Embed Size (px)

Citation preview

RUSSIA > OIL & GAS

JUNE 18, 2014

1

Copyright © 2003-2014. Gazprombank (Open Joint-Stock Company)

Research Department

INDUSTRY UPDATE Analysts:

Alexander Nazarov [email protected]

Ivan Khromushin [email protected]

Alexey Dorokhov [email protected]

Ekaterina Zinovyeva [email protected]

Yury Tulinov, CFA [email protected]

Erik DePoy

Russian Oil and Gas Basic industry overview

Russian oil and gas industry handbook. In this report we provide a basic

description of the Russian oil and gas industry, including profiles of major

companies, and discuss the sector’s role in the Russian and global economy as

well as the main trends.

Russia is the world’s largest hydrocarbon producer, producing 15% of

total hydrocarbons. Russia produces 12.8% of global oil and 17.6% of global

gas, making the country the world’s top oil and gas producer on a combined

basis. In 2013, Russia produced 10.5 mln bpd of oil, ranking second in terms of

global production after Saudi Arabia. In 2013, Russia also produced 684 bcm of

gas, making it the world’s second-largest gas producer after the US.

Oil and gas industry – the most important for Russia’s economy. Russia’s

significant weight in the global economy has historically been underpinned by

the country’s strong oil and gas sector. As of 2013, the sector accounted for

28% of Russia’s GDP, 67% of the country’s exports and 56% of total revenues

of the federal budget.

Eastern focus, strengthening ties with China. Asian markets have become a

strategic focus of export diversification, with the fastest progress achieved in

relations with China. Russian-Chinese cooperation boomed in 2013, including large-

scale export contracts (Rosneft’s contract with CNPC, preliminary agreements with

Sinopec), JVs, and Chinese companies buying stakes in Russian projects

(Sinopec’s purchase of a 20% stake in NOVATEK’s Yamal-LNG). In May 2014,

Gazprom signed a $400 bln, 30-year gas export contract to China for annual

deliveries of 38 bcm of gas, which may boost its non-CIS gas exports by almost

25% starting from 2019, and announced plans to renew negotiations on a further

increase of gas exports to China using the Western route.

Oil and gas accounts for 50% of the Russian equity market and 22% of the

bond market. The oil and gas sector accounts for 50% (oil – 33%, gas – 17%) of

the Russian equity market’s capitalization, with weekly turnover in oil and gas

equities averaging $1.0-1.5 bln per day (~50% is outside Russia, 38% on

Moscow Exchange, 11% OTC). In the Eurobond corporate universe, oil and gas

issues comprise 31% of the total amount outstanding, with a bigger input only

from the financial sector (44%). Among local non-government bonds, 11% of

the amount outstanding is attributed to oil and gas issues.

Largest Russian oil and gas companies – low leverage, cheap valuation,

high dividend yields. Russian oil and gas companies trade with significant

discounts to international DM and EM peers, have low leverage, stable or even

growing outlooks, and offer good dividend yields. We highlight excellent

investment opportunities with good returns in both equity and fixed income

instruments.

Our top picks include Lukoil among the blue chips, and dividend names such as

the preferred shares of SurgutNG, Bashneft and Tatneft.

Russian oil and gas production

Source: CDU TEK, Gazprombank estimates

Russia’s share in global hydrocarbons production, 2013

Source: CDU TEK, BP

Russian oil and gas sector valuation*

* hereafter as of June 16, 2014

Source: Bloomberg, Gazprombank estimates

10.4

10.5 10.5 10.5

672

684

691 691

660

670

680

690

700

10.2

10.3

10.4

10.5

10.6

10.7

2012 2013 2014E 2015E

Oil (LHS) Gas (RHS)

mln bpd bcm

Russia 8.1 bln boe

15%

Others 44.6 bln boe

85%

Bashneft

Gazprom neft

Lukoil

Rosneft

Tatneft

Gazprom

Novatek

EM

DM

2х

4х

6х

8х

10х

12х

14х

1х 3х 5х 7х 9х

P/E

15

EV/EBITDA 15

RUSSIA > OIL & GAS

JUNE 18, 2014

2

CONTENTS

Russian economy and oil and gas sector ...................................................................................................... 3

Macroeconomics ..............................................................................................................................................................................................................3

Sino-Russian cooperation ............................................................................................................................................................................................3

Oil and gas prices .................................................................................................................................................. 5

Oil prices .............................................................................................................................................................................................................................5

Gas prices ............................................................................................................................................................................................................................6

Russian oil and gas sector main facts ............................................................................................................ 8

Industry overview ...........................................................................................................................................................................................................8

Russian oil and gas: main players ......................................................................................................................................................................... 10

Industry trends.............................................................................................................................................................................................................. 11

Regulations ..................................................................................................................................................................................................................... 14

Unconventional oil and gas ...................................................................................................................................................................................... 15

Cooperation with China ................................................................................................................................... 17

Asia-Pacific and China: the most promising oil markets ............................................................................................................................ 17

Rosneft: the most Asia-oriented Russian oil major ....................................................................................................................................... 17

Gazprom Eastern gas program ............................................................................................................................................................................... 18

Lukoil ................................................................................................................................................................................................................................. 18

Gazprom Neft ................................................................................................................................................................................................................. 18

Corporate profiles ............................................................................................................................................. 19

Gazprom ........................................................................................................................................................................................................................... 19

NOVATEK ......................................................................................................................................................................................................................... 21

Rosneft .............................................................................................................................................................................................................................. 23

Lukoil ................................................................................................................................................................................................................................. 25

Gazprom Neft ................................................................................................................................................................................................................. 27

Bashneft ............................................................................................................................................................................................................................ 29

Surgutneftegas ............................................................................................................................................................................................................... 31

Tatneft ............................................................................................................................................................................................................................... 33

SIBUR ................................................................................................................................................................................................................................. 35

Oil and gas sector on financial markets ..................................................................................................... 37

Equity markets .............................................................................................................................................................................................................. 37

Appendix ............................................................................................................................................................... 41

RUSSIA > OIL & GAS

JUNE 18, 2014

3

RUSSIAN ECONOMY AND OIL AND GAS SECTOR

Macroeconomics

At present, Russia enjoys steady positions among the world’s largest economies.

According to the IMF and WTO, as of 2013 Russia ranked eighth globally in terms of

nominal GDP ($2.1 trln), sixth in nominal GDP based on PPP valuation ($2.6 trln) and

thirteenth in external trade turnover ($868 bln).

Russia’s significant weight in the global economy has historically been underpinned by the

country’s strong oil and gas sector. According to GPB estimates, as of 2013 the sector

contributed 28% to Russia’s GDP, 67% to the country’s exports and 56% to total revenues of

the federal budget.

Unsurprisingly, Russia’s key macro gauges exhibit high sensitivity to the level of oil

prices. For example, according to GPB estimates, for 2014 a decrease of the year-

average Urals price from $110/bbl to $100/bbl would prompt a 0.3-0.7 pps

deceleration of the country’s real GDP growth, a 3.0-3.2 pps decrease in the volume

of investment and a 1.1-1.2 pps deterioration of the federal budget surplus (as a

percentage of GDP). That said, we do not see significant downside risks for our

average Brent oil price forecast for this year ($108/bbl).

It is also important to note that given the relative stabilization of both selling prices and

production volumes, the oil and gas sector has not been the driving force of the Russian

economy in recent years. As such, over 2013 the contribution of minerals extraction to

Russia’s real GDP growth (+1.3%) totaled just 0.1 pps.

Sino-Russian cooperation

Asian markets have become a strategic focus of export diversification for many Russian

companies, with the fastest progress achieved in relations with China. Imports from

China have also been flourishing on the back of increasing private sector consumption.

In general, over the past five years Russia’s trade turnover with China has expanded by

2.3x times, demonstrating a spectacular 5Y CAGR of 18%.

In 2013, China contributed 10% of Russia’s consolidated imports and exports, lagging

behind the EU’s figure of 48%. However, this figure has potential for further growth –

according to Russian and Chinese government officials, trade turnover between the two

countries could reach $100 bln in 2015 (vs. $89 bln in 2013) and may double over the

next five years, to $200 bln in 2020.

One should not be misled by the stagnation of Sino-Russian trade volumes in 2013

totaling $89.2 bln (vs. $88.2 bln in 2012), as this was primarily caused by plunging

volumes of Russian exports to China (-10.2% YoY). This is likely to reverse in view of

the recent hydrocarbon deals agreed between the two countries.

