Embed Size (px)

Citation preview

Aligning Fiduciary Duties with

Pension Risk ManagementOctober 16, 2017 Mark Simons

Of Counsel, Morgan Lewis & Bockius, LLP

Russ Proctor, CFA, FSA, EADirector, Pacific Life Insurance Co.

Marty MeninDirector, Pacific Life Insurance Co.

Agenda

• Aligning Fiduciary Duties with Pension Objectives

• Working with Independent Fiduciaries and Other

Intermediaries to Manage Plan Risk

• Solutions to Manage Pension Risk

• Solutions to Help Defined Contribution Participants

Manage Longevity Risk

Fiduciary Duties for Qualified Plans

ERISA Fiduciary Duties – What You Need to Know

• ERISA’s fiduciary standards of prudence, exclusive

benefit and diversification

• Requirement to follow written plan documents

• ERISA’s conflict of interest and self-dealing

prohibited transaction rules

• Key words: Procedural prudence, 95-1, fiduciary

delegation, risk management and documentation

Working with Independent Fiduciaries and Other Intermediaries to Manage Plan Risk

Fiduciary Risk Management: Use of Independent

Fiduciaries, Advisors and Other Intermediaries

• What does it mean to “outsource” fiduciary duties?– Key words: OCIOs, outsourced named fiduciaries,

3(38) vs. 3(21) advisors

• What responsibilities remain?– Selection and monitoring

– Other responsibilities are based on specifics – contract terms are important

• What we’re seeing…

Managing Pension Risk

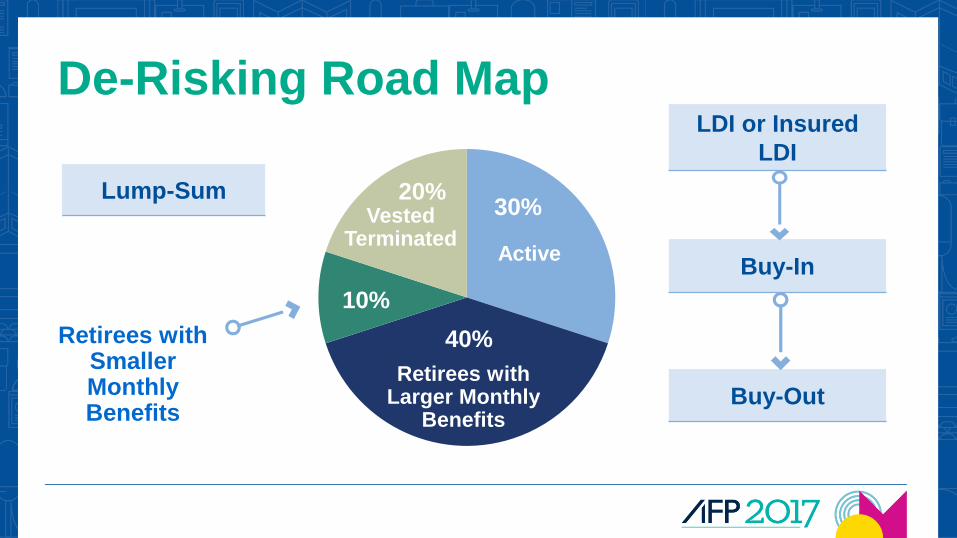

De-Risking Road Map

30%

40%

10%

20%

Active

Vested Terminated

Retirees with Larger Monthly

Benefits

Retirees with Smaller Monthly Benefits

LDI or Insured

LDI

Buy-In

Buy-Out

Lump-Sum

PRT Selection Process

• Selection of intermediaries

• Review of insurance companies (95-1)

