Embed Size (px)

Citation preview

Louisiana State UniversityLSU Digital Commons

LSU Historical Dissertations and Theses Graduate School

1988

An Investigation of Internal Auditor Judgment onthe Importance of Indicators of Potential FinancialFraud: An Analytic Hierarchy Process Approach.Barbara Ann ApostolouLouisiana State University and Agricultural & Mechanical College

Follow this and additional works at: https://digitalcommons.lsu.edu/gradschool_disstheses

This Dissertation is brought to you for free and open access by the Graduate School at LSU Digital Commons. It has been accepted for inclusion inLSU Historical Dissertations and Theses by an authorized administrator of LSU Digital Commons. For more information, please [email protected].

Recommended CitationApostolou, Barbara Ann, "An Investigation of Internal Auditor Judgment on the Importance of Indicators of Potential Financial Fraud:An Analytic Hierarchy Process Approach." (1988). LSU Historical Dissertations and Theses. 4555.https://digitalcommons.lsu.edu/gradschool_disstheses/4555

INFORMATION TO USERS

The most advanced technology has been used to photograph and reproduce this manuscript from the microfilm master. UMI films the text directly from the original or copy submitted. Thus, some thesis and dissertation copies are in typewriter face, while others may be from any type of computer printer.

The quality of this reproduction is dependent upon the quality of the copy submitted. Broken or indistinct print, colored or poor quality illustrations and photographs, print bleedthrough, substandard margins, and improper alignment can adversely affect reproduction.

In the unlikely event that the author did not send UMI a complete manuscript and there are missing pages, these will be noted. Also, if unauthorized copyright material had to be removed, a note will indicate the deletion.

Oversize materials (e.g., maps, drawings, charts) are reproduced by sectioning the original, beginning at the upper leii-hand corner and continuing from left to right in equal sections with small overlaps. Each original is also photographed in one exposure and is included in reduced form at the back of the book. These are also available as one exposure on a standard 35mm slide or as a 17" x 23" black and white photographic print for an additional

Photographs included in the original manuscript have been reproduced xerographically in this copy. Higher quality 6" x 9" black and white photographic prints are available for any photographs or illustrations appearing in this copy for an additional charge. Contact UMI directly to order.

University Microfilms International A Bell & Howell Information Company

3Q0 North Zeeb Road. Ann Arbor. Ml 48106-1346 USA 313/761-4700 800/521-0600

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

Order Number 8904524

An investigation of internal auditor judgment on the importance of indicators of potential financial fraud: An analytic hierarchy process approach

Apostolou, Barbara Ann, Ph.D.The Louisiana State University and Agricultural and Mechanical CoL, 1988

UMI300 N, Zeeb Rd.Ann Arbor, MI 48106

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

AN INVESTIGATION OF INTERNAL AUDITOR JUDGMENT ON THE IMPORTANCE OF INDICATORS

OF POTENTIAL FINANCIAL FRAUD: AN ANALYTICHIERARCHY PROCESS APPROACH

A Dissertation

Submitted to the Graduate Faculty of the Louisiana State University and

Agricultural and Mechanical College in partial fulfillment of the

requirements for the degree of Doctor of Philosophy

inThe Department of Accounting

byBarbara Ann Apostolou

B.S., Plymouth State College* 1979 M.B.A.* Plymouth State College* 1984

August 1988

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

ACKNOWLEDGEMENTS

I wish to express my sincere appreciation to the members of my dissertation committee for their ongoing support and valuable assistance: Professors Vincent C.Brenner (chairman)* Robert M. Harper* Michael J. R.Hoffman* W. Douglas McMillin (economics)* and Glenn E. Sumners.

I would especially like to thank the Institute of Internal Auditors Research Foundation for their generous financial support of this project.

Two individuals deserve special recognition— my husband* Professor Nick Apostolou* for his endless support and devotion and my sister* Susan Keir* for leading the way to LSU. This dissertation is dedicated to them.

i i

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

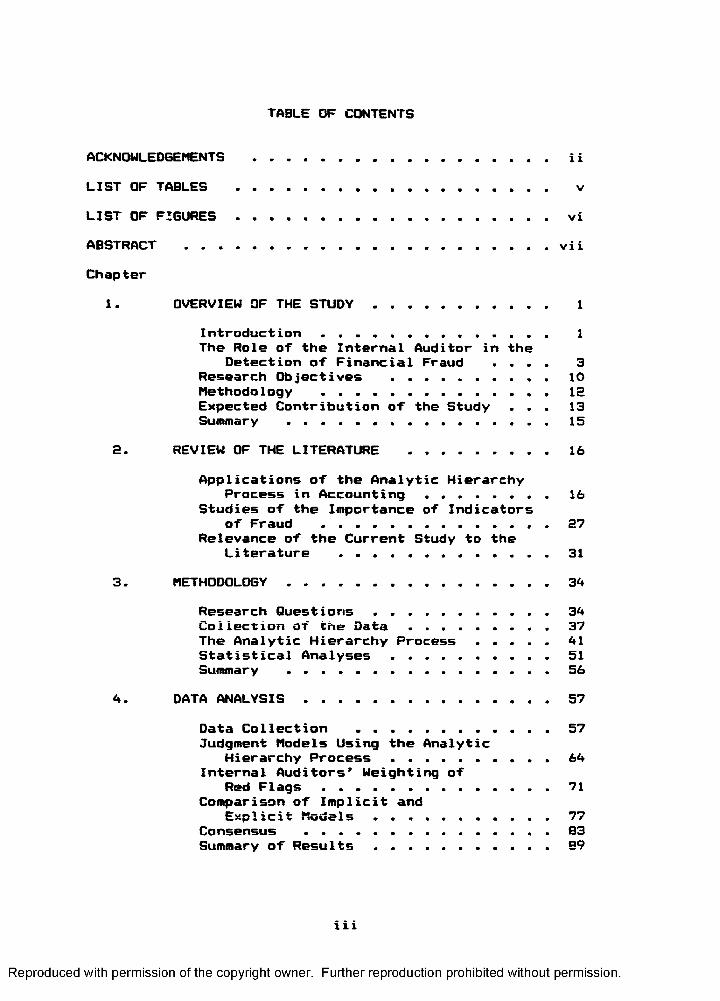

TABLE OF CONTENTS

ACKNOWLEDGEMENTS ...................................... i iLIST OF TABLES ....................................... vLIST OF F I G U R E S ......................................... viABSTRACT ...............................................viiChapter

1. OVERVIEW OF THE S T U D Y ...................... 1Introduction . . . . . . ............... 1The Role of the Internal Auditor in the

Detection of Financial Fraud . . . . 3Research Objectives ................... 10Methodology ...............................ISExpected Contribution of the Study . . . 13Summary ..................... 15

S. REVIEW OF THE LITERATURE ....................16Applications of the Analytic Hierarchy

Process in Accounting . . . . . . . . 16Studies of the Importance of Indicators

of Fraud .............. 27Relevance of the Current Study to the

Literature ............................ 313. METHODOLOGY ...................................34

Research Questions ...................... 34Collection of the D a t a ....................37The Analytic Hierarchy Process ......... 41Statistical Analyses ................... 51Summary ...................................56

4. DATA A N A L Y S I S .................................57Data Collection ........................ 57Judgment Models Using the Analytic

Hierarchy Process . ................. 64Internal Auditors1 Weighting of

Red F l a g s .............................. 71Comparison of Implicit and

Explicit Models ................... 77Consensus . . . . . ................... 83Summary of R e s u l t s ........................ 89

iii

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

5. SUMMARY AND CONCLUSIONS ......................92Summary and Implications . ...............92Limitations .......... 96Suggestions for Future Research . . . . 98

BIBLIOGRAPHY .......................................... 101APPENDIX ........................................... 104VITA ................................................... 124

iv

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

LIST OF TABLESTable Page4-1. Summary of Subjects’ Experience as

Internal A u d i t o r ................... 604-2. Summary of Subjects* Combined Experience a?.

