Embed Size (px)

Citation preview

i

AN ASSESSMENT OF THE CAUSES OF NON PERFORMING LOANS IN

TANZANIA COMMERCIAL BANKS:

A CASE OF NMB BANK PLC

BY

Phides Selestine Mchopa

A Dissertation Submitted to School of Business in Partial Fulfillment of the

Requirements for the Award of Master Degree in Business Administration

(MBA - Corporate Management) of Mzumbe University

2013

ii

CERTIFICATION

We, the undersigned, certify that we have read and hereby recommend for acceptance by the Mzumbe

University, a dissertation/thesis entitled an assessment of the causes of non-performing loans in

Tanzania commercial banks; a case of NMB bank PLC, Kenyatta road branch (Mwanza), in

partial/fulfillment of the requirements for award of the degree of Master of Business Administration

of Mzumbe University.

____________________________________

Major Supervisor

____________________________________

Internal Examiner

Accepted for the Board of School of Business

______________________________________________

DEAN, BOARD OF SCHOOL OF BUSINESS

iii

DECLARATION AND COPYRIGHT

I, Phides Selestine Mchopa, declare that this Dissertation is my own original work and that it has not

been presented and will not be presented to any other university for a similar or any other degree

award.

Signature ___________________________

Date________________________________

©

This dissertation is a copyright material protected under the Berne Convention, the Copyright Act 199

and other international and national enactments, in that behalf, on intellectual property. It may not be

reproduced by any means in full or in part, except for short extracts in fair dealings, for research or

private study, critical scholarly review or discourse with an acknowledgement, without the written

permission of Mzumbe University, on behalf of the author.

iv

ACKNOWLEDGEMENT

First of all I would like to express my exceptional thanks to almighty God for energizing me and make me

able to fulfill my academic responsibilities.

The successful of this report is the result of the commitment of many individuals all of whom deserve my

appreciation. So I would like to express my sincerely gratitude to my research supervisor Jasinta Msamula

whose encouragement, tolerance, patience, and full support from the initial to the final stage enabled me

to come up with this report together with Mr. Makoye.

Also I would like to thank my Family, particularly my beloved husband Lucas Mniko, my beloved

children Lulu, Loreen and Lisa, for their courage and support for the whole time since I started my

studies.

v

ABREVIATIONS

BOT – Bank of Tanzania

GDP – Gross Domestic Product

MSE’s – Micro and Small Enterprises

NMB – National Microfinance Bank

SME’s – Small and Medium Enterprises

SPSS – Statistical Package for Social Science research

US – United States

1

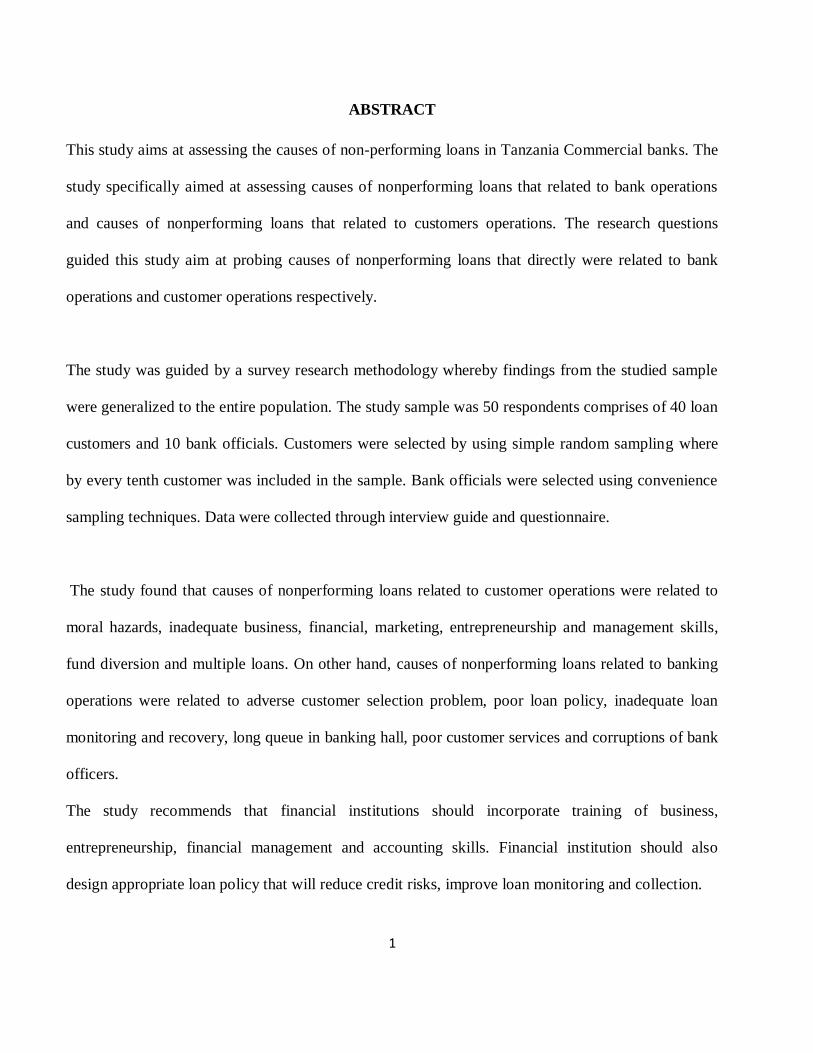

ABSTRACT

This study aims at assessing the causes of non-performing loans in Tanzania Commercial banks. The

study specifically aimed at assessing causes of nonperforming loans that related to bank operations

and causes of nonperforming loans that related to customers operations. The research questions

guided this study aim at probing causes of nonperforming loans that directly were related to bank

operations and customer operations respectively.

The study was guided by a survey research methodology whereby findings from the studied sample

were generalized to the entire population. The study sample was 50 respondents comprises of 40 loan

customers and 10 bank officials. Customers were selected by using simple random sampling where

by every tenth customer was included in the sample. Bank officials were selected using convenience

sampling techniques. Data were collected through interview guide and questionnaire.

The study found that causes of nonperforming loans related to customer operations were related to

moral hazards, inadequate business, financial, marketing, entrepreneurship and management skills,

fund diversion and multiple loans. On other hand, causes of nonperforming loans related to banking

operations were related to adverse customer selection problem, poor loan policy, inadequate loan

monitoring and recovery, long queue in banking hall, poor customer services and corruptions of bank

officers.

The study recommends that financial institutions should incorporate training of business,

entrepreneurship, financial management and accounting skills. Financial institution should also

design appropriate loan policy that will reduce credit risks, improve loan monitoring and collection.

2

TABLE OF CONTENTS

CERTIFICATION ........................................................................................................................................... i

DECLARATION AND COPYRIGHT ........................................................................................................... iii

ACKNOWLEDGEMENT; ............................................................................................................................. iv

ABREVIATIONS; ...................................................................................................................................... v ABSTRACT ................................................................................................................................................... 1

CHAPTER ONE ............................................................................................................................................. 7

INTRODUCTION .......................................................................................................................................... 7

1.1 Background of the Problem ................................................................................................................. 9 1.2 Problem Statement ............................................................................................................................. 10 1.3 Objectives of Study ........................................................................................................................... 11 1.3.1 The General Objectives ..................................................................................................................... 11 1.3.2 The specific objectives of the study ................................................................................................... 11 1.3.3 Research Question ............................................................................................................................ 11 1.4 Scope of the Study ............................................................................................................................. 11 1.5 Significance the Study ....................................................................................................................... 12 1.6 Limitations of the Study..................................................................................................................... 12

CHAPTER TWO .......................................................................................................................................... 13

LITERATURE REVIEW .............................................................................................................................. 13

2.1 Theoretical Literature Review .............................................................................................................. 13 2.1.1 The theory of Information Asymmetric in explain cause of non-performing loans ............................. 13 2.1.2 Framework for Monitoring the Development of Non-performing loans ............................................ 13 2.1.3 Relationship of Non-performing loans and Macro Economic conditions ..................................... 14 2.1.4 Relationship between Non performing loans and Eeconomic performance ........................................ 15 2.2 Empirical Literature .......................................................................................................................... 16 2.2.1 Non performing loans and Interest rates as a variable ........................................................................ 16 2.2.2 The relationship between Non performing Loans and Size of the Bank.............................................. 16 2.2.3 The relationship between Non performing Loans and Bank Policy .................................................... 17 2.2.4 The relationship between Non performing loans and Ownership concentration .................................. 17 2.2.5 The relationship of Non-performing loans and Ownership structure ........................................... 18 2.3 Conceptual Framework ........................................................................................................................ 19 2.3.1 Dependent Variable.................................................................................................................... 19 2.3.2 Independent Variable ................................................................................................................. 19 2.3.2 Variable Related to Bank Operations .......................................................................................... 19 2.3.3 Variable Related to Customer Operations ................................................................................... 19 2.4 Research Gap ...................................................................................................................................... 21

CHAPTER THREE ....................................................................................................................................... 22

3

RESEACH METHODOLOGY ..................................................................................................................... 22

3.1 Research Design ................................................................................................................................ 22 3.2 Study Area......................................................................................................................................... 22 3.3 Units of Study.................................................................................................................................... 23 3.4 Population of the Study ...................................................................................................................... 23 3.5 Sampling Frame ................................................................................................................................ 23 3.6 Sample size ....................................................................................................................................... 23 3.7 Sampling technique ........................................................................................................................... 24 3.8 Data Collection Method ..................................................................................................................... 24 3.8.1 Primary Data .................................................................................................................................... 24 3.8.2 Secondary Data ................................................................................................................................. 24 3.8.3 Field Experience ............................................................................................................................... 24 3.9 Research Methods ............................................................................................................................. 25 3.9.1 Quantitative Research Methodology.................................................................................................. 25 3.10 Tools of Data Collection .................................................................................................................... 26 3.11 Measurement and measuring scale ..................................................................................................... 26 3.12 Data Reliability and Validity .............................................................................................................. 26 3.12.1 Test of Reliability ...................................................................................................................... 26 3.12.2 Test of Validity .......................................................................................................................... 26

Data Editing .................................................................................................................................................. 27

Data Processing............................................................................................................................................. 27

CHAPTER 4 ................................................................................................................................................. 28

4.0 FINDINGS PRESENTATION AND ANALYSIS ................................................................................... 28

4.1. DEMOGRAPHIC CHARACTERISTICS OF RESPONDENTS ......................................................... 28 4.1.1 Primary occupation of respondents.................................................................................................... 28

5.0 DISCUSSION OF FINDINGS ................................................................................................................ 39

5.1 Demographic Characteristics of Respondents ....................................................................................... 39 5.1.1 Analysis of the sample ...................................................................................................................... 39 5.1.1.1 Primary Occupation of respondents ................................................................................................ 39 5.1.1.2. Working capacity of respondents .................................................................................................. 40 5.1.1.3 Education level of the respondents ................................................................................................. 40 5.1.1.4 Reasons for starting business.......................................................................................................... 41 5.1.4 Reasons for choosing type of business .............................................................................................. 42 5.1.1.5 Possibility for leaving the current job ............................................................................................. 43 5.1.1.6 Ways of starting business; .............................................................................................................. 44 5.1.1.7 Source of starting business; ............................................................................................................ 45 5.1.1.8 Marital status ................................................................................................................................. 46 5.1.1.9 Sources of credit ............................................................................................................................ 46 5.1.10 Critical business problem; ............................................................................................................... 47 5.1.1.11 Income obtained from business; ................................................................................................... 48 5.1.12 Change in amount of business ......................................................................................................... 48

4

5.2. CAUSES OF NON-PERFORMING LOANS RELATED TO CUSTOMERS OPERATION .................. 50

5.2.1 General business management skills ................................................................................................. 50 5.2.2. Financial Management Skills ........................................................................................................... 50 Figure 5.2.2 financial management skills ................................................................................................... 51 5.2.3 Accounting and book- keeping skills ................................................................................................. 51 5.2.4 Sales and marketing skills ................................................................................................................. 52 4.2.5 Entrepreneurship skills...................................................................................................................... 52 4.2.6. Transport services skills ................................................................................................................... 53

5.3. CAUSES OF NON-PERFORMING LOANS RELATED TO BANK OPERATIONS ............................ 57

SUMMARY, CONCLUSSION AND RECOMENDATION ......................................................................... 58

6.1. SUMMARY ....................................................................................................................................... 58

Financial Management Skills ............................................................................................................. 58

Accounting and book- keeping skills.................................................................................................. 58

Entrepreneurship skills ...................................................................................................................... 59

Transport services skills ..................................................................................................................... 59 6.1.3 Causes of non-performing loans related to Bank Opoperations .......................................................... 59 6.2 Conclusion; ......................................................................................................................................... 59 6.3 Recommendations; .............................................................................................................................. 60

Reference ...................................................................................................................................................... 62

5

LIST OF TABLES

Table 4.1.1 Primary Occupation of Respondent……………………………..……32

Table 4.1.2: Respondents working capacity………………………………………..33

Table 4.1.3 Education level of respondent…………………………………………33

Table 4.1.4 Reasons for starting business…………………………………….……34

Table 4.1.5 Reason for choosing business………………………………………….34

Table 4.1.8 Source of money for starting…………………………………………..36

Table 1.4.9 marital status of respondent……………………………………….…..36

Table 4.1.10 Source of credits for business………………………………….………37

Table 4.1.11 Critical business problem…………………………………………...…37

Table 4.1.12 Amount of income received from Business……………………………38

Table 4.1.13 Change in volume of business………………………………………….38

Table 4.1.14 Customers of business………………………………………………….48

Table 4.2.1 General business management skills….………………………………..39

Table 4.2.2 Financial management skills……………………………….…………...40

Table 4.2.3 Awareness of accounting and book keeping………………….………...40

Table 4.2.4 Sales and marketing skills…………………………………………….....41

Table 4.2.5 Received service of awareness of Entrepreneurship skills……………...41

6

LIST OF FIGURES

Figure 5.1.1 Primary occupation of respondents…………………...……..…43

Figure 5.1.2 working capacity of the respondents…………………….…….43

Figure 5.1.3 Education level of respondents………………………….……..45

Figure 5.1.4 Reasons for starting business……………………………..……46

Figure 5.1.4 Reason for choosing Business………………………….……....46

Figure 5.1.5 Possibility for leaving current business……………………..….48

Figure 5.1.6 Ways of starting business………………………………….…...48

Figure 5.1.7 Sources of starting business………………………………….…49

Figure 5.1.8 Marital status…………………………………………………....50

Figure 5.1.9 Source of credit ………………………………………………….51

Figure 5.1.10 Critical business problems………………………………………..51

Figure 5.1.11 Amount of income obtained from Business……………………...52

Figure 5.1.12 Change in amount of business……………………………………53

Figure 5.2.1 Received general business management skills……………………54

Figure 5.2.2 Financial management skills……………………………………..55

Figure 4.2.3 Awareness of accounting and book keeping……………………...56

Figure 5.2.4 Awareness of sales and marketing skills………………………….57

Figure 5.3.1 Non-performing loans related to bank operation ………………...58

Figure 4.2.6 Transport services skills……………………………………..……58

7

CHAPTER ONE

INTRODUCTION

This study aims at assessing the causes of non-performing loans in Tanzania Commercial bank. The

study specifically aims at assessing causes of nonperforming loans that related to bank operations and

causes of nonperforming loans that related to customers operations.

Loans form 80% portion of the total assets in commercial banks in Tanzania (BOT annual reports,

2012). These assets generate huge interest income for banks which to a large extent determines the

financial performance of banks. However, some of these loans usually fall into non-performing status

and adversely affect the performance of banks. In view of the critical role banks play in an economy,

it is essential to identify causes of non-performing loans. This is because non-performing loans can

affect the ability of banks to play their role in the development of the economy. The study focused on

National Microfinance Bank Abbreviated as NMB due to the reason that NMB bank has more than

140 branches across Tanzania, the case of Kenyatta road Mwanza branch.

According to NMB Credit Policy 2012, a non-performing loan is a loan that is in default or close to

being in default. Many loans become non-performing after being in default for 90 days. The policy

continues to describe that “A loan is nonperforming when payments of interest and principal are past

due by 90 days or more, or at least 90 days of interest payments have been capitalized, refinanced or

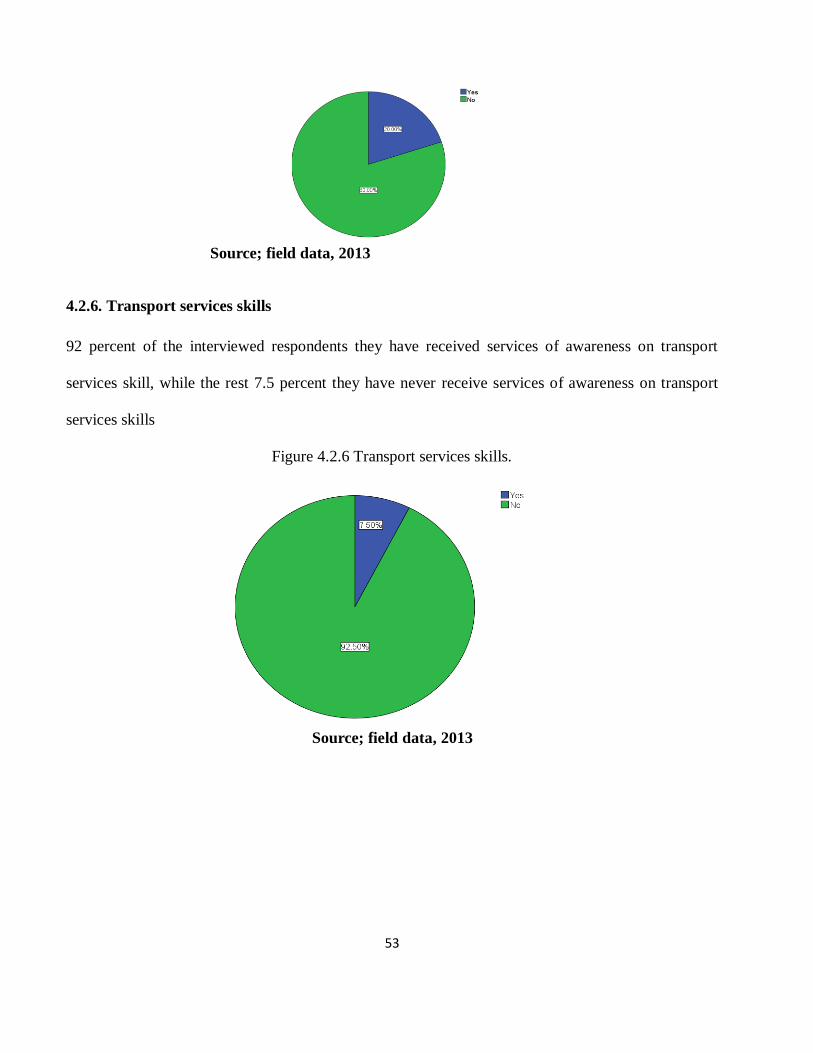

delayed by agreement, or payments are less than 90 days overdue.

