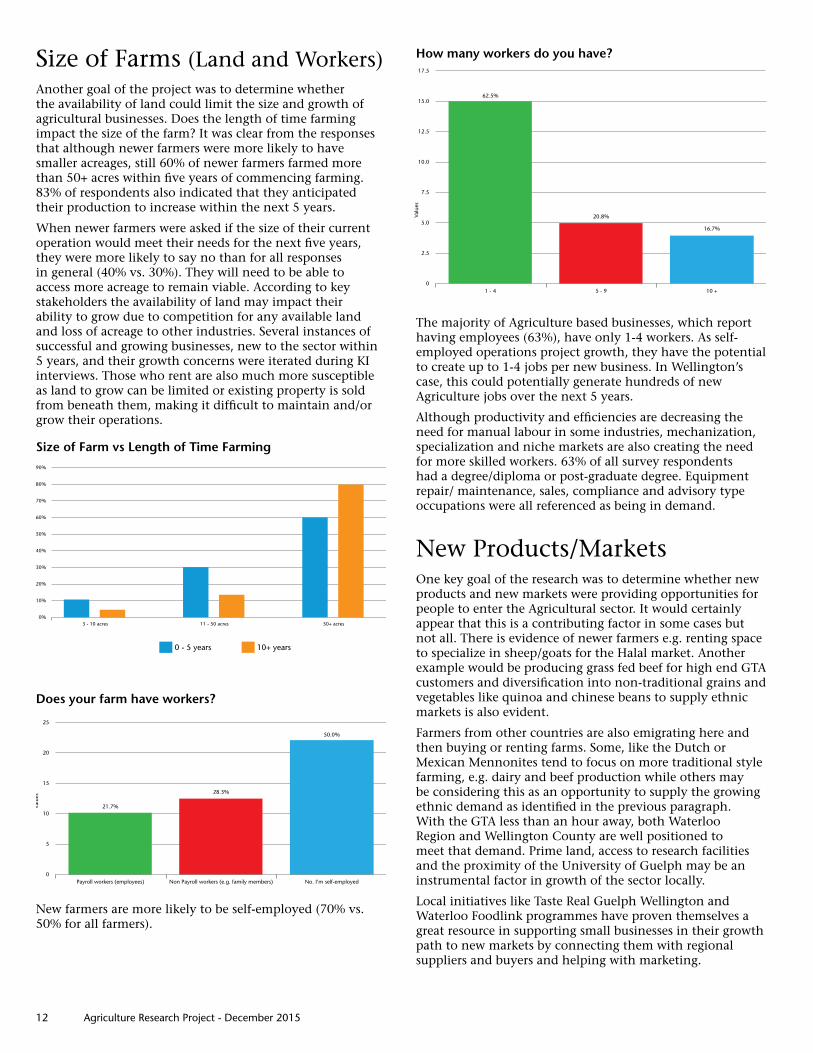

Size of Farms (Land and Workers)Another goal of the project was to determine whether the availability of land could limit the size and growth of agricultural businesses . Does the length of time farming impact the size of the farm? It was clear from the responses that although newer farmers were more likely to have smaller acreages, still 60% of newer farmers farmed more than 50+ acres within five years of commencing farming . 83% of respondents also indicated that they anticipated their production to increase within the next 5 years .

When newer farmers were asked if the size of their current operation would meet their needs for the next five years, they were more likely to say no than for all responses in general (40% vs . 30%) . They will need to be able to access more acreage to remain viable . According to key stakeholders the availability of land may impact their ability to grow due to competition for any available land and loss of acreage to other industries . Several instances of successful and growing businesses, new to the sector within 5 years, and their growth concerns were iterated during KI interviews . Those who rent are also much more susceptible as land to grow can be limited or existing property is sold from beneath them, making it difficult to maintain and/or grow their operations .

Size of Farm vs Length of Time Farming

Does your farm have workers?

New farmers are more likely to be self-employed (70% vs . 50% for all farmers) .

How many workers do you have?

The majority of Agriculture based businesses, which report having employees (63%), have only 1-4 workers . As self-employed operations project growth, they have the potential to create up to 1-4 jobs per new business . In Wellington’s case, this could potentially generate hundreds of new Agriculture jobs over the next 5 years .

Although productivity and efficiencies are decreasing the need for manual labour in some industries, mechanization, specialization and niche markets are also creating the need for more skilled workers . 63% of all survey respondents had a degree/diploma or post-graduate degree . Equipment repair/ maintenance, sales, compliance and advisory type occupations were all referenced as being in demand .

New Products/MarketsOne key goal of the research was to determine whether new products and new markets were providing opportunities for people to enter the Agricultural sector . It would certainly appear that this is a contributing factor in some cases but not all . There is evidence of newer farmers e .g . renting space to specialize in sheep/goats for the Halal market . Another example would be producing grass fed beef for high end GTA customers and diversification into non-traditional grains and vegetables like quinoa and chinese beans to supply ethnic markets is also evident .

Farmers from other countries are also emigrating here and then buying or renting farms . Some, like the Dutch or Mexican Mennonites tend to focus on more traditional style farming, e .g . dairy and beef production while others may be considering this as an opportunity to supply the growing ethnic demand as identified in the previous paragraph . With the GTA less than an hour away, both Waterloo Region and Wellington County are well positioned to meet that demand . Prime land, access to research facilities and the proximity of the University of Guelph may be an instrumental factor in growth of the sector locally .

Local initiatives like Taste Real Guelph Wellington and Waterloo Foodlink programmes have proven themselves a great resource in supporting small businesses in their growth path to new markets by connecting them with regional suppliers and buyers and helping with marketing .

Agriculture Research Project - December 2015 13

KEY CONSIDERATIONSIt is clear that we have only scratched the surface with this research but some clear findings are already evident from this initial piece of work .

1) A centralized registry of available acreage for rent/purchase would make it easier and quicker for new farmers to locate available land

2) There is potential for municipalities (or others) to take over (buy) large farms up for sale in their jurisdiction and lease/rent out that land on 3-5-10 year time periods to new or growing farms

3) More in depth research is required to investigate specific key industry growth, the various reasons for that growth and how to best support future growth in these key industries

4) Zoning/bylaw considerations to balance Ag growth with the real need for population growth and land management e .g . re housing, quarrying, etc .

.

5) Bring all Ag stakeholders together regularly (Annual event?) and provide greater opportunities for collaboration between County of Wellington, Waterloo Region and beyond

6) How to potentially tie into new initiatives e .g . Growing Forward 2, Premier’s Challenge, etc

If this region of Ontario is, in fact, an incubator for the province’s entire Agriculture sector, it is imperative that we fully understand the opportunities and implications we are facing in order to be able to manage and maintain that momentum of growth/change and the next generation of new farmers .

14 Agriculture Research Project - December 2015

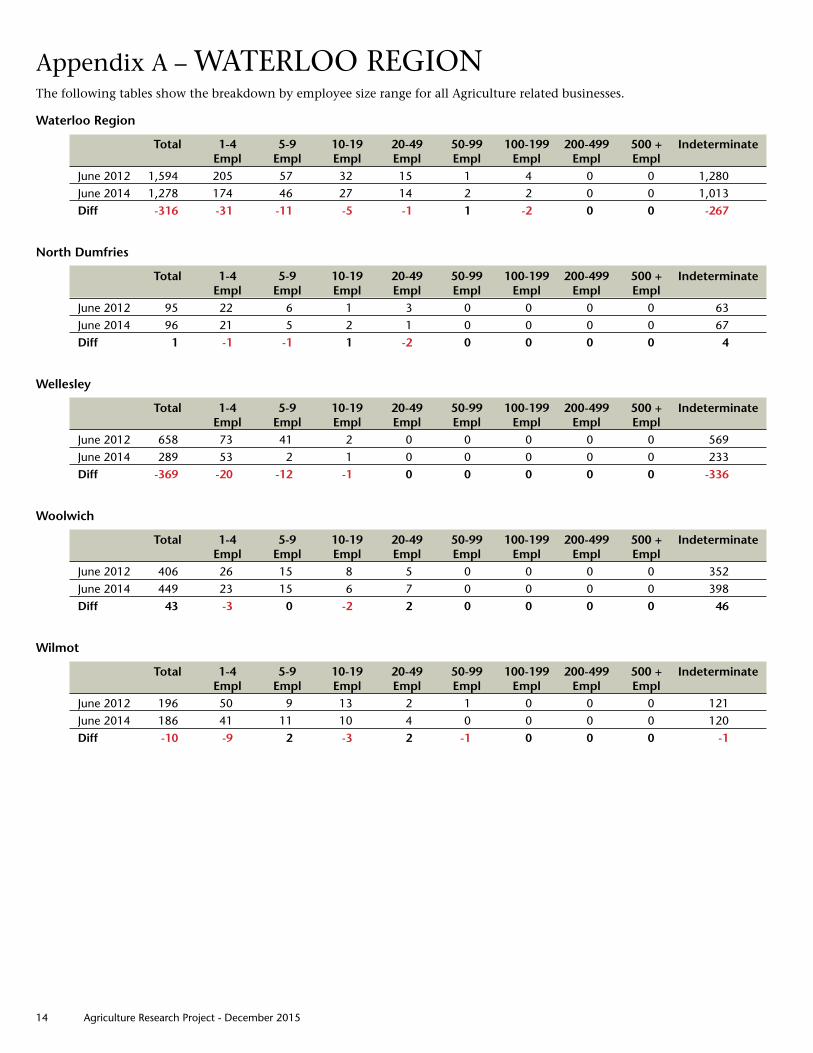

Appendix A – WATERLOO REGIONThe following tables show the breakdown by employee size range for all Agriculture related businesses .

