Embed Size (px)

Citation preview

Learning Objectives:After reading this chapter you should be able to do the following:

1 Describe the regulatory requirements of the Companies Acts, IFRS 3 and IFRS 10 with regard to consolidated financial statements.

2 Explain the nature of goodwill on acquisition and describe the provisions of IFRS 3 concerning its accounting treatment.

3 Prepare consolidated statements of financial position, including the entries for goodwill and non-controlling interests using the proportionate share approach.

4 Prepare consolidated statements of financial position, including the entries for goodwill and non-controlling interests using the fair value approach.

5 Prepare consolidated statements of comprehensive income (consolidated statements of profit or loss), including the entries for non-controlling interests and simple examples of intragroup sales.

An introduction to consolidated financial statements

Chapter 34

34.1 Introduction When a company purchases shares in another company with the intention of holding the shares on a long-term basis they are shown as a non-current asset in the final financial statements of the company that owns the shares. Where the company owns a relatively large number of shares in another company; usually in excess of 50 per cent of the other company’s issued equity share capital, they are considered to be in control of the other company. The company that owns the shares is referred to as the parent (or holding) company. The company whose shares are owned is referred to as a subsidiary of the parent company. When this situation arises, these two companies are said to constitute a group. Thus, a group exists when a parent company has one or more subsidiaries. Where the parent company owns all the issued equity share capital of a subsidiary it is referred to as a wholly owned subsidiary. If the parent company owns more than 50 per cent but less than 100 per cent of the issued equity share capital of a subsidiary, it is referred to as a partially owned or partly owned subsidiary. The majority of large companies typically have to prepare consolidated financial statements. A real life example of how a group is formed or changes is now provided.

REAL WORLD EXAMPLE 34.1

Kwik Fit – requirement for group accounts

On 3 March 2011 Kwik Fit was taken over by the Japanese company Itochu. The takeover by Itochu is one of many takeovers that Kwik Fit has been involved in. The most notable of these occurred in 1999, when Ford Motor Company purchased Kwik Fit for £1 billion. Kwik Fit was then sold by Ford to the private equity group CVC after accounting irregularities were found regarding the understatement of liabilities in their accounts. CVC purchased Kwik Fit for £350 million. However, it then sold the company to the private equity firm PAI in 2005 for £800 million. Itochu purchased Kwik Fit in a deal worth £637 million (including £450 million of debt).

Source: Author.

Where a group exists, the law requires consolidated (also known as ‘group’) financial statements to be prepared. In simple terms, consolidated financial statements are a combination of the final financial statements of a parent company with those of its subsidiary (or subsidiaries). Thus, where a group exists, a separate set of financial statements must be prepared for the entities outlined in Figure 34.1

Figure 34.1

The parent company

One for each subsidiary

Consolidated financialstatements of the parent

company and its subsidiary(or subsidiaries)

Financialstatements

Group financial statement requirements

2 ChApter 34 An introduction to consolidated financial statements

The consolidated financial statements of the parent will be included in the annual report of the parent company, along with its own financial statements.

Learning Activity 34.1

Examine GlaxoSmithKline plc’s financial statements. Note how details are provided for both the group and the parent company separately.

http://www.gsk.com/reports-and-publications.html

34.2 Identifying business combinations Consolidated financial statements are governed by the Companies Act 2006 as well as IFRS 3 – Business combination (IASB, 2013a), IFRS 10 – Consolidated Financial Statements (IASB, 2013b), IFRS 12 Disclosure of Interests in Other Entities (IASB, 2013c).

When two or more separate entities come together to form one reporting entity this is known as a business combination (IFRS 3). In most instances one company gains control (the acquiring company). In these instances consolidated financial statements are required to be prepared. IFRS 3 defines a group as ‘a parent and all its subsidiaries’. In it a parent is defined as ‘an entity that has one, or more subsidiaries’ and a subsidiary is defined as ‘an entity, including an unincorporated entity such as a partnership: that is, controlled by another entity (the parent)’. In short, a group may include bodies other than limited companies. However, for simplicity, this chapter is confined to entities that are limited companies, and where there is only one subsidiary.

The rules relating to whether a group exists (and thus whether consolidated financial statements must be prepared) are rather complex, in order to avoid companies circumventing the law. They focus on what constitutes a subsidiary. In the introduction a subsidiary was defined in simple terms as being a company where more than 50 per cent of its issued equity share capital is owned by another company. To be more accurate, this refers to the company’s voting shares. Moreover, this is only meant to be indicative of the main criterion of what constitutes a parent–subsidiary relationship: namely where one entity exercises control over another entity.

Thus, according to IFRS 10 consolidation is required when a company (parent) has control over another entity (subsidiary). IFRS 10 defines control as requiring three elements:

a power;

b exposure to variable returns; and

c the investor’s ability to use power to affect its amount of variable returns.

Control is defined in IFRS 10 as

“An investor controls an investee when the investor is exposed, or has rights, to variable returns from its involvement with the investee and has the ability to affect those returns through its power over the investee.”The Companies Act and IFRS 3 require that parent entities provide financial information about the

economic activities of their groups by preparing consolidated financial statements. Preparing group financial statements involves a process of adjusting and combining financial information from the individual financial statements of a parent and its subsidiaries in order to prepare consolidated financial statements that present financial information for the whole group as a single economic entity.

334.2 Identifying business combinations

There is one final key term that needs to be explained at this point. As mentioned earlier, some subsidiaries may be only partially owned by a parent company. This means that a minority of its shares are owned by other organizations and/or individuals who also have a financial interest in the entity. These are thus referred to as ‘non-controlling interests’. Non-controlling interests are defined in IFRS 10 as ‘the equity in a subsidiary not attributable directly or indirectly, to a parent’ (discussed in more detail later). Non-controlling interests are also referred to as minority interests in the UK.

34.3 Goodwill on acquisition When one company buys another company (by purchasing its shares), the price paid is usually greater than the value of its net assets. The excess of the purchase price over the value of its net assets gives rise to what is referred to as ‘goodwill on acquisition’, or more accurately, purchased goodwill. This is defined in IFRS 3 as:

“An asset representing future economic benefits arising from assets acquired in a business combination that are not individually identified and separately recognised.”It is calculated, in simple terms, as the difference between the cost of an acquired entity and the aggregate

of the fair values of that entity’s identifiable assets, liabilities and contingent liabilities. Where there are non-controlling interests the value of the non-controlling interest also has to be assumed to form part of the overall value, hence is added to the cost to get the total goodwill figure for the whole company.

There are complex rules about what constitutes the ‘fair values’ of an acquired entity’s identifiable assets and liabilities. These are too advanced for an introductory textbook, and it is sufficient at this stage to point out that book values are not usually ‘fair values’. However, for the sake of simplicity, this chapter assumes that the book values are ‘fair values’.

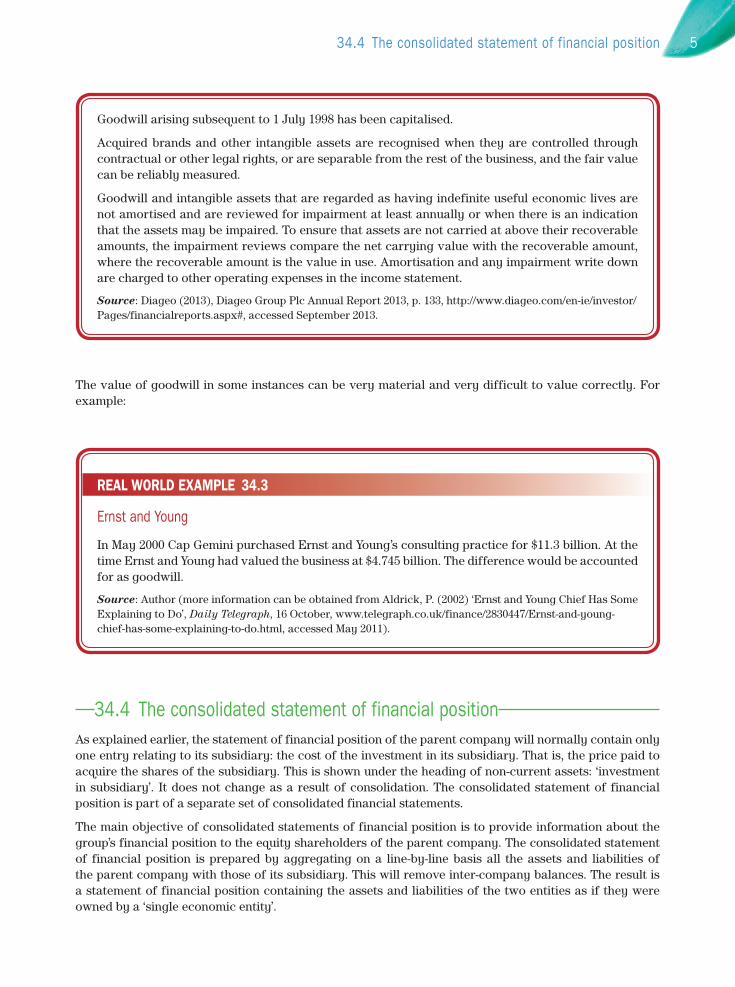

Goodwill was dealt with in detail in Chapter 26 on changes in partnerships. Students following a syllabus that does not include changes in partnerships, but does include goodwill, are advised to read the two sections entitled ‘the nature of goodwill’ and ‘the recognition of goodwill in financial statements’ at this point, if they have not already done so. The most relevant aspect of the latter is that IFRS 3 requires goodwill to be capitalized as an intangible asset and impaired to fair value when/if it diminishes in value (it cannot be revalued upwards). The recommended accounting treatment can be found in Diageo Group plc’s financial statements.

REAL WORLD EXAMPLE 34.2

Diageo Group plc

Accounting policies

(Note: This is just an extract. The accounting policy covers brands and other intangible assets but only the goodwill sections have been extracted.)

Brands, goodwill and other intangible assets

Goodwill represents the excess of the aggregate of the consideration transferred, the value of any non-controlling interests in the subsidiary acquired and the fair value of any previously held equity interest in the subsidiary acquired over the fair value of the identifiable net assets acquired.

4 ChApter 34 An introduction to consolidated financial statements

REAL WORLD EXAMPLE 34.3

ernst and Young

In May 2000 Cap Gemini purchased Ernst and Young’s consulting practice for $11.3 billion. At the time Ernst and Young had valued the business at $4.745 billion. The difference would be accounted for as goodwill.

Source: Author (more information can be obtained from Aldrick, P. (2002) ‘Ernst and Young Chief Has Some Explaining to Do’, Daily Telegraph, 16 October, www.telegraph.co.uk/finance/2830447/Ernst-and-young-chief-has-some-explaining-to-do.html, accessed May 2011).

Goodwill arising subsequent to 1 July 1998 has been capitalised.

Acquired brands and other intangible assets are recognised when they are controlled through contractual or other legal rights, or are separable from the rest of the business, and the fair value can be reliably measured.

Goodwill and intangible assets that are regarded as having indefinite useful economic lives are not amortised and are reviewed for impairment at least annually or when there is an indication that the assets may be impaired. To ensure that assets are not carried at above their recoverable amounts, the impairment reviews compare the net carrying value with the recoverable amount, where the recoverable amount is the value in use. Amortisation and any impairment write down are charged to other operating expenses in the income statement.

Source: Diageo (2013), Diageo Group Plc Annual Report 2013, p. 133, http://www.diageo.com/en-ie/investor/Pages/financialreports.aspx#, accessed September 2013.

The value of goodwill in some instances can be very material and very difficult to value correctly. For example:

34.4 the consolidated statement of financial positionAs explained earlier, the statement of financial position of the parent company will normally contain only one entry relating to its subsidiary: the cost of the investment in its subsidiary. That is, the price paid to acquire the shares of the subsidiary. This is shown under the heading of non-current assets: ‘investment in subsidiary’. It does not change as a result of consolidation. The consolidated statement of financial position is part of a separate set of consolidated financial statements.

