Embed Size (px)

Citation preview

AANN IINNTTEERRNNSSHHIIPP RREEPPOORRTT

OONN

HABIB BANK LIMITED CORPORATE

CENTER FAISALABAD

BBYY

AASSMMAA YYAASSIINN

A REPORT SUBMITED IN PARTIAL FULFILLMENT OF THE

REQUIREMENT FOR THE DEGREE OF

MASTER IN BUSINESS ADMINISTRATION (MBA)

DEPARTMENT OF BUSINESS MANAGEMENT SCIENCES

UNIVERSITY OF AGRICULTURE FAISALABAD

EXECUTIVE SUMMARY

My department requires this report. The purpose of report is to write down all the major

activities that I performed in that particular branch during my internship training. It

Comprises of:

Formal part

Introduction of the organization

SWOT Analysis

PEST Analysis and Environmental Scanning

Products and services

Deposit department

Remittance department

Export Refinance Scheme (Part 1, Part 11)

Import and export department

HRM department

Credit and administrative department

Financial Analysis of the client

Work done by me

Suggestions and recommendations

CONTENTS

Sr. No. Title

1. Executive summary

2. Contents

3. Acknowledgement

4. Introduction

5. Products of HBL

6. SWOT and PEST Analysis

7. Span of management

8. Departmentalization

9. Financial Analysis of the Client

10. Suggestions

Acknowledgment

All praises belong to almighty Allah who the supreme authority knows the ultimate relation

underlying all sorts of phenomenon going on in this universe & whose blessing & exaltation

flourished my thought & thrived my ambitions to have the cherished fruit of my modest

efforts my humblest thanks to the Holy Prophet Hazrat Muhammad (PBUH) who is forever a

torch of guidance & knowledge for humanity as a whole.

We deem it our utmost pleasure to avail this opportunity to express gratitude &

deep sense of obligation to my revered teachers and HBL‟s relationship manager Mr.

Zaiuddin and Mr.Waseem Bhati for their valuable and dexterous guidance, untiring help,

compassionate attitude, kind behavior, moral support and enlightened supervision during this

whole project.

Finally, I would like to extend hurtful thanks to my adoring parents and friends for their day

and night prayers sacrifices and encouragement, moral and financial support throughout the

course of our study.

May all of them live long and enjoy a happy life!

BANKS AND SCOPE OF BANKING

WHAT IS BANK?

A bank is an institution for the custody, loan or exchange of money for sanctioning

credit, for transferring funds by domestic foreign bills of exchange. It is a pipeline through

which currency moves into and out of circulation.

As it is clear from the definition of banking, the main activity or function of

banking is borrowing and lending of money with a margin of gain. However, as far as the

present day banking is concerned, there are a number of different banks, set up under specific

different objectives, performing various functions.

INTRODUCTION OF HBL:

HABIB BANK GROUP is a leader in Pakistan‟s services industry. An extensive

network of 1425 domestic branches the largest in Pakistan and 55 international branches to

meet customer needs. Perhaps the HABIB BANK LIMITED establish in 1941 at Bombay.

But its history starts in 1841 when a young boy name Ismail Habib reach Bombay for job.

After some time he got the job with a dealer in utensils and non ferrous metals.Ismail Habib

was very keen and intelligent and became partner of his boss. Later on he was elected as a

president of the market. Many years later he expended his business. He engaged in private

banking. So‟ HBL has come a long way from its modest beginnings in Bombay in 25 august,

1941 when it commenced business with a fixed capital of 25000 rupees.

Impressed by its initial performance, Quaid-e-Azam Muhammad Ali Jinah asked the

bank to move its operation to Karachi after the creation of Pakistan, HBL establish itself in

the Quaid‟s city in 1943 and became a symbol of pride and progress for the people of

Pakistan. During the early days of newly born state, government of Pakistan faces the great

problem of fund shortage. This time HBL again helped the governance of Pakistan and came

to rescue to provide Pakistan with assistance of no t less than 8 crore.

Besides this, HABIB BANK has been a pioneer in providing innovative banking

services such as first installation of mainframe computer in Pakistan followed by ATM and

more Internet banking facilities in all branches. The main strength of HBL brand is its great

services to all customers especially to the corporate customers and its prominent head office

building that has dominated Karachi‟s skyline for 35 years.