Internal and External Auditor ............. 604-3. Breakdown of Subjects by Industry Membership . 614-4. Breakdown of Subjects by State Where

E m p l o y e d .....................................624-5. Summary of Degrees Held by S u b j e c t s .......... 634-6. Summary of Subjects by Professional

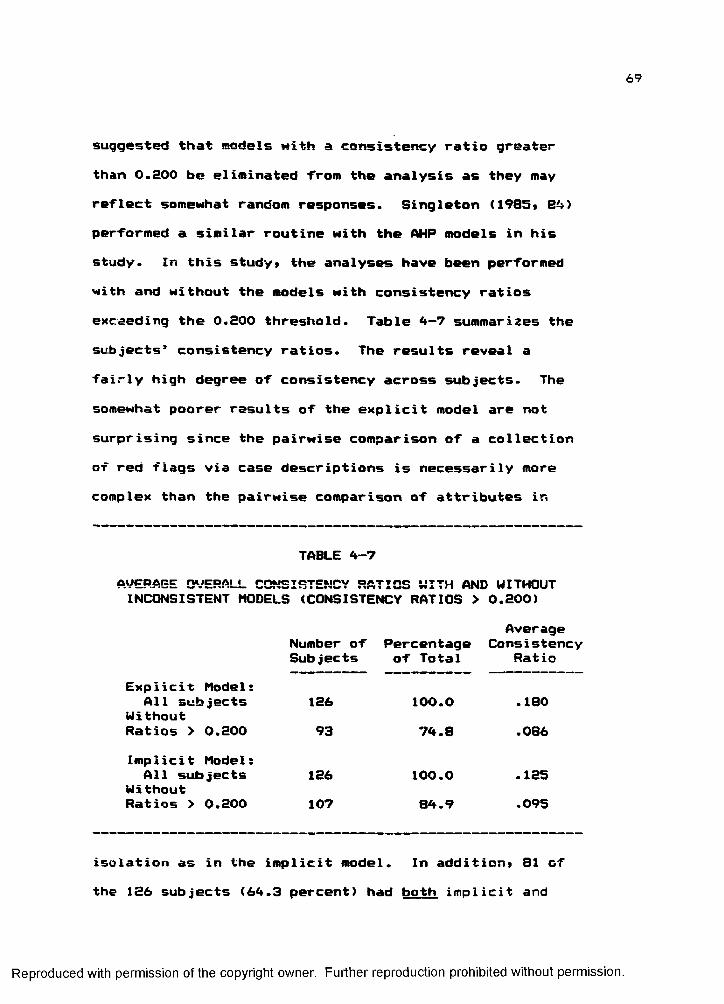

Certification ........................ 634-7. Average Overall Consistency Ratios With and

Without Inconsistent Models (Consistency Ratios > 0 . 200)............................ 69

4-8. Summary of Inconsistent Models Based onExperience as Internal Auditor ......... 70

4-9. Average Weights on Red F l a g s ................... 734—10. Frequency Distribution of Management

Characteristics ............................ 764—11. Results of Spearman’s Rho Analysis ...........794-12. Results of Correlation Analysis................. 794-13. Correlation of Implicit and Explicit Weights

on Firms Across Subjects ................. 804-14. Frequency Distributions of Implicit and

Explicit Models ............................ 834-15. Measures of C o n s e n s u s ..........................884-16. Measures of Consensus Based on Subjects’

Combined Experience as Internal andExternal A u d i t o r ................... 89

4-17. Summary of Hypothesis Test Results.............90

v

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

LIST OF FIGURES Figure Page2—1. Analytical Review Procedure Hierarchy . . . . 182-2. Accounts Receivable Hierarchy . . ........... 202-3. Hierarchy of Internal Controls in a LAN . . . 222-4. Hierarchy of Qualitative Characteristics . . . 243—1. Hierarchy of Red Flags that Indicate the

Potential for Financial Fraud . . . . . . . 383-2. Advantages of the Analytic Hierarchy Process . 433-3. The Pairwise Comparison Scale ............... 473-4. Matrices for Pairwise Comparisons ........... 503-5. Matrices and Priority Vectors for Implicit

Choice of Firm ............................ 544-1. Dominance Matrix and Priority Vector for

Example Subject’s Explicit AHP Model . . . . 654-2. Dominance Matrices and Priority Vectors for

Example Subject’s Implicit AHP Model . . . . 67

vi

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

ABSTRACT

Financial fraud has become a serious problem to the business community. As a result• regulators and financial statement users have leaked to the auditing profession for answers to the problem. The role of the internal auditor has received significant attention due to the unique position they fill. That is» they are positioned to observe and test financial and operational activities of the firm on a continuous basis. In addition! internal auditors are able to devote more time to the deterrence and detection of financial fraud than their external counterparts.

The National Commission on Fraudulent Financial Reporting (Treadway Commission) issued its final report in October 1987 following a two-year investigation of the problem of financial fraud. An effective internal audit function was mentioned as a chief variable in the detection and deterrence of financial fraud. Both the Treadway Commission and the American Institute of Certified Public Accountants (Statement on Auditing Standards No. 53i The Auditor’s Responsibility to Detect and Report Errors and Irregularities. May 1988) published lists of indicators or red flags of financial fraud.

This study focused on the internal auditor’s ability to identify red flags and rank their importance to the overall assessment of the potential for financial fraud.

vii

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

The Analytic Hierarchy Process was used to model the judgment of each subject who participated in this study.In addition* measures of consensus were computed to evaluate the overall level of agreement between the subjects on the importance rankings of the red flags.

In general* internal auditors ranked management red flags as most important to the overall evaluation of the potential for financial fraud* followed by firm then industry red flags. Conclusions as to the rankings within each of the three principal groupings of red flags were not so clear.

vii i

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

CHAPTER 1 OVERVIEW OF THE STUDY

IntroductionThe auditor’s responsibility For the detection oF

Financial Fraud has recently received signiFicant attention From regulators and users oF Financial statements as well as the auditing proFession. In response to growing concerns oF various parties over the auditor’s role in the detection oF Financial Fraud, a private-sector initiative to study Fraudulent Financial reporting was created in 1985. This initiative resulted in the National Commission on Fraudulent Financial Reporting, or the Treadway Commission, named aFter its chairman, Former Securities and Exchange Commissioner (SEC), James C. Treadway, Jr. The Treadway Commission was jointly sponsored by the American Institute oF Certified Public Accountants (AICPA), the American Accounting Association (AAA), the Financial Executives Institute (FEI), the Institute oF Internal Auditors (IIA); and the National Association oF Accountants (NAA) (Treadway 1987, 1).

As a result oF the increased Focus upon the detection oF Financial Fraud, the role oF the internal

1

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

2

auditor has received attention. In particular* the IIA has become increasingly visible in efforts to address the responsibility of internal auditors in the prevention* detection* and reporting of financial fraud. In addition to their co-sponsorship of the Treadway Commission* the IIA published a report entitled The Role of the Internal Auditor in the Deterrence* Detection, and Reporting of Fraudulent Financial Reporting for the benefit of the Treadway Commission (IIA 1986). This report outlined the internal auditor’s responsibilities in addressing the problem of financial fraud in addition to providing recommendations for improved coordination between external and internal auditors in the detection of financial fraud. The internal auditor’s responsibilities are clearly set forth in Statement of Internal Auditing Standards (SIAS) No. 3* Deterrence* Detection*Investigation* and Reporting of Fraud (IIA 1985).Furthermore* SIAS No. 5* Internal Auditors’ Relationships with Independent Outside Auditors (IIA 1987) calls for increased coordination of effort between internal and external auditors to enhance efficiency and minimize duplication of effort.

The Treadway Commission defined financial fraud as "intentional or reckless conduct* whether act or omission* that results in materially misleading financial statements." This definition excludes unintentional errors that have a material impact on the financial

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

3

statements* as weii as "corporate improprieties such as tax fraud * employee embezzlements* or violations of environmental or product safety regulations" (Treadway 1987* 2). The AICPA includes financial fraud within its definition of irregularities— "intentional misstatements or amissions of amounts or disclosures in financial statements" (AICPA 1988* 2). 5IA5 No. 3 defines financial fraud as an "array of irregularities and illegal acts characterized by intentional deception" (IIA 1985* 2). These three groups concur that financial fraud is characterized by both intent and misleading financial statements.

The first section of this chapter will describe in some detail the role of the internal auditor in the detection of financial fraud. In the second section* the research objectives of the study will be discussed* followed by a description of the proposed methodology. Lastly* the expected contribution of this study will be presented.