The main objective of consolidated statements of financial position is to provide information about the group’s financial position to the equity shareholders of the parent company. The consolidated statement of financial position is prepared by aggregating on a line-by-line basis all the assets and liabilities of the parent company with those of its subsidiary. This will remove inter-company balances. The result is a statement of financial position containing the assets and liabilities of the two entities as if they were owned by a ‘single economic entity’.

534.4 the consolidated statement of financial position

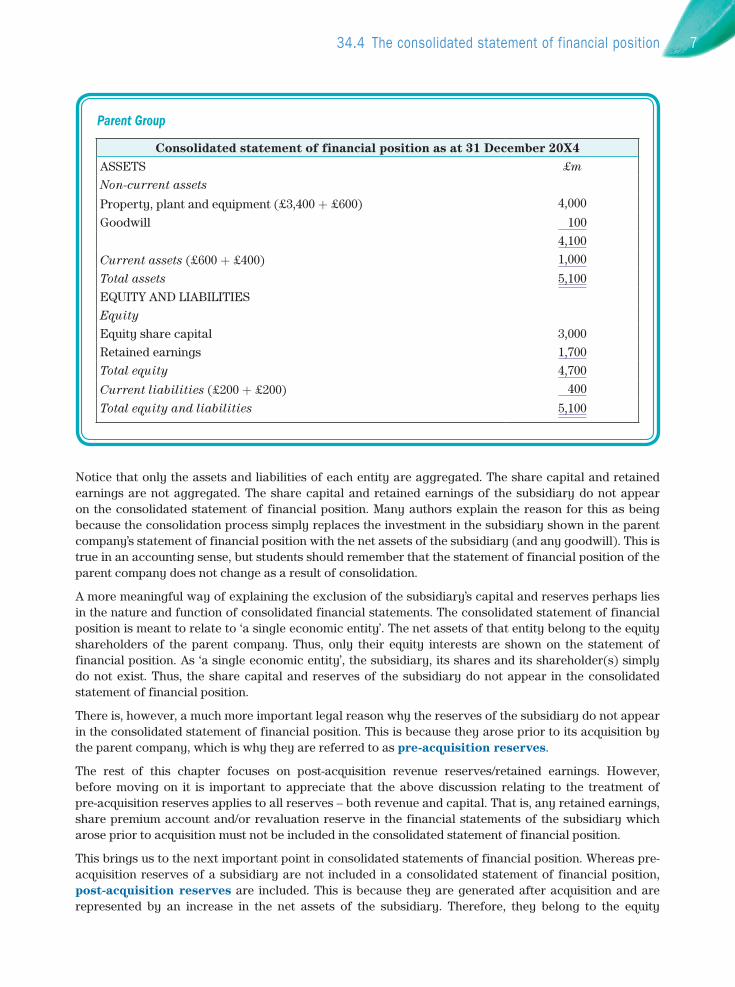

A working ledger account, the ‘cost of control account’ is usually established when preparing group financial statements. It is used to eliminate the ledger account balances that are not simply combined. The balance on this account is goodwill on acquisition. The cost of the investment in the subsidiary and the equity that is taken over at the date of the business combination are transferred to this account. A simple illustration is given in Worked Example 34.1.

WORKED EXAMPLE 34.1

The following are the statements of financial position of Parent plc and Subsidiary Ltd as at 31 December 20X4:

Parent plc Subsidiary LtdASSETS £’million £’millionNon-current assetsProperty, plant and equipment 3,400 600Investment in Subsidiary Ltd 900 –

4,300 600Current assets 600 400Total assets 4,900 1,000EQUITY AND LIABILITIESEquityEquity share capital 3,000 500Retained earnings 1,700 300Total equity 4,700 800Current liabilities 200 200Total equity and liabilities 4,900 1,000

Parent plc purchased all the equity shares of Subsidiary Ltd on 31 December 20X4. The assets and liabilities of Subsidiary Ltd are shown in its financial statements at what are agreed to be appropriate fair values.

Required

Prepare a consolidated statement of financial position as at 31 December 20X4.

Workings

Cost of control account20X4 Details £m 20X4 Details £m31 Dec Inv. in Subsidiary Ltd 900 31 Dec 100% Share capital 500

100% Retained earnings 300 Goodwill 100900 900

Purchased goodwill = the price paid less the net assets taken over = £900m - (£1,000m - £200m) = £100m.

6 ChApter 34 An introduction to consolidated financial statements

Parent Group

Consolidated statement of financial position as at 31 December 20X4ASSETS £mNon-current assets

Property, plant and equipment (£3,400 + £600) 4,000

Goodwill 1004,100

Current assets (£600 + £400) 1,000

Total assets 5,100EQUITY AND LIABILITIESEquityEquity share capital 3,000Retained earnings 1,700Total equity 4,700

Current liabilities (£200 + £200) 400

Total equity and liabilities 5,100

Notice that only the assets and liabilities of each entity are aggregated. The share capital and retained earnings are not aggregated. The share capital and retained earnings of the subsidiary do not appear on the consolidated statement of financial position. Many authors explain the reason for this as being because the consolidation process simply replaces the investment in the subsidiary shown in the parent company’s statement of financial position with the net assets of the subsidiary (and any goodwill). This is true in an accounting sense, but students should remember that the statement of financial position of the parent company does not change as a result of consolidation.

A more meaningful way of explaining the exclusion of the subsidiary’s capital and reserves perhaps lies in the nature and function of consolidated financial statements. The consolidated statement of financial position is meant to relate to ‘a single economic entity’. The net assets of that entity belong to the equity shareholders of the parent company. Thus, only their equity interests are shown on the statement of financial position. As ‘a single economic entity’, the subsidiary, its shares and its shareholder(s) simply do not exist. Thus, the share capital and reserves of the subsidiary do not appear in the consolidated statement of financial position.

There is, however, a much more important legal reason why the reserves of the subsidiary do not appear in the consolidated statement of financial position. This is because they arose prior to its acquisition by the parent company, which is why they are referred to as pre-acquisition reserves.

The rest of this chapter focuses on post-acquisition revenue reserves/retained earnings. However, before moving on it is important to appreciate that the above discussion relating to the treatment of pre-acquisition reserves applies to all reserves – both revenue and capital. That is, any retained earnings, share premium account and/or revaluation reserve in the financial statements of the subsidiary which arose prior to acquisition must not be included in the consolidated statement of financial position.

This brings us to the next important point in consolidated statements of financial position. Whereas pre-acquisition reserves of a subsidiary are not included in a consolidated statement of financial position, post-acquisition reserves are included. This is because they are generated after acquisition and are represented by an increase in the net assets of the subsidiary. Therefore, they belong to the equity

734.4 the consolidated statement of financial position

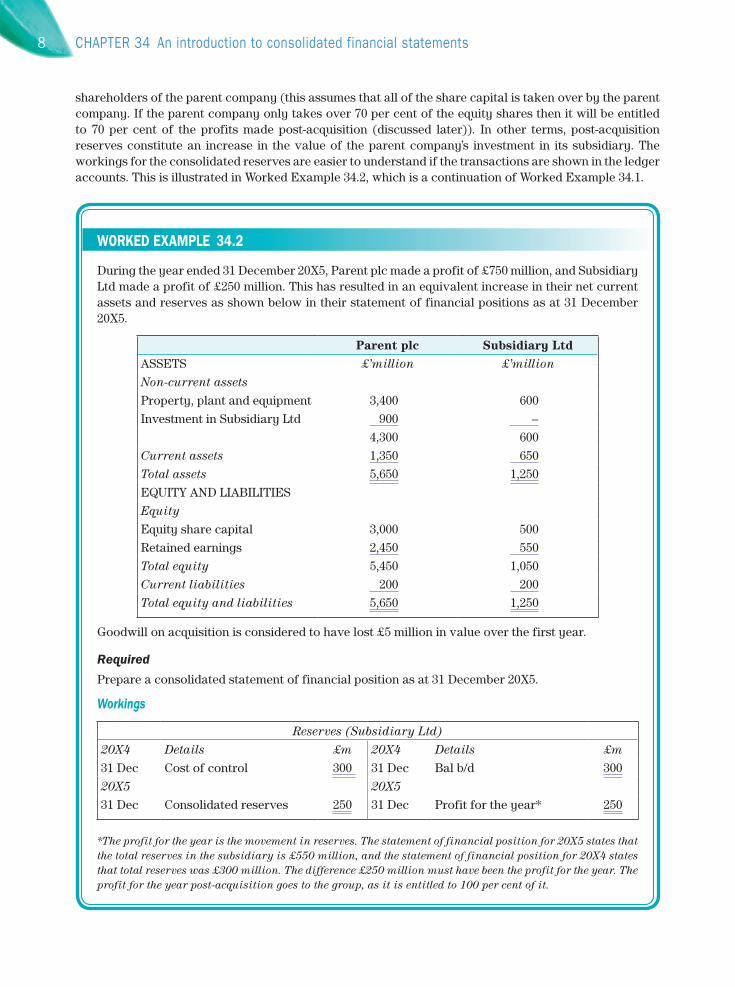

shareholders of the parent company (this assumes that all of the share capital is taken over by the parent company. If the parent company only takes over 70 per cent of the equity shares then it will be entitled to 70 per cent of the profits made post-acquisition (discussed later)). In other terms, post-acquisition reserves constitute an increase in the value of the parent company’s investment in its subsidiary. The workings for the consolidated reserves are easier to understand if the transactions are shown in the ledger accounts. This is illustrated in Worked Example 34.2, which is a continuation of Worked Example 34.1.

WORKED EXAMPLE 34.2

During the year ended 31 December 20X5, Parent plc made a profit of £750 million, and Subsidiary Ltd made a profit of £250 million. This has resulted in an equivalent increase in their net current assets and reserves as shown below in their statement of financial positions as at 31 December 20X5.

Parent plc Subsidiary LtdASSETS £’million £’millionNon-current assetsProperty, plant and equipment 3,400 600Investment in Subsidiary Ltd 900 –

4,300 600Current assets 1,350 650Total assets 5,650 1,250EQUITY AND LIABILITIESEquityEquity share capital 3,000 500Retained earnings 2,450 550Total equity 5,450 1,050Current liabilities 200 200Total equity and liabilities 5,650 1,250

Goodwill on acquisition is considered to have lost £5 million in value over the first year.

Required

Prepare a consolidated statement of financial position as at 31 December 20X5.

Workings

Reserves (Subsidiary Ltd)20X4 Details £m 20X4 Details £m31 Dec Cost of control 300 31 Dec Bal b/d 30020X5 20X531 Dec Consolidated reserves 250 31 Dec Profit for the year* 250

*The profit for the year is the movement in reserves. The statement of financial position for 20X5 states that the total reserves in the subsidiary is £550 million, and the statement of financial position for 20X4 states that total reserves was £300 million. The difference £250 million must have been the profit for the year. The profit for the year post-acquisition goes to the group, as it is entitled to 100 per cent of it.

8 ChApter 34 An introduction to consolidated financial statements

Reserves (Parent plc)20X4 Details £m 20X4 Details £m31 Dec Consolidated reserves 1,700 31 Dec Bal b/d 1,70020X5 20X531 Dec Consolidated reserves 750 31 Dec Profit for the year* 750

*The profit for the year is the movement in reserves. The statement of financial position for 20X5 states that the total reserves in the subsidiary is £2,450 million, and the statement of financial position for 20X4 states that total reserves was £1,700 million. The difference £750 million must have been the profit for the year. All of the profits of the parent are the group’s.

The only group-specific adjustment is the impairment of goodwill by £5 million. The double entry for this will be:

Debit: Statement of comprehensive income group (retained earnings)

£5,000,000

Credit: Goodwill account £5,000,000

Being the impairment of goodwill by £5 million in the year ended 31 December 20X5.

