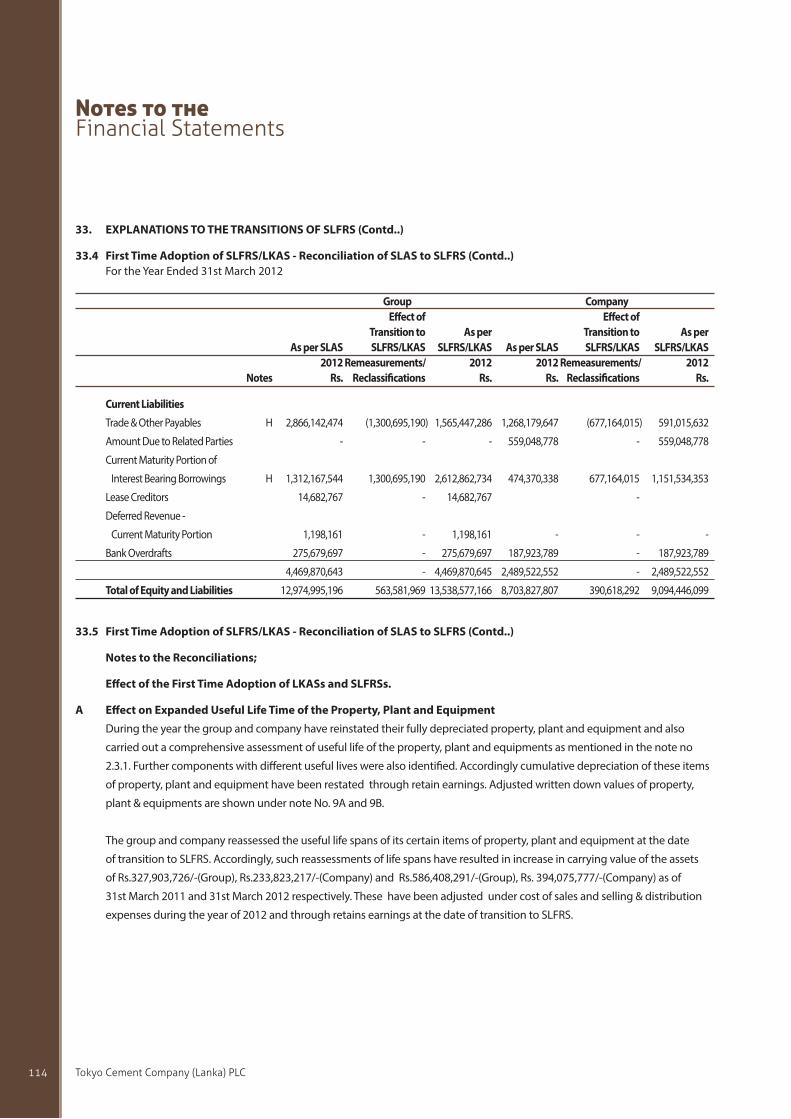

Embed Size (px)

Citation preview

aliveAnnual Report 2012/13

We are the embodiment of strength and stability In an uncertain world we are certainty.

We materialise dreams into concrete detail,sensation and sentiment into solid reality.

We build the future in harmony with nature, and people. We are the living reality, of strength and sustainability.

Tokyo Cement SOLID BUT alive.

Tokyo Cement Company (Lanka) PLC2 C

Vision

Mission

VisionTo be the leading partner in nation - building;

setting standards that exceed expectations

MissionReinforcing market leadership by

empowering our people, driving innovation, pursuing

sustainable development, assuring consistent quality, and

committing to impeccable service; thereby

building shareholder value and cementing consumer trust.

3Annual Report 2012/13

ContentsPerformance Highlights 4, Corporate Profile 8, Products 10, Chairman’s statement 16, Message of the

Japanese Joint Venture Partner 18, Managing Director’s Message 20, Board of Directors 24, Major

Projects 30, Annual Report of the Directors 32, Corporate Governance 38, Risk Management 42,

Sustainability Report 46, Directors Responsibilities 54, Audit Committee Report 56, Report of the

Remuneration Committee 58, Nomination Committee Report 59, Independent Auditor’s Report 60,

Statement of Comprehensive Income 61, The Statement of Financial Position 62, Statement of Changes

in Equity 64, Statement of Cash Flow 65, Significant Accounting Policies 67, Notes to the Financial

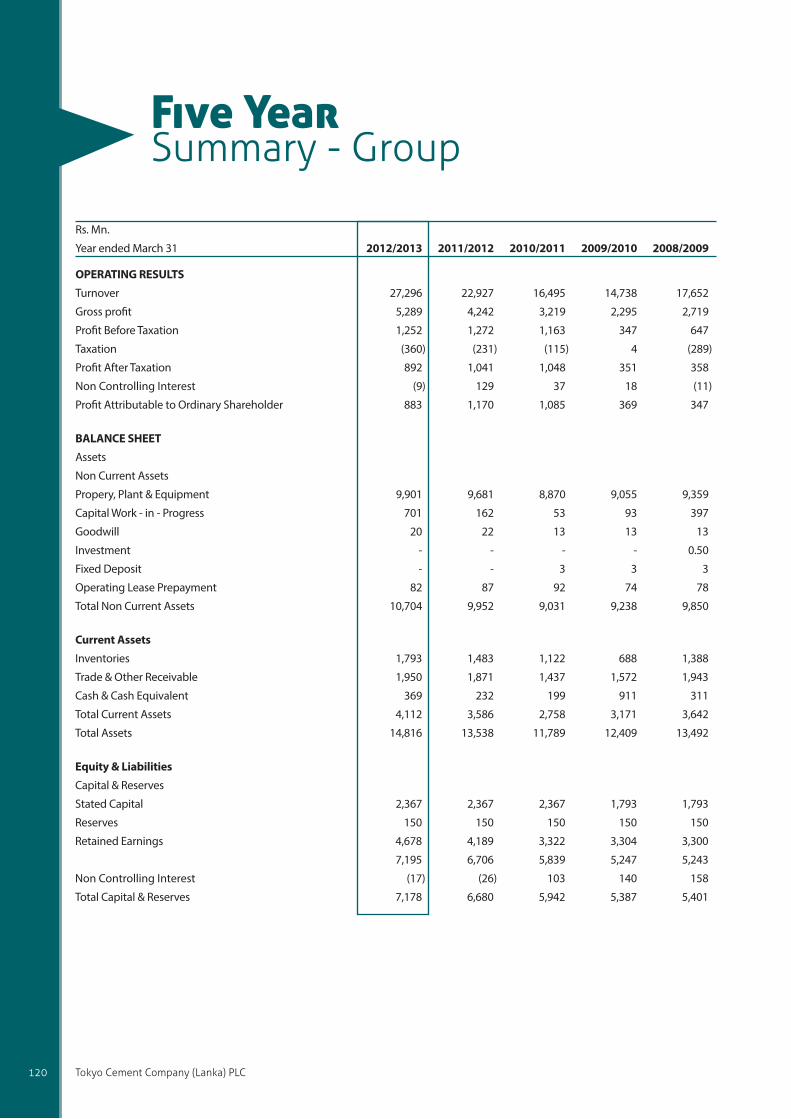

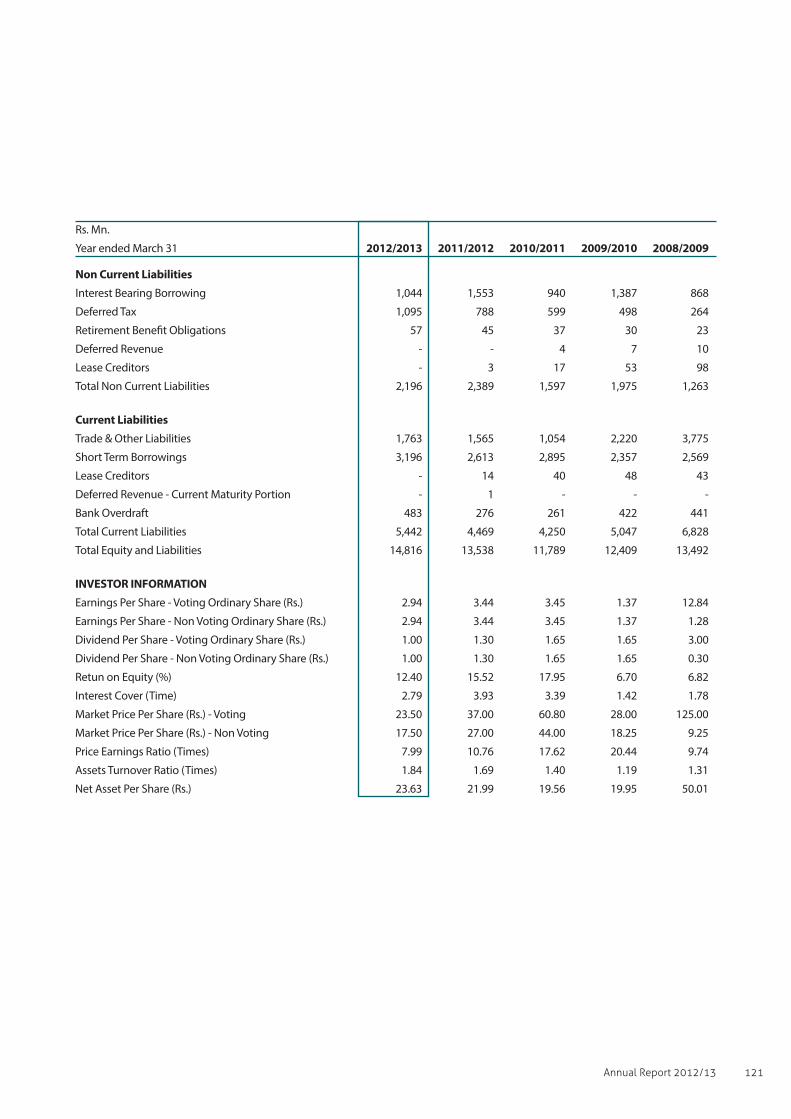

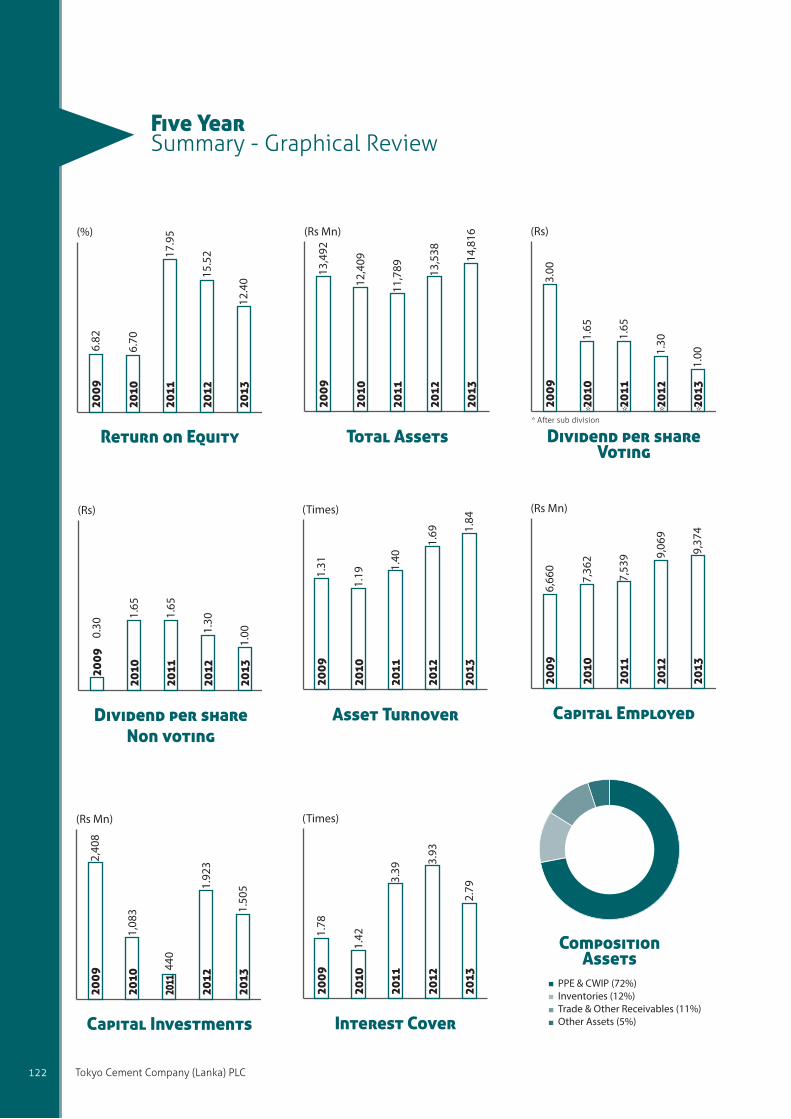

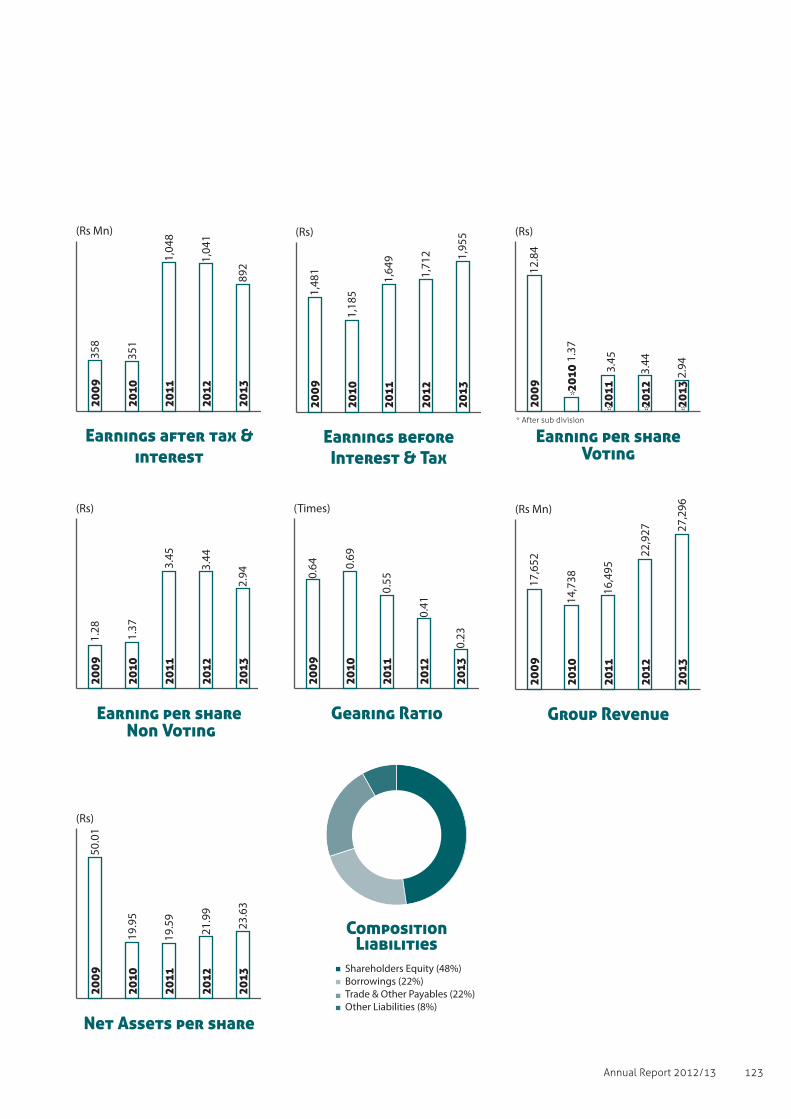

Statements 86, Shareholder & Investor Information 117, Five Year Summary 120,

Notice of Meeting 124

Tokyo Cement Company (Lanka) PLC4

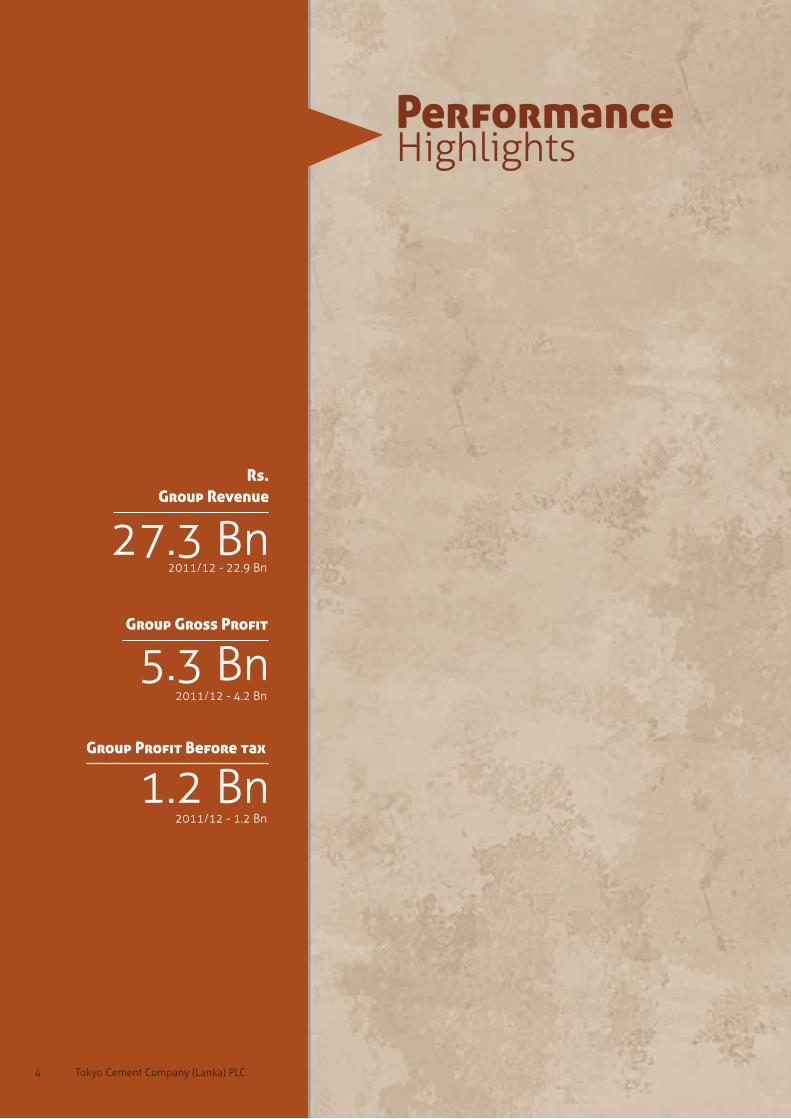

Performance

Highlights

Group Revenue

27.3 Bn

5.3 Bn2011/12 - 4.2 Bn

1.2 Bn2011/12 - 1.2 Bn

Rs.