A financial intermediary is an institution that acts as an intermediary by matching supply and demand

of funds (Beck, 2001). Heffernan (1996) defines banks as intermediaries between depositors and

borrowers in an economy which are distinguished from other types of financial firms by offering

deposit and loan products. Bossone (2001) agrees arguing that banks are special intermediaries

because of their unique capacity to finance production by lending their own debt to agents willing to

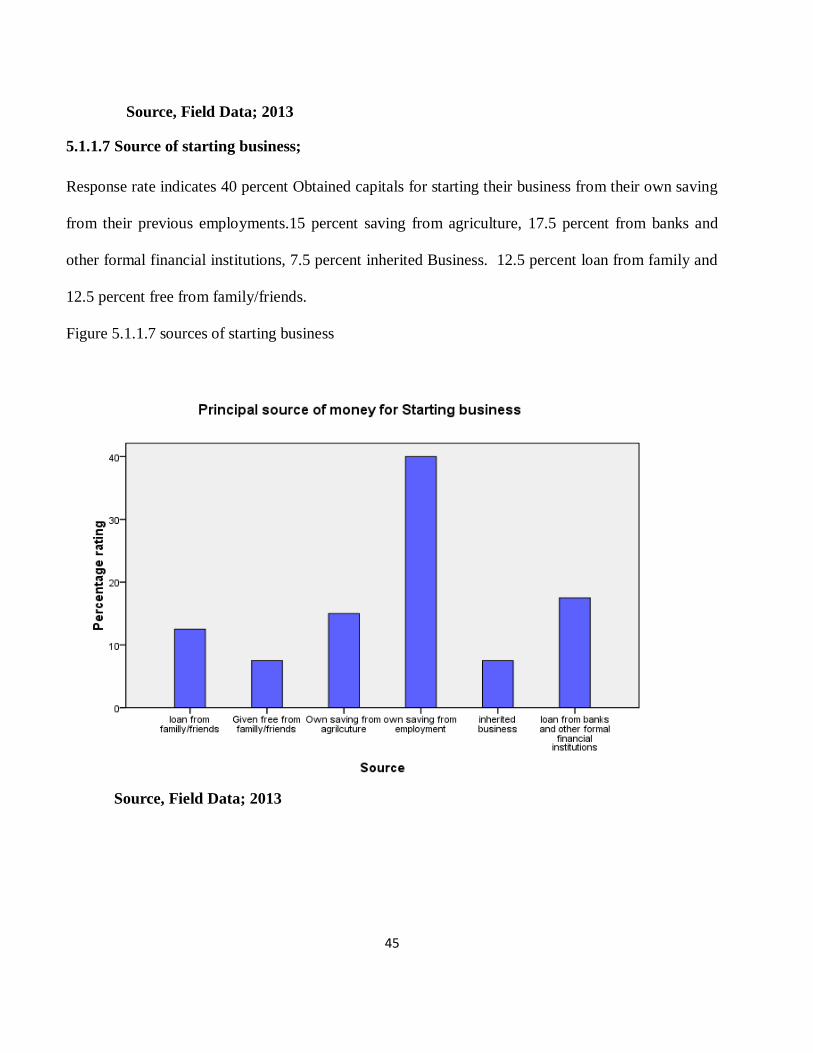

accept it and to use it as money.

8

Commercial banks are the dominant financial institutions in most economies (Rose, 1997). Greuning

and Bratanovic (2003), argue that commercial banks play a critical role to emerging economies where

most borrowers have no access to capital markets. Well functioning commercial banks accelerate

economic growth, while poorly functioning commercial banks are an impediment to economic

progress and aggravate poverty (Barth et.al, 2001; Khan and Senhadji, 2001) in Richard (2011).

The traditional role of a bank is lending and loans make up the bulk of their assets (Njanike, 2009).

According to the research by Havrilesky and Boorman (1994), interest on loans contributes

significantly to interest income of commercial banks. Reed and Gill (1989) pointed out that

traditionally 85 percent of commercial banks‟ income is contributed by interest on loans. Loans

therefore represent the majority of a bank’s asserts (Saunders and Cornett, 2005). Lending is not an

easy task for banks because it creates a big problem which is called non performing loans (Chhimpa

J, 2002) as cited in (Upal, 2009). Due to the nature of their business, commercial banks expose

themselves to the risks of default from borrowers (Waweru and Kalami, 2009).

According to Alton and Hazen (2001) non performing loans are those loans which are ninety days or

more past due or no longer accruing interest. Hennie (2003) agrees arguing that non performing loans

are those loans which are not generating income. This is further supported by Caprio and Klingebiel

(1996), cited in Fofack (2005), who define non performing loans as those loans which for a relatively

long period of time do not generate income that is, the principal and or interest on these loans have

been left unpaid for at least ninety days. Non- performing loans are also commonly described as loans

in arrears for at least ninety days (Guy, 2011). Therefore in this study, non performing loans are loans

that are ninety or more days delinquent in payments of interest and/or principal (Bexley and

Nenninger, 2012).

The term “bad loans” as described by Basu (1998) in Fofack (2005) is used interchangeably with

non- performing and impaired loans. Berger and De Young, (1997) also consider these types of loans

as “problem loans”. In effect, these would be considered bad or toxic assets on the bank’s books

(Bexley and Nenninger, 2012). These descriptions were used interchangeably during the study.

According to Berger and De Young (1997), non performing loans could be injurious to the financial

performance of banking institutions.

9

According to Kroszner (2002) in Waweru and Kalami (2009), non-performing loans are closely

associated with banking crises. Greenidge and Grosvenor (2010), argue that the magnitude of non-

performing loans is a key element in the initiation and progression of financial and banking crises.

Guy (2011) agrees arguing that non performing loans have been widely used as a measure of asset

quality among lending institutions and are often associated with failures and financial crises in both

the developed and developing world. Reinhart and Rogoff (2010) as cited in Louzis et al (2011) point

out that non- performing loans can be used to mark the onset of a banking crisis. Despite ongoing

efforts to control bank lending activities, non performing loans are still a major concern for both

international and local regulators (Boudriga et al, 2009)

1.1 Background of the Problem

Over the years, there have been an increased number of significant bank problems in both, matured as

well as emerging economies (Brownbridge and Harvey, 1998; Basel, 1999, 2004) cited in Richard

(2011). Bank problems, mostly failures and financial distress have afflicted numerous banks, many of

which have been closed down by regulatory authorities (Brownbridge, 1998). This in turn led to

contraction of activities, decline in output, and imposition of substantial costs on the economy

(Chijoriga, 1997; Brownbridge and Harvey, 1998) cited in Richard (2011). Borio and Lowe (2002)

observed that the cost of banking crises in terms of output loss has been high; typically double digit

percentage of GDP

Studies in other countries show that most of bank failures have been caused by non performing loans

(Brownbridge, 1998). Ahmad (2002), in analyzing the Malaysian financial system, reported a

significant relationship between credit risk and financial crises and concluded that credit risk had

already started to build up before the onset of the 1997 Asian financial crisis, and became more

serious as non performing loans increased. Li (2003) and Fofack (2005) also found this relationship

to be significant. There is evidence that the level of non -performing loans in the US started to

increase substantially in early 2006 in all sectors before the collapse of the sub-prime mortgage

market in August 2007 (Greenidge and Grosvenor, 2010).

10

Nishimura et al (2001) studied the situation in Japan and concluded that some of the loans made to

companies during the bubble era became non- performing when the bubble burst. The findings of

Caprio and Klingebiel (2002) cited in Fofack (2005), show that in Indonesia, non-performing loans

represented about 75% of total loan assets which led to the collapse of over sixty banks in 1997.

While some countries such as Sweden, Norway, Finland, Australia and Spain do not seem to be

exposed to non performing loans (less than 1 percent) other countries such as Egypt, Nigeria,

Philippines, Morocco, Algeria and Tunisia (more than 15 percent) suffer severely from bad loans

(Boudriga et al, 2009).

Palubinskas and Stough (1999) note that the failure of a bank is mainly seen as a result of

mismanagement because of bad lending decisions made with respect to wrong appraisal of credit

status, or the repayment of non-performing credits and excessive focus on giving loans to certain

customers. Goodhart et al (1998) also state that poor credit control, which results in undue credit r isk,

causes bank failure. Chimerine (1998) adds that a bad lending tradition leads to a large portfolio of

unpaid loans. This results in insolvency of banks and reduces funds available for fresh advances,

which eventually causes a financial crisis. Goodhart et al. (1998) add connected lending to the causes

of bank failure. Palubinskas and Stough (1999) note that lack of dependable financial information on

borrowers to help in assessing creditworthiness causes a bank failure.

1.2 Problem Statement

According to the Mid-Year Fiscal Policy Statement (2012) the upward trend in non-performing loans

and recent bank failures in Tanzania is a cause for concern. Despite lessons obtained from the 2008

World financial crisis, banks are still suffering from non performing loans.

The loan-to-deposit ratio of NMB, calculated on the basis of total bank deposits increased from 84.6

percent in May 2012 to 86.2 percent in December 2012 (NMB Loan Report, 2012). According to the

Mid-Year Quarterly SME loan performance Statement presented on the 18th of July, non-performing

loans were 9.9 percent as at 30 June 2012. The report also indicates that non performing loans in

NMB Bank increased from 6 percent on average at end-December 2011 to 8 percent at end-June

2012. This is higher than the prudential threshold of 2 percent stipulated in Basel II (Basel, 2004;

11

ADF, 2012). Non-performing loans could rise further with the ongoing deceleration in economic

activity. This gives a reasonable concern for scholars to assess causes of nonperforming loans in

commercial bank. The study assessed casuses related to both banking and customer operations.the

study area was NMB Kenyatta Road Branch located in Mwanza City Tanzania.

1.3 Objectives of Study

1.3.1 The General Objectives

The general objective of the study is to assess the causes of non-performing loans in Tanzania

commercial banks.

1.3.2 The specific objectives of the study

The specific objectives of the study is

1.3.2.1 To assess the causes of non- performing loans related to banking operations

1.3.2.2 To assess the causes of non- performing loans related to customers operations,

1.3.3 Research Question

The study addressed the following research questions

1.3.3.1 How do bank- related causes contribute to non-performing loans?

1.3.3.2 How do customers-related causes contribute to non-performing loans?

1.4 Scope of the Study

The study focuses on the causes of non-performing loans that related to banking and customers

operation. The study area is NMB Bank Limited; one of Tanzania largest banks in terms of deposit

and branch network. This is premised on the fact that the Bank has been operating long enough to

give the kind of academic insight the study seeks to offer. Besides, the bank lends to almost all the

major sectors of the economy. Again, the nation-wide operation of the bank presents an opportunity

for a national outlook of the issues under the study.

12

1.5 Significancece the Study

The findings of this study added new knowledge to the existing knowledge gap of causes of non-

performing loans related to banking and customer operations. The study is of benefits to Banking

monitoring master plan and indicator information, financial institutions, financial markets, Policy

maker, business community, and the community at large. The study is going to explore and

recommends potential areas that bankers and customers need to put more efforts when utilizing loans

services. On the other hand, policy makers benefited in the sense that, the findings provided informed

suggestion on how credit policy should be improved to accommodate the causes of non-performing

loans related to bank operations and causes of non-performing loans related to customer operations.

With good and sound credit policy and easy implementation of the policies, more individuals,

businesses, and the community at large will be able to access, utilize and benefit from financial

capital service.

1.6 Limitations of the Study

This study was limited by interruption of our respondents by customers especially in collection of

data. This is due to the fact that as we were collecting data in their working place (shops) so data

collection was sometimes interrupted by customers who come to buy products in their shops, so it

takes a very long time to complete a single questionnaire.

But also the study face the limitation of respondents (especially SME’s customers) they afraid

providing cooperation thinking that we were government agency trying to investigate their income for

the aim of deducting high taxes from their business. So, researcher was required to educate them on

the reasons for conducting this study. Also shortage of funds was among limitations.

1.7 Organization of the study;

This study is organized in five chapters. Chapter one presents background introduction, problem

statement, research objectives, research questions and significance of the study

Chapter two review of literature both theoretical and empirical related to cause of non performing

loans in commercial banks, Chapter three presents study methodology, chapter four presents research

findings and lastly chapter five presents discussion, summary and conclusion

13

CHAPTER TWO

LITERATURE REVIEW

2.1 Theoretical Literature Review

2.1.1 The theory of Information Asymmetric in explain cause of non-performing loans

The theory of asymmetric information tells us that it may be difficult to distinguish well from bad

borrowers (Auronen, 2003) in Richard (2011), which may result into adverse selection and moral

hazards problems. The theory explains that in the market, the party that possesses more information

on a specific item to be transacted (in this case the borrower) is in a position to negotiate optimal

terms for the transaction than the other party (in this case, the lender) (Auronen, 2003) in Richard

(2011). The party that knows less about the same specific item to be transacted is therefore in a

position of making either right or wrong decision concerning the transaction. Adverse selection and

moral hazards have led to significant accumulation of non-performing loans in banks (Bester, 1994;

Bofondi and Gobbi, 2003).

2.1.2 Framework for Monitoring the Development of Non-performing loans

In scholar studies, problem loans are often used as an exogenous variable to explain other banking

outcomes such as bank performance, failures, and bank crises. However, some studies investigate

problem loans as an endogenous variable; GDP growth, inflation and interest rates are common

macro-economic factors, while size and lending policy are micro-economic. These variables are by

no means exhaustive, but they provide a useful framework for monitoring the development of non-

performing loans (Guy, 2011).

More recent researches started examining the fragility of the Argentinean Banking system over the

1993-1996 period; they argue that non performing loans are affected by both bank specific factors

and macroeconomic factors. To separate the impact of bank specific and macroeconomic factors, the

14

authors employ survival analysis. Using a dynamic model and a panel dataset covering the period

1985-1997 to investigate the determinants of problem loans of Spanish commercial and saving banks,

Salas and Saurina (2002) reveal that real growth in GDP, rapid credit expansion, bank size, capital

ratio and market power explain variation in non- performing loans. Furthermore, Jimenez and Saurina

(2005) examine the Spanish banking sector from 1984 to 2003; they provide evidence that non

performing loans are determined by GDP growth, high real interest rates and lenient credit terms.

This study attributes the latter to disaster myopia, herd behaviour and agency problems that may

entice bank managers to lend excessively during boom periods (Guy, 2011).

2.1.3 Relationship of Non-performing loans and Macro Economic conditions

Meanwhile, Rajan and Dhal (2003) utilize panel regression analysis to report that favourable

macroeconomic conditions and financial factors such as maturity, cost and terms of credit, banks size,

and credit orientation impact significantly on the non performing loans of commercial banks in India.

Babihuga (2007), in an IMF working paper, explores the relationship between several

macroeconomic variables and financial soundness indicators (capital adequacy, profitability, and

asset quality) based on country aggregate data.

She explained the cross-country heterogeneity by differences in interest rates, inflation, and other

macroeconomic factors. However, the study does not consider the impact of industry specific drivers

of problem loans. Most empirical studies examine the influence of the macroeconomic environment

on non performing loans (Louzis et al, 2011). Rinaldi and Sanchis-Arellano (2006) analyze household

non performing loans for a panel of European countries and provide empirical evidence that

disposable income, unemployment and monetary conditions have a strong impact on non performing

loans.

Berge and Boye (2007) find that problem loans are highly sensitive to the real interest rates and

unemployment for the Nordic banking system over the period 1993–2005. Lawrence (1995) examines

the theoretical literature of life-cycle consumption model and introduces explicitly the probability of

default. This model implies that borrowers with low incomes have higher rates of default due to

increased risk of facing unemployment and being unable to settle their obligation. Additionally, in

equilibrium, banks charge higher interest rates to riskier clients. Rinaldi and Sanchis-Arellano (2006)

15

extend Lawrence’s model by assuming that agents borrow in order to invest in real or financial assets.

They argue that the probability of default depends on current income and the unemployment rate,

which is linked to the uncertainty regarding future income and the lending rates.

Breuer (2006), using Bankscope data, analyses the impact of legal, political, sociological, economic,

and banking institutions on problem bank loans. Nevertheless, her study suffers from a

representativeness bias due to the fact that Bankscope data on non performing loans are only

available for a very limited number of countries and for a few numbers of banks. Other studies

focusing on the macroeconomic determinants of non-performing loans include Cifter et al. (2009),

Nkusu (2011) and Segoviano et al. (2006).

2.1.4 Relationship between Non performing loans and Eeconomic performance

Carey (1998) argues that “the state of the economy is the single most important systematic factor

influencing diversified debt portfolio loss rates” (Carey, 1998, p. 1382). Quagliarello (2007) finds

that the business cycle affects non performing loans for a large panel of Italian banks over the period

1985–2002. Furthermore, Cifter et al. (2009) provides empirical evidence for a lagged impact of

industrial production on the number of non performing loans in the Turkish financial system over the

period 2001–2007.

Salas and Saurina (2002) estimate a significant negative contemporaneous effect of GDP growth on

non performing loans and infer the quick transmission of macroeconomic developments to the ability

of economic agents to service their loans (Bangia et al., 2002; Carey, 2002). Nkusu (2011)

investigating the macroeconomic determinants of loan defaults through panel regressions and panel

vector autoregressive models. The author suggests that hike in interest rates result in deterioration of

borrower’s repayment capacity and hence, cause of increase in non-performing loans.

There is significant empirical evidence to suggest that local economic conditions explain to some

extent, the variation in non-performing loans experienced by banks (Keeton and Morris, 1987; Sinkey

and Greenwalt, 1991; Salas and Saurina, 2002; Rajan and Dhal, 2003) as cited in (Greenidge and

Grosvenor, 2010) Research conducted in the Caribbean includes that of Khemraj and Pasha (2009),

16

who examined the determinants of non-performing loans in Guyana. The empirical results revealed

that with the exception of the inflation rate and bank size, all other factors have a significant

relationship with the non performing loan ratio (Greenidge and Grosvenor, 2010).

2.2 Empirical Literature

2.2.1 Non performing loans and Interest rates as a variable

Causes and treatment of non-performing loans were studied in detail by Bloem and Gorter (2001).

They agreed that “bad loans” may considerably rise due to abrupt changes in interest rates. They

discussed various international standards and practices on recognizing, valuing and subsequent

treatment of non-performing loans to address the issue from view point of controlling, management

and reduction measures.

A study conducted by Espinoza and Prasad (2010) focused on macroeconomic and bank specific

factors influencing non-performing loans and their effects in GCC Banking System. After a

comprehensive analysis, they found that higher interest rates increase non performing loans but the

relationship was not statistically significant.

2.2.2 The relationship between Non performing Loans and Size of the Bank

Salas and Saurina (2002) find a negative relation between bank size and non performing loans and

argue that bigger size allows for more diversification opportunities. Hu et al. (2004) and Rajan and

Dhal (2003) report similar empirical evidence

Another strand of literature has focused on the degree of loan concentration in various sectors, and

proposes that vulnerabilities within sectors of high loan concentration tend to exacerbate the non

performing ratio (Herring and Wachter, 1999) as cited in (Guy, 2011). However, Stiroh (2004) does

not find evidence of benefits from diversification in the form of reduced risk, for the US banking

system, since non-interest income growth was highly correlated with net interest income during the

1990s.

17

2.2.3 The relationship between Non performing Loans and Bank Policy

The moral hazard of too-big-to-fail banks represents another channel relating bank-specific features

with non performing loans (Louzis et al, 2011). A policy concern is that too-big-to-fail banks may

resort to excessive risk taking since market discipline is not imposed by its creditors who expect

government protection in case of a bank‟s failure (Stern and Feldman, 2004). Consequently, large

banks may increase their leverage too much and extend loans to lower quality borrowers (Louzis et

al, 2011). Boyd and Gertler (1994) argue that in the 1980s the tendency of US large banks towards

riskier portfolios was encouraged by the US government’s too-big-to-fail policy. On the other hand,

Ennis and Malek (2005) examine US banks‟ performance across size classes over the period 1983–

2003 and conclude that the evidence for the too-big-to-fail distortions is in no way definite. Hu et al

(2006) also show that bank size is negatively related to non performing loans.

