Embed Size (px)

Citation preview

2021ANNUAL REPORTA M A G A S A K I S H I N K I N B A N K

CONTENTS

1 Message from the President

2 Special Message from the President on the Bank’s 100th Anniversary

4 Amagasaki Shinkin Bank and Local Communities

6 At a Glance

7 Financial Section

13 Corporate Data

For the Next 100 YearsValuing our history and ideals,

working hand-in-hand with the local community to achieve growth

Seiji SakudaPresident

Message from the President

Seiji Sakuda, President

We wish to express our great appreciation and sincere thanks to our customers for their continued patronage.

Thanks to everyone in the Bank’s orbit, we celebrated our 100th anniversary on June 6, 2021. Founded in the industrial city of Amagasaki between Osaka and Kobe in 1921, the Bank’s basic management principle has long been to contribute to the local community, prioritizing business activities aimed at stimulating the local economy and achieving sustained progress. Over the course of a full century, the Bank has maintained steady, healthy operations, overcome countless difficulties, and developed into a leading Japanese shinkin bank. This success is due entirely to the warm support of our customers over the years, for which we are eternally grateful.

Each year, we prepare this English-language version of our annual report as a means of proactively disclosing information on our activities and further deepening your understanding of Amagasaki Shinkin Bank. We hope you will find it informative and useful.

In fiscal 2020, the second year of the new Reiwa Era in Japan, our net profit from operations (indicating profitability of business operations) totaled ¥5.6 billion, with ordinary income of ¥3.7 billion and a net income of ¥2.4 billion. Our net profit from core operations—which represents our fundamental earning power as a financial institution—was ¥5.6 billion, indicating steadiness in a tough profit environment. The Bank’s capital adequacy ratio, an indicator of management soundness, was 16.37%, which is significantly higher than the Japanese domestic standard of 4% and is exceptionally high relative to the other major shinkin banks.

In October 2020, the Japan Credit Rating Agency, Ltd. (JCR), one of Japan’s leading rating agencies, assigned our Bank a Long-term Issuer Rating of “A” (single A flat). This high rating reflects the high value that our sound and pragmatic management policies inspire.

The ongoing coronavirus situation continues to have a serious impact on the regional economy. As a regional financial institution, one that specializes in working with small and medium-sized enterprises, we are taking step to resolve issues and create new value in response to the needs of our community and customers. Since our founding, we have carried forward a deep-rooted spirit of mutual aid, and based firmly in these principles, we aim to provide support for the community and our customers and help bring about a brighter future for all.

We look forward to your continued support and encouragement as we pursue these initiatives.

July 2021

ANNUAL REPORT 2021 1

Seiji SakudaPresident

Gratitude for Community—Our Path and Outlook

Support for local companies—our founding

and ongoing mission for a full century

We celebrated our 100th anniversary on June 6, 2021, a

significant milestone that would not have been possible

without the support of the Amagasaki community and our

customers for whom I have the deepest gratitude.

Amashin, as the Bank is known colloquially, first

opened its doors in times of depression following the

World War I, in the year 1921. The central figure behind

the Bank’s founding was a man named Matsuo Takaichi,

born in Okayama Prefecture and enlisted early on by his

father to help run his business. After the Panic of 1907

and ensuing depressed market that followed the Russo-

Japanese War, his father’s business was unable to survive

and so Matsuo went to work for a company in Osaka,

while taking up residence in the city of Amagasaki. Many

small and medium-sized enterprises in Amagasaki had

also fallen on hard times, and understanding the pain of

business owners acutely, Matsuo tried to figure out a way

to help them. He sought the advice of an associate in

Osaka, also of Okayama descent, Mr. Nakae. Taking the

model of the credit cooperative at which the president of

Matsuo’s company was a director, the two searched for a

way to establish the cooperative that evolved into our

Bank. Naturally, the two had to build confidence from the

community from scratch. Oral history tells us that upon

launching the credit association, the two appealed to

leading members of the community to lend their weight

to the project. With that cooperation from the local

community, the banking cooperative was established, and

to this day has been carrying out its primary mission of

working for the benefit of local society. That spirit and its

embodiment are built into our DNA and continue to

animate Amashin.

The management of the Bank has been notably

trustworthy since its founding. One foundational

approach to our business is the attitude of working quietly

behind the scenes, something that all employees are

schooled in. Even our head office does not stand out and

was purposely established off a main street. I joined the

Bank in 1985, prior to Japan’s bubble era. As inflated

assets took hold of the economy over the next half decade,

the Bank did not lose its good sense. So when the bubble

finally collapsed and many financial institutions and

companies that had speculated recklessly went under,

Amashin was hardly affected, and this earned the further

trust of people in the community.

Special Messagefrom the President

on the Bank’s100th Anniversary

With gratitude and passion

for this community,

may we have another

100 years.

Support from the community and local region for

100 years.

What has changed and what has remained steady

over time?

While keeping in mind lessons from the past, we

look to guide the Bank toward a bright future.

2 AMAGASAKI SHINKIN BANK

Special Message from the President on the Bank’s 100th Anniversary

Strengthening our consulting activities and

resolving issues to help local communities

We believe that the role of financing small and medium-

sized enterprises is to assist companies and contribute to

the community. Out of that conviction, we have long

pursued two tracks wholeheartedly—providing consulting

services and carrying out activities to benefit the local

community. Our focuses in consulting are: facilitating the

process of starting up a local business; assisting business

owners who struggle with business succession issues; and

protecting local employment. We therefore started

developing expertise and building a record in early-stage

support for startups, business succession, and active

engagement in mergers and acquisitions. We also team up

with outside experts and governmental organizations to

respond to the need for high-level, specialized consulting

in a rapidly evolving business environment. Our ability to

coordinate high-level consulting has led to many successful

cases. This experience has also built up the skills and

preparedness of our employees, expanded our collaborative

network, and bolstered our consulting track capabilities.

We anticipate the fields to cover will only continue to

expand, engendering a concomitant need for specialized

expertise. We therefore plan to widen our range of contacts

to address those growing needs for problem-solving, and

based on the organizational DNA of Amashin, will train

employees to stand by the side of and reliably support our

customers.

