Embed Size (px)

Citation preview

Allocation of CO2 Emission Allowances in RGGI

Dallas Burtraw, Karen Palmer, Danny KahnResources for the Future

Presentation to RGGI Stakeholder MeetingApril 6, 2005

Thanks to: The Energy Foundation, The Packard Foundation and New York Community Trust

Project Goals

1) Measure cost of various approaches to initial distribution of allowances. We do not consider costs outside the electricity sector.

2) Describe distributional consequences between consumers and producers, and among producers.

3) Identify ancillary effects and other considerations.

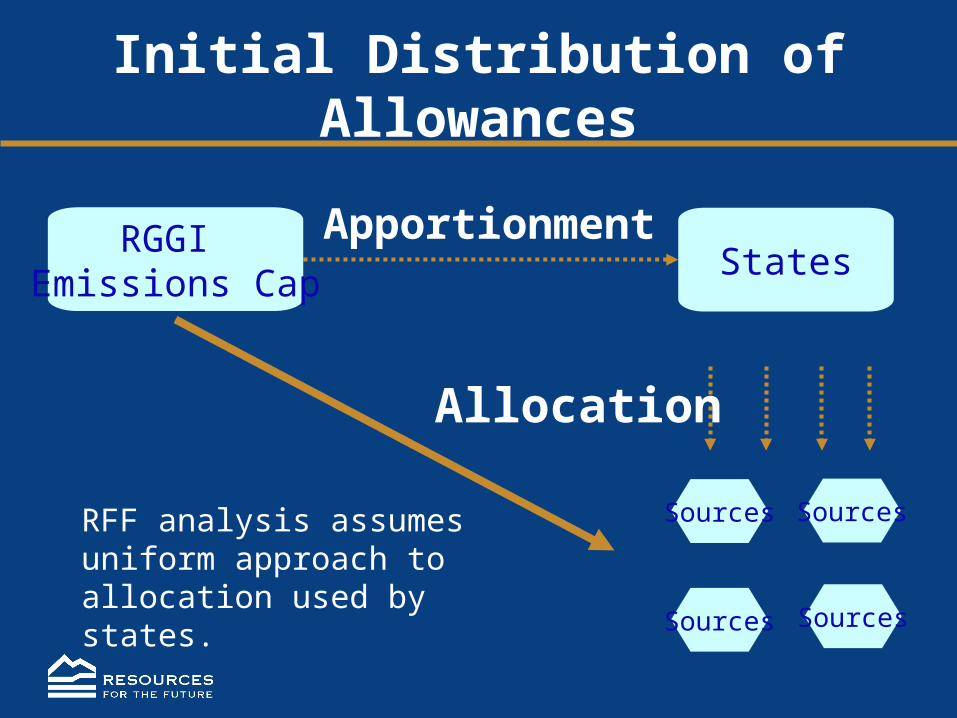

Initial Distribution of Allowances

Sources

Sources

Sources

Sources

RGGI Emissions Cap

StatesApportionment

Allocation

RFF analysis assumes uniform approach to allocation used by states.