2011/12 - 22.9 Bn

5Annual Report 2012/13

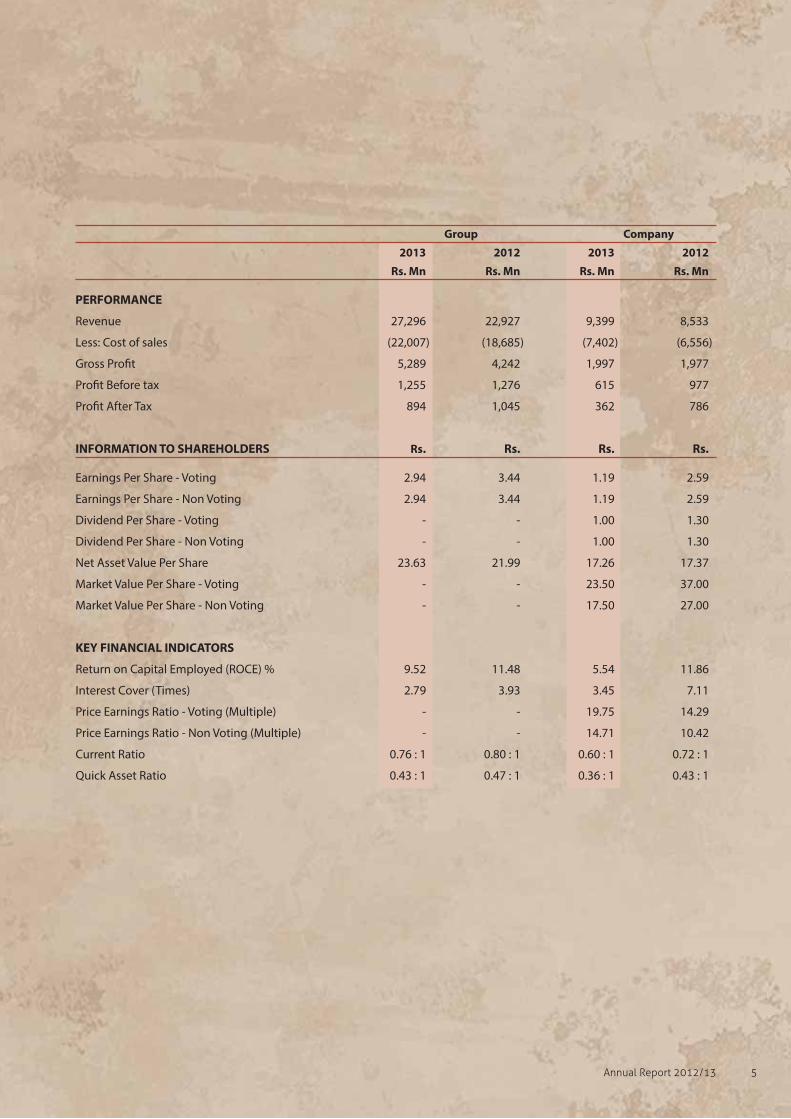

Group Company

2013 2012 2013 2012

Rs. Mn Rs. Mn Rs. Mn Rs. Mn

PERFORMANCE

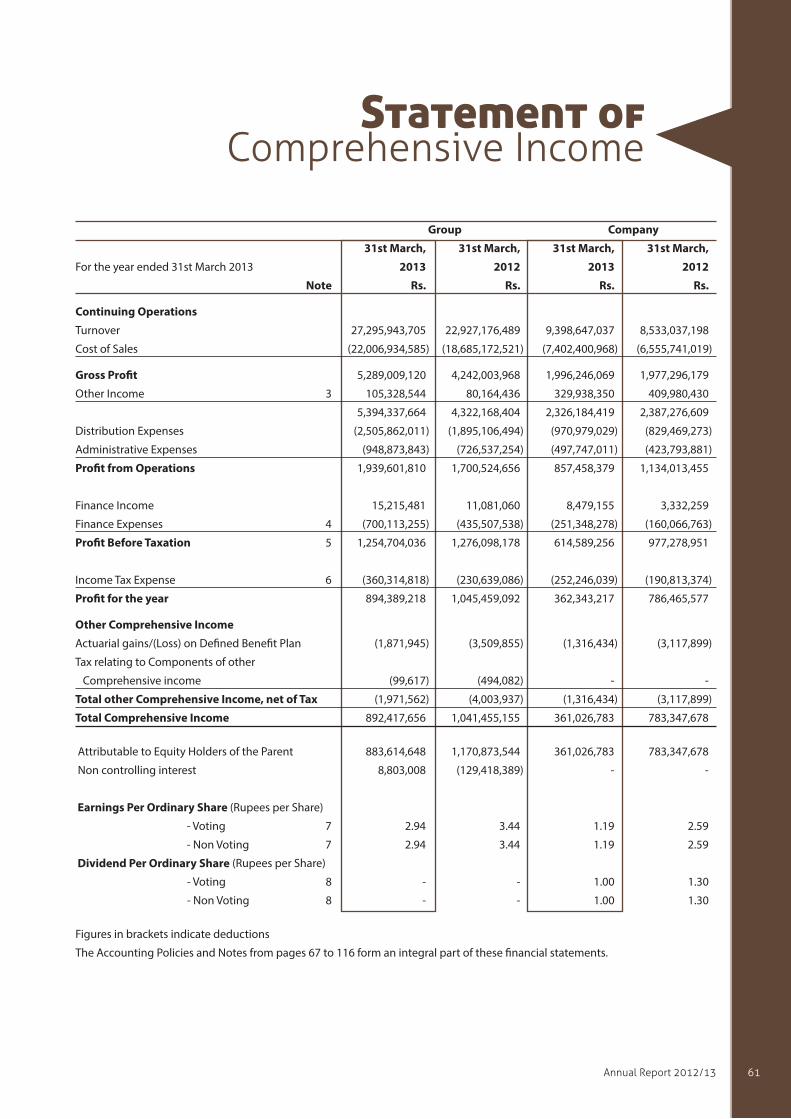

Revenue 27,296 22,927 9,399 8,533

Less: Cost of sales (22,007) (18,685) (7,402) (6,556)

Gross Profit 5,289 4,242 1,997 1,977

Profit Before tax 1,255 1,276 615 977

Profit After Tax 894 1,045 362 786

INFORMATION TO SHAREHOLDERS Rs. Rs. Rs. Rs.

Earnings Per Share - Voting 2.94 3.44 1.19 2.59

Earnings Per Share - Non Voting 2.94 3.44 1.19 2.59

Dividend Per Share - Voting - - 1.00 1.30

Dividend Per Share - Non Voting - - 1.00 1.30

Net Asset Value Per Share 23.63 21.99 17.26 17.37

Market Value Per Share - Voting - - 23.50 37.00

Market Value Per Share - Non Voting - - 17.50 27.00

KEY FINANCIAL INDICATORS

Return on Capital Employed (ROCE) % 9.52 11.48 5.54 11.86

Interest Cover (Times) 2.79 3.93 3.45 7.11

Price Earnings Ratio - Voting (Multiple) - - 19.75 14.29

Price Earnings Ratio - Non Voting (Multiple) - - 14.71 10.42

Current Ratio 0.76 : 1 0.80 : 1 0.60 : 1 0.72 : 1

Quick Asset Ratio 0.43 : 1 0.47 : 1 0.36 : 1 0.43 : 1

Tokyo Cement Company (Lanka) PLC6 CTokyo Cement Company (Lanka) PLC6

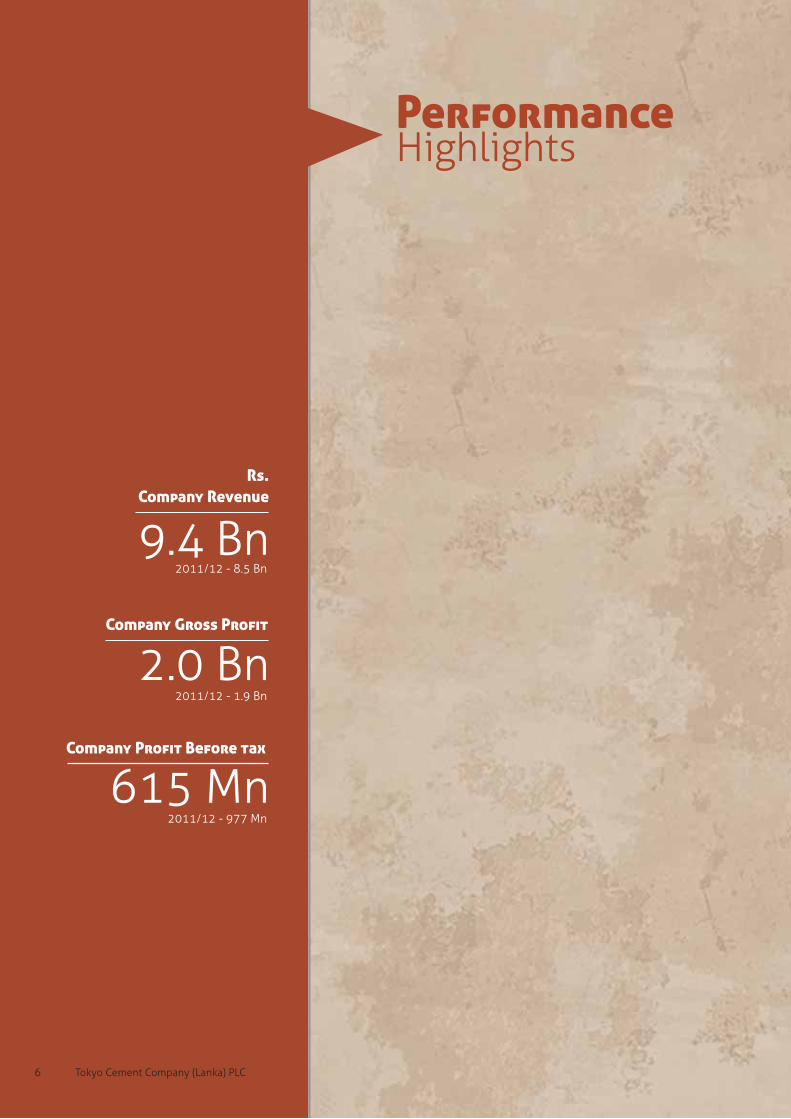

Performance

Highlights

Company Revenue

9.4 Bn

2.0 Bn2011/12 - 1.9 Bn

615 Mn2011/12 - 977 Mn

2011/12 - 8.5 Bn

Rs.

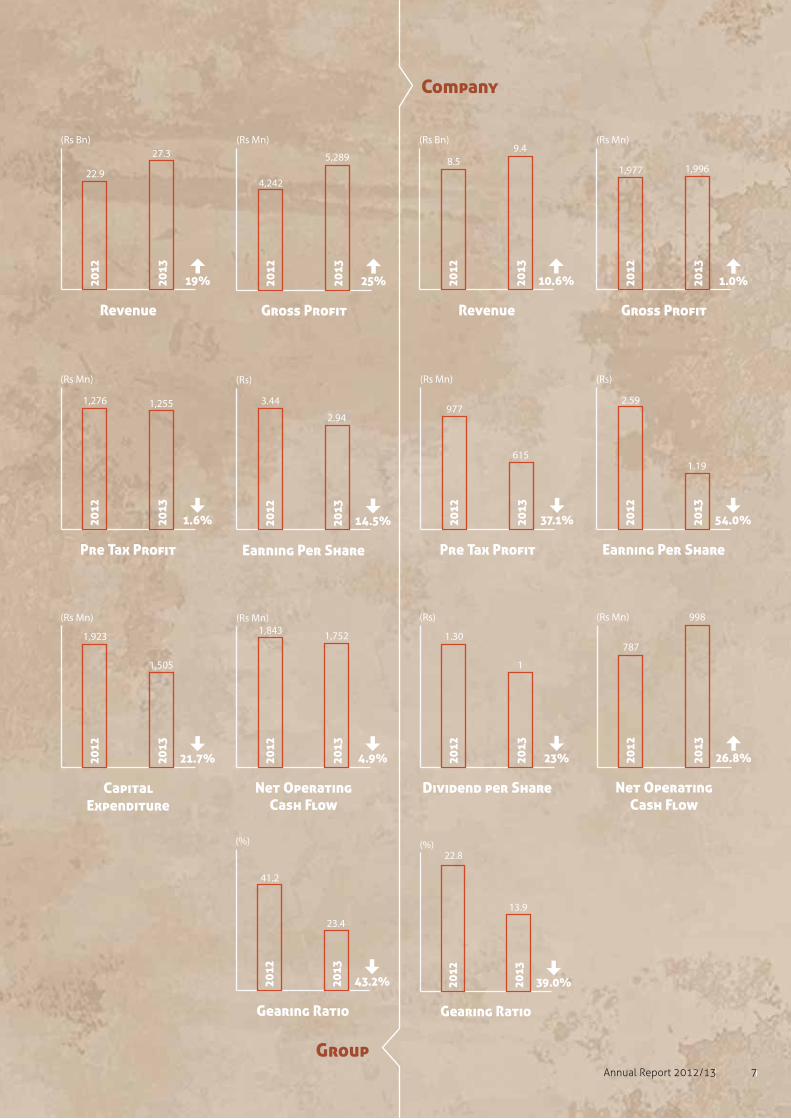

7Annual Report 2012/13 77777777AnAAnnAnAnnAnnAnnAnAnnualuualuauauuu ReReReReReReReRRRR porporporporpopppp t 2t 222t 22t 222201201201201211012012012012012012101120 20 //13/13/13/13/ 7Annual Report 2012/13

Gross Profit

20

12

20

13

4,242

(Rs Mn)

5,289

25%

Gross Profit

20

12

20

13

1,977

(Rs Mn)

1,996

1.0%

Pre Tax Profit

20

12

20

13

1,276

(Rs Mn)

1,255

1.6%

Pre Tax Profit

20

12

20

13

977

(Rs Mn)

615

37.1%

Earning Per Share

20

12

20

13

3.44

(Rs)

2.94

14.5%

Earning Per Share

20

12

20

13

2.59

(Rs)

1.19

54.0%

Capital

Expenditure

20

12

20

13

1,923

(Rs Mn)

1,505

21.7%

Dividend per Share

20

12

20

13

1.30

(Rs)

1

23%

Net Operating

Cash Flow

20

12

20

13

1,843(Rs Mn)

1,752

4.9%

Net Operating

Cash Flow

20

12

20

13

787

(Rs Mn) 998

26.8%

Gearing Ratio

20

12

20

13

41.2

(%)

23.4

43.2%

Gearing Ratio

20

12

20

13

22.8(%)

13.9

39.0%

Revenue

20

12

20

13

8.5

(Rs Bn)9.4

10.6%

Revenue

20

12

20

13

22.9

(Rs Bn)

27.3

19%

Tokyo Cement Company (Lanka) PLC8

Our biomass power plant is a ground breaking achievement and an inspiration for environmentally friendly manufacturing.