Consolidated reserves20X5 Details £m 20X5 Details £m31 Dec Goodwill impairment 5 1 Jan Reserves (Parent plc) 1,700

31 Dec Reserves (Subsidiary Ltd) 25031 Dec Balance c/d 2,695 Reserves (Parent plc) 750

2,700 2,70020X6 1 Jan Balance b/d 2,695

Parent group

Consolidated statement of financial position as at 31 December 20X5ASSETS £mNon-current assets

Property, plant and equipment (£3,400 + £600) 4,000

Goodwill (£100 - £5) 95

4,095

Current assets (£1,350 + £650) 2,000

Total assets 6,095EQUITY AND LIABILITIESEquityEquity share capital 3,000Retained earnings 2,695Total equity 5,695

Current liabilities (£200 + £200) 400

Total equity and liabilities 6,095

934.4 the consolidated statement of financial position

34.5 Non-controlling interests (statement of financial position) So far in this section it has been assumed that the subsidiary is wholly owned. As has already been mentioned, a subsidiary may be partially owned by its parent company, in which case there will be a non-controlling interest, as defined earlier. What needs to be explained at this stage is why non-controlling interests appear in consolidated statements of financial position. The reason is essentially that one of the basic underlying principles of consolidation is that consolidated financial statements are prepared on the basis that the parent and subsidiary are ‘a single economic entity’. That is, all the assets and liabilities of the parent and subsidiary are aggregated without regard to the proportion of the subsidiary’s voting shares that are owned by the parent. However, it must be recognized that a proportion of these net assets is owned/financed by the other (non-controlling) shareholders. This is achieved by entering the value of the non-controlling interest on the consolidated statement of financial position as a part of the group’s capital. There are two methods allowed under IFRS 3, the non-controlling interest’s proportionate share of the acquiree’s identifiable net assets (proportionate share approach) or at fair value. The difference between the two methods is that the goodwill recognized in the parent group statement of financial position under the proportionate share approach represents that attributable to the proportion owned by the parent company only, whereas under the fair value approach, goodwill represents the amount attributable to the whole company on the date of acquisition. As a consequence of the fair value approach, the balance on the goodwill account will be higher, as will the balance on the non-controlling interests account and future write-offs to the income statement on diminution in value will be higher.

The two approaches are covered in Worked Examples 34.3 and 34.4.

The movement in non-controlling interests is best explained using a ledger account. At this stage, when consolidating, it is recommended that the subsidiary’s equity accounts and two group ledger accounts are opened: the ‘cost of control’ and ‘non-controlling interests’. This is illustrated in Worked Examples 34.3 and 34.4. The latter is a continuation of the former.

WORKED EXAMPLE 34.3 (proportionate share approach)

The following are the statements of financial position of Holding plc and Subsidiary Ltd as at 31 December 20X4:

Holding plc Subsidiary LtdASSETS £m £mNon-current assetsProperty, plant and equipment 3,760 600Investment in Subsidiary Ltd 540 –

4,300 600Current assets 600 400Total assets 4,900 1,000EQUITY AND LIABILITIESEquityEquity share capital 3,000 500Retained earnings 1,700 300Total equity 4,700 800Current liabilities 200 200Total equity and liabilities 4,900 1,000

10 ChApter 34 An introduction to consolidated financial statements

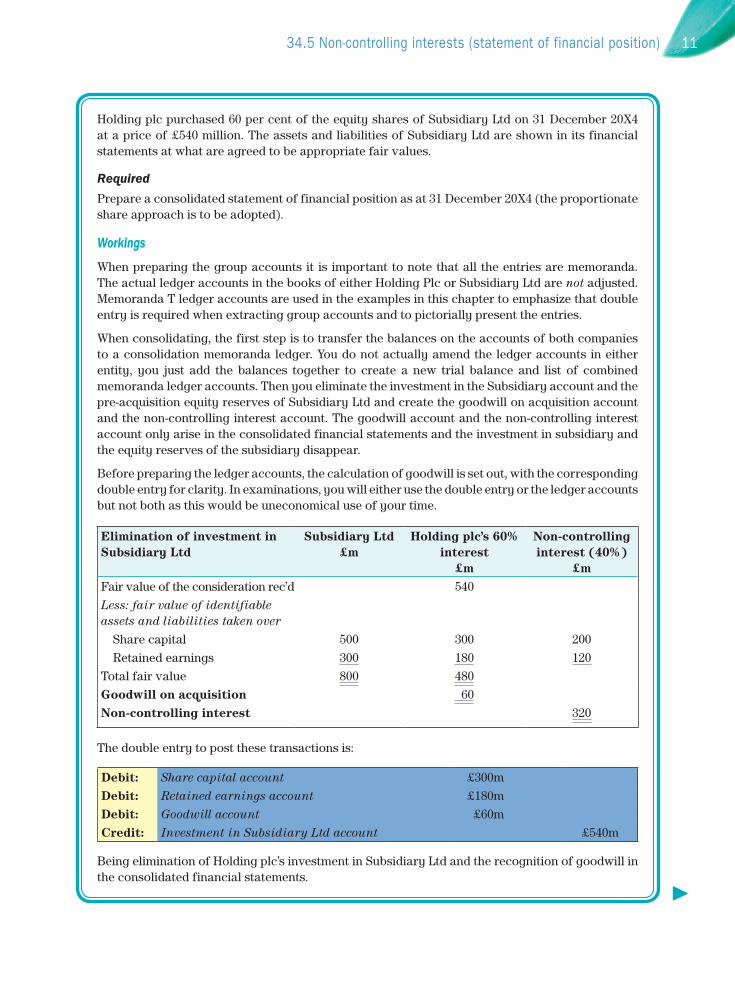

Holding plc purchased 60 per cent of the equity shares of Subsidiary Ltd on 31 December 20X4 at a price of £540 million. The assets and liabilities of Subsidiary Ltd are shown in its financial statements at what are agreed to be appropriate fair values.

Required

Prepare a consolidated statement of financial position as at 31 December 20X4 (the proportionate share approach is to be adopted).

Workings

When preparing the group accounts it is important to note that all the entries are memoranda. The actual ledger accounts in the books of either Holding Plc or Subsidiary Ltd are not adjusted. Memoranda T ledger accounts are used in the examples in this chapter to emphasize that double entry is required when extracting group accounts and to pictorially present the entries.

When consolidating, the first step is to transfer the balances on the accounts of both companies to a consolidation memoranda ledger. You do not actually amend the ledger accounts in either entity, you just add the balances together to create a new trial balance and list of combined memoranda ledger accounts. Then you eliminate the investment in the Subsidiary account and the pre-acquisition equity reserves of Subsidiary Ltd and create the goodwill on acquisition account and the non-controlling interest account. The goodwill account and the non-controlling interest account only arise in the consolidated financial statements and the investment in subsidiary and the equity reserves of the subsidiary disappear.

Before preparing the ledger accounts, the calculation of goodwill is set out, with the corresponding double entry for clarity. In examinations, you will either use the double entry or the ledger accounts but not both as this would be uneconomical use of your time.

Elimination of investment in Subsidiary Ltd

Subsidiary Ltd £m

Holding plc’s 60% interest

£m

Non-controlling interest (40%)

£mFair value of the consideration rec’d 540Less: fair value of identifiable assets and liabilities taken over

Share capital 500 300 200Retained earnings 300 180 120

Total fair value 800 480Goodwill on acquisition 60Non-controlling interest 320

The double entry to post these transactions is:

Debit: Share capital account £300mDebit: Retained earnings account £180mDebit: Goodwill account £60mCredit: Investment in Subsidiary Ltd account £540m

Being elimination of Holding plc’s investment in Subsidiary Ltd and the recognition of goodwill in the consolidated financial statements.

►

1134.5 Non-controlling interests (statement of financial position)

Debit: Share capital account £200mDebit: Retained earnings account £120mCredit: Non-controlling interests account £320m

Being recognition of the non-controlling interests in the consolidated financial statements.

The entries in the ledger accounts for the proportionate share approach.

Cost of control account20X4 Details £m 20X4 Details £m31 Dec Inv. in Subsidiary Ltd 540 31 Dec 60% Share capital 300

60% Retained earnings 180 Goodwill 60540 540

Subsidiary Ltd reserves20X4 Details £m 20X4 Details £m31 Dec Cost of control (60%) 180 31 Dec Balance b/d 30031 Dec Non-controlling interest (40%) 120

300 300

Subsidiary Ltd Share capital20X4 Details £m 20X4 Details £m31 Dec Cost of control (60%) 300 31 Dec Balance c/d 50031 Dec Non-controlling interest (40%) 200

500 500

Non-controlling interest20X4 Details £m 20X4 Details £m

31 Dec Reserves Subsidiary (40%) 12031 Dec Balance c/d 320 31 Dec Share capital: Subsidiary

(40%)200

320 320 20X5 1 Jan Balance b/d 320

Holding group

Consolidated statement of financial position as at 31 December 20X4ASSETS £mNon-current assets

Property, plant and equipment (£3,760 + £600) 4,360

Goodwill 604,420

◀

12 ChApter 34 An introduction to consolidated financial statements

Current assets (£600 + £400) 1,000

Total assets 5,420

EQUITY AND LIABILITIES

Equity attributable to owners of the parent

Equity share capital 3,000

Retained earnings 1,700

4,700

Non-controlling interest 320

Total equity 5,020

Current liabilities (£200 + £200) 400

Total equity and liabilities 5,420

WORKED EXAMPLE 34.4 (fair value approach)

Required

Using the information and statements of financial position of Holding plc and Subsidiary Ltd as detailed in Worked Example 34.3 prepare a consolidated statement of financial position as at 31 December 20X4 (the fair value approach is to be adopted).

Workings

The fair value approach can also be regarded as the gross approach.

Elimination of investment in Subsidiary Ltd

Subsidiary Ltd £m

Holding plc’s 60% interest

£m

Non-controlling interest (40%)

£m

Fair value of the consideration received 540 540

Plus: Non-controlling interest measured at fair value (£540 × 40/60)

360

Total fair value of the subsidiary 900

Less: fair value of identifiable assets and liabilities taken over

Share capital 500 300 200

Retained earnings 300 180 120

Total fair value 800 480 320

Goodwill on acquisition 100 60 40

Non-controlling interest 360

►

1334.5 Non-controlling interests (statement of financial position)

The double entry to post these transactions are:

Debit: Share capital account £300m

Debit: Retained earnings account £180m

Debit: Goodwill account £60m

Credit: Investment in Subsidiary Ltd account £540m

Being elimination of Holding plc’s investment in Subsidiary Ltd and the recognition of goodwill in the consolidated financial statements.

Debit: Share capital account £200m

Debit: Retained earnings account £120m

Debit: Goodwill account £40m

Credit: Non-controlling interests account £360m

Being recognition of the non-controlling interests in the consolidated financial statements.

The entries in the memoranda ledger accounts for the fair value approach.

Cost of control account

20X4 Details £m 20X4 Details £m

31 Dec Inv. in Subsidiary Ltd 540 31 Dec 60% Share capital 300

60% Retained earnings 180

Goodwill 60

540 540

Goodwill account

20X4 Details £m 20X4 Details £m

31 Dec Cost of control 60

31 Dec Non-controlling interest 40 31 Dec Balance c/d 100

100 100

Non-controlling interests

20X4 Details £m 20X4 Details £m

31 Dec Reserves Subsidiary (40%) 120

31 Dec Share capital: Subsidiary (40%) 200

31 Dec Balance c/d 320 31 Dec Goodwill 40

320 320

20X5

1 Jan Balance b/d 320

◀

14 ChApter 34 An introduction to consolidated financial statements

To this point the worked examples have only dealt with subsidiary pre-acquisition reserves. In the next two examples post-acquisition subsidiary reserve movements are considered. In simple terms, the subsidiary’s reserve accounts are to be split into pre-acquisition and post-acquisition. Pre-acquisition reserves are treated as outlined in Worked Examples 34.3 and 34.4. Post-acquisition reserves are adjusted for any group only transactions, such as goodwill impairments, and are then split between the parent company reserves account and the non-controlling interest account in the memoranda ledger consolidation accounts. This is best explained using an example.

