Embed Size (px)

DESCRIPTION

AGSA SCoAG 2009. Annual report presentation October 2009. Mission. - PowerPoint PPT Presentation

Citation preview

Page 1

AGSA SCoAG 2009

Annual report presentation

October 2009

2

Mission

The Auditor-General of South Africa has a constitutional mandate and, as the Supreme Audit Institution (SAI) of South

Africa, it exists to strengthen our country’s democracy by enabling oversight, accountability and governance in the public

sector through auditing, thereby building public confidence.

This is our reputation promise.

3

Table of contents

Overview

Key highlights

Simplicity

Visibility of leadership

Strengthen human resources

Funding

Lead by Example

Conclusion

4

Overview of AG Commitment

The AGSA remains committed to the following goals in order to impact positively on all aspects of public sector accountability:

– ensuring simplicity, clarity and relevance of the messages contained in all our reports, including the quality, timeliness and deepening of stakeholders’ understanding of our reports

– improving the visibility of our leadership through clear communication in championing the implementation of audit recommendations

– strengthening the human resource strategy with particular emphasis on the comprehensive trainee auditor scheme

– focusing on the funding model with a view to stabilising our margins and cash flow situation

– leading by example on matters of risk management, internal controls and transformation

5

• Communication of audit report outcomes to key stakeholder through road shows

• Annual quality results of category “excellent” exceeded and surpassed that of prior years

• 50% improvement in the timely submission of annual financial statements for PFMA organisations

• 36% improvement in the timely submission of annual financial statements for MFMA municipalities

• Completion of audit reports within the statutory deadlines

– PFMA organisations (99%)

– Other PFMA organisations (98%)

– MFMA organisations (92%)

• Significant decrease in vacancies of 35% from 2007 (724) to 2009 (471)

• Achievement of retention rate of 11% compared to industry average of 16%

• AGSA hosted the AFROSAI 11th General Assembly in Pretoria from 13 to 17 October 2008. It was attended by delegates and observers from 51 countries

Key Highlights

6

Simplicity and clarity of our reports

Key Achievements

• Continued our efforts to influence the achievement of unqualified reports in all spheres of government, which is central to the realisation of our constitutional mandate

• Communicated with simplicity, clarity and relevance to our stakeholders through road shows and door-to-door visits

• Continued focus on the quality and timeliness of our products including audit reports

• Streamlined performance auditing function

• Continued our contribution in international auditing to the United Nations Board of Auditors

• Tabled to Parliament 38 performance audits reports, 6 of national departments, 2 of public entities, 30 provincial departments.

7

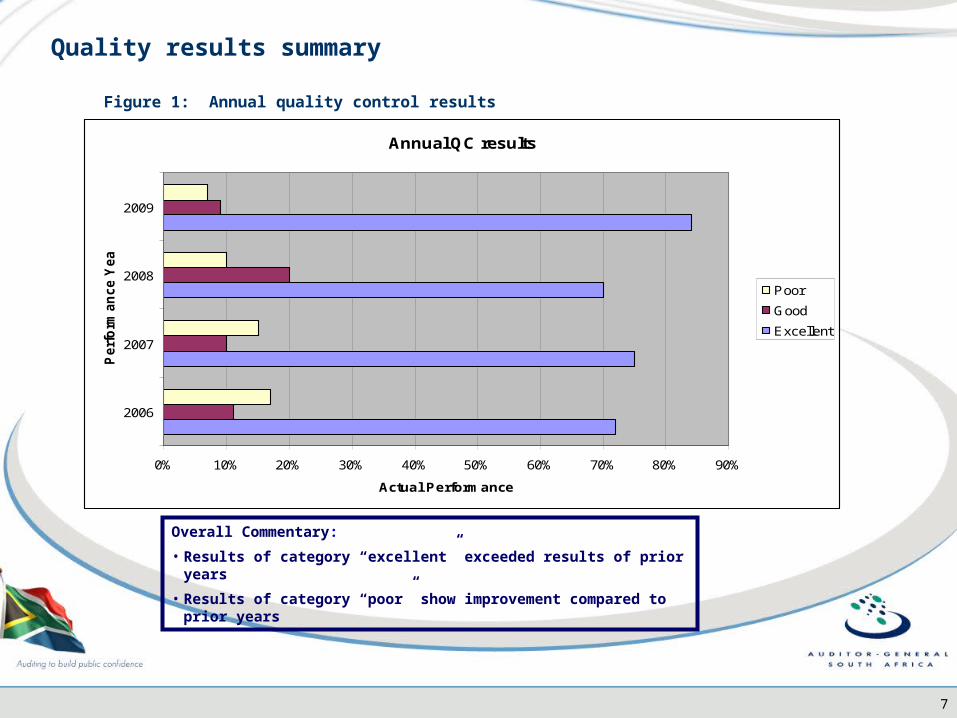

Figure 1: Annual quality control results

Annual QC results

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

2006

2007

2008

2009

Perf

orm

an

ce Y

ear

Actual Performance

Poor

Good

Excellent

Overall Commentary:

• Results of category “excellent” exceeded results of prior years

• Results of category “poor” show improvement compared to prior years

Quality results summary

8

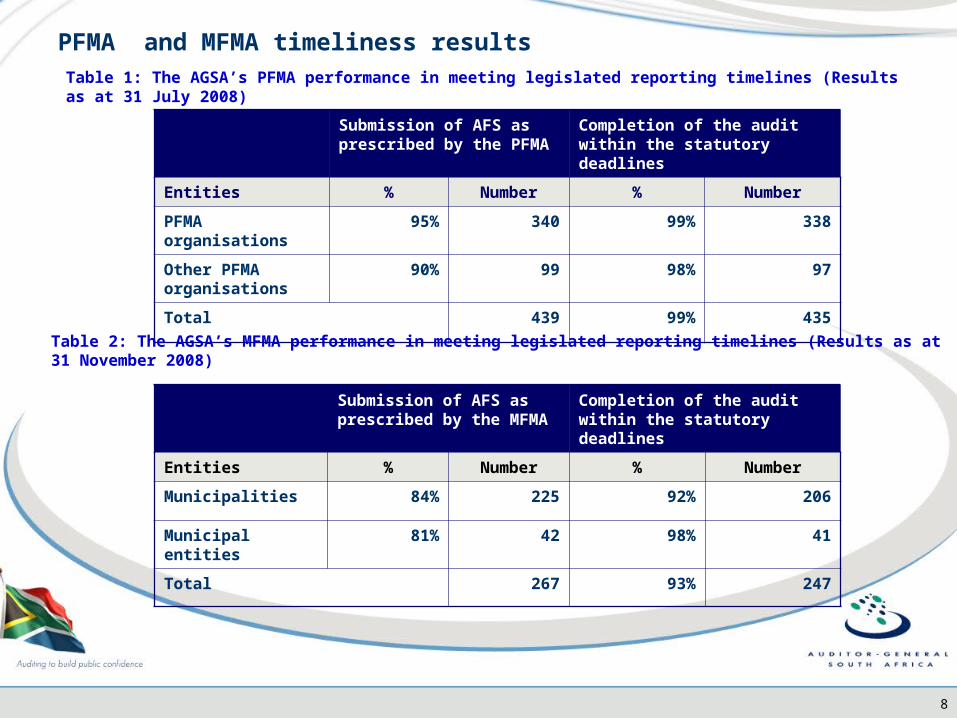

Submission of AFS as prescribed by the PFMA

Completion of the audit within the statutory deadlines

Entities % Number % Number

PFMA organisations 95% 340 99% 338

Other PFMA organisations

90% 99 98% 97

Total 439 99% 435

Table 1: The AGSA’s PFMA performance in meeting legislated reporting timelines (Results as at 31 July 2008)

PFMA and MFMA timeliness results

Submission of AFS as prescribed by the MFMA

Completion of the audit within the statutory deadlines

Entities % Number % Number

Municipalities 84% 225 92% 206

Municipal entities 81% 42 98% 41

Total 267 93% 247

Table 2: The AGSA’s MFMA performance in meeting legislated reporting timelines (Results as at 31 November 2008)

9

Simplicity and clarity of our reports

Key Challenges Initiatives

Insufficient capacity to do performance audits Regular reviews by the Performance Audit Advisory Committee

10

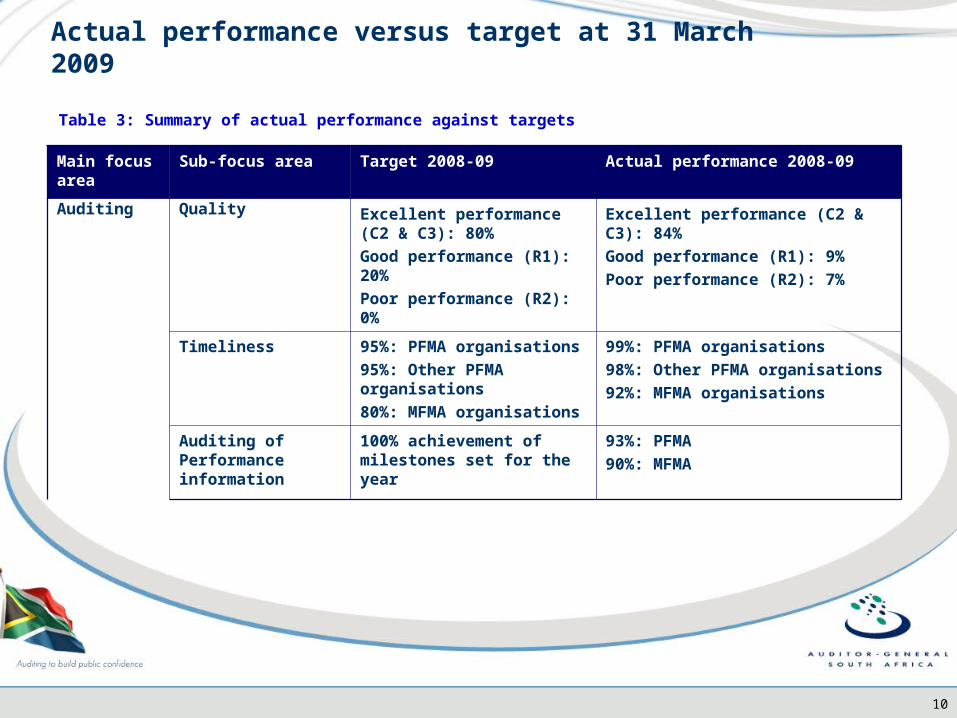

Main focus area

Sub-focus area Target 2008-09 Actual performance 2008-09

Auditing Quality Excellent performance (C2 & C3): 80%

Good performance (R1): 20%

Poor performance (R2): 0%

Excellent performance (C2 & C3): 84%

Good performance (R1): 9%

Poor performance (R2): 7%

Timeliness 95%: PFMA organisations

95%: Other PFMA organisations

80%: MFMA organisations

99%: PFMA organisations

98%: Other PFMA organisations

92%: MFMA organisations

Auditing of Performance information

100% achievement of milestones set for the year

93%: PFMA

90%: MFMA

Table 3: Summary of actual performance against targets

Actual performance versus target at 31 March 2009

11

Key achievements

• Engaged the media on the audit process so that they can appropriately communicate audit outcomes

• Reviewed our vision, mission and values so as to drive a performance-driven culture

• Trained and empowered our leadership to better understand their leadership communication role

• Signed a Memorandum of Understanding (MoU) with the Public Protector and the Office of the Public Service Commission.

