Embed Size (px)

Citation preview

Alternative Risk ApproachesPresented by

David Kalainoff, Vice PresidentTransatlantic Reinsurance Company

Seamus Tivnan, Senior Vice PresidentMarsh Management Services (Cayman), Ltd.

Philip Reischman, Executive Vice PresidentGallagher Healthcare Insurance Services

Medical Professional Liability SymposiumMarch 21 – 22, 2002

Chicago, IL

Alternative Risk DefinedAlternative Risk Defined

Alternative (adj.):offering a choice of two or

more things; offering a second thing or proposition

1

Risk (n.):the chance of loss; the degree of probability of loss

Source: Webster’s Third World International Dictionary (unabridged)

Alternative Risk DefinedAlternative Risk Defined

Alternative Risk (n.):the option for an Insured to pay a

lot of premium for limited coverage under a Contract of Insurance or Reinsurance that no one understands, but for which the Broker receives a stout commission!

Source: The Cynical Brokers’ Dictionary2

Characteristics of Alternative Risk ProgramsCharacteristics of Alternative Risk Programs

Loss Sensitive

Finite (Aggregate) Limit

Significant Rate On Line

Investment Income Recognition

Prospective Or Retrospective

3

Re-Emergence Of Alternative Risk ProgramsRe-Emergence Of Alternative Risk Programs

Massive Premium Increases

Retention Increases

Desire For Frequency Protection

Desire For Long-Term Stability

4

Escalating migration of premium into ART market (1997-2002)

0

10

20

30

40

50

60

70

80

90

1997* 1998* 1999* 2000* 2001* 2002*

% o

f mar

ket

-5

0

5

10

15

20

25

30

35

40

Ann

ual p

rem

ium

gro

wth

US Commercial Market Global Alternative Market

US Commercial Market Annual Premium Growth Global Alternative Market Annual Premium Growth

Business Moves To ARTBusiness Moves To ART

5

Types Of Alternative Risk VehiclesTypes Of Alternative Risk Vehicles

Direct Insurance

Captive Vehicles

Risk Retention Groups

Reinsurance

Capital Market Structures

6

A good forecaster is not smarter than everyone else…he merely has his ignorance

better organized

7

Deep ThoughtsDeep Thoughts

A Captptive………..………..

Take Prisoner

Keep On Confinement Or Under Restraint

Unable To Escape

Source: Oxford English Reference Dictionary - 2nd Edition

8

What Is A Captive………..What Is A Captive………..

Licensed Insurance Company

Formed To Insure Or Reinsure The Risk Of Its Owners Or Unrelated Parties Of Their Choosing

Regulated Under Special Legislation

Located Offshore Or Onshore

Admitted Only In Its Domicile And Non-Admitted In All Other Jurisdictions

9

Captive VehiclesCaptive Vehicles

Single Parent

Group / Association

Rent-a-Captive / Cell Type

10

Captive Vehicles - Single ParentCaptive Vehicles - Single Parent

A Licensed Insurance Company Primarily Designed To Insure The Risks Of The Parent

Generally One Shareholder And ‘One’ Insured

Migrated To Multiple Insured

11

Captive Vehicles - Group / AssociationCaptive Vehicles - Group / Association

Stock Or Mutual Or ‘Single Parent’

Homogeneous Or Heterogeneous

Multi Line

Fully Pooled, Layering Of Losses And Sharing By Participants Within Layers

Aggregate Limits, Securitization Of Gaps

12

Captive Vehicles – Rent-a-Captive / Cell TypeCaptive Vehicles – Rent-a-Captive / Cell Type

R-a-C - ‘Pooled’ Resources, But Separate Fully Collateralized Programs

Access To ART Market Without The Capital Outlay, Administration

Segregated Portfolio / Protected Cell

‘Legalized’ R-a-C

Tax Deductibility Issues• Pooling / Sharing Within Cells

Biggest Concern - New Untested Legislation13

IRS Tax Deductibility TestIRS Tax Deductibility Test

Existence Of Risk Transfer

Presence Of Risk Distribution

Case Law Matching

Unrelated Premium Or ‘Single Parent’

14

Captive Vehicles - Why?Captive Vehicles - Why?

