Embed Size (px)

Citation preview

Alternative financing structures for the aviation industryGregory ManPartner and Head of Debt Capital Markets (Middle East)Norton Rose Fulbright (Middle East) LLP

October 4, 2016

Agenda• Introduction• Islamic Finance in perspective• What is Islamic Finance?• Introduction to Sukuk• Emirates ECA backed Sukuk• Future innovations

20

21

Muslim Demographics

Islamic Finance in perspective

22

• Estimates of the current size of the Islamic Finance market range from [US]$1.66 trillion to [US]$2.1 trillion with expectations of market size to be [US]$3.4 trillion by end of 2018

• One of the fastest growing segment of the financial industry• Despite rapid growth, global Islamic finance market only represents around 1% of

worldwide financial services industry• 1.6 billion Muslims (23% of the world’s population)• In 2015 it was reiterated that the world’s Muslim population will grow twice as fast as non-

Muslim over the next three decades• Popularity in non-Muslim jurisdictions• Islamic finance is a credible alternative to conventional finance• Regulations changing globally to accommodate

What is Islamic Finance?

23

• As practised today, Islamic finance involves the application of Shari’a principles to financial activity of Muslims in the modern world

• Traditional techniques and structures available for centuries, evolved and refined, within parameters of Islamic jurisprudence, to accommodate modern financial institutions and modern banking

• Applicable to range of financial products• Ethical form of financing that aims to create business activities that generate a fair and

equitable profit from transactions that are backed by real assets• Often try to achieve similar commercial outcome to conventional financing• Requires an understanding of the Shari’a

What is the Shariah?

24

Shariah is the religious law of Islam. It has two principal sources:• The Qur’an - the sacred book that records the word of God as revealed to the Prophet

Muhammad (PBUH)“Oh you who believe! Fear Allah (God) and give up what remains of your demand for usury, if you are indeed believers. If you do not, take notice of war from Allah and His Apostle: but if you turn back, you shall have your capital sums: deal not unjustly, and you shall not be dealt with unjustly” (Qur’an 278-279)

• The Hadith - the body of documents that records the Sunnah (the practice or “life-example”) of the Prophet Muhammad (PBUH)

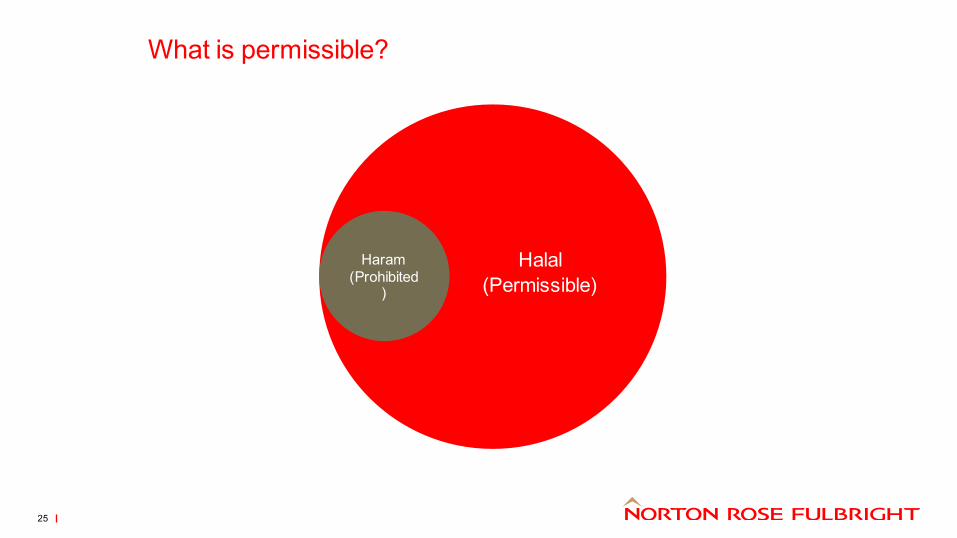

What is permissible?

