Embed Size (px)

Citation preview

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 1/40

Critical Success Factors

Stakeholders

Top Management

Vision

Strategy

Mission

Middle Management

First-Line Management

Planning Organizing

DirectingControlling

Economic

Social

Technological

Political

Marketing

Finance

HumanResources

Operations

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 2/40

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 3/40

A lternate Types of Investments

Bonds: Definition A bond is a promise by the issuer or

borrower (government or corporation) torepay an investor (the lender) a set dollar amount (the principal), at a set date (thedate of final maturity), and to pay theinvestor a fixed rate of interest (the couponrate) each year

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 4/40

Characteristics of A ll Bonds

Face Value ± Most bonds are initially sold at a face value

(par value) of $1,000 per bondLength of Life/Date of Final Maturity ± Most bonds have a relatively long life from the

time they are initially sold (issued) until thetime that they mature (date of final maturity)

± This is referred to as the bond¶s ³run tomaturity´ or ³life expectancy´ and is normally20 years

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 5/40

± However, some bonds may have a longer run

to maturity (for example 30 years) or a shorter run to maturity (10 or 15 years) ± For the sake of simplicity, we will always

assume that a bond will have a life

expectancy (or run to maturity) of 20 years

Date of Final Maturity ± A t the end of it¶s life, a bond is said to

³mature´ and the issuer will repay the principal($1,000) to the holder of the bond

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 6/40

Coupon Rate ± Each year the owner of a bond will receive a

fixed rate of interest from the issuer of thebond

± The amount of interest received annually is

determined by the following formula

A nnual Interest = Coupon Rate X Face or Par Value ($1,000)

± A n investor will never receive anything morethan this amount of interest, but will alsonever receive anything less than this amount

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 7/40

± If the issuer of a bond fails to pay the required

amount of interest to the investor, it isconsidered to be an act of bankruptcy ± The bondholders can then take action to force

the company to liquidate its assets and use

the proceeds to pay their outstanding claims(all interest owed plus full repayment of theprincipal loaned)

± How Is This A ccomplished?The Bond Indenture (Contract)The Bond TrusteeThe Order of Liquidation

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 8/40

Order of Liquidation( A ccording to Canadian Bankruptcy Law)

Secured Creditors (Banks, Bondholders)Preferred Creditors (Government)

Unsecured Creditors (Suppliers,Employees, Debenture Holders)Preferred Stockholders

Common Stockholders

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 9/40

In view of the foregoing, Bonds are usuallyvery safe investmentsIf the issuer defaults on the terms of thebond indenture, the trustee can force the

company to sell the assets pledged assecurity for the loan (as outlined in theindenture) and then use the proceeds topay the bondholder¶s claimsThe types of security pledged as collateralgive rise to different types of bonds

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 10/40

Different Types of Bonds

Type of Bond Type of Collateral

Mortgage Bonds Real Property (land, buildings)

Collateral Trust Bonds Stocks and Bonds (Securities)

Equipment Trust Bonds Machinery and Equipment

Debentures No Collateral. Bondholders areunsecured creditors

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 11/40

Reading Bond Quotations

in the Financial PressIssuer Coupon Maturity Bid

Canada 5.50 Jun1/09 106.48*

Bell 6.55 May1/29 99.42*

* A ctual Selling Price = Bid Price x 10

Government of Canada 5.5 of ¶09 = $1,064.80Bell Canada 6.55 of ¶29 = $994.20

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 12/40

The Rough Bond Yield FormulaThe rough bond yield formula assumes that the Investor

holds the bond until the date of final maturity

= A nnual Interest + A nnual Capital Gain X 100%Purchase Price of Bond

= (Coupon Rate X Par Value) + (Par Value ± P. Price)

# years to MaturityPurchase Price of Bond

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 13/40

Example #1:

Calculate the yield on a GM 10 of Oct. 1 ¶18 purchasedfor $900 on October 1, 2008?

Yield = A nnual Interest/Bond + A nnual Capital Gain (Loss)Purchase Price/Bond

= (10% X $1,000) + $1,000 - $90010 years

$900= $110 = 12.22%

$900

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 14/40

Example 2:

Calculate the yield on a GM 10 of Oct 1 ¶18 purchasedfor $1,100 on October 1, 2008?

