Embed Size (px)

Citation preview

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Conclusions

An introduction to stock-flow consistent modelsin macroeconomics

M. R. Grasselli

Mathematics and Statistics - McMaster University

Masterclasses on New Approachesto Economic Challenges

OECD-NAEC, April 17, 2019

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Conclusions

1 Introduction

2 Discrete-time SFC modelsBenchmark model

3 Continuous-time SFC modelsGoodwin modelKeen model

4 ExtensionsStabilizing governmentSpeculationStock PricesGreat ModerationEffective Demand and Inventories

5 Conclusions

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Conclusions

Stock-Flow Consistent models

Stock-flow consistent models emerged in the last decadeas a common language for many heterodox schools ofthought in economics.

They consider both real and monetary factorssimultaneously.

Specify the balance sheet and transactions betweensectors.

Accommodate a number of behavioural assumptions in away that is consistent with the underlying accountingstructure.

Reject the RARE individual (representative agent withrational expectations) in favour of SAFE (sectoral averagewith flexible expectations) modelling.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Conclusions

Stock-Flow Consistent models

Stock-flow consistent models emerged in the last decadeas a common language for many heterodox schools ofthought in economics.

They consider both real and monetary factorssimultaneously.

Specify the balance sheet and transactions betweensectors.

Accommodate a number of behavioural assumptions in away that is consistent with the underlying accountingstructure.

Reject the RARE individual (representative agent withrational expectations) in favour of SAFE (sectoral averagewith flexible expectations) modelling.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Conclusions

Stock-Flow Consistent models

Stock-flow consistent models emerged in the last decadeas a common language for many heterodox schools ofthought in economics.

They consider both real and monetary factorssimultaneously.

Specify the balance sheet and transactions betweensectors.

Accommodate a number of behavioural assumptions in away that is consistent with the underlying accountingstructure.

Reject the RARE individual (representative agent withrational expectations) in favour of SAFE (sectoral averagewith flexible expectations) modelling.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Conclusions

Stock-Flow Consistent models

Stock-flow consistent models emerged in the last decadeas a common language for many heterodox schools ofthought in economics.

They consider both real and monetary factorssimultaneously.

Specify the balance sheet and transactions betweensectors.

Accommodate a number of behavioural assumptions in away that is consistent with the underlying accountingstructure.

Reject the RARE individual (representative agent withrational expectations) in favour of SAFE (sectoral averagewith flexible expectations) modelling.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Conclusions

Stock-Flow Consistent models

Stock-flow consistent models emerged in the last decadeas a common language for many heterodox schools ofthought in economics.

They consider both real and monetary factorssimultaneously.

Specify the balance sheet and transactions betweensectors.

Accommodate a number of behavioural assumptions in away that is consistent with the underlying accountingstructure.

Reject the RARE individual (representative agent withrational expectations) in favour of SAFE (sectoral averagewith flexible expectations) modelling.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Conclusions

Heterodox insight 1: money is not neutral

Money is hierarchical: currency is a promise to pay gold(or settle taxes); deposits are promises to pay currency;securities are promises to pay deposits.

Financial institutions are market-makers straddling twolevels in the hierarchy: central banks, banks, securitydealers.

The hierarchy is dynamic: discipline and elasticity changein time.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Conclusions

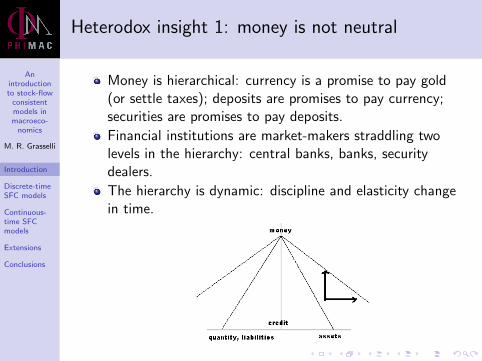

Heterodox insight 1: money is not neutral

Money is hierarchical: currency is a promise to pay gold(or settle taxes); deposits are promises to pay currency;securities are promises to pay deposits.

Financial institutions are market-makers straddling twolevels in the hierarchy: central banks, banks, securitydealers.

The hierarchy is dynamic: discipline and elasticity changein time.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Conclusions

Heterodox insight 1: money is not neutral

Money is hierarchical: currency is a promise to pay gold(or settle taxes); deposits are promises to pay currency;securities are promises to pay deposits.

Financial institutions are market-makers straddling twolevels in the hierarchy: central banks, banks, securitydealers.

The hierarchy is dynamic: discipline and elasticity changein time.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Conclusions

Heterodox insight 2: money is endogenous

Banks create money and purchasing power.

Reserve requirements are never binding.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Conclusions

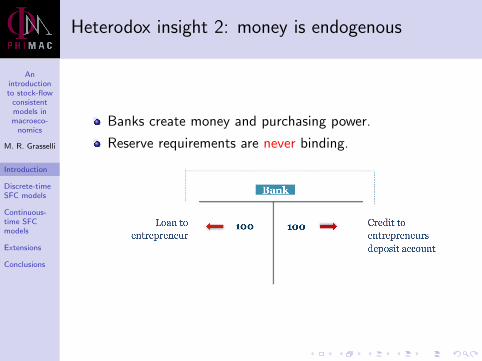

Heterodox insight 2: money is endogenous

Banks create money and purchasing power.

Reserve requirements are never binding.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Conclusions

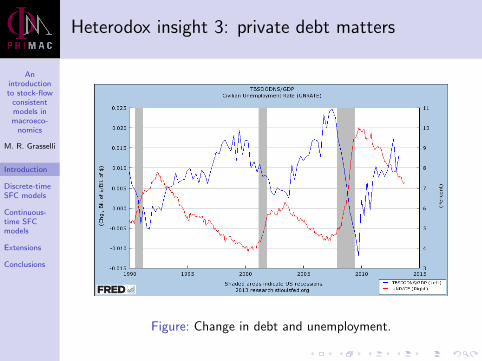

Heterodox insight 3: private debt matters

Figure: Change in debt and unemployment.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Conclusions

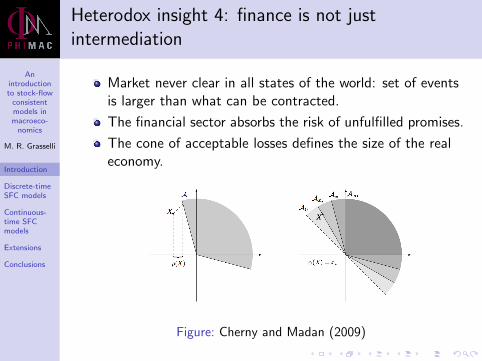

Heterodox insight 4: finance is not justintermediation

Market never clear in all states of the world: set of eventsis larger than what can be contracted.

The financial sector absorbs the risk of unfulfilled promises.

The cone of acceptable losses defines the size of the realeconomy.

Figure: Cherny and Madan (2009)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Conclusions

Heterodox insight 4: finance is not justintermediation

Market never clear in all states of the world: set of eventsis larger than what can be contracted.

The financial sector absorbs the risk of unfulfilled promises.

The cone of acceptable losses defines the size of the realeconomy.

Figure: Cherny and Madan (2009)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Conclusions

Heterodox insight 4: finance is not justintermediation

Market never clear in all states of the world: set of eventsis larger than what can be contracted.

The financial sector absorbs the risk of unfulfilled promises.

The cone of acceptable losses defines the size of the realeconomy.

Figure: Cherny and Madan (2009)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Benchmarkmodel

Continuous-time SFCmodels

Extensions

Conclusions

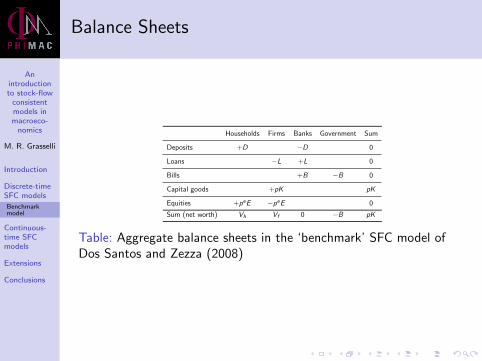

Balance Sheets

Households Firms Banks Government Sum

Deposits +D −D 0

Loans −L +L 0

Bills +B −B 0

Capital goods +pK pK

Equities +peE −peE 0

Sum (net worth) Vh Vf 0 −B pK

Table: Aggregate balance sheets in the ‘benchmark’ SFC model ofDos Santos and Zezza (2008)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Benchmarkmodel

Continuous-time SFCmodels

Extensions

Conclusions

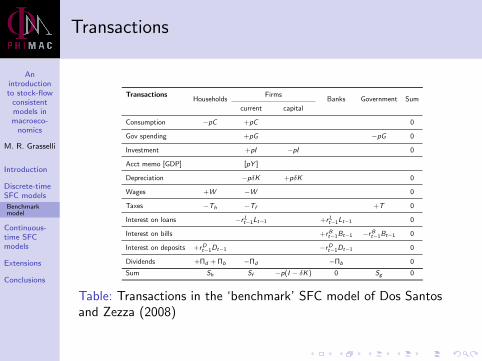

Transactions

TransactionsHouseholds

FirmsBanks Government Sum

current capital

Consumption −pC +pC 0

Gov spending +pG −pG 0

Investment +pI −pI 0

Acct memo [GDP] [pY ]

Depreciation −pδK +pδK 0

Wages +W −W 0

Taxes −Th −Tf +T 0

Interest on loans −rLt−1Lt−1 +rLt−1Lt−1 0

Interest on bills +rBt−1Bt−1 −rBt−1Bt−1 0

Interest on deposits +rDt−1Dt−1 −rDt−1Dt−1 0

Dividends +Πd + Πb −Πd −Πb 0

Sum Sh Sf −p(I − δK ) 0 Sg 0

Table: Transactions in the ‘benchmark’ SFC model of Dos Santosand Zezza (2008)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Benchmarkmodel

Continuous-time SFCmodels

Extensions

Conclusions

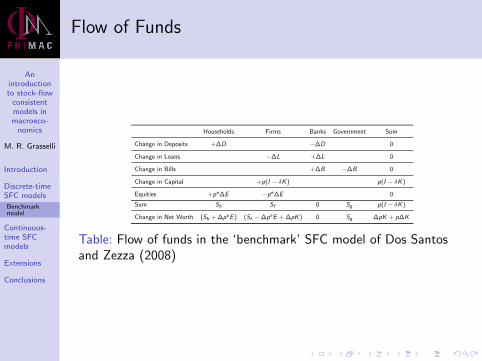

Flow of Funds

Households Firms Banks Government Sum

Change in Deposits +∆D −∆D 0

Change in Loans −∆L +∆L 0

Change in Bills +∆B −∆B 0

Change in Capital +p(I − δK ) p(I − δK )

Equities +pe∆E −pe∆E 0

Sum Sh Sf 0 Sg p(I − δK )

Change in Net Worth (Sh + ∆peE ) (Sf −∆peE + ∆pK ) 0 Sg ∆pK + p∆K

Table: Flow of funds in the ‘benchmark’ SFC model of Dos Santosand Zezza (2008)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Benchmarkmodel

Continuous-time SFCmodels

Extensions

Conclusions

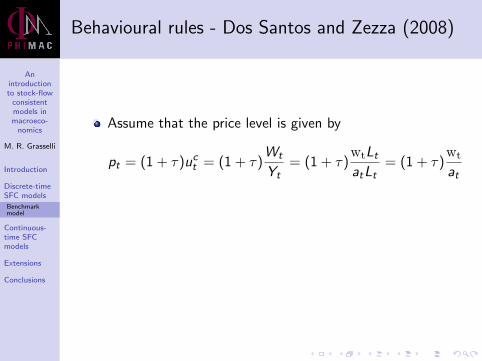

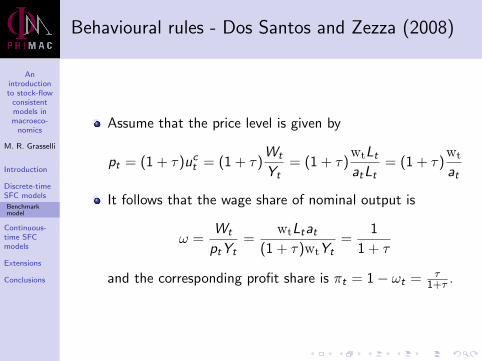

Behavioural rules - Dos Santos and Zezza (2008)

Assume that the price level is given by

pt = (1 + τ)uct = (1 + τ)Wt

Yt= (1 + τ)

wtLtatLt

= (1 + τ)wt

at

It follows that the wage share of nominal output is

ω =Wt

ptYt=

wtLtat(1 + τ)wtYt

=1

1 + τ

and the corresponding profit share is πt = 1− ωt = τ1+τ .

