Embed Size (px)

Citation preview

Service sectors restrictiveness and economic performance: an

estimation for the MENA1 region

Novella Bottini, Mohamed Ali Marouani and Laura Munro

2

Abstract This article aims at assessing barriers to service provision in the banking and telecom (fixed and

mobile) sectors of four MENA countries, and the impact of these restrictions on firm performance. The

analysis is focused on computation of aggregate and modal trade restrictiveness indexes (TRIs) by

sector, drawing on information gathered from detailed questionnaires. These TRIs are used as

regressors of firms‟ economic performance indicators. The estimated coefficients of the TRIs are then

used to compute aggregate and modal tax equivalents of service restrictions by sector. The first

conclusion of this article is that significant regulatory reforms have taken place in the service sectors

over the last decade, but that a broad range of restrictions still remain. The most significant change in

these service sectors has been the lifting or softening of constraints on foreign equity participation.

These regulatory reforms, however, have had varying degrees of impact on market structure depending

on the country and the sector. The second conclusion is that service restrictions have an impact on

economic performance in the three studied sectors. While a rent-creating effect seems to dominate

restrictions on banking and fixed telecom sectors, a cost-inefficiency effect seems to dominate the

mobile telecom sector. Finally, interactions between modal restrictions seem to be taking place,

especially in the telecom sectors.

I Introduction

Given the large share of services in the world‟s GDP (around 60%) and their much lower

share in world trade (around 30%) trade theorists and practitioners have to understand the

reasons behind this difference and the contribution of regulatory service barriers to the

relatively low level of trade in services (Dee, 2003). Once we improve our knowledge of the

impediments to trade in services, we also need to understand the links between these

impediments and economic performance.

As argued by Konan and Kim (2004), the MENA region is a good candidate for an

examination of service trade policies due to its low economic performance in comparison to

other regions in the world. Moreover, high unemployment rates in the region, especially

among educated youth, argue in favor of developing service sectors, which are more intensive

in skilled labor.

1 Middle East and North Africa

2 Bottini : OECD and Cattaneo University -LIUC- ([email protected]); Marouani: Université Paris 1-

Panthéon-Sorbonne, DIAL, ERF and OECD visiting expert for this study ([email protected]);

Munro: OECD and Columbia University ([email protected]).

Acknowledgement: The authors would like to thank Raed Safadi for his constant support. The paper

has benefited from helpful comments from Dale Andrew, Bernard Hoekman, Douglas Lippoldt, Margit

Molnar, Hildegunn Nordas, Ben Shepherd, delegates at the Working Party of the Trade Committee,

and participants at the ERF 15th

Annual Conference in Cairo, Egypt. The authors also gratefully

acknowledge the financial support of the International Development Research Centre (IDRC) for the

realization of this study.

Measuring service restrictions provides a more objective basis for domestic policy debates, as

well as for bilateral, regional and international negotiations through more transparent

evaluations of reciprocity in concession-making (Findlay & Warren, 2000). Our investigation

can in this regard be useful in view of the Euro-Mediterranean negotiations on services

liberalization that were launched in the Marrakech Ministerial on 24 March 2006 with

participation from the EU, Egypt, Israel, Jordan, Lebanon, Morocco, the Palestinian Authority

and Tunisia. The EU has also begun to engage in bilateral negotiations with Egypt, Morocco

and Tunisia since the end of 2006.

However, assessing trade in services barriers is more difficult than assessing barriers to trade

in goods. Indeed, as noted by Hoekman (2006), given the domestic regulatory nature of

barriers to trade in services, there is no information on these restrictions in the form of

databases (as in the case of tariffs, for example). The quantification of these barriers must be

preceded by a collection of information on a sector-by-sector basis, relying on government

documents and the expertise of sector specialists (Mattoo, Stern, & Gianni, 2008). A useful

tool to synthesize this qualitative information is the Trade Restrictiveness Index (TRI)34

.

Although this method has been mainly applied in manufacturing sector analysis (Irwin, 2007),

it has also been adapted for services studies. The TRI translates qualitative information on

services regulations into an aggregated quantitative score by sector.

The two main benefits of synthesizing qualitative information in a quantitative index are first,

to enable the comparison of restrictions across countries at the sectoral level, and second, to

determine the impact of barriers on trade in services and on different variables of economic

performance. The main risk of such an exercise, however, is the traditional one researchers

face when moving from qualitative information on policy to a synthetic quantitative index:

some dose of subjectiveness. The methodological improvements proposed by researchers on

these subjects such as the use of factor analysis techniques try to minimize the subjectivity5.

The first objective of this article is to improve the estimation of service restrictions of barriers

in the banking and telecom (fixed and mobile) sectors of four MENA countries (Egypt,

Jordan, Morocco and Lebanon (for the banking sector only)). The choice of these sectors has

been driven by the idea that further integration of the MENA region into the world economy

would require the development of telecommunication sectors (mainly for backbone service

sectors where the region seems to have a comparative advantage) but also of efficient banking

services to help exporters better compete in the international markets.

Country selection for this study is primarily driven by recent reforms that have been

implemented in these sectors. The four countries included in this study have started domestic

reform programs to varying degrees in the analyzed service sectors. It is, thus, interesting to

assess the progress of reforms implemented at this stage. Given the scarce evidence available

for the MENA region and for developing countries in general, our analysis improves the

understanding of service barriers and offers useful policy implications.

This analysis covers the evolution of the regulatory framework of service sectors, as well as

the implementation of these regulations and their degree of restrictiveness. From this

perspective, we consider the following questions: Which reforms have reduced barriers to

trade in services in recent years? What disparities exist between regulations in principle and

in practice? How does the government maintain control despite the implementation of liberal

3 The concept of the Trade Restrictiveness Index was first proposed by Anderson & Neary (1994).

4 It is worth noting that this index captures restrictions to both foreign and domestic firms. Hence it is

not a pure „trade‟ restrictiveness index but it includes also constraint on domestic provision. 5 See Boylaud & Nicoletti (2000) for the use of factor analysis in determining the weights of the

different components of a synthetic index.

reforms? Foreign equity limits, for example, have been relaxed in most MENA countries in

recent years, yet many service markets remain dominated by state-owned or domestic

enterprises. High levels of state control persist in such cases through conflicting regulations

that protect current market structures.

The second objective of this study is to capture the impact of impediments to trade in services

on firm performance. Following Dihel and Shepherd (2007) we use sectoral firm performance

indicators as a proxy for the price-cost margin and we estimate the impact of TRI (both

aggregate and modal TRI) on them. In particular, the inclusion of modal TRI (the four modes

defined by the GATS6) allows us to investigate the issue of complementarity and substitution

between modes. The innovation of this work includes improvement in the regression‟s

econometric specification and greater reliance on developing countries data in the samples.

Different useful policy insights could be drawn from this analysis. Indeed, the sign of the TRI

coefficient in the regression also offers relevant policy conclusions. A positive impact of the

TRI on the price-cost margin suggest a rent-creating effect, i.e. policy that protects the local

market by allowing firms to charge a price mark up over marginal costs. On the other side, a

negative sign indicates a cost-creating effect, and consequently, a cost-inefficient market. The

implicit hypothesis behind this analysis is that firms in an uncompetitive environment charge

a lower mark up because they are constrained by higher costs induced by the higher levels of

protection. Accordingly, a negative TRI in the regression is associated with a cost-inefficient

market. As suggested by Hoekman (2006), “if the policies generate real costs, removing them

may give rise to much greater welfare gains than is the case if the policies generate rents that

are captured by domestic agents”. Indeed, while in the first case we would remove a market

inefficiency, in the second case we support a redistribution of income. While domestic firms

could suffer market share losses owing to the increased competition, local consumers (final

and intermediate) would gain in terms of better service quality, wider choice and lower prices.

However, in reality, service barriers are always rent-creating and cost-creating at the same

time. Given that performance indicators include both effects, the sign of the coefficient gives

us the dominant effect. A powerful tool to disentangle the two different effects would be to

separately regress the TRI on costs and prices. However, as these kinds of data are rarely

available, we follow the literature and rely on price-cost margins, which are accessible

through company account databases.

The third objective of this study is to compute tax equivalents of service restrictions. A tax

equivalent is the wedge between the actual price and the price that would prevail without

service barriers. The estimation of tax equivalents of services barriers was pioneered by the

Australian Productivity Commission. They can be used as inputs for modelling exercises such

as those performed by Konan and Kim (2004) or Konan and Maskus (2006).

The rest of the article is organized as follows: section two presents the methodology of the

article, section three presents the results and section four concludes.

6 Cross-border supply (mode 1) refers to the supply of a service from the country of the supplier into

the country of the consumer. Consumption abroad (mode 2) involves the purchase of services by the

consumer while abroad in the country of the supplier. Commercial presence (mode 3) entails the

supplier providing services through foreign-based establishment in the country of the consumer.