• Auditor-General was appointed as the first vice-chair of INTOSAI and continued as President of AFROSAI

• AFROSAI held its 11th General Assembly in Pretoria, South Africa from 13 to 17 October 2008. The assembly was hosted by the AGSA and was attended by delegates and observers from 51 countries.

Visibility of Leadership

12

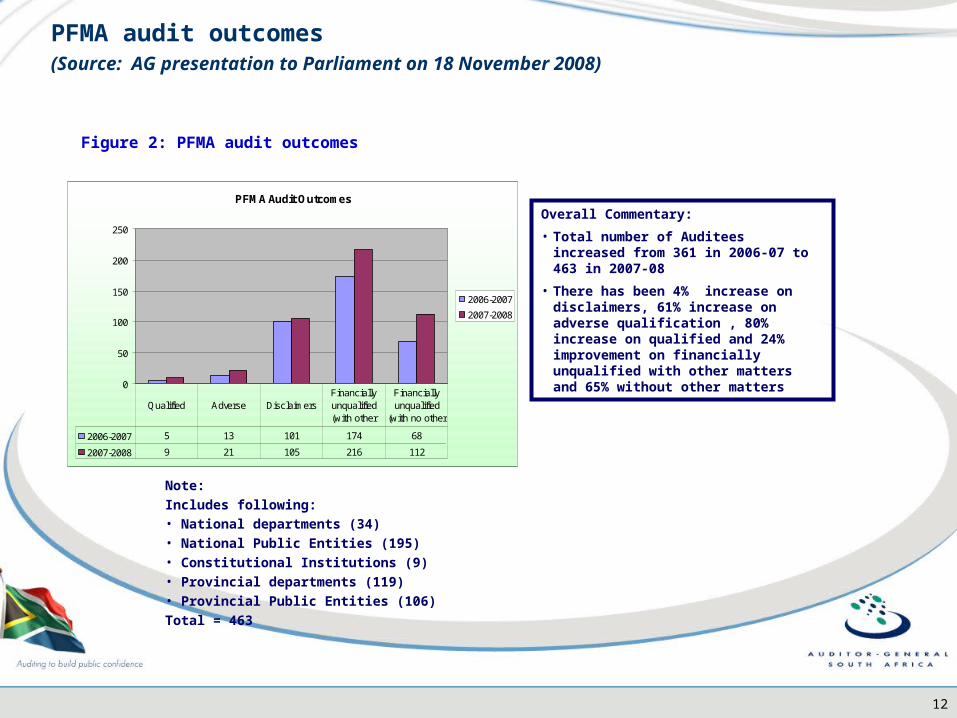

PFMA audit outcomes (Source: AG presentation to Parliament on 18 November 2008)

Overall Commentary:

• Total number of Auditees increased from 361 in 2006-07 to 463 in 2007-08

• There has been 4% increase on disclaimers, 61% increase on adverse qualification , 80% increase on qualified and 24% improvement on financially unqualified with other matters and 65% without other matters

Figure 2: PFMA audit outcomes

PFMA Audit Outcomes

0

50

100

150

200

250

2006-2007

2007-2008

2006-2007 5 13 101 174 68

2007-2008 9 21 105 216 112

Qualified Adverse DisclaimersFinancially unqualified (with other

Financially unqualified

(with no other

Note:

Includes following:• National departments (34)• National Public Entities (195)• Constitutional Institutions (9)• Provincial departments (119)• Provincial Public Entities (106)

Total = 463

13

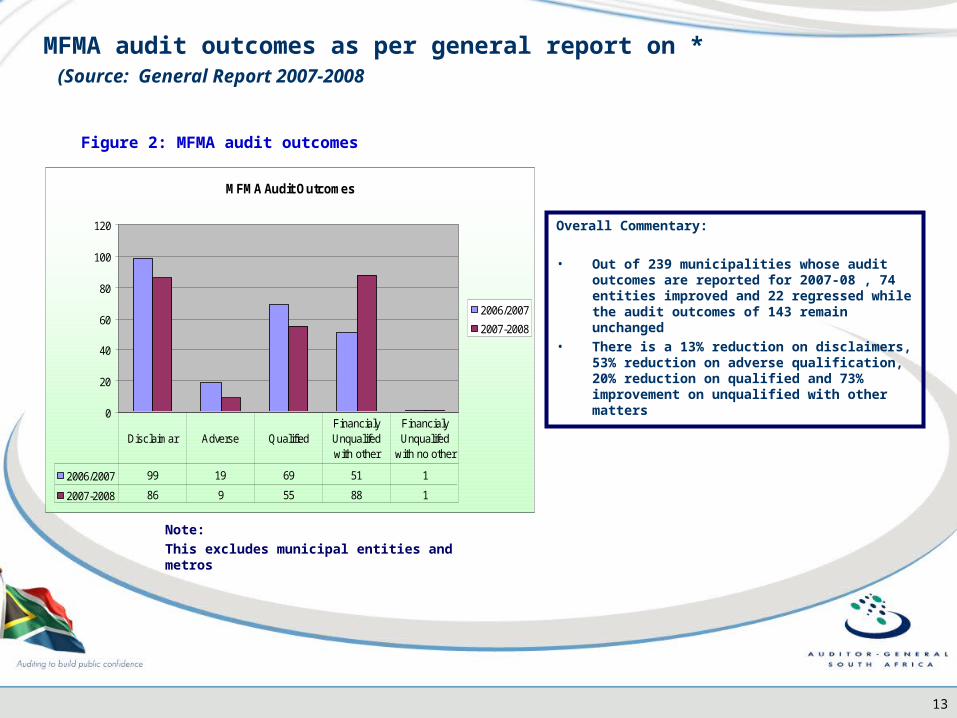

MFMA audit outcomes as per general report on * (Source: General Report 2007-2008

Figure 2: MFMA audit outcomes

MFMA Audit Outcomes

0

20

40

60

80

100

120

2006/2007

2007-2008

2006/2007 99 19 69 51 1

2007-2008 86 9 55 88 1

Disclaimar Adverse QualifiedFinancialy Unqualifed with other

Financialy Unqualifed

with no other

Overall Commentary:

• Out of 239 municipalities whose audit outcomes are reported for 2007-08 , 74 entities improved and 22 regressed while the audit outcomes of 143 remain unchanged

• There is a 13% reduction on disclaimers, 53% reduction on adverse qualification, 20% reduction on qualified and 73% improvement on unqualified with other matters

Note:

This excludes municipal entities and metros

14

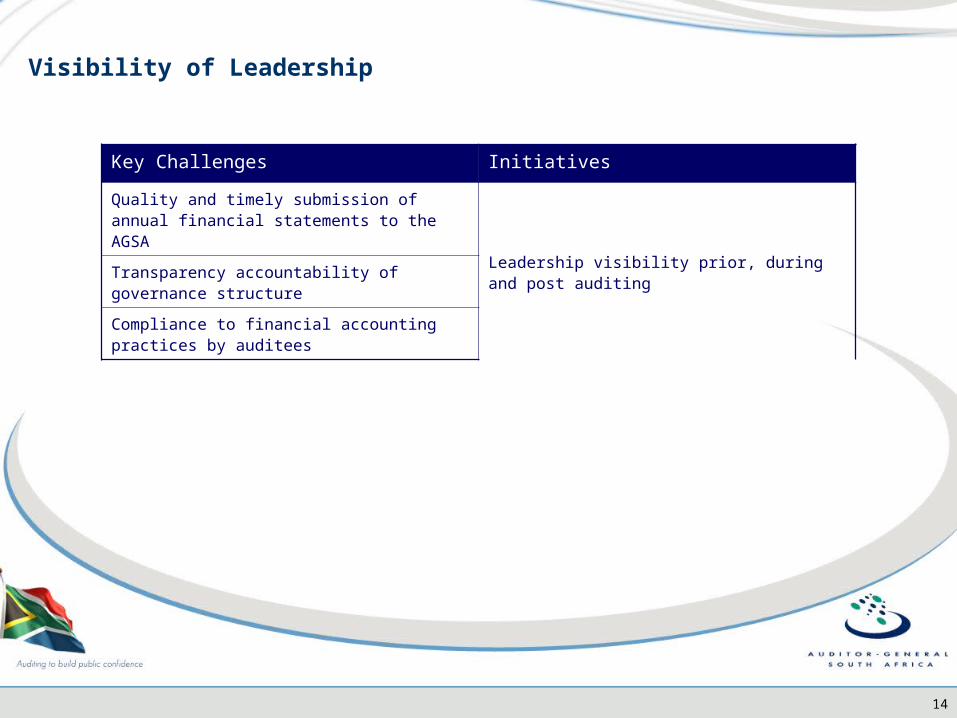

Visibility of Leadership

Key Challenges Initiatives

Quality and timely submission of annual financial statements to the AGSA

Leadership visibility prior, during and post auditingTransparency accountability of governance structure

