Embed Size (px)

Citation preview

3/23/20043/23/2004 11

An Examination of Private Oil Company An Examination of Private Oil Company GrowthGrowth

Rob ArnottRob ArnottOIES Internal SeminarOIES Internal Seminar

2525thth November 2003November 2003

3/23/20043/23/2004 22

Private oil company growthPrivate oil company growth

Overview of global industry trendsOverview of global industry trends–– Regional costs and capital migrationRegional costs and capital migration

Industry costs and implicationsIndustry costs and implications–– Why is further consolidation likely?Why is further consolidation likely?

Company specific growthCompany specific growth–– Where will growth come from?Where will growth come from?

ConclusionsConclusions–– How much more risk are companies taking on?How much more risk are companies taking on?

3/23/20043/23/2004 33

Capital growth is key to equity investorsCapital growth is key to equity investors

Source: LSE, NYSE

3/23/20043/23/2004 44

Reserve growth influences share priceReserve growth influences share price

Source: LSE, NYSE, Morgan Stanley

3/23/20043/23/2004 55

Replacement figures are deceptiveReplacement figures are deceptive

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

0% 50% 100% 150% 200% 250% 300%

Reserves Replacement %

Res

erve

s R

epla

cem

ent C

ost $

/boe

Africa/Middle East

Asia-Pacific

US

Canada

Europe

Latin America

Source: Company data, JS Herold

3/23/20043/23/2004 66

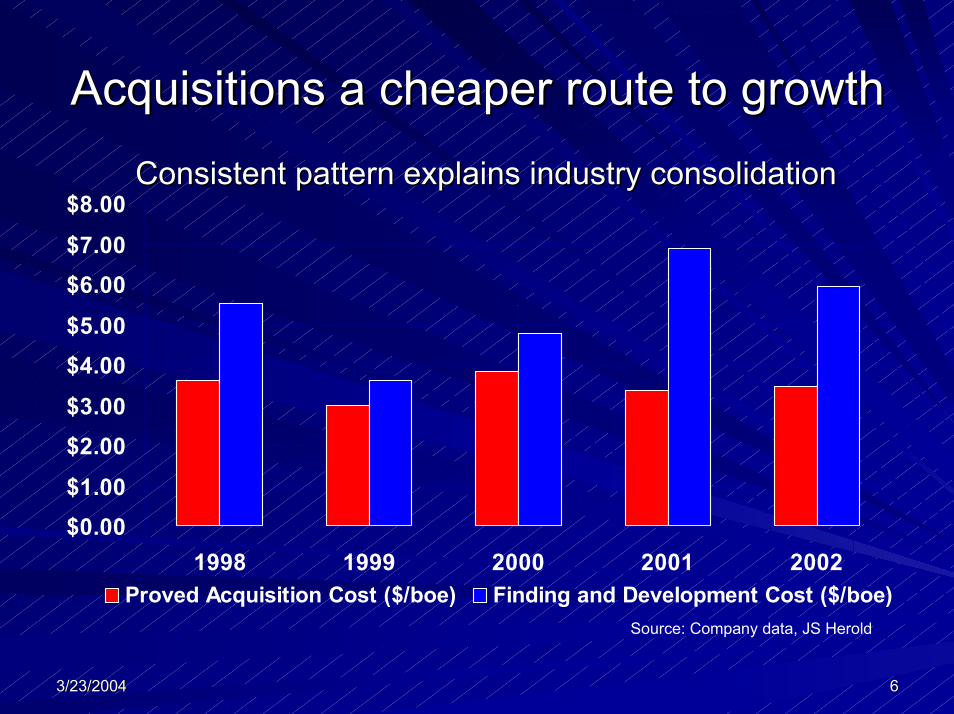

Acquisitions a cheaper route to growthAcquisitions a cheaper route to growth

$0.00$1.00

$2.00$3.00

$4.00$5.00

$6.00$7.00

$8.00

1998 1999 2000 2001 2002Proved Acquisition Cost ($/boe) Finding and Development Cost ($/boe)

Consistent pattern explains industry consolidationConsistent pattern explains industry consolidation

Source: Company data, JS Herold

3/23/20043/23/2004 77

US, Canada and Europe overheatedUS, Canada and Europe overheated

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

Europe LatinAmerica

Asia-Pacific Canada US Africa/MiddleEast

Proved Acquisition Cost ($/boe) Finding and Development Cost ($/boe)