The Role of the Internal Auditor in the Detection of Financial Fraud

The Cohen Commission In 197*., the AICPA established an independent

commission to "develop conclusions and recommendations regarding the appropriate responsibilities of independent auditors" (Cohen 1978* xi). The Commission on Auditors’

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

Responsibilities became known as the Cohen Commission after its chairman* Manuel F. Cohen. Its final report was issued in 1978.

Included among the recommendations summarized in the report was clarification of the independent auditor’s responsibility for the detection of fraud. The auditor’s primary concern should be with "intentional misrepresentations in or omissions from financial statements*“ or financial fraud. The Cohen Commission stressed that "an audit should be designed to provide reasonable assurance that the financial statements are not affected by material fraud" (Cohen 1978* 36).

In January 1977* Statement on Auditing Standards (SAS) No. 16* The Independent Auditor’s Responsibility for the Detection of Errors and Irregularities (AICPA 1977)* was issued* coinciding with preliminary recommendations of the Cohen Commission. SAS No. 16 states that the auditor has fulfilled the responsibility to detect errors or irregularities when the audit has been carried out in accordance with generally accepted auditing standards (GAAS). However* the audit program should be designed to detect errors and irregularities that have a material impact on the financial statements.

The Cohen Commission focused on the independent auditor’s role and responsibility. The Commission called for increased attention by auditors in the detection of financial fraud. SAS No. 9* The Effect of an Internal

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

5

Audit Function on the Scope of the Independent Auditor's Examination (AICPA 1975* A)* notes that "the independent auditor may make use of internal auditors to provide direct assistance in performing an examination in accordance Mith generally accepted auditing standards." Although an independent auditor may not subordinate his or her judgment to that of the internal auditor* valuable assistance may be available from the internal auditor in the evaluation of the potential for financial fraud.

Regulatory PressureThe Foreign Corrupt Practices Act of 1977 covers

all domestic corporations required to file annual reports under the Securities Exchange Act of 1934 (Greanias 1982, 1—17). These firms must create and maintain a system of internal accounting controls. The primary purpose of the internal accounting control system is to maintain accountability for assets and ensure that transactions are authorized and properly recorded. The role of the internal auditor gained importance Mith the passage of this legislation* since the presence of an effective internal auditing staff is a strong internal accounting control feature.

In late 1986* Congressman Ron Wyden introduced a revised version of a bill (HR5439) drafted in response to recent business failures associated with financial fraud. This bill, the Financial Fraud and Disclosure Act of

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

6

1996, which is still pending before Congress, would amend the Securities Exchange Act of 1934 by requiring that audits of public companies include reasonable procedures for detection of material financial fraud. Furthermore, the bill would require that auditors report fraudulent activities to appropriate enforcement and regulatory authorities Cl). S. Congress 1986), an action that is currently not required.

In response, the Auditing Standards Board (ASB) issued a new SAS to supersede existing SAS No. 16. SAS No. 53, entitled The Auditor’s Responsibility to Detect and Report Errors and Irregularities, requires auditors to design their audits to detect material errors and irregularities, consistent with the recommendation made in the Uyden bill. However, SAS No. 53 calls for the auditor to report financial fraud to the audit committee for its disposition, rather than to enforcement or regulatory authorities (AICPA 1988).

According to SAS No. 9, independent auditors may consider the work of the internal auditor in determining the nature, timing, and extent of audit procedures to be performed (AICPA 1975). Since more stringent requirements are forthcoming with respect to the independent auditor’s responsibility to detect and report financial fraud, the role of the internal auditor is becoming more important. As one independent auditor

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

7

notes:Often- internal auditors are best positioned to

detect fraud because they can devote more time to its discovery. In addition* they knot* the entity and its operations better than independent auditors (Levy 1985. 79).

In summary, congressional pressure (i.e.. Uyden bill) hascoincided Mith the issuance of SAS No. 53 that Millrequire the independent auditor to detect and reportmaterial fraud. The Treadway Commission has applaudedthis effort by the ASB. Clearly, the role of theinternal auditor is important as a result of his or herintimate association with the firm through both financialand operational audits.

The Treadway Commission Report The Treadway Commission published its final report

in October 1987. This report consists of detailed recommendations as follows (Treadway 1987* 11-16):

I. Recommendations for the Public Company. The Commission indicates that prevention and detection of financial fraud begins with the company, and that it is up to management to "set the tone” for integrity in financial reporting.

II. Recommendations for the Independent Public Accountant. The role of the independent auditor is secondary to that of management, but is still critical to the detection of

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

e

financial fraud. Among other things* the report suggests that the independent auditor be required to detect material financial fraud if it exists.

III. Recommendations to the SEC and Others toImprove the Reoulatorv and Leoal Environment. These recommendations essentially call for increased SEC sanctions and enforcement power along with improved regulation of the public accounting profession.

IV, Recommendations for Education. The Commissioncalls for increased attention on ethics inaccounting and business curricula.

Recommendations for the internal auditor arespecifically addressed in Part I of the Report (Treadway1907 * 37-39):

Properly organized and effectively operated* internal auditing gives management and the audit committee a way to monitor the reliability and the integrity of financial and operating information. The internal audit function is an important element in preventing and detecting fraudulent financial reporting.

The Report calls for public companies to adopt IIAprofessional standards and to ensure that their internalaudit departments are objective. In addition* internalauditors should consider the impact of nonfinancial auditfindings (as a result of operational audits) on thepotential for financial fraud. The Commission believesthat the implementation of these recommendations* when

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

9

effectively coordinated with efforts of the independent auditor, can assist in the prevention and detection of financial fraud.

Internal Auditing StandardsIn 1985, the IIA issued SIAS No. 3 (IIA 1985) to

set forth guidance on the internal auditor’s responsibility to prevent, detect, and report financial fraud. SIAS No. 3 appropriately offers general guidance without identifying specific audit procedures that the internal auditor should carry out. In particular, SIAS No. 3 states that "internal auditors should have sufficient knowledge of fraud to be able to identify indicators that fraud might have been committed" (IIA 1985, 1). If indicators of fraud are present and detected, the internal auditor should perform additional audit procedures. In addition, the internal auditor is required to report incidences of financial fraud to “management or the board of directors" (IIA 1985, 3).

The report issued by the IIA (1986) for the Treadway Commission echoes the requirements set forth in SIAS No. 3. That is, the internal auditor has a responsibility to identify indicators of fraud and expand audit procedures accordingly. Furthermore, this report calls for improved coordination between internal and external auditors in the detection of financial fraud (IIA 1986).

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

10

The Institute of Internal Auditors recently issuedSIAS No. 5i Internal Auditors’ Relationships withIndependent Outside Auditors (IIA 1987). SIAS No. 5focuses on the working relationship of internal andexternal auditors as recommended by the TreadwayCommission (1987! 39):

Appropriate involvement by the internal auditors at the corporate level» effectively coordinated to avoid duplication of the independent public accountants* efforts! can help prevent and detect fraudulent financial reporting.

In particular! SIAS No. 5 requires maximum coordinationto minimize duplication of effort and promote efficiency.The internal audit director is responsible for thiscoordination of effcrt! including the process ofeducating the internal auditor on the audit approach usedby the external auditor. The issuance of SIAS No. 5strengthens the need to study internal auditors sincetheir judgments are integral to the completion of theannual financial audit.

Research ObjectivesIndicators of the Potential for

Financial FraudIdentifying the potential for fraud is a complex

judgment task for the auditor. This judgment requiresthe auditor to assess attributes of the environment thatsuggest fraud may have occurred. Much attention has beengiven to identifying indicators (red flags) of financial

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

11

'fraud is aid in the auditor’s evaluation. Many auditors use red-flag lists to assist Mith this process* although a study performed by Albrecht and Romney (1986) found that these lists Mere inconsistent across fraud firms and contained invalid red flags. In response to the demand for a comprehensive red-flag list* the AICPA incorporated such a list in SAS No. S3 (AICPA 1988, 4-5).Furthermore* the TreadMay Commission identified and discussed red flags in their report (TreadMay 1987* 154- 163).