Ten years ago, as we celebrated our 90th anniversary,

we launched activities aimed at solving issues faced by the

local community. The Ama-chan and Shin-chan Project

involves efforts made by each branch based on the needs of

their individual communities. Branch employees meet with

community leaders to identify issues and then take action

to resolve them—a process that has led to many clear

successes. The Amashin Green Project is an effort to plant

trees over a period of 10 years to build a forest over 100

years as part of Hyogo Prefecture’s Amagasaki 21st

Century Forest Creation Project. We became the first

“seedling foster company” in the project. After the

planting phase ends, we plan to continue with thinning

efforts and other upkeep to ensure that the coastal

woodland area stays healthy and becomes a relaxing spot

for area residents to enjoy, while also developing ideas for

its beneficial use. As a cooperative financial institution, the

Bank’s very structure and business activities share the same

principles as the UN’s SDGs (sustainable development

goals), and in 2019 we issued the Amashin SDGs

Declaration to clarify and strengthen our efforts in the key

items we are targeting.

Benevolent financing of small and medium-

sized enterprises for the community,

employees and Amashin

We are now ready to embark on another 100 years of

activity in Amagasaki. Even though the future is uncertain

as we prepare to live with COVID-19 long-term, our basic

policy of facing local issues head-on and resolving them

remains a steady focus. I like to think of our stakeholders

in three groups—the local community, our employees, and

Amashin—forming a triangle of mutual benefit. I also feel

that we must maintain each intersection in a healthy way,

using various approaches and angles to constantly build a

strong win–win–win relationship. Valuing our founding

spirit is a key part of that effort, along with keeping the

local community and our customers close to our hearts. So,

I will continue to impress upon all of our employees the

importance of the Bank’s founding spirit in mutual aid as

we carry out activities of which we can be proud. I hope

that we can continue to deepen our relationships to people

in the community and serve as an indispensable institution

that is an integral part of our community and region.

ANNUAL REPORT 2021 3

Amagasaki Shinkin Bank and Local Communities

Amagasaki Shinkin Bank’s Consulting Services

Amagasaki Shinkin Bank shares a common destiny with the small and medium-sized enterprises in the region. Because we are a shinkin bank working in close contact with members of the local community, we are the only institution capable of offering consulting services that consider the development of a business from a common perspective. By sharing information from our daily conversations with customers at our business headquarters, we give careful consideration to the kind of support we can provide and the solutions we can offer.Moreover, we offer voluntary and proactive consulting services in collaboration with specialized external institutions and affiliated companies.

Amagasaki Shinkin Bank aims to be the financial institution its customers choose expressly for our consulting services.

Support for Startup or Business Renewal

Our business startup support financing and Saturday consultations on how to start a business are two examples of the many forms of support we offer. During fiscal 2020, the Bank provided support for a startup or business renewal for 1,546 clients (as of March 31, 2021).Note: Total includes clients financed at less than 5 years from founding; clients

given a startup loan; and clients that attended our startup seminar.

● The Amashin Startup and Growth Support FundThis fund is a joint initiative with Shinkin Capital Co., Ltd. (a limited liability investment project partner) and a first for a shinkin bank. The fund is designed to provide funds

We are now in the final year of our four-year management plan that started in fiscal 2018. Through its implementation, we have maintained a foreground presence in the region. The true value of the Amashin Business Model has become apparent as we work together at every level of the Bank, coordinating efforts toward operational reforms to reach new levels. These initiatives demonstrate the key role we play as the number one financial institution in the area.

Fiscal 2021

100 Years On: Embracing challenges with an eye on the next levelWorking together on operational reforms to continue to evolve

Implement our consulting capabilities

Fresh initiatives in line with demand in an age of “the new normal”

Strengthen activities that contribute to the region

Be proactive in expanding our range of activities to help resolve issues

Amashin Business Model

Generate public valueStrengthen

partnerships

Promote sustainability in society by achieving the SDGsStimulate the local economy and achieve sustainable development

Build promise in the community and create an eco-friendly city

Build a sustainable and steady earnings base

Establish a lasting management structure

【The Local Community】

【Amashin】Materialize our long-term vision

Motivate and give purposePromote personal growth and

good health

【Our Employees】

1. Demonstrating the true value of the Amashin Business Model• Implement our consulting capabilities Fresh initiatives in line with demand in an age of “the new normal”• Strengthen our activities that contribute to the region Be proactive in expanding our range of activities to help resolve issues

2. Achieve our long-term vision and plans• Utilize a forward-looking sales strategy that matches the needs of the

region and customers• Utilize a good personnel strategy and personnel training

3. Build a sustainable, stable revenue base• Reappraise current ideas and carry over heightened earning power Build heightened earning power and a revenue base

4. Establish a lasting management structure• Strengthen the business management system Achieve operational reforms and strengthen our business management• Implement a lasting management strategy Keep an eye on the next level

We aim to generate new value from a customer’s business or growth potential, and are working to expand our system’s capabilities to research and propose viable solutions for a range of management issues that a customer may face.We also proactively engage in financing based on improved capabilities in assessing business feasibility that rely on skill and judgment rather than on merely requiring a security.(As of March 31, 2021: 10,449 business feasibility assessment clients, ¥599.9 billion balance of loans outstanding, 58.7% of all loans/69.1% of the balance)

Consultation aligned with a company’s phase of development

Phases ofdevelopment

1,346 clients¥35 billion

Startup phase

2,113 clients¥107 billion

Growth phase

11,773 clients¥615.1 billion

Stability phase

2,567 clients¥111.1 billion

Transition phase

Business support system by phase of development (17,799 total credit recipients, ¥868.3 billion total balance of loans outstanding)

• Startup phase: Up to 5 years from founding or business renewal • Growth phase: Sales on average in last 2 fiscal terms over 120%

higher than previous 5 fiscal terms• Stability phase: Sales on average in last 2 fiscal terms 80–120%

compared to previous 5 fiscal terms

• Transition phase: Sales on average in last 2 fiscal terms under 80% compared to previous 5 fiscal terms; and period in which loan terms changed or payments were overdue

(Balance of loans outstanding as of March 31, 2021)

Implement Our Consulting Capabilities

4 AMAGASAKI SHINKIN BANK

directly to customers who are starting or who have recently started a new business to provide them with capital or to strengthen their management.Since being established in 2015, the fund has served a total of 15 clients, utilizing ¥443.71 million.