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Benchmarkmodel

Continuous-time SFCmodels

Extensions

Conclusions

Behavioural rules - Dos Santos and Zezza (2008)

Assume that the price level is given by

pt = (1 + τ)uct = (1 + τ)Wt

Yt= (1 + τ)

wtLtatLt

= (1 + τ)wt

at

It follows that the wage share of nominal output is

ω =Wt

ptYt=

wtLtat(1 + τ)wtYt

=1

1 + τ

and the corresponding profit share is πt = 1− ωt = τ1+τ .

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Benchmarkmodel

Continuous-time SFCmodels

Extensions

Conclusions

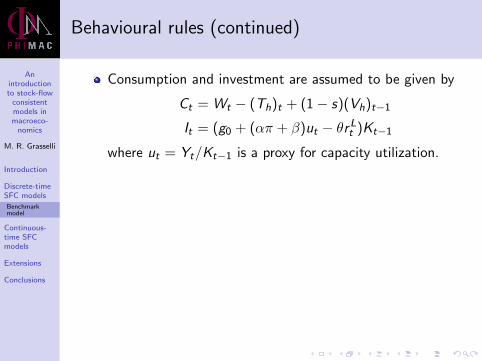

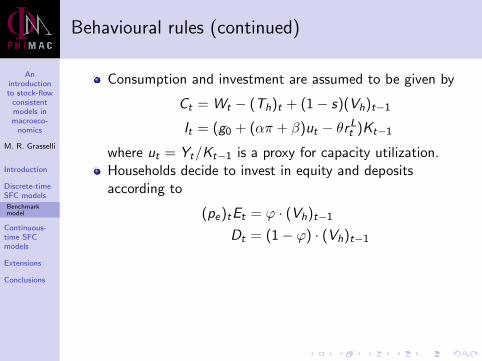

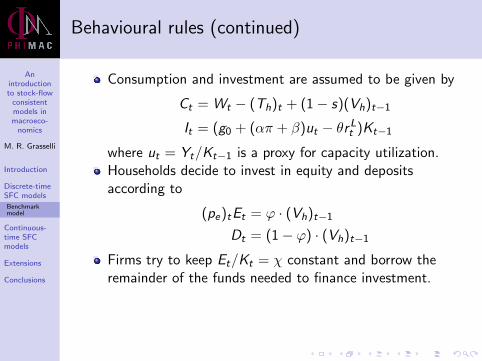

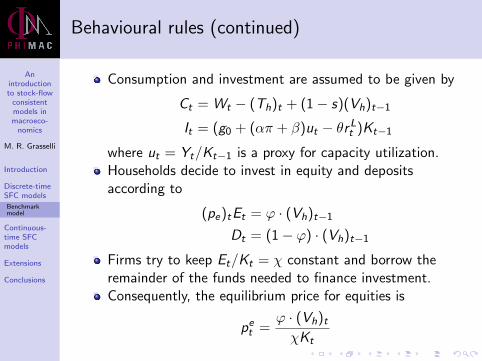

Behavioural rules (continued)

Consumption and investment are assumed to be given by

Ct = Wt − (Th)t + (1− s)(Vh)t−1

It = (g0 + (απ + β)ut − θrLt )Kt−1

where ut = Yt/Kt−1 is a proxy for capacity utilization.

Households decide to invest in equity and depositsaccording to

(pe)tEt = ϕ · (Vh)t−1

Dt = (1− ϕ) · (Vh)t−1

Firms try to keep Et/Kt = χ constant and borrow theremainder of the funds needed to finance investment.Consequently, the equilibrium price for equities is

pet =ϕ · (Vh)tχKt

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Benchmarkmodel

Continuous-time SFCmodels

Extensions

Conclusions

Behavioural rules (continued)

Consumption and investment are assumed to be given by

Ct = Wt − (Th)t + (1− s)(Vh)t−1

It = (g0 + (απ + β)ut − θrLt )Kt−1

where ut = Yt/Kt−1 is a proxy for capacity utilization.Households decide to invest in equity and depositsaccording to

(pe)tEt = ϕ · (Vh)t−1

Dt = (1− ϕ) · (Vh)t−1

Firms try to keep Et/Kt = χ constant and borrow theremainder of the funds needed to finance investment.Consequently, the equilibrium price for equities is

pet =ϕ · (Vh)tχKt

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Benchmarkmodel

Continuous-time SFCmodels

Extensions

Conclusions

Behavioural rules (continued)

Consumption and investment are assumed to be given by

Ct = Wt − (Th)t + (1− s)(Vh)t−1

It = (g0 + (απ + β)ut − θrLt )Kt−1

where ut = Yt/Kt−1 is a proxy for capacity utilization.Households decide to invest in equity and depositsaccording to

(pe)tEt = ϕ · (Vh)t−1

Dt = (1− ϕ) · (Vh)t−1

Firms try to keep Et/Kt = χ constant and borrow theremainder of the funds needed to finance investment.

Consequently, the equilibrium price for equities is

pet =ϕ · (Vh)tχKt

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Benchmarkmodel

Continuous-time SFCmodels

Extensions

Conclusions

Behavioural rules (continued)

Consumption and investment are assumed to be given by

Ct = Wt − (Th)t + (1− s)(Vh)t−1

It = (g0 + (απ + β)ut − θrLt )Kt−1

where ut = Yt/Kt−1 is a proxy for capacity utilization.Households decide to invest in equity and depositsaccording to

(pe)tEt = ϕ · (Vh)t−1

Dt = (1− ϕ) · (Vh)t−1

Firms try to keep Et/Kt = χ constant and borrow theremainder of the funds needed to finance investment.Consequently, the equilibrium price for equities is

pet =ϕ · (Vh)tχKt

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Benchmarkmodel

Continuous-time SFCmodels

Extensions

Conclusions

Behavioural rules (continued)

Banks are assumed to meet the demand for loans by firmsand deposits by households.

In addition, banks set the interest rate on deposits as equalto the interest rate on government bills and the interestrate on loans as a fixed on markup on the rate on deposits.

The government chooses the level of spending Gt , theinterest rate rbt and the level of taxes Tt , with the amountof debt determined as a residual.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Benchmarkmodel

Continuous-time SFCmodels

Extensions

Conclusions

Behavioural rules (continued)

Banks are assumed to meet the demand for loans by firmsand deposits by households.

In addition, banks set the interest rate on deposits as equalto the interest rate on government bills and the interestrate on loans as a fixed on markup on the rate on deposits.

The government chooses the level of spending Gt , theinterest rate rbt and the level of taxes Tt , with the amountof debt determined as a residual.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Benchmarkmodel

Continuous-time SFCmodels

Extensions

Conclusions

Behavioural rules (continued)

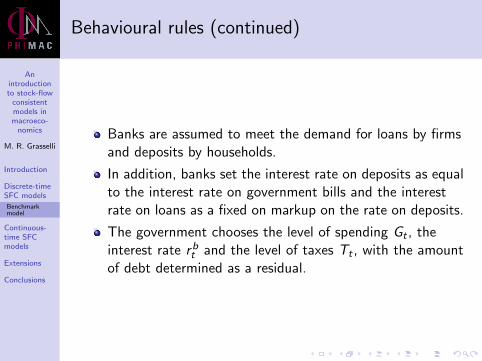

Banks are assumed to meet the demand for loans by firmsand deposits by households.

In addition, banks set the interest rate on deposits as equalto the interest rate on government bills and the interestrate on loans as a fixed on markup on the rate on deposits.

The government chooses the level of spending Gt , theinterest rate rbt and the level of taxes Tt , with the amountof debt determined as a residual.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Benchmarkmodel

Continuous-time SFCmodels

Extensions

Conclusions

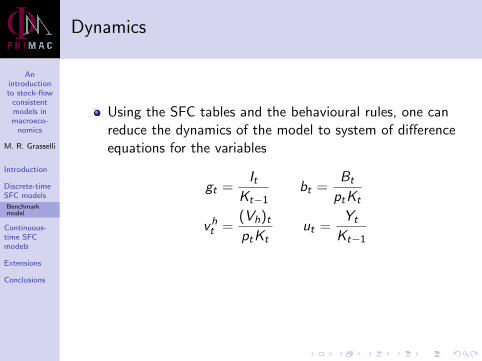

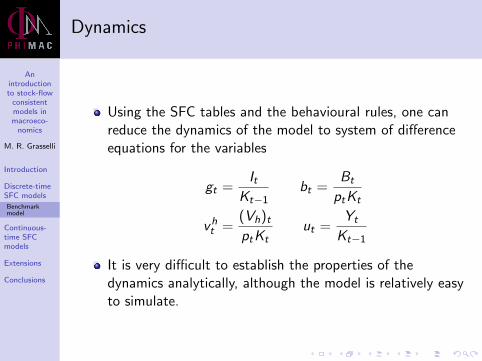

Dynamics

Using the SFC tables and the behavioural rules, one canreduce the dynamics of the model to system of differenceequations for the variables

gt =It

Kt−1bt =

Bt

ptKt

vht =(Vh)tptKt

ut =Yt

Kt−1

It is very difficult to establish the properties of thedynamics analytically, although the model is relatively easyto simulate.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Benchmarkmodel

Continuous-time SFCmodels

Extensions

Conclusions

Dynamics

Using the SFC tables and the behavioural rules, one canreduce the dynamics of the model to system of differenceequations for the variables

gt =It

Kt−1bt =

Bt

ptKt

vht =(Vh)tptKt

ut =Yt

Kt−1

It is very difficult to establish the properties of thedynamics analytically, although the model is relatively easyto simulate.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

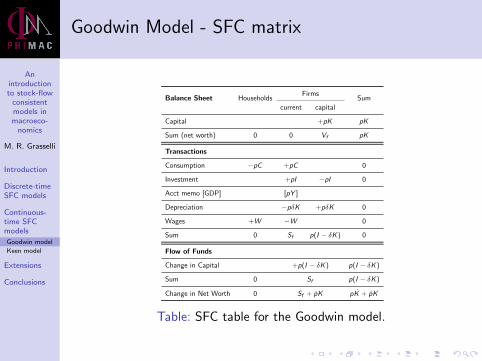

Goodwin Model - SFC matrix

Balance Sheet HouseholdsFirms

Sum

current capital

Capital +pK pK

Sum (net worth) 0 0 Vf pK

Transactions

Consumption −pC +pC 0

Investment +pI −pI 0

Acct memo [GDP] [pY ]

Depreciation −pδK +pδK 0

Wages +W −W 0

Sum 0 Sf p(I − δK ) 0

Flow of Funds

Change in Capital +p(I − δK ) p(I − δK )

Sum 0 Sf p(I − δK )

Change in Net Worth 0 Sf + pK pK + pK

Table: SFC table for the Goodwin model.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