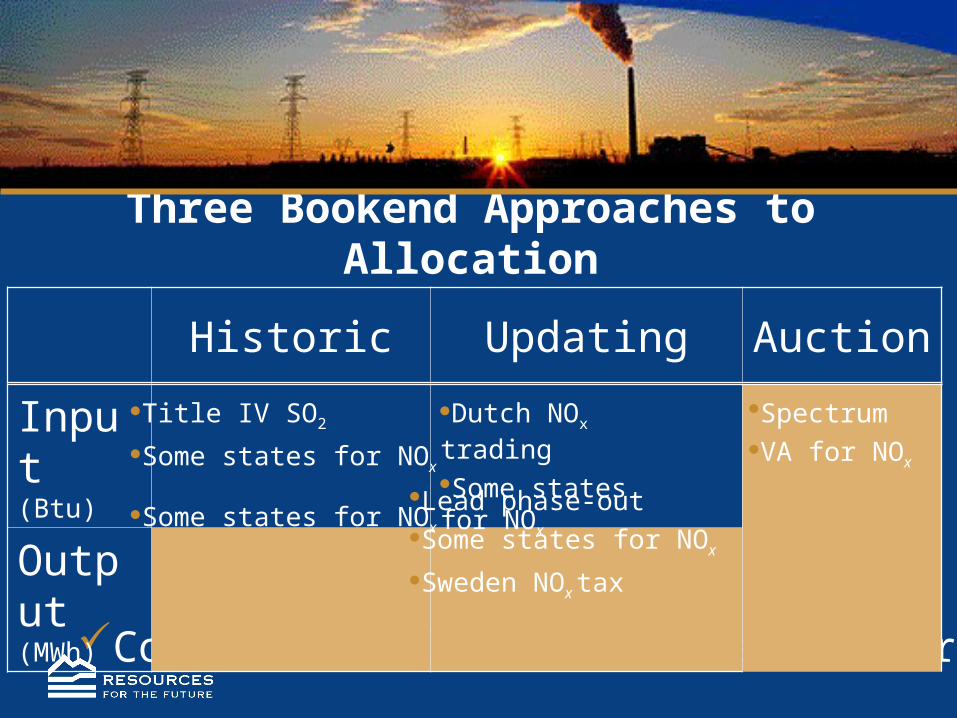

Three Bookend Approaches to Allocation

Historic Updating Auction

Common formula across fuels, sources?

Input(Btu)

Output(MWh)

Title IV SO2

Some states for NOx

Some states for NOx

Dutch NOx trading

Some states for NOx

Lead phase-outSome states for NOx

Sweden NOx tax

Spectrum VA for NOx

Scenarios

Policy: Start at 2008 baseline CO2 emissions and phase down by 20% by 2025 in nine state region.

Three bookend approaches to allocation:

Auction: Revenues have value in analysis.

Historic Generation: Allocation to all incumbent emitters based on 1999 shares of generation.

Updating: Allocation to emitters based on generation from 2 years previous.

About a dozen derivative approaches and combinations are also explored.

General Conclusions First…

Due to electricity deregulation, Auction and Historic approaches yield the same electricity price, and the same social cost. We do not look at costs outside electricity sector (doing so would favor an Auction).

Updating yields a slightly lower electricity price and more generation in the region, but at a higher social cost. Updating yields lower emissions of SO2, NOx, mercury in region.

Allowance value is at least four times the social cost.

The initial distribution of allowances determines which producers and consumers bear the cost of the program.

1) Economic Efficiency

Generally, the Auction and Historic approaches are similar because of competitive pricing in northeast electricity markets.

The Auction and Historic approaches are more efficient than the Updating approach.

Substantial variety exists among Updating approaches, with some approaches also relatively efficient.

