Embed Size (px)

Citation preview

Shanzhai 1

Shanzhai in and out of China: Lessons for Manufacturers from Small States

Nigel Williams1, Ke Rong,2 Tom Ridgman and Y. Shi1 Business Systems Department, Business School, University of Bedfordshire, 2Doctoral

Researcher, Institute for Manufacturing, University of Cambridge

Shanzhai 2

Abstract

Indigenous consumer goods manufacturing SMEs from small developing countries or small

states face significant challenges: limited home markets, restricted access to finance and little

indigenous technological development. Existing prescriptions for improving performance of

individual firms are of limited value in the short or medium term as they require a level of

institutional support that is not available in small states. For these organizations, building and

managing international relationships is necessary in order to access complementary resources

and capabilities to match the innovation, quality or performance of better funded foreign rivals.

However, little research to date has examined how SMEs build or leverage manufacturing

networks.

This work seeks to provide useful guidance to small state firms by examination of successful

emerging market SMEs using an international manufacturing network perspective. One such

grouping are the” Shanzhai” firms based in the Shenzen Region of China. With origins in the

watch making industry, these firms have successfully utilized networks to design and produce in-

creasingly complex technological consumer products. In this paper, the characteristics of these

organizations are reviewed to create a framework for managing international manufacturing net-

works by SMEs. Using case studies of exporters from Trinidad and Tobago, a small state in the

Caribbean, the framework is then used to analyze their operations and suggest areas for improve-

ment.

INTRODUCTION

Over time, manufacturing has evolved from factory production to connected networks of

industrial activity(Michael, 2004). Firms therefore need to adopt a position in these structures

that enables them to access the knowledge and materials necessary to serve

customers(Brookfield & Ren-Jye, 2005). This is a challenge for firms from small developing

countries or small states. Characterized by a narrow resource base, (relatively) weak institutions

and a high degree of openness (Easterly & Kraay, 2000), they are a relatively recent phenomenon

and have emerged as a result of historical processes: Decolonization and De-federation (Henrikson,

1999). In Decolonization, former colonial territories were given up by their former owners and

became independent states. In De-federation, clusters of geographically close territories were

broken into individual countries. For organizations from these states, internationalization is an

imperative rather than a choice due to the small home market. The governments of these states

have expended significant effort in order to build international firms utilizing a variety of policy

instruments (Downes, 2004). These initiatives, however have been based on a limited

understanding of the internationalization process of firms from these particular resource

environments and results have been mixed. As a highly fragmented and heterogeneous region,

the Caribbean is an appropriate location for examining the activities of firms from small

developing countries.

Despite their relatively small size, the islands attract a disproportionate level of attention due, in

part, to their role in world historical events (Sahay, Robinson, & Cashin, 2006). As former

colonies, Caribbean islands have long been integrated in the world economy, importing labour

and exporting commodities to Europe and later, the United States (Demas, 1978). With a

combined population of 37 million people (Secretariat, 2007), it contains countries that are

highly heterogeneous, varying in size and income. Like many other colonies in Africa and Asia,

the nations of the Caribbean became independent in the 1960s and 70s(Payne & Sutton, 2001).

Unlike their larger counterparts, however, the Caribbean faces particular constraints:

1) Externally driven economies.

Over its history, Caribbean nations have relied on exports. During the colonial period, they

exported commodities such as sugar for processing at the colonial centre. Post independence,

economic structures have reconfigured to incorporate services such as tourism and semi finished

goods such as petrochemicals. However, they are still heavily export dependent. Due to their

export dependence, external events impact significantly on local conditions. Changes in

commodity prices vary domestic incomes significantly. In some countries, production of key

export commodities are dominated by large multinationals whose decisions may dictate

economic performance (Pantin, Sandiford, & Henry, 2002).

2) Higher per capita income than many developing countries,

Partially due to their long history of exports, most Caribbean countries can be classified as

middle income developing countries. This factor makes them inherently unattractive for

industries that rely on low cost labour. Intervention by the state is required to make production of

these items possible.

3) Dependence on preferential access Schemes

A significant proportion of Caribbean exports rely on trade agreements for access to markets. For

example, the region’s agricultural commodities such as Sugar and Bananas are sold under long

term arrangements with Europe at a higher price than those produced by rivals. Since the region

has not developed markets independently for these products, any change in agreements can

adversely affect domestic economies.

The heavy dependence on a narrow range of exports and preferential trade agreements has been

of great concern to Caribbean states. Their openness results in a higher level of exposure to the

demands of international competition without many of the tools available to their larger

counterparts. These countries have attempted to compensate for these circumstances, and

Caribbean leaders since the 1950’s have employed state resources in their quest for development

(Klak, 1995). Primarily through application of industrial policy, Caribbean states have attempted

to diversify their economies to produce a wider range of items and generate employment.

However, the small and fragmented nature of Caribbean markets means that output from these

industries needed to be directed towards international markets for any success (Farrell, 1980).

While development theory outlines the paths firms from small states may take to become more

competitive (Vonortas, 2002), it provides little guidance on how to do so. Manufacturing strategy

research indicates the performance standards and practices that a firm should adopt to become

more competitive(Barnes, Bessant, Dunne, & Morris, 2001), but face limited applicability in the

resource constrained environment of small states. This paper seeks to provide an alternative to

the technology commercialization focus of policy prescriptions(Borras, 2009) by comparing

manufacturing development in a Caribbean country (Trinidad and Tobago) to an emerging

market region that has experienced consistent systematic upgrading (Shenzen). First, existing

theoretical perspectives on production networks and manufacturing strategy are reviewed. Next

comparative case studies are conducted that compare origins, characteristics and capabilities of

TT and Shenzen firms. The results are analyzed to provide recommendations for both firm

management and policymakers in small states.

LITERATURE REVIEW

While globally distributed production systems have existed since the 1600’s (Wallerstein, 2000),

only recently has academic research emerged to analyze and describe how firms operate in

global production systems. The development oriented Commodity chain concept (Taylor, 1988)

was the first such attempt, which viewed production as a set of interlinked, internationally

distributed activities to convert raw materials to finished goods. Country economic development

was modeled as movement within these structures which was a radical departure from the

dominant paradigm at the time of national development based on inter country trade.

Later work in Global commodity chains (GCC) extended this concept to examine the complete

set of actors and their interactions involved in the production of a given product or service

(Leslie & Reimer, 1999). GCC widened the scope of research from the geographic scope of

production activities to incorporate transformation processes, governance structures and the

institutional contexts in which activities are performed(Gereffi, 1999). These dimensions were

used to classify GCCs as Producer Driven or Buyer Driven. Producer Driven chains are ones in

which capital intensive manufacturers own or control multiple levels of a hieratically organized

production system. Buyer Driven chains are less structured networks of suppliers and retailers

who create items under a single brand or label(Gereffi, 2001). The issue of governance in these

structures have been further refined in the Global Value Chain research network (see

www.globalvaluechain.org). to incorporate dimensions of transaction complexity,

communication processes and supplier capabilities(Gereffi, Humphrey, & Sturgeon, 2005). The

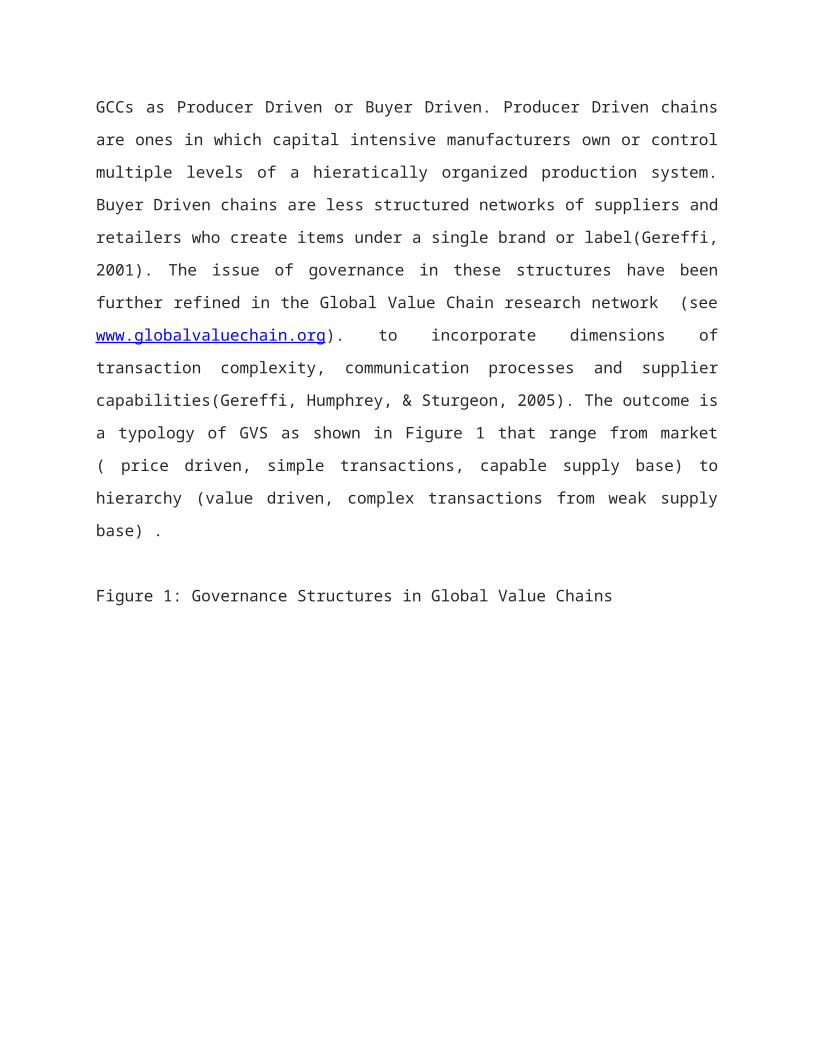

outcome is a typology of GVS as shown in Figure 1 that range from market ( price driven,

simple transactions, capable supply base) to hierarchy (value driven, complex transactions from

weak supply base) .