Compliance to financial accounting practices by auditees

15

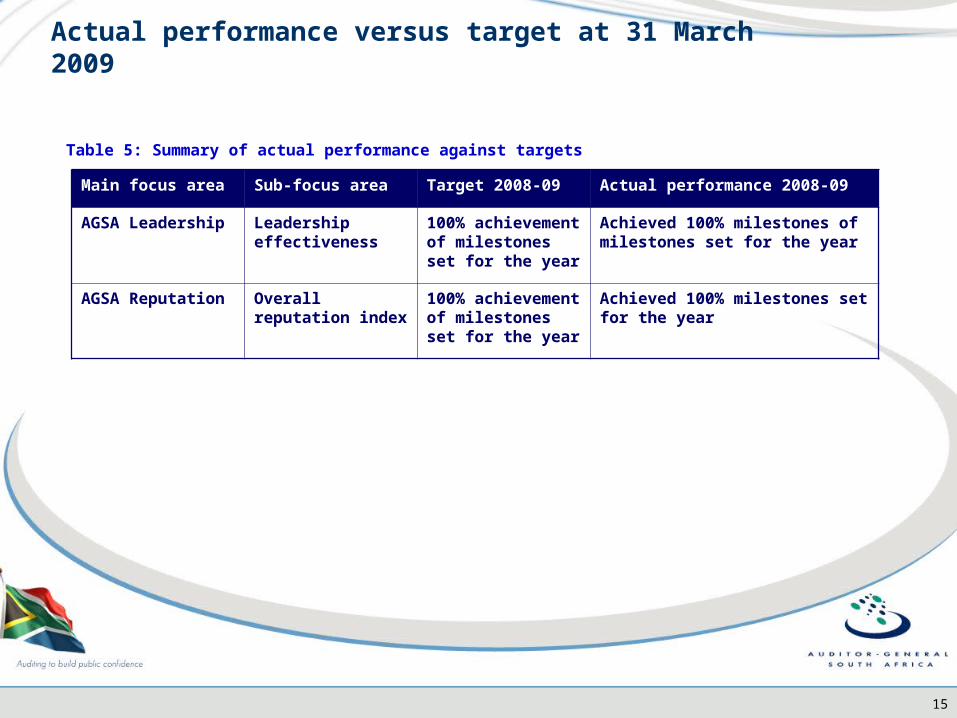

Main focus area Sub-focus area Target 2008-09 Actual performance 2008-09

AGSA Leadership Leadership effectiveness

100% achievement of milestones set for the year

Achieved 100% milestones of milestones set for the year

AGSA Reputation Overall reputation index

100% achievement of milestones set for the year

Achieved 100% milestones set for the year

Table 5: Summary of actual performance against targets

Actual performance versus target at 31 March 2009

16

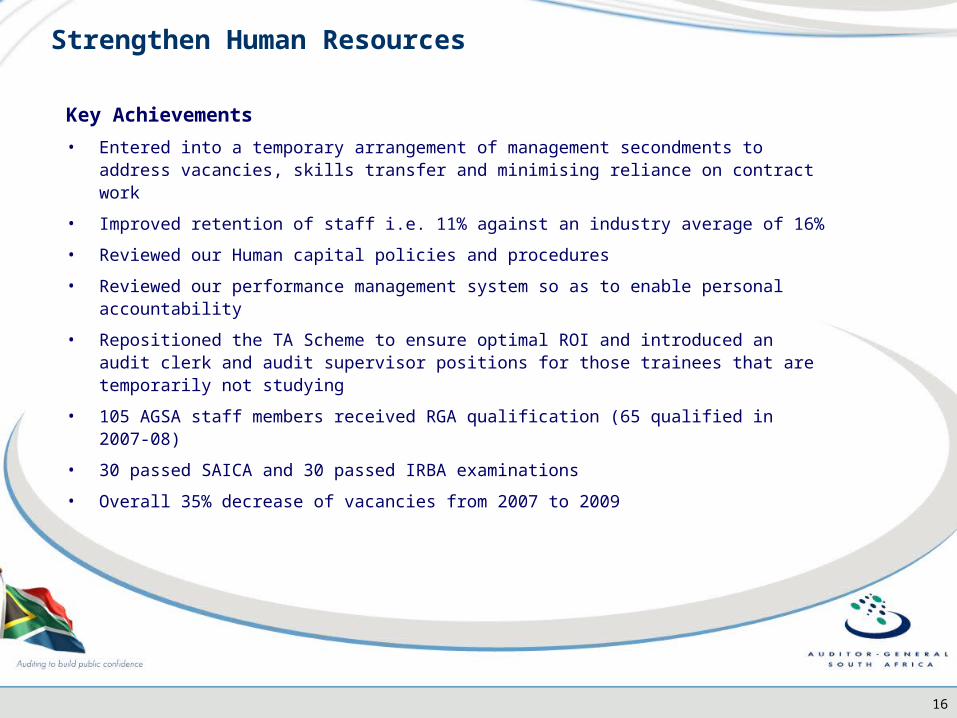

Key Achievements

• Entered into a temporary arrangement of management secondments to address vacancies, skills transfer and minimising reliance on contract work

• Improved retention of staff i.e. 11% against an industry average of 16%

• Reviewed our Human capital policies and procedures

• Reviewed our performance management system so as to enable personal accountability

• Repositioned the TA Scheme to ensure optimal ROI and introduced an audit clerk and audit supervisor positions for those trainees that are temporarily not studying

• 105 AGSA staff members received RGA qualification (65 qualified in 2007-08)

• 30 passed SAICA and 30 passed IRBA examinations

• Overall 35% decrease of vacancies from 2007 to 2009

Strengthen Human Resources

17

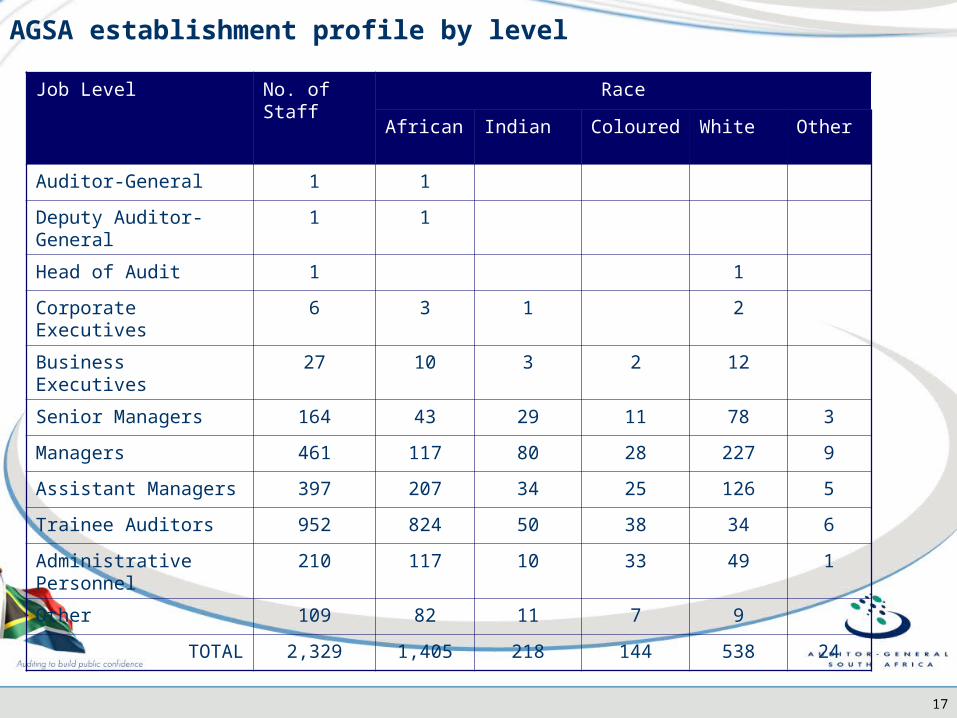

AGSA establishment profile by level

Job Level No. of Staff Race

African Indian Coloured White Other

Auditor-General 1 1

Deputy Auditor-General 1 1

Head of Audit 1 1

Corporate Executives 6 3 1 2

Business Executives 27 10 3 2 12

Senior Managers 164 43 29 11 78 3

Managers 461 117 80 28 227 9

Assistant Managers 397 207 34 25 126 5

Trainee Auditors 952 824 50 38 34 6

Administrative Personnel 210 117 10 33 49 1

Other 109 82 11 7 9

TOTAL 2,329 1,405 218 144 538 24

18

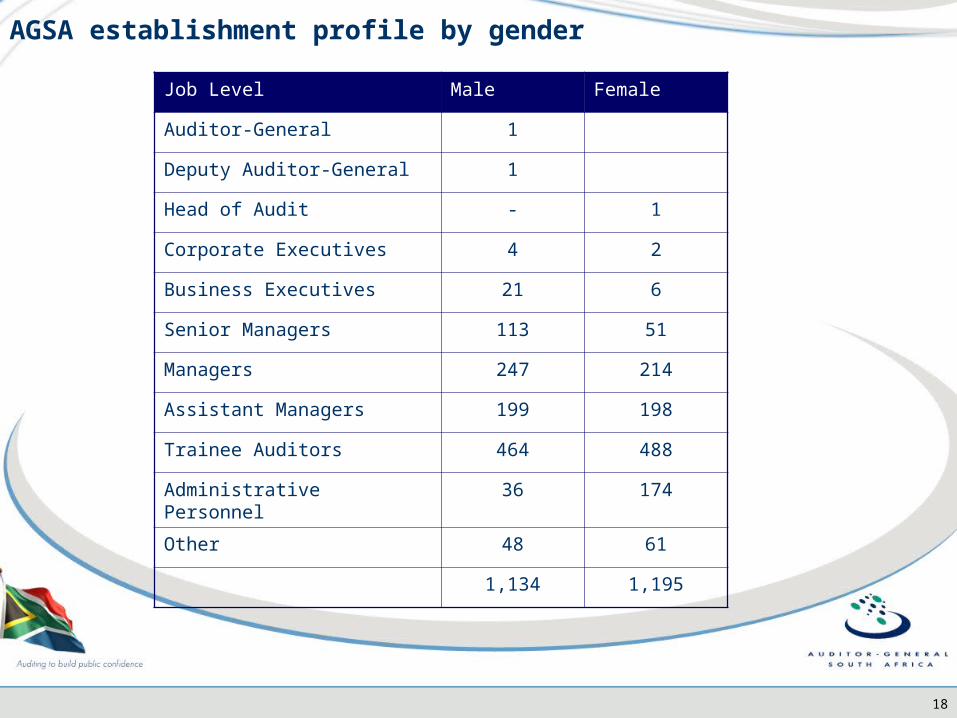

Job Level Male Female

Auditor-General 1

Deputy Auditor-General 1

Head of Audit - 1

Corporate Executives 4 2

Business Executives 21 6

Senior Managers 113 51

Managers 247 214

Assistant Managers 199 198

Trainee Auditors 464 488

Administrative Personnel 36 174

Other 48 61

1,134 1,195

AGSA establishment profile by gender

19

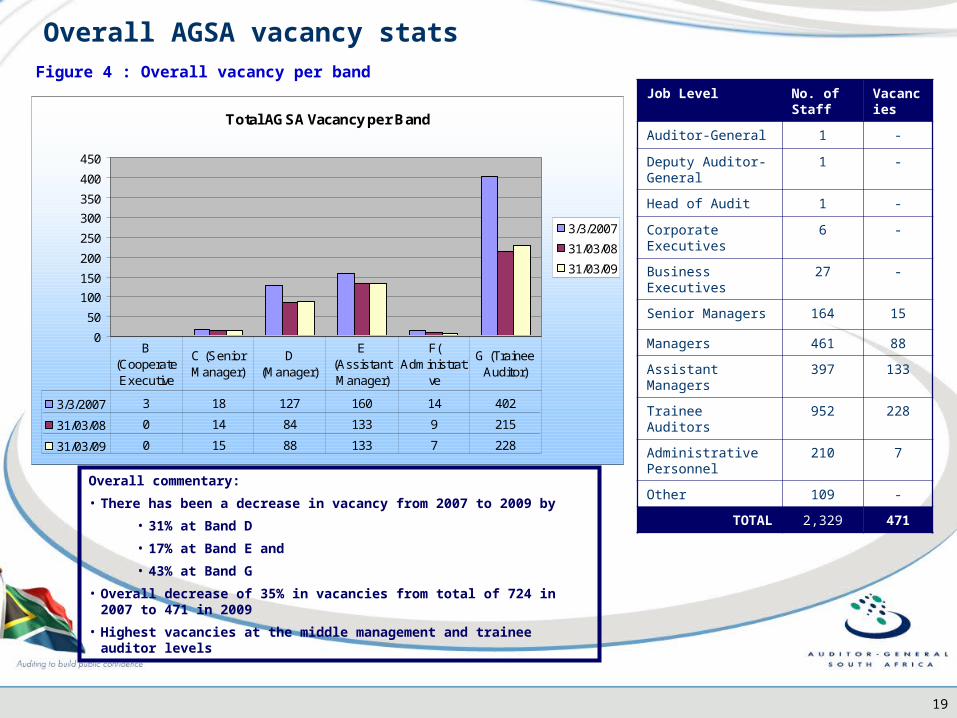

Overall commentary:

• There has been a decrease in vacancy from 2007 to 2009 by

• 31% at Band D

• 17% at Band E and

• 43% at Band G

• Overall decrease of 35% in vacancies from total of 724 in 2007 to 471 in 2009

• Highest vacancies at the middle management and trainee auditor levels

Figure 4 : Overall vacancy per band

Overall AGSA vacancy stats

Total AGSA Vacancy per Band

0

50

100

150

200

250

300

350

400

450

3/3/2007

31/03/08

31/03/09

3/3/2007 3 18 127 160 14 402

31/03/08 0 14 84 133 9 215

31/03/09 0 15 88 133 7 228

B (Cooperate Executive

C (Senior Manager)

D (Manager)

E (Assistant Manager)

F( Administrati

ve

G (Trainee Auditor)

Job Level No. of Staff

Vacancies

Auditor-General 1 -

Deputy Auditor-General

1 -

Head of Audit 1 -

Corporate Executives

6 -

Business Executives 27 -

Senior Managers 164 15

Managers 461 88

Assistant Managers 397 133

Trainee Auditors 952 228

Administrative Personnel

210 7

Other 109 -

TOTAL 2,329 471

20

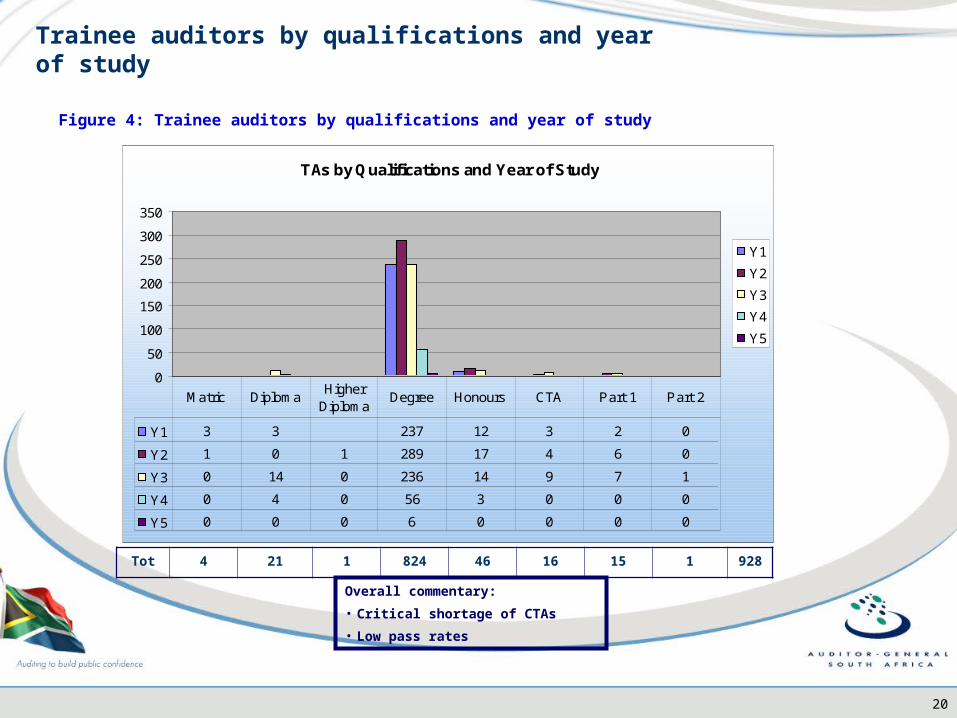

Trainee auditors by qualifications and year of study

Figure 4: Trainee auditors by qualifications and year of study

Tot 4 21 1 824 46 16 15 1 928

TAs by Qualifications and Year of Study

0

50

100

150

200

250

300

350

Y1

Y2

Y3

Y4

Y5

Y1 3 3 237 12 3 2 0

Y2 1 0 1 289 17 4 6 0

Y3 0 14 0 236 14 9 7 1

Y4 0 4 0 56 3 0 0 0

Y5 0 0 0 6 0 0 0 0

Matric DiplomaHigher

DiplomaDegree Honours CTA Part 1 Part 2

Overall commentary:

• Critical shortage of CTAs

• Low pass rates

21

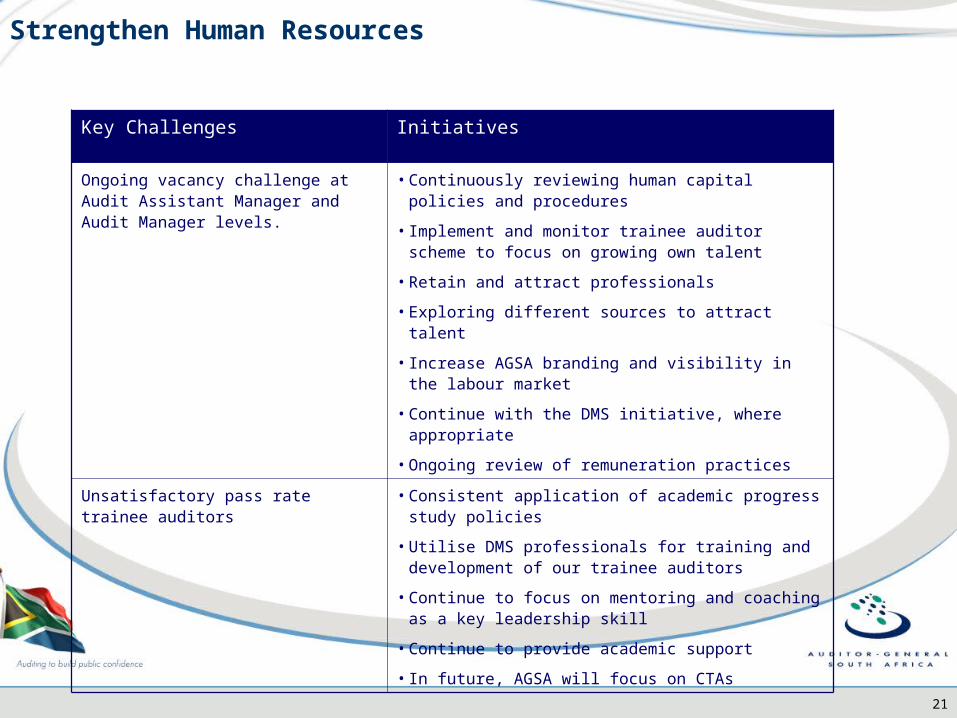

Strengthen Human Resources

Key Challenges Initiatives

Ongoing vacancy challenge at Audit Assistant Manager and Audit Manager levels.

• Continuously reviewing human capital policies and procedures

• Implement and monitor trainee auditor scheme to focus on growing own talent

• Retain and attract professionals

• Exploring different sources to attract talent

• Increase AGSA branding and visibility in the labour market

• Continue with the DMS initiative, where appropriate

• Ongoing review of remuneration practices

Unsatisfactory pass rate trainee auditors • Consistent application of academic progress study policies

• Utilise DMS professionals for training and development of our trainee auditors

• Continue to focus on mentoring and coaching as a key leadership skill

• Continue to provide academic support

• In future, AGSA will focus on CTAs

22

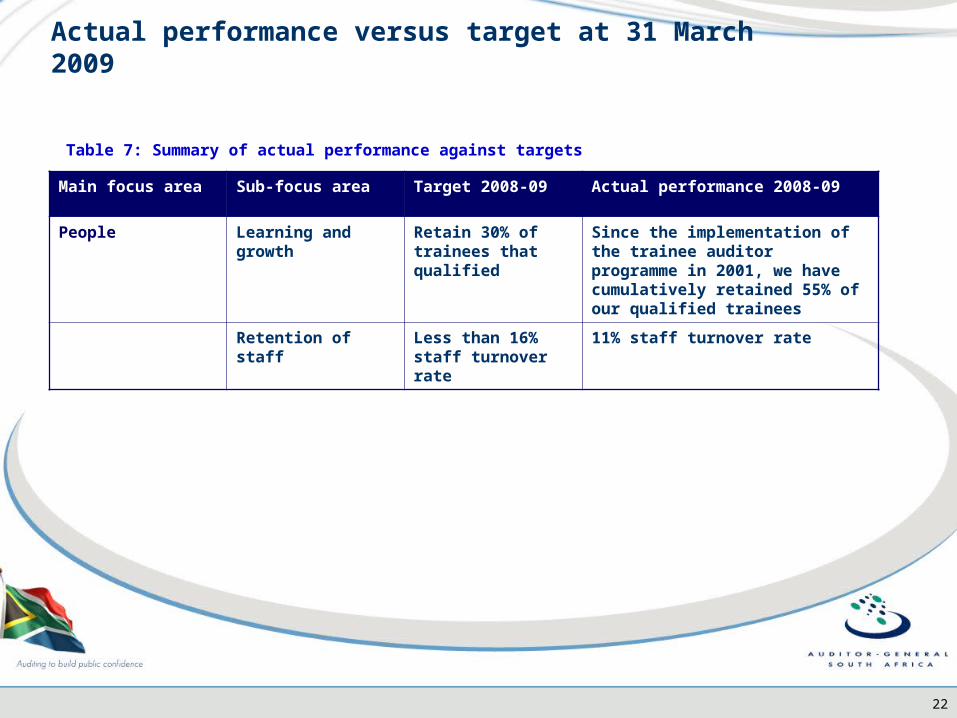

Main focus area Sub-focus area Target 2008-09 Actual performance 2008-09

People Learning and growth Retain 30% of trainees that qualified

Since the implementation of the trainee auditor programme in 2001, we have cumulatively retained 55% of our qualified trainees