Waterloo Region

Total 1-4 5-9 10-19 20-49 50-99 100-199 200-499 500 + Indeterminate Empl Empl Empl Empl Empl Empl Empl Empl

June 2012 1,594 205 57 32 15 1 4 0 0 1,280June 2014 1,278 174 46 27 14 2 2 0 0 1,013Diff -316 -31 -11 -5 -1 1 -2 0 0 -267

North Dumfries

Total 1-4 5-9 10-19 20-49 50-99 100-199 200-499 500 + Indeterminate Empl Empl Empl Empl Empl Empl Empl Empl

June 2012 95 22 6 1 3 0 0 0 0 63June 2014 96 21 5 2 1 0 0 0 0 67Diff 1 -1 -1 1 -2 0 0 0 0 4

Wellesley

Total 1-4 5-9 10-19 20-49 50-99 100-199 200-499 500 + Indeterminate Empl Empl Empl Empl Empl Empl Empl Empl

June 2012 658 73 41 2 0 0 0 0 0 569June 2014 289 53 2 1 0 0 0 0 0 233Diff -369 -20 -12 -1 0 0 0 0 0 -336

Woolwich

Total 1-4 5-9 10-19 20-49 50-99 100-199 200-499 500 + Indeterminate Empl Empl Empl Empl Empl Empl Empl Empl

June 2012 406 26 15 8 5 0 0 0 0 352June 2014 449 23 15 6 7 0 0 0 0 398Diff 43 -3 0 -2 2 0 0 0 0 46

Wilmot

Total 1-4 5-9 10-19 20-49 50-99 100-199 200-499 500 + Indeterminate Empl Empl Empl Empl Empl Empl Empl Empl

June 2012 196 50 9 13 2 1 0 0 0 121June 2014 186 41 11 10 4 0 0 0 0 120Diff -10 -9 2 -3 2 -1 0 0 0 -1

Agriculture Research Project - December 2015 15

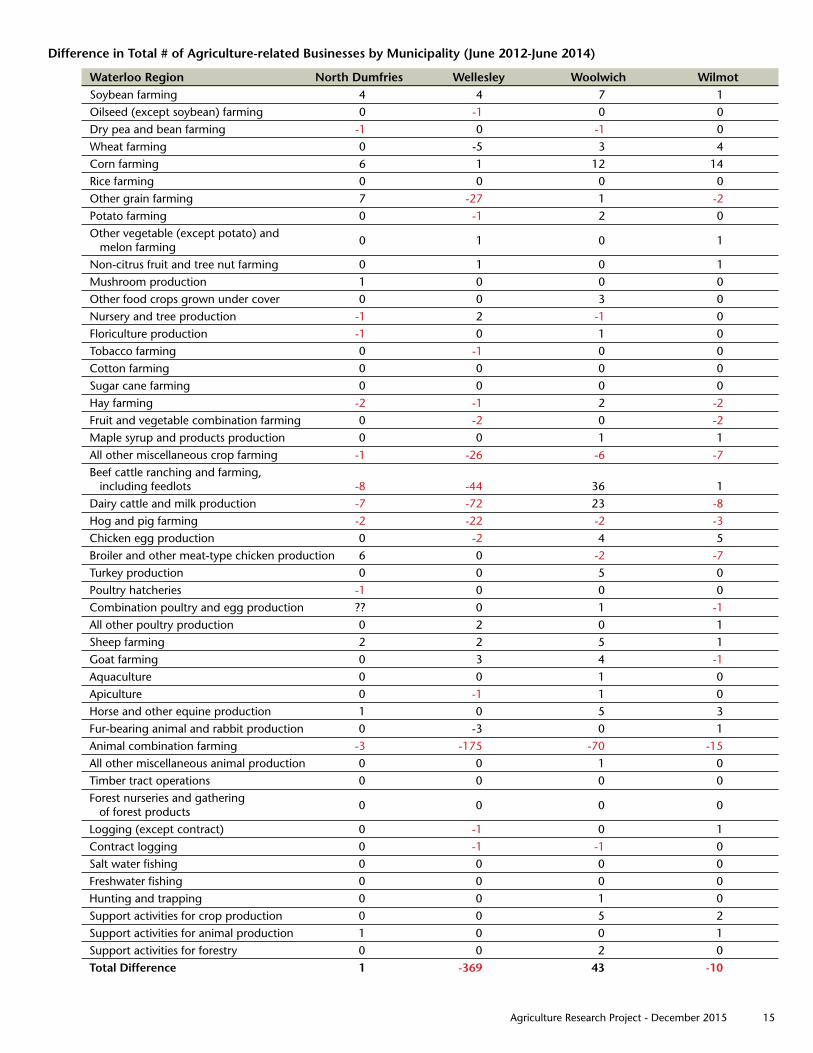

Difference in Total # of Agriculture-related Businesses by Municipality (June 2012-June 2014)

Waterloo Region North Dumfries Wellesley Woolwich WilmotSoybean farming 4 4 7 1Oilseed (except soybean) farming 0 -1 0 0Dry pea and bean farming -1 0 -1 0Wheat farming 0 -5 3 4Corn farming 6 1 12 14Rice farming 0 0 0 0Other grain farming 7 -27 1 -2Potato farming 0 -1 2 0Other vegetable (except potato) and melon farming 0 1 0 1

Non-citrus fruit and tree nut farming 0 1 0 1Mushroom production 1 0 0 0Other food crops grown under cover 0 0 3 0Nursery and tree production -1 2 -1 0Floriculture production -1 0 1 0Tobacco farming 0 -1 0 0Cotton farming 0 0 0 0Sugar cane farming 0 0 0 0Hay farming -2 -1 2 -2Fruit and vegetable combination farming 0 -2 0 -2Maple syrup and products production 0 0 1 1All other miscellaneous crop farming -1 -26 -6 -7Beef cattle ranching and farming, including feedlots -8 -44 36 1Dairy cattle and milk production -7 -72 23 -8Hog and pig farming -2 -22 -2 -3Chicken egg production 0 -2 4 5Broiler and other meat-type chicken production 6 0 -2 -7Turkey production 0 0 5 0Poultry hatcheries -1 0 0 0Combination poultry and egg production ?? 0 1 -1All other poultry production 0 2 0 1Sheep farming 2 2 5 1Goat farming 0 3 4 -1Aquaculture 0 0 1 0Apiculture 0 -1 1 0Horse and other equine production 1 0 5 3Fur-bearing animal and rabbit production 0 -3 0 1Animal combination farming -3 -175 -70 -15All other miscellaneous animal production 0 0 1 0Timber tract operations 0 0 0 0Forest nurseries and gathering of forest products 0 0 0 0

Logging (except contract) 0 -1 0 1Contract logging 0 -1 -1 0Salt water fishing 0 0 0 0Freshwater fishing 0 0 0 0Hunting and trapping 0 0 1 0Support activities for crop production 0 0 5 2Support activities for animal production 1 0 0 1Support activities for forestry 0 0 2 0Total Difference 1 -369 43 -10

16 Agriculture Research Project - December 2015

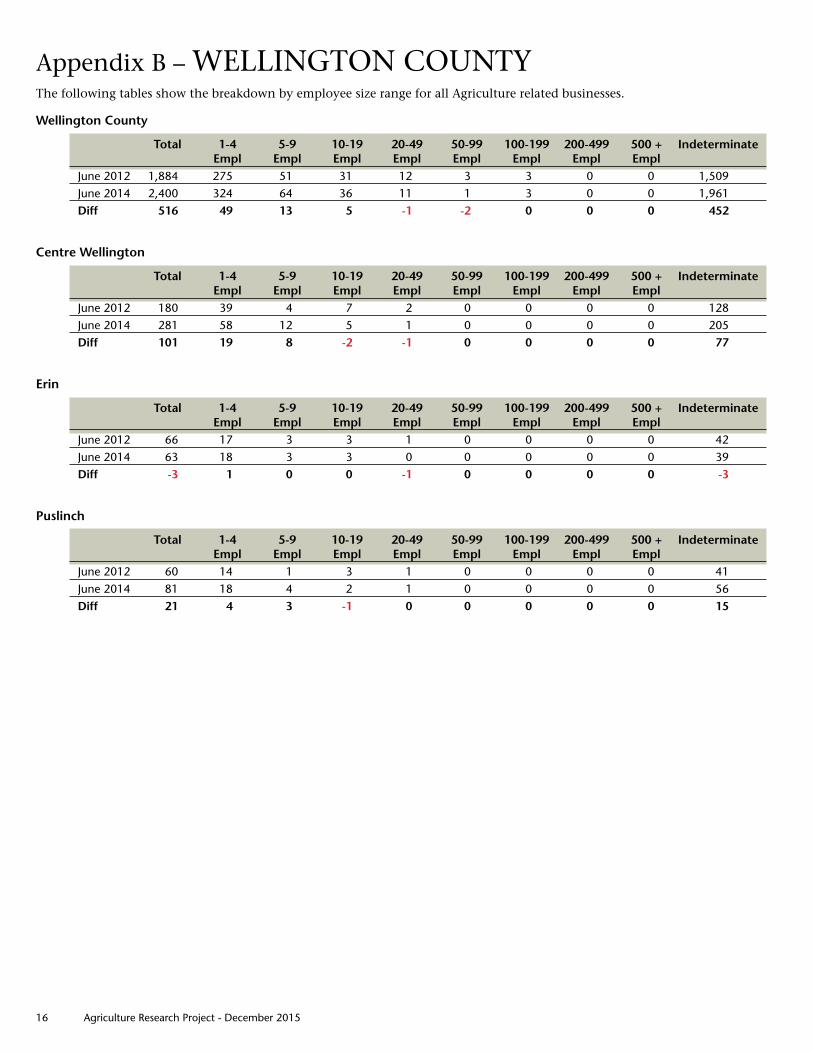

Appendix B – WELLINGTON COUNTYThe following tables show the breakdown by employee size range for all Agriculture related businesses .