In a seminal study, Berle and Means (1933) in Louzis et al. (2011) argue that dispersed ownership of

corporate equity may lead to a poorer performance of the firm as the incentive of shareholders to

monitor the management weakens. An opposing view is that an efficient capital market imposes

discipline on firm’s management and therefore dispersed ownership should not have an effect on

firm’s performance (Fama, 1980) as cited in (Louzis et al., 2011). A strand in the empirical literature

tests these contrasting views using loan quality as an indicator of riskiness but evidence is

inconclusive (Louzis et al, 2011).

2.2.4 The relationship between Non performing loans and Ownership concentration

Iannotta et al. (2007) find a link between higher ownership concentrations and loan quality using a

sample of 181 large banks over the period 1999–2004, thus lending support to the Berle and Means

view. On the other hand, Laeven and Levine (2009) employ data on 279 banks and find a positive

association between greater cash flow rights of a large owner and risk taking. Furthermore, Shehzad

et al. (2010) present empirical evidence, from a data set comprising 500 banks from 2005 to 2007,

18

that ownership proxied by three levels of shareholding (10%, 20% and 50%) has a positive impact on

the non performing loans ratio when the level of ownership concentration is defined at 10% but a

negative impact when the level of level of ownership concentration is defined at 50%.

Therefore they suggest that sharing of control may have adverse effects on the quality of loans

extended up to a level, but in cases of a strong controlling owner, bank’s management becomes more

efficient leading to lower non performing loans. Azofra and Santamaria (2011) find that high levels

of ownership concentration benefit both the bank’s profitability and efficiency for a sample of

Spanish commercial banks.

2.2.5 The relationship of Non-performing loans and Ownership structure

Empirically, Novaes and Werlang (1995) report lower performance for state controlled banks in

Brazil and Argentina due to high proportion of problem loans given to government. Micco et al.

(2004), analyze 50,000 financial institutions with different ownership types covering 119 countries.

They conclude that non performing loans tend to be higher for banks with state ownership than for

other groups. Hu et al. (2004) use a panel of Taiwanese banks and find a positive correlation between

capital share owned by the state and the level of non- performing loans. Garcia-Marco and Robles-

Fernandez (2007) investigate the relationship between risk taking and ownership structure. They

document that commercial banks (mainly private owned) are more exposed to risk than deposit banks

(mainly state owned). More recently Hu et al (2006) analysed the relationship between non

performing loans and ownership structure of commercial banks in Taiwan with a panel dataset

covering the period 1996-1999. The study shows that banks with higher government ownership

recorded lower non-performing loans. Using a pseudo panel-based model for several Sub-Saharan

African countries, Fofack (2005) finds evidence that economic growth, real exchange rate

appreciation, the real interest rate, net interest margins, and inter-bank loans are significant

determinants of non-performing loans in these countries. The author attributes the strong association

between the macroeconomic factors and non-performing loans to the undiversified nature of some

African economies.

19

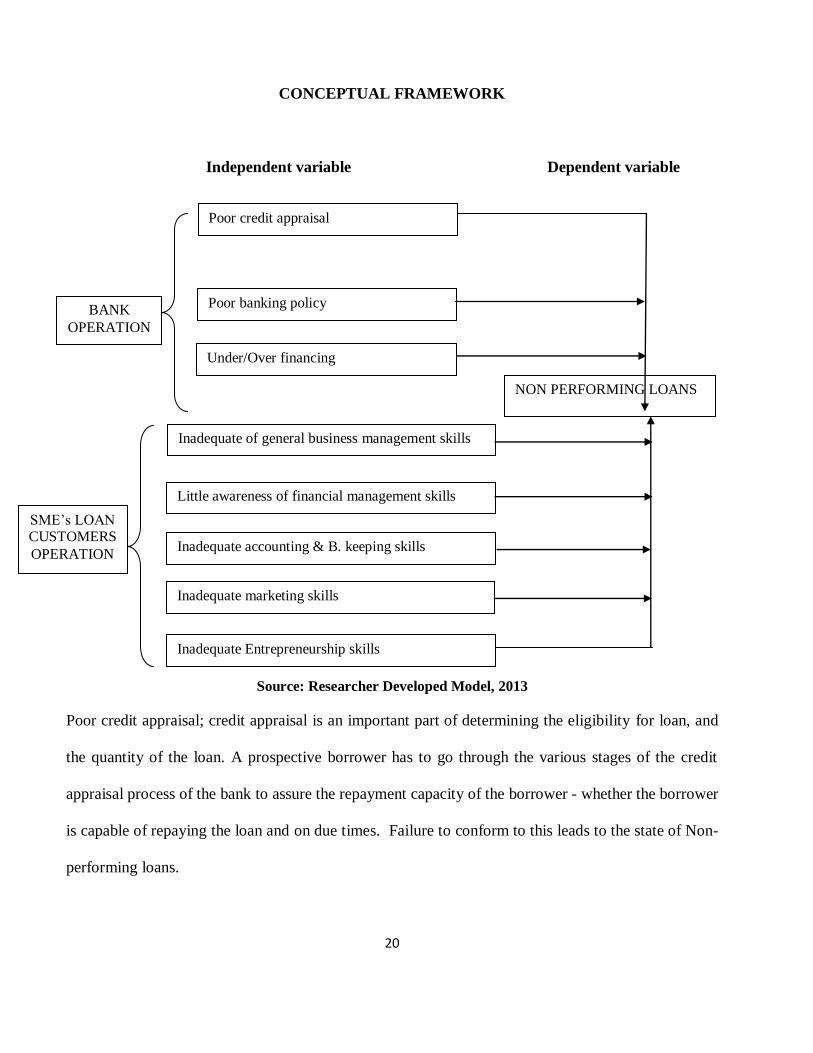

2.3 Conceptual Framework

2.3.1 Dependent Variable

Dependent variable that guides this research is non-performing loans. Non-performing loans depends

on numerous of variables that can be grouped mainly into bank operations variables and customer

operations variables.

2.3.2 Independent Variable

Independent variables are grouped into banking operations variables and customer operations variable

2.3.2 Variable Related to Bank Operations

Variables that related to bank operations are credit policy, credit appraisal, competition, queue, and

under or over financing

2.3.3 Variable Related to Customer Operations

Variable those are related to customer operations are moral hazards, inadequate business, financial,

marketing, entrepreneurship and management skills, fund diversion and multiple loans

20

CONCEPTUAL FRAMEWORK

Independent variable Dependent variable

Source: Researcher Developed Model, 2013

Poor credit appraisal; credit appraisal is an important part of determining the eligibility for loan, and

the quantity of the loan. A prospective borrower has to go through the various stages of the credit

appraisal process of the bank to assure the repayment capacity of the borrower - whether the borrower

is capable of repaying the loan and on due times. Failure to conform to this leads to the state of Non-

performing loans.

Poor credit appraisal

Poor banking policy

Under/Over financing

Inadequate marketing skills

Inadequate Entrepreneurship skills

Inadequate accounting & B. keeping skills

Little awareness of financial management skills

Inadequate of general business management skills

NON PERFORMING LOANS

BANK

OPERATION

SME’s LOAN CUSTOMERS

OPERATION

21

Competition from other credit institution also leads to non-performing loans. SMEs loan customers

tend to have more than one loan from different financial institutions which make it hard for them to

make loan repayment timely, so this lead to non-performing loans.

Long banking queue in banking hall; this discourages SMEs loan customers in repaying their loans,

due to the reason that they are required to spend long time in banking queue something which

demoralizes customers and eventually non-performing loans.

Poor banking policy; other banking policy does not assure loan repayment by the SME’s loan

customers, so these kinds of policies lead to Non-performing loans due to the fact that banking

policies especially credit policies when they are not conducive.

On the other hand, business skills like financial management skills, Accounting and Book-keeping

skills, marketing skills and entrepreneurship skills are very important in business operation, so

inadequacy skills affect loan repayments leading to non-performing loans.

2.4 Research Gap

From the above empirical studies, authors attribute association factors and non performing loans to

the undiversified nature of African economies. While it might true to Tanzanian commercial banks,

this research study grouped non-performing loans factors into two groups; factors related to bank

operations and factors relating to customers operations. The aim is to enable each group to come with

strategies to reduce non performing loans in Tanzania commercial banks.

22

CHAPTER THREE

RESEACH METHODOLOGY

3.1 Research Design

The study adopted the use of a descriptive case research design. The case study approach was

preferred by the researcher due to time constrain and also on the availability and reliability of data

from the NMB Plc Kenyatta Road – Mwanza. Also the researcher works within the banking sector

thus it was easier to collect data from the respondents. This descriptive case research was aimed at

getting detailed information regarding the Causes of nonperforming loans to Tanzania Commercial

Banks. A descriptive study is concerned with finding out the what, where and how of a phenomenon

(Ngechu, 2004). Descriptive research design was chosen because it enabled the researcher to infer the

findings to a larger population with high level of accuracy. The focus of the study was both

quantitative and qualitative in order to gain a better understanding and more insightful interpretation

of the results. According to Coopers and Schindler (2004) descriptive studies are more formalized

and typically structured with investigative questions.

3.2 Study Area

The study was conducted at NMB Bank PLC, Kenyatta road branch, Mwanza City Tanzania.

Kenyatta Raoad Branch was the first Branch of National Microfinance Loan to lend to SMEs

Customers since 2000. This has brought enough experience to Bank officer and large base of

experienced SMEs borrowers. In 2012 he branch recorded high Non performing loan of 21%

compared to other NMB branches offering the same product

23

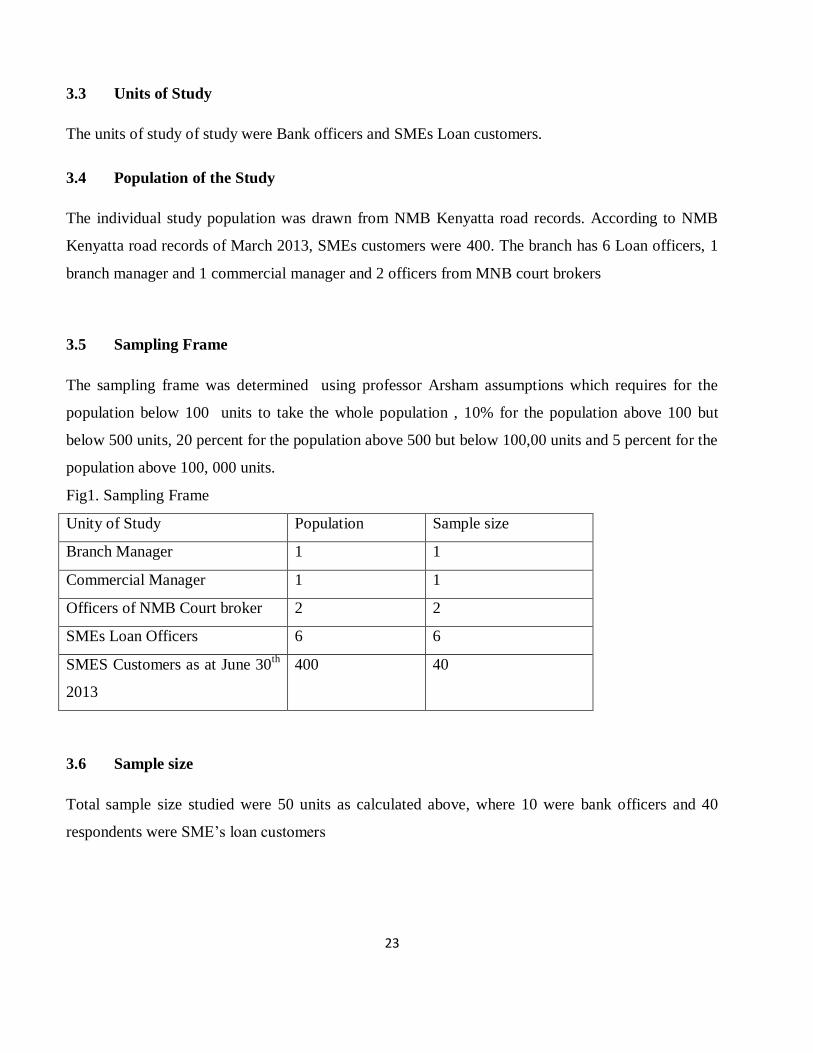

3.3 Units of Study

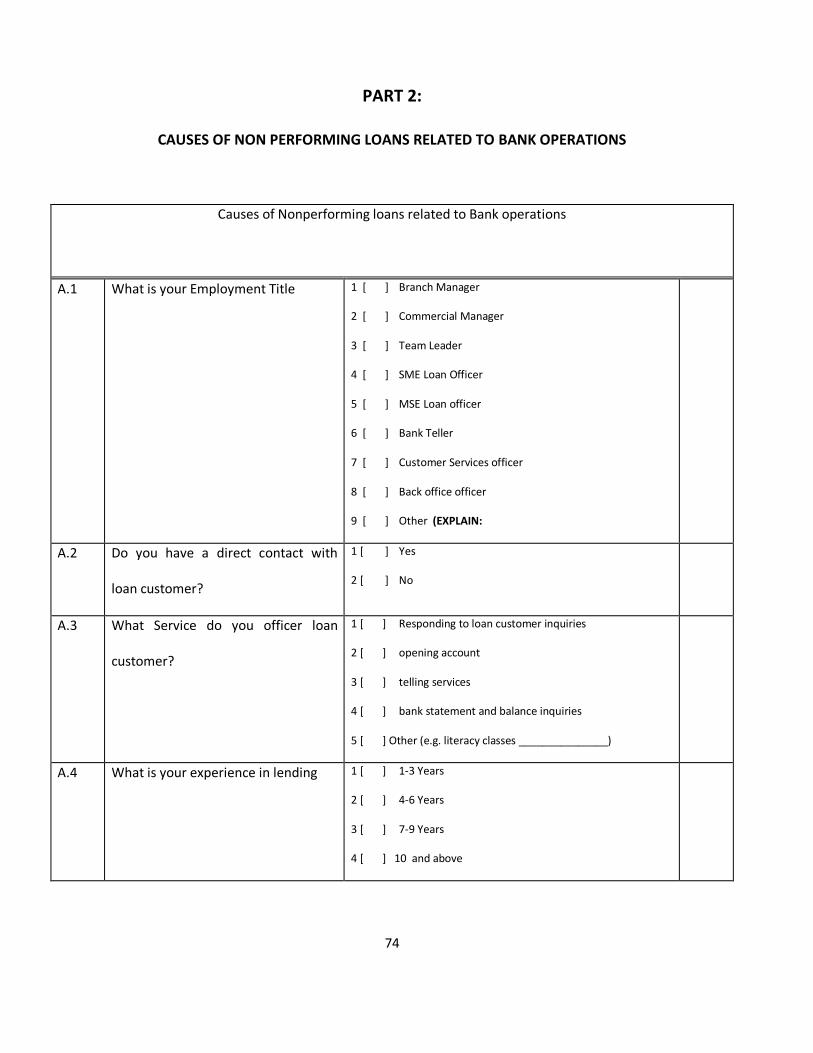

The units of study of study were Bank officers and SMEs Loan customers.

3.4 Population of the Study

The individual study population was drawn from NMB Kenyatta road records. According to NMB

Kenyatta road records of March 2013, SMEs customers were 400. The branch has 6 Loan officers, 1

branch manager and 1 commercial manager and 2 officers from MNB court brokers

3.5 Sampling Frame

The sampling frame was determined using professor Arsham assumptions which requires for the

population below 100 units to take the whole population , 10% for the population above 100 but

below 500 units, 20 percent for the population above 500 but below 100,00 units and 5 percent for the

population above 100, 000 units.

Fig1. Sampling Frame

Unity of Study Population Sample size

Branch Manager 1 1

Commercial Manager 1 1

Officers of NMB Court broker 2 2

SMEs Loan Officers 6 6

SMES Customers as at June 30th

2013

400 40

3.6 Sample size

Total sample size studied were 50 units as calculated above, where 10 were bank officers and 40

respondents were SME’s loan customers

24

3.7 Sampling technique

The study employed random sampling where every participant had a chance to be included in the

sample, where in the total number of 400 SME’s loan customers, 40 respondents were picked

randomly by using the random number table.

3.8 Data Collection Method

3.8.1 Primary Data

Primary data were obtained using interview schedules and questionnaire. The researcher conducted

face to face interviews with Branch Managers, Commercial managers, SMEs loan officers and SMEs

customers. Interviews with bank staff explored financial institutional framework, policy and

experience of credit administration and performance trends. Causes of nonperforming loans related to

bank was established. The SMEs questionnaire included structured questions from which the

interviewer noted down respondents’ responses that best matched their views or experiences, giving

inference on causes of nonperforming loans related to customers of SMES loans. The use of

questionnaire to extract perception is rationalized by public role as intended ultimate SMEs loans

3.8.2 Secondary Data

Secondary data were collected from NMB published annual and quarterly reports, financial markets,

businesses and governments annual reports, Bank of Tanzania performance reports, Poverty related

reports, National Surveys, SMEs customers credit files and other literature.

3.8.3 Field Experience

Field data were collected from 15th June 2013 to 29

th June 2013. The researcher approached NMB

PLC staffs and SME’s Loan customers to collect data from them. Participants from NMB Plc include;

commercial manager, SME’s loan officer, ME loan officer, Customer service officer, and bank teller.

Also, the researcher chose randomly 40 SME’s loans customers from Liberty Street, City Center-

Mwanza. On 15th

June 2013, the questionnaires were given to all key informants and were collected

back after five days.

25

Assisted by two trained researchers, data were managed to be collected from SME’s Loans customers

from 21st to 29

th June 2013. Data were collected from 40 SME’s loans customers in Liberty Street.

SME’s loans customers provided a very good cooperation during the interview and were relaxing

when responding to questions. But some of them were worried that perhaps the government agency

was trying to spy on their income, so as to pay high tax. But we tried to explain that the purpose of

research that it was mainly for academic purpose.

3.9 Research Methods

This study is a quantitative one. The aim was to quantify the cause relationship of nonperforming

loans in commercial bank related to banking and customer operations.

3.9.1 Quantitative Research Methodology

To obtain information about causes of nonperforming loans related to banks and customers,

quantitative approach was used, because most causes are well documented by banks. The studies rank

them and identify which cause contributes most and which cause contributes least.

Since the focus was on causes of nonperforming loans, it was scientific to start with the survey where

a large amount of general information was gathered towards the different causes. But, the outcomes

resulting from the survey was not taken as valid immediately. By use of in-depth interviews possible

remarkable errors was investigated as well as additional information that can contribute to the validity

of statistical outcomes.

Because the survey as well as the in-depth interviews contained with help of individuals, businesses

and government agencies another method was needed. This method was a field experiment; focus

groups were established. These focus groups specifically addressed causes of nonperforming loans

from bank and customers perspectives

This sequential design was dominated by quantitative method that aimed at assessing the factors

causing non-performing loans. The field study complements and deepened the survey results

followed by an experiment to check for the results for both steps (Flick 2007, 95)

26

And for the case of Research design, this study descriptive technique was employed.

3.10 Tools of Data Collection

Data was collected through interview schedules and questionnaire. The interview schedules contained

a set of questions, which were filled by enumerators. The researcher enumerated the answers by

cross-examination in order to find out the truth. During enumeration the researcher explained the

aims and objects of the study and also removed difficulties which respondents failed to understand.

3.11 Measurement and measuring scale

The study employed nominal and ordinal scales. Numbers were assigned to category of respondents

and questions. For instance male were assigned no. 1 and female no. 2. Causes were ranked in order.

Arbitrary scales measuring method were developed in order to demonstrate causes of nonperforming

loans

3.12 Data Reliability and Validity

3.12.1 Test of Reliability

In order to ensure reliability of interview guide, the study standardized the measurement for all

categories of respondents. This enabled to reduce external source of variation such as boredom,

fatigue and biases. Designing measurement directions that had no variation from one group to group

and broadening the sample of items tested reliability.