Figure 1: Governance Structures in Global Value Chains

Source: Gereffi et al 2005

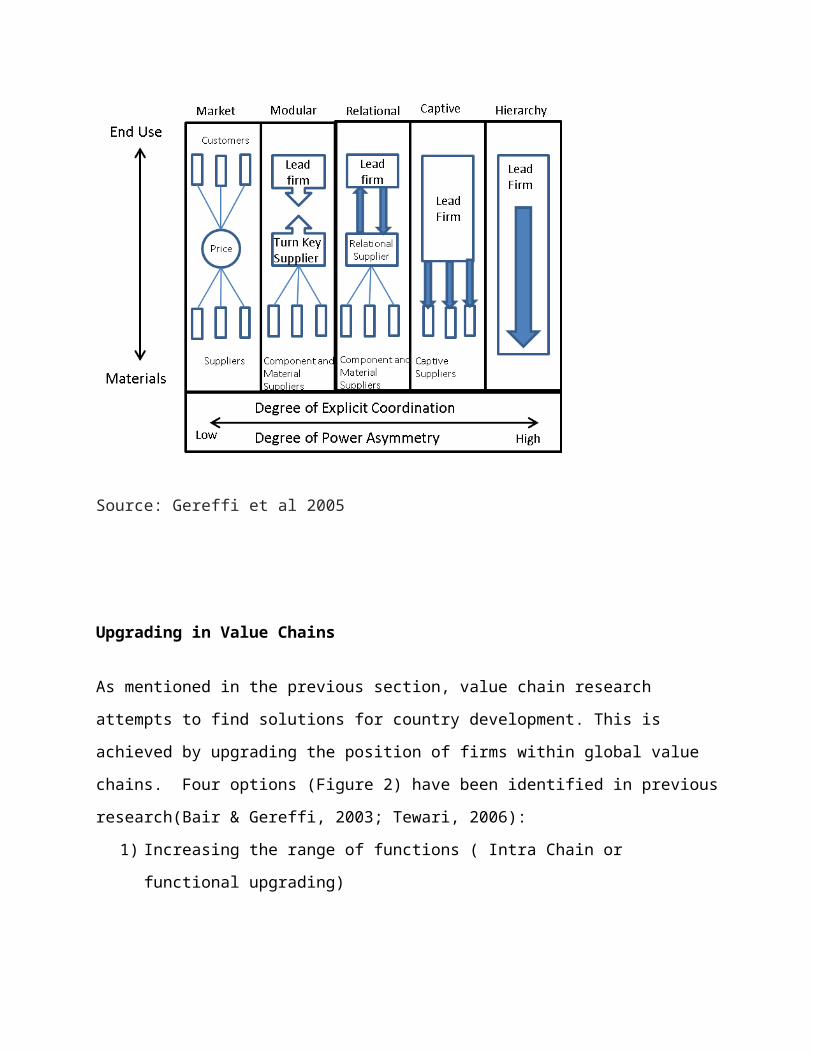

Upgrading in Value Chains

As mentioned in the previous section, value chain research attempts to find solutions for country

development. This is achieved by upgrading the position of firms within global value chains.

Four options (Figure 2) have been identified in previous research(Bair & Gereffi, 2003; Tewari,

2006):

1) Increasing the range of functions ( Intra Chain or functional upgrading)

2) Product Upgrading (Improving the quality or functions of products)

3) Process Upgrading (Reducing costs or increasing quality of domestic production pro-

cesses)

4) Inter Chain upgrading (moving from one industry to another)

Figure 2: Upgrading in Global Value Chains

.

GCC/GVC research offers little guidance on how this upgrading is to be accomplished. Work

has pointed to improvement of “capabilities”(Gereffi, 2005) but with little detail as to how these

capabilities would be built. However, a body of knowledge exists in the manufacturing literature

on the means by which firms define and change the role of manufacturing over time.

Internal (Factory) Upgrading

The strategic role of the manufacturing function was first highlighted in the late 1960’s(Skinner,

1969) as a means to build competitive advantage in organizations. Further development of this

Internal External

Process

Product Inter Chain

Intra Chain

Upgrading options

Options f

idea attempted to change the role of manufacturing from passive to active (Wheelwright, 1984).

More recently, researchers have highlighted the need for aligning manufacturing capabilities

with market requirements (Hill & Westbrook, 1997). These concepts have been linked into 3

paradigms of manufacturing strategy (C Voss, 1995): Competing, Strategic Choices and Best

Practice.

1. Competing School

The competing school examines the capabilities that a firm should have or develop in order to

meet organizational objectives (Wheel Wright, 1984). Examples of this approach are Hill’s

framework(Hill & Westbrook, 1997) and manufacturing audits (Platts & Gregory, 1990).

2. Strategic Choice

The strategic choices paradigm adopts a holistic approach(Ward, Bickford, & Leong, 1996) to

manufacturing, examining the need for internal and external coherence in manufacturing

strategy (Kim & Lee, 1993).

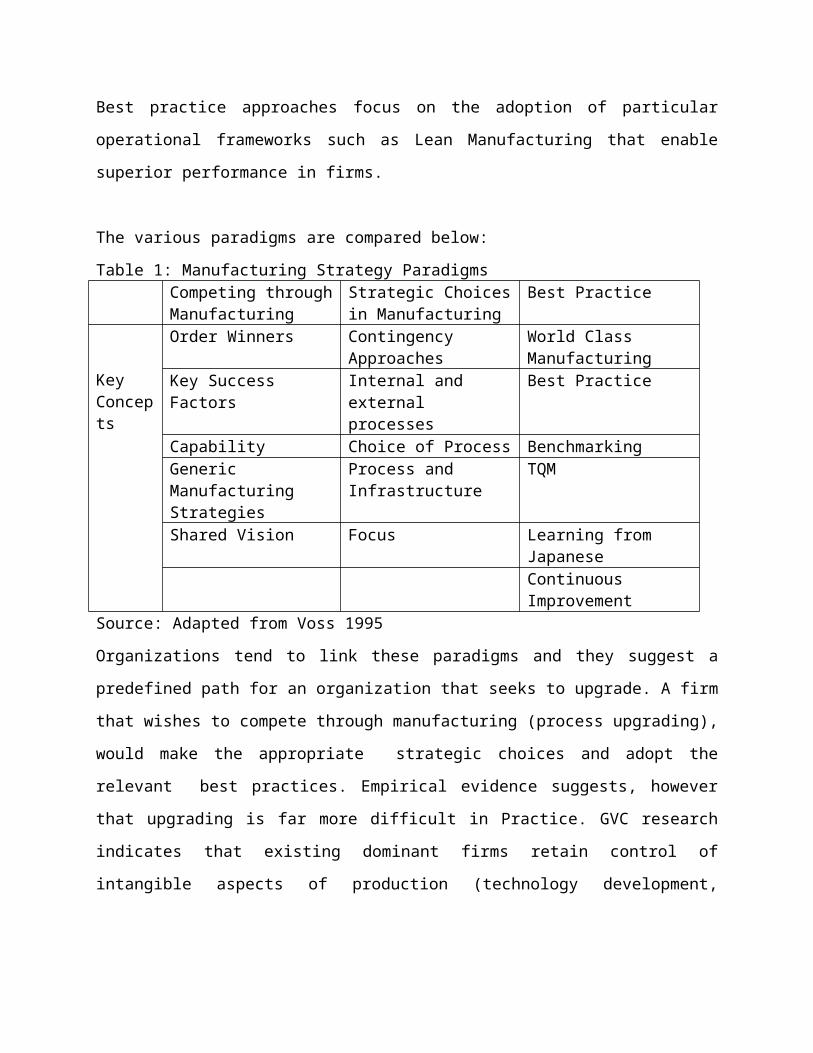

3. Best Practice Approaches

Best practice approaches focus on the adoption of particular operational frameworks such as

Lean Manufacturing that enable superior performance in firms.