Red-flag lists can assist the auditor in the evaluation of the potential for financial fraud.HoMevsr, the use of a list does not eliminate the need for internal auditor judgments. For example* if "material related-party transactions" is a red'flag, the internal auditor must be able to identify this characteristic during the course of the audit in addition to Meighting its importance in the presence or absence of other red flags.

Research Questions In vieM of the role that the internal auditor may

serve in the detection of financial fraud* it is important that he or she is able to identify red flags in the audit environment. The nature* timing* and extent of financial audit procedures performed (by both the internal and external auditor) Mill depend to a great

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

12

extent upon the overall evaluation of the potential for financial fraud. The purpose of this research was to investigate the internal auditor’s judgment on the relative importance of specific red flags. As stated) both the AICPA (1988) 4-5) and the Treadway Commission (1987) 154-163) generated comprehensive red-flag lists. However) no research had been performed to determine whether internal auditors perceive these items as red flags.

In addition to modeling the internal auditor’s judgment as to the relative importance of specific red flags) this research also addressed whether internal auditors achieve consensus. In particular) the extent to which internal auditors agree with one another on the weighting of the importance of red flags of financial fraud was examined. Finally) the study investigated whether internal auditors make explicit judgments of the potential for financial fraud in a manner consistent with their modeled judgment.

Methodology The Analytic Hierarchy Process

The methodology used in this study was the Analytic Hierarchy Process (AHP) advanced by Saaty (1986)1988).The AHP is a technique for modeling judgments and for providing the decision maker with a means for selecting among alternatives. This approach is especially well-

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

13

suited to situations involving qualitative attributes. Furthermorei the AHP can handle complex judgment tasks involving interrelated cues with varying degrees of impact on the decision.

The application of the AHP involves complex matrix operations. Saaty and others have developed software (Decision Support Software 1983)? called Expert Choice? to perform the necessary computations. This study employed Expert Choice.

Expected Contribution of the Study The role of the internal auditor in the deterrence

and detection of financial fraud is clearly recognized. Considerable emphasis has been placed by regulators? the public? and those within the auditing profession on the importance of the internal auditor's role in the detection of financial fraud. This study provides information on the internal auditor's ability to identify and weight th'e importance of red flags relative to one another. In addition? measures of consensus provide information about the extent to which internal auditors agree with one another on their evaluations of the relative importance of red flags.

SAS No. 9 acknowledges the importance of the internal auditor as a valuable resource to the independent auditor in carrying out audits in accordance with GAAS. The more information that the independent

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

14

auditor obtains Mith respect to the ability of the internal auditor to support the independent audit* the greater the potential for improved coordination and efficiency between the two groups of auditors. In addition* the recent issuance of SIAS No. 5 (IIA 1985) reinforces the need for internal and external auditors to coordinate their efforts. This study offers insight to the independent auditor into the judgment quality of internal auditors in their evaluation of the potential for financial fraud.

According to Libby (1981* 3)* judgment research is important in that it may reveal when steps need to be taken to improve the judgment process. Improvement may take the form of additional education for the judge* development of judgment aids or decision models* and so forth. This study investigated the use of a decision aid* the Analytic Hierarchy Process. The results of this study provide information as to the usefulness of the AHP in real situations calling for the evaluation of the potential for financial fraud.

tFurthermore* the AHP is only recently beginning t? receive attention as a tool for modeling judgment in complex situations. This study advances the use of the AHP in the auditing literature. In addition* it provides additional insight into the advantages and disadvantages of the AHP as a methodology* for the benefit of future research in audit judgment.

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

15

SummaryThis chapter has presented a general overview of

the study. The role of the internal auditor in the detection of -financial fraud has been described. In addition* the research questions and methodology have been summarized. The remaining chapters will present a review of the relevant literature* a detailed description of the methodology* analysis of the data* and conclusions of the research.

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

CHAPTER S REVIEW OF THE LITERATURE

The purpose of this chapter is to review and summarize the literature relevant to this research study* as well as to demonstrate how the current project will contribute to the literature. Areas of research relevant to this purpose include:

1. Applications of the Analytic Hierarchy Process (AHP) in accounting and auditing.

S. Attempts to measure the importance of red flags.

Applications of the Analytic Hierarchy Process in Accounting

The AHP is applicable to a wide variety of decision problems* and has received attention as a decision aid in fields such as health* politics* marketing* and education (Zahedi 1986* lOl). The application of the AHP in accounting-related research has been fairly recent* and has been primarily associated with auditing. This section of the literature review will evaluate two published and three unpublished research studies in the accounting literature. These studies represent a review of applications of the AHP in accounting. In addition* a

16

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

17

brief review of the criticisms of the AHP is presented.

Arr ington* Hillison* and JensenArrington* Hillison* and Jensen (1984) were the

first to publish an auditing application of the AHP. The major objective of their study was to introduce the AHP as a technique to model the judgment of auditors. To accomplish this end* they used a small sample of auditors in an Analytical Review Procedure (ARP) task.

The authors attempted to determine how auditors weight multiple attributes to select ARPs (Arrington* Hillison* and Jensen 1984* 899). Previous research typically examined only one dimension of the choice of ARP* such as predictive accuracy of the model. The AHP allows for examination of many dimensions that enter the decision simultaneously. The hierarchy developed hy Arrington* Hillison* and Jensen (1984* 300-301) is included in Figure 2-1.

Six subjects were used in this study* 3 academicians and 3 practitioners* and all were considered experts in analytical review procedures and had extensive auditing experience. The actual task was divided into 8 distinct phases. In the first stage* subjects were asked to make all possible pairwise comparisons of the attributes in level 1 of the hierarchy using Saaty’s (1988* 54) response scale. These responses allowed the researchers to use the AHP to generate dominance matrices

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

18

and priority weights for each attribute for each subject. The second stage of the task required the subjects to make paired comparisons of each alternative with respect to each attribute. For example* they compared Box- Jenkins to Random-Walk with respect to Statistical Performance using the Saaty (1988* 54) response scale.

Level 0 Selection of Analytical Review Procedure(Objective)Level 1 Statistical Performance

Model Robustness Ease of Application Understandab i1i ty Costs

Regression (54 quarters in base period) Regression 0 6 quarters in base period) Box—Jenkins Random-Walk Random-Ua1k-Dr i ft

Figure 2-1. Analytical Review Procedure Hierarchy.

The final phase of the study was performed by the researchers* and resulted in the ranking of the alternatives by subject and on average. This procedure entailed multiplying the weights derived in stage one by the result obtained in stage two to generate overall rankings for each ARP alternative. The rankings represent the selection of ARP made by subjects when all 5 of the hierarchical attributes were simultaneously evaluated.

Consistency ratios for each subject were less than

Level 2 (Alternatives)

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

19

the .10 threshold established by Saaty (1988* 21)*indicating that the subjects Mere fairly consistent intheir own judgmental process. Howeverf little agreementMas noted betMeen experts in the selection of ARP*although the 2 Regression Models and Random-Walk modelMere preferred to Box—Jenkins and Random-Walk—Drift.

The authors concluded that the AHP is a very usefultool for modeling auditor judgment* especially Mhenqualitative attributes are integral to the decisionprocess. The AHP is particularly Mell-suited formodeling multiple attributes and for determining theimportance of individual attributes. This study islimited in that only (a subjects were employed* however*this action is appropriate in an exploratory study. Tosum* the authors note:

AHP is applicable to any number of auditing processes in which qualitative* nonmetric dimensions influence the quality of professional judgments. . . . such as materiality* internal control evaluation* opinion qualifications* and strategic planning (Arrington* Hillison* and Jensen 1984, 309).

Lin* Mock* and Wright Lin* Mock, and Wright (1984) demonstrated the use

of the AHP as an aid in planning audit procedures associated with accounts receivable. Similar to the Arrington, Hillison* and Jensen (1984) study, this paper was an attempt to introduce the AHP as a technique for modeling the judgment of auditors. Although they did not

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

20

carry out a full-scale study* they demonstrated how the AHP would work in an actual research setting. The hierarchy they structured is quite simplistic* and is detailed in Figure 2-2 (Lin* Mock* and Uright 19B4, 93* 94).