Traditional• Cash Flow, Reduced Costs, Direct

Reinsurance Placement

Recent• No Option - Cannot Afford Or Cannot

Find

Control Own Destiny

15

Captive Vehicles - How?Captive Vehicles - How?

Feasibility• 3 - 6 Months, c. $25k

Implementation• 1 - 3 Months, From $15k

Capitalization• From $120k

Administration• From $75k

16

A novice uses statistics like a drunkard uses a lamppost…for

support, not illumination

17

Deep ThoughtsDeep Thoughts

Captive Vehicles - Where?Captive Vehicles - Where?

Basically Anywhere

Onshore• Vermont• Hawaii

Offshore• Bermuda

Cayman• 550, 47 New In 2001, 70 Plus In 2002?

18

Captive Domiciles - What to Look For?Captive Domiciles - What to Look For?

Accessibility

Flexibility

Stability

Infrastructure• Physical• Professional• Legislative

19

Go Off-Shore - “Less Regulation”Go Off-Shore - “Less Regulation”

Cayman Islands• Removed From FATF Blacklist• IMF Visit• Tax Treaty• Regulator

– Autonomous– Enforcement Powers– On Site Inspections

Know Your Customer

20

Healthcare Captive Vehicles - Where?Healthcare Captive Vehicles - Where?

Cayman Islands

Healthcare Captive Capital

Harvard Group Started And All Followed

180 Healthcare Related Captives

One In Three Of The Market

$800m In Premium

$4B In Assets21

Risk Retention GroupsRisk Retention Groups

All Insureds Are Members (Owners)

Single State Domicile

Registration In 49 States

Can Eliminate Need For Fronting

Subject To NAIC Reporting Requirements

Higher Capitalization Requirements

22

Alternative Risk Finance Captive OptionAlternative Risk Finance Captive Option

Advantages• Long-Term Solution• Generate Investment

Income• Benefit From

Experience• Tax Advantages• Access Reinsurance• Control Of Destiny• Executive Focus

Disadvantages• Assumption Of Risk• Costs To Form And

Operate• Internal Costs• Restricted Capital• Fronting Challenges

23

Captive OptionCaptive OptionRole of Primary CarrierRole of Primary Carrier

Fronting Vehicle

Claims Management

Underwriting / Actuarial Report

Excess Of Loss Or Quota Share

24

Captive OptionCaptive OptionRole Of ReinsurersRole Of Reinsurers

Underwriting and Actuarial Support

Excess Of Loss And Quota Share

Loss Portfolio Transfers

Capacity Support

25

Facts are stubborn, but statistics are more pliable

26

Deep ThoughtsDeep Thoughts

Goal: Achieve Efficient Frontier Of Risk Retention / Risk Transfer For Mutual Benefit Of Buyers And Underwriters

Excess Alternative Risk StructuresExcess Alternative Risk Structures

Types Of Structures

Annual Aggregate Deductibles (AAD) Buffer Layers Commutation Options Co-Insurance Swing Rating Plans No Insurance

27

Example:Current Retention = $5 Million Each And EveryRenewal Retention = $10 Million Each And Every

Annual Aggregate DeductibleAnnual Aggregate Deductible

28

Comments: Insured Has Protection For Frequency Of Severe

Losses Insurer / Reinsurer Gets Larger Risk Margin Works Better On Excess Layer

AAD Approach:Renewal Retention = $5 MillionAnnual Aggregate Deductible = $5 To $10 Million

