Embed Size (px)

Citation preview

Amity Business School

Entrepreneurship& New Venture

Creations

1

Amity Business School

Source of fund

2

Amity Business School

3

You see What You Believe…

Amity Business School

4

You see What You Believe…

Amity Business School

Financing Difficulties for Start-ups Most difficult phase to raise capital is the financing

valley of death, particularly as an entrepreneur you may not have anything other than the idea and its worth in the eyes of funding organizations.

Generally investors, from angels to venture capitalists and bankers would like to back a venture that has sure chances of success.

Start-up must show that it has customers who are willing to pay upfront or otherwise for buying the product or availing service from them.

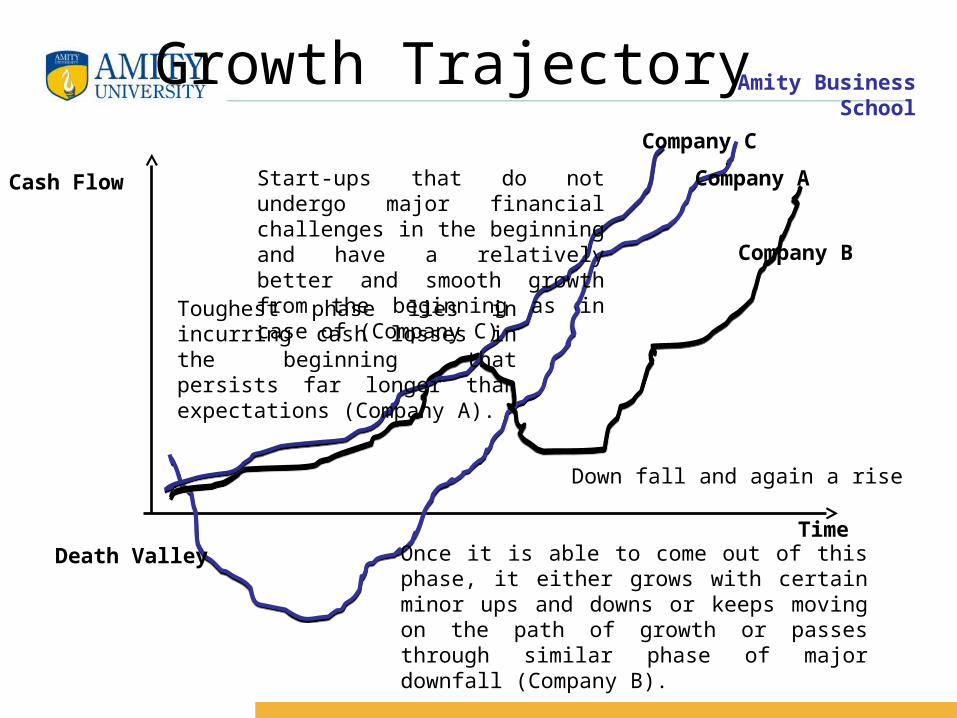

Amity Business SchoolGrowth Trajectory

Time

Cash Flow

Death Valley

Down fall and again a rise

Company C

Company A

Company B

Once it is able to come out of this phase, it either grows with certain minor ups and downs or keeps moving on the path of growth or passes through similar phase of major downfall (Company B).

Toughest phase lies in incurring cash losses in the beginning that persists far longer than expectations (Company A).

Start-ups that do not undergo major financial challenges in the beginning and have a relatively better and smooth growth from the beginning as in case of (Company C)

Amity Business School

Raising FinanceWhat for do you need the money? How much money is required?

What type of money is required by you?

When exactly do you need money?

What is stored for investors in offering you a money?

What are the exit options available to investors?

