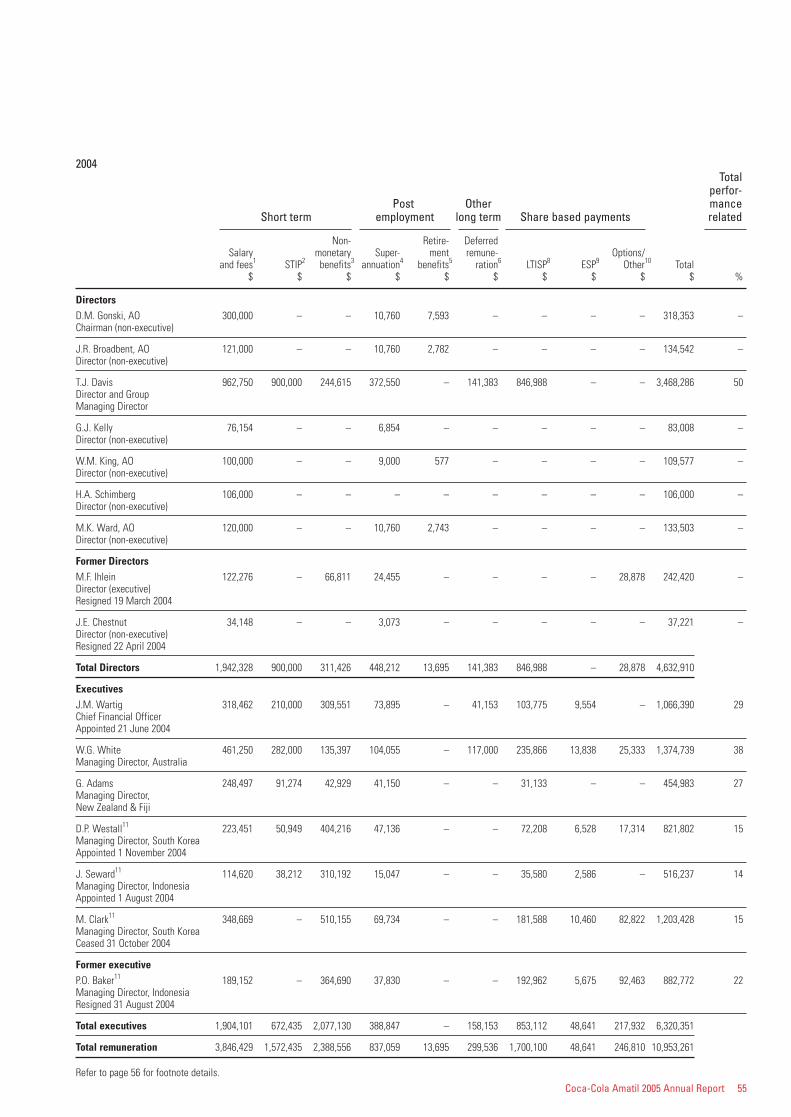

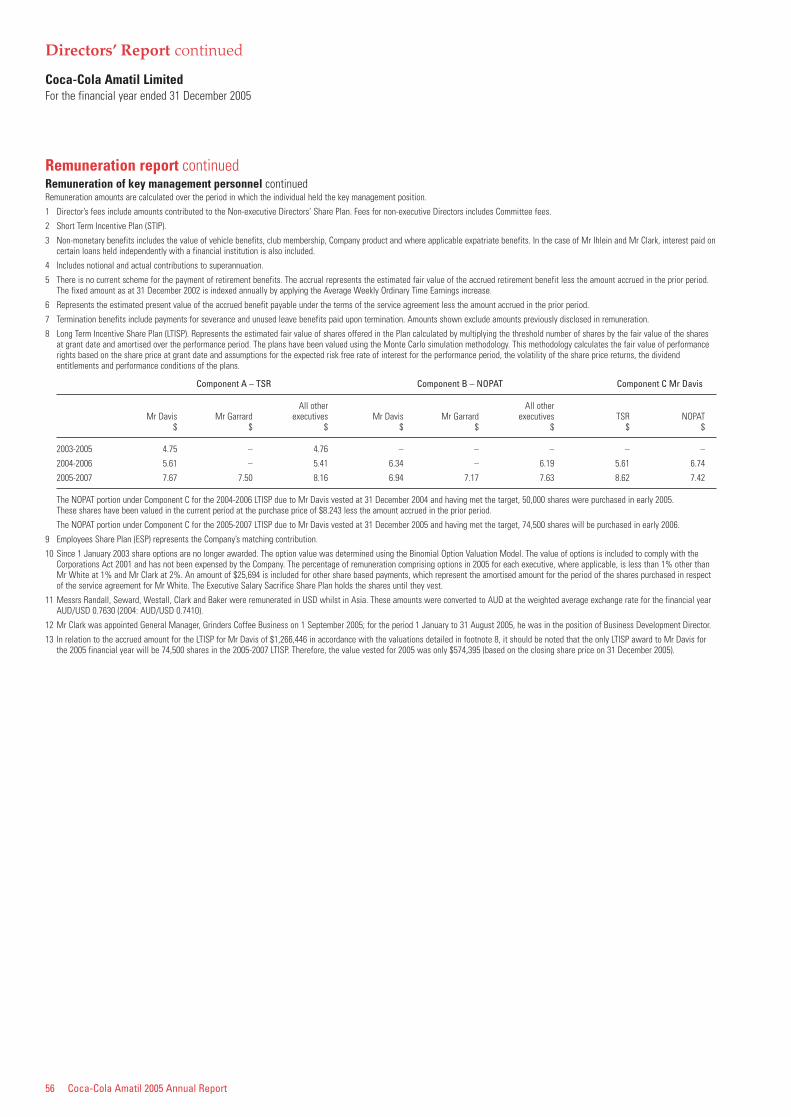

Embed Size (px)

Citation preview

All day. Every day.

Annual Report 2005

Contents

Chairman’s Report 2

Group Managing Director’s Review of Operations 4

Key Business Drivers 8

CCA at a Glance 14

Business Review 16

Five Year Financial Performance Summary 21

Corporate Social Responsibilities Report 22

CCA People 26

Senior Management 29

Board of Directors 30

Corporate Governance 32

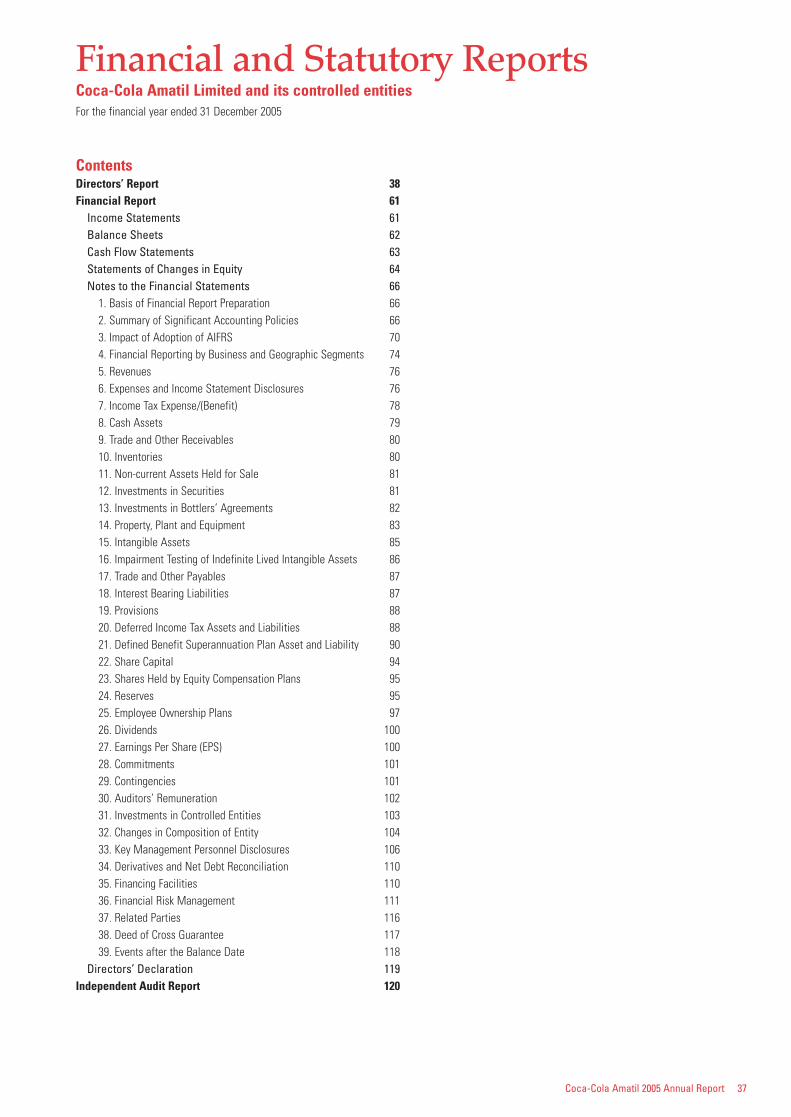

Financial and Statutory Reports 37

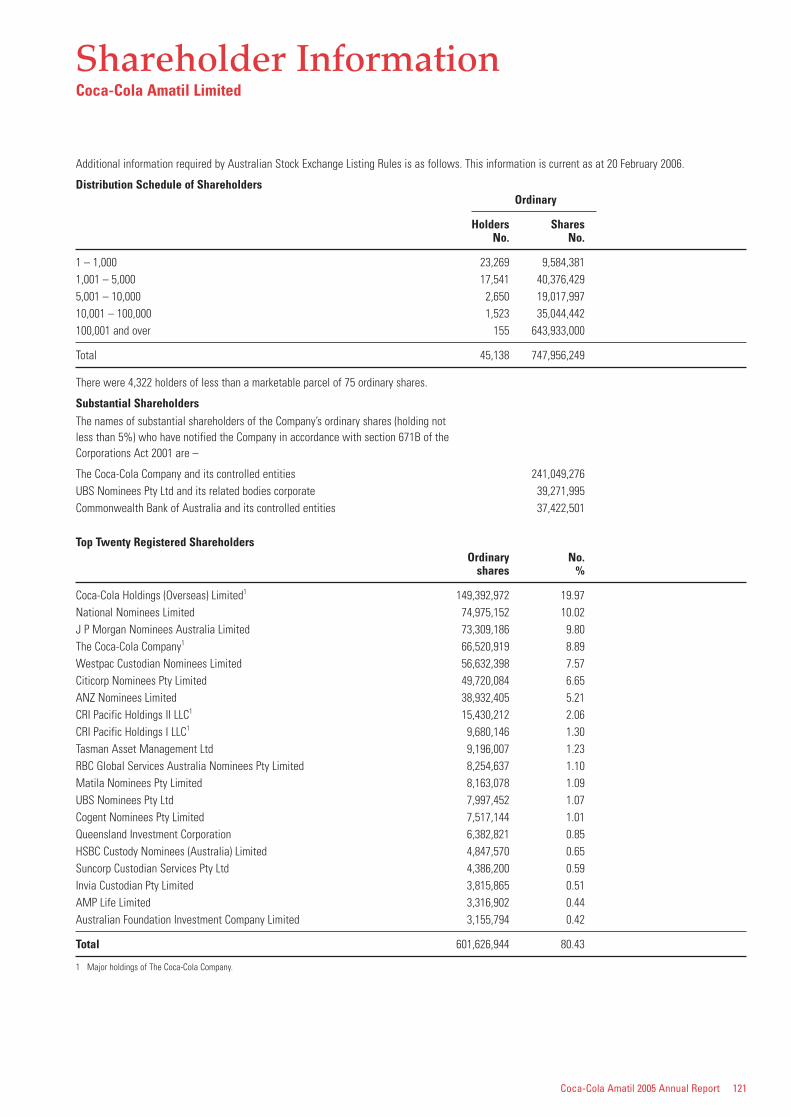

Shareholder Information 121

Glossary 123

Company Directories 124

Calendar of Events 2006 125

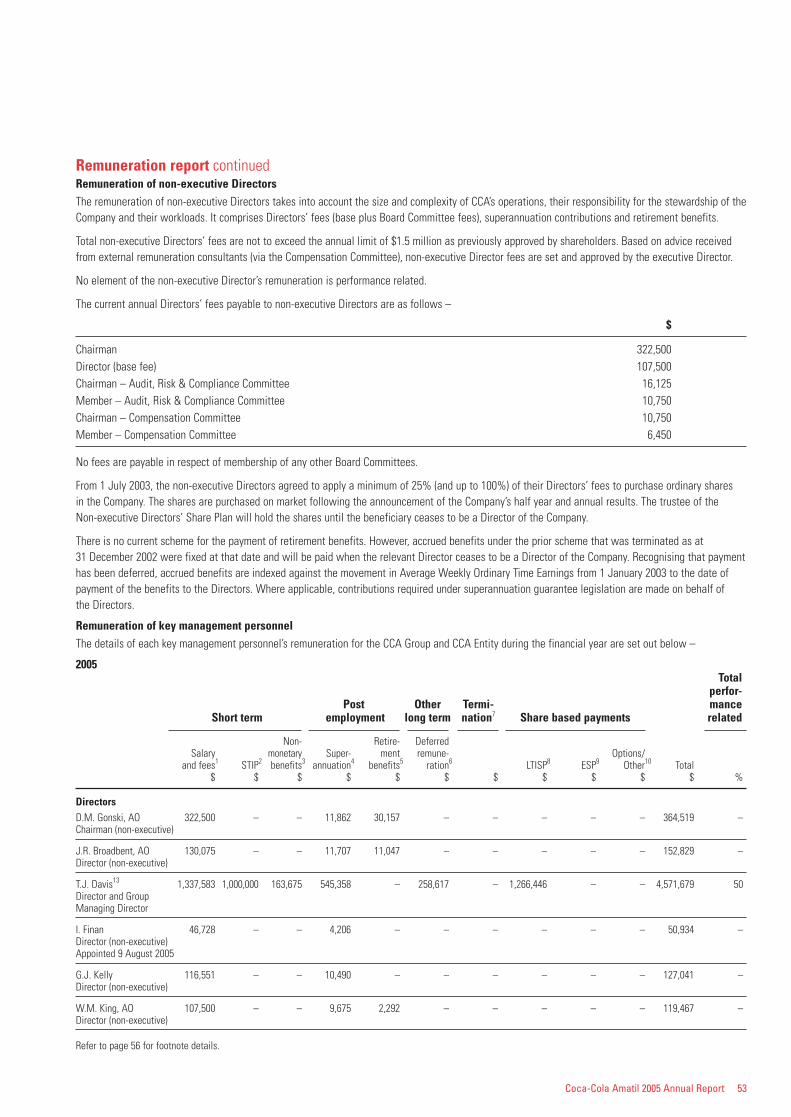

AGMAnnual General Meeting will be held on Wednesday, 3 May 2006 at 2pm at the City Recital Hall, Angel Place(Pitt Street entrance), Sydney.