The various paradigms are compared below:

Table 1: Manufacturing Strategy ParadigmsCompeting through Manufacturing

Strategic Choices in Manufacturing

Best Practice

Key Concepts

Order Winners Contingency Approaches World Class Manufacturing

Key Success Factors Internal and external processes

Best Practice

Capability Choice of Process BenchmarkingGeneric Manufacturing Strategies

Process and Infrastructure

TQM

Shared Vision Focus Learning from JapaneseContinuous Improvement

Source: Adapted from Voss 1995

Organizations tend to link these paradigms and they suggest a predefined path for an

organization that seeks to upgrade. A firm that wishes to compete through manufacturing

(process upgrading), would make the appropriate strategic choices and adopt the relevant best

practices. Empirical evidence suggests, however that upgrading is far more difficult in Practice.

GVC research indicates that existing dominant firms retain control of intangible aspects of

production (technology development, marketing) and shift the tangible aspects to low cost

countries(Gereffi, 2001).

The growth of outsourcing and the increasing importance of services in manufacturing (Slack,

Lewis, & Bates, 2004) has increased the complexity of the upgrading process. Globally

distributed manufacturing networks have distinct capabilities based on dispersion and

coordination(Yongjiang Shi & Gregory, 1998) . Strategic targets accessibility is derived from

the geographic dispersion of manufacturing network. This capability enables access to markets,

tangible (materials) and intangible resources (skilled employees, social connections)(Tain-Jy,

Homin, & Ying-hua, 2004). Thriftiness ability is derived from the coordination of an

international production network(Thomas, Ian, Wilkinson, & Johnston, 2002). Manufacturing

mobility refers to the flexibility of a given international network(Y. Shi & Gregory, 2005).

Firms may transfer technology, product lines or management among subsidiaries. Finally,

learning ability can be derived from the network’s access to geographically distributed sources of

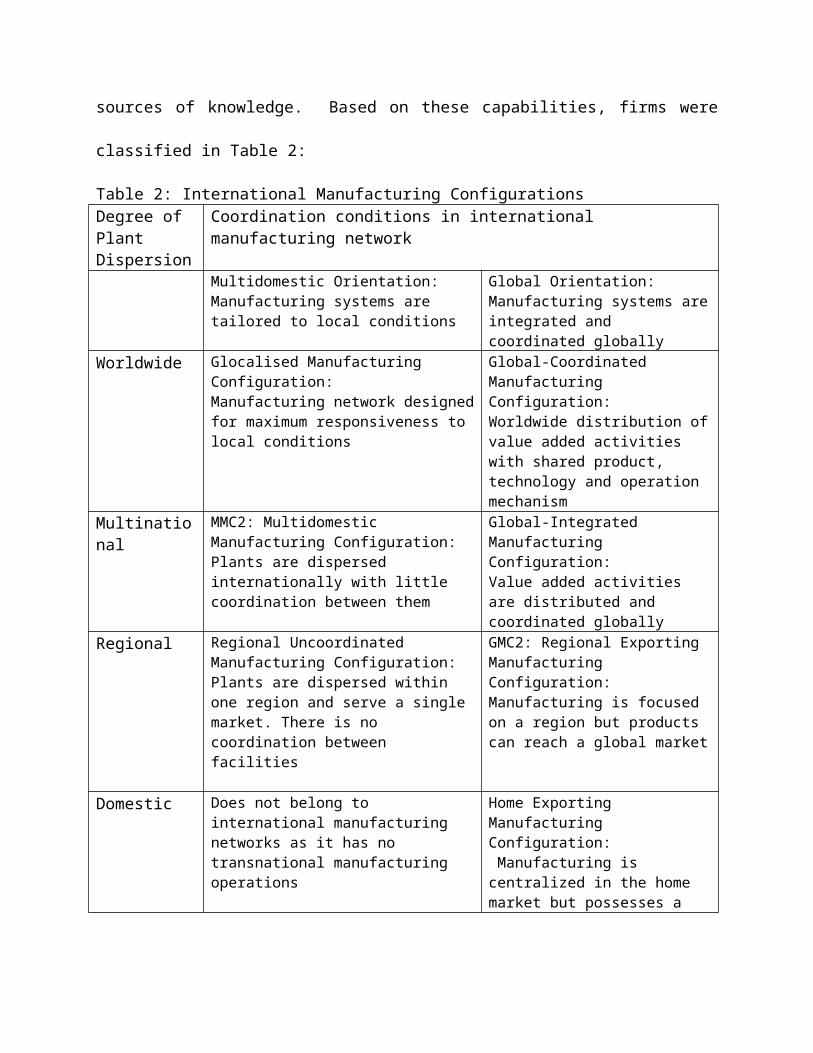

knowledge. Based on these capabilities, firms were classified in Table 2:

Table 2: International Manufacturing ConfigurationsDegree of Plant Dispersion

Coordination conditions in international manufacturing network

Multidomestic Orientation:Manufacturing systems are tailored to local conditions

Global Orientation:Manufacturing systems are integrated and coordinated globally

Worldwide Glocalised Manufacturing Configuration:Manufacturing network designed for maximum responsiveness to local conditions

Global-Coordinated Manufacturing Configuration:Worldwide distribution of value added activities with shared product,

technology and operation mechanismMultinational MMC2: Multidomestic Manufacturing

Configuration:Plants are dispersed internationally with little coordination between them

Global-Integrated Manufacturing Configuration:Value added activities are distributed and coordinated globally

Regional Regional Uncoordinated Manufacturing Configuration:Plants are dispersed within one region and serve a single market. There is no coordination between facilities

GMC2: Regional Exporting Manufacturing Configuration:Manufacturing is focused on a region but products can reach a global market

Domestic Does not belong to international manufacturing networks as it has no transnational manufacturing operations

Home Exporting Manufacturing Configuration: Manufacturing is centralized in the home market but possesses a global logistics system

For firms seeking to upgrade within value chains, current research can provide little useful

guidance. Paradigms such as GCC/GVC identify opportunities for upgrading within a given

value chain, but provide little direction to achieve it. Manufacturing strategy research identifies

paths of development for a firm wishing to accomplish internal upgrading while International

manufacturing research describes the capabilities of networked multinational firms. Virtual

manufacturing network research holds some promise for firms from small states,but little is

known of the practices and capabilities of these organizations(Chang, Makatsoris, Richards, &

Shi, 2004). A useful approach may be to examine the practices and capabilities of such

organizations to determine what lessons they may hold for manufacturers from small states.

RESEARCH METHOD

Comparative research in development has generally taken a quantitative perspective examining

the degree and change in sophistication of exports(Hausmann, Hwang, & Rodrik, 2007; S. Lall,

1993). This approach has been criticized as superficial as it is difficult to correlate export

statistics with the capabilities of domestic firms(Barrell & Pain, 1999). While local producers

may be integrated into international manufacturing networks, their role may be in low level

activities only. For manufacturing research, a method that was capable of revealing underlying

processes was necessary. Case studies provide such an opportunity, by enabling the examination

of organizational realities, they provide a framework for building theory in a given context(C.

Voss, Tsikriktsis, & Frohlich, 2002). For this research, a comparative method was used in which

consumer goods manufacturers in two differing regions. The first was Trinidad and Tobago, a

small state in the Caribbean and the second was the Shenzen regional of china. Data was

collected on the network configuration and current practices of firms in both regions using

several tools. For the origins, archival data on the respective sector was collected and analyzed.

The network configuration and current practices were assessed using interviews with

owners/managers and observations of organizations.

FINDINGS: TRINIDAD AND TOBAGO

Located in the Caribbean, Trinidad and Tobago (TT), has a population of 1.3 million and a GDP

per capita of $17000 USD. A former British colony, it began self-government in 1956 and since

then has attempted policy interventions to build a diversified industrial sector. The result has

been mixed with the emergence of a globally competitive energy industry and a regionally

oriented sector, made primarily of import substituting firms. Each policy approach reflected the

prevailing development ideology at the time along with the particular economic circumstances of

energy exporters like TT. From 1956 to 1967, the state acted a promoter, attempting to attract

MNEs to TT. Based on the strategy of Industrialization by Invitation (Lewis, 1950), it was hoped

that these firms would bring technology and access to developed country markets. However,

these firms utilized the incentives offered by the TT government to build regionally oriented

subsidiaries and the intended outcomes were not achieved.

Supported by increasing energy revenue, TT shifted it’s stance from actively courting MNEs to

regulating their activities. From 1967 to 1986, the state became an entrepreneur, investing in a

number of industries. At the same time, a framework of import protection was established and a

number of new manufacturing operations were started. Some of these entrants converted existing

craft operations to mass production while others utilized formal (joint venture) and informal

linkages with foreign MNEs to access technology. A fall in commodity prices in 1982 led to a

deep recession in TT. With the guidance of the IMF, TT began to open its economy, dismantling

its import barriers. From 1988 to 2000, the view of FDI was changed again and the state became

a facilitator, actively marketing TT as an investment destination. Local firms were encouraged to

retool, with government support provided for improving quality, design and production.