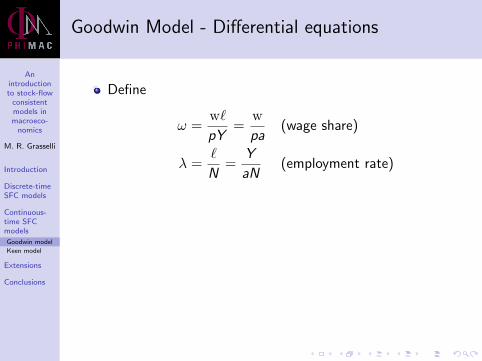

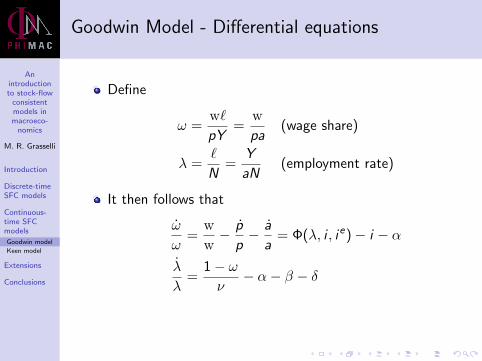

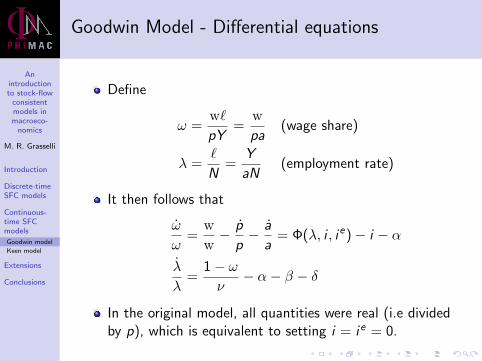

Goodwin Model - Differential equations

Define

ω =w`

pY=

w

pa(wage share)

λ =`

N=

Y

aN(employment rate)

It then follows that

ω

ω=

w

w− p

p− a

a= Φ(λ, i , ie)− i − α

λ

λ=

1− ων− α− β − δ

In the original model, all quantities were real (i.e dividedby p), which is equivalent to setting i = ie = 0.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

Goodwin Model - Differential equations

Define

ω =w`

pY=

w

pa(wage share)

λ =`

N=

Y

aN(employment rate)

It then follows that

ω

ω=

w

w− p

p− a

a= Φ(λ, i , ie)− i − α

λ

λ=

1− ων− α− β − δ

In the original model, all quantities were real (i.e dividedby p), which is equivalent to setting i = ie = 0.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

Goodwin Model - Differential equations

Define

ω =w`

pY=

w

pa(wage share)

λ =`

N=

Y

aN(employment rate)

It then follows that

ω

ω=

w

w− p

p− a

a= Φ(λ, i , ie)− i − α

λ

λ=

1− ων− α− β − δ

In the original model, all quantities were real (i.e dividedby p), which is equivalent to setting i = ie = 0.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

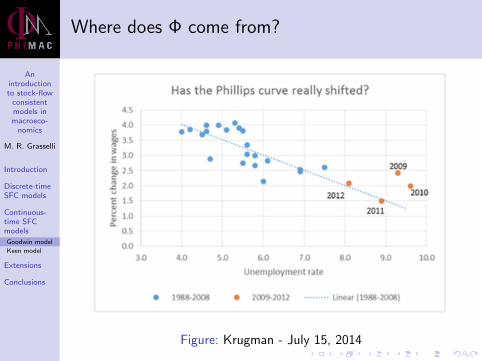

Where does Φ come from?

Figure: Krugman - July 15, 2014

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

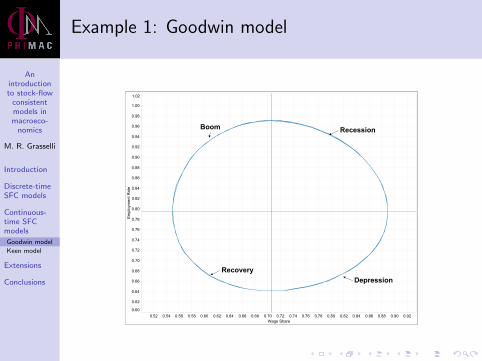

Example 1: Goodwin model

0.52 0.54 0.56 0.58 0.60 0.62 0.64 0.66 0.68 0.70 0.72 0.74 0.76 0.78 0.80 0.82 0.84 0.86 0.88 0.90 0.92Wage Share

0.60

0.62

0.64

0.66

0.68

0.70

0.72

0.74

0.76

0.78

0.80

0.82

0.84

0.86

0.88

0.90

0.92

0.94

0.96

0.98

1.00

1.02

Employment Rate

Boom Recession

DepressionRecovery

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

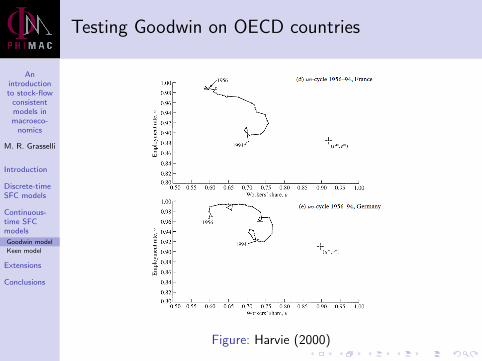

Testing Goodwin on OECD countries

Figure: Harvie (2000)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

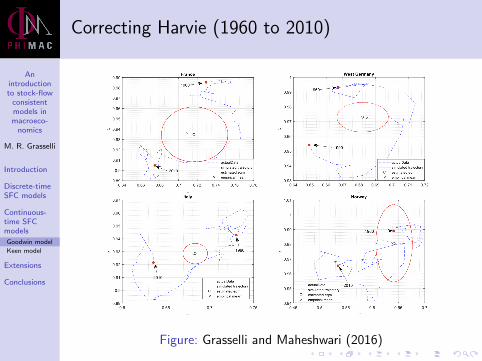

Correcting Harvie (1960 to 2010)

Figure: Grasselli and Maheshwari (2016)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

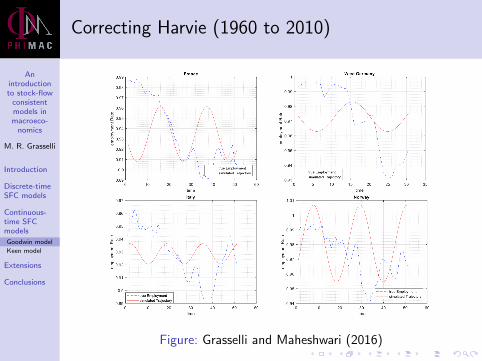

Correcting Harvie (1960 to 2010)

Figure: Grasselli and Maheshwari (2016)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

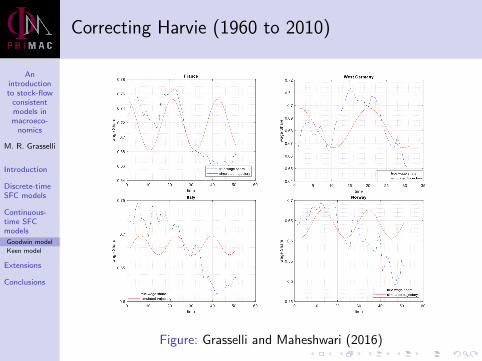

Correcting Harvie (1960 to 2010)

Figure: Grasselli and Maheshwari (2016)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

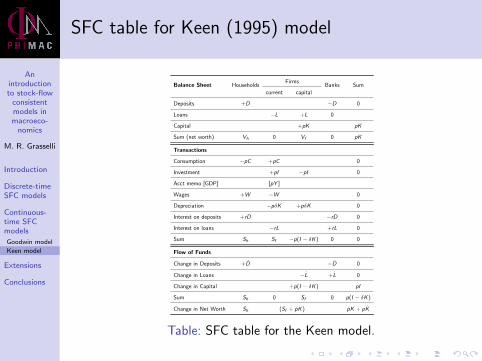

SFC table for Keen (1995) model

Balance Sheet HouseholdsFirms

Banks Sum

current capital

Deposits +D −D 0

Loans −L +L 0

Capital +pK pK

Sum (net worth) Vh 0 Vf 0 pK

Transactions

Consumption −pC +pC 0

Investment +pI −pI 0

Acct memo [GDP] [pY ]

Wages +W −W 0

Depreciation −pδK +pδK 0

Interest on deposits +rD −rD 0

Interest on loans −rL +rL 0

Sum Sh Sf −p(I − δK ) 0 0

Flow of Funds

Change in Deposits +D −D 0

Change in Loans −L +L 0

Change in Capital +p(I − δK ) pI

Sum Sh 0 Sf 0 p(I − δK )

Change in Net Worth Sh (Sf + pK ) pK + pK

Table: SFC table for the Keen model.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

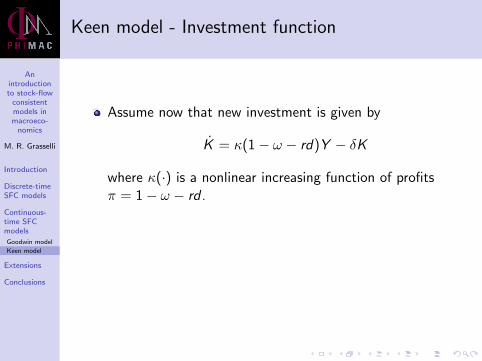

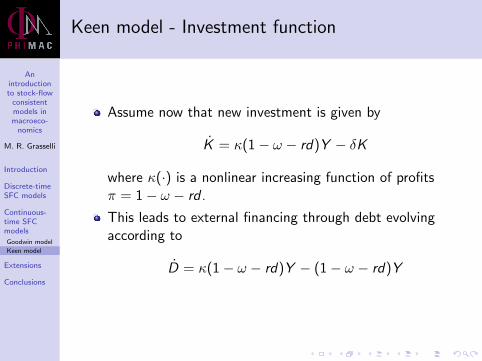

Keen model - Investment function

Assume now that new investment is given by

K = κ(1− ω − rd)Y − δK

where κ(·) is a nonlinear increasing function of profitsπ = 1− ω − rd .

This leads to external financing through debt evolvingaccording to

D = κ(1− ω − rd)Y − (1− ω − rd)Y

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

Keen model - Investment function

Assume now that new investment is given by

K = κ(1− ω − rd)Y − δK

where κ(·) is a nonlinear increasing function of profitsπ = 1− ω − rd .

This leads to external financing through debt evolvingaccording to

D = κ(1− ω − rd)Y − (1− ω − rd)Y

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

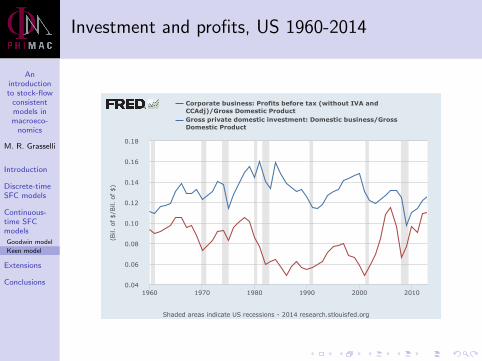

Investment and profits, US 1960-2014

0.04

0.06

0.08

0.10

0.12

0.14

0.16

0.18

1960 1970 1980 1990 2000 2010

ShadedareasindicateUSrecessions-2014research.stlouisfed.org

Corporatebusiness:Profitsbeforetax(withoutIVAandCCAdj)/GrossDomesticProductGrossprivatedomesticinvestment:Domesticbusiness/GrossDomesticProduct

(Bil.

of$/B

il.o

f$)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

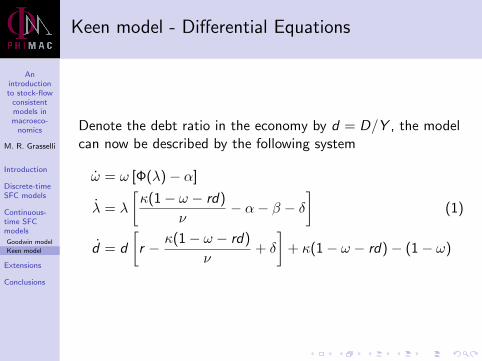

Keen model - Differential Equations

Denote the debt ratio in the economy by d = D/Y , the modelcan now be described by the following system

ω = ω [Φ(λ)− α]

λ = λ

[κ(1− ω − rd)

ν− α− β − δ

](1)

d = d

[r − κ(1− ω − rd)