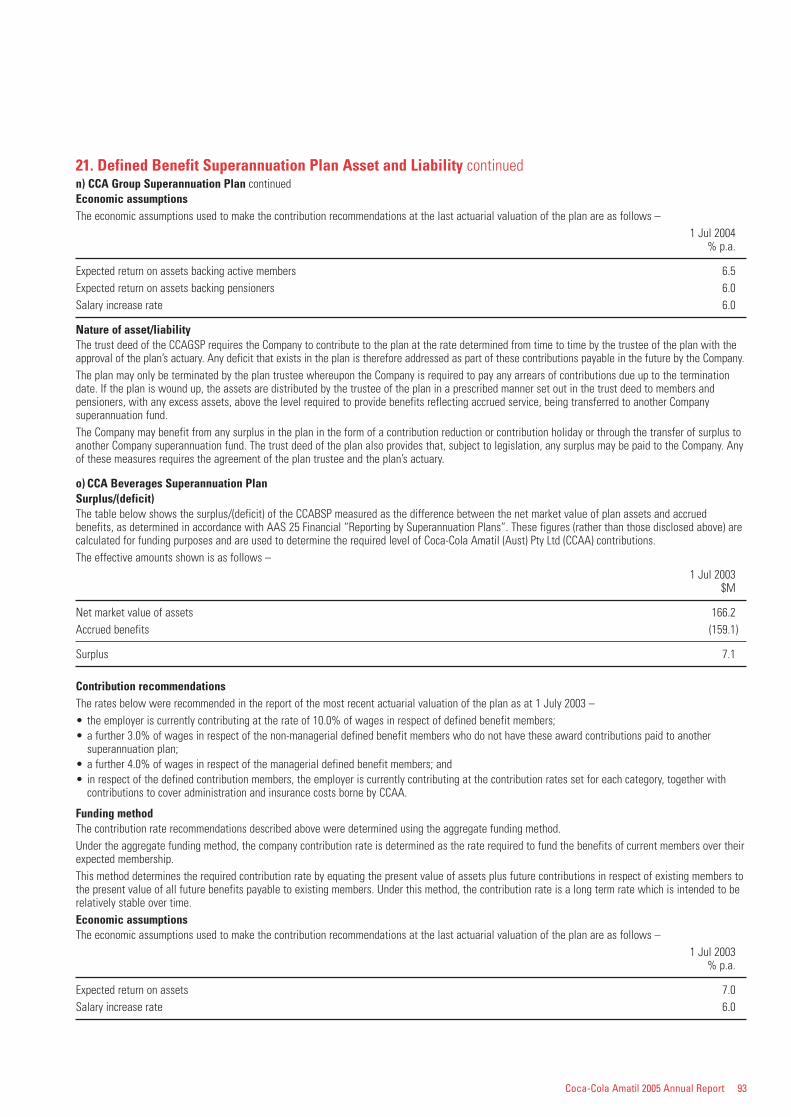

In 2005, Coca-Cola Amatil (CCA) delivered another strong result with its fifth consecutive year of double-digitnet profit growth. This has been achieved by continuing to focus on innovation and expansion of the brandportfolio, increasing the availability of products whilestriving to become the supplier of choice every time to ourcustomers. In doing so, CCA is able to refresh, energise and hydrate our consumers - all day every day.

2 Coca-Cola Amatil 2005 Annual Report

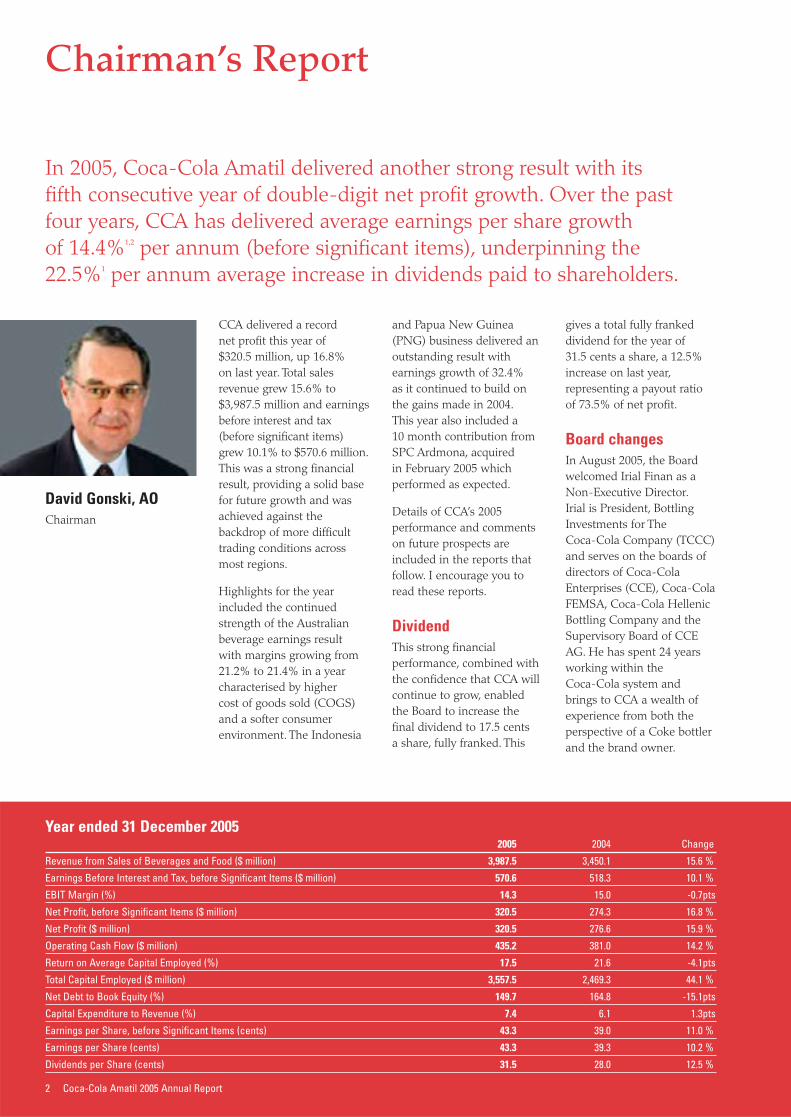

Chairman’s Report

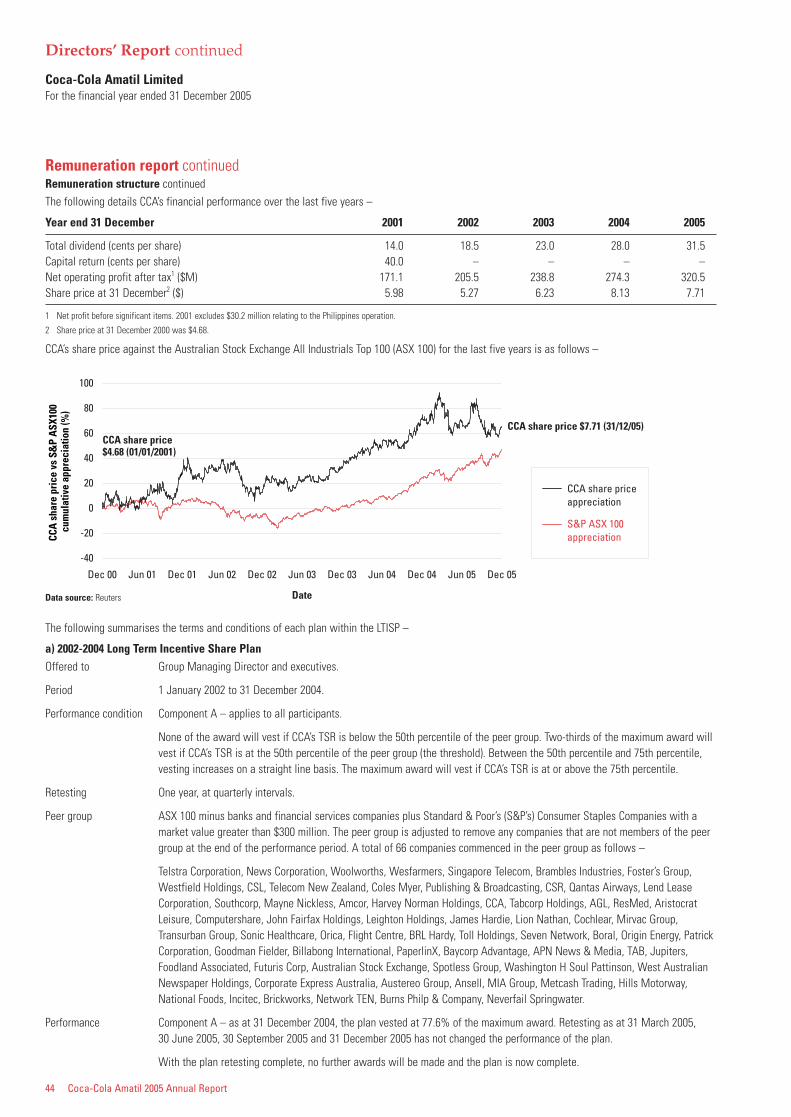

In 2005, Coca-Cola Amatil delivered another strong result with its fifth consecutive year of double-digit net profit growth. Over the past four years, CCA has delivered average earnings per share growth of 14.4%1,2 per annum (before significant items), underpinning the 22.5%1 per annum average increase in dividends paid to shareholders.

CCA delivered a record net profit this year of $320.5 million, up 16.8% on last year. Total salesrevenue grew 15.6% to$3,987.5 million and earningsbefore interest and tax(before significant items)grew 10.1% to $570.6 million.This was a strong financialresult, providing a solid basefor future growth and wasachieved against thebackdrop of more difficulttrading conditions acrossmost regions.

Highlights for the yearincluded the continuedstrength of the Australianbeverage earnings result with margins growing from21.2% to 21.4% in a yearcharacterised by higher cost of goods sold (COGS)and a softer consumerenvironment. The Indonesia

and Papua New Guinea(PNG) business delivered anoutstanding result withearnings growth of 32.4% as it continued to build onthe gains made in 2004.This year also included a 10 month contribution fromSPC Ardmona, acquired in February 2005 whichperformed as expected.

Details of CCA’s 2005performance and commentson future prospects areincluded in the reports thatfollow. I encourage you toread these reports.

DividendThis strong financialperformance, combined withthe confidence that CCA willcontinue to grow, enabledthe Board to increase thefinal dividend to 17.5 cents a share, fully franked. This

gives a total fully frankeddividend for the year of 31.5 cents a share, a 12.5%increase on last year,representing a payout ratio of 73.5% of net profit.

Board changesIn August 2005, the Boardwelcomed Irial Finan as aNon-Executive Director.Irial is President, BottlingInvestments for The Coca-Cola Company (TCCC)and serves on the boards ofdirectors of Coca-ColaEnterprises (CCE), Coca-ColaFEMSA, Coca-Cola HellenicBottling Company and theSupervisory Board of CCEAG. He has spent 24 yearsworking within the Coca-Cola system and brings to CCA a wealth ofexperience from both theperspective of a Coke bottlerand the brand owner.

David Gonski, AOChairman

Year ended 31 December 20052005 2004 Change

Revenue from Sales of Beverages and Food ($ million) 3,987.5 3,450.1 15.6 %

Earnings Before Interest and Tax, before Significant Items ($ million) 570.6 518.3 10.1 %

EBIT Margin (%) 14.3 15.0 -0.7pts

Net Profit, before Significant Items ($ million) 320.5 274.3 16.8 %

Net Profit ($ million) 320.5 276.6 15.9 %

Operating Cash Flow ($ million) 435.2 381.0 14.2 %

Return on Average Capital Employed (%) 17.5 21.6 -4.1pts

Total Capital Employed ($ million) 3,557.5 2,469.3 44.1 %

Net Debt to Book Equity (%) 149.7 164.8 -15.1pts

Capital Expenditure to Revenue (%) 7.4 6.1 1.3pts

Earnings per Share, before Significant Items (cents) 43.3 39.0 11.0 %

Earnings per Share (cents) 43.3 39.3 10.2 %

Dividends per Share (cents) 31.5 28.0 12.5 %

Coca-Cola Amatil 2005 Annual Report 3

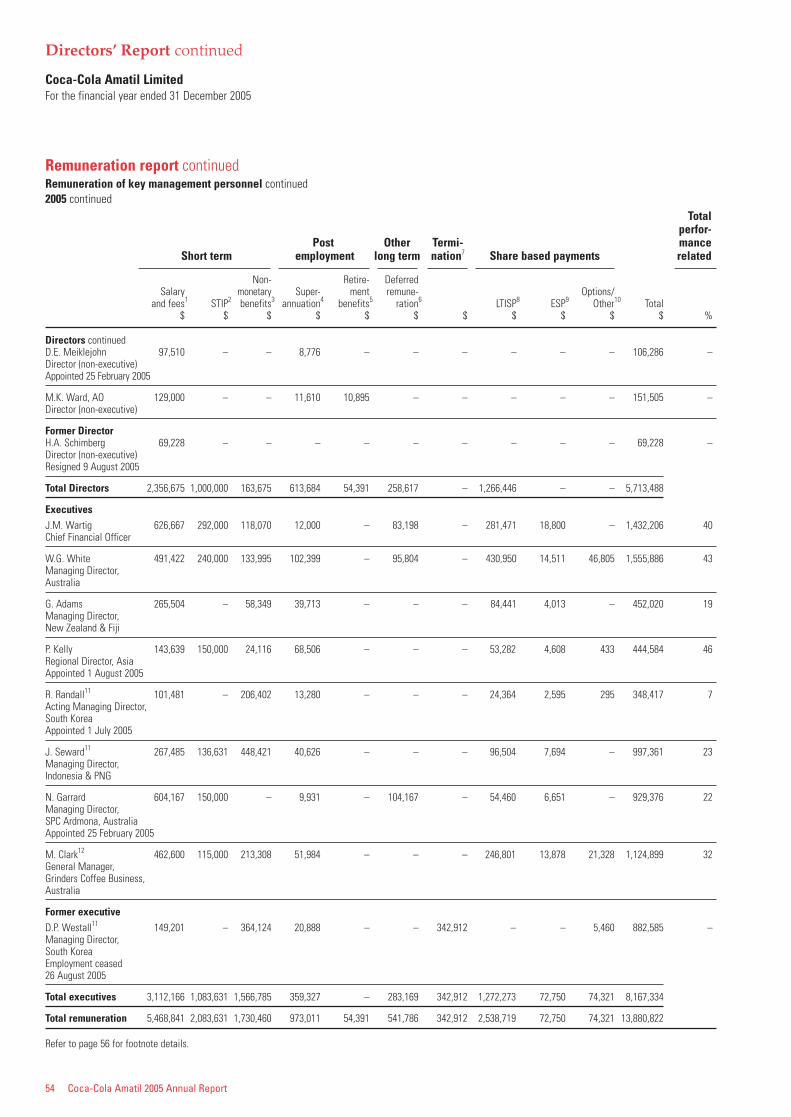

Irial replaced HenrySchimberg who, as one of TCCC’s nominees on the Board, retired in August 2005 after serving as a Non-Executive Director.The Board records its sincereappreciation of the valuablecontribution made by Henryover the past five years.

Corporate governanceCCA has an ongoingcommitment to transparencyand good corporategovernance. This AnnualReport includes a number of statements on the robustcorporate governancestructure and riskmanagement frameworkprevailing throughout CCA.CCA has always maintaineda high level of corporategovernance and we continueto refine our practices in thisarea each year.

The Coca-ColaCompanyThe Board is pleased withthe strengthening of therelationship between CCAand TCCC. TCCC holds 32% of the shares in CCA,and nominates two Non-Executive Directors ofthe current eight memberBoard. CCA’s Related PartyCommittee, comprising theIndependent Directors,reviewed all materialtransactions between CCAand TCCC in 2005 and is animportant forum for dealingwith governance issues.

Corporate socialresponsibilityCCA strongly supports socialand environmental activitiesthrough its community andenvironmental programs.These programs help tosustain business performanceby strengthening thecommunities in which weoperate, improving businessefficiency and developingrelationships withstakeholders, and ultimatelyleading to increasedshareholder returns.

EmployeesOne of the underlyingstrengths of the Group is thequality of its people. Theircommitment to CCA’s corevalues underpins theexcellent results achieved thisyear. On behalf of the Board,I would like to thank allemployees for their specialefforts and contributions in 2005.

David Gonski, AO

Net Profit2

$ million

0504030201150

300

450

600

570.

6

518.

3

470.

0

421.

9

372.

3

050403020170

140

210

280

350

320.

5

274.

3

238.

8

205.

5

171.