Every year on consolidation the balances of the asset and liability accounts are just added together as in Worked Example 34.3. However, the consolidation memoranda ledger equity reserve accounts from the previous years would be carried forward and adjusted for the changes made to the reserve accounts in the current year. This is because the changes in the assets and liability accounts are captured in the equity reserve accounts so these changes need to be made or the group accounts will not balance. The process is shown in Worked Example 34.5. The carried forward ledger transactions relating to prior years are highlighted in this question. So, for example, you would not have to prepare the cost of consolidation account again.

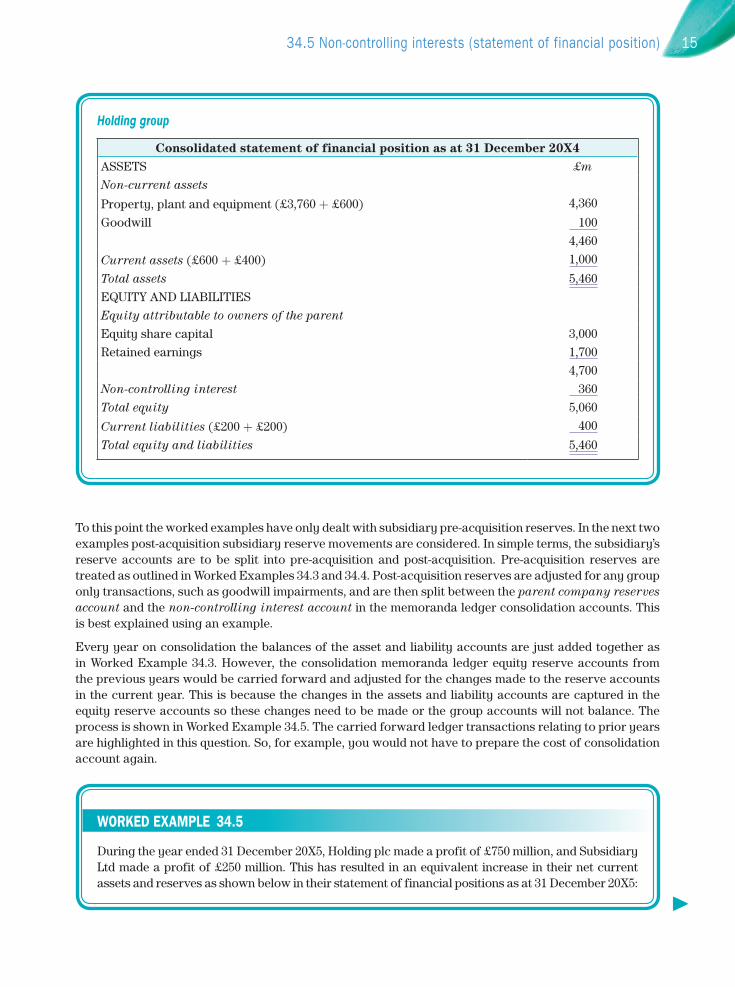

Holding group

Consolidated statement of financial position as at 31 December 20X4ASSETS £mNon-current assets

Property, plant and equipment (£3,760 + £600) 4,360

Goodwill 1004,460

Current assets (£600 + £400) 1,000

Total assets 5,460EQUITY AND LIABILITIESEquity attributable to owners of the parentEquity share capital 3,000Retained earnings 1,700

4,700Non-controlling interest 360Total equity 5,060

Current liabilities (£200 + £200) 400

Total equity and liabilities 5,460

WORKED EXAMPLE 34.5

During the year ended 31 December 20X5, Holding plc made a profit of £750 million, and Subsidiary Ltd made a profit of £250 million. This has resulted in an equivalent increase in their net current assets and reserves as shown below in their statement of financial positions as at 31 December 20X5:

►

1534.5 Non-controlling interests (statement of financial position)

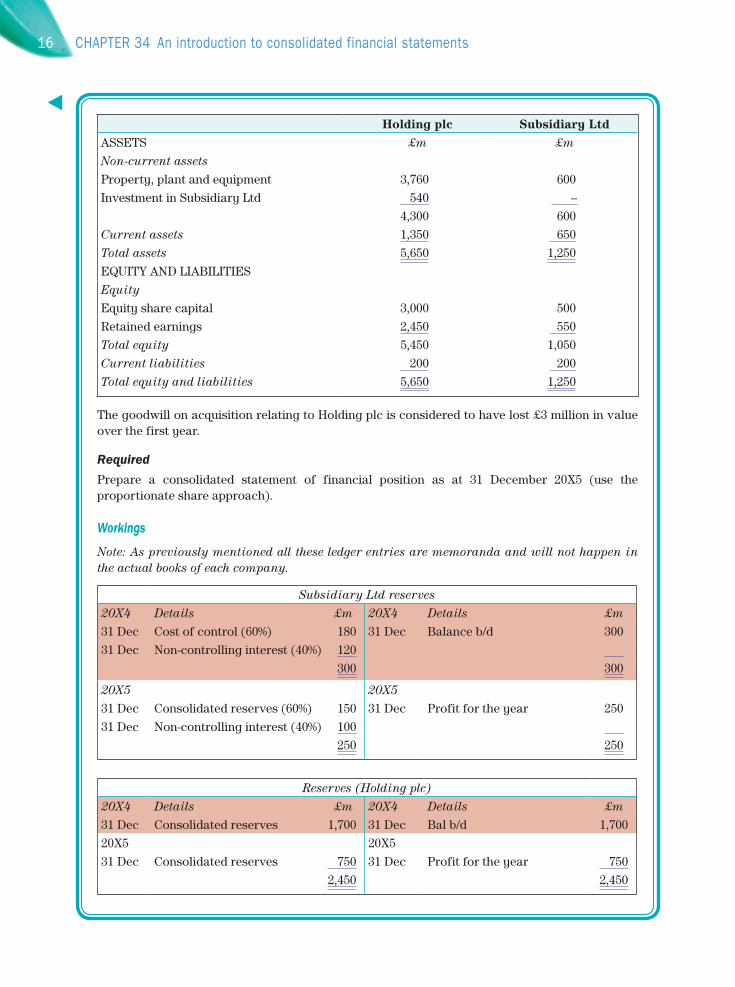

Holding plc Subsidiary LtdASSETS £m £mNon-current assetsProperty, plant and equipment 3,760 600Investment in Subsidiary Ltd 540 –

4,300 600Current assets 1,350 650Total assets 5,650 1,250EQUITY AND LIABILITIESEquityEquity share capital 3,000 500Retained earnings 2,450 550Total equity 5,450 1,050Current liabilities 200 200Total equity and liabilities 5,650 1,250

The goodwill on acquisition relating to Holding plc is considered to have lost £3 million in value over the first year.

Required

Prepare a consolidated statement of financial position as at 31 December 20X5 (use the proportionate share approach).

Workings

Note: As previously mentioned all these ledger entries are memoranda and will not happen in the actual books of each company.

Subsidiary Ltd reserves20X4 Details £m 20X4 Details £m31 Dec Cost of control (60%) 180 31 Dec Balance b/d 30031 Dec Non-controlling interest (40%) 120

300 300

20X5 20X531 Dec Consolidated reserves (60%) 150 31 Dec Profit for the year 25031 Dec Non-controlling interest (40%) 100

250 250

Reserves (Holding plc)20X4 Details £m 20X4 Details £m31 Dec Consolidated reserves 1,700 31 Dec Bal b/d 1,70020X5 20X531 Dec Consolidated reserves 750 31 Dec Profit for the year 750

2,450 2,450

◀

16 ChApter 34 An introduction to consolidated financial statements

Consolidated reserves20X5 Details £m 20X5 Details £m31 Dec Goodwill impairment 3 1 Jan Reserves (Holding plc) 1,700

31 Dec Profit (Subsidiary Ltd) 60% 15031 Dec Balance c/d 2,597 Profit (Holding plc) 100% 750

2,600 2,60020X6 1 Jan Balance b/d 2,597

Non-controlling interests20X4 Details £m 20X4 Details £m

31 Dec Reserves Subsidiary (40%) 12031 Dec Balance c/d 320 31 Dec Share capital: Subsidiary

(40%)200

320 32020X5 20X5

1 Jan Balance b/d 32031 Dec Balance c/d 420 31 Dec Profit in year Subsidiary (40%) 100

420 42020X6 1 Dec Balance b/d 420

Holding group

Consolidated statement of financial position as at 31 December 20X5ASSETS £mNon-current assets

Property, plant and equipment (£3,760 + £600) 4,360

Goodwill (£60 - £3) 57

4,417

Current assets (£1,350 + £650) 2,000

Total assets 6,417EQUITY AND LIABILITIESEquity attributable to owners of the parentEquity share capital 3,000Retained earnings 2,597

5,597Non-controlling interests 420Total equity 6,017

Current liabilities (£200 + £200) 400

Total equity and liabilities 6,417

1734.5 Non-controlling interests (statement of financial position)

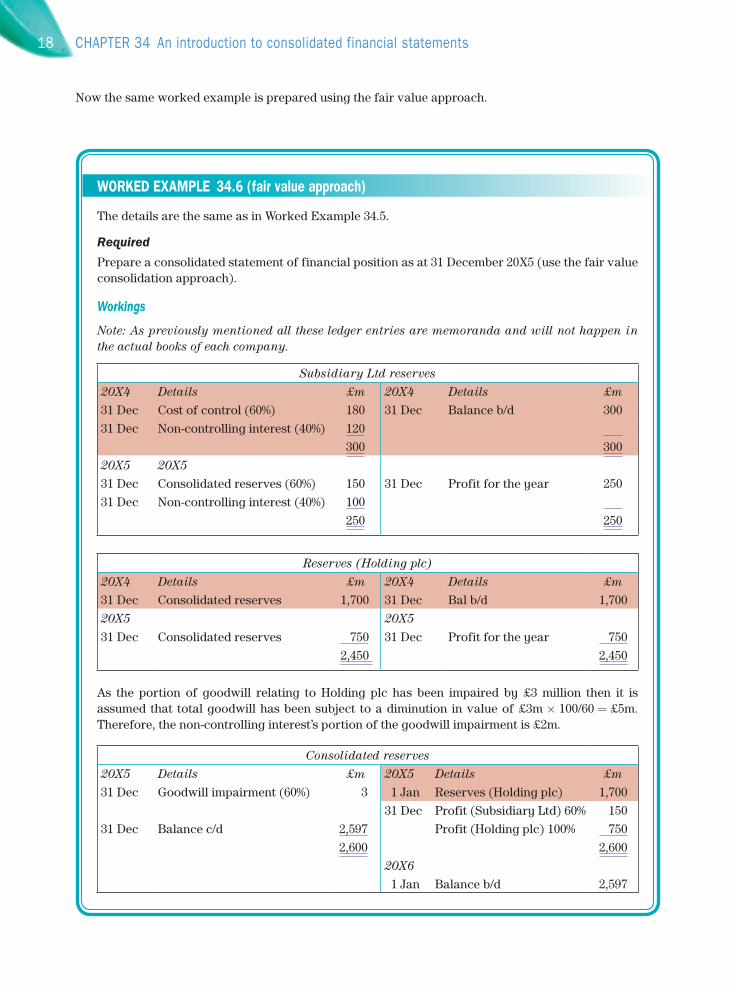

Now the same worked example is prepared using the fair value approach.

WORKED EXAMPLE 34.6 (fair value approach)

The details are the same as in Worked Example 34.5.

Required

Prepare a consolidated statement of financial position as at 31 December 20X5 (use the fair value consolidation approach).

Workings

Note: As previously mentioned all these ledger entries are memoranda and will not happen in the actual books of each company.