All Members of Management and Staff Are Contributing to the Region as “Corporate Citizens”

Promoting Environmental Preservation Activities

Amashin Green Premium

In 2011, we established the “Amashin Green Premium” award program, which recognizes environmentally outstanding technologies, products, production methods, initiatives, and ideas of local community members to drive the development of new technologies and creation of an environment-oriented culture.For the tenth Amashin Green Premium initiative, which was held from June 22 to August 21, 2020, we received a total of 133 entries from 129 applicants in the three categories of environmental projects, environmental activities, and environmental ideas. The final selection was based on two phases documentation screening and a presentation. The winning entry was from Kankyo System Co., Ltd., entitled “The Visualization of Water Quality and Commodification of an Apparatus to Automatically Raise and Lower a Water Quality Meter.”

Contributing to the Community

“Ama-chan and Shin-chan Project”

This project got its start ten years ago upon the Bank’s 90th anniversary. It was launched to meet the needs of the local community and neighborhood associations as a way to deepen the Bank’s connection to people in the local area and help resolve issues they face through active planning that utilizes the main strengths of the Bank.Since fiscal 2020, we have been making a shift to activities that align with the key

items in the Amashin SDGs Declaration. We will utilize established connections with the local community and work proactively to further those activities, helping to resolve local issues by working together at all levels within the Bank.

Promoting Art, Culture and Sports

World Piggy Bank Museum

The World Piggy Bank Museum houses one of the world’s largest collections of savings boxes (piggy banks), including more than 14,000 items from 62 countries. As of September 2020, a total of 40,000 people have seen the collection. The museum, which was opened in April 1984 with the objective of creating a unique cultural site in Amagasaki City, has since attracted many fans of piggy banks from the surrounding community and visitors from within and outside Hyogo Prefecture.

Thoroughgoing Compliance

At a time when financial institutions are being held to an exceptionally high bar with respect to their ethical standards and corporate social responsibility, our Bank has fully embraced its social mission and public nature. We have pledged to undertake our daily operations in accordance with the Shinkin Bank Act (Credit Union Act) and other laws and ethical standards. In recognition of our inherent responsibility as a financial institution to collaborate with members of the local community, we have identified thoroughgoing compliance as a critically important management obligation that we are committed to carrying out.

Initiatives to Prevent Money Laundering and Terrorist Financing

Preventing money laundering and terrorist financing are high-priority responsibilities we are addressing together with the international community. In addition to having established the Money Laundering and Terrorism Financing Prevention Policy, our Bank is developing an appropriate framework to prevent illicit use of financial services.

ANNUAL REPORT 2021 5

At a Glance

Financial Review

Profit and Loss

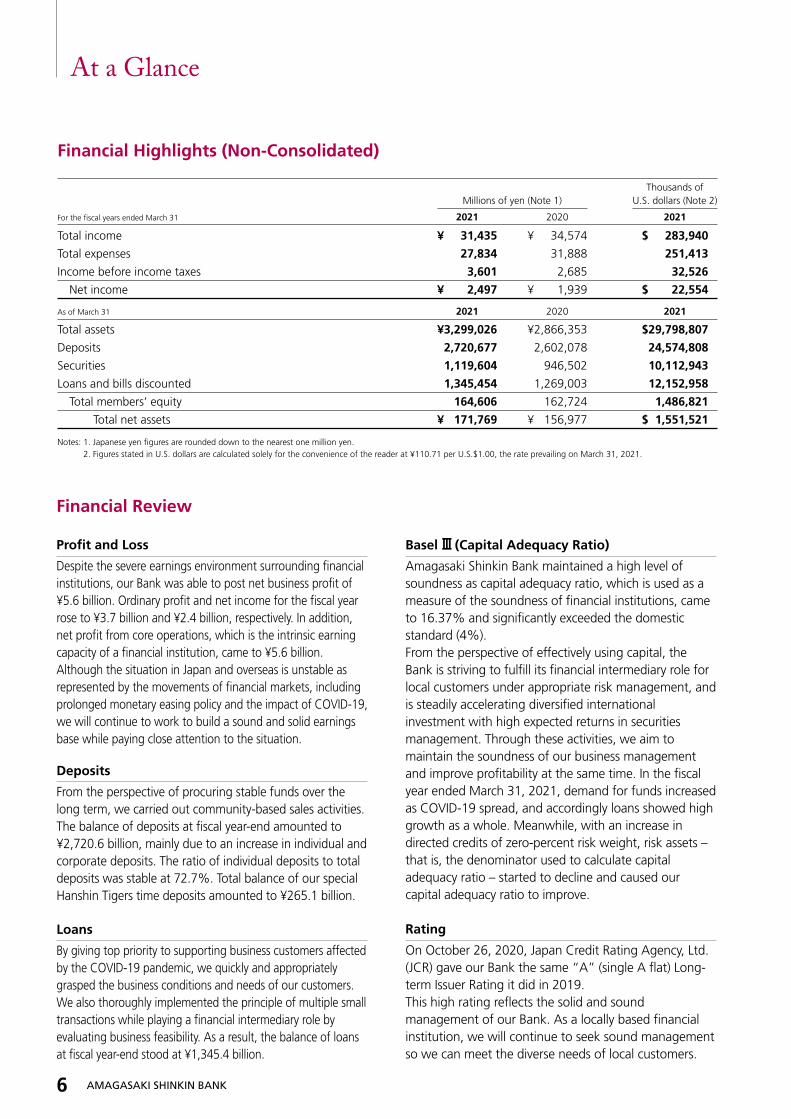

Despite the severe earnings environment surrounding financial institutions, our Bank was able to post net business profit of ¥5.6 billion. Ordinary profit and net income for the fiscal year rose to ¥3.7 billion and ¥2.4 billion, respectively. In addition, net profit from core operations, which is the intrinsic earning capacity of a financial institution, came to ¥5.6 billion. Although the situation in Japan and overseas is unstable as represented by the movements of financial markets, including prolonged monetary easing policy and the impact of COVID-19, we will continue to work to build a sound and solid earnings base while paying close attention to the situation.