1

05040302010

5

10

15

20

25

17.5

21.6

10.2

8.8

7.6

05040302010

7

14

21

28

35

31.5

28.0

23.0

18.5

14.0

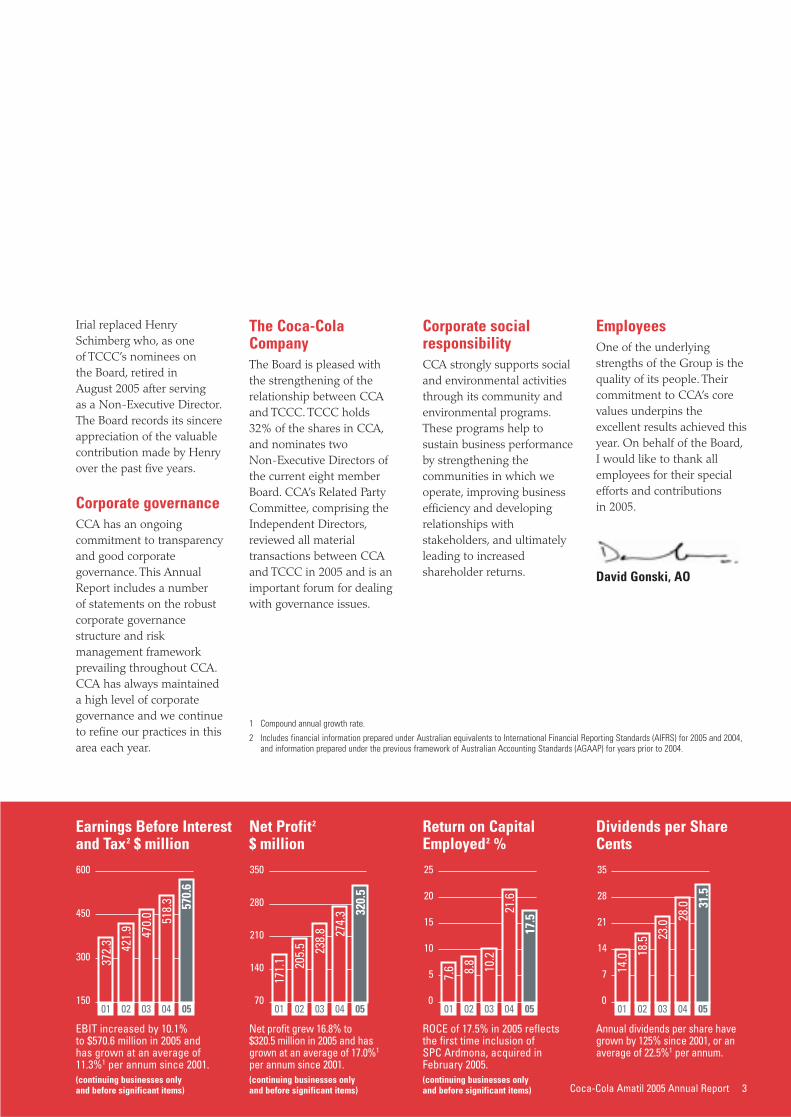

EBIT increased by 10.1% to $570.6 million in 2005 and has grown at an average of11.3%1 per annum since 2001. (continuing businesses only and before significant items)

Net profit grew 16.8% to $320.5 million in 2005 and hasgrown at an average of 17.0%1

per annum since 2001.(continuing businesses only and before significant items)

ROCE of 17.5% in 2005 reflectsthe first time inclusion of SPC Ardmona, acquired inFebruary 2005.(continuing businesses only and before significant items)

Annual dividends per share havegrown by 125% since 2001, or anaverage of 22.5%1 per annum.

Earnings Before Interestand Tax2 $ million

Return on CapitalEmployed2 %

Dividends per ShareCents

1 Compound annual growth rate.

2 Includes financial information prepared under Australian equivalents to International Financial Reporting Standards (AIFRS) for 2005 and 2004,and information prepared under the previous framework of Australian Accounting Standards (AGAAP) for years prior to 2004.

4 Coca-Cola Amatil 2005 Annual Report

Group Managing Director’s Review of Operations

At CCA, we ultimately judge our success by how well we grow the revenueand profits of our customers, confident that this commitment will provide arobust platform for us to continuously innovate our product range, maintainour category leadership positions and in turn grow our profitability.

In 2005, we were again ableto achieve a strong financialoutcome for the year bybalancing market shareobjectives with volume andpricing realisation and costmanagement discipline.

Strong gains were madeacross the Group in theexecution of the Company’skey business drivers whichhas led to further increases in revenue generated fromsources other than carbonatedbeverages. We commencedbusiness in 2005 with over80,000 new customers, over45,000 new cold drink coolerswere placed and our customerservice initiatives again sawthe Company win manyawards for service excellence.

By the successful execution ofthis customer focused strategy,earnings per share (ongoing

business and before significantitems) has increased at acompound annual growth rate of 14.4% since 2001 anddividends per share haveincreased by 125%, or anaverage of 22.5% per annum.

To maintain this momentum,we shall continue to target the creation of a perfectlymerchandised beveragelandscape in every outlet.New product development,cold drink cooler placementsand the expansion of ournon-carbonated beverageportfolio remain corepriorities. The execution ofthese priorities will allow us toexpand the size and value ofour relationship with both thecustomer and the consumer,by providing the right productin the right package, deliveredthrough the right channel atthe right price, for the rightoccasions.

2005 reviewIn 2005, CCA continued todeliver on its commitment to consistently improve itsfinancial returns, deliveringits fifth consecutive year of double-digit net profitgrowth.

• Net profit, beforesignificant items, increased16.8% to $320.5 million.

• Earnings per share, beforesignificant items, increased11.0% to 43.3 cents.

• Operating cash flowincreased 14.2% to $435.2 million.

• Dividends per shareincreased 12.5% to 31.5 cents, 100% franked.

Terry DavisGroup Managing Director

Broadening our business base

2001

Sale of Coca-Cola BottlersPhilippines in April.

Fanta flavour range launchedin Australia and New Zealand.

The launch of the space saving‘fridge mate’ multi-can pack.

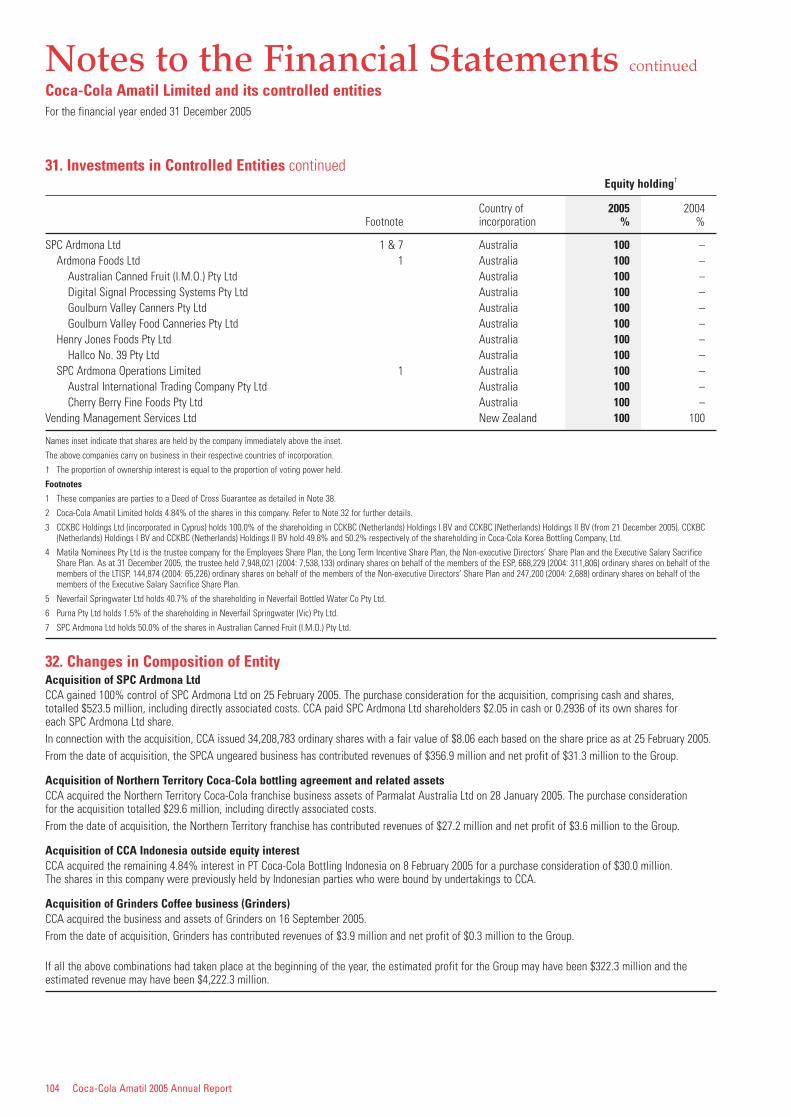

CCA has expanded its product offering in beveragesand food by growing its business organically as wellas by acquiring businesses that can build our brandportfolio or improve our manufacturing anddistribution capability. Over the past five years, CCAhas invested around $950 million on 10 acquisitions,across Australia, New Zealand and Indonesia, whileraising over $2.4 billion in consideration from thesale of assets.

Coca-Cola Amatil 2005 Annual Report 5

Against the backdrop ofhigher COGS and morecompetitive tradingconditions, earnings beforeinterest and tax (EBIT), beforesignificant items, increased by 10.1% to $570.6 milliondue to strong results fromAustralia, Indonesia, PNGand a ten month contributionfrom SPC Ardmona (SPCA).

Australia achieved earningsgrowth of 5.3%, growingmargins from 21.2% to21.4%. This is a strong result for the business in a year characterised byhigher COGS and a softerconsumer environment.CCA maintained marketshare in foodstores despiteincreased price competition,a testament to the strengthof the brand portfolio.

Earnings for the Pacific(New Zealand & Fiji)region were lower due togreater price competition and weaker foodstoresrevenue in New Zealand.As a result, the New Zealandbusiness did not fully recoverCOGS increases for 2005.

Although recording a loss for the first time in 2005,South Korea achieved somesignificant trading milestonesincluding a broadening of its product range to includeMinute Maid, the world’sbiggest juice brand; a 32%increase in the number of cold drink coolers in the trade and improvedmerchandising which led to gains in shelf space.

CCA has also achieved two major breakthroughs in addressing its operatingcost base in South Korea.Agreement has been reachedwith the Unions to redeployup to 200 people into salesroles and an early retirement plan has been offered toemployees to reduce theemployee base by at least6%. These initiatives willmaterially lower the cost ofdoing business in SouthKorea and cost recovery willflow through progressivelyfrom the second half of 2006.

Indonesia & PNGachieved an outstanding32.4% growth in EBIT,before significant items.This excellent result wasdriven by improved in-market execution which saw electric cold drinkcoolers and the customerbase grow by over 20% inIndonesia. The result was

achieved in a challengingenvironment which sawsignificant fuel priceincreases and inflation inIndonesia. PNG delivered astrong full year result withsolid EBIT margins.

SPCA delivered a solid resultin the first ten months underCCA ownership, despiteincreased competition fromimported private labelproducts. We are very pleasedwith how quickly the businesshas integrated with CCA and the business is makinggood progress in transitioningto a modern customer servicefocused organisation.Investments have been made in customer servicecapability to strengthen keyrelationships and capitalcommitments made towarehouse consolidation and capacity expansion tobuild a stronger operatingplatform for the future.

2002 20042003 2005

Acquisition of Rio Beverages, a juice manufacturer, in New Zealand.

Acquisition of Pacific Beverages,a manufacturer, marketer anddistributor of fruit juices, cordialsand other beverages in Australia.

Sale of PET manufacturingfacilities in Australia.

Vanilla Coke launched inAustralia and New Zealand.

L&P launched in New Zealand.

Neverfail Springwater andPeat’s Ridge Springs acquiredgiving CCA access to thehome and office deliverywater market in Australia.

Diet Coke with Vanillalaunched in Australia.

National rollout of Frestea in Indonesia.

Acquisition of Quirk’sRefrigeration in Australia.

Acquisition of Crusta FruitJuices in Australia.

Opening of CCA’s firstautomated distributionwarehouse in Mentone,Victoria.

Sprite zero launched in New Zealand.

E2 Energy launched in New Zealand.

CCA becomes the soleAustralian Coca-Cola licenseefollowing the acquisition of theNorthern Territory Coca-Colabeverages licence.

Acquisition of SPCA in Australia.

Acquisition of Grinders Coffeein Australia.

Sprite zero launched in Australia.

Minute Maid launched inSouth Korea.

6 Coca-Cola Amatil 2005 Annual Report

Group Managing Director’s Review of Operations continued

Launch of Coca-Cola zeroIn January 2006, CCAAustralia undertook itsbiggest ever product launch.Coca-Cola zero, with the realtaste of Coca-Cola and zerosugar, is a significant initiativeby the Coca-Cola system tomeet consumer demand forlower calorie beverages.

TCCC and CCA’s $18 millionlaunch campaign included anunprecedented integratedmedia program, acceleratedcooler placements andextensive in-fieldmerchandising.

In mid January, a 1,000 strongMarket Impact Team (MIT)joined CCA’s sales force for a two week intensivemerchandising effort. TheMIT consisted of local CCAemployees redeployed fromnon-sales roles and 198international employees from 42 countries within the Coca-Cola system.

Customer and consumerresponse to the launch has been overwhelming,far exceeding expectations.The first five week period of scan data indicated thatthe total cola category grew by more than 20% infoodstores, with Coca-Colabrands up significantly.In the first two months of the year, Coca-Cola zero,

combined with a solidsummer season, has resultedin Australian volumesgrowing by more than 10%.

Coca-Cola zero is expected tobecome a significant productwithin CCA’s brand portfolioand was launched into New Zealand in February.

Capital managementCCA’s priorities for using its cash flow are to reinvest in value-adding growthopportunities and to pay out a high portion of profits toshareholders as dividends.

The most significant use ofcash over the next three yearswill be in the construction ofautomated warehouses inSydney and Auckland for atotal cost of $250 million.

The success of CCA’s firstautomated warehouse inMentone in Victoria underpinsour confidence that theseinvestments will materiallyimprove customer servicelevels while generating costsavings for CCA.

CCA’s cold drink coolerrollout continued in 2005.CCA deployed over 45,000coolers at a cost of $74 millionand the business will spend asimilar amount in 2006.

CCA is committed tomaintaining the highdividend payout ratio.The current payout ratio of73.5% of net profit is withinthe target payout range of70% to 80%.