Companies overpaying to achieve growthCompanies overpaying to achieve growth

Source: Company data, JS Herold

3/23/20043/23/2004 88

Migration of capital away from USMigration of capital away from US

-24%

-8%

47%

69%

40%

-40%

-20%

0%

20%

40%

60%

80%

US Canada Europe Africa/MiddleEast

Asia-Pacific

Spending changes 2000Spending changes 2000--20022002

Source: Company data, Harrison Lovegrove

3/23/20043/23/2004 99

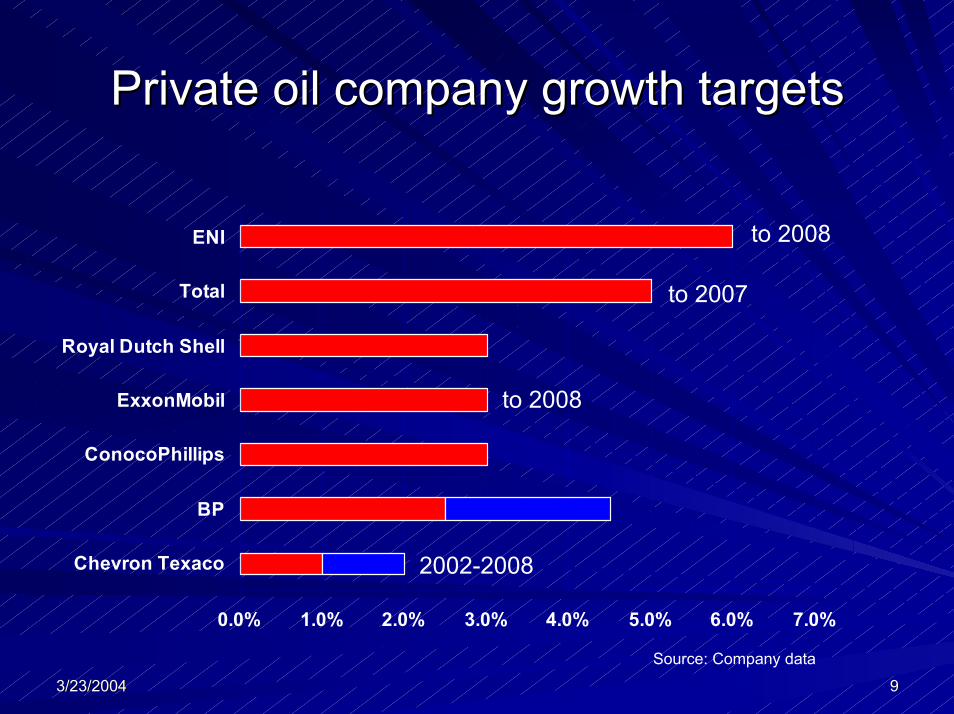

Private oil company growth targetsPrivate oil company growth targets

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0%

Chevron Texaco

BP

ConocoPhillips

ExxonMobil

Royal Dutch Shell

Total

ENI to 2008

to 2007

to 2008

2002-2008

Source: Company data

3/23/20043/23/2004 1010

The real cost of growthThe real cost of growth

-10

-5

0

5

10

15

20

$3.00 $5.00 $7.00 $9.00 $11.00 $13.00 $15.00Spending per boe produced

Ann

ual p

rodu

ctio

n gr

owth

(%)

Majors

E and P companies

Smaller companies chase growth at shareholders expenseSmaller companies chase growth at shareholders expense

Source: Company data, JS Herold

3/23/20043/23/2004 1111

Growth without acquisitions unrealisticGrowth without acquisitions unrealisticEven revised targets are unlikely to be achievedEven revised targets are unlikely to be achieved

02468

101214161820

80% 100% 120% 140% 160% 180%

3-Year F&D Replacement %

3-Ye

ar A

vg. F

&D

Cos

t $/b

oe

0% 3% 5%

Super-majorsInt.-Integrated

Int.-EP

Can.-EP Can.-Int

US.-Int

Small US.-EP

Super-EP Mid US.-EP

Large US.-EP

Source: Company data, JS Herold, OIES

3/23/20043/23/2004 1212

Decline versus growthDecline versus growth

More and more growth projects are needed to infill decline

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Chevron Texaco BP ConocoPhillips ExxonMobil Royal DutchShell

Total ENI

Ann

ual d

eclin

e ra

te (%

)

0.0%10.0%20.0%30.0%40.0%50.0%60.0%70.0%80.0%90.0%100.0%

% n

ew g

row

th u

sed

up

Annual decline 2002-2007 (%) % of new growth used infilling decline

Source: Company data, OIES

3/23/20043/23/2004 1313

BP’s oil production growth 2002BP’s oil production growth 2002--20072007

-400-200

0200400600800

100012001400

Europe NorthAmerica

Africa LatinAmerica

Asia-Pacific

MiddleEast

Russia Total

Prod

uctio

n m

boe/

d

Reliance on Russia a high risk strategy?Reliance on Russia a high risk strategy?