Amity Business School

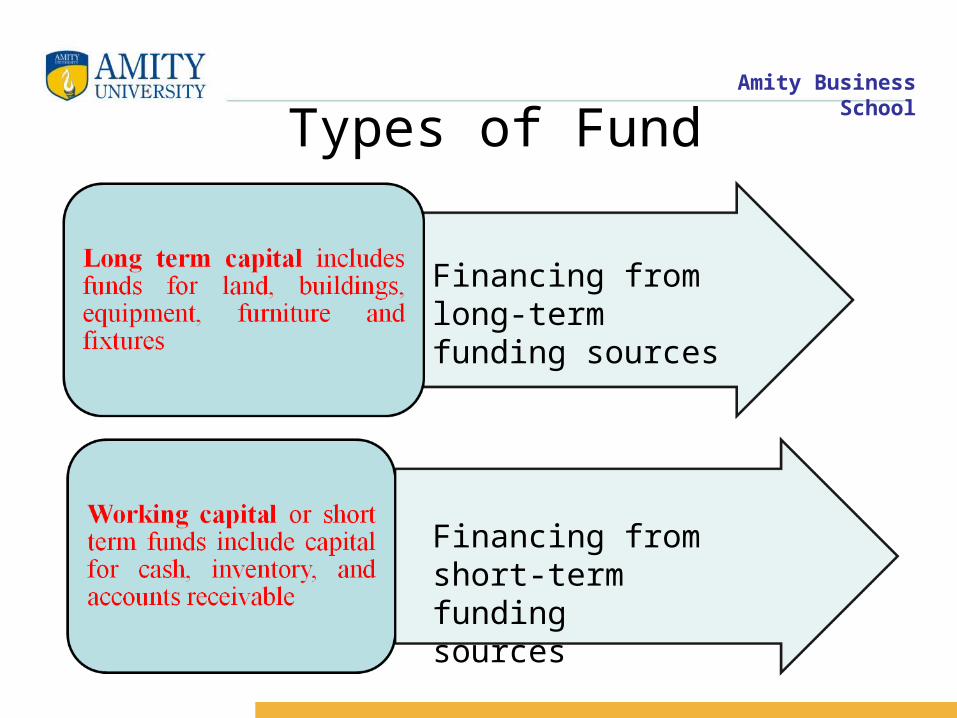

Types of Fund

Financing from long-term funding sources

Financing from short-term funding sources

Amity Business School

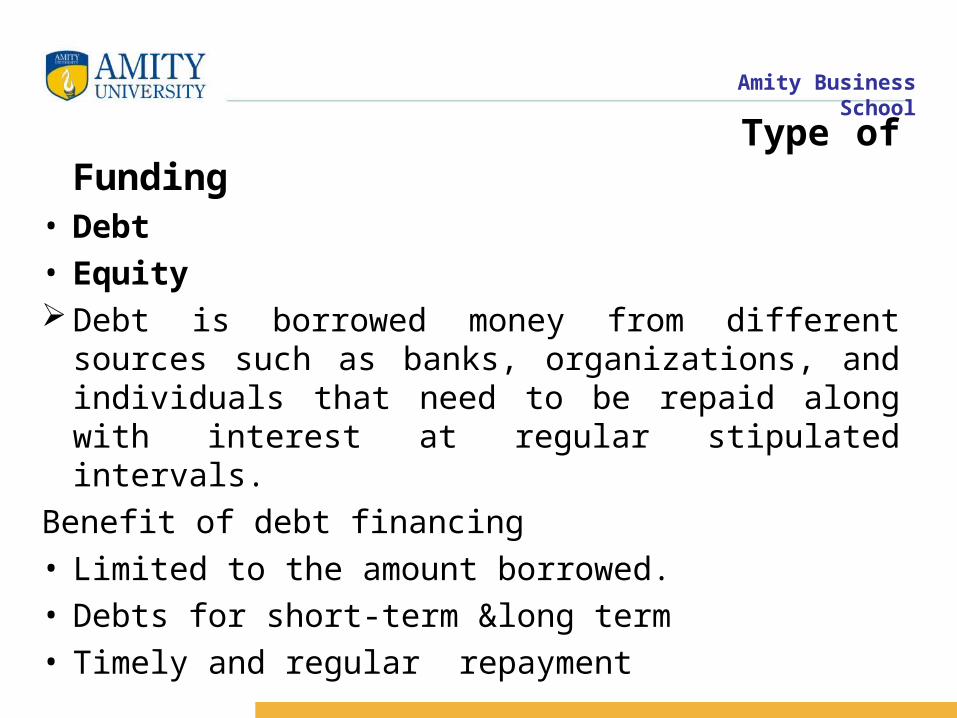

Type of Funding• Debt• Equity Debt is borrowed money from different sources such

as banks, organizations, and individuals that need to be repaid along with interest at regular stipulated intervals.

Benefit of debt financing • Limited to the amount borrowed.• Debts for short-term &long term• Timely and regular repayment

Amity Business School

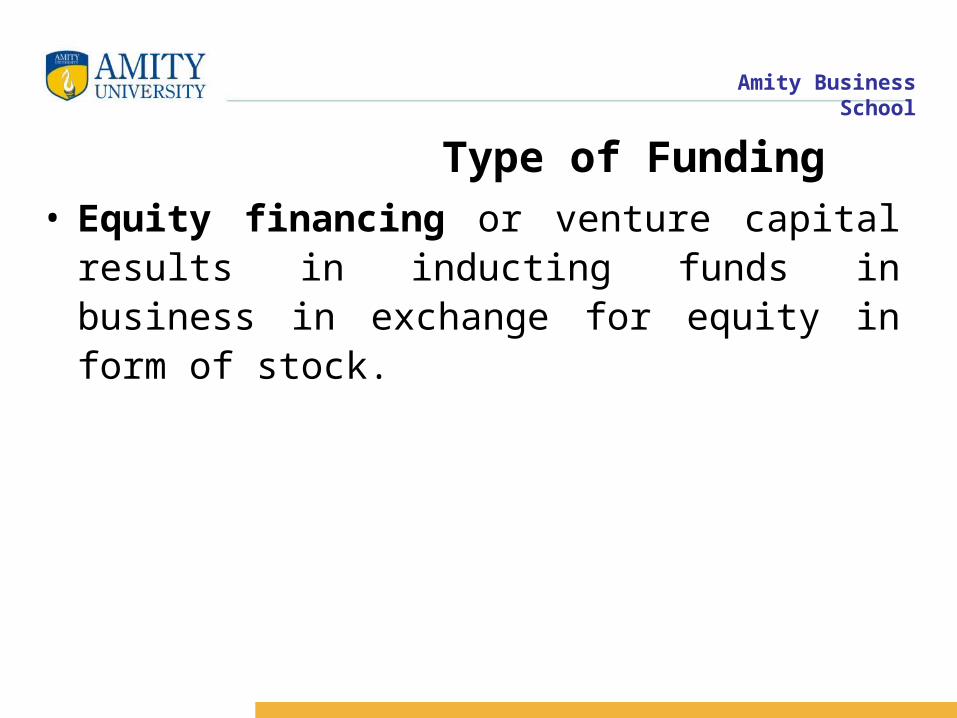

Type of Funding• Equity financing or venture capital results in

inducting funds in business in exchange for equity in form of stock.