Direct investment flows also provide evidence of strengthening economic ties between

the two countries. Direct investment by Chinese companies in Russia has more than

doubled since 2009, to $374 mln in 9M13. Russia’s direct investment in China has been

relatively small of late (in our view, mainly due to China’s limitations on capital flows

from abroad), but we highlight a tripling of the figure YoY in 2012 to $63 mln.

On the corporate level, Sino-Russian cooperation boomed in 2013, including large-scale

export contracts, upstream and downstream JVs (Rosneft’s contract with CNPC, preliminary

agreements with Sinopec) and purchases of stakes in Russian projects by Chinese

companies (Sinopec’s purchase of a 20% stake in NOVATEK’s Yamal-LNG). In May 2014,

Gazprom signed a $400 bln 30-year gas export contract to China for deliveries of up to 38

bcm per year, which could boost its non-CIS gas exports by almost 25% starting from 2019.

Aside from oil and gas, this cooperation has extended to the utilities sector, including the

construction of Tianwan NPP by Rosatom for the Jiangsu Nuclear Power Corporation, and

potential electricity exports from the Russian Far East to China by Inter RAO.

RUSSIA > OIL & GAS

JUNE 18, 2014

4

Oil & gas sector is the key element of Russia’s economy… … but not its key driver of late

Source: State Statistics Service, Finance Ministry, Gazprombank estimates

Source: CBR

Sino-Russian trade turnover is expanding… … as are mutual direct investment flows

Source: Economy Ministry

Source: CBR

67%

56%

28%

0%

10%

20%

30%

40%

50%

60%

70%

80%

EXPORTS BUDGET REVENUES GDP

SHARE OF OIL & GAS SECTOR (2013)

-10.0%

-5.0%

0.0%

5.0%

10.0%

-5%

0%

5%

10%

15%

20%

25%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

SHARE OF MINERALS EXTRACTION IN RUSSIAN REAL GDP GROWTH, % (LHS)

RUSSIA REAL GDP GROWTH, % YOY

21.3 25.8 40.3 44.1 39.6

17.5

29.6

38.9 44.1 49.6

38.8

55.4

79.2 88.2 89.2

0

20

40

60

80

100

2009 2010 2011 2012 2013

EXPORT TO CHINA IMPORT FROM CHINA

$ bln

25.1 21.6 29.8 19.6 62.8

-49.3

231.4

336.3

125.9

449.6

-100

0

100

200

300

400

500

2008 2009 2010 2011 2012

DIRECT INVESTMENTS TO CHINA DIRECT INVESTMENTS FROM CHINA

$ bln

RUSSIA > OIL & GAS

JUNE 18, 2014

5

OIL AND GAS PRICES

Oil prices

Alongside its position as the most vital commodity for the world economy, oil also

remains one of the most liquid financial assets and its price is highly sensitive to major

trends on global financial markets.

We expect the Fed, ECB and central banks of other key OECD countries to remain

accommodative in their monetary policy, which should provide additional support to

nominal oil prices. We see the Brent price averaging $108/bbl in 2014 and remaining

above $100/bbl in the medium term, gradually rising to $121/bbl by 2020 with 2% CAGR

(mid-cycle Brent price of $110/bbl in real terms), driven by ongoing demand growth

(especially in Asia and non-OECD countries in other regions), a natural decline in oil

production from existing fields, and quite limited additional supply, with the rates of US

shale oil production being one of the key risks on the supply side in the short term.

Brent price and GPB forecast, $/bbl Global oil demand 2012-15, mln bpd

Source: Bloomberg, Gazprombank estimates

Source: IEA, EIA, OPEC, BP, Gazprombank estimates

Despite the considerably improved production outlook in non-OPEC countries,

particularly due to the expansion of shale oil projects, OPEC countries will play a key

role in the development of the global oil market in the long term.

We expect demand for non-OPEC crude, which would balance OPEC’s strength on the

oil market, to remain high, leading to higher costs of each incremental barrel required to

meet rising oil demand.

Capital and production costs of new projects on the higher end of the supply curve are

already approaching $100/bbl, thereby providing long-term support to oil price levels.

50

60

70

80

90

100

110

120

130

2006 2009 2012 2015E 2018E 2021E

85

86

87

88

82

84

86

88

90

2012 2013 2014E 2015E

mln bbl/d

RUSSIA > OIL & GAS

JUNE 18, 2014

6

Oil prices set to balance budgets of major oil and gas exporters

Source: BP, EIA, Gazprombank estimates

Long-term oil price performance, $/bbl US crude oil inventories, mln bbl

Source: Bloomberg

Source: US Department of Energy

Gas prices

Russia

Regulated gas tariffs for Russian industrial customers will be kept flat in 2014 and prices

for residential consumers are set to rise at a 30% discount to inflation rates. Still, due to

the base effect, the effective rates of regulated tariff increases would be 7.5% for

industrial consumers and 8.1% on average. The regulated prices will set the stage for

the average realization prices of independent gas producers on the domestic market.

We expect the average Gazprom realization price to Russia for 2014 to exceed

$105/mcm, with prices in different regions varying depending mainly on the distance

from key producing regions. The prices for final consumers are further increased by

VAT (18%), the cost of gas transportation by distribution networks and the commissions

of supply companies, adding $25-35/mcm to wholesale prices. The average level of

prices for final customers is $130-140/mcm.

Europe

Oil-linked prices in Europe. Gazprom sells gas to European countries on the base of

long-term contracts extending until 2025-35, with gas prices predominantly linked to the

basket of oil products with a lag of 6-9 months. The contracts envisage the mechanism

108.5 106.0 102.0 100.0 99.8

90.0 90.0 87.0 85.0

77.5 75.0

65.0 60.0

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

50

60

70

80

90

100

110

120

RU

SS

IA

IND

ON

ES

IA

ME

XIC

O

AZ

ER

BA

IJA

N

NO

RW

AY

IRA

Q

ALG

ER

IA

SA

UD

I AR

AB

IA

OM

AN

NIG

ER

IA

KU

WA

IT

QA

TA

R

VE

NE

ZU

ELA

OIL PRICE BALANCING THE BUDGET HYDROCARBON EXPORTS

$/bbl mln boe

0

20

40

60

80

100

120

140

160

2000 2002 2004 2006 2008 2010 2012 2014

BRENT BRENT YEAR AVERAGE

$/bbl

300

320

340

360

380

400

420

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2009-2014 RANGE 2014 2013

mln bbls

RUSSIA > OIL & GAS

JUNE 18, 2014

7

of price renegotiations in case of substantial changes of the situation on the gas market.

Over the past 2-3 years, Gazprom has substantially adjusted the terms of long-term

contracts for the key market of Western Europe, where the level of competition with

LNG is especially strong, introducing up to 15% of spot market indexation in its long-

term contracts. We expect the average Gazprom realization price in Europe in 2014 to

be in the range of $370-380/mcm. We expect gas prices on the markets of East

European countries to show substantial 15-20% premiums to West European markets

due to limited availability of spot gas.

We think that the oil link will retain its leading positions in volume terms in Europe at

least over the next 3-5 years.

Heightened political tension gave rise to various speculations regarding the prospects

for Gazprom’s gas transit to Europe through Ukraine, as well as potential disruption of

the company’s gas export sales to Ukraine.

Transit risk is indeed one of the largest risk factors for Gazprom. Still, we note that the

role of gas exports through Ukraine has diminished substantially following the launch of

Nord Stream at full capacity and currently the share of transit through Ukraine is below

50% of gas exports to Europe vs. over 80% in 2005-06. Moreover, almost half of current

export flow through Ukraine can be redistributed to other routes, leaving ca. 30% in the

risk zone. The impact could be further softened by Gazprom’s underground gas storage

capacity in Europe. The launch of the South Stream pipeline in 2015-16 may completely

eliminate the issue of transit risks for Gazprom.

Spot NBP prices (Europe). Due to the outflow of LNG deliveries from European

markets to premium Asian markets, we expect strong performance by European spot

prices, including NBP. We expect average NBP prices in 2014 to total $310-350/mcm,

being relatively close to Gazprom prices or exceeding them in the winter season.

The inflow of additional gas from new LNG projects at end 2015 through 2017 may exert

temporary pressure on European spot prices, although we expect the new gas to be

mostly absorbed by Asian countries. European authorities may increase their efforts to

raise the share of hub-based pricing of imported gas in Europe by strengthening

regulations and promoting hub-based gas trading.