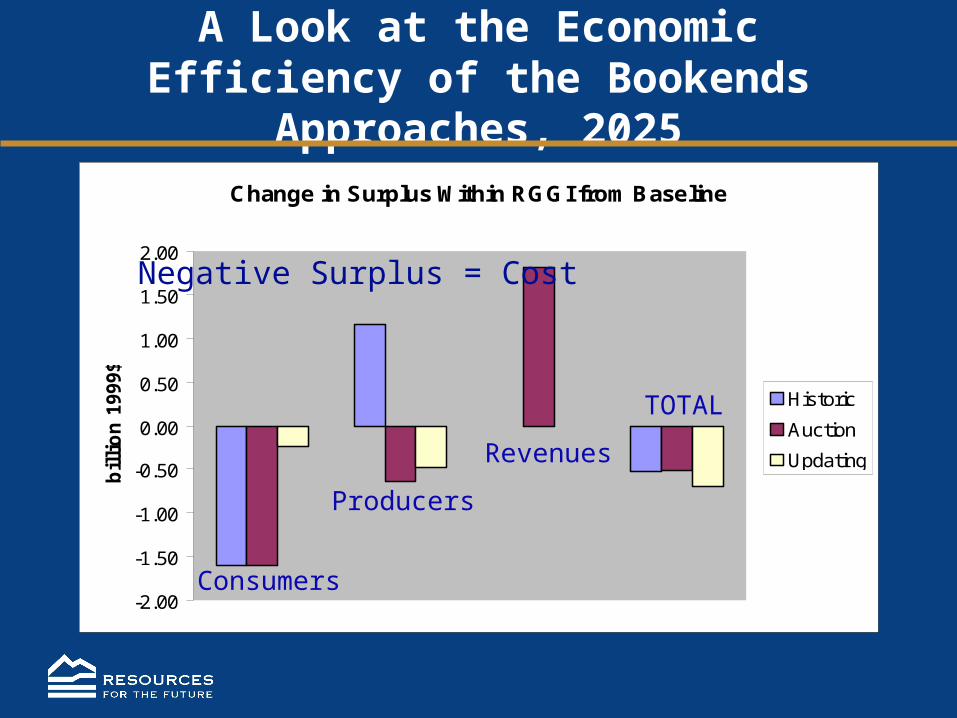

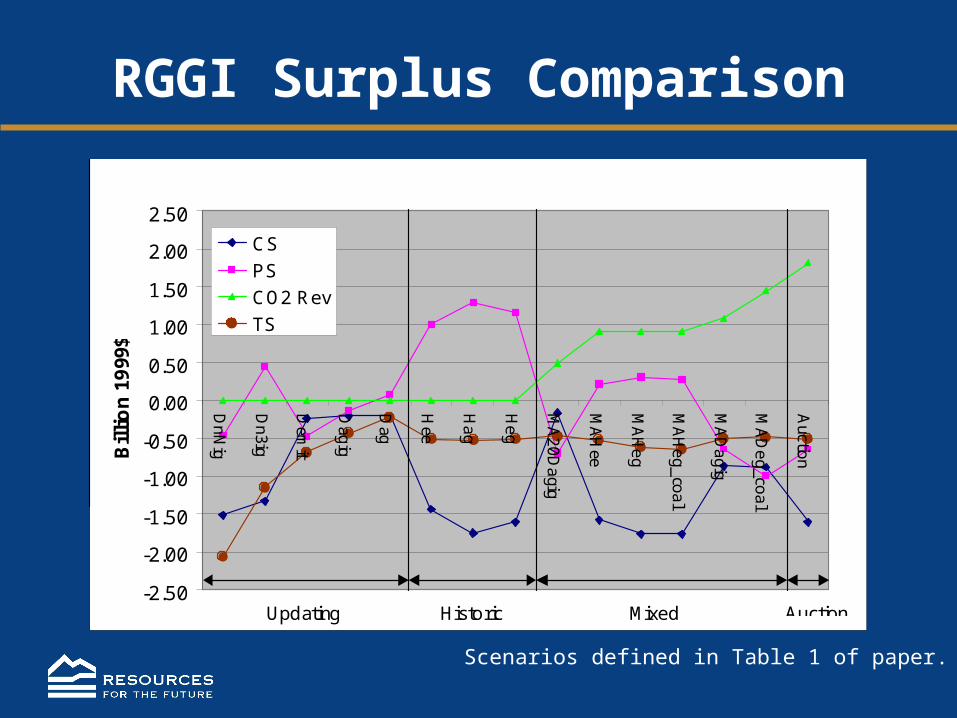

A Look at the Economic Efficiency of the Bookends Approaches, 2025

Change in Surplus Within RGGI from Baseline

-2.00

-1.50

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

bil

lio

n 1

999$

Historic

Auction

Updating

Consumers

TOTAL

Revenues

Producers

Negative Surplus = Cost

Additional Cases

Transmission Constraints

High Natural Gas Prices

Renewable Policies None of these potential outcomes increase the cost of RGGI

relative to the respective baselines.

Tighter gas or transmission constraints benefit producers in the aggregate. These constraints have a greater impact on electricity price than does the RGGI program.

Mixed Cases Combining approaches generally leads to intermediate results.

2) Allowances as Compensation

Compensation is justification for free distribution. How much compensation is sufficient?

Firms charge consumers for using emission allowances, whether the allowances were received for free or at a cost.

Fixed price contracts mitigate the ability to pass through costs in the short run.

Are other segments of the economy/society also candidates for compensation?