Movement of natural persons (mode 4) relates to the supply of services by an individual from the

country of the supplier (for short or long-term) in the country of the consumer.

II Methodology

In service sectors, barriers take the form of quotas, prohibition, licenses and government

regulation, none of which can be directly quantified. Owing to these features, our analysis

requires different steps of analysis. The first step is the computation of TRIs. Then, the

computed restrictions are regressed on sectoral performance7 to identify their economic

impact. Finally, the estimated TRI coefficients are matched with the TRI index and

transformed into tax equivalents. This section provides a detailed explanation of the

methodology applied in the three steps enumerated above.

II.1 The First Step: The TRI Computation

To compute the TRI, we have gathered qualitative information through questionnaires

completed by government agencies and country reports written by trade experts in the MENA

region8, as well as supplementary research. The qualitative information has been used to

determine the values of the different components of the sectoral aggregate and modal indexes.

The weight of each component has been determined through principal component analysis

(Marouani and Munro, 2009).

Assessing the restrictiveness of barriers to trade in services involves the identification of the

relevant barriers, their classification and their quantification, and the assessment of their

impact on trade and/or economic performance. This section discusses the different

methodological approaches to identification, classification and quantification.

The identification

To develop our questionnaires we relied on a similar set of questions to those put forward in

Dihel & Shepherd (2007), who draw on work by the Australian Productivity Commission

(Mcguire & Schuele, 2000). The indexes address key issues for each sector, such as foreign

equity limits and movement of workers. Relying on these indexes allows us to use data on

non-MENA developing countries gathered by Dihel & Shepherd (2007) in the factor analysis

(discussed further in the following section), which is a necessary input given the small size of

the MENA countries sample.

The classification

Service barriers can be classified according to various criteria such as by mode or de facto

versus de jure. As services are traded by mode, and as WTO and bilateral negotiations are

categorized accordingly, it is useful to disaggregate the sectoral trade restrictiveness indexes

by mode (Dihel & Shepherd, 2007). Cross-border supply (mode 1) refers to the supply of a

service from the country of the supplier into the country of the consumer. Consumption

abroad (mode 2) involves the purchase of services by the consumer while abroad in the

country of the supplier. Commercial presence (mode 3) entails the supplier providing

services through foreign-based establishment in the country of the consumer. Movement of

natural persons (mode 4) relates to the supply of services by an individual from the country of

the supplier in the country of the consumer. This classification offers a clearer picture of the

7 Performance indicators are not the same for banking and telecom: the net interest margin (NIM) used

in the banking sector is more important for consumers, while the performance indicator used in

telecom, EBITDA is more a profit index for firms. 8 Qualitative information was gathered in the context of the OECD-IDRC-ERF project “Promoting

trade in services in the MENA region”. Country reports were drafted by Lahcen Achy (Morocco), Jad

Chaaban (Lebanon), Ahmed Ghoneim (Egypt), and Marwan Kardoosh (Jordan). As information from

the four country reports is used heavily throughout our analysis, we do not cite the former on every

occasion.

nature of services restrictions and permits the isolation of barriers with the highest potential

impact on services trade.

To the extent possible, we also classify restrictions as de facto versus de jure. While our

assessment of the individual index components is based primarily on national legislation,

certain components take into account the absence of implementation due to other constraints,

such as conflicting legislations. For example, if a country puts no restrictions on the

commercial establishment of foreign banks, but at the same time no foreign bank exists in the

country, we take indirect restrictions into account in the index computation to the extent that

information is available.

The quantification

The index is constructed so that each component could have either a „yes or no‟ answer or

three or more response categories (see Marouani and Munro (2009) for index components).

We relied on the statistical method, drawing from data gathered for Dihel & Shepherd (2007).

The variant of factor analysis used for these sectors is principal component analysis. This

approach was used to determine the weight of each component in the aggregate TRIs and the

weight of each component in the modal TRIs. With this approach, weights are computed in

order to maximize the variance of scores within the sample of countries. Each weight is the

contribution of the given component to the index variance and does not reflect a subjective

judgment of the component‟s relative relevance or importance to trade.

The sectoral principal component analyses (PCA) are thus run at two levels: the first level is

performed with all the components of the index to determine aggregate sectoral weights,

while the second group of PCAs are run at the modal level (with the different components of

each mode separately) to determine sectoral modal weights. The aggregate and modal weights

calculated can be found in Marouani and Munro (2009). Index components are normalized9

before the computation of aggregate and modal scores. The scores obtained are then rescaled

to avoid negative values. This is in line with the Dihel and Shepherd methodology, permitting

the comparison of results across the two studies.

Given the estimation techniques used to calculate the TRI, the interpretation of results

requires particular care and should be viewed within the bounds of the approach. In view of

the way the analysis is structured, it is not useful to compare TRI across sectors because each

sector‟s TRI evaluates different components. At the same time, cross-country comparisons

are more robust.

II.2 The Second Step: the Economic Impact of TRI.

The best way of estimating the impact of the TRI on banking and telecom companies‟

performance would be to use price data10

as a dependent variable (Kalirajan et al (2000) for

9 To normalize, the average and standard deviation of the country values are first computed for each

index component. The difference between the raw indicator value and the average is then

divided by the standard deviation to derive the normalized indicator value. This calculation

converts all indicators to a common scale with an average of zero and a standard deviation of

one.

10 Also quantitative data could be used as dependent variable in the regression (Warren, 2000 for

telecom). In this case, calculating the tax equivalent requires additional information: the elasticity of

demand which allows us to transform percentage variation in quantities into percentage variation in

prices (%ΔP=%ΔQ/η)

banking; Trewin (2000) for telecommunications services). However, owing to the lack of this

kind of information, we use price-cost margins, which are readily available from accounting

datasets.

The main advantage of this kind of data is that problems of international comparability are

overcome, as data included in the financial statements follow international standards11

. There

are drawbacks to this approach, but they do not seriously compromise the results.

First of all, MNEs operate on both domestic markets and overseas, and often engage in other

activities (for example some fixed telecom companies also participate in mobile services).

Since company financial statements are derived from consolidated balance sheets, data refer

to general firm activities and hence include profit, assets and liabilities related also to other

markets and activities. We control for this problem by excluding from our dataset firms that

rely much more on overseas activities, such as in Mexico.

Secondly, price-cost margin could include changes in prices and costs due to „second round

effects‟, which dilute the direct effects of the restrictions. Consequently, the real direct effects

could be underestimated (Kalirajan, 2000).

Given our objectives, the first best would be to use data only for MENA countries or at least

for similar developing countries. As explained in the previous section, the estimated

coefficient of the TRI on sector performance plays a key role in the tax equivalent

computation and hence the original sample needs to be fairly representative to obtain a

consistent analysis (Dee, 2003). However, this approach is not feasible as the small size of the

sample impedes a reliable econometric analysis. This problem could be partially overcome in

the first step of analysis since we use firm level data (although the number of banks and

telecom companies in each country is limited). However, it persists in the second stage owing

to the narrow variability of our main variable, the TRI, which is computed only for one year

in each country. Hence, we try to defeat the limited time variability by increasing the

longitudinal dimension of the panel, i.e. adding more countries. As a result, we use both data

for developing and developed countries. In doing so, we fulfil the variability requirement and,

although the differences in the business environment in these countries, we still base our

estimates on a fairly representative sample12

.

II.2.1 Data Source and Variable Description

The estimation of this type of model requires the availability of both firm and country-level

data. Consequently, data are collected from different sources. Firm level data, for firms in

both developed and developing countries, are derived from the financial statements reported

by Datastream13

. Regulation data for the banking sector are taken from the Banking

Regulation Survey (2003-2005), the quarterly interest rates are from IMF data, and telecom

sectoral indicators are from the ITU Yearbooks of Statistics (1996-2005). TRI computation

for non-MENA countries (both aggregate and modal) are taken from Dihel and Shepherd

(2007).

11

However the use of this kind of data is widespread in trade and service literature; see for example

Nguyen-Hong (2000). 12

The decision to add both developing and developed countries can be considered as a second best

choice due to the limited data availability for developing countries: relying on a mixed sample is

preferable than using only data for developed countries (see also the productivity commission‟s

analysis for the APEC economies in Dee (2003)). 13

Data for the Egyptian telecom sector and for some Lebanese banks are taken from the financial

statement available online.

The main variables in this stage of the analysis are the aggregate and modal TRIs.

Our estimation analysis also requires the inclusion of different controls, both at the firm and

country level, which are described in the following section.

II.2.1.a Banking Services

Following the literature, the specification of the econometric model for the banking sector is

based on the Ho and Saunders (1981) theoretical model that investigates bank margin

determinants. This model has been the basis of many empirical analyses and has been

enhanced with the inclusion of other variables such as the effect of regulation (Saunders and

Schumacher, 1997; Kalirajan et al, 2000; Dihel and Shepherd, 2007).