Gas prices, 2013-14

Source: Bloomberg, Gazprom

0

100

200

300

400

500

600

700

JAN 13 APR 13 JUL 13 OCT 13 JAN 14 APR 14

HENRY HUB JAPAN LNG NBP GAZPROM

$/mcm

RUSSIA > OIL & GAS

JUNE 18, 2014

8

LNG. Prices for LNG deliveries to Asian countries declined almost 5% YoY to an

average of $589/mcm in 2013, but were still more than 50% above average European

spot prices – NBP (NBPGDAHD Index) averaged $380/mcm – and the price of long-

term Gazprom contracts ($378/mcm). Prices for LNG deliveries to Europe averaged

$379/mcm in 2013, i.e. matching the level of spot prices.

Events during 2013 showed that LNG prices are very sensitive to changes in the gas

market environment. Prices for LNG delivery to the US East Coast increased eightfold,

from $143/mcm in November 2013 to $1,160/mcm in February 2014 due to high gas

demand during the unseasonably cold winter.

Over 70% of LNG trade takes place on the basis of long-term contracts. The prices of

such contracts are mainly linked to oil prices, an oil product basket (Asia), main regional

benchmarks (NBP in Europe and Henry Hub in the US), or the combination of oil-link

and spot benchmarks.

Gas and LNG prices in 2013 LNG global netback* dynamics

Source: Bloomberg * LNG price minus shipping cost

Source: Bloomberg

RUSSIAN OIL AND GAS SECTOR MAIN FACTS

Industry overview

Russia produces 12.8% of global oil and 17.6% of global gas, making the country

the world’s top oil and gas producer on a combined basis. In 2013, Russia produced

10.5 mln bpd of oil, ranking second in terms of global production after Saudi Arabia.

In 2013, Russia also produced 684 bcm of gas, making it the world’s second-largest

gas producer after the US. In 2014, according to our base case, Russian oil and gas

production should be almost flat YoY at 10.5 mln bpd of oil and condensate and ca.

680-690 bcm of gas amid a stable oil price – the Brent price should average

$108/bbl.

In terms of reserves, Russia ranks fourth globally in terms of oil and gas reserves with

a 10% share. Russia holds reserves of 87.2 bln bbl of crude oil, ranking eighth in the

world. Russia also holds 33 tcm of gas reserves, ranking second in terms of reserves

globally after Iran. We note that these reserves do not include tight oil and gas

reserves – Russia is also one of the world’s largest holders of tight and other non-

conventional hydrocarbon resources. Russian oil and gas companies also have a

number of large-scale upstream and downstream projects throughout the world.

589

379 380

133

383

619

361 338

116

385

0

100

200

300

400

500

600

700

JAPAN LNG EUROPE LNG NBP HENRY HUB GAZPROM AV. EUROPE

2013 2012

$/mcm

180

230

280

330

380

430

480

May-10 Apr-11 Mar-12 Feb-13 Jan-14

ANNUAL NETBACK AVERAGE NETBACK

$/mcm

RUSSIA > OIL & GAS

JUNE 18, 2014

9

Russian hydrocarbon reserves share, bln boe Russian hydrocarbon production share, bln boe

Source: EIA Source: EIA

Russian oil and gas production Top holders of shale oil and gas technically recoverable resources

Source: CDU TEK, Gazprombank estimates Source: EIA

Russia 294 bln boe

10%

Others 2,552 bln boe

90%

Russia 8.1 bln boe

15%

Others 44.6 bln boe

85%

10.4

10.5 10.5 10.5

672

684

691 691

660

665

670

675

680

685

690

695

10.2

10.3

10.4

10.5

10.6

10.7

2012 2013 2014E 2015E

OIL (LHS) GAS (RHS)

mln bpd bcm

52

74

101

117

118

130

140

179

184

244

0 50 100 150 200 250 300

Brazil

South Africa

Australia

Mexico

Canada

Russia

Algeria

Argentina

US

China

OIL GAS

bln boe

RUSSIA > OIL & GAS

JUNE 18, 2014

10

Russian oil and gas: main players

Russia’s oil and gas sector is rather concentrated. The two largest gas companies

(Gazprom and NOVATEK) accounted for 77% of the country’s total gas production in

2013, while the six largest oil companies (Rosneft, Lukoil, Surgutneftegas, Gazprom

Neft, Tatneft and Bashneft) accounted for 79% of the country’s total oil production.

Gas is mainly transported through the trunk pipeline system operated by Gazprom. Oil

and oil products are transported mainly via the trunk pipeline system operated by the

state-controlled operator Transneft directly to Russian or international customers or to

export sea ports, and partially by railroad.

Russian oil companies are continually increasing refining volumes and refining quality

(in terms of light products yield) and have mostly completed the quality program

ensuring compliance with Euro-5 environmental standards. Gasoline production is

projected to reach 39.5 mln tonnes in 2015, up 3.4% compared to 2012, and is expected

to amount to 14.2% of refining volumes.

Russia’s top oil producers, 2013, mln bpd Russia’s top gas producers, 2013, bcm

Source: CDU TEK Source: EIA

Russian refining volumes, 2013, mln tonnes Russian gasoline production, 2013, mln tonnes

Source: CDU TEK, Gazprombank estimates Source: CDU TEK, Gazprombank estimates

ROSNEFT 3.9

LUKOIL 1.7

SURGUTNG 1.2

GAZPROM NEFT

0.6

TATNEFT 0.5

BASHNEFT 0.3

GAZPROM 0.3

OTHERS 1.8

ROSNEFT 41

LUKOIL 19 SURGUTNG

12

GAZPROM NEFT

13

GAZPROM 476

NOVATEK 53

OTHERS 70

266

272

275

278

256

260

264

268

272

276

280

2012 2013 2014E 2015E

mln tonnes

38.2

38.7

39.1

39.5

37

38

39

40

2012 2013 2014E 2015E

mln tonnes

RUSSIA > OIL & GAS

JUNE 18, 2014

11

Industry trends

Russian exports – EU accounts for the lion’s share of hydrocarbon exports from Russia so far – 32% of oil and 25% of gas produced

Source: Gazprombank

Capex of major Russian oil and gas companies: inflation of capex observed but there are no sharp spikes

Dividend payments of major Russian oil and gas companies – we expect a gradual increase of dividend payments

Source: company data, Gazprombank estimates Source: company data, Gazprombank estimates

CHINA

EUROPE

REST

OF THE WORLD

Oil exports 0.6 mln bpd

Gas exports 59 bcm

Oil exports 3.4 mln bpd

Gas exports 173 bcm

Oil exports 0.4 mln bpd

Gas exports 0.6 bcm OTHER

ASIA

Oil exports 0.3 mln bpd

Gas exports 14 bcm

OIL AND GAS

RUSSIA

PRODUCTION CONSUMPTION

Oil 10.5 mln bpd 5.8 mln bpd

Gas 684 bcm 436 bcm

46 46 42 46

15 18 25 25

12 15

18 18 23

26 25 24 95

104 110 114

0

20

40

60

80

100

120

2012 2013 2014E 2015E

GAZPROM ROSNEFT LUKOIL OTHERS

$ bln

6 4 5

8

2

3 3

3 3

3

3

3 5

6 5

4

16 15

16

18

0

4

8

12

16

20

2012 2013 2014E 2015E

GAZPROM ROSNEFT LUKOIL OTHERS

$ bln

RUSSIA > OIL & GAS

JUNE 18, 2014

12

Free cash flow of major Russian oil and gas companies – steady FCF generation despite capex inflation

Discretionary free cash flow of major Russian oil and gas companies – small decrease expected on the back of increased dividends

* including long-term prepayments on oil supply agreements

Source: company data, Gazprombank estimates

* including long-term prepayments on oil supply agreements

Source: company data, Gazprombank estimates

Chinese imports: Russia’s share is not large, but will grow in the near future

Source: Gazprombank

3 10 10

5 1

19 23

24

7

1

1 4

11

13 11 12

22

43 45 44

-5

5

15

25

35

45

2012 2013 2014E 2015E

GAZPROM ROSNEFT* LUKOIL OTHERS

$ bln

-3

6 4 -3

-2

16 20

20

4 -1 -2

1

6

7 6

8

5

28 28 26

-10

-5

0

5

10

15

20

25

30

35

40

2012 2013 2014E 2015E

GAZPROM ROSNEFT* LUKOIL OTHERS

$ bln

CHINA

RUSSIA

Oil imports 0.4 mln bpd

Gas imports 0.6 bcm

REST OF THE WORLD

Oil imports 2.1 mln bpd

Gas imports 6 bcm

ASIA AND MIDDLE EAST

Oil imports 3.1 mln bpd

Gas imports 35 bcm

RUSSIA > OIL & GAS

JUNE 18, 2014

13

Decent dividend yields. The oil and gas sector is one of the best dividend payers in

Russia and a decent payer compared to international majors. We expect an average

dividend yield of 6.0% for the Russian oil sector for 2013.