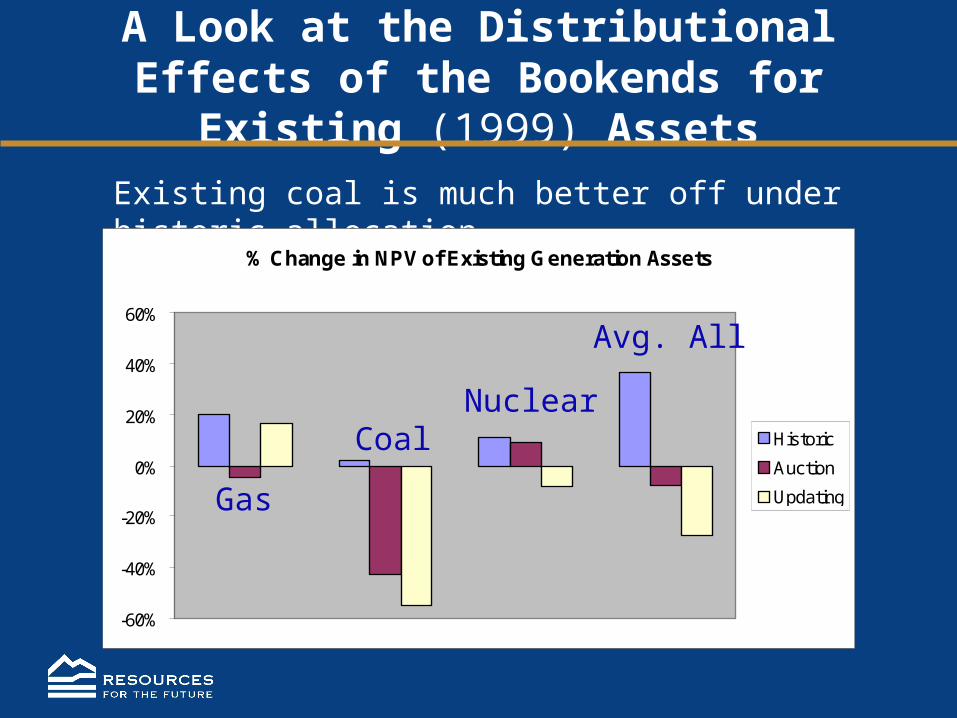

A Look at the Distributional Effects of the Bookends for Existing (1999) Assets

Existing coal is much better off under historic allocation

% Change in NPV of Existing Generation Assets

-60%

-40%

-20%

0%

20%

40%

60%

Historic

Auction

UpdatingGas

Avg. All

NuclearCoal

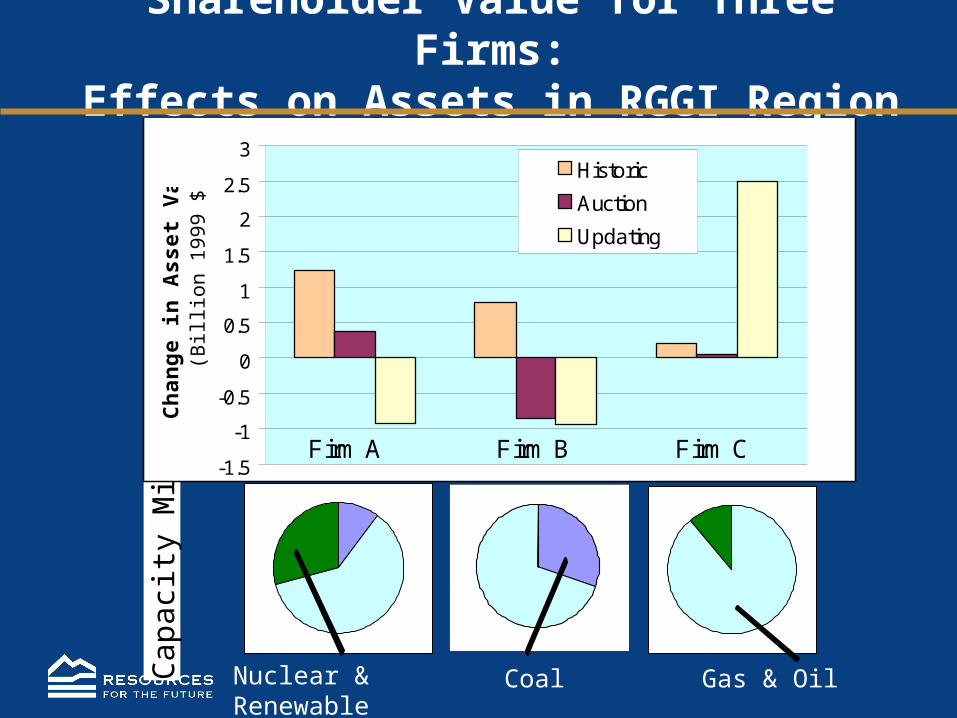

Shareholder Value for Three Firms:Effects on Assets in RGGI Region

Nuclear & Renewable Gas & Oil

Cap

acit

y M

ix

Coal

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

3C

ha

ng

e in

As

se

t V

alu

e(B

illio

n 19

99 $

)Historic

Auction

Updating

Firm A Firm CFirm B

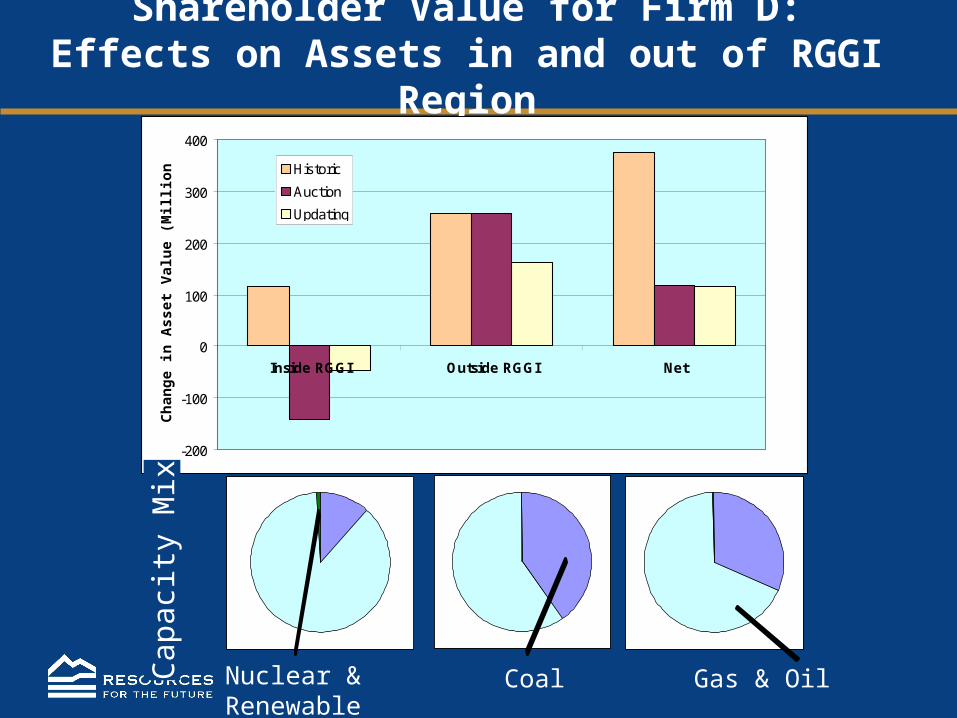

Shareholder Value for Firm D:Effects on Assets in and out of RGGI Region

-200

-100

0

100

200

300

400

Inside RGGI Outside RGGI Net

Ch

ang

e in

Ass

et V

alu

e (M

illi

on

199

9 $) Historic

Auction

Updating

Nuclear & Renewable Gas & Oil