Retention of staff Less than 16% staff turnover rate

11% staff turnover rate

Table 7: Summary of actual performance against targets

Actual performance versus target at 31 March 2009

23

Key achievements

• Completed financial turnaround plan

• Amended AGSA funding model

Funding

24

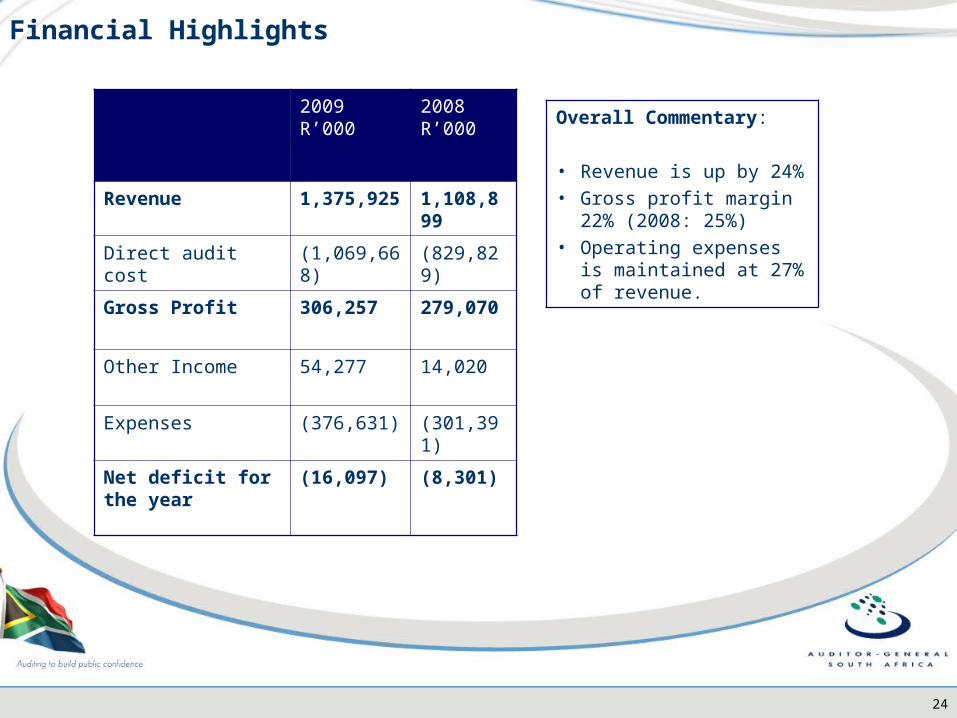

Financial Highlights

2009 R’000

2008 R’000

Revenue 1,375,925 1,108,899

Direct audit cost (1,069,668) (829,829)

Gross Profit 306,257 279,070

Other Income 54,277 14,020

Expenses (376,631) (301,391)

Net deficit for the year

(16,097) (8,301)

Overall Commentary:

• Revenue is up by 24%• Gross profit margin 22%

(2008: 25%)• Operating expenses is

maintained at 27% of revenue.

25

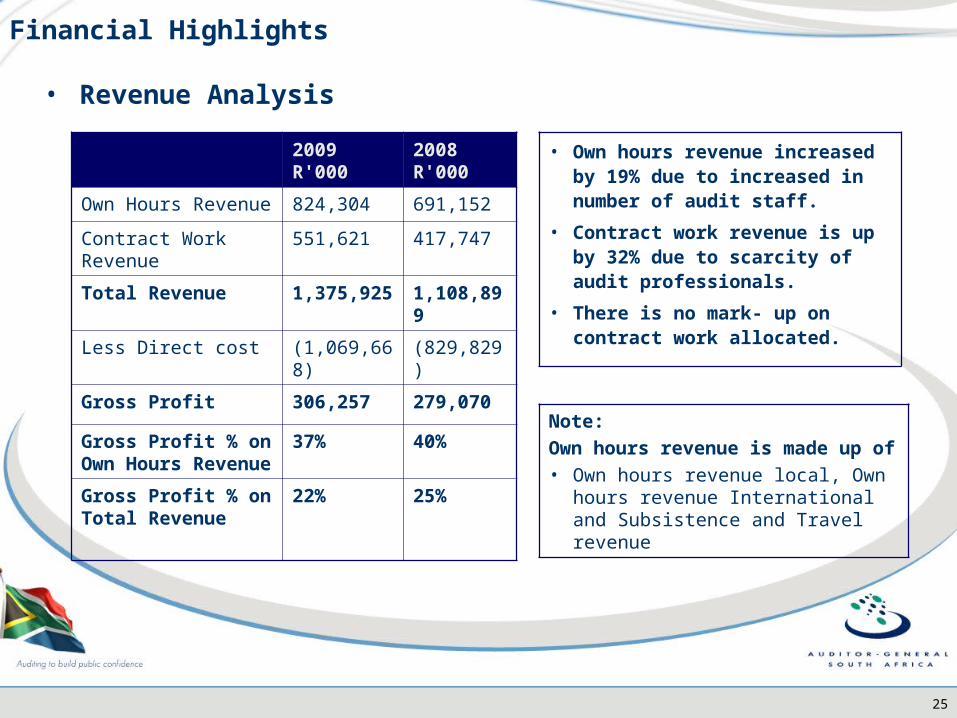

Financial Highlights

• Revenue Analysis

2009 R'000

2008 R'000

Own Hours Revenue 824,304 691,152

Contract Work Revenue

551,621 417,747

Total Revenue 1,375,925 1,108,899

Less Direct cost (1,069,668) (829,829)

Gross Profit 306,257 279,070

Gross Profit % on Own Hours Revenue

37% 40%

Gross Profit % on Total Revenue

22% 25%

• Own hours revenue increased by 19% due to increased in number of audit staff.

• Contract work revenue is up by 32% due to scarcity of audit professionals.

• There is no mark- up on contract work allocated.

Note:

Own hours revenue is made up of • Own hours revenue local, Own hours

revenue International and Subsistence and Travel revenue

26

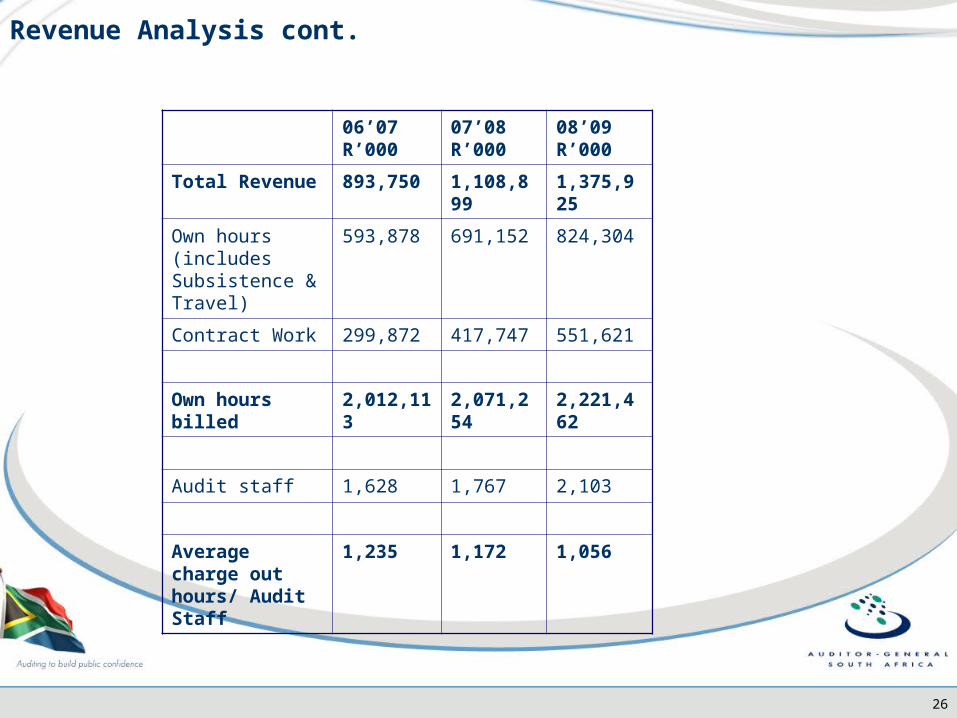

Revenue Analysis cont.

06’07 R’000

07’08 R’000

08’09 R’000

Total Revenue 893,750 1,108,899 1,375,925

Own hours (includes Subsistence & Travel)

593,878 691,152 824,304

Contract Work 299,872 417,747 551,621

Own hours billed 2,012,113 2,071,254 2,221,462

Audit staff 1,628 1,767 2,103

Average charge out hours/ Audit Staff

1,235 1,172 1,056

27

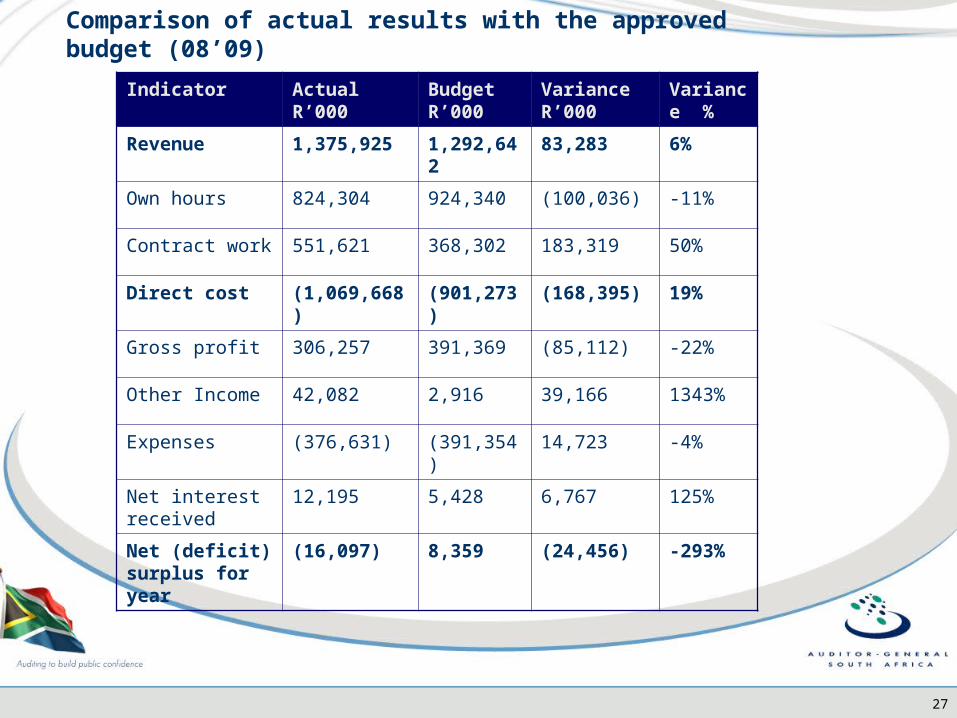

Comparison of actual results with the approved budget (08’09)

Indicator Actual R’000

Budget R’000

Variance R’000

Variance %

Revenue 1,375,925 1,292,642 83,283 6%

Own hours 824,304 924,340 (100,036) -11%

Contract work 551,621 368,302 183,319 50%

Direct cost (1,069,668) (901,273) (168,395) 19%

Gross profit 306,257 391,369 (85,112) -22%

Other Income 42,082 2,916 39,166 1343%

Expenses (376,631) (391,354) 14,723 -4%

Net interest received

12,195 5,428 6,767 125%

Net (deficit) surplus for year

(16,097) 8,359 (24,456) -293%

28

Comparison of actual results with the approved budget (08’09) cont.