ν+ δ

]+ κ(1− ω − rd)− (1− ω)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

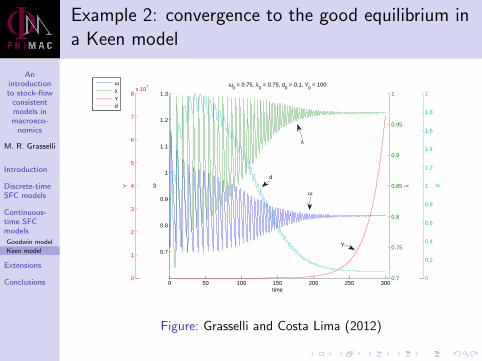

Example 2: convergence to the good equilibrium ina Keen model

0.7

0.75

0.8

0.85

0.9

0.95

1

λ

ωλYd

0

1

2

3

4

5

6

7

8x 10

7

Y

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

d

0 50 100 150 200 250 300

0.7

0.8

0.9

1

1.1

1.2

1.3

time

ω

ω0 = 0.75, λ

0 = 0.75, d

0 = 0.1, Y

0 = 100

d

λ

ω

Y

Figure: Grasselli and Costa Lima (2012)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

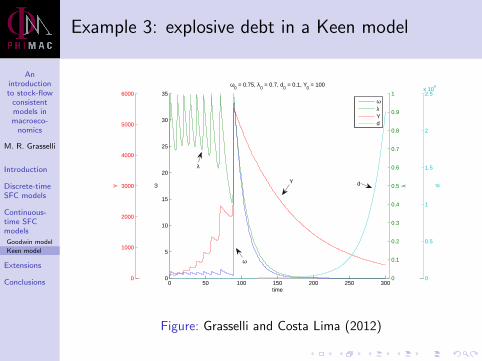

Example 3: explosive debt in a Keen model

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

λ

0

1000

2000

3000

4000

5000

6000

Y

0

0.5

1

1.5

2

2.5x 10

6

d

0 50 100 150 200 250 3000

5

10

15

20

25

30

35

time

ω

ω0 = 0.75, λ

0 = 0.7, d

0 = 0.1, Y

0 = 100

ωλYd

λ

Y d

ω

Figure: Grasselli and Costa Lima (2012)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

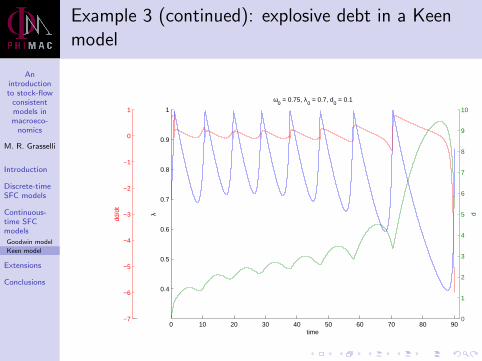

Example 3 (continued): explosive debt in a Keenmodel

0

1

2

3

4

5

6

7

8

9

10

d

−7

−6

−5

−4

−3

−2

−1

0

1dd

/dt

0 10 20 30 40 50 60 70 80 90

0.4

0.5

0.6

0.7

0.8

0.9

1

time

λ

ω0 = 0.75, λ

0 = 0.7, d

0 = 0.1

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

Corporate Debt share in the US 1950-2014

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1950 1960 1970 1980 1990 2000 2010

ShadedareasindicateUSrecessions-2014research.stlouisfed.org

NonfinancialBusiness;CreditMarketInstruments;Liability,Level/GrossDomesticProduct

(Bil.of$/Bil.of$)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

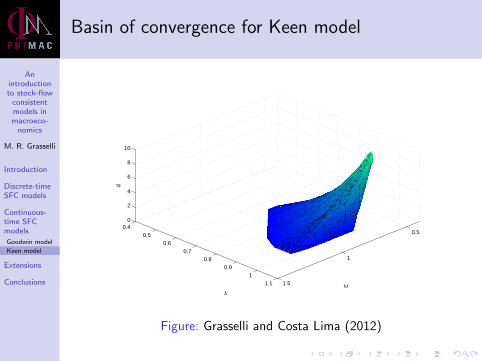

Basin of convergence for Keen model

0.5

1

1.5

0.40.5

0.60.7

0.80.9

11.1

0

2

4

6

8

10

ωλ

d

Figure: Grasselli and Costa Lima (2012)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

Keen model with inflation- equilibria

Apart from the interior equilibrium (ω1, λ1, d1) and theexplosive equilibria of the form (ω2, λ2, d2) = (0, 0,±∞),the system has a new undesirable equilibrium of the form(ω3, 0, b3) where

ω3 =1

ξ+

Φ(0)− αξηp(1− γ)

and b3 solves the nonlinear equation

b [i(ω3) + g(1− ω3 − rb)− r ] = κ(1−ω3− rb)− 1 +ω3 .

Notice that

i(ω1) =Φ(λ1)− α

1− γ>

Φ(0)− α1− γ

= i(ω3) ,

so that this type of equilibrium is necessarily deflationary.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

Keen model with inflation- equilibria

Apart from the interior equilibrium (ω1, λ1, d1) and theexplosive equilibria of the form (ω2, λ2, d2) = (0, 0,±∞),the system has a new undesirable equilibrium of the form(ω3, 0, b3) where

ω3 =1

ξ+

Φ(0)− αξηp(1− γ)

and b3 solves the nonlinear equation

b [i(ω3) + g(1− ω3 − rb)− r ] = κ(1−ω3− rb)− 1 +ω3 .

Notice that

i(ω1) =Φ(λ1)− α

1− γ>

Φ(0)− α1− γ

= i(ω3) ,

so that this type of equilibrium is necessarily deflationary.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

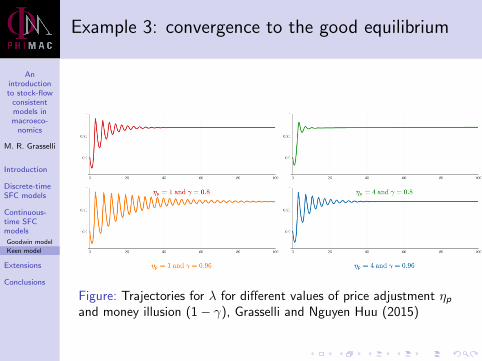

Example 3: convergence to the good equilibrium

Figure: Trajectories for λ for different values of price adjustment ηpand money illusion (1− γ), Grasselli and Nguyen Huu (2015)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

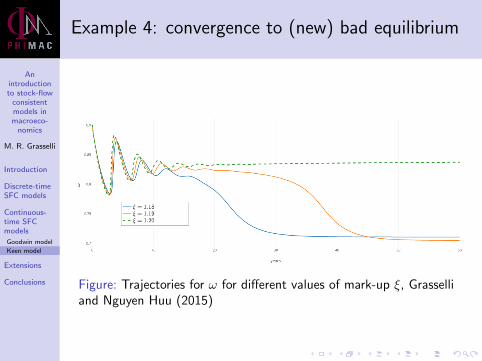

Example 4: convergence to (new) bad equilibrium

Figure: Trajectories for ω for different values of mark-up ξ, Grasselliand Nguyen Huu (2015)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Goodwin model

Keen model

Extensions

Conclusions

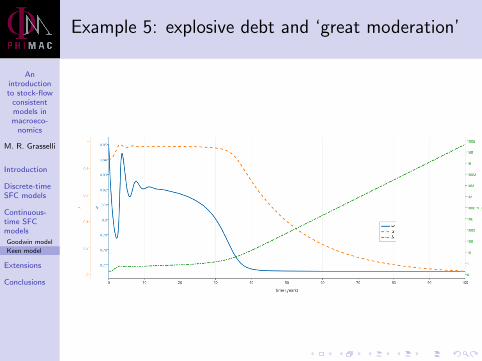

Example 5: explosive debt and ‘great moderation’

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

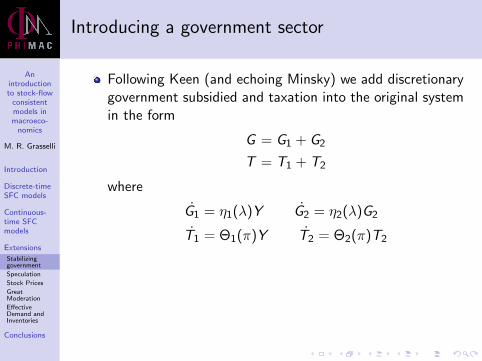

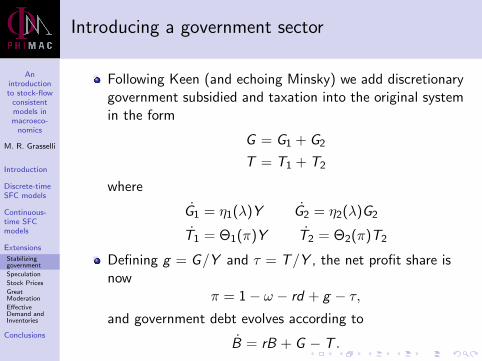

Introducing a government sector

Following Keen (and echoing Minsky) we add discretionarygovernment subsidied and taxation into the original systemin the form

G = G1 + G2

T = T1 + T2

where

G1 = η1(λ)Y G2 = η2(λ)G2

T1 = Θ1(π)Y T2 = Θ2(π)T2

Defining g = G/Y and τ = T/Y , the net profit share isnow

π = 1− ω − rd + g − τ,and government debt evolves according to

B = rB + G − T .

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Introducing a government sector

Following Keen (and echoing Minsky) we add discretionarygovernment subsidied and taxation into the original systemin the form

G = G1 + G2

T = T1 + T2

where

G1 = η1(λ)Y G2 = η2(λ)G2

T1 = Θ1(π)Y T2 = Θ2(π)T2

Defining g = G/Y and τ = T/Y , the net profit share isnow

π = 1− ω − rd + g − τ,and government debt evolves according to

B = rB + G − T .

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

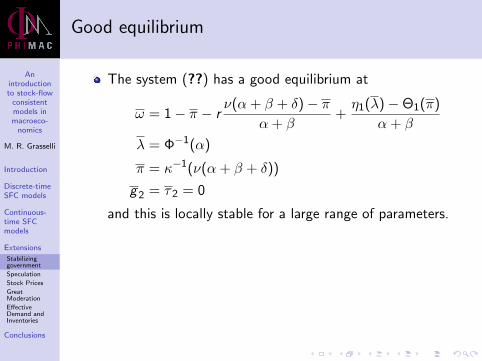

Good equilibrium

The system (??) has a good equilibrium at

ω = 1− π − rν(α + β + δ)− π

α + β+η1(λ)−Θ1(π)

α + β

λ = Φ−1(α)

π = κ−1(ν(α + β + δ))

g2 = τ2 = 0

and this is locally stable for a large range of parameters.

The other variables then converge exponentially fast to

d =ν(α + β + δ)− π

α + β

g1 =η1(λ)

α + β

τ1 =Θ1(π)

α + β

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

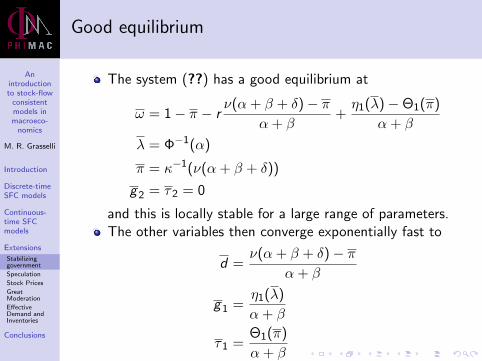

Good equilibrium

The system (??) has a good equilibrium at

ω = 1− π − rν(α + β + δ)− π

α + β+η1(λ)−Θ1(π)

α + β

λ = Φ−1(α)

π = κ−1(ν(α + β + δ))

g2 = τ2 = 0

and this is locally stable for a large range of parameters.The other variables then converge exponentially fast to

d =ν(α + β + δ)− π

α + β

g1 =η1(λ)

α + β

τ1 =Θ1(π)

α + β

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Bad equilibria - destabilizing a stable crisis

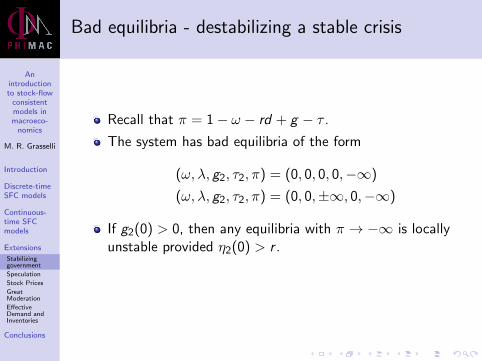

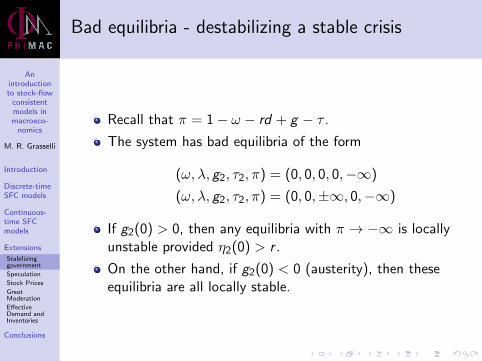

Recall that π = 1− ω − rd + g − τ .