Wellington County

Total 1-4 5-9 10-19 20-49 50-99 100-199 200-499 500 + Indeterminate Empl Empl Empl Empl Empl Empl Empl Empl

June 2012 1,884 275 51 31 12 3 3 0 0 1,509June 2014 2,400 324 64 36 11 1 3 0 0 1,961Diff 516 49 13 5 -1 -2 0 0 0 452

Centre Wellington

Total 1-4 5-9 10-19 20-49 50-99 100-199 200-499 500 + Indeterminate Empl Empl Empl Empl Empl Empl Empl Empl

June 2012 180 39 4 7 2 0 0 0 0 128June 2014 281 58 12 5 1 0 0 0 0 205Diff 101 19 8 -2 -1 0 0 0 0 77

Erin

Total 1-4 5-9 10-19 20-49 50-99 100-199 200-499 500 + Indeterminate Empl Empl Empl Empl Empl Empl Empl Empl

June 2012 66 17 3 3 1 0 0 0 0 42June 2014 63 18 3 3 0 0 0 0 0 39Diff -3 1 0 0 -1 0 0 0 0 -3

Puslinch

Total 1-4 5-9 10-19 20-49 50-99 100-199 200-499 500 + Indeterminate Empl Empl Empl Empl Empl Empl Empl Empl

June 2012 60 14 1 3 1 0 0 0 0 41June 2014 81 18 4 2 1 0 0 0 0 56Diff 21 4 3 -1 0 0 0 0 0 15

Agriculture Research Project - December 2015 17

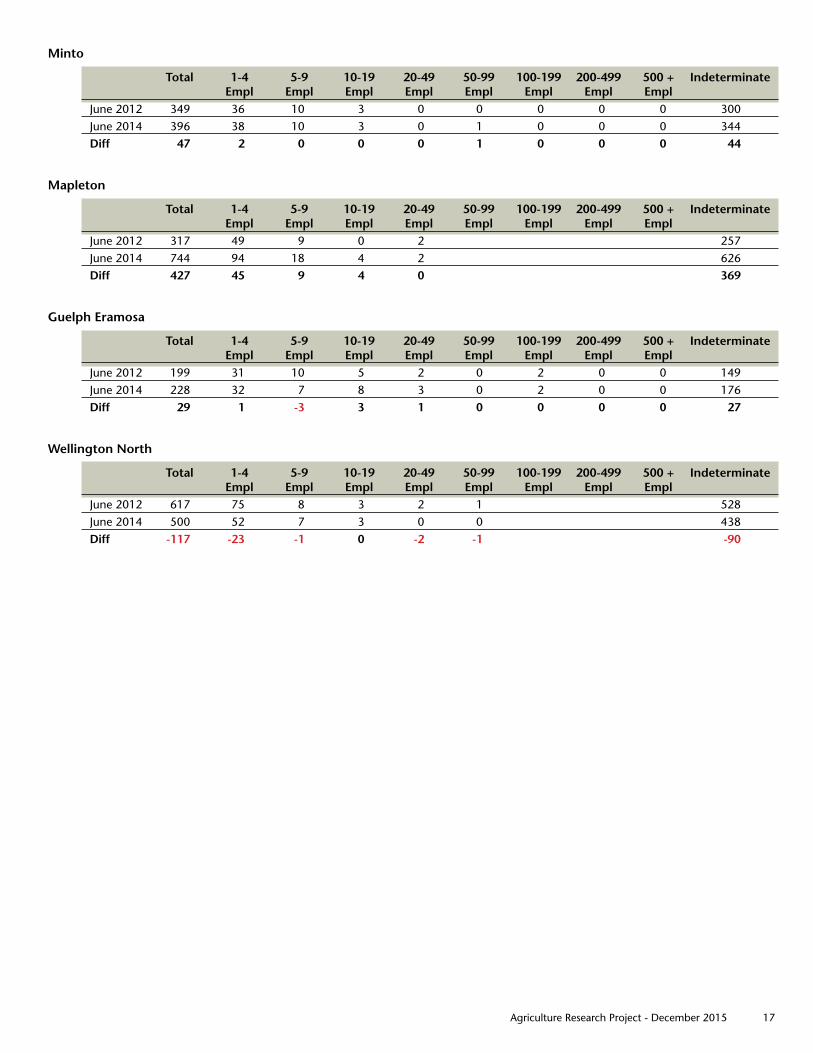

Minto

Total 1-4 5-9 10-19 20-49 50-99 100-199 200-499 500 + Indeterminate Empl Empl Empl Empl Empl Empl Empl Empl

June 2012 349 36 10 3 0 0 0 0 0 300June 2014 396 38 10 3 0 1 0 0 0 344Diff 47 2 0 0 0 1 0 0 0 44

Mapleton

Total 1-4 5-9 10-19 20-49 50-99 100-199 200-499 500 + Indeterminate Empl Empl Empl Empl Empl Empl Empl Empl

June 2012 317 49 9 0 2 257June 2014 744 94 18 4 2 626Diff 427 45 9 4 0 369

Guelph Eramosa

Total 1-4 5-9 10-19 20-49 50-99 100-199 200-499 500 + Indeterminate Empl Empl Empl Empl Empl Empl Empl Empl

June 2012 199 31 10 5 2 0 2 0 0 149June 2014 228 32 7 8 3 0 2 0 0 176Diff 29 1 -3 3 1 0 0 0 0 27

Wellington North

Total 1-4 5-9 10-19 20-49 50-99 100-199 200-499 500 + Indeterminate Empl Empl Empl Empl Empl Empl Empl Empl

June 2012 617 75 8 3 2 1 528June 2014 500 52 7 3 0 0 438Diff -117 -23 -1 0 -2 -1 -90

18 Agriculture Research Project - December 2015

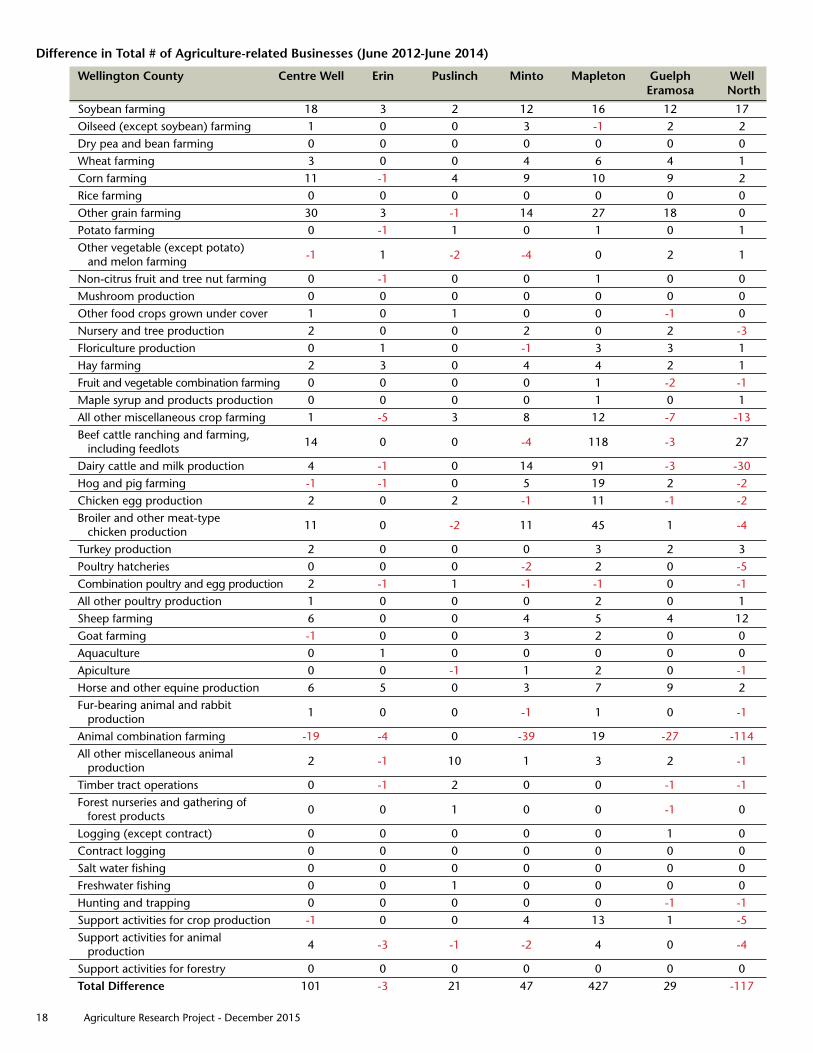

Difference in Total # of Agriculture-related Businesses (June 2012-June 2014)

Wellington County Centre Well Erin Puslinch Minto Mapleton Guelph Well Eramosa North

Soybean farming 18 3 2 12 16 12 17Oilseed (except soybean) farming 1 0 0 3 -1 2 2Dry pea and bean farming 0 0 0 0 0 0 0Wheat farming 3 0 0 4 6 4 1Corn farming 11 -1 4 9 10 9 2Rice farming 0 0 0 0 0 0 0Other grain farming 30 3 -1 14 27 18 0Potato farming 0 -1 1 0 1 0 1Other vegetable (except potato) and melon farming -1 1 -2 -4 0 2 1

Non-citrus fruit and tree nut farming 0 -1 0 0 1 0 0Mushroom production 0 0 0 0 0 0 0Other food crops grown under cover 1 0 1 0 0 -1 0Nursery and tree production 2 0 0 2 0 2 -3Floriculture production 0 1 0 -1 3 3 1Hay farming 2 3 0 4 4 2 1Fruit and vegetable combination farming 0 0 0 0 1 -2 -1Maple syrup and products production 0 0 0 0 1 0 1All other miscellaneous crop farming 1 -5 3 8 12 -7 -13Beef cattle ranching and farming, including feedlots 14 0 0 -4 118 -3 27

Dairy cattle and milk production 4 -1 0 14 91 -3 -30Hog and pig farming -1 -1 0 5 19 2 -2Chicken egg production 2 0 2 -1 11 -1 -2Broiler and other meat-type chicken production 11 0 -2 11 45 1 -4