Tokyo Cement - investing big in

sustainable energy

Our corporate heritage includes the unique

distinction of being a pioneer in manufacturing, as

the Sri Lanka’s first private cement manufacturer.

This pioneering spirit remains a guiding force

in forming our corporate policies and business

strategies even today.

When Tokyo Cement was formed in 1982, as a

joint venture between Sri Lanka’s St Anthony’s

Consolidated and Japan’s Mitsui Mining Company

that was later name changed to Nippon Coke and

Engineering Company, we took on the mammoth

challenge of constructing the country’s first,

automated cement plant, in the Eastern coast

of Trincomalee. We then went on to build Tokyo

Cement into one of Sri Lanka’s most valuable

brands and the country’s largest manufacturer

of cement. Today we are proud to be the market

leader in Sri Lanka’s cement industry with over

seven hundred employees and Rs. 14 billion in

assets.

This journey has seen many achievements and

accolades coming our way, as we continued to

9Annual Report 2012/13

lead the way in new products and technologies, and

sustainable manufacturing. We are the first cement

manufacturer in the country, to qualify for the SLS, ISO

9002 and ISO 14001 certifications. Tokyo Cement is Sri

Lanka’s first automated cement factory and we have

successfully implemented a pipe conveyor system to

transport raw materials, to prevent environmental

pollution from clinker dust. Other technical advancements

include an electronic rotary packer and a vertical roller

press for manufacturing. The use of modern technologies

has ensured the consistent, international standard of our

products.

Over the years, we have continued to identify national

economic needs and to develop our business strategy

to respond to such needs. This has ensured economic

benefits not only for the company but the entire

country. One such initiative was our decision to invest

in renewable energy. This choice has saved the company

millions of rupees in energy costs and reduced the

burden on the national grid. Our biomass power plant

is a ground breaking achievement and an inspiration

for environmentally friendly manufacturing. We have

now taken another step in this direction by establishing

a dendro power plant, that will help green the country

while providing electricity and incomes for rural

communities. Over the years, we have introduced many

other environmental conservation initiatives that will

benefit future generations.

Another such initiative that has national significance

is our decision to acquire a fleet of ships, to mitigate

shipping cost volatilities. Freight costs are subject to

external market dynamics and are beyond the company’s

control. Therefore, sudden spikes in freight costs have

significant and unavoidable negative impacts on the

company’s balance sheet. Our decision to invest in our

own fleet of vessels therefore, has saved the company,

and the country, millions of dollars by avoiding chartering

of vessels to transport raw materials.

We have also addressed a pressing national need for

skilled construction labour. Most masons in Sri Lanka’s

construction sector do not have formal training and

recognised qualifications. This has had a severe negative

impact on their prospects for career growth and

employment opportunities in the formal sector. Skilled

masons are also a key requirement to meet government

goals for national development. Therefore, we created a

dedicated training centre for masons called the

A Y S Gnanam Construction Training Academy. The

Academy serves a national purpose and also caters to

the personal aspirations of hundreds of young people

in Sri Lanka, by paving the way for nationally and

internationally recognised qualifications in masonry. We

are happy to announce that by now, the A Y S Gnanam

Construction Training Academy is turning out qualified

personnel to support the future growth of our country.

Over the years we have introduced many new products

to the local market and we hope to introduce many

more exciting new products in the coming years. All our

new products have become extremely popular in the

domestic market and have also contributed towards

improving construction industry standards through our

new products.

As a responsible corporate citizen, governed by a

philosophy of sustainable manufacturing, we will

continue to respond to economic and social needs in the

country.

Tokyo Cement Company (Lanka) PLCTokyo Cement Company (Lanka) PLC10

Cement

Strength Class 42.5 N

SLS 107 : 2008

“Tokyo Super” brand OPC is a general purpose cement which can be used

in the production of all type of concrete used in structural and non-

structural applications.

Typical applications:

“Tokyo Super” OPC is compatible with most of the admixtures complying to

BSEN & ASTM standards. Tokyo Super

Ordinary Portland Cement

Strength Class 42.5 N

SLS 107 : 2008

“Tokyo Super” Portland Pozzolana Cement (TSPPC) is a Blended Hydraulic

Cement produced by inter-grinding fly ash with cement clinker.

“Tokyo Super” Portland Pozzolana Cement is produced to conform to SLS

1247 : 2008 Strength Class 42.5 N standard specification. This cement

is highly resistant to chemical attack and suitable for concreting and in

mortar in marine and sulphate containing soil environments. This cement

is a low heat cement and can use for mass scale concreting.

Blended cements are a lever to reduce carbon dioxide emission and it’s a

“Greener Cement”. Tokyo Super

Portland Pozzolana Cement

Strength Class 42.5 N

SLS 107 : 2008

“Nippon” is the premium brand of Ordinary Portland Cement manufactured

by Tokyo Cement Co. (Lanka) PLC. “Nippon” cement meets the stringent

quality requirement specified by Sri Lanka Standards Institution (SLS

107:2008) Strength Class 42.5 N for Ordinary Portland Cement. This cement

is suitable for structural and pre-cast concrete requiring high compressive

strength. This cement also can be used as a general purpose cement.

“Nippon” cement is compatible with most of the admixtures complying to

BSEN & ASTM standards. Nippon

Ordinary Portland Cement (OPC)

11Annual Report 2012/13 11Annual Report 2012/13

Tile Adhesives

Thin set cement base tile adhesive, which can be used for fixing ceramic,

porcelain, terracotta, granite tiles etc. on mortar screed or concrete base.

“Tokyo Superbond” Standard Set tile adhesive can be used for fixing tiles

on walls and floors.

Highly workable mix with high water retention capability make fixing

tiles on floors and walls easier, economical and resulting a high bond

strength.

Tokyo Superbond

Standard Application

Specially formulated tile adhesive to develop high bond strength within

a short time of 6 hours. This adhesive is suitable for fixing any type of

tiles, marble, granite etc. on new or existing tiled or cemented surfaces.

Advantage of using this adhesive allows grouting in 2 hours and use of

the premises after 6 hours of laying tiles.

Tokyo Superbond

Quick Setting

Tokyo Superbond High Performance tile adhesive is specially formulated to

result high bonding strength. In addition to use of this adhesive for fixing

normal all types of tiles, it is highly recommended for fixing large format

(3’x3’ or 4’x4’) porcelain or fully vitrified tiles on floors and walls.

This adhesive is suitable for fixing tiles on an existing tiled or cemented

floor without breaking. Suitable for tiling kitchens and bathrooms where

hot water is used frequently.

Tokyo Superbond

High Performance

Lay Tiles on Tiles

Tokyo Cement Company (Lanka) PLC12

Flooring Waterproofing

Concrete

“Tokyo Superflow” flooring is a SWF-leveling cementitious flooring

compound which can be applied manually or by pump to achieve rapid,

flat levelled substrate prior to the application of the final floor finish.

Typical uses are in warehouses, factories, manufacturing facilities, hospitals,

commercial buildings, residential and domestic properties etc.

Flooring Compound (Standard)

“Tokyo Super Water Proofer” is a cement base material suitable for interior

or exterior surface where water proofing is required.

“Tokyo Super Water Proofer” is highly resistant to standing water or wind

driver rain water and intended for use in vertical, horizontal, and overhead

surfaces. Typical uses are in water sealing bathrooms, overhead slabs, walls,

joints etc.

Tokyo Super

Waterproofing

Consists of a mix of river sand with metal (05-20 mm) by weight basis and

cement in a separate bag. Only necessary to add required quantity of water

to make a workable concrete mix.

Equivalent concrete grade is G20. “Tokyo Super-mix” Concrete-mix can be

used for slabs, drive ways, pavements etc.

Available in 50 kg bags and 30 bags cover 10ft x 10ft x 0.25 ft

“Dry Concrete”

13Annual Report 2012/13 13Annual Report 2012/13

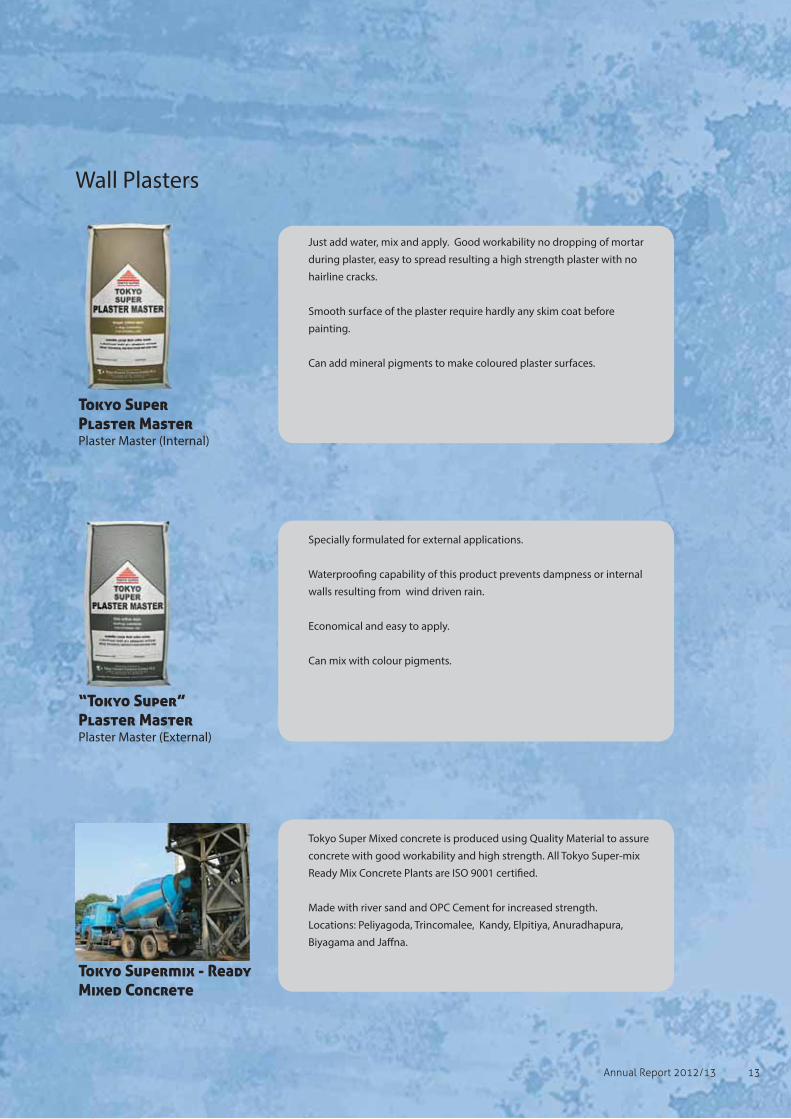

Wall Plasters

Just add water, mix and apply. Good workability no dropping of mortar

during plaster, easy to spread resulting a high strength plaster with no

hairline cracks.

Smooth surface of the plaster require hardly any skim coat before

painting.

Can add mineral pigments to make coloured plaster surfaces.

Tokyo Super

Plaster Master (Internal)

Specially formulated for external applications.

Waterproofing capability of this product prevents dampness or internal

walls resulting from wind driven rain.

Economical and easy to apply.

Can mix with colour pigments.

“Tokyo Super”

Plaster Master (External)

Tokyo Super Mixed concrete is produced using Quality Material to assure

concrete with good workability and high strength. All Tokyo Super-mix

Ready Mix Concrete Plants are ISO 9001 certified.

Made with river sand and OPC Cement for increased strength.

Locations: Peliyagoda, Trincomalee, Kandy, Elpitiya, Anuradhapura,

Biyagama and Jaffna.

Tokyo Cement Company (Lanka) PLC14

15Annual Report 2012/13

Tokyo Cement Company (Lanka) PLC16

In reviewing the performance of your company for the

year ended 31st March 2013, it is relevant to address the

state of the global economy during the period, and its

impact on the local economy. Of course, the demand for

of the company’s product, in the main, is dependent on

the state of the local economy. Accordingly, brief surveys

of both the global and domestic economies follow.

Global Economy

The continuing poor state of the economies of major

industrial countries, was not conducive to world trade.

Global economic growth continued to slow down during

the year: it is estimated at 3.3%. Sluggish output in the

main advanced economies, fragile financial conditions

and increased in unemployment remain key concerns.

Growth of the US economy is beginning to recover.

However, recession in Europe is deeper than anticipated

and recovery will be protracted. China is experiencing a

slowdown. In the Middle East, problems in Iran, Egypt and

Syria continues. At the time of writing, favourable news

from Japan is that its economy is on the mend.

Sri Lanka Economy

Year 2012 was one of challenges on the economic front.

The poor state of the global economy had an adverse

impact on the local economy. The European Union

crisis, slow growth in the US and the continuing crises in

Iran & Syria impacted the country’s exports. Inclement

weather, with flash floods followed by drought, prevailed

17Annual Report 2012/13

The Government continues to engage in major infrastructure development projects

with foreign borrowings.

in the country’s agriculture. The drop in the value of

exports was significant. Revenue collection was far below

target. The totality of losses by state owned enterprises

was substantial. On the plus side an increase in worker

remittances was recorded, tourism earnings rose and

tea prices remained firm. The rupee over the period was

devalued by 11.6%, and the high interest rate regime

continued. The country’s growth rate was 6.4%. The

Government continues to engage in major infrastructure

development projects financed mainly with foreign

borrowings. It is refreshing to see a drop in the value of

imports, and the concerted efforts being taken to address

to the shortcomings on the economic front.

Performance of the Group

The Managing Director’s message has dealt in detail

about the performance of the Group, and I believe it

would suffice if I highlight only items of significance.

Revenue increased by 19% due to demand growth and

rupee depreciation. The after tax profit was Rs. 894 Mn

as compared with Rs.1,045 Mn the previous year. The

drop in the main was due to the five months delay in

receiving Consumer Affairs authority for an increase in the

administrated price due to a depreciation of the rupee.

Further, the rise in banks’ lending rates and increase in the

quantum of the Company’s borrowing for the purchase of

two additional ships also had an impact on profitability.

Contributions from the batching plants in line of business

were encouraging. I am pleased to report our new

product, cement bond, has been very encouraging and it

is planned to expand this line of activity.

I am optimistic about a moderate growth in demand for

cement in the foreseeable future. To meet this eventuality,

an expansion programme is in place by way of a new

mill. Generous tax concessions have been received on

the investment. Its cost is estimated at US$ 50 Mn, to be

financed by a combination of internal generation and

bank borrowing. The company’s second Dendro Plant at

Dehiattakandiya costing Rs.1.5 billion is expected to be

commissioned by December 2013.

Acknowledgement

Your company is fortunate in having a committed and

loyal staff at all levels, and I thank them all.

Mr. K. Yanagihara, our Japanese director who was a board

member for 14 years retired and returned to Japan. I

record my appreciation for his services rendered and wish

him a long period of happy retirement.

To my fellow directors who have at all times guided and

adviced me, I salute them sincerely.

Edgar Gunatunga

Chairman

29th June 2013

Tokyo Cement Company (Lanka) PLC18

19Annual Report 2012/13

On behalf of the Japanese Joint Venture partner, I

would like to express our heartfelt appreciation to the

shareholders of Tokyo Cement Company (Lanka) PLC for

the confidence you have granted to the members

of the Board.

I would like to extend my sincere thanks to the customers,

dealers and staff of Tokyo Cement Group for exceptional

consideration and support.

In financial year 2012/13, the total sales of Tokyo Cement

Group have increased from the previous year, because

of expansion of cement demand by activation of the Sri

Lankan economy and the revival project in North and

East districts. But, the consolidated profits of the group

have decreased due to delay in granting price increase

approval and rise in financial cost.

In financial year 2013/14, because the cement demand

is expected to expand, Tokyo Cement Group takes an

important role more and more in this field. I believe that

the group will contribute greatly to the society and grow

significantly.

I hope the financial year 2013/14 would be a prosperous

year for the Tokyo Cement Group.

Yoshichika Nishoi

President

Nippon Coke & Engineering Co. Ltd

29th June 2013

I believe that the group will contribute greatly to the society and grow

Tokyo Cement Company (Lanka) PLC20

It gives me great pleasure to welcome our shareholders

to our 31st Annual General Meeting and to report that

your Company continued to sustain profits despite a

challenging year. I also take this opportunity to announce

a new three-year growth strategy for your Company, in

line with Tokyo Cement’s sustainability principles.