3.12.2 Test of Validity

The study tested internal validity of the interview guide ability to measure causal relationship of

nonperforming loans. In order to be confident with the instrument, the researcher administered the

instrument to focus group discussion in order to test the adequacy and coverage of the causes of

nonperforming loans. Participants agreed in principle for items to include in the interview guide to

adequately covering causes of nonperforming loans under study. Using panel of staffs who are

27

responsible issue and approve loans (loans officer) form NMB Kenyatta road who judged how well

the instrument meets the standard,

More over the instrument was tested to see if it was in conformity with predicted correlation with

other theoretical propositions. This brought confident for the instrument to produce intended results

3.12.3 Data analysis

In data analysis the following was employed

Data Editing

Data editing was employed during the point filling the questionnaire, also further editing of primary

data was done in the stage of sorting and analysis. Thus, in both the stages, the researcher reviewed

the reasons lead to non-performing loans in Tanzania commercial banks.

Data Processing

The researcher also processed data at the process of answering the research questions, whereby

percentages and frequency distribution were used to process data.

28

CHAPTER FOUR

FINDINGS PRESENTATION AND ANALYSIS

4.1. Demographic Characteristics of Respondents

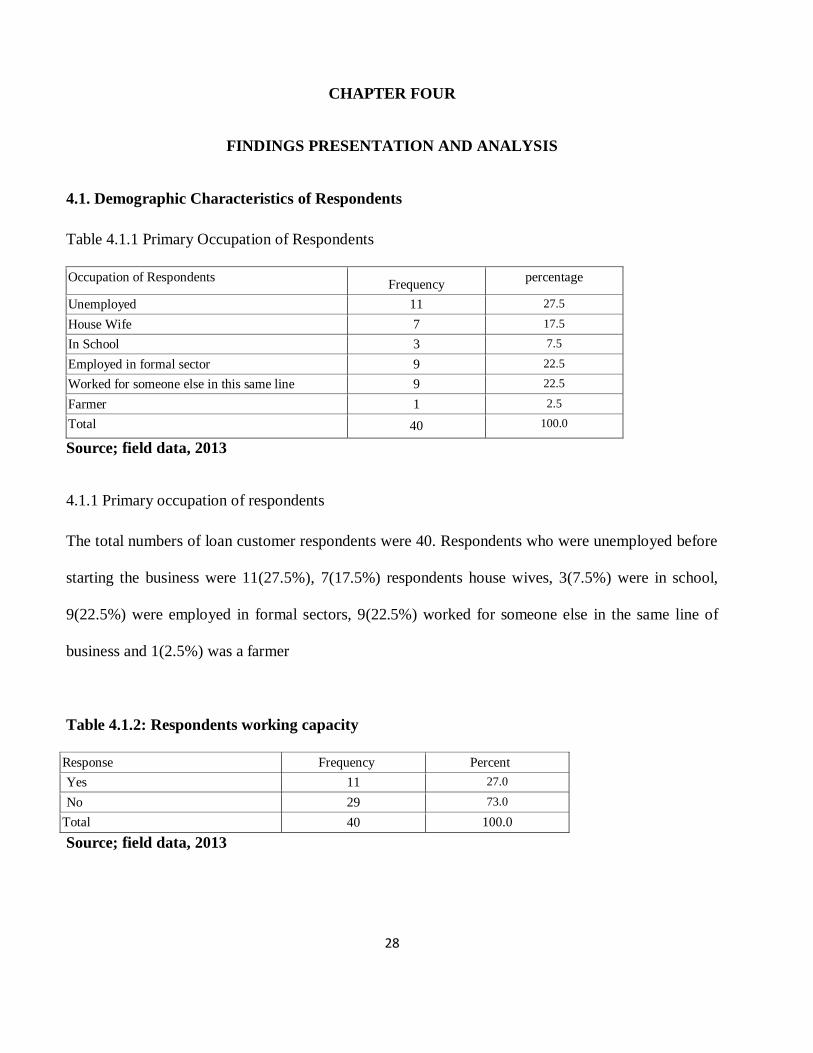

Table 4.1.1 Primary Occupation of Respondents

Occupation of Respondents Frequency

percentage

Unemployed 11 27.5

House Wife 7 17.5

In School 3 7.5

Employed in formal sector 9 22.5

Worked for someone else in this same line 9 22.5

Farmer 1 2.5

Total 40 100.0

Source; field data, 2013

4.1.1 Primary occupation of respondents

The total numbers of loan customer respondents were 40. Respondents who were unemployed before

starting the business were 11(27.5%), 7(17.5%) respondents house wives, 3(7.5%) were in school,

9(22.5%) were employed in formal sectors, 9(22.5%) worked for someone else in the same line of

business and 1(2.5%) was a farmer

Table 4.1.2: Respondents working capacity

Response Frequency Percent

Yes 11 27.0

No 29 73.0

Total 40 100.0

Source; field data, 2013

29

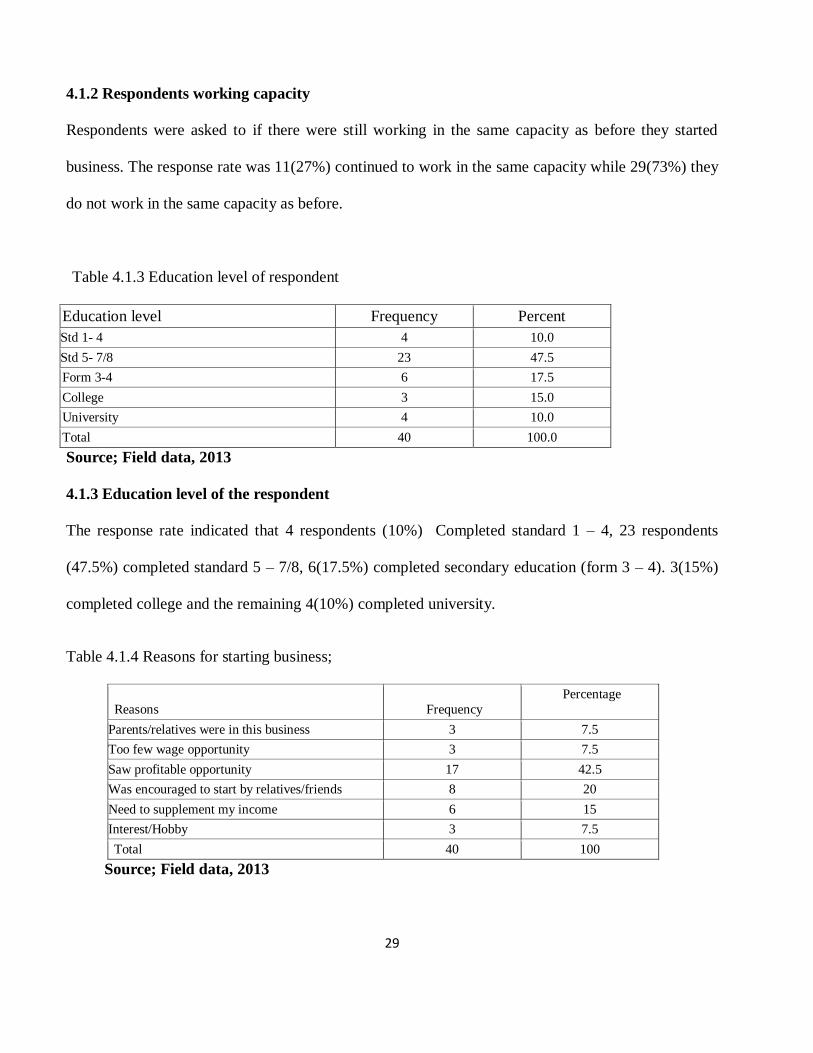

4.1.2 Respondents working capacity

Respondents were asked to if there were still working in the same capacity as before they started

business. The response rate was 11(27%) continued to work in the same capacity while 29(73%) they

do not work in the same capacity as before.

Table 4.1.3 Education level of respondent

Education level Frequency Percent

Std 1- 4 4 10.0

Std 5- 7/8 23 47.5

Form 3-4 6 17.5

College 3 15.0

University 4 10.0

Total 40 100.0

Source; Field data, 2013

4.1.3 Education level of the respondent

The response rate indicated that 4 respondents (10%) Completed standard 1 – 4, 23 respondents

(47.5%) completed standard 5 – 7/8, 6(17.5%) completed secondary education (form 3 – 4). 3(15%)

completed college and the remaining 4(10%) completed university.

Table 4.1.4 Reasons for starting business;

Reasons Frequency

Percentage

Parents/relatives were in this business 3 7.5

Too few wage opportunity 3 7.5

Saw profitable opportunity 17 42.5

Was encouraged to start by relatives/friends 8 20

Need to supplement my income 6 15

Interest/Hobby 3 7.5

Total 40 100

Source; Field data, 2013

30

4.1.4 Reasons for starting business

The response rate indicates that 3(7.5%) started new business because their parents/relatives were in

business.3 (7.5%) due to few wage opportunities. 17(42.5%) choose to start business because they

saw that it is profitable opportunity to them, 8(20%) said that they started business because they were

encouraged to start business by their friends/ Relatives.6 (15%) due to the need to supplement their

income, 3(7.5%) start businesses because of interests/Hobby.

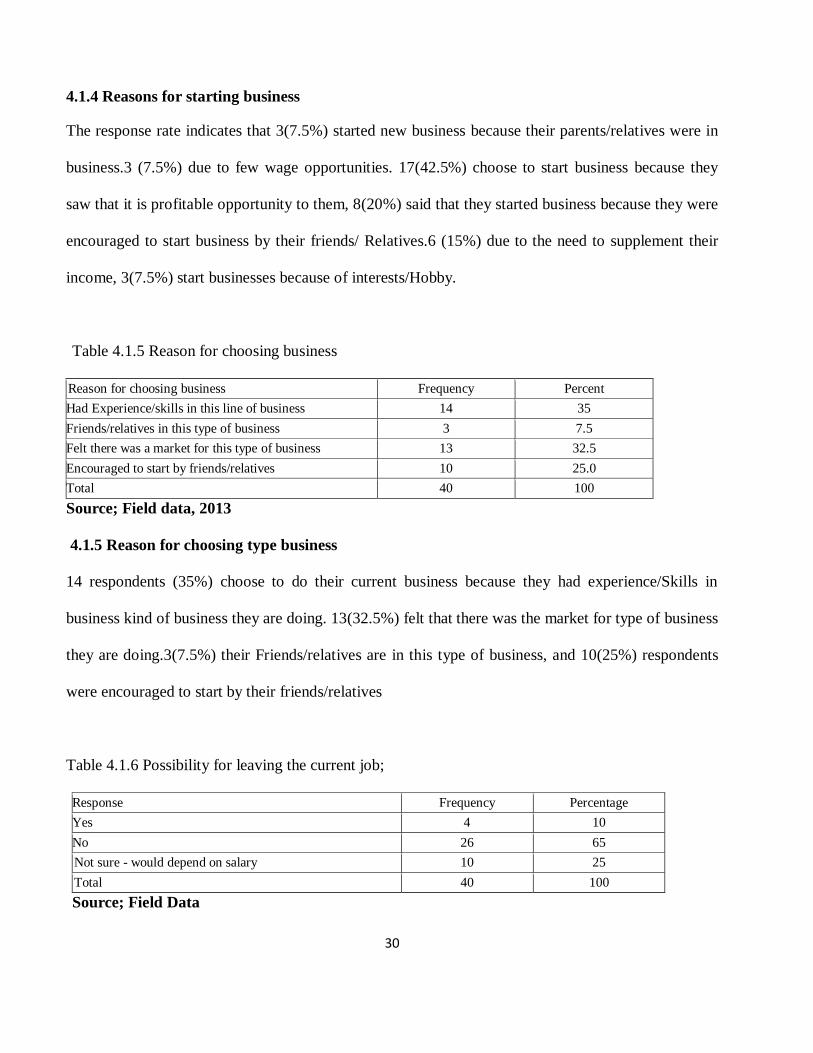

Table 4.1.5 Reason for choosing business

Reason for choosing business Frequency Percent

Had Experience/skills in this line of business 14 35

Friends/relatives in this type of business 3 7.5

Felt there was a market for this type of business 13 32.5

Encouraged to start by friends/relatives 10 25.0

Total 40 100

Source; Field data, 2013

4.1.5 Reason for choosing type business

14 respondents (35%) choose to do their current business because they had experience/Skills in

business kind of business they are doing. 13(32.5%) felt that there was the market for type of business

they are doing.3(7.5%) their Friends/relatives are in this type of business, and 10(25%) respondents

were encouraged to start by their friends/relatives

Table 4.1.6 Possibility for leaving the current job;

Response Frequency Percentage

Yes 4 10

No 26 65

Not sure - would depend on salary 10 25

Total 40 100

Source; Field Data

31

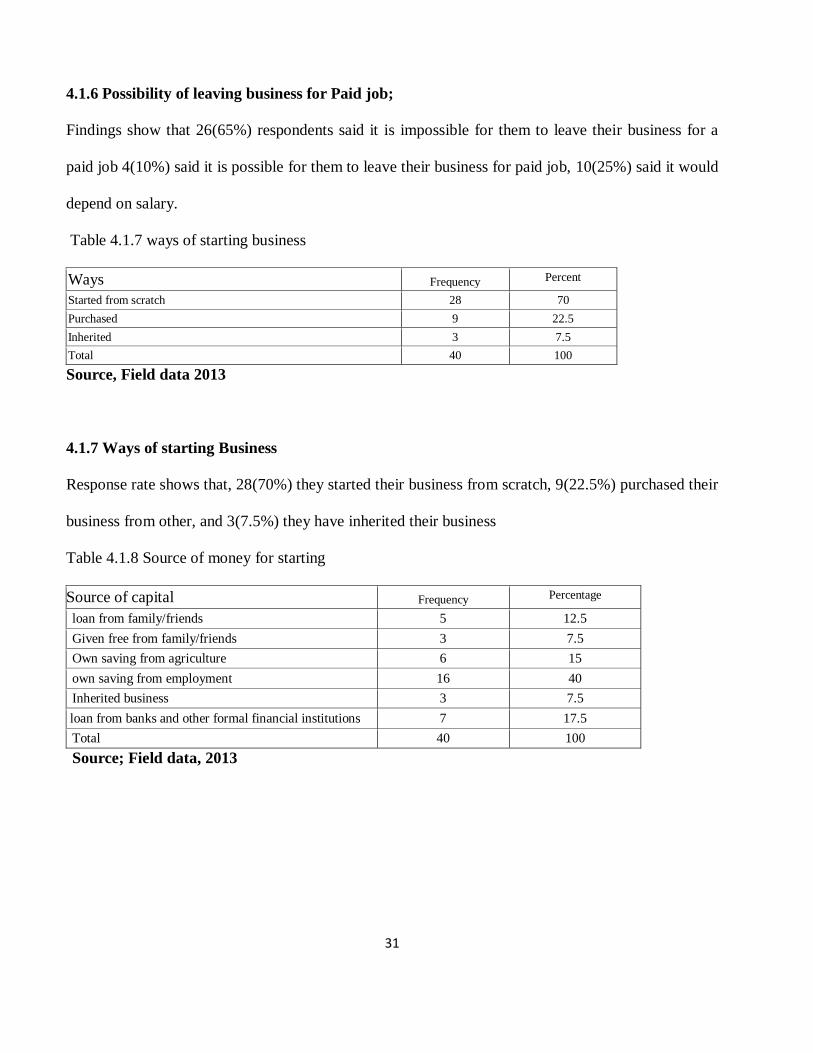

4.1.6 Possibility of leaving business for Paid job;

Findings show that 26(65%) respondents said it is impossible for them to leave their business for a

paid job 4(10%) said it is possible for them to leave their business for paid job, 10(25%) said it would

depend on salary.

Table 4.1.7 ways of starting business

Ways Frequency Percent

Started from scratch 28 70

Purchased 9 22.5

Inherited 3 7.5

Total 40 100

Source, Field data 2013

4.1.7 Ways of starting Business

Response rate shows that, 28(70%) they started their business from scratch, 9(22.5%) purchased their

business from other, and 3(7.5%) they have inherited their business

Table 4.1.8 Source of money for starting

Source of capital Frequency Percentage

loan from family/friends 5 12.5

Given free from family/friends 3 7.5

Own saving from agriculture 6 15

own saving from employment 16 40

Inherited business 3 7.5

loan from banks and other formal financial institutions 7 17.5

Total 40 100

Source; Field data, 2013

32

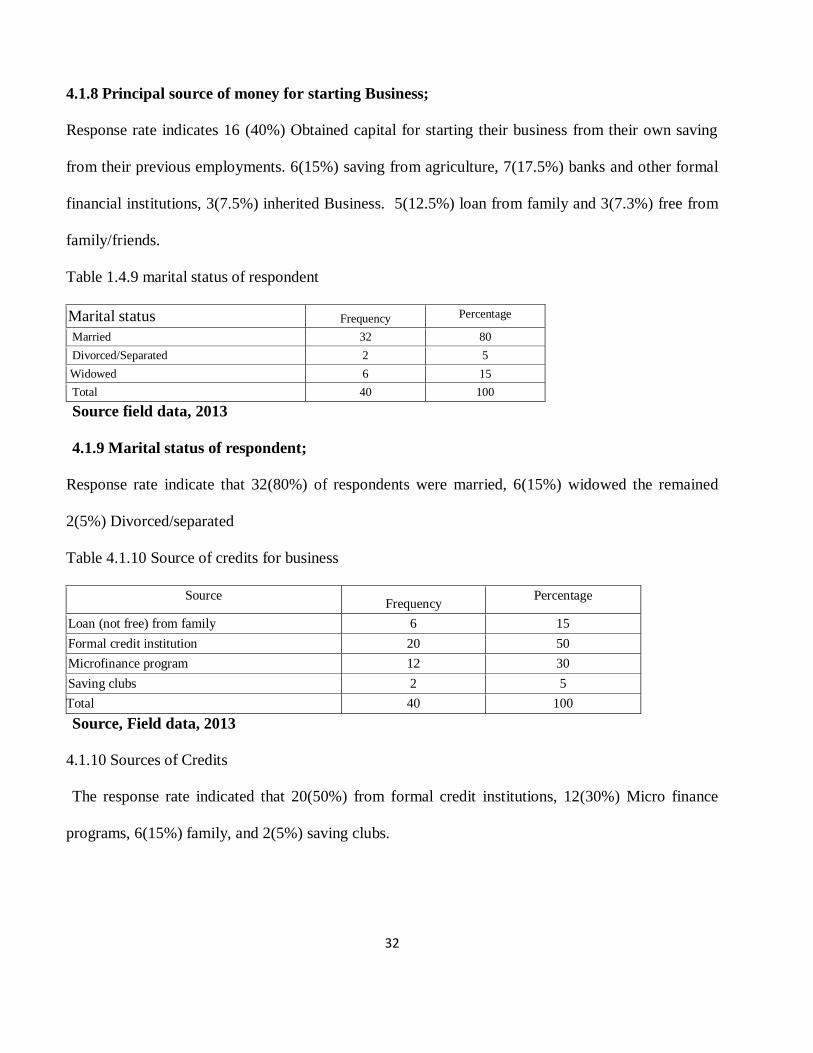

4.1.8 Principal source of money for starting Business;

Response rate indicates 16 (40%) Obtained capital for starting their business from their own saving

from their previous employments. 6(15%) saving from agriculture, 7(17.5%) banks and other formal

financial institutions, 3(7.5%) inherited Business. 5(12.5%) loan from family and 3(7.3%) free from

family/friends.