25

Haram (Prohibited

)

Halal(Permissible)

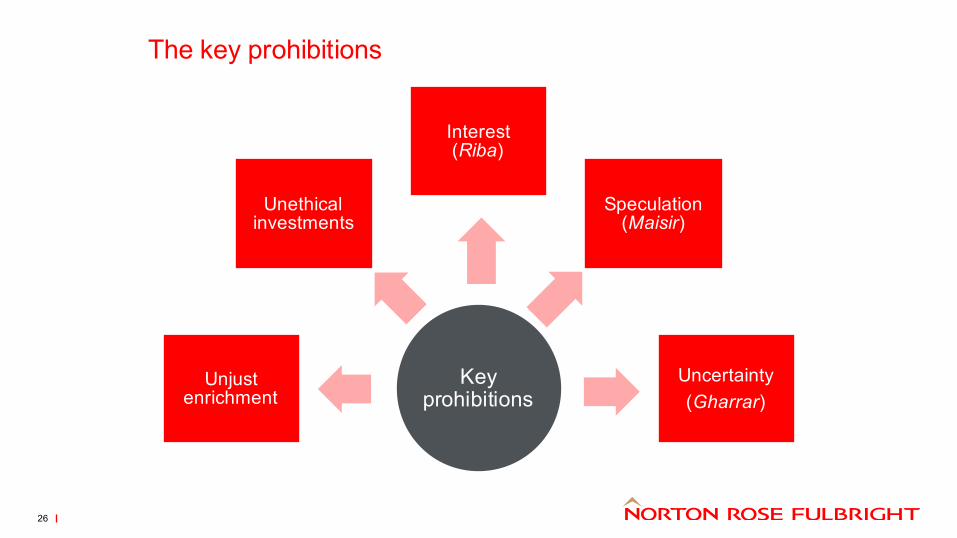

The key prohibitions

26

Key prohibitions

Unjust enrichment

Unethical investments

Interest (Riba)

Speculation (Maisir)

Uncertainty(Gharrar)

The concept of riba

27

• Probably the best known and biggest practical difference from conventional finance• Underlying concept stems from the nature of money in Islam

– Money has no intrinsic value and is simply a means of facilitating trade– Money is not a commodity– Money can only be exchanged for the same at par value

• There should be no charge for the use of money• Financial activities that are approved in Islam:

– Trading and enterprise - the prohibition of riba does not preclude obtaining a rate of return on an investment or profit from a commercial venture

– Taking security (including guarantees) – if it guards against negligence, willful wrongdoing or breach of contract of customers/partners

• Islamic finance is sometimes said to be “asset based” as the trading of assets is often used to create obligations (where money is just the payment mechanism)

The basic difference*

28

Bank Client

Conventional

Islamic

Bank Client

money

money

money + money (interest)

Goods and Services

*Courtesy of Sheikh Nizam Yaquby

Common Islamic financing structures

29

The typical Islamic Financing structures• Goods Murabaha (cost-plus financing)• Tawarruq / Commodity Murabaha (murabaha financing through the use of a commodity)• Ijara /Ijara-wa Iqtina (leasing / leasing with a promise to sell)• Mudaraba (participation financing)• Musharaka (partnership / equity financing)• Wakala (agency)• Istisna’a (variation of murabaha that permits goods to be financed while under

construction or manufacture)• Sukuk (Islamic bonds)

What is a Sukuk?

30

• Capital markets instrument sometimes called an Islamic “bond”• Trust certificate which represents an undivided beneficial ownership interest in an

underlying asset/venture• To the extent that underlying assets generate a profit, profit can be distributed to

certificate holders• Returns based on profits from assuming risk related to ownership• Profit payments can therefore not be guaranteed• Requirement for “tangibility” in order for Sukuk to be tradeable

Sukuk-al-ijara structure (lease structure) – acquisition finance

31

Investors

Issuance Proceeds

SukukPrincipal & Profit

Airline Aircraft manufacturerAssignment Agreement

Service Agency Agreement

Purchase Price

Title

SPV/Issuer/Lessor“owner”

Airline/Lessee

Rental Payments

Lease Agreement

Sale Undertaking

Purchase Undertaking

Sukuk-al-manafa’a (usufruct structure) – corporate funding

32

Investors

Issuance ProceedsSukukPrincipal &

Profit

Emirates (as Agent)

Emirates(as Seller)Revenue

Appointment as Service Agent

Sale of Rights to Travel (measured in ATKMs)SPV / Issuer

Third parties

Revenue from Rights to Travel

Sale of Allotted Rights to Travel

(materialised through sale of

tickets

Emirates (as Obligor)