Subsidiary Ltd reserves20X4 Details £m 20X4 Details £m31 Dec Cost of control (60%) 180 31 Dec Balance b/d 30031 Dec Non-controlling interest (40%) 120

300 30020X5 20X531 Dec Consolidated reserves (60%) 150 31 Dec Profit for the year 25031 Dec Non-controlling interest (40%) 100

250 250

Reserves (Holding plc)20X4 Details £m 20X4 Details £m31 Dec Consolidated reserves 1,700 31 Dec Bal b/d 1,70020X5 20X5

31 Dec Consolidated reserves 750 31 Dec Profit for the year 7502,450 2,450

As the portion of goodwill relating to Holding plc has been impaired by £3 million then it is assumed that total goodwill has been subject to a diminution in value of £3m × 100/60 = £5m. Therefore, the non-controlling interest’s portion of the goodwill impairment is £2m.

Consolidated reserves20X5 Details £m 20X5 Details £m31 Dec Goodwill impairment (60%) 3 1 Jan Reserves (Holding plc) 1,700

31 Dec Profit (Subsidiary Ltd) 60% 15031 Dec Balance c/d 2,597 Profit (Holding plc) 100% 750

2,600 2,600 20X6

1 Jan Balance b/d 2,597

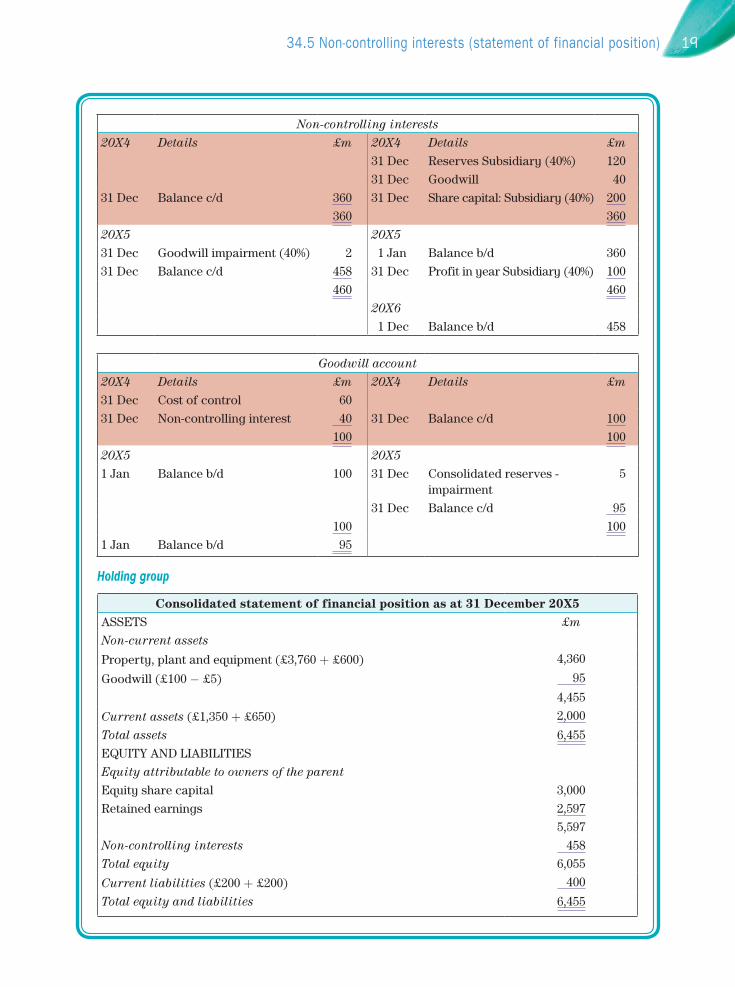

18 ChApter 34 An introduction to consolidated financial statements

Non-controlling interests20X4 Details £m 20X4 Details £m

31 Dec Reserves Subsidiary (40%) 12031 Dec Goodwill 40

31 Dec Balance c/d 360 31 Dec Share capital: Subsidiary (40%) 200360 360

20X5 20X531 Dec Goodwill impairment (40%) 2 1 Jan Balance b/d 36031 Dec Balance c/d 458 31 Dec Profit in year Subsidiary (40%) 100

460 46020X6 1 Dec Balance b/d 458

Goodwill account20X4 Details £m 20X4 Details £m31 Dec Cost of control 6031 Dec Non-controlling interest 40 31 Dec Balance c/d 100

100 10020X5 20X51 Jan Balance b/d 100 31 Dec Consolidated reserves -

impairment 5

31 Dec Balance c/d 95100 100

1 Jan Balance b/d 95

Holding group

Consolidated statement of financial position as at 31 December 20X5ASSETS £mNon-current assets

Property, plant and equipment (£3,760 + £600) 4,360

Goodwill (£100 - £5) 95

4,455

Current assets (£1,350 + £650) 2,000

Total assets 6,455EQUITY AND LIABILITIESEquity attributable to owners of the parentEquity share capital 3,000Retained earnings 2,597

5,597Non-controlling interests 458Total equity 6,055

Current liabilities (£200 + £200) 400

Total equity and liabilities 6,455

1934.5 Non-controlling interests (statement of financial position)

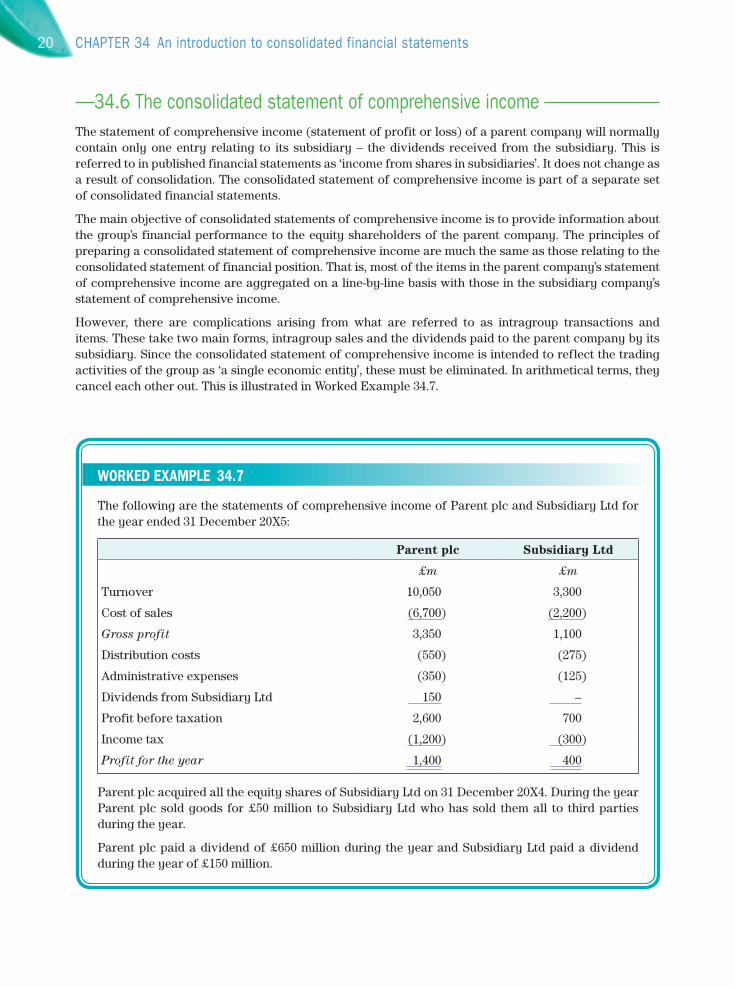

34.6 the consolidated statement of comprehensive income The statement of comprehensive income (statement of profit or loss) of a parent company will normally contain only one entry relating to its subsidiary – the dividends received from the subsidiary. This is referred to in published financial statements as ‘income from shares in subsidiaries’. It does not change as a result of consolidation. The consolidated statement of comprehensive income is part of a separate set of consolidated financial statements.

The main objective of consolidated statements of comprehensive income is to provide information about the group’s financial performance to the equity shareholders of the parent company. The principles of preparing a consolidated statement of comprehensive income are much the same as those relating to the consolidated statement of financial position. That is, most of the items in the parent company’s statement of comprehensive income are aggregated on a line-by-line basis with those in the subsidiary company’s statement of comprehensive income.

However, there are complications arising from what are referred to as intragroup transactions and items. These take two main forms, intragroup sales and the dividends paid to the parent company by its subsidiary. Since the consolidated statement of comprehensive income is intended to reflect the trading activities of the group as ‘a single economic entity’, these must be eliminated. In arithmetical terms, they cancel each other out. This is illustrated in Worked Example 34.7.

WORKED EXAMPLE 34.7

The following are the statements of comprehensive income of Parent plc and Subsidiary Ltd for the year ended 31 December 20X5:

Parent plc Subsidiary Ltd

£m £m

Turnover 10,050 3,300

Cost of sales (6,700) (2,200)

Gross profit 3,350 1,100

Distribution costs (550) (275)

Administrative expenses (350) (125)

Dividends from Subsidiary Ltd 150 –

Profit before taxation 2,600 700

Income tax (1,200) (300)

Profit for the year 1,400 400

Parent plc acquired all the equity shares of Subsidiary Ltd on 31 December 20X4. During the year Parent plc sold goods for £50 million to Subsidiary Ltd who has sold them all to third parties during the year.

Parent plc paid a dividend of £650 million during the year and Subsidiary Ltd paid a dividend during the year of £150 million.

20 ChApter 34 An introduction to consolidated financial statements

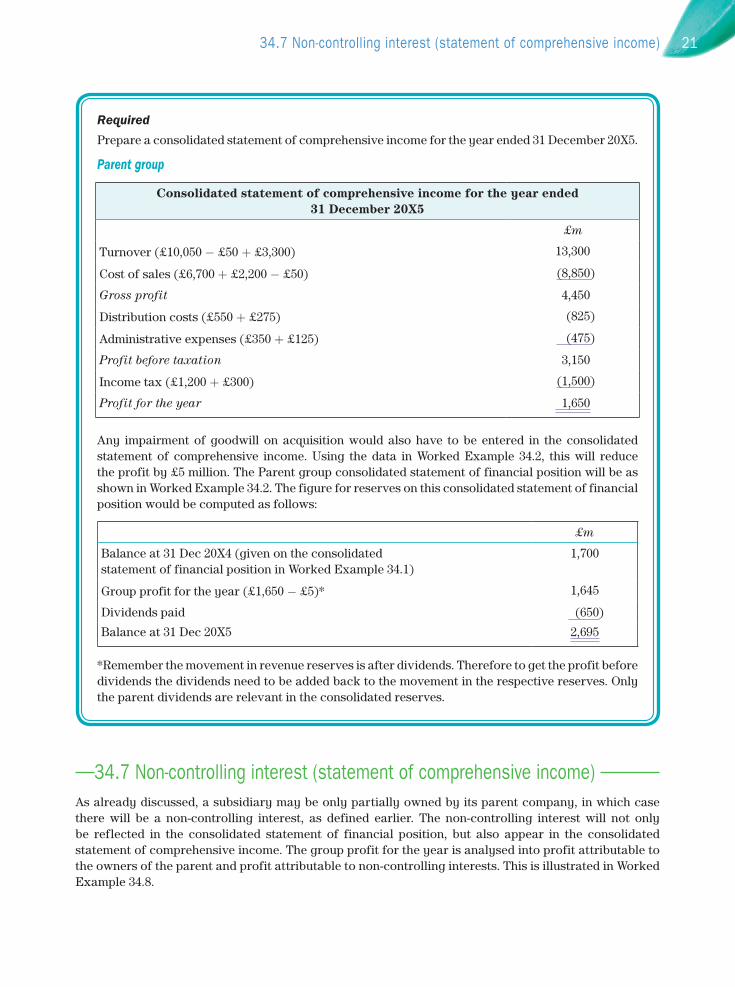

Required

Prepare a consolidated statement of comprehensive income for the year ended 31 December 20X5.

