Embed Size (px)

DESCRIPTION

gfgghhfhgf

Citation preview

Ai-Abbas Suger Mills Limited: A CaseStudey by Amna Qadir

From reports1 (reports)

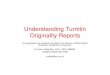

Processed on 20-Jun-2014 16:52 PKTID: 435836658Word Count: 6279

Similarity Index

18%Internet Sources: 18%Publications: 0%Student Papers: N/A

Similarity by Source

1

2

3

4

Turnitin Originality Report

sources:

8% match (Internet from 21-Mar-2014)http://aasml.com/governance.php

5% match (Internet from 21-Mar-2014)http://aasml.com/plants.php

4% match (Internet from 21-Mar-2014)http://aasml.com/profile.php

2% match (Internet from 20-Apr-2012)http://www.aasml.com/accounts/Al-AbbasSugarAnnual2010Final.pdf

paper text:“ Al – Abbas Sugar Mills Limited: A Case Study ” By Amna Qadir Student of MBA – 3.5Yrs (Finance),COMSATS Institute of Information and Technology, Abbottabad. [email protected] Project SupervisorMr. Zaheer Ahmed Swati Lecturer Accounting, COMSATS Institute of Information and Technology,Abbottabad. [email protected] Department of Management Sciences COMSATS Institute ofInformation and Technology, Abbottabad. “ Al – Abbas Sugar Mills Limited: A Case Study ” Chapter – 1: ?INTRODUCTION: 1.1. Brief of Sugar: th Pakistan is the 5 largest country in the world in terms of area undersugarcane cultivation, th th 11 by production and 60 in yield (Shaukat). Sugarcane is the primary rawmaterial for the production of sugar. Sugar is one of the most essential commodities used in every houseand it also plays a significant role in the diet of human beings. Sugar is the most widely used form ofcarbohydrates. 1.2. Sugar Manufacturing Process: Sugar exists in various forms and may be utilized fromdifferent sources in nature. It can be produced by many sources like sugarcane, sugar beet, maple palm,coconut and apple, but the most convenient for production on large scale and considerable quantities is thesugarcane and sugar beet (Memon). Thus, like many other countries all over the world, sugarcane is themajor source of production of sugar in Pakistan. The process for sugarcane refining after its cultivationinvolves the following stages: ? Pressing of the sugarcane to extract the juice. ? Boiling this extracted juiceuntil it begins to thicken and sugar begins to crystallize. ? Spinning the crystals in a centrifuge to remove thesyrup, producing raw sugar. ? Refining the raw sugar by washing and filtering to remove remaining non-sugaringredients and color. ? Crystallizing, drying and packaging the refined sugar. 1.3. Significance of the study:

Turnitin Originality Report https://www.turnitin.com/newreport_printview.asp?eq=0&eb=0&esm=-2...

1 of 16 25-Jun-14 6:26 PM

There is not much evidence of work done in sugar industry in Pakistan. This project is an attempt tocontribute to the study on Al-Abbas Sugar Mills Limited. The broad objective of this study is to analyze thecompany’s financial data since its inception, whereas the specific objectives of the study include analyzingthe data using various financial techniques including the horizontal and vertical analysis. Besides, analysisof the variables in terms of measures of central tendency and dispersion, correlations and line graphs helpanalyze the major shifts in the data. The results of this study can be used by the public and private sectors.The authorities concerned can use the results for taking special steps to improve future production. Also, theadvisors, researchers and scholars can use the findings of the study for future refinement. 1.4. Breakdownof the study: An overview of the global scenario followed by the industry and company profile is given inChapter-2. The next chapter quotes the products and services offered by Al-Abbas Sugar Mills Limited.Chapter-4 describes the best practices observed by the company in accordance with the code of corporategovernance. Financial analysis including methodology, descriptive statistics, data analysis using variousfinancial techniques, swot analysis and comparison of the company with the industry leading to limitations ofthe study and recommendations are described in Chapter-5. Fig 1.1 Process of the Case Study SugarSector Industry Overview Data Collection Selection of Company Data Processing Data Analysis andInterpretation Recommendations Chapter – 2: ? THEORETICAL REVIEW : 2.1. Global Scenario: Theinternational trade in sugar has changed dramatically over the past fifty years. Sugar is imported or exportedin huge quantities all around the world and has become an integral component of the economic relationshipsamong nations. Because of that unique position, the trade in sugar has been affected by a wide range ofdifferent forces, including global politics, health consciousness, the emergence of developing nations assuppliers and consumers, and many others. Sugar is mainly produced from two sources, Sugarcane andBeet. The costs of producing sugar from sugarcane are lower with respect to processing the sugar beets.The world market price has historically been one of the most volatile of all commodity prices because of theresidual nature of the world market (M.Ammar Arif Nakhuda, 2010). The global sugar market is alsoexperiencing a scenario of sugar deficit, as production has failed to meet the consumption. Consumption isalso expected to increase in the global sugar market, thus creating a balance in the global sugar scenario.With global oil prices remaining firm, significant amount of sugarcane diversion may happen for ethanolproduction, which will hamper sugar production (Malu, 2007). 2.2. Sugar Industry in Pakistan: After Textiles,the sugar industry is the second largest agro based industry in Pakistan. The share of sugar industry invalue added of agriculture and GDP are 3.2 percent and 0.7 percent respectively (Saeed, 2013). PakistanSugar Mills Association (PSMA) has 83 sugar mills of Pakistan listed province vise. Among these 83 namesof Sugar Mills listed on their website, 45 are located in Punjab, 30 in Sindh and 8 in KPK (Pakistan SugarMills Association, Islamabad, 2011). 2.3. Production of Sugar in Pakistan: Sugarcane is grown on around amillion hectares and provides the raw material for Pakistan’s 83 sugar mills. These 83 mills have thecapacity to produce 7.0 million tons of sugar but since the per hectare production of sugar in Pakistan is60th probably the lowest in world because of using ancient technology, Pakistan produces only 3 to 3.5million tons sugar on average. In Pakistan, the sugar is mainly produced as molasses which is the lessrefined forms of sugar and the sugar produced by the sugar mills owned by organized players of the industry.2.4. Background of Al-Abbas Group: Al-Abbas Sugar Mills Limited is a member of a group of companiescalled Al-Abbas Group. (Al-Abbas Sugar Mills Limited, 2012) The group has made an impression on thesugar, industrial alcohol, fiber board, alloys industry as well as leaving an incredible mark on the sugarindustry. The Al-Abbas Group includes the following: ? Al-Abbas Sugar Mills Limited. ? Al-Abbas IndustriesLimited. ? Al-Abbas Cement Industries Limited. ? Javedan Cement Company Limited. 2.5. CompanyAnalysis:

Turnitin Originality Report https://www.turnitin.com/newreport_printview.asp?eq=0&eb=0&esm=-2...

2 of 16 25-Jun-14 6:26 PM

3Al-Abbas Sugar Mills Limited is a progressive company that was

incorporated in May, 1991. The shares of the Company were listed onApril, 1992 at the Karachi Stock Exchange (Guarantee) Limited.

Soon

3after its incorporation the company stood on sound financial and

operational footings that paved the way for its future growth.

Al-Abbas Sugar Mills Limited has two established units. One unit is located at Mirwah Gorchani, TalukaMirpukhas and the other at Dhabeji Thatta. The unit at Mirwah Gorchani, Taluka Mirpukhas has

3sugarcane crushing capacity of 7,500 tons per day and its capacity of

processing molasses into quality industrial alcohol is about 170,000 liters per

day. The Company has also installed 6 MW power plants to cater power

requirement of sugar and distillery unit at the

same location. 4 While the unit

3at Dhabeji Thatta has 15 MW captive power coal fired plant and has

capacity to manufacture 27,220 M.T of different alloys per annum. The tankterminal unit of the company which is located at Kemari Karachi has the

storage capacity of 34,900 M.T of liquids.

It began to produce sugar in 1994. The industrial alcohol production was started

3in 2000, alloys in 2005 and power generation in 2010.

(Al-Abbas Sugar Mills Limited, 2012) The company installed its highly developed ethanol plant in the year2000. Another major accomplishment for the company was the successful installment of the ethanol distilleryreflecting

2the company’s belief in calculated expansion and diversification by

expanding its real financial strength and its ability.

Turnitin Originality Report https://www.turnitin.com/newreport_printview.asp?eq=0&eb=0&esm=-2...

3 of 16 25-Jun-14 6:26 PM

Granulated white sugar of high commercial value is produced by the company that

3has a definite edge in the market. The company became one of the only

three sugar mills in Pakistan

in 1997-98, that produced sugar according to the international quality standards in all respects. Fine alcoholof good quality and reputation

3is being exported to Europe, Japan, UAE, Saudi Arabia and Philippine.

The company ventured into inorganic growth by acquiring Al-Abbas Industries Limited in 2007 as part of thecompany’s strategic planning. It produces

3various types of alloys product to meet the whole country’ s demand.

Eventually, the Al-Abbas Sugar Mills Limited was amalgamated with the Al-Abbas Industries Limited. TheCompany is concerned about preserving the

3environment and well aware of its Corporate Social Responsibility. In

order to achieve this objective, a waste water treatment plant wasinstalled in 2001

3making significant contribution towards the economy of the sugar plant.

The Management of the Company bears a special interest in improving the

social conditions of its employees and residents around the plant with

evident concern for environment.

The company does so by investing

3in several social projects including establishing a primary school that offers

good quality education at nominal cost, financial support on a continuous

basis to a foundation to develop and maintain a school and medical complex

that spreads over 20 acres.

Turnitin Originality Report https://www.turnitin.com/newreport_printview.asp?eq=0&eb=0&esm=-2...

4 of 16 25-Jun-14 6:26 PM

2.5.1.

4Vision: “Al-Abbas Sugar Mills Limited is committed to earn reputation of

a reliable manufacturer and supplier of good quality white sugar,industrial alcohol, calcium carbide, and alloys in local and internationalmarkets.” 2.5.2. Mission: ? To be a profitable organization and to meet the

expectation of all stakeholders. ? To become competitive in local and

international markets by concentrating on quality of core products. ? Topromote best use and development of human resources in a safeenvironment, as an equal opportunity employer. ? To use advancetechnology for efficient and cost effective operations.

2.5.3. Objective: The company’s objective is to improve in manufacturing, selling and distribution of highquality sugar in Pakistan, provide leadership to drive new business and to position the company at theforefront of the sugar industry. Al-Abbas Sugar Mills Limited’s financial objectives focus on achievingacceptable profitability in pursuit of its vision and mission, long-term health and its ultimate survival. 2.5.4.Business Profile: The Company's fortunes soared as a result of the impact of sound financial policies,advanced technology, innovative approach and

3production planning combined with creative marketing and management

strategies,

3and from the perspective of profitability as well as overall corporate

image, the Company was firmly placed in a distinct position in the industry.

(Al- Abbas Sugar Mills Limited, 23rd Annual Report, 2013) CRUSHING CAPACITY of Mirwah Gorchani 7,500M.Ton sugarcane per day HEAD

4OFFICE 2nd Floor, Pardesi House, Survey No. 2/1, R.Y. 16, Old Queens

Road, Karachi - 74000 Tel: (+92-21) 111-111-224 Fax: (+92-21) 32470090

FACTORIES / LOCATION

41. Mirwah Gorchani, Distt. Mirpurkhas, Sindh 2. Main National Highway,

Dhabeji, Sindh

Turnitin Originality Report https://www.turnitin.com/newreport_printview.asp?eq=0&eb=0&esm=-2...