Amity Business School

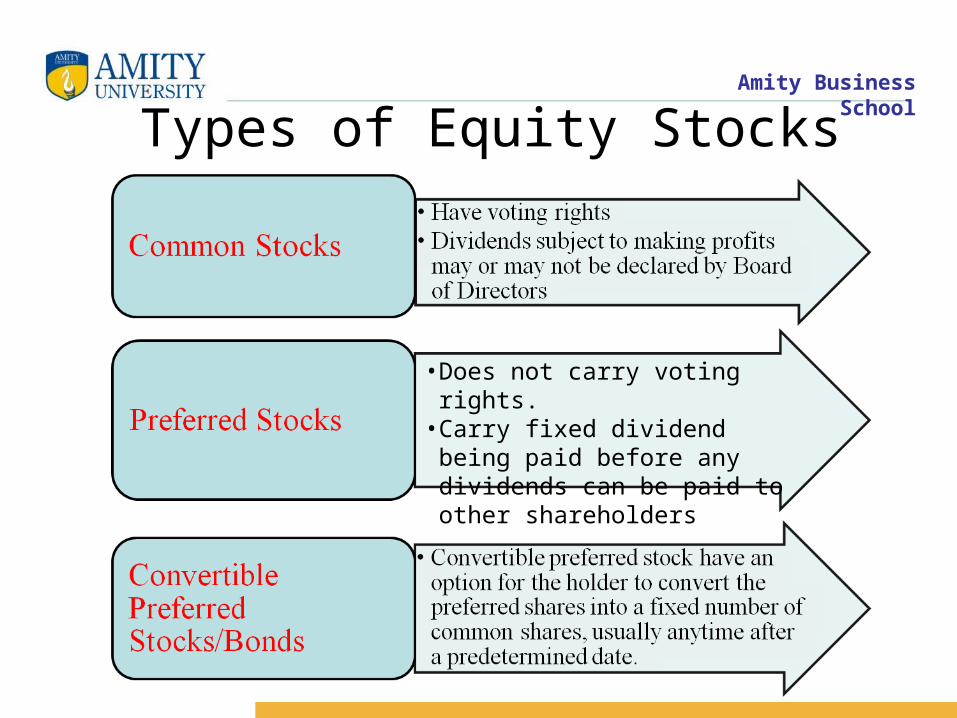

Types of Equity Stocks

• Does not carry voting rights.• Carry fixed dividend being paid

before any dividends can be paid to other shareholders

Amity Business School

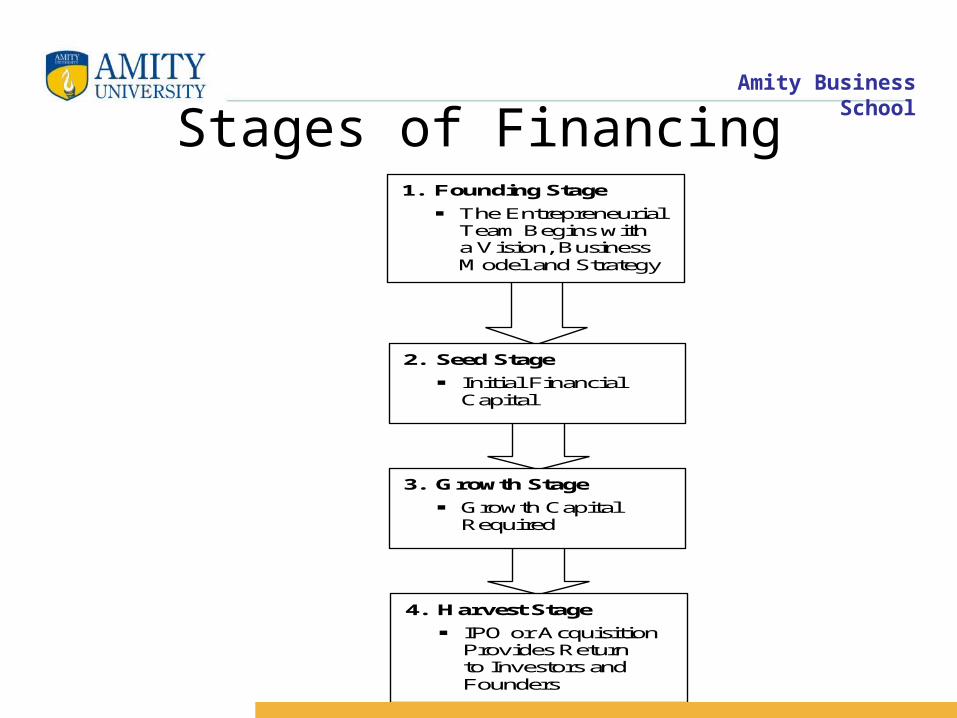

Stages of Financing

1. Founding Stage

The Entrepreneurial Team Begins with a Vision, Business Model and Strategy

2. Seed Stage

Initial Financial Capital

3. Growth Stage

Growth Capital Required

4. Harvest Stage

IPO or Acquisition Provides Return to Investors and Founders

Amity Business School

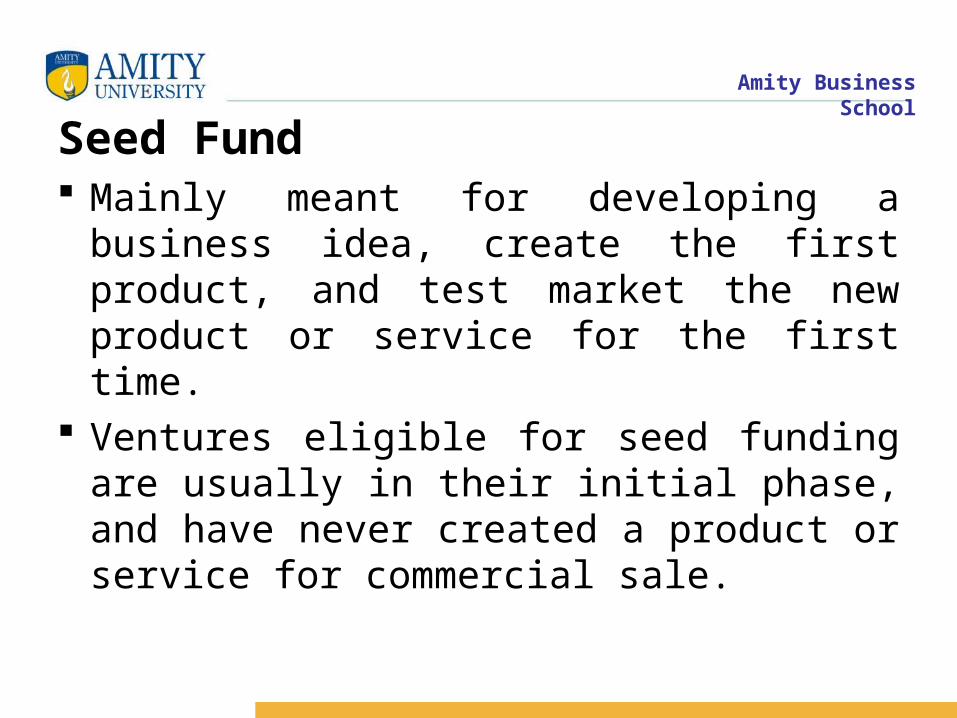

Seed Fund Mainly meant for developing a business idea,

create the first product, and test market the new product or service for the first time.

Ventures eligible for seed funding are usually in their initial phase, and have never created a product or service for commercial sale.

Amity Business School

14

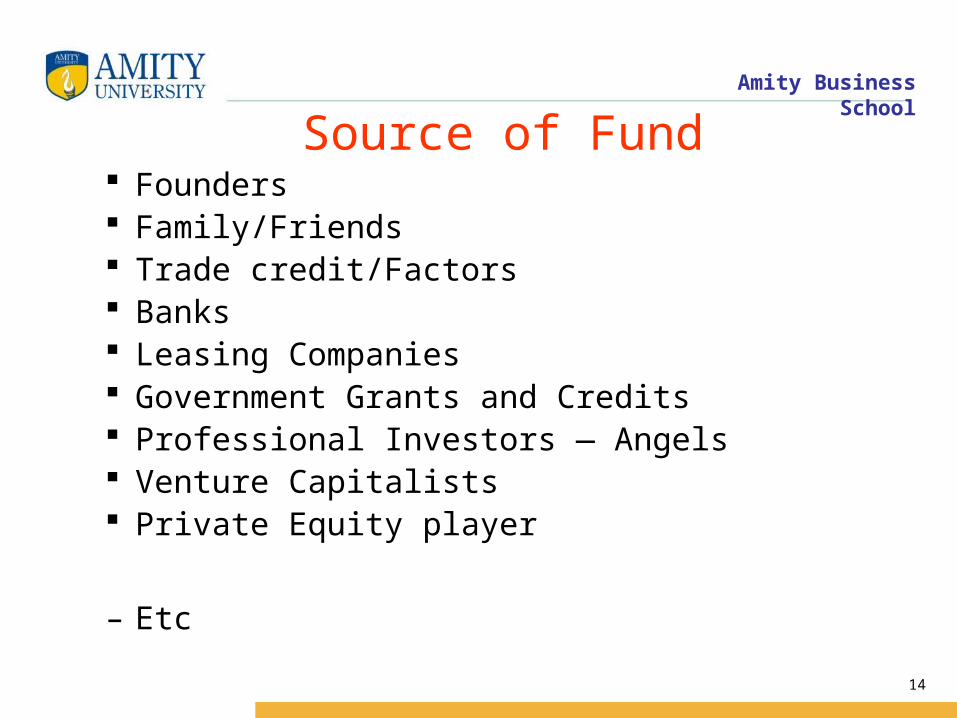

Source of Fund Founders Family/Friends Trade credit/Factors Banks Leasing Companies Government Grants and Credits Professional Investors — Angels Venture Capitalists Private Equity player