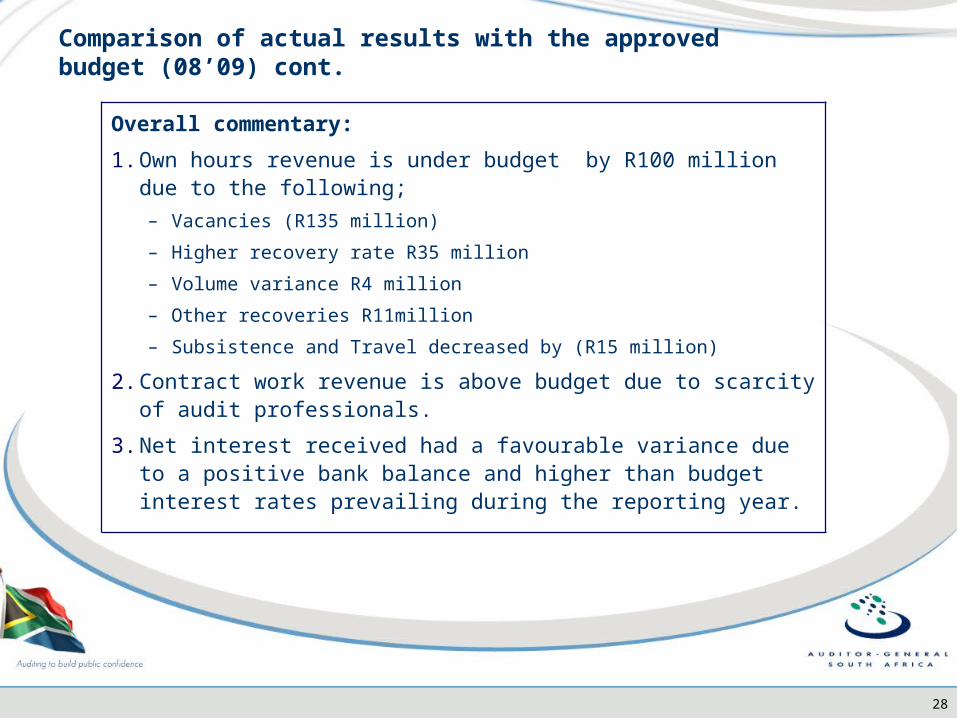

Overall commentary:

1. Own hours revenue is under budget by R100 million due to the following;

– Vacancies (R135 million)

– Higher recovery rate R35 million

– Volume variance R4 million

– Other recoveries R11million

– Subsistence and Travel decreased by (R15 million)

2. Contract work revenue is above budget due to scarcity of audit professionals.

3. Net interest received had a favourable variance due to a positive bank balance and higher than budget interest rates prevailing during the reporting year.

29

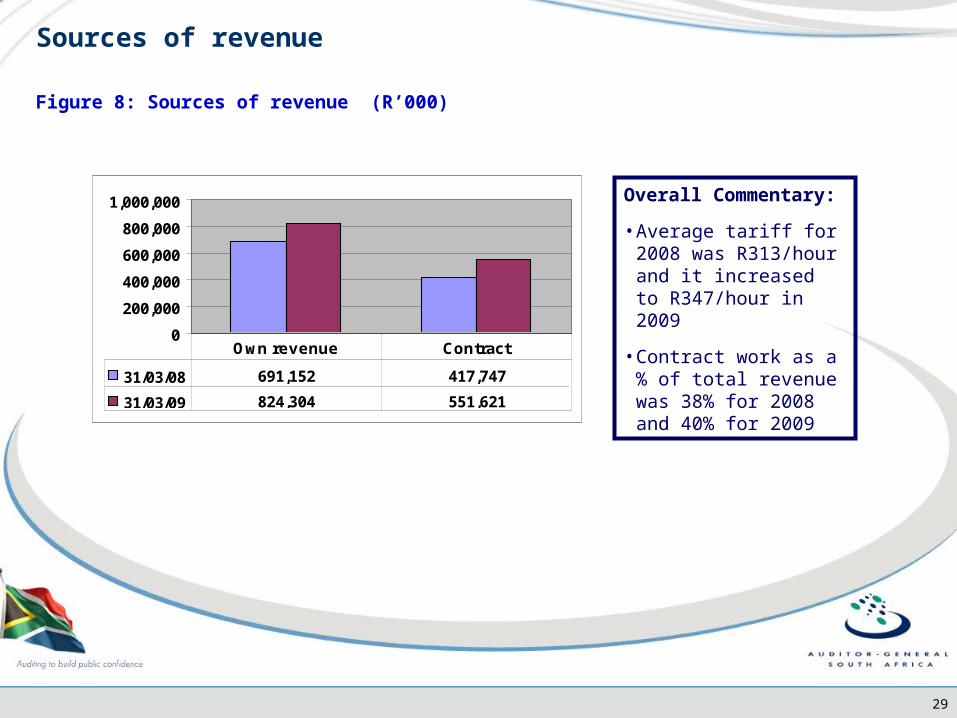

Figure 8: Sources of revenue (R’000)

Sources of revenue

0

200,000

400,000

600,000

800,000

1,000,000

31/03/08 691,152 417,747

31/03/09 824,304 551,621

Own revenue Contract

Overall Commentary:

• Average tariff for 2008 was R313/hour and it increased to R347/hour in 2009

• Contract work as a % of total revenue was 38% for 2008 and 40% for 2009

30

Financial Highlights

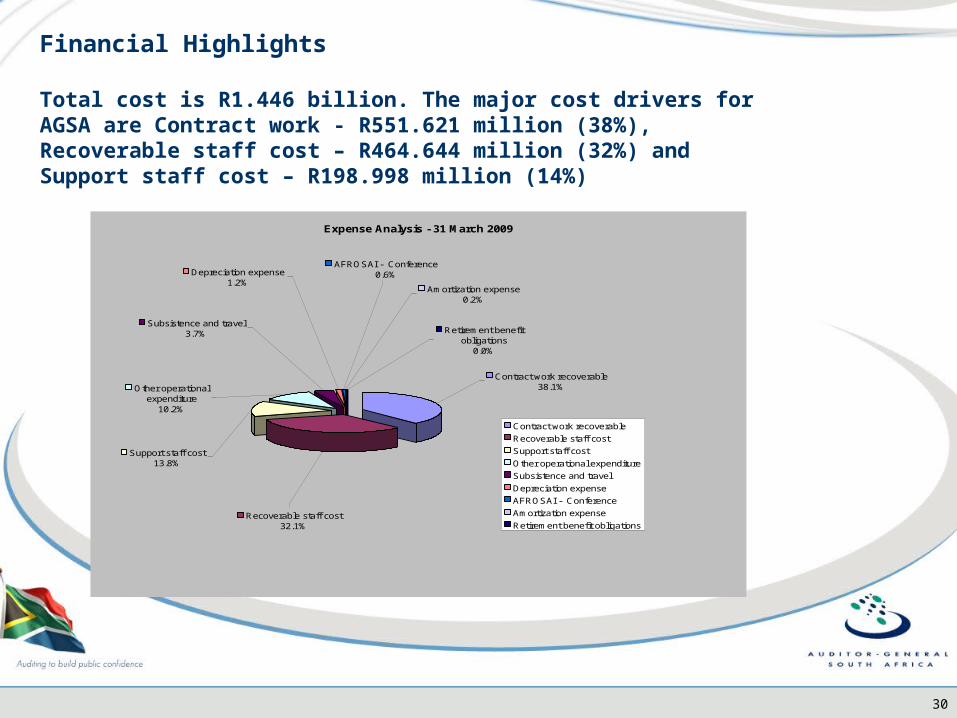

Total cost is R1.446 billion. The major cost drivers for AGSA are Contract work - R551.621 million (38%), Recoverable staff cost – R464.644 million (32%) and Support staff cost – R198.998 million (14%)

Expense Analysis - 31 March 2009

Contract work recoverable38.1%

Amortization expense0.2%

Retirement benefit obligations

0.0%

Other operational expenditure

10.2%

Subsistence and travel3.7%

AFROSAI - Conference0.6%Depreciation expense

1.2%

Support staff cost13.8%

Recoverable staff cost32.1%

Contract work recoverable

Recoverable staff cost

Support staff cost

Other operational expenditure

Subsistence and travel

Depreciation expense

AFROSAI - Conference

Amortization expense

Retirement benefit obligations

31

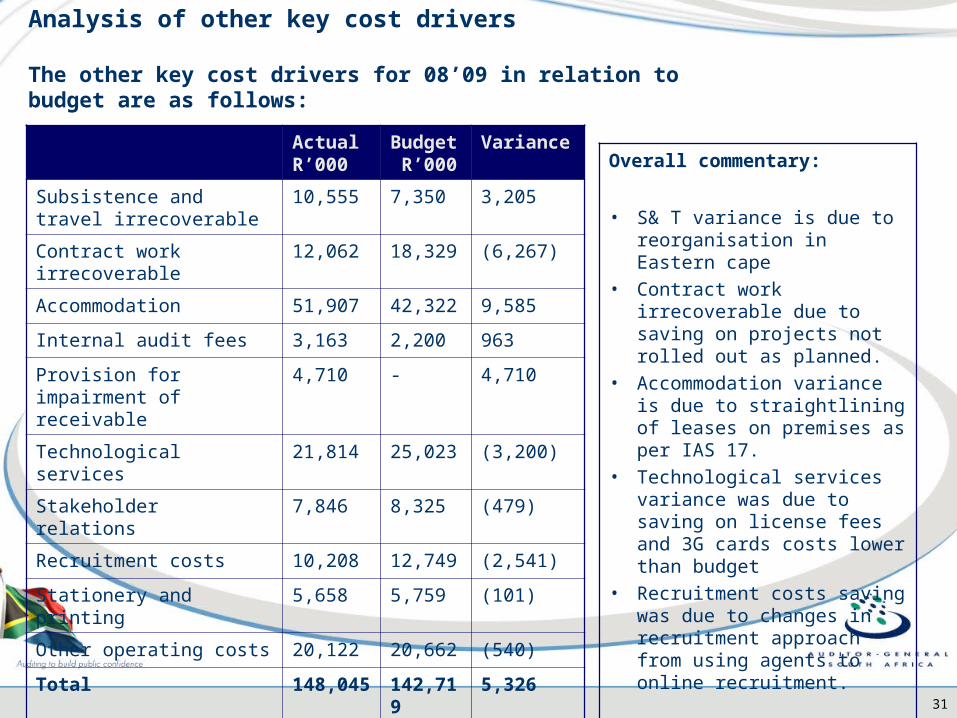

Analysis of other key cost drivers

The other key cost drivers for 08’09 in relation to budget are as follows:

Actual R’000

Budget R’000

Variance

Subsistence and travel irrecoverable

10,555 7,350 3,205

Contract work irrecoverable 12,062 18,329 (6,267)

Accommodation 51,907 42,322 9,585

Internal audit fees 3,163 2,200 963

Provision for impairment of receivable

4,710 - 4,710

Technological services 21,814 25,023 (3,200)

Stakeholder relations 7,846 8,325 (479)

Recruitment costs 10,208 12,749 (2,541)

Stationery and printing 5,658 5,759 (101)

Other operating costs 20,122 20,662 (540)

Total 148,045 142,719 5,326

Overall commentary:

• S& T variance is due to reorganisation in Eastern cape

• Contract work irrecoverable due to saving on projects not rolled out as planned.

• Accommodation variance is due to straightlining of leases on premises as per IAS 17.