Deposits

From the perspective of procuring stable funds over the long term, we carried out community-based sales activities. The balance of deposits at fiscal year-end amounted to ¥2,720.6 billion, mainly due to an increase in individual and corporate deposits. The ratio of individual deposits to total deposits was stable at 72.7%. Total balance of our special Hanshin Tigers time deposits amounted to ¥265.1 billion.

Loans

By giving top priority to supporting business customers affected by the COVID-19 pandemic, we quickly and appropriately grasped the business conditions and needs of our customers. We also thoroughly implemented the principle of multiple small transactions while playing a financial intermediary role by evaluating business feasibility. As a result, the balance of loans at fiscal year-end stood at ¥1,345.4 billion.

Financial Highlights (Non-Consolidated)

Millions of yen (Note 1)Thousands of

U.S. dollars (Note 2)

For the fiscal years ended March 31 2021 2020 2021

Total income ¥ 31,435 ¥ 34,574 $ 283,940

Total expenses 27,834 31,888 251,413

Income before income taxes 3,601 2,685 32,526

Net income ¥ 2,497 ¥ 1,939 $ 22,554

As of March 31 2021 2020 2021

Total assets ¥3,299,026 ¥2,866,353 $29,798,807

Deposits 2,720,677 2,602,078 24,574,808

Securities 1,119,604 946,502 10,112,943

Loans and bills discounted 1,345,454 1,269,003 12,152,958

Total members’ equity 164,606 162,724 1,486,821

Total net assets ¥ 171,769 ¥ 156,977 $ 1,551,521

Notes: 1. Japanese yen figures are rounded down to the nearest one million yen.2. Figures stated in U.S. dollars are calculated solely for the convenience of the reader at ¥110.71 per U.S.$1.00, the rate prevailing on March 31, 2021.

Basel Ⅲ (Capital Adequacy Ratio)

Amagasaki Shinkin Bank maintained a high level of soundness as capital adequacy ratio, which is used as a measure of the soundness of financial institutions, came to 16.37% and significantly exceeded the domestic standard (4%). From the perspective of effectively using capital, the Bank is striving to fulfill its financial intermediary role for local customers under appropriate risk management, and is steadily accelerating diversified international investment with high expected returns in securities management. Through these activities, we aim to maintain the soundness of our business management and improve profitability at the same time. In the fiscal year ended March 31, 2021, demand for funds increased as COVID-19 spread, and accordingly loans showed high growth as a whole. Meanwhile, with an increase in directed credits of zero-percent risk weight, risk assets – that is, the denominator used to calculate capital adequacy ratio – started to decline and caused our capital adequacy ratio to improve.

Rating

On October 26, 2020, Japan Credit Rating Agency, Ltd. (JCR) gave our Bank the same “A” (single A flat) Long-term Issuer Rating it did in 2019.This high rating reflects the solid and sound management of our Bank. As a locally based financial institution, we will continue to seek sound management so we can meet the diverse needs of local customers.

6 AMAGASAKI SHINKIN BANK

Financial Section

Non-Consolidated Balance SheetThe Amagasaki Shinkin Bank

Millions of yen (Note 1)Thousands of

U.S. dollars (Note 2)

As of March 31 2021 2020 2021

Assets

Cash and due from banks ¥ 747,556 ¥ 572,229 $ 6,752,380

Monetary claims purchased 18,796 15,209 169,776

Money held in trust 25,755 15,761 232,634

Trading account securities 2 0 18

Securities 1,119,604 946,502 10,112,943

Loans and bills discounted 1,345,454 1,269,003 12,152,958

Foreign exchanges 1,857 2,086 16,773

Other assets 17,130 16,686 154,728

Tangible fixed assets 19,853 20,275 179,324

Intangible assets 976 974 8,815

Deferred tax assets 932 6,072 8,418

Customers’ liabilities for acceptances and guarantees 9,075 8,058 81,970

Reserve for possible loan losses (7,970) (6,508) (71,989)

<Reserve for individual possible loan losses> <(5,314)> <(4,068)> <(47,999)> Reserve for investment losses — — —

Total assets ¥3,299,026 ¥2,866,353 $29,798,807

Liabilities and net assets

Liabilities:

Deposits ¥2,720,677 ¥2,602,078 $24,574,808

Certificates of deposit — — —

Borrowings 383,820 28,848 3,466,895

Payables under securities lending transactions — 53,364 —

Foreign exchanges 9 1 81

Other liabilities 8,545 11,409 77,183

Other reserves 2,601 2,896 23,493

Reserve for retirement allowance 2,524 2,714 22,798

Deferred tax liability — — —

Acceptances and guarantees 9,075 8,058 81,970

Total liabilities 3,127,257 2,709,376 28,247,285

Net assets:

Paid-in capital 14,597 14,769 131,848

Reserve 15,127 15,127 136,636

Earned surplus:

Voluntary reserves 132,226 130,726 1,194,345

Unappropriated profit 2,654 2,099 23,972

Total members’ equity 164,606 162,724 1,486,821

Difference of other marketable securities 7,130 (5,533) 64,402

Deferred hedge profit/loss 33 (213) 298

Total net assets 171,769 156,977 1,551,521

Total liabilities and net assets ¥3,299,026 ¥2,866,353 $29,798,807

Notes: 1. Japanese yen figures are rounded down to the nearest one million yen.2. Figures stated in U.S. dollars are calculated solely for the convenience of the reader at ¥110.71 per U.S.$1.00, the rate prevailing on March 31, 2021.