Table 1.4.9 marital status of respondent

Marital status Frequency Percentage

Married 32 80

Divorced/Separated 2 5

Widowed 6 15

Total 40 100

Source field data, 2013

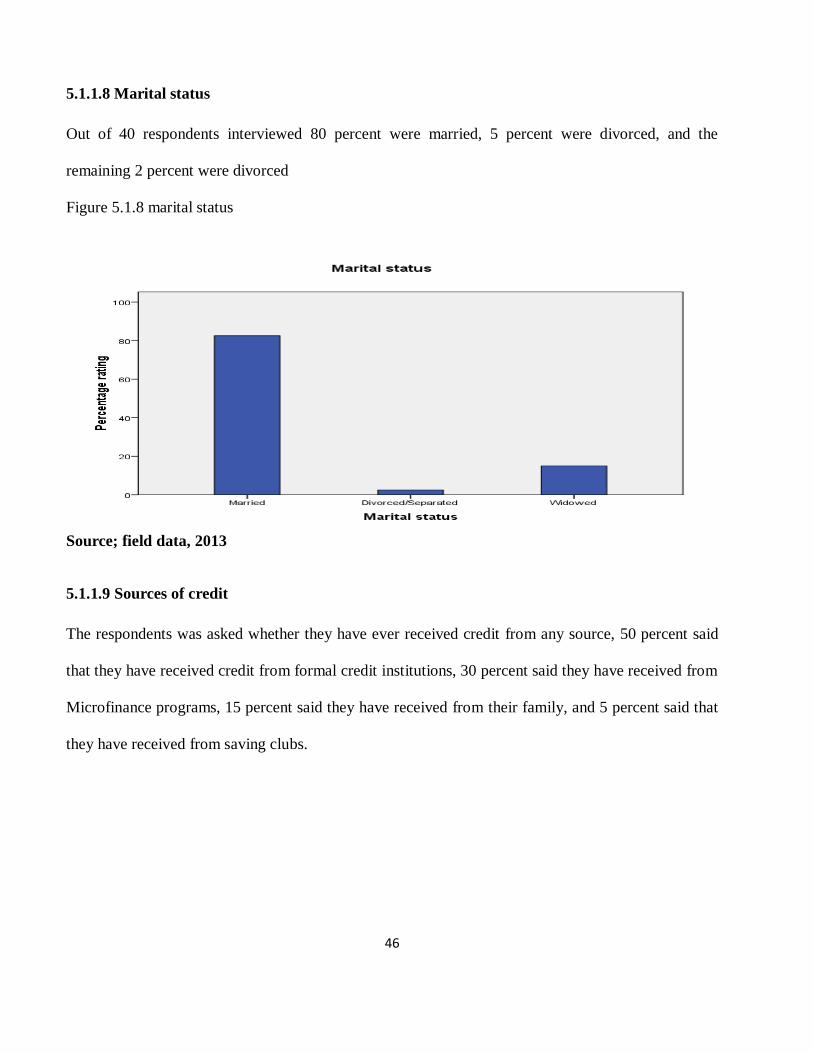

4.1.9 Marital status of respondent;

Response rate indicate that 32(80%) of respondents were married, 6(15%) widowed the remained

2(5%) Divorced/separated

Table 4.1.10 Source of credits for business

Source Frequency

Percentage

Loan (not free) from family 6 15

Formal credit institution 20 50

Microfinance program 12 30

Saving clubs 2 5

Total 40 100

Source, Field data, 2013

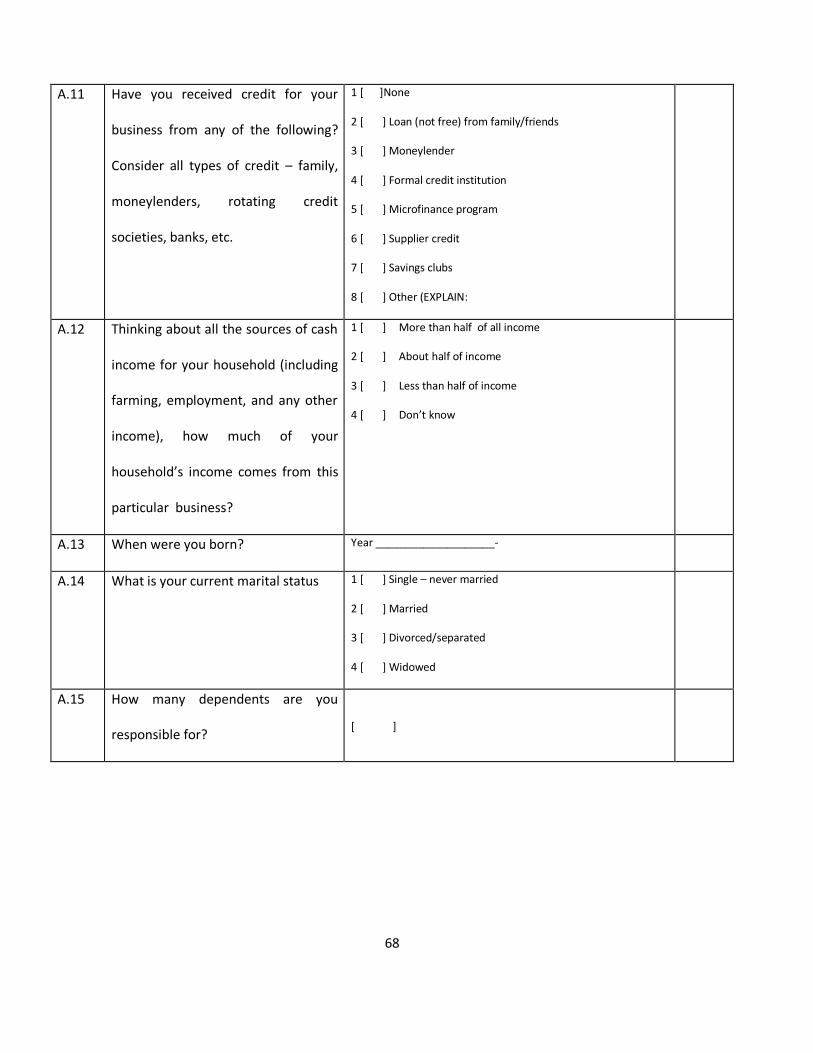

4.1.10 Sources of Credits

The response rate indicated that 20(50%) from formal credit institutions, 12(30%) Micro finance

programs, 6(15%) family, and 2(5%) saving clubs.

33

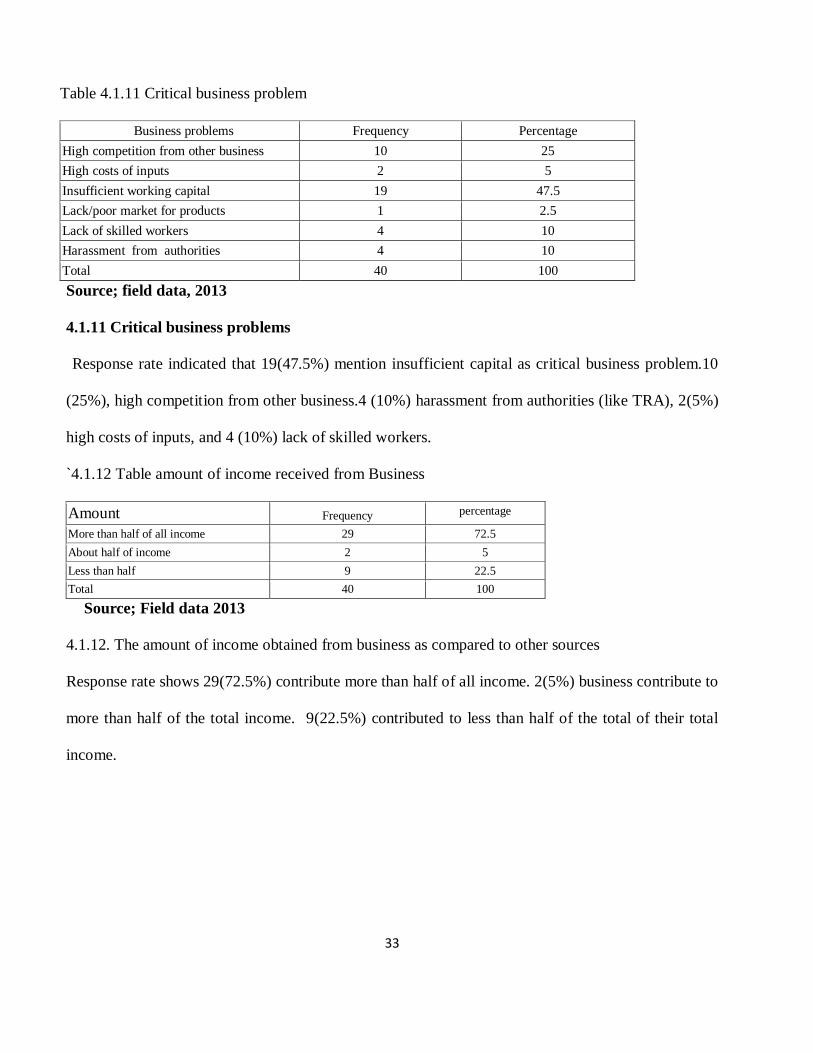

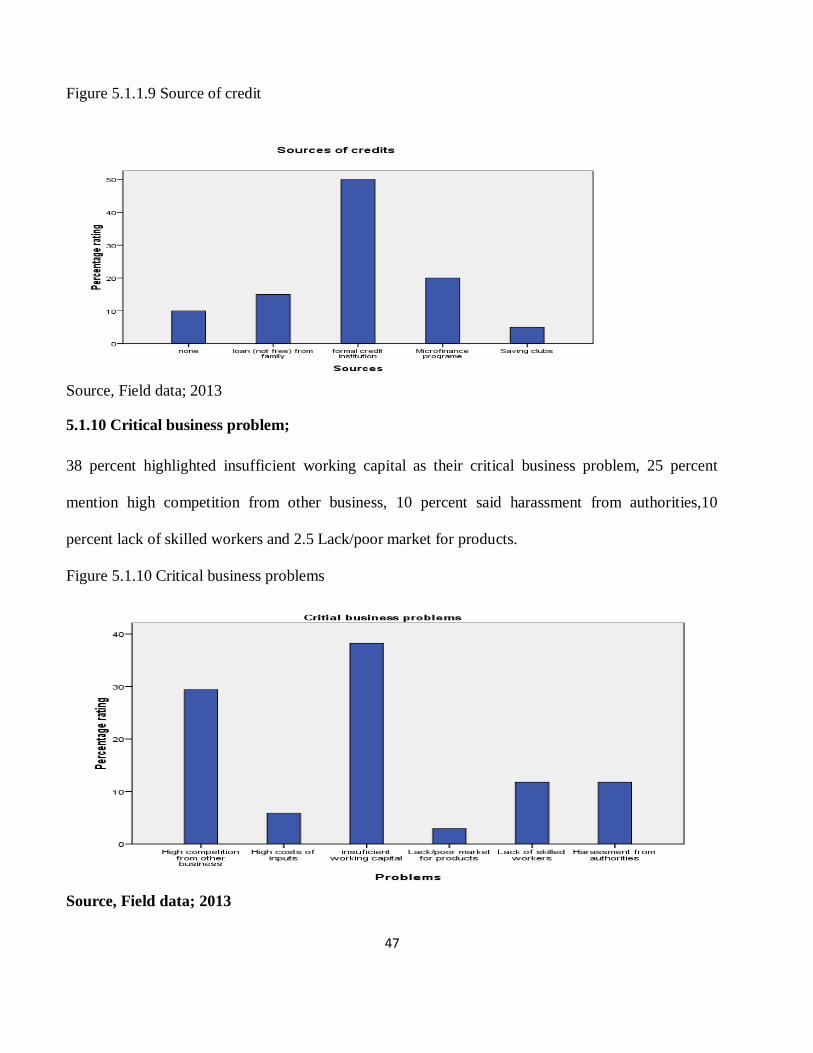

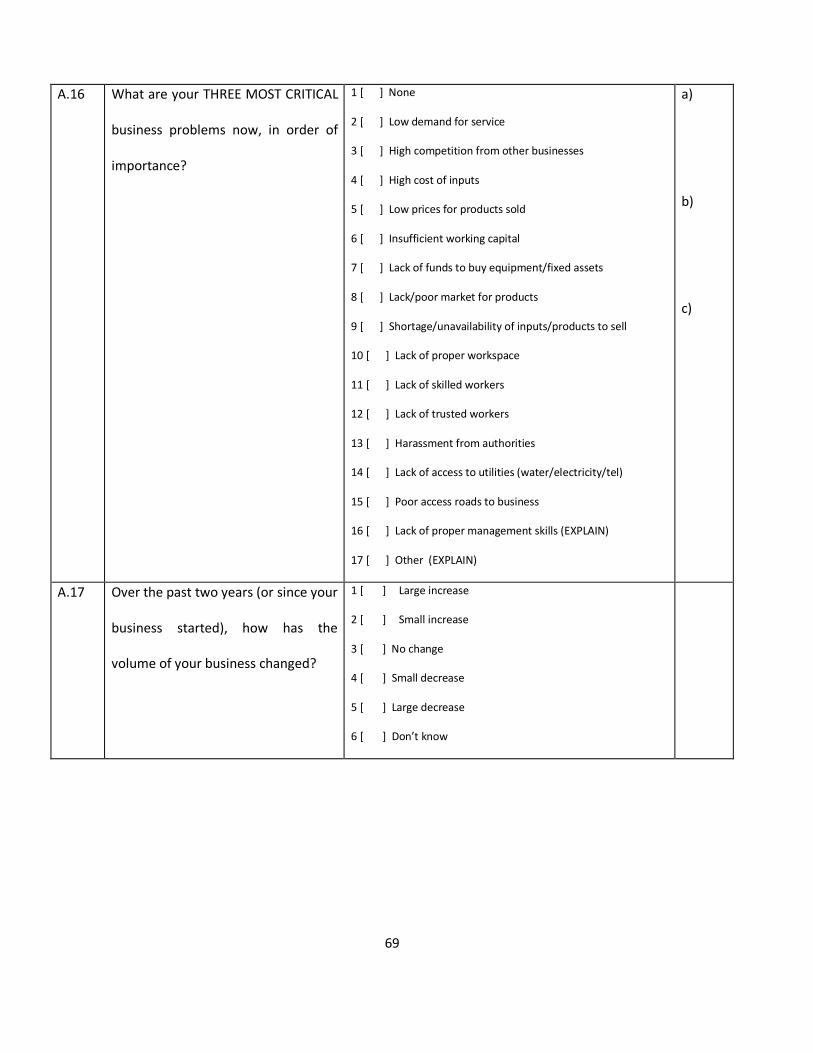

Table 4.1.11 Critical business problem

Business problems Frequency Percentage

High competition from other business 10 25

High costs of inputs 2 5

Insufficient working capital 19 47.5

Lack/poor market for products 1 2.5

Lack of skilled workers 4 10

Harassment from authorities 4 10

Total 40 100

Source; field data, 2013

4.1.11 Critical business problems

Response rate indicated that 19(47.5%) mention insufficient capital as critical business problem.10

(25%), high competition from other business.4 (10%) harassment from authorities (like TRA), 2(5%)

high costs of inputs, and 4 (10%) lack of skilled workers.

`4.1.12 Table amount of income received from Business

Amount Frequency percentage

More than half of all income 29 72.5

About half of income 2 5

Less than half 9 22.5

Total 40 100

Source; Field data 2013

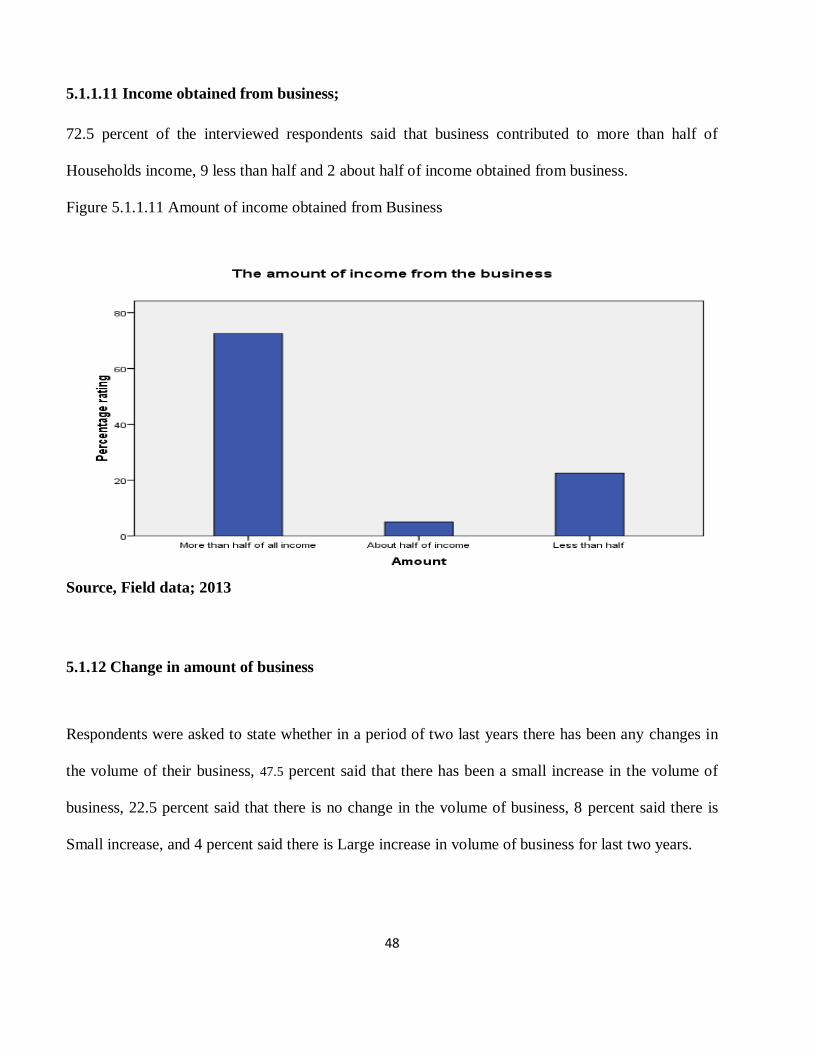

4.1.12. The amount of income obtained from business as compared to other sources

Response rate shows 29(72.5%) contribute more than half of all income. 2(5%) business contribute to

more than half of the total income. 9(22.5%) contributed to less than half of the total of their total

income.