Turkey production 2 0 0 0 3 2 3Poultry hatcheries 0 0 0 -2 2 0 -5Combination poultry and egg production 2 -1 1 -1 -1 0 -1All other poultry production 1 0 0 0 2 0 1Sheep farming 6 0 0 4 5 4 12Goat farming -1 0 0 3 2 0 0Aquaculture 0 1 0 0 0 0 0Apiculture 0 0 -1 1 2 0 -1Horse and other equine production 6 5 0 3 7 9 2Fur-bearing animal and rabbit production 1 0 0 -1 1 0 -1

Animal combination farming -19 -4 0 -39 19 -27 -114All other miscellaneous animal production 2 -1 10 1 3 2 -1

Timber tract operations 0 -1 2 0 0 -1 -1Forest nurseries and gathering of forest products 0 0 1 0 0 -1 0

Logging (except contract) 0 0 0 0 0 1 0Contract logging 0 0 0 0 0 0 0Salt water fishing 0 0 0 0 0 0 0Freshwater fishing 0 0 1 0 0 0 0Hunting and trapping 0 0 0 0 0 -1 -1Support activities for crop production -1 0 0 4 13 1 -5Support activities for animal production 4 -3 -1 -2 4 0 -4

Support activities for forestry 0 0 0 0 0 0 0Total Difference 101 -3 21 47 427 29 -117

Agriculture Research Project - December 2015 19

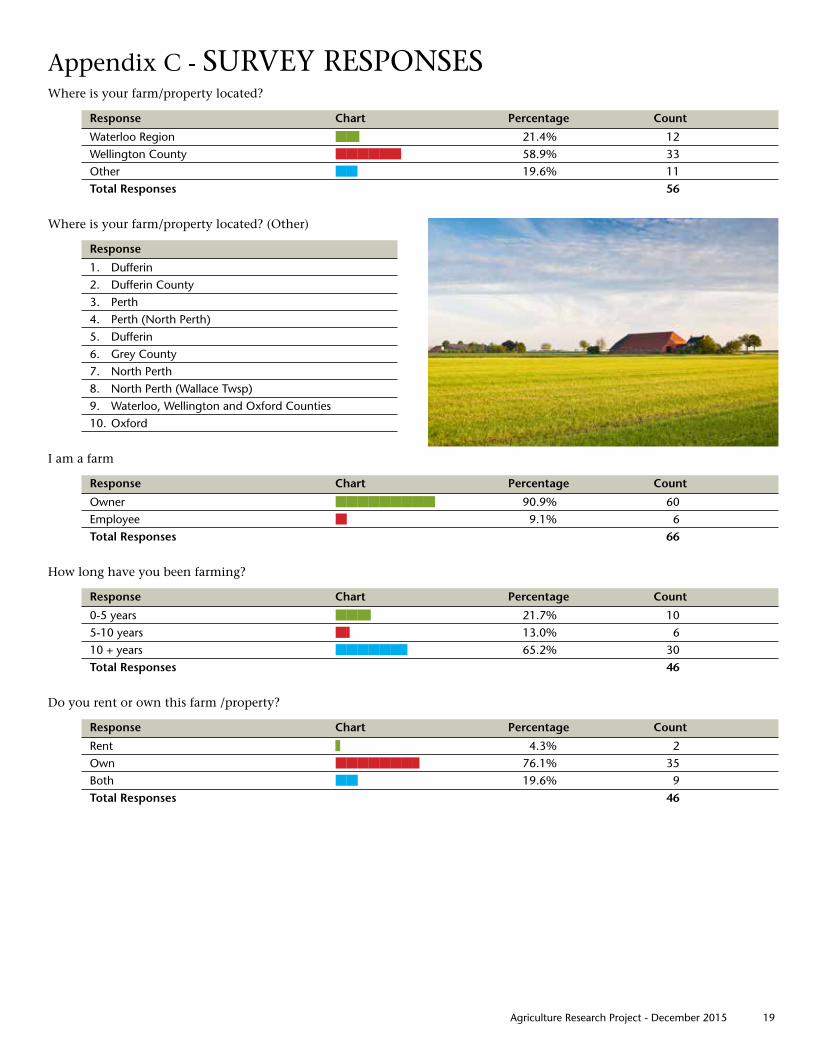

Appendix C - SURVEY RESPONSESWhere is your farm/property located?

Response Chart Percentage Count

Waterloo Region nn 21.4% 12Wellington County nnnnnn 58.9% 33Other nn 19.6% 11Total Responses 56

Where is your farm/property located? (Other)

Response

1. Dufferin 2. Dufferin County3. Perth4. Perth (North Perth)5. Dufferin6. Grey County7. North Perth8. North Perth (Wallace Twsp)9. Waterloo, Wellington and Oxford Counties10. Oxford

I am a farm

Response Chart Percentage Count

Owner nnnnnnnnn 90.9% 60Employee n 9.1% 6Total Responses 66

How long have you been farming?

Response Chart Percentage Count

0-5 years nnn 21.7% 105-10 years nn 13.0% 610 + years nnnnnnn 65.2% 30Total Responses 46

Do you rent or own this farm /property?

Response Chart Percentage Count

Rent n 4.3% 2Own nnnnnnnn 76.1% 35Both nn 19.6% 9Total Responses 46

20 Agriculture Research Project - December 2015

How did you get into farming?

Response Chart Percentage Count

Family farm operation nnnnn 47.8% 22Rural lifestyle - former non-farmer n 8.7% 4Former farmer in another country n 4.3% 2Entrepreneur - new business opportunies nn 19.6% 9Moved from urban centre nn 13.0% 6Training program 0.0% 0Other, please specify... n 10.9% 5Total Responses 46

How did you get into farming? (Other, please specify . . .)

Response

1. Raised on a farm2. From family farm in SK. worked in ag industry as sales manager, viictim of corporate merger so started farming3. Grew up on a farm, only lifestyle I know4. Grew up on a farm, but then purchased our own farm.5. Grew up on a farm, worked on farms, bought our own at age 21

Does your farm have workers?

Response Chart Percentage Count

Payroll workers (employees) nnn 21.7% 10Non Payroll workers (e,g, family members) nnn 28.3% 13No. I’m self-employed nnnnn 50.0% 23Total Responses 46

How many workers are on your farm?

Response Chart Percentage Count

1-4 nnnnnnn 62.5% 155-9 nn 20.8% 510+ nn 16.7% 4Total Responses 24

Do you have any formal training related to Agriculture?

Response Chart Percentage Count

Yes nnnnnn 53.8% 14No nnnnn 46.2% 12Total Responses 26

Agriculture Research Project - December 2015 21

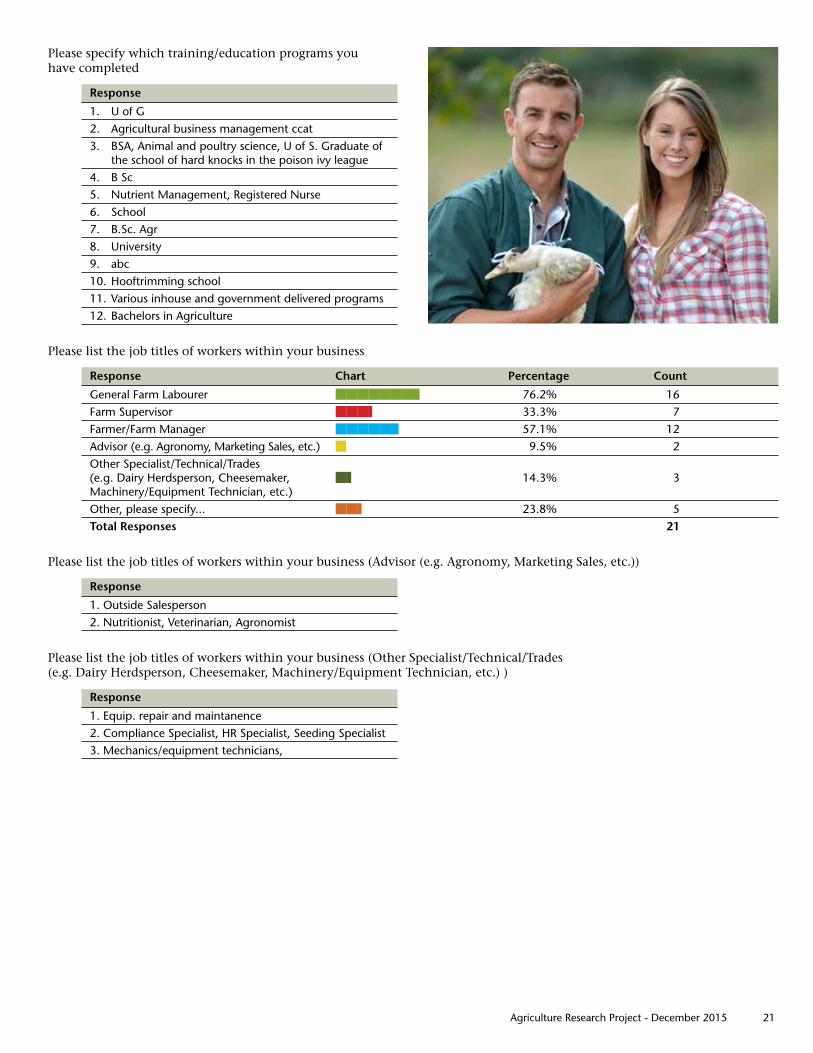

Please specify which training/education programs you have completed

Response

1. U of G2. Agricultural business management ccat3. BSA, Animal and poultry science, U of S. Graduate of the school of hard knocks in the poison ivy league4. B Sc5. Nutrient Management, Registered Nurse6. School7. B.Sc. Agr8. University9. abc10. Hooftrimming school11. Various inhouse and government delivered programs12. Bachelors in Agriculture

Please list the job titles of workers within your business

Response Chart Percentage Count

General Farm Labourer nnnnnnnn 76.2% 16Farm Supervisor nnnn 33.3% 7Farmer/Farm Manager nnnnnn 57.1% 12Advisor (e.g. Agronomy, Marketing Sales, etc.) n 9.5% 2Other Specialist/Technical/Trades (e.g. Dairy Herdsperson, Cheesemaker, nn 14.3% 3 Machinery/Equipment Technician, etc.) Other, please specify... nnn 23.8% 5Total Responses 21

Please list the job titles of workers within your business (Advisor (e .g . Agronomy, Marketing Sales, etc .))