5 of 16 25-Jun-14 6:26 PM

3. Oil Installation Area, Kemari, Karachi, Sindh BOARD OF DIRECTORS MR. MUHAMMAD IQBAL USMANChairman

1MR. SHUNAID QURESHI Chief Executive Officer MR. ASIM GHANI Executive

Director MR. ZUHAIR ABBAS Chief Financial Officer COMPANY SECRETARY

MR. ZUHAIR ABBAS

MANAGEMENT TEAM MR. SAYYED RAFAY AKBER RASHDI Chairman Audit Committee MR. TARIQ IQBALSecretary of Internal Audit MR. DURAID QURESHI Head of Human Resource and Remuneration MR. TAHIRHUSSAIN MEMON

1Head of Procurement MR. GHULAM MUHAMMAD SOOMRO General Manager

Plant Mirwah MR. ARIF HUSSAIN General Manager Production Mirwah MR.

GHULAM AKBER General Manager Cane Mirwah MR. UMER BOZDAR General

Manager Mechanical Mirwah MR. AVES COACHINWALA General Manager

Operation Dhabeji

AUDITORS HAROON ZAKARIA & CO. Chartered Accountants ? PRODUCTS AND SERVICES: Products andServices of Al-Abbas SM Ltd 3-1 Bagasse Services Al-Abbas Sugar Mills Limited Ferro Alloys White RefinedSugar Ethanol Molasses 3.1. Products: Al-Abbas Sugar Mills Limited yields the following products during itsproduction and manufacturing of sugar: 3.1.1.

2White Refined Sugar: White refined sugar is the most odorous form of

sugar, produced from sugarcane. At harvest time, farmers cut off the

sugarcane and transport them to a sugar processing plant to be pressed.The flavor of white refined sugar is relatively neutral, making it a popularchoice for baking and sweetening drinks.

3.1.2.

2Molasses: Molasses is a thick, brown to deep black, honey-like

substance made when cane or beet sugar is processed. Molasses hassomewhat more nutritional value than white or brown sugar. It is usedprimarily in alcohol and food items.

3.1.3.

Turnitin Originality Report https://www.turnitin.com/newreport_printview.asp?eq=0&eb=0&esm=-2...

6 of 16 25-Jun-14 6:26 PM

2Ethanol: Ethanol, also called ethyl alcohol, pure alcohol, grain alcohol, or

drinking alcohol, is a volatile, flammable, colorless liquid. It is

2one of the oldest recreational drugs, best known type of alcohol found in

alcoholic beverages, it is also used in thermometers, as a solvent, and asa fuel. In common usage, it is often referred to simply as alcohol or spirits.

3.1.4. Bagasse: Bagasse is the fibrous matter that remains after sugarcane

stalks are crushed to extract their juice. It is currently used as a biofueland in the manufacture of pulp and paper products and buildingmaterials. 3.1.5. Ferro Alloys: Calcium carbide is produced industrially in

an electric arc furnace from a mixture of lime and coke at approximately2000 °C,

used since

21888. Pure calcium carbide is a colorless solid. Calcium carbide is used

in carbide lamps.

2Ferrosilicon is used as a source of silicon.

2Ferrosilicon is a basis for manufacturing of pre-alloys like magnesium

ferrosilicon (FeSiMg), used for modification of melted malleable iron. 3.2.

Services:

3.2.1 Tank Terminals: The storage tank terminals of Al-Abbas Sugar Mills Limited earned a profit of Rs. 9.716million during the year 2012. It has extensive terminals located at

2Oil Installation Area, Kemari, Karachi and covered operations of 5,700

square foot

2that comprises of 12 tanks having aggregate storage capacity of 34,920

Turnitin Originality Report https://www.turnitin.com/newreport_printview.asp?eq=0&eb=0&esm=-2...

7 of 16 25-Jun-14 6:26 PM

M.T and is capable of having storage of all types of chemical and

dangerous goods. The tanks are

2fitted with overfilled alarm and equipped with pigging system.

The company is currently handling the cargo of its various clients and the company itself. 3.2.2.

2Warehouse: The Company has warehouse facility having 45,000 square

feet capacity located at Dhabeji. The proximity of the warehouse from BinQasim and export processing zone gives added advantage to the

customers for quick dispatch of their goods. (Al-Abbas Sugar

Mills Limited, 2012) ? BEST PRACTICES: Following principles form the basis for the best practicesobserved at Al-Abbas Sugar Mills Limited: 4.1.

1Quality Products: ? Care about quality of the product and try to compete

nationally and internationally. ? Always try to stay updated with introduction

of new technology and promote culture of change of in the company. ?

Maintain highest degree of technical standards. 4.2. Dealing with

employees:

? Recognizes and rewards all the

1employees for their performance. ? Provide very friendly working

atmosphere for all the employees and treat them as family members. ? All

employees are treated uniformly according to their organizational status.

4.3. Compliance with the law of country: The company always adheres to the

prevailing laws. Utmost care is taken by the company to discharge all the

legal responsibilities. 4.4 Internal control and financial reporting: ? A very

sound and reliable internal control system has been implemented in the

organization, which is well understood by all the employees and parties

dealing with the company. ? Financial planning is a core activity of the

system through which efficient and effective utilization of financial andhuman resources is ensured. ? Financial reporting system employed by the

Turnitin Originality Report https://www.turnitin.com/newreport_printview.asp?eq=0&eb=0&esm=-2...

8 of 16 25-Jun-14 6:26 PM

company is very effective and transparent and is being relied upon by

society at large. 4.5. Dealing with suppliers and service providers: ?