Parent group

Consolidated statement of comprehensive income for the year ended 31 December 20X5

£m

Turnover (£10,050 - £50 + £3,300) 13,300

Cost of sales (£6,700 + £2,200 - £50) (8,850)

Gross profit 4,450

Distribution costs (£550 + £275) (825)

Administrative expenses (£350 + £125) (475)

Profit before taxation 3,150

Income tax (£1,200 + £300) (1,500)

Profit for the year 1,650

Any impairment of goodwill on acquisition would also have to be entered in the consolidated statement of comprehensive income. Using the data in Worked Example 34.2, this will reduce the profit by £5 million. The Parent group consolidated statement of financial position will be as shown in Worked Example 34.2. The figure for reserves on this consolidated statement of financial position would be computed as follows:

£m

Balance at 31 Dec 20X4 (given on the consolidated statement of financial position in Worked Example 34.1)

1,700

Group profit for the year (£1,650 - £5)* 1,645

Dividends paid (650)

Balance at 31 Dec 20X5 2,695

*Remember the movement in revenue reserves is after dividends. Therefore to get the profit before dividends the dividends need to be added back to the movement in the respective reserves. Only the parent dividends are relevant in the consolidated reserves.

34.7 Non-controlling interest (statement of comprehensive income) As already discussed, a subsidiary may be only partially owned by its parent company, in which case there will be a non-controlling interest, as defined earlier. The non-controlling interest will not only be reflected in the consolidated statement of financial position, but also appear in the consolidated statement of comprehensive income. The group profit for the year is analysed into profit attributable to the owners of the parent and profit attributable to non-controlling interests. This is illustrated in Worked Example 34.8.

2134.7 Non-controlling interest (statement of comprehensive income)

WORKED EXAMPLE 34.8

The following are the statements of comprehensive income of Holding plc and Subsidiary Ltd for the year ended 30 June 20X5:

Holding plc Subsidiary Ltd£m £m

Turnover 10,050 3,300Cost of sales (6,700) (2,200)Gross profit 3,350 1,100Distribution costs (550) (275)Administrative expenses (290) (125)Dividends from Subsidiary Ltd 90 –Profit before taxation 2,600 700Income tax (1,200) (300)Profit for the year 1,400 400

Holding plc acquired 60 per cent of the equity shares of Subsidiary Ltd on 30 June 20X4.

Holding plc paid a dividend of £650 million during the year and Subsidiary Ltd paid a dividend during the year of £150 million.

Required

Prepare a consolidated statement of comprehensive income for the year ended 30 June 20X5.

WorkingsNon-controlling interest = 40 per cent × £400m = £160m

Holding Group Consolidated statement of comprehensive income for the year ended 30 June 20X5

£m

Turnover (£10,050 + £3,300) 13,350

Cost of sales (£6,700 + £2,200) (8,900)

Gross profit 4,450

Distribution costs (£550 + £275) (825)

Administrative expenses (£290 + £125) (415)

Profit before taxation 3,210

Income tax (£1,200 + £300) (1,500)

Profit for the year 1,710Profit attributable to:Owners of the parent 1,550Non-controlling interests 160

1,710

Notice that the profit for the year in the consolidated statement of comprehensive income that is attributable to the equity holders of the parent company equals the profit for the year

22 ChApter 34 An introduction to consolidated financial statements

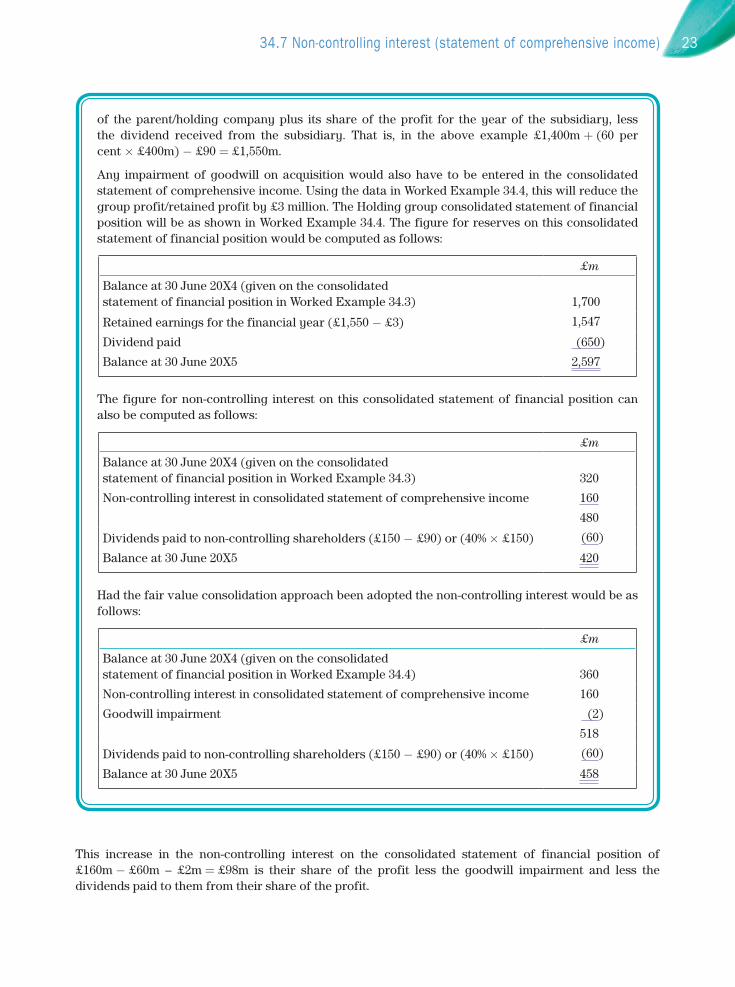

of the parent/holding company plus its share of the profit for the year of the subsidiary, less the dividend received from the subsidiary. That is, in the above example £1,400m + (60 per cent × £400m) - £90 = £1,550m.

Any impairment of goodwill on acquisition would also have to be entered in the consolidated statement of comprehensive income. Using the data in Worked Example 34.4, this will reduce the group profit/retained profit by £3 million. The Holding group consolidated statement of financial position will be as shown in Worked Example 34.4. The figure for reserves on this consolidated statement of financial position would be computed as follows:

£m

Balance at 30 June 20X4 (given on the consolidated statement of financial position in Worked Example 34.3) 1,700

Retained earnings for the financial year (£1,550 - £3) 1,547

Dividend paid (650)

Balance at 30 June 20X5 2,597

The figure for non-controlling interest on this consolidated statement of financial position can also be computed as follows:

£m

Balance at 30 June 20X4 (given on the consolidated statement of financial position in Worked Example 34.3) 320

Non-controlling interest in consolidated statement of comprehensive income 160

480

Dividends paid to non-controlling shareholders (£150 - £90) or (40% × £150) (60)

Balance at 30 June 20X5 420

Had the fair value consolidation approach been adopted the non-controlling interest would be as follows:

£m

Balance at 30 June 20X4 (given on the consolidated statement of financial position in Worked Example 34.4) 360

Non-controlling interest in consolidated statement of comprehensive income 160

Goodwill impairment (2)

518

Dividends paid to non-controlling shareholders (£150 - £90) or (40% × £150) (60)

Balance at 30 June 20X5 458

This increase in the non-controlling interest on the consolidated statement of financial position of £160m - £60m – £2m = £98m is their share of the profit less the goodwill impairment and less the dividends paid to them from their share of the profit.

2334.7 Non-controlling interest (statement of comprehensive income)

Learning Activity 34.2

Visit the website of a large listed/quoted public limited company that has a subsidiary whose shares are also listed, and find their latest annual report and financial statements. Examine the contents of the statement of comprehensive income (statement of profit or loss), statement of financial position and notes to the financial statements, paying particular attention to the items relating to goodwill and non-controlling interests.

Summary

The Companies Act 2006 as well as IFRS 3 and IFRS 10 require the preparation of consolidated financial statements where a group exists. A group is defined as a parent and all its subsidiaries. There are detailed legal regulations regarding when a parent–subsidiary relationship exists. The main criteria include: where the parent has the power to control decisions that impact on the entity’s variable returns. Control refers to the power that a parent has to govern the operating and financial policies of the subsidiary so as to have benefits from its activities.

Consolidated financial statements are defined in IFRS 3 as the financial statements of a group presented as those of a single economic entity. Consolidation is the process of adjusting and combining financial information from the individual financial statements of a parent and its subsidiaries in order to prepare consolidated financial statements that present financial information for the group as a single economic entity.

Consolidated financial statements include a consolidated statement of comprehensive income (statement of profit or loss) and a consolidated statement of financial position. These are prepared by aggregating on a line-by-line basis most of the items in the parent’s financial statements with those in the subsidiary’s financial statements while at the same time eliminating certain intra-group items, referred to above as adjustments.

The process of consolidation usually gives rise to goodwill on acquisition. This must be accounted for in accordance with IFRS 3 (i.e. impaired), which refers to it as ‘purchased goodwill’. Two methods of consolidation are permitted – the proportionate share approach and the fair value approach.

Where a subsidiary is only partially owned by the parent, the process of consolidation also gives rise to non-controlling interests in both the consolidated statement of comprehensive income and the consolidated statement of financial position. Non-controlling interests are defined in IFRS 10 as ‘the equity in a subsidiary not attributable directly or indirectly, to a parent’. Non-controlling interests are also referred to as minority interests in the UK.

The group profit for the year is analysed into profit attributable to the owners of the parent and profit attributable to non-controlling interests. The non-controlling interest is also shown in the consolidated statement of financial position as part of the group’s overall equity capital, and represents their share of the subsidiary’s net assets.

Key terms and concepts

business combination 3

consolidated financial statements 3

control 3

cost of control account 6

24 ChApter 34 An introduction to consolidated financial statements

Review questions

34.1 Define each of the following in accordance with the Companies Act 2006, IFRS 3 – Business Combinations (IASB, 2013a) and International Financial Reporting Standard 10 – Consolidated Financial Statements (IASB, 2013b):

a a group;

b a subsidiary;

c consolidated financial statements;

d consolidation.

34.2 Describe fully the provisions of IFRS 3 with regard to what constitutes a parent and a subsidiary.

34.3 a Explain the nature of goodwill arising on the acquisition of a subsidiary and how it is measured.

b Describe the requirements of IFRS 3 – Business Combinations (IASB, 2013a) with regard to the accounting treatment of purchased goodwill.

34.4 a Explain the objective(s) of consolidated financial statements.

b Describe in general terms the principles of consolidation.

34.5 Parhold plc has bought for cash of £12 million all the voting shares of Subsid plc, whose net assets have been valued at £10 million. Describe how this transaction would affect:

a the statement of financial position of Parhold plc; and

b the statement of financial position of Parhold Group, given that Subsid plc is the only subsidiary.

You need only describe the effects on these statements of financial position on the date of acquisition of Subsid’s shares.

34.6 Given the circumstances in Question 34.5 above, describe how this relationship between Parhold plc and Subsid plc would affect the following at the end of the first accounting year after acquisition:

a the financial statements of Subsid plc;

b the financial statements of Parhold plc; and

c the consolidated financial statements of Parhold Group.