Response

1. Outside Salesperson2. Nutritionist, Veterinarian, Agronomist

Please list the job titles of workers within your business (Other Specialist/Technical/Trades (e .g . Dairy Herdsperson, Cheesemaker, Machinery/Equipment Technician, etc .) )

Response

1. Equip. repair and maintanence2. Compliance Specialist, HR Specialist, Seeding Specialist3. Mechanics/equipment technicians,

22 Agriculture Research Project - December 2015

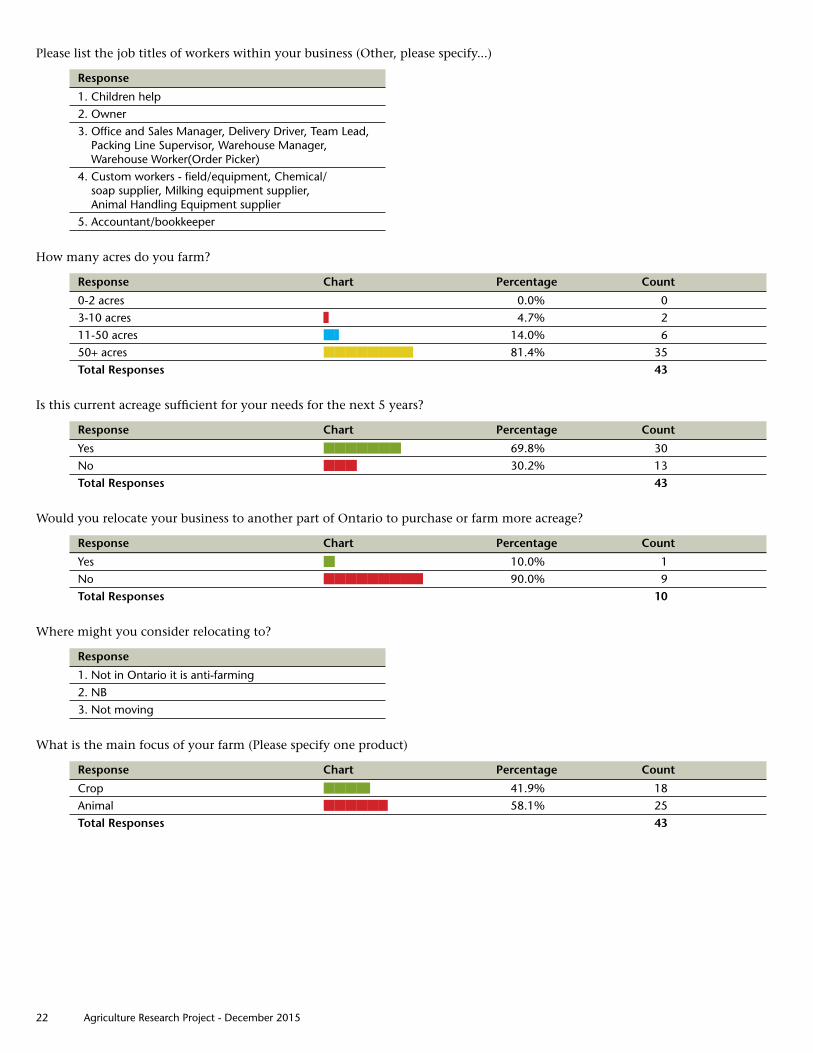

Please list the job titles of workers within your business (Other, please specify . . .)

Response

1. Children help2. Owner3. Office and Sales Manager, Delivery Driver, Team Lead, Packing Line Supervisor, Warehouse Manager, Warehouse Worker(Order Picker)4. Custom workers - field/equipment, Chemical/ soap supplier, Milking equipment supplier, Animal Handling Equipment supplier5. Accountant/bookkeeper

How many acres do you farm?

Response Chart Percentage Count

0-2 acres 0.0% 03-10 acres n 4.7% 211-50 acres nn 14.0% 650+ acres nnnnnnnnn 81.4% 35Total Responses 43

Is this current acreage sufficient for your needs for the next 5 years?

Response Chart Percentage Count

Yes nnnnnnn 69.8% 30No nnn 30.2% 13Total Responses 43

Would you relocate your business to another part of Ontario to purchase or farm more acreage?

Response Chart Percentage Count

Yes n 10.0% 1No nnnnnnnnn 90.0% 9Total Responses 10

Where might you consider relocating to?

Response

1. Not in Ontario it is anti-farming2. NB3. Not moving

What is the main focus of your farm (Please specify one product)

Response Chart Percentage Count

Crop nnnn 41.9% 18Animal nnnnnn 58.1% 25Total Responses 43

Agriculture Research Project - December 2015 23

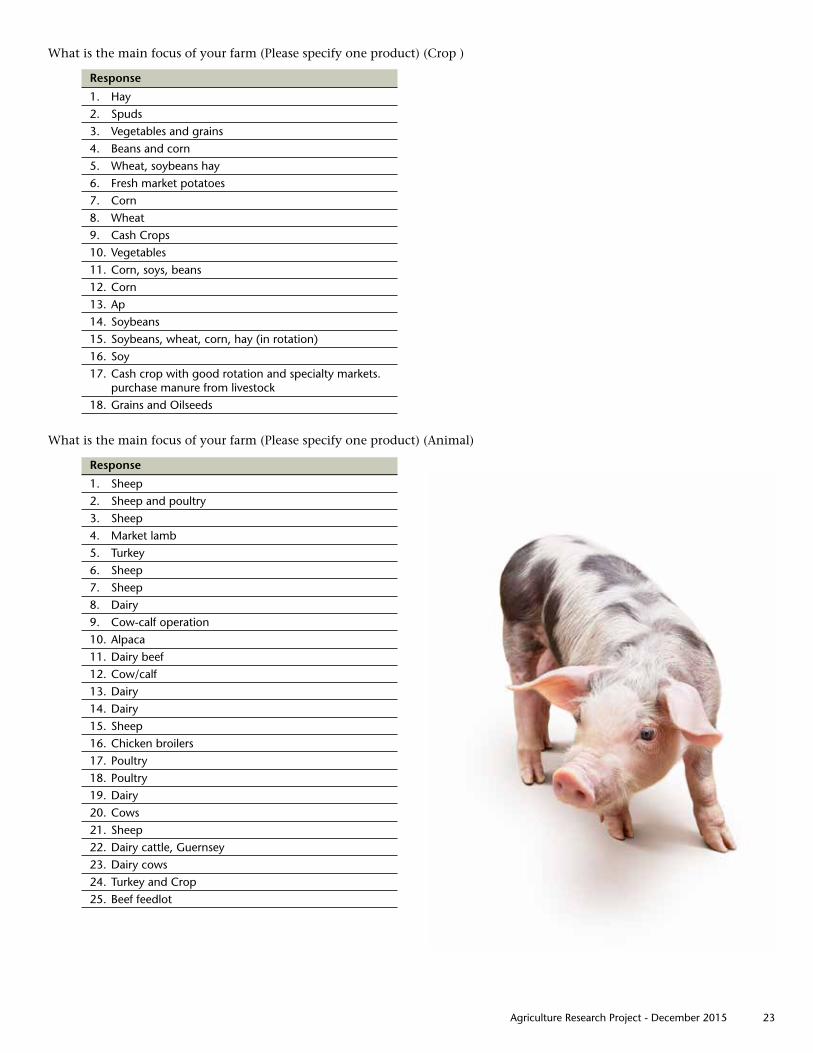

What is the main focus of your farm (Please specify one product) (Crop )

Response

1. Hay2. Spuds3. Vegetables and grains4. Beans and corn5. Wheat, soybeans hay6. Fresh market potatoes7. Corn8. Wheat9. Cash Crops10. Vegetables11. Corn, soys, beans12. Corn13. Ap14. Soybeans15. Soybeans, wheat, corn, hay (in rotation)16. Soy17. Cash crop with good rotation and specialty markets. purchase manure from livestock 18. Grains and Oilseeds

What is the main focus of your farm (Please specify one product) (Animal)

Response

1. Sheep2. Sheep and poultry3. Sheep4. Market lamb5. Turkey6. Sheep 7. Sheep8. Dairy9. Cow-calf operation 10. Alpaca11. Dairy beef12. Cow/calf13. Dairy14. Dairy15. Sheep16. Chicken broilers17. Poultry18. Poultry19. Dairy20. Cows21. Sheep22. Dairy cattle, Guernsey23. Dairy cows24. Turkey and Crop25. Beef feedlot