Large caps to yield 5-6%. The largest Russian oil and gas companies will provide

decent dividend yields for 2013, including 5.0% at Gazprom, 5.1% at Rosneft and 5.9%

at Lukoil.

Second tier to provide even larger dividends. The Russian oil and gas sector

contains unique dividend plays, including mainly preferred shares. The prefs of three

Russian oil companies in particular (Bashneft, Surgutneftegas and Tatneft) may bring

yields of 7-11% for 2013.

Russian oil and gas company final dividend yields

Source: company data, Gazprombank estimates

11.4%

8.5% 8.3%

6.6% 6.6%

5.1% 5.0% 4.5% 3.8% 3.5%

2.9% 2.8% 2.2%

1.1% 1.0%

0%

2%

4%

6%

8%

10%

12%

BA

SH

NE

FT

PR

EF

BA

SH

NE

FT

CO

M

SU

RG

UT

NG

PR

EF

NIZ

HN

EK

AM

SK

NE

FT

EK

HIM

P

RE

F

TA

TN

EF

T P

RE

F

RO

SN

EF

T

GA

ZP

RO

M

NIZ

HN

EK

AM

SK

NE

FT

EK

HIM

C

OM

TA

TN

EF

T C

OM

GA

ZP

RO

M N

EF

T

EU

RA

SIA

DR

ILLI

NG

LUK

OIL

SU

RG

UT

NG

CO

M

NO

VA

TE

K

TR

AN

SN

EF

T

RUSSIA > OIL & GAS

JUNE 18, 2014

14

Regulations

As we mentioned above, Russian oil and gas plays a crucial role for Russia’s economy

and budget income. That said, the lion’s share of revenues of Russian oil companies is

subject to taxation.

In addition to income tax (20%), the fiscal regime for Russian oil companies consists of

two major parts aside from corporate income tax: the mineral extraction tax (MET) and

export duty if crude is exported.

The MET represents a royalty payable by the producer on the volume of extracted

resources, and differs between oil and gas production. For oil, the calculation of the duty

involves some adjustments for the oil price and changes in the ruble exchange rate

against the dollar. The base MET rate for gas and gas condensate starting July 1, 2014

will be calculated as 15% of the weighted-average selling price of gas and gas

condensate on domestic and export markets.

In order to stimulate development of Arctic and East Siberia hydrocarbon resources,

certain tax breaks were adopted for production in these areas depending on the

complexity of developments in the region (with developments in the Arctic offshore, for

example, receiving the greatest relief). A special tax regime is also applied to tight oil

producers in order to intensify the development of abundant shale resources of the

Bazhenov formation.

An export duty applies to oil, gas and oil products exported from Russia. The oil export

duty is calculated according to a special formula based on the average official

Mediterranean and Rotterdam price in the previous month and then applied from the

start of the following month. Overall, the MET and export duty takes about 70% of oil

companies’ export revenue per barrel. The export duty for gas is 30% of the sale price.

Thus far there have been no special oil or gas tax breaks for supplies to China, except

for the gas (MET break may be granted) – tax breaks in Russia are mainly linked not to

sales destination, but to production region origination, with a few minor exceptions.

Domestic oil product sales are also subject to excise taxes, which account for about

20% of product prices depending on quality (Euro 4-5 to Euro 1-3)

Russia’s two main oil taxes, $/bbl

Source: Gazprombank estimates

22 23 24 26

55 53 53 53

33 31 31 31

110 108 108 110

0

20

40

60

80

100

120

2012 2013 2014E 2015E

MET Export duty Urals price

$/bbl

NETBACK

RUSSIA > OIL & GAS

JUNE 18, 2014

15

There are no official regulatory restrictions or pricing regulations on oil and oil product

exports and pricing, both externally and domestic. In gas, the export of natural gas is a

monopoly right for Gazprom (excluding LNG), while domestic gas prices for Gazprom

are regulated both for industrial and residential users. Although gas prices are not

regulated for other Russian gas producers, the regulated gas price is a benchmark, so

the actual prices do not differ much from regulated prices.

However, independent gas producers provide certain discounts on their gas sales to

industrial customers on the domestic market, which is actively used in competition with

Gazprom.

Unconventional oil and gas

The so-called shale revolution altered the very core of the US gas market, spilled over to

many other sectors in the US economy and seriously affected key regional gas markets

globally. However, we believe that its effect (decreasing US gas imports, fall in US gas

prices, declining global coal prices) has already taken its toll, while shale gas production

growth in the US has sharply decelerated and is unlikely to be followed by a similar

boom elsewhere in the foreseeable future. That said, we note the possibility of the start

of commercial production in China and Argentina.

Moreover, the shale revolution has had a rather limited direct impact on Russian

companies. In Europe, for example, Gazprom faces competition not with shale gas, but

mainly pipeline gas, LNG and coal. However, the indirect influence of the shale

revolution has been felt via the oil price.

Unconventional gas production by 2035 and its share in total gas production

Source: IEA

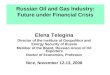

Russia is one of the largest holders of tight oil resources in the world, mostly

concentrated in the Bazhenov shale formation in Western Siberia. We consider tight oil

resources as an important source of potential support for Russian total oil production for

2016-20 and beyond, as crude output from conventional fields in Russia may start to

decline YoY.

However, further development of tight oil resources largely depends on the

government’s position in terms of the tax support regime for tight oil producers balanced

by its appetite for tax revenues to the budget. We think that further easing is required to

make shale oil production economically viable for oil companies.

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

100

200

300

400

500

600

US

A

CH

INA

CA

NA

DA

AU

ST

RA

LIA

IND

IA

RU

SS

IA

AR

GE

NT

INA

ME

XIC

O

IND

ON

ES

IA

ALG

ER

IA

EC

TIGHT GAS COALBED METHANE SHALE GAS SHARE OF UNCONVENTIONAL GAS IN TOTAL PRODUCTION

bcm

RUSSIA > OIL & GAS

JUNE 18, 2014

16

Russian major shale oil resources

Source: IHS CERA, IEA, Gazprombank

BAZHENOV

FORMATION

TIGHT OIL PRODUCTION IN RUSSIA

2013 2025E 2040E

14.8 m bpd 360m bpd 1,100 m bpd

RUSSIA > OIL & GAS

JUNE 18, 2014

17

COOPERATION WITH CHINA

Starting from 2009, Russian oil majors have increasingly looked at Asia as a strategic

market and consider it the most important vector for diversification. The launch of the

ESPO pipeline and Rosneft’s large-scale long-term crude export contracts to China made

the expansion of Russian oils to Asia a reality and laid the foundation for a further

substantial increase of hydrocarbon exports to the region as well as broader cooperation

in the energy sphere.

Asia-Pacific and China: the most promising oil markets

Asian markets are expected to remain the key centers for long-term oil demand growth in

the world. Oil demand in the Asia-Pacific region is expected to grow at double the average

rate of world oil consumption. According to IEA forecasts, China will likely account for 60%

of total oil demand growth in Asia to 2030. Thus, the Chinese market is currently one of

the most attractive options for diversification of exports of Russian oil and gas.

Currently most of China’s oil imports come from the Middle East (over 50%). Alongside

China’s further deregulation of its oil and gas market, this could create further

opportunities for other exporters.

Most Russian oil and gas companies consider Asia and specifically China as a strategic

export market, and are designing and undertaking large-scale projects aimed at export

diversification to Asia.

The long-term trend of export diversification to Asia is organically matched by the

rising share of oil production in East Siberia and intensive oil demand growth in

Asia (specifically China).

Russian crude supplies to Asia may reach 65 mln tonnes by 2020 and up to 80 mln

tonnes by 2035, with a proportional reduction of exports to Western markets.

Substantial capex needs arising from the development of Eastern projects may be

partially counterbalanced by fiscal stimulus provided by the government as well as

potential funding from Asian partners. Russian oil and gas majors primarily have

healthy borrowing capacity and apply the same profitability criteria to the Eastern

projects as to the rest of the upstream project portfolio.