Mission statement

TToo bbee rreeccooggnniizzeedd aass tt hhee lleeaadd iinngg ff iinnaanncc iiaa ll iinnss tt ii tt uutt iioonn oo ff

PPaakk iiss ttaann aanndd aa ddyynnaa mmiicc iinntteerrnnaa tt iioonnaa ll bbaannkk iinn tt hhee ee mmeerrggiinngg mmaa rrkkee ttss ,,

pprroovviidd iinngg oouurr ccuuss ttoo mmeerrss wwii tthh aa pp rreemmiiuumm ssee tt oo ff iinnnnoovvaa tt iivvee pprroodduucc ttss

aanndd sseerrvviicceess ,, aanndd ggrraanntt iinngg ss uuppeerr iioorr vvaa lluuee ttoo oouurr ss ttaakkeehhoo llddee rrss ––

sshhaa rreehhoo llddee rrss ,, ccuuss ttoo mmeerrss aanndd eemmppllooyyee eess ..

Values of HBL

HHuummiilliittyy::

WWee eennccoouurraaggee aa ccuullttuurree ooff mmuuttuuaall rreessppeecctt aanndd ttrreeaatt bbootthh oouurr tteeaamm mmeemmbbeerrss aanndd

ccuussttoommeerrss wwiitthh hhuummiilliittyy aanndd ccaarree..

IInntteeggrriittyy::

FFoorr uuss,, iinntteeggrriittyy mmeeaannss aa ssyynneerrggiicc aapppprrooaacchh ttoowwaarrddss aabbiiddiinngg oouurr ccoorree vvaalluueess.. UUnniitteedd

wwiitthh tthhee ffoorrccee ooff sshhaarreedd vvaalluueess aanndd iinntteeggrriittyy,, wwee ffoorrmm aa nneettwwoorrkk ooff aa wweellll--iinntteeggrraatteedd

tteeaamm..

MMeerriittooccrraaccyy::

AAtt eevveerryy lleevveell,, ffrroomm sseelleeccttiioonn ttoo aaddvvaanncceemmeenntt,, wwee hhaavvee ddeessiiggnneedd aa ccoonnssiisstteenntt ssyysstteemm

ooff hhuummaann rreessoouurrccee pprraaccttiicceess,, bbaasseedd oonn oobbjjeeccttiivvee ccrriitteerriiaa tthhrroouugghhoouutt aallll tthhee llaayyeerrss ooff

tthhee oorrggaanniizzaattiioonn.. WWee aarree,, tthheerreeffoorree,, aabbllee ttoo aacchhiieevvee aa ssppeecciiffiicc lleevveell ooff ppeerrffoorrmmaannccee aatt

eevveerryy llaayyeerr ooff tthhee oorrggaanniizzaattiioonn..

TTeeaamm WWoorrkk::

OOuurr tteeaamm ssttrriivveess ttoo bbeeccoommee aa ccoohheessiivvee aanndd uunniiffiieedd ffoorrccee,, ttoo ooffffeerr yyoouu,, tthhee ccuussttoommeerr,, aa

lleevveell ooff sseerrvviiccee bbeeyyoonndd yyoouurr eexxppeeccttaattiioonnss.. TThhiiss ffoorrccee iiss ddeerriivveedd ffrroomm ppaarrttiicciippaattiivvee

aanndd ccoolllleeccttiivvee eennddeeaavvoorrss,, aa ccoommmmoonn sseett ooff ggooaallss aanndd aa ssppiirriitt ttoo sshhaarree tthhee gglloorryy aanndd tthhee

ssttrreennggtthh ttoo ffaaccee ffaaiilluurreess ttooggeetthheerr..

CCuullttuurree ooff IInnnnoovvaattiioonn::

wwee aaiimm ttoo bbee pprrooaaccttiivveellyy rreessppoonnssiivvee ttoo nneeww iiddeeaass,, aanndd ttoo rreessppeecctt aanndd rreewwaarrdd tthhee

aaggeennttss,, lleeaaddeerrss aanndd ccrreeaattoorrss ooff cchhaannggee..

PRODUCTS AND SERVICES OFFERED BY HBL

PRODUCTS:

o HBL Muhafiz Rupee Travellers Cheques

o HBL Auto Finance

o HBL Flexi Loans for salaried personnel

o HBL LifeStyles Financing Scheme

o HBL i-Card

o HBL House Financing Loans

o HBL Easy Access

o HBL Fast Transfer

o Haryali Agricultural Loans

o HBL E-Bank

SERVICES:

o Retail Banking

The Retail Banking network, with 1425 branches, is the core strength of

Habib Bank. The network provides HBL with the largest diversified low cost deposit base of

any bank in Pakistan, and forms the basis for many of our other business lines: corporate and

investment banking and treasury activities. The network provides HBL with the largest

diversified low cost deposit base of any bank in Pakistan, and forms the basis for many of our

other business lines: corporate and investment banking and treasury activities.

o Commercial Banking:

Enterprises operating in the middle market contribute significantly to the

economy of a country. During FY-2000 HBL‟s management decided to address this issue.