34

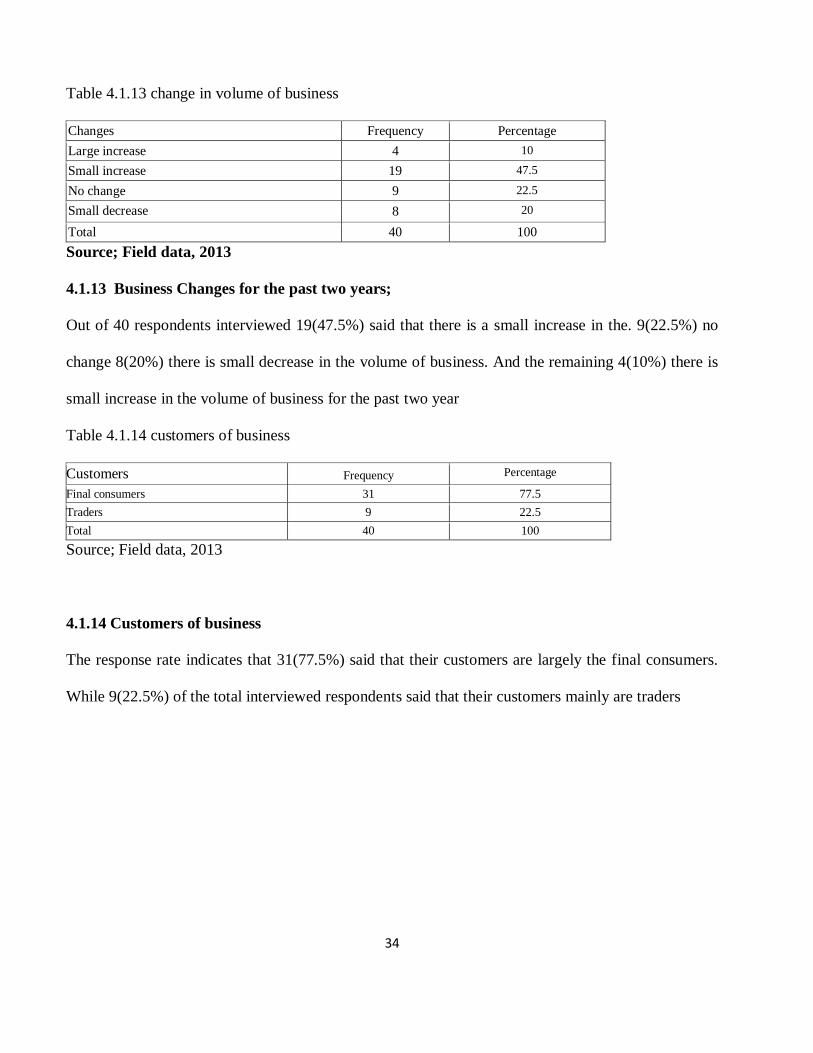

Table 4.1.13 change in volume of business

Changes Frequency Percentage

Large increase 4 10

Small increase 19 47.5

No change 9 22.5

Small decrease 8 20

Total 40 100

Source; Field data, 2013

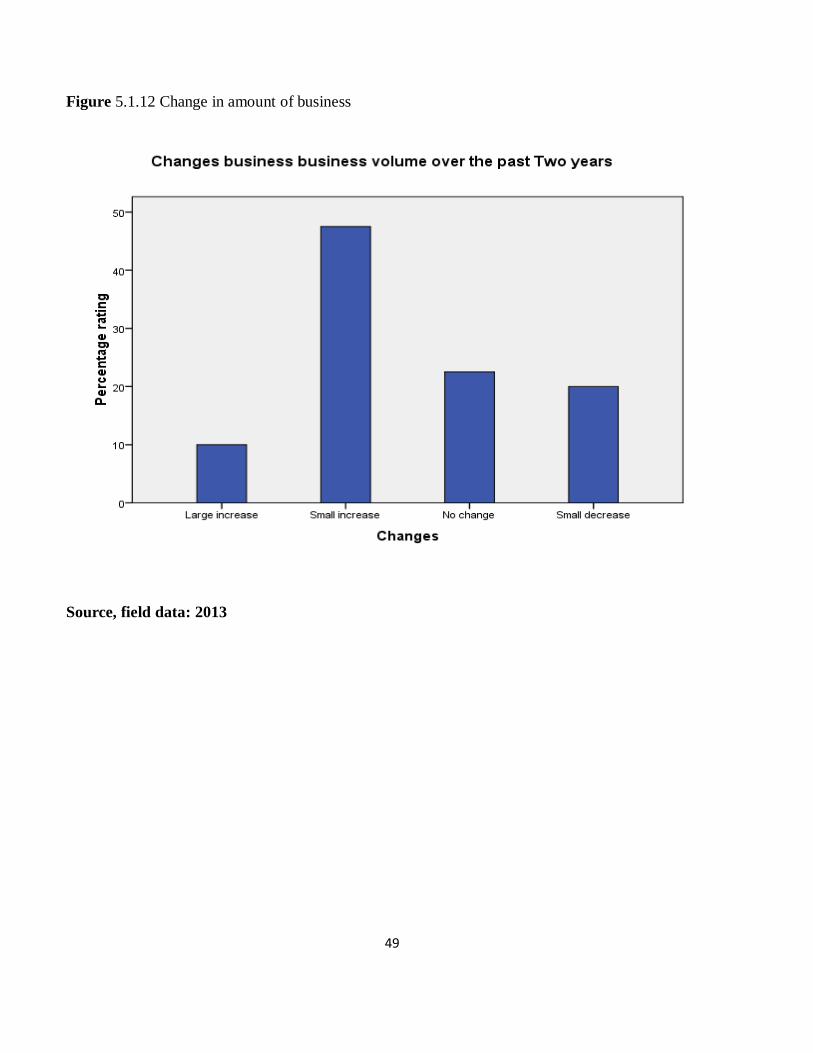

4.1.13 Business Changes for the past two years;

Out of 40 respondents interviewed 19(47.5%) said that there is a small increase in the. 9(22.5%) no

change 8(20%) there is small decrease in the volume of business. And the remaining 4(10%) there is

small increase in the volume of business for the past two year

Table 4.1.14 customers of business

Customers Frequency Percentage

Final consumers 31 77.5

Traders 9 22.5

Total 40 100

Source; Field data, 2013

4.1.14 Customers of business

The response rate indicates that 31(77.5%) said that their customers are largely the final consumers.

While 9(22.5%) of the total interviewed respondents said that their customers mainly are traders

35

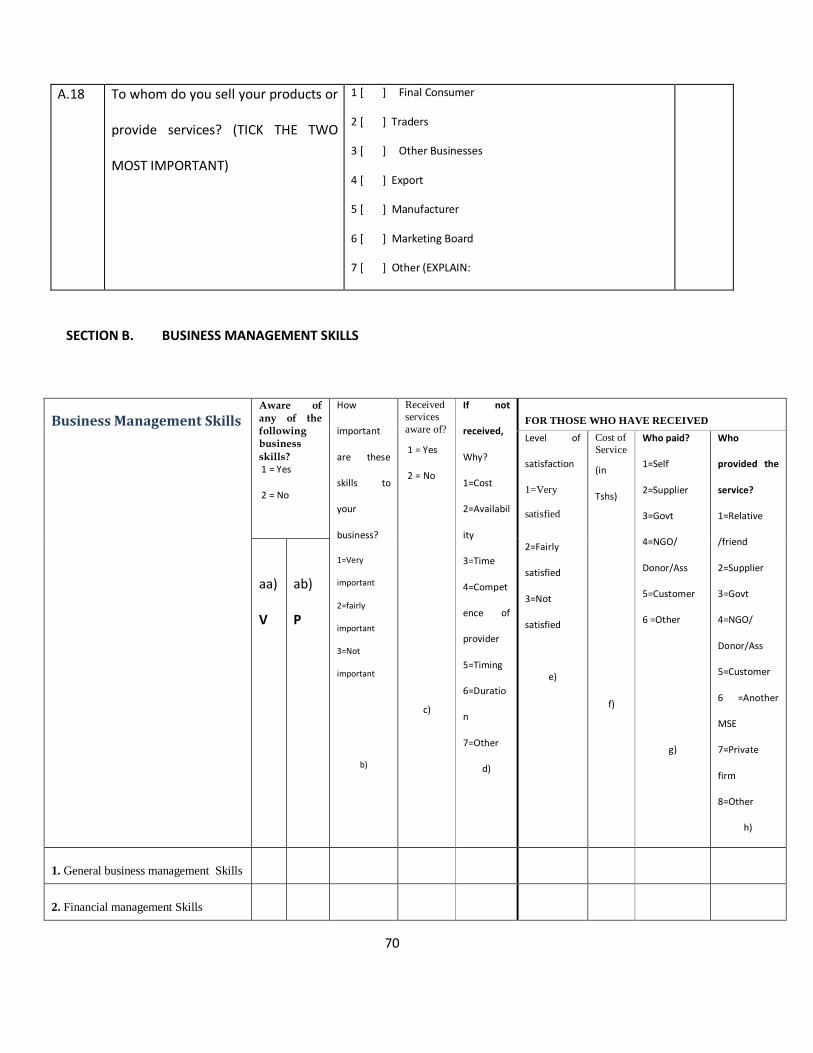

4.2. CAUSE OF NON-PERFORMING LOANS RELATED TO CUSTOMERS OPERATION

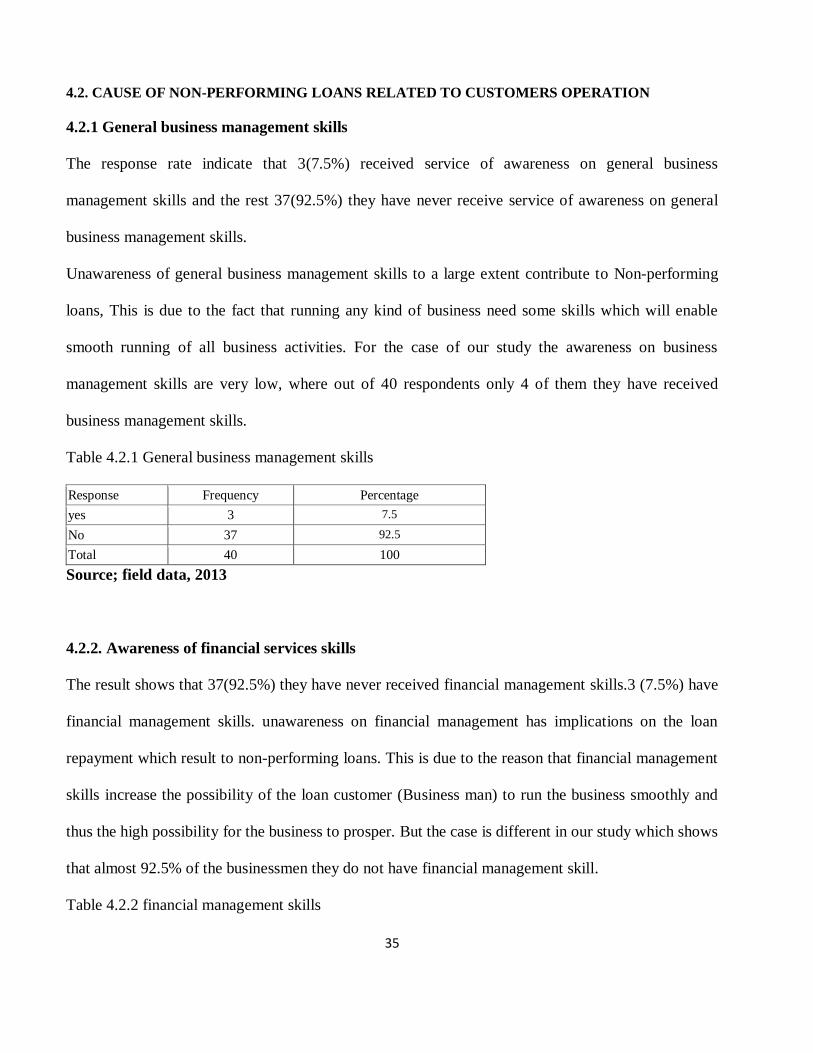

4.2.1 General business management skills

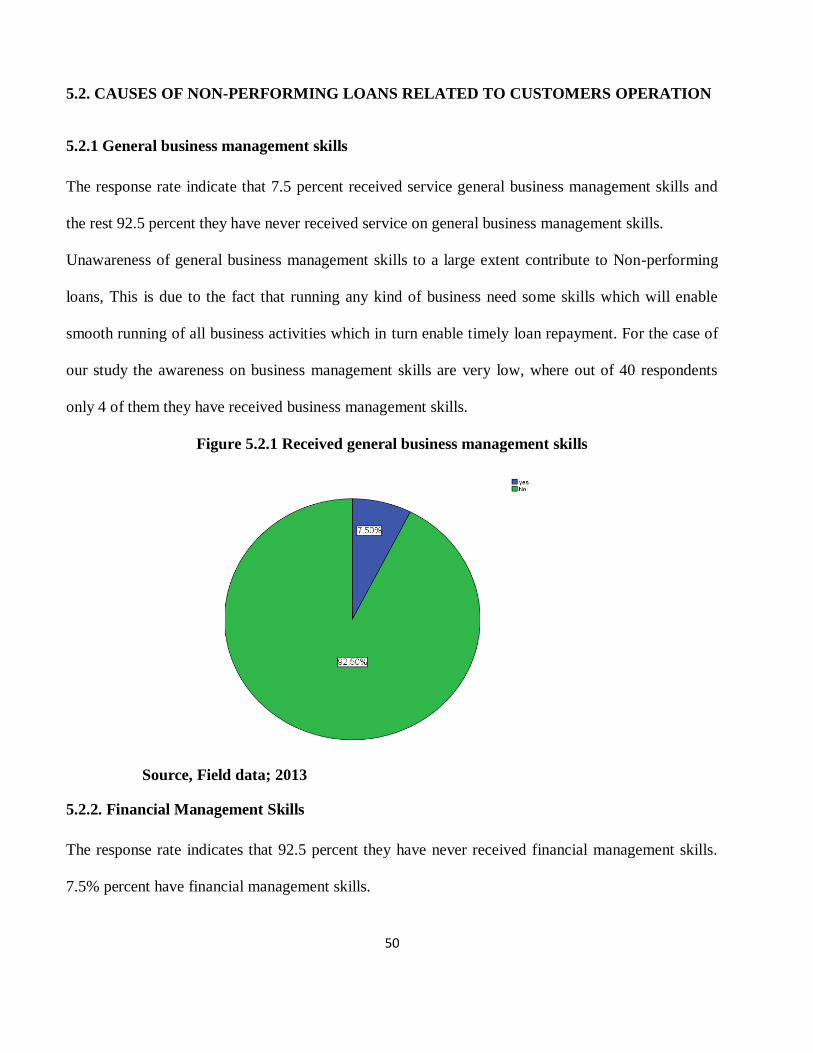

The response rate indicate that 3(7.5%) received service of awareness on general business

management skills and the rest 37(92.5%) they have never receive service of awareness on general

business management skills.

Unawareness of general business management skills to a large extent contribute to Non-performing

loans, This is due to the fact that running any kind of business need some skills which will enable

smooth running of all business activities. For the case of our study the awareness on business

management skills are very low, where out of 40 respondents only 4 of them they have received

business management skills.

Table 4.2.1 General business management skills

Response Frequency Percentage

yes 3 7.5

No 37 92.5

Total 40 100

Source; field data, 2013

4.2.2. Awareness of financial services skills

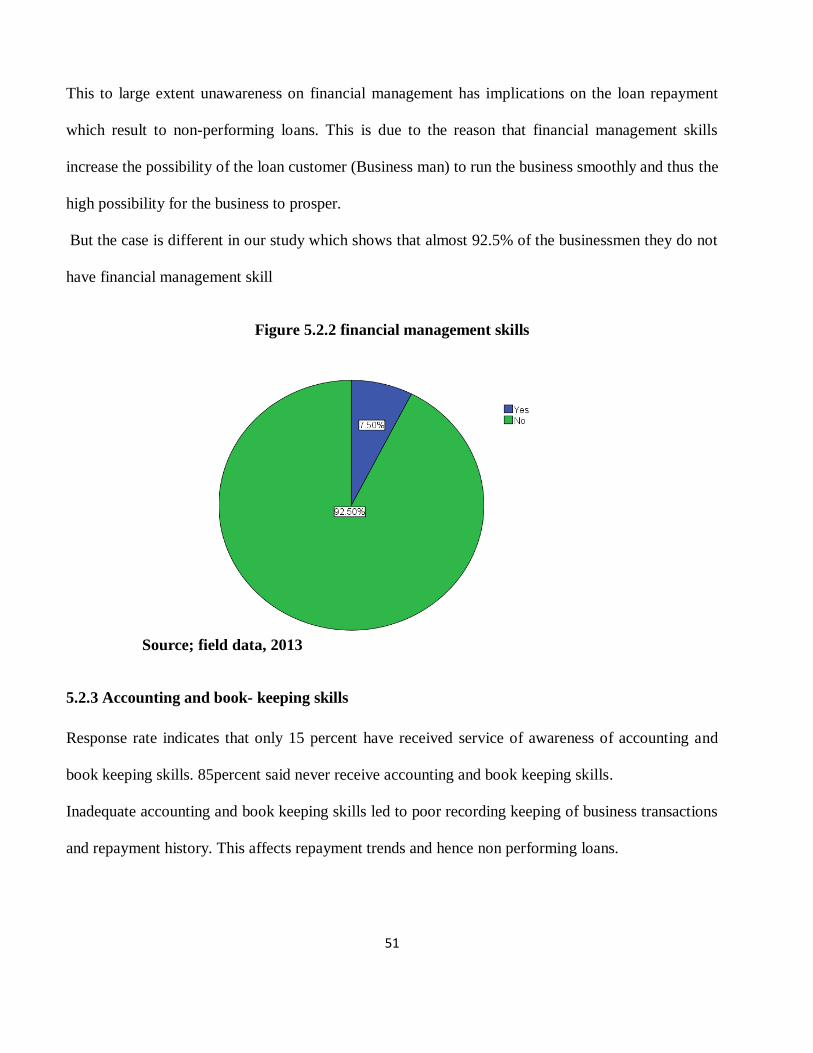

The result shows that 37(92.5%) they have never received financial management skills.3 (7.5%) have

financial management skills. unawareness on financial management has implications on the loan

repayment which result to non-performing loans. This is due to the reason that financial management

skills increase the possibility of the loan customer (Business man) to run the business smoothly and

thus the high possibility for the business to prosper. But the case is different in our study which shows

that almost 92.5% of the businessmen they do not have financial management skill.