Economic developments

Sri Lanka’s economy grew by 6.4% in 2012 on the

backdrop of two consecutive years of 8% growth. On the

production sector, economic growth was mainly driven

by the Industry sector. The expansion in the Industry

sector by 10.3% in 2012 was predominantly sustained

by the sharp increase in construction activities. Services

sector growth moderated to 4.6% in 2012, from 8.6% in

the previous year, and the agriculture sector improved

to 5.8% in 2012, compared to the growth of 1.4% in the

previous year.

In a significant development, in early 2012, the Central

Bank adopted a tight monetary policy stance by raising

policy interest rates and imposing a ceiling on rupee

lending by licensed banks, to moderate credit growth.

Further, from February 2012, the Central Bank allowed

greater flexibility in the determination of the exchange

21Annual Report 2012/13

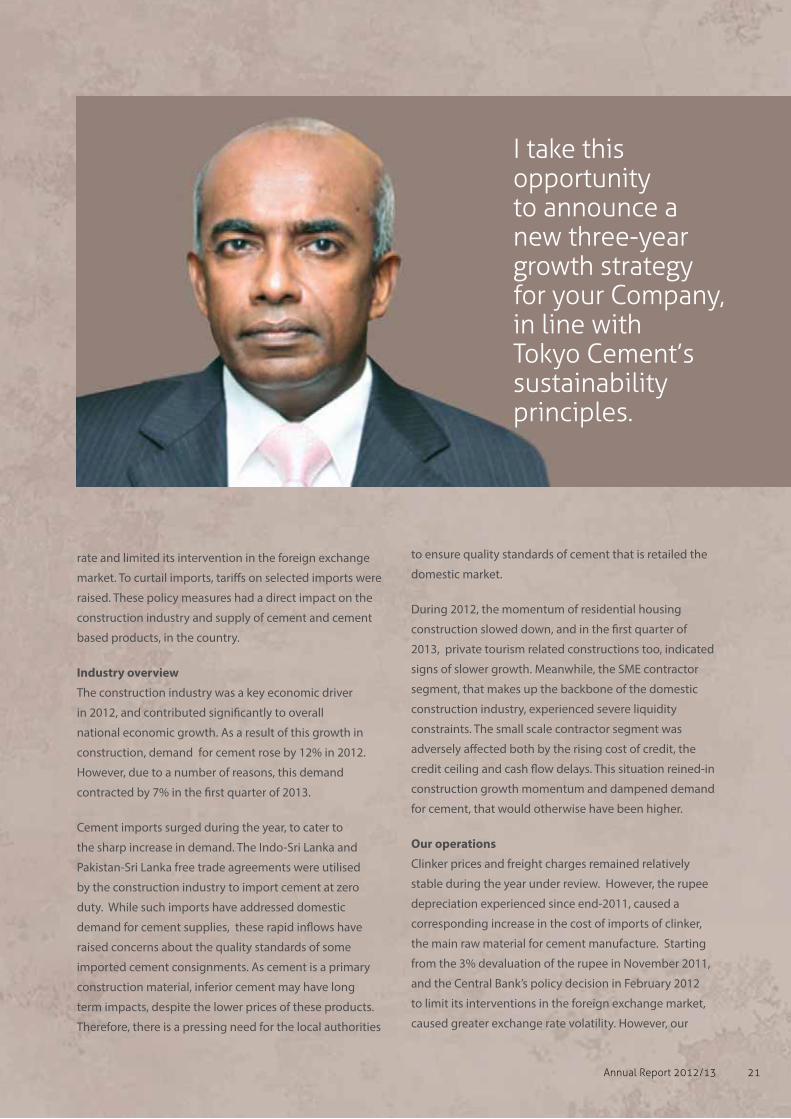

rate and limited its intervention in the foreign exchange

market. To curtail imports, tariffs on selected imports were

raised. These policy measures had a direct impact on the

construction industry and supply of cement and cement

based products, in the country.

Industry overview

The construction industry was a key economic driver

in 2012, and contributed significantly to overall

national economic growth. As a result of this growth in

construction, demand for cement rose by 12% in 2012.

However, due to a number of reasons, this demand

contracted by 7% in the first quarter of 2013.

Cement imports surged during the year, to cater to

the sharp increase in demand. The Indo-Sri Lanka and

Pakistan-Sri Lanka free trade agreements were utilised

by the construction industry to import cement at zero

duty. While such imports have addressed domestic

demand for cement supplies, these rapid inflows have

raised concerns about the quality standards of some

imported cement consignments. As cement is a primary

construction material, inferior cement may have long

term impacts, despite the lower prices of these products.

Therefore, there is a pressing need for the local authorities

I take this opportunity to announce a new three-year growth strategy for your Company, in line with Tokyo Cement’s sustainability principles.

to ensure quality standards of cement that is retailed the

domestic market.

During 2012, the momentum of residential housing

construction slowed down, and in the first quarter of

2013, private tourism related constructions too, indicated

signs of slower growth. Meanwhile, the SME contractor

segment, that makes up the backbone of the domestic

construction industry, experienced severe liquidity

constraints. The small scale contractor segment was

adversely affected both by the rising cost of credit, the

credit ceiling and cash flow delays. This situation reined-in

construction growth momentum and dampened demand

for cement, that would otherwise have been higher.

Our operations

Clinker prices and freight charges remained relatively

stable during the year under review. However, the rupee

depreciation experienced since end-2011, caused a

corresponding increase in the cost of imports of clinker,

the main raw material for cement manufacture. Starting

from the 3% devaluation of the rupee in November 2011,

and the Central Bank’s policy decision in February 2012

to limit its interventions in the foreign exchange market,

caused greater exchange rate volatility. However, our

Tokyo Cement Company (Lanka) PLC22

MMannaagging DDireeccttorr’ss

MMessssaagee

request to the Consumer Affairs Authority to increase the

price of cement, in line with increasing import costs, was

not granted approval for five months. Therefore, Tokyo

cement’s price revision took place only after a five month

delay.

This delay in price adjustment, together with the rising

cost of credit, had a direct impact on our bottom line

by reducing overall profitability, despite higher sales

and revenues. Meanwhile, the upward price revision

of cement, resulted in an immediate drop in demand

for cement. However, this situation can be expected to

reverse in the new financial year, in the face of growing

demand.

In discussing business operations, I must make it a

point to mention that your Company’s sustainable

manufacturing policies are now evincing tangible

financial benefits for the Company. Although energy

costs, in the form of increased costs of fuel and electricity,

are a serious concern for Sri Lanka’s manufacturing sector,

Tokyo Cement has been shielded from this severe cost

increase due to our sustainable energy initiatives. Our

decision to invest in the renewable energy source of

biomass, has made us energy self sufficient and protected

the Company from energy cost increases and disruptive

power shortages.

Financial review

Tokyo cement recorded a 19% growth in top line due to

the sharp increase in cement demand compared to the

previous year. As a result our total revenues increased from

Rs. 22.9 billion in 2011/12 to Rs. 27.3 billion in the current

financial year. Despite five months delay in granting of

price increase approval in line with cost increases by the

Consumer Affairs Authority the operating profit in the year

under review had positive results. Nevertheless increase in

lending rates, elevated borrowings for capital assets, first

time adoption of SLFRS and related tax effects resulted in

having consolidated profit before tax of Rs. 1.2 billion and

profit after tax of Rs. 894 million in the financial year under

review.

Product development

To keep pace with international trends and to ensure best

value for money for Sri Lankan consumers, Tokyo Cement

has consistently invested in research and development

(R&D). In the current financial year, we upgraded

our laboratory in Trincomalee to ISO 17025 standard.

Therefore, we are now an independent laboratory,

formally accredited to provide testing facilities for cement

and concrete products. We hope our services in this

regard will contribute towards the development of the

domestic construction industry, by facilitating innovations

and setting industry standards, while ensuring high

quality for consumers.

In the new financial year, we hope to introduce a range

of exciting value added new products to the market that

will enhance the capabilities of the local construction

industry.

Future outlook

We anticipate a 10% year on year demand growth

for cement over the medium term, fuelled by major

government infrastructure projects and also private

sector investments. The trend of lowering interest

rates will contribute towards sustaining this demand.

Therefore, we have formulated a three year, US$ 50 million

expansion strategy, for capacity growth and new product

development, to cater to this demand growth. Our new

growth strategy will continue through 2013 to end- 2015.

As part of our expansion strategy we propose to set up

a new cement manufacturing facility, with a capacity

of 1 million MTs of cement per year. The new company,

called the Tokyo Eastern Cement Company Ltd, will be

located in Trincomalee, adjoining our existing factory. We

are currently in the process of finalising a 33 years lease

agreement with the government for the land, to construct

the factory. We will also introducing many new products

to the market over the next three years.

23Annual Report 2012/13

In line with our philosophy of sustainable business, our

expansion plan is formulated within a framework of

environment conservation. Therefore, we will set up a

new biomass power plant to cater to the energy needs

of our new cement manufacturing plant. The power

plant will have an output of 10MW, which is adequate

to support the energy requirements of the new facility.

Therefore, we will not add to the demand on the national

grid through our business expansion.

We have already initiated Sri Lanka’s first grid connected

dendro power project, under Tokyo Cement Power Lanka

Ltd, which will be commissioned in December 2013, and

will add 5MW to the national grid. The dendro plant is

located in Dehiattakandiya in Mahiyanganaya and is a

Rs. 1.5 billion investment. While being environmentally

friendly, the dendro plant will also contribute towards

uplifting rural livelihoods as we will educate local families

to grow and harvest Gliricidia plants and will regularly

purchase Gliricidia stems, as fuel for the dendro plant. In

addition to these sustainable practices, we have already

initiated many more environmentally friendly practices,

that are explained further in our sustainability report.

As part of our production expansion programme we will

upgrade our private dock in Trincomalee to enable the

arrival of larger ships. The channel will be deepened and

the jetty extended to permit ships of 28,000 MTs capacity

to dock, compared to the current 20,000 MTs of capacity.

During the previous financial year we purchased two

vessels and within next three financial years we propose

to add another two vessels to our fleet.

Appreciations

I extend a special note of appreciation to Mr K Yanagihara

for his long and dedicated services to the Company as the

Joint Managing Director of Tokyo cement from 1998 to

2012. Mr Yanagihara is admired and respected not only

for his industry expertise but also his adaptability and

considerate personality. My very best wishes go with Mr

Yanagihara in his retirement.

I extend my appreciations as always, to our shareholders

for their support of the Company and the Board of

Directors and management of Tokyo Cement, for their

valuable inputs during the year. I also thank all my staff

for their commitment and hard work. Last but not least, I

wish to thank all our loyal customers and dealers.

S R Gnanam

Managing Director

29th June 2013

Tokyo Cement Company (Lanka) PLC24

Directors

25Annual Report 2012/13

Chairman

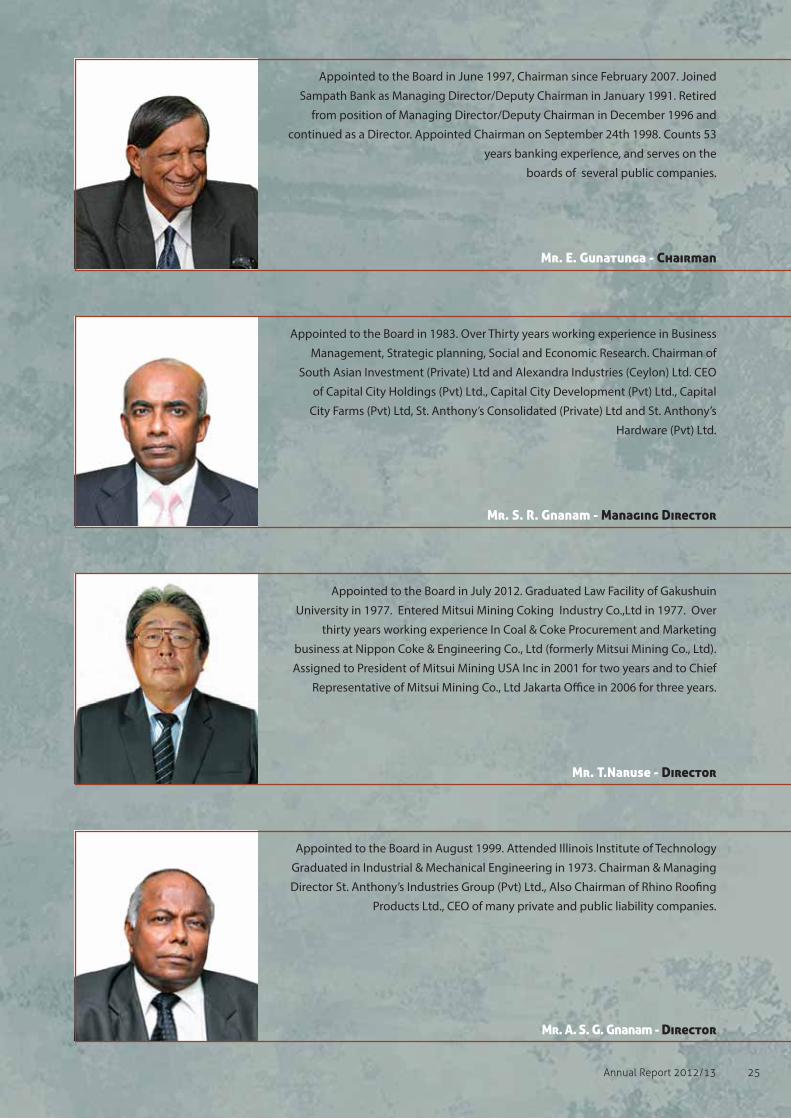

Appointed to the Board in 1983. Over Thirty years working experience in Business

Management, Strategic planning, Social and Economic Research. Chairman of

South Asian Investment (Private) Ltd and Alexandra Industries (Ceylon) Ltd. CEO

of Capital City Holdings (Pvt) Ltd., Capital City Development (Pvt) Ltd., Capital

City Farms (Pvt) Ltd, St. Anthony’s Consolidated (Private) Ltd and St. Anthony’s

Hardware (Pvt) Ltd.

Appointed to the Board in July 2012. Graduated Law Facility of Gakushuin

University in 1977. Entered Mitsui Mining Coking Industry Co.,Ltd in 1977. Over

thirty years working experience In Coal & Coke Procurement and Marketing

business at Nippon Coke & Engineering Co., Ltd (formerly Mitsui Mining Co., Ltd).

Assigned to President of Mitsui Mining USA Inc in 2001 for two years and to Chief

Representative of Mitsui Mining Co., Ltd Jakarta Office in 2006 for three years.

Appointed to the Board in August 1999. Attended Illinois Institute of Technology

Graduated in Industrial & Mechanical Engineering in 1973. Chairman & Managing

Director St. Anthony’s Industries Group (Pvt) Ltd., Also Chairman of Rhino Roofing

Products Ltd., CEO of many private and public liability companies.

Appointed to the Board in June 1997, Chairman since February 2007. Joined

Sampath Bank as Managing Director/Deputy Chairman in January 1991. Retired

from position of Managing Director/Deputy Chairman in December 1996 and

continued as a Director. Appointed Chairman on September 24th 1998. Counts 53

years banking experience, and serves on the

boards of several public companies.

Tokyo Cement Company (Lanka) PLC26

Directors

27Annual Report 2012/13

Appointed to the Board in May 2007. Fellow Member of The Institute of Chartered

Accountants of Sri Lanka and England & Wales and holder of General Science

Degree from the University of London. Former senior partner of KPMG Ford,

Rhodes, Thornton & Company. Director of Haycarb PLC, Dipped Products PLC,

Acme Printing & Packaging PLC, Acme Packaging Solutions (Pvt) Ltd., Tea Factories

Small Holders PLC, Hayleys MGT Knitting Mills PLC, Hayleys Advantis Ltd. and in

many Public Limited Companies.

Appointed to the Board in 1983 over fifty three years of finance and management

experience in Sri Lanka. B.Com (London), F.C.A. (UK), F.C.A. (Sri Lanka). Chairman of

Central Finance Company PLC in the year 2006. Served as the Executive Chairman

of Ceylon Tobacco Company PLC and was a Director of Hatton National Bank PLC,

Richard Peiris & Company PLC, Associated Motorways PLC and Brown & Company PLC.

Appointed to the Board in February 2007. Bachelor of Arts from University of

Texas, MBA from University of Melbourne. Managing Director of South Asian

Investment (Private) Ltd., Orion City Group, Rhino Roofing Group and also in the

Board of Private, Public and listed companies. Has wide experience at leading

corporate sector institutions in the garments trade,

manufacturing and services.