24 Agriculture Research Project - December 2015

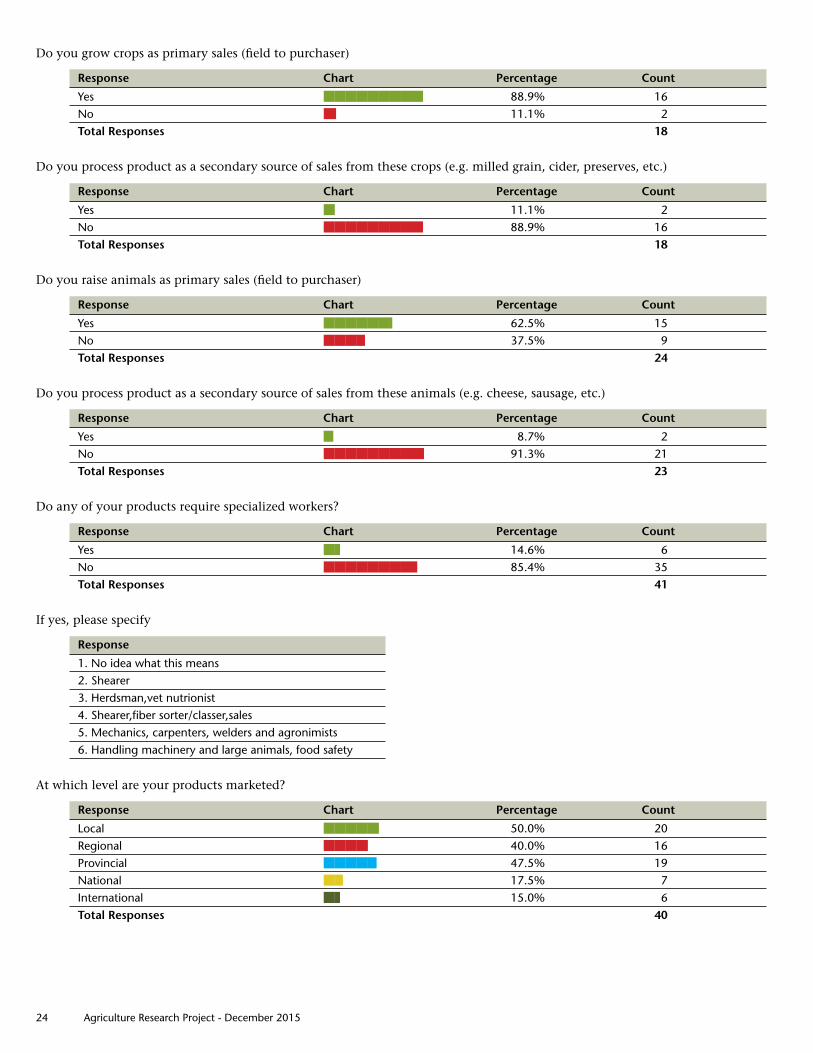

Do you grow crops as primary sales (field to purchaser)

Response Chart Percentage Count

Yes nnnnnnnnn 88.9% 16No n 11.1% 2Total Responses 18

Do you process product as a secondary source of sales from these crops (e .g . milled grain, cider, preserves, etc .)

Response Chart Percentage Count

Yes n 11.1% 2No nnnnnnnnn 88.9% 16Total Responses 18

Do you raise animals as primary sales (field to purchaser)

Response Chart Percentage Count

Yes nnnnnnn 62.5% 15No nnnn 37.5% 9Total Responses 24

Do you process product as a secondary source of sales from these animals (e .g . cheese, sausage, etc .)

Response Chart Percentage Count

Yes n 8.7% 2No nnnnnnnnnn 91.3% 21Total Responses 23

Do any of your products require specialized workers?

Response Chart Percentage Count

Yes nn 14.6% 6No nnnnnnnnn 85.4% 35Total Responses 41

If yes, please specify

Response

1. No idea what this means2. Shearer3. Herdsman,vet nutrionist4. Shearer,fiber sorter/classer,sales5. Mechanics, carpenters, welders and agronimists6. Handling machinery and large animals, food safety

At which level are your products marketed?

Response Chart Percentage Count

Local nnnnn 50.0% 20Regional nnnn 40.0% 16Provincial nnnnn 47.5% 19National nn 17.5% 7International nn 15.0% 6Total Responses 40

Agriculture Research Project - December 2015 25

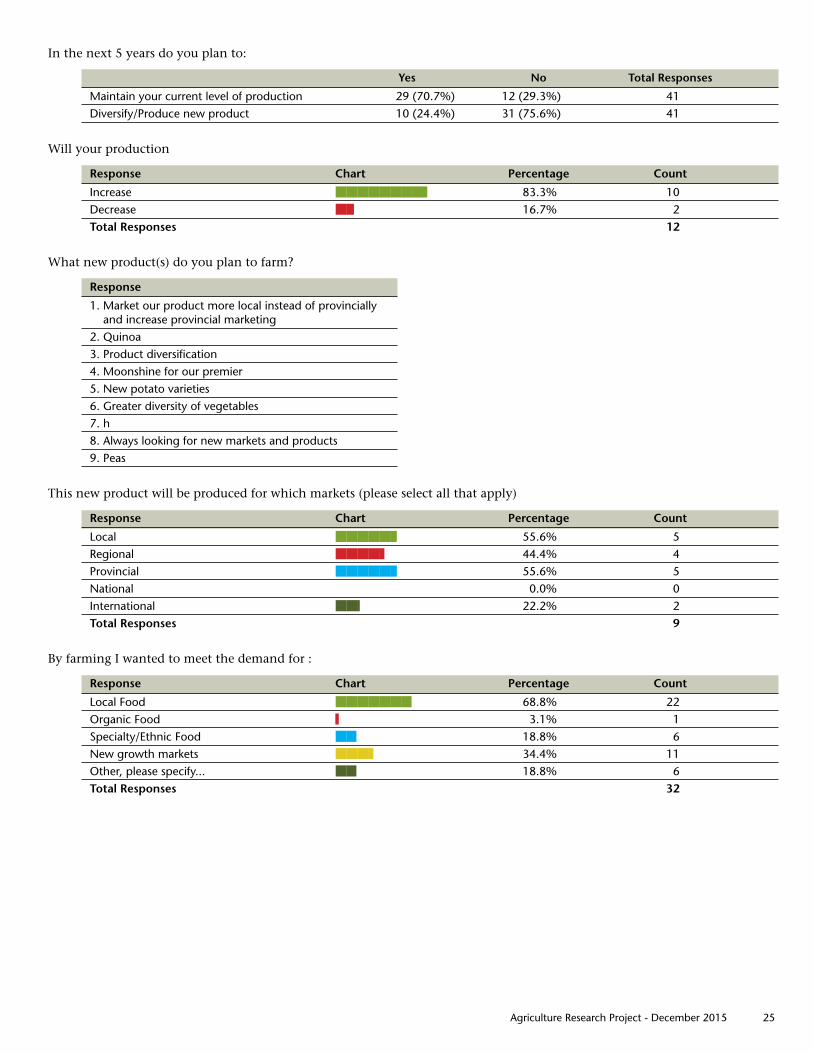

In the next 5 years do you plan to:

Yes No Total Responses

Maintain your current level of production 29 (70.7%) 12 (29.3%) 41Diversify/Produce new product 10 (24.4%) 31 (75.6%) 41

Will your production

Response Chart Percentage Count

Increase nnnnnnnnn 83.3% 10Decrease nn 16.7% 2Total Responses 12

What new product(s) do you plan to farm?

Response

1. Market our product more local instead of provincially and increase provincial marketing2. Quinoa3. Product diversification4. Moonshine for our premier5. New potato varieties6. Greater diversity of vegetables7. h8. Always looking for new markets and products9. Peas

This new product will be produced for which markets (please select all that apply)

Response Chart Percentage Count

Local nnnnnn 55.6% 5Regional nnnnn 44.4% 4Provincial nnnnnn 55.6% 5National 0.0% 0International nnn 22.2% 2Total Responses 9

By farming I wanted to meet the demand for :

Response Chart Percentage Count

Local Food nnnnnnn 68.8% 22Organic Food n 3.1% 1Specialty/Ethnic Food nn 18.8% 6New growth markets nnnn 34.4% 11Other, please specify... nn 18.8% 6Total Responses 32

26 Agriculture Research Project - December 2015

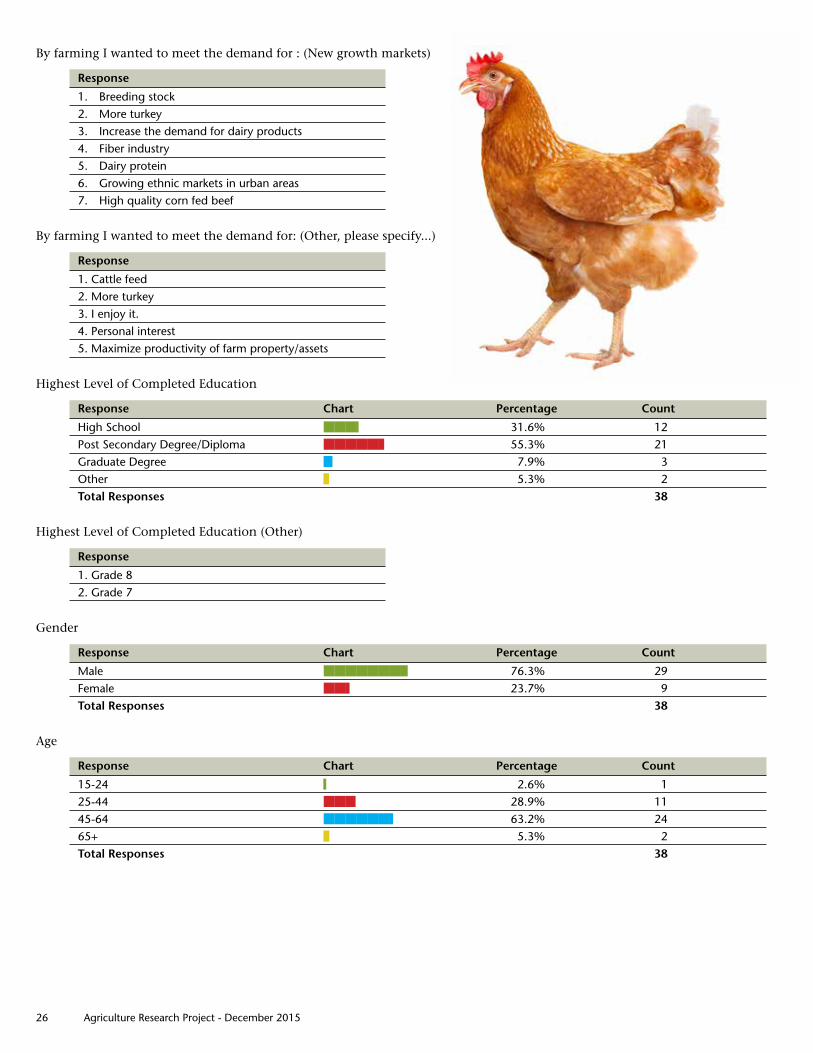

By farming I wanted to meet the demand for : (New growth markets)

Response

1. Breeding stock2. More turkey3. Increase the demand for dairy products4. Fiber industry5. Dairy protein6. Growing ethnic markets in urban areas7. High quality corn fed beef

By farming I wanted to meet the demand for: (Other, please specify . . .)