Given its vast resource base in East Siberia and the Far East of Russia as well as

long-term crude export agreements with Chinese companies, Rosneft is the clear

leader in this process. Gazprom becomes the key player in the gas area with the

conclusion of a gas export contract with China. Among other Russian oil and gas

companies, Surgutneftegas, Lukoil, SIBUR, Gazprom Neft and NOVATEK will also

play a significant role in exports to Asian markets.

Developments over the past several weeks may improve the ties of Russian oil

companies to Asian partners, including an increase in the number and volume of

joint projects, and accelerated realization of key projects of Russian oil and gas

companies aimed at Asian markets.

Diversification of crude exports to Asian markets gives Russian oil companies a long-

term fundamental base to increase their value through the development of greenfields in

Eastern Siberia and the Far East, and to secure access to new export markets.

Rosneft: the most Asia-oriented Russian oil major

Rosneft is the most Asia-oriented Russian oil major and has the largest portfolio of joint

projects with Chinese NOCs. Large-scale agreements with CNPC and Sinopec clearly

show Rosneft’s commitment to rebalance the company’s export structure and increase

the role of Asian markets in its global strategy.

RUSSIA > OIL & GAS

JUNE 18, 2014

18

Oil supply. Rosneft is the leader among Russian oil companies by volume of crude

exports to China. In 2013, Rosneft exported 15 mln tonnes to China (0.3 mln bpd) and

another 8.6 mln tonnes to Asian markets through Kozmino seaport. We expect

Rosneft’s oil exports to Asian markets to ramp up quickly; in 2014 the company may

send 21-22 mln tonnes of oil to China by pipeline and increase the total amount of

exports to Asia to more than 30 mln tonnes (over 34% of its non-CIS exports).

The total volume of Rosneft’s crude oil deliveries to China (including direct deliveries by

ESPO and Kozmino, exports through Kazakhstan and additional deliveries to Tanjin

refinery starting from 2020) may rise to 60 mln tonnes (1.2 mln bpd) by 2020, and the

share of exports to Asia in Rosneft’s revenues may total up to 25%.

Gazprom Eastern gas program

In Eastern Russia, Gazprom owns an abundant resource base that is set to be used for

gasification of Eastern Siberia and the Far East as well as potential gas deliveries to

foreign markets, primarily in Asia.

Gas deliveries to China. In May 2014, Gazprom signed a $400 bln contract with CNPC

for annual delivery of 38 bcm of gas to China. The contract became the ever-largest

contract between Russia and China, organically complementing a previously signed

long-term oil delivery contract between Rosneft and CNPC. As a result of the contract,

Gazprom may take ca. 15% of the Chinese gas market by 2020 and increase the

volume of its non-CIS gas exports by almost 25%.

The implied price of the contract is ca. $360-380/mcm, on our calculations. The

agreement envisages the prepayment of $25 bln. Russia also offered to cancel the gas

MET for gas fields participating in the project, while the Chinese party agreed to reduce

the taxation of gas imported from Russia.

Key elements of the project will include the Power of Siberia pipeline, development of

the Chayanda and Kovykta gas fields, and construction of gas refining and helium

plants. There is also a probability of some participation by independent gas producers in

the project during one of its stages. According to Gazprom, the total volume of

investments in the project on Russian territory will exceed $55 bln. We expect

Gazprom’s capex to increase from $44 bln in 2013 to $46-50 bln per year in 2015-19.

Gazprom has also announced plans to renew negotiations in the near future on further

increase of gas exports to China using the Western route.

Lukoil

With the launch of West Qurna-2 in 2014, Lukoil aims to become an important player on

the Chinese oil market. The company is already delivering around 300 kt of oil via ESPO

to China and Southeast Asia per month.

At end March 2014, Lukoil launched its largest upstream project – the West Qurna-2

field in Iraq – and produced 120 kbpd at the field, while the end 2014 target stands at

400 kbpd and is set to reach peak production of around 1.2 mln bpd in 2017. Lukoil

considers Asian countries and China as key markets for its share in the project’s

production (up to 200 kbpd) and we do not exclude that the lion’s share of the Iraqi part

of the field’s output will also go directly to Asian markets.

Gazprom Neft

Gazprom Neft holds licenses for the development of several greenfields in Eastern Siberia,

including the Kuyumbinskoye and Chonskiy fields, which are expected to be launched by

2016-17. Gazprom Neft’s production from these fields may reach 9.5 mln tpa by 2020, which

will most likely be delivered to Asian markets, including China, via the ESPO pipeline.

Another potential oil field whose resources may be used for export to Asian markets is

Messoyakha located in northeast Siberia. Proved 2P reserves are 48.3 mln tonnes with

peak production of 3.5 mln tpa by 2026. Gazprom Neft is currently in the stage of

constructing infrastructure at the field.

RUSSIA > OIL & GAS

JUNE 18, 2014

19

CORPORATE PROFILES

Gazprom

Gazprom is the largest public natural gas and hydrocarbons producer in the world.

The company holds 123 bln boe of proved reserves and produces 9.5 mln bpd,

accounting for 70% of Russian and 15% of world gas production. Gas has the

dominant share in Gazprom’s reserves and production, with 91% and 87% shares,

respectively. Gazprom’s key producing assets are located in Yamalo-Nenets

Autonomous District in the North of West Siberia. The high quality of Gazprom’s

upstream assets makes it the best company among global oil and gas majors by lifting

costs and upstream capex per barrel.

Gazprom has an exclusive right to export Russian gas via its pipeline, and owns and

operates the world’s largest trunk gas pipeline network that connects its fields with Russian

and European markets, accounting for 57% of gas revenues and 32% of total revenues.

Gazprom has a well-developed oil and condensate business and is the largest electricity

producer in Russia. Liquids production accounts for 30% of Gazprom’s revenues.

Gazprom’s oil subsidiary, Gazprom Neft, is the fourth-largest oil company in Russia.

Company-specific drivers

Positive export outlook, gas exports to Europe (57% of gas revenues, 32% of

total revenues) to stay close to the record levels of 2013, gas prices to remain

broadly flat, declining 2.5% YoY in Europe in 2014.

Dividend growth. A switch to 25% IFRS dividends payouts is possible in 2015-16

and could lead to an increase in dividend distribution. Gazprom’s DPS may reach

$0.34 in 2015-16E, up more than 60% from the current level.

Long-term gas supply contract with China for 38 bcm p.a., or almost 25% of 2013

exports to Europe, including a $25 bln prepayment, providing market diversification and

boosting non-CIS gas exports by almost 25% starting from 2019.

Switch to gas MET formula on July 1 adds long-term predictability to gas taxation

and links the tax burden to average realized prices vs. fixed tax rates used previously.

Strong credit profile with one of the lowest degrees of leverage among

EM/CIS/Asian peers and significant borrowing headroom under internal

indebtedness and rating agencies limits (min. $48 bln as of end 2013).

Company-specific risks

Capex risk. Simultaneous implementation of several large-scale projects – Yamal

peninsula development, gas pipelines to Europe (Bovanenkovo-Ukhta, South

Stream, Southern corridor) and the Eastern gas program – may drive Group capex to

over $45-50 bln in 2015-17, pressuring FCF and requiring additional borrowings.

Funding needs, however, could partially be covered by long-term prepayments

totaling $25 bln agreed under the gas delivery contract to China.

Regulation. Risk of sanctions, lifting of re-export limitations, leveling of realization

prices in European countries, change in regulatory treatment of key pipeline projects.

Taxation changes. Risks of cancellation of part of export duty tax breaks (up to

3-4% of EBITDA), risk of further potential revision of gas MET formula

parameters over the next 2-3 years.

Transit risk. Gazprom transports through Ukraine ca. 50% of its gas exports to

Europe. Further non-payment for gas by Ukraine and intensification of discussion

of gas supply and transit issues may lead to a temporary interruption of transit.

Gazprom may reduce the share of Ukrainian transit to ca. 35% of European

exports. The launch of South Stream may almost fully eliminate this risk by 2016.