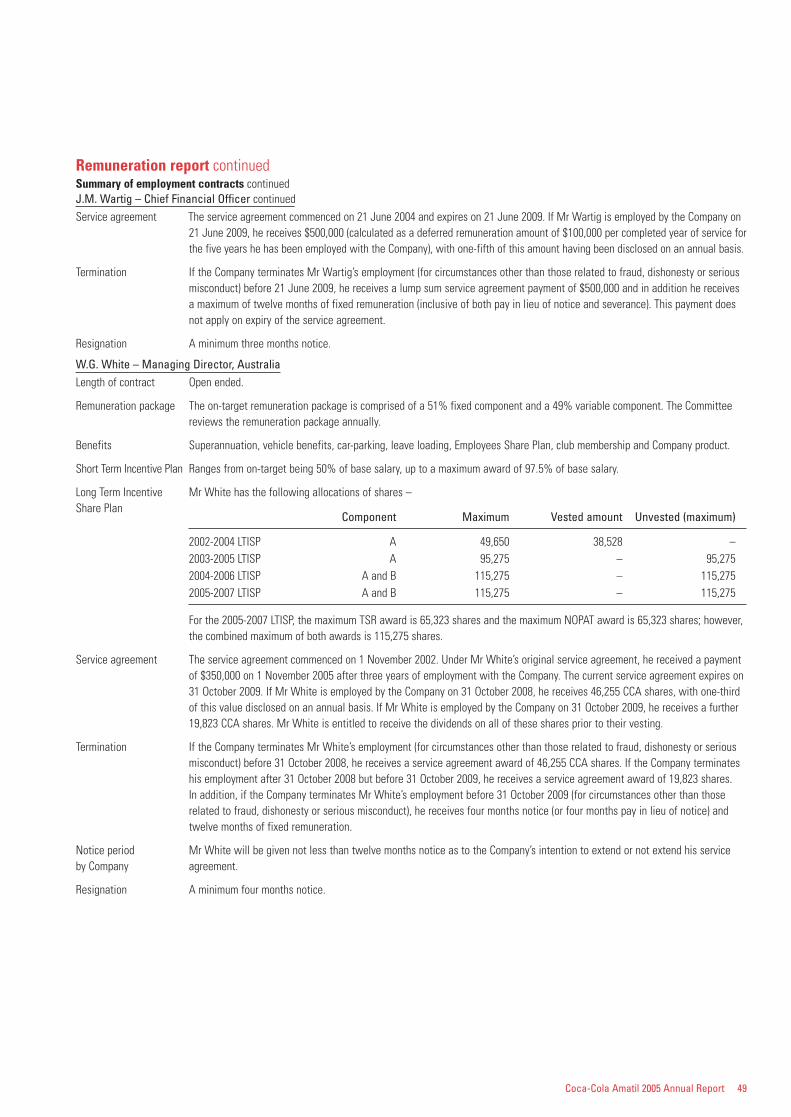

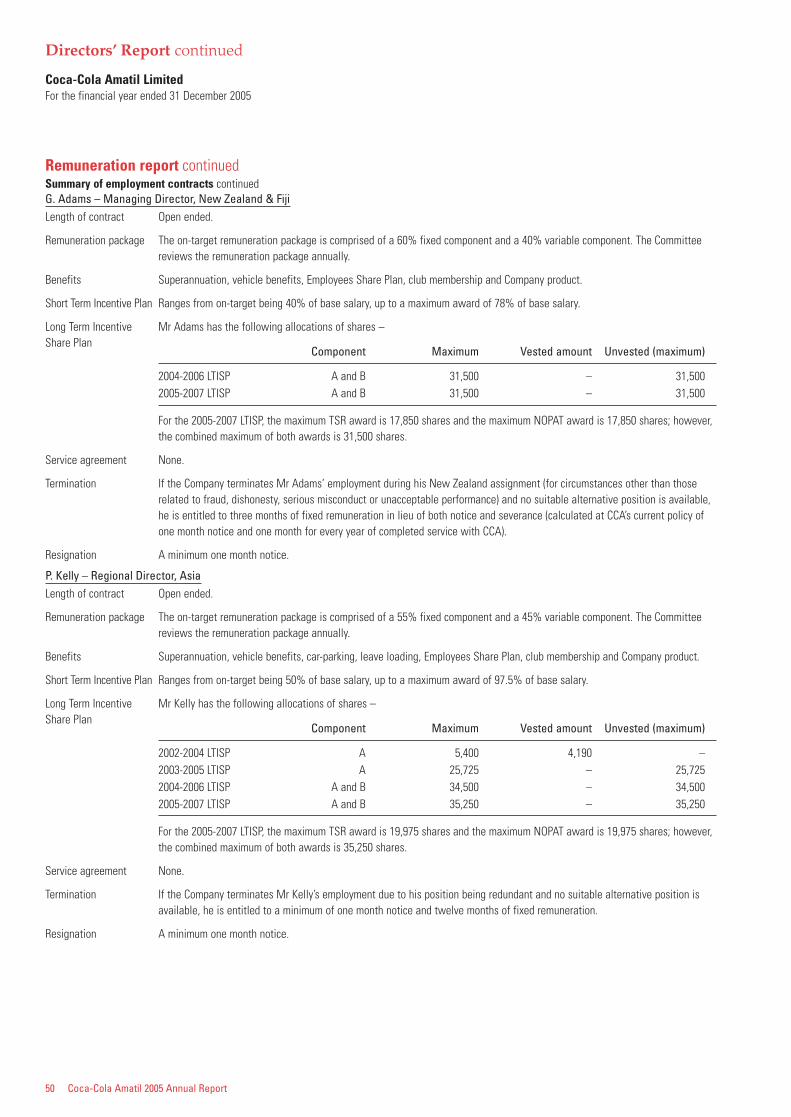

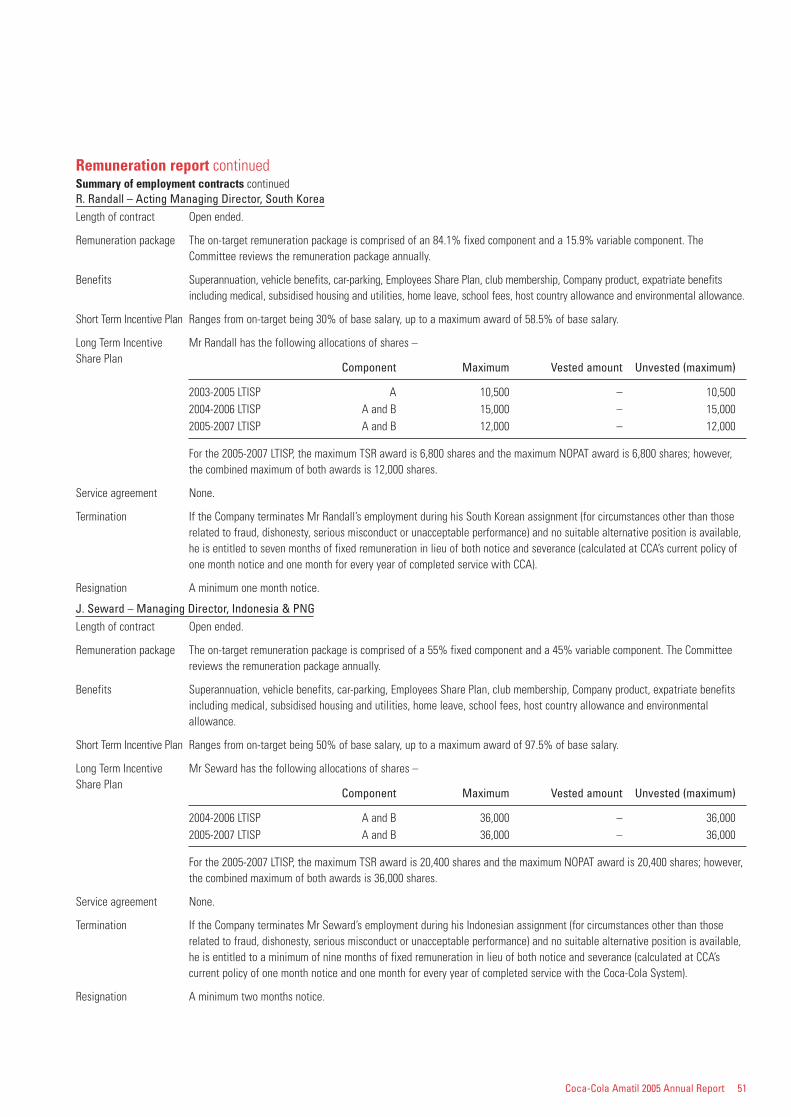

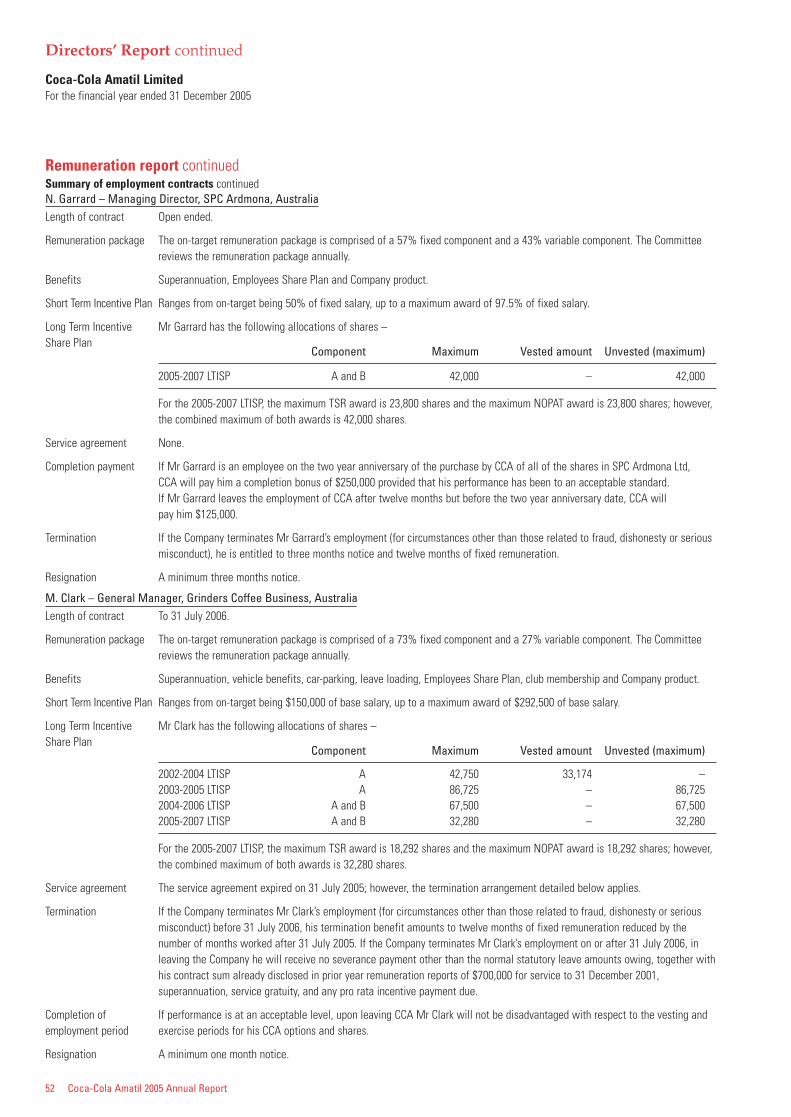

CCA’s expansion into non-carbonated beverages and food

200520010

25

50

75

100%

95%71%

20%

9%5%Carbonated soft drinks

Non-carbonated beverages

Food

By broadening the product offering, CCA has grown its non-carbonated beverage business intobottled water, juice, sports drinks, ready-to-drink teaand with the acquisition of SPC Ardmona, CCA hasentered the ready-to-eat deciduous fruit category.Since 2001, revenue generated from non-carbonatedbeverages and food has grown from 5% to 29% of totalrevenue in 2005. Combined with strong cost discipline,EBIT margins have grown from 11.4% to 14.3%.

Revenue split

Share price – Relative performance

Coca-Cola Amatil 2005 Annual Report 7

International FinancialReporting Standards CCA has adopted Australianequivalents to InternationalFinancial ReportingStandards (AIFRS) for 2005.The financial report for thefull year to 31 December2005 is CCA’s first full yearreport under the newstandards. AIFRS will have a negligible impact onearnings in future years andwill not affect cash flows,debt servicing capability or the ability of CCA to paydividends. More detail on thechanges is included in Note 3to the Financial Report.

Our peopleIt is important that werecognise the efforts of thenearly 19,000 people who are the foundation of CCA.They have been integral indelivering this year’sperformance and positioningthe Company to meet ourfuture objectives.

Our people are the face of our Company and oursuccess would not bepossible without theirpassion for our brands,and their commitment anddedication to improving ourbusiness each day.

2006 outlookThe growth in 2006 will beunderpinned by the strongnew product pipeline, led by the launch of Coca-Colazero in Australia and New Zealand. Our goal is togrow per capita consumptionof our products and toreinforce our brand portfolio’sleadership position.We expect the higher levelsof marketing spend fromboth CCA and TCCC willdrive additional volume andvalue growth. The solid startto 2006 provides us with ahigh level of confidence that

CCA will continue toimprove its market positionand deliver another year ofsolid earnings growth.

Terry DavisGroup Managing Director

60

100

140

180

220

2001 2002 2003 2004 2005

Coca-Cola Amatil

S&P ASX 100 Index

Note: CCA’s share price and the S&P ASX 100 Indexhave been indexed to 100from 1 January 2001 to allowmeaningful comparison.

8 Coca-Cola Amatil 2005 Annual Report

Key BusinessDrivers

The organisation remains focused on growing per capita consumptionof its beverage and food brands in each of its markets. To achieve thisoutcome, CCA concentrates on the successful execution of five keybusiness drivers:

Product and package innovation

Non-carbonated beverage and food growth

Expanding the availability of CCA products into new outlets

Customer service enhancement

Revenue management and cost discipline

12

345

New product launches

2005 review In 2005, CCA launched 74new and innovative productsand packages, contributing tothe more than 250 newproducts launched by CCAover the past five years.Some of the new productswhich have becomeimportant to the CCA brand portfolio include:

• e2 Energy in New Zealand;

• Minute Maid in South Korea; and

• Frestea in Indonesia.

In January 2006, CCAAustralia undertook itsbiggest ever product launch.Coca-Cola zero, with the realtaste of Coca-Cola and zerosugar, is a significantinitiative by the Coca-Cola

system to meet consumerdemand for lower caloriebeverages. Both customerand consumer response to the launch has beenoverwhelming, far exceedingexpectations.

In Australia, Deep Spring wasreformulated and relaunchedin a new proprietary bottle.A new more ‘squeezable’Powerade pack wasintroduced which is lighter.It uses 10% less resin, saving$2 million per annum inproduction costs. Sprite zerowas successfully launched inAustralia at the beginning of2005, growing total Spritebrand revenues for the yearby 10%.

New Zealand introducedsome exciting new rotationalCoke flavours includingCoke with Raspberry andCoke Citra. The classic L&Pbrand entered the low caloriesegment launching L&PSweet As and as a resultgrew L&P brand revenue by 9%1. Keri juice, thenumber one juice brand inNew Zealand, released the innovative new three litre‘easy grip’ bottle, furtherstrengthening the brand’sposition.

In Indonesia, CCA focusedon expanding the soft drinkculture and in 2005introduced new carbonatedproducts including the Fanta‘Splash’ bottle, Fanta Creamyand Sprite Ice. Together with new pack sizes, thesebrands grew CSD revenue by12%1 in 2005.

1 In local currency

Coca-Cola Amatil 2005 Annual Report 9

CCA is continuously expanding itsproduct and package offering tobring sizzle to categories andexcitement to our consumers.We aim to:

• keep categories fresh and exciting by delivering products that meet the changing needs of consumers;

• introduce brand extensions that leverage the strength of our core brands;

• expand into new product categories; and

• develop creative and lower cost packaging solutions.

Coca-Cola Amatil 2005 Annual Report 9

1 Key Business Driver

Product and package innovation

05040302010

20

40

60

80

In 2005, CCA launched 74 newand innovative products and haslaunched more than 250 newproducts over the past five years.

In September 2005, CCApurchased the Grinderspremium roasted coffeebusiness in Australia. The acquisition will furtherenhance CCA’s productoffering in the high growthhotel, restaurant and café channel.

10 Coca-Cola Amatil 2005 Annual Report

2 Key Business Driver

Non-carbonated beverage and food growth

CCA is making good progress inbuilding its presence in health andwellbeing categories through its non-carbonated beverages andready-to-eat packaged fruit business.Over the last four years, CCA has increased its presence in:

• bottled water – including single serve and home and office delivered;

• juice – including single serve and freshly squeezed;

• sports drinks – Powerade;

• ready-to-drink tea – Nestea; and

• ready-to-eat deciduous fruit.

2005 reviewGrowing per capitaconsumption of non-alcoholicbeverages continues to be akey priority for CCA and has underpinned CCA’sinvestment in the bottledwater, juice and sports drinks categories. With theacquisition of SPCA in 2005,CCA now has a strongpresence in the growingready-to-eat deciduous fruit segment. Since 2001,CCA has increased annualrevenue from sources otherthan carbonated beverages from 5% to 29%.

In Australia, CCA has apowerful portfolio of waterbrands including MountFranklin, Pump and Neverfail.

In 2005, CCA launchedMount Franklin LightlySparkling and MountFranklin Still in glass bottlesto cater to the growing hotel,restaurant and café channel.

Fruitopia was relaunched inJune 2005, kick starting CCA’sjuice growth in Australia.Fruitopia J was launched as a single serve offering intothe convenience and leisurechannel. Fruitopia Classic,a premium chilled product,caters to the grocery channeland Fruitopia Alive is CCA’sfirst fruit smoothie offering.It’s a nutritious and deliciousblend of juices with all thegoodness of a daily hit of fruit.

The world’s biggest juicebrand Minute Maid waslaunched in South Korea inJune 2005. In its first eightmonths Minute Maid hascaptured around 20% of the100% juice segment. TheMinute Maid 100% juicerange includes Bone PLUS,Heart PLUS and Kids PLUSand a Fresh Mix range of lessthan 25% juice products.

In Indonesia, CCA launchedFrestea Green, a ready-to-drink green tea.

SPC Ardmona, developer ofthe unique resealable FridgePack, extended the range in2005 with Beetroot, PinkLady Apple and Pineappleofferings. These products,aimed at accessing the snackand breakfast market, havecontributed to significantcategory growth with SPCA’sshare growing from nothingto 22% in just three years.