Dr. H. Cabral Appointed to the Board in March 2009. President’s Counsel, Ph.D.

in Corporate Law (University of Canberra), Australia, Commissioner - Law

Commission of Sri Lanka, Member (NCED-National Council for Economic

Development), Legal Cluster, Member - Board of Studies - Council of Legal

Education SL, Lecturer and Examiner - University of Wales, University of Colombo

and Sri Lanka Law College, Vice-President - BRIPASL (Business Recovery and

Insolvency Practitioners’ Association of SL), Member - Academic Board of Studies -

Institute of Chartered Accountants of Sri Lanka.

Tokyo Cement Company (Lanka) PLC28

Directors

Annual Report 2012/13 29

Appointed to the board in March 2011, Counts thirty years of experience in policy

making and providing economic advisory services, on both macroeconomic and

structural issues at National and Intergovernmental levels. Obtained Bachelors

and Masters in Economics from the Cambridge University of UK and subsequently

obtained a Doctorate from the University of Sussex. Immediate involvement as a

Director, Economic Affairs at the Commonwealth Secretariat. Has been involved

in advising the Prime Minister and the Minister of Economic Reform, Science and

Technology, Sri Lanka on negotiating with Bretton Woods institutions and other

major donors, the Central Bank of Sri Lanka and the Ministry of Finance & Planning

on matters relating to macroeconomics and structural reforms.

Appointed to Board in 2012. Graduated from Keio University in 1981 with a

Bachelor of Economics. Specialises in International legal issues, Overseas Projects

planning and administration. Joined “Mitsui Mining Company Ltd” in 1981 as a

Business Clerk and has served as Manager of Coal & Coke Department and General

Manager of Personnel & General Affairs Department.

Appointed as Group General Manager in 1991. B.A (Hons) Econ, B. Phil (Hons)

Econ. FCMA FCA & Attorney-At-Law. Director - Fuji Cement Company (Lanka)

Limited,Tokyo Super Cement Company Lanka (Pvt) Limited, Tokyo Cement

Colombo Terminal (Pvt) Limited,Tokyo Cement Power (Lanka) Limited, Tokyo

Eastern Cement Company Limited. Counts over 25 years of

experience in different industries.

Projects

Tokyo Cement Company (Lanka) PLC30

Ba

nd

aranaike I ntern atio nal Airp

ort

Havelock C it y Co n do min

iu

ms

South e rn Hig h way

Norochc h ali Pow er Plant

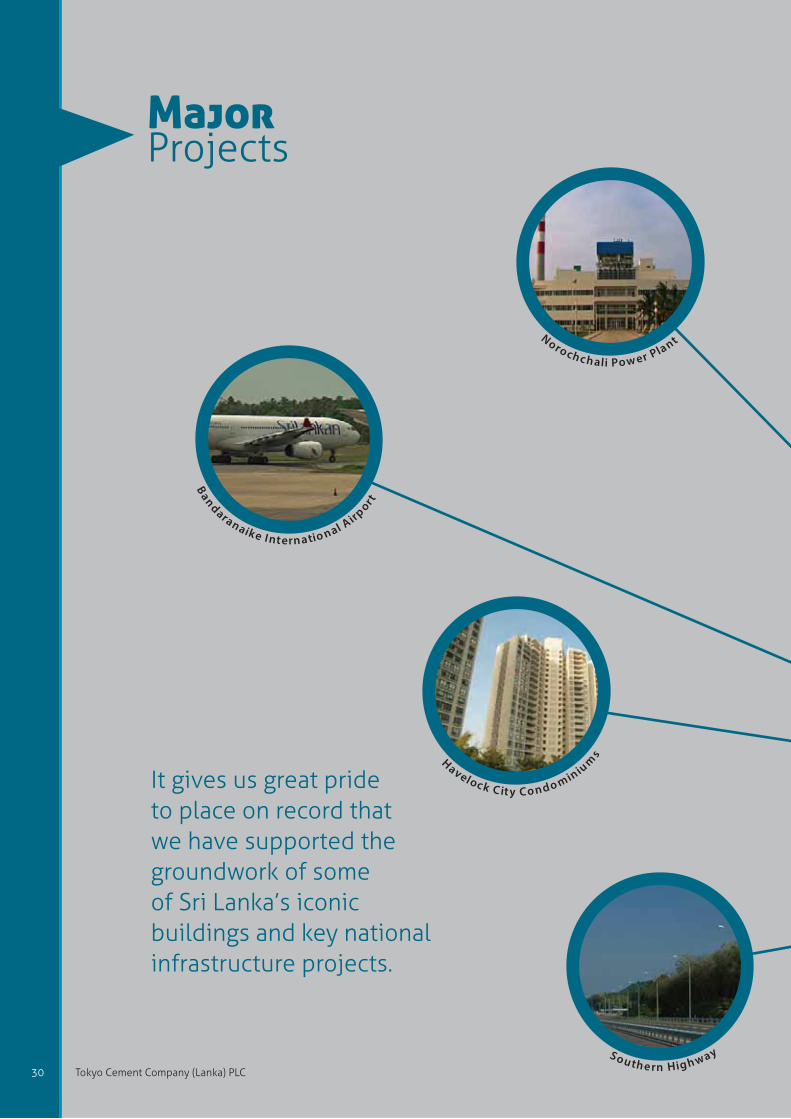

It gives us great pride to place on record that we have supported the groundwork of some of Sri Lanka’s iconic buildings and key national infrastructure projects.

31Annual Report 2012/13

M an a m pitiya Bridg e

Up per Ko t m ale Pow er P

lan

t

Por t o f H a m b a ntota

Tokyo Cement Company (Lanka) PLC32

Directors

Management discussion and analysis

About the company

Tokyo Cement Company (Lanka) PLC is a public

quoted company listed in the Colombo Stock

Exchange, involved in the manufacture of cement

and cement based products. The company’s

subsidiaries are Fuji Cement Company (Lanka)

Limited, Tokyo Super Cement Company Lanka

(Private) Limited, Tokyo Cement Power (Lanka)

Limited and Tokyo Cement Colombo Terminal

(Private) Limited, and Tokyo Eastern Cement

Company Limited.

Principle Activities

The Company’s core activities are the manufacture

of ordinary Portland Cement, Portland Pozzolana

Cement, masonry cement, tile adhesives, water

proofing products, pre-mix concrete and ready-

mix concrete.

Group structure

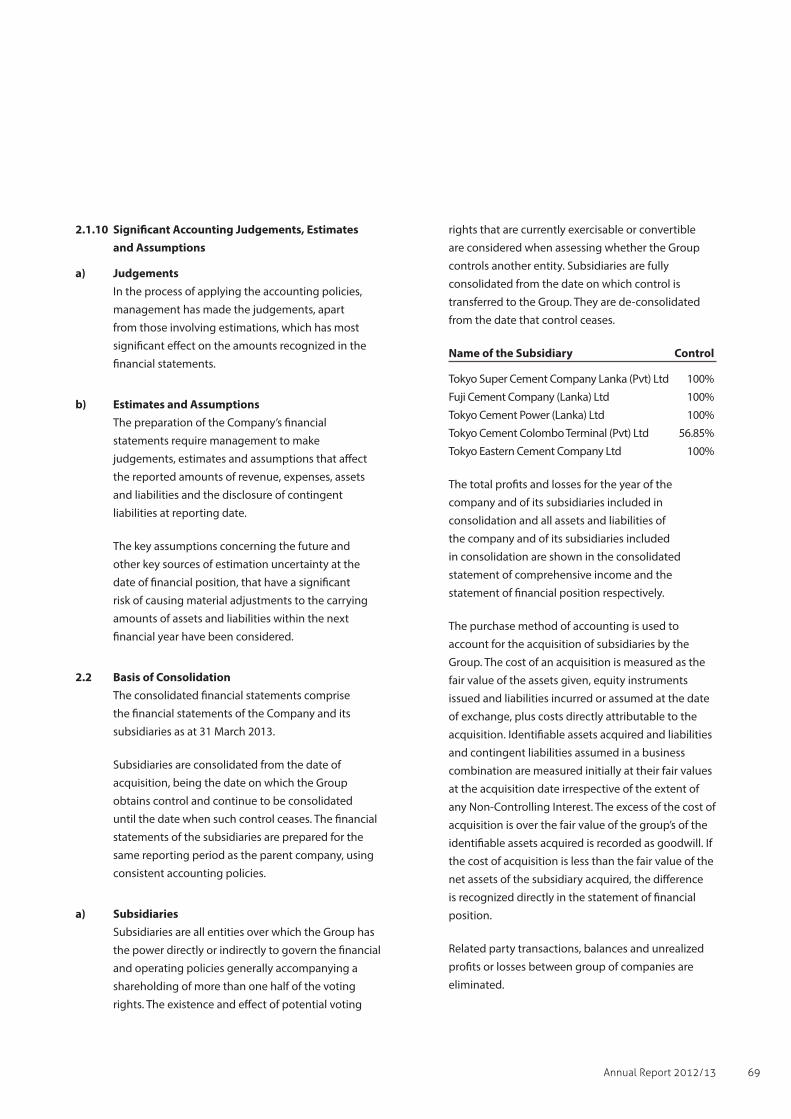

Tokyo Cement Company (Lanka) Plc Subsidiaries

percentage of holding

100% owned

Limited. 100% owned

Limited. 56.85% owned

100% owned

100% owned

Global cement industry

The IMF in its World Economic Outlook report

noted that global economic prospects have

improved but the bumpy recovery and skewed

macroeconomic policy mix in advanced

economies are complicating policy making in

emerging market economies. World output growth

is forecast to reach 3.25% in 2013 and 4% in 2014

from a 3.2% growth in 2012. In the major advanced

economies, activity is expected to gradually

accelerate, following a weak start to 2013, with the

United States in the lead. In emerging market and

developing economies, activity has already picked

up steam.

Worldwide demand for cement is expected to

grow at 4.9% per year, up to 2017. The global

production volume increased by 4.1% in 2012,

for a total output of 3.73 billion MTs. The forecast

increases over the next four years will see global

per capita cement consumption grow from 448 kg

per person in 2009, to 539 kg per person in 2012

and 645 kg per person by 2017.

North America is projected to show one of the

strongest growth trends in the future. Growth in

China is expected to be positive but moderate,

while markets in Sub-Saharan Africa and some

recovering North African markets will see growth

above 6%. Latin America is expected to decelerate,

with growth falling to 5.6% as the Brazilian market

moderates. Asia (excluding China) will see growth

accelerating with Indonesia and Philippines seeing

strong growth in the next years.

Sri Lankan cement industry

In 2012, Sri Lanka’s construction sector expanded

compared to 2011, driven by large government

infrastructure projects and also some significant

private sector investments. This growth in the

construction sector resulted in higher demand for

cement. Nevertheless, demand for articles made

of concrete, cement and plaster, recorded declines,

thus negating to some extent the expansionary

impact of cement production on the industrial

production index (IPI).

It was encouraging that the government

continued to support the domestic cement

industry during 2012. The Ministry of Industry and

Commerce initiated a programme to enhance the

quality of concrete and cement based products,

33Annual Report 2012/13

to improve industrial productivity and facilitating the

construction sector. To attract investments into the sector

and promote domestic manufacture of cement, a 5-year

tax holiday, followed by a concessionary tax rate of 12%,

were granted to the cement industry.

Sri Lankan legal framework

Cement is a price controlled product in Sri Lanka and

is regulated by the Consumer Affairs Authority (CAA).

Therefore, the company requires written approval from

the CAA to increase cement prices.

Review of Operations

A Review of Operational and financial performance, the

future plans of the company and the group are described

in grater detail in the chairman’s message, managing

director’s review. These reports together with the audited

financial statements of the company and the group reflect

the respective state of affairs of the company and the

group.

Significant Accouting Policies

The significant accounting policies adopted in the

preparation of Financial Statements are given on page 67

to page 85 of the Annual Report.

Convergence and adapting of Sri Lanka Accounting

Standards (SLFRSs/LKASs)

The Company and the group prepared their annual

financial statements upto 31st March 2012 in accordance

with Sri Lanka Accounting Standards which were in effect

applicable for said period.

Sri Lanka converging fully with the international financial

reporting standard (IFRS), the institute of chartered

accountants of Sri Lanka has issued new Sri Lanka

Accounting standard (commonly known as SLFRSs/LKASs)

which is applicable for financial period begining after 1st

January 2012.

The financial statement prepared for 31st March 2013

are the 1st financial statement which are prepared in

accordance with these Sri Lanka accouning standards

(SLFRSs/LKASs). As required by the standards, the

company and the group have prepared their operning

statements of financial position(previously known as

balance sheet) as at 1st April 2011 on the basis that these

standards were applicable retrospectively with all the

applicable adjustment directly recognized in the opening

reserves. Accordingly the financial statements for the

period ended 31st March 2012 were restated to be in

accordance with SLFRSs/LKASs.

Income statement of the company and the group

Group revenue and profits

Group revenues rose 19% to Rs.27.3 billion during the

financial year ended March 31, 2013, from Rs.22.9 billion

reported during the same period a year earlier. Company

revenues rose to Rs. 9.4 billion during the year under review,

from Rs. 8.5 billion in the previous year.

Consolidated gross profits gained 25%, to Rs. 5.3 billion in

2012/13, from Rs.4.2 billion a year earlier. Company gross

profits increased to Rs.2.0 billion during the year under

review, from Rs. 1.9 billion in the previous year. However

consolidated profit before tax was Rs 1.2 billion and profit

after tax was Rs 894 million during the financial year

under review as against consolidated profit before tax of

Rs.1.27 billion and profit after tax of Rs 1.0 billion in the

year 2011/12.

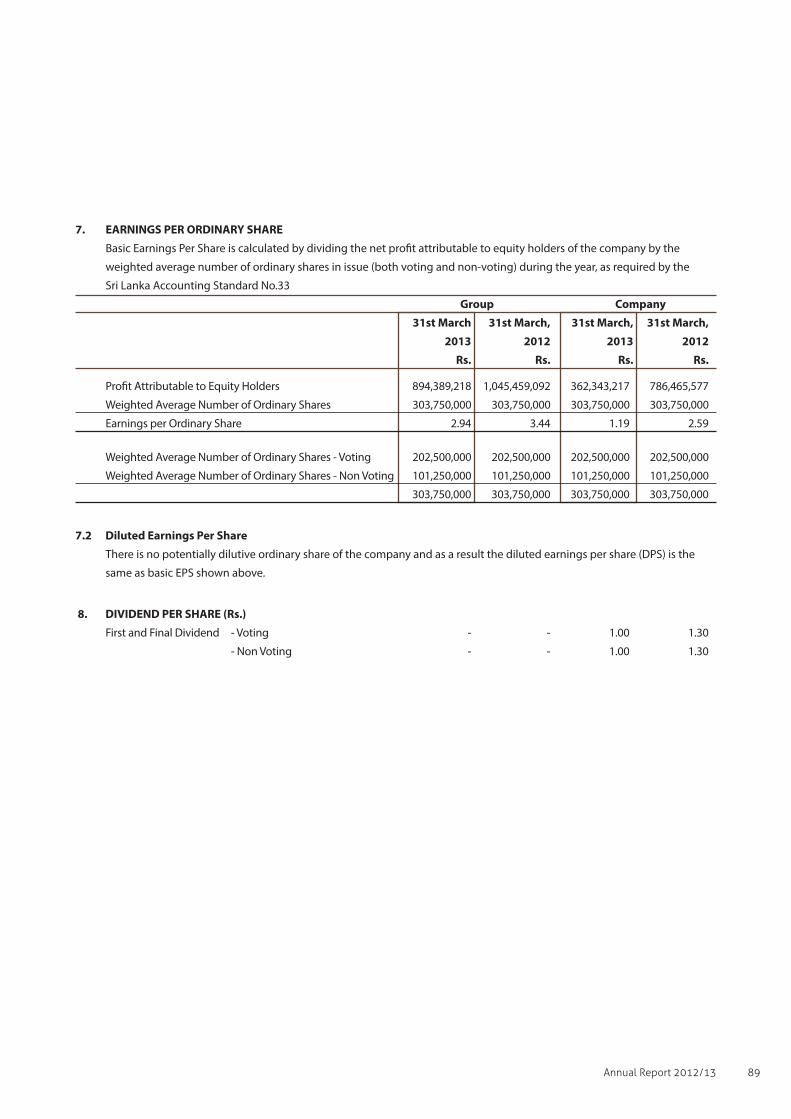

Profit attributable to equity holders decreased by 24.5%

to Rs.884 million during the year under review, from

Rs.1,171 million over the 2011/12 financial year.

Donations

The Group donated Rs.5.9 million to numerous charities

during the year.

Taxation

The Company is not liable for income tax on it’s main

income at the Balance Sheet date. Deferred tax is

provided using the liability method on temporary

differences at the Balance Sheet date between the tax

bases of assets and liabilities, and their carrying amounts

for financial reporting purposes.

