Embed Size (px)

Citation preview

American Bar AssociationSection of Taxation

Insurance Tax CommitteeAustin, TX

Sept. 14, 2017

BEPS CbC Reporting and MLI Developments

Jesse EggertKPMG

Carol TelloEversheds-Sutherland (US) LLP

BEPS Country-by-Country Reporting

• Three-Tier Approach Master File

Provides standardized information relative to all MNEgroup members

Local File Provides information about material transactions of the

local taxpayer Country-by-Country report

Provides information about the global allocation of the group income and taxes as well as indicators of the location of economic activity within the group

CbC Guidance

• OECD Guidance on the Implementation of Country-by-Country Reporting (Updated July 2017) Who has to file Timing and preparation of filing of the CbC report Conditions for jurisdictions to obtain and use a CbC report Government-to-government exchanges Master file/local file to be implemented though local country

legislation or administrative procedures and filed directly with the tax administrations in each relevant jurisdiction

CbC Guidance

Who has to file• Multinational group companies with an annual

consolidated group revenue of €750M (or its near equivalence in another currency, which is USD850M) No other exemptions other than for international

transportation and inland waterways income covered by a treaty

• Threshold should exclude 85-90% of multinational group companies but capture 90% of corporate revenues

• Revenue threshold will be reviewed in the 2020 review of implementation

4

CbC Guidance - Timing and Preparation of CbC Report

• Reporting periods (MNE fiscal years) based on financial statementconsolidated reporting periods MNE fiscal years are not taxable years or the financial reporting

periods of individual subsidiaries

• The first reports will be required for MNE fiscal years beginning on or after January 1, 2016.

• For fiscal years ending on December 31, the first CbC reports will be due by December 31, 2017, i.e., 12-months after the end of 2016.

• U.S. date starts for accounting periods that begin on or after June 30,2016 but allows for an early reporting period so that the OECD reporting requirement is met.

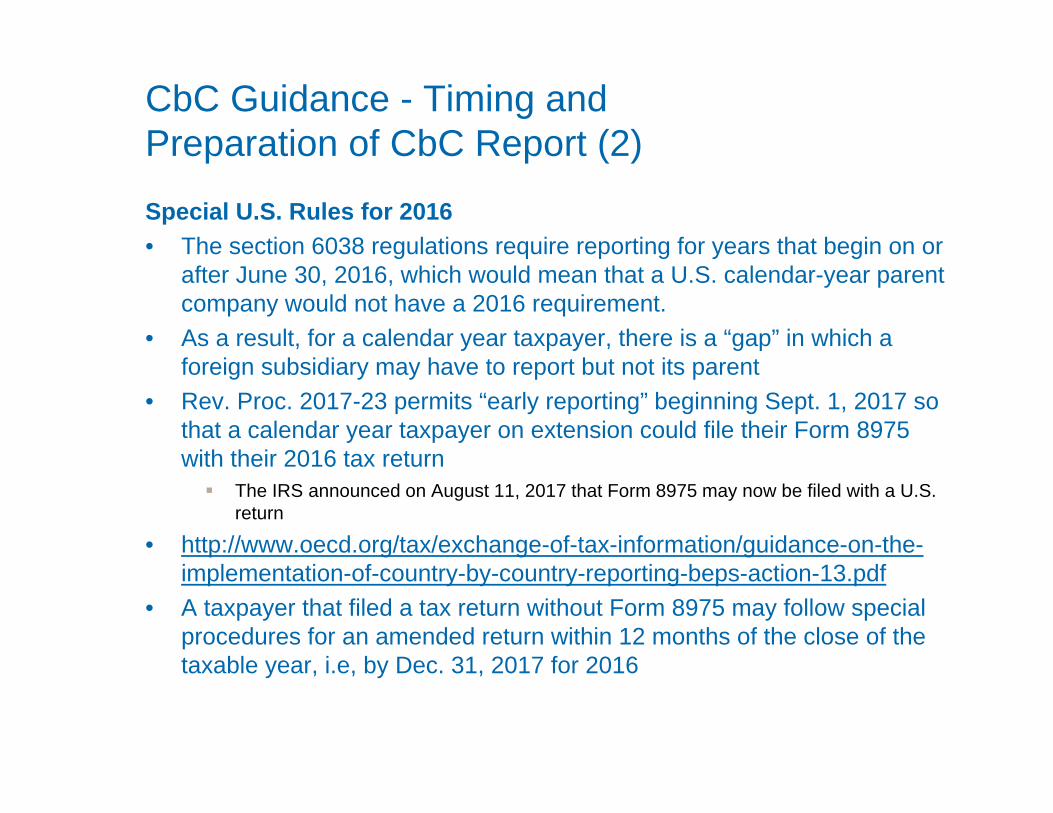

CbC Guidance - Timing and Preparation of CbC Report (2)

Special U.S. Rules for 2016• The section 6038 regulations require reporting for years that begin on or

after June 30, 2016, which would mean that a U.S. calendar-year parent company would not have a 2016 requirement.