Combined with an opening regional market, these improved firms met with success in export

markets. The petrochemical sector began growing and with increases in commodity prices,

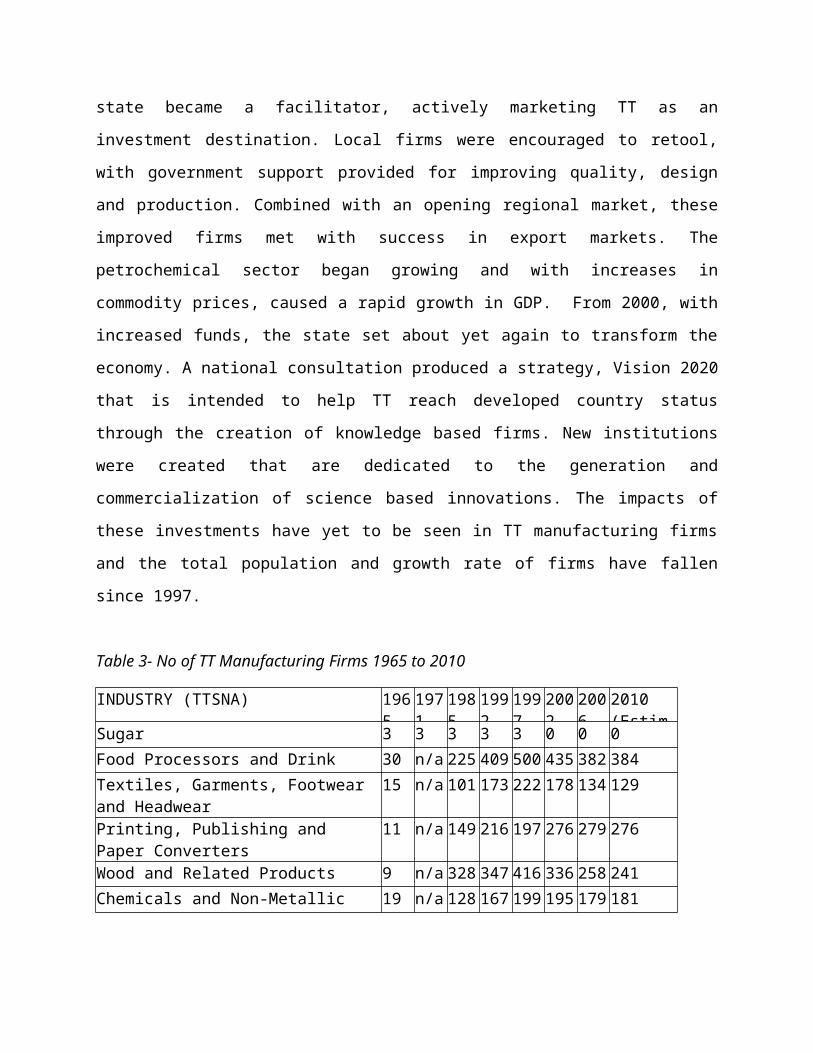

caused a rapid growth in GDP. From 2000, with increased funds, the state set about yet again to

transform the economy. A national consultation produced a strategy, Vision 2020 that is intended

to help TT reach developed country status through the creation of knowledge based firms. New

institutions were created that are dedicated to the generation and commercialization of science

based innovations. The impacts of these investments have yet to be seen in TT manufacturing

firms and the total population and growth rate of firms have fallen since 1997.

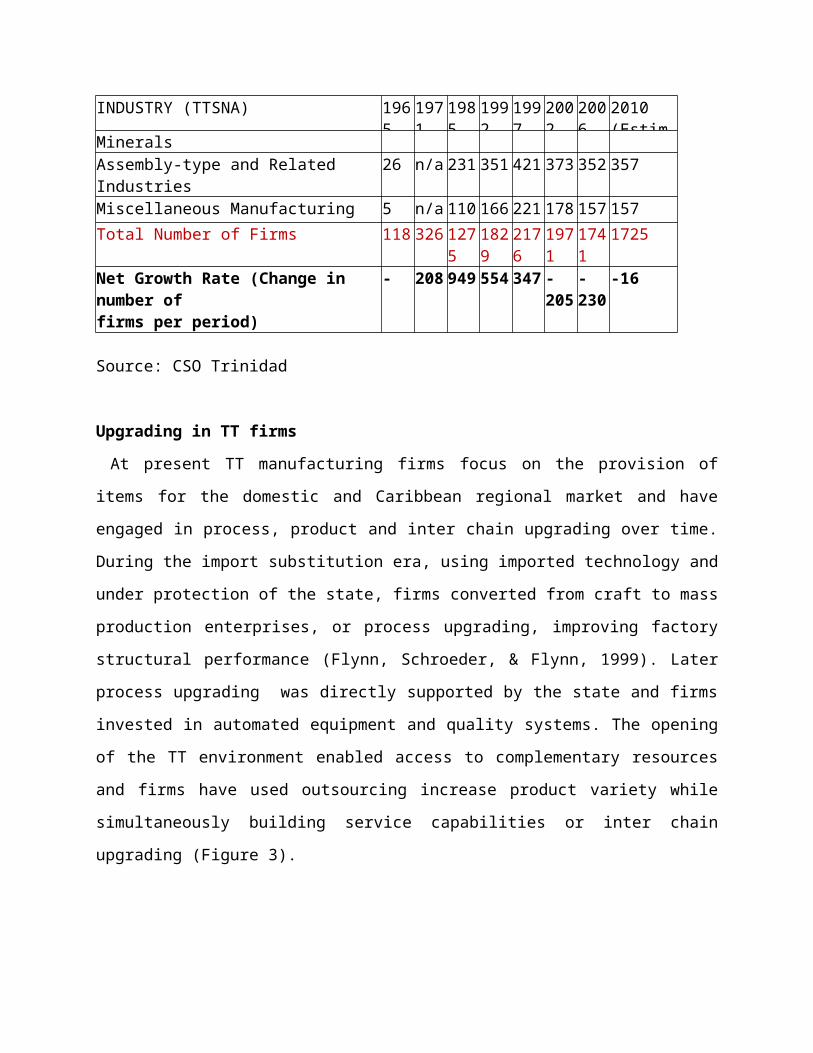

Table 3- No of TT Manufacturing Firms 1965 to 2010

INDUSTRY (TTSNA) 19651971

19851992

19972002

20062010(Estimate)

Sugar 3 3 3 3 3 0 0 0Food Processors and Drink 30 n/a 225 409 500 435 382 384Textiles, Garments, Footwear and Headwear

15 n/a 101 173 222 178 134 129

Printing, Publishing and Paper Converters 11 n/a 149 216 197 276 279 276Wood and Related Products 9 n/a 328 347 416 336 258 241Chemicals and Non-Metallic Minerals 19 n/a 128 167 199 195 179 181Assembly-type and Related Industries 26 n/a 231 351 421 373 352 357Miscellaneous Manufacturing 5 n/a 110 166 221 178 157 157Total Number of Firms 118 326 1275182

92176197

117411725

Net Growth Rate (Change in number offirms per period)

- 208 949 554 347 -205 -230 -16

Source: CSO Trinidad

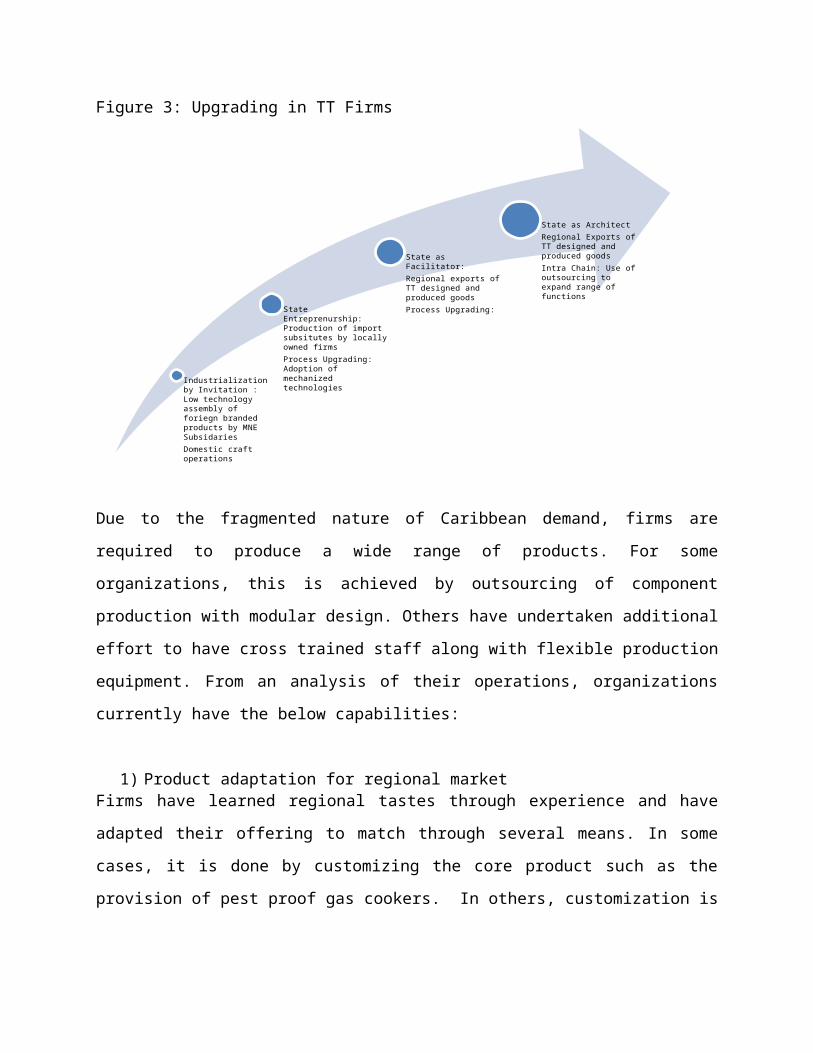

Upgrading in TT firms

At present TT manufacturing firms focus on the provision of items for the domestic and

Caribbean regional market and have engaged in process, product and inter chain upgrading over

time. During the import substitution era, using imported technology and under protection of the

state, firms converted from craft to mass production enterprises, or process upgrading, improving

factory structural performance (Flynn, Schroeder, & Flynn, 1999). Later process upgrading was

directly supported by the state and firms invested in automated equipment and quality systems.