Level 0 Selection of Audit Procedure for Accounts(Objective) ReceivableLevel 1 Reliability Cost Validity

Level 2 Analytical Review(Alternatives)

Confirmations Test of Subsequent Collections

Figure 2-2. Accounts Receivable Hierarchy.

To carry out this hypothetical study* subjects would be required to make all possible pairwise comparisons of the attributes on Level 1. In addition* all possible pairwise comparisons of Level 2 with respect to each Level 1 criteria would be required. The Saaty (1988* 54) response scale would be used to measure the judgments.

Lin* Mock* and Wright (1984) intended that their paper be used to introduce the AHP as a potentially powerful tool for modeling auditor judgments. Theysummarized by stating?

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

S I

. . . this approach offers the potential for greater rigor and efficiency when compared to traditional heuristic evidence evaluation procedures. The AHP is also relatively easy to apply and understand and usually requires limited decision maker time (Lin, Mock, and Uright 1984,96) .

HarperHarper (1964) used the AHP in his DBA dissertation

at Florida State University. He modeled EDP auditor judgment of internal controls in Local Area Networks (LANs). A LAN is a popular configuration of microcomputei— workstations linked together in one installation. Since LANs represent a fairly recent development in computer installations, the internal controls in place may differ from more traditional settings.

One of Harper’s (1984, 83) principal research objectives was to identify the internal accounting controls unique to a LAN in a sales transaction processing setting. Five EDP auditing experts from Big Eight accounting firms were interviewed by the researcher and resulted in the identification of 17 internal control attributes appropriate to a LAN (Harper 1984, 88-89). Based on the outcome of this phase of the research, a hierarchy was developed and is included in Figure 2-3 (Harper 1984, 91).

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

22

Level 0 Evaluation ef Iateraal Control(Objective}Level 1 Uurkstation Processing Data 1 Prograa Supervisory

Controls Controls Security ControlsLevel 2 PM w t r r Rtfuniy LOSS

InitTr PRICE CeopCode KeyPersSDOCS R-fi QMN6E PAPERMkRs OUTPUT BkUp

RsBiskPuMnt

PM - Nulti-level passwords InitTr = Initiation of transactions SOOCS = Source Documents HkRs = Uortstation restrictions INPUT = Input controls R-fl = Run-to-Run controls

PRICE - Pricing controls OUTPUT = Output controls PuMnt = Passuord naintenance

RdOnly = Read-but-not-urite protection Conpcode = Coepiled prograa code CHANGE = Control of nontransactional changes BkUp = Backup and recovery

RsBisk = Physical restriction to disks LOGS = Cooputer logs

Keypers = Monitoring of key persons PAPER = Hard-copy docunents

Figure 2-3. Hierarchy of Internal Controls in a LAM.

ft second important research objective involved the determination of the relative importance to individual auditors of the internal accounting controls identified by the 5 Big Eight auditors (Harper 198<»f 83). The AHP was used to model EDP auditors* judgments within the context of the hierarchy described in Figure 2-3. The subjects consisted of a nationwide sample of experienced EDP auditors employed with Big Eight firms. A total sample of 51 subjects represented a 60 percent response rate to the mailed questionnaire. The questionnaire consisted of a series of pairwise comparisons at levels 1 and 2 o* the hierarchy! measured with Saaty*s (1988i 5b)

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

23

response scale. Note that in this particular study* the subjects were not asked to select among alternatives as in the Arrington* Hillison* and Jensen (19B4) or Lin* Mock* and Wright (1904) studies.

Once the individual subject’s AHP models were developed* consensus vss measured by computing intei—

rater correlations for every pair of EDP auditors. The result of the correlation analysis indicated consensus to be quite low (Harper 1984* 134—135)* suggesting that the EDP auditors failed to agree on the relative weights placed on the importance of the various controls in the hierarchical model.

Harper’s efforts represented an initial attempt to use the AHP to model the judgment of auditors in a computer processing environment. Additional research in this area should be directed toward refinement of the hierarchy and investigation into the implications of the low consensus measures. This exploratory study has generated an initial AHP model that should be subjected to further research.

SingletonSingleton (1985) used the AHP in his Ph.D.

dissertation at Louisiana State University. The focus of his study was to examine the qualitative characteristicsset forth in Statement of Financial Accounting Concents No . 2 ; Qualitative Characteristics of Accounting

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

24

Information (FASB 1980). He specifically analyzed them to determine if they are operationalf comprehensive! and parsimonious.

The AHP did not serve as the primary methodology in his study. Rather( he applied it to generate weights for linear models that were used to predict each subject’s choice of accounting method. The AHP was used to compute priority weights for the level 1 categories and for each of the nine level 8 qualitative characteristics examined. Subjects were asked to make all possible pairwise comparisons of the characteristics using Saaty's (1988!54) response scale. The hierarchy established for purposes of Singleton’s (1985) study is included in Figure 8-4.

Level 0(Objective) Decision Usefulness

Level 1 Relevance Reliability

Level 8 Predictive value VerifiabilityFeedback value NeutralityTimeliness ComparabilityComparability Representational

faithfulness

Figure 8-4. Hierarchy of Qualitative Characteristics.

McDermottMcDermott (19Bfe) used the AHP in her Ph.D.

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

25

dissertation at the George Washington University. She studied EDP auditor judgment of the internal accounting control system in a microcomputer environment. Her research was specifically directed to generating a working AHP model of EDP auditor judgment of internal controls in an effort to reduce the subjectivity associated with such reviews.

The initial phase of this research involved the development of the AHP hierarchy based upon a thorough review of the relevant literature. The result was a working AHP model consisting of four levels in the hierarchy:

Level 1: Focus — A Strong Internal Accounting ControlSystem

Level 8: Factors — Special Control ConsiderationsLevel 3: Scenarios — Risks/ExposuresLevel A: Sub-Factors — Controls/Compensating Controls

Thirty-five cues were incorporated into the hierarchy:6 on level 2> 6 on level 3* and 83 on level A (McDermott 1906, 73-78).

The second phase of this study involved the use of a questionnaire to which 39 EDP auditors responded, representing a 78 percent response rate (McDermott 1986, 93). These auditors were asked to select the 5 most important cues associated with each factor on each level of the hierarchy. The results were used to modify the working AHP model into a refined AHP model. While the

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

86

latter retains the same -Four levels as the original hierarchy* the components of the model were revised to reflect the subjective judgment of the expert EDP auditors.

The third and final phase of the study was to test the refined model (McDermott 1986* 111-118). Three EDP auditors who had participated in the second phase of the study were used to make all possible pairwise comparisons of attributes at each level of the hierarchy with respect to its immediate criteria. Expert Choice (Decision Support Software 1983) software was used which incorporates Saaty's (1988* 54) response scale in making the judgments as to the relative importance of each item in the pairs. Local and global weights were computed for each cue for each of the 3 subjects. Results suggest little agreement between subjects as to the relative importance of elements in the hierarchy. The sample size was too small to draw inferences.

McDermott's (1986) study provided a contribution to the literature in that it represented an attempt to use the AHP to model auditor judgments. She reported that the model is a general one that is suitable for further study of its potential application in practice. The subjects involved in the study were positively impressed by the use of the AHP as a judgment aid.

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

£7

Criticisms of the Analytic Hierarchy Process

Lin (1987, 4) notes that the AHP is becoming the most frequently used method to elicit judgments. The major limitation he observes is that the number of pairwise comparisons can become unwieldy as the quantity cf attributes in the model becomes large. However, Saaty (1986, 33) contends that no more than 5 to 9 attributes should be examined at a given level of the hierarchy, since the human mind is generally incapable of processing more. If the researcher adheres to this rule, the task should remain manageable.

Dyer and Uendell (1984/85) are especially critical of the AHP. They observe that the rankings of alternatives may be arbitrary in some instances. This premise is illustrated in their paper by introducing an irrelevant alternative into their AFP model that alters the ranking of the alternatives. This is viewed as a shortcoming of the AHF since irrelevant information should be excluded from the solution. However, they note that when correct attributes are incorporated into the model, the results from the AHP approximate a correct solution (Dyer and Uendell 1984/85, 31).

Studies of the Importance of Indicators of Fraud

Two studies appear in the literature that attempt to measure the importance of red flags in the auditor’s

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

28

judgment of the potential for fraud. One deals with red flags associated with employee fraud (i.e.* embezzlement) and is based on information acquired from actual case studies involving internal auditors. The second study investigated financial fraud and obtained data from partners in CPA firms.