Sale of Outstanding

Rights to Travel

Exercise Price

Purchase Price

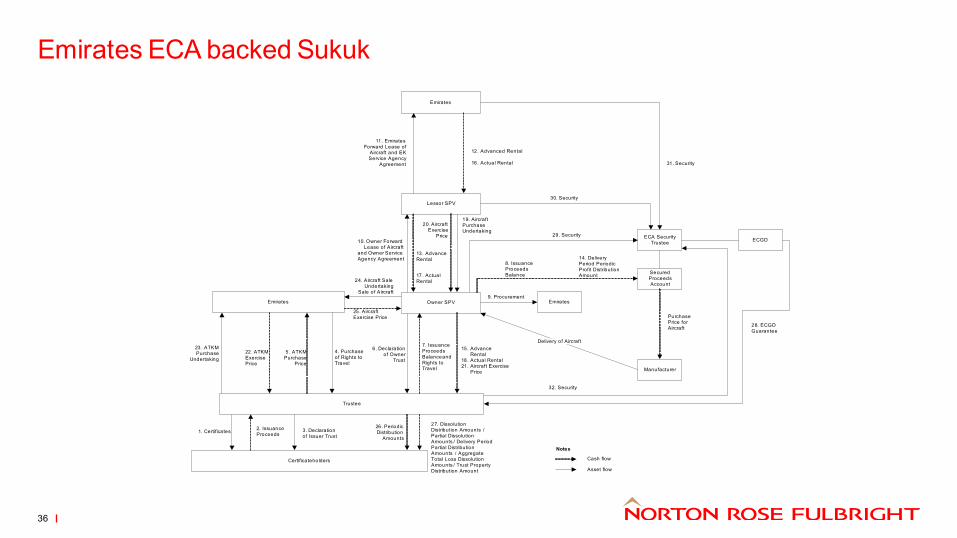

Why did Emirates choose to do an ECA backed Sukuk?

33

• First UK Export Finance backed Sukuk for aircraft financing• Largest ever capital markets offering in the aviation space with an Export Credit Agency

guarantee• First Sukuk to be used to pre-fund the acquisition of aircraft• First ever Sukuk financing for 4 A380 aircraft• Regulation S and Rule 144A offering• Admitted to listing and trading on the London Stock Exchange and on NASDAQ Dubai