The opening of the TT environment enabled access to complementary resources and firms have

used outsourcing increase product variety while simultaneously building service capabilities or

inter chain upgrading (Figure 3).

Figure 3: Upgrading in TT Firms

Due to the fragmented nature of Caribbean demand, firms are required to produce a wide range

of products. For some organizations, this is achieved by outsourcing of component production

with modular design. Others have undertaken additional effort to have cross trained staff along

with flexible production equipment. From an analysis of their operations, organizations currently

have the below capabilities:

Industrialization by Invitation : Low technology assembly of foriegn branded products by MNE SubsidariesDomestic craft operations

State Entreprenurship: Production of import subsitutes by locally owned firmsProcess Upgrading: Adoption of mechanized technologies

State as Facilitator:Regional exports of TT designed and produced goodsProcess Upgrading:

State as ArchitectRegional Exports of TT designed and produced goodsIntra Chain: Use of outsourcing to expand range of functions

1) Product adaptation for regional marketFirms have learned regional tastes through experience and have adapted their offering to match

through several means. In some cases, it is done by customizing the core product such as the

provision of pest proof gas cookers. In others, customization is provided by services, integrating

recycling and warranties to provide a region specific offer that importers cannot easily match.

2) Supply Relationship Management

Aided by the open economy, companies have outsourced significant sections of their product

realization process to foreign suppliers. While all organizations import raw materials, others

import components and entire units. Firms also import intellectual property in the form of

designs.

3) Demand Management

Within the region, organizations maintain close contact with their customer base since deep

customer knowledge forms the basis of their ability to adapt products for regional tastes. As

such, manufacturers prefer to sell directly to retailers within the region, resorting to distributors

as a last resort. One firm, a battery company, has extended it’s services to include reverse

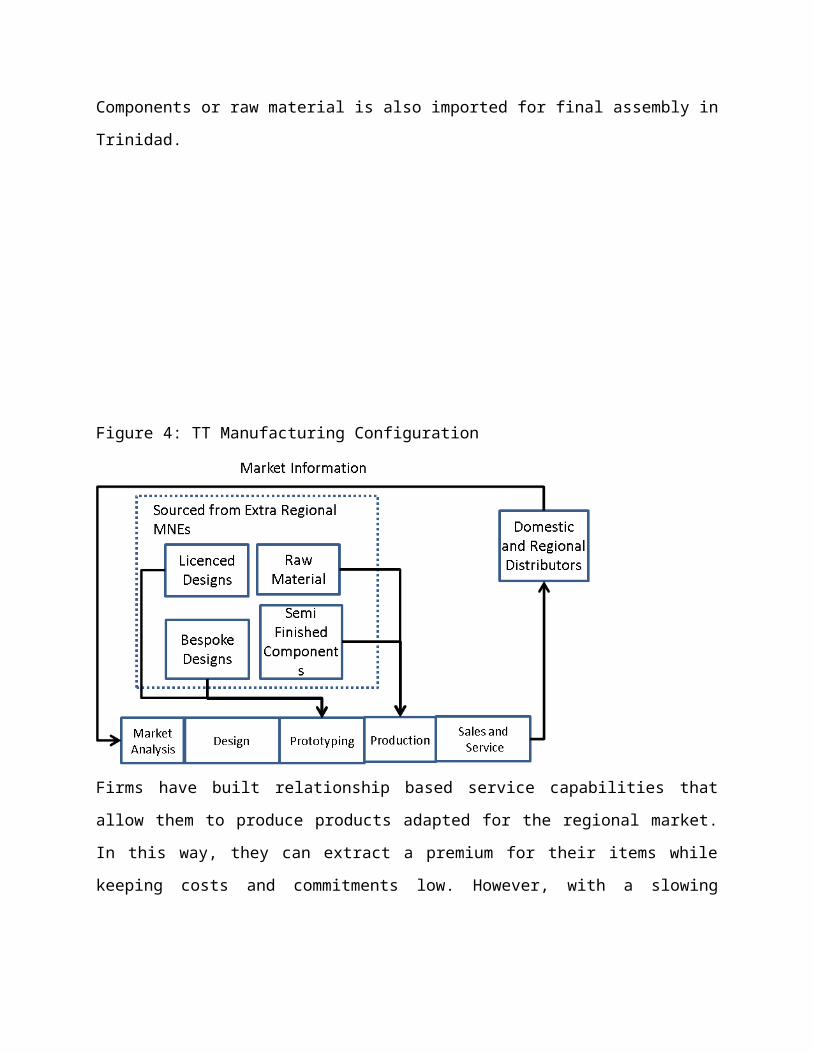

logistics, taking responsibility for the entire life cycle of its product. Figure 4 shows how TT

manufacturing system is configured. Close linkages with regional distributors provide market

information that guides product development. Firms may design products in house, import

licensed designs from MNEs or commission Bespoke designs, generally from foreign providers.

Components or raw material is also imported for final assembly in Trinidad.

Figure 4: TT Manufacturing Configuration

Firms have built relationship based service capabilities that allow them to produce products

adapted for the regional market. In this way, they can extract a premium for their items while

keeping costs and commitments low. However, with a slowing regional economy and increased

pressure from international competitors, manufacturing growth has stagnated. The state’s current

strategy of building technology driven firms may face difficulty as the organizations surveyed

lack the resources for commercialization of science based innovations. To improve local

manufacturing, it is necessary to examine a region from a developing country that has been able

to systematically upgrade without significant investments in research.

FINDINGS: SHENZHEN

Shenzhen area, the core part of PRD (Pearl River Delta) in south of China was become the world

manufacturing centre for many kinds of products like toys, MP3 players, consumer electronics

and mobile phone (Shih et al. 2010). Currently, the Shenzhen manufacturing network composing

of thousands of inter-dependent grass-root SMEs and was also being popularly called Shanzhai

manufacturing network since 2008. Shanzhai originally and literally means “mountain village” in

Chinese, here it introduced Chinese SMEs starting with producing low-cost mobile phone to

rebel against the top mobile companies by quickly adopting the emerging indigenous innovative

ideas and technology and also integrate the local manufacturing network (Zhu & Shi 2010).

However, the Shanzhai phenomenon is not brand-new since it started with China’s open reform

in 1978 by imitating and producing low-cost products including watches, VCD, DVD, MP3

players, TV. They have since grown to incorporate a significant volume of the mobile phone

market and accounted for 25% of MTK shipments in 2009 Beyond scale, it has also been

suggested that Shanzhai mobile phones are constraining the profits of established, branded

manufacturers(Agrawal 2009).