Coca-Cola Amatil 2005 Annual Report 11

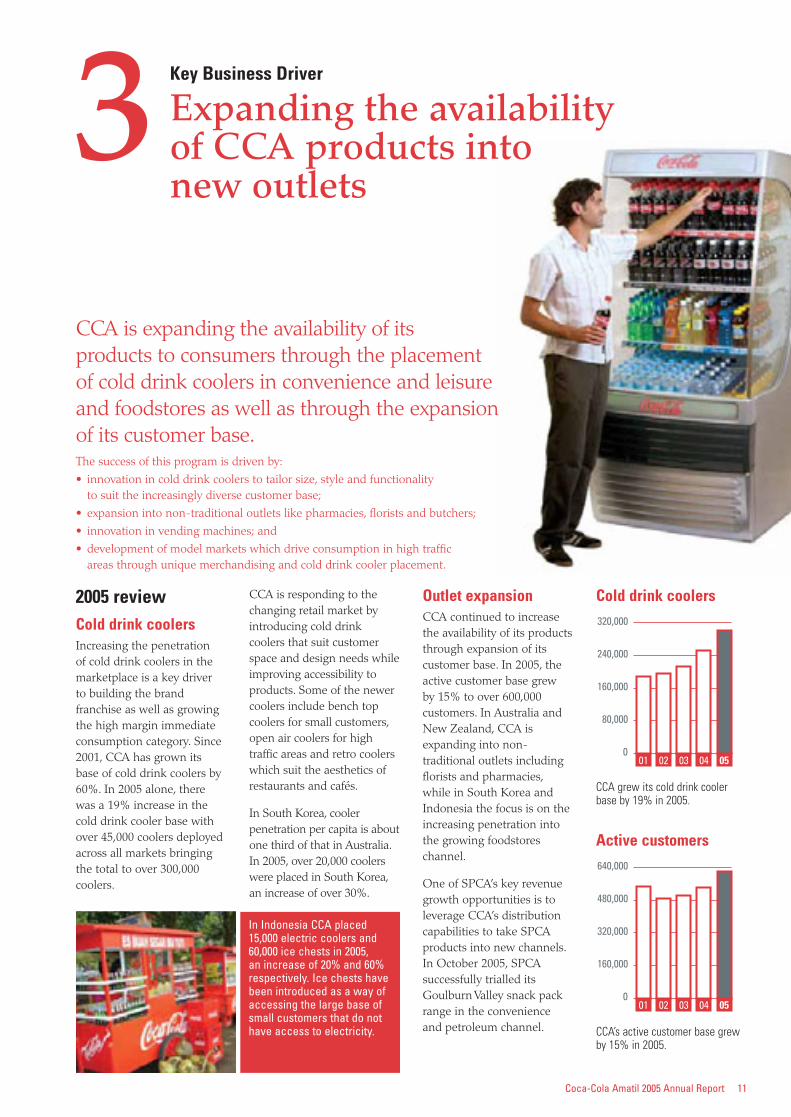

3CCA is expanding the availability of its products to consumers through the placement of cold drink coolers in convenience and leisure and foodstores as well as through the expansion of its customer base.The success of this program is driven by:

• innovation in cold drink coolers to tailor size, style and functionality to suit the increasingly diverse customer base;

• expansion into non-traditional outlets like pharmacies, florists and butchers;

• innovation in vending machines; and

• development of model markets which drive consumption in high traffic areas through unique merchandising and cold drink cooler placement.

2005 reviewCold drink coolersIncreasing the penetration of cold drink coolers in themarketplace is a key driver to building the brandfranchise as well as growingthe high margin immediateconsumption category. Since2001, CCA has grown itsbase of cold drink coolers by60%. In 2005 alone, therewas a 19% increase in thecold drink cooler base withover 45,000 coolers deployedacross all markets bringingthe total to over 300,000coolers.

CCA is responding to thechanging retail market byintroducing cold drinkcoolers that suit customerspace and design needs whileimproving accessibility toproducts. Some of the newercoolers include bench topcoolers for small customers,open air coolers for hightraffic areas and retro coolerswhich suit the aesthetics ofrestaurants and cafés.

In South Korea, coolerpenetration per capita is aboutone third of that in Australia.In 2005, over 20,000 coolerswere placed in South Korea,an increase of over 30%.

Outlet expansionCCA continued to increasethe availability of its productsthrough expansion of itscustomer base. In 2005, theactive customer base grew by 15% to over 600,000customers. In Australia andNew Zealand, CCA isexpanding into non-traditional outlets includingflorists and pharmacies,while in South Korea andIndonesia the focus is on theincreasing penetration intothe growing foodstoreschannel.

One of SPCA’s key revenuegrowth opportunities is toleverage CCA’s distributioncapabilities to take SPCAproducts into new channels.In October 2005, SPCAsuccessfully trialled itsGoulburn Valley snack packrange in the convenience and petroleum channel.

Cold drink coolers

CCA grew its cold drink coolerbase by 19% in 2005.

05040302010

80,000

160,000

240,000

320,000

Active customers

CCA’s active customer base grewby 15% in 2005.

05040302010

160,000

320,000

480,000

640,000

Key Business Driver

Expanding the availability of CCA products into new outlets

In Indonesia CCA placed15,000 electric coolers and60,000 ice chests in 2005, an increase of 20% and 60%respectively. Ice chests havebeen introduced as a way ofaccessing the large base ofsmall customers that do nothave access to electricity.

CCA is the leader in developing industry solutions that help improve customer and CCA profitability.

In Australia CCA has implemented shelf friendly packaging that will reduce handling, increase speed of shelf replenishment and facilitate outstanding product presentation on shelf.

2005 review Coke ConnectCCA’s Coke Connect call centres have beenestablished in Australia andNew Zealand to provide alow cost, high quality,reliable ordering system forcustomers, tailoring serviceby customer and channel,enabling the sales force tofocus more time onconceptual selling.

In Australia, the success hasbeen outstanding:

• Coke Connect generatedsales of over $1 billion in2005;

• 75,000 (or 79%) ofcustomer orders aremanaged by CokeConnect;

• more than 80% of allorders are placed via Coke Connect; and

• 2.6 million telesales callsare made annually or10,500 per day.

SPC ArdmonaimprovementsBy utilising the CCACustomer Business Planningmodel, SPCA has improvedbrand ranging, shelfpresence, service levels and category profitability.Utilising Aztec and A.C.Nielsen data, revenuemanagement, forecastaccuracy and customercategory profitability arebeing gradually improved.Positive feedback has alreadybeen received from customersregarding the new approach.

Shelf ready packagingCCA is the leader indeveloping industry solutionsthat help improve customerand CCA profitability.

In Australia CCA hasimplemented shelf friendlypackaging that will reducehandling, increase speed ofshelf replenishment andfacilitate outstanding productpresentation on shelf.

12 Coca-Cola Amatil 2005 Annual Report

4 Key Business Driver

Customer service enhancement

Satisfying our customers is CCA’s top priority. Bydeveloping tailored solutions for our key customers,CCA aims to grow each of our customers’categoryprofitability and to be there supplier of choice.We strive to:

• deliver all customer orders in full, on time and accurately invoiced;

• make ourselves increasingly easy to do business with through greater use of technology;

• strengthen our sales force capability through our ‘Coke Connect’ call centres; and

• develop customer solutions, from shelf ready packaging to channel specific packs,to cater to customer requirements.

5 Key Business Driver

Revenue management and cost discipline

Coca-Cola Amatil 2005 Annual Report 13

We endeavour to create a perfectly merchandisedbeverage landscape, supplying the right product inthe right pack, delivered through the right channel at the right price, for the right consumption occasion.We are continuously researching the consumer to optimise the volume, mix and price outcome:

• with a relentless focus on creating impulse purchases by making the purchase simple andcompelling for our consumers; and

• with equal commitment we are focused on driving costs down for us and our customersthrough supply chain improvement.

2005 review Automated distributionCCA’s $30 million automateddistribution centre in Victoria,opened in June 2004, hasgenerated annual cost savingsof $7 million. CCA hasachieved improvements incustomer service with areduction in turnaround timefor orders and improvementsin pick accuracy, as well asbenefiting from improvementsin labour productivity.

As a result of the success ofthe Victorian facility, CCA hascommenced development of

similar facilities in Sydney andAuckland, due for completionin mid 2008. At a combinedcost of $250 million, theSydney and Aucklandautomated warehousesrepresent significantinvestments in enhancingcustomer service whilereducing supply chain costs.

WarehouseconsolidationWarehouse consolidation has commenced with theconstruction of a $15 millionwarehouse, adjacent to thecurrent Sheppartonmanufacturing facility.

SPCA will reduce the numberof offsite finished goodswarehouses from 12 to twowith expectations of savingsto be in excess of $2 millionper annum. The new facilityis expected to be operationalby the end of 2006.

Increasing productpresenceIn the convenience andleisure channel, CCA hasplaced thousands of thestylish Mount Franklin ‘wave’racks over the past twelvemonths with a wide range of customers. The water

category has great potential,with consumption per capitagrowing as consumers drinkmore water as both a coldand ambient product.

Channel specificpackagingCCA has a wide range ofcustomers with differentproduct and packagingneeds. In the hotels,restaurants and café channel, CCA has introducedtraditional glass bottles as apoint of differentiation to improve our customers’and CCA’s profitability.

As a result of the success of CCA’s first automated distributioncentre in Victoria, CCA has commenced development of similarfacilities in Sydney and Auckland which are due for completion in mid 2008. At a combined cost of $250 million, the Sydney and Auckland automated warehouses represent significantinvestments in enhancing customer service while reducing supply chain costs.

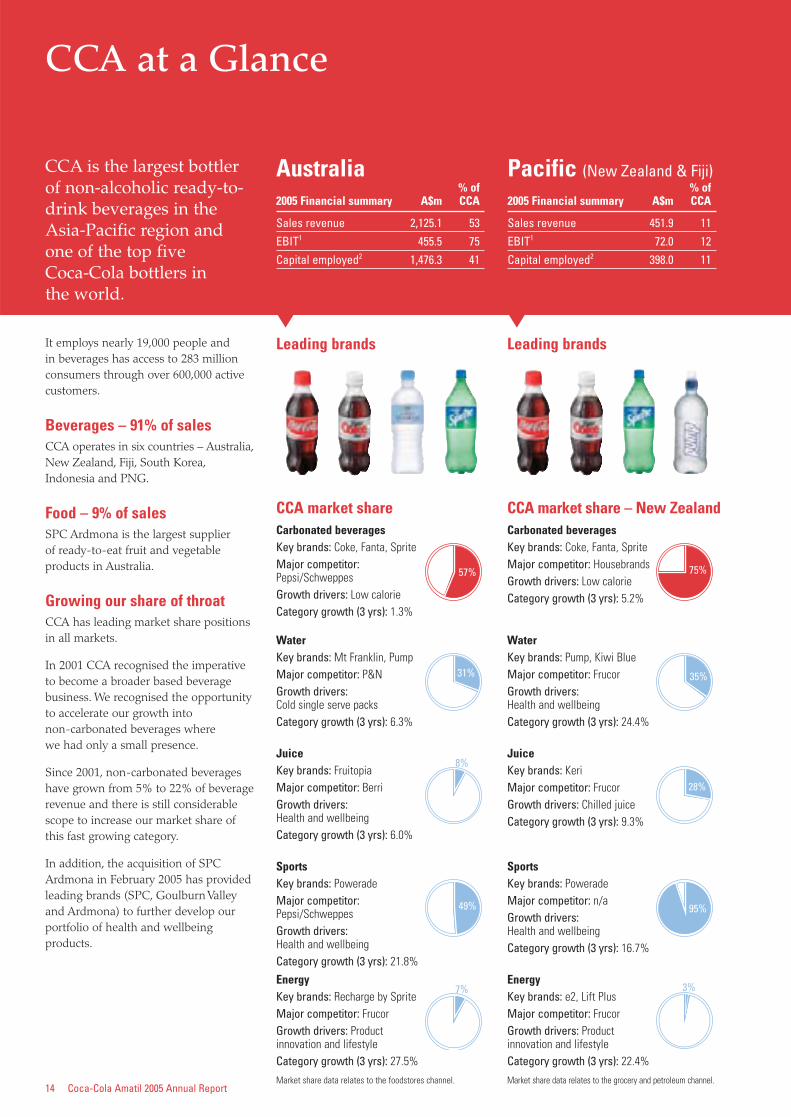

CCA market shareCarbonated beveragesKey brands: Coke, Fanta, SpriteMajor competitor:Pepsi/SchweppesGrowth drivers: Low calorieCategory growth (3 yrs): 1.3%

SportsKey brands: PoweradeMajor competitor:Pepsi/SchweppesGrowth drivers:Health and wellbeingCategory growth (3 yrs): 21.8%

WaterKey brands: Mt Franklin, PumpMajor competitor: P&NGrowth drivers:Cold single serve packsCategory growth (3 yrs): 6.3%

EnergyKey brands: Recharge by SpriteMajor competitor: FrucorGrowth drivers: Productinnovation and lifestyleCategory growth (3 yrs): 27.5%

Market share data relates to the foodstores channel.

JuiceKey brands: FruitopiaMajor competitor: BerriGrowth drivers:Health and wellbeingCategory growth (3 yrs): 6.0%

CCA market share – New ZealandCarbonated beveragesKey brands: Coke, Fanta, SpriteMajor competitor: HousebrandsGrowth drivers: Low calorieCategory growth (3 yrs): 5.2%

SportsKey brands: PoweradeMajor competitor: n/aGrowth drivers:Health and wellbeingCategory growth (3 yrs): 16.7%

WaterKey brands: Pump, Kiwi BlueMajor competitor: FrucorGrowth drivers:Health and wellbeingCategory growth (3 yrs): 24.4%

EnergyKey brands: e2, Lift PlusMajor competitor: FrucorGrowth drivers: Productinnovation and lifestyleCategory growth (3 yrs): 22.4%

Market share data relates to the grocery and petroleum channel.

JuiceKey brands: KeriMajor competitor: FrucorGrowth drivers: Chilled juiceCategory growth (3 yrs): 9.3%

14 Coca-Cola Amatil 2005 Annual Report

CCA at a Glance

CCA is the largest bottlerof non-alcoholic ready-to-drink beverages in theAsia-Pacific region andone of the top five Coca-Cola bottlers in the world.

Australia% of

2005 Financial summary A$m CCA

Sales revenue 2,125.1 53EBIT1 455.5 75Capital employed2 1,476.3 41

Pacific (New Zealand & Fiji)% of

2005 Financial summary A$m CCA

Sales revenue 451.9 11EBIT1 72.0 12Capital employed2 398.0 11

It employs nearly 19,000 people and in beverages has access to 283 millionconsumers through over 600,000 activecustomers.

Beverages – 91% of salesCCA operates in six countries – Australia,New Zealand, Fiji, South Korea,Indonesia and PNG.

Food – 9% of salesSPC Ardmona is the largest supplier of ready-to-eat fruit and vegetableproducts in Australia.

Growing our share of throatCCA has leading market share positionsin all markets.

In 2001 CCA recognised the imperativeto become a broader based beveragebusiness. We recognised the opportunityto accelerate our growth into non-carbonated beverages where we had only a small presence.

Since 2001, non-carbonated beverageshave grown from 5% to 22% of beveragerevenue and there is still considerablescope to increase our market share ofthis fast growing category.

In addition, the acquisition of SPCArdmona in February 2005 has providedleading brands (SPC, Goulburn Valleyand Ardmona) to further develop ourportfolio of health and wellbeingproducts.

Leading brands Leading brands

57%

31%

8%

49%

7%

75%

35%

28%

95%

3%

CCA market share – IndonesiaCarbonated beveragesKey brands: Sprite, Fanta, CokeMajor competitor: PepsiGrowth drivers:New flavours and packsCategory growth (3 yrs): -3.0%

SportsKey brands: Powerade IsotonicMajor competitor: Pocari SweatGrowth drivers:Health and wellbeingCategory growth (3 yrs): 23.0%

Market share data relates to all channels.