Yield = A nnual Interest/Bond + A nnual Capital Gain (Loss)Purchase Price/Bond

= (10% X $1,000) + $1,000 - $1,10010 years

$1,100= $ 90 = 8.18 %

$1,100

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 15/40

Summary: Bond YieldsIf a Bond sells at a discount (less than $1,000)

The Yield is greater than the Coupon Rate

If a Bond sells at a premium (greater than $1,000)

The Yield is less than the Coupon Rate

If a Bond sells at Par or Face Value ($1,000)

The Yield is equal to the Coupon Rate

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 16/40

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 17/40

A nnouncements

New Venture Concept Statements are duethis Friday, October 10 at 12:00 Noon indrop boxes outside T A Office P1002Hard copy turned in to drop boxes by12:00 Noon«no exceptionsElectronic copy to Turnitin.com by 12:00

Midnight«no exceptionsTurnitin Instructions posted on CourseWebsite under ³ A ssignments´ Folder

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 18/40

Why Do Bond Prices Vary

Inversely With Interest Rates?Once a bond has been sold, the coupon rate onthat bond is fixed for the entire life of the bondIf new bonds of similar risk are sold bearing a

higher coupon rate (due to the fact that interestrates have risen in the economy)Then rational investors will prefer to purchasethese new bonds (with higher coupon rates)

rather than the old bonds (with lower couponrates) in order to obtain the higher rates of interest

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 19/40

Why Do Bond Prices Vary

Inversely With Interest Rates?Rational investors will only be willing toown the old (lower coupon rate) bond if that bond¶s yield is equal to that of thenew bondsThe only way for this to happen is if theprice of the old bond falls (sells at adiscount )Summary: Interest rates have gone up

and bond prices have fallen

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 20/40

The Rough Bond Yield FormulaThe rough bond yield formula assumes that the Investor

holds the bond until the date of final maturity

= A nnual Interest + A nnual Capital Gain X 100%Purchase Price of Bond

= (Coupon Rate X Par Value) + (Par Value ± P. Price)

# years to MaturityPurchase Price of Bond

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 21/40

Determining Bond PricesExample: What would you pay for aBell 8 of Oct 1 2018, if similar risk bondsissued today have coupon rates of

10%?1998 2008 2018

Bell 8 of Oct 1 2018issued at par = $80/yr

New bond sells at 10% coupon = $100/yr Will you pay $1,000 for Bell 8 of µ18?

pay what will what will yield the sameas the new bonds or 10%will pay less than $1,000

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 22/40

Sample Examination Problem #1: Interest RatesRise in the Economy

How much would a rational investor pay for aBell Canada 8 of Oct 1 ¶18 if bonds of similar riskwere issued today at a coupon rate of 10%?

Solution:The investor is indifferent as to whether he or sheowns the Bell 8 of ¶18 or the new bond with a couponrate of 10% when the yields on the two bonds areequalYield on Bell 10 of ¶28 = Yield on Bell 8 of µ18

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 23/40

Therefore, let the purchase price that a rationalinvestor will pay today for a Bell 8 of ¶18 be X

10% = (8% X $1,000) + ($1,000 ± X)10 years

X

.1X = $80 + ($1,000 ± X)10 yrs

X = $800 + $1,000 ± X2X = $1,800X = $ 900

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 24/40

Summary:Interest rates in the economy have risenfrom 8% (when the Bell 8 of ¶18 was firstIssued in 1998) to their current level of 10%(the coupon rate on the newly issued bonds)

The effect on the market price of a Bell 8 of ¶18 isan decrease from $1,000 in 1998 to a price of

$900 on October 1, 2008.

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 25/40

Why Do Bond Prices VaryInversely With Interest Rates?

Once a bond has been sold, the coupon rate onthat bond is fixed for the entire life of the bondIf new bonds of similar risk are sold bearing a

lower coupon rate (due to the fact that interestrates have fallen in the economy)Then rational investors will prefer to purchasethe old bonds (with higher coupon rates) rather than the new bonds (with lower coupon rates) inorder to obtain the higher rates of interest

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 26/40

Why Do Bond Prices VaryInversely With Interest Rates?