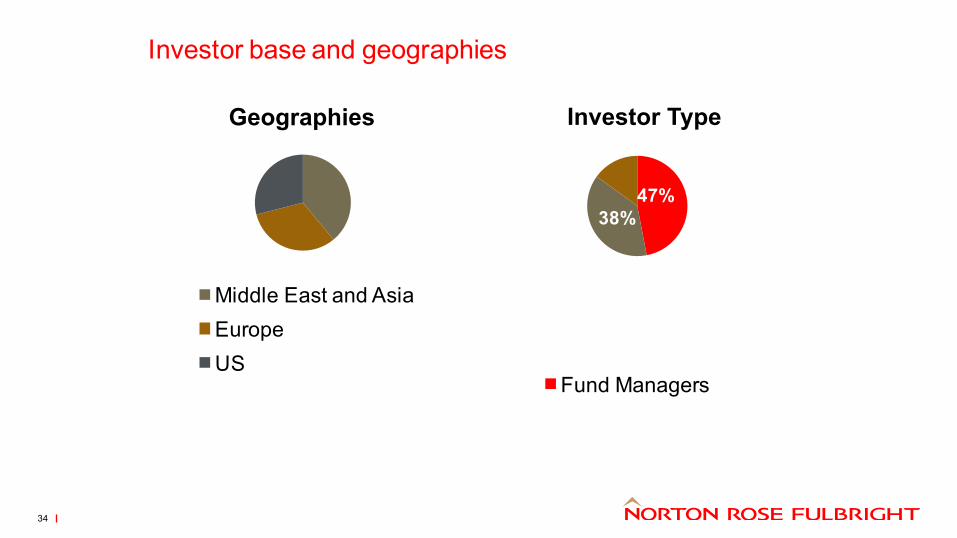

Investor base and geographies

39%

32%

29%

Geographies

Middle East and AsiaEurope US

47%38%

15%Investor Type

Fund Managers

34

0

20

40

60

80

100

120

140

2006 2007 2008 2009 2010 2011 2012 2013 2014

Annual Sukuk issuances

35

Emirates ECA backed Sukuk

36

Emirates

Lessor SPV

ECGD

Secured ProceedsAccount

Emirates Owner SPV Emirates

Manufacturer

Trustee

Certificateholders

12. Advanced Rental

16. Actual Rental

11. EmiratesForward Lease of

Aircraft and EK Service Agency

Agreement

10. Owner Forward Lease of Aircraft

and Owner Service Agency Agreement

20. Aircraft Exercise

Price

13. Advance Rental

17. Actual Rental

19. Aircraft Purchase Undertaking

30. Security

31. Security

29. Security

14. DeliveryPeriod Periodic Profit Distribution Amount

8. Issuance ProceedsBalance

28. ECGDGuarantee

Purchase Price for Aircraft

9. Procurement

15. Advance Rental

18. Actual Rental21. Aircraft Exercise

Price

7. Issuance Proceeds Balance and Rights to Travel

6. Declaration of Owner

Trust

4. Purchase of Rights to Travel

5. ATKM Purchase

Price

22. ATKM Exercise Price

23. ATKM Purchase

Undertaking

25. Aircraft Exercise Price

24. Aircraft Sale Undertaking

Sale of Aircraft

27. Dissolution Distribution Amounts /Partial Dissolution Amounts / Delivery Period Partial Distribution Amounts / Aggregate Total Loss Dissolution Amounts / Trust Property Distribution Amount

3. Declaration of Issuer Trust

2. Issuance Proceeds1. Certificates

26. Periodic Distribution

Amounts

Notes

ECA Security Trustee

Cash flow

Asset flow

Delivery of Aircraft

32. Security

Future innovations

37

• Islamic EETCs– some structural challenges

• Tax leasing structures– already utilise capital market products– could be adapted for Sukuk

International

Latin AmericaBogotáCaracasRio de Janeiro

* associate office** alliance

AfricaBujumbura**Cape TownCasablancaDar es SalaamDurbanHarare**JohannesburgKampala**

Middle EastAbu DhabiBahrainDubaiRiyadh*

AustraliaBrisbaneMelbournePerthSydney

AsiaBangkokBeijingHong KongJakarta*ShanghaiSingaporeTokyo

Central AsiaAlmaty

EuropeAmsterdamAthensBrusselsFrankfurtHamburgLondon

MilanMoscowMunichParisPiraeusWarsaw

CanadaCalgaryMontréalOttawa

QuébecToronto

USAAustinDallasDenverHoustonLos AngelesMinneapolisNew YorkPittsburgh-

SouthpointeSan AntonioSt LouisWashington DC

38

Contact details

39

Gregory ManPartner, Head of debt capital markets (Middle East)Norton Rose Fulbright (Middle East) LLPTel +971 4 369 [email protected]

DisclaimerNorton Rose Fulbright US LLP, Norton Rose Fulbright LLP, Norton Rose Fulbright Australia, Norton Rose Fulbright Canada LLP and Norton Rose Fulbright South Africa Inc are separate legal entities and all of them are members of Norton Rose Fulbright Verein, a Swiss verein. Norton Rose Fulbright Verein helps coordinate the activities of the members but does not itself provide legal services to clients.References to ‘Norton Rose Fulbright’, ‘the law firm’ and ‘legal practice’ are to one or more of the Norton Rose Fulbright members or to one of their respective affiliates (together ‘Norton Rose Fulbright entity/entities’). No individual who is a member, partner, shareholder, director, employee or consultant of, in or to any Norton Rose Fulbright entity (whether or not such individual is described as a ‘partner’) accepts or assumes responsibility, or has any liability, to any person in respect of this communication. Any reference to a partner or director is to a member, employee or consultant with equivalent standing and qualifications of the relevant Norton Rose Fulbright entity.The purpose of this communication is to provide general information of a legal nature. It does not contain a full analysis of the law nor does it constitute an opinion of any Norton Rose Fulbright entity on the points of law discussed. You must take specific legal advice on any particular matter which concerns you. If you require any advice or further information, please speak to your usual contact at Norton Rose Fulbright.

41