Embed Size (px)

Citation preview

Amortisation of Loans

A loan repayment can be thought of as consisting of two components:(1) interest on the outstanding loan

(2) repayment of part of the loan

This perspective of loan repayment is called amortisation.

The key to this process is the fact that the principal outstanding is the present value of the remaining payments.

1

Example

Consider the following loan: $5000 over 5 years at 12% compounded monthly.

Monthly repayment:

rr

RAn)1(1

01.0)01.1(1

500060

R

60125 ,01.01212.0 nr

2

The interest component of this payment will change (decrease) as repayments are made.

22.111$R

955.445000 R

3

For the first payment,

The principal outstanding at the beginning of the period is $5000.

:. Interest charged in that period

50 $

500001.0

Payment $111.22 Interest $50

Part repayment $61.22

4

After 3 years, (which is 36 repayments)

The principal outstanding is given by

r

rRA

n)1(1

24 payments are yet to be made.

69.2362 $

01.0

)01.1(122.111

24

A

5

So interest charged

63.23 $

69.236201.0

leaving 111.22 23.63

$ 87.59

as part repayment from the principal.

6

At the beginning of the last period:

The principal outstanding is 11 (1.01)

111.22 $ 110.120.01

A

The interest charged for the period will be

10.1 $12.11001.0

and 12.110$10.122.111

will “pay out” the remaining principal.7

The total interest paid (sometimes called the finance charge)

20.1673 $

50006022.111

A table showing the repayment analysis is called an amortisation schedule.

8

Amortisation schedule

R Principaloutstanding

Interest Payment Principalrepaid

1 5000 50 111.22 61.22

2 4938.78 49.39 111.22 61.83

3 4876.95 48.77 111.22 62.45

.

.

.

.

.

.

.

.

.

.

....

60 110.12 1.10 111.22 110.12

T 1673.20 6673.20 5000.00

9

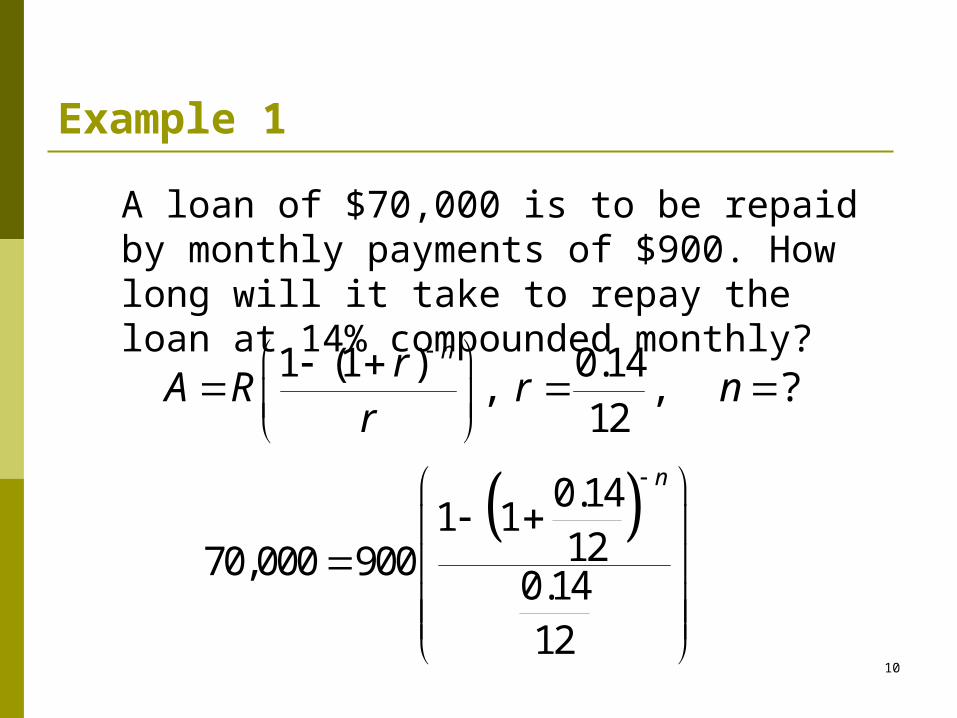

Example 1

A loan of $70,000 is to be repaid by monthly payments of $900. How long will it take to repay the loan at 14% compounded monthly?

1 (1 ) 0.14, , ?

12

nrA R r n

r

0.141 1

1270,000 9000.1412

n

10

0.141 1

1270,000 9000.1412

n

0.141 170,000 12

0.1490012

n

70,000 0.14 0.141 1

900 12 12

n

11

0.14 70,000 0.141 1

12 900 12

n

0.14 70,000 0.14ln 1 ln 1

12 900 12n

70,000 0.14

ln 1900 12 205.1486

0.14ln 1

12

n

205.1486n12

The loan would be repaid in 205.1486 months (206 months, the last repayment < $900).

This is equivalent to 17 years 2 months.

13

Example 2: Finance charge

Suppose you have the choice of taking out an $80,000 mortgage at 12% compounded monthly for either 15 years or 30 years. How much saving is there in the finance charge if you were to choose the 15-year mortgage?

Principal = 80,000

1. Taken over 15 years,

1801215 01.012

12.0 nr

14

So1801 1.01

80,0000.01

R

and14.960$R

Total interest is given by:

960.14 180 80,000 $92,825.20 15

2. Taken over 30 years3601 1.01

80,0000.01

$822.89

R

R

Total interest is given by:

822.89 360 80,000 $216,240.40

16

Interest over 15 years $92,825.20

Interest over 30 years $216,240.40

Interest saved by taking the loan over the shorter time

Taking the loan over 30 years has the advantage of lower repayments but much more money is repaid in total.

216,240.40

92,825.20$123,415.20

17

Example 3

A loan of $2000 is being amortised over 48 months at an interest rate of 12% compounded monthly. Find:

(a) the monthly payment

(b) the principal outstanding at the beginning of the 36th month

(c) the interest in the 36th payment

(d) the principal in the 36th payment

(e) the total interest paid. 18

(a) the monthly payment

48 ,01.012

12.0

)1(1

nr

r

rRA

n

...97.372000

01.0

01.112000

48

R

R

67.52R

Monthly repayments are $52.6719

b) The principal outstanding at the beginning of the 36th month.

At the beginning of the 36th period there are 13 payments remaining

The outstanding principal is $639.08

08.639

01.001.11

67.5213

A

20

(c) Interest in the 36th payment will be

(d) the principal repaid in the 36th repayment

(e) the total interest is given by

39.6$08.63901.0

28.46$39.667.52

16.528$20004867.52

21