• Technological services variance was due to saving on license fees and 3G cards costs lower than budget

• Recruitment costs saving was due to changes in recruitment approach from using agents to online recruitment.

32

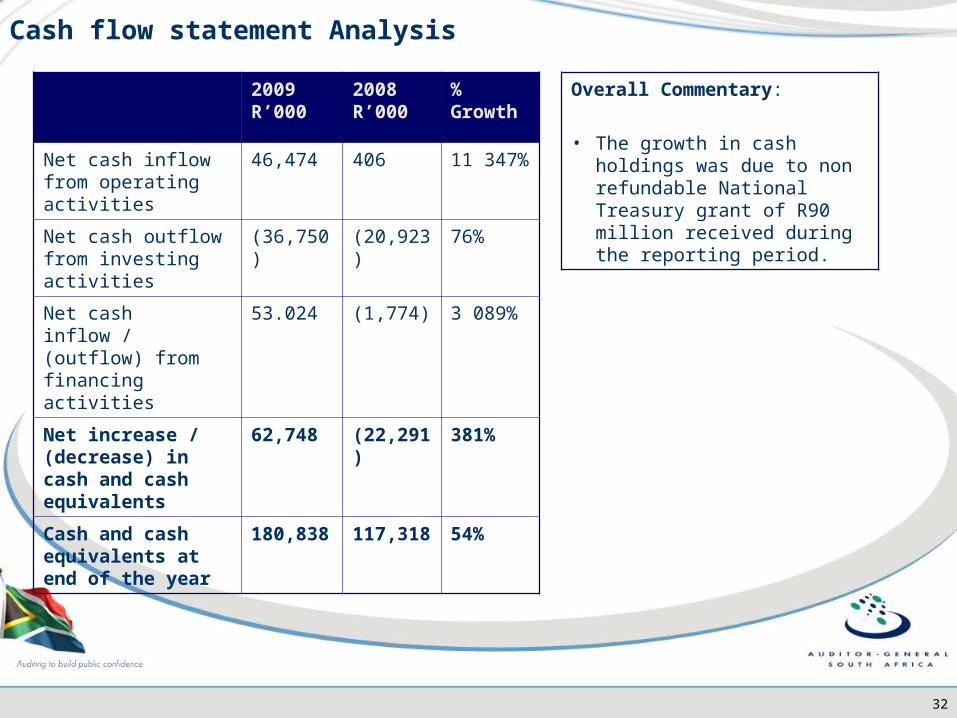

Cash flow statement Analysis

2009 R’000

2008 R’000

% Growth

Net cash inflow from operating activities

46,474 406 11 347%

Net cash outflow from investing activities

(36,750) (20,923) 76%

Net cash inflow / (outflow) from financing activities

53.024 (1,774) 3 089%

Net increase / (decrease) in cash and cash equivalents

62,748 (22,291) 381%

Cash and cash equivalents at end of the year

180,838 117,318 54%

Overall Commentary:

• The growth in cash holdings was due to non refundable National Treasury grant of R90 million received during the reporting period.

33

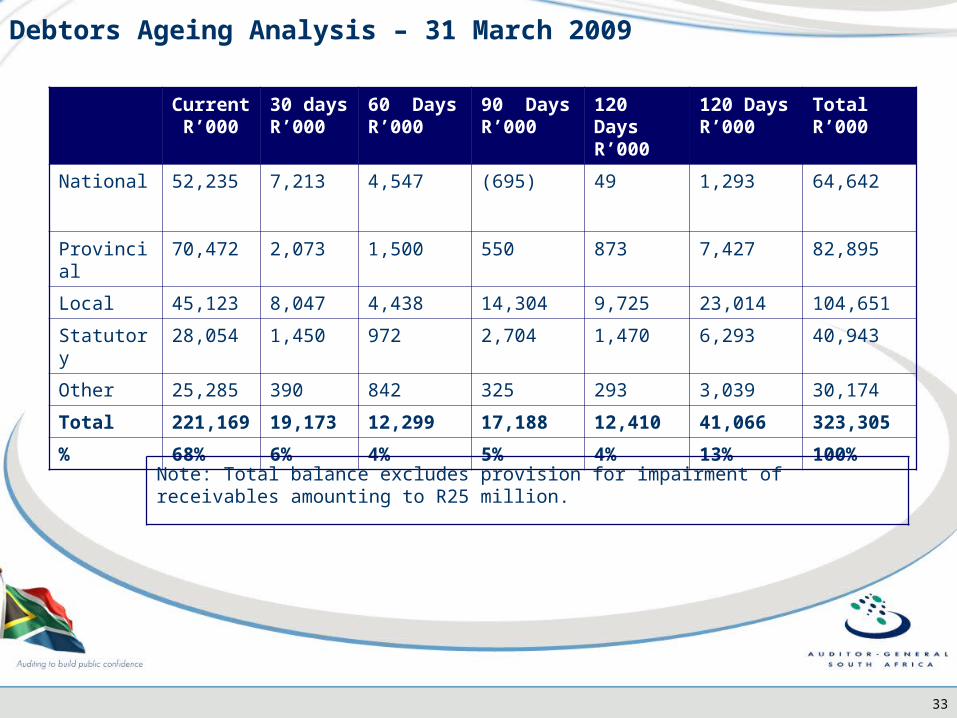

Debtors Ageing Analysis – 31 March 2009

Current R’000

30 days R’000

60 Days R’000

90 Days R’000

120 Days R’000

120 Days R’000

Total R’000

National 52,235 7,213 4,547 (695) 49 1,293 64,642

Provincial 70,472 2,073 1,500 550 873 7,427 82,895

Local 45,123 8,047 4,438 14,304 9,725 23,014 104,651

Statutory 28,054 1,450 972 2,704 1,470 6,293 40,943

Other 25,285 390 842 325 293 3,039 30,174

Total 221,169 19,173 12,299 17,188 12,410 41,066 323,305

% 68% 6% 4% 5% 4% 13% 100%

Note: Total balance excludes provision for impairment of receivables amounting to R25 million.

34

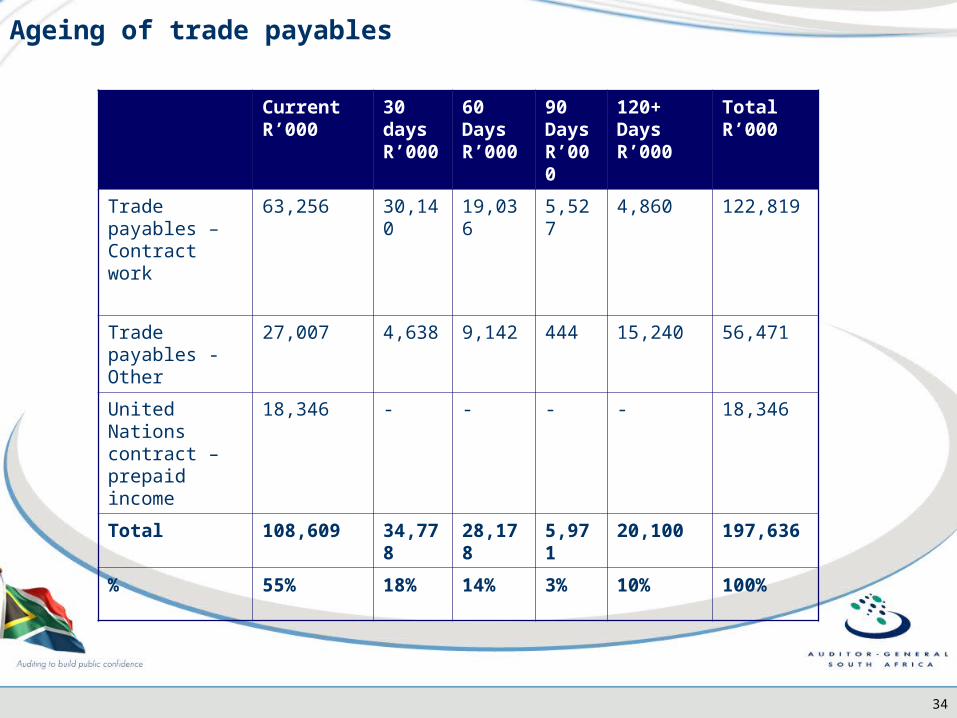

Ageing of trade payables

Current R’000

30 days R’000

60 Days R’000

90 Days R’000

120+ Days R’000

Total R’000

Trade payables – Contract work

63,256 30,140 19,036 5,527 4,860 122,819

Trade payables - Other

27,007 4,638 9,142 444 15,240 56,471

United Nations contract – prepaid income

18,346 - - - - 18,346

Total 108,609 34,778 28,178 5,971 20,100 197,636

% 55% 18% 14% 3% 10% 100%

35

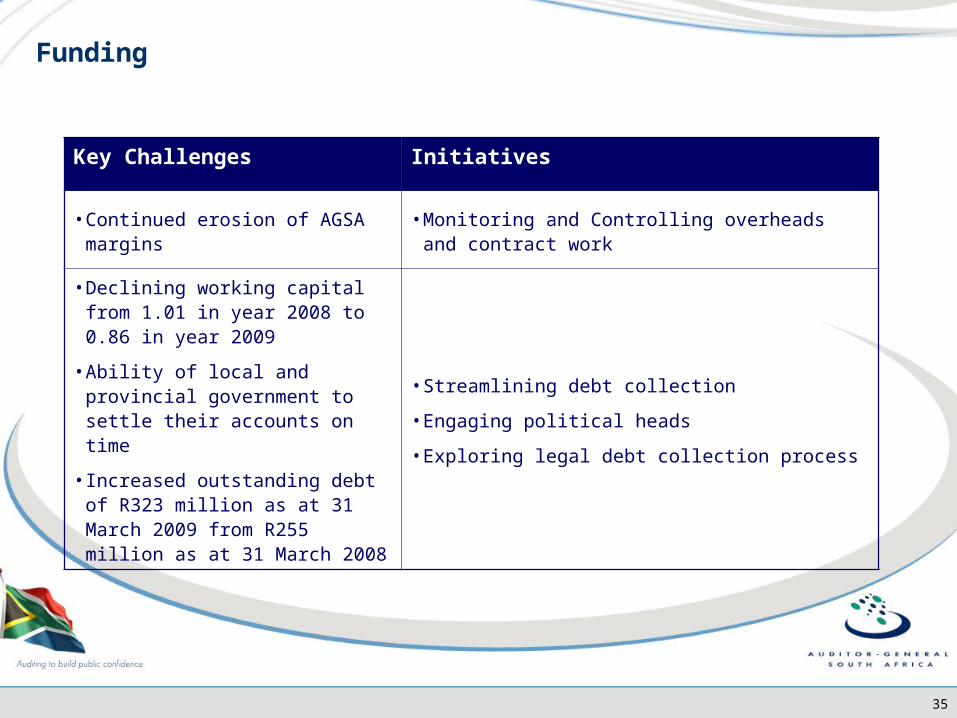

Funding

Key Challenges Initiatives

• Continued erosion of AGSA margins • Monitoring and Controlling overheads and contract

work

• Declining working capital from 1.01 in year 2008 to 0.86 in year 2009

• Ability of local and provincial government to settle their accounts on time

• Increased outstanding debt of R323 million as at 31 March 2009 from R255 million as at 31 March 2008