Table 4.2.2 financial management skills

36

Response Frequency Percentage

Yes 3 7.5

No 37 92.5

Total 40 100

Source; field data, 2013

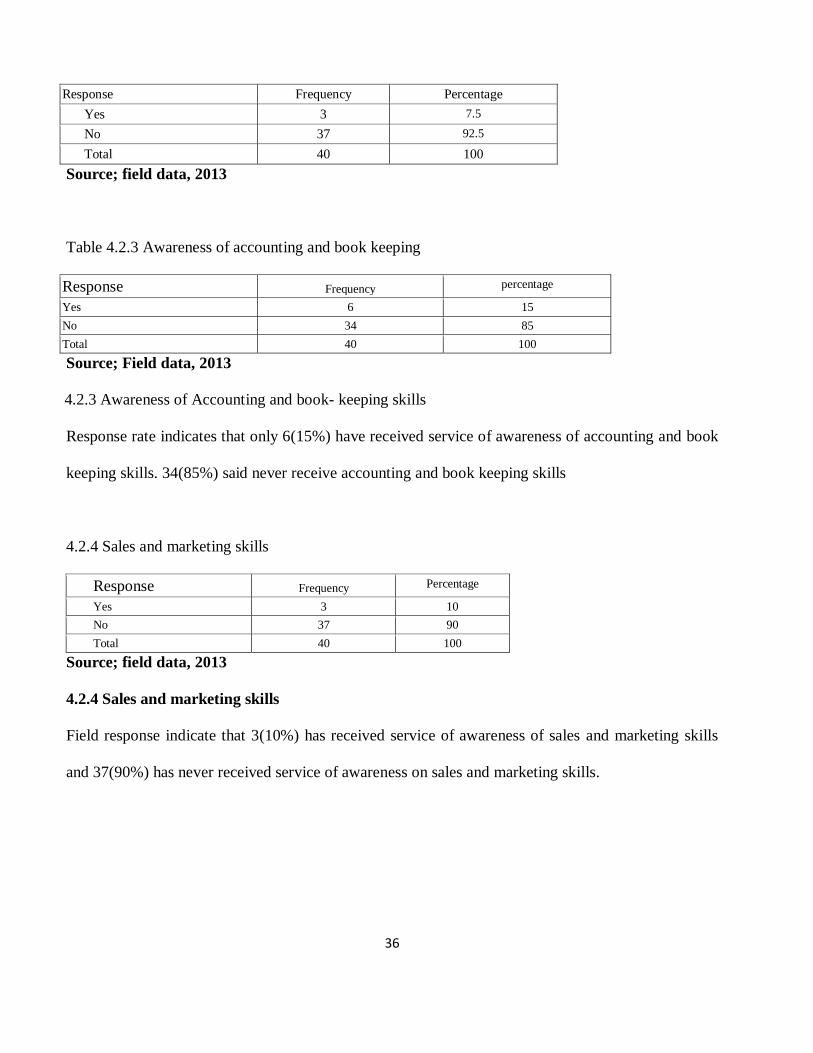

Table 4.2.3 Awareness of accounting and book keeping

Response Frequency percentage

Yes 6 15

No 34 85

Total 40 100

Source; Field data, 2013

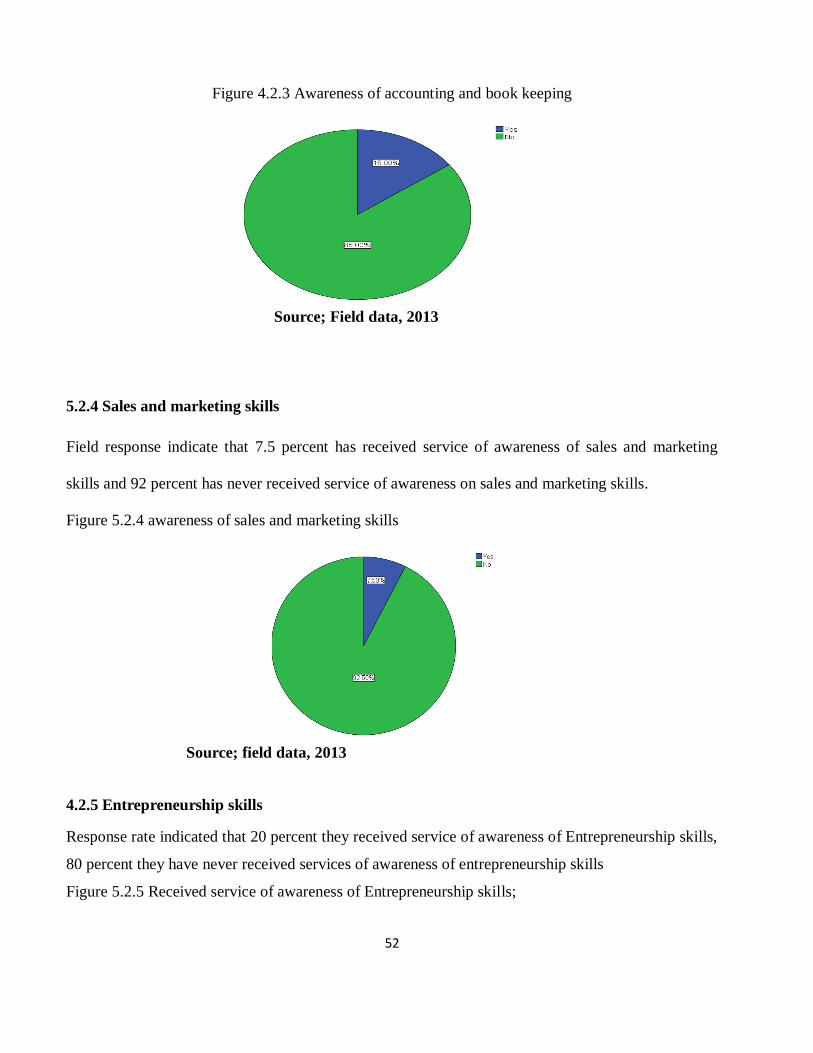

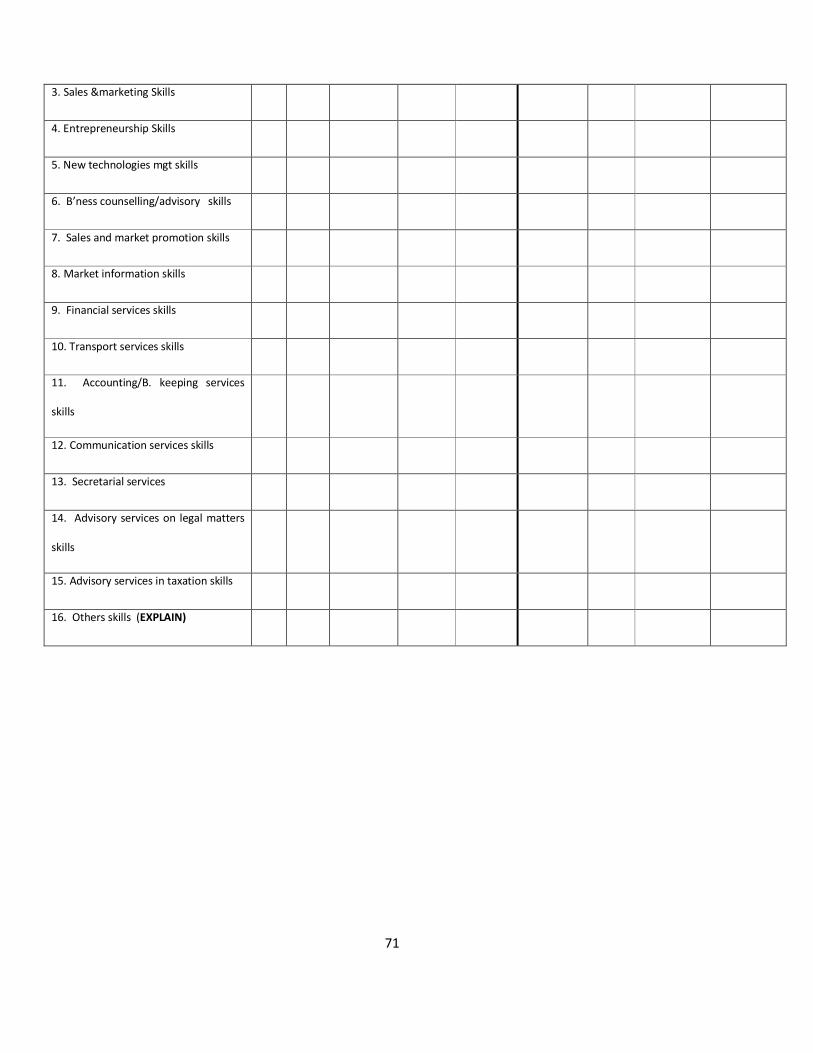

4.2.3 Awareness of Accounting and book- keeping skills

Response rate indicates that only 6(15%) have received service of awareness of accounting and book

keeping skills. 34(85%) said never receive accounting and book keeping skills

4.2.4 Sales and marketing skills

Response Frequency Percentage

Yes 3 10

No 37 90

Total 40 100

Source; field data, 2013

4.2.4 Sales and marketing skills

Field response indicate that 3(10%) has received service of awareness of sales and marketing skills

and 37(90%) has never received service of awareness on sales and marketing skills.

37

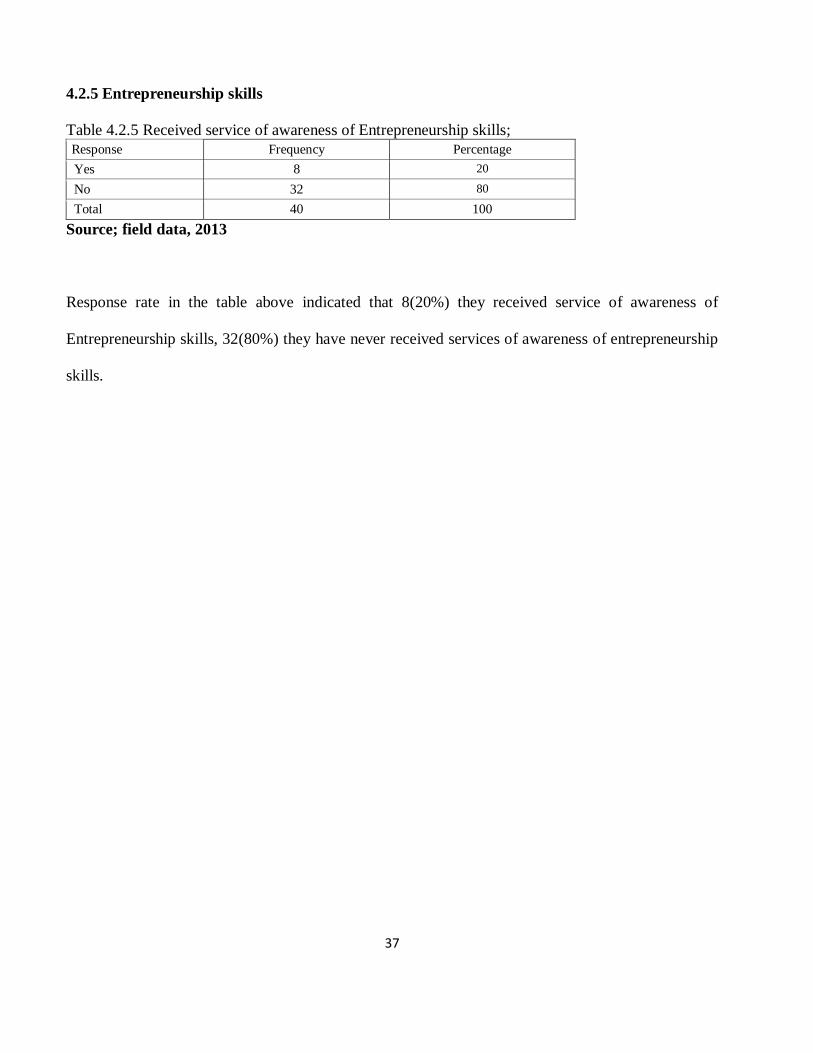

4.2.5 Entrepreneurship skills

Table 4.2.5 Received service of awareness of Entrepreneurship skills;

Response Frequency Percentage

Yes 8 20

No 32 80

Total 40 100

Source; field data, 2013

Response rate in the table above indicated that 8(20%) they received service of awareness of

Entrepreneurship skills, 32(80%) they have never received services of awareness of entrepreneurship

skills.

38

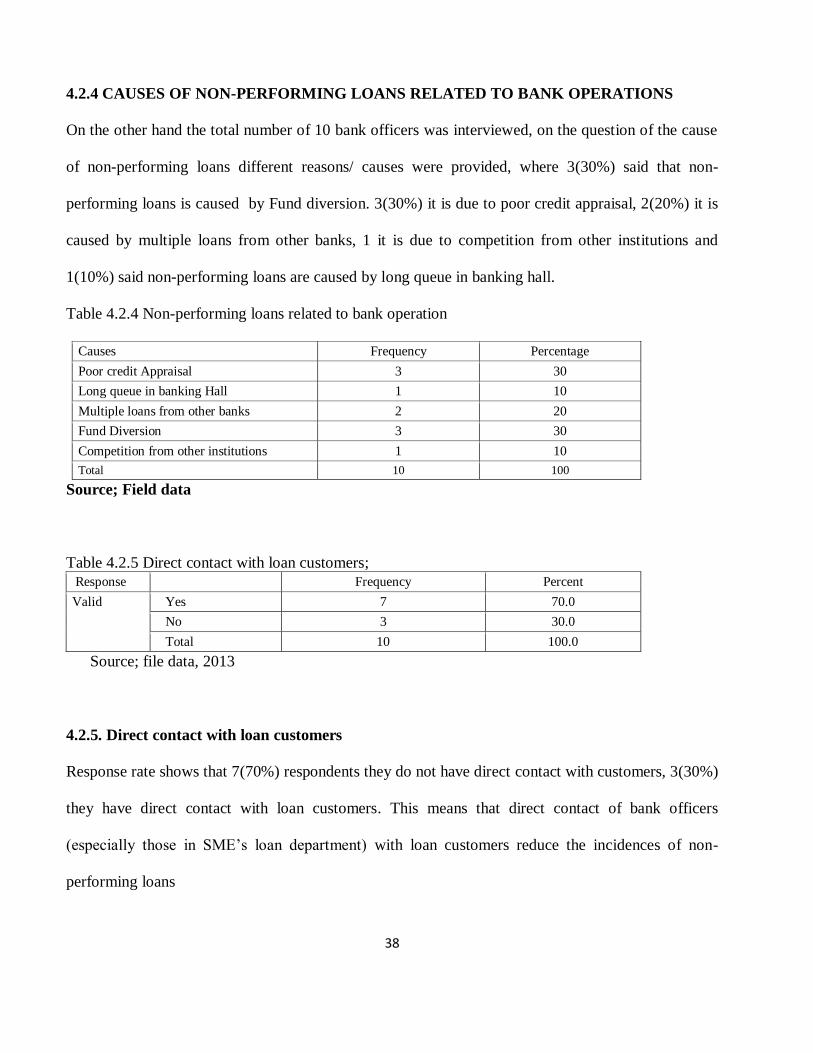

4.2.4 CAUSES OF NON-PERFORMING LOANS RELATED TO BANK OPERATIONS

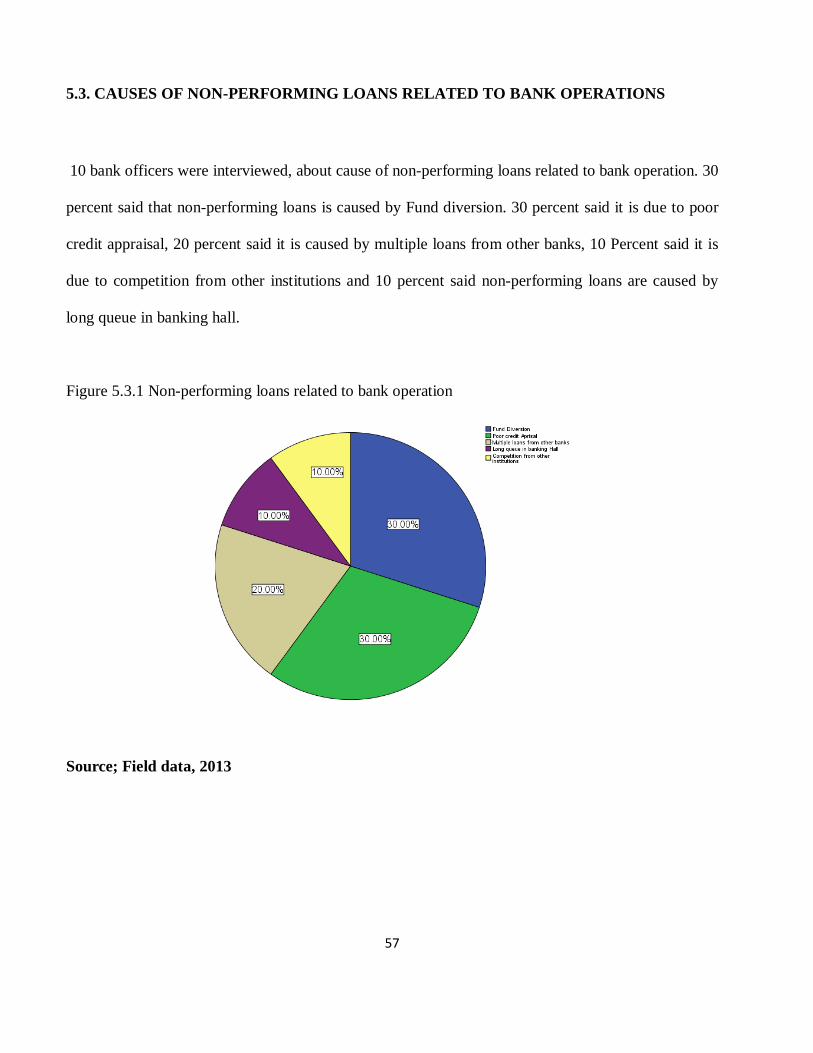

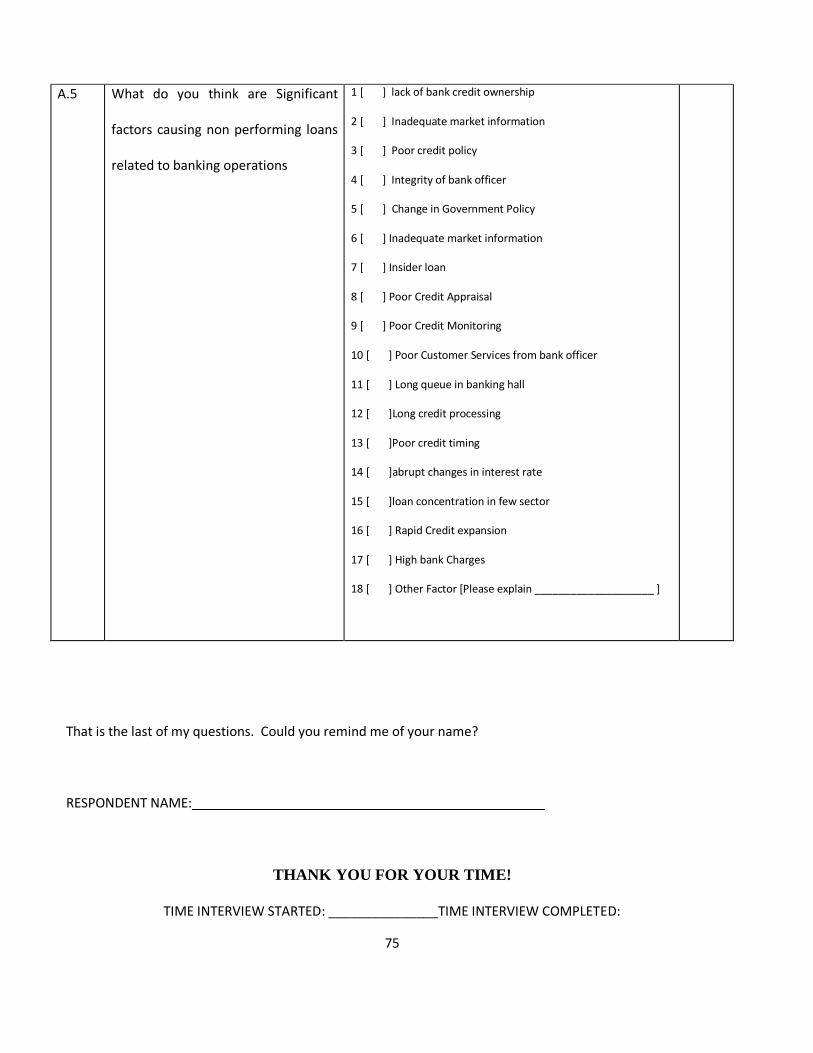

On the other hand the total number of 10 bank officers was interviewed, on the question of the cause

of non-performing loans different reasons/ causes were provided, where 3(30%) said that non-

performing loans is caused by Fund diversion. 3(30%) it is due to poor credit appraisal, 2(20%) it is

caused by multiple loans from other banks, 1 it is due to competition from other institutions and

1(10%) said non-performing loans are caused by long queue in banking hall.