Cap

acit

y M

ix

Coal

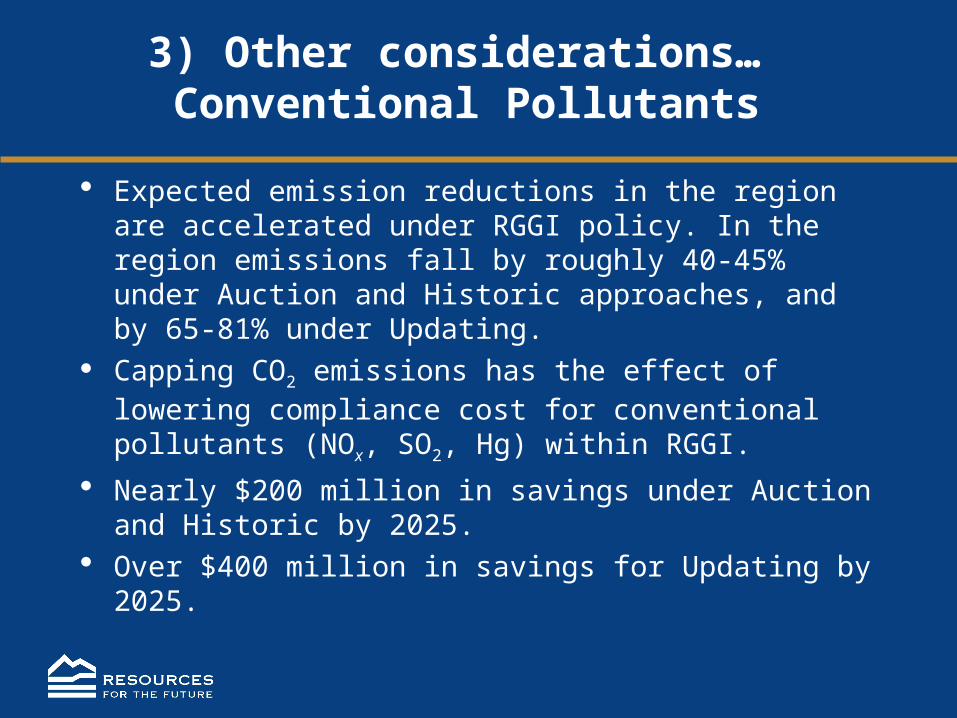

Expected emission reductions in the region are accelerated under RGGI policy. In the region emissions fall by roughly 40-45% under Auction and Historic approaches, and by 65-81% under Updating.

Capping CO2 emissions has the effect of lowering compliance cost for conventional pollutants (NOx, SO2, Hg) within RGGI.

Nearly $200 million in savings under Auction and Historic by 2025.

Over $400 million in savings for Updating by 2025.

3) Other considerations… Conventional Pollutants

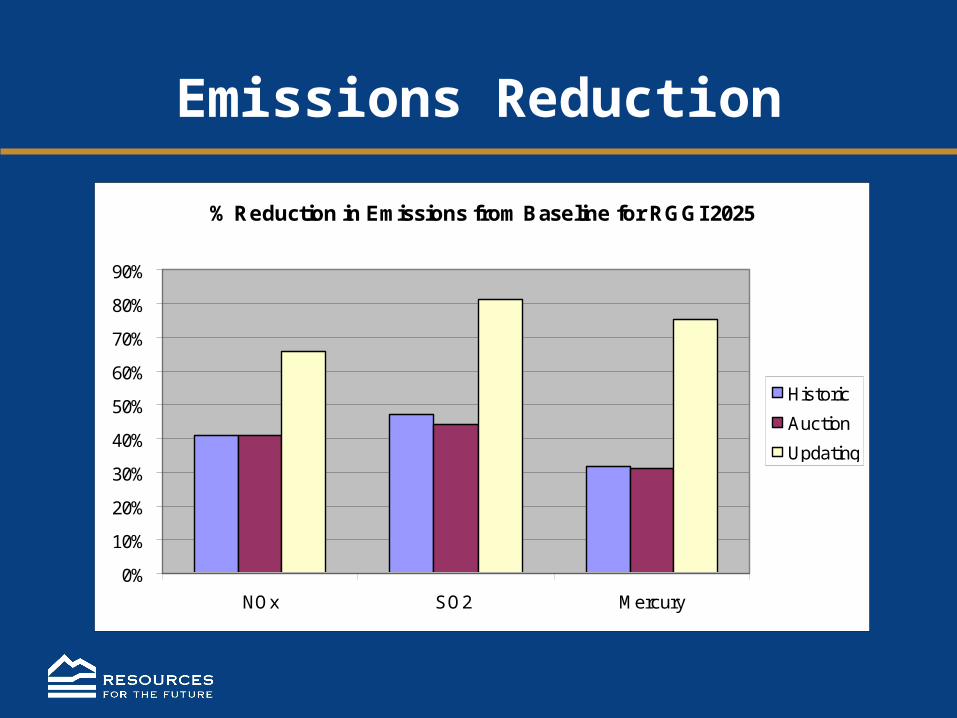

Emissions Reduction

% Reduction in Emissions from Baseline for RGGI 2025

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

NOx SO2 Mercury

Historic

Auction

Updating

Closing Observations

Auction, Historic are most efficient but Updating leads to lower electricity prices.

Change in shareholder value depends on the portfolio of assets. A firm may have facilities that lose and that gain value, inside and outside of the region.

Cost of the RGGI policy is not sensitive to natural gas or transmission constraints. Tighter constraints benefit producers in the aggregate in the baseline. These constraints have a greater impact on electricity price than does the RGGI program.

Combining approaches generally leads to intermediate results. We suggest the emphasis given to compensation versus

efficiency can differ between the short run and long run for RGGI planners.

For More Information

www.rff.org/multipollutant

Experiments

Simulation model: Highly parameterized national model of electricity sector.

Regulation: Limited restructuring. Scenario: Start at 2008 baseline emissions and

phase down by 20% by 2025. RGGI: Nine state region with MAAC power region

split. All new emitting plants in MAAC located outside of RGGI with new renewable plants inside RGGI.