Tokyo Cement Company (Lanka) PLC34

Directors

For Group Companies under BOI tax holidays, deferred

tax during the tax holiday period has been recognised for

temporary differences, when reversals of such differences

extend beyond the tax exemption period, taking into

account the requirements of LKASs 12 and The Institute

of Chartered Accountants of Sri Lanka (ICASL) council’s

ruling on deferred tax. Please refer accounting policy

number 2.4.2.2.2 in page 80.

Dividends

Your Directors have recommended a tax free first and

final dividend of Rs 1.00 per share, amounting to Rs 202.5

million on issued stated capital of ordinary voting shares

and Rs 1.00 per share amounting to Rs 101.25 million on

issued stated capital of non-voting ordinary shares of the

company for the financial year under review.

The dividend warrant will be posted on or before 21st

August 2013 and the shares will be quoted ex-dividend

with effect from on 12th August 2013 as per the rules of

Colombo Stock Exchange.

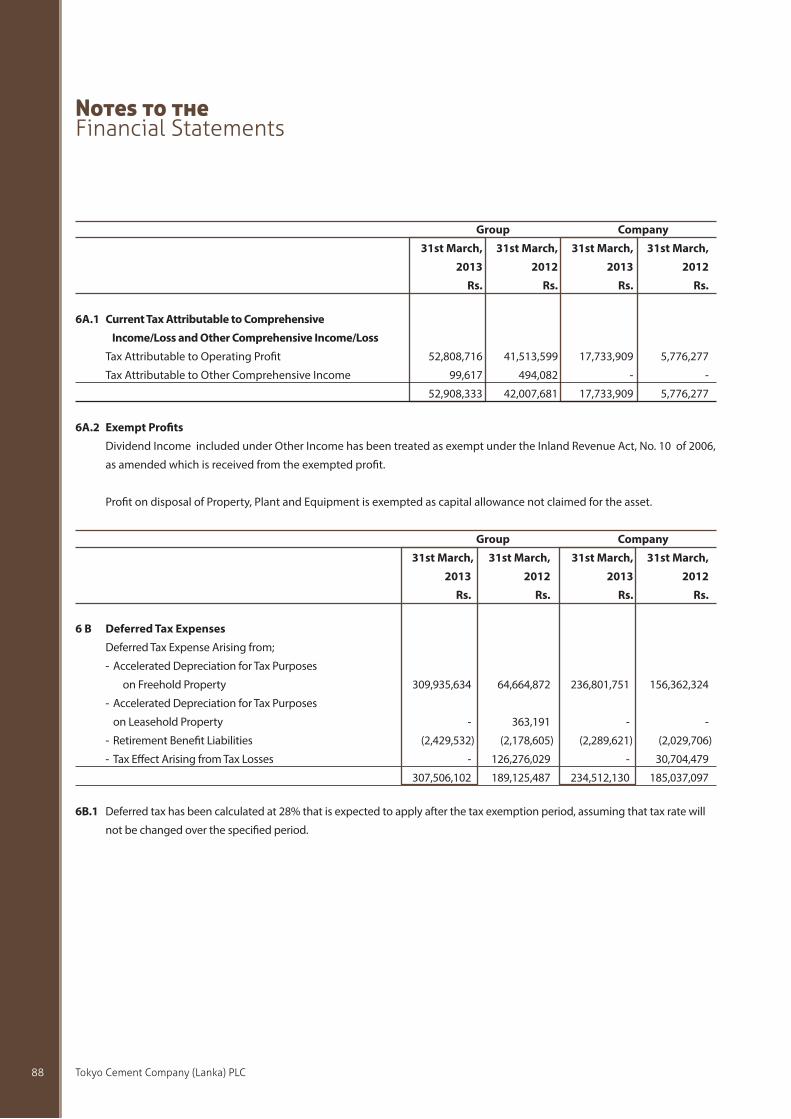

Earning per share

Please refer note 07 on page 89.

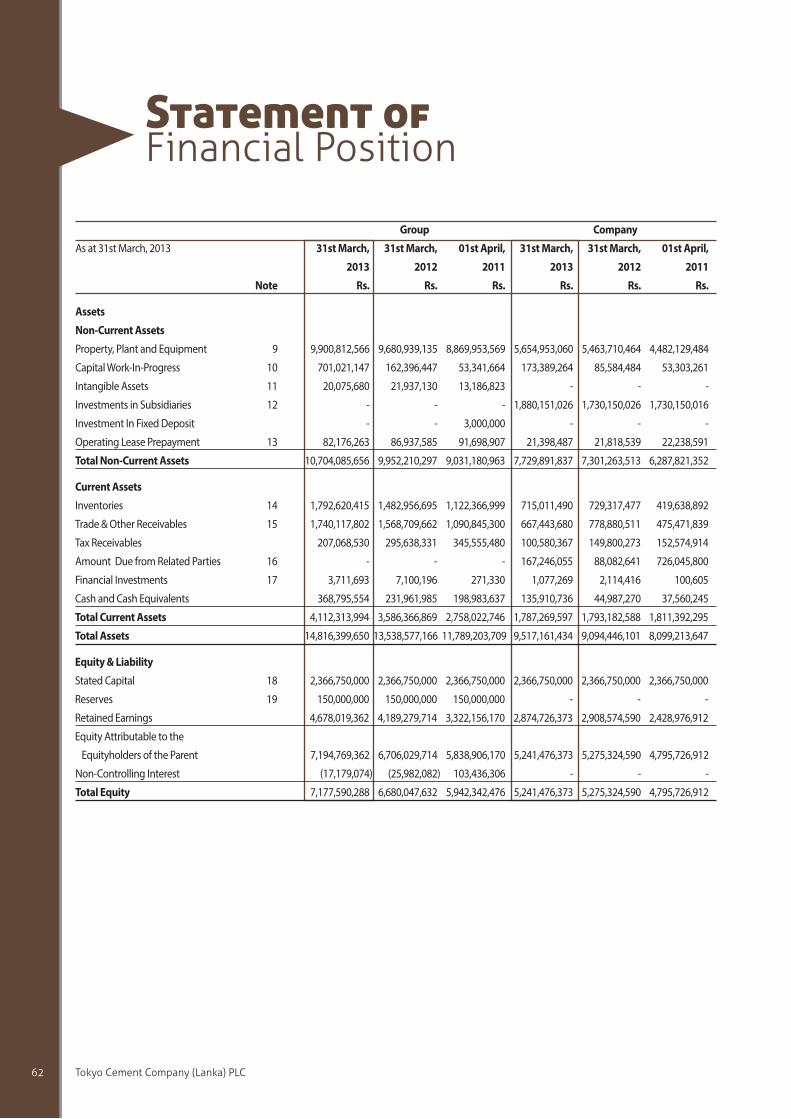

Financial position of the company and the group

Stated capital

The Company’s stated capital at the end of the year under

review, was represented by 202.5 million ordinary voting

shares and 101.25 million ordinary non-voting shares.

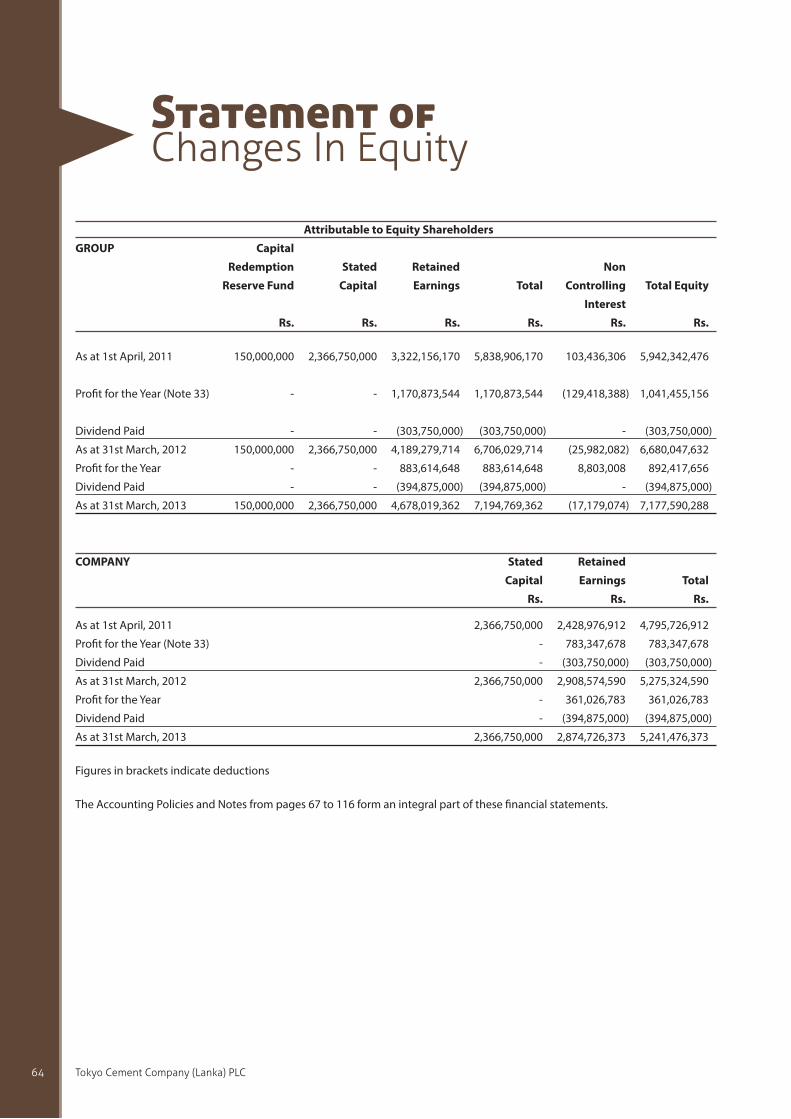

Reserves

The Group’s total reserves totaled Rs.4.8 billion, as at

March 31, 2013, compared with Rs. 4.3 billion a year

earlier. This includes Rs. 150 million in capital reserves and

Rs.4.7 billion in revenue reserves.

Debt

Group’s long term debts amounted to Rs.1.0 billion as

against Rs.1.5 billion in the previous year. Company long

term debts amounted to Rs.433 million rupees, as at

March 31, 2013, as against Rs.728 million a year earlier.

Group’s short term liabilities stood at Rs. 3.2 billion,

against Rs. 2.6 billion a year ago.

Group had incured a interest cost of Rs. 700 million during

the year as against Rs. 435 million incured in the previous

year.

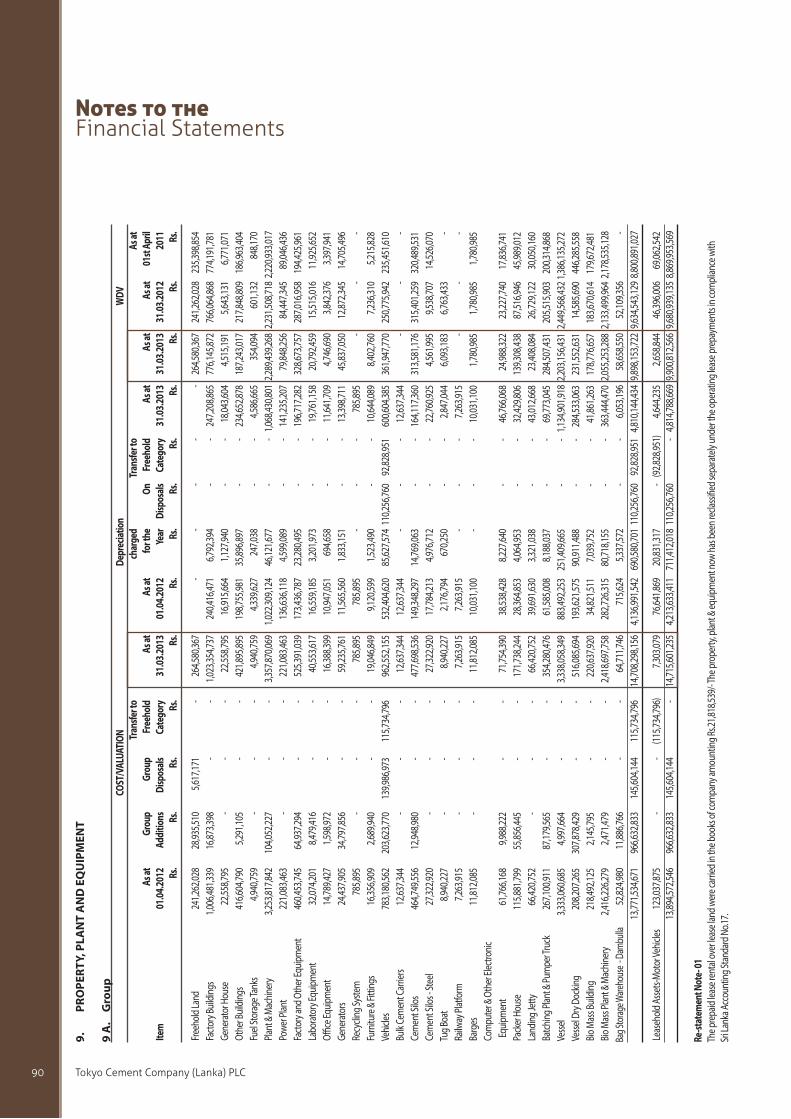

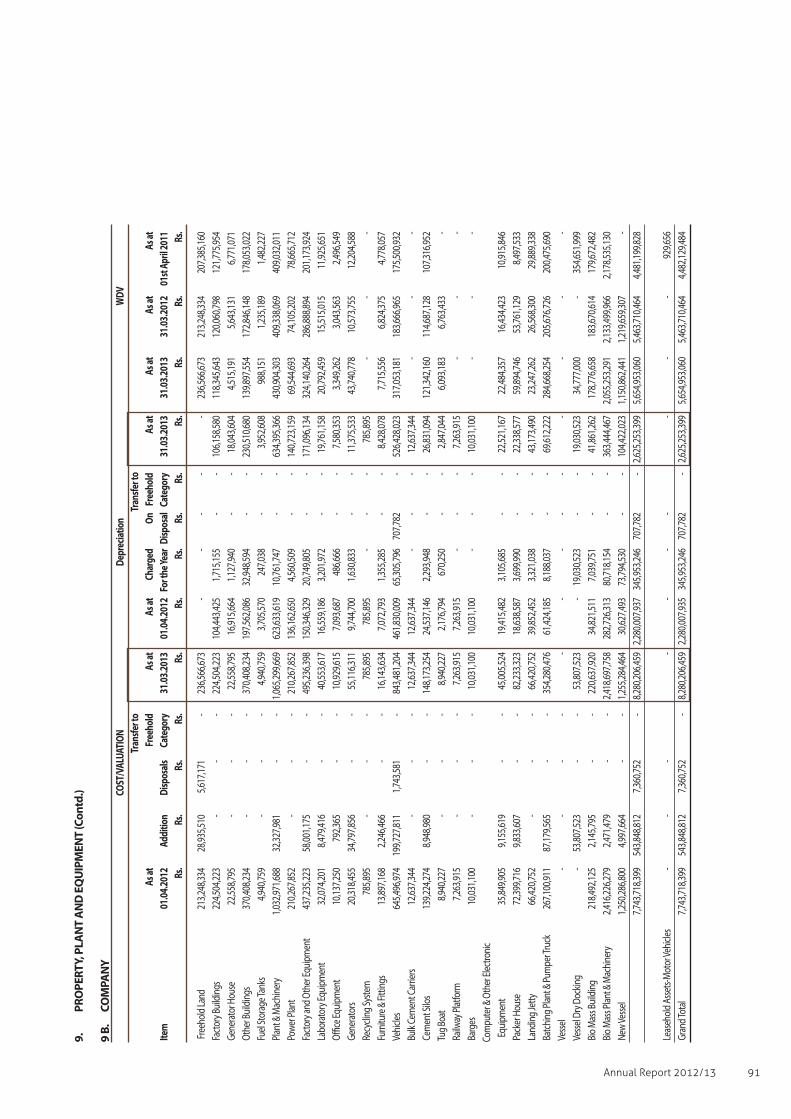

Property, plant and equipment

The consolidated property, plant and equipment costs,

at the year ended March 31, 2013 was Rs.14.7 billion,

as against Rs.13.9 billion recorded at the end of the

preceding year. The cost of company’s property, plant

and equipments at the year end were at Rs. 8.2 billion,

compared to Rs.7.7 billion a year earlier.

The group’s total capital expenditure for the year under

review was Rs.1.5 billion as against Rs.1.9 billion in the

previous year. A total of Rs.145.6 million worth of group

assets were disposed of during the year.

