Embed Size (px)

Citation preview

Air Arabia

Air Arabia, based out of Sharjah in the UAE, pioneered the low-cost carrier (LCC) model

in the Middle East, being the first to introduce it successfully in the region. Its fleet today

consists of nine aircrafts, which it flies to 32 destinations around the Middle East and the

Indian Sub Continent. The company plans to grow the fleet to 34 aircrafts by 2015, to be

utilized on existing routes and new potential routes in the region.

Core competitive strengths of Air Arabia include its first mover advantage, its ability to

quickly scale up, a young fleet, high utilization of its aircrafts, its strong and established

brand, its established and effective distribution network, its efficient low cost base and

highly favourable home and regional market dynamics.

Core drivers for the company include high expected economic growth, the

demographic mix in the UAE and the region, the current low penetration rate of LCCs,

the high elasticity of demand, growth in air travel infrastructure and the expected

deregulation and liberalization of the sector.

•

•

•

Current Price: NA Country: United Arab Emirates

Fair value Target: NA Sector: Airlines / Transportation

Recommendation: NA Exchange: Dubai Financial Market

March 12th, 2007

Pre IPO CoverageEquity Research

Sector Coverage Team

Kareem Z. Murad+9714 3199 [email protected]

Ahmad Shahin+9714 3199 [email protected]

Equities research

March 12th, 2007 2

Air Arabia

Contents

INVESTMENT HIGHLIGHTS .........................................................3

COMPANY OVERVIEW ................................................................4

DESCRIPTION ................................................................................................................................... 4

THE HUB .......................................................................................................................................... 5

ORGANIZATION STRUCTURE .......................................................................................................... 5

OWNERSHIP STRUCTURE ............................................................................................................... 6

SUBSIDIARIES .................................................................................................................................. 6

OPERATIONS .................................................................................................................................... 6

KEY OPERATING DATA .................................................................................................................... 7

MILESTONES .................................................................................................................................... 7

FLEET ................................................................................................................................................ 7

PASSENGER TRAFFIC....................................................................................................................... 8

ROUTES ............................................................................................................................................ 9

CORE COMPETITIVE STRENGTHS ................................................................................................. 11

SWOT ............................................................................................................................................. 11

COMPANY STRATEGY ................................................................................................................... 12

USES OF RAISED CAPITAL ............................................................................................................ 16

INDUSTRY OVERVIEW ..............................................................17

REGIONAL DRIVERS ...................................................................................................................... 19

PENETRATION RATES .................................................................................................................... 24

PASSENGER TRAFFIC GROWTH BY REGION ............................................................................... 25

PORTER’S 5 FORCES ..................................................................................................................... 25

OUTLOOK ....................................................................................................................................... 26

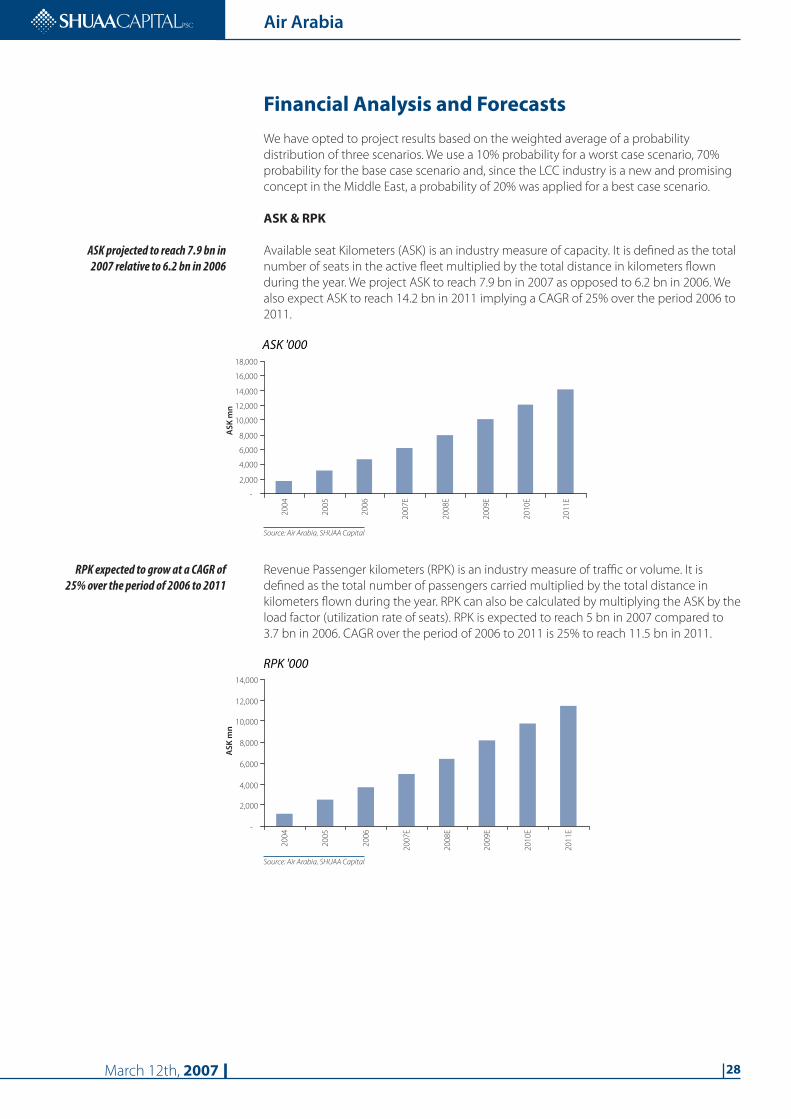

FINANCIAL ANALYSIS AND FORECASTS ......................................28

ASK & RPK ..................................................................................................................................... 28

REVENUES, PASSENGER GROWTH AND REVENUES PER PASSENGER ..................................... 29

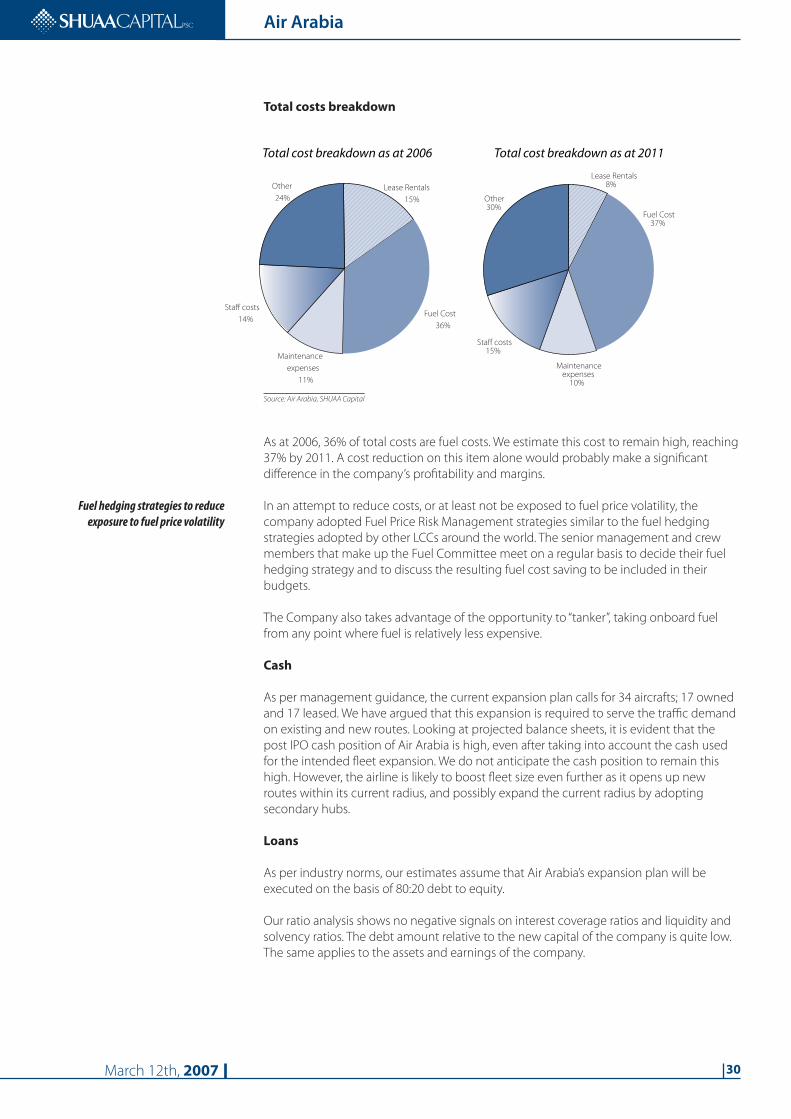

TOTAL COSTS BREAKDOWN ......................................................................................................... 30

CASH .............................................................................................................................................. 30

LOANS ............................................................................................................................................ 30

GOODWILL AND AMORTIZATION ................................................................................................ 31

EBITDAR AND EBITDAR MARGIN ................................................................................................ 31

NET PROFITS AND NET PROFIT MARGIN..................................................................................... 31

GLOBAL PEERS .......................................................................32

FINANCIALS AND KEY RATIOS ...................................................33

APPENDIX ..............................................................................36

Equities research

March 12th, 2007 3

Air Arabia

Investment Highlights

Air Arabia pioneered the low cost carrier model in the Middle East, being the first to

introduce it successfully in the region.