RTD teaKey brands: FresteaMajor competitor: SosroGrowth drivers: Fruit flavoursCategory growth (3 yrs): 8.0%

WaterKey brands: AdesMajor competitor: AquaGrowth drivers: Low availabilityof quality drinking waterCategory growth (3 yrs): 14.0%

SPCA market shareCanned FruitKey brands: Goulburn Valley, SPCMajor competitor: Golden CircleGrowth drivers:Resealable Fridge PackCategory growth (3 yrs): 7.5%

Tinned tomatoesKey brands: ArdmonaMajor competitor:Imports and housebrandsGrowth drivers:Value-added productsCategory growth (3 yrs): 2.0%

Fruit snacksKey brands: Goulburn Valley, SPCMajor competitor: n/aGrowth drivers:Health and wellbeingCategory growth (3 yrs): 5.0%

Baked beans & spaghettiKey brands: SPCMajor competitor: HeinzGrowth drivers:Health and wellbeingCategory growth (3 yrs): 2.2%

SpreadsKey brands: IXLMajor competitor:Cottees, St DalfourGrowth drivers: Premium jamsCategory growth (3 yrs): -2.9%

Coca-Cola Amatil 2005 Annual Report 15

South Korea% of

2005 Financial summary A$m CCA

Sales revenue 630.7 16EBIT1 -6.6 -1Capital employed2 705.8 19

Indonesia & PNG% of

2005 Financial summary A$m CCA

Sales revenue 427.9 11EBIT1 42.9 7Capital employed2 259.2 7

SPC Ardmona% of

2005 Financial summary A$m CCA

Sales revenue (10 months) 351.9 9EBIT1 (10 months) 45.7 7Capital employed2 815.9 22

Leading brands Leading brands Leading brands

CCA market shareCarbonated beveragesKey brands: Coke, FantaMajor competitor: LotteGrowth drivers: New packagingand brand extensionsCategory growth (3 yrs): -10.0%

SportsKey brands: PoweradeMajor competitor: Dong-AGrowth drivers:Health and wellbeingCategory growth (3 yrs): -2.8%

JuiceKey brands: Minute MaidMajor competitor: LotteGrowth drivers:Health and wellbeingCategory growth (3 yrs): -2.8%

RTD teaKey brands: NesteaMajor competitor: LotteGrowth drivers: Asian teaCategory growth (3 yrs): 20.3%

Market share data relates to hyper and supermarkets, mom and pop stores and convenience channels.

WaterKey brands: Soonsoo100Major competitor: NongshimGrowth drivers:Health and wellbeingCategory growth (3 yrs): 8.0%

48%

6%

13%

20%

5%

89%

15%

1%

2%

66%

90%

29%

36%

25%

1 CCA Group EBIT of $570.6 million includes $38.9 million of corporate/unallocated costs not included in the above summary.2 CCA Group capital employed of $3,557.5 million as at 31 December 2005 includes ($97.7) million of corporate/unallocated capital employed not included in the above summary.

16 Coca-Cola Amatil 2005 Annual Report

Business Review

2005 overviewThe Australian businessachieved EBIT growth of5.3% on revenue growth of4.1%. This is a solid result ina non-alcoholic ready-to-drink (NARTD) beveragemarket that experiencedsofter demand, due to higherfuel prices and generallylower consumer spending.Increases in commoditycosts, including PET resin,aluminium and sugar, wererecovered through higherpricing and other revenuemanagement initiatives.

CCA continued todemonstrate the strength of its brand portfolio,

maintaining its market sharein foodstores in 2005.CCA’s pricing discipline and category leadershipstrategy continue to deliver a sustainable platform forgrowing customer andconsumer relationships.

HighlightsProduct & package innovation:Major CSD launches for 2005included Sprite zero andCoke with Lime. Sprite zerohas been a great success,growing total Sprite revenueby 10%. CSD brands againdelivered positive revenuegrowth, led by diet CSDs,

with diet Coke growing morethan 8%. The diet categoryhas delivered 10% revenuegrowth per annum over the past three years asconsumers shift to lowercalorie beverage options. Thelaunch of Coca-Cola zero inJanuary 2006 has given asignificant boost to CCA’slow calorie CSD portfolio.

Non-carbonated beveragesexpansion: CCA’s non-carbonated beveragesdelivered another solid yearof growth, accounting forover 20% of CCA’s Australianrevenue. Growth was led bywater, with Mount Franklinand Pump both growingrevenue around 15% in 2005.Fruitopia J, Classic and

Alive (launched mid 2005)contributed 3 million unitcases of additional volume.

Cold drink cooler placement:CCA’s cooler placementprogram continues to drivestrong performances in boththe convenience and leisureand foodstores channels, witha 12% net increase in colddrink coolers in the year.

Outlet expansion: Retailcustomer numbers grew,in net terms, by almost 4%.This growth has beenachieved from a focus onranging our products in non-traditional outletsincluding pharmacies andnewsagents and by growingthe hotel, restaurant and café channel.

Year ended 31 December2005 2004 Change

Sales revenue ($ million) 2,125.1 2,041.6 4.1%Revenue per unit case $6.60 $6.32 4.4%Volume (million unit cases) 322.0 322.9 -0.3%EBIT ($ million) 455.5 432.5 5.3%EBIT margin 21.4% 21.2% 0.2ptsCapital expenditure to revenue 7.8% 6.3% –

The Australian businessrepresents 41% of CCA’s(excluding corporate/unallocated) capital employed.

Note: all 2001-2003 numbers preparedunder AGAAP. All 2004 and 2005numbers prepared under AIFRS

05040302010

550

1,100

1,650

2,200

2,12

5.1

2,04

1.6

1,88

2.9

1,77

6.8

1,67

5.1

05040302010

125

250

375

500

455.

5

432.

5

377.

7

317.

0

288.

9

Revenue increased 4.1% in2005 and has increased at aCAGR2 of 6.1% since 2001.

Earnings increased 5.3% in2005 and have increased at aCAGR2 of 12.1% since 2001.

AustraliaWarwick WhiteManaging Director, Australia

Nessa O’SullivanChief Financial Officer,Australia

Capital Employed Revenue $M EBIT1 $M

41%41%

Australia

1 Before significant items.2 Compound annual growth rate.

Coca-Cola Amatil 2005 Annual Report 17

Year ended 31 December2005 2004 Change

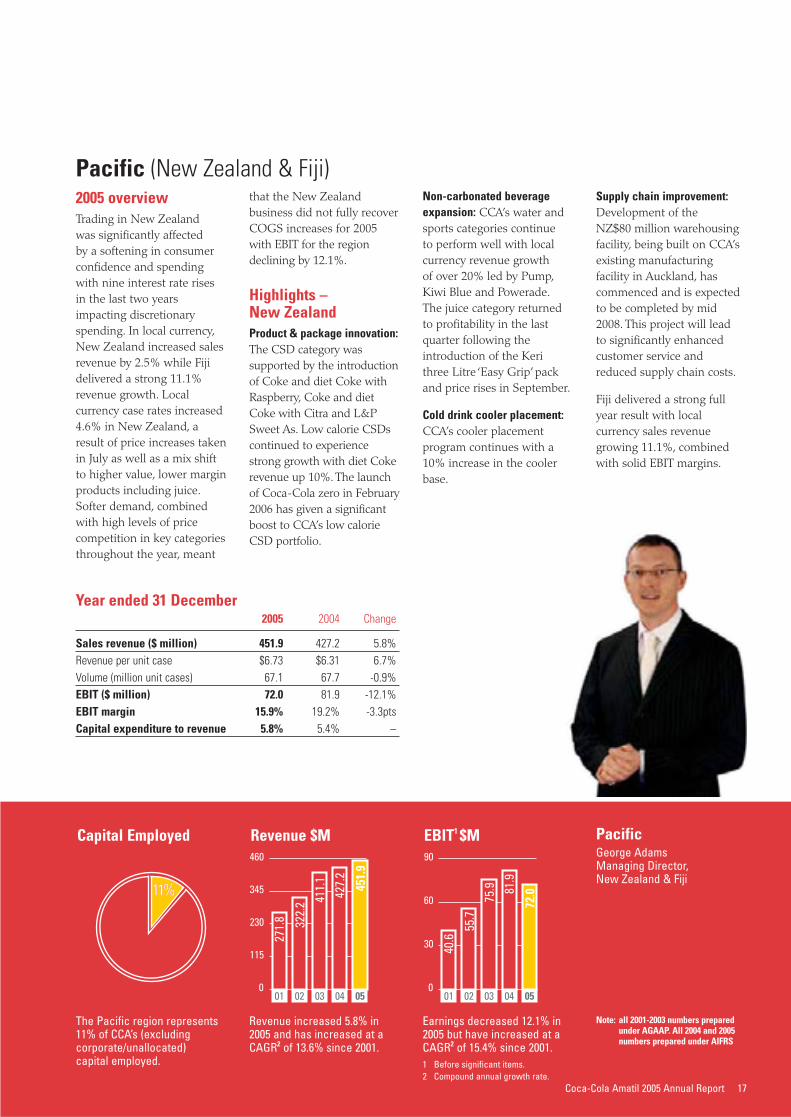

Sales revenue ($ million) 451.9 427.2 5.8%Revenue per unit case $6.73 $6.31 6.7%Volume (million unit cases) 67.1 67.7 -0.9%EBIT ($ million) 72.0 81.9 -12.1%EBIT margin 15.9% 19.2% -3.3ptsCapital expenditure to revenue 5.8% 5.4% –

Note: all 2001-2003 numbers preparedunder AGAAP. All 2004 and 2005numbers prepared under AIFRS

The Pacific region represents11% of CCA’s (excludingcorporate/unallocated)capital employed.

05040302010

115

230

345

460

451.

9

427.

2

411.

1

322.

2

271.

8

05040302010

30

60

90

72.081

.9

75.9

55.7

40.6

Revenue increased 5.8% in2005 and has increased at aCAGR2 of 13.6% since 2001.

Earnings decreased 12.1% in2005 but have increased at aCAGR2 of 15.4% since 2001.

PacificGeorge AdamsManaging Director,New Zealand & Fiji

Capital Employed Revenue $M EBIT1 $M

11%11%

2005 overviewTrading in New Zealand was significantly affected by a softening in consumerconfidence and spendingwith nine interest rate risesin the last two yearsimpacting discretionaryspending. In local currency,New Zealand increased salesrevenue by 2.5% while Fijidelivered a strong 11.1%revenue growth. Localcurrency case rates increased4.6% in New Zealand, aresult of price increases takenin July as well as a mix shiftto higher value, lower marginproducts including juice.Softer demand, combinedwith high levels of pricecompetition in key categoriesthroughout the year, meant

that the New Zealandbusiness did not fully recoverCOGS increases for 2005with EBIT for the regiondeclining by 12.1%.

Highlights – New ZealandProduct & package innovation:The CSD category wassupported by the introductionof Coke and diet Coke withRaspberry, Coke and dietCoke with Citra and L&PSweet As. Low calorie CSDscontinued to experiencestrong growth with diet Cokerevenue up 10%. The launchof Coca-Cola zero in February2006 has given a significantboost to CCA’s low calorieCSD portfolio.

Non-carbonated beverageexpansion: CCA’s water andsports categories continue to perform well with localcurrency revenue growth of over 20% led by Pump,Kiwi Blue and Powerade.The juice category returnedto profitability in the lastquarter following theintroduction of the Keri three Litre ‘Easy Grip’ packand price rises in September.

Cold drink cooler placement:CCA’s cooler placementprogram continues with a10% increase in the coolerbase.

Supply chain improvement:Development of the NZ$80 million warehousingfacility, being built on CCA’sexisting manufacturingfacility in Auckland, hascommenced and is expectedto be completed by mid2008. This project will lead to significantly enhancedcustomer service andreduced supply chain costs.

Fiji delivered a strong fullyear result with localcurrency sales revenuegrowing 11.1%, combinedwith solid EBIT margins.

Pacific (New Zealand & Fiji)

1 Before significant items.2 Compound annual growth rate.

18 Coca-Cola Amatil 2005 Annual Report

Business Review continued

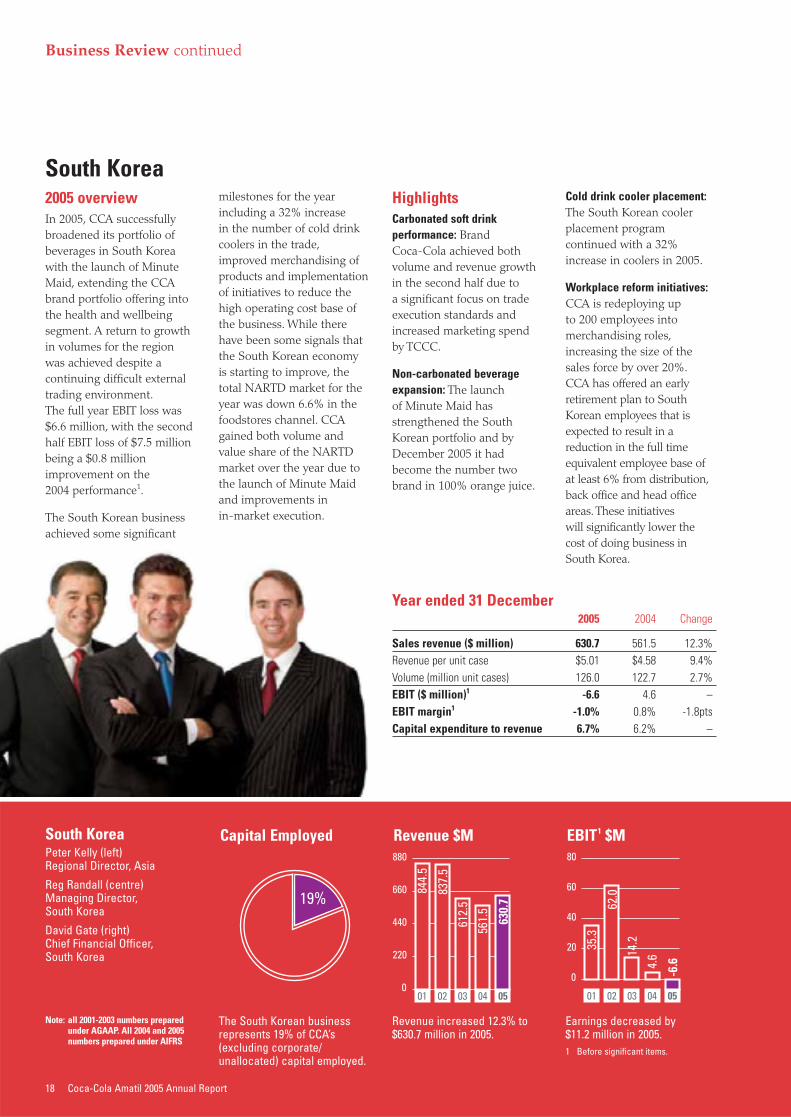

Year ended 31 December2005 2004 Change

Sales revenue ($ million) 630.7 561.5 12.3%Revenue per unit case $5.01 $4.58 9.4%Volume (million unit cases) 126.0 122.7 2.7%EBIT ($ million)1 -6.6 4.6 –EBIT margin1 -1.0% 0.8% -1.8ptsCapital expenditure to revenue 6.7% 6.2% –

The South Korean businessrepresents 19% of CCA’s(excluding corporate/unallocated) capital employed.

05040302010

220

440

660

880

630.

7

561.

5

612.

5

837.

5

844.

5

0504030201

0

20

40

60

80

-6.64.

614.2

62.0

35.3

Revenue increased 12.3% to$630.7 million in 2005.

Earnings decreased by $11.2 million in 2005. 1 Before significant items.

South KoreaPeter Kelly (left)Regional Director, Asia

Reg Randall (centre)Managing Director, South Korea

David Gate (right)Chief Financial Officer, South Korea

Capital Employed Revenue $M EBIT1 $M

19%

2005 overviewIn 2005, CCA successfullybroadened its portfolio ofbeverages in South Koreawith the launch of MinuteMaid, extending the CCAbrand portfolio offering intothe health and wellbeingsegment. A return to growthin volumes for the regionwas achieved despite acontinuing difficult externaltrading environment.The full year EBIT loss was$6.6 million, with the secondhalf EBIT loss of $7.5 millionbeing a $0.8 millionimprovement on the 2004 performance1.