• Final bid day

• Selection of insurance company or companies

• Transfer of participant data

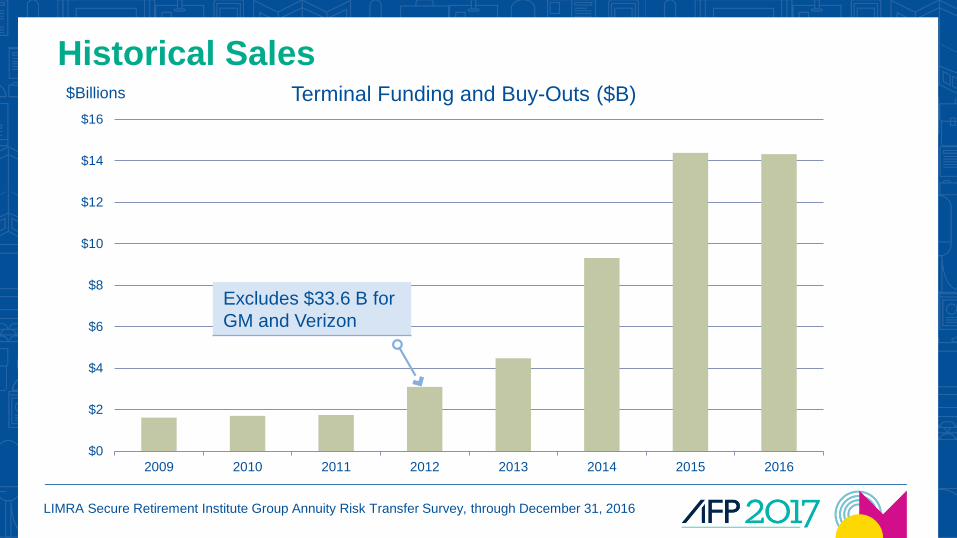

PRT – Increased Activity

Historical SalesTerminal Funding and Buy-Outs ($B)

LIMRA Secure Retirement Institute Group Annuity Risk Transfer Survey, through December 31, 2016

$0

$2

$4

$6

$8

$10

$12

$14

$16

2009 2010 2011 2012 2013 2014 2015 2016

$Billions

Excludes $33.6 B for

GM and Verizon

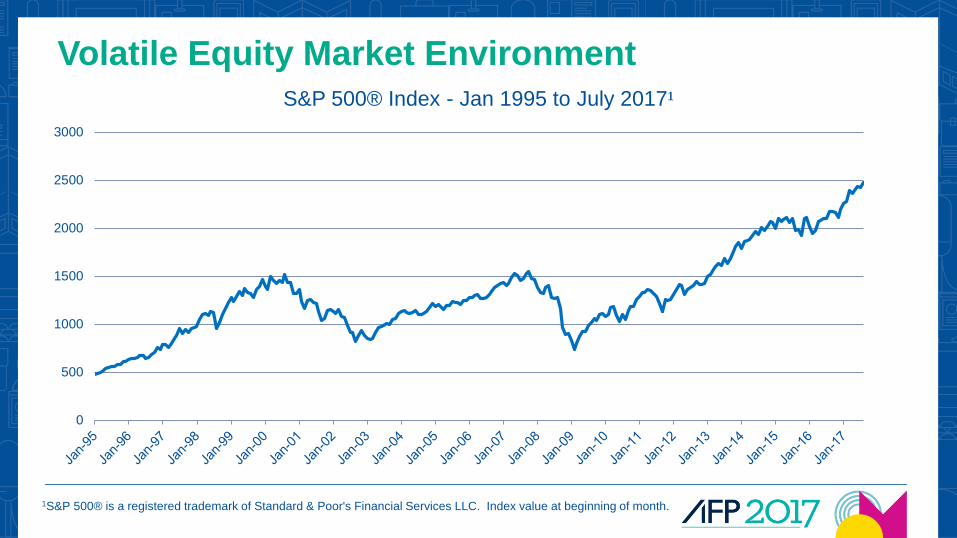

Volatile Equity Market Environment

S&P 500® Index - Jan 1995 to July 2017¹

1S&P 500® is a registered trademark of Standard & Poor's Financial Services LLC. Index value at beginning of month.