A low-cost carrier or low-cost airline is an airline that generally offers low flight fares by

eliminating many traditional passenger services. The business model is typically based

on cost reduction by operating a single passenger class, a single type of airplane, and the

absence of ‘free’ in-flight catering and other additional services.

The company uses Sharjah International Airport as its main hub, making it the first

passenger airline to use the airport as a hub, and contributing massively to traffic through

the airport.

Air Arabia fleet today consists of nine aircrafts, which it flies to 32 destinations around

the Middle East and the Indian Sub Continent. The company plans to grow the fleet to 34

owned and leased aircrafts by 2015, to be utilized on existing routes and new potential

routes within a 4-5 hours flying time radius from its hub.

Core competitive strengths of Air Arabia include its first mover advantage, its ability to

quickly scale up, a young fleet, its high utilization of its aircrafts its strong and established

brand, its established and effective distribution network, its efficient low cost base and

highly favorable home and regional market dynamics.

Core risks include market resistance due to underdeveloped perception of LCCs,

sluggish liberalization of the sector, higher fuel costs, and the risk of deterioration on the

geopolitical front in the region.

Demand for air transportation services in the Middle East has shown substantial

growth in recent years, with passenger traffic in the Middle East increasing by a CAGR of

9% over the past five years. The primary drivers of this growth include strong economic

growth, lower fares, supportive demographic trends, growth in tourism, deregulation and

liberalization, and improved infrastructure. We expect demand in this sector to continue

to exceed global averages for the foreseeable future.

The price elasticity of demand for air transport is high, and we are therefore expecting

LCCs to enjoy higher growth rates than conventional airlines in the region, especially that

the sector currently enjoys a very low penetration rate.

The expatriate population of the UAE is estimated at around 80% of the country’s total

population, the highest rate in the GCC, the majority of which are from neighboring

countries. We believe that this demographic mix represents one of the core growth

drivers for Air Arabia going forward.

The company plans to utilize the proceeds from the upcoming IPO to grow its fleet

across its existing routes and into new regional routes. Other areas of potential growth

include the adoption of a second hub to broaden the airlines coverage in the region.

We project revenues of Air Arabia to reach AED 2.5 bn by 2011, representing a CAGR

of 26.3% from 2006, driven by the high load factors and in anticipation of new aircrafts

joining the current fleet. The number of passengers traveling with Air Arabia is expected

to grow at a CAGR of 25% between 2006 and 2011, reaching 5.263 million passengers by

2011, stimulated by the positive outlook of the industry and the region.

Air Arabia became profitable after its first full year of operation in 2004. We expect net

profits to double in 2007 reaching AED 226 mn and grow commensurately with gross

profits and EBITDAR at a CAGR of 29.6% to reach AED 369 mn by 2011 compared to AED

101 mn in 2006. We expect margins to reach 15% by 2011 versus 14% in 2006.

•

•

•

•

•

•

•

•

•

•

•

•

Equities research

March 12th, 2007 4

Air Arabia

Company overview

Description

Air Arabia pioneered the low-cost carrier (LCC) model in the Middle East, being the first

to introduce it successfully in the region. It was established on the 3rd of February 2003

by an Ameeri decree issued by the ruler of Sharjah, His Highness Dr. Sheikh Sultan Bin

Mohamed Al Qassimi. Sharjah’s International Airport is the company’s main hub. Air Arabia

began with a mission to revolutionize air travel in the region, much in the same way that

the introduction of low cost carriers revolutionized travel in the US, Europe and Asia, by

offering good value for money, and a safe, reliable operation. Air Arabia, as a business,

aims to be known for its low fares, growing business volume and profitability, highest

operational standards, a motivated work force and efficient management.

A low-cost carrier (LCC) or low-cost airline is an airline which is able to offer generally low

flight fares by eliminating many traditional passenger services. The concept was incepted

in the United States before spreading to Europe in the early 90’s. A low cost carrier’s

business model is typically based on cost cuts such as a single passenger class, a single

type of airplane (commonly the Airbus A 320 or Boeing 737), and the absence of ‘free’ in-

flight catering and other additional services.

Air Arabia is effectively modeled after leading American and European LLCs and is

customized to local preferences. However, we believe that the demographic structure

and intra-regional travel practice of the MENA might better fit the American model. This

is due to the fact that a large portion of the inhabitants of the US choose to work or study

away from their home states, driving a large number of ‘visiting friends and family’ (VFF)

travelers, which is similar to trends witnessed in expatriate-laden populations of the Gulf.

Such travelers tend to lean towards low cost carriers, which make multiple visits more

feasible economically.

Air Arabia’s value proposition is to offer individuals in the region - who were previously

discouraged from frequent regional travel by the high fares of conventional airlines - the

ability to travel almost at will. This value proposition has affected, and will continue to

affect, the whole regional airline industry, and is now one of the core factors boosting

growth in passenger traffic going forward.

First low cost carrier concept in the Middle East, established with a

mission to revolutionize air travel

Modelled after the US & European LCCs, however, the demographics of

the region better fit the US model

Equities research

March 12th, 2007 5

Air Arabia

The hub

Sharjah International Airport was established in 1932, serving as a stopover point for

flights en-route to their final destinations in India and Australia. As both the UAE and

the emirate of Sharjah grew in stature over the years, the airport has since expanded to

connect all major international destinations. However, substantial growth in passenger

traffic only really took off after the establishment of Air Arabia, as it was the first passenger

carrier to adopt the airport as a hub.

Sharjah International Airport is 10 kilometers away from Sharjah city centre and about 15

kilometers away from the emirate of Dubai. It is also in the vicinity of the smaller northern

and eastern emirates of the UAE. It operates an open sky policy that has enhanced its

flexibility and competitiveness, and that have attracted a broad number of carriers,

primarily from central and south Asia.

In October 2003, the first Air Arabia flight took off from Sharjah Airport heading to Bahrain,

marking the airline’s official launch of operations.

Sharjah International Airport handles at least 1,800 aircraft and some 100,000 passengers

every month. Below is a chart displaying the passenger movement at Sharjah

International airport, and Air Arabia’s contribution to that movement.

Source: Sharjah International Airport, Air Arabia, SHUAA Capital

Organization structure

Adel A. AliChief Executive Officer

HH Sheikh Abdullah Bin

Mohammed Al Thani

Chairman

Mohammad Al Qassimi

Advisor Operations & Technical

(Vacant)

Manager of Internal Audit

Oussama Alfonse Salah

Quality and Safety Manager

Imad Raad

Manager Corporate Security

Ali Hamdany

Director of IT &

Corporate Projects

Kyle Haywood

Commercial Director

Mohamed Ahmed

Director of Operations &

Maintenance

Donald Hubbard

Director of Strategy &

Planning

Paul Suckling

Director of Finance &

Administration

Source: Air Arabia, SHUAA Capital

Passenger movement

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2000 2001 2002 2003 2004 2005 2006

Pa

sse

ng

er

tra

ffic

'00

0

Other airlines Air Arabia passengers

Passenger movement

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2000 2001 2002 2003 2004 2005 2006

Pa

sse

ng

er

tra

ffic

'00

0

Other airlines Air Arabia passengers

Air Arabia adopted Sharjah International Airport as its main hub for cost efficiency

and due to its proximity to Dubai and accessibility to northern emirates.

Equities research

March 12th, 2007 6

Air Arabia

Ownership structure

Source: Air Arabia, SHUAA Capital

Subsidiaries

Subsidiary Place of incorporation Percentage ownership Activities

Red Marketing Communications FZE

Sharjah Airport International Free Zone 100% Providing marketing, advertisement agency and

communication services.

Information Systems Association FZC

Sharjah Airport International Free Zone 51% ownership, a joint venture with John Keels

Holding Limited

Providing IT services for the business require-

ments of Air Arabia in addition to IT solutions &

services for low cost carriers globally.

Sharjah Aviation Services

Sharjah Airport International Free Zone 50% joint venture with the

government of Sharjah

Ground handling

Haeco Sharjah Aircraft Maintenance Ltd.*

Sharjah International Airport 51% joint venture with Honk Kong listed Haeco Engineering and maintenance

*announced on 12th of March 2007

Source: Air Arabia, SHUAA Capital

Operations

Typically, the vast majority of low cost carriers’ revenues are passenger-related. In 2005 and

2006, over 95% of the revenues of Air Arabia were passenger revenues, 3% were baggage

revenues and the remaining 2% came in from cargo activities.

Passenger revenues are a function of load factor and airfare, where the load factor is the

average number of occupied seats relative to total seats available for all flights made

during the year.

A good estimate for air fares, and by extension passengers’ cost savings in LCCs, is revenue

per available seat kilometers (RASK) (revenues * seat capacity * kilometers traveled).