On November 1, 2000 Commercial Banking came into being.

TThhee oobbjjeeccttiivvee ooff sseettttiinngg--uupp CCoommmmeerrcciiaall BBaannkkiinngg wwaass ttwwoo--ffoolldd::

FFiirrsstt ttoo ssttoopp tthhee eerroossiioonn ooff mmaarrkkeett sshhaarree iinn tthhee mmiiddddllee mmaarrkkeett;;

Second, to regain the lost market share

Commercial Banking is making headway with improvement not only in terms of the business

figures but also in its ambiance. Renovation of is being carried out in order to give a

professional look to all the Commercial Banking Centers.

o Corporate Banking:

The Corporate Banking Group serves large institutional customers who

require sophisticated products in an environment of intense competition. HBL Corporate &

Investment Banking Group is now recognized as a market leader and regularly arranges and

participates in most large structured finance deals.

o International Operations:

HBL‟s ability to operate successfully in diversified markets and cultures is

a function of a long history in international banking – when first international branch was

opened in 1951. The Bank‟s branches in financial centers continue to provide efficient trade

settlement and reimbursement services to the entire network and business with other banks.

SWOT ANALYSIS

STRENGTHS:

Goodwill & historical background

Professional and well trained staff

Largest customer base

HBL is Pakistan's largest commercial bank

HBL has a domestic network of 1,425 branches with an international network of 48

branches in 26 countries

20% share of HBL in financial market

Large Balance sheet size

Decentralized authority

WEAKNESSES:

Unfavorable union activities and management conflicts

Checking System is at intra-department level

Weak marketing policies

Nepotism & Favorism

Infected portfolio still exists as bad debts

Centralized management in particular areas

OPPORTUNITIES:

Opportunities for growth and expansion in cash management.

Faster market growth represents opportunity to grow and diversify

Restoration of investor‟s confidence and pick up in private sector investment flows.

Large deposit base and funds flow can help to avail related market opportunities

THREATS:

Adverse & unstable government policies

Political instability

Advance technology

Competition from other banks

PEST ANALYSIS AND ENVIRONMENTAL SCANING

A broad view of market is important when management is interested in introducing

better services for customers. Rapid technological change, global competition and the

diversity of buyers preferences in many markets require the constant attention of the market

vouchers to identify promises business opportunities, see the shifting requirements of the

buyers, evaluate changes in competitors positioning and guide the choice of which buyers to

target and classify them according to respective segments.

Identification of external and macro factors that influence buyers and thus change the size

and composition of market overtime involves initially building customer profiles. These

influences include:

Political and legal environment

Economic trends

Socio cultural environment

Technological factors

POLITICAL AND LEGAL ENVIRONMENT

Banks are strongly affected by the political and legal considerations. This environment is

composed of regulatory agencies and government law that influence and limit various

organizations and individuals. Mostly these laws create new opportunities for business.

Business legislation has following main purposes

To protect banking companies from unfair competition.

To protect consumers from unfair business practices adopted by banking companies

To protect the interest of the society from unbridled business behavior.

ECONOMIC TRENDS

A banking market requires better consumer market in volume along with higher

borrowing power. The available borrowing power depends on:

Consumer income

Saving rates

Consumption patrons

Rates of interest

Budget deficit

Exchange rates

Cost of living

Inflation

SOCIO-CULTURAL ENVIRONMENT

A society is shaped by beliefs, norms and values. People in a society consciously and

unconsciously interact with:

Themselves

Others

Organization

Society

Nature

Following are the main factors. Which arise because of change in socio-cultural

environment?

Consciousness about services

Concern for environment

Improved customer relation

TECHNOLOGICAL FACTORS

Forces of technological advancement have played the most dramatic role in

shaping the lives of people. The rate of change of technology has greatly affected the rate of

growth of economy. New technology is creating deep rooted affects which could be observed

in long run. The improvement techniques involved in on line banking. In brief PEST analysis

affects the overall banking companies and provides us the information about the external

macro condition.