Purchase only from very reliable parties, acquire service of competent

people and ensure to safeguard their interests by taking all necessarysteps in dealing with them strictly on fair basis. ? The company always tries

to build confidence, reliability and trust by ensuring fulfillment ofcommitments with suppliers and service providers. 4.6. Goal of the

company: ? The company always strives to produce high standard products

whether it is for local or international markets. ? Provide reliableinformation to all business partners. ? Keep all assets in superfine

condition and safeguard them from all possible risks.

(Al- Abbas Sugar Mills Limited, 2012) (23rd Annual Report, 2013, 2013) ? FINANCIAL ANALYSIS: Thefinancial analysis for this study is as follows: 5.1. Methodology: The methodology used for the processingand analysis of the secondary data available in the Balance Sheet analysis of Joint Stock Companies Listedon the Karachi Stock Exchange for the time period involves descriptive statistical analysis, the correlationamong variables followed by horizontal and vertical analysis. 5.1.1. Data Length and Period under study:The period under study for the data collection, assessment and time series analysis of Al- Abbas Sugar MillsLimited comprises of 21 years that is from 1993 to 2013. 5.1.2. Variables: The variables that have beenused to analyze the performance and growth of the company are as follows: Table 5.1 SR Variables fromIncome Statement Sales Revenue CA Variables from Balance Sheet Current Assets GP NP Gross Profit NetProfit CL TA TL Current Liabilities Total Assets Total Liabilities TE Shareholders’ Equity 5.1.3. Techniquesapplied: The data has been appropriately tabulated and classified to analyze using the tools like descriptivestatistics to quantitatively describe the main features of the available data. Data analysis with the help ofline graphs of variables and correlation are also discussed. Horizontal and vertical analysis of the data for21 years has also been carried out to undergo trend analysis. 5.2. Descriptive Statistics: Measures ofcentral tendency including the mean and median, and the measures of variability including the standarddeviation, the minimum and maximum values of the variables, kurtosis and skewness have been used toanalyze the quantitative data. Table 5.2 Descriptive Statistics Sales Gross Profit, Net Profit Current TotalCurrent Total Total Revenue SR GP NP Assets, CA Assets, TA Liabilities, CL Liabilities, TL Equity, TE Std.Deviation Skewness Kurtosis Range Minimum Maximum N Mean Median Valid Missing 21 0 2402.711423.00 2082.637 .992 -.388 6353 0 6353 21 0 332.29 194.00 335.289 1.358 .560 1159 0 1159 21 0140.52 86.00 143.866 1.357 1.403 550 -11 539 21 0 911.14 673.00 917.482 1.269 .968 3244 47 3291 210 2029.00 1463.00 1555.497 .967 -.569 4761 568 5329 21 0 993.62 738.00 954.082 1.252 .934 3402 643466 21 0 1306.10 925.00 1113.149 1.101 -.074 3681 267 3948 21 722.86 599.00 502.081 1.167 .7911875 87 1962 0 The standard deviation represents the extent of variation among the data. There is lessvariation in the data of gross profit, net profit before tax, current assets and current liabilities. Because thedata is dispersed over a wide range of values, thus great variations have been observed in the salesrevenue, total assets, total liabilities and total equities. Skewness describes the degree of asymmetry of adistribution around its mean. If the skewness is positive, it indicates that the distribution has an asymmetrictail extending toward more positive values. While negative skewness shows a distribution with an

Turnitin Originality Report https://www.turnitin.com/newreport_printview.asp?eq=0&eb=0&esm=-2...