Comparing the 2004 and 2005 RASK of Air Arabia to that of Emirates Airlines, the largest

UAE based conventional carrier, we find that the RASK of Air Arabia is 35% and 27% lower

than that of Emirates Airlines, respectively.

Source: Emirates Airlines, Company, SHUAA Capital

Pre IPO ownership structure

27%

15%

20%

15%

23%

Department of Civil Aviation

Sharjah International Airport Authority

Al Maha Holding

Institutional investors

Other investors

Post IPO ownership structure12%

7%

9%

7%

10%

55%

Department of Civil Aviation

Sharjah International Airport Authority

Al Maha Holding

Institutional investors

Other investors

Free Float

Pre IPO ownership structure

27%

15%

20%

15%

23%

Department of Civil Aviation

Sharjah International Airport Authority

Al Maha Holding

Institutional investors

Other investors

Post IPO ownership structure12%

7%

9%

7%

10%

55%

Department of Civil Aviation

Sharjah International Airport Authority

Al Maha Holding

Institutional investors

Other investors

Free Float

RASK for conventional airlines vs LCC

0.0

2.0

4.0

6.0

8.0

10.0

2004 2005

RA

SK

(ce

nts

)

RASK Emirates (cents) RASK Air Arabia (cents)

35%

27%

RASK for conventional airlines vs LCC

0.0

2.0

4.0

6.0

8.0

10.0

2004 2005

RA

SK

(ce

nts

)

RASK Emirates (cents) RASK Air Arabia (cents)

35%

27%

Air fares for Air Arabia are on average 27% less than local

conventional airlines as at 2005

Equities research

March 12th, 2007 7

Air Arabia

In addition to the air-travel services, Air Arabia provides several on-board, on-ground and

logistic services that are purchased, optionally and separately, from the ticket charges.

Ground Services are limited to coaching services that provide airport drop-off and pick up

(only within UAE and Istanbul) at special relatively low-price rates.

Visa Assistance services are also provided by Air Arabia, whereby the passenger contacts

Air Arabia for visa assistance in UAE and any other country of destination.

Key operating data

Key operating data 2004 2005 2006

No. of routes 15 23 32

No. of passengers 546,587 1,132,912 1,762,810

Seat factor % 68 79 80

No of aircraft at year end 4 5 8

Average no. of aircrafts 4 5.2 6.8

ASK ‘000 1,734,696 3,172,349 4,695,667

RPK ‘000 1,179,593 2,506,156 3,737,751

Block hrs per aircraft per day 9.2 12.9 14.5

No. of sectors flown 5,398 9,412 13,512

Block hours 13,385 24,478 35,902

Average no. of employees 250 314 464

Source: Air Arabia, SHUAA Capital

Milestones

Source: Air Arabia website, SHUAA Capital

Fleet

Air Arabia’s fleet today consists of 9 aircraft (8 at the end of 2006 and an additional aircraft

joining the fleet early 2007), all of which are leased aircrafts. However, the company

intends to place orders to purchase additional aircrafts, following its IPO. As per the

company’s existing strategy, the fleet is to increase in size to 34 owned and leased aircraft

by 2015. Consistent with the traditional model for LCCs, all aircrafts will likely continue to

be of a single type, the narrow bodied Airbus A320.

According to Air Arabia’s management, the increase of its fleet size is a strategic decision

based primarily on demand for existing routes, as well as new potential routes. The

company believes that a significant portion of the 34-aircraft fleet will be required to

service existing routes through increasing the number of trips to existing destinations,

while agreements to fly to other destinations will drive the demand for further aircrafts.

2003 2007

Launch of

Air Arabia

Fleet:

2 aircrafts

Fleet:

4 aircrafts

Dec 04

Fleet:

9 aircrafts

Jan 07Dec 05

Fleet:

5 aircrafts

Oct 06

3 million

passengers

March 07

Dec 06

Fleet:

8 aircrafts

2 million

passngers

Mar 06

1 million passengers

since launch

Jun 05

Air Arabia 500,000 passenger

celebration

Oct-04

First plane departing

Sharjah

Oct 03

Dec 032003

IPO Start

2003 2007

Launch of

Air Arabia

Fleet:

2 aircrafts

Fleet:

4 aircrafts

Dec 04

Fleet:

9 aircrafts

Jan 07Dec 05

Fleet:

5 aircrafts

Oct 06

3 million

passengers

March 07

Dec 06

Fleet:

8 aircrafts

2 million

passngers

Mar 06

1 million passengers

since launch

Jun 05

Air Arabia 500,000 passenger

celebration

Oct-04

First plane departing

Sharjah

Oct 03

Dec 032003

IPO Start

Fleet today consists of 9 leased aircrafts and is expected to reach 34

aircrafts owned & leased by 2015

Equities research

March 12th, 2007 8

Air Arabia

Below are tables detailing existing, ordered and to be potentially ordered aircrafts.

Existing fleet

Aircraft type and registration no. Lessor Date of Lease Date of Delivery Lease Period Option to Extend

A-ABA (MSN2158) ILFC1 10/09/2003 24/02/2004 5 years 2 years

A6-ABD (MSN2349) ILFC 10/09/2003 25/01/2005 5 years 2 years

A6-ABB (MSN2166) ILFC 10/09/2003 23/03/2004 5 years 2 years

A6-ABC (MSN2278) ILFC 10/09/2003 13/10/2004 5 years 2 years

A-ABE (MSN2712) CIT2 31/07/2006 17/03/2006 6 years -

A6-ABF (MSN2764) CIT 30/11/2005 28/04/2006 6 years -

A6-ABG (MSN2930) CIT 30/11/2005 31/10/2006 6 years -

A6-ABH(MSN2964) CIT 22/02/2006 28/11/2006 6 years -

A6-ABI (MSN3044) CIT 04/09/2006 23/02/2007 6 years -

1 International Lease Finance Corporation, 2 CIT Aerospace International

Source: Air Arabia, SHUAA Capital

The mentioned fleet expansion is to be achieved through ownership and lease of aircrafts

by 2015. As highlighted in the chart below, management currently has a clear idea on

the division between leasing and owning aircrafts. It is important to note, however, that

current management plans are subject to change with the possible introduction of new

routes. Following the IPO, the company will have more cash available on its books going

forward, which may influence its strategic thinking.

Source: Air Arabia, SHUAA Capital

Passenger traffic

Since Air Arabia started operations, its annual number of passengers has been showing

very strong growth, with 1.7 million passengers in 2006, 47% higher than in 2005.

This increase in passenger traffic was accompanied by increases in operating aircrafts,

destinations, average sector flights per year and most importantly, load factors. Taken

together, these factors reflect the increased awareness of Air Arabia’s brand and its

business model, and by extension, highlighting the potential market of the LCC model in

the Middle East.

Source: Air Arabia, SHUAA Capital

Air Arabia fleet

4 5 8 11 12 13 13 10 12 14 16 17

3

leased aircrafts owned aircrafts

6 1213

1415

17

-

5

10

15

20

25

30

35

40

20

04

20

05

20

06

20

07

E

20

08

E

20

09

E

20

10

E

20

11

E

20

12

E

20

13

E

20

14

E

20

15

E

Air

cra

fts

Air Arabia fleet

4 5 8 11 12 13 13 10 12 14 16 17

3

leased aircrafts owned aircrafts

6 1213

1415

17

-

5

10

15

20

25

30

35

40

20

04

20

05

20

06

20

07

E

20

08

E

20

09

E

20

10

E

20

11

E

20

12

E

20

13

E

20

14

E

20

15

E

Air

cra

fts

Passenger & revenue per passenger

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Dec-

04

Dec-

05

Dec-

06

Dec-

07E

Dec-

08E

Dec-

09E

Dec-

10E

Dec-

11E

Pa

sse

ng

ers

’00

0

0

50

100

150

200

250

300

350

400

450

500

Re

ve

nu

e p

er

pa

sse

ng

er

AE

D

Number of Passengers Revenues / Passenger

Passenger & revenue per passenger

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Dec-

04

Dec-

05

Dec-

06

Dec-

07E

Dec-

08E

Dec-

09E

Dec-

10E

Dec-

11E

Pa

sse

ng

ers

’00

0

0

50

100

150

200

250

300

350

400

450

500

Re

ve

nu

e p

er

pa

sse

ng

er

AE

D

Number of Passengers Revenues / Passenger

Air Arabia’s passenger traffic grew by 47% in 2006 to reach 1.7 mn passengers

Equities research

March 12th, 2007 9

Air Arabia

Routes

We provide a graphical illustration of Air Arabia’s currently scheduled flight routes.

Additionally, we also identify potential new destinations that Air Arabia could add to its

current portfolio of destinations.

Our selection of additional destinations is based on an estimate of a 4-5 hour flying time

radius from Air Arabia’s home base of Sharjah. Going forward, we expect the addition

of secondary hubs to significantly widen Air Arabia’s potential coverage reach, with

incremental 4-5 hour radius additions from each new hub.