ANNUAL REPORT 2021 7

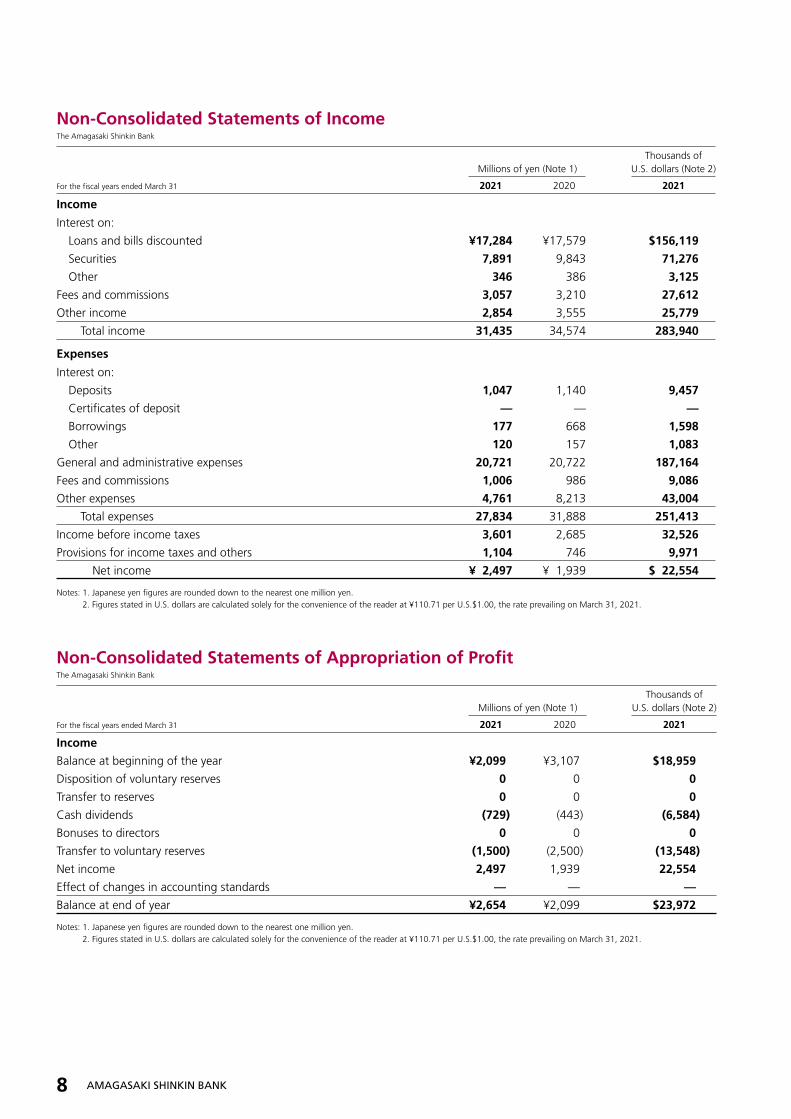

Non-Consolidated Statements of IncomeThe Amagasaki Shinkin Bank

Millions of yen (Note 1)Thousands of

U.S. dollars (Note 2)

For the fiscal years ended March 31 2021 2020 2021

Income

Interest on:

Loans and bills discounted ¥17,284 ¥17,579 $156,119

Securities 7,891 9,843 71,276

Other 346 386 3,125

Fees and commissions 3,057 3,210 27,612

Other income 2,854 3,555 25,779

Total income 31,435 34,574 283,940

Expenses

Interest on:

Deposits 1,047 1,140 9,457

Certificates of deposit — — —

Borrowings 177 668 1,598

Other 120 157 1,083

General and administrative expenses 20,721 20,722 187,164

Fees and commissions 1,006 986 9,086

Other expenses 4,761 8,213 43,004

Total expenses 27,834 31,888 251,413

Income before income taxes 3,601 2,685 32,526

Provisions for income taxes and others 1,104 746 9,971

Net income ¥ 2,497 ¥ 1,939 $ 22,554

Notes: 1. Japanese yen figures are rounded down to the nearest one million yen.2. Figures stated in U.S. dollars are calculated solely for the convenience of the reader at ¥110.71 per U.S.$1.00, the rate prevailing on March 31, 2021.

Non-Consolidated Statements of Appropriation of ProfitThe Amagasaki Shinkin Bank

Millions of yen (Note 1)Thousands of

U.S. dollars (Note 2)

For the fiscal years ended March 31 2021 2020 2021

Income

Balance at beginning of the year ¥2,099 ¥3,107 $18,959

Disposition of voluntary reserves 0 0 0

Transfer to reserves 0 0 0

Cash dividends (729) (443) (6,584)

Bonuses to directors 0 0 0

Transfer to voluntary reserves (1,500) (2,500) (13,548)

Net income 2,497 1,939 22,554

Effect of changes in accounting standards — — —

Balance at end of year ¥2,654 ¥2,099 $23,972

Notes: 1. Japanese yen figures are rounded down to the nearest one million yen.2. Figures stated in U.S. dollars are calculated solely for the convenience of the reader at ¥110.71 per U.S.$1.00, the rate prevailing on March 31, 2021.

8 AMAGASAKI SHINKIN BANK

Notes to Non-Consolidated Financial Statements

1. Basis of Presenting Financial Statements

The accompanying financial statements of the The Amagasaki Shinkin Bank (the “Bank”) are prepared in accordance with accounting principles and practices generally accepted in Japan, the Shinkin Bank Act, and other applicable rules and regulations. In preparing these financial statements, certain reclassifications and rearrangements have been made to the Bank’s non-consolidated financial statements issued domestically in order to present them in a form that is more familiar to readers outside Japan, and notes not required based on accounting principles in Japan have been provided for readers’ reference.

2. Japanese Yen Amounts and U.S. Dollar Amounts

All yen figures are rounded down to the nearest ¥1 million, and some totals may not correspond with the sum of constituent figures owing to rounding. The translations of Japanese yen amounts into U.S. dollar amounts are included solely for readers’ convenience and have been made at the rate of ¥110.71 to U.S.$1.00, the rate prevailing on March 31, 2021.

3. Accounting Policies

(a) Trading Account SecuritiesTrading account securities are valued by the mark-to-market method, and the cost of securities sold is calculated by the moving-average method.

(b) SecuritiesHeld-to-maturity debt securities are stated at cost and are amortized by the straight-line depreciation method using the moving-average method. Shares in subsidiaries and affiliates are stated at cost using the moving- average method. Of other securities, shares, etc., with quoted market prices are valued by the market-value method based on average prices during the month prior to the end of the fiscal year, and securities other than shares, etc., with quoted market prices are valued by the mark-to-market method based on market prices, etc., in principle on the balance sheet date (cost of securities sold is calculated by the moving-average method). However, other securities for which there is significant difficulty in determining fair value are stated at cost using the moving-average method. The full amount of net unrealized gains and losses on other securities is recorded directly within Net Assets.