Price-cost margin in the banking sector is usually captured by the net interest margin (NIM).

NIM is computed as the sum of total net interest income (interest earned minus interest paid

on borrowed funds) divided by total interest-earning assets (any asset, such as a loan, that

generates interest income). This measure is closest to the price customers pay for bank

services and, hence, is better suited to the aim of our analysis. Moreover, it is usually

preferred to other bank performance indicators, such as return on equity (ROE).

Saunders and Schumacher identify three main determinants of NIM: prudential regulation;

net expenses from other activities, and the pure spread. Prudential regulation is measured as

liquidity (LIQ_ratio) and capital requirement (K_ratio) ratios. These requisites are necessary

to limit risk of default and preserve the solvency of banks. Usually these requirements

represent additional costs for banks and could be compensated by raising NIMs (Kalirajan et

al., 2000). For this reason, we would expect positive estimated coefficients of these two

regressors.

Net expenses from other activities are measured as the difference between other operational

costs, other than interest expenses, and other earnings divided by total assets (NIERAT). Also

in this case, an increase in net non-interest operating expenses could be covered by an

increase in NIMs.

Finally, the „pure spread‟ represents country-specific features, i.e. economy-wide

characteristics that are constant across all banks in a specific country. It includes the market

structure computed as the fraction of deposits held by the five largest banks14

(concentration

ratio or C5); the interest rate volatility computed as the variance of annualised quarterly

deposit rates (INT_VAR); and prudential regulation (3.1 = capital adequacy, 7.1 = existence

of explicit diversification requirements, 7.3.1 = liquidity reserves, 8.10 = compulsory deposit

insurance, 9.1 = formal definition of non-performing loans). The aggregate TRI (TRI_AGG)

and the different TRIs by mode (TRI_M1; TRI_M2; TRI_M3; TRI_M4) are important

components of the pure spread as well.

II.2.1.b Telecom Services

Specification of the econometric model for the telecommunication sectors relies on a general

specification that is based on models for other sectors that emphasize the importance of

controlling for both firm and country level features (Betancourt and Gautschi, 1993; and

Saunders and Schumacher, 1997).

Following the empirical analysis for other services (engineering, accounting, and

distribution), the price-cost margin is measured as the EBITDA margin, i.e. earnings before

14

The market structure is captured also by a firm-level variable that measures the bank‟s market share.

interest, taxes and accounting depreciation divided by revenues. Among the firm-level

determinants of telecom sector performance15

we identify capital intensity (K_int), which

measures the firm‟s use of capital in producing services and is measured as the ratio of capital

over total sales. It represents both support capacity for the innovation process and the

availability of transmission infrastructure16

and thus should exert a positive impact on firm

profit. Sales (net_sales) and total employment (tot_empl) are used as proxies for firm size.

Large firms are expected to be more stable, as they would generally offer a wider assortment

of products, have broader network coverage, and have reached a critical size to stay in the

market. Hence, size is expected to correlate positively with profit levels. Growth in sales

(g_sales) captures the firm performance and competitiveness. Indeed, it is always linked to an

increase in demand boosted by the introduction of a new product, the acquisition of other

companies, etc. The increase in sales induces an increase in firm profits. Market share

(mkt_share) is computed as firm revenue divided by total telecom revenues. Given that some

firms operate in both the fixed and mobile sectors, the denominator is computed as the sum of

mobile and fixed revenues. An increase in market share mirrors an increase in the firm‟s

market power and could lead to an increase in its profit.

Moving to the economy-wide features, we control for specific fixed and mobile elements. The

sector performance data are captured by the recent growth in fixed telecom or mobile revenue

(fx_revenue_g, mobile_revenue_g), the number of main lines per capita (fx_tel_lines_pop),

or the number of cellular subscribers per capita in the case of mobiles (mob_subs_pop). All of

these elements should have a positive impact on firm profit. The quality of service provision

and the technological level are captured by the percentage of digital mainlines

(mob_subs_digitalshare). Finally, we control for regulation (calculated as the first principal

component of different indicators, as in from Dihel and Shepherd (2007)) and for trade

restrictions (both aggregate and by mode).

II.2.2 Estimation Strategy

The Australian Productivity Commission proposes a two-stage approach to estimating the

impact of TRI on firm performance. The first stage estimation investigates the firm-level

determinants of firm performance in order to capture the sectoral performance due solely to

specific country features17

, the so-called „adjusted price-cost margin‟. The estimation

equation for the first stage is the following:

)= (1)

where i refers to the firm in a particular sector, j to the country. PCM is the firm performance

(NIM for banks and EBITDA margin for telecom firms), X is the firm level characteristics

described above, c is the country dummy. All the variables are average values over the period

2002-2006. Equation (1) is estimated using country-level fixed effect.

The country dummies capture the adjusted price-cost margin and then are used as dependent

variables in the second stage:

= (2)

Where Zj includes all the country-specific features presented above and TRI refers both to the

aggregate and modal TRI. Equation (2) is estimated using OLS. TRI is the base for the tariff

15

These variables are the same both for the mobile and for the fixed telecom firms. 16

However telecom firms often rent transmission supports rather than buying them. 17

It corresponds to the „pure spread‟ in the banking sector. It doesn‟t take a specific name in the

telecom sectors.

equivalent computation. The main rationale behind the two-stage approach is to avoid a bias

estimation due to the inclusion of both firm and sectoral-level regressors. In the presence of

group effects of firms within an economy errors may be correlated and a single-stage

estimation could produce a bias estimate (Moulton, 1986). Conversely, this technique has

three severe drawbacks. First, it assumes two independently distributed error terms, but the

first step ignores it (Nguyen-Hong, 2000). Second, the country dummy estimation heavily

depends on the regressor choice in the first stage and this could impact the TRI significance in

the second stage. Lastly, the second step estimation relies on a very limited variation (we

have just one observation for each country). The final drawback is particularly striking in the

estimation for the telecom sector where the limited number of observations for the mobile

adjusted price-cost margin leads us to put fixed and mobile telecom companies in the same

sample.

The single-step estimation, with the inclusion of both firm-level and country-level data,

allows us to overcome these shortcomings. In particular, this approach directly captures the

impact of barriers on each firms‟ profit margin instead of only explaining the economy wide-

effect of restrictions on each country. In doing so, it exploits the firm level variation in price-

cost margin as opposed to an aggregate fixed effect. Thanks to this additional variability we

estimate separately the impact of TRI on the fixed and mobile sector. Moreover, the bias-

estimation problem is evaded by clustering the errors at the country level, after testing for the

real importance of the country level effect. The main problem using this approach is the

multicolinearity among country level variables. However, the variables that were dropped

owing to multicolinearity were usually not significant in the two-stage approach. The

estimated model is the following:

)= (3)

We estimate the impact of TRI on banking and telecom firm performance using both the two-

stage and one-stage approach. However, we base our comments on the two-stage results and

use the one-stage approach as a robustness check. Finally, while in the two-stage approach

errors are corrected by heteroschedasticity, in the one-stage approach the clustering of data at

country level already gives robust standard errors.

II.3 The Tax Equivalent Estimation

The econometric model above estimates the impact of restrictions on sectoral performance.

Coefficient estimates and TRI values are all the necessary information to transform the TRI

into a tax equivalent that is the hypothetical tax imposing a similar effect on firm‟s

performance as the barriers captured by TRI. A tax equivalent is generally defined as the

percentage price18

increase arising from barriers, i.e how much current prices are exceeding

efficient prices as a consequence of barriers. Mathematically, the tax equivalent is computed

by applying the following formula:

where PCM0j indicates the price-cost margin in country j in the case of no restrictions (i.e.

TRI equal to zero), ceteris paribus. The inclusion of the minimum and maximum of the

estimated 95% confidence interval provides policymakers with a more flexible tool, which is

necessary given the nature of the analysis. Unlike Shepherd and Dihel (2007), we do not

18

In our analysis we refer to the increase in price–cost margin due to barriers.

apply the bootstrapping technique, since it often produces non-significant coefficients and,

consequently, wide intervals that are not very relevant for policy reform design.

III RESULTS

III.1 TRI

III.1.1 Introduction

The following section discusses the results of the TRI indices estimated according to the

methodology presented above. TRI scores provide a point of comparison, indicating which

MENA countries have higher levels of restrictions on trade in services for each sector.

Drawing conclusions about the economic impact of these restrictions is limited, however,

given the subjective nature of the index.

In aggregate, no single country ranked most open or most restricted across all sectors.

Jordan‟s TRI values were generally lower than those of the other MENA countries in this

study. For other countries, however, the TRIs have revealed varying levels of openness across

the various service sectors.