Existing routes

Source: Air Arabia, SHUAA Capital

Today, Air Arabia has scheduled flights to 32 destinations around the Middle East and

the Indian Sub Continent. The routes operated all fall within a 4-5 hour flying time radius

from Sharjah international Airport, and hence are concentrated in the Gulf, the broader

Middle East, East Africa, Central and South Asia. Given the short haul nature of its routes,

traffic on Air Arabia is primarily point-to-point. The routes represent the population origin

mix within the UAE and intra-regional tourism flows accurately. The carrier flies routes

which are traditionally popular with conventional carriers in the region. In addition, Air

Arabia began flying to new routes that conventional carriers have not offered historically,

and which have generated new point-to-point traffic. Destination airports include both

primary and secondary airports. A number of popular destinations that fall within the

target radius are still missing, such as Cairo, primarily due to restrictions and limitations on

landing rights.

Arctic Circle

Tropic of CancerTropic of Cancer

Tropic of Capricorn

Equator Equator

Tropic of Capricorn

ATLANTICPACIFIC PACIFIC

OCEANOCEAN

OCEAN

ARCTIC OCEANARCTIC OCEAN

Somoa

Venezuela

Uruguay

United States

United Kingdom

Tunisia

Trinidad & Tobag oTogo

Switz.

Sweden

Suriname

Spain

Slovenia

Slovakia

Sierra Leone

Serb. &Mont.

Senegal

Sao Tome & Princip e

Portugal

Poland

Peru

Paraguay

Panama

Norway

Nigeria

Niger

Nicaragua

Neth.

Morocco

Mongolia

Mexico

Mauritania

Malta

Mali

Mace.

Lux.

Lithuania

Libya

Liberia

Latvia

S. Korea

N. Korea

Japan

Jamaica

Italy

Ireland

Iceland

Hungary

HondurasHaiti

Guyana

Guinea-BissauGuinea

Guatemala

Greenland

Ghana

Germany

Gambia

French Guiana

France

Finland

Estonia

Equatorial Guinea

El Salvado r

Ecuador

Dom. Rep.

Denmark

Czech Rep.

Cuba

Croatia

Coted'Ivoir

Costa Ric a

Colombia

Chil e

Cape Verde

Canad a

Cameroon

Burkina Fas o

Brazi l

Bos. &Herz.

Bolivi a

Benin

Beliz e

Bel.

Belarus

Bahamas

Austria

Argentina

Algeria

Albania

Western Sahara

1000 Km0

Ukraine

Mold.Romania

Russia

(Occupied by Morocco)

China

U.A.E. Jaipur

Kathmandu

Almaty

Astana

Alexandria

Assiut

Jeddah

Khartoum

Sana’a

Nagpur

Mumbai

Chennai

Thuravanthapuram

Colombo

Arctic Circle

Tropic of CancerTropic of Cancer

Tropic of Capricorn

Equator Equator

Tropic of Capricorn

ATLANTICPACIFIC PACIFIC

OCEANOCEAN

OCEAN

ARCTIC OCEANARCTIC OCEAN

Somoa

Venezuela

Uruguay

United States

United Kingdom

Tunisia

Trinidad & Tobag oTogo

Switz.

Sweden

Suriname

Spain

Slovenia

Slovakia

Sierra Leone

Serb. &Mont.

Senegal

Sao Tome & Princip e

Portugal

Poland

Peru

Paraguay

Panama

Norway

Nigeria

Niger

Nicaragua

Neth.

Morocco

Mongolia

Mexico

Mauritania

Malta

Mali

Mace.

Lux.

Lithuania

Libya

Liberia

Latvia

S. Korea

N. Korea

Japan

Jamaica

Italy

Ireland

Iceland

Hungary

HondurasHaiti

Guyana

Guinea-BissauGuinea

Guatemala

Greenland

Ghana

Germany

Gambia

French Guiana

France

Finland

Estonia

Equatorial Guinea

El Salvado r

Ecuador

Dom. Rep.

Denmark

Czech Rep.

Cuba

Croatia

Coted'Ivoir

Costa Ric a

Colombia

Chil e

Cape Verde

Canad a

Cameroon

Burkina Fas o

Brazi l

Bos. &Herz.

Bolivi a

Benin

Beliz e

Bel.

Belarus

Bahamas

Austria

Argentina

Algeria

Albania

Western Sahara

1000 Km0

Ukraine

Mold.Romania

Russia

(Occupied by Morocco)

China

INDIAN

OCEAN

YemenY

Sri LankaSomalia

India

U.A.E. Jaipur

Kathmandu

Kabul

Almaty

Astana

Tehran

YerevanIstanbul

AleppoLatakia

BeirutDamascus

AmmanAlexandria

Assiut

Luxor

Jeddah

Khartoum

Sana’a

Riyadh DohaBahrain

Dammam

Kuwait

Nagpur

Mumbai

Chennai

KochiThuravanthapuram

Colombo

Currently fly to 32 destination airports including primary and

secondary airports around the Middle East & Indian Sub-continent

Equities research

March 12th, 2007 10

Air Arabia

The company is currently operating at an average load factor of 80%, compared with a

2006 average of 73% for the industry (including conventional airlines). This higher load

factor indicates the potential and need for more frequent flights to existing destinations,

either by increasing the daily operating time per aircraft or by adding new aircrafts to

cater to these destinations.

The chart below illustrates the scheduled number of flights per week to destination

countries against their average load factors, as per 2006 data. The intention is to show the

countries with highest traffic demand. India, through its main destination hubs of Kochi,

Mumbai, Nagpur, Jaipur and Thiruvananthapuram, is the destination with the most traffic.

Source: Air Arabia, SHUAA Capital

Source: Air Arabia, SHUAA Capital

Prospect routes

Madinah

Ankara

Salalah

Addis Ababa

Bangalore

Aqaba

Taba

Aswan

Luxor

Cairo

Tehran

Calcutta

VishakhapatnamHyderabad

Mangalore

Karachi

Lahore

Islamabad

Peshawar

Delhi

Calicuta

Coimbatore

Pune

Al Arish

Goa

Isfahan

Baghdad

ErbilErbil

Madras

Dhaka

Amritsar

MuscatAhmedabad

Shiraz

INDIAN

OCEAN

Sudan

Sri LankaSomalia

JJordaJordaJ danadaJordaAqabAqabbbbababb

IraqIraq

India

Ethiopia

EritreEEE

Egypt

U.A.E.

Saudi ArabiaSaudi ArabiS

Kazakhstan

Source: SHUAA Capital

Flights per week from Sharjah airport to destination

0

5

10

15

20

25

30

35

40

Ba

hra

in

Eg

ypt

Ira

n

Jord

an

KS

A

Ku

wa

it

Leb

an

on

Om

an

Qa

tar

Su

da

n

Syr

ia

Yem

en

Ind

ia

Ka

zakh

sta

n

Ne

pa

l

Sri

La

nka

Turk

ey

Fli

gh

ts

0

10

20

30

40

50

60

70

80

90

100

Lo

ad

Fa

cto

r

Flights Load factor

Flights per week from Sharjah airport to destination

0

5

10

15

20

25

30

35

40

Ba

hra

in

Eg

ypt

Ira

n

Jord

an

KS

A

Ku

wa

it

Leb

an

on

Om

an

Qa

tar

Su

da

n

Syr

ia

Yem

en

Ind

ia

Ka

zakh

sta

n

Ne

pa

l

Sri

La

nka

Turk

ey

Fli

gh

ts

0

10

20

30

40

50

60

70

80

90

100

Lo

ad

Fa

cto

r

Flights Load factor

Passenger traffic to & from destinations in 2006

-

50

100

150

200

250

300

350

400

450

Ba

hra

in

Eg

ypt

Ira

n

Jord

an

KS

A

Ku

wa

it

Leb

an

on

Om

an

Qa

tar

Su

da

n

Syr

ia

Yem

en

Ind

ia

Ka

zakh

sta

n

Ne

pa

l

Sri

La

nka

Turk

ey

Nu

mb

er

of

pa

sse

ng

ers

'00

0

Passenger traffic to & from destinations in 2006

-

50

100

150

200

250

300

350

400

450

Ba

hra

in

Eg

ypt

Ira

n

Jord

an

KS

A

Ku

wa

it

Leb

an

on

Om

an

Qa

tar

Su

da

n

Syr

ia

Yem

en

Ind

ia

Ka

zakh

sta

n

Ne

pa

l

Sri

La

nka

Turk

ey

Nu

mb

er

of

pa

sse

ng

ers

'00

0

Equities research

March 12th, 2007 11

Air Arabia

There remain many prospective routes that Air Arabia may add in the future, and that

lie well within the four hour target flying radius, depending on a larger fleet, and more

importantly, landing rights. In addition to Cairo, Air Arabia has yet to introduce any flights

to Pakistan, whose expatriates make up 10% of the UAE population. Routes to new

destinations in Southern and Eastern Europe, Eastern Africa Central Asia and India may

also prove to be attractive prospects for the Airline in the future.

Core competitive strengths

Despite intensifying regional competition, the LCCs industry remains comparatively

immature. Air Arabia, being the first mover in this high-growth industry, is pre-eminently

positioned to capitalize on the expected growth of regional low-cost air travel demand.