34.7 a Define a non-controlling interest in accordance with IFRS 10 – Consolidated Financial Statements (IASB, 2013b).

group 3

minority interest 4

non-controlling interest 4

parent 2

partly owned subsidiary 2

pre-acquisition reserves 7

post-acquisition reserves 7

proportionate share approach 10

purchased goodwill 4

subsidiary 2

wholly owned subsidiary 2

25review questions

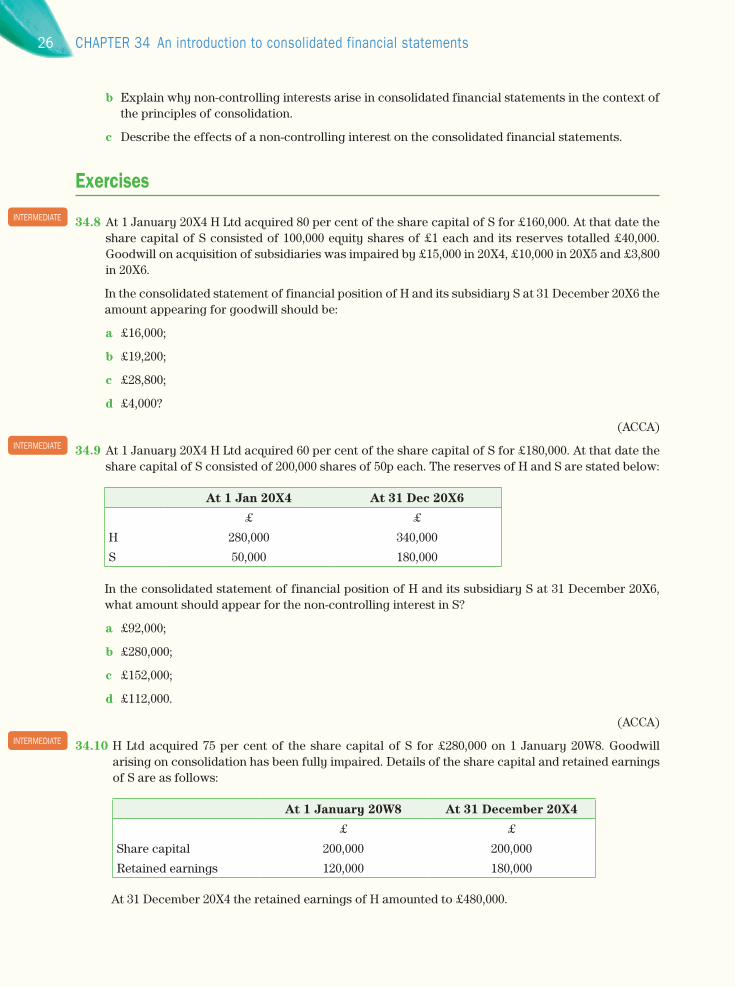

b Explain why non-controlling interests arise in consolidated financial statements in the context of the principles of consolidation.

c Describe the effects of a non-controlling interest on the consolidated financial statements.

Exercises

34.8 At 1 January 20X4 H Ltd acquired 80 per cent of the share capital of S for £160,000. At that date the share capital of S consisted of 100,000 equity shares of £1 each and its reserves totalled £40,000. Goodwill on acquisition of subsidiaries was impaired by £15,000 in 20X4, £10,000 in 20X5 and £3,800 in 20X6.

In the consolidated statement of financial position of H and its subsidiary S at 31 December 20X6 the amount appearing for goodwill should be:

a £16,000;

b £19,200;

c £28,800;

d £4,000?

(ACCA)

34.9 At 1 January 20X4 H Ltd acquired 60 per cent of the share capital of S for £180,000. At that date the share capital of S consisted of 200,000 shares of 50p each. The reserves of H and S are stated below:

At 1 Jan 20X4 At 31 Dec 20X6

£ £

H 280,000 340,000

S 50,000 180,000

In the consolidated statement of financial position of H and its subsidiary S at 31 December 20X6, what amount should appear for the non-controlling interest in S?

a £92,000;

b £280,000;

c £152,000;

d £112,000.

(ACCA)

34.10 H Ltd acquired 75 per cent of the share capital of S for £280,000 on 1 January 20W8. Goodwill arising on consolidation has been fully impaired. Details of the share capital and retained earnings of S are as follows:

At 1 January 20W8 At 31 December 20X4

£ £

Share capital 200,000 200,000

Retained earnings 120,000 180,000

At 31 December 20X4 the retained earnings of H amounted to £480,000.

INterMeDIAte

INterMeDIAte

INterMeDIAte

26 ChApter 34 An introduction to consolidated financial statements

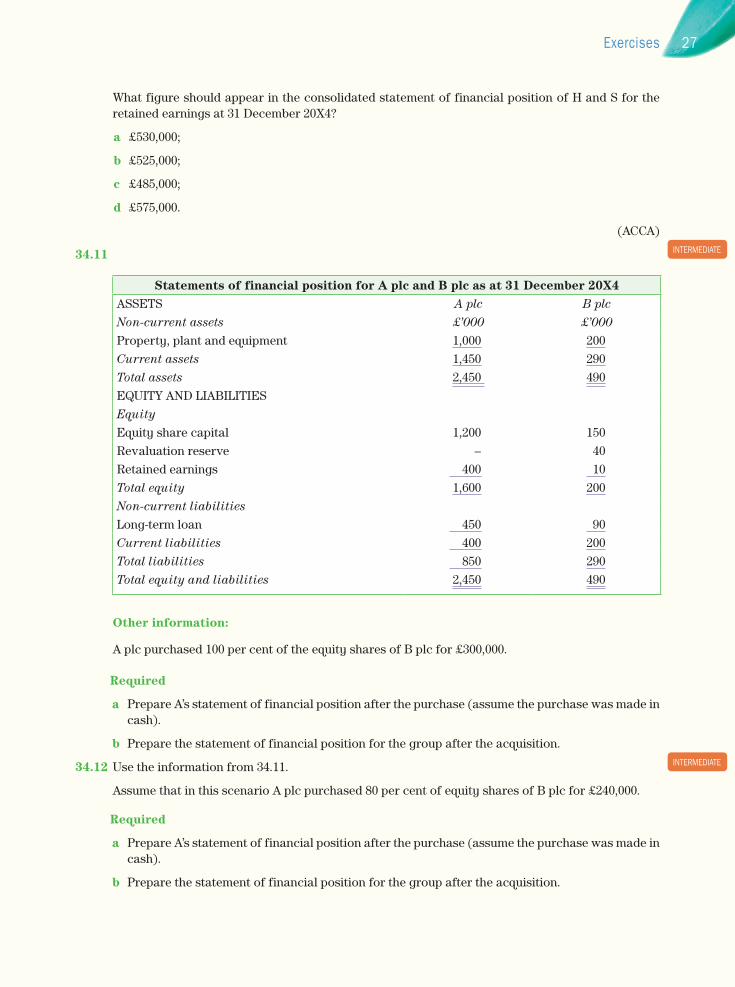

What figure should appear in the consolidated statement of financial position of H and S for the retained earnings at 31 December 20X4?

a £530,000;

b £525,000;

c £485,000;

d £575,000.

(ACCA)

34.11

Statements of financial position for A plc and B plc as at 31 December 20X4ASSETS A plc B plcNon-current assets £’000 £’000Property, plant and equipment 1,000 200Current assets 1,450 290Total assets 2,450 490EQUITY AND LIABILITIESEquityEquity share capital 1,200 150Revaluation reserve – 40Retained earnings 400 10Total equity 1,600 200Non-current liabilitiesLong-term loan 450 90Current liabilities 400 200Total liabilities 850 290Total equity and liabilities 2,450 490

Other information:

A plc purchased 100 per cent of the equity shares of B plc for £300,000.

Required

a Prepare A’s statement of financial position after the purchase (assume the purchase was made in cash).

b Prepare the statement of financial position for the group after the acquisition.

34.12 Use the information from 34.11.

Assume that in this scenario A plc purchased 80 per cent of equity shares of B plc for £240,000.

Required

a Prepare A’s statement of financial position after the purchase (assume the purchase was made in cash).

b Prepare the statement of financial position for the group after the acquisition.

INterMeDIAte

INterMeDIAte

27exercises

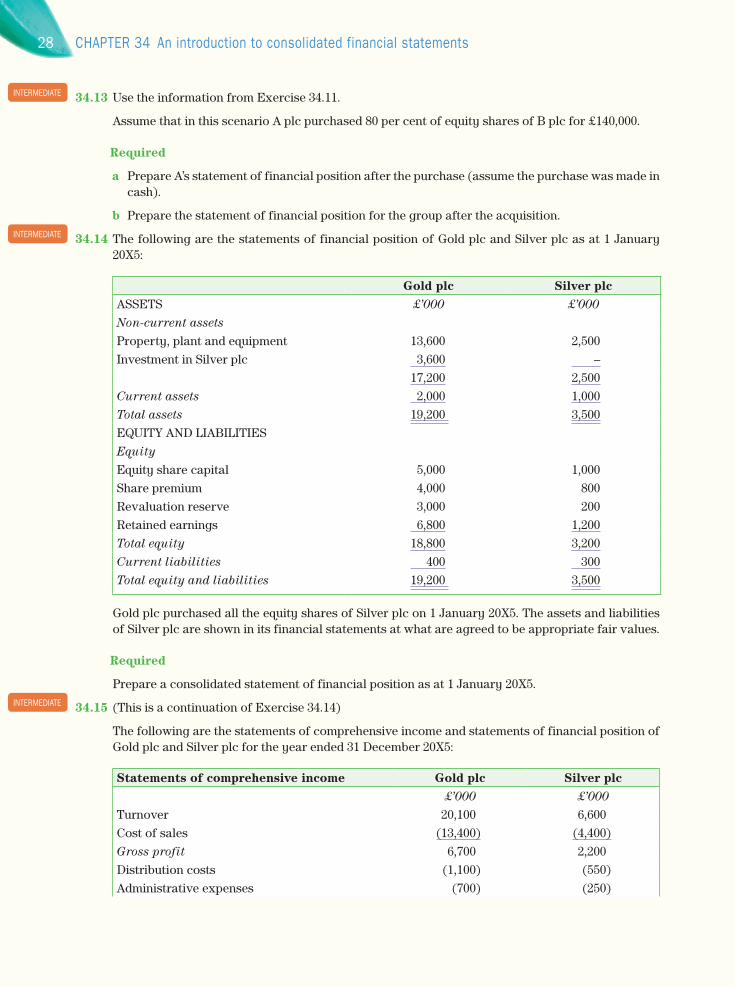

34.13 Use the information from Exercise 34.11.

Assume that in this scenario A plc purchased 80 per cent of equity shares of B plc for £140,000.

Required

a Prepare A’s statement of financial position after the purchase (assume the purchase was made in cash).

b Prepare the statement of financial position for the group after the acquisition.

34.14 The following are the statements of financial position of Gold plc and Silver plc as at 1 January 20X5:

Gold plc Silver plcASSETS £’000 £’000Non-current assetsProperty, plant and equipment 13,600 2,500Investment in Silver plc 3,600 –

17,200 2,500Current assets 2,000 1,000Total assets 19,200 3,500EQUITY AND LIABILITIESEquityEquity share capital 5,000 1,000Share premium 4,000 800Revaluation reserve 3,000 200Retained earnings 6,800 1,200Total equity 18,800 3,200Current liabilities 400 300Total equity and liabilities 19,200 3,500

Gold plc purchased all the equity shares of Silver plc on 1 January 20X5. The assets and liabilities of Silver plc are shown in its financial statements at what are agreed to be appropriate fair values.

Required

Prepare a consolidated statement of financial position as at 1 January 20X5.

34.15 (This is a continuation of Exercise 34.14)

The following are the statements of comprehensive income and statements of financial position of Gold plc and Silver plc for the year ended 31 December 20X5:

Statements of comprehensive income Gold plc Silver plc£’000 £’000

Turnover 20,100 6,600Cost of sales (13,400) (4,400)Gross profit 6,700 2,200Distribution costs (1,100) (550)Administrative expenses (700) (250)

INterMeDIAte

INterMeDIAte

INterMeDIAte

28 ChApter 34 An introduction to consolidated financial statements

Dividends from Silver plc 300 –Profit before taxation 5,200 1,400Income tax (2,400) (600)Profit for the year 2,800 800

Statements of financial position Gold plc Silver plcASSETS £’000 £’000

Non-current assets

Property, plant and equipment 13,600 2,500

Investment in Silver plc 3,600 –

17,200 2,500

Current assets 3,500 1,500

Total assets 20,700 4,000

EQUITY AND LIABILITIES

Equity

Equity share capital 5,000 1,000

Share premium 4,000 800

Revaluation reserve 3,000 200

Retained earnings 8,300 1,700

Total equity 20,300 3,700

Current liabilities 400 300

Total equity and liabilities 20,700 4,000

Other information

Gold plc paid a dividend of £1,300,000 during the year and Silver plc paid a dividend of £300,000 during the year.

Required

Prepare a consolidated statement of comprehensive income for the year and a consolidated statement of financial position as at 31 December 20X5. Goodwill has not diminished in value.