Data included in our calculations are the most current information available through the end

of 2007. We rely heavily on country chapters for our cross-country analysis19

. Comparisons

are frequently drawn to TRI scores from the Dihel & Shepherd (2007) study, for which data

were gathered up to 2005.

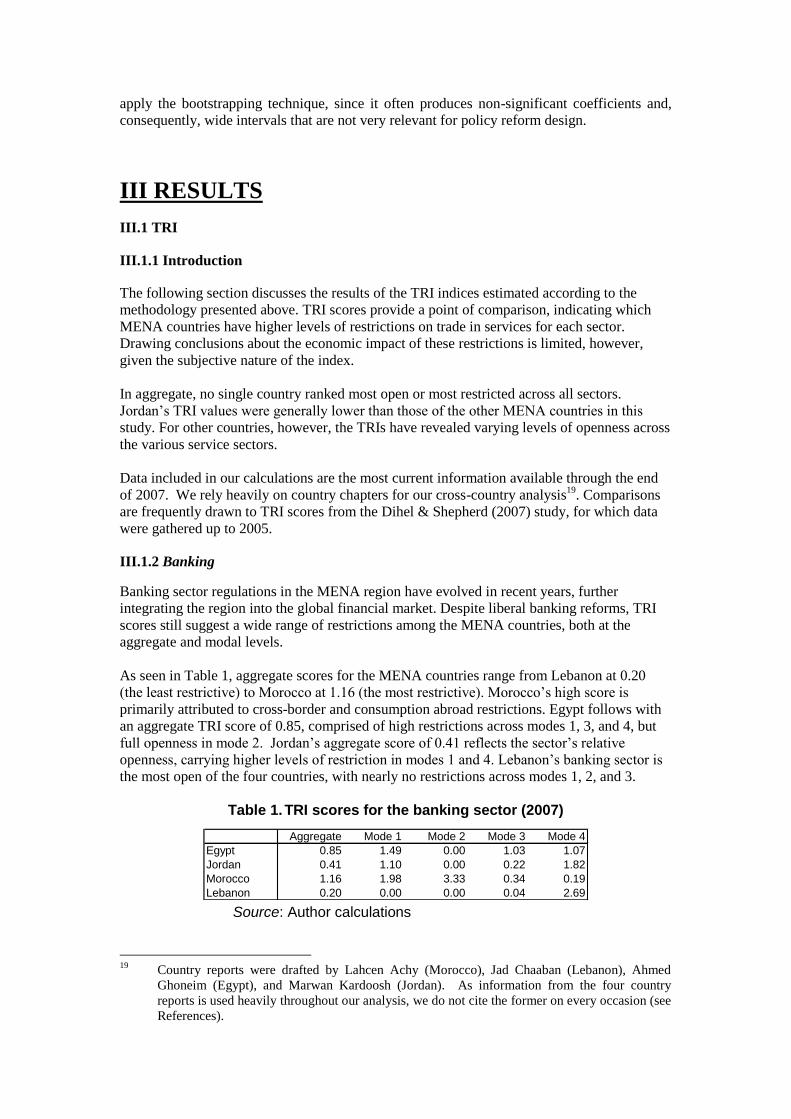

III.1.2 Banking

Banking sector regulations in the MENA region have evolved in recent years, further

integrating the region into the global financial market. Despite liberal banking reforms, TRI

scores still suggest a wide range of restrictions among the MENA countries, both at the

aggregate and modal levels.

As seen in Table 1, aggregate scores for the MENA countries range from Lebanon at 0.20

(the least restrictive) to Morocco at 1.16 (the most restrictive). Morocco‟s high score is

primarily attributed to cross-border and consumption abroad restrictions. Egypt follows with

an aggregate TRI score of 0.85, comprised of high restrictions across modes 1, 3, and 4, but

full openness in mode 2. Jordan‟s aggregate score of 0.41 reflects the sector‟s relative

openness, carrying higher levels of restriction in modes 1 and 4. Lebanon‟s banking sector is

the most open of the four countries, with nearly no restrictions across modes 1, 2, and 3.

Table 1. TRI scores for the banking sector (2007)

Aggregate Mode 1 Mode 2 Mode 3 Mode 4

Egypt 0.85 1.49 0.00 1.03 1.07

Jordan 0.41 1.10 0.00 0.22 1.82

Morocco 1.16 1.98 3.33 0.34 0.19

Lebanon 0.20 0.00 0.00 0.04 2.69 Source: Author calculations

19

Country reports were drafted by Lahcen Achy (Morocco), Jad Chaaban (Lebanon), Ahmed

Ghoneim (Egypt), and Marwan Kardoosh (Jordan). As information from the four country

reports is used heavily throughout our analysis, we do not cite the former on every occasion (see

References).

Regarding mode 1, Lebanon is the only country in this study with no cross-border restrictions

in the banking sector. Banks, corporations, and households in Lebanon are permitted to both

borrow and make deposits on a cross-border basis, i.e. from foreign banks situated abroad.

Lebanon and Jordan‟s lower mode 1 scores are reasonable given the large cross-border trade

of services that has historically been taking place in the region (Jordan mainly with the

Palestinian territories and Lebanon with Syria and many other MENA countries). Morocco

and Egypt record higher restriction levels, but these levels have relaxed in recent years. Prior

to 1991, Moroccan companies, for example, were not allowed to borrow from abroad.

Lowering restrictions on foreign exchange control has allowed Attijari Wafa Bank to open a

subsidiary in Senegal and to take majority ownership of the former Tunisian „Banque du

Sud‟.

TRI results for mode 2 reveal Morocco‟s banking sector to be the most restrictive. Residents

of Morocco are not authorized to purchase financial services abroad. Residents of Egypt,

Jordan, and Lebanon, meanwhile, are completely unrestricted in mode 2.

Mode 3 barriers have decreased across Egypt, Jordan, and Morocco relative to TRI scores

from the Dihel & Shepherd (2007) study. Egypt‟s aggregate score for mode 3, however, still

reflects high restrictiveness. Morocco has slightly lower mode 3 restrictions, but is the only

country of those analyzed in this study that imposes foreign equity limits. While Moroccan

regulation previously limited foreign ownership to 49%, this restriction was recently lifted.

The new Moroccan banking law reserves however the right to limit foreign ownership in a

major bank20

if acquiring such interests would imply majority control21

.

Egypt has liberalized as well, reforming several regulations in 1991 that had previously

discriminated against private, and thus foreign, banks. For example, foreign partners are now

allowed majority equity holdings in joint venture banks. Liberalization reforms such as these,

however, have been slow to generate an impact in practice. Of Egypt‟s four banks, three

remain 100% domestically-owned public banks. The Bank of Alexandria (the smallest of the

four banks) was recently privatized and is now 80% foreign-owned. There has been

discussion of further plans for privatization, but nothing has materialized as of yet.

Lebanese regulation on foreign equity limits was liberalized more recently. In 2001, foreign

ownership rights in the banking sector rose from 30% to 100% in an effort to promote an

influx of FDI. Five of Lebanon‟s six largest banks currently include foreign equity, two of

which have a foreign majority holding.

Meanwhile, four of Jordan‟s six largest banks have a majority foreign ownership. Two of

Morocco‟s six largest banks have a majority foreign ownership (four of the six are partially

foreign-owned). Likewise, two of Lebanon‟s six largest banks have a majority of foreign

ownership (five of the six are partially foreign-owned).

TRI analysis reveals that Morocco and Lebanon are the most liberal in regards to the issuance

of banking licenses. Jordan‟s license procedures are relatively open apart from a higher fee

than that of the other countries in this study. Alternatively, license issuance in Egypt is more

restricted, as it is determined by discretionary approval of the Central Bank of Egypt. Entry in

the Egyptian banking sector is restricted according to economic needs, limiting both the entry

of new domestic and foreign banks and the number of foreign bank branches. (All other

20

Represents more than 12% in terms of assets, deposits, or credits of the entire Moroccan

banking system. 21

As an example of use of this discretionary power we can cite the refusal by Bank Al Maghrib of

the French Caisse d‟Epargne offer to buy 25% of BMCE bank (one of the largest banks in

Morocco).

countries studied have no policy restrictions on the entry of new banks.) The historical trend

in Egypt of favoritism of public banks over private banks has lessened, however, in recent

years. A bank privatization program was also introduced to promote market consolidation

and increase competition in the private sector.

Mode 4, the movement of natural persons, poses varying levels of restrictions across the

MENA countries. TRI scores indicate that Jordan is the most restrictive in mode 4 overall,

while Morocco is the most liberal. The entrance of short-term corporate transfer employees is

relatively unrestricted across all countries, but time limits are imposed more stringently on the

movement of natural persons for temporary movement longer stays. While Morocco has had

no restrictions on the Board of Director composition for many years now, restrictions have

only recently been eliminated in both Egypt and Jordan. Lebanon‟s Board of Director

restrictions remain high.