– Etc

Amity Business School

15

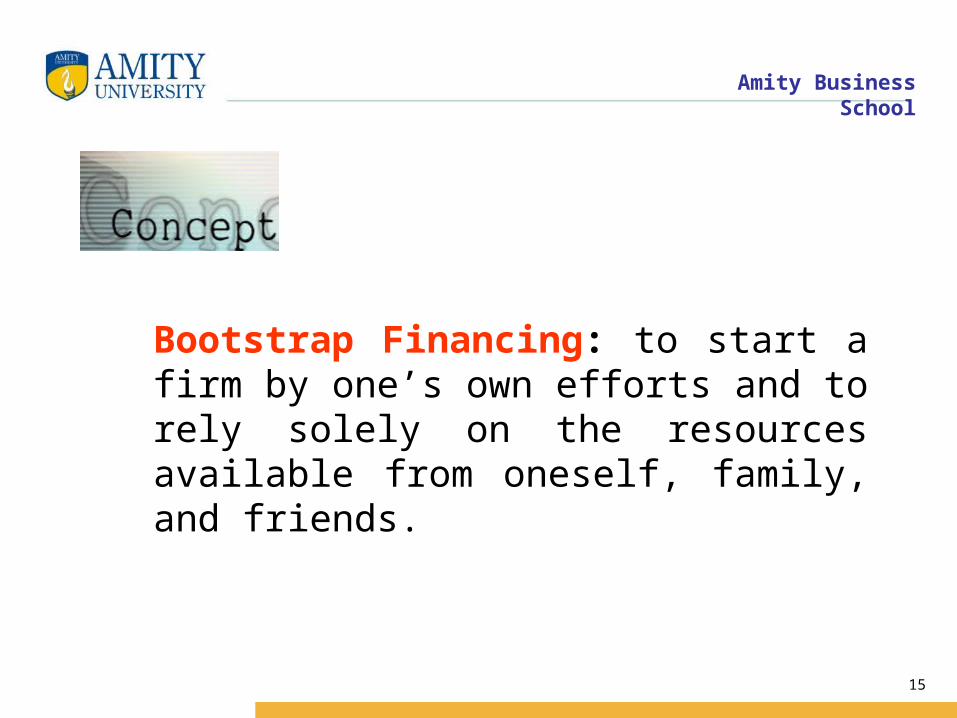

Bootstrap Financing: to start a firm by one’s own efforts and to rely solely on the resources available from oneself, family, and friends.