The system has bad equilibria of the form

(ω, λ, g2, τ2, π) = (0, 0, 0, 0,−∞)

(ω, λ, g2, τ2, π) = (0, 0,±∞, 0,−∞)

If g2(0) > 0, then any equilibria with π → −∞ is locallyunstable provided η2(0) > r .

On the other hand, if g2(0) < 0 (austerity), then theseequilibria are all locally stable.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

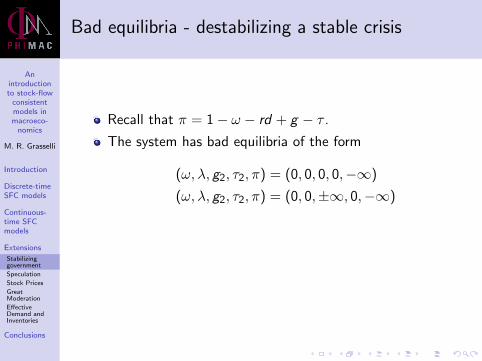

Bad equilibria - destabilizing a stable crisis

Recall that π = 1− ω − rd + g − τ .

The system has bad equilibria of the form

(ω, λ, g2, τ2, π) = (0, 0, 0, 0,−∞)

(ω, λ, g2, τ2, π) = (0, 0,±∞, 0,−∞)

If g2(0) > 0, then any equilibria with π → −∞ is locallyunstable provided η2(0) > r .

On the other hand, if g2(0) < 0 (austerity), then theseequilibria are all locally stable.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Bad equilibria - destabilizing a stable crisis

Recall that π = 1− ω − rd + g − τ .

The system has bad equilibria of the form

(ω, λ, g2, τ2, π) = (0, 0, 0, 0,−∞)

(ω, λ, g2, τ2, π) = (0, 0,±∞, 0,−∞)

If g2(0) > 0, then any equilibria with π → −∞ is locallyunstable provided η2(0) > r .

On the other hand, if g2(0) < 0 (austerity), then theseequilibria are all locally stable.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Bad equilibria - destabilizing a stable crisis

Recall that π = 1− ω − rd + g − τ .

The system has bad equilibria of the form

(ω, λ, g2, τ2, π) = (0, 0, 0, 0,−∞)

(ω, λ, g2, τ2, π) = (0, 0,±∞, 0,−∞)

If g2(0) > 0, then any equilibria with π → −∞ is locallyunstable provided η2(0) > r .

On the other hand, if g2(0) < 0 (austerity), then theseequilibria are all locally stable.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

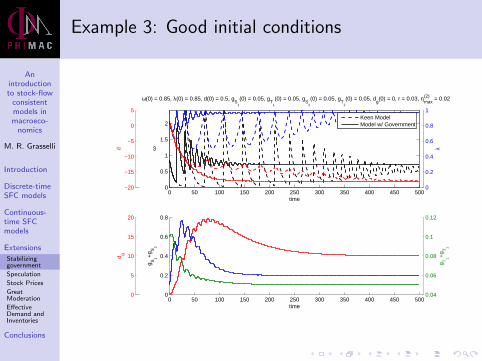

Example 3: Good initial conditions

0

0.2

0.4

0.6

0.8

1

λ

−20

−15

−10

−5

0

5d

0 50 100 150 200 250 300 350 400 450 5000

0.5

1

1.5

2

time

ω

ω(0) = 0.85, λ(0) = 0.85, d(0) = 0.5, gS

1

(0) = 0.05, gT

1

(0) = 0.05, gS

2

(0) = 0.05, gT

2

(0) = 0.05, dg(0) = 0, r = 0.03, η

max(2) = 0.02

Keen ModelModel w/ Government

0.04

0.06

0.08

0.1

0.12

g T1+

g T2

0

5

10

15

20

d g

0 50 100 150 200 250 300 350 400 450 5000

0.2

0.4

0.6

0.8

time

g S1+

g S2

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

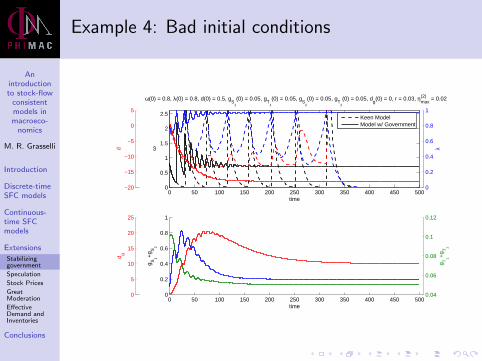

Example 4: Bad initial conditions

0

0.2

0.4

0.6

0.8

1

λ

−20

−15

−10

−5

0

5d

0 50 100 150 200 250 300 350 400 450 5000

0.5

1

1.5

2

2.5

time

ω

ω(0) = 0.8, λ(0) = 0.8, d(0) = 0.5, gS

1

(0) = 0.05, gT

1

(0) = 0.05, gS

2

(0) = 0.05, gT

2

(0) = 0.05, dg(0) = 0, r = 0.03, η

max(2) = 0.02

Keen ModelModel w/ Government

0.04

0.06

0.08

0.1

0.12

g T1+

g T2

0

5

10

15

20

25

d g

0 50 100 150 200 250 300 350 400 450 5000

0.2

0.4

0.6

0.8

1

time

g S1+

g S2

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

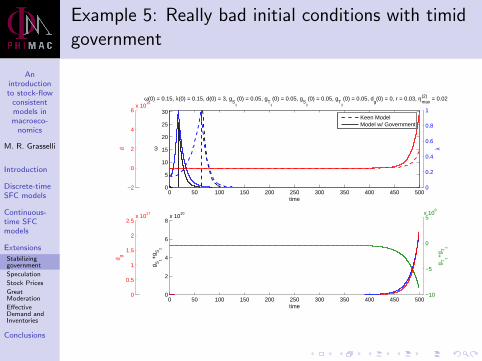

Example 5: Really bad initial conditions with timidgovernment

0

0.2

0.4

0.6

0.8

1

λ

−2

0

2

4

6x 10

16

d

0 50 100 150 200 250 300 350 400 450 5000

5

10

15

20

25

30

time

ω

ω(0) = 0.15, λ(0) = 0.15, d(0) = 3, gS

1

(0) = 0.05, gT

1

(0) = 0.05, gS

2

(0) = 0.05, gT

2

(0) = 0.05, dg(0) = 0, r = 0.03, η

max(2) = 0.02

Keen ModelModel w/ Government

−10

−5

0

5x 10

8

g T1+

g T2

0

0.5

1

1.5

2

2.5x 10

17

d g

0 50 100 150 200 250 300 350 400 450 5000

2

4

6

8x 10

10

time

g S1+

g S2

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

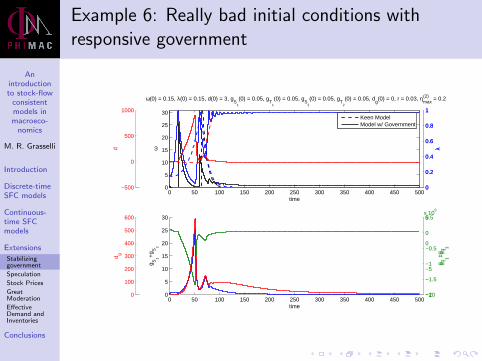

Example 6: Really bad initial conditions withresponsive government

0

0.2

0.4

0.6

0.8

1

λ

−10

−5

0

5x 10

8

g T1+

g T2

0

0.2

0.4

0.6

0.8

1

λ

−500

0

500

1000d

0 50 100 150 200 250 300 350 400 450 5000

5

10

15

20

25

30

time

ω

ω(0) = 0.15, λ(0) = 0.15, d(0) = 3, gS

1

(0) = 0.05, gT

1

(0) = 0.05, gS

2

(0) = 0.05, gT

2

(0) = 0.05, dg(0) = 0, r = 0.03, η

max(2) = 0.2

Keen ModelModel w/ Government

−2

−1.5

−1

−0.5

0

0.5

g T1+

g T2

0

100

200

300

400

500

600

d g

0 50 100 150 200 250 300 350 400 450 5000

5

10

15

20

25

30

time

g S1+

g S2

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

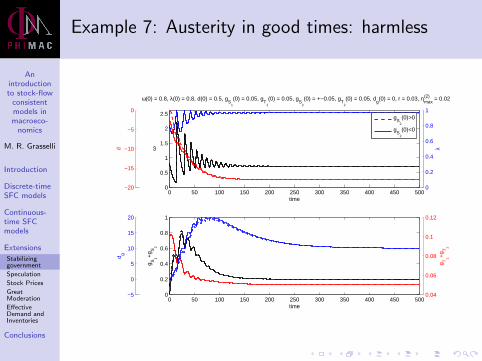

Example 7: Austerity in good times: harmless

0

0.2

0.4

0.6

0.8

1

λ

−20

−15

−10

−5

0d

0 50 100 150 200 250 300 350 400 450 5000

0.5

1

1.5

2

2.5

time

ω

ω(0) = 0.8, λ(0) = 0.8, d(0) = 0.5, gS

1

(0) = 0.05, gT

1

(0) = 0.05, gS

2

(0) = +−0.05, gT

2

(0) = 0.05, dg(0) = 0, r = 0.03, η

max(2) = 0.02

g

S2

(0)>0

gS

2

(0)<0

0.04

0.06

0.08

0.1

0.12

g T1+

g T2

−5

0

5

10

15

20

d g

0 50 100 150 200 250 300 350 400 450 5000

0.2

0.4

0.6

0.8

1

time

g S1+

g S2

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

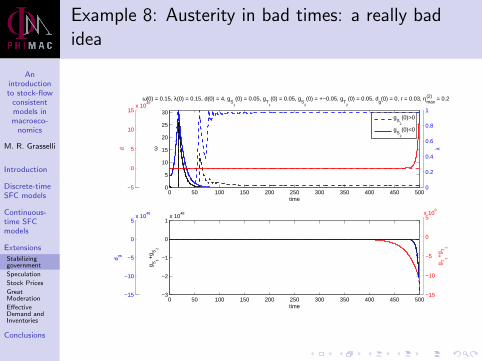

Example 8: Austerity in bad times: a really badidea

0

0.2

0.4

0.6

0.8

1

λ

−5

0

5

10

15x 10

48

d

0 50 100 150 200 250 300 350 400 450 5000

5

10

15

20

25

30

time

ω

ω(0) = 0.15, λ(0) = 0.15, d(0) = 4, gS

1

(0) = 0.05, gT

1

(0) = 0.05, gS

2

(0) = +−0.05, gT

2

(0) = 0.05, dg(0) = 0, r = 0.03, η

max(2) = 0.2

g

S2

(0)>0

gS

2

(0)<0

−15

−10

−5

0

5x 10

8

g T1+

g T2

−15

−10

−5

0

5x 10

48

d g

0 50 100 150 200 250 300 350 400 450 500−3

−2

−1

0

1x 10

48

time

g S1+

g S2

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

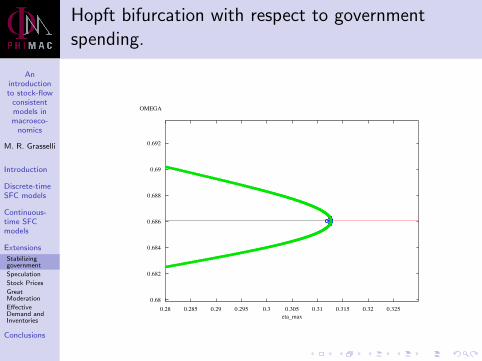

Hopft bifurcation with respect to governmentspending.