9 of 16 25-Jun-14 6:26 PM

asymmetric tail extending toward more negative values. The skewness of the 21 years data is substantialand is far from being symmetrical for all other variables except for the sales revenue and total assets.Kurtosis denotes the relative peakedness or flatness of a distribution compared with the normal distribution.Positive kurtosis suggests a relatively peaked distribution while in case of negative kurtosis a relatively flatdistribution is observed. Sales revenue, total assets and total liabilities have negative kurtosis and give arelatively flatter than a normal distribution. 5.3. Data Analysis: Figure 4. 1 Assets = Liabilities +Shareholders' Equity TL. 32% TA. 50% TE. 18% Taking the averages of all the data for 21 years andcomputing for the accounting equation revels that total assets comprise of the 50 percent of the overallequation while on average, the total liabilities form 32 percent and total shareholders’ equity contributingabout 18 percent. Figure 4. 2 Sales Revenue Export Sales 43% (Rs. 1272.91m) Local Sales 57% (Rs.1667.9m) The two major components of sales revenue are the local sales and the export sales. Thecompany’s major focus had been the local sales of up to 57 percent which amounts to Rs. 1,667.9m whileits exports of 43 percent or Rs. 1,272.91m on average have been observed to be increasing since itsinception. 5.3.1 Sales Revenue, SR: Figure 4. 3 (Million Rupees) Sales Revenue, SR 7000 6000 SalesRevenue, SR 5000 4000 3000 2000 1000 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 YearsThere has been a gradual increase in sales revenue from both the local and export sales with an evidentincrease in 2001. With an increasing trend, it suddenly showed an increase in the year 2010 and then isseen to remain somewhat constant. The typical daily sales are Rs. 2,402.73m and the centre of the data islocated at 1,423.4. The values in the data are farther away from the mean, on average. 5.3.2. Gross Profit,GP: Figure 4. 4 (Million Rupees) Gross Profit, GP 1400 1200 Gross Profit, GP 1000 800 600 400 200 0 1 23 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 Years Since 1993, the gross profit has been observedto be consistent for quite a few years. There has been significant increase in the gross profit in the years2001 and 2004. It remains constant for some years and then began to increase in 2009. The peaked valueof Rs. 1,159.3m in 2012 indicates a significant increase in the company’s gross profit. 5.3.3. Net Profitbefore Tax, NP: Figure 4. 5 Net Profit before tax, NP (Million Rupees) 600 Net Profit before tax, NP 500 400300 200 100 0 -100 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 Years As is evident from figure4.5, Al-Abbas Sugar Mills Limited has experienced many fluctuations in its net profit before tax through these21 years. The most remarkable change can be seen in 2001 with an increase and a sudden decrease in thefollowing year of 2002. However, it has managed to elevate in the next two years and the rest of the years.The highest net profit before tax of Rs. 539.3m has been observed in 2012. 5.3.4. Total Assets, TA: Figure4. 6 (Million Rupees) Total Assets, TA 6000 5000 Total Assets, TA 4000 3000 2000 1000 0 1 2 3 4 5 6 7 8 910 11 12 13 14 15 16 17 18 19 20 21 Years Al-Abbas Sugar Mills Limited has been able to maintain its totalassets for quite a long time. Moreover, the total assets have increased significantly in 2008 and 2011. It hasslightly decreased since then. 5.3.5. Total Liabilities, TL: Figure 4. 7 (Million Rupees) Total Liabilities, TL4500 4000 Total Liabilities, TL 3500 3000 2500 2000 1500 1000 500 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 1516 17 18 19 20 21 Years Total liabilities have been observed to show similar trend as total assets. Asignificant increase in the total liabilities is obvious in 2008 and 2011. However, it has declined in thefollowing two years. 17 5.3.6. Total Shareholders' Equity, TE: Figure 4. 8 (Million Rupees) TotalShareholders' Equity, TE 2500 Total Shareholders' Equity, TE 2000 1500 1000 500 0 1 2 3 4 5 6 7 8 9 1011 12 13 14 15 16 17 18 19 20 21 Years The total shareholders’ equity, as is evident from the above figurehas consistently increased since 1993 and had its highest value of Rs. 1,962m in 2013. 5.3.7. SR, GP andNP: Figure 4. 9 (Million Rupees) SR, GP and NP 7000 6000 5000 4000 GP 3000 NP 2000 SR 1000 0 1 2 34 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 -1000 As is obvious, in its initial years the company didnot make much profit. The gross profit and the net profit both moved together throughout the years. In year

Turnitin Originality Report https://www.turnitin.com/newreport_printview.asp?eq=0&eb=0&esm=-2...

10 of 16 25-Jun-14 6:26 PM

2000, the gross profit and the net profit before tax experience very close values which may be a result oflower operating expenses. However, the sales revenue showed an increasing trend over the years withrespect to the net profit before tax and gross profit. 5.4. Correlation: Correlation is a quantitative index, astandard statistical measurement of the degree of relationship or association between two sets of variables.In this study the correlation coefficient analysis has been undertaken to find out the relationship among thevariables, which is a measure of linear association. Table 5.3 Correlations Sales Revenue, SR Net Profit,Total Assets, TA NP Total Liabilities, TL Total Shareholders’ Equity, TE Pearson Correlation Sales Revenue,SR Sig. (2-tailed) N Net Profit, Pearson Correlation NP Sig. (2-tailed) N Total Assets, Pearson CorrelationTA Sig. (2-tailed) N Total Liabilities, Pearson Correlation TL Sig. (2-tailed) N Total Pearson CorrelationShareholders’ Sig. (2-tailed) Equity, TE N 1 21 .869** .000 21 .947** .000 21 .896** .000 21 .947** .000 211 21 .853** .000 21 .791** .000 21 .889** .000 21 1 21 .984** .000 21 .917** .000 21 1 21 .831** .000 21 121 **. Correlation is significant at the 0.01 level (2-tailed). There exists a positive correlation among all thevariables. Sales revenue is strongly correlated to total assets and total shareholders’ equity. That is whenshareholders’ equity increases; we can expect the sales revenue to increase. Total assets have a strongcorrelation with sales revenue and net profit as well. Total shareholders’ equity has strong correlation withsales revenue and total assets while having positive correlation with net profit and total liabilities. 5.5.Financial Statement Analysis: Financial statement analysis generally is based on comparative financial datafor a series of years. Horizontal analysis provides a direct year-to-year comparison of one company’sperformance while vertical analysis shows the relationship of each item on a financial statement to a baseamount on that financial statement for the same year. 5.5.1. Horizontal Analysis: In order to get trend,horizontal analysis has been carried out by calculating absolute change and percentage change by usingFixed Base method. o Absolute Change: Fixed Base Method = Current Year Value – Base Year Value oPercentage Change: Fixed Base Method = (Current Year Value / Base Year Value) X 100 As is evident fromthe calculated results of horizontal analysis shown in Annexure – D, 1993 is taken as the base year and therest are the comparison years for comparative balance sheet and income statement analyses. Items on thebalance sheet for the proceeding years have been compared with the items of balance sheet for the year1993. An increasing trend has been observed in the total and current assets of Al-Abbas Sugar Mills Limited.There has been a sudden increase in the total and current assets in 2001 and then in 2011 with respect tothe initial total and current assets held by the company in 1993. With a gradual increase in the company’stotal and current liabilities since its inception, a drastic increase was obvious in the 2001 leading to anincreasing trend in its liabilities and then another sudden increase in 2011 again. Similarly, the totalshareholders’ equity increased in 2001 but bears the largest contribution in 2013. Similarly, items on theincome statement for the proceeding years have been compared with those for the year 1993. Net Salesshowed highest absolute and percentage changes in the year 2010 while the highest changes in absolutevalues and percentage of gross profit and net profit have been observed in the year 2012. 5.5.2. VerticalAnalysis: The vertical analysis compares each separate figure to one specific figure in the financialstatement, which is reported as a percentage. o Vertical Analysis of Balance Sheets: Computing all balancesheet items as a percentage of Total Assets ( Balance Sheet Items / Total Assets X 100 ) o Vertical Analysisof Income Statements: Computing each income statement item as a percentage of Sales (Income StatementItems / Sales X 100 ) The calculated results of the vertical analysis of balance sheet and income statementare shown in Annexure – E. For comparative balance sheet, current assets and current liabilities showedhighest percentages in the years 2011 and 2012. While for computing the comparative income statement,1994 has been taken as the base year. Gross profit and net profit before tax show deviation with highestpercentages with respect to sales in the year 2004. 5.6. SWOT Analysis: The major strengths, weaknesses,

Turnitin Originality Report https://www.turnitin.com/newreport_printview.asp?eq=0&eb=0&esm=-2...