Earlier this year, Air Arabia was awarded the ‘Low Cost Airline of the Year 2006’ award by

the Centre of Asia Pacific Aviation (CAPA), in recognition of its strong strategic contribution

for the aviation industry. CAPA is a leading aviation consulting services provider, airline

conferences organizer, aviation news publisher and analysis provider in the Asia Pacific

region, the Indian Subcontinent and Middle East.

Below are what we believe to be the company’s core competitive strengths at this point:

Clear first mover advantage in the region

Established and effective distribution network

Young fleet (low maintenance cost)

Efficient low cost base

An ability to scale up quickly

Highly favorable home and regional market dynamics

Efficient aircraft utilization

SWOT

Strengths

• Strong brand identity, being the first

low cost carrier in the region

• Taking Sharjah International Airport as

an operational hub

• Scheduled flights already established

around the region

• Safe (new air crafts fleet), not

compromising the safety for price

• Very young fleet

Opportunities

• Inbound / outbound tourism growth in

UAE

• Anticipated population growth will

tend to raise the frequency of business

travel

• Strong Economic growth

• Establishment of secondary hubs to

widen reach radius

• Single GCC Visa

• Potential intra gulf double daily flights

• Hub in the Mediterranean to gain

access to North Africa (Libya, Tunis,

Algeria and Morocco)

Threats

• New LCCs being established in the

region

• Conventional airline carriers on

regional routes

• Traffic and landing rights

• Deterioration in geopolitical

environment

Weaknesses

• Based in Sharjah airport which create

inconvenience to Dubai & Abu Dhabi

based clients (due to huge traffic

congestion)

• No incentive program (compared

with skywards)

• Perception of low price means

compromising safety

Source: SHUAA Capital

•

•

•

•

•

•

•

With a potential to add many new routes in the future

Equities research

March 12th, 2007 12

Air Arabia

Company strategy

Corporate strategy The company aims to revolutionize air travel in the region and to become the leading low

cost carrier in the Middle East, taking advantage of the prevalent low penetration rate and

substantial potential for increased air travel. To achieve its vision, it will have to attend to

the key market requirements of substantially lower fares and adequate supply capacities.

The successful low cost structure is vital for the success and survival of Air Arabia’s

business model. The strategy should be focused on gaining more cost efficiencies to

maintain competitive fares. Maintaining low fare structure is the key driver given the price

elasticity of demand and the likely increase in competition, even against conventional

airlines on certain destinations. Regional conventional airlines have recently started

to focus on lowering their fares by achieving economies of scale and gaining cost

efficiencies.

In the case of Air Arabia, a key success factor in cost savings is their operations from

a small and un-congested hub. The benefits are shorter times to take off, taxi-in and

taxi-out; resulting in costs savings on fuel and repair costs. Air Arabia on average needs

around 5 minutes from the time they turn on their engines to get to the takeoff runway,

as opposed to almost 30 minutes in large congested airports. This means that there

are 25 minutes per trip per aircraft of fuel saving and lower engine usage and therefore

maintenance.

According to regulations, one cabin crew member is required per 50 passengers. Since Air

Arabia’s aircrafts are fitted with 162 seats, no more than 4 crew members are necessary per

flight; acting as another cost cut.

A vital role Air Arabia plays is deciding on its optimal seat configuration and concentrating

on maintaining that level. The decision on fitting all aircrafts with 162 seats came from

taking into consideration the optimal load factor, cabin space and weight for regional air

travel.

Source: IATA

Airlines tend to compensate for higher costs by charging higher than average fares and

excess luggage fees. Indeed factors such as pollution have already caused some countries

to consider, and in some cases, to implement, further limitations on weight.

Since its establishment, Air Arabia has succeeded in regularly increasing scheduled flights

to various destinations. Today it travels to 32 destinations, and will soon commence its

scheduled flights to Ahmadabad in India and Karachi and Peshawar in Pakistan. Potential

for further growth still exists given that a number of airports/destinations, within a 4 to 5

hour flight time radius, are yet to be penetrated.

Passenger load factor by region

68.6

72.7

76.4

72.673.6

79.5

75.1

68.3

74.6

77.0

73.0 73.4

80.2

76.0

60

65

70

75

80

85

Africa AsiaPacific

Europe LatinAmerica

MiddleEast

NorthAfrica

Total

2005 2006

Passenger load factor by region

68.6

72.7

76.4

72.673.6

79.5

75.1

68.3

74.6

77.0

73.0 73.4

80.2

76.0

60

65

70

75

80

85

Africa AsiaPacific

Europe LatinAmerica

MiddleEast

NorthAfrica

Total

2005 2006

Success depends on the ability to maintain cost efficiency

Operations from a secondary and un-congested hub is a key success factor

Equities research

March 12th, 2007 13

Air Arabia

Based on the potential for growth in existing routes, which are subject to current airport

capacity constraints, increasing the airline’s fleet size has become a priority. This is

especially the case if the airline is to continue to grow its overall market share in regional

air travel, as well as retaining its leading position among Low Cost Carriers in the Middle

East.

As mentioned earlier the company is currently operating 9 leased aircrafts and has the

ambition to operate 34 aircraft, owned and leased, by 2015. However, according to the

management, these numbers do not fully take into consideration other potential routes

or regulatory developments that can open doors to even bigger markets.

In the medium to long term, Air Arabia may adopt a second regional hub to enhance its

intra-regional capacity. We believe that this will be a key development for the airline, as it

would allow it to expand its regional profile and to increase its radius of coverage.

Competitive strategyCompetitive advantage is usually achieved by either price leadership or through

differentiation. However, as we have been arguing, the price competitiveness in the case

of Air Arabia is the main anchor for its business.

The low fare structure has increased the number of passengers traveling in general, and

in turn, increased the size of the market. Based on IATA surveys, 30% of the decision to

choose one flight over another is determined by price, while the remaining 70% is divided

between other considerations like frequent flyer programs, convenience and a positive

flight experience, each accounting for less than 30% of the decision. In other words, price

is the single most important factor in choosing flights for most travelers.

The survey defines the cost-driven competitive advantage, which Air Arabia currently

enjoys.

We identify Air Arabia’s competition -for the time being - as regional conventional airlines,

whose fares are almost 40% higher than that of Air Arabia. Conventional airlines might

be offering other added value services that contribute to the passengers’ experience, but

as shown above, ticket prices play a determining role in choosing between an LCC and a

conventional carrier.

Source: IATA

Air Arabia has the advantage of having the flexibility to increase its fares slightly because

it retains a temporary semi-monopoly, given the minimal competition from other LCC’s in

the region. However, we do not believe that it will increase its fares. Instead, we believe Air

Arabia will concentrate on penetrating new markets and establishing a competitive edge

over future potential competitors down the line, in an attempt to boost its brand equity in

the region.

As Air Arabia operates from a secondary airport, it tends to benefit from lower costs (less

fuel consumption) and higher turnover (more trips per aircraft) due to less congestion in

Airline criteria of flight choice

0%

5%

10%

15%

20%

25%

30%

35%

Price Frequent flier Convenient

schedules

Non-stop

flights

Previous

good

experience

Other

Airline criteria of flight choice

0%

5%

10%

15%

20%

25%

30%

35%

Price Frequent flier Convenient

schedules

Non-stop

flights

Previous

good

experience

Other

Air Arabia may adopt a secondary hub to increase radius of coverage

High price elasticity of demand

Equities research

March 12th, 2007 14

Air Arabia

the airport. This is since taxi, takeoff and landing are usually more efficient than at larger,

busier airports. Lower airport fees compared with larger regional hubs is also crucial in

retaining cost benefits.

On the down side, access to destination airports remains limited by capacity constraints,

reluctance in adopting open skies policies, and the reciprocation of access to airports

between flag carriers (national carriers). The Middle East region continues to be

dominated by flag carriers, while Air Arabia is the smallest among three flag-carriers in the