0.68

0.682

0.684

0.686

0.688

0.69

0.692

OMEGA

0.28 0.285 0.29 0.295 0.3 0.305 0.31 0.315 0.32 0.325eta_max

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Speculative flow

To introduce the destabilizing effect of purely speculativeinvestment, we consider a modified version of the previousmodel with

L = pI + rLL− κLL + F

Df = pY −W + rfDf − κLL + F

where F denotes a speculative flow modelled by

F = Ψ(g(π) + i(ω))pY ,

where Ψ() is an increasing function of the nominal growth ratein the economy. Notice that this still satisfies

L− Df = pI − Π.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

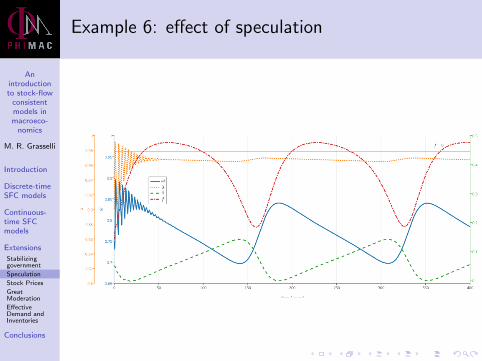

Example 6: effect of speculation

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

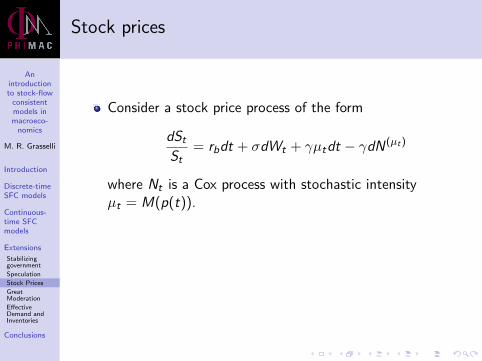

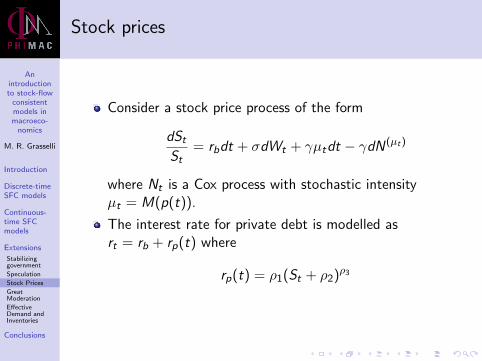

Stock prices

Consider a stock price process of the form

dStSt

= rbdt + σdWt + γµtdt − γdN(µt)

where Nt is a Cox process with stochastic intensityµt = M(p(t)).

The interest rate for private debt is modelled asrt = rb + rp(t) where

rp(t) = ρ1(St + ρ2)ρ3

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Stock prices

Consider a stock price process of the form

dStSt

= rbdt + σdWt + γµtdt − γdN(µt)

where Nt is a Cox process with stochastic intensityµt = M(p(t)).

The interest rate for private debt is modelled asrt = rb + rp(t) where

rp(t) = ρ1(St + ρ2)ρ3

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

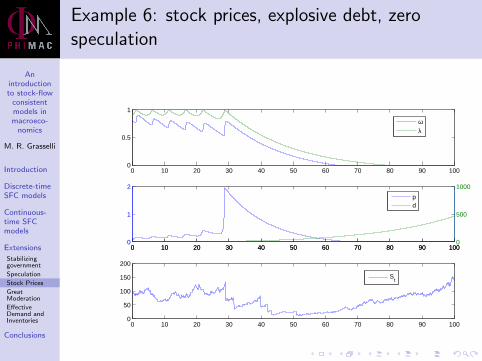

Example 6: stock prices, explosive debt, zerospeculation

0 10 20 30 40 50 60 70 80 90 1000

0.5

1

ωλ

0 10 20 30 40 50 60 70 80 90 1000

1

2

0 10 20 30 40 50 60 70 80 90 1000

500

1000

pd

0 10 20 30 40 50 60 70 80 90 1000

50

100

150

200

St

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

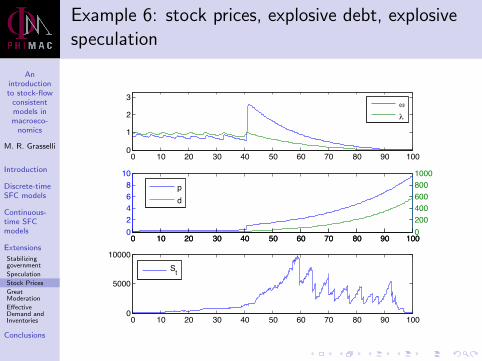

Example 6: stock prices, explosive debt, explosivespeculation

0 10 20 30 40 50 60 70 80 90 1000

1

2

3

ω

λ

0 10 20 30 40 50 60 70 80 90 10002468

10

0 10 20 30 40 50 60 70 80 90 10002004006008001000

pd

0 10 20 30 40 50 60 70 80 90 1000

5000

10000

St

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

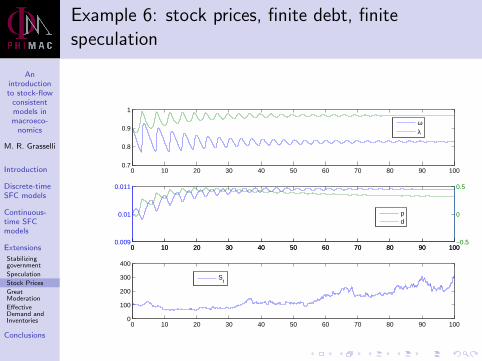

Example 6: stock prices, finite debt, finitespeculation

0 10 20 30 40 50 60 70 80 90 1000.7

0.8

0.9

1

ωλ

0 10 20 30 40 50 60 70 80 90 1000.009

0.01

0.011

0 10 20 30 40 50 60 70 80 90 100−0.5

0

0.5

pd

0 10 20 30 40 50 60 70 80 90 1000

100

200

300

400

St

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

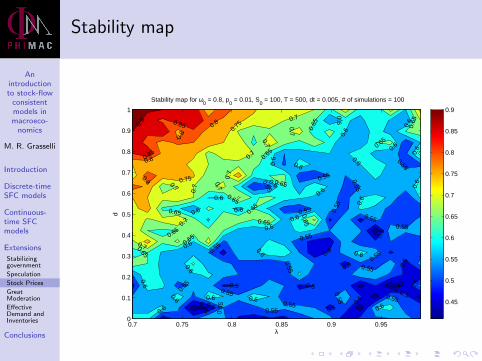

Stability map

0.5

0.5

0.55

0.55

0.55

0.55

0.55

0.55

0.55

0.550.550.

55

0.6

0.6

0.6

0.6

0.6

0.6

0.6

0.6

0.65

0.65

0.65

0.65 0.65

0.65

0.65

0.65

0.7

0.7

0.7

0.7

0.7

0.75

0.75

0.8

0.8

0.85

0.85

0.5

0.55

0.55

0.55

0.6

0.6

0.55

0.6

0.55

0.50.6

0.6

0.5

0.6

0.65

0.55

0.9

0.55

0.6

0.7

0.5

0.55

0.55

0.65

0.6

0.65 0.60.7

0.7

0.65

0.8

0.6

0.6

0.6

0.60.6

0.6

0.45 0.

5

0.45

0.6

0.55

0.7

0.5

0.8

0.65

0.5

0.6

0.7

0.5

0.5

0.6

0.6

λ

d

Stability map for ω0 = 0.8, p

0 = 0.01, S

0 = 100, T = 500, dt = 0.005, # of simulations = 100

0.7 0.75 0.8 0.85 0.9 0.950

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0.45

0.5

0.55

0.6

0.65

0.7

0.75

0.8

0.85

0.9

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

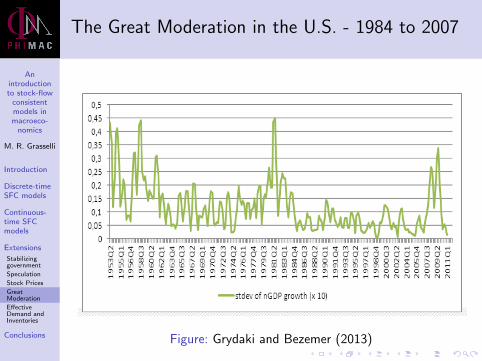

The Great Moderation in the U.S. - 1984 to 2007

Figure: Grydaki and Bezemer (2013)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Possible explanations

Real-sector causes: inventory management, labour marketchanges, responses to oil shocks, external balances , etc.

Financial-sector causes: credit accelerator models, financialinnovation, deregulation, better monetary policy, etc.

Grydaki and Bezemer (2013): growth of debt in the realsector.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Possible explanations

Real-sector causes: inventory management, labour marketchanges, responses to oil shocks, external balances , etc.

Financial-sector causes: credit accelerator models, financialinnovation, deregulation, better monetary policy, etc.

Grydaki and Bezemer (2013): growth of debt in the realsector.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Possible explanations

Real-sector causes: inventory management, labour marketchanges, responses to oil shocks, external balances , etc.

Financial-sector causes: credit accelerator models, financialinnovation, deregulation, better monetary policy, etc.

Grydaki and Bezemer (2013): growth of debt in the realsector.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

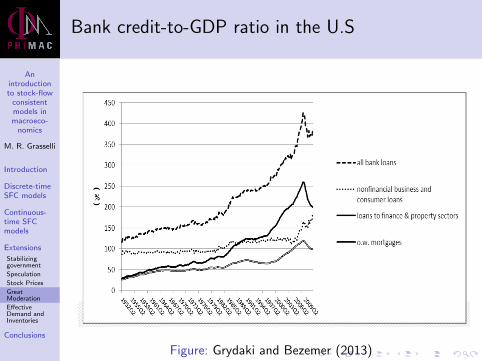

Bank credit-to-GDP ratio in the U.S

Figure: Grydaki and Bezemer (2013)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

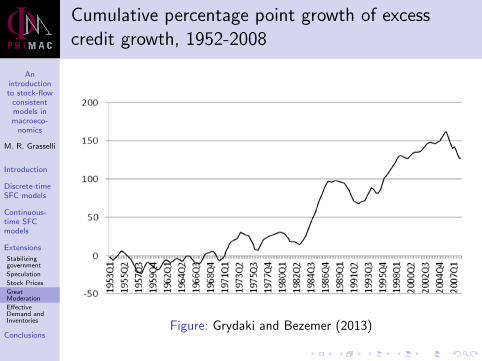

Cumulative percentage point growth of excesscredit growth, 1952-2008

Figure: Grydaki and Bezemer (2013)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

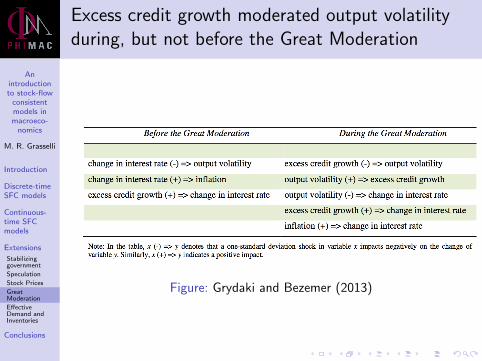

Excess credit growth moderated output volatilityduring, but not before the Great Moderation

Figure: Grydaki and Bezemer (2013)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