• As a result, for a calendar year taxpayer, there is a “gap” in which a foreign subsidiary may have to report but not its parent

• Rev. Proc. 2017-23 permits “early reporting” beginning Sept. 1, 2017 so that a calendar year taxpayer on extension could file their Form 8975 with their 2016 tax return The IRS announced on August 11, 2017 that Form 8975 may now be filed with a U.S.

return

• http://www.oecd.org/tax/exchange-of-tax-information/guidance-on-the-implementation-of-country-by-country-reporting-beps-action-13.pdf

• A taxpayer that filed a tax return without Form 8975 may follow special procedures for an amended return within 12 months of the close of the taxable year, i.e, by Dec. 31, 2017 for 2016

CbC Guidance

Conditions for jurisdictions to obtain and use a CbC report• Confidentiality

Legal protections on the use of information and rules re: what persons to whom information may be disclosed

• Consistency Ultimate parent files CbC report in its residence jurisdiction Standard template to be used

• Appropriate use To assess high-level transfer pricing risk and other BEPS-related risks Adjustments should NOT be proposed on the basis of an income allocation

formula based on the CbC data Any adjustments made based on the CbC data will be conceded by the

local Competent Authority CbC data can be used as a basis for further inquiries in the course of an

audit

CbC Guidance

Government-to-government exchanges• Framework

Ultimate parent files CbC report in its country of residence Residence country automatically exchanges with countries where

the MNE group operates that comply with the required conditions If an exchange failure occurs, local filing or filing with the next tier

country is secondary mechanism• Implementation package

Key elements of model domestic legislation Exchange of information /competent authority procedures Domestic legislation required to be introduced in a timely manner Ongoing monitoring to occur and to be considered in the 2020

review

Current Status of CbCR

• Over 700 bilateral exchange agreements entered into by 30 jurisdictions (as of May 2017) Excel spreadsheet for exchange relationships http://www.oecd.org/tax/beps/country-by-country-exchange-

relationships.htm

• First exchanges to take place in 2018• 64 signatories to Multilateral Competent Authority

Agreement (as of June 22, 2017)• U.S. will enter into bilateral agreements

19 bilateral CAAs signed (as of 8/21/2017)

Form 8975 – Schedule A

Overview of Outcomes of MLI signing ceremony

13

MLI - Background

BEPS Action 15

Several BEPS Action Items produced changes to OECD Model Tax Convention to address: Hybrid Mismatches (Action 2) Treaty Abuse (Action 6) Artificial Avoidance of Permanent Establishment (Action 7) Improving Dispute resolution (Action 14)

Implementing through bilateral treaty negotiation would take years or even decades

Action 15 explored possibility of a single instrument to modify all tax treaties at once

Overview of MLI

Developed by “Ad Hoc Group” of 100 jurisdictions and countries Not an amending protocol – operates alongside existing treaties Function is to implement agreed final BEPS recommendations with limited

modification Exception: Arbitration provision developed by Sub-Group of Ad Hoc

Group as part of the MLI negotiation Text finalized November 24, 2017 Signing ceremony June 7, 2017