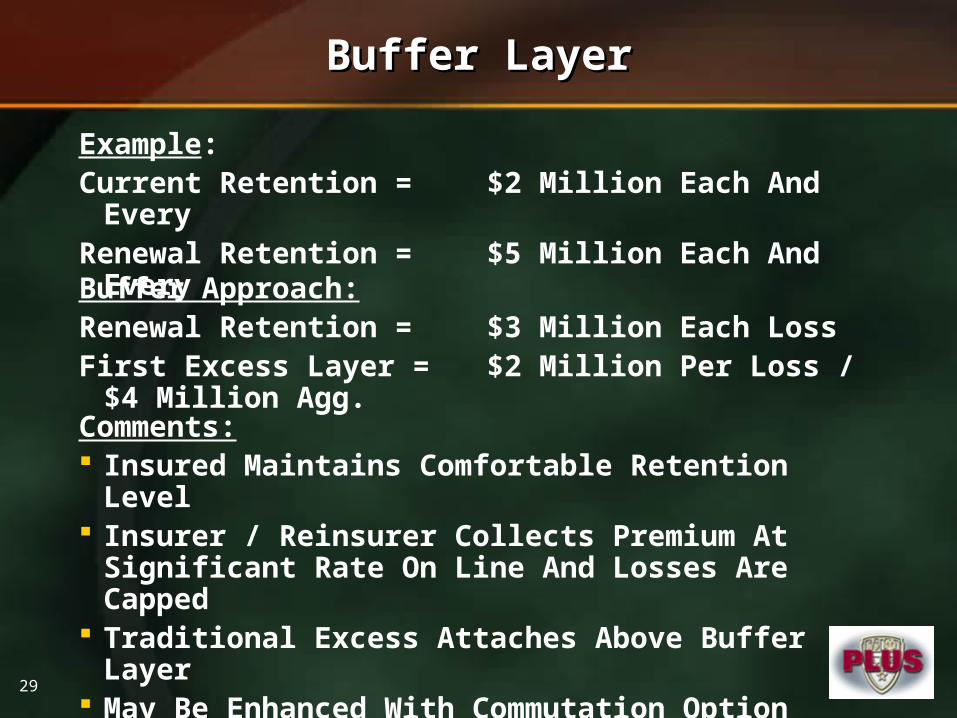

Example:Current Retention = $2 Million Each And EveryRenewal Retention = $5 Million Each And Every

Buffer LayerBuffer Layer

29

Buffer Approach:Renewal Retention = $3 Million Each LossFirst Excess Layer = $2 Million Per Loss / $4 Million

Agg.Comments: Insured Maintains Comfortable Retention Level Insurer / Reinsurer Collects Premium At Significant Rate

On Line And Losses Are Capped Traditional Excess Attaches Above Buffer Layer May Be Enhanced With Commutation Option

Example:Insured Has Option To Commute Coverage And Assume The Previous Insured / Reinsured Risk Retrospectively

Commutation OptionsCommutation Options

30

Formula:Gross Written Premium

– Expense Component– Risk Margin+ Accumulated Investment Income= Experience Account

Commute At:24 Mos. Post Expiration = 100% Of Experience Account36 Mos. Post Expiration = 75% of Experience Account48 Mos. Post Expiration = 50% of Experience AccountAfter 48 Mos. = Option Lost

Comments: Works Better On Working Layers Or On First

Excess Layers

Insured Has Retrospective Look At Losses Before Assuming Higher Retention

Contract Documentation Is Critical

Insured Solvency Is Important

Initial Premium Is Higher Than Similar Deal Without Commutation

Commutation OptionsCommutation Options

31

Like dreams, statistics are a form of wish

fulfillment

32

Deep ThoughtsDeep Thoughts

Other ApproachesOther Approaches

Swing Rates

Co-Insurance

Indexing

33

Comments: Designed To Protect Underwriter, But Give

Benefit Of Favorable Experience To Insureds Work Best In Working Layers All Are Re-emerging As Rates Increase

The “No Insurance” OptionThe “No Insurance” Option

Formal Self Insurance Vehicle• Captive• Trust

Prudent Funding Level• Actuarially Developed• Limits Consistent With Balance Sheet

And Industry

Modified Negotiation Postures• No Insurance• Community Support

34

The statistics on sanity are that one out of every four Americans is

suffering from some form of mental illness. Think of your

three best friends. If they’re okay, then it’s you.

35

Deep ThoughtsDeep Thoughts

Material Underwriting IssuesMaterial Underwriting Issues

Insured / Reinsured Funding Levels

Claims Management

Loss Control / Risk Management

36

Alternative Risk StructuresAlternative Risk StructuresThe FutureThe Future

Clearly Market Driven And Utilization Will Increase

Preserves Premium (And Hopefully Underwriting Profit) For Commercial Insurers / Reinsurers

Downward Bias In Retention Levels And Risk Margins As Market Softens

37

Statistics are like bikinis…what they reveal is suggestive, but what they conceal is vital.

38

Deep ThoughtsDeep Thoughts

QuestionsAnd

Answers

Alternative Risk ApproachesAlternative Risk Approaches

39