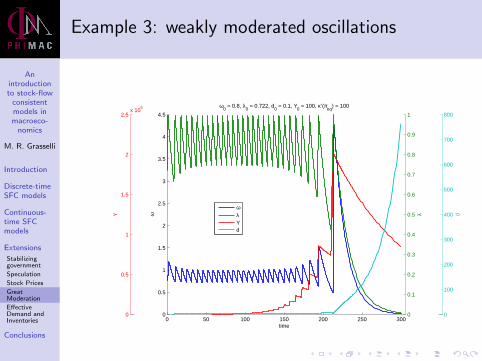

Example 3: weakly moderated oscillations

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

λ

0

0.5

1

1.5

2

2.5x 10

6

Y

0

100

200

300

400

500

600

700

800

d

0 50 100 150 200 250 3000

0.5

1

1.5

2

2.5

3

3.5

4

4.5

time

ω

ω0 = 0.8, λ

0 = 0.722, d

0 = 0.1, Y

0 = 100, κ’(π

eq) = 100

ωλYd

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

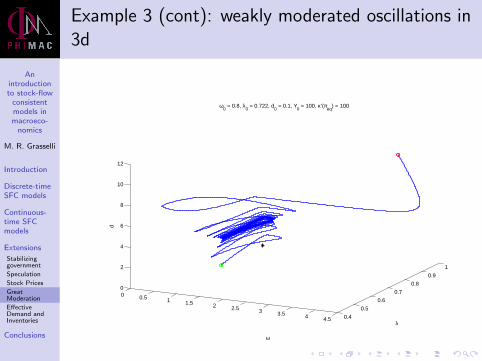

Example 3 (cont): weakly moderated oscillations in3d

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5 0.4

0.5

0.6

0.7

0.8

0.9

1

0

2

4

6

8

10

12

λ

ω0 = 0.8, λ

0 = 0.722, d

0 = 0.1, Y

0 = 100, κ’(π

eq) = 100

ω

d

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

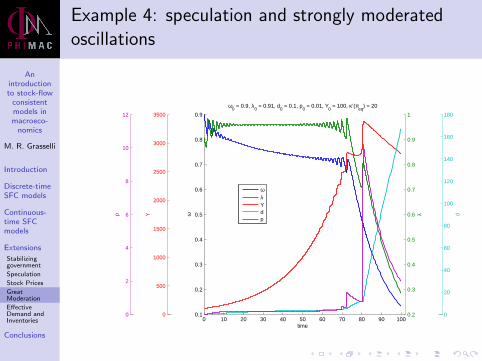

Example 4: speculation and strongly moderatedoscillations

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

λ

0

500

1000

1500

2000

2500

3000

3500

Y

0

20

40

60

80

100

120

140

160

180

d

0

2

4

6

8

10

12p

0 10 20 30 40 50 60 70 80 90 1000.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

time

ω

ω0 = 0.9, λ

0 = 0.91, d

0 = 0.1, p

0 = 0.01, Y

0 = 100, κ’(π

eq) = 20

ωλYdp

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

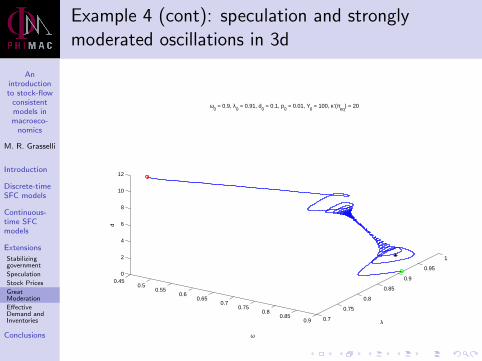

Example 4 (cont): speculation and stronglymoderated oscillations in 3d

0.450.5

0.550.6

0.650.7

0.750.8

0.850.9 0.7

0.75

0.8

0.85

0.9

0.95

1

0

2

4

6

8

10

12

λ

ω0 = 0.9, λ

0 = 0.91, d

0 = 0.1, p

0 = 0.01, Y

0 = 100, κ’(π

eq) = 20

ω

d

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

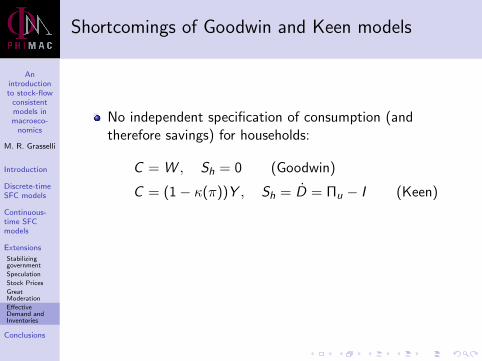

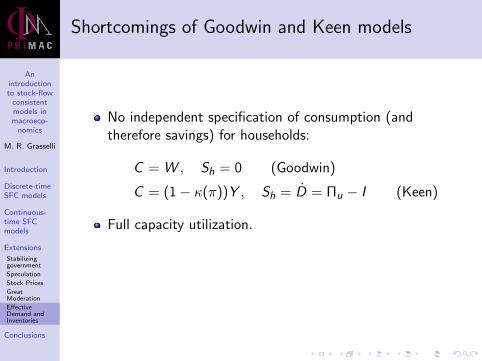

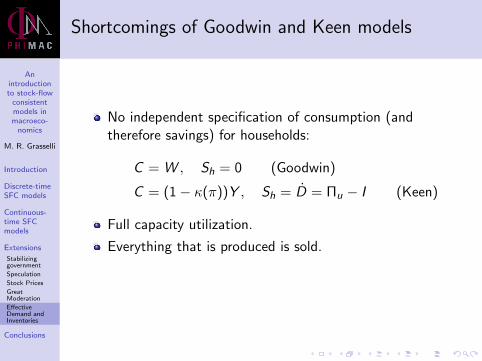

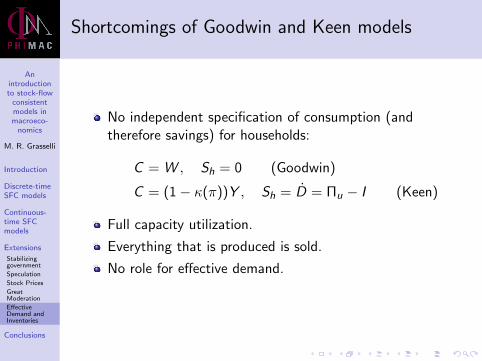

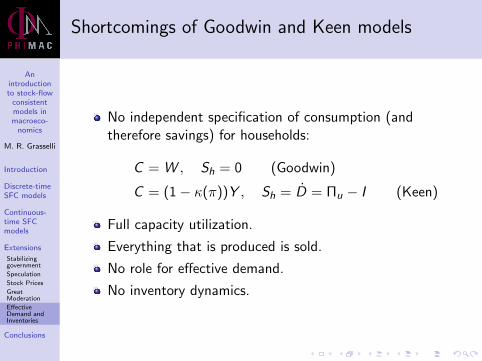

Shortcomings of Goodwin and Keen models

No independent specification of consumption (andtherefore savings) for households:

C = W , Sh = 0 (Goodwin)

C = (1− κ(π))Y , Sh = D = Πu − I (Keen)

Full capacity utilization.

Everything that is produced is sold.

No role for effective demand.

No inventory dynamics.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Shortcomings of Goodwin and Keen models

No independent specification of consumption (andtherefore savings) for households:

C = W , Sh = 0 (Goodwin)

C = (1− κ(π))Y , Sh = D = Πu − I (Keen)

Full capacity utilization.

Everything that is produced is sold.

No role for effective demand.

No inventory dynamics.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Shortcomings of Goodwin and Keen models

No independent specification of consumption (andtherefore savings) for households:

C = W , Sh = 0 (Goodwin)

C = (1− κ(π))Y , Sh = D = Πu − I (Keen)

Full capacity utilization.

Everything that is produced is sold.

No role for effective demand.

No inventory dynamics.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Shortcomings of Goodwin and Keen models

No independent specification of consumption (andtherefore savings) for households:

C = W , Sh = 0 (Goodwin)

C = (1− κ(π))Y , Sh = D = Πu − I (Keen)

Full capacity utilization.

Everything that is produced is sold.

No role for effective demand.

No inventory dynamics.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Shortcomings of Goodwin and Keen models

No independent specification of consumption (andtherefore savings) for households:

C = W , Sh = 0 (Goodwin)

C = (1− κ(π))Y , Sh = D = Πu − I (Keen)

Full capacity utilization.

Everything that is produced is sold.

No role for effective demand.

No inventory dynamics.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

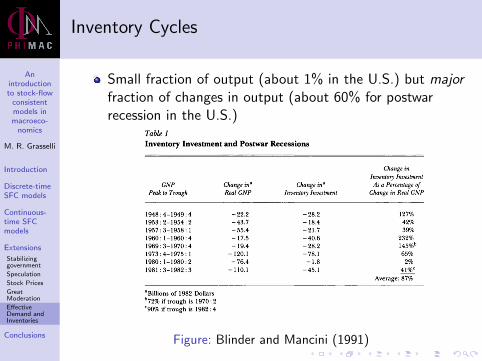

Inventory Cycles

Small fraction of output (about 1% in the U.S.) but majorfraction of changes in output (about 60% for postwarrecession in the U.S.)

Figure: Blinder and Mancini (1991)

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

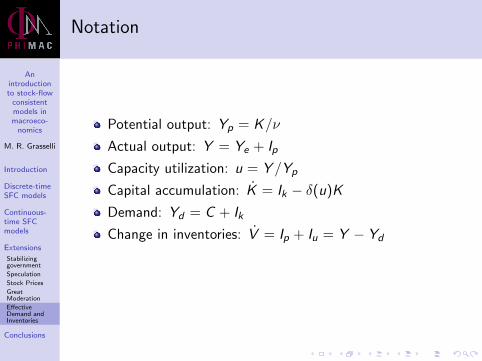

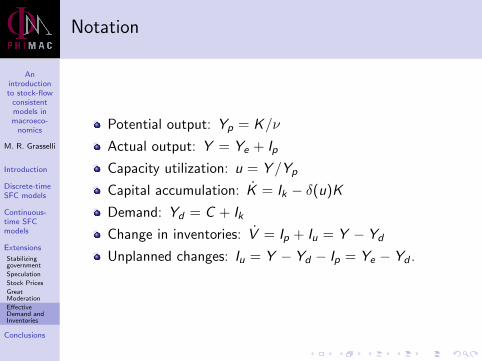

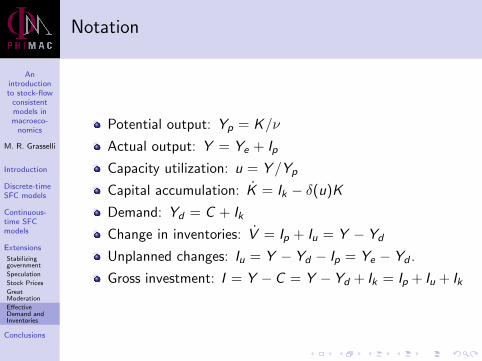

Notation

Potential output: Yp = K/ν

Actual output: Y = Ye + Ip

Capacity utilization: u = Y /Yp

Capital accumulation: K = Ik − δ(u)K

Demand: Yd = C + Ik

Change in inventories: V = Ip + Iu = Y − Yd

Unplanned changes: Iu = Y − Yd − Ip = Ye − Yd .

Gross investment: I = Y −C = Y −Yd + Ik = Ip + Iu + Ik

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Notation

Potential output: Yp = K/ν

Actual output: Y = Ye + Ip

Capacity utilization: u = Y /Yp

Capital accumulation: K = Ik − δ(u)K

Demand: Yd = C + Ik

Change in inventories: V = Ip + Iu = Y − Yd

Unplanned changes: Iu = Y − Yd − Ip = Ye − Yd .

Gross investment: I = Y −C = Y −Yd + Ik = Ip + Iu + Ik

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Notation

Potential output: Yp = K/ν

Actual output: Y = Ye + Ip

Capacity utilization: u = Y /Yp

Capital accumulation: K = Ik − δ(u)K

Demand: Yd = C + Ik

Change in inventories: V = Ip + Iu = Y − Yd

Unplanned changes: Iu = Y − Yd − Ip = Ye − Yd .

Gross investment: I = Y −C = Y −Yd + Ik = Ip + Iu + Ik

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Notation

Potential output: Yp = K/ν

Actual output: Y = Ye + Ip

Capacity utilization: u = Y /Yp

Capital accumulation: K = Ik − δ(u)K

Demand: Yd = C + Ik

Change in inventories: V = Ip + Iu = Y − Yd

Unplanned changes: Iu = Y − Yd − Ip = Ye − Yd .

Gross investment: I = Y −C = Y −Yd + Ik = Ip + Iu + Ik

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Notation

Potential output: Yp = K/ν

Actual output: Y = Ye + Ip

Capacity utilization: u = Y /Yp

Capital accumulation: K = Ik − δ(u)K

Demand: Yd = C + Ik

Change in inventories: V = Ip + Iu = Y − Yd

Unplanned changes: Iu = Y − Yd − Ip = Ye − Yd .