Details regarding the movement of assets extent and

location of propeties and number of buildings are

provided in the note 9 to the Financial Statements.

Current assets

The total current assets of the group, as at March 31, 2013,

were valued at Rs. 4.1 billion, as against Rs.3.6 billion in

the previous year. The total current assets of the company

stood at Rs. 1.8 billion as at 31st March 2013, as equivalent

to the current assets position of the company as of March

31, 2012.

Post-balance sheet events

Please refer note 31 on page 110.

Outstanding litigations

In the opinion of the Directors and the company lawyers/

legal counsel, litigations pending against the company

will not have major impact to the Financial Statements.

Contingencies and commitments

Information with regards to contingent liabilities and

capital commitments as at March 31, 2013, are given

35Annual Report 2012/13

in notes 26 & 27 on page 102 to 103 of the Financial

Statement.

Going concern

The preparation of financial statements have been done

on the going concern basis, as confirmed in the Statement

of Directors’ Responsibilities on page 54.

Shareholders information

Information provided separately from page 117 to 119.

Substantial shareholdings

The twenty Substantial shareholders and the percentage

held by each of them as at March 31, 2013 appear on

page 119.

Equitable tretment to shareholders

The directors at all times ensure that all shareholders are

treated equitably.

Information on the Board of Directors and Board sub committees

Board of Directors

Board committees

The Board has appointed a number of committees, with

specified terms of reference, to improve management

effectiveness of the company. Accordingly the following

committees have been constituted

The reports of the committees are given on page 56 to 59

of the Annual Report.

Directors’ responsibilities for financial statements

The Directors are responsible for the preparation and

presentation of Financial Statements of the company to

reflect a true and fair view of the state of its affairs. The

Statement of Directors’ Responsibilities for the Financial

Statements is given on page 54 of this Annual Report.

Recommendation for re-election

Mr. A. S. G. Gnanam retires by rotation in terms of the

articles of association of the company and offer himself

for re-election at the forthcoming annual general

meeting.

Mr. Edgar Gunatunga attend the age of 70 years on 2002

and in accordance with section 210 (2) of the companies

Act no 07 of 2007, vacates office at the forthcoming

Annual General Meeting. A notice of a resolution has

been received that the age limit of 70 years referred to in

section 210(1) of the said companies act shall not apply to

Mr. Edgar Gunatunga who has attend the age of 70 and

that he be re-elected as a Director at the Annual General

Meeting.

Directors’ remuneration

Directors’ remuneration in respect of the group and the

company for the financial year ended March 31, 2013 are

given in note 05 on page 86 of the Annual Report.

Directors’ Interests

The Directors’ Interests in the Company contracts appear

on page 107 to 109 of the Financial Statements and have

been declared at the meetings of the Directors.

Apart from the information disclosed, the Directors have

no other direct or indirect interest in any contracts or

proposed contracts pertaining to the business of the

group.

Mr. Edgar Gunatunga ChairmanMr. S.R. Gnanam Managing DirectorMr. A.S.G. Gnanam Non Executive DirectorMr. E.J. Gnanam Non Executive DirectorMr. R. Seevaratnam Non Executive Independent

DirectorDr. Harsha Cabral Non Executive Independent

DirectorDr. Indrajit Coomaraswamy Non Executive Independent

DirectorMr. T. Naruse Nominee Director of Nippon

Coke & Engineering Company Limited, Japan

Mr. S.V. Wanigasekera Nominee Director of Nippon Coke & Engineering Company Limited, Japan

Mr. S. Takihara Nominee Director of Nippon Coke & Engineering Company Limited, Japan

Tokyo Cement Company (Lanka) PLC36

Directors

Director’s meetings

The Board of Directors met eight times during the year

under review.

Director’s Shareholding

Director’s Shareholding - Ordinary Shares

Interest register

As required by the Companies Act No. 07 of 2007 Interest

Registers have been maintained by the company.

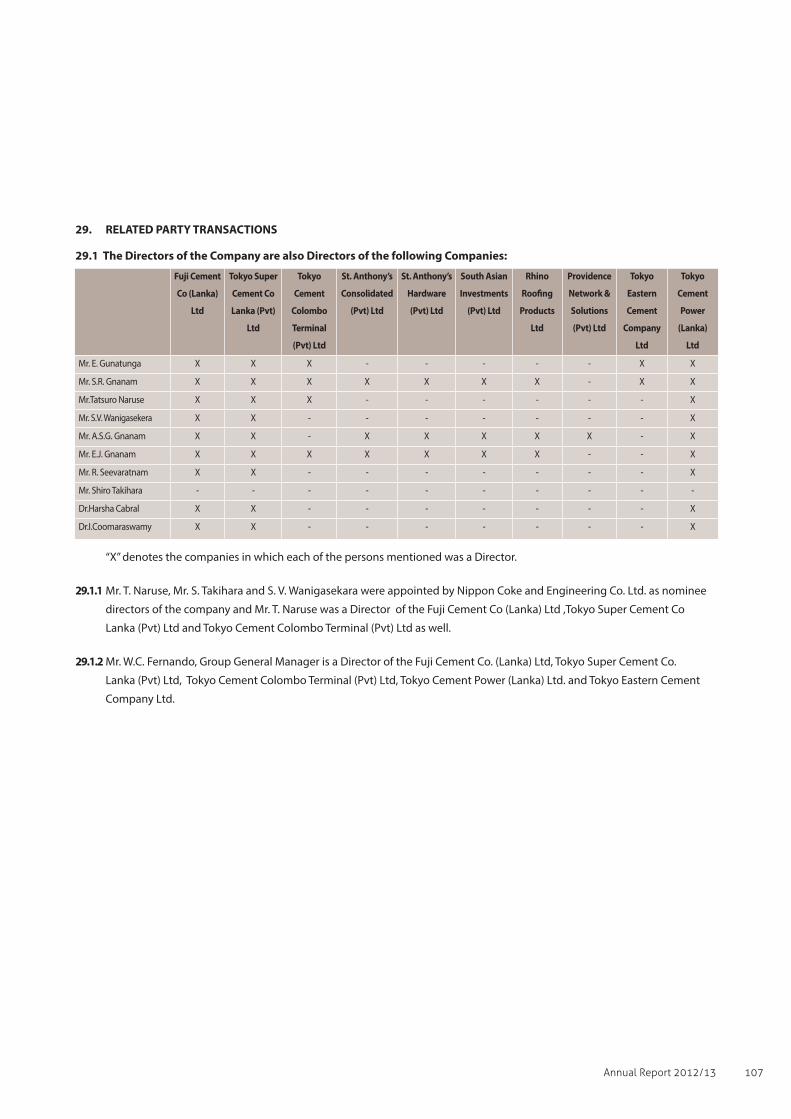

Related party transactions

Directors have disclosed related party transactions and

such transactions are given in notes 29 on page 107 to

109 of the Annual Report.

Employment policies

In employment practices, the group continues to abide by

its non-discriminatory policy on gender, race and religion.

The group respects each and every individual and career

advancement opportunities are provided to all employees

without exception.

The group is as committed as always to creating a

zero-lost-workday work environment, with occupational

health and safety being a primary imperative within our

operations.

We had a total of 669 permanent employees and 72

casual workers on our payroll as at March 31, 2013.

They received a total remuneration package of

Rs.449 million, which exceeds the remuneration payments

of the previous year by Rs.62 million rupees.

Corporate governance

The company considers sound governance measures

and appropriate internal control as an integral facet of

operations. The practices followed by the company are set

out on page 38 to 41.

Risk manangement

The directors have established and adhere to a

comprehensive risk management framework at both

strategic business units and group levels to ensure the

achivements of their corporate objectives. The categories

of risks faced by the group are identified and significance

of those risk are evaluated on basis of impact of such risks

and the probability of occurance of such risks. Based on

the significance of risks mitigating strategies are adopted

by the group. The Board of Directors reviews the risk

management process through the audit committee. The

risk management report of the group is on pages 42 to 43

of this report.

Voting ordinary shares Non voting ordinary shares

No of shares

held as at March

31, 2013

No of shares

held as at March

31, 2012

No of shares

held as at March

31, 2013

No of shares

held as at

March

31, 2012

Local Joint Venture Partner -

St. Anthony’s Consolidated (Pvt) Ltd. 55,687,252 55,687,252 - -

Mr. Gnanam A. S. G. 11 11 - -

Mr. Gnanam S. R. - Managing Director 11 11 - -

Mr. Gnanam E. J. 11 11 - -

Mr. Edgar Gunatunga - Chairman 2,212 - 1,000 -

Foreign Joint Venture Partner - Nippon Coke & Engineering Co. Ltd. 49,004,932 55,687,432 - -

Nominee Directors of Foreign Collaborator - - -

Mr. Wanigasekera S. V. 5,400 5,400 14,487 13,487

Mr. Naruse T. - - - -

Mr. Takihara S. Independent Directors - - - -

Mr. Ranjeevan Seevaratnam - - - -

Dr. Harsha Cabral - - - -

Dr. Indrajit Coomaraswamy - - - -

Total 104,699,829 111,380,117 15,487 13,487

Total Shares in Issued 202,500,000 202,500,000 101,250,000 101,250,000

37Annual Report 2012/13

Internal controls

The Board of Directors ensures that the group has an

effective internal control system which ensures that

assets of the company and the group are safeguarded

and appropriate systems are in place to minimize and

detect frauds, errors and other irregularities. The system

ensures that the group adapts procedures which result in

financial and operational effectiveness and efficiency. The

statement of directors responsibilities on page 54 and the

audit committee report setout on page 56 of this report

provide further infomation in respect of the above.

Statutory payments

The Directors to the best of their knowledege are satisfied

that all statutory financial obligation to the government

and to the employees have been either duly paid or

adequately provided for in the financial statements. A

confirmation of same is included in the statement of

directors responsibilities on page 54 of this annual report.

Customers

The Directors consider the patronage extended by our

customers as invaluable, titling them - the greatest source

of strength and inspiration in the forward journey of

the company. The company continues to be committed

to provide total satisfaction to our customer base by

enhancing the quality of our products and services.

Suppliers

The group continues to thrive on the strong bonds with

all its suppliers, based on trust and reliability.

Sustainability

The company continues its unequivocal commitment to

environmental conservation and preservation, instituting

best practices in the effecient use of natural resources

to ensure that future generation will have a planet that’s

green, safe and healthy. Company is the first Sri Lankan

Company in cement industry to obtain the ISO 14001

Environmental Management Certificate, and during the year

2011/12 laboratories of our company qualified for ISO 17025

standards. During the year under review our vocational

traning institute in Dambulla, the A Y S Gnanam construction

traning acadamy was recognised by the ceylon chamber

of commerce as the best CSR project in 2012. Details of our

activities are given in sustainability report in in page 46 to 51

of this annual report.

Research and Development (R&D)

The company continued to invest in R&D this year as well.

Auditors

The independent auditors report on the financial statements

is given on page 60 of the annual report. The retiring auditors

Messrs BDO Partners, Chartered Accountants have stated

their willingness to continue in office and resolution to

grant authority to the Board to determine their remuneration

will be proposed at the Annual General Meeting.

The fees payable to auditors Messrs BDO Partners, Chartered

Accountants are given in note 05 on page 86 of the annual

report. As far as the directors are aware, the auditors have

neither any other relationship with the company nor

any of its subsidiries that would have an impact on their

independence.

Messrs BDO Partners, Chartered Accountants, the auditors of

the company are also the auditors of all subsidiaries of the

group. The list of subsidiaries, audited by them is included on

page 69 of the annual report.

Annual general meeting

The Annual General Meeting will be held on 8th August

2013. The notice of the Annual General Meeting appears on

page 124.

S R Gnanam T Naruse

Managing Director Director

Seccom (Private) Limited

Company Secretaries

29th June 2013

Tokyo Cement Company (Lanka) PLC3838

Governance

Corporate governance is expected to achieve

strategic aims of the business within a sound

framework of controls in the best interest of

stakeholders in compliance with laws, regulations

of the country while maintaining higher standards

of business ethics.

We maintain the highest standards in corporate

governance, instituting best practices in all

areas to ensure complete transparency and

accountability in terms of principles and provisions

laid down in the Code of Best Practice on

Corporate Governance published by the Institute

of Chartered Accountants of Sri Lanka (ICASL).

Being the only listed corporate entity in

Sri Lanka who manufacture cement, our

corporate governance framework is based

on a comprehensive approach to sustainable

development and environmental protection which

is beyond mere compliance with the rules and

regulations.

Board of Directors

Shareholders appoint Board of Directors at the

Annual General Meeting except for the nominee

Directors of Nippon Coke & Engineering Co. Ltd.

Board of Directors consists of ten (10) members.

Of the Board of Directors three (3) Directors are

Independent non-executive Directors and five (5)

directors are non-executive Directors. Company is

a joint venture by St. Anthony’s consolidated (Pvt)

Ltd and Nippon Coke & Engineering Co. Ltd.

All Non-Executive Directors are professionals

in the field of banking,economic, legal and

accountancy with vast experience in business and

administration.

Corporate Governance Process

The Board of Directors formulates overall

business strategy in association with corporate

management and determine corporate goals

which are communicated down the management

hierarchy through a systematic budgetary control

procedure approved by the Board of Directors.

Board of Directors review the corporate and

operational performance of the group each month

in the context of political economic social and

technological environment and provide direction

to corporate management in managing the

business. In order to assist the Board of Directors

in implementation of their role following sub

committees have been formed.

Audit Committee

The Audit Committee comprises of four Non-

Executive Directors of which two are independent.

Chairmen of the Audit Committee is a member of

the Institute of Chartered Accountants of Sri Lanka.

Audit Committee assists the Board of Directors in

its general oversight of financial reporting, Risk

Management, internal controls and functions

relating to internal and external audit and

monitoring of compliance with laws, regulations

and best practices.

This Committee meets quarterly and the Managing

Director, Group General Manager, Chief Financial

Officer and Internal Auditor participates Audit

Committee meeting upon invitation. The report of

the Audit Committee appears on page 56 to 57.

Audit Committee Members

Mr. R. Seevaratnam - Chairman

Mr. Edgar Gunatunga

Mr. S. V. Wanigasekera

Dr. Harsha Cabraal

Remuneration Committee

The Remuneration Committee comprises three

Directors of which two are an Independent

Non-Executive Director’s. The Committee is

empowered to examine any matters relating to

remuneration paid to executive members. Their

terms of reference also encompass the review of

39Annual Report 2012/13

matters relating to human resources management of the

Company.

Remuneration Committee Members

Dr. Harsh Cabral - Chairman

Mr. R. Seevaratnam

Mr. S. R. Gnanam

Nomination Committee

The Nomination Committee comprises six directors of

which three are an independent Non-Executive Directors.

The Committee is responsible for recommend to board

the process of selecting Chairman and Managing Director,

Identifying suitable persons for appointment to the Board

as Executive and Non-Executive Directors.

Nomination Committee Members

Dr. Indrajit Coomaraswamy - Chairman

Mr. Edgar Gunatunga

Mr. S. R. Gnanam

Mr. T. Naruse

Mr. R. Seevaratnam

Dr. Harsha Cabral

Internal Control and Monitoring

Board of Directors are responsible for maintenance

of an effective system of internal control to ensure

effectiveness and efficiency of operations, reliability of

financial reporting, compliance with applicable laws

and regulations, conduct its business in an orderly and

efficient manner, safeguard its assets and resources, deter

and detect errors, fraud, and theft, ensure accuracy and

completeness of its accounting data, produce reliable

and timely financial and management information, and

ensure adherence to its policies and plans.

Board of directors achieve monitoring of operations

through monthly board meetings and review of various

management information obtained at these meetings

including reports of the intenal auditors. Internal Control

is implemented through the corporate management

by ensuring adherence to board accepted policies

and adequacy of internal control implemented by the

management is measured through the Internal Audit

team who shall review the systems and controls in

accordance with a board approved audit plan.

This includes surprise audits of sales depots, ready

mix cement operations, and factory. These reports are

scrutinised and discussed by the members of the Audit

Committee and suitable action is taken where necessary,

in consultation with senior management. Members

of the Audit Committee also reviews monthly/interim

financial statements submitted to the Board, and ensures

financial information reported are in compliance with

various accounting standards promulgated by Institute of

Chartered Accountants of Sri Lanka.

Information Technology

Group has initiated implementation of a Enterprise

Resource Planning system wide across the company and

its subsidiaries to integrate the corporate headquarters,

sales depots, and factory. While IT facilitates transaction

processing and reporting in a more systematic and

effective manner it also entail IT governance risk which

affect confidentiality integrity and availability. Board

is aware of the risk IT entails and necessary IT system

security and controls have been taken into consideration

and will be further reviewed when the ERP system is fully

operational in compliances with best practices for IT

governance and risk management.