Working permits pose restrictions of varying levels across the four countries. Egypt is the

most restrictive, issuing work permits according to numerical limits determined by an

Economic Needs Test, as imposed by a decree in 2003. The number of foreigners allowed to

work in any one establishment is capped at 10% of total employees. In some industries (e.g.

tourism), foreigners are not allowed to work at all. Lebanon, Jordan, and Morocco have lower

restriction levels than Egypt, limiting work permits according to professional qualifications

and basic approval processes.

It seems that the least restrictive countries on mode 3 (Lebanon and Jordan) are the most

restrictive on mode 4. Opening on mode 3 facilitates the influx of foreign capital (mainly

from GCC countries), while closing on mode 4 protects white-collar workers and important

stakeholders in the banking system. Both Lebanon and Jordan impose particularly short

limitations on the time allowed in the temporary movement of long stay employees.

Lebanon‟s high mode 4 TRI score is also derived from the country‟s requirement that a

majority of the Board of Directors be Lebanese nationals (while Egypt, Jordan, and Morocco

have no restrictions in this area).

In conclusion, the banking sector‟s recent transformation in the MENA region has had a large

impact on many countries‟ regulatory frameworks, particularly with regard to the

involvement of private and foreign capital.

The main reforms that introduced or amended the banking law in the four countries of interest

(1993 and 2001 in Lebanon; 2000 in Jordan; 2003 in Egypt and 2006 in Morocco) have lifted

the foreign equity limits on the ownership of banks. This has prompted an increase of foreign

participation, namely in Lebanon, Morocco and Jordan. In Egypt, despite the regulatory

reform, most of the largest banks are currently publicly owned, which demands a

privatization (as in the case of the Bank of Alexandria), or at least a partial opening to private

capital needs to accompany the regulatory reform. In Morocco the liberalization process has

also been cautious since the Moroccan authorities control foreign participation in their largest

banks. They also constrain the operations of foreign banks by the amount of capital allocated

to their business in Morocco.

III.1.3 Telecom

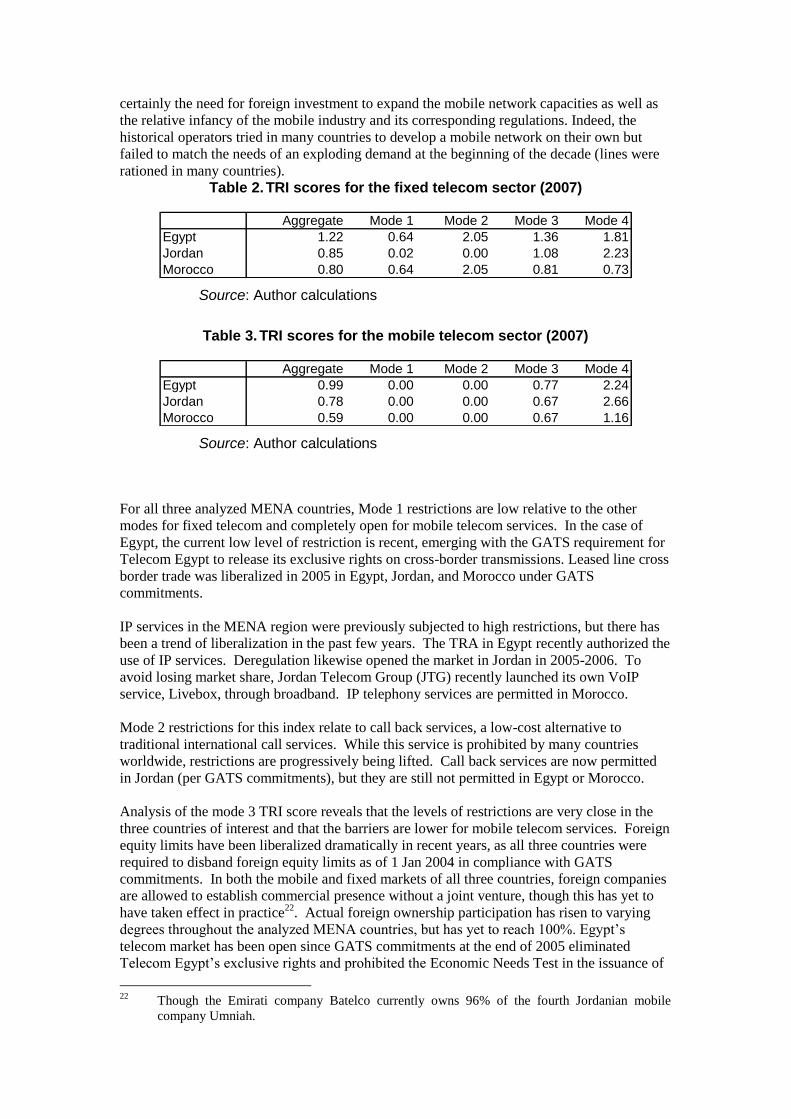

Dihel & Shepherd (2007) noted that Middle East countries ranked among the most restrictive

for trade in fixed telecom services (relative to Asian and Transition economies). For Egypt,

Jordan and Morocco, however, aggregate scores have declined since the former study. As

Table 3 shows, the aggregate TRI scores for fixed telecom range from 0.80 in Morocco to

1.22 in Egypt. The mobile sector is more open than fixed telephony in all three countries,

ranging from 0.59 in Morocco to 0.99 in Egypt (Table 4). The main reason behind this is

certainly the need for foreign investment to expand the mobile network capacities as well as

the relative infancy of the mobile industry and its corresponding regulations. Indeed, the

historical operators tried in many countries to develop a mobile network on their own but

failed to match the needs of an exploding demand at the beginning of the decade (lines were

rationed in many countries).

Table 2. TRI scores for the fixed telecom sector (2007)

Aggregate Mode 1 Mode 2 Mode 3 Mode 4

Egypt 1.22 0.64 2.05 1.36 1.81

Jordan 0.85 0.02 0.00 1.08 2.23

Morocco 0.80 0.64 2.05 0.81 0.73

Source: Author calculations

Table 3. TRI scores for the mobile telecom sector (2007)

Aggregate Mode 1 Mode 2 Mode 3 Mode 4

Egypt 0.99 0.00 0.00 0.77 2.24

Jordan 0.78 0.00 0.00 0.67 2.66

Morocco 0.59 0.00 0.00 0.67 1.16

Source: Author calculations

For all three analyzed MENA countries, Mode 1 restrictions are low relative to the other

modes for fixed telecom and completely open for mobile telecom services. In the case of

Egypt, the current low level of restriction is recent, emerging with the GATS requirement for

Telecom Egypt to release its exclusive rights on cross-border transmissions. Leased line cross

border trade was liberalized in 2005 in Egypt, Jordan, and Morocco under GATS

commitments.

IP services in the MENA region were previously subjected to high restrictions, but there has

been a trend of liberalization in the past few years. The TRA in Egypt recently authorized the

use of IP services. Deregulation likewise opened the market in Jordan in 2005-2006. To

avoid losing market share, Jordan Telecom Group (JTG) recently launched its own VoIP

service, Livebox, through broadband. IP telephony services are permitted in Morocco.

Mode 2 restrictions for this index relate to call back services, a low-cost alternative to

traditional international call services. While this service is prohibited by many countries

worldwide, restrictions are progressively being lifted. Call back services are now permitted

in Jordan (per GATS commitments), but they are still not permitted in Egypt or Morocco.

Analysis of the mode 3 TRI score reveals that the levels of restrictions are very close in the

three countries of interest and that the barriers are lower for mobile telecom services. Foreign

equity limits have been liberalized dramatically in recent years, as all three countries were

required to disband foreign equity limits as of 1 Jan 2004 in compliance with GATS

commitments. In both the mobile and fixed markets of all three countries, foreign companies

are allowed to establish commercial presence without a joint venture, though this has yet to

have taken effect in practice22

. Actual foreign ownership participation has risen to varying

degrees throughout the analyzed MENA countries, but has yet to reach 100%. Egypt‟s

telecom market has been open since GATS commitments at the end of 2005 eliminated

Telecom Egypt‟s exclusive rights and prohibited the Economic Needs Test in the issuance of

22

Though the Emirati company Batelco currently owns 96% of the fourth Jordanian mobile

company Umniah.

licenses. International services and leased-line services have sold a minority share, but local

and long-distance services remain 100% owned by Egypt Telecom. Potential market entrants

have been discouraged by market saturation and the high set-up costs of establishing a new

network. Egypt Telecom has refused to lease its network to new market entrants, as has been

done by the incumbent in Morocco since 2007, thus overcoming this obstacle and facilitating

consumer choice. Egypt‟s mobile telecom market has been liberalized more quickly than

fixed telecom and currently has foreign ownership in all three mobile operators.