Amity Business School

Debt Funding

16

Amity Business School

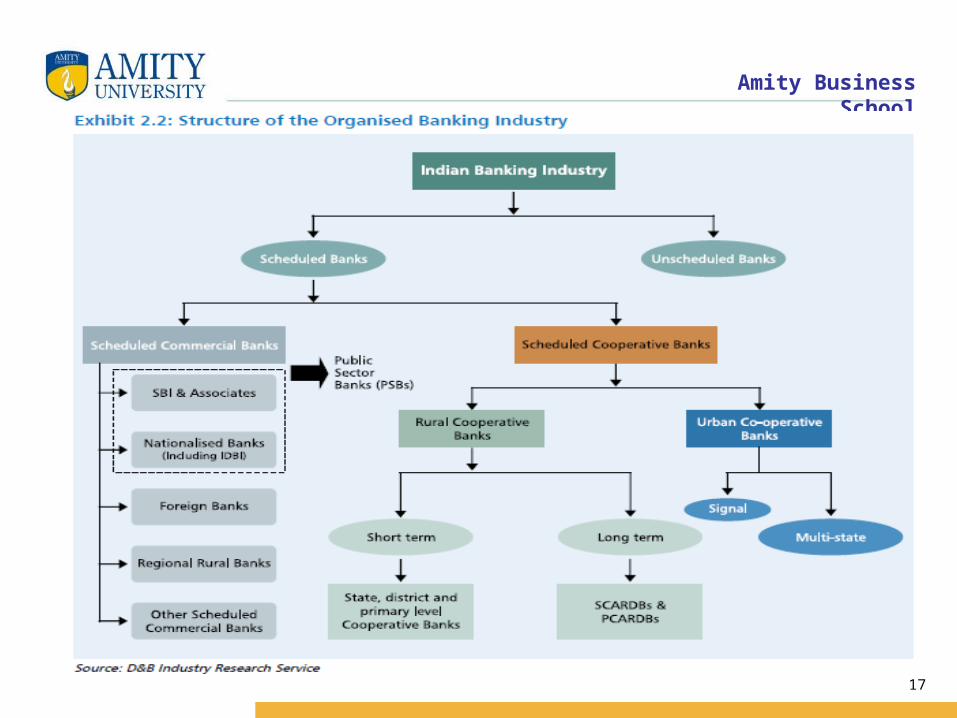

17

Amity Business School

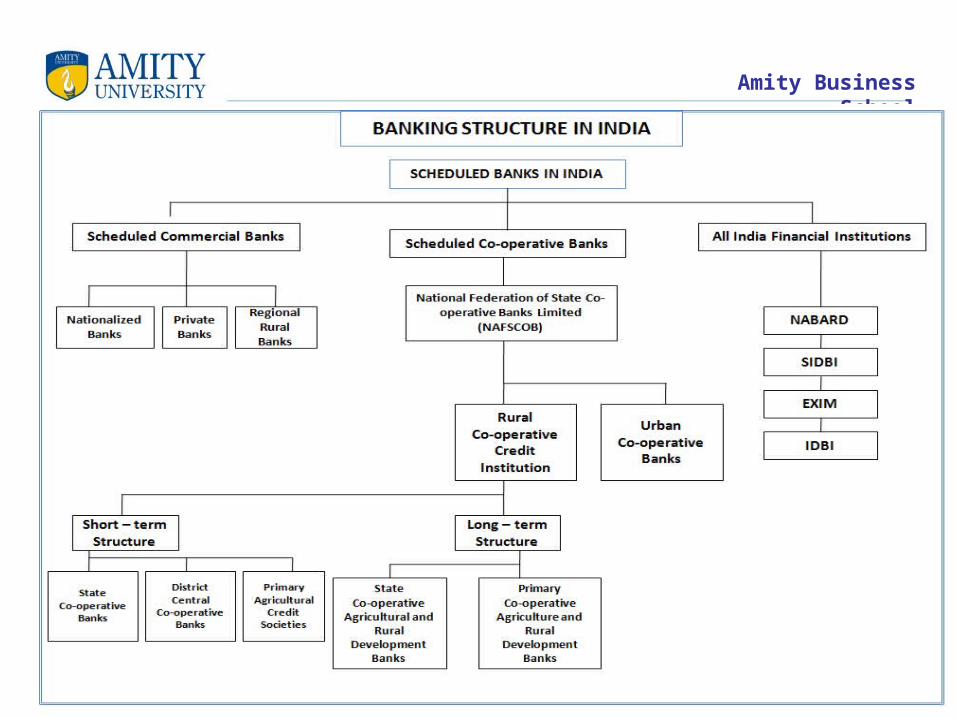

18

Amity Business School

19

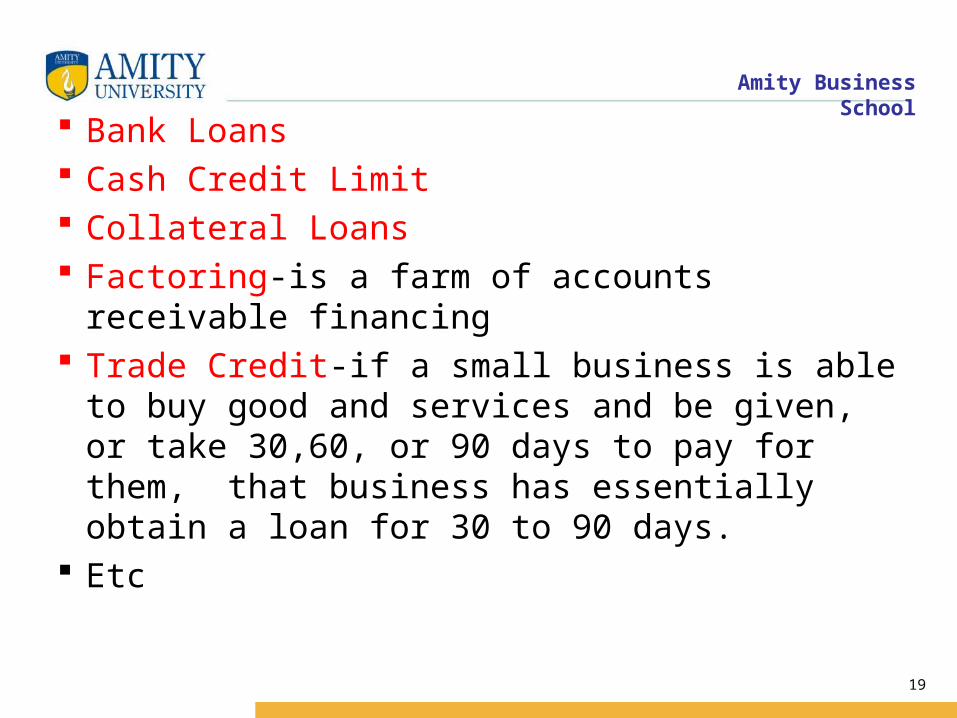

Bank Loans Cash Credit Limit Collateral Loans Factoring-is a farm of accounts receivable

financing Trade Credit-if a small business is able to buy

good and services and be given, or take 30,60, or 90 days to pay for them, that business has essentially obtain a loan for 30 to 90 days.

Etc

Amity Business SchoolCash credit• A cash credit is a short-term cash loan to a

company. A bank provides this type of funding, but only after the required security is given to secure the loan. Once a security for repayment has been given, the business that receives the loan can continuously draw from the bank up to a certain specified amount.

20

Amity Business School Line of credit

• Credit source extended to a government, business or individual by a bank or other financial institution.

• A line of credit may take several forms, such as overdraft protection, demand loan, special purpose, export packing credit, term loan, discounting, purchase of commercial bills, traditional revolving credit card account, etc.

• It is effectively a source of funds that can readily be tapped at the borrower's discretion. Interest is paid only on money actually withdrawn. (However, the borrower may be required to pay an unused line fee, often an annualized percentage fee on the money not withdrawn.) Lines of credit can be secured by collateral, or may be unsecured.

• Lines of credit are often extended by banks, financial institutions and other licensed consumer lenders to creditworthy customers (though certain special-purpose lines of credit may not have creditworthiness requirements) to address liquidity problems; such a line of credit is often called a personal line of credit. The term is also used to mean the credit limit of a customer, that is, the maximum amount of credit a customer is allowed.

21

Amity Business SchoolCash credit in India

• Banks offer cash credit accounts to businesses to finance their "working capital" requirements (requirements to buy raw materials or "current assets", as opposed to machinery or buildings, which would be called "fixed assets"). The cash credit account is similar to current accounts as it is a running account (i.e., payable on demand) with cheque book facility. But unlike ordinary current accounts, which are supposed to be overdrawn only occasionally, the cash credit account is supposed to be overdrawn almost continuously. The extent of overdrawing is limited to the cash credit limit that the bank sanctioned. This sanction is based on an assessment of the maximum working capital requirement of the organization minus the margin. The organization finances the margin amount from its own funds.

• Generally, a cash credit account is secured by a charge on the current assets (inventory) of the organization. The kind of charge created can be either pledge or hypothecation

22

Amity Business SchoolFactoring• is a financial transaction and a type of

debtor finance in which a business sells its accounts receivable (i.e., invoices) to a third party (called a factor) at a discount

• A Business will sometimes Factor its Receivable Assets to meet its present and immediate Cashneeds

• Forfaiting is a Factoring arrangement used in International Trade Finance by Exporters who wish to sell their receivables to a forfaiter

23

Amity Business School

• Factoring is not the same as invoice discounting• Factoring is the sale of receivables, whereas invoice discounting is

a borrowing that involves the use of the accounts receivable assets as collateral for the Loan

• in some other markets, such as the UK, invoice discounting is considered to be a form of factoring, involving the "assignment of receivables", that is included in official factoring statistics

• It is therefore also not considered to be borrowing in the UK. In the UK the arrangement is usually confidential in that the debtor is not notified of the assignment of the receivable and the seller of the receivable collects the debt on behalf of the factor.

• In the UK, the main difference between factoring and invoice discounting is confidentiality

24

Amity Business SchoolCollateral Loans

• In lending agreements, collateral is a borrower's pledge of specific property to a lender, to secure repayment of a loan.

• The collateral serves as protection for a lender against a borrower's default—that is, any borrower failing to pay the principal and interest under the terms of a loan obligation. If a borrower does default on a loan (due to insolvency or other event), that borrower forfeits (gives up) the property pledged as collateral, with the lender then becoming the owner of the collateral. In a typical mortgage loan transaction, for instance, the real estate being acquired with the help of the loan serves as collateral. Should the buyer fail to pay the loan under the mortgage loan agreement, the ownership of the real estate is transferred to the bank. The bank uses the legal process of foreclosure to obtain real estate from a borrower who defaults on a mortgage loan obligation. A pawnbroker is an easy and common example of a business that may accept a wide range of items

rather than just dealing with cash.