11 of 16 25-Jun-14 6:26 PM

opportunities and threats to Al-Abbas Sugar Mills Limited are shown in the figure below: SWOT Analysis 1STRENGTHS: • Generates revenue for the industry • Employment • Provides essential products to otherindustries • Good R&D capabilities WEAKNESSES: • Poor management and planning • Unable to meetdomestic needs • Lack of technology and modernization • Lack of education OPPORTUNITIES: THREATS: •Exporting to other countries • Increase in fuel prices • Large area of cultivable land • Recent floods available• Smuggling • International exposure and systematic branding efforts • Artificial shortages, cartelling andhoarding • Pest attacks 5.7. Comparison with industrial sector: The calculation and analysis of the companyin isolation holds less importance and meaning. Thus, in order to get the true essence of the company’sefforts and contribution towards the industry, a comparison of 15 years of data (from 1999 to 2013) ofAl-Abbas Sugar Mills Limited with the overall sugar sector is presented here in detail. Assuming the salesrevenue, total assets, liabilities and total shareholders’ equity remains same as the last year; thus, the datafor the year 2013 has been taken as the estimated values of previous year, 2012. 5.7.1 Sales Revenue,SR: Figure 5.7.1 160000 140000 120000 100000 80000 60000 40000 20000 0 1 2 3 4 (Million Rupees)Sales Revenue, SR 5 6 7 8 9 10 11 12 13 14 15 SUGAR SECTOR AABS Sales revenue for Al-Abbas SugarMills Limited remained consistent with the overall sugar sector in 1999 and 2000. The industry began togrow since then with slight shifts and reached the highest value of Rs.144, 796.87m of overall sales revenuein 2011. 5.7.2. Gross Profit, GP: Figure 5.7.2 (Million Rupees) 18000 16000 14000 12000 10000 80006000 4000 2000 0 Gross Profit, GP 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 SUGAR SECTOR AABS The grossprofit of Al-Abbas Sugar Mills Limited remains somewhat consistent throughout comparatively to the sugarsector on the whole. However, the overall sugar sector represents major shifts with Rs.6, 391.5m in 2006while Rs.17, 133m in the year 2011. 5.7.3. Net Profit before Tax, NP: Figure 5.7.3 (Million Rupees) 6000 NetProfit, NP 5000 4000 3000 2000 1000 0 -1000 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 -2000 SUGARSECTOR AABS Similarly, Al-Abbas Sugar Mills Limited had smooth net profit before taxes for the last fifteenyears. But the sugar sector at large has experienced many fluctuations in net profit before taxes. This maybe the result of various extraneous factors such as climatic changes, floods, political and proceduralimpacts. 24 5.7.4. Total Assets, TA: Figure 5.7.4 140000 120000 100000 80000 60000 40000 20000 0 1 23 4 (Million Rupees) Total Assets, TA 5 6 7 8 9 10 11 12 13 14 15 SUGAR SECTOR AABS Although therehas been a gradual increase in the company’s total assets, but they have been observed to show consistentvalues as compared to the sector. As is evident from the figure 5.7.4, total assets in the sugar sector haveshown gradual increase over these years. The highest total assets of the sugar sector have been aboutRs.132, 282m in 2012. 5.7.5. Total Liabilities, TL: Figure 5.7.5 (Million Rupees) 500000 450000 400000350000 300000 250000 200000 150000 100000 50000 0 Total Liabilities, TL 1 2 3 4 5 6 7 8 9 10 11 12 1314 15 SUGAR SECTOR AABS The company’s total liabilities showed variations but total liabilities of thesector on the whole represented an increasing trend in the last fifteen years. The total liabilities reached thehighest value of Rs.457, 133m in 2010. 5.7.6. Total Shareholders' Equity, TE: Figure 5.7.6 (Million Rupees)40000 Total Shareholders' Equity, TE 35000 30000 25000 20000 15000 10000 5000 0 1 2 3 4 5 6 7 8 9 1011 12 13 14 15 SUGAR SECTOR AABS Total shareholders’ equity has been observed to be graduallyincreasing for the company and the sugar sector for the fifteen years period as well. But the rate of increasein total shareholders’ equity was greater than that of the company itself. 5.7.7. SR, GP and NP: Figure 5.7.7(Million Rupees) 160000 140000 120000 100000 80000 60000 40000 20000 0 SR, GP and NP -20000 1 23 4 5 6 7 8 9 10 11 12 13 14 15 SR GP NP Sales revenue has been observed to be gradually increasing forthe last fifteen years. Similarly, gross profit and net profit before tax for the sugar sector move together butthe degree of increase in sales revenue is greater. This may be due to the increasing indirect and operatingexpenses over the years. Although the gross profit remained consistent however, the net profit before tax for

Turnitin Originality Report https://www.turnitin.com/newreport_printview.asp?eq=0&eb=0&esm=-2...