Gross investment: I = Y −C = Y −Yd + Ik = Ip + Iu + Ik

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Notation

Potential output: Yp = K/ν

Actual output: Y = Ye + Ip

Capacity utilization: u = Y /Yp

Capital accumulation: K = Ik − δ(u)K

Demand: Yd = C + Ik

Change in inventories: V = Ip + Iu = Y − Yd

Unplanned changes: Iu = Y − Yd − Ip = Ye − Yd .

Gross investment: I = Y −C = Y −Yd + Ik = Ip + Iu + Ik

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Notation

Potential output: Yp = K/ν

Actual output: Y = Ye + Ip

Capacity utilization: u = Y /Yp

Capital accumulation: K = Ik − δ(u)K

Demand: Yd = C + Ik

Change in inventories: V = Ip + Iu = Y − Yd

Unplanned changes: Iu = Y − Yd − Ip = Ye − Yd .

Gross investment: I = Y −C = Y −Yd + Ik = Ip + Iu + Ik

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Notation

Potential output: Yp = K/ν

Actual output: Y = Ye + Ip

Capacity utilization: u = Y /Yp

Capital accumulation: K = Ik − δ(u)K

Demand: Yd = C + Ik

Change in inventories: V = Ip + Iu = Y − Yd

Unplanned changes: Iu = Y − Yd − Ip = Ye − Yd .

Gross investment: I = Y −C = Y −Yd + Ik = Ip + Iu + Ik

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

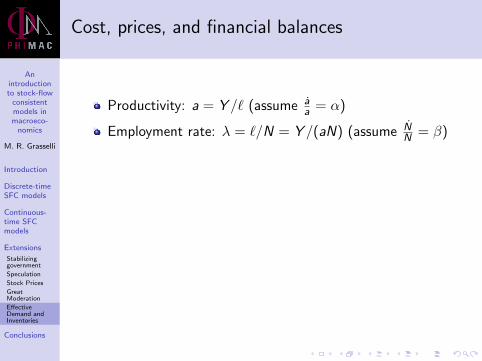

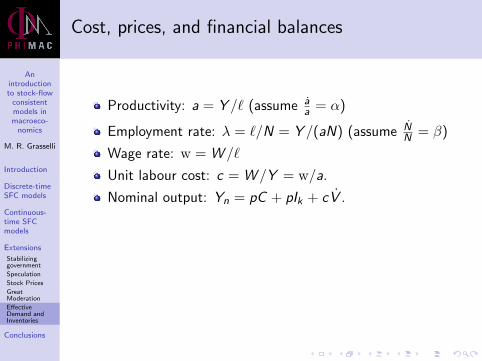

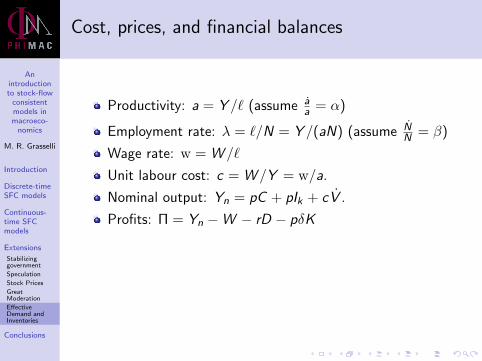

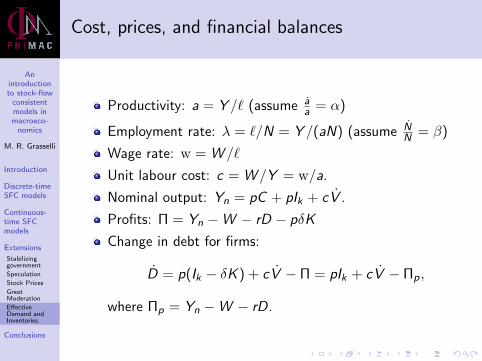

Cost, prices, and financial balances

Productivity: a = Y /` (assume aa = α)

Employment rate: λ = `/N = Y /(aN) (assume NN = β)

Wage rate: w = W /`

Unit labour cost: c = W /Y = w/a.

Nominal output: Yn = pC + pIk + cV .

Profits: Π = Yn −W − rD − pδK

Change in debt for firms:

D = p(Ik − δK ) + cV − Π = pIk + cV − Πp,

where Πp = Yn −W − rD.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Cost, prices, and financial balances

Productivity: a = Y /` (assume aa = α)

Employment rate: λ = `/N = Y /(aN) (assume NN = β)

Wage rate: w = W /`

Unit labour cost: c = W /Y = w/a.

Nominal output: Yn = pC + pIk + cV .

Profits: Π = Yn −W − rD − pδK

Change in debt for firms:

D = p(Ik − δK ) + cV − Π = pIk + cV − Πp,

where Πp = Yn −W − rD.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Cost, prices, and financial balances

Productivity: a = Y /` (assume aa = α)

Employment rate: λ = `/N = Y /(aN) (assume NN = β)

Wage rate: w = W /`

Unit labour cost: c = W /Y = w/a.

Nominal output: Yn = pC + pIk + cV .

Profits: Π = Yn −W − rD − pδK

Change in debt for firms:

D = p(Ik − δK ) + cV − Π = pIk + cV − Πp,

where Πp = Yn −W − rD.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Cost, prices, and financial balances

Productivity: a = Y /` (assume aa = α)

Employment rate: λ = `/N = Y /(aN) (assume NN = β)

Wage rate: w = W /`

Unit labour cost: c = W /Y = w/a.

Nominal output: Yn = pC + pIk + cV .

Profits: Π = Yn −W − rD − pδK

Change in debt for firms:

D = p(Ik − δK ) + cV − Π = pIk + cV − Πp,

where Πp = Yn −W − rD.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Cost, prices, and financial balances

Productivity: a = Y /` (assume aa = α)

Employment rate: λ = `/N = Y /(aN) (assume NN = β)

Wage rate: w = W /`

Unit labour cost: c = W /Y = w/a.

Nominal output: Yn = pC + pIk + cV .

Profits: Π = Yn −W − rD − pδK

Change in debt for firms:

D = p(Ik − δK ) + cV − Π = pIk + cV − Πp,

where Πp = Yn −W − rD.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Cost, prices, and financial balances

Productivity: a = Y /` (assume aa = α)

Employment rate: λ = `/N = Y /(aN) (assume NN = β)

Wage rate: w = W /`

Unit labour cost: c = W /Y = w/a.

Nominal output: Yn = pC + pIk + cV .

Profits: Π = Yn −W − rD − pδK

Change in debt for firms:

D = p(Ik − δK ) + cV − Π = pIk + cV − Πp,

where Πp = Yn −W − rD.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

Cost, prices, and financial balances

Productivity: a = Y /` (assume aa = α)

Employment rate: λ = `/N = Y /(aN) (assume NN = β)

Wage rate: w = W /`

Unit labour cost: c = W /Y = w/a.

Nominal output: Yn = pC + pIk + cV .

Profits: Π = Yn −W − rD − pδK

Change in debt for firms:

D = p(Ik − δK ) + cV − Π = pIk + cV − Πp,

where Πp = Yn −W − rD.

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

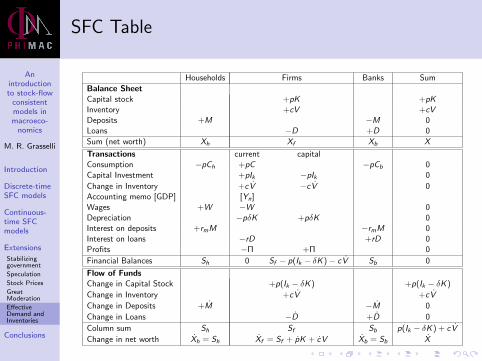

SFC Table

Households Firms Banks Sum

Balance SheetCapital stock +pK +pKInventory +cV +cVDeposits +M −M 0Loans −D +D 0

Sum (net worth) Xh Xf Xb X

Transactions current capitalConsumption −pCh +pC −pCb 0Capital Investment +pIk −pIk 0

Change in Inventory +cV −cV 0Accounting memo [GDP] [Yn]Wages +W −W 0Depreciation −pδK +pδK 0Interest on deposits +rmM −rmM 0Interest on loans −rD +rD 0Profits −Π +Π 0

Financial Balances Sh 0 Sf − p(Ik − δK )− cV Sb 0

Flow of FundsChange in Capital Stock +p(Ik − δK ) +p(Ik − δK )

Change in Inventory +cV +cV

Change in Deposits +M −M 0

Change in Loans −D +D 0

Column sum Sh Sf Sb p(Ik − δK ) + cV

Change in net worth Xh = Sh Xf = Sf + pK + cV Xb = Sb X

Anintroductionto stock-flow

consistentmodels inmacroeco-

nomics

M. R. Grasselli

Introduction

Discrete-timeSFC models

Continuous-time SFCmodels

Extensions

Stabilizinggovernment

Speculation

Stock Prices

GreatModeration

EffectiveDemand andInventories

Conclusions

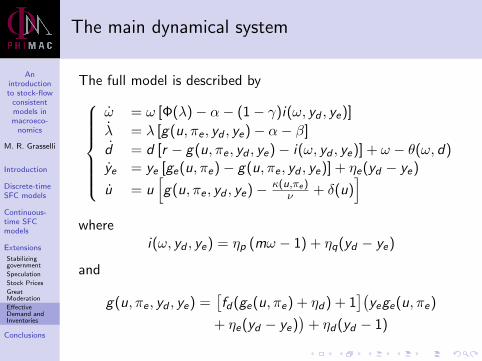

The main dynamical system

The full model is described by

ω = ω [Φ(λ)− α− (1− γ)i(ω, yd , ye)]

λ = λ [g(u, πe , yd , ye)− α− β]

d = d [r − g(u, πe , yd , ye)− i(ω, yd , ye)] + ω − θ(ω, d)ye = ye [ge(u, πe)− g(u, πe , yd , ye)] + ηe(yd − ye)

u = u[g(u, πe , yd , ye)− κ(u,πe)

ν + δ(u)]

wherei(ω, yd , ye) = ηp (mω − 1) + ηq(yd − ye)

and

g(u, πe , yd , ye) =[fd(ge(u, πe) + ηd) + 1

](yege(u, πe)

+ ηe(yd − ye))

+ ηd(yd − 1)

Anintroductionto stock-flow

consistentmodels inmacroeco-

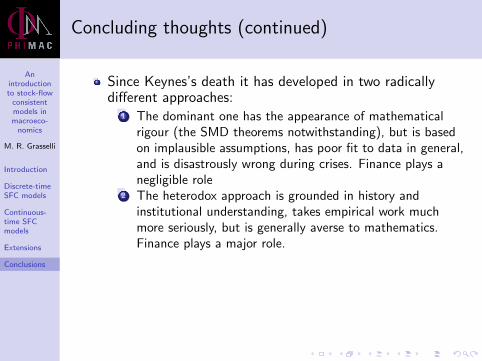

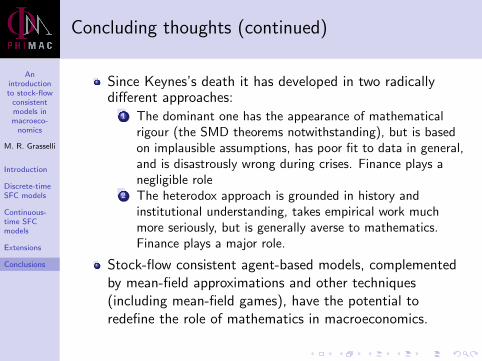

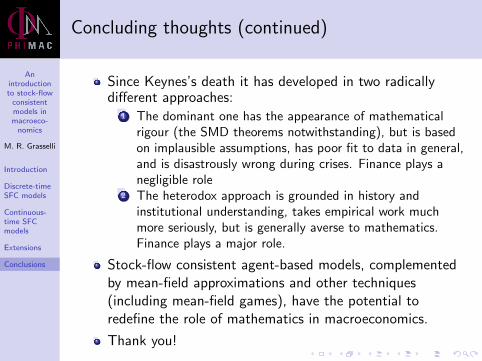

nomics