25

Amity Business School

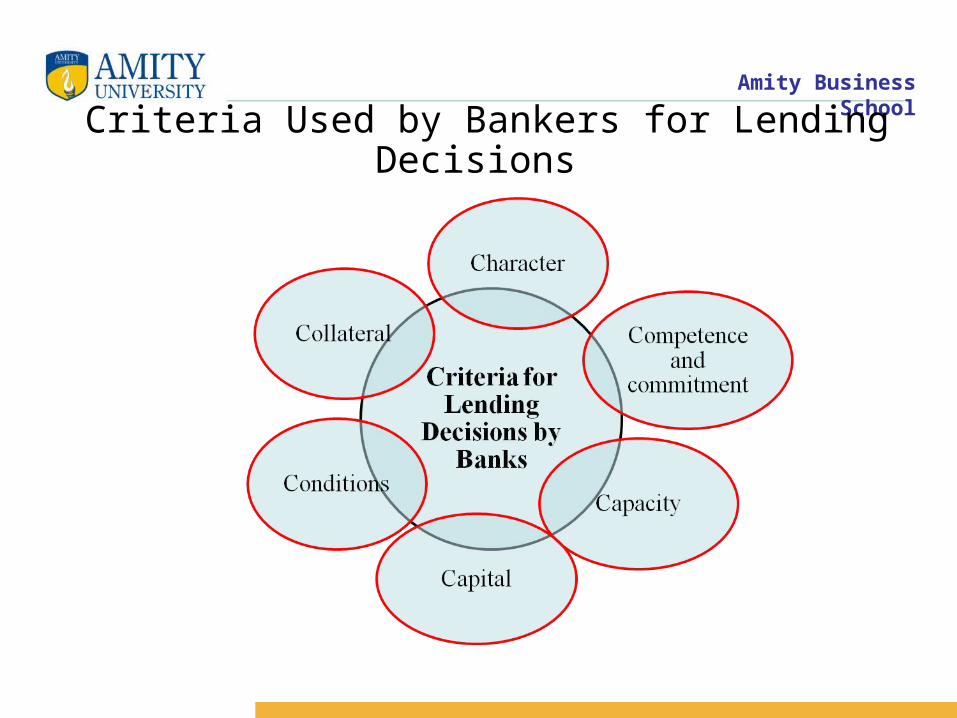

Criteria Used by Bankers for Lending Decisions

Amity Business School

27

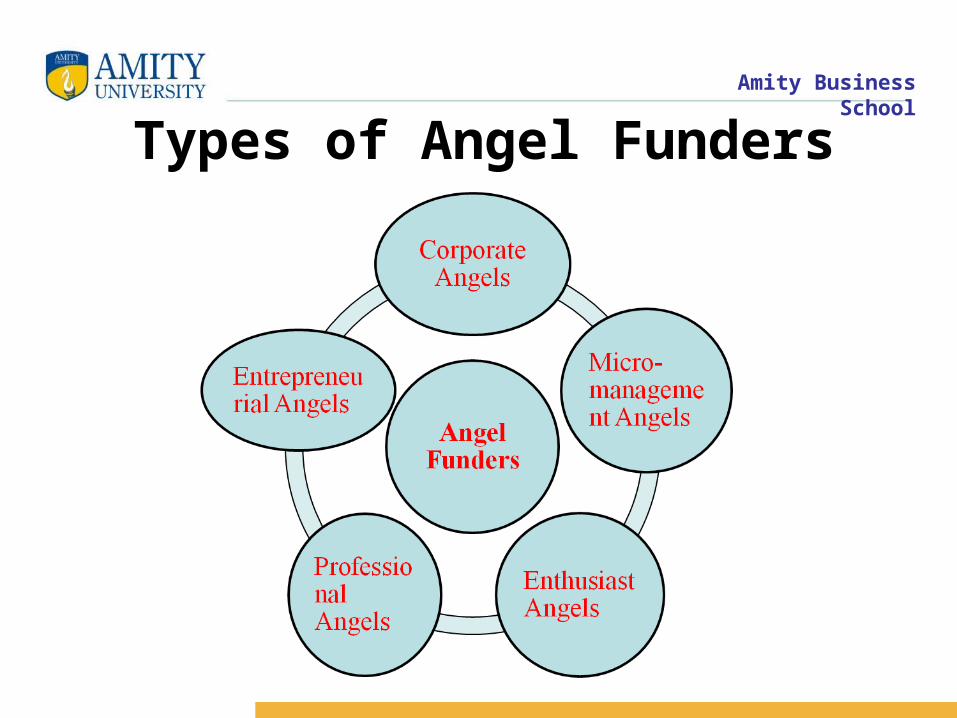

Angels are wealthy individuals, usually experienced entrepreneurs, who invest in business start-ups in exchange for equity in the new ventures.

In India: Indian Angel Network(IAN) with many chapters-Mumbai Angels, Chennai Angels

Amity Business School

Types of Angel Funders

Amity Business School

29

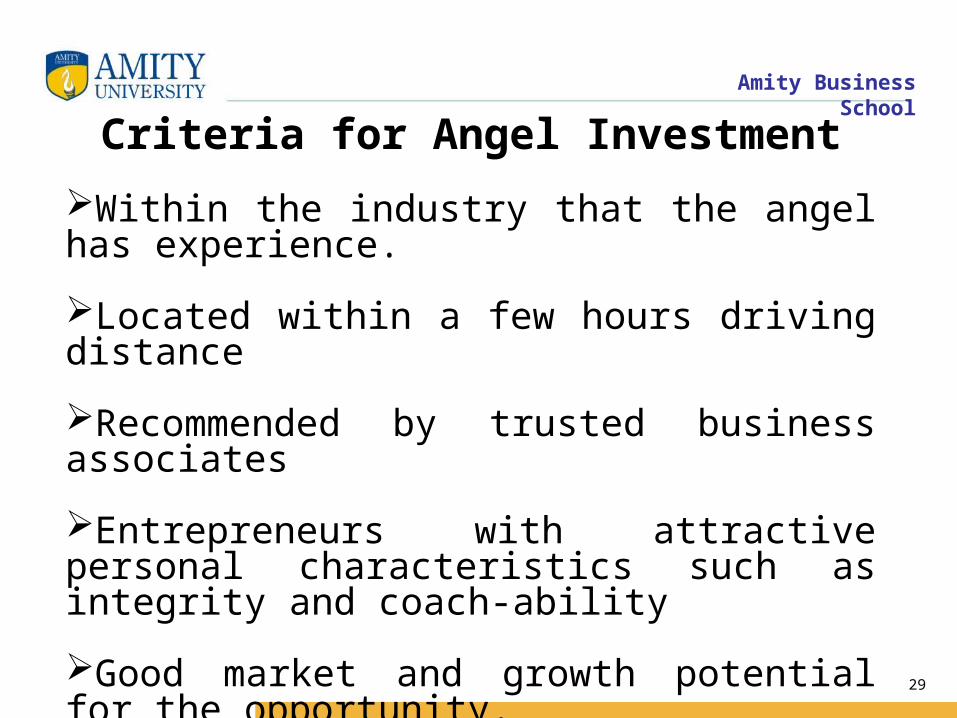

Criteria for Angel Investment

Within the industry that the angel has experience.

Located within a few hours driving distance

Recommended by trusted business associates

Entrepreneurs with attractive personal characteristics such as integrity and coach-ability

Good market and growth potential for the opportunity.

Amity Business School

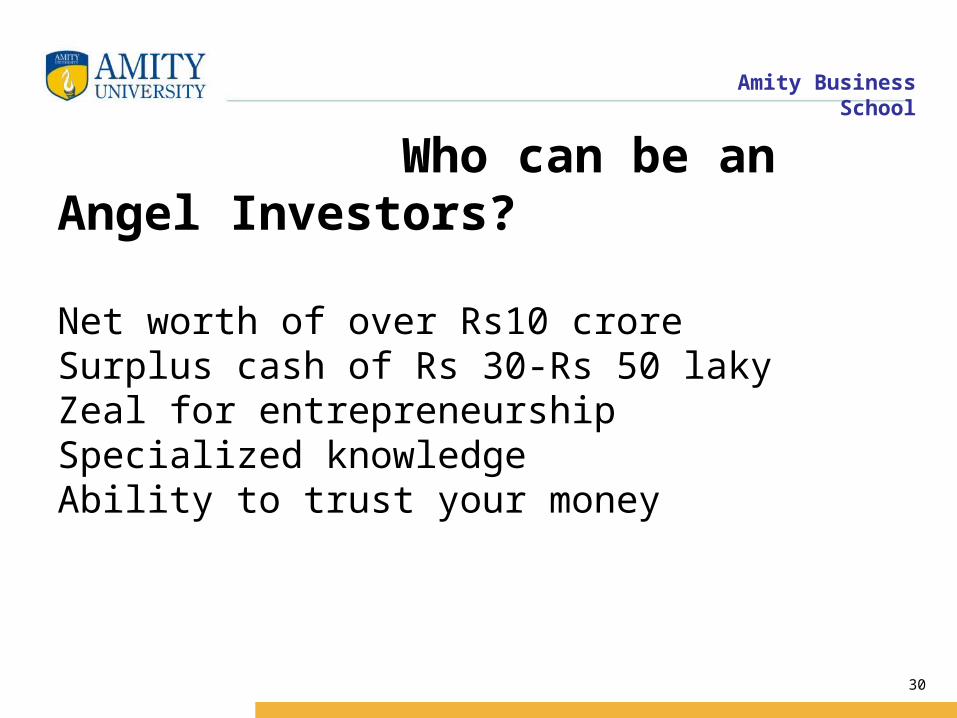

Who can be an Angel Investors?