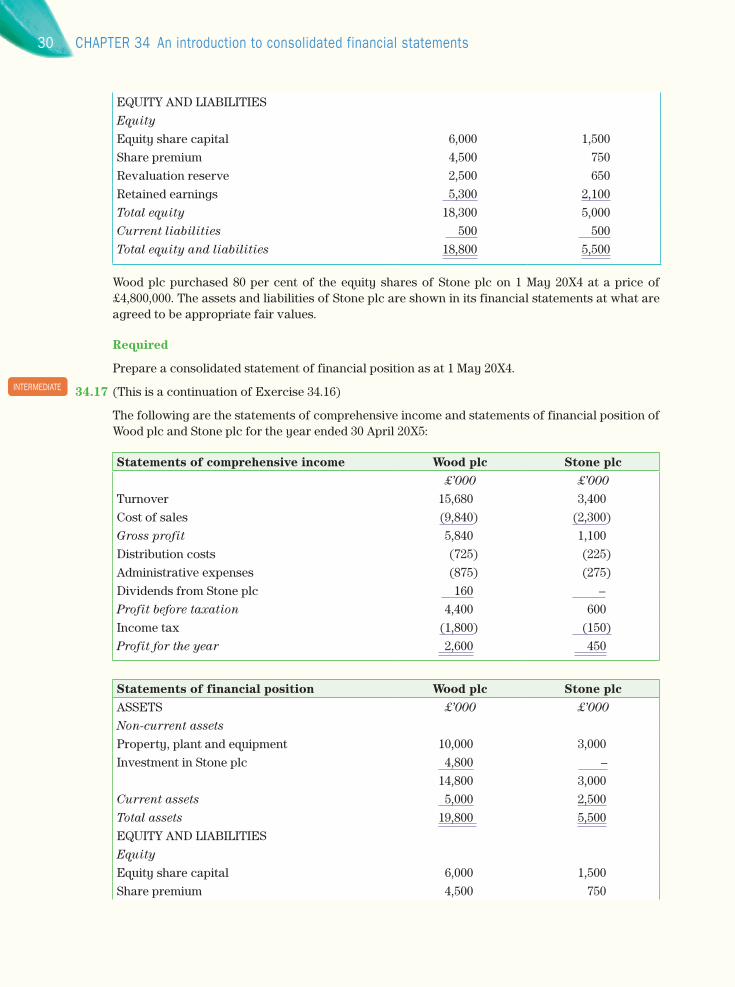

34.16 The following are the statements of financial positions of Wood plc and Stone plc as at 1 May 20X4:

Wood plc Stone plcASSETS £’000 £’000

Non-current assets

Property, plant and equipment 10,000 3,000

Investment in Stone plc 4,800 –

14,800 3,000

Current assets 4,000 2,500

Total assets 18,800 5,500

INterMeDIAte

29exercises

EQUITY AND LIABILITIESEquityEquity share capital 6,000 1,500Share premium 4,500 750Revaluation reserve 2,500 650Retained earnings 5,300 2,100Total equity 18,300 5,000Current liabilities 500 500Total equity and liabilities 18,800 5,500

Wood plc purchased 80 per cent of the equity shares of Stone plc on 1 May 20X4 at a price of £4,800,000. The assets and liabilities of Stone plc are shown in its financial statements at what are agreed to be appropriate fair values.

Required

Prepare a consolidated statement of financial position as at 1 May 20X4.

34.17 (This is a continuation of Exercise 34.16)

The following are the statements of comprehensive income and statements of financial position of Wood plc and Stone plc for the year ended 30 April 20X5:

Statements of comprehensive income Wood plc Stone plc£’000 £’000

Turnover 15,680 3,400Cost of sales (9,840) (2,300)Gross profit 5,840 1,100Distribution costs (725) (225)Administrative expenses (875) (275)Dividends from Stone plc 160 –Profit before taxation 4,400 600Income tax (1,800) (150)Profit for the year 2,600 450

Statements of financial position Wood plc Stone plcASSETS £’000 £’000Non-current assetsProperty, plant and equipment 10,000 3,000Investment in Stone plc 4,800 –

14,800 3,000Current assets 5,000 2,500Total assets 19,800 5,500EQUITY AND LIABILITIESEquityEquity share capital 6,000 1,500Share premium 4,500 750

INterMeDIAte

30 ChApter 34 An introduction to consolidated financial statements

Revaluation reserve 2,500 650Retained earnings 6,400 2,350Total equity 19,400 5,250Current liabilities 400 250Total equity and liabilities 19,800 5,500

Other information

Wood plc paid a dividend of £1,500,000 during the year and Stone plc paid a dividend of £200,000 during the year.

Required

Prepare a consolidated statement of comprehensive income for the year and a consolidated statement of financial position as at 30 April 20X5. Goodwill has not diminished in value.

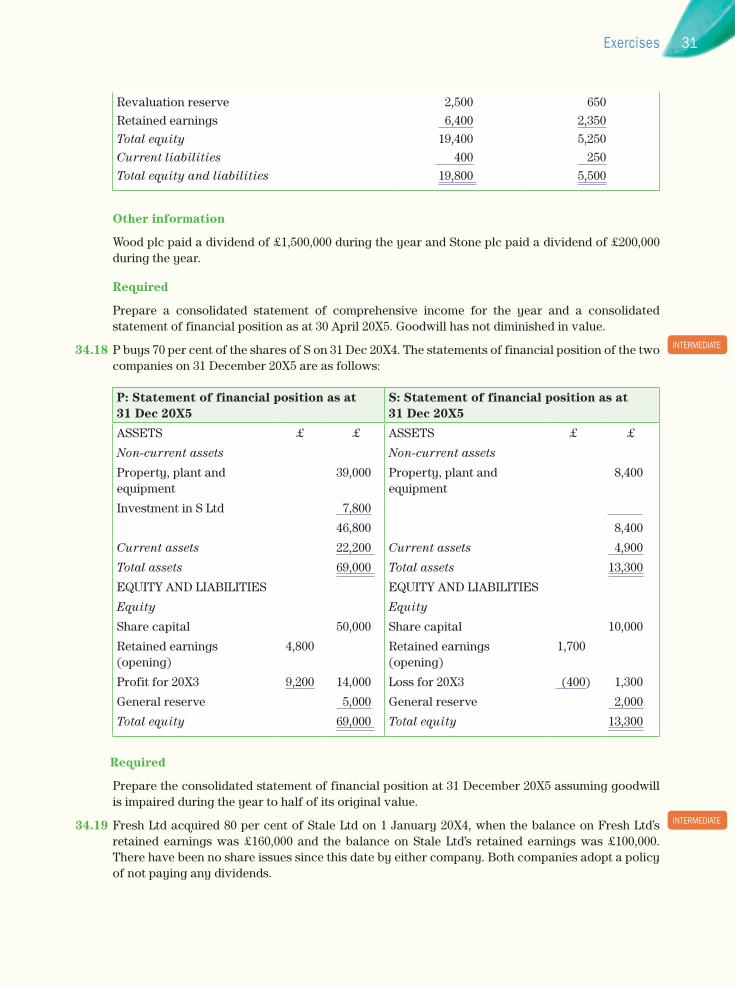

34.18 P buys 70 per cent of the shares of S on 31 Dec 20X4. The statements of financial position of the two companies on 31 December 20X5 are as follows:

P: Statement of financial position as at 31 Dec 20X5

S: Statement of financial position as at 31 Dec 20X5

ASSETS £ £ ASSETS £ £

Non-current assets Non-current assets

Property, plant and equipment

39,000 Property, plant and equipment

8,400

Investment in S Ltd 7,800

46,800 8,400

Current assets 22,200 Current assets 4,900

Total assets 69,000 Total assets 13,300

EQUITY AND LIABILITIES EQUITY AND LIABILITIES

Equity Equity

Share capital 50,000 Share capital 10,000

Retained earnings (opening)

4,800 Retained earnings (opening)

1,700

Profit for 20X3 9,200 14,000 Loss for 20X3 (400) 1,300

General reserve 5,000 General reserve 2,000

Total equity 69,000 Total equity 13,300

Required

Prepare the consolidated statement of financial position at 31 December 20X5 assuming goodwill is impaired during the year to half of its original value.

34.19 Fresh Ltd acquired 80 per cent of Stale Ltd on 1 January 20X4, when the balance on Fresh Ltd’s retained earnings was £160,000 and the balance on Stale Ltd’s retained earnings was £100,000. There have been no share issues since this date by either company. Both companies adopt a policy of not paying any dividends.

INterMeDIAte

INterMeDIAte

31exercises

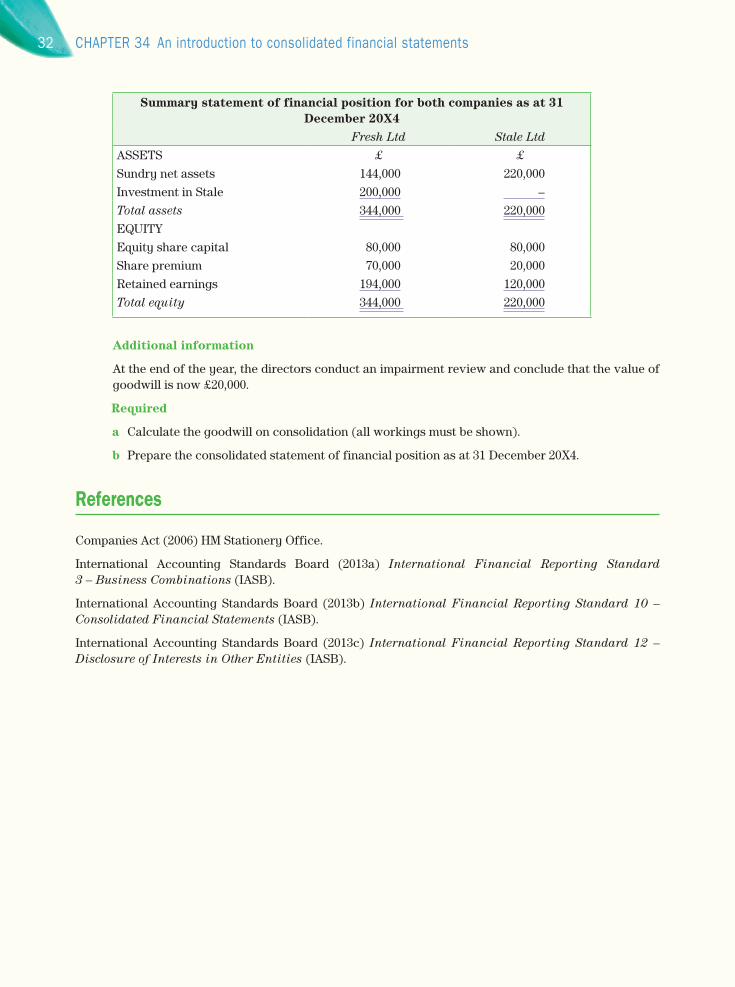

Summary statement of financial position for both companies as at 31 December 20X4

Fresh Ltd Stale LtdASSETS £ £Sundry net assets 144,000 220,000Investment in Stale 200,000 –Total assets 344,000 220,000EQUITYEquity share capital 80,000 80,000Share premium 70,000 20,000Retained earnings 194,000 120,000Total equity 344,000 220,000

Additional information

At the end of the year, the directors conduct an impairment review and conclude that the value of goodwill is now £20,000.

Required

a Calculate the goodwill on consolidation (all workings must be shown).

b Prepare the consolidated statement of financial position as at 31 December 20X4.

References

Companies Act (2006) HM Stationery Office.

International Accounting Standards Board (2013a) International Financial Reporting Standard 3 – Business Combinations (IASB).

International Accounting Standards Board (2013b) International Financial Reporting Standard 10 – Consolidated Financial Statements (IASB).

International Accounting Standards Board (2013c) International Financial Reporting Standard 12 – Disclosure of Interests in Other Entities (IASB).

32 ChApter 34 An introduction to consolidated financial statements