Albrecht* Howe* and RomneyIn their 1964 study* Albrecht* Howe* and Romney

attempted to rank the importance of red flags of employee fraud or embezzlement. Based upon a review of the literature* the authors developed a list of 50 potential indicators (red flags) of employee fraud. These red flags were incorporated into a questionnaire that was mailed to internal auditors representing 325 different companies that had experienced employee fraud and had agreed in advance to participate in the study".' Only 212 of the internal auditors returned usable responses (Albrecht* Howe* and Romney 1984* 14).

The questionnaire asked each subject to provide detailed information on the fraud that had actually occurred in his or her company* including perpetrator characteristics as well as organizational conditions that may have allowed the fraud. This demographic data was used to determine if relationships exist among variables (e.g.* education level of perpetrator with amount of the fraud). Significance of these relationships was measured

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

29

with the Chi-Square statistic.The second and third parts of the questionnaire

asked subjects to evaluate two sets of' red flags. One set was a list of 85 perpetrator characteristics* and the other was a list of 85 organizational characteristics.The evaluation was with respect to the fraud reported by the subject company. Each red flag was rated on a 7- point Likert scale (Strongly disagree to Strongly agree!.For example* one question was "The perpetrator(s) had unusually high personal debts*" to which the subject would respond with his or her level of agreement (Albrecht* Howe* and Romney 1984* 30).

The researchers generated a wealth of statistics from this questionnaire survey. A significant finding of their study was that perpetrator characteristics were not consistent across fraud cases. Nonetheless* the authors suggest that the information presented should be useful to internal auditors in their efforts to deter and detect employee fraud.

Albrecht and Romney In a study similar to Albrecht* Howe* and Romney

(1984)* Albrecht and Romney (1986) attempted to validate a list of 87 potential red flags of management or financial fraud. The red flags used in the study were constructed from an extensive review of fraud-related literature. Since no attempt had previously been made to

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

30

validate red-flag lists used by auditors in practice* a primary purpose of the research Mas to assess the predictive ability of red flags.

The research hypothesis Mas that red flags have predictive ability if they appear in fraud situations and do not appear in no-fraud situations. In an effort to make this determination* the authors developed tmo questionnaires. One Mas sent to audit partners on engagements Mhere fraud had not been found. The second questionnaire Mas mailed to audit partners on engagements that had experienced financial fraud. The partners Mere asked to respond Mhether each of the 87 red flags Mas present* absent* or if they did not knoM. In addition* each was asked to rank the 5 most salient red flags on the fraud engagements (Albrecht and Romney 1986* 325- 326).

The proposed sample consisted of asking 20 CPA firms to complete 20 questionnaires each* 10 fraud clients and 10 no-fraud clients. In addition* since the researchers were unable to identify 10 fraud clients for each of the firms* they asked that these firms send remaining fraud questionnaires to "partners of their choice who had experience with management fraud." Of the 200 fraud questionnaires delivered* 27 responded. Thirty-six of the no-fraud group returned their questionnaires (Albrecht and Romney 1986* 325—326).

Using the Chi-Square statistic* the researchers

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

3 i

'found that significant differences between the fraud andno-fraud groups existed with only 31 of the 87 red flags.Howeveri some of the red flags proved to be untestabledue to infrequency of occurrence. The significant redflags consisted of both personal factors and companyfactors. Auditor perceptions of the 5 most salient redflags were (Albrecht ana Romney 19S6'i~33H>:

Too Much Trust in Key Executives Key Executives Living Beyond Means Domination of the Company by One or Two Strong

Individuals Inadequate Internal Control System Significant Related-Party TransactionsThe results of this study should be viewed with

caution. The sample size was quite small* suggesting thatthe results are not necessarily generalizable. Inaddition* since many of the red flags proved to beuntestable* no conclusion can be drawn with respect totheir predictive ability.

Relevance of the Current Study to the Literature

Judgment Studies of Internal Auditors

Published studies attempting to model the judgmentof internal auditors are scarce in the auditingliterature. The importance of judgment research wasstressed by Libby (1981* 8-3):

Why should accountants be interested in individual judgment and decision making? The general answer is that decision making is an intrinsic part of the current practice of accounting. . . . The quality

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

32

of these decisions* among others* will determine the accountant’s success in the marketplace.Whether accountants are concerned with their own or others’ decisions* the focus of their concern is on the improvement of decisions.

Libby (1981* 3) suggests that three options are availablefor the improvement of decisions:

1. Change the information.S. Educate the decision maker to change the way he

or she processes information.3. Replace the decision maker with a model.

This study will focus on options S and 3. First* byidentifying how an internal auditor perceives theimportance of red flags* areas for potential improvementof the judgment process can be suggested. Second* theAHP may serve as a decision aid to the internal auditorin his or her efforts to assess the potential forfinancial fraud.

This study will fill a void in the literature inthat it represents an initial attempt to model thejudgment of internal auditors. Since judgment studies ofinternal auditors in other task settings are scarce* thisstudy will serve to stimulate research into the judgmentof internal auditors in general. This aspect of theresearch is especially important in view of the criticalrole internal auditors play in the performance of theaudit function.

Studies of the Importance of Red Flags

Only two studies appear in the literature that

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

33

examine the importance of red flags. These research efforts are actually post mortem analyses of actual fraud cases* and do not represent the judgment of auditors or others as to the importance of the red flags. In addition* the sample sizes in these studies were quite small* compromising the generalizability of the results.

Treadway (1987, 154-163) and the AICPA (1988, 4-5> have generated comprehensive lists of red flags of financial fraud following lengthy investigations. This study will attempt to determine whether internal auditors perceive these red flags as relevant to the assessment of the potential for financial fraud. Furthermore* the relative importance of the various red flags will be evaluated. The findings from this research will provide the means for internal auditors to improve their decision processes with respect to the assessment of the potential for financial fraud.

Use of the AHP to Model the Judgment of Internal Auditors

The use of the AHP in accounting and auditing is still in its infancy. Studies employing the AHP have only appeared in the literature since 1984* and have been exploratory in nature. This research effort will extend the AHP beyond the exploratory stage to a full-scale study of internal auditor judgment. In addition* this study will be the first AHP study to examine internal auditors in particular.

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

CHAPTER 3 METHODOLOGY

The purpose of this chapter is to outline the research methodology used in this study. The research questions and related hypotheses are discussed first* followed by a detailed explanation of the data collection prucess in the second section. The third section offers a complete description of the Analytic Hierarchy Process (AHP) along with its relevance to addressing the research questions. The fourth section describes statistical tests that were employed to test the research hypotheses.

Research Questions This study was directed toward obtaining evidence

to answer three specific research questions. These research questions relate to the overall purpose of investigating the judgment of the internal auditor on the importance of indicators (red flags) of the potential for financial fraud. Each question* a discussion of its importance* and its related research hypothesis* if applicable* follows:1. How do internal auditors perceive the importance of

the red flags that indicate the potential for financial fraud?Roth thp ATCPA (1908- A—5) and the Treadway

Commission (1987* 15A-163) have generated comprehensive

3 A

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

35

red-flag lists that are in general agreement. The importance of the red flags relative to one another was evaluated using the AHP to determine whether any are considered to be more important than others. Figure 3-1 presents the red flags evaluated in this study. Since neither the AICPA nor the Treadway Commission prioritized the red flags they have identified* this study offers the first attempt to do so from the internal auditor's perspective.S. Are explicit judgments made by an internal auditor

in hypothetical firm descriptions consistent with the implicit judgments made by the corresponding AHP model?This question addressed the ability of the AHP

model to operate as a judgment aid to the internal auditor. In developing the judgment model* the internal auditor was asked to evaluate individual red flags. However* in real situations* they may be confronted with many red flags simultaneously. This question considered whether the internal auditor's modeled judgment is consistent with explicit judgments made in hypothetical case situations. It was* in fact* a test of the AHP model. The research hypothesis associated with this question (stated in the null form) was (for each sub ject):

HI: There is no agreement between the explicitranking of firms by a subject and the implicit rankinq of firms by the subject’s AHP model.