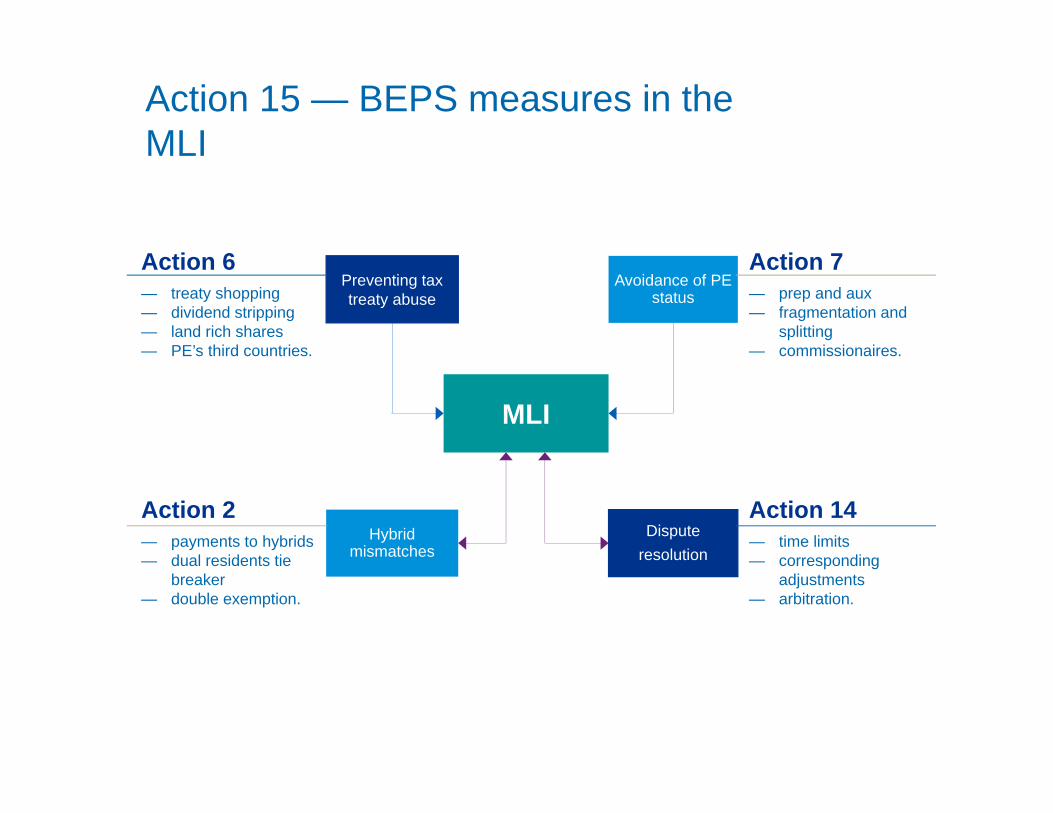

Action 15 — BEPS measures in the MLI

MLI

Action 2— payments to hybrids— dual residents tie

breaker— double exemption.

Action 6— treaty shopping— dividend stripping— land rich shares— PE’s third countries.

Action 7— prep and aux— fragmentation and

splitting— commissionaires.

Action 14— time limits— corresponding

adjustments— arbitration.

Preventing tax treaty abuse

Disputeresolution

Avoidance of PE status

Hybrid mismatches

Outcome of MLI signing ceremony – June 7

Who signed the MLI 67 jurisdictions signed (68 covered), with three more (Mauritius,

Cameroon, and Nigeria) signing later 6 additional jurisdictions expressed intent to sign More jurisdictions expected to sign by end of 2017

Treaties impacted 1,135 treaties impacted (2,382 listed) 85 percent of treaties between signatories covered.

Provisional MLI positions published Information provided at signing includes:

tax treaties covered options chosen Information about existing provisions affected by MLI reservations made

Modifications to individual tax treaties are based on interaction between choices made by each signatory.

MLI signatories (as of August 9, 2017)

Americas Europe/Eurasia ASPAC AfricaMiddle-East

ArgentinaChileColombia Costa RicaMexicoUruguay

CanadaJamaica*Panama*

AndorraArmeniaAustriaBelgiumBulgariaCroatia

CyprusCzech Rep.DenmarkFinlandFranceGeorgiaGermany Greece

Guernsey Hungary IcelandIrelandIsle of MannItaly

JerseyLatviaLiechtensteinLithuaniaLuxembourgMaltaMonacoNetherlands

Norway*PolandPortugalRomaniaRussiaSan Marino

SerbiaSlovak R.SloveniaSpainSwedenSwitzerlandTurkeyUKEstonia*

AustraliaChinaFijiHong Kong**IndiaIndonesia

JapanKoreaNew ZealandPakistanSingapore

Burkina FasoEgyptGabonIsraelKuwaitNigeria

Senegal

SeychellesSouth AfricaCote d’Ivoire*Lebanon*Tunisia*

*Committed to sign in the future

Procedural matters

Signatories can amend their MLI Positions freely until ratification

After ratification countries can opt in to more provisions, or remove reservations

Consolidated texts might be prepared in local jurisdictions, but will not be legal documents

Expected that first modifications will become effective in course of 2018

Effective Dates

Entry into force begins after five countries ratify

Entry into effect

Entry into effect may be modified or delayed through reservation

Once at least five signatories ratify, the MLI enters into force with respect to those Parties as of the first day of the month following three calendar months after the fifth deposit Example: If fifth deposit is made September 2017, entry info force for first five

Parties is January 1, 2018 Subsequent parties have same three-month period after deposit until entry into force

Withholding tax: takes effect first day of calendar year after both parties to CTA have MLI enter into force Example: If entry into force is February 1, 2018, effective date is 1/1/2019.