Response

1. Cattle feed2. More turkey3. I enjoy it.4. Personal interest5. Maximize productivity of farm property/assets

Highest Level of Completed Education

Response Chart Percentage Count

High School nnnn 31.6% 12Post Secondary Degree/Diploma nnnnnn 55.3% 21Graduate Degree n 7.9% 3Other n 5.3% 2Total Responses 38

Highest Level of Completed Education (Other)

Response

1. Grade 82. Grade 7

Gender

Response Chart Percentage Count

Male nnnnnnnn 76.3% 29Female nnn 23.7% 9Total Responses 38

Age

Response Chart Percentage Count

15-24 n 2.6% 125-44 nnn 28.9% 1145-64 nnnnnnn 63.2% 2465+ n 5.3% 2Total Responses 38

Agriculture Research Project - December 2015 27

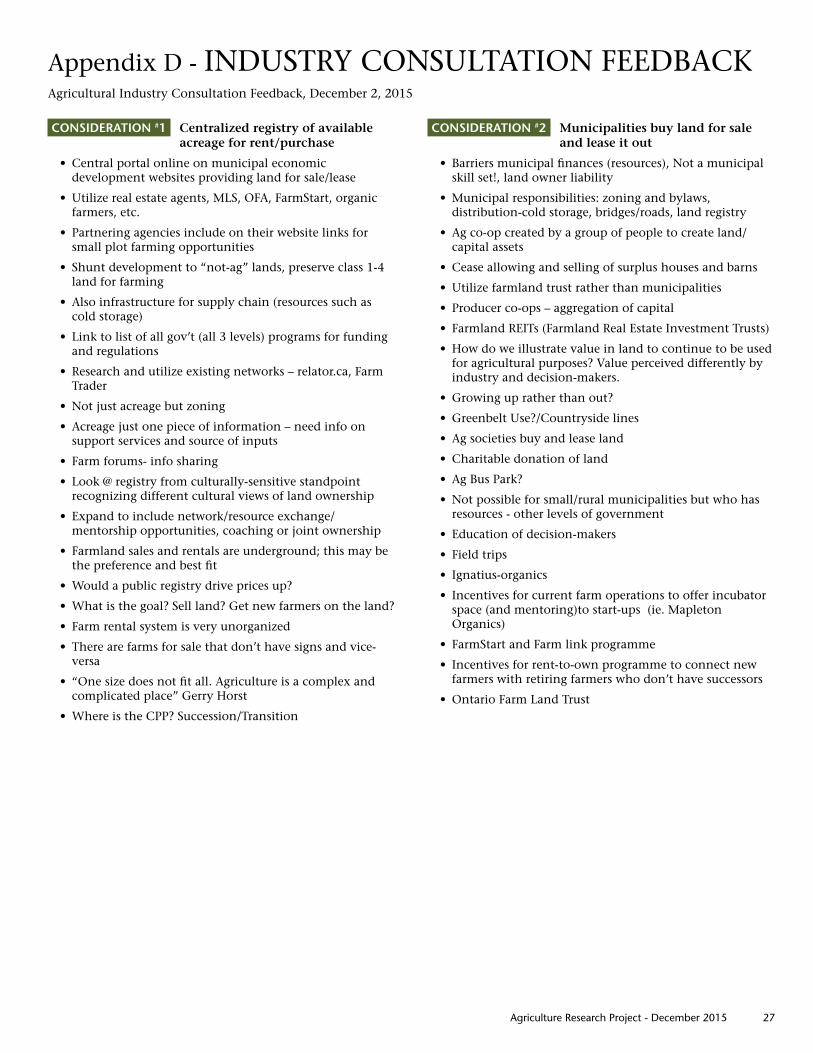

CONSIDERATION #1 Centralized registry of available acreage for rent/purchase

• Central portal online on municipal economic development websites providing land for sale/lease

• Utilize real estate agents, MLS, OFA, FarmStart, organic farmers, etc .

• Partnering agencies include on their website links for small plot farming opportunities

• Shunt development to “not-ag” lands, preserve class 1-4 land for farming

• Also infrastructure for supply chain (resources such as cold storage)

• Link to list of all gov’t (all 3 levels) programs for funding and regulations

• Research and utilize existing networks – relator .ca, Farm Trader

• Not just acreage but zoning

• Acreage just one piece of information – need info on support services and source of inputs

• Farm forums- info sharing

• Look @ registry from culturally-sensitive standpoint recognizing different cultural views of land ownership

• Expand to include network/resource exchange/mentorship opportunities, coaching or joint ownership

• Farmland sales and rentals are underground; this may be the preference and best fit

• Would a public registry drive prices up?

• What is the goal? Sell land? Get new farmers on the land?

• Farm rental system is very unorganized

• There are farms for sale that don’t have signs and vice-versa

• “One size does not fit all . Agriculture is a complex and complicated place” Gerry Horst

• Where is the CPP? Succession/Transition

CONSIDERATION #2 Municipalities buy land for sale and lease it out

• Barriers municipal finances (resources), Not a municipal skill set!, land owner liability

• Municipal responsibilities: zoning and bylaws, distribution-cold storage, bridges/roads, land registry

• Ag co-op created by a group of people to create land/capital assets

• Cease allowing and selling of surplus houses and barns

• Utilize farmland trust rather than municipalities

• Producer co-ops – aggregation of capital

• Farmland REITs (Farmland Real Estate Investment Trusts)

• How do we illustrate value in land to continue to be used for agricultural purposes? Value perceived differently by industry and decision-makers .

• Growing up rather than out?

• Greenbelt Use?/Countryside lines

• Ag societies buy and lease land

• Charitable donation of land

• Ag Bus Park?

• Not possible for small/rural municipalities but who has resources - other levels of government

• Education of decision-makers

• Field trips

• Ignatius-organics

• Incentives for current farm operations to offer incubator space (and mentoring)to start-ups (ie . Mapleton Organics)

• FarmStart and Farm link programme

• Incentives for rent-to-own programme to connect new farmers with retiring farmers who don’t have successors

• Ontario Farm Land Trust

Appendix D - INDUSTRY CONSULTATION FEEDBACK Agricultural Industry Consultation Feedback, December 2, 2015

28 Agriculture Research Project - December 2015

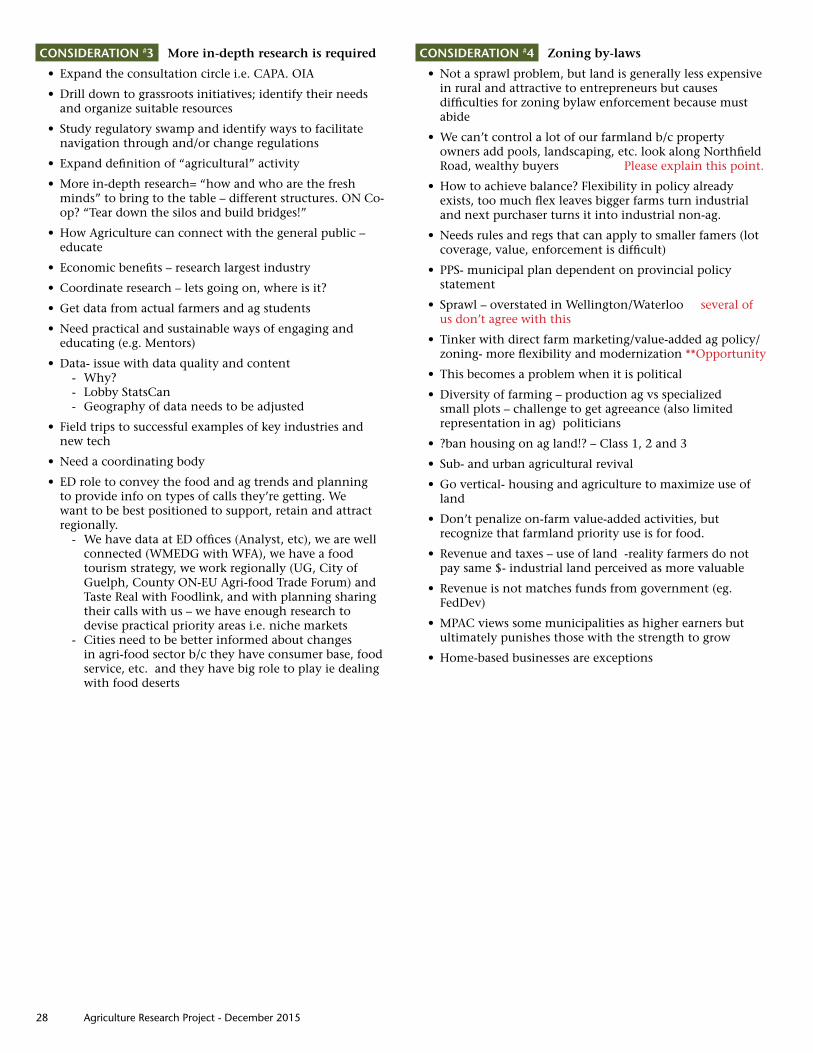

CONSIDERATION #3 More in-depth research is required

• Expand the consultation circle i .e . CAPA . OIA

• Drill down to grassroots initiatives; identify their needs and organize suitable resources

• Study regulatory swamp and identify ways to facilitate navigation through and/or change regulations

• Expand definition of “agricultural” activity

• More in-depth research= “how and who are the fresh minds” to bring to the table – different structures . ON Co-op? “Tear down the silos and build bridges!”