Jordan‟s formerly government-owned incumbent in fixed line services was privatized in

2000, to be followed by a declaration of market openness in 2005 in compliance with GATS

commitments. The Jordanian mobile market is much more open as four firms operate in this

sector (relative to two or three mobile companies in the other countries despite much larger

populations), the three largest of which are foreign majority-owned (Zain, Orange Jordan,

Umniah). The internet sector also appears very competitive with currently 12 service

providers.

Foreign ownership is permitted in Morocco, and was first introduced by the incumbent Maroc

Telecom who sold 35 percent to Vivendi Universal of France in 2001 (further shares were

later sold in 2004). A second and third fixed telecom licenses were issued (to Meditel and

Maroc Connect) in 2005, further widening the market. Morocco‟s mobile telecom sector first

opened to competition in 1999 with the issuance of a license to Meditel. A further succession

of licenses was released in 2004. Morocco currently has three operators competing in each

segment, i.e. fixed, mobile, and internet.

The Moroccan Government and telecom regulator (ANRT) restrict the entry of new firms in

both the fixed and mobile telecom markets, as exclusive rights are believed necessary to

attract strategic investment, as well as in order to allow the provision of universal service in

fixed telecom services. In this regard the second mobile operator was offered exclusive rights

for a four-year period, as well as a direct international access from 1st Jan 2002. Here marks a

difference with Jordan where licenses do not grant exclusivity periods.

Varying levels of restrictiveness affect license regulation in the analyzed MENA countries.

Egyptian fixed and mobile licenses are issued according to the discretionary decision of the

licensing authority. Selections were made according to economic needs until the end of 2005,

but this measure was lifted by GATS commitments. Jordanian fixed licenses are issued with

basic entry requirements, and mobile licenses are awarded by competitive tender. Moroccan

fixed and mobile licenses are issued by competitive tender, but are issued individually for

specific services as opposed to general licenses covering all telecom services (as in the EU).

Mode 4 restrictions are similar to those in the other services sectors. Jordan records the

highest restriction levels in Mode 4, while Morocco is the most liberal23

.

In conclusion, the main issues for the telecom sectors in the MENA region are how to

improve the quality and coverage of the telecom service while lowering prices. Indeed the

quality and price of telecom services are an important determinant of the attractiveness of

backbone services in the region but also of the countries competitiveness.

Competition across the MENA countries is greater in the mobile sector than the fixed sector,

which has only opened recently. Foreign capital has risen dramatically during the current

decade due to the MENA telecom market‟s growing potential. New firms (joint-ventures

between foreign and domestic capital) have in some cases been offered periods of exclusivity.

23

See discussion in the previous section on the banking sector for more information.

Despite the lifting the monopoly of the Public Telecommunication Operators (PTOs) on the

fixed sector, high barriers to entry remain. This market would be more competitive if the

PTOs would lease their networks to competitors as has been the case in Morocco. IP

telephony development can also have a dramatic impact on telecom prices. But the studied

countries are still reluctant to promote commercial use of this technology on a higher scale.

III.3 The impact of TRI on economic performance.

III.3.1 Banking

In the first stage, firm level estimations24

(Table 1 –left side- in Appendix 1) show that the

capital ratio and the liquidity ratio are positive and significant. This is the expected sign, as

these two ratios are prudential factors that ensure the solvency of banks. The non-interest

expenses ratio is also positive and significant, which could mean that banks charge a higher

interest margin to compensate for higher non-interest costs. These results are coherent with

the wide empirical evidence on net interest margin determinants (Kunt and Huizinga, 1998).

The market share is not significant. The estimations are robust to the introduction of dummies

for MENA and developing countries.

Moving to the second stage of the analysis25

, where we regress country level variables on the

estimated „pure spread‟, our results suggest that the main variable of interest, the aggregate

TRI, is positive and significant (Table 1 -right side- in Appendix 1). In particular a 1%

increase in the aggregate TRI would induce a 0.1% increase in the „pure spread‟ in MENA

countries, on average and ceteris paribus 26

. Hence, a higher TRI would lead to a higher pure

spread and consequently an increase in the rent effect, which dominates the cost-inefficiency

effect. This result is robust to the inclusion of different controls and is confirmed by the one-

stage regressions (see Table 1 in Appendix 2). Removing restrictions in the banking sector

would favor income redistribution from banks to customers.

The analysis at the modal level (regression mode by mode, Table 2 in Appendix 1) reveals

that mode 3 is positive and highly significant27

. In particular, a 1% increase in mode 3 would

induce a 0.25% increase in the „pure‟ spread, on average and ceteris paribus 28

. The impact of

a change in mode 3 is more effective then a general change in the aggregate TRI. This

suggests that restrictions to commercial presence are rent-creating. However, it is possible

that some restrictions composing mode 3 could be cost-creating while others could be rent-

24

When the variables are significant, the null hypothesis of coefficients non-different from zero is

rejected at the 1% level. However, given the presence of non-normally distributed residuals, their

significance could actually be lower. The same holds for the estimation of country dummies, which are

used as dependent variables in the second stage of the analysis, but there is no reason to expect

insignificant coefficients. The R-square is around 0.8 meaning that the regression explains 80% of the

estimated model.

25

The R-squared at the second level of the analysis are generally lower (below 20%) but the regression

specification tests are largely satisfied since they fail to reject the null hypothesis at the 10% level.

26

The increase in developing and developed countries would be of 0.14% and 0.04%, respectively. It is

important to highlight that a percentage increase of TRI is not easy to determine given the nature of the

index.

27

Not surprisingly, the aggregate TRI and the variable that presents the higher weight in its

computation present the same sign and same significance level.

28

The increase in developing and developed countries would be of 0.51% and 0.4%, respectively.

creating, since what we observe is the net effect. It would thus be interesting to regress

individual index modal components on the performance indicator to disentangle the different

effects. Finally mode 4 is negative but not robust and modes 1 and 2 are not significant. This

is not surprising given the low importance of these modes in the banking sector29

. If we put

the four modal TRIs together in the regression we obtain the same results except that mode 4

turns to be strongly significant30

. The possible interaction between modes is carefully studied

by adding the interacted mode to the last specification (results not reported). The results

suggest that restrictions to cross-border supply (mode 1) and FDI (mode 3) are

complementary: if both are high, they would cause cost inefficiency. Indeed, if MNE

established in a country cannot supply their service abroad, it could reduce the scope of

economies of scale and increase costs. Finally, although the interaction between mode 3 and

mode 4 is not statistically significant, if we include it in the specification mode 3 loses its rent

creating effect. It could suggest that the presence of MNEs has a rent creating effect only if

employee movement is not restricted and hence if MNEs can hire national employees. In the

banking sector, staff plays a key role and it is important to hire competent persons or at least

to provide proper training.

With regards to other control variables, they are almost stable across different models. First of

all, among the prudential regulation variables, the only significant one is the „compulsory

deposit insurance‟ (eight_one), which has a negative impact on the pure spread. This is

understandable since countries that are subject to this requirement face lower risk and hence

lower interest spreads. The net interest variation presents the expected positive sign31

but is

not significant. A possible explanation for this result is that our sample included countries that

were hit by financial crises during the period of analysis (in particular Argentina and

Uruguay) and consequently report very high interest variation. Excluding these countries

from the sample, the interest variation turns to be significant. Countries recently hurt by

financial crises deserve special attention. Indeed, these countries simultaneously present

lower net interest margins (the financial crisis dummy is negative and significant) and

aggregate TRI above the sample mean. As a result aggregate TRI in these countries is not

significant (TRI_aggFinancialCrisis). These results could suggest that the financial crisis has

induced a strengthening of the banking regulation, which had a positive impact on banking

sector performance32

.

III.3.2 Fixed telecom

The first stage regression for telecom (Table 3 in Appendix 1, left side)33

suggests that capital

intensity and market share have a positive impact on EBITDA, which conforms to the theory.

29

Moreover, these two modes turn to be significant in the one-stage approach. So, evidence of their

influence on the pure spread is not clear and requires further analysis.

30

Statistical test supports the adoption of this specification where all the modes are introduced at the

same time.

31

The literature suggests that a higher interest variation induces a higher net interest margin to

compensate for higher risk.

32

Evidence on the improvement in the financial sector indicators are provided by the World Bank

(2007) with regards to the sharp decrease in the share of non-performing loans and, more generally, by

Turner (2007).

33

As we already highlighted for the banking sectors, the first stage regressions in the fixed telecom

sector are also characterized by high R-squared (the model estimation explains around 80% of

dependent variable variation) and non-linear residuals. The second stage regressions are very strong:

the R-squared is around 60% and the diagnostic test usually does not reject the null hypothesis.

On the other side, net sales have a negligible impact (also when transformed in elasticity) and

sales growth is not significant. Once again these results are robust to the inclusion of MENA

and developing dummies.