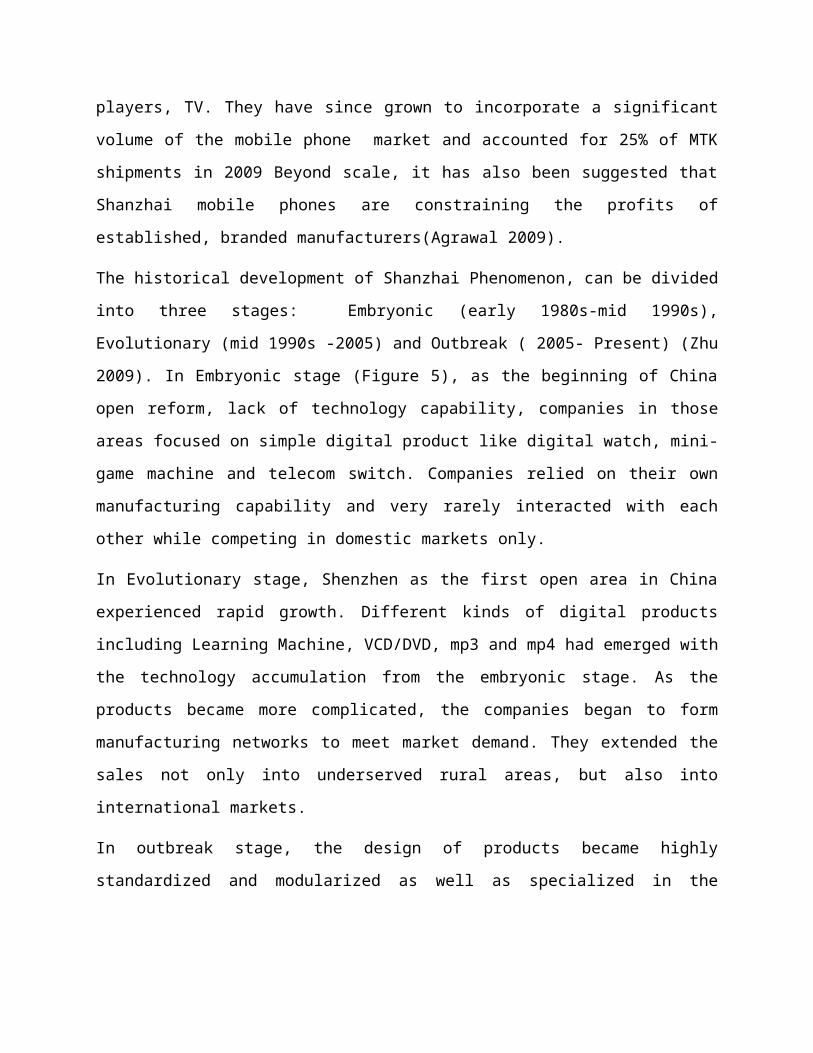

The historical development of Shanzhai Phenomenon, can be divided into three stages:

Embryonic (early 1980s-mid 1990s), Evolutionary (mid 1990s -2005) and Outbreak ( 2005-

Present) (Zhu 2009). In Embryonic stage (Figure 5), as the beginning of China open reform, lack

of technology capability, companies in those areas focused on simple digital product like digital

watch, mini-game machine and telecom switch. Companies relied on their own manufacturing

capability and very rarely interacted with each other while competing in domestic markets only.

In Evolutionary stage, Shenzhen as the first open area in China experienced rapid growth.

Different kinds of digital products including Learning Machine, VCD/DVD, mp3 and mp4 had

emerged with the technology accumulation from the embryonic stage. As the products became

more complicated, the companies began to form manufacturing networks to meet market

demand. They extended the sales not only into underserved rural areas, but also into international

markets.

In outbreak stage, the design of products became highly standardized and modularized as well as

specialized in the appearance. In order to meet those requirements, the manufacturing network in

Shenzhen area became more fragmented while increasing the ease and depth of collaboration.

The region also focused on the production of consumer electronics, with huge shipment like

mobile phone and netbooks. At this stage the Shanzhai name was adopted to describe those

digital products from local companies which are very novel, low price and highly localized,

successfully competing with international firms.

Figure 5: Shanzhai firm Evolution

Fig.1 Shanzhai development stage Source: (Zhu 2009)

Currently, there are estimated ten thousands firms in those manufacturing network including

Industrial and mechanical design, production, assembly and distribution. They maintain strong

links to distribution and retail centres including SEG Plaza, Mingtong Digital and Yuanwang

Digital Mall in Huaqiang North, the centre of Shenzhen city (Shih et al. 2010). Around 200,000

people are working within the Shanzhai manufacturing network.

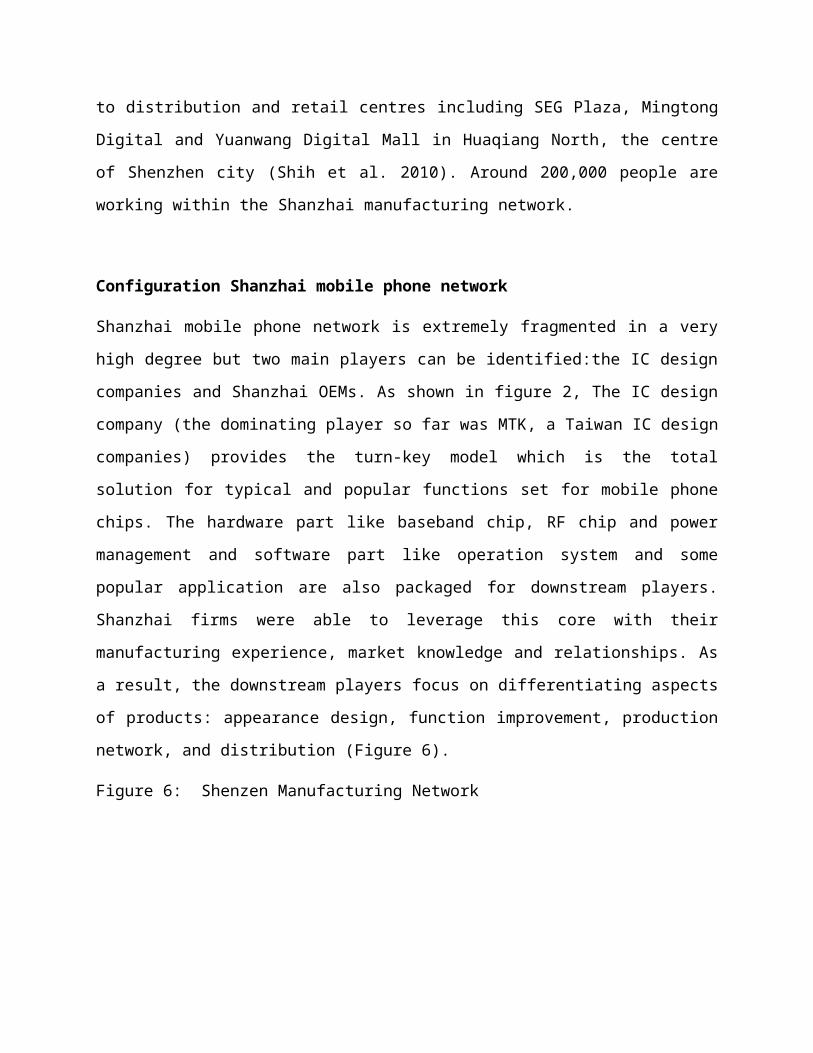

Configuration Shanzhai mobile phone network

Shanzhai mobile phone network is extremely fragmented in a very high degree but two main

players can be identified:the IC design companies and Shanzhai OEMs. As shown in figure 2,

The IC design company (the dominating player so far was MTK, a Taiwan IC design companies)

provides the turn-key model which is the total solution for typical and popular functions set for

mobile phone chips. The hardware part like baseband chip, RF chip and power management and

software part like operation system and some popular application are also packaged for

downstream players. Shanzhai firms were able to leverage this core with their manufacturing

experience, market knowledge and relationships. As a result, the downstream players focus on

differentiating aspects of products: appearance design, function improvement, production

network, and distribution (Figure 6).

Figure 6: Shenzen Manufacturing Network

Regarding to the another key role of Shanzhai network, Shan-zhai OEMs in Fig.2 coordinate the

whole manufacturing network’s cooperation and achieve rapid market responses including IC

design, ID&MD( Industrial design and Mechanical design), Casing, distributors as well as EMS

company.

Table 4: Shanzhai network players list

Players Full name BusinessMTK MediaTek Provide turnkey model as chips total solutionIDH Independent design house System design based on MTK’s turnkey model including

hardware and software part.ID&MD Industrial design and

Mechanical designFocusing on appearance design and inside mechanical design

Casing Casing model company Providing the handset shell and partEMS Electronic Manufacturing

serviceAssembly and manufacturing

Shanzhai OEM

Shanzhai Original equipment manufacturer

Coordinate all the partners inside Shanzhai network

Franchising Market distribution channel The distribution channel into 4th,5th tier market like rural area

Three Shanzhai mobile phone projects to demonstrate Shanzhai phenomenon

characteristics

So far, Shanzhai mobile phones were divided into three categories: firstly, making cell phones

novel and creative in terms of appearance and unique functions to meet specific area; secondly,

imitating the design and the function of brand cell phones with much lower price; the third one is

to paste some fashionable logo on the handset. With the unique interface and unbelievable low

price, Shanzhai mobiles were very popular and renewed with significant functions in a very

quick step. More and more market feedback was passed to MTK. MTK began to adopt the useful

information and decided to co-evolve with local players.

Three typical mobile phone projects have been studied by in-depth case study during 2008-2009

in Shenzhen area in order to demonstrate the distinguish characteristics of Shanzhai

manufacturing network.

Case 1: the pure innovative product – Belt light Mobile

This mobile was named Belt-light Mobile, which meant the lights around the frame of handset

would be shining one by one like the horse running. This kind of design was very popular in the

2008. No brand companies have designed it yet. Furthermore, in order to meet the farmers’

requirement in the remote area like rural place, this mobile phone also had 6 speakers to make it

enough volume when it got ring. Because when farmers were working, they usually place the

mobile phone far away and they need such mobile phone with strong stereo to remind him there

was a call. For the 2008 olympics game, Shanzhai OEM also made this kind of mobile phone

with big screen like 2.8 inches and TV broadcast function.