0

500

1000

1500

2000

2500

3000

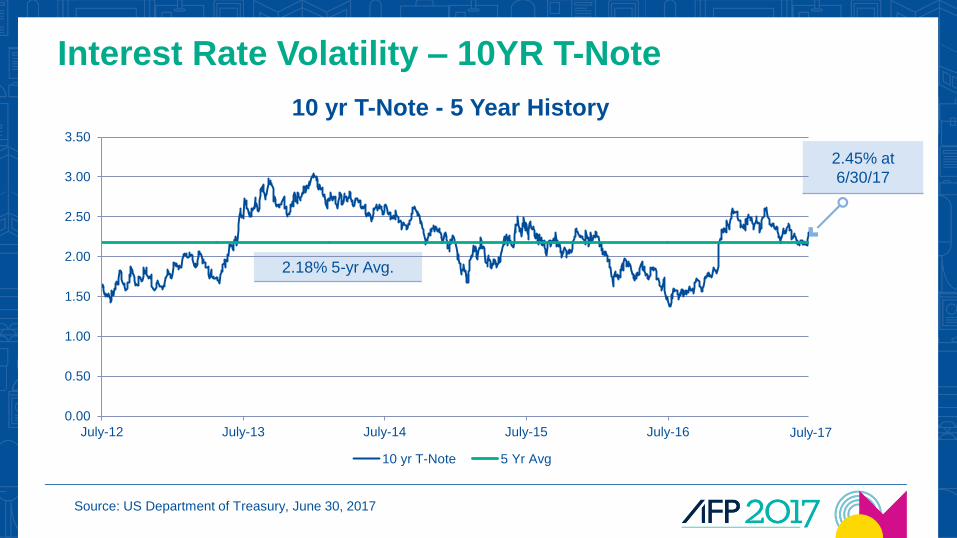

Interest Rate Volatility – 10YR T-Note

Source: US Department of Treasury, June 30, 2017

2.45% at

6/30/17

2.18% 5-yr Avg.

July-17

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

July-12 July-13 July-14 July-15 July-16

10 yr T-Note - 5 Year History

10 yr T-Note 5 Yr Avg

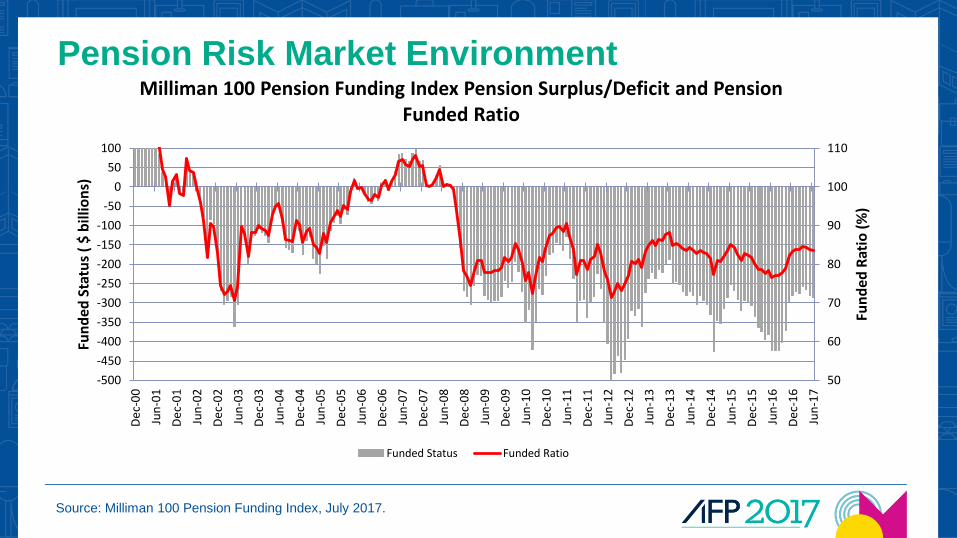

Pension Risk Market Environment

Source: Milliman 100 Pension Funding Index, July 2017.

50

60

70

80

90

100

110

-500

-450

-400

-350

-300

-250

-200

-150

-100

-50

0

50

100D

ec-

00

Jun

-01

De

c-0

1

Jun

-02

De

c-0

2

Jun

-03

De

c-0

3

Jun

-04

De

c-0

4

Jun

-05

De

c-0

5

Jun

-06

De

c-0

6

Jun

-07

De

c-0

7

Jun

-08

De

c-0

8

Jun

-09

De

c-0

9

Jun

-10

De

c-1

0

Jun

-11

De

c-1

1

Jun

-12

De

c-1

2

Jun

-13

De

c-1

3

Jun

-14

De

c-1

4

Jun

-15

De

c-1

5

Jun

-16

De

c-1

6

Jun

-17

Fun

ded

Rat

io (

%)

Fun

ded

Sta

tus

( $

bill

ion

s)Milliman 100 Pension Funding Index Pension Surplus/Deficit and Pension

Funded Ratio

Funded Status Funded Ratio

PBGC Premium Increases

Flat Rate Premium (Per Participant)

$35 $42

$49

$57 $64

$69 $74

$80

$-

$10

$20

$30

$40

$50

$60

$70

$80

$90

2012 2013 2014 2015 2016 2017 2018 2019

Premium rates, Pension Benefit Guaranty Corporation website. December 31, 2016

0.9%

1.4%

2.4%

3.0%3.4%

3.9%

4.4%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

2013 2014 2015 2016 2017 2018 2019

PBGC Premium Increases

Variable Rate Premium (Unfunded Liability)