Gazprom shareholder structure

Source: Company, Gazprombank estimates

Gazprom key metrics

GAZPROM BBB-/Baa1/BBB

Ticker, LSE OGZD LI

Ticker MICEX GAZP RX

Current price $4.2

Target price $6.1

Upside potential 46%

Recommendation OVERWEIGHT

MCap $99 bln

EV $143 bln

2014E 2015E

P/E 3.0x 3.1x

EV/EBITDA 2.4x 2.5x

Source: Bloomberg, Gazprombank estimates

Gazprom share price performance

Source: Bloomberg

Gazprom eurobond spreads to UST

Source: Bloomberg

Others 47%

Government 50%

Treasury stock 3%

80%

90%

100%

110%

120%

JAN-14 MAR-14 MAY-14

GAZPROM MICEX

200

300

400

500

600

5/3 8/1 10/30 1/28 4/28

bps GAZPRU 37

GAZPRU 4.95 22

GAZPRU 18

RUSSIA > OIL & GAS

JUNE 18, 2014

20

Gazprom’s key gas assets

Source: company data, Gazprombank

Gazprom IFRS financials, $ mln

2012 2013 2014E 2015E 2016E

Revenues 153,411 164,989 170,449 177,290 185,822

EBITDA 54,495 65,177 59,655 56,875 57,965

EBITDA margin 35.5% 39.5% 35.0% 32.1% 31.2%

Free cash flow 3,117 10,144 9,600 5,400 3,904

Financial debt 49,406 55,056 53,290 58,881 66,792

Net debt/EBITDA 0.6x 0.5x 0.6x 0.7x 0.8x

Gas production, bcm 488 488 506 506 499

Source: company data, Gazprombank estimates

Cash flow dynamics Debt maturity profile as of end 2013

Source: company data, Gazprombank estimates Source: company data, Gazprombank estimates

RUSSIA

YNAO, YAMAL

SHTOKMAN

KAMCHATKA

GAS FIELDS

VLADIVOSTOK-LNG

PROJECT

LNG

ZAPOLYARNOE

YAMBURGSKOYE

CHAYANDINSKOYE

KOVIKTINSKOYE SAKHALIN II, III

SAKHALIN II

Power of Siberia

Balagansk

TO CHINA

Smolensk

TO EUROPE

Ukhta

Gryazovets

Saint-Petersburg

TO EUROPE

Blagoveshchensk

Torzhok

Yamal — Europe Novy Urengoy

Izhevsk

Elets

TO EUROPE

Krasnodar

TO EUROPE

TO TURKEY

Blue Stream

South Stream

Urengoi — Pomary — Uzhgorod

Nord Stream

Bovanenkovo — Ukhta

GAS PIPELINES

BOVANENKOVO

URENGOISKOYE

Moscow

KIRINSKY

BLOCK

GAS PIPELINES

UNDER CONSTRUCTION

Khabarovsk

ASTRAKHANSKOYE

(10)

(5)

0

5

(100)

(50)

0

50

100

2011 2012 2013 2014E 2015E 2016E

$ BLN $ BLN

DIVIDENDS CAPEX (INCL % CAPITALIZED)

OPERATING CF DISCRETIONARY CF (RHS)

10

7 6 5

8

3

16

0

3

6

9

12

15

18

2014 2015 2016 2017 2018 2019 2020 AND LATER

$ BLN

LOCAL BONDS LOANS EUROBONDS

RUSSIA > OIL & GAS

JUNE 18, 2014

21

NOVATEK

NOVATEK is Russia’s second-largest gas company with 2013 gas production of

approximately 62 bcm of gas and 4.8 mln tonnes of liquid hydrocarbons, mainly gas

condensate. NOVATEK’s principal operating areas are concentrated in the Yamal-

Nenets Autonomous District (YNAO) in Western Siberia. YNAO is the most significant

gas producing region in Russia, accounting for approximately 90% of Russia’s natural

gas production and approximately 17% of global gas production. NOVATEK in 2013

accounted for 8% of Russian gas production and 18% of the Russian domestic end-

customer gas market.

NOVATEK also operates the Purovsky gas condensate stabilization plant and Ust-Luga

stable gas condensate fractionation complex. NOVATEK owns 60% of Yamal LNG

(20% owned by Total, 20% by CNPC), which is an LNG project with annual capacity of

16.5 mln tonnes and scheduled to start production in 2017.

Company-specific drivers

Unique combination of growth and FCF. NOVATEK may provide a unique

combination of double-digit growth in production of hydrocarbons and significant

free cash flow (FCF) generation. Usually oil companies provide growth in FCF,

which is especially attractive for a liquid stock with MCap of about $30 bln.

Yamal-LNG – Russia‘s largest LNG plant. Yamal-LNG will be the largest

Russian and the northernmost LNG plant in the world with one of the cheapest

upstream bases among global LNG plant projects. The LNG plant, which will start

output in 2017, will be a transformative project for NOVATEK – the company may

transform from a Russian gas domestic player (currently approximately 60-70% of

NOVATEK’s revenues come from domestic gas sales) into an international

diversified oil and gas major. Notably, 75% of LNG is contracted already.

Pro-active M&A player. NOVATEK uses its FCF to expand its business both

organically and through M&A. In 2012-13 alone, NOVATEK purchased stakes in

attractive greenfields, Nortgas and SeverEnergia, which will account for at least

30% of the company’s consolidated production by 2017. As we mentioned above,

NOVATEK generates enough free cash flow to look for more M&A in the future.

LNG supplies to China and project financing with the help of China. During

the visit of President Putin to China in May 2014, NOVATEK signed a contract to

supply 3 mln tpa of LNG to CNPC. On the same day, China Development Bank

Corporation, Vnesheconombank, Gazprombank and Yamal-LNG signed a

memorandum on project financing for the Yamal-LNG project.

Company-specific risks

Regulatory risks in taxation and gas tariffs. Although starting in 2014, gas tariffs

will grow at a slower rate than inflation and the new gas MET formula will be

introduced, Russian oil and gas taxation may change to the detriment of oil and

gas companies.

Lower than expected growth. NOVATEK is the most expensive company in the

Russian oil and gas universe on multiples, but the premium is justified by growth.

Lower than expected growth may create uncertainty regarding the company’s

prospects, while the premium valuation may seem unjustified to investors.

Inflation of Yamal-LNG capex. Upward revision of Yamal-LNG capex may lead

investors to revisit the attractiveness of the project.

NOVATEK shareholder structure

Source: Company, Gazprombank estimates

NOVATEK key metrics

NOVATEK BBB-/Baa3/BBB-

Ticker, LSE NVTK LI

Ticker MICEX NVTK RX

Current price, ADR $122

Target price, ADR $185

Upside potential 52%

Recommendation OVERWEIGHT

MCap $35 bln

EV $39 bln

2014E 2015E

P/E 10.9x 9.5x

EV/EBITDA 8.7x 8.0x

Source: Bloomberg, Gazprombank estimates

NOVATEK share price performance

Source: Bloomberg

NOVATEK eurobond spreads to UST

Source: Bloomberg

Others 27%

V. Mikhelson 25%

G. Timchenko 23%

Total SA 15%

Gazprom 10%

70%

80%

90%

100%

110%

Jan-14 Mar-14 May-14

NOVATEK MICEX

100

200

300

400

500

600

5/3 8/1 10/30 1/28 4/28

bps NVTKRM 22

NVTKRM 16

RUSSIA > OIL & GAS

JUNE 18, 2014

22

NOVATEK’s key assets

Source: company data, Gazprombank

NOVATEK IFRS financials, $ mln

2012 2013 2014E 2015E 2016E

Revenues 6,790 9,370 11,438 12,747 14,650

EBITDA 3,123 3,819 4,542 4,955 5,668

EBITDA margin 46.0% 40.8% 39.7% 38.9% 38.7%

Free cash flow 1,014 718 1,944 2,565 3,046

Financial debt 4,362 5,060 3,052 2,296 1,752

Net debt/ EBITDA, x 1.2x 1.3x 0.7x 0.3x 0.04x

Hydrocarbons production, mln boe 405 439 444 482 517

Source: company data, Gazprombank estimates

Cash flow dynamics Debt maturity profile as of 1Q14

Source: company data, Gazprombank estimates Source: company data, Gazprombank estimates

RUSSIA

PUROVSK

YAMAL-LNG

CORE UPSTREAM

UST LUGA

GAS AND GAS

CONDENSATE

PRODUCTION

REFINING LNG

(2)

(1)

0

1

2

3

(4)

(2)

0

2

4

6

2011 2012 2013 2014E 2015E 2016E

$ BLN $ BLN

OPERATING CF CAPEX

DIVIDENDS DISCRETIONARY CF

0.6 0.4

1.6

0.05

0.5

0.5 0.5

0.1

0.6

0.0

0.3

0.6

0.9

1.2

1.5

1.8

1Y 1-2Y 2-3Y 3-4Y 4-5Y AFTER 5Y

$ BLN

LOCAL BONDS LOANS EUROBONDS

1.6

0.8

RUSSIA > OIL & GAS

JUNE 18, 2014

23

Rosneft

Rosneft is the largest listed crude oil producer and reserves holder in the world and the

second-largest listed company globally by hydrocarbon reserves and production volumes

after Gazprom. Most of Rosneft's activity is located in Russia with its main resource base

being Western Siberia, while Eastern Siberia is the second-largest producing region.