Rational investors will only be willing toown the new (lower coupon rate) bond if that bond¶s yield is equal to that of the old bondsThe only way for this to happen is if theprice of the old bond rises (sells at a

premium )

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 27/40

Investors will bid up the price of the old

bond until its yield is equal to that of thenew bond

Summary: Interest rates have gone downand bond prices have risen

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 28/40

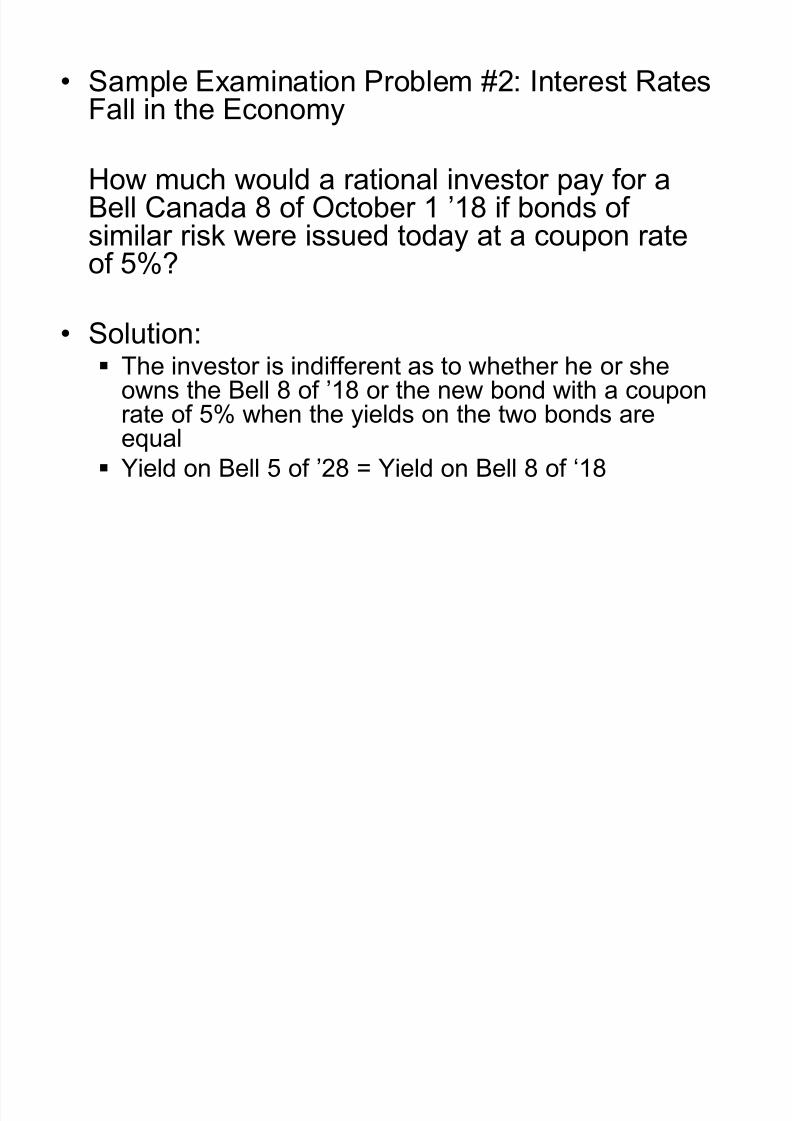

Sample Examination Problem #2: Interest RatesFall in the Economy

How much would a rational investor pay for aBell Canada 8 of October 1 ¶18 if bonds of similar risk were issued today at a coupon rateof 5%?

Solution:The investor is indifferent as to whether he or sheowns the Bell 8 of ¶18 or the new bond with a couponrate of 5% when the yields on the two bonds areequalYield on Bell 5 of ¶28 = Yield on Bell 8 of µ18

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 29/40

Therefore, let the purchase price that arational investor will pay today for a Bell 8 of ¶18 be X

5% = (8% X $1,000) + ($1,000 ± X)10 years

X

.05X = $80 + ($1,000 ± X)10 yrs

.5X = $800 + $1,000 ± X1.5X = $1,800

X = $1,200

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 30/40

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 31/40

Other Features Possessed ByS ome Bonds

The Call or Redemption Feature (Callableor Redeemable Bonds) ± A llows the issuer to repurchase the bond for a

predetermined fixed price at the issuer¶sdiscretion prior to the date of final maturity