12 of 16 25-Jun-14 6:26 PM

the sugar sector showed negative values in the years 2001, 2002, 2003 and 2007. Limitations: Care hasbeen taken while gathering, analyzing and interpreting the data. However, following were the limitations whileconducting the study. ? While computing the horizontal and vertical analysis of income statement, 1994 wastaken as the base year to get viable results. ? For comparative analysis of Al-Abbas Sugar Mills Limited withthe overall sugar sector, data of overall sugar sector for only fourteen years, from 1999 to 2012, wasavailable. ? The data for the year 2013 was assumed to be similar to the previous year that is 2012. ?Conclusion: Al-Abbas Sugar Mills Limited aims at enhancing its sugar manufacturing and production facilities.Descriptive statistical analysis technique has been used to disintegrate the secondary data for a specifiedtime frame of 21 years from 1993 through 2013. A detailed company analysis of Al-Abbas Sugar MillsLimited on various aspects has been observed to analyze the company’s growth potential. In time seriesanalysis of 21 years, less variation in the data of gross profit, net profit before tax, current assets andcurrent liabilities has been observed. In years 2008 and 2011, major shifts in Sales Revenue (SR), TotalAssets (TA) and Total Liabilities (TL) are evident. While Net Profit Before Tax (NP) and Gross Profit (GP)have been observed to remain consistent for quite a long time. On the basis of a comparative analysis,Al-Abbas Sugar Mills Limited has been observed to show sales revenue, gross profit, net profit, total assetsand liabilities and total shareholders’ equity of the sugar sector to be increasing at a greater rate than thecompany itself. Recommendations: Based upon the analysis of the company and corporate activities,following are the recommendations drawn for the Al-Abbas Sugar Mills Limited: • Upgrade to latesttechnology. • Improve storage and warehousing facilities. • Enhance hygiene of the workers and the product.• Educate the workers and employees. • Provide a productive and efficient working environment. • Improvetransportation for timely delivery of the raw material and the final product. •

1Ensure and safeguard the interests of all stakeholders.

REFERENCES Al-Abbas Sugar Mills Limited. (2012). Retrieved May 4, 2014, from Al-Abbas Sugar MillsLimited: http://www.aasml.com/ Al-Abbas Sugar Mills Limited. (2012). Retrieved May 31, 2014, fromAl-Abbas Sugar Mills Limited: http://www.aasml.com/ Al-Abbas Sugar Mills Limited, 23rd Annual Report,2013. M.Ammar Arif Nakhuda, A. S. (2010). Sugar Industry of Pakistan. Karachi. Malu, R. S. (2007).COMPANY ANALYSIS IN SUGAR SECTOR. Pune, India. Memon, Z. A. Internship report bawany sugar millsltd. Pakistan Sugar Mills Association, Islamabad. (2011). Retrieved May 5, 2014, fromhttp://www.psmacentre.com/aboutus.php?id=4&type=membersList&status=1 Saeed, K. (2013). Overview ofSugar Industry in Pakistan. The Lahore Chamber of Commerce and Industry, Research and DevelopmentDepartment. Lahore: The Lahore Chamber of Commerce and Industry. Shaukat, M. I. (n.d.). Acomprehensive study about Sugarcane in Pakistan. ANNEXURE – A

1Mr. Shunaid Qureshi Chief Executive Officer Mr. Shunaid Qureshi

Presently holding the office of Chairman Pakistan Ethanol ManufacturersAssociation (P.E.M.A.). He continued as Chairman of Pakistan Sugar MillsAssociation (All Pakistan Basis) for the term 2007-2008 (Sindh Zone). Heendured his services as Chairman of F.P.P.C.I Standing Committee on"WAPDA Affairs", for the term ending Dec. 2010.

Turnitin Originality Report https://www.turnitin.com/newreport_printview.asp?eq=0&eb=0&esm=-2...

13 of 16 25-Jun-14 6:26 PM

Mr. Asim Ghani Executive Director

1Mr. Asim has very extensive experience in procurement and handling of

molasses. Besides, this he acts as Executive Director in managing thedaily affairs of Dhabeji unit of the Al-Abbas Sugar Mills

1Limited. Mr. Duraid Quresh Director Mr. Duraid Qureshi is the Chief

Executive Officer (CEO) of HUM Network Limited, (satellite Channel). From2001-2003 he was the CEO of Eye Entertainment. Prior to this he was theChief Operating Officer of Al-Abbas Sugar Mills Limited responsible for alloperating work at the mill. Mr.

1Ali Jehangir Siddiqui Director Mr. Ali Jahangir Siddiqui is the Managing

Partner of JS Private Equity, Pakistan's largest private equity firm.

Executive Director JS, Investments Ltd. 2002-2003.

1Director with Crosby, a private equity firm, based in Hong Kong.

Associate with Tech pacific Capital.

1Mr. Siddiqui holds a B.A. in Economics from Cornell University.

1Mr. Suleman Lalani Director Mr. Suleman Lalani joined Jahangir Siddiqui

& Co. Limited (JSCL) on March 1, 2012 as Chief Executive Officer.

1Executive Director Finance & Operations and Company Secretary of JS

Investments Limited.

Started his career with JSCL in 1992.

1Promoted to the position of Chief Operating Officer of JS Investment

Turnitin Originality Report https://www.turnitin.com/newreport_printview.asp?eq=0&eb=0&esm=-2...

14 of 16 25-Jun-14 6:26 PM

Bank Limited

in 2000.

1Joined The First MicroFinance Bank Limited as its CFO and Company

Secretary

in 2002.

1Fellow member of the Institute of Chartered Accountants of Pakistan and

has 20 years of experience in the financial services sector.