Fig.7 Belt light Mobile phone source:(Shanzhaiji website 2008)

Case 2: the imitating one: Nokic phone

Case 1 was the most representative product for Shanzhai mobile phone, which is very innovative

reflecting the local requirements with low price. However, in order to meet the requirement of

owning brand mobile phone. Shanzhai OEM also produced the imitating one as Fig.8 with 7

changes according to the Chinese regulation to protect IP in some degree. However with

innovative teamwork, the project we interviewed was just hugely copying the NOKIA E71.

Fig.8 Shanzhai Nokia Source: interview

Seen from the Fig.7 we got from the ID&MD company serving for this project, the manager told

us it was very easy to imitate brand mobile phone if they saw the original picture. In this project,

they changed name Nokia to Nokic, slightly changed the chamfer angle of four side of handset

shell, the thickness of handset, the central button of keyboard and so on. Besides industrial

design for appearance, the mechanical design should adapt with chips board size and other

peripherals like camera, stereos, microphone. However, mechanical design was very flexible as it

was un-visualized for customers. The price of this mobile was a little higher than that in Case 1,

because it would take more times to imitate the brand mobile phone.

Case 3: the brand copy one: LV phone

The product in Case 3 as Fig.8 was the combination of the original design and some famous

logo. In this project we interviewed, they produced LV phone to meet those fashionable fans.

Besides LV logo, all part of this phone was designed by local ID&MD company. This Shanzhai

OEM brought the ideas from local people’s favour on LV brand. Besides this, we also found

there were also some similar designs in the market. The sales record reminded us people like

those fashionable phone with some famous logo on them. However, this kind of mobile phone

was definitely illegal if sold on the international market due to the unauthorized usage of the LV

brand.

Fig.9 Shanzhai phone with fashionable logo

Cross Cases Comparison

Those three cases already demonstrated the typical three products in the Shanzhai market. Tab.2

compared those three cases in several dimensions including technology, design, popularity,

casing, price and mainstream. In technology side, they use similar technology like MTK chips,

those kinds of IDH system design. Specifically in ID&MD level, Case 1 used original design

similar to Case 3, while Case 2 was imitating the brand mobile phone. So in that way, the casing

model process was slightly complicated and lead-time was slightly longer for Case 2. The

product in Case 2 was most popular than the other two cases. Regarding to IP issues, products in

Case 1 was exporting many to international market, followed by Case 2, and Case 3. Case 2

product was of highest price comparing with other two, because its design and longer lead-time.

Tab.5 Cross cases comparisonCase 1 Case 2 Case 3

Technology Hardware: MTKSoftware: IDHDesign: local

Hardware: MTKSoftware: IDHDesign: local

Hardware: MTKSoftware: IDHDesign: local

ID+MD Original design by embedding local factors

Copying with seven place different

Original design with famous logo

Casing Easy High requirement EasyPopularity Normally, popular in

occasionsVery popular Popular

distribution Expansion to 5th tier market, rural area and big international export

Expansion to 5th tier market, rural area and some international export

Expansion to 5th tier market, rural area

Price(GBP) 30-40 50-60 40-50Lead time Normally Slightly longer NormallyMainstream

Yes Less Not at all

The above examples provide an overview of Shanzhai manufacturing characteristics:

Market Driven Design bottom-up idea emerged within local market, Shanzhai OEM put many

new functions and ideas into the final design like: six stereo, big screen, TV, double SIM cards

and so on.

Flexible and visual collaboration- all the players in the Shanzhai network was coordinated by

Shanzhai OEMs, who make the information transparent and easy to share through the supply

chain’s channel.

Fast decision marking- Shanzhai OEMs make the mobile phone updating in very short term

about three months. So they began to make the decision as fast as possible in order to capture

with local market information change.

Transaction in currency- in order to shorten the very process, Shanzhai network like to use

currency to do transaction.

Low-cost business model- they lead the good-enough idea but also make the mobile phone

diversity. Their strategy was to start with low-level product but approach the high level product

like brand mobile phone companies.

As well as some weak points:

Some IP issues- there are still some mobile phone imitating the brand mobile phone and also use

the brand logo as well.

Some quality control side- Testing process was normally shortened by the Shanzhai mobile

which let the mobile phone not very reliable. However, Shanzhai phone was proposed to meet

the people with low level live condition at bottom of pyramids (Prahalad & Hart 1999).

Shanzhai firms are also seeking to build on their advantages by borrowing the tools and tech-

niques of the open source movement(Lakhani & von Hippel, 2003). Firms are adopting the

Google Android software (Eiman, 2009) to power their creations and they are currently develop-

ing an online communication community as an alternative to existing marketplaces for applica-

tions. Firms are also exploring establishing production facilities in other emerging markets, inter-

nationalizing the Shanzhai system.

Manufacturing Systems Compared

TT and Shanzhai firms share a focus on adapting products for fragmented markets and through

factory and network configurations, they produce a high variety of products with short

production runs. Firms also attempt to maintain direct contact with end users as they provide

useful data for new features that enable differentiation from imports. However, while TT firms

are limited to the Caribbean, Shanzhai firms have been able to tap into demand for low cost

products worldwide. This has been accomplished this through a combination of inter chain,

product and process upgrading.

Over time, they have moved from digital watches to DVD players, to mobile phones and tablets,

building positions in entirely new industries. Within the mobile phone industry, they have been

producing successively more complex products as they attempt to meet evolving customer needs.

To do so, they have had to master new technologies and production techniques, or process

upgrading. By contrast, TT firms have largely remained within their industries of origin, making

incremental product and process adjustments. The outcome is dramatic, with a highly localized

production network, Shanzhai firms can design, produce and deliver items rapidly. Table 6

compares a typical production cycle:

Table 6 Operational Practices ComparedShanzhai TT

Activity Time Practice Time TT FirmCore Sys-tem Design

Day 1-3

Normally, IDH will deliver core system design based on MTK solu-tion to Shanzhai OEM’s

Month 1-3 month

Based on product, firm creates concept, licenses design or commissions design from partnerFirm generates designs internally or sends brief to foreign partner.

Detail De-sign

Day 3-10

In the same time, Shanzhai OEM also contact with ID+MD company (industry design and mechanism design), and also this company take the responsibility to make the first model for the new mobile phone. This will takes 10 days

Production Day 11-15

Shanzhai OEM will coordinate ID+MD company, IDH, casing companies and EMS company to fi-nally confirm the production plan. Finally, shanzhai OEM will initiate sufficient production to cover costs (minimum 20000). If sales are good, more items will be comis-sioned

Month 3-9

Select supplier for com-ponents and sub-assem-blies. Schedule and exe-cute internal production

Case and Accessory Production

Day 15-26

Casing supplier builds items and shanzhai OEM also purchase all the accessories of mobile phone and then deliver to EMS company to as-sembly and test.

Assembly Day 27-28

EMS assembly them only takes 1-2 days

Month 9-10

Assemble in Internal Fa-cility

Distribution Day 28

Then distribute to agency in the 4th

tier and 5 tier until rural area.Month 11-12

Distribute in Caribbean Region

Both TT and Shanzhai firms manage virtual production networks with relational governance

structures. Linkages with retailers and distributors guide product development by providing

detailed information on customer requirements. However, domestic supply relationships enable

the disaggregation of production by Shanzhai firms into small segments, allowing them to act as

project driven organizations.

DISCUSSION AND CONCLUSION

It is fitting that an island that was among the first to be involved in global commodity chains

should draw lessons from an even older civilization for building competitive manufacturing

enterprises. In both cases, the state intervened as a means of achieving rapid industrialization but

while the Shanzhai manufacturers have been able to achieve systematic upgrading, producing

items of increasing complexity, TT firms have not. Unlike many developing country firms,

Shanzhai firms occupy a primary role in international commodity chains. This position is

enabled by the availability of a sophisticated domestic supply base, a spillover from China’s

success in attracting electronic industry FDI (Liu & Shu, 2003). This has supported firms

evolution to a project based operation mode as they are able to rely on nearby local firms for

intangibles such as process and product design. Outsourced activities are managed through

actor networks and the community places a premium on data exchange, sharing designs and

techniques. By evolving a distinct community of practice in manufacturing, they have built a

self-renewing capacity for indigenous upgrading.

Overall, Shanzhai firms suggest a development path based on Knowledge (skills, relationships)

rather than property (patents, licenses) based resources(Miller & Shamsie, 1996). Presently, TT,

like many other countries, intends to create knowledge based entrepreneurial organizations in

targeted areas of manufacturing, Biotech, IT and Creative industries. A target for research

spending has been set at 2% of GDP in 2020, based on the current outlay by developed countries,

a tenfold increase on the 2004 figure (Vision2020, 2005). However, developed and developing

countries have adopted different approaches to growing knowledge intensive firms. The former

have implemented support measures for all aspects of the commercialization process: product,

process and organizational innovation (Borras, 2009). By contrast, developing country

policymakers focus only on product innovation (Sanjaya Lall & Teubal, 1998) with support

measures for R&D driven development (Hadjimanolis & Dickson, 2001). Domestic institutional

weaknesses in these countries limit the state’s ability to enforce property rights, a key enabler of

technology based innovation(Freeman, 1995), making success of this strategy doubtful.