(c) Tangible Fixed AssetsTangible fixed assets (excluding Leases) of the Bank are depreciated by the declining-balance method, except for buildings acquired on or after April 1, 1998 (excluding facilities installed in buildings), which are depreciated by the straight-line method.

(d) Foreign Currency TranslationAssets and liabilities denominated in foreign currencies are translated into Japanese yen at exchange rates prevailing at the balance sheet date (date of closing of accounts).

(e) Reserve for Possible Loan LossesThe reserve for possible loan losses is provided according to the Bank’s standards for write-offs and reserves.• Regarding loans to legally bankrupt entities (“bankrupt obligors”) or entities in equivalent situations (“substantially bankrupt obligors”), the balance of book values after direct deduction, less the estimated amounts for disposable collateral and collectible guarantees, is set aside in the reserve for possible loan losses.

• Regarding loans to entities that are now operating but are very likely to fail in the future (“bankruptcy risk obligors”), the balance of loans less the estimated amounts of disposable collateral and collectible guarantees is calculated, and the portion of this amount deemed necessary based on the consideration of the obligor’s overall payment abilities is set aside in the reserve for possible loan losses.• For other loans, amounts are set aside in the reserve for possible loan losses based on the Bank’s estimate rate of credit losses, which is calculated based on actual credit losses in specific periods in the past. For all loans, the associated marketing department performs asset assessments in accordance with the Bank’s internal rules for the self- assessment of assets. The Bank’s asset audit department, which is in dependent from the Bank’s other divisions, audits the assessment results. With respect to collateral, claims with guarantees, etc., associated with bankrupt obligors and substantially bankrupt obligors, the amounts for the value of collateral and recognized collectible amounts of guarantees are deducted from the asset amount, and the remainder is deemed to be the unrecoverable amount, which is then directly deduced from the value of the asset.

(f) Derivatives• Derivative transactions are valued based on the mark-to-market method.• The deferred method of hedge accounting is applied to transactions for hedging against interest rate risks arising from the Bank’s financial assets and liabilities in accordance with the stipulations of “Accounting and Auditing Treatment of Accounting Standards for Financial Instruments in the Banking Industry” (Japanese Institute of Certified Public Accountants (JICPA) Industry Audit Committee Report No. 24). The effectiveness of fair value hedges is assessed for each identified group of hedged items, and, in the case of hedges for offsetting market fluctuations, the loans, etc., that are hedged and the corresponding group of hedging instruments, such as interest rate swaps with the same maturity grouping, are compared.• The deferred method of hedge accounting is applied to transactions for hedging against foreign exchange fluctuation risk associated with foreign currency-denominated assets and liabilities in accordance with “Accounting and Auditing Treatment of Accounting for Foreign Currency Transactions in the Banking Industry” (JICPA Industry Audit Committee Report No. 25). The effectiveness of hedges—defined as currency swaps, foreign exchange swaps, and other similar transactions intended to hedge the risks of borrowing and lending in different currencies by swapping the borrowing currency for the lending currency—is assessed by confirming the foreign currency position of the hedged monetary assets and liabilities and of the hedging instruments. In addition, to hedge the foreign exchange risk for other foreign currency-denominated securities (other than debt securities), the securities to be hedged are specified in advance and the fair value hedges are arranged given the satisfaction of such conditions as the condition that a liability may exist due to future differences in spot and forward rates that is greater than the foreign currency-based acquisition cost of the associated foreign currency-denominated security.

(g) Reserve for Retirement AllowancesThe Bank provides the necessary amount for retirement allowances to be paid to its employees, based on the estimated retirement allowance liabilities and pension assets as of the end of the fiscal year under review.

ANNUAL REPORT 2021 9

4. Securities and Trading Account Securities

Securities as of March 31, 2021 and 2020 consisted of the following:

Millions of yen

2021 2020

National government bonds ¥ 217,784 ¥186,311

Municipal government bonds 144,704 151,369

Corporate bonds 343,486 291,664

Stocks 13,005 18,622

Other securities 400,621 298,533

Total ¥1,119,604 ¥946,502

Trading account securities as of March 31, 2021 and 2020 consisted

of the following:

Millions of yen

2021 2020

National government bonds ¥2 ¥0

Total ¥2 ¥0

5. Loans and Bills Discounted

Loans and bills discounted as of March 31, 2021 and 2020 consisted of the following:

Millions of yen

2021 2020

Bills discounted ¥ 14,250 ¥ 24,159

Loans on bills 27,716 40,588

Loans on deeds 1,267,532 1,161,048

Overdrafts 35,955 43,208

Total ¥1,345,454 ¥1,269,003

6. Deposits

Deposits as of March 31, 2021 and 2020 consisted of the following:

Millions of yen

2021 2020

Current deposits ¥ 82,724 ¥ 74,030

Ordinary deposits 1,111,537 899,431

Savings deposits 27,283 26,278

Deposits at notice 640 31,783

Time deposits 1,481,719 1,553,495

Other deposits 16,772 17,059

Total ¥2,720,677 ¥2,602,078

7. Subsequent Event

The Ordinary General Members’ Meeting, held on June 18, 2021, duly approved the following year-end appropriation of unappropriated profit as of March 31, 2021:

Millions of yen

2021

Unappropriated profit as of March 31, 2021 ¥2,654

Appropriations:

Transfer to reserve —

Cash dividends (3 percent per year) 729

Bonus to directors —

Transfer to voluntary reserve 1,800

Balance carried forward ¥ 124

Five-Year Summary of Selected Financial Data (Non-Consolidated Basis)