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

36

3. Do internal auditors achieve consensus in their weighting of the importance of the different red flags and categories of red flags?Consensus is a measure of the degree to which the

internal auditors agree with each other on the weightsthey have assigned to the importance of the different redflags. As Libby (1981* 31) notes* "where the lack ofobjective criterion data makes the direct measurement ofachievement impossible* the consensus judgment of expertsoften serves as a substitute criterion." He also remarksthat when the auditor's judgment is challenged* defenserequires that generally accepted or consensus procedureswere followed.

In this study* consensus was measured at bothlevels 1 and 8 of the hierarchy depicted in Figure 3-1.Level 1 represents general categories of red flagcharacteristics. Level 8 provides more specific detailfor each of the level 1 categories. This researchquestion was concerned with the degree to which theinternal auditors agree on the ranking of the importanceof the level 1 categories as well as the ranking of thespecific red flags within each category.

The following research hypotheses (stated in thenull form) directly addressed consensus of internalauditor judgment (Figure 3-1):

H8: Internal auditors fail to achieve consensusin ranking the importance of the level 1categories of red flags that indicate thepotential for financial fraud.

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

37

H3: Internal auditors fail to achieve consensusin ranking the importance of firm characteristics that indicate the potential for financial fraud.

HA: Internal auditors fail to achieve consensusin ranking the importance of industry characteristics that indicate the potential for financial fraud.

H5: Internal auditors fail to achieve consensusin ranking the importance of management characteristics that indicate the potential for financial fraud.

Collection of the Data The Subjects

The subjects used in this study Mere practicing internal auditors. Since this study Mas an effort to model the judgment of internal auditors; the use of these subjects ensured they were trained and experienced in the profession of internal auditing. Furthermore* prac v iCi ny internal auditors should be familiar with promulgated literature on financial fraud such as SIAS No. 3 (IIA, 1985) and the Treadway Report (1987).

As will be explained in a later section* the task was administered in two phases to minimize the possibility that the subjects would be sensitized to the research questions. As a result* the task was administered to the subjects in person. The subjects were obtained by gaining access to educational seminars* professional meetings* and firms. The task was also completed by internal auditors visiting the Louisiana

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

38

Level 0 Evaluation of Potential for Financial Fraud

Level 1 FireCharacteristics

IndustryCharacteristics

IbnageaentCharacteristics

Level 2 Frequent and significant transactions involving unusually difficult or coupler calculations (FC1)The elistence of financial stateaest elenents that depend heavily on the exercise of subjective judgnent (FC2)Organization is decentralized uithout .adequate oonitoring (FC3)

Profitability of entity relative to its industry is inadequate or inconsistent (ICllDirection of change in entity's industry is declining uith nany business failures (IC2)

Rate of change in entity’s industry is rapid (products! services* lines of business! or scifeods of operating! (IC3i

Sensitivity of operating results to econoaic factors (inflation« interest rates! is high (FCh)Solvency probleos or other natters that bring into question the entity’s ability to continue in elistence are present (FC5)Material related-party transactions (FC4)

Nanagenent operating and financial decisions are doninated by a single individual (NCI)Nanagenent’s attitude touard financial reporting is unduly aggressive (HC2)

Nanageuent turnover is high* particularly senior accounting personnel (HC3iNanagenent’s coapensation is tied to reported earnings (Ntt)Nanageoent places undue enphasis on seeting earnings projections (SC5)

Level 3 Evaluation of Alternative Fins Alpha Coapany* Sanaa Goapaayi Oaega Coapanyi Zeta Coapany

Figure 3-1. Hierarchy of Red Flags that Indicate the Potential for Financial Fraud.

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

39

State University campus in conjunction with the Internal Audit Pilot School. The subjects represented various industries* experience levels* educational backgrounds* and geographical locations.

The TaskThe subjects Here provided with an instrument

consisting of two distinct parts. The first part requested that the subjects read four short individual case studies about hypothetical companies* nherein specific red flags mere varied (Figure 3-1). A subsequent section describes how these cases were constructed. After reading the cases* the subjects were asked to make all possible pairwise comparisons of the cases with respect to the following question using Saaty’s (1988* 54) response scale:

Which company has the greater potential for theoccurrence of financial fraud?

This phase of the task provided data on the explicit judgment of the internal auditors necessary to address the second research question and HI.

Immediately after the first part of the instrument was collected* the second part was administered. The subjects were asked to make pairwise comparisons of the individual red flags by using Saaty’s (1988* 54) response scale. These responses generated the AHP model* the weights placed by the subjects on each red flag* and the implicit judgments. This data enabled the researcher to

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

40

completely address the first and second research questions and HI.

A complete copy of the research instrument is included in the appendix. The actual instrument was prepared in booklet form with the following pages facing each other:

Part I: pages 8 and 3* A and 5* 6 and 7Part II: pages 1 and 8* 3 and 4* 5 and 6*

7 and 8* 9 and 10Close inspection of this instrument reveals why theresearcher administered it in two phases. If the secondphase been administered first* the subjects would becued to look for the specific red flags in the casestudies. However* by administering the case studiesfirst* the subjects did not have the opportunity toadjust their responses based on the subsequentinformation* which is more explicit. The case studieswere written in such a way that the specific red flagswere disguised* and they did not appear to be a strongcue to the subjects in completing the task.

The subjects were also requested to supply some demographic data. While no specific hypotheses were designated for using this data* it assisted the researcher in interpreting results obtained in testing Hi through H5. In addition* the subjects were given an opportunity to express their opinion about the instrument and the importance of the subject matter.

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

41

Finally* two versions of the instrument were used to vary order of presentation. The results were compared to determine whether order had an effect on the responses or not. Previous studies using the AHP indicated that order of presentation did not present any difficulty for the researcher.

The Analytic Hierarchy Process Overview

The methodology used in this study was the Analytic Hierarchy Process (AHP) advanced by Saaty (1986*1988).The AHP is a technique for modeling judgments and for providing the decision maker with a means to choose among alternatives. This approach is especially well-suited to situations involving qualitative attributes.Furthermore* the AHP can handle complex judgment tasks involving interrelated cues with varying degrees of impact on the decision.

Saaty (1986* 17-18) discusses how natural principles of analytic thought underlie the AHP. Saaty and others theorize that humans tend to structure reality into pieces of homogeneous information in a hierarchical manner. Analysis is more manageable when a complex task is reduced to comparison of pairs of items so that priorities of importance may be established. As Saaty (1986, 18) states:

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

48

The analytic hierarchy process incorporates both the qualitative and the quantitative aspects of human thought: the qualitative to define theproblem and its hierarchy and the quantitative to express judgments and preference concisely. The (analytic hierarchy) process is designed to integrate these dual properties.The AHP combines both the deductive and the systems

approach to understanding complex problems. Saaty (1986* 6) notes:

The AHP enables us to structure a system and its environment into mutually interacting parts and then to synthesize them by measuring and ranking the impact of these parts on the entire system.

The AHP* therefore* provides a structured approach tojudgments by eliminating confusion brought about by"piecemeal explanations arrived at through deduction"(Saaty 1986* 6).

The AHP has emerged as a potent tool for makingjudgments. It Mas created to accommodate both logic and

» • ■»- wpersonal values without forcing the judge to think in a manner that is unnatural. Mental agility* background* and wisdom are used to develop the hierarchy of the problem while logic* intuition* and experience provide the judgments (Saaty 1986* 88). As such* there exist many advantages to the use of the AHP to model expert judgments. Figure 3-8 provides a summary of the positive aspects of the AHP (Saaty 1986* 83).

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

43

Unity:Thn AHP provides a single, easily understood, flexible model (or a wide range of unstructured problems

Process Repetition:The AHP enables people to refine their definition of a problem and to improve their judgment and understanding through repetition

Judgment and Conaensus:The AHP does not insist on consensus but synthesizes a representative outcome from diverse judgments

Tradeoffs:The AHP takes into consideration the relative priorities of factors in a system and enables people to select the best alternative based on their goals

Synthesis:The AHP leads to an overall estimate of the desirability of each alternative

Complexity:The AHP integrates deductive and systems approaches in solving complex problems

The AHP can deal with the interdependence of elementsin a system and dess net insist on linear thinking

Hierarchic Structuring: The AHP reflects the natural tendency of the mind to sort elements of a system into different levels and to group like elements in each level

Measurement:The AHP provides a scale for measuring intangibles and a method for establishing priorities

Consistency:The AHP tracks the logical consistency of judgments used in determining priorities

Figure 3-2. Advantages of the Analytic Hierarchy Process. Reprinted* by permission* from Thomas J. Saaty*Decision Making for Leaders (Pittsburgh:University of Pittsburgh* 1986)* 23.