Moving to the second stage of the analysis, the impact of the aggregate TRI on „country level

EBITDA‟ is positive and significant (Table 3 in Appendix 11, right side). In particular, a 1%

increase in the aggregate TRI induces a 0.33% increase in the „country level EBITDA‟, on

average and ceteris paribus 34

. The estimation results are robust to different specifications and

are corroborated by the results in the one-stage approach (Table 2 in Appendix 2). We can

infer that restrictions in the fixed telephony sector TRI have mainly a rent-creating effect. At

the modal level, TRI_M3 is positive and significant. In particular, a 1% increase in the TRI

mode 3 induces a 0.34% increase in the „country level EBITDA‟, on average and ceteris

paribus35

. Once again, it mirrors the sign and significance of the aggregate TRI. TRI_M1,

TRI_M2 and TRI_M4 are not significant36

(Table 4 and 5 in Appendix 1). Moreover, any of

the interaction modes turns to be significant. Hence, in the fixed and the mobile telecom

sector, a policy focused only on mode 3 restrictions would have a greater impact than in the

banking sector.

If we observe the other control variables, prudential regulation in fixed telecom has a positive

effect on EBITDA. The rate of fixed lines over population has a negative impact on EBITDA,

which can be explained by lower opportunities to increase the size of the domestic market in

countries where this rate is high (i.e. mature sectors). Finally, while the mobile subscribers

digital share is not significant, the share of mobile subscribers over the population has a

positive coefficient. This could seem counterintuitive given the expected substitution between

fixed and mobile services. A possible explanation could be that many companies that offer

fixed telecom services also entered into the mobile telecom business, and the increase in the

number of subscribers had a positive impact on their profits.

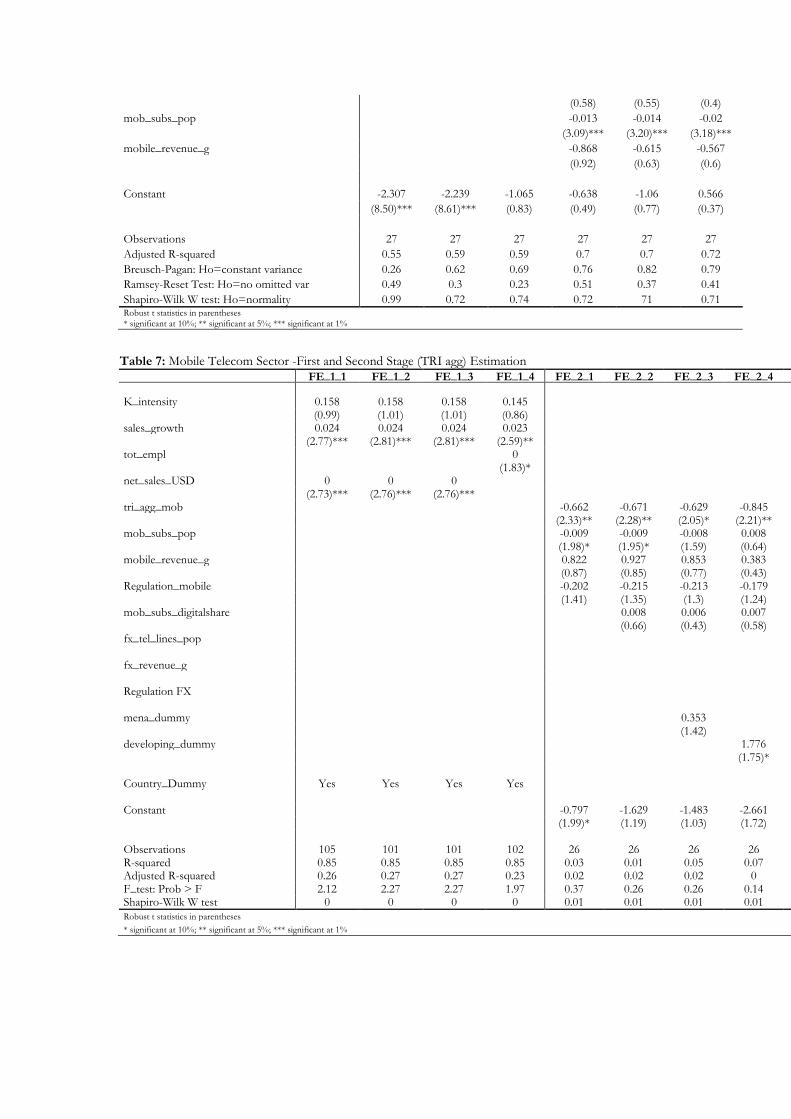

III.3.3 Mobile telecom

Looking at the first stage regression results (Table 7 in Appendix 1, left side)37

we notice that

capital intensity is not significant, while sales growth has a positive and significant effect on

EBITDA. These results shed light on the structural difference between the mobile and the

fixed telecom sectors. Unlike the latter, the mobile sector is younger and more dynamic,

mainly in terms of sales growth in developing countries, and it requires lower capital intensity

(in terms of tangible fixed assets)38

.

Moving to the second stage regression, Table 7 in Appendix 1 (right side) shows that the

aggregate TRI has a negative and significant effect on EBITDA in the mobile telephony,

34

The increase in developing and developed countries would be of 0.30% and 0.06%, respectively.

35

The increase in developing and developed countries would be of 0.28% and 0.07%, respectively.

36

Also in this case the statistical test supports the adoption of the specification where all the modes are

introduced at the same time.

37

Regression results for the mobile sector are less sound than for other sectors. Indeed, while the other

sector is high in the first stage and the residuals are non-normally distributed; in the second stage the R

squared are very low and the null hypothesis of the diagnostic test are not rejected. The one stage

approach presents a discrete R squared (48%, closed to the fixed telecom one).

38

For example mobile companies can rent the signal towers which can be shared by different

companies.

suggesting a cost-creating effect. In particular, a 1% increase in the aggregate TRI induces a

0.59% increase in the „country level EBITDA‟, on average and ceteris paribus 39

. At the

modal level (Table 8 in Appendix 1), TRI_M1, TRI_M2 and TRI_M4 are not significant40

,

while TRI_M3 is negative and significant. In particular, a 1% increase in the TRI mode 3

induces a 0.50% increase in the „country level EBITDA‟, on average and ceteris paribus41

.

Also in this case, as already emphasized for the fixed telecom sector, aggregate TRI and

mode 3 would have a similar impact on the sector performance. Interaction modes are not

significant. These results show that the policy implications of liberalizing mobile and fixed

telephony markets will not be the same. The gains in terms of mobile liberalization should be

higher because it should induce a reduction in production costs and the removal of market

inefficiencies.

However, one can wonder why barriers to fixed telephony liberalization are more rent-

creating while restrictions on mobile telephony are more cost-increasing. This result observed

for the aggregate TRI is echoed by the mode 3 coefficient. The main difference could thus

come from the different implications of foreign investments in the two sectors. Indeed, while

a significant part of the fixed network is already there, the cellular network is still in progress,

especially in developing countries. Thus, increased foreign participation in the fixed

telephony would mainly have an impact on the rent distribution, while an increase in

investment in mobile telephony could reduce costs by expanding the network (i.e. increasing

the number of subscriber permits to reduce fixed costs per subscriber).

Concerning interactions between modes, we observe that mode 2 turns to be non significant

when the four modes are included simultaneously in the regression. However, the sign of

mode 3, which is by far the main vector of trade in mobile telephony, remains negative and

strongly significant. This would indicate that mode 3 is not influenced by modal interaction in

the mobile sector (while the opposite result was found for fixed telephony).

III.4 Tax equivalents

Analysis of the tax equivalents results provides two main insights. First, our results are higher

than those obtained in previous studies (e.g. Dihel and Shepherd, 2007), an expected result

given of our reliance on developing countries‟ firm data in the sample. Indeed, the impact of

TRI on economic performance is usually higher in developing countries than in developed

countries.

Second, in table 4 we note that tax equivalents are higher in the mobile sector than in the

fixed sector, despite higher restrictions in the fixed sector in the three studied countries. This

is due to the fact that the impact of restrictions is higher in mobile telephony. Indeed, tax

equivalents result from the combination of a level of restrictions and an impact of these

restrictions on the price-cost margin.

Table 4: Tax equivalents of restrictions in banking, fixed and mobile telecom

39

The increase in developing and developed countries would be of 0.58% and 0.11%, respectively.

40

However, they are positive and significant in the one-stage approach (Table in Appendix 2). We can

thus not draw any strong conclusions on the significance of these variables. However, given their

limited impact on the mobile sector, this result is not too worrying.