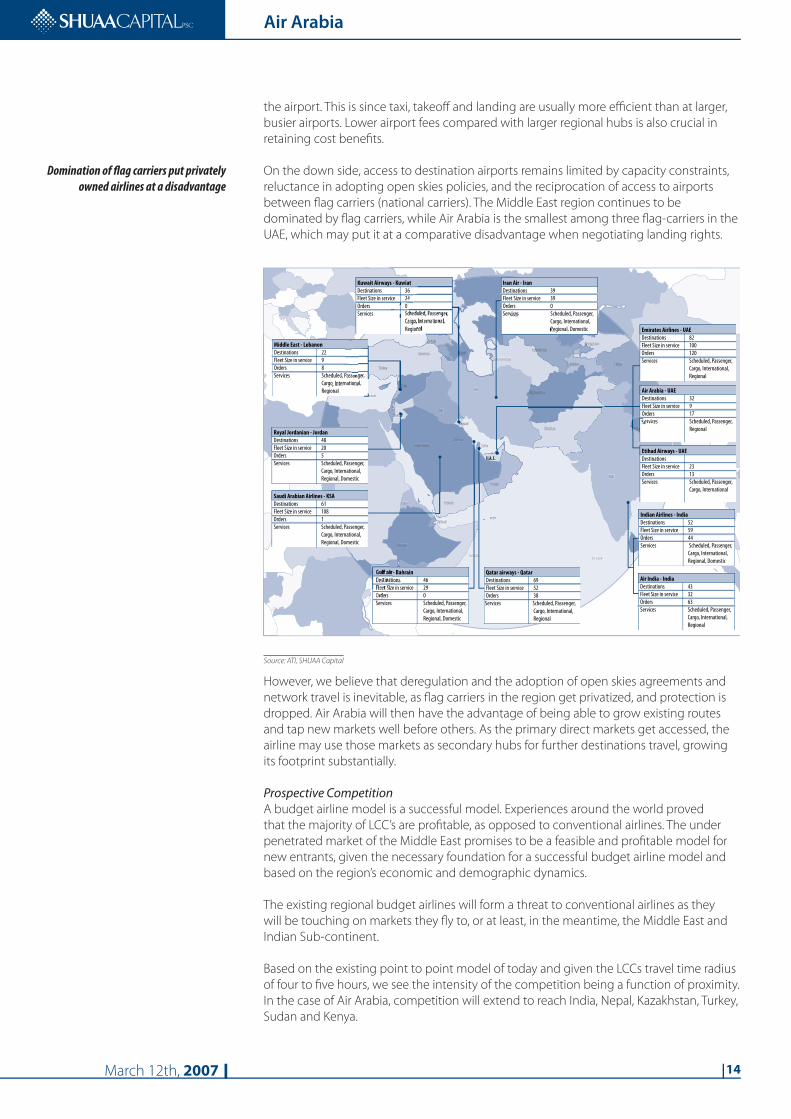

UAE, which may put it at a comparative disadvantage when negotiating landing rights.

1000 Km0

INDIAN

OCEAN

TurkmenistanT

Sudan

Sri LankaSomalia

Bahrain

Iraq

India

Ethiopia

EritreE e

Egypt

Iran

U.A.E.

Saudi Arabia

Kazakhstan

Gulf air - Bahrain

Destinations 46Fleet Size in service 29Orders 0Services Scheduled, Passenger,

Cargo, International, Regional, Domestic

Iran Air - Iran

Destinations 39Fleet Size in service 39Orders 0Services Scheduled, Passenger,

Cargo, International, Regional, Domestic

Kuwait Airways - Kuwiat

Destinations 36Fleet Size in service 24Orders 0Services Scheduled, Passenger,

Cargo, International, Regional

Middle East - Lebanon

Destinations 22Fleet Size in service 9Orders 8Services Scheduled, Passenger,

Cargo, International, Regional

Qatar airways - Qatar

Destinations 69Fleet Size in service 52Orders 38Services Scheduled, Passenger,

Cargo, International, Regional

Indian Airlines - India

Destinations 52Fleet Size in service 59Orders 44Services Scheduled, Passenger,

Cargo, International, Regional, Domestic

Air India - India

Destinations 43Fleet Size in service 32Orders 63Services Scheduled, Passenger,

Cargo, International, Regional

Royal Jordanian - Jordan

Destinations 48Fleet Size in service 20Orders 5Services Scheduled, Passenger,

Cargo, International, Regional, Domestic

Saudi Arabian Airlines - KSA

Destinations 61Fleet Size in service 108Orders 1Services Scheduled, Passenger,

Cargo, International, Regional, Domestic

Air Arabia - UAE

Destinations 32Fleet Size in service 9Orders 17Services Scheduled, Passenger,

Regional

Emirates Airlines - UAE

Destinations 82Fleet Size in service 100Orders 120Services Scheduled, Passenger,

Cargo, International, Regional

Etihad Airways - UAE

Destinations Fleet Size in service 23Orders 13Services Scheduled, Passenger,

Cargo, International

Source: ATI, SHUAA Capital

However, we believe that deregulation and the adoption of open skies agreements and

network travel is inevitable, as flag carriers in the region get privatized, and protection is

dropped. Air Arabia will then have the advantage of being able to grow existing routes

and tap new markets well before others. As the primary direct markets get accessed, the

airline may use those markets as secondary hubs for further destinations travel, growing

its footprint substantially.

Prospective CompetitionA budget airline model is a successful model. Experiences around the world proved

that the majority of LCC’s are profitable, as opposed to conventional airlines. The under

penetrated market of the Middle East promises to be a feasible and profitable model for

new entrants, given the necessary foundation for a successful budget airline model and

based on the region’s economic and demographic dynamics.

The existing regional budget airlines will form a threat to conventional airlines as they

will be touching on markets they fly to, or at least, in the meantime, the Middle East and

Indian Sub-continent.

Based on the existing point to point model of today and given the LCCs travel time radius

of four to five hours, we see the intensity of the competition being a function of proximity.

In the case of Air Arabia, competition will extend to reach India, Nepal, Kazakhstan, Turkey,

Sudan and Kenya.

Domination of flag carriers put privately owned airlines at a disadvantage

Equities research

March 12th, 2007 15

Air Arabia

The Middle East already has three operational LCC’s in the UAE, Saudi Arabia (domestic

carrier) and Kuwait, as well as other airlines currently being set up. However, we expect

that others will be announcing their setup in the very near future. The Saudi Arabian

General Authority of Civil Aviation is already evaluating domestic travel demands and is

willing to provide private air carriers with licenses if deemed necessary.

A brief overview of a few regional budget carriers other than Air Arabia: Al Jazeera Airways was formed in Kuwait in November 2004 following the placement

of 70% its share capital. Operations started in 2005 with services from Kuwait to Dubai.

Towards the end of 2006, Al Jazeera was operating a fleet of four Airbus A320 aircraft

on scheduled services to 15 destinations, namely Assiut, El Nouzha, Luxor, and Sharm

El Sheikh in Egypt; Cochin, Mumbai/Bombay and Delhi in India; and Aleppo, Bahrain,

Damascus, Kuwait, Amman, Beirut, Dubai and Mashad in the Middle East.

A fifth A320 aircraft joined the Al Jazeera fleet in January 2007, and a sixth is due before

the end of the year, while four others are expected to be delivered by 2010. In February

2007, Al Jazeera introduced operations from a second hub, becoming the first low cost

carrier to operate from Dubai International Airport. Initial services will link Dubai with

Bahrain. Six further routes from Dubai to Kuwait, Mumbai, Kochi, New Delhi, Muscat and

Salalah will be introduced on 27 March 2007.

RAK Airways, a start-up LCC in the northernmost emirate of the UAE, is planning to

launch during this year and plans to cater for flights to the GCC, Levant, Europe, Africa

and Indian Sub-continent. RAK Airways was established through a royal decree and will

launch with authorized capital of AED 1.5 bn of which AED 850 mn paid up capital. The

airline currently owns 1 Boeing 757 aircraft and announced plans to place an order for 15

passenger aircraft from Airbus or Boeing.

In Saudi Arabia, National Air Services (NAS), the only licensed private aircraft operator

in the Kingdom, announced its plans to launch a low-cost carrier in the country. Saudi

National Air Services (SNAS) currently operates scheduled and non-scheduled cargo

services throughout the Middle East on behalf of DHL Express, serving all major regional

cities. It is expected to commence with its low cost passenger business in 2007 with four

Airbus A320 aircraft.

Sama Airlines is currently operating a Boeing 737-300 between Saudi Arabian cities. It

is planning to widen its operations to service Intra Middle Eastern routes with 2 or 3

additional Boeing aircrafts that will be joining its current fleet by 2008. The airline was

established by the Saudi company, Investment Enterprises, and will be operationally

assisted by UK advisory firm Mango Aviation Partners. Sama is one of 6 companies

pursuing national carrier licenses from the Saudi Arabia’s General Authority for Civil

Aviation (GACA).

In India, Air Deccan, Air India Express, Go Air, IndiGo Airlines, Paramount Airways and

SpiceJet, make up the 6 existing LCC’s to date. Pakistan has a single operating LCC, Aero

Asia International. If we adopt the view that LCC’s travel radius is around 4 to 5 hours,

then the Indian and Pakistani LCC’s will compete with Air Arabia on regions east of UAE.

Competition might be on routes to Iran, Qatar, Oman, Pakistan, Afghanistan, Kazakhstan

and Sri Lanka.

Indian LCC’s will primarily compete domestically and with Asian airlines on destinations

like China, Malaysia, Indonesia and other South East Asian countries that have significant

potential passenger traffic and above average business growth potentials. On this basis,

we believe that Indian LCC’s are targeting a different niche than Air Arabia is, and that it is

therefore not to be considered as a high threat.

Few operational Middle Eastern LLCs, but competition is expected to increase

Al Jazeera currently operates 5 aircrafts servicing 15 destinations

RAK to start operations in 2007 with 1 aircraft but expected to purchase

an additional 15 aircrafts

Sama Airlines is operating 1 aircraft between Saudi Arabia cities

Equities research

March 12th, 2007 16

Air Arabia

Should open skies agreements and network airlines be implemented, thus allowing

Indian carriers to land in the UAE and fly from the UAE to other destinations, then Indian

LCCs may cause a threat to Air Arabia.