Premium rates, Pension Benefit Guaranty Corporation website. December, 2016

Assumes 3% annual increase in National Average Wages

Buy-Out

Buy-Out: Key Features

• Can cover part or all of the plan participants

• For Covered Participant Group:– Transfers all pension obligations and risks

to insurer

– Removes the pension liability from plan sponsor’s balance sheet

– Plan sponsor no longer subject to PBGC premiums and other expenses

– Insurer provides all annuitant servicing

1. Liability for accounting based on current market discount rate for retiree liability

2. Estimated administrative expenses including actuarial fees and PBGC fixed-rate premium of $80 per person

3. Estimated investment management fees (assumes 50 bps per year)

4. Estimated cost of defaults on high-quality bond portfolio (assumes 30 bps per year)

5. This is the true economic cost if the plan sponsor retained the liability

100%5%

5%3% 113%

1. Retiree GAAP Liability 2. Admin & PBGC Expenses

3. Investment Management

4. Investment Default Risk

5. Retiree Economic Cost

Liab

ility

(C

ost

)For illustrative purposes only.

Case Study: Reducing Expense With a Buy-Out

Economic Cost of Retiree Liability (Small Benefits) with RP2014

Indirect DollarPlan Sponsor Cost

Direct DollarPlan Sponsor Cost

Plan Sponsors Adopt RP2014 Mortality

Annuity cost

may be < 105%

Buy-In

Buy-In vs. Buy-Out: What is the Difference?

• Buy-In is similar to Buy-Out except:

– Settlement accounting?

– Contract value remains an asset of the plan/trust

– Change in plan’s funded status?

– No communication required to participants

– Revocable?

• May be converted to Buy-Out

When Does a Buy-In Make Sense?

• Qualified Plans– Underfunded plan

– Unrecognized losses

– Not ready to terminate

• Nonqualified Plans– Defined benefit SERP

Buy-In Case Study #1:

Delay Recognition of Settlement Loss

• Buy-In purchased in August 2015

• Buy-In contract covered current retirees

• Converted to buy-out in April 2016

• Settlement accounting triggered in 2016 at conversion

• Loss recognized in 2016 instead of 2015

• Plan terminated in 2016

For illustrative purposes only.

Managing DC Plan Longevity Risk

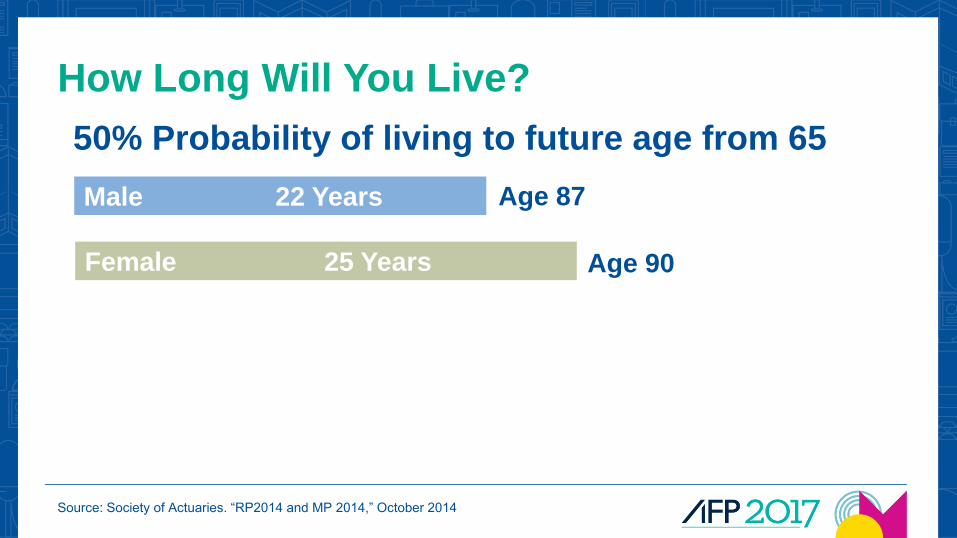

How Long Will You Live?

Male 22 Years

Female 25 Years

Age 87

Age 90

Source: Society of Actuaries. “RP2014 and MP 2014,” October 2014

50% Probability of living to future age from 65

How Long Will You Live?