ANNEXURE – B PHOTOCOPY THEN SCAN Source: Balance Sheet Analysis of Joint Stock CompaniesListed on KSE, Volume-II, 1993-99, SBP. 31 ANNEXURE - C Variables used in the study: Sales Revenue,SR = Local Sales + Export Sales Gross Profit, GP = Sales – Cost of Sales Net Profit before Tax, NP =Operating Profit – Financial Expenses Total Assets, TA = (Liquid Assets Cash + Inventories + Other CurrentAssets) + Fixed Assets after deducting accumulated depreciation Total Liabilities, TL = (Preferred Shares +Debentures + Other Fixed Liabilities) + Current Liabilities Total Shareholders' Equity, TE = Ordinary ShareCapital + Surplus Complete data sheet of Al-Abbas Sugar Mills Limited for the period of 21 years from 1993to 2013 is given here. Insert Last page Balance Sheet and income stat items for report ANNEXURE - DHorizontal Analysis of Balance Sheet 1993-02 Horizontal Analysis of Balance Sheet 2003-13 Al - AbbasSugar Mills Ltd. Comparative Income Statement Horizontal Analysis, Items are in "Million Rupees"(September 30, 1993 - 2013) Net Sales, SR Gross Profit, GP Net Income/Profit, NP SR Absolute ChangePercentage Change GP Absolute Change Percentage Change NP Absolute Change Percentage Change1993 0 - - 0 - - 0 - - 1994 325.1 0.00 100.00 91.8 0.00 100.00 28.6 0.00 100.00 1995 766.2 441.10 235.68118.9 27.10 129.52 44.7 16.10 156.29 1996 578.6 253.50 177.98 111 19.20 120.92 49.8 21.20 174.131997 720.8 395.70 221.72 98.2 6.40 106.97 41.1 12.50 143.71 1998 1013.7 688.60 311.81 128.3 36.50139.76 37.2 8.60 130.07 1999 1173 847.90 360.81 165 73.20 179.74 88.2 59.60 308.39 2000 963 637.90296.22 111.4 19.60 121.35 71.4 42.80 249.65 2001 2019.9 1694.80 621.32 260.4 168.60 283.66 118.289.60 413.29 2002 1401.6 1076.50 431.13 67.6 -24.20 73.64 -10.8 -39.40 -37.76 2003 1327.4 1002.30408.31 193.4 101.60 210.68 86 57.40 300.70 2004 1423.4 1098.30 437.83 333.4 241.60 363.18 211.3182.70 738.81 2005 1845.7 1520.60 567.73 194 102.20 211.33 70.5 41.90 246.50 2006 2514.3 2189.20773.39 198.1 106.30 215.80 31.6 3.00 110.49 2007 2842.3 2517.20 874.28 251.5 159.70 273.97 173.3144.70 605.94 2008 2931.1 2606.00 901.60 212 120.20 230.94 104.3 75.70 364.69 2009 4166.9 3841.801281.73 785.6 693.80 855.77 337.1 308.50 1178.67 2010 6352.9 6027.80 1954.14 756.6 664.80 824.18276.1 247.50 965.38 2011 6220.5 5895.40 1913.41 940.1 848.30 1024.07 324.5 295.90 1134.62 20125964.2 5639.10 1834.57 1159.3 1067.50 1262.85 539.3 510.70 1885.66 2013 5906.7 5581.60 1816.89802.2 710.40 873.86 331 302.40 1157.34 * 1994 is taken as the Base Year ANNEXURE - E VerticalAnalysis of Balance Sheet 1993-02 Vertical Analysis of Balance Sheet 2003-13 Al - Abbas Sugar Mills Ltd.Comparative Income Statement Vertical Analysis, Items are expressed as “Percentage of Sales"(September 30, 1993 - 2013) Net Sales, SR Gross Profit, GP Net Income/Profit, NP SR Percentage Change

Turnitin Originality Report https://www.turnitin.com/newreport_printview.asp?eq=0&eb=0&esm=-2...

15 of 16 25-Jun-14 6:26 PM

GP Percentage Change NP Percentage Change 1993 0 - 0 - 0 - 1994 325.1 100.00 91.8 28.24 28.6 8.801995 766.2 100.00 118.9 15.52 44.7 5.83 1996 578.6 100.00 111 19.18 49.8 8.61 1997 720.8 100.0098.2 13.62 41.1 5.70 1998 1013.7 100.00 128.3 12.66 37.2 3.67 1999 1173 100.00 165 14.07 88.2 7.522000 963 100.00 111.4 11.57 71.4 7.41 2001 2019.9 100.00 260.4 12.89 118.2 5.85 2002 1401.6 100.0067.6 4.82 -10.8 -0.77 2003 1327.4 100.00 193.4 14.57 86 6.48 2004 1423.4 100.00 333.4 23.42 211.314.84 2005 1845.7 100.00 194 10.51 70.5 3.82 2006 2514.3 100.00 198.1 7.88 31.6 1.26 2007 2842.3100.00 251.5 8.85 173.3 6.10 2008 2931.1 100.00 212 7.23 104.3 3.56 2009 4166.9 100.00 785.6 18.85337.1 8.09 2010 6352.9 100.00 756.6 11.91 276.1 4.35 2011 6220.5 100.00 940.1 15.11 324.5 5.22 20125964.2 100.00 1159.3 19.44 539.3 9.04 2013 5906.7 100.00 802.2 13.58 331 5.60 * 1994 is taken as theBase Year Chapter – 3: Chapter – 4: Chapter – 5: 1 2 3 5 6 7 8 9 10 11 12 13 14 15 16 18 19 20 21 22 2325 26 27 28 29 30 32 33 34 35 36 37 38 39 40 41 42 43 44 45

Turnitin Originality Report https://www.turnitin.com/newreport_printview.asp?eq=0&eb=0&esm=-2...

16 of 16 25-Jun-14 6:26 PM