Table 4.2.4 Non-performing loans related to bank operation

Causes Frequency Percentage

Poor credit Appraisal 3 30

Long queue in banking Hall 1 10

Multiple loans from other banks 2 20

Fund Diversion 3 30

Competition from other institutions 1 10

Total 10 100

Source; Field data

Table 4.2.5 Direct contact with loan customers;

Response Frequency Percent

Valid Yes 7 70.0

No 3 30.0

Total 10 100.0

Source; file data, 2013

4.2.5. Direct contact with loan customers

Response rate shows that 7(70%) respondents they do not have direct contact with customers, 3(30%)

they have direct contact with loan customers. This means that direct contact of bank officers

(especially those in SME’s loan department) with loan customers reduce the incidences of non-

performing loans

39

CHAPTER FIVE

5.0 DISCUSSION OF FINDINGS

This chapter gives the analysis and the discussion of findings of the Causes of non-performing related

to Bank and customers operations

5.1 Demographic Characteristics of Respondents

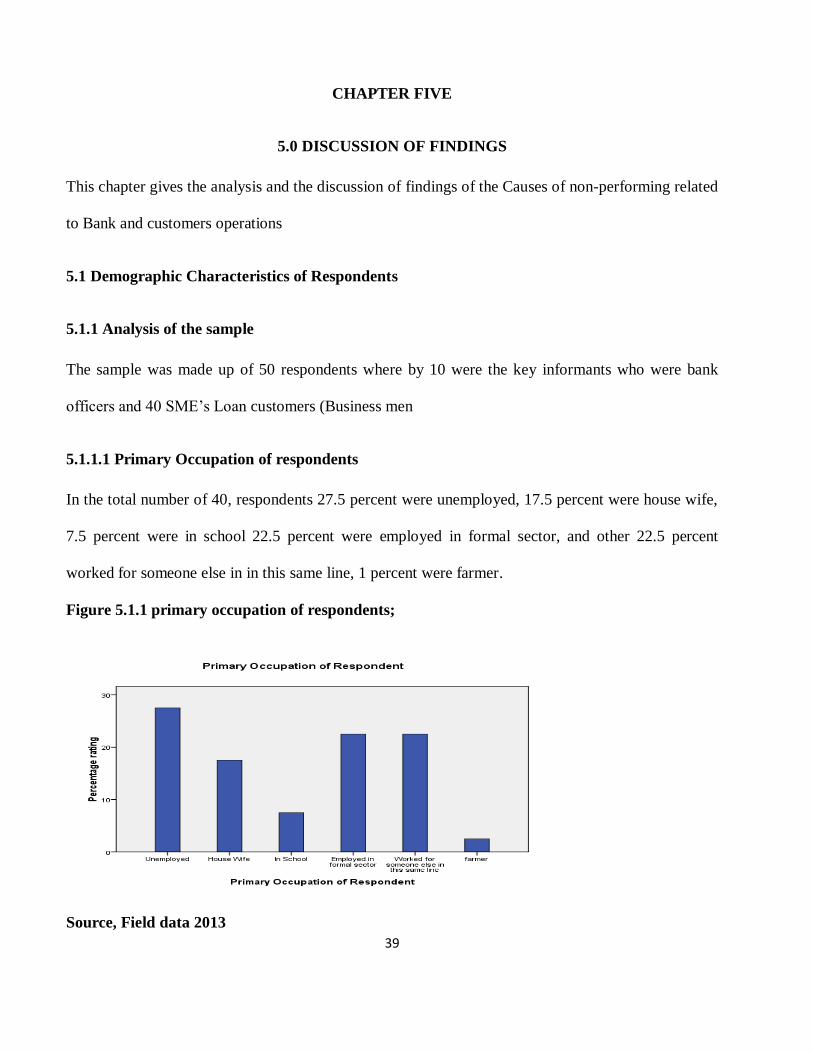

5.1.1 Analysis of the sample

The sample was made up of 50 respondents where by 10 were the key informants who were bank

officers and 40 SME’s Loan customers (Business men

5.1.1.1 Primary Occupation of respondents

In the total number of 40, respondents 27.5 percent were unemployed, 17.5 percent were house wife,

7.5 percent were in school 22.5 percent were employed in formal sector, and other 22.5 percent

worked for someone else in in this same line, 1 percent were farmer.

Figure 5.1.1 primary occupation of respondents;

Source, Field data 2013

40

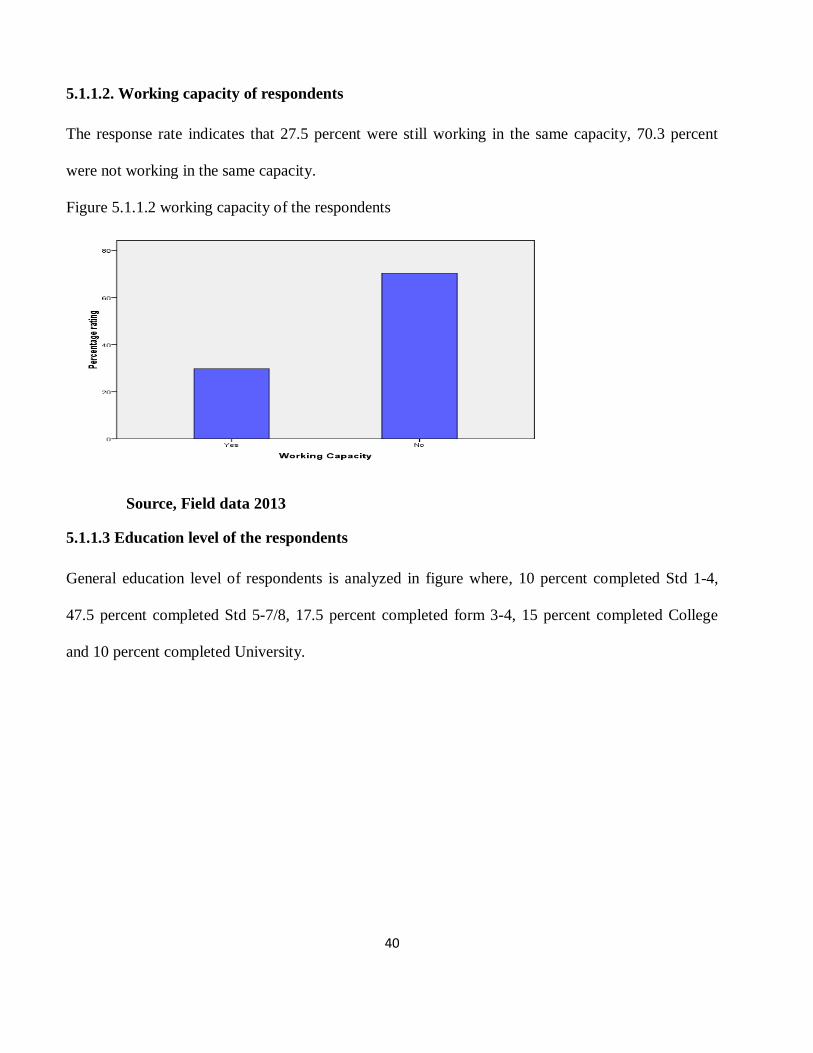

5.1.1.2. Working capacity of respondents

The response rate indicates that 27.5 percent were still working in the same capacity, 70.3 percent

were not working in the same capacity.

Figure 5.1.1.2 working capacity of the respondents

Source, Field data 2013

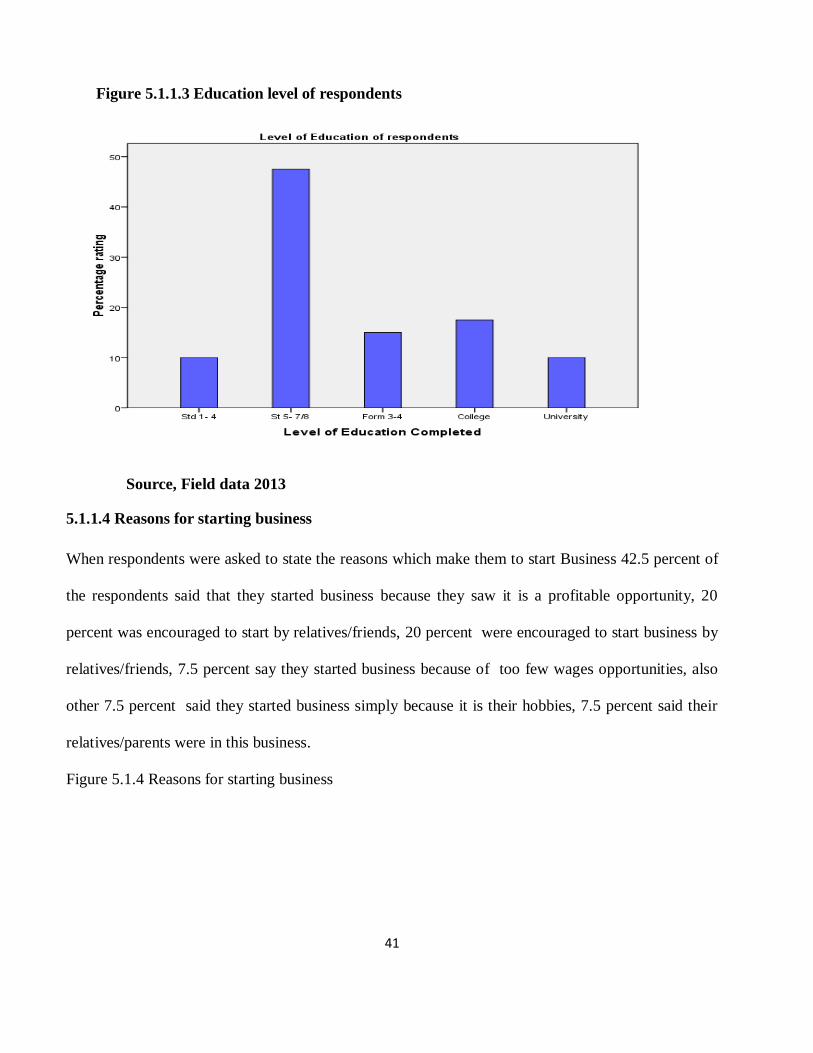

5.1.1.3 Education level of the respondents

General education level of respondents is analyzed in figure where, 10 percent completed Std 1-4,

47.5 percent completed Std 5-7/8, 17.5 percent completed form 3-4, 15 percent completed College

and 10 percent completed University.

41

Figure 5.1.1.3 Education level of respondents

Source, Field data 2013

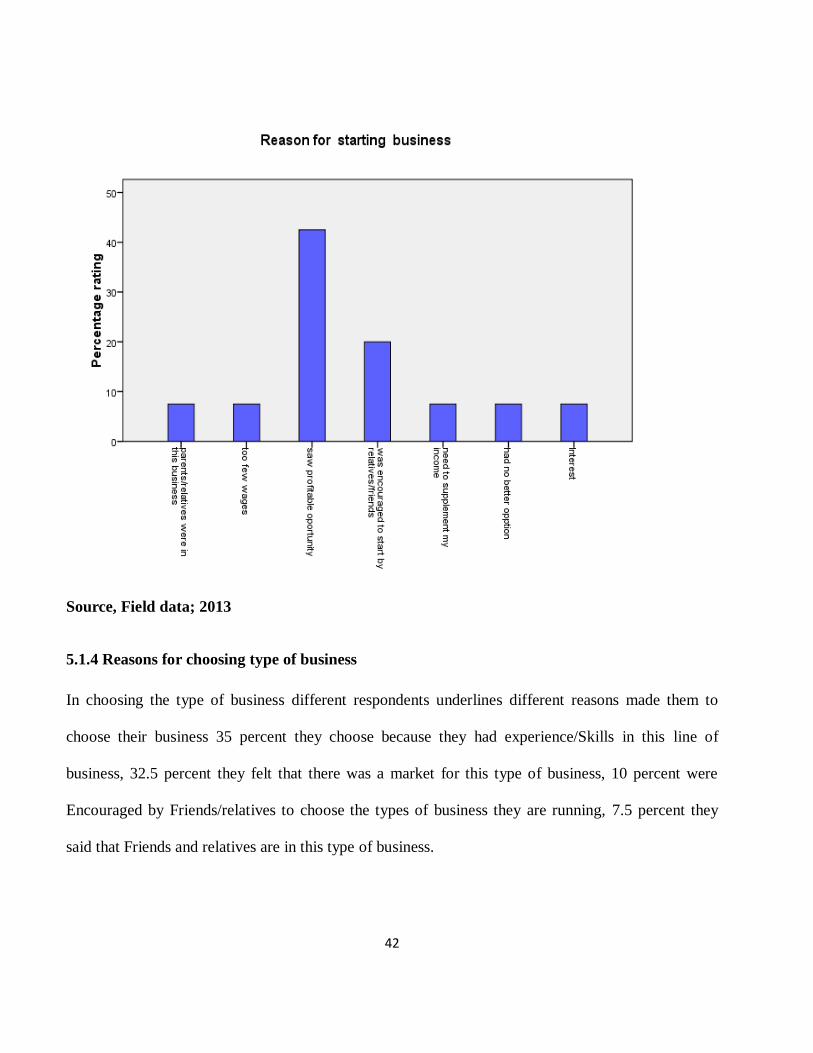

5.1.1.4 Reasons for starting business

When respondents were asked to state the reasons which make them to start Business 42.5 percent of

the respondents said that they started business because they saw it is a profitable opportunity, 20

percent was encouraged to start by relatives/friends, 20 percent were encouraged to start business by

relatives/friends, 7.5 percent say they started business because of too few wages opportunities, also

other 7.5 percent said they started business simply because it is their hobbies, 7.5 percent said their

relatives/parents were in this business.

Figure 5.1.4 Reasons for starting business

42

Source, Field data; 2013

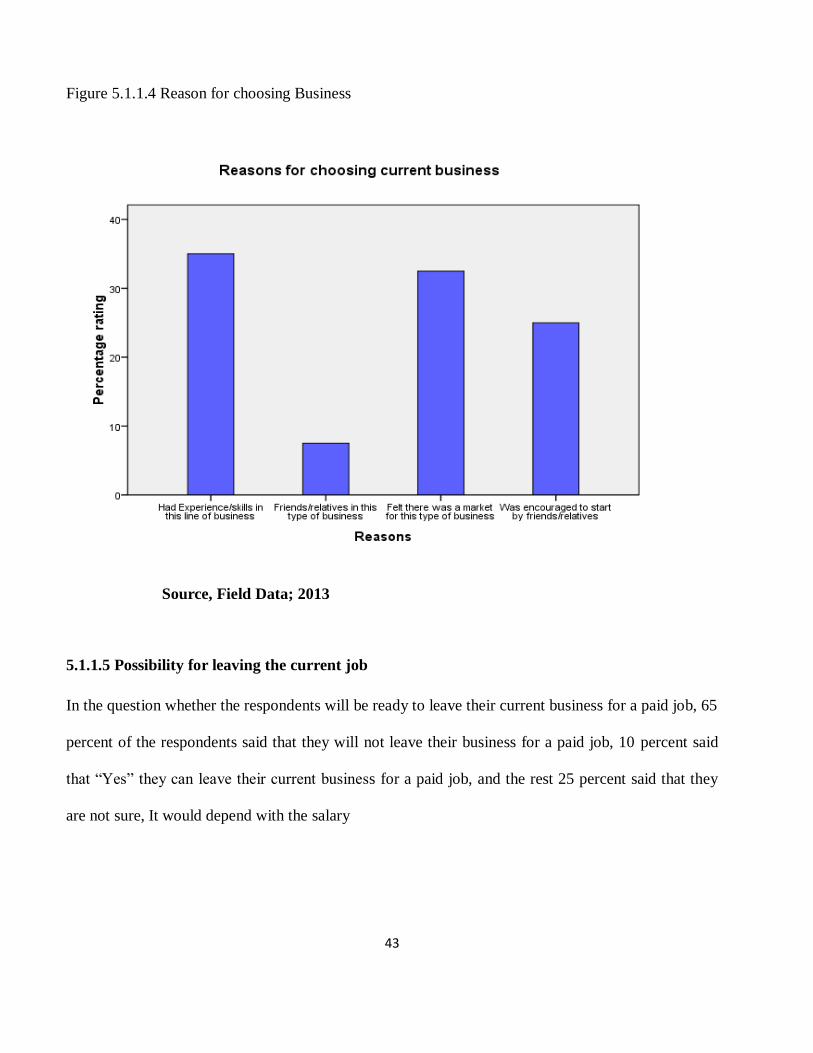

5.1.4 Reasons for choosing type of business

In choosing the type of business different respondents underlines different reasons made them to

choose their business 35 percent they choose because they had experience/Skills in this line of

business, 32.5 percent they felt that there was a market for this type of business, 10 percent were

Encouraged by Friends/relatives to choose the types of business they are running, 7.5 percent they

said that Friends and relatives are in this type of business.

43

Figure 5.1.1.4 Reason for choosing Business

Source, Field Data; 2013

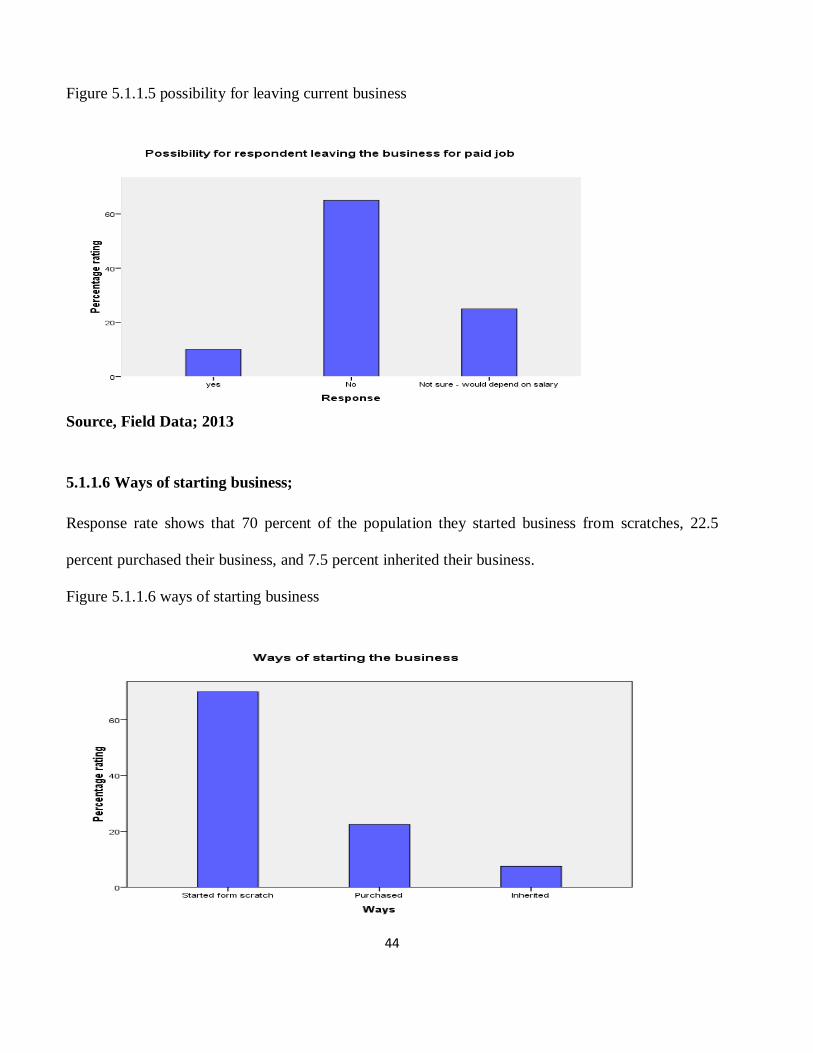

5.1.1.5 Possibility for leaving the current job

In the question whether the respondents will be ready to leave their current business for a paid job, 65

percent of the respondents said that they will not leave their business for a paid job, 10 percent said

that “Yes” they can leave their current business for a paid job, and the rest 25 percent said that they

are not sure, It would depend with the salary

44

Figure 5.1.1.5 possibility for leaving current business

Source, Field Data; 2013

5.1.1.6 Ways of starting business;

Response rate shows that 70 percent of the population they started business from scratches, 22.5