Embed Size (px)

Citation preview

An Energy Outlook for 2019 Macro Trends and Perspectives

Regina MayorGlobal Sector Head and US Sector Leader Energy and Natural ResourcesJanuary 8, 2019

2© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 710228

2© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 773491 #KPMGGEC

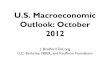

-20%

-15%

-10%

-5%

0%

5%

10%

Dow Jones NYSE Energy Index

Overall positive company outlooks, but less certainty on the economic front

90% CEOs confident in their company’s growth prospects

67% CEOs confident in growth of the global economy

© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 773491

Source: 2018 KPMG CEO Survey, Wall Street Journal

Dow Jones -5%NYSE Energy Index -19%

3© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 710228

3© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 773491

CPE code: ccf6 #KPMGGEC© 2018 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 773491 #KPMGGEC

While prices are down confidence remains within the sector

© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 773491

Source: 2018 KPMG CEO Survey, EIA

88% Oil & Gas 89% Power & Utilities CEOs confident in their company’s growth prospects

40

50

60

70

80

90

WTI Brent

4© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 710228

Although prices have been volatile, rig counts have steadily increased over the year

Sources: Baker Hughes, U.S. Energy Information Administration; CNBC; Bloomberg

1,527

750526

747 799 860 865 885

333

226

132

183 194 187 189 198

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2014 2015 2016 2017 Mar-18 Jun-18 Sep-18 Dec-18

Oil Gas

U.S. Rig Count

What does this mean for rig counts going into 2019?

11.7

44%

$42

U.S. oil production now at 11.7 mbpd

WTI minimum price since June 2016

WTI maximum price since June 2016

$77930

1083+16%

5© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 710228

And breakeven prices have come down allowing for continued production in this environment

Chart Source: Wood Mackenzie

20

30

40

50

60

70

80

ThreeForks

Bakken BoneSpring

Niobrara SCOOP/STACK

EagleFord

Wolf-camp

Midland

Wolf-camp

Delaware

LowerTertiary

Pliocene Jurassic Miocene SubsaltMiocene

Duvernay Montney Cardium

Less competitive

More competitive

Lower 48 states Gulf of Mexico Canada Basin average 12-month average WTI oil futures price

$80 per barrel

Disruptive Forces in Oil & Gas

7© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 710228

Mobility

Urbanization

Rise ofMillennials

Multi-generationalWorkforce

AgingPopulation

DownholeTechnology

EOR Techniques

Pad Spacing

Seismic ReservoirAnalysis

Drones/remoteManagement

IntelligentAnimation

Big Data

Blockchain

Internet ofThings

At the same time several macro disruptive forces are at play

8© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 710228© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 623964 8

Demographics are influencing the industry

50% of the workforce will be millennials by 2020

77% of HR executives within Oil & Gas recognize the need for the workforce to be transformed, yet less than half are confident in HR’s actual ability to transform

The Future of HR

The Changing Workforce

Source: KPMG HR Survey

9© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 710228© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member

firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 623964 9

Technology impacts are top of mind for Energy CEOs

Artificial Intelligence 85% of Oil & Gas CEOs report they’re piloting AI or have already begun implementation of AI for some processes

Job Growth58% of Oil & Gas CEO’s feel that AI and robotic technologies will create more jobs

10© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 710228

Companies are also focusing on managing commodity price volatility through targeted improvements…

Adoption of lean six sigma techniques and digital technology/automation to reduce waste in current processes, drive increased design and process standardization, and eliminate rework and quality issues

Streamlined and standardized processes

Work along side contractors and suppliers to identify potential areas to reduce costs and increase efficiency through greater coordination of forecast, design changes, adoption of latest technologies, and execution performance

Increased integration with contractors

Task level planning geared around standard processes, driving increased ability to predict performance, leverage predictive analytics, reduce variation, establish roles and responsibilities, and improve performance

Effective field level execution planning

Performance management and accountability

Performance accountability driven down to the field level, with an integrated approach with contractors to establish a “one-team” performance mentality

11© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 710228

11© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 773491

Additionally companies are focusing on an alternate energy portfolio

Drivers of the Renewable Energy Transition

1. Increased competiveness of renewable pricing 2. Investor pressure to reduce carbon3. Customer and employee pressure for same4. Changes to information reporting standards5. Industry peer pressure

EV/AVs and the Impact on Demand

13© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 710228

Expansion in mileage will result from substantial increases at both ends of the age spectrum

Safe independence for the kids

Children will have the freedom tosafely travel to meet up with friendsor go to the movies or countless other activities

Convenience of “my time”

Working parents and young adultscan travel further to work as AVtechnology allows them to beproductive even during thecommute

Independence for seniors

The safety of seniors driving asthey age will no longer be aconcern and they can continuebeing active

9,95012,935

14,650

9,672

12,13713,044

14,878

12,966

Pre-driving (0 – 15)

Young Adults (16 – 29)

Parents (30 – 64)

Seniors(65+)

2015 2040

U.S. personal miles traveled (PMT) per capita

+22%

+1%

+2%

+34%

14© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 710228

These combined forces result in an inflection point for both vehicle ownership models and mileage trends as forces begin to take hold

Regional Total Cost of Ownership (TCO) tipping-point on the horizon

U.K. to Ban Internal Combustion Engine Vehicles by 2040The Guardian, July 25th

California utility regulatorsare turning electric vehiclesinto grid resourcesGreentech Media, April 13th

Ecosystem view of U.S. vehicle miles traveled (VMT)2016 – 2040(a)

Alphabet's Waymo Taps Avis For Self-DrivingCar Maintenance ServicesForbes, June 26th

Examples of the new mobility ecosystem emerging

Note: (a) Other includes motorcycles, non-AV MaaS, and non-AV commercial personal vehicles (e.g. police cars)

Personal Miles Traveled on a Personally Owned Vehicle with no Autonomous Capabilities

AV PersonalICE

AV Personal– EV

AV MaaS– EV

4.3

2.9

1.9

0.6

Thank you

Regina Mayor - Global Sector Head and U.S. Sector Leader of Energy and Natural ResourcesPhone: 713 319 3137Email: [email protected]

© 2019 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. NDPPS 710228

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

kpmg.com/socialmedia

Some or all of the services described herein may not be permissible for KPMG audit clients and their affiliates.