With oil production of 4.2 mln bpd, Rosneft's share in global oil output reaches 4.5%.

Rosneft hydrocarbon reserves (33 bln boe) and production (5.1 mln boepd) exceed

those of ExxonMobil by 31% and 22%, respectively. Rosneft has the largest greenfield

portfolio among Russian oil companies. In addition, Rosneft also has over 318 bln boe

of risked resources on the Russian sea shelf.

Rosneft is the most Asia-oriented Russian oil major and by far the largest oil exporter to

China and Asia-Pacific countries. Agreements with CNPC and the export contract

memorandum with Sinopec envisage an increase of oil exports to China from a current

0.3 to 1.0-1.2 mln bpd. In Nakhodka, Rosneft is designing Russia’s largest refining and

petrochemicals complex (0.6 mln bpd), aimed at Asia-Pacific markets.

Rosneft is also the third-largest gas producer in Russia, with its share of gas reaching

26% in reserves and 17% in production. Rosneft aims to more than double gas

production by 2020 and is seeking opportunities for LNG and pipeline gas exports from

its East Siberian and Sakhalin assets to China and Asian markets.

Rosneft is the largest refiner in Russia, with the strongest positions among Russian oils

in East Siberia and the Far East. Rosneft’s refining throughput reaches 2.0 mln bpd. The

company operates the largest retail network of over 2,700 retail stations.

Company-specific drivers

High operational efficiency. Lowest lifting costs, F&D costs and upstream capex

per barrel among Russian and global oil majors.

Attractive medium-term growth prospects. Liquid production CAGR by 2020

over 1% and hydrocarbon output CAGR of ca. 2%, which are above the broadly flat

national levels.

Extension of tax breaks for East Siberian projects, offshore projects, tax breaks

for tight oil. Tax breaks are designed to raise greenfield IRR to 16.3%.

Solid level of dividend commitments at 25% of net income under IFRS.

Advance payments by CNPC and Sinopec for long-term crude supply contracts

totaling an estimated $95 bln available for withdrawal by 2015-17.

Credit portfolio optimization. Gradual refinancing of ST debt raised for the TNK-

BP acquisition: $10.6 bln of the $24.6 bln in 2Y lines has already been repaid,

reducing the refinancing overhang in 2014-15 from $37 bln to a current $31 bln.

Company-specific risks

Capex risk. A number of capital intensive projects create risks of further capex

growth and a lack of clear project prioritization.

Further acquisitions. Market perception of the company’s further acquisitions

would depend on strategic fit, price parameters and impact on leverage.

Weaker upstream performance. Due to a combination of geologic factors and efforts

to optimize capex budgets, Rosneft may moderately reduce production targets.

Potential share overhang. The planned privatization of up to a 19.5% stake in

Rosneft’s equity for 2014-16 may create a share overhang.

Substantial increase in interest rates. The majority of Rosneft’s debt has floating

rates and is based on LIBOR, which is currently close to historic long-term lows of

around 0.25%. Growth in rates could lead to an increase in debt service expenses.

Rosneft shareholder structure

Source: company, Gazprombank estimates

Rosneft key equity metrics

ROSNEFT BBB-/Baa1/-

Ticker, LSE ROSN LI

Ticker MICEX ROSN RX

Current price $7.3

Target price $8.8

Upside potential 20%

Recommendation NEUTRAL

MCap $77 bln

EV $143 bln

2014E 2015E

P/E 5.6x 5.3x

EV/EBITDA 4.5x 4.0x

Source: Bloomberg, Gazprombank estimates

Rosneft share price performance

Source: Bloomberg

Rosneft eurobond spreads to UST

Source: Bloomberg

Others 11%

Government 69.5%

BP 19.8%

80%

90%

100%

110%

JAN-14 MAR-14 MAY-14

ROSNEFT MICEX

150

250

350

450

5/3 8/1 10/30 1/28 4/28

bps ROSNRM 22ROSNRM 17TMENRU 20

RUSSIA > OIL & GAS

JUNE 18, 2014

24

Rosneft’s key assets

Source: company data, Gazprombank

Rosneft IFRS financials, $ mln

2012 2013 2014E 2015E 2016E

Revenues 98,680 147,140 161,767 167,408 177,293

EBITDA 19,891 29,384 31,569 35,245 38,047

EBITDA margin 20.2% 20.0% 19.5% 21.1% 21.5%

Free cash flow (incl. LT prepayments) 579 18,542 23,480 23,524 16,625

Financial debt 32,628 72,474 51,296 33,452 26,131

Net debt/EBITDA 1.1x 2.2x 1.4x 0.8x 0.4x

Oil production, mln bbl 893 1,398 1,523 1,525 1,557

Source: Company, Gazprombank estimates

Cash flow dynamics Debt maturity profile as of 1Q14

Source: company, Gazprombank estimates Source: company, Gazprombank estimates

RUSSIA

PURNEFTEGAZ

VANKOR

CLUSTER

VERKHNECHONSKOYE

YUGANSKNEFTEGAZ

UVAT

SAMOTLOR

OIL PRODUCTION

ASSETS

GAS PROJECTS

ORENBURGNEFT

REFINERY

TUAPSE

SAMARA

SARATOV

RYAZAN

YANOS (50%)

TOMSKNEFT

NIZHNEVARTOVSK

KOMSOMOLSK

ACHINSKANGARSK SAKHALIN-1, 3, 5

GAS PROJECTS

TAAS-YURIAKH

YURUBCHENO-

TOKHOMSKOYE

SEVERNAYA NEFT

CAUCASUS

(14)

(7)

0

7

14

21

(40)

(20)

0

20

40

60

2011 2012 2013 2014E 2015E 2016E

$ BLN $ BLN

OPERATING CF CAPEX DIVIDENDS DISCRETIONARY CF (RHS)

13

18

8 8

25

0

5

10

15

20

25

30

2Q14-4Q14 2015 2016 2017 2018 AND LATER

$ bln

LOCAL BONDS EUROBONDS LOANS

RUSSIA > OIL & GAS

JUNE 18, 2014

25

Lukoil

Lukoil is the largest holder of oil reserves among privately owned listed oil and gas

companies and one of the largest integrated oil companies in the world. In Russia,

Lukoil is the second-largest oil company, producing 16% of the country’s oil output, and

is the largest private player in the oil industry.

Most of Lukoil’s activity is located in Russia, with its main resource base being Western

Siberia. As of end 2013, Lukoil held 13.4 bln bbl of oil reserves under SEC standards

and produced 2.2 mln boepd of hydrocarbons, of which liquids production reached a

total of 1.9 mln bpd.

Lukoil also actively participates in international projects in CIS countries and Iraq

and has substantial refining and retail assets in Europe. We expect Lukoil to market

over 0.2 mln bpd of crude from its Iraqi projects in Chinese and other Asian markets

from 2015.

Lukoil is Russia’s second-biggest company in terms of refining volumes and operates the

second-largest (after Rosneft) retail network in Russia numbering 2,400 stations.

Lukoil key managers – Vagit Alekperov and Leonid Fedun – are the company’s largest

shareholders, which reduces potential conflicts of interest with minority shareholders. In

2009, Lukoil approved a new strategy aimed at improving FCF generation and providing

higher returns to shareholders, and has increased dividends by over 100% since 2009.

Company-specific drivers

Production turnaround. After oil production dropped 7.9% in 2009-12 (-2.8%

CAGR), Lukoil achieved remarkable success in production stabilization by

implementing modern field development and drilling technologies, including a

dramatic increase of horizontal drilling. Lukoil showed 1.2% oil production growth in

2013 and is expected to reach over 4% liquids CAGR in 2013-16. Growth centers:

West Qurna-2 (Iraq), Imilorskoye field in West Siberia, Caspian, Timan-Pechora

and Urals fields.

Consistent increase in dividends with 15% targeted dividend CAGR until 2021

and expected dividend yield of 5.7% for 2013. Possible start of share buyback at

end 2014 – early 2015.