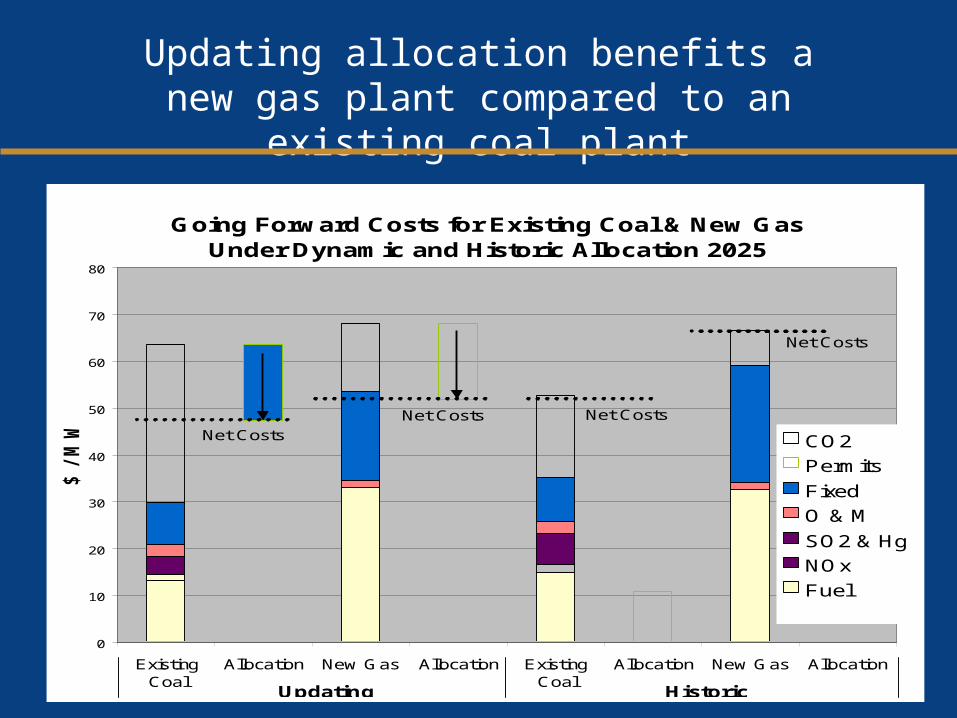

Going Forward Costs for Existing Coal & New Gas Under Dynamic and Historic Allocation 2025

0

10

20

30

40

50

60

70

80

ExistingCoal

Allocation New Gas Allocation ExistingCoal

Allocation New Gas Allocation

$ / M

WH

CO2

Permits

Fixed

O & M

SO2 & Hg

NOx

Fuel

Updating Historic

Net Costs

Net Costs

Net Costs

Net Costs

Updating allocation benefits a new gas plant compared to an existing coal plant

What is meant by Efficiency? There are several measures of efficiency

Engineering measures. Technical (static) economic efficiency – equalize marginal

cost at facilities will minimize resource costs. This is the usual measure of success of trading programs but it is not a complete measure of efficiency.

Dynamic efficiency – technological change. Most important measure is social cost within formal benefit-

cost analysis – changes in economic surplus. In the short run efficiency may be less important than

feasibility. In the long run efficiency is crucial if society moves towards more substantial carbon reduction goals.