• How Agriculture can connect with the general public – educate

• Economic benefits – research largest industry

• Coordinate research – lets going on, where is it?

• Get data from actual farmers and ag students

• Need practical and sustainable ways of engaging and educating (e .g . Mentors)

• Data- issue with data quality and content - Why? - Lobby StatsCan - Geography of data needs to be adjusted

• Field trips to successful examples of key industries and new tech

• Need a coordinating body

• ED role to convey the food and ag trends and planning to provide info on types of calls they’re getting . We want to be best positioned to support, retain and attract regionally . - We have data at ED offices (Analyst, etc), we are well connected (WMEDG with WFA), we have a food tourism strategy, we work regionally (UG, City of Guelph, County ON-EU Agri-food Trade Forum) and Taste Real with Foodlink, and with planning sharing their calls with us – we have enough research to devise practical priority areas i .e . niche markets - Cities need to be better informed about changes in agri-food sector b/c they have consumer base, food service, etc . and they have big role to play ie dealing with food deserts

CONSIDERATION #4 Zoning by-laws

• Not a sprawl problem, but land is generally less expensive in rural and attractive to entrepreneurs but causes difficulties for zoning bylaw enforcement because must abide

• We can’t control a lot of our farmland b/c property owners add pools, landscaping, etc . look along Northfield Road, wealthy buyers Please explain this point .

• How to achieve balance? Flexibility in policy already exists, too much flex leaves bigger farms turn industrial and next purchaser turns it into industrial non-ag .

• Needs rules and regs that can apply to smaller famers (lot coverage, value, enforcement is difficult)

• PPS- municipal plan dependent on provincial policy statement

• Sprawl – overstated in Wellington/Waterloo several of us don’t agree with this

• Tinker with direct farm marketing/value-added ag policy/zoning- more flexibility and modernization **Opportunity

• This becomes a problem when it is political

• Diversity of farming – production ag vs specialized small plots – challenge to get agreeance (also limited representation in ag) politicians

• ?ban housing on ag land!? – Class 1, 2 and 3

• Sub- and urban agricultural revival

• Go vertical- housing and agriculture to maximize use of land

• Don’t penalize on-farm value-added activities, but recognize that farmland priority use is for food .

• Revenue and taxes – use of land -reality farmers do not pay same $- industrial land perceived as more valuable

• Revenue is not matches funds from government (eg . FedDev)

• MPAC views some municipalities as higher earners but ultimately punishes those with the strength to grow

• Home-based businesses are exceptions

Agriculture Research Project - December 2015 29

CONSIDERATION #5 Bring stakeholders together regularly

• Consider how people can get together to achieve goals, deal with concerns, etc . - workshops, webinars, conference, panel discussions, annual ag summit - email, Skype - trade focus, business practices, education opportunity, regional/provincial/national focus - around an issue? Policy issues/regulations - together: web, face-to-face, network - survey ag biz to see what they want to talk about- when can they attend?

• Since PPS didn’t provide enough clarity around ag issues, province digging deeper via a report currently in draft to be completed winter, speaks to on farm biz

• Wellington Waterloo to include minimum primary ag uses on properties . Enforcement?

• Taste Real Source It Here: B2B networking and learning opportunities . We know our areas id greatest growth across all agri-food chain, useful to share .

• Urban planners and politicians need to better aware of policy implications on rural .

• Events’ audiences are too targeted . Need regional and diverse Ag Day to discuss this!

• This is a workshop about JOBS- so if ag stakeholders get together, it has to be about: - Finding and retaining skilled labour - Who is out there? Give us a website! - Are they interested in ag and/or ag-related business? - How does ag find and attract good labour? - Creative compensation strategies - “selling” the many ag opportunities that exist - Training agri-business employers to be good employers – it’s all about “attitude”

• In addition to annual meeting, utilize technology for continuous/fluid consultation

• Increase intern opportunities to broaden next generation’s awareness of issues

• Provincial Ag Ec Dev Forum already exists – OMAFRA and partner municipality (was in Chatham Kent 2015) Caledon next year?

• Promoting events/collabs already in place

• OMAFRA Dateline (Ag calendar)

• Collaboration is mobilized around common issue/interest where benefit of working together is clear

• Foodlink Waterloo and Taste Real –Source it Here B2B expand?

• Who decides who’s at the table? Inclusivity? Openness>

• Future-focussed

CONSIDERATION #6 Tie into new initiatives

• Communication and collaboration between business and decision makers

• Before initiatives are developed, make sure that: - They are coordinated - They are understood - They can be implemented

• Task Force

• Directory of programs

• Get a group to develop and implement communications program about initiatives- webinars, marketing, training

• Training sessions with all initiatives

• Farming is diverse-size and markets- and keeps changing

• Myths/misconceptions/lack of information

• Many bodies deal with farming issues

• Need exchange of ideas among different sectors – farmers/government

• Farmers are a close network, are they exchanging ideas with people outside the field

• Get planners informed/involved in the conversation eg . Urban planners re: zoning issues, trends in farming

• ED and planning have good communication

• Feel that Wellington OP provides good flexibility, always willing to speak to ppl

• Increase student wage grant amount for farms this will enable farms to employ more students

• GFZ training – employee and employer training

• Fund a labour pool website for FARMS and agriculture related business ** Exists through OFVGA

• Closer relationships between producers and academic institutions and supply chain to explore ideas and initiatives

30 Agriculture Research Project - December 2015

Actions and Next Step Ideas

#1 Central Registry

• Cultural aspect mentioned= Mennonites (land sale registry)

• One size does not fit all

#2 Take over land

• Working with farmers for incubator land/mentors (FarmStart) expanding this into WW

• Improve communication between municipal/regional decision-makers and ag business owners/operators

#3 Research

• Field trips to successful businesses

• Need better employment data in rural Ontario

#4 Zoning

• Must include decision makers and ensure policies are reasonable for the Ag

• Farmland and value-added expansion and development to support production profitability (land use)

• By-law enforcement and planning need to be educated on value of ag sector

• Improve communication between municipal/regional decision-makers and ag business owners/operators

#5 Ag Stakeholders

• Celebrate successes and positives of the two regions

• Continue info sharing as ag network for Waterloo-Wellington

• Ag food summit – best practices, what’s going on across sector

• Ag jobs forum

• Success stories

• Youth in agriculture

• Create a website for farmers and agri-business owners who have jobs to fill AND for skilled people who are actually interested in working in agriculture and ag-related business

• Support current initiatives and opportunities (cross-regional) ie . Upcoming Source it Here B2B event, Taste Real, Foodlink

• Improve communication between municipal/regional decision-makers and ag business owners/operators

• Collaboration is needed beyond the ag sector – ag stakeholders need to be aware of other sectors just as they need to be aware of ag

• Education is key to demonstrating value across stakeholder groups

#6 New initiatives

• Expand definition of agricultural activities

• Debunking myths about what “agriculture” is!

• Ag network summit – time to address issues/opportunities

• Mentor/succession program

• Stress the importance of connecting with new farmers

• Incubating deals more with people – use existing farms (?) (new ones) to house interns and help them start off in farming

Other Actions/Next Steps

• Protect our farmland

• Reinforcing networks of farmers to provide effective advice to farmers (new ones especially)

• Education in the school system

• Career options in livestock/crop/tech

• A balanced approach to conventional vs organic with the economic and philosophical aspects

• Need to address aging workforce as a factor in the workforce shortage

• Ag is a business, let it be a business

• 50% of citizens are “new” . Fastest growth indigenous youth . Are they at the table?

• Who gets to choose who “comes to the table”?

• Are all at the table equal?

• What is the real issue that necessitates these meetings?

Agriculture Research Project - December 2015 31

Christopher Bryant

Jana Burns, County of Wellington

Ted Clark

Danielle Collins, Ontario Federation of Agriculture

Elaine Corbett, Ontario Genomics

Laurel Davies Snyder, Township of Woolwich

Harold Devries, Guelph-Wellington Business Enterprise Centre

Mike Driscoll, Harvest Hop and Malt

Crystal Ellis, Township of Mapleton

Ron Gaudet, Region of Waterloo

Janet Harrop

Catherine Heal, Region of Waterloo

Gerry Horst, Ministry of Agriculture, Food and Rural Affairs

Tim Horton, Horst Systems

Mandy Jones, County of Wellington

Barbara Maly, City of Guelph

Christina Mann, Taste Real

Chuck Martin, Martin Mills

Don McKay, County of Wellington

Ron Miziolek, Waterloo Flowers

Tony Morris, P .Ag ., Meridian Credit Union

Robyn Mulder, Town of Erin

Mark Paoli, County of Wellington

Jennifer Pfennings, Pfennings Organics

Justin Pfennings, Pfennings Organics

Ian Roger, Guelph/Eramosa Township

Patricia Rutter, Township of Centre Wellington

Taylor Selig, Ontario Agri-Food Education

Sandy Shantz, Township of Woolwich

Lindsay Stallman, Ontario Agricultural College, University of Guelph

David Stubbs, Region of Waterloo

Carol Tyler, REAPOntario

Joe Varamo, Ontario Agricultural College, University of Guelph

Jeremy Vink, Township of Woolwich

Paul Walker

Deborah Whale

Chris White, Guelph/Eramosa Township

Belinda Wick-Graham, Town of Minto

Scott Wilson

Lori Woodham, Township of Mapleton

Appendix E – CONSULTATION PARTICIPANT LIST (December 2, 2015)

218 Boida Ave, Unit 5 Ayr, Ontario N0B 1E0 www.workforceplanningboard.com

![Workers’ Compensation Training for Supervisors [Presenter’s Name] 2008](https://img.pdfslide.net/doc/110x75/56649d9c5503460f94a84e53/workers-compensation-training-for-supervisors-presenters-name-2008.jpg)