± This fixed price is determined by the Call

Schedule printed on the Bond certificate

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 32/40

Why is a call feature attached to a bond?A llows the issuer the flexibility to buy backthe outstanding bonds if interest rates fallsubstantially in the future

Disadvantageous to the investor«why?Callables usually pay a higher couponthan non-callables

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 33/40

The Conversion Feature (ConvertibleBonds) ± A llows the investor the right to convert the

bond into a prescribed number of commonshares in the same company

± May allow the investor to realize a capital gainat some time in the future if the firm¶s commonstock appreciates substantially in value

± Favourable to the investor ± Convertibles often sell at lower coupon rates

than non-convertibles

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 34/40

Extendible/Retractable Feature ± A llows the investor the option to extend the

life of the bond beyond it¶s maturity date(extendible) or have the bond refunded beforeits date of final maturity (retractable)

± Favourable to the investor ± Can see which way interest rates have moved(and are likely to move) and make thedecision to extend (if interest rates have fallen

below the coupon rate of the bond) or toretract (if interest rates have risen above thecoupon rate of the bond)

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 35/40

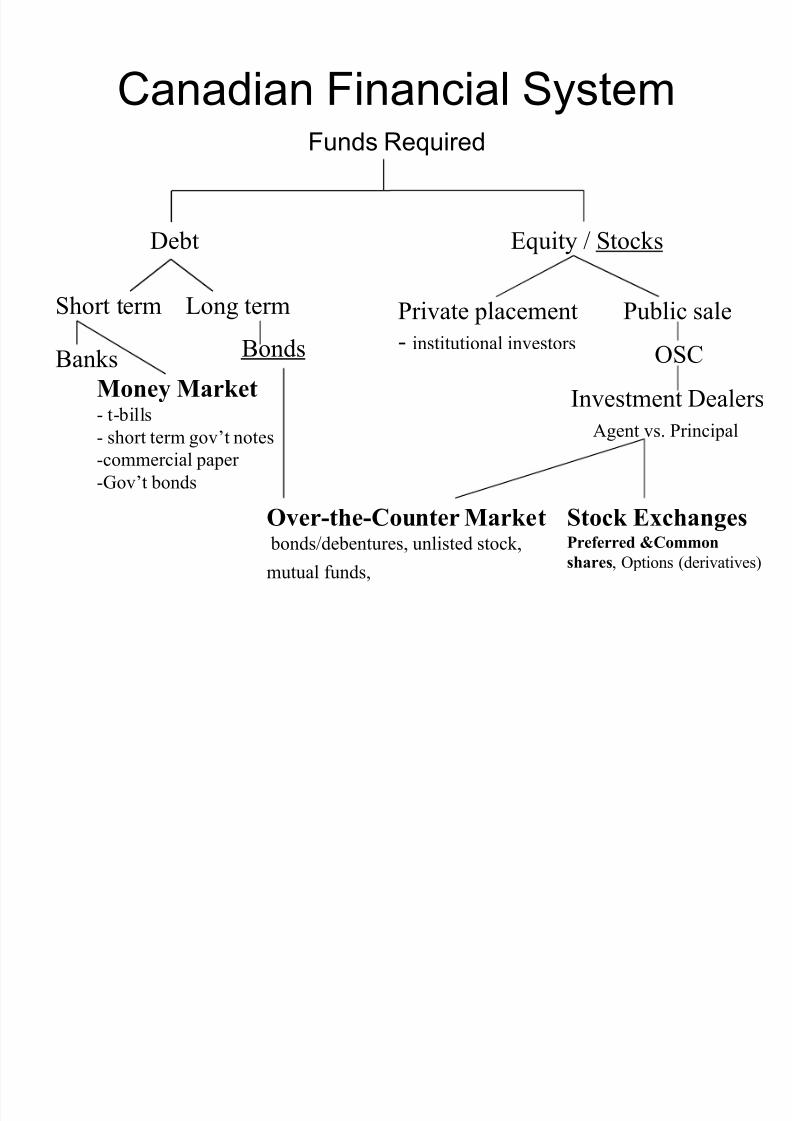

Canadian Financial SystemFunds Required

Debt Equity / Stocks

Money Market- t-bills- short term gov¶t notes-commercial paper -Gov¶t bonds

Banks

Private placement- institutional investors

Public sale

OSC

Over-the-Counter Market bonds/debentures, unlisted stock,

mutual funds,

Stock ExchangesPreferred &Commonshares , Options (derivatives)