Male 22 Years

Female 25 Years

Age 87

Age 90

Source: Society of Actuaries. “RP2014 and MP 2014,” October 2014

50% Probability of living to future age from 65

Last survivor of a couple 29 Years Age 94

How Long Will You Live?

Male 22 Years

Female 25 Years

Age 87

Age 90

Source: Society of Actuaries. “RP2014 and MP 2014,” October 2014

50% Probability of living to future age from 65

Last survivor of a couple 29 Years Age 94

Age 100Last survivor of a couple – 20% chance of living > 35 Years

20% Probability of living to age 100 from 65

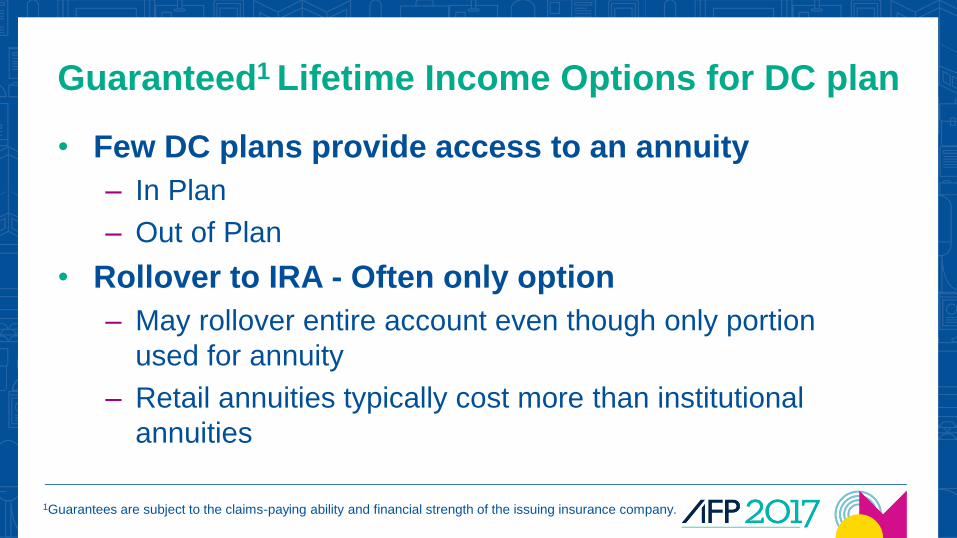

Guaranteed1 Lifetime Income Options for DC plan

• Few DC plans provide access to an annuity

– In Plan

– Out of Plan

• Rollover to IRA - Often only option

– May rollover entire account even though only portion

used for annuity

– Retail annuities typically cost more than institutional

annuities

1Guarantees are subject to the claims-paying ability and financial strength of the issuing insurance company.

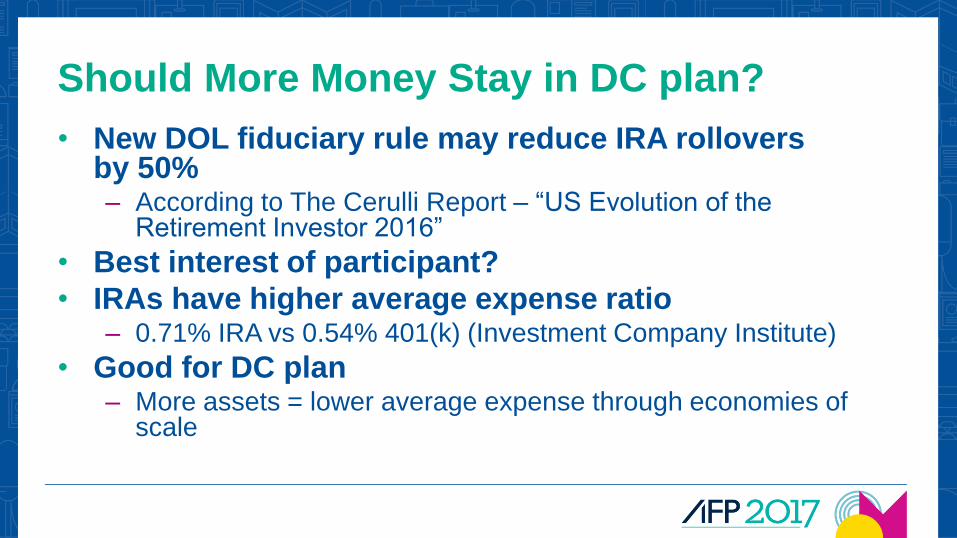

Should More Money Stay in DC plan?