Source: Company data, OIES

3/23/20043/23/2004 1414

Shell’s oil production growth 2002Shell’s oil production growth 2002--20072007

-300

-200-100

0100

200

300400

500

Europe NorthAmerica

Africa LatinAmerica

Asia-Pacific

MiddleEast

Russia Total

Prod

uctio

n m

boe/

d

Growth reliant on Nigeria (Bonga, NLNG Growth reliant on Nigeria (Bonga, NLNG liquids)liquids)

Source: Company data, OIES

3/23/20043/23/2004 1515

Exxon’s oil production growth 2002Exxon’s oil production growth 2002--20072007

Growth from Bonga (Nigeria) + Kizomba/Dalia (Angola)Growth from Bonga (Nigeria) + Kizomba/Dalia (Angola)

-200

0

200

400

600

800

1000

1200

Europe NorthAmerica

Africa LatinAmerica

Asia-Pacific

MiddleEast

Other Total

Prod

uctio

n m

boe/

d

Source: Company data, OIES

3/23/20043/23/2004 1616

Total’s oil production growth 2002Total’s oil production growth 2002--20072007

-100-50

050

100150200250300350400450

Europe NorthAmerica

Africa LatinAmerica

Asia-Pacific

MiddleEast

Other Total

Prod

uctio

n m

boe/

d

Deepwater Africa the key (Nigeria: BongaMain, Congo: Deepwater Africa the key (Nigeria: BongaMain, Congo: Moho, Angola: Dalia)Moho, Angola: Dalia)

Source: Company data, OIES

3/23/20043/23/2004 1717

BP’s gas production growth 2002BP’s gas production growth 2002--20072007

-150

-100

-50

0

50

100

150

Europe NorthAmerica

Africa LatinAmerica

Asia-Pacific

MiddleEast

Russia Total

Prod

uctio

n m

boe/

d

A switch from Europe and North America to Egypt, Algeria A switch from Europe and North America to Egypt, Algeria and Trinidad LNGand Trinidad LNG

Source: Company data, OIES

3/23/20043/23/2004 1818

Shell’s gas production growth 2002Shell’s gas production growth 2002--20072007

-150

-100

-50

0

50

100

150

200

Europe NorthAmerica

Africa LatinAmerica

Asia-Pacific

MiddleEast

Russia Total

Prod

uctio

n m

boe/

d

NW shelf Australia and Nigeria LNG the driversNW shelf Australia and Nigeria LNG the drivers