Millions of yen

For the fiscal years ended March 31 2021 2020 2019 2018 2017

Total income ¥ 31,435 ¥ 34,574 ¥ 33,580 ¥ 35,201 ¥ 43,079

Total expenses 27,834 31,888 29,469 29,166 34,972

Income before income taxes 3,601 2,685 4,110 6,035 8,107

Provisions for income taxes and others 1,104 746 1,147 1,693 2,380

Net income ¥ 2,654 ¥ 2,099 ¥ 3,107 ¥ 4,341 ¥ 5,726

On March 31 2021 2020 2019 2018 2017

Total assets ¥3,299,026 ¥2,866,353 ¥2,779,521 ¥2,734,402 ¥2,711,939

Deposits 2,720,677 2,602,078 2,569,440 2,534,603 2,511,319

Securities 1,119,604 946,502 809,784 768,421 818,635

Loans and bills discounted 1,345,454 1,269,003 1,282,302 1,263,284 1,254,242

Paid-in capital 14,597 14,769 14,887 15,002 15,015

Total members’ equity 164,606 162,724 161,349 159,098 155,369

Total net assets ¥ 171,769 ¥ 156,977 ¥ 167,635 ¥ 163,910 ¥ 161,451

10 AMAGASAKI SHINKIN BANK

Supplementary Consolidated Financial Information

Millions of yen (Note 1)Thousands of

U.S. dollars (Note 2)

For the fiscal years ended March 31 2021 2020 2021

For the fiscal year: Total income ¥ 31,948 ¥ 35,045 $ 288,573 Total expenses 28,202 32,193 254,737 Income before income taxes 3,746 2,852 33,836 Net income ¥ 2,473 ¥ 1,957 $ 22,337At year-end: Deposits ¥2,718,262 ¥2,599,439 $24,552,994 Loans and bills discounted 1,343,345 1,266,027 12,133,908 Securities 1,118,127 945,020 10,099,602 Total assets 3,298,352 2,864,735 29,792,719 Total members’ equity 166,341 164,476 1,502,492 Total net assets ¥ 174,377 ¥ 159,544 $ 1,575,079Notes: 1. Japanese yen figures are rounded down to the nearest one million yen.

2. Figures stated in U.S. dollars are calculated solely for the convenience of the reader at ¥110.71 per U.S.$1.00, the rate prevailing on March 31, 2021.

Independent Auditor and Independent Auditor’s ReportThe Amagasaki Shinkin Bank

In accordance with the provisions of Article 38-2-3 of the Shinkin Bank Act, KPMG AZSA & Co. has audited Amagasaki Shinkin Bank’s Balance Sheet, Statements of Income, and Statements of Appropriation of Profit in fiscal 2020 and fiscal 2021.

Reserve or the Coverage of Non-Consolidated Risk-Managed Loans under the Shinkin Bank Law

Millions of yen

2021 2020

For the fiscal years ended March 31

Balance (A)

Collateral or guarantees (B)

Reserve for possible loan losses (C)

Total coverage ratio (B+C)/A Balance

Loans to bankrupt borrowers ¥ 1,100 ¥ 1,100 ¥ 0 100.0% ¥ 2,100Delinquent loans 56,100 46,100 5,300 91.6% 43,900Loans past due three months and more 0 — 0 8.2% —Restructured loans 600 500 0 81.6% 800 Total ¥58,000 ¥47,800 ¥5,300 91.6% ¥47,000Notes: 1. The total coverage ratio has been stated with an upper limit of 100%.

2. Amounts of less than ¥100 million have been omitted.

Coverage of Loans under Disclosure Requirements of the Financial Reconstruction LawMillions of yen

2021 2020

For the fiscal years ended March 31

Balance disclosed (a)

Amount of coverage (b)

Amount of esti-mated collateral or guarantees (c)

Reserve for possible loan

losses (d)

Coverage ratio (b/a)

Reserve ratio

d/(a-c)Balance

disclosed

Non-performing loans under disclosure requirements of the Financial Reconstruction Law (A) ¥ 58,100 53,300 47,900 5,300 91.7% 52.7% ¥ 47,100Loans to borrowers under bankruptcy proceedings and equivalent loans 5,100 5,100 4,700 400 100.0% 100.0% 7,300Loans at risk 52,200 47,500 42,600 4,900 91.0% 51.1% 38,900Loans requiring caution 600 500 500 0 81.4% 30.8% 800Normal assets 1,297,800 1,231,000 Total (B) ¥1,355,900 ¥1,278,100Non-performing loan ratio (A/B x 100) 4.28% 3.68%Notes: 1. The total coverage ratio and reserve ratio have been stated with an upper limit of 100%.