• New DOL fiduciary rule may reduce IRA rollovers by 50%– According to The Cerulli Report – “US Evolution of the

Retirement Investor 2016”

• Best interest of participant?

• IRAs have higher average expense ratio– 0.71% IRA vs 0.54% 401(k) (Investment Company Institute)

• Good for DC plan– More assets = lower average expense through economies of

scale

Advantages of Guaranteed Lifetime Income

Options in DC plan

• Plan can negotiate lower or no commissions

• Receive wholesale pricing

• Retain non-annuitized assets in plan

– lower average expense for participants

Fiduciary Duties of Guaranteed Lifetime Income

Options in DC plan

• Communication

• Safety of Insurance company

• Offer more than one company?

• Administration/Coordination of quotes

• Recent Treasury and DOL guidance

• Role of outsourcing

• Portability

Questions?

Appendix

BiographiesMark Simons

Mark is of counsel in the top-ranked benefits practice of Morgan, Lewis & Bockius LLP, with 27 years of experience in advising clients on matters related to qualified and non-qualified retirement plans. In particular, Mark advises plan sponsors on matters related to fiduciary governance and regulatory compliance under Titles I and II of ERISA, and has assisted a wide variety of corporate plan sponsors and related fiduciaries in de-risking their tax-qualified defined benefit plans.

Russ Proctor, FSA, CFA, EA, MAAA

Russ joined Pacific Life in 2011 as a director in the Retirement Solutions Division. He is responsible for consulting with companies to reduce and remove financial risk inherent in their pension plans through the Pacific Life buy-out, buy-in, and insured LDI solutions. Russ also works with companies who have defined contribution plans, such as a 401(k) or 403(b) plan, to provide guaranteed lifetime income options for plan participants.

Prior to joining Pacific Life, Russ was a retirement consultant with more than 24 years of experience, most recently as a principal with Mercer Human Resource Consulting. He provided strategic retirement consulting on all aspects of pension, 401(k), and executive retirement plans. He also conducted asset-liability modeling studies for clients and co-authored several articles including one on Liability Driven Investing.

Russ holds a Bachelor of Science degree in actuarial science from Drake University. He is a Fellow of the Society of Actuaries (FSA), a Fellow of the Conference of Consulting Actuaries (FCA), an Enrolled Actuary (EA) and a Member of the American Academy of Actuaries (MAAA). He is also Chartered Financial Analyst Charterholder (CFA).

Biographies

Marty Menin

Marty joined Pacific Life in 2012 as a director in the Retirement Solutions Division. He is responsible for consulting with

companies to customize solutions that solve the financial risk inherent in their pension plans through the Pacific Life

suite of pension-risk products. Marty also works with companies who have defined contribution plans, such as 401(k)

or 403(b) plans, to provide guaranteed lifetime income options for plan participants.

Prior to joining Pacific Life, Marty held a variety of positions in the insurance and employee benefits industry for firms

such as Prudential, Mullin/TBG, Marsh & McLennan, Merrill Lynch, and MetLife.

Marty holds a Bachelor of Science degree in mathematics and economics from University of California, Los Angeles.

Pacific Life Insurance CompanyInstitutional & Structured Products

700 Newport Center DriveNewport Beach, CA 92660

(877) 536-4382, Option 1 • www.PacificLifePRT.com [email protected]

This material is not intended to be used, nor can it be used by any taxpayer, for the purpose of avoiding U.S. federal, state, or local tax penalties. This material is written to support the promotion or marketing of the transaction(s) or matter(s) addressed by this material. Pacific Life, its distributors, and respective representatives do not provide tax, accounting, or legal advice. Any taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor or attorney.

Pacific Life is a product provider. It is not a fiduciary and therefore does not give advice or make

recommendations regarding insurance or investment products. Only an advisor who is also a fiduciary is

required to advise if the product purchase and any subsequent action taken with regard to the product are in

their client’s best interest.

Insurance products are issued by Pacific Life Insurance Company in all states except New York. Product

availability and features may vary by state. Pacific Life is solely responsible for the financial obligations

accruing under the products it issues. rantees are backed by the financial strength and claims-paying ability

of the issuing insurance company.