Airline Country Established Base Fleet Destinations

Air Deccan India 2003 Bangalore 29 57

Air India Express India 2005 Cochin 7 11

Spice Jet India 2005 New Dehli 6 11

GoAir India 2004 Mumbai 3 12

Indigo Airlines India 2006 Dehli 3 11

Paramount Airways India 2005 Chennai 2 6

Air Arabia UAE 2003 Sharjah 8 32

Al Jazeera Airways Kuwait 2005 Kuwait 4 7

Source: Companies websites

Uses of raised capital

Given the above average growth potential in the budget airline business, and the fact

that the Middle East remains a virgin market for budget airlines, Air Arabia aims to be the

first carrier to penetrate this market and to acquire substantial market share by increasing

its fleet, increasing the frequency of its flights on existing routes, as well as introducing

new, potentially lucrative routes as the industry in the region deregulates, and the

transportation infrastructure develops.

The company has decided to raise its capital by AED 2.6 billion through an initial public

offering to reach AED 4.67 billion, in order to fund the increase its fleet from the current 9

leased aircrafts to 34 owned and leased aircrafts within the next ten years, and to finance

other capital expenditure directed at the purchase of engines and other fixed assets.

As per our estimates, the capital expenditure financing will be 80 pct debt versus 20 pct

equity.

Proceeds from the IPO are to be used in the fleet expansion plan

and to establish secondary hubs to widen the destination routes

Equities research

March 12th, 2007 17

Air Arabia

Industry Overview

A budget airline or a low cost carrier is an airline that generally charges a low fare in

comparison with conventional passenger carriers. This concept originated in the US and

soon afterwards moved to Europe and Asia, before finally penetrating the Middle East in

2003, when Air Arabia made its debut.

The typical low cost carrier business model is characterized by the practices that enable

LCC’s to cost cuts vis-à-vis conventional carriers. Those characteristics are typically as

follows:

Single passenger class

Single type of airplane (commonly the Airbus A320 or Boeing 737), reducing

training and servicing costs.

Simple fare scheme (typically fares increase as the plane fills up, which rewards

early reservations)

Unreserved seating (encouraging passengers to board early and quickly)

Flying to cheaper, less congested secondary airports and flying early in the

morning or late in the evening to avoid air traffic delays and take advantage of

lower landing fees

Short flights and fast turnaround times (allowing maximum utilization of air-

craft)

Simplified routes, emphasizing point-to-point traffic instead of transfers at hubs

(again enhancing aircraft utilization)

Eliminating disruption due to delayed passengers or luggage missing due to

connecting flights

Emphasis on direct sales of tickets, especially over the Internet (avoiding fees

and commissions paid to travel agents and Computer Reservations Systems)

Encouraged use and issuance of the electronic ticket

Employees working in multiple roles, for instance flight attendants also cleaning

the aircraft or working as gate agents (limiting personnel costs)

"Free" in-flight catering and other "complimentary" services are eliminated, and

replaced by optional paid-for in-flight food and drink (which represent an ad-

ditional profit source for the airline).

Aggressive fuel hedging programs.

"Unbundling" of ancillary charges (showing airport fees, taxes as separate

charges rather than as part of the advertised fare) to make the "headline fare"

appear lower.

These characteristics are heavily geared towards cutting unnecessary costs

related to labor, aircraft and fuel, infrastructure, distribution and seat density

adjustments.

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

LCCs characterized by:

Equities research

March 12th, 2007 18

Air Arabia

The charts below are examples of the American, European model and the Middle East

cost saving structure models.

Source: IATA, Emirates Airlines, Air Arabia, SHUAA Capital

In the American model, a low cost carrier saves around 40% on costs versus a

conventional carrier, while the European LCC saves around 67.8% on their costs. However,

cost differences today are less than they were in 2004, as conventional carriers started to

cut some costs in order to maximize profits and to regain market share lost to LCCs.

The trend is that as the number of regional LCC’s increase and force tighter profit

margins across the entire industry, cost cuts and lower prices no longer become a

competing factor, but more of the norm. Competition therefore tends to shift towards the

differentiation of products or services. This is reflected in the difference between US and

European markets’ cost-cutting, which is lower in the US (40%) than in Europe (67.8%).

That is because the US market is more saturated than the European one.

As for the Middle Eastern model, we decided to compare Air Arabia, the first LCC in the

region, to Emirates Airlines, the UAE’s largest conventional carrier, and a highly efficient

and profitable one at that. The chart above suggests that the cost saving is approximately

50.4%

As we mentioned earlier, the cost advantage is maintained through the efficiency of

costing and other factors that affect the industry as a whole. These factors contribute to

the growth of LCC model and are vital when considering entry into an under-penetrated

and untapped market such as the Middle East.

Cost gap European model as at year 2004

11.8

0.51.5

2.3

2.6

1.1

3.8

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

Ne

two

rk

Air

line

Lab

ou

r

Air

cra

ft a

nd

fue

l

Infr

ast

ruc

ture

Pro

du

ct

dis

trib

uti

on

ove

rhe

ad

Se

at

de

nsi

ty

ad

just

me

nt

Rya

na

ir L

CC

Eu

rop

ea

n

Mo

de

l

Eu

ro c

en

ts p

er

AS

K

67.8%

Cost gap for US Model as at year 2004

7

0.20.7

0.41.1

0.4

4.2

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

Ne

two

rkA

irlin

e

Lab

ou

r

Air

cra

ft a

nd

fue

l

Infr

ast

ruc

ture

Pro

du

ct

dis

trib

uti

on

ove

rhe

ad

Se

at

de

nsi

tya

dju

stm

en

t

So

uth

we

stLC

C U

SM

od

el

US

ce

nts

pe

r A

SK

40%

Cost gap UAE model as at year 2005

24.41

2.462.27

2.02

12.11

1.381.151.280.67

1.07

0.00

5.00

10.00

15.00

20.00

25.00

30.00

Em

ira

tes

Air

line

s

Fue

l an

d O

il

Em

plo

yee

Air

cra

ft

op

era

tin

g

Sa

les

an

d

Ma

rke

tin

g

Ha

nd

ling

Ca

teri

ng

De

pre

cia

tio

n

Oth

er

Air

Ara

bia

AE

D c

en

t p

er

AS

K

50.4%

Cost gap European model as at year 2004

11.8

0.51.5

2.3

2.6

1.1

3.8

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

Ne

two

rk

Air

line

Lab

ou

r

Air

cra

ft a

nd

fue

l

Infr

ast

ruc

ture

Pro

du

ct

dis

trib

uti

on

ove

rhe

ad

Se

at

de

nsi

ty

ad

just

me

nt

Rya

na

ir L

CC

Eu

rop

ea

n

Mo

de

l

Eu

ro c

en

ts p

er

AS

K

67.8%

Cost gap for US Model as at year 2004

7

0.20.7

0.41.1

0.4

4.2

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

Ne

two

rkA

irlin

e

Lab

ou

r

Air

cra

ft a

nd

fue

l

Infr

ast

ruc

ture

Pro

du

ct

dis

trib

uti

on

ove

rhe

ad

Se

at

de

nsi

tya

dju

stm

en

t

So

uth

we

stLC

C U

SM

od

el

US

ce

nts

pe

r A

SK

40%

Cost gap UAE model as at year 2005

24.41

2.462.27

2.02

12.11

1.381.151.280.67

1.07

0.00

5.00

10.00

15.00

20.00

25.00

30.00

Em

ira

tes

Air

line

s

Fue

l an

d O

il

Em

plo

yee

Air

cra

ft

op

era

tin

g

Sa

les

an

d

Ma

rke

tin

g

Ha

nd

ling

Ca

teri

ng

De

pre

cia

tio

n

Oth

er

Air

Ara

bia

AE

D c

en

t p

er

AS

K

50.4%

LCCs cost saving is significant even as market penetration rates increase

Equities research

March 12th, 2007 19

Air Arabia

Regional drivers

Demand for transportation services in the Middle East, and in particular air transportation,

has shown substantial growth in recent years. Passenger traffic in the Middle East has

increased by a CAGR of 9% over the past five years, compared to average global growth of

5% over the same period. The primary drivers of this growth include:

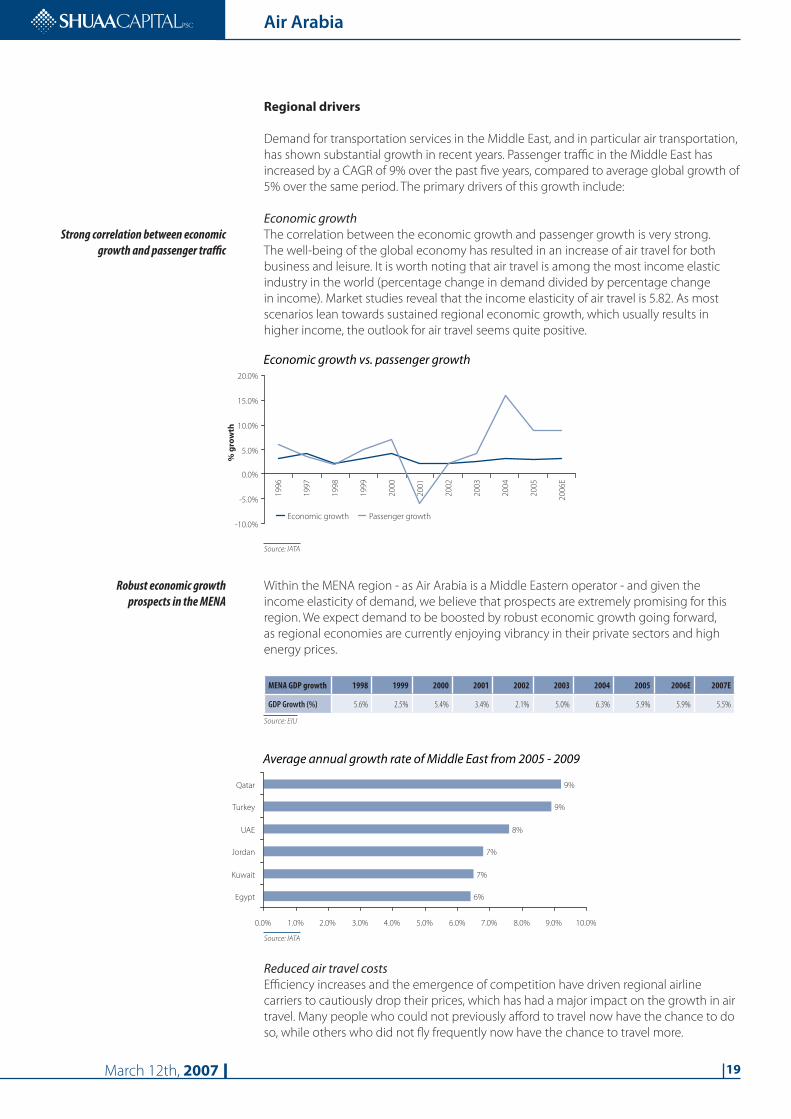

Economic growthThe correlation between the economic growth and passenger growth is very strong.

The well-being of the global economy has resulted in an increase of air travel for both

business and leisure. It is worth noting that air travel is among the most income elastic

industry in the world (percentage change in demand divided by percentage change

in income). Market studies reveal that the income elasticity of air travel is 5.82. As most

scenarios lean towards sustained regional economic growth, which usually results in

higher income, the outlook for air travel seems quite positive.

Source: IATA

Within the MENA region - as Air Arabia is a Middle Eastern operator - and given the

income elasticity of demand, we believe that prospects are extremely promising for this

region. We expect demand to be boosted by robust economic growth going forward,

as regional economies are currently enjoying vibrancy in their private sectors and high

energy prices.

MENA GDP growth 1998 1999 2000 2001 2002 2003 2004 2005 2006E 2007E

GDP Growth (%) 5.6% 2.5% 5.4% 3.4% 2.1% 5.0% 6.3% 5.9% 5.9% 5.5%

Source: EIU

Source: IATA

Reduced air travel costsEfficiency increases and the emergence of competition have driven regional airline

carriers to cautiously drop their prices, which has had a major impact on the growth in air

travel. Many people who could not previously afford to travel now have the chance to do

so, while others who did not fly frequently now have the chance to travel more.

Economic growth vs. passenger growth

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

E

Economic growth Passenger growth

% g

row

th

Economic growth vs. passenger growth

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

E

Economic growth Passenger growth

% g

row

th

Average annual growth rate of Middle East from 2005 - 2009

6%

7%

7%

8%

9%

9%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0% 9.0% 10.0%

Egypt

Kuwait

Jordan

UAE

Turkey

Qatar

Average annual growth rate of Middle East from 2005 - 2009

6%

7%

7%

8%

9%

9%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0% 9.0% 10.0%

Egypt

Kuwait

Jordan

UAE

Turkey

Qatar

Robust economic growth prospects in the MENA

Strong correlation between economic growth and passenger traffic

Equities research

March 12th, 2007 20

Air Arabia

Given the high price elasticity of demand, LCCs in the region should enjoy even higher

growth rates than conventional airlines due to their significantly lower ticket prices. An

analysis done by IATA revealed that frequency of flying is mainly driven by lower fares.

Below is a summary of the results of IATA’s analysis.

Source: IATA

Demographics of the regionThe population of the Middle East has been growing at a CAGR of 2% since 1998 reaching

around 380 million in 2005, of which a large number of individuals, mainly the younger

population, are relocating from their home countries to the GCC. The majority of such

relocations are work-related, and the main destinations are UAE, Saudi Arabia, Kuwait and

Qatar.

Regional demographics, whether in terms of population growth or by composition, will

play an important role in shaping regional air transportation trends. The breakdown of the

population illustrates the potential market share and potential growth driver for LCCs in

the region clearly.

Source: EIU

The expatriate population of the UAE is estimated at around 80% of the country’s total

population, the highest rate of foreigners in the GCC. The majority of expatriates are

originally from neighboring countries. Most residents who originate from neighboring

countries retain strong ties with friends and family in their home countries, with some

even supporting their direct family back home. This trend in particular is clear from the

country’s gender demographics, in which males constitute over 70%.

What makes you fly more frequently

Safety on ground10%

lower fares49%

Frequent Flyer

Programs (FFP's)

10%

Safety on board13%

Other12%

Schedules6%

What makes you fly more frequently

Safety on ground10%

lower fares49%

Frequent Flyer

Programs (FFP's)

10%

Safety on board13%

Other12%

Schedules6%

300

320

340

360

380

400

420

1998 1999 2000 2001 2002 2003 2004 2005 2006E 2007E

Mil

lio

n

Sh

are

of

wo

rld

po

pu

lati

on

5.4%

5.5%

5.6%

5.7%

5.8%

5.9%

6.0%

6.1%

Population

Population growth

Share of world population (%)

300

320

340

360

380

400

420

1998 1999 2000 2001 2002 2003 2004 2005 2006E 2007E

Mil

lio

n

Sh

are

of

wo

rld

po

pu

lati

on

5.4%

5.5%

5.6%

5.7%

5.8%

5.9%

6.0%

6.1%

Population

Population growth

Share of world population (%)

80% of UAE population are expatriates from neighbouring countries therefore

driving significant VFF passenger traffic

Equities research

March 12th, 2007 21

Air Arabia

The chart below shows the breakdown of the UAE population by origin.

Source: Wikipedia

TourismRegional tourism has emerged as a key driver of air travel, on the back of increased intra-

Arab business and leisure travel, as well as cultural and religious travel. According to the

United Nations World Tourism Organization (UNWTO), the Middle East was the fastest

growing region in the world in terms of tourism arrivals between 2000 and 2005, going

from 25.2 million arrivals in 2000 to 39.7 million arrivals in 2005, implying a CAGR of 9.5%.

Regional economies have benefited strongly from this trend, which has been further

solidified by concrete economic policies geared toward increasing tourism’s share of

regional economies. Specifically, tourism is increasingly viewed by local governments as

a key sector of economic growth and as an important vehicle of economic diversification

for the region’s oil-based economies. Cities such as Dubai have made concerted efforts to

build world-class leisure and hospitality facilities. In fact, Dubai boasts the leading hotel

occupancy rate and average revenue per room in the world, and its excellent conference

facilities and free economic zones are viewed as catalysts to be emulated in other parts of

the Middle East.

Religious travel is also increasing in volumes and in scope, with more money being

spent on developing adequate infrastructure to accommodate ever-increasing number

of pilgrims from all over the world. Regional air travel has moreover proved resilient to

political instability, as exemplified by Egypt’s tourism arrivals, which have increased year-

on-year despite several incidents.

The UNWTO predicts substantial growth for the tourism sector in the region. 2005 figures

reveal that tourism grew by 11% in the Middle East and Africa region, its fastest rate in

five years. Based on these figures, the Middle East’s share of global tourism is expected to

grow to 4.4% by 2020, from 2.2% in 1995. This would make the region the fastest growing

tourist destination the world, ahead even of Asia-Pacific, which is expected to grow at

6.7% per annum over the same period. The foregoing will provide ample opportunity for

growth for the air travel industry.

Population in the UAE

South Asians50%

Arabs23%

UAE nationals19%

Others8%

Population in the UAE

South Asians50%

Arabs23%

UAE nationals19%

Others8%

Middle East is the fastest growing region in the world in terms of tourism

arrivals between 2000 and 2005

Middle East share of global tourism to increase to 4.4% by 2020

Equities research

March 12th, 2007 22

Air Arabia

The pie chart below breaks down inbound tourism to the region by purpose of visit, as

per the World Tourism Organization’s (WTO) estimates. As illustrated, travelers seeking

leisure, recreation and holidays account for the majority of the total (52%), while travelers

visiting friends and family follow with a 24% share of the total number of travelers.

Source: World Tourism Organization