2. Amounts of less than ¥100 million have been omitted.

ANNUAL REPORT 2021 11

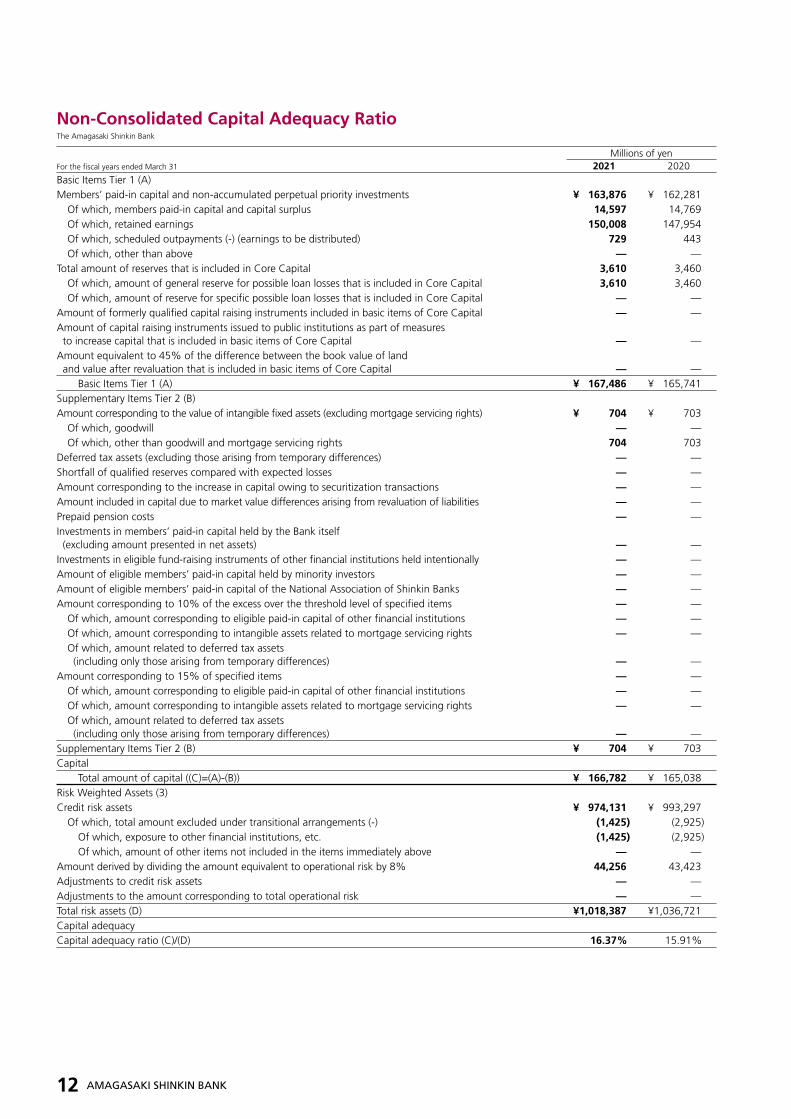

Non-Consolidated Capital Adequacy RatioThe Amagasaki Shinkin Bank

Millions of yenFor the fiscal years ended March 31 2021 2020Basic Items Tier 1 (A)Members’ paid-in capital and non-accumulated perpetual priority investments ¥ 163,876 ¥ 162,281 Of which, members paid-in capital and capital surplus 14,597 14,769 Of which, retained earnings 150,008 147,954 Of which, scheduled outpayments (-) (earnings to be distributed) 729 443 Of which, other than above — —Total amount of reserves that is included in Core Capital 3,610 3,460 Of which, amount of general reserve for possible loan losses that is included in Core Capital 3,610 3,460 Of which, amount of reserve for specific possible loan losses that is included in Core Capital — —Amount of formerly qualified capital raising instruments included in basic items of Core Capital — —Amount of capital raising instruments issued to public institutions as part of measures to increase capital that is included in basic items of Core Capital — —Amount equivalent to 45% of the difference between the book value of land and value after revaluation that is included in basic items of Core Capital — — Basic Items Tier 1 (A) ¥ 167,486 ¥ 165,741Supplementary Items Tier 2 (B)Amount corresponding to the value of intangible fixed assets (excluding mortgage servicing rights) ¥ 704 ¥ 703 Of which, goodwill — — Of which, other than goodwill and mortgage servicing rights 704 703Deferred tax assets (excluding those arising from temporary differences) — —Shortfall of qualified reserves compared with expected losses — —Amount corresponding to the increase in capital owing to securitization transactions — —Amount included in capital due to market value differences arising from revaluation of liabilities — —Prepaid pension costs — —Investments in members’ paid-in capital held by the Bank itself (excluding amount presented in net assets) — —Investments in eligible fund-raising instruments of other financial institutions held intentionally — —Amount of eligible members’ paid-in capital held by minority investors — —Amount of eligible members’ paid-in capital of the National Association of Shinkin Banks — —Amount corresponding to 10% of the excess over the threshold level of specified items — — Of which, amount corresponding to eligible paid-in capital of other financial institutions — — Of which, amount corresponding to intangible assets related to mortgage servicing rights — — Of which, amount related to deferred tax assets

(including only those arising from temporary differences) — —Amount corresponding to 15% of specified items — — Of which, amount corresponding to eligible paid-in capital of other financial institutions — — Of which, amount corresponding to intangible assets related to mortgage servicing rights — — Of which, amount related to deferred tax assets

(including only those arising from temporary differences) — —Supplementary Items Tier 2 (B) ¥ 704 ¥ 703Capital Total amount of capital ((C)=(A)-(B)) ¥ 166,782 ¥ 165,038Risk Weighted Assets (3)Credit risk assets ¥ 974,131 ¥ 993,297 Of which, total amount excluded under transitional arrangements (-) (1,425) (2,925) Of which, exposure to other financial institutions, etc. (1,425) (2,925) Of which, amount of other items not included in the items immediately above — —Amount derived by dividing the amount equivalent to operational risk by 8% 44,256 43,423Adjustments to credit risk assets — —Adjustments to the amount corresponding to total operational risk — —Total risk assets (D) ¥1,018,387 ¥1,036,721Capital adequacyCapital adequacy ratio (C)/(D) 16.37% 15.91%

12 AMAGASAKI SHINKIN BANK

Corporate Data

President

Seiji Sakuda

Organization Chart

Board of Directors

The Amagasaki Shinkin Bank

International Department

3-30, Kaimei-cho, Amagasaki, Hyogo 660-0862, Japan

Telephone: 06-6412-5440

SWIFT BIC: AMASJPJZ

Bank Management Indices as of March 31, 2021

Loans: 1,345,454 millions of yen

Deposits: 2,720,677 millions of yen

Capital Adequacy Ratio (non-consolidated): 16.37%

Capital Adequacy Ratio (consolidated): 16.58%

Long-term Issuer Rating: “A” (JCR) (single A flat)

Branches: 90

Employees: 1,302

an

Tokyo

AmagasakiOsakaKobe

Directory

Comprehensive Risk Management Committee

General Members’ Meeting

Board of Directors

Chairman of the Board of Directors

President

Deputy President

Senior Managing Directors

Managing Directors

Directors

Auditors

Inspection Department

Securities & Investment Department

General Planning Department International Department Loan Center

Loan Administration Department

Loan Department I

Loan Department II

Solutions Promotion Department

Regional Support Department

Business Promotion Department

Branches

Corporate Management Department

Secretaries Office

Systems & Operations Department

Compliance & Risk Administration Department

Senior Managing Directors

Kenji Watanabe

Yasuhiro Imai

Atsuhiro Wada

Managing Directors

Kouzou Nagakawa

Naruaki Ueno

Kotaro Ozawa

Sadayuki Sugimori

Directors

Takuji Kobayashi

Yasaka Matsuda

Hirohisa Taguchi

Auditors

Yoshinori Nishida

Seiichi Ueno

Toshifumi Miyanaga

Norisaburo Ikuta

(As of July 1, 2021)

ANNUAL REPORT 2021 13

Printed in Japan

3-30, Kaimei-cho, Amagasaki, Hyogo 660-0862, Japan

https://www.amashin.co.jp