• Streamlining debt collection

• Engaging political heads

• Exploring legal debt collection process

36

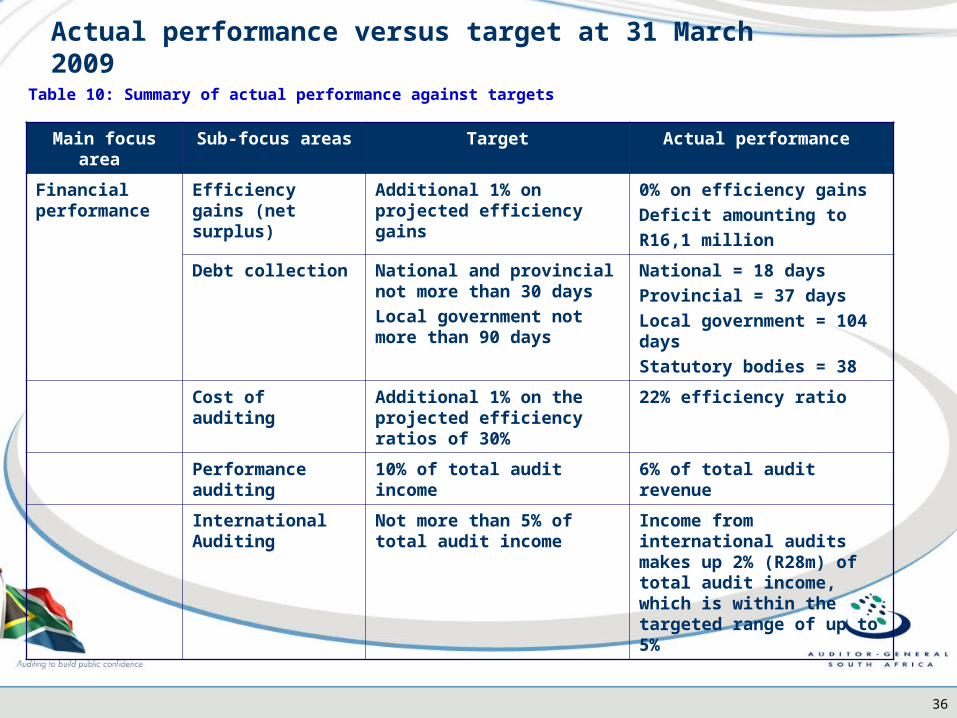

Main focus area Sub-focus areas Target Actual performance

Financial performance

Efficiency gains (net surplus)

Additional 1% on projected efficiency gains

0% on efficiency gains

Deficit amounting to

R16,1 million

Debt collection National and provincial not more than 30 days

Local government not more than 90 days

National = 18 days

Provincial = 37 days

Local government = 104 days

Statutory bodies = 38

Cost of auditing Additional 1% on the projected efficiency ratios of 30%

22% efficiency ratio

Performance auditing

10% of total audit income 6% of total audit revenue

International Auditing

Not more than 5% of total audit income

Income from international audits makes up 2% (R28m) of total audit income, which is within the targeted range of up to 5%

Table 10: Summary of actual performance against targets

Actual performance versus target at 31 March 2009

37

Key achievements

• Developed AGSA BBBEE strategy

• Achieved Employment Equity set target: 80% on targeted group and 20% on non-targeted group

• Crafted the organisational wide risk management framework to cover strategic, financial and operational risks that are monitored by EXCO on a regular basis

• Revamped ICT, HC and Finance processes

Lead by Example

38

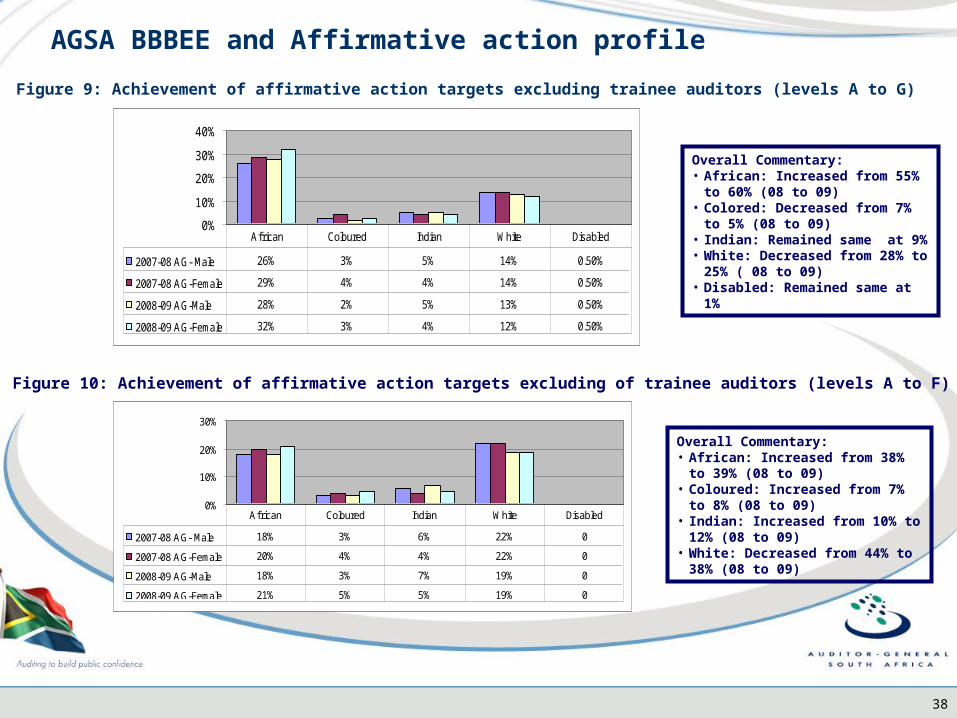

Figure 9: Achievement of affirmative action targets excluding trainee auditors (levels A to G)

Figure 10: Achievement of affirmative action targets excluding of trainee auditors (levels A to F)

Overall Commentary:• African: Increased from 55% to 60%

(08 to 09)• Colored: Decreased from 7% to 5%

(08 to 09)• Indian: Remained same at 9%• White: Decreased from 28% to 25%

( 08 to 09)• Disabled: Remained same at 1%

Overall Commentary:• African: Increased from 38% to 39%

(08 to 09)• Coloured: Increased from 7% to 8%

(08 to 09)• Indian: Increased from 10% to 12%

(08 to 09)• White: Decreased from 44% to 38%

(08 to 09)

AGSA BBBEE and Affirmative action profile

0%

10%

20%

30%

40%

2007-08 AG- Male 26% 3% 5% 14% 0.50%

2007-08 AG-Female 29% 4% 4% 14% 0.50%

2008-09 AG-Male 28% 2% 5% 13% 0.50%

2008-09 AG-Female 32% 3% 4% 12% 0.50%

African Coloured Indian White Disabled

0%

10%

20%

30%

2007-08 AG- Male 18% 3% 6% 22% 0

2007-08 AG-Female 20% 4% 4% 22% 0

2008-09 AG-Male 18% 3% 7% 19% 0

2008-09 AG-Female 21% 5% 5% 19% 0

African Coloured Indian White Disabled

39

Size of firms Allocation target

( % )

Budget

( RM )

% of budget total

Actual

( RM )

% of Actual

total

Big and large 45% 101 45% 146 47%

Medium 35% 78 35% 107 34%

Small 20% 45 20% 58 19%

100% 224 100% 311* 10%

BBBEE audit work allocation

Table 12: Allocation of audit work to private audit firms

*Note: The reporting is based on 20% allocation only

40

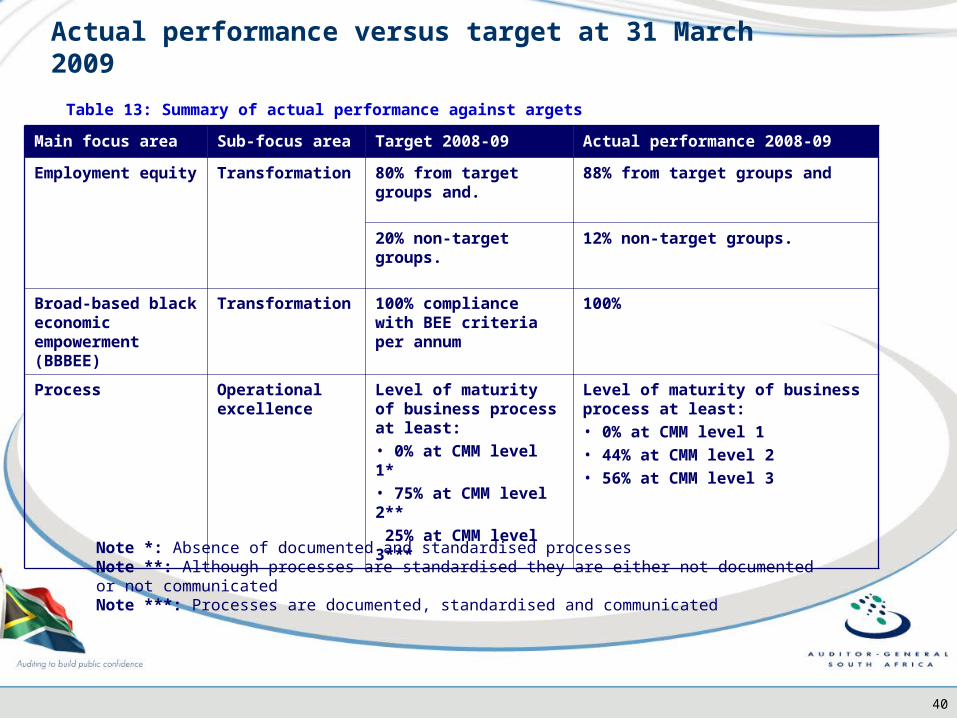

Main focus area Sub-focus area Target 2008-09 Actual performance 2008-09

Employment equity Transformation 80% from target groups and.

88% from target groups and

20% non-target groups. 12% non-target groups.

Broad-based black economic empowerment (BBBEE)

Transformation 100% compliance with BEE criteria per annum

100%

Process Operational excellence

Level of maturity of business process at least:• 0% at CMM level 1*• 75% at CMM level 2**

25% at CMM level 3***

Level of maturity of business process at least:• 0% at CMM level 1• 44% at CMM level 2• 56% at CMM level 3

Note *: Absence of documented and standardised processesNote **: Although processes are standardised they are either not documented or not communicatedNote ***: Processes are documented, standardised and communicated

Table 13: Summary of actual performance against argets

Actual performance versus target at 31 March 2009

41

Conclusions

• Submission of timely performance reports addressed with auditees, with National & Provincial Treasuries

• AGSA Financial sustainability addressed through the implementation of the revised Funding model in 2009

• AGSA Risks closely monitored

• Leadership visibility being improved

• More focus on the recruitment and retention of Trainee Auditors to address skills shortage

• Substantial development & growth of key processes

• BBBEE closely monitored