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

Structuring a HierarchyFundamental to the application of the AHP is the

development of a hierarchy that structures a system into its component parts. Hierarchies are created to direct a system toward a desired goal or objective. The top level of' the hierarchy represents the broad objective of the judgment. Subsequent levels of the hierarchy represent homogeneous clusters of attributes related to their immediate criterion. The bottom level of the hierarchy consists of the alternatives available.

Since no specific rules exist for developing a hierarchy, thoughtful consideration must enter into its preparation. The development of the hierarchy for this project drew heavily from the comprehensive red-flag lists published by the Treadway Commission (1987, 154- 163) and the AICPA (1988, 4-5). The red flags that appear in the hierarchy are Horded in essentially the same manner as these sources. Fortunately, the amount of judgment necessary is minimized in this case since the red flags tend to follow a natural hierarchy. The hierarchy used in this study is included in Figure 3-1.

Level 0 represents the overall objective. In this study, it is the evaluation of the potential for financial fraud. Level 1 establishes three general groupings of characteristics that should be considered in the evaluation of the potential for financial fraud according to Treadway (1987, 154—i63) and the AICPA

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

45

(1988, 4-5). Level S provides more detail with respect to each grouping of characteristics. Finally, level 3 consists of the alternatives available to the judge.

The level 3 alternatives represent hypothetical firms. Each firm reflects one set of red flag characteristics as being dominant, with the exception of the Zeta Company, which demonstrates the absence of any red flags The red f 1 rr; characteristics associated with each firm are as follows:

Alpha Company: Management CharacteristicsGamma Company: Industry CharacteristicsOmega Company: Firm CharacteristicsZeta Company: Absence of Red Flags

The AHP model formed by the subjects made an implicit selection of the firm with the most potential for financial fraud based upon the importance placed by the subject on each red flag. For example, a subject who weighted Firm Characteristics as being most important in the evaluation of financial fraud generated a model that selected Omega Company, since that category of red flags is clearly dominant.

As described, the subjects were previously asked to make explicit judgments as to the firm with the most potential for financial fraud. This wes accomplished by asking the subjects to read each case description and develop priority rankings using Saaty’s (1988, 54)

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

46

response scale. Data gathered -from these tasks was used to address the second research question.

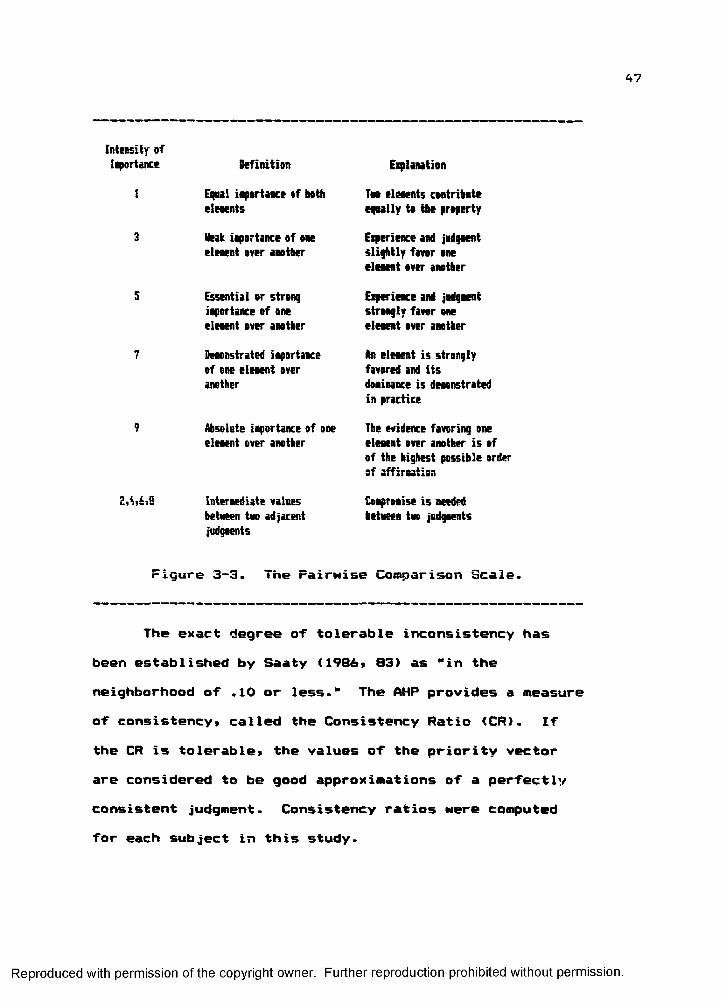

The Measurement Scale Saaty has developed a ratio measurement scale for

purposes of implementing the AHP (1988* 54). This scale* bounded at one and nine* is reproduced in Figure 3—3.The purpose of the scale is to establish weights as to the relative importance of each element in the hierarchy* to evaluate the consistency of the judgment (discussed below)* and to come to a decision.

Consistency Ratio Saaty (1986* 82-85) discusses the relevance of

judgment consistency to the AHP. In this sense* consistency refers to transitivity and magnitude. For example* if A is preferred to B by a multiple of 3* and B is equally preferred to C» then A should be preferred to C by a multiple of 3. However* as Saaty notes* humans violate consistency routinely for many reasons. For example* they may feel differently over time about the topic* or new information may cause them to change their opinions. If humans were perfectly consistent* they would not be permitted to change their minds or to accept new ideas. As a result* some judgment inconsistency must be tolerated.

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

Intensity ofIiportance Definition Explanation

1 Equal importance of both eleoents

Tut eleients contribute egnally to the property

3 Ueak iiportance of one elenent over another

Experience and judgient slightly favor one eleient over another

5 Essential or strong iiportance of one eleient over another

Experience and judgient strongly favor one eleient over another

7 Demonstrated importance of one eleient over another

An eleient is strongly favored and its doiinance is demonstrated in practice

9 Absolute iiportance of one eleient over another

The evidence favoring one eleient over another is of of the highest possible order of affirsatisn

a,4,4,5 intermediate values betmeen tuo adjacent

Coapromise is needed betneen tno judgments

judgments

Figure 3-3. The Pairwise Comparison Scale.

The exact degree of tolerable inconsistency has been established by Saaty (1986* 83) as "in the neighborhood of .10 or less." The AHP provides a measure of consistency* called the Consistency Ratio (CR). If the CR is tolerable* the values of the priority vector are considered to be good approximations of a perfectly consistent judgment. Consistency ratios were computed for each subject in this study.

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

48

Priority MatricesThe initial step toward the establishment of

priorities in an AHP model is to make pairwise comparisons against a given criterion. Saaty (1986* 76) demonstrates that the matrix is the favored approach for this analysis since it is able to identify the dual aspects of priorities. That is* one element is dominated and the other is dominating.

To carry out the pairwise comparison process! a matrix is prepared at each level of the hierarchy for each criterion. The matrices for this research study are shown in Figure 3-4i and should be read in conjunction with the hierarchy in Figure 3-1. Gnes are placed on the diagonals since an element compared to itself is of equal significance. Pairwise comparisons were made by comparing the left-hand element with the column element.For example> in the Level 1 matrix! the subject was asked to measure the relative importance of Industry Characteristics to Firm Characteristics using the Pairwise Comparison Scale in Figure 3-3. If the subject believed that Industry Characteristics are absolutely more important than Firm Characteristics in the evaluation of the potential for financial fraud! then a 9 would be placed in row 3, column 1. Alternatively! the reciprocal value! l/9i should be placed in row li column 3. This process continued for all possible pairwise

Reproduced with permission of the copyright owner. Further reproduction prohibited without permission.

49

comparisons in each matrix. The general rule is that C(n x n — n)/ai comparisons must be made in each matrix.