The South Korean businessachieved some significant

milestones for the yearincluding a 32% increase in the number of cold drinkcoolers in the trade,improved merchandising ofproducts and implementationof initiatives to reduce thehigh operating cost base ofthe business. While therehave been some signals thatthe South Korean economyis starting to improve, thetotal NARTD market for theyear was down 6.6% in thefoodstores channel. CCAgained both volume andvalue share of the NARTDmarket over the year due tothe launch of Minute Maidand improvements in in-market execution.

HighlightsCarbonated soft drinkperformance: Brand Coca-Cola achieved bothvolume and revenue growthin the second half due to a significant focus on tradeexecution standards andincreased marketing spendby TCCC.

Non-carbonated beverageexpansion: The launch of Minute Maid hasstrengthened the SouthKorean portfolio and byDecember 2005 it hadbecome the number twobrand in 100% orange juice.

Cold drink cooler placement:The South Korean coolerplacement programcontinued with a 32%increase in coolers in 2005.

Workplace reform initiatives:CCA is redeploying up to 200 employees intomerchandising roles,increasing the size of thesales force by over 20%.CCA has offered an earlyretirement plan to SouthKorean employees that isexpected to result in areduction in the full timeequivalent employee base ofat least 6% from distribution,back office and head officeareas. These initiatives will significantly lower thecost of doing business in South Korea.

South Korea

Note: all 2001-2003 numbers preparedunder AGAAP. All 2004 and 2005numbers prepared under AIFRS

Coca-Cola Amatil 2005 Annual Report 19

Year ended 31 December2005 2004 Change

Sales revenue ($ million) 427.9 419.8 1.9%Revenue per unit case $3.45 $3.71 -7.0%Volume (million unit cases) 124.0 113.1 9.6%EBIT ($ million)1 42.9 32.4 32.4%EBIT margin1 10.0% 7.7% 2.3ptsCapital expenditure to revenue 9.0% 6.1% –

Indonesia & PNG represent 7% of CCA’s (excludingcorporate/unallocated)capital employed.

05040302010

100

200

300

400

500

427.

9

419.

8

450.

6496.

1

479.

6

05040302010

10

20

30

40

50

42.9

32.4

28.5

28.8

49.8

Revenue increased 1.9% to$427.9 million in 2005.

Earnings increased 32.4% in2005 and have increased at aCAGR2 of 14.2% since 2002.

Indonesia & PNGPeter Kelly (left)Regional Director, Asia

John Seward (centre)Managing Director, Indonesia & PNG

Steve Gallagher (right)Chief Financial Officer,Indonesia

Capital Employed Revenue $M EBIT1 $M

7%

2005 overviewThe Indonesian businessdelivered a standout result in2005 as it continued to buildon the gains made in 2004.Improved in-market executionhelped to drive increasedconsumption of CCA’sproducts and has been wellsupported by increased brandinvestment from TCCC.

In local currency terms,Indonesia delivered itshighest ever sales revenueand EBIT, with sales revenuegrowth of 13.2% and EBIT1

growth of 49.6%. However,

due to the 11% depreciationof the Indonesian Rupiahover the period, EBIT1 inAustralian dollars for theregion showed an increase ofonly 32.4% to $42.9 million.While the Indonesianbusiness has benefited fromthe removal of the 10% luxurygoods tax on carbonated softdrinks, the external marketconditions continued to bechallenging with naturaldisasters, currencyfluctuations and the removalof the fuel subsidy by theIndonesian Government.

Highlights – IndonesiaExpanding the soft drinkculture: Volume growth inIndonesia continues to gainmomentum by increasing theavailability and presence ofthe brands. Revenue fromCSDs grew by 12%, in localcurrency terms, led by brandCoca-Cola, Sprite and Fanta.

Product & package innovation:In 2005, major new productlaunches included Poweradeand Frestea Green Tea. TheCSD portfolio was expandedthrough the introduction ofpackage size and flavourextensions.

Outlet expansion: Indonesia’sactive customer base grew byover 20% to nearly 400,000direct served customers,supported by a larger salesforce.

Cold drink cooler placement:A key element of the strategyis to increase the presenceand availability of coldproduct. In 2005, coolernumbers increased by 20%and 60,000 ice chests wereplaced in the trade, anincrease of 60% for the year.

PNG delivered a strong full year result with localcurrency sales revenuegrowing 7.1% combined with solid EBIT margins.

Indonesia & PNG

1 Before significant items.2 Compound annual growth rate.

Note: all 2001-2003 numbers preparedunder AGAAP. All 2004 and 2005numbers prepared under AIFRS

20 Coca-Cola Amatil 2005 Annual Report

Business Review continued

Year ended 31 December2005 2004 Change

(10 months)

Sales revenue ($ million) 351.9 – –EBIT ($ million) 45.7 – –EBIT margin 13.0% – –Capital expenditure to revenue 6.2% – –

SPC Ardmona represents 22%of CCA’s (excluding corporate/unallocated) capital employed.

SPC ArdmonaNigel Garrard (left)Managing Director, SPC Ardmona

Steve Perkins (right)Chief Financial Officer,SPC Ardmona

Capital Employed

22%

2005 overviewFor the first 10 months under CCA ownership, SPCAdelivered a solid earningsresult with EBIT of $45.7 million, which wasslightly ahead of CCA’sexpectations. This wasdespite the impact of a softerconsumer environment inAustralia, as well as anintensifying competitiveenvironment which sawgreater competition fromimported private labelproducts.

2005 has been a year oftransition for SPCA, withinvestments in customerservice capability tostrengthen key relationships,

and capital commitmentsmade to warehouseconsolidation and capacityexpansion to build a strongeroperating platform for thefuture.

HighlightsProduct & package innovation:SPCA extended the uniqueresealable Fridge Pack rangein 2005 with Beetroot, PinkLady Apple and Pineappleofferings. The resealableFridge Pack, aimed ataccessing the snack andbreakfast market, hascontributed to significantgrowth in the fruit categorywith SPCA’s share, growingfrom nothing to 22% in justthree years.

New channel opportunities:One of SPCA’s key revenuegrowth opportunities is toleverage CCA’s distributioncapabilities to take SPCAproducts into new channels.In October 2005, SPCAsuccessfully trialled itsGoulburn Valley snack packrange in the convenience andpetroleum channel.

Supply chain improvements:Construction commenced of a $15 million warehousewhich will consolidate thenumber of offsite finishedgoods warehouses from 12 to two with expectations of savings to be in excess of $2 million per annum.In addition, SPCA will drivemanufacturing efficiencies by

increasing capacity by 30% for the high growth resealable plastic fruit packsand achieve cost reduction in the post production,labelling and handlingactivities through upgradingof manufacturing equipment.In 2006, SPCA willcommence triallingalternative productionmethods that will allow forthe production of more fruitbased products out of themain fruit season. Thisshould reduce inventorypeaks, increase ability to packto order and better utilise the permanent work force.

SPC Ardmona

Coca-Cola Amatil 2005 Annual Report 21

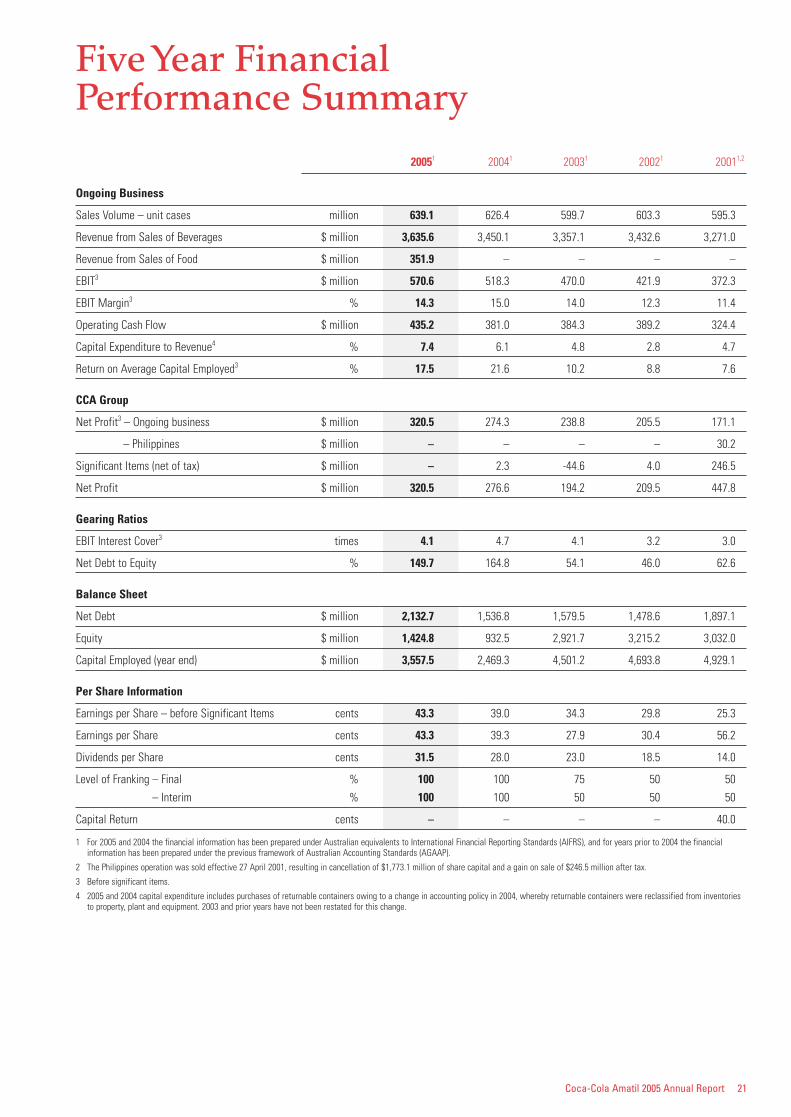

Five Year Financial Performance Summary

20051 20041 20031 20021 20011,2

Ongoing Business

Sales Volume – unit cases million 639.1 626.4 599.7 603.3 595.3

Revenue from Sales of Beverages $ million 3,635.6 3,450.1 3,357.1 3,432.6 3,271.0

Revenue from Sales of Food $ million 351.9 – – – –

EBIT3 $ million 570.6 518.3 470.0 421.9 372.3

EBIT Margin3 % 14.3 15.0 14.0 12.3 11.4

Operating Cash Flow $ million 435.2 381.0 384.3 389.2 324.4

Capital Expenditure to Revenue4 % 7.4 6.1 4.8 2.8 4.7

Return on Average Capital Employed3 % 17.5 21.6 10.2 8.8 7.6

CCA Group

Net Profit3 – Ongoing business $ million 320.5 274.3 238.8 205.5 171.1

– Philippines $ million – – – – 30.2

Significant Items (net of tax) $ million – 2.3 -44.6 4.0 246.5

Net Profit $ million 320.5 276.6 194.2 209.5 447.8

Gearing Ratios

EBIT Interest Cover3 times 4.1 4.7 4.1 3.2 3.0

Net Debt to Equity % 149.7 164.8 54.1 46.0 62.6

Balance Sheet

Net Debt $ million 2,132.7 1,536.8 1,579.5 1,478.6 1,897.1

Equity $ million 1,424.8 932.5 2,921.7 3,215.2 3,032.0

Capital Employed (year end) $ million 3,557.5 2,469.3 4,501.2 4,693.8 4,929.1

Per Share Information

Earnings per Share – before Significant Items cents 43.3 39.0 34.3 29.8 25.3

Earnings per Share cents 43.3 39.3 27.9 30.4 56.2

Dividends per Share cents 31.5 28.0 23.0 18.5 14.0

Level of Franking – Final % 100 100 75 50 50

– Interim % 100 100 50 50 50

Capital Return cents – – – – 40.0

1 For 2005 and 2004 the financial information has been prepared under Australian equivalents to International Financial Reporting Standards (AIFRS), and for years prior to 2004 the financialinformation has been prepared under the previous framework of Australian Accounting Standards (AGAAP).

2 The Philippines operation was sold effective 27 April 2001, resulting in cancellation of $1,773.1 million of share capital and a gain on sale of $246.5 million after tax.

3 Before significant items.

4 2005 and 2004 capital expenditure includes purchases of returnable containers owing to a change in accounting policy in 2004, whereby returnable containers were reclassified from inventoriesto property, plant and equipment. 2003 and prior years have not been restated for this change.

22 Coca-Cola Amatil 2005 Annual Report

Corporate Social Responsibilities Report

Across our six markets, CCA operates as a local business united with each local area through employees, customers, consumers andneighbours and government and community groups.

As a business, CCA activelysupports its localcommunities through:

• providing directemployment in the regionand ensuring employeesdevelop skills in safeworkplaces;

• using local materials andsuppliers wherever practicalto aid the development ofthat location; and

• providing a profitableconsumer product thatassists our customers’businesses to grow.

Providing support to socialand environmental activitiesis firmly entrenched in CCA’sbusiness plans. The creationof profits enables CCA toexpand our community andenvironmental programs. Inturn, these programs help to

sustain business performanceby strengthening localeconomies, improvingbusiness efficiency anddeveloping relationships withstakeholders, ultimatelyleading to increasedshareholder returns.

Our communityAcross six geographiclocations, CCA providessupport to establishedprograms while alsosupporting new, innovativeprograms that focus on socialissues which benefit localcommunities.

In Australia, Indonesia andSouth Korea, this support is channelled throughFoundations jointly fundedby CCA and TCCC. Manyprograms supported through

these Foundations are basedon the promotion of healthyactive lifestyles in youngpeople and empoweringthem through education.

In 2005, CCA Indonesiacontinued to assist inrebuilding efforts after the 2004 Boxing Day Tsunami. Support throughThe Coca-Cola IndonesiaFoundation (CCIF) includes the allocation of AUD 1 million to be spentacross 2005-06 on revitalizingsmall businesses within Aceh. To date, AUD 500,000 has been disbursed to 250entrepreneurs in the form of kiosks, ice chests, workingcapital and other assistance to support their businesses.

Coca-Cola Indonesia’sLearning Centre Programreceived a CSR Award fromthe Asian Institute ofManagement for assistancewhich has helped transformpublic libraries into LearningCentres. Since 2000, theProgram has developed 24 Learning Centres across14 provinces.

In 2005, CCA in South Koreasupported local events suchas the 9th InterdisciplinaryCongress on Women andFood Bank’s Food DonationDay, with Foundationsupport channelled to 16 underprivileged groupsincluding orphanages andfacilities for the disabled and elderly.

The Active Factor program supports a number of initiativestargeted towards increasing activity in children. Active Factor is aproactive and responsible approach to helping government andcommunity groups address the issues of obesity in Australia.

Over 300,000 people attended the 12th annualCoca-Cola Christmas in the Park in Auckland and Christchurch, New Zealand. In 2006, theevent won a judges special mention award at the New Zealand Sponsorship Awards.

Coca-Cola Amatil 2005 Annual Report 23

New Zealand, PNG and Fijifocused their 2005 activitieson a range of communityprograms.

In New Zealand, CCAcontinued its support ofcommunity and non-profitorganisations includingYouthline and Out of School Care and Recreation(OSCAR). In partnershipwith OSCAR, the Coca-Colasystem supports activelifestyles through theunbranded ‘Go Kids!’program, with up to 11,000children participating each day.

In 2005, Australia allocatedapproximately AUD 1 millionthrough the Coca-ColaAustralia Foundation. Fundswere allocated to innovativeprograms focused ondisadvantaged youth as well

as programs which deliverthe capacity to touch andchange lives.

Examples of the programssupported in 2005 include:

• Australian Literacy andNumeracy Foundation’s‘Remote Schools Project’which provided accreditedliteracy course work toEnglish teachers andIndigenous non-teachersin remote, isolated orcountry schools;

• The Barnardos Australia‘Parenting Skills Program’which is aimed atdeveloping a unique skills-based parentingprogram for the family oftroubled adolescents; and

• Beyond Empathy’s‘Pathways’ mentoringstrategy which is aimed atproviding disadvantaged

young people withleadership skills toestablish and manage artsprojects within their owncommunities, to effectchange and eventuallybreak the welfare cycle.