Other taxes: Effective for taxable periods beginning on or after six months after date MLI enters into force for both parties Example: If entry into force is February 1, 2018, provisions take effect for taxable

years beginning on or after August 1, 2018 (i.e. 1/1/19 for calendar year taxpayers)

11 countries elected to delay entry into effect until domestic procedures are complete Roughly half made other reservations affecting entry into effect

19

Key Provisions of MLI

20

Treaty Abuse

• Minimum Standard on treaty abuse Preamble language regarding purpose of treaties Principal Purposes Test (PPT) – adopted by ALL signatories Benefits not granted “if it is reasonable to conclude . . . that obtaining

that benefit was one of the principal purposes of any arrangement or transaction”

• Optional Simplified LOB to be paired with PPT – adopted by 12 jurisdictions Argentina, Armenia, Bulgaria, Chile, Colombia, India, Indonesia, Mexico,

Russia, Senegal, the Slovak Republic and Uruguay• 365 holding period for direct dividend rate (31 countries)• Expansion and one-year lookback for Real Property Holding Cos (40

countries)• Provision to Deny Benefits to Triangular PE Arrangements (22 countries) Does not apply to PE in one of the Contracting States

Artificial Avoidance of PE• Commissionaire Arrangements and Similar Strategies (Article 12) Expanded DAPE test: person that habitually plays a “principal role” leading to the

conclusion of contracts for the sale of goods of or provision of services of a related enterprise without material modification by the enterprise

Provides that an agent that acts exclusively or almost exclusively on behalf of one or more closely related enterprises is not an independent agent

Adopted by 30 countries, including many in LATAM, France, India, Indonesia, Japan, the Netherlands, New Zealand and Spain

• Specific Activity Exemptions (Article 13) Subjects specific activity exemptions from PE status to testing for preparatory or

auxiliary status (i.e., no longer safe harbor) (adopted by 33 countries) Anti-fragmentation provision to apply where an enterprise or closely related enterprise

carries on business activities in the same place or at another place in the same State that rise to the level of a PE (adopted by 39 countries)

• Contract Splitting to avoid Construction/Extraction PEs (Article 14) Aggregates (1) time spent (in excess of 30 days in the aggregate) at a building site

project by an enterprise, and (2) time spent during different periods (in excess of 30 days) by closely related enterprises at the same site (adopted by 26 countries)

• Mandatory MAP provisions (Articles 16 and 17) Allowing taxpayers to present to either Competent Authority Alternatively, allowing taxpayers to present to Competent Authority of

state of residence Obligation to endeavor to resolve cases Corresponding adjustments

• Optional Mandatory Binding Arbitration 26 Countries opted to apply, covering 150 treaties Choice between “last best offer” (“baseball-style”) or “independent

opinion” arbitration If one jurisdiction chooses baseball and one chooses independent

opinion, independent opinion applies Basic framework provided, but competent authority agreement is needed Model competent authority agreement to be developed

Dispute Resolution

“Hybrid Mismatches”

• Transparent Entities (Article 3) Provision addressing whether an item of income derived through a

transparent entity is eligible for treaty relief Adopted by 25 countries

• Dual Resident Entities (Article 4) Residence tie-breaker rule for persons other than individuals based on

whether the competent authorities can mutually agree on a single Jurisdiction of residence

Adopted by 27 countries • Limitation on Elimination of Double Taxation (Article 5) 3 Alternative approaches to prevent exemption for dividends received

if the issuer is entitled to a deduction for the dividend Adopted by 15 countries, with an additional 26 willing to permit

application by treaty partner

![MCQ 2011 Bar Taxation[1]](https://img.pdfslide.net/doc/110x75/577cdae21a28ab9e78a6cd15/mcq-2011-bar-taxation1.jpg)