Net worth of over Rs10 croreSurplus cash of Rs 30-Rs 50 lakyZeal for entrepreneurshipSpecialized knowledgeAbility to trust your money

30

Amity Business School

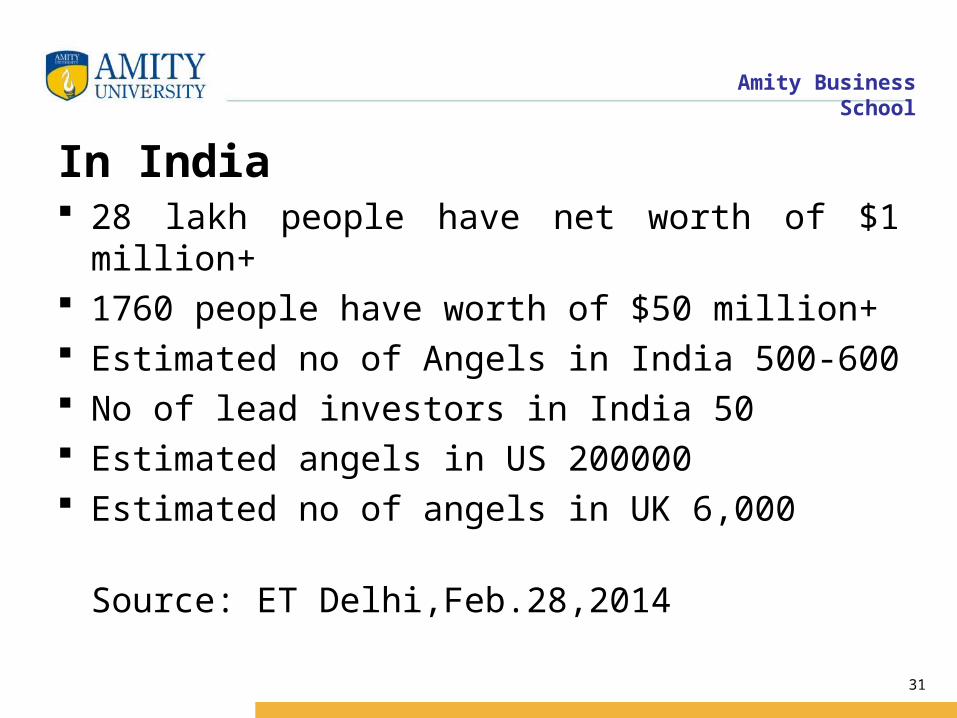

In India 28 lakh people have net worth of $1 million+ 1760 people have worth of $50 million+ Estimated no of Angels in India 500-600 No of lead investors in India 50 Estimated angels in US 200000 Estimated no of angels in UK 6,000

Source: ET Delhi,Feb.28,2014

31

Amity Business School

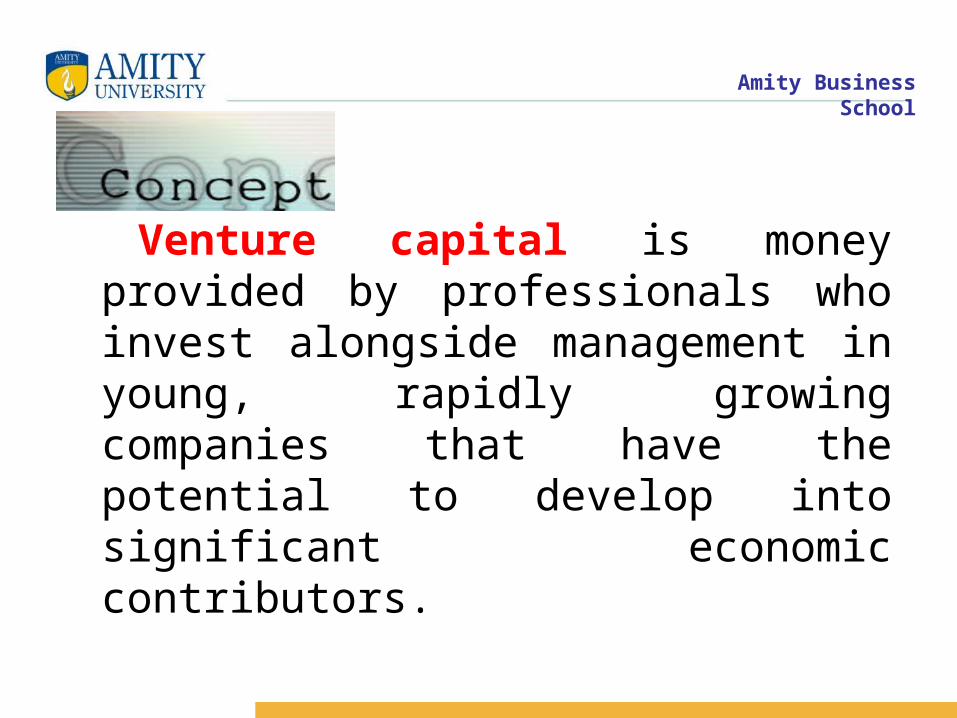

Venture capital is money provided by professionals who invest alongside management in young, rapidly growing companies that have the potential to develop into significant economic contributors.

Amity Business School

Venture capitalist generally:

Finance new and rapidly growing companies

Purchase equity securities

Assist in the development of new products or services

Add value to the company through active participation

Take higher risks with the expectation of higher rewards

Have a long-term orientation

Amity Business School

VC look for following attributes while considering a

seed capital project:

Project management skills of an entrepreneur

Technical competence on the part of investors

A very long prospectfor investment

Ability of venture capitalist to work with the scientists

and technologists as opposed to managers

Amity Business School

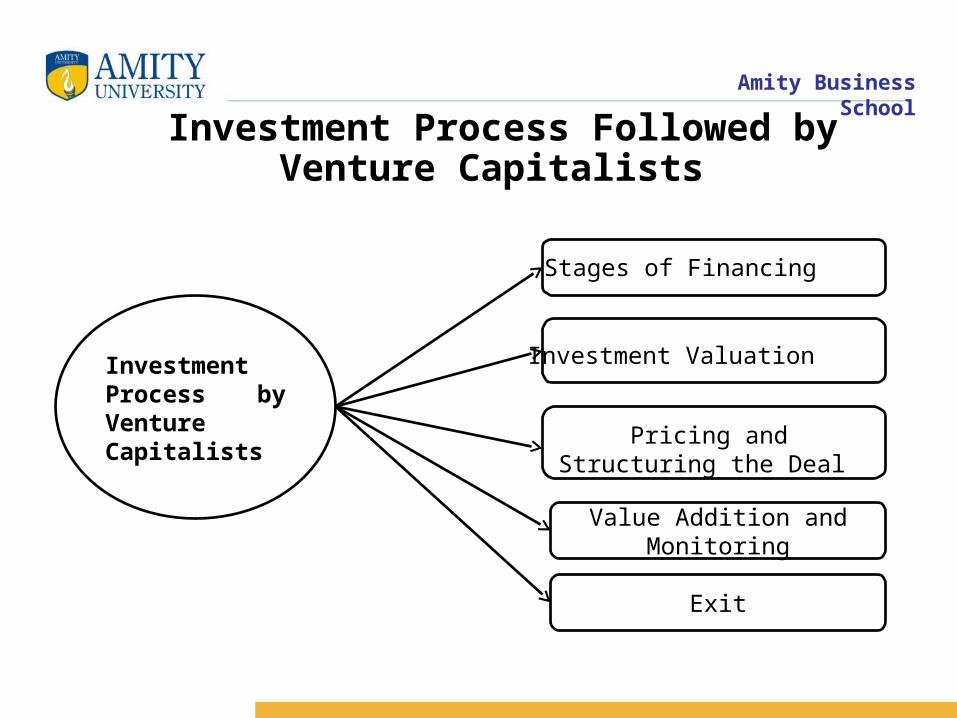

Investment Process Followed by Venture Capitalists

Value Addition and Monitoring

Exit

Pricing and Structuring the Deal

Investment Valuation

Stages of Financing

Investment Process by Venture Capitalists

Amity Business School

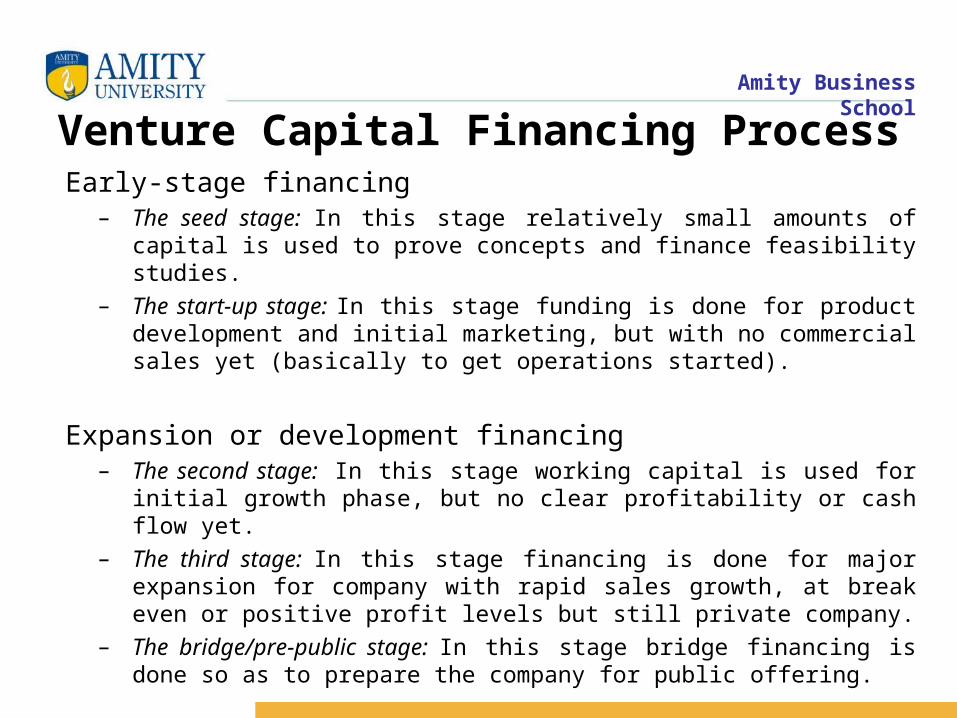

Venture Capital Financing ProcessEarly-stage financing

– The seed stage: In this stage relatively small amounts of capital is used to prove concepts and finance feasibility studies.

– The start-up stage: In this stage funding is done for product development and initial marketing, but with no commercial sales yet (basically to get operations started).

Expansion or development financing– The second stage: In this stage working capital is used for initial growth

phase, but no clear profitability or cash flow yet.

– The third stage: In this stage financing is done for major expansion for company with rapid sales growth, at break even or positive profit levels but still private company.

– The bridge/pre-public stage: In this stage bridge financing is done so as to prepare the company for public offering.

Amity Business School

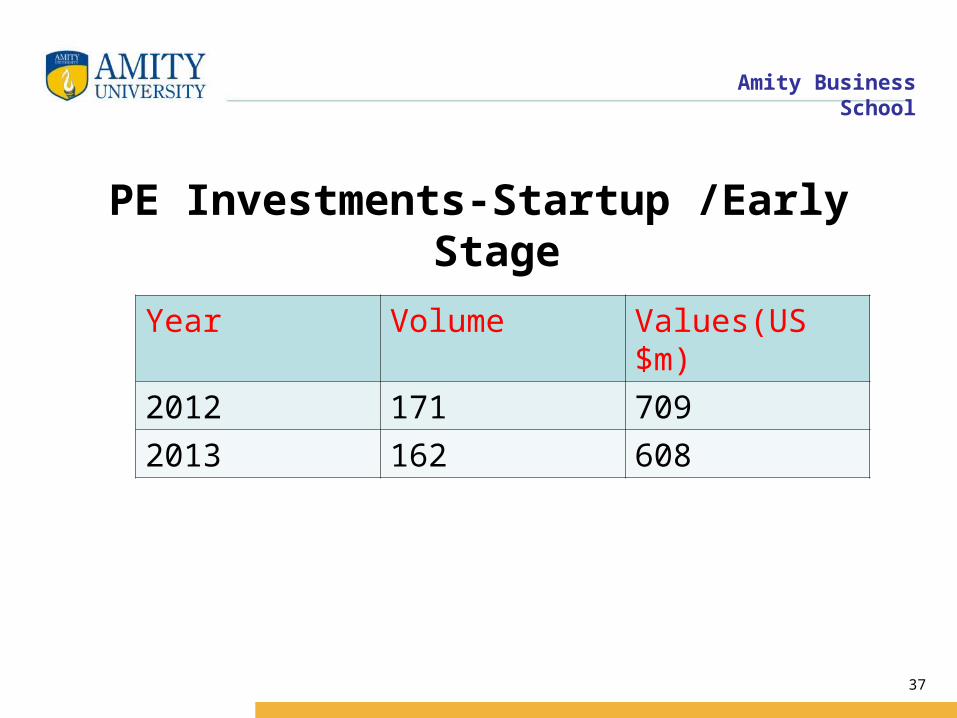

PE Investments-Startup /Early Stage

37

Year Volume Values(US $m)

2012 171 709

2013 162 608

Amity Business School

Lease Finance Equipment leasing is a process of funding that

involves the lender to buy and own equipment, and then rent it out to a business at a flat monthly rate for a specified number of months. At the end of the lease period, the business may purchase the equipment for its fair market value or a fixed or predetermined amount, continue leasing, lease new equipment or return it.