Health and wellbeingCCA is aware of thecommunity concern andongoing public discussionover the impact that lessactive lifestyles are having onour physical health. CCA istaking a leadership positionin the debate and developinga wide-ranging approach tothe issue:

• we are expanding ourbeverage range to providechoice for everyone –carbonated beveragescontaining sugar, lowcalorie beverages, water,plain and flavoured

mineral waters, fruit juices,sports drinks, iced tea andcoffee. Our fruit andvegetable productioncompany, SPC Ardmona,makes a large range ofhealthy fruit snacks;

• we actively supportprograms designed toencourage young people to be more physicallyactive; and

• we engage in responsiblemarketing practicesparticularly in regard tochildren – we do not aimor direct any marketingactivity to children under12, and since 2004,we have voluntarilywithdrawn our carbonatedbeverages containing sugarfrom primary schools inAustralia and NewZealand for consumptionby students.

CCA Indonesia continued to assist victims of the2004 Boxing Day Tsunami. AUD 500,000 of the AUD 1 million pledged by The Coca-Cola IndonesiaFoundation has already been disbursed.

24 Coca-Cola Amatil 2005 Annual Report

Corporate Social Responsibilities Report continued

Our environmentCCA is committed tounderstanding andminimising any adverseenvironmental impacts of our beverage and foodmanufacturing activities,recognising the key areas of impact are water andenergy use, and postconsumer waste.

Our key beverage operationsacross Australia, NewZealand, South Korea and Indonesia have certifiedISO14001 environmentalmanagement systems inplace, ensuring risksassociated with ourmanufacturing processes are identified andappropriately managed.

Saving water/reducing wasteAdvanced data collectionprocesses enable us to track our environmentalperformance within the keyareas of water and energyuse and waste, and identifyopportunities for furtherimprovement. For beveragemanufacturing, CCAmeasures the amount ofwater and energy used in theproduction of one litre of finished beverage. 2005saw Australian beverageoperations further embracewater conservation with theimplementation of watersavings initiatives resulting in a 4% reduction in wateruse per finished beveragelitre. This equates to a directwater saving of over 95 million litres.

Improvements in wastemanagement across ourAustralian beverageoperations have also seen anincrease in onsite recyclingrates, bringing the currentrate to 77% diversion fromlandfill. In New Zealand,CCA currently recycles 86%of all its solid waste and isconstantly looking for newand innovative ways toreduce waste.

Better packagingCCA’s commitment to wastereduction and best practicein manufacturing alsoextends to our continuedinvolvement in nationallybased packaging initiatives.

We recognise that as amanufacturer of fast-movingconsumer goods, we have arole to play in reducing theenvironmental impact of ourpackaging on the community.CCA’s methodology foraddressing this issue variesacross our geographiclocations due to variations inpackaging, reprocessing andcollection facilities.

The New Zealand businesshas joined forces withindustry, government, andwaste management non-government organisations as active members of the2004 Packaging Accord andthe Government-led LitterAlliance. The Accord hasstretch recycling targets forpaper (55%), aluminium(65%), glass (55%), plastic(23%) and steel (43%) to be

CCA is an active player in the community, proudly partnering with several national and state-based Australian charities. Mission Australia,CanTeen, WWF and Children’s Hospitals in each state benefit from support that includes product donations and employee donations.

Coca-Cola Amatil 2005 Annual Report 25

reached by 2008. CCA playeda pivotal role in the industrygroup that solved the glasscollection crisis that almosttoppled kerbside collection in New Zealand.

The New Zealand businesshas also established abeverage industry actiongroup (EBAG) to address and achieve the targets setunder the Packaging Accord.Achievements of this groupto date include membercompanies ensuring all theirpackaging is recyclable anddevelopment of nationalevent recycling guidelines.These have been successfullytrialled at Coca-ColaChristmas in the Park inAuckland and Christchurch.

CCA, with the support of theMinister of Environment andEBAG, launched the firstindustry-led public placerecycling trial in Botany,Auckland.

In Australia, CCA continuesits involvement in theNational PackagingCovenant (NPC), throughinitiatives undertakenthroughout our operationsand within the publicdomain. The co-regulatoryagreement between industryand all spheres ofgovernment has set anoverall recycling target of65% for achievement by2010. CCA will play an activerole in contributing to theachievement of this target.Implementation of the

Environmental Code ofPractice for Packagingdemonstrates ourcommitment to theprinciples of shared product stewardship.

Helping consumers recycleIn 2004, CCA Australiacommenced a five yearstrategy working with localgovernment and authoritiesto increase the recovery ofpackaging for our productsconsumed away from thehome. CCA’s Public PlaceRecycling program continuesto grow in strength andimpact since its launch in December 2004 andinitiatives established in 2005include targeted recyclingprograms at Taronga ParkZoo and Thredbo AlpineVillage in New South Wales.

SPCA has a renewed focuson environmentalperformance, with targetedreductions in water andenergy consumption, andsolid waste reduction to take effect in 2006.

Changes in packaging designhave resulted in a number of packaging modifications,including reduction in canheight which has saved morethan 100 tonnes of steel.SPCA is also exploringpartnership programs withinits local communities whichpromote public placerecycling and education toreinforce more sustainablewaste behaviours.

Summary of environmental performance of key Australian operations in 2005

Water consumed

1.39 litres of water are used in making 1 litre of finished product.

Solid waste to landfill

0.71 kg of solid waste goes tolandfill for every 1,000 litres of finished product made.

Energy consumed

0.24 MJ of energy are used in making 1 litre of finished product.

Solid waste to recycling

2.34 kg of solid waste goes torecycling for every 1,000 litres

of finished product made.

These figures represent performance of carbonated beverage operations within Australia.

Being the market leader hasanother upside – it meanswe attract the best people towork for us.

As well, we actively seek thebest. Our talent search anddevelopment programs arefocused on finding peoplewho are comfortablechallenging the status quoand who can create andexecute innovative solutionsfor our customers.

Our remuneration programshave been progressivelychanged to reward individualand team performances.This in turn has createdstrong internal competitionfor promotion.

A key focus for 2005 has been to improve theleadership capability acrossall levels of management.The Company has rolled outcomprehensive leadershipprograms across the Group.

A successful strategy in thepast 12 months has been thetransfer of key managementfrom CCA into our newbusinesses. In 2005, weacquired SPC Ardmona and Grinders coffee and bothorganisations, like Neverfailwhich we acquired in 2003,have benefited from seniormanagers transferring fromCCA Beverages into salesand finance functions.These managers and theirexisting teams have had animmediate impact on therelationship with our

customers – planning hasbeen improved, growthinitiatives are beingdeveloped and at SPCA therehas been a positive change in the in-store positioning of products.

CCA’s leadership programshave enjoyed particularsuccess in businesses inIndonesia, South Korea,PNG and Fiji. In Indonesia,for example, a key initiativefor developing leaders of the future was the NationalGraduate Training Program,where 53 universitygraduates were selected from 1900 applicants acrossIndonesia to take part in anintensive 10 month program.

Those participants whograduate in May 2006 will beplaced in leadership rolesacross the country.

In New Zealand and South Korea, ’Coke Uni’was launched – a staff

development program whichincluded comprehensiveleadership training and salesskills. In New Zealand, the‘Leading the Way’ program,which used externalexecutive coaches, won the International CoachFederation AustralasianOrganisational Award.

Below: The Mentone DistributionCentre employees who contributedto CCA winning the prestigiousComino Trophy. From left to right:Jenny Hall, Process ImprovementCo-ordinatorSimon Wilkins, ProcessImprovement Manager Tracey Wagner, who manages the Mentone Distribution Centre

26 Coca-Cola Amatil 2005 Annual Report

CCA People

We make and sell some of the most loved consumer brands in the world.In Australia, for example, brand Coca-Cola is placed in more shoppingtrolleys than any other grocery product – it’s been number one for arecord 13 years in a row.

Awards

2005 Australian Packaging Awards

Silver Award in the ‘ConsumerAcceptability’ category for SPCBrekky Fruit range.

Foodbank Award for Innovationfor Share A Can contribution

Every Drop Counts programwith Sydney Water

CCA New South Wales wasawarded the highest honourduring the Sydney WaterAnnual Water ConservationAwards (10 November 2005),with the Sustainable BusinessPractices and ProcessesAward. This award reflects theongoing water savings as wellas a business commitment toresponsible water usemanagement.

Comino Trophy for Storage and Handling of Materials For significant achievement inthe techniques and technologyof materials handling andstorage throughout the supply chain.

Improvements, innovation andorganisational impacts in rawmaterials, manufacturing,distribution, fulfilment,shipping, freight forwarding,wholesale and retailoperations.

SPC Ardmona Australian Beverages

CCA recognises that the keyto our success is to attractand retain the best people,and we are developing arange of new and innovativeplans to deliver moreflexibility in the workplace.

We recognise the importanceand value of a balanced anddiverse workforce, with agood mix of men andwomen from different agegroups right across theexperience spectrum.

In Australia, our people canpurchase additional annualleave, which has been verywell received. As well, thereare programs to helpworking parents, includingthe provision of childcareduring school holidays.

New Zealand Beverages

Coca-Cola Amatil 2005 Annual Report 27

Below: New Zealand managers whoparticipated in ‘Leading the Way’ in June 2005. From left to right:Sally Doherty, OD ManagerHamish Wright, BusinessDevelopment Manager HoReCaBrendan Lindsay, National Channel Development ManagerKim Dorling, Supply ChainPerformance ManagerGraeme Urbahn, PutaruruManufacturing ManagerKylla Peterson, Supply PlanningManagerColin Satele, Business Development ManagerMarc Brokenshire, Market Manager C&L

Kiwi Blue dressed to impressA stylish bottle andcontemporary logo designhanded the silver medal toKiwi Blue Pure Spring Water atthe 2005 Summit CreativeAwards in Portland, Oregon.

Coke cleans up New Zealand Beverage AwardsThe second annual NZJBABeverage Awards were held inAuckland on 7 October 2005,where 56 products wereentered.

CCA and TCCC topped the fieldin the following categories:

Water still or sparkling:Kiwi Blue Still Spring Water

Reconstituted fruit juice:Keri Crush Tropical

Diet/light: L&P Sweet As

Carbonated beverages:Coca-Cola Raspberry

Energy/lifestyle: e2 EnergyCitrus Kick

Packaging award: Kiwi BlueStill Spring Water 600mL PET

28 Coca-Cola Amatil 2005 Annual Report

CCA People continued

CCA is the largest bottler of non-alcoholic ready-to-drinkbeverages in the Asia-Pacific region and one of the top five Coca-Cola bottlers in the world, employing close to 19,000 people.CCA beverages operates in six countries – Australia, New Zealand,Fiji, South Korea, Indonesia and Papua New Guinea and hasaccess to 283 million consumers through over 600,000 activecustomers. SPC Ardmona is primarily Australian based and is the largest supplier of ready-to-eat fruit and vegetable products in Australia.

When it comes to health andsafety at work, CCA believesthat all workplace injuries arepreventable, and we continueto be committed to providingand maintaining a safe andhealthy workplace for allemployees, suppliers,contractors and visitors.We acknowledge thatOccupational Health andSafety (OH&S) is the

responsibility ofmanagement and eachemployee and we recognisethe importance of promotingthe highest principles andpractices to ensure healthand safety across ouroperations.

The CCA OH&SManagement System is anintegrated management

system which is constantlyevolving. The systems aremodelled on a ’best practice’approach where all OH&Slegislative requirements areconsidered and the nationalCCA standard is based onthe most stringent level.Each country of operation or business unit has adesignated OH&S

representative responsible forplanning and reporting onOH&S performance to theBoard each quarter.

The Emerging Leader Program in Australia aims to provide theindividual with key informationwhich will assist them indeveloping a number ofmanagement skills and behavioursto be an effective leader at CCA.

1. 2. 3. 4. 5. 6. 7.

Coca-Cola Amatil 2005 Annual Report 29

Senior Management

1. John WartigChief Financial Officer, Age 49

Appointed in June 2004

Background: John waspreviously Senior Vice PresidentFinance for Cadbury SchweppesAmericas Beverages (a US$3 billion operating revenuedivision of Cadbury SchweppesPlc). Prior financial roles withinCadbury Schweppes includedFinance Director – Operations,with global responsibilities across the total Beverages andConfectionary group and SVPFinance – Asia Pacific Beverages.

John is an Australian citizen whohas worked both in Australia andoverseas. He has held a numberof senior financial roles withinFMCG companies and hasextensive operational and M&A experience.

2. Warwick WhiteManaging Director –Australia, Age 44

Appointed in November 2002

Background: Warwick has 24years in the Coca-Cola system and rejoined Coca-Cola Amatil inNovember 2002 as the ManagingDirector of Australia.

Warwick has held mainlymarketing and generalmanagement roles since joiningthe Coca-Cola system in the early1980s. Prior to joining CCA,Warwick was the RegionalDirector for Coca-Cola HellenicBottling Company withresponsibility for Ireland, Poland,Hungary, Czech Republic andSlovakia. This was preceded by 13 years in Great Britain, Europeand Ireland in progressively more senior roles.

3. Peter KellyRegional Director – Asia, Age 40

Appointed in August 2005

Background: Peter has over 18 years in the Coca-Cola system,joining The Coca-Cola Company in 1988 in Marketing and CCA in1993 to take up state and thennational general managementroles. Most recent roles havebeen as Director of BusinessDevelopment for the CCA Groupand as Director of Operations and Logistics for the Australianbusiness.

4. Reg RandallManaging Director – South Korea, Age 41

Appointed in February 2006

Background: Reg has over 8 years experience in the Coca-Cola system and joined CCAas General Manager for the SouthEast Division in South Korea. Hehas been in South Korea for oversix and a half years during whichtime he has also held the roles of Executive Director Marketingand Executive Director SalesOperations. Reg came to Koreafrom South Africa where he wasthe General Manager, Zululand for the largest South AfricanCoca-Cola Bottler, ABI. He hasalso held senior roles in sales,marketing and generalmanagement within the FMCGindustry in South Africa.

5. George AdamsManaging Director – New Zealand & Fiji, Age 39

Appointed in December 2003

Background: George joined CCAin early December 2003. He hasworked as Finance Director forBritish Telecom Regions based in Ireland. He brings valuableexperience to CCA’s managementteam having also spent 10 yearsin the Coca-Cola system in Europein a number of finance, IT andcommercial roles.

6. John Seward Managing Director –Indonesia & PNG, Age 49

Appointed in August 2004

Background: John has spent nineyears in the Coca-Cola system,joining CCA in 2004 having run theNigerian Bottler for Coca-ColaHellenic Bottling Company since1997. Prior to this, he has heldsenior positions in the FMCG andthe packaging businesses inEurope, Middle East and in the US.The majority of his career has beenin sales and operations both instaff and general managementroles and he brings a wealth ofinternational experience to CCA.

7. Nigel GarrardManaging Director – SPC Ardmona, Age 45

Appointed in February 2005

Background: A qualifiedChartered Accountant, Nigeljoined SPC Ltd in 2000 asManaging Director and has over14 years experience in the foodindustry. He was instrumental inthe successful merger of SPC andArdmona Foods, creating one ofAustralia’s leading foodmanufacturers. Prior to joiningSPCA, Nigel undertook a numberof regional roles in Australia andNew Zealand over a 10 yearperiod with the US based ChiquitaBrands International. Nigel is alsocurrently Chairman of NationalFood Industry Strategy Ltd.

30 Coca-Cola Amatil 2005 Annual Report

Board of Directors

1. David Gonski, AOChairman, Non-ExecutiveDirector (Independent) – Age 52

Joined the Board in October1997 – Chairman of Related PartyCommittee and NominationsCommittee and member ofCompensation Committee.

Background: Solicitor for 10 years with the law firm ofFreehills and thereafter acorporate adviser in the firm ofWentworth Associates, now partof the Investec group.

Degree: Bachelors of Law andCommerce from the University of New South Wales.

Other Listed Company Boards:Australia and New ZealandBanking Group Ltd; WestfieldGroup.

Other Directorships held in thelast three years: ING Group(2004); John Fairfax Holdings Ltd(2005).