Start of capex reimbursement for West Qurna-2. The launch of the West Qurna-2

field in Iraq in 1Q14 will add over $5 bln per year to Lukoil’s EBITDA in 2014-17, as

the company would receive fast capex reimbursement through a high share in project

revenues in the initial years of production.

Strong credit profile. Lukoil’s leverage at 0.5x net debt/EBITDA is among the

lowest in the Russian oil and gas universe. Has solid borrowing headroom of

$9-10 bln under internal leverage limitations (0.2x debt/capitalization), which is

stricter than current standalone credit rating requirements.

Tax breaks for offshore fields, hard-to-recover oil. Lukoil is one of the key

beneficiaries from the tax breaks for offshore fields and hard-to-recover oil.

Company-specific risks

Capex overruns. The implementation of complex upstream and refinery

modernization projects may lead to further upward revision of capex budgets and

pressure on operating cash flow.

Acceleration of production decline at brownfields. Acceleration of production

decline rates at West Siberian brownfields may have a negative impact on the

production trend and operating cash flow.

Suboptimal capital allocation. Inefficient acquisitions. Substantial increase of

exposure to Iraq. Substantial increase in spending on risky exploration projects

outside of Russia.

Lukoil shareholders structure

Source: company data, Gazprombank estimates

Lukoil key equity metrics

LUKOIL BBB-/Baa2/BBB

Ticker, LSE LKOD LI

Ticker MICEX LKOH RX

Current price $62.0

Target price $87.7

Upside potential 41%

Recommendation OVERWEIGHT

MCap $53 bln

EV $62 bln

2014E 2015E

P/E 3.9x 3.5x

EV/EBITDA 2.8x 2.5x

Source: Bloomberg, Gazprombank estimates

Lukoil share price performance

Source: Bloomberg

Lukoil eurobond spreads to UST

Source: Bloomberg

Others 58%

V. Alekperov 21%

Treasury stock 11%

L. Fedun 10%

80%

90%

100%

110%

JAN-14 MAR-14 MAY-14

LUKOIL MICEX

150

250

350

450

5/3 8/1 10/30 1/28 4/28

bps LUKOIL 23LUKOIL 17LUKOIL 20

RUSSIA > OIL & GAS

JUNE 18, 2014

26

Lukoil’s key assets

Source: company data, Gazprombank

Lukoil US GAAP financials, $ mln

2012 2013 2014E 2015E 2016E

Revenues 139,171 141,452 138,759 146,253 157,884

EBITDA 18,872 18,564 22,068 24,788 27,334

EBITDA margin 13.6% 13.1% 15.9% 16.9% 17.3%

Free cash flow 7,350 1,492 1,030 3,866 4,086

Financial debt 6,621 10,821 11,176 10,625 10,530

Net debt/EBITDA 0.2x 0.5x 0.5x 0.4x 0.3x

Oil production, mln bbl 677 684 681 748 785

Source: company data, Gazprombank estimates

Cash flow dynamics Debt maturity profile as of 2013

Source: company data, Gazprombank estimates Source: company data, Gazprombank estimates

RUSSIA

VOLGOGRAD

REFINERY

NIZHNY

NOVGOROD

UKHTA

URAY

AND KOGALYM

PERM

CRUDE OIL

AND GAS RESERVES

NORTHERN

CASPIAN

VOLGA

URALS

TIMAN-PECHORA

BOLSHEKHETSKAYA

WESTERN SIBERIA

WEST QURNA 2

IRAQ

KAZAKHSTAN

UZBEKISTANAZERBAIJAN

(2)

0

2

4

6

(40)

(20)

0

20

40

2011 2012 2013 2014E 2015E 2016E

$ BLN $ BLN

OPERATING CF CAPEX

DIVIDENDS DISCRETIONARY CF (RHS)

1.3 1.7

0.2 0.6

3.1

3.8

0.0

1.0

2.0

3.0

4.0

5.0

2014 2015 2016 2017 2018 2019 AND LATER

$ bln

CONVERTIBLES EUROBONDS BANK LOANS

RUSSIA > OIL & GAS

JUNE 18, 2014

27

Gazprom Neft

Gazprom Neft is Russia’s fourth-largest oil company. The company’s key upstream

assets are located in West Siberia, which is the main Russian oil production province.

Gazprom Neft holds 10 bln boe of proved reserves, with hydrocarbon production

reaching 1.3 mln boepd and oil accounting for over 80% of total production volume.

Gazprom Neft has shown very impressive growth over the past six years, raising oil

production by 16% and hydrocarbons production by over 40%. Such growth is set to

continue, as the company has one of the largest greenfield portfolios among Russian

oils. Gazprom Neft aims to further increase hydrocarbons production by 54% by 2020,

and may reach the best rates of production growth CAGR among Russian oil majors

until 2020 of 6.3%.

Being a listed oil subsidiary of Gazprom, Gazprom Neft benefits from the program to

transfer several oil and condensate fields from the parent company, including the first oil

field in the Russian Arctic shelf (Prirazlomnoye), as well as from synergies in field

development, downstream and logistics.

Gazprom Neft is one of the most active players in the Russian downstream market,

operating the country’s third-largest retail network. Since 2007, the company has

boosted its refining by more than 60% and has nearly tripled its retail sales.

Company-specific drivers

Assignment of several large oil and gas condensate fields from Gazprom

(Prirazlomnoye, Dolginskoye, Orenburg, Novoport), expected to provide up to

16 mln tonnes of incremental production by 2020 (30% of the expected oil

production increase).

Effective greenfield development in the northern part of West Siberia and in

East Siberia, boosted by tax breaks. The government has made key decisions

on major tax breaks for greenfields (MET and in some cases export duty breaks),

aiming to provide at least 16.3% IRR.

Active development of the downstream business aimed at further increasing

the domestic market share in premium segments (retail sales of high-octane

gasoline, diesel, sales of jet fuel, bunker fuel, lubricants).

Attractive dividend profile. The company’s dividend policy envisages the

payment to shareholders of 25% of IFRS net income as well as the repayment of

semi-annual interim dividends.

Healthy credit and liquidity profile. As of 1Q14, net debt/EBITDA stood at 0.6x

and is expected to remain well below moderate the internal limit of 1.5x in the

foreseeable future. Additional flexibility is provided by the $5.6 bln cash cushion,

covering most of the company’s capex financing needs in 2014.

Company-specific risks

Capex. We expect capex to rise from $6.6 bln in 2013 to $10 bln in 2014 and

$8 bln in 2015 against the backdrop of continuing greenfield development. A

substantial part of Gazprom Neft’s greenfield projects is accounted using the

equity method and is not consolidated on the company’s balance sheet. The

development of complex projects in new frontier regions poses a natural risk of

capex overruns.

M&A. The company remains active on the M&A market, which incurs price risks as

well as risks of suboptimal capital allocation. Potential acquisition targets include

E&P and retail assets in Russia as well as refineries in Europe and Asian markets,

including Vietnam. In additional, payment for the Prirazlomnoye field may exceed

$3.0 bln.

Gazprom Neft shareholder structure

Source: company data, Gazprombank estimates

Gazprom Neft key equity metrics

GAZPROM NEFT BBB-/Baa2/BBB

Ticker, LSE GAZ LI

Ticker MICEX SIBN RX

Current price $4.4

MCap $21 bln

EV $29 bln

2014E 2015E

P/E 4.0x 4.0x

EV/EBITDA 3.1x 2.8x

Source: Bloomberg, Gazprombank estimates

Gazprom Neft share price performance

Source: Bloomberg

Gazprom Neft eurobond spreads to UST

Source: Bloomberg

Others 4%

Gazprom 96%

80%

90%

100%

110%

JAN-14 MAR-14 MAY-14

GAZPROM NEFT MICEX

200

300

400

500

600

5/3 8/1 10/30 1/28 4/28

bps GAZPRU 37

GAZPRU 4.95 22

GAZPRU 18

RUSSIA > OIL & GAS

JUNE 18, 2014

28

Gazprom Neft’s key assets

Source: company data, Gazprombank

Gazprom Neft IFRS financials, $ mln

2012 2013 2014E 2015E 2016E

Revenues 48,827 47,267 52,887 57,361 64,258

EBITDA 8,436 9,592 9,407 10,261 12,582

EBITDA margin 17.3% 20.3% 17.8% 17.9% 19.6%

Free cash flow 2,349 2,141 993 1,868 3,933

Financial debt 7,659 9,590 10,152 11,031 10,694

Net debt/EBITDA 0.6x 0.7x 1.0x 1.0x 0.8x