Source: Company data, OIES

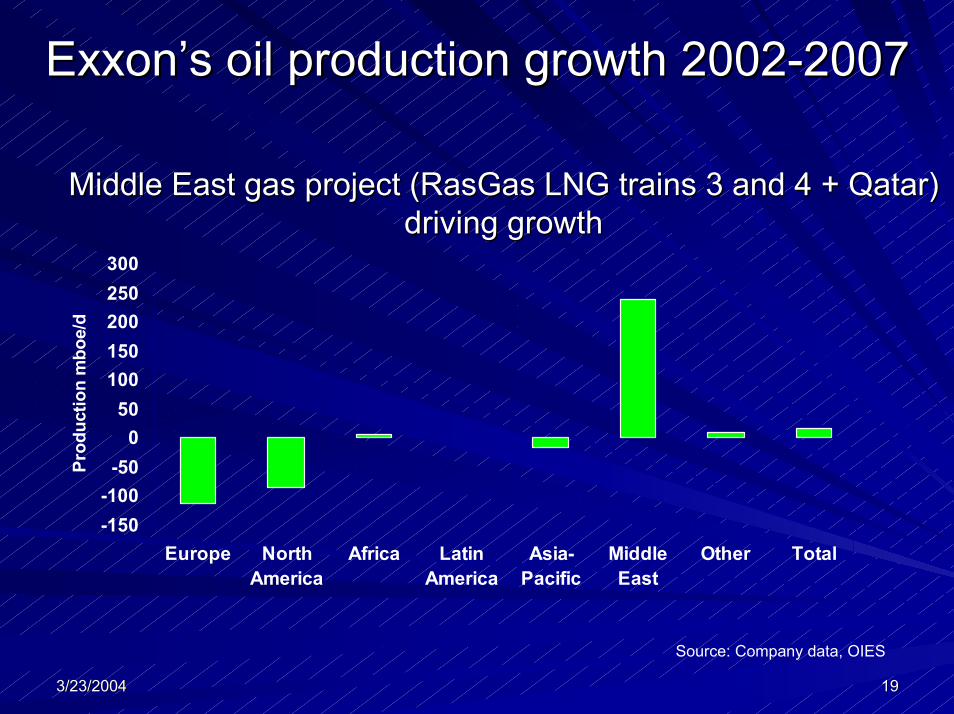

3/23/20043/23/2004 1919

Exxon’s oil production growth 2002Exxon’s oil production growth 2002--20072007

-150-100

-500

50100150200250300

Europe NorthAmerica

Africa LatinAmerica

Asia-Pacific

MiddleEast

Other Total

Prod

uctio

n m

boe/

d

Middle East gas project (Middle East gas project (RasGasRasGas LNG trains 3 and 4 + Qatar) LNG trains 3 and 4 + Qatar) driving growth driving growth

Source: Company data, OIES

3/23/20043/23/2004 2020

Total’s gas production Total’s gas production growthgrowth 20022002--20072007

-100

-500

50100

150

200250

300

Europe NorthAmerica

Africa LatinAmerica

Asia-Pacific

MiddleEast

Other Total

Prod

uctio

n m

boe/

d

A more even spread from Indonesia, Venezuela (Yucal), A more even spread from Indonesia, Venezuela (Yucal), Argentina (Carina/Aries), Argentina (Carina/Aries),

Source: Company data, OIES

3/23/20043/23/2004 2121

Oil is still driving production growthOil is still driving production growth

Targets will only be met if ‘oil’ developments proceed as planneTargets will only be met if ‘oil’ developments proceed as plannedd

-3.0%-2.0%-1.0%0.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%

BP ChevronTexaco

ConocoPhillips ENI ExxonMobil Royal DutchShell

Total

CA

GR

(%)

Oil Growth Gas GrowthSource: Company data, OIES

3/23/20043/23/2004 2222

Oil regaining share of production mixOil regaining share of production mix

Only in Total does gas increase proportionatelyOnly in Total does gas increase proportionately

0.0%5.0%

10.0%15.0%20.0%25.0%30.0%35.0%40.0%45.0%50.0%

BP Chevron Texaco ConocoPhillips ENI ExxonMobil Royal DutchShell

Total

% G

as

2002 2007Source: Company data, OIES

3/23/20043/23/2004 2323

OPEC exposure is increasingOPEC exposure is increasing

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

BP Chevron Texaco ConocoPhillips ENI ExxonMobil Royal DutchShell

Total

OPE

C O

il as

a p

erce

ntag

e of

tota

lpr

oduc

tion

2002 2007

3.6 million b/d out of 15.8 million b/d will come from OPEC 3.6 million b/d out of 15.8 million b/d will come from OPEC in 2007in 2007

220

628270

553

639719

581

Figure show oil production mb/d

Source: Company data, OIES

3/23/20043/23/2004 2424

The equity market expects growth but The equity market expects growth but delivery is at risk delivery is at risk

Source: Morgan Stanley

3/23/20043/23/2004 2525

More access on easier terms please!More access on easier terms please!Further consolidation inevitableFurther consolidation inevitable–– US, Canada and Europe are exUS, Canada and Europe are ex--growthgrowth–– Acquisition costs still below FD costsAcquisition costs still below FD costs

Oil continues to drive POC production growthOil continues to drive POC production growth–– Companies are not shifting to gas Companies are not shifting to gas –– Increasing differentiation between companiesIncreasing differentiation between companies

Capital flowing from low risk to high riskCapital flowing from low risk to high risk–– OPEC exposure increasingOPEC exposure increasing–– Technical and political risk increasingTechnical and political risk increasing

3/23/20043/23/2004 2626

An Examination of Private Oil Company An Examination of Private Oil Company GrowthGrowth

Rob ArnottRob ArnottOIES Internal SeminarOIES Internal Seminar

2525thth November 2003November 2003