Investment DealersAgent vs. Principal

Short term Long term

Bonds

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 36/40

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 37/40

Characteristics of Preferred Shares

The characteristics of preferred shares willbe discussed in lectures on thewhiteboards.No power point slides will be posted onthis topic, with the exception of thefollowing example of a participating feature

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 38/40

Participating Preferred Example

Ex ample:- $1,000,000 net profit- 50% dividend rate

- 50,000 shares of 10% cumulative participatingpreferreds with $10 par value- dividends in arrears 1 yr.- participation commences when common dividends

reach $3/share- 100,000 shares common stock

What is the amount of dividends per share for bothcommon and preferred?

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 39/40

8/8/2019 Alternate Types of Investments Bonds 2009

http://slidepdf.com/reader/full/alternate-types-of-investments-bonds-2009 40/40

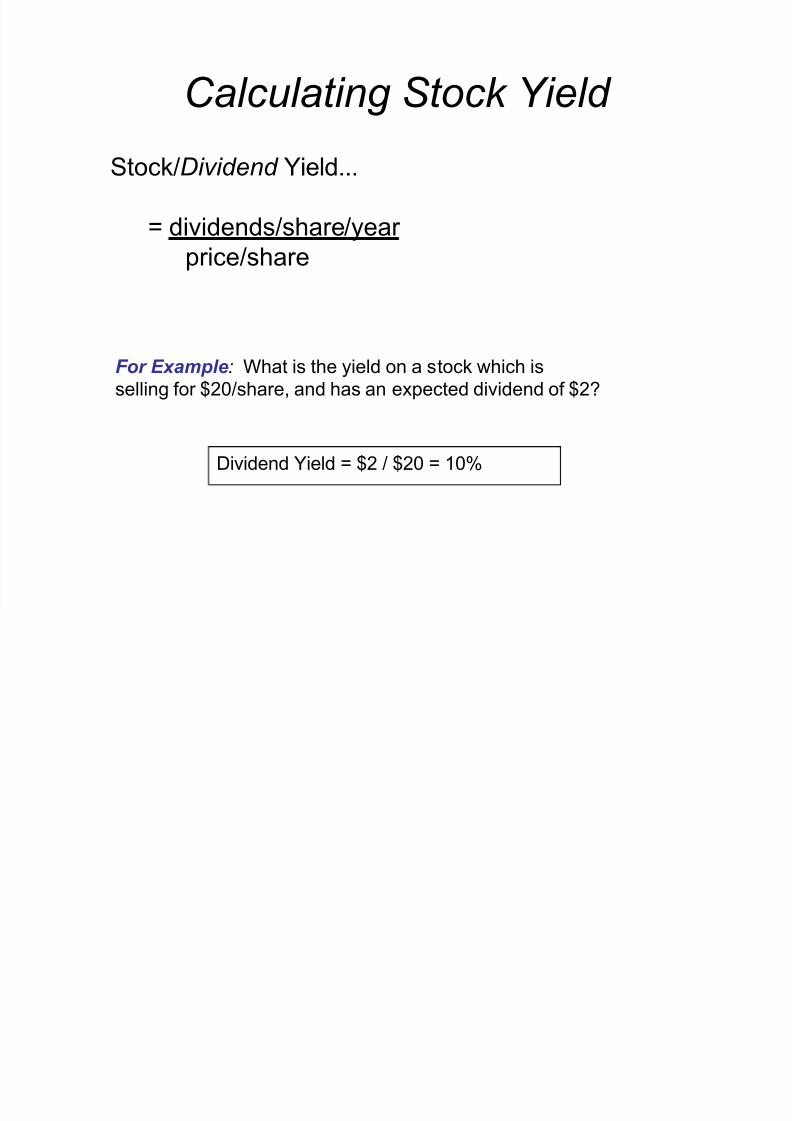

C alculating Stock Yield

Stock/ Dividend Yield...

= dividends/share/year price/share

F or Ex ample : What is the yield on a stock which isselling for $20/share, and has an expected dividend of $2?

Dividend Yield = $2 / $20 = 10%