Going Concern

The Board is tasked with ensuring that the company is

a ‘going concern’ and therefore adopts processes and

features into its decision making and in the preparation

of financial statements, to form a solid foundation of

sufficient resources to continue operations into the

foreseeable future.

Transparency

The Board discloses full information, both financial

and non financial information within the bounds of

commercial realities. Being the only cement manufacturer

Tokyo Cement Company (Lanka) PLC40

Governance

listed on the Colombo Stock Exchange, it is committed

to a responsible business philosophy. Publication of

quarterly accounts and the release of the Annual Report

and Audited Accounts are complied within the stipulated

time frame.

Investor Relations

The Company continues to maintain good

communication with all shareholders comprising both

corporates and individuals. The Board invites questions

from shareholders during the General Meeting. In

addition, the Chairman and Executive Directors meet

institutional investors and analysts to discuss the

company’s performance. Share price sensitive information

not available to other shareholders is not divulged during

this meeting.

Shareholder Value and Returns

We are firmly committed to constituting a Board of

Directors who are eminent, erudite and well respected as

we strongly believe that this adds value to the company,

a fact that is reflected in the strong share value we have

gained over the years. The Board also maintains an

attractive dividend rate aligned to the expectations of the

shareholders as well as for Capital formations of future

expansion.

External governance

As a responsible corporate citizen group adheres to

regulations, codes of best practices etc, adopted by

different governing bodies including following:

issued by Institute of Chartered Accountants of Sri

Lanka and Securities & Exchange Commission of Sri

Lanka

of 2002 and other revenue related regulations and

subsequent amendment

amendments

the industry in force

We summarise below the extent to which the group is

in compliance with the rules set out in Section 7.10 of

the Colombo Stock Exchange listing rules on corporate

governance.

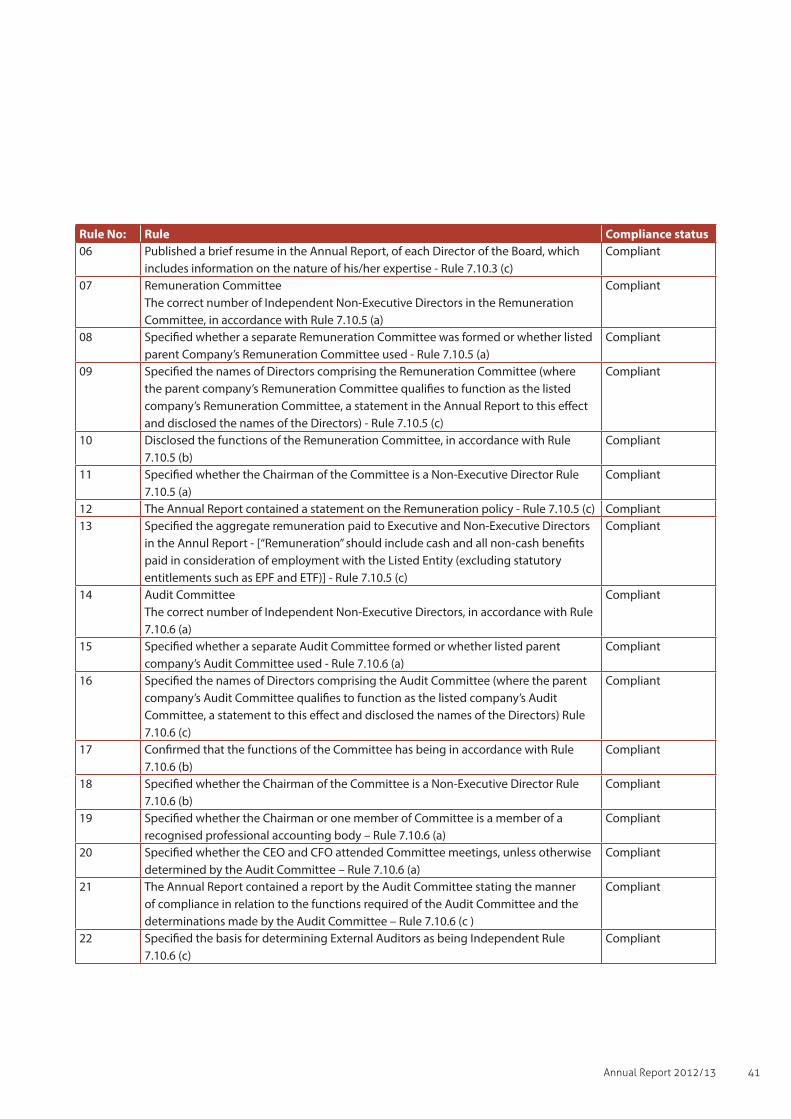

Rule No: Rule Compliance status

01 Board of Directors

The correct number of Non-Executive Directors, in accordance with Rule 7.10.1 (a)

Compliant

02 The correct number of Independent Non-Executive Directors, in accordance with Rule

7.10.2 (a)

Compliant

03 Specified whether the Non-Executive Directors submitted a Declaration annually of

his/her independence or non-independence to the Board of Directors - Rule 7.10.2 (b)

Compliant

04 Confirmed that the Board of Directors made an annual determination as to the

independence or non-independence of each Non-Executive Director based on the

Declaration mentioned above and other information available to the Board and states

the names of Non-Executive Directors determined to be ‘Independent’ – Rule 7.10.3 (a)

Compliant

05 If the Director does not qualify as ‘Independent’, but if the Board taking into account all

the circumstances is of the opinion that the Non-Executive Directors is ‘Independent”,

the Board has specified, in the Annual Report, the qualification not met under Rule

7.10.4 of the CSE Listing Rules and the basis for determining the Director to be

‘Independent’ Rule 7.10.3 (b)

N/A

41Annual Report 2012/13

Rule No: Rule Compliance status

06 Published a brief resume in the Annual Report, of each Director of the Board, which

includes information on the nature of his/her expertise - Rule 7.10.3 (c)

Compliant

07 Remuneration Committee

The correct number of Independent Non-Executive Directors in the Remuneration

Committee, in accordance with Rule 7.10.5 (a)

Compliant

08 Specified whether a separate Remuneration Committee was formed or whether listed

parent Company’s Remuneration Committee used - Rule 7.10.5 (a)

Compliant

09 Specified the names of Directors comprising the Remuneration Committee (where

the parent company’s Remuneration Committee qualifies to function as the listed

company’s Remuneration Committee, a statement in the Annual Report to this effect

and disclosed the names of the Directors) - Rule 7.10.5 (c)

Compliant

10 Disclosed the functions of the Remuneration Committee, in accordance with Rule

7.10.5 (b)

Compliant

11 Specified whether the Chairman of the Committee is a Non-Executive Director Rule

7.10.5 (a)

Compliant

12 The Annual Report contained a statement on the Remuneration policy - Rule 7.10.5 (c) Compliant

13 Specified the aggregate remuneration paid to Executive and Non-Executive Directors

in the Annul Report - [“Remuneration” should include cash and all non-cash benefits

paid in consideration of employment with the Listed Entity (excluding statutory

entitlements such as EPF and ETF)] - Rule 7.10.5 (c)

Compliant

14 Audit Committee

The correct number of Independent Non-Executive Directors, in accordance with Rule

7.10.6 (a)

Compliant

15 Specified whether a separate Audit Committee formed or whether listed parent

company’s Audit Committee used - Rule 7.10.6 (a)

Compliant

16 Specified the names of Directors comprising the Audit Committee (where the parent

company’s Audit Committee qualifies to function as the listed company’s Audit

Committee, a statement to this effect and disclosed the names of the Directors) Rule

7.10.6 (c)

Compliant

17 Confirmed that the functions of the Committee has being in accordance with Rule

7.10.6 (b)

Compliant

18 Specified whether the Chairman of the Committee is a Non-Executive Director Rule

7.10.6 (b)

Compliant

19 Specified whether the Chairman or one member of Committee is a member of a

recognised professional accounting body – Rule 7.10.6 (a)

Compliant

20 Specified whether the CEO and CFO attended Committee meetings, unless otherwise

determined by the Audit Committee – Rule 7.10.6 (a)

Compliant

21 The Annual Report contained a report by the Audit Committee stating the manner

of compliance in relation to the functions required of the Audit Committee and the

determinations made by the Audit Committee – Rule 7.10.6 (c )

Compliant

22 Specified the basis for determining External Auditors as being Independent Rule

7.10.6 (c)

Compliant

Tokyo Cement Company (Lanka) PLC42

Risk

Management

Enterprise risk management is a process, effected

by an entity’s board of directors, management,

and other personnel, applied in strategy

setting and across the enterprise, designed

to identify potential events that may affect

the entity, and manage risk to be within the

risk appetite, to provide reasonable assurance

regarding the achievement of entity objectives.

Companies set themselves strategic and business

objectives, then manage risks that threaten

the achievement of those objectives. Internal

control and risk management should supplement

entrepreneurship, but not replace it. Increased

shareholder value is the reward for successful risk

taking and the role of internal control is to manage

risk appropriately rather than to eliminate it.

At Tokyo Cement first defense line of risk

management is rest with the divisional managers

who identify risks at their operations, evaluating

and managing the risks that they originate

within the approved risk appetite and policies

set by the board of directors. The second line of

defense includes the support functions, finance,

administration, operations, and technology. Each

of these functions, in close relationship with the

business units, ensures that risks in the business

units have been appropriately identified and

managed. The third line of defense is the internal

audit function that independently assesses the

effectiveness of the processes created in the

first and second lines of defense and provides

assurance on these processes to the Board of

Directors through the Audit Committee.

Risks are assessed on the basis of the consequence

of risks if such risk materializes and the likelihood

of materializing such risk. Any significant risk

above a threshold is requiring the response of the

management. Risks are assessed both as gross risk

and net risk. The assessment of gross risk involves

the identification of possible effect without any

mitigating actions. Net risk assessment considers

possible loss when mitigating action taken.

Major risks, evaluation of those risks in terms of

impact if those risks occur and probability of such

occurrence and mitigating actions to detect such

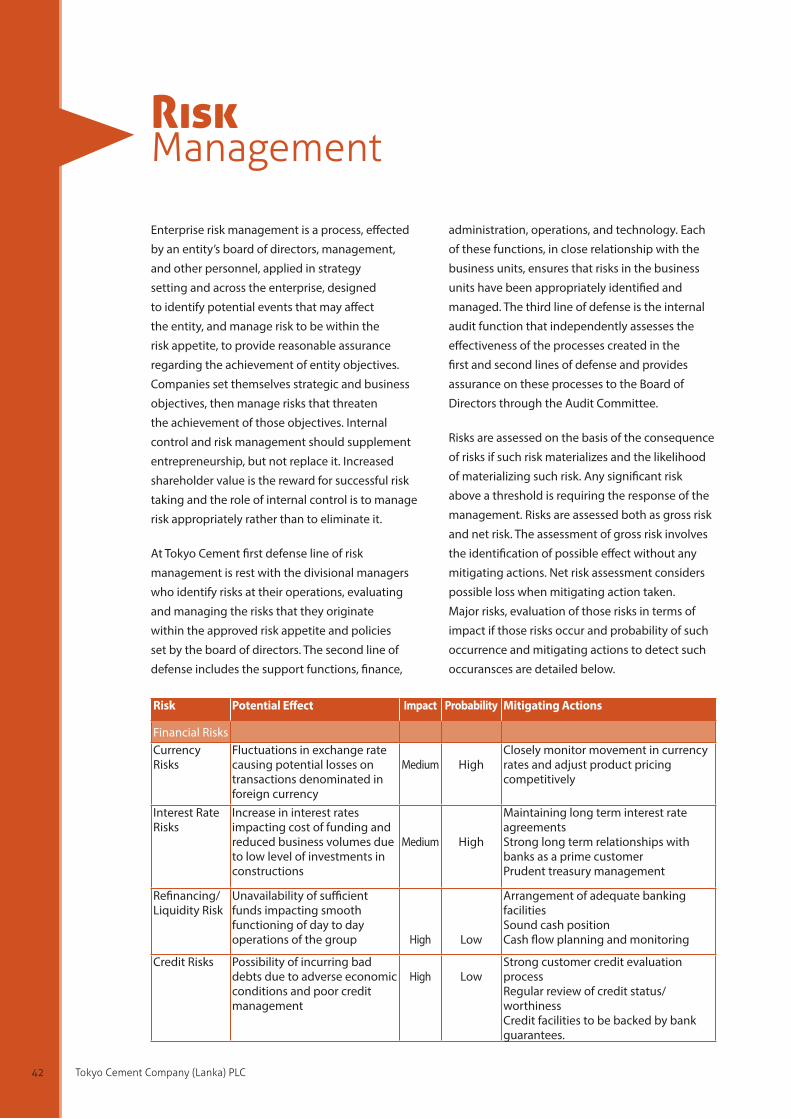

occuransces are detailed below.

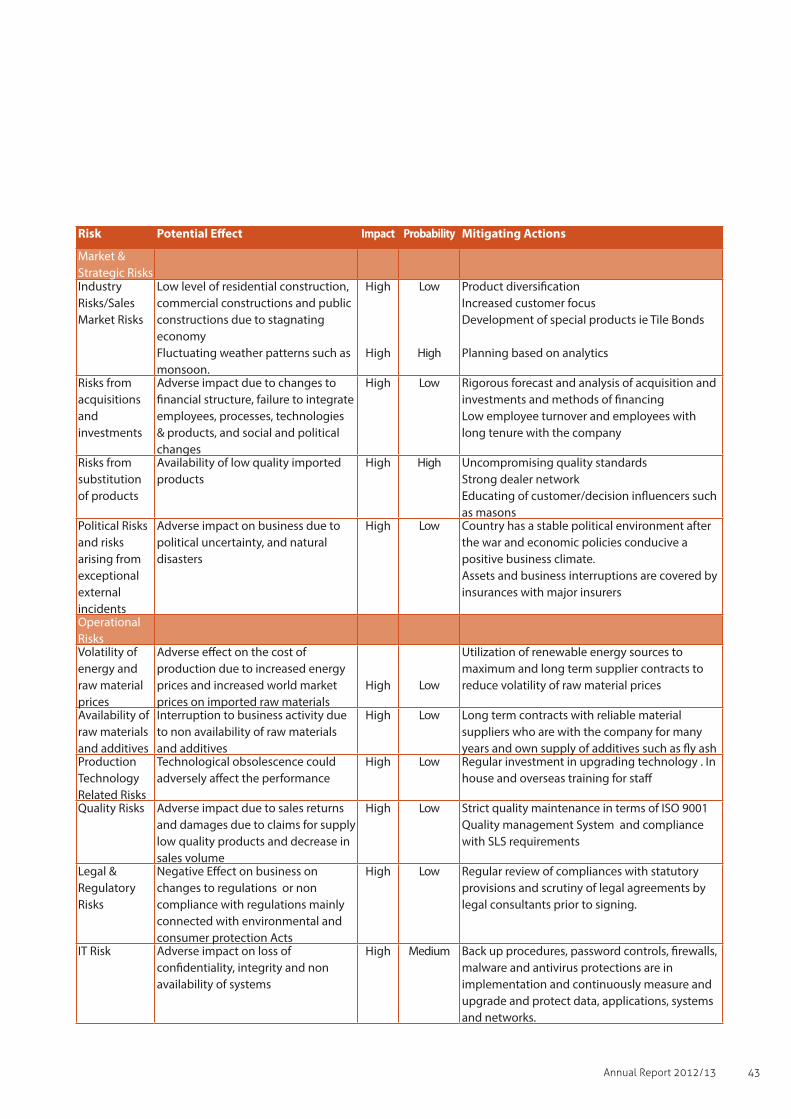

Risk Potential Effect Impact Probability Mitigating Actions

Financial Risks

Currency Risks

Fluctuations in exchange rate causing potential losses on transactions denominated in foreign currency

Medium HighClosely monitor movement in currency rates and adjust product pricing competitively

Interest Rate Risks

Increase in interest rates impacting cost of funding and reduced business volumes due to low level of investments in constructions

Medium High

Maintaining long term interest rate agreementsStrong long term relationships with banks as a prime customerPrudent treasury management

Refinancing/Liquidity Risk

Unavailability of sufficient funds impacting smooth functioning of day to day operations of the group High Low

Arrangement of adequate banking facilitiesSound cash position Cash flow planning and monitoring

Credit Risks Possibility of incurring bad debts due to adverse economic conditions and poor credit management

High LowStrong customer credit evaluation processRegular review of credit status/worthinessCredit facilities to be backed by bank guarantees.

43Annual Report 2012/13

Risk Potential Effect Impact Probability Mitigating Actions

Market &

Strategic RisksIndustry