A systemic approach that is cognizant of domestic realities is needed and lessons from the

Shanzhai firms may help craft an approach better suited to the Small state environment. A focus

on building a domestic supply base along with stronger linkages between firms can support rapid

product development. Trinidad is also home to a competitive energy cluster and developing inter

sector linkages may aid manufacturing firms’ upgrading. While their appropriation of foreign IP

has caused some concern to competitors, Shanzhai production capabilities support the creation of

unique solutions for low cost markets. Current developments in open source software and

hardware may also soon reduce the need for direct copying, and distinct brands may emerge over

time.

REFERENCES

Bair, J., & Gereffi, G. (2003). Upgrading, uneven development, and jobs in the North American apparel industry. Global Networks, 3, 143-169.

Barnes, J., Bessant, J., Dunne, N., & Morris, M. (2001). Developing manufacturing competitiveness within South African industry: the role of middle management. Technovation, 21(5), 293-309.

Barrell, R., & Pain, N. (1999). Domestic institutions, agglomerations and foreign direct investment in Europe. [Article]. European Economic Review, 43(4-6), 925-934.

Borras, S. (2009). The Widening and Deepening of Innovation Policy: What Conditions Provide for Effective Governance? : CIRCLE (Centre for Innovation, Research and Competence in the Learning Economy), Lund University.

Brookfield, J., & Ren-Jye, L. (2005). The Internationalization of a Production Network and the Replication Dilemma: Building Supplier Networks in Mainland China. Asia Pacific Journal of Management, 22(4), 355-380.

Chang, Y. S., Makatsoris, H. C., Richards, H. D., & Shi, Y. (2004). A Roadmap of Manufacturing System Evolution Evolution of Supply Chain Management (pp. 341-365): Springer US.

Demas, W. G. (1978). The Caribbean and the New International Economic Order Journal of Interamerican Studies and World Affairs, 20(3), 34.

Downes, A. S. (2004). Arthur Lewis and Industrial Development in the Caribbean: An Assessment. Paper presented at the The Lewis Model after 50 years: Assessing Sir Arthur Lewis’ Contribution to Development Economics and Policy. from http://www.sed.manchester.ac.uk/research/events/conferences/arthurlewispapers.htm

Easterly, W., & Kraay, A. (2000). Small States, Small Problems? Income, Growth, and Volatility in Small States. World Development, 28(11), 2013-2027.

Eiman, K. (2009). MobSens: Making Smart Phones Smarter, 8, 50-57.Farrell, T. (1980). Arthur Lewis and the Case for Caribbean Industrialisation. . Social and Economic

Studies, 29(4), 52-75.Flynn, B. B., Schroeder, R. G., & Flynn, E. J. (1999). World class manufacturing: an

investigation of Hayes and Wheelwright's foundation. Journal of Operations Management, 17(3), 249-269.

Freeman, C. (1995). The 'National System of Innovation' in historical perspective. Camb. J. Econ., 19(1), 5-24.

Gereffi, G. (1999). International trade and industrial upgrading in the apparel commodity chain. Journal of International Economics, 48(1), 37-70.

Gereffi, G. (2001). Beyond the Producer-driven/Buyer-driven Dichotomy The Evolution of Global Value Chains in the Internet Era. IDS Bulletin, 32(3), 30-40.

Gereffi, G. (2005). Export-Oriented Growth and Industrial Upgrading : Lessons from the Mexican Apparel Case 1 A case study of Global Value Chain analysis. 1-18.

Gereffi, G., Humphrey, J., & Sturgeon, T. (2005). The governance of global value chains. Review of International Political Economy, 12(1), 78 - 104.

Hadjimanolis, A., & Dickson, K. (2001). Development of national innovation policy in small developing countries: the case of Cyprus. Research Policy, 30(5), 805-817.

Hausmann, R., Hwang, J., & Rodrik, D. (2007). What you export matters. Journal of Economic Growth, 12(1), 1-25.

Henrikson, A. K. (1999). Small States in World Politics Paper presented at the Conference on Small States

Hill, T., & Westbrook, R. (1997). The strategic development of manufacturing: Market analysis for investment priorities. European Management Journal, 15(3), 297-302.

Kim, Y., & Lee, J. (1993). Manufacturing strategy and production systems: An integrated framework. Journal of Operations Management, 11(1), 3-15.

Klak, T. (1995). A Framework for Studying Caribbean Industrial Policy Economic Geography, 71(3), 297-317.

Lakhani, K. R., & von Hippel, E. (2003). How open source software works: "free" user-to-user assistance. Research Policy, 32(6), 923-943.

Lall, S. (1993). Promoting technology development: the role of technology transfer and indigenous effort. Third World Quarterly, 14(1), 95.

Lall, S., & Teubal, M. (1998). "Market-stimulating" technology policies in developing countries: A framework with examples from East Asia. World Development, 26(8), 1369-1385.

Leslie, D., & Reimer, S. (1999). Spatializing commodity chains. Progress in Human Geography, 23(3), 401-420.

Lewis, A. W. (1950). The industrialization of the British West Indies. Caribbean Economic Review, 2(May), 1-39.

Liu, X. H., & Shu, C. (2003). Determinants of export performance: Evidence from Chinese industries. [Article]. Economics of Planning, 36(1), 45-67.

Michael, T. (2004). Transportation Effectiveness and Manufacturing Firm Performance. The International Journal of Logistics Management, 15(2), 31 - 50.

Miller, D., & Shamsie, J. (1996). The Resource-Based View of the Firm in Two Environments: The Hollywood Film Studios from 1936 to 1965 The Academy of Management Journal, 39(3), 519-543.

Pantin, D., Sandiford, W., & Henry, M. (2002). Cake, Mama Cocoa or ?: Alternatives facing the Caribbean Banana Industry. In K. Nurse (Ed.), Caribbean Economies and Global Restructuring (Vol. 1, pp. 47-87). Kingston: Ian Randle Publications.

Payne, A., & Sutton, P. (2001). Dr Eric Williams and the National Development State in Trinidad and Tobago. In A. Hennessy & G. Heuman (Eds.), Charting Caribbean Development (Vol. 1, pp. 30-64). London: Macmillan Education.

Platts, K. W., & Gregory, M. J. (1990). Manufacturing Audit in the Process of Strategy Formulation. International Journal of Operations & Production Management, 10(9), 21.

Sahay, R., Robinson, D. O., & Cashin, P. (2006). Overview. In R. Sahay, D. O. Robinson & P. Cashin (Eds.), The Caribbean: From Vulnerability to Sustained Growth (Vol. 1, pp. 1-13). Washington, D.C.: International Monetary Fund.

Secretariat, C. C. (2007). www.Caricomstats.org Retrieved 19/11/2008, 2008Shi, Y., & Gregory, M. (1998). International manufacturing networks--to develop global

competitive capabilities. Journal of Operations Management, 16(2-3), 195-214.

Shi, Y., & Gregory, M. (2005). Emergence of global manufacturing virtual networks and establishment of new manufacturing infrastructure for faster innovation and firm growth. Production Planning & Control, 16, 621-631.

Skinner, W. (1969). Manufacturing: missing link in corporate strategy. Harvard Business review(May- June).

Slack, N., Lewis, M., & Bates, H. (2004). International Journal of Operations & Production Management. The two worlds of operations management research and practice: Can they meet, should they meet?, 24(4), 16.

Tain-Jy, C., Homin, C., & Ying-hua, K. (2004). Foreign direct investment and local linkages. Journal of International Business Studies, 35(4), 320-333.

Taylor, P. J. (1988). World Systems Analysis and Regional Geography. The Professional Geographer, 40(3), 259 - 265.

Tewari, M. (2006). Is Price and Cost Competitiveness Enough for Apparel Firms to Gain Market Share in the World after Quotas? A Review. Global Economy Journal, 6(4), 1-46.

Thomas, R., Ian, F., Wilkinson, W., & Johnston, J. (2002). Measuring network competence: some international evidence. Journal of Business & Industrial Marketing, 17(2), 119 - 138.

Vision2020 (2005). Vision 2020 Sub-Committee on Science, Technology and Innovation.Vonortas, N. S. (2002). Building competitive firms: technology policy initiatives in Latin

America. Technology in Society, 24(4), 433.Voss, C. (1995). Paradigms of Manufacturing Strategy. International Journal of Operations and

production management, 15(4).Voss, C., Tsikriktsis, N., & Frohlich, M. (2002). Case research in operations management.

International Journal of Operations & Production Management, 22(2), 24.Wallerstein, I. (2000). Globalization or the Age of Transition? International Sociology, 15(2),

249-265.Ward, P. T., Bickford, D. J., & Leong, G. K. (1996). Configurations of manufacturing strategy,

business strategy, environment and structure. Journal of Management, 22(4), 597-626.Wheel Wright, S. C. (1984). Manufacturing strategy: Defining the missing link. Strategic

Management Journal, 5(1), 77-91.Wheelwright, S. C. (1984). Manufacturing Strategy: Defining the Missing Link. Strategic

Management Journal, 5(1), 77-91.