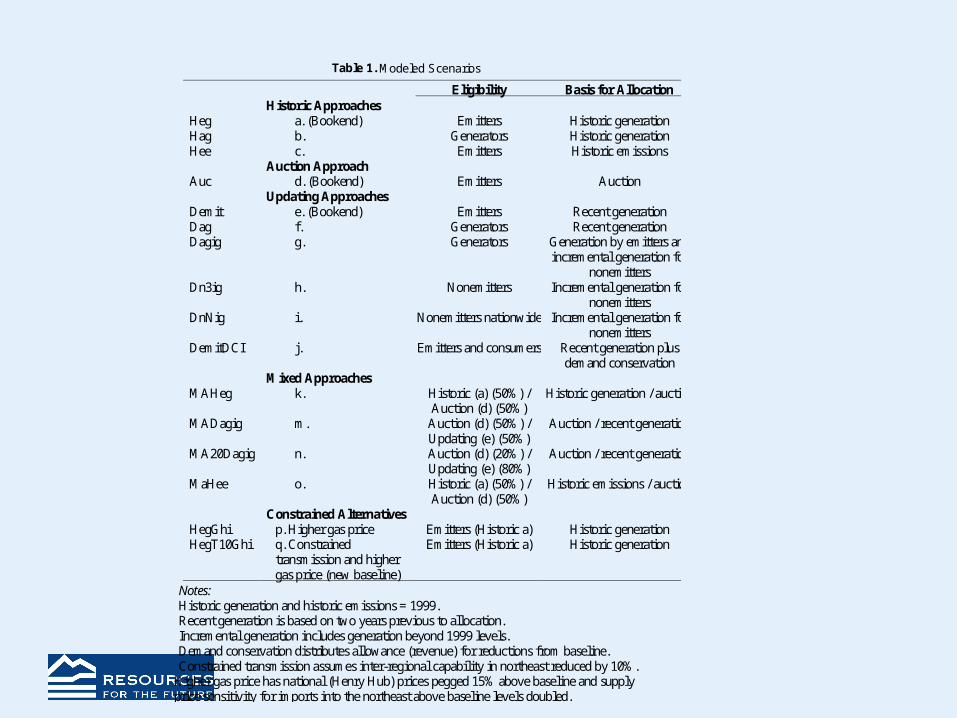

Table 1. Modeled Scenarios

Eligibility Basis for Allocation Historic Approaches Heg a. (Bookend) Emitters Historic generation Hag b. Generators Historic generation Hee c. Emitters Historic emissions Auction Approach Auc d. (Bookend) Emitters Auction Updating Approaches Demit e. (Bookend) Emitters Recent generation Dag f. Generators Recent generation Dagig g. Generators Generation by emitters and

incremental generation for nonemitters

Dn3ig h. Nonemitters Incremental generation for nonemitters

DnNig i. Nonemitters nationwide Incremental generation for nonemitters

DemitDCI j. Emitters and consumers Recent generation plus demand conservation

Mixed Approaches MAHeg k. Historic (a) (50%) /

Auction (d) (50%) Historic generation / auction

MADagig m. Auction (d) (50%) / Updating (e) (50%)

Auction / recent generation

MA20Dagig n. Auction (d) (20%) / Updating (e) (80%)

Auction / recent generation

MaHee o. Historic (a) (50%) / Auction (d) (50%)

Historic emissions / auction

Constrained Alternatives HegGhi p. Higher gas price Emitters (Historic a) Historic generation HegT10Ghi q. Constrained

transmission and higher gas price (new baseline)

Emitters (Historic a) Historic generation

Notes: Historic generation and historic emissions = 1999. Recent generation is based on two years previous to allocation. Incremental generation includes generation beyond 1999 levels. Demand conservation distributes allowance (revenue) for reductions from baseline. Constrained transmission assumes inter-regional capability in northeast reduced by 10%.

Higher gas price has national (Henry Hub) prices pegged 15% above baseline and supply price sensitivity for imports into the northeast above baseline levels doubled.

RGGI Surplus Comparison

-2.50

-2.00

-1.50

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

Dn

Nig

Dn

3ig

Dem

it

Dag

ig

Dag

Hee

Ha

g

He

g

MA

20

Da

gig

MA

Hee

MA

He

g

MA

He

g_

coa

l

MA

Da

gig

MA

De

g_co

al

Auctio

nBil

lio

n 1

999

$

CS

PS

CO2 Rev

TS

Updating Historic Mixed Auction

Scenarios defined in Table 1 of paper.

Change in Asset Value

Scenarios defined in Table 1 of paper.

Change in Asset Value Compared to Baseline

-300

-250

-200

-150

-100

-50

0

50

100

150

200

De

mit

Da

g

Da

gig

Dn

3ig

Dn

Nig

Au

ction

MA

20

Da

gig

MA

Da

gig

MA

De

g_

coa

l

MA

He

e

MA

He

g

MA

He

g_

coa

l

Ha

g

He

g

He

e$

pe

r k

W

NuclearGasCoalAll

Updating HistoricMixed Auction

Limitations in Bookend Analysis

Electricity imports from Canada do not change. Out-of-merit-order dispatch due to long-term fuel

contracts is captured only approximately. We do not capture long-term contracts for nuclear.

Intra-regional transmission constraints are captured only partly.

We examine higher natural gas prices, renewable policies, imports from Canada and transmission constraints in sensitivity analysis.