41

The increase in developing and developed countries would be of 0.50% and 0.08%, respectively.

in four MENA countries (in %)

Banking Fixed Telecom Mobile telecom

Val Min Max Val Min Max Val Min Max

Egypt

AGG 35 21 50 54 33 79 101 9 271

M1 28 17 40 15 1 30 0 0 0

M2 5 3 8 2 0 47 0 0 0

M3 136 96 184 67 40 98 51 5 118

M4 63 44 84 68 5 169 356 267 466

Jordan

AGG 15 10 22 35 22 50 73 7 181

M1 20 12 28 0 0 1 0 0 0

M2 5 3 8 0 0 0 0 0 0

M3 20 15 25 50 31 72 43 4 97

M4 129 86 183 89 6 239 506 368 684

Morocco

AGG 50 30 74 33 21 46 52 5 118

M1 39 23 56 15 1 30 0 0 0

M2 853 187 3063 2 0 47 0 0 0

M3 32 25 41 35 22 50 43 4 97

M4 9 12 7 23 2 49 119 96 145

Lebanon

AGG 7 5 10

M1 0 0 0

M2 5 2 8

M3 3 2 4

M4 241 150 365

IV Conclusions

Our study aimed to assess the restrictiveness of barriers to trade in banking and telecom

services in the MENA region. Focusing on a select group of MENA countries, the analysis

goes beyond previous studies to consider the environment in which these restrictions have

evolved (e.g. regulatory framework, government behavior, etc.). Each index has been

computed at both the aggregate and modal levels to provide a more comprehensive picture of

current restrictions for policymakers involved in domestic reform and regional and

multilateral negotiations. The sectoral aggregate and modal trade restrictiveness indexes

developed have then been used as explanatory variables in firm level regressions to assess

their impact on economic performance.

One of the main contributions of this study is its collection of information not available from

secondary sources. The level of detail offered by this research strengthens the reliability of

our TRI results and helps us to better understand the interactions between regulatory reforms,

implementation and actual restrictiveness. De facto/ de jure gaps revealed in our analysis

supports the case for future detailed, regular assessments of service barriers in practice as well

as in the legislation.

Among the innovations in the empirical framework, we increase the dataset coverage by

adding firms from developing countries and we cover a more recent time period than previous

studies.

The first conclusion of this article is that there have been significant regulatory reforms over

the last decade in the selected service sectors of the four studied countries, but that a broad

range of restrictions still remain. The most significant change in these service sectors has

been the lifting or softening of constraints imposed on foreign equity participation. These

regulatory reforms, however, have had varying degrees of impact on market structure

depending on the countries and the sectors.

The second conclusion is that service restrictions have an impact on economic performance in

the three studied sectors. While a rent-creating effect seems to dominate restrictions on

banking and fixed telecom sectors, a cost-inefficiency effect seems to dominate the mobile

telecom sector. This means that liberalizing mobile sector telephony would induce potentially

higher gains than liberalizing the two other sectors. But this conclusion could be modified if

we think in terms of input-output analysis. Indeed, fixed telephony for example is the main

input of internet providers and is an important input of many back-bone services. Thus, a

reduction of fixed telephony prices is not simply a matter of rent redistribution, but also a

matter of technical development and of competitiveness.

At the modal level, mode 3 seems to be the most critical feature in all the sectors. Liberalizing

mode 3, by relaxing limitations on commercial presence, would have the greatest impact on

firms‟ performance and on income redistribution. However, in the banking sector, mode 4

also matters. Studying the possible interactions between modes is also particularly significant

for policy makers. Indeed, the impact of reforming regulations concerning one of the four

modes will be different depending on the regulations dealing with the other modes interacting

with the former. Our results suggest that mode 3 and mode 1 are complementary in the

banking sector: if an MNE establishes an affiliate in a country and it cannot supply their

services abroad, this restriction could reduce the scope of economies of scale and increase

costs. Finally, we found some evidence of a substitution effect between mode 3 and mode 4.

Indeed, if we include the interaction between these two modes, the former turns to be non

significant. This could suggest that the presence of MNEs has a rent creating effect only if

employee movement is not restricted and hence if MNEs can hire national employees. For the

telecom and mobile sector we don‟t find any evidence of an interaction between modes.

Hence, in the fixed and the mobile telecom sector, a policy focused only on mode 3

restrictions would have a greater impact than in the banking sector.

With regards to the technical issues, future work could improve the analysis by further

exploiting the time dimension. In particular, we would apply a random effect estimator on a

firm level panel, which would allow us to estimate time-invariant firm features, such as the

TRI. Moreover, the tax equivalent estimations would be more accurate if we could rely only

on developing country data and if we could use price data instead of firm performance data as

dependent variables. However, data availability is a major constraint for such improvements.

As a next step, an assessment of the impact of the different reforms implemented by the

analyzed countries would be useful. However, such an evaluation is not an easy task given the

multiplicity of direct and indirect effects. Ex ante and ex post qualitative and quantitative

assessments must be conducted at the sectoral level but also at the economy-wide level to

capture the interaction between the various sectoral reforms.

Annex 1: Two-Stage Estimation Table 1: Banking Sector -First and Second Stage (TRI agg) Estimation

FE_1

_1 FE_1

_2 FE_1

_3 FE_2

_1 FE_2

_2 FE_2

_3 FE_2

_4 FE_2

_5 FE_2

_6 FE_2

_7 FE_2

_8

ln_K_RATIO 0.203 0.203 0.206

(6.34)***

(5.18)***

(6.00)***

ln_LIQ_RATIO 0.06 0.06 0.06

(3.47)***

(3.66)***

(4.22)***

ln_NIERAT 0.289 0.289 0.292

(9.61)***

(8.83)***

(9.52)***

MENA_dummy -2.381

(1.83)

* ln_mkt_share 0.003 (0.41) TRI_agg 0.225 0.241 0.278 0.285 0.248 0.187 0.266 0.259

(2.03)

** (1.98)

* (2.00)

* (1.95)

* (1.89)

* (1.93)

* (1.85)

* (1.96)

* C5 0.437 0.448 0.474 0.285 0.45 0.432 0.475 0.503 (1.28) (1.28) (1.32) (1.12) (1.28) (1.27) (1.32) (1.27) eight_ten -0.389 -0.401 -0.413 -0.341 -0.397 -0.398 -0.42 -0.382

(2.52)

** (2.53)

** (2.50)

** (2.33)

** (2.49)

** (2.49)

** (2.38)

** (2.35)

** int_var 0.001 0.002 0.001 0 0.001 0.001 0.001

(1.19) (1.55) (1.22) (0.19) (0.99)

(1.21) (1.24)

Financris_dummy -0.371 -0.453 -0.637 -0.564 -0.312 -

0.486 -0.483

(2.79)***

(2.41)**

(2.68)**

(2.28)** (1.63)

(2.39)**

(2.34)**

TRI_agg Financial Crisis -0.21

(2.32)

** seven_one -0.198 (1.53)

three_one -

6.047 (0.72) nine_one -0.113 (0.68) Country Dummy Yes Yes Yes No No No No No No No No

Constant -1.855 -1.868 -1.925 -1.774 -1.874 -1.738 -

1.347 -1.843

(6.47)***

(6.32)***

(6.09)***

(8.53)***

(6.30)***

(6.63)***

(2.33)**

(6.78)***

Observations 923 923 923 46 46 46 46 46 46 46 46 Adjusted R-squared 0.77 0.77 0.77 0.11 0.09 0.09 0.22 0.08 0.11 0.11 0.08 Breusch-Pagan: Ho=constant variance 0.25 0.25 0.21 0.04 0.02 0.01 0 0.02 0 0 0.01 Ramsey-Reset Test: Ho=no omit. Var 0.09 0.11 0.12 0.13 0.18 0.15 0 0.11 0.29 0 0.16 Shapiro-Wilk W test: Ho=normality 0 0 0 0 0 0 0 0 0 0 0 Absolute value of t statistics in parentheses

* significant at 10%; ** significant at 5%; *** significant at 1%

Table 2: Banking Sector - Second Stage (modal TRI) Estimation

FE_2_1

FE_2_2

FE_2_3

FE_2_4

FE_2_5

FE_2_6

FE_2_7

FE_2_8

FE_2_9

FE_2_10

FE_2_11

FE_2_12

FE_2_13

FE_2_14

FE_2_15

tri_m1

0.123

0.122

0.138

0.07

7 0.06

9 0.12

(1.41)

(1.39)

(1.16)

(0.92

) (0.76

) (1.17

)

tri_m2

0.049

0.052

0.043

-

0.032

-0.02

3

-0.10

3

(0.89)

(0.91)

(0.52)

(0.5) (0.32

) (1.35

)

tri_m3

1.006

1.038

0.984

0.96

8 0.97

8 0.97

5

(1.92)*

(1.94)*

(1.78)*

(2.18)**

(2.16)**

(2.22)**

tri_m4

-0.21

4

-0.21

5

-0.25

1

-0.19

5

-0.19

3

-0.22

4

-1.63 -1.6

(1.92)*

(2.08)**

(2.06)**

(2.54)**

C5

0.414

0.416

-0.41

5

0.382

0.386