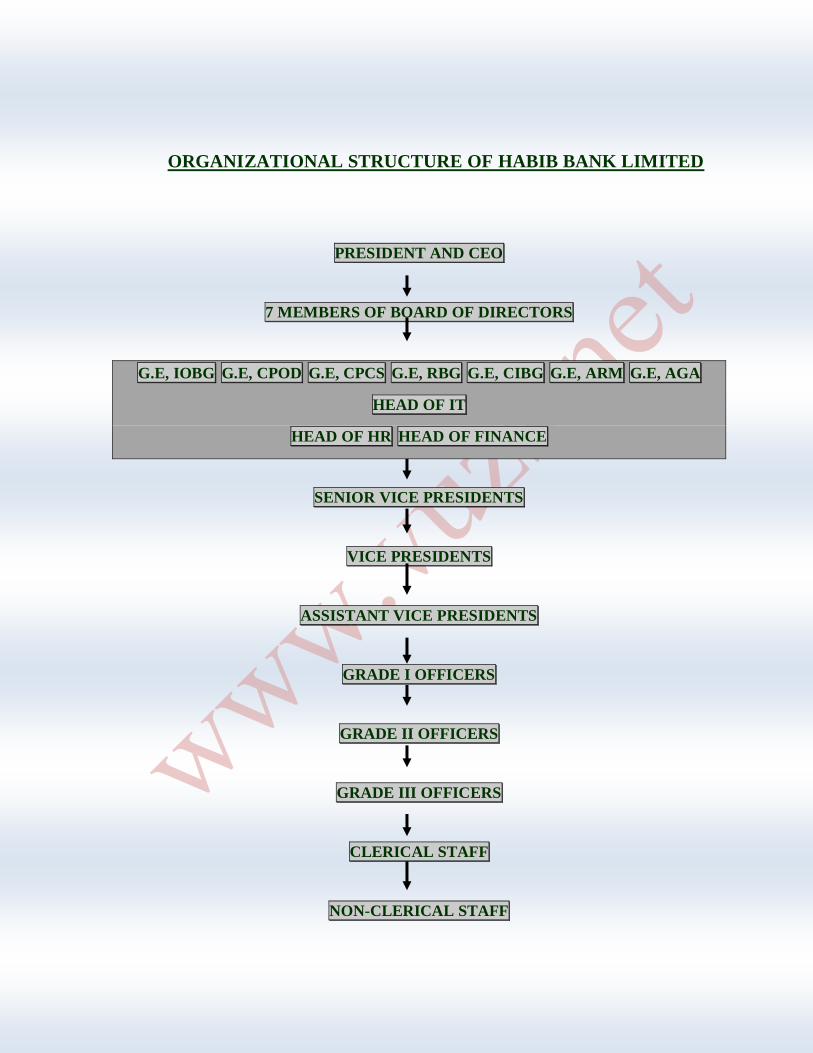

ORGANIZATIONAL STRUCTURE OF HABIB BANK LIMITED

PRESIDENT AND CEO

7 MEMBERS OF BOARD OF DIRECTORS

G.E, IOBG G.E, CPOD G.E, CPCS G.E, RBG G.E, CIBG G.E, ARM G.E, AGA

HEAD OF IT

HEAD OF HR HEAD OF FINANCE

SENIOR VICE PRESIDENTS

VICE PRESIDENTS

ASSISTANT VICE PRESIDENTS

GRADE I OFFICERS

GRADE II OFFICERS

GRADE III OFFICERS

CLERICAL STAFF

NON-CLERICAL STAFF

Members of Board of Directors:

G.E GROUP EXECUTIVE

IOBG INTERNATIONAL AND OVERSEAS BANKING GROUP

CPOD CORPORATE PLANNING AND ORGANIZATIONAL DEVELOPMENT

CPCS CREDIT POLICY AND COMPANY SECRETARY

RBG RETAIL BANKING GROUP

CIBG CORPORATE AND INSTITUTIONAL BANKING GROUP

ARM ASSETS REMEDIAL MANAGEMENT

AGA AUDIT AND GENERAL INFORMATION

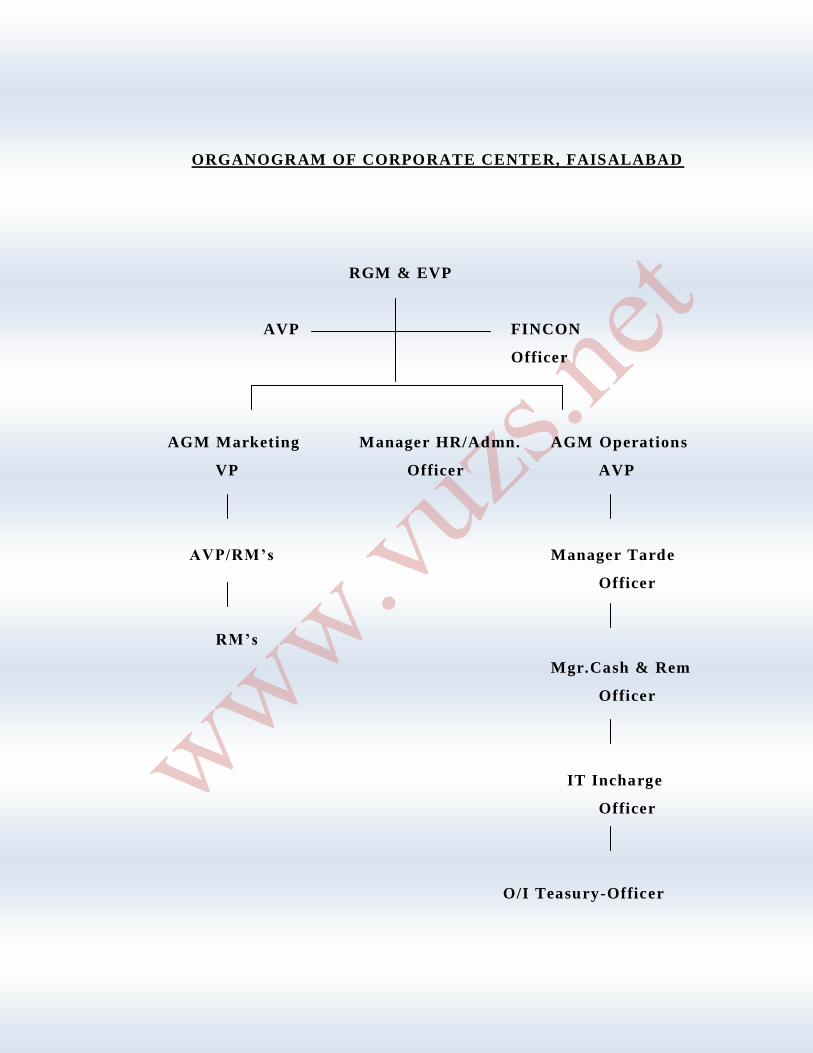

ORGANOGRAM OF CORPORATE CENTER, FAISALABAD

RGM & EVP

AVP FINCON

Officer

AGM Marketing Manager HR/Admn. AGM Operations

VP Officer AVP

AVP/RM’s Manager Tarde

Officer

RM’s

Mgr.Cash & Rem

Officer

IT Incharge

Officer

O/I Teasury-Officer

DEPOSIT DEPARTMENT

Bank deals in money and they are merely mobilizing funds within the economy. They

borrow from one person and lend to another, the difference between the rate of borrowing

lending forms their spread or gross profit. Therefore we can rightly state that deposits are the

blood of the bank which causes the body of an institution to get to work. These deposits are

liability of the bank so from point of view of bank we can refer to them as liabilities.

TYPES OF ACCOUNT:

1) CURRENT ACCOUNT:

In this type of accounts the client is allowed to deposit or withdraw money as and

when he likes. He may, thus, deposits or withdraws money several times in a day if he likes.

There is also no restriction of amount to be deposited or withdrawn. However, there is

requirement of minimum balance maintenance of Rs.5000/-. Usually this type of account is

opened by the businessmen. No profit is paid by the bank and no service charges are

deducted by the bank on current deposits account.

Eligibility:

i. All Pakistani‟s Resident/Non-Resident, Individuals (Single-Jointly) Companies/Firms

etc. can open and operate the Account but he should be a corporate customer.

ii. Any Foreign National Individuals (Single-Jointly) having valid Resident Pakistan

VISA/Work Permit can open and operate the Account.

Requirements for Opening of Account:

Duly filled prescribed A/C opening FORM.

Attested photocopy of N.I.C./Passport of Account Holder(s), Proprietor, Partners,

Directors and office Bearers as the case may be.

Certified true copy of the certificate of incorporation or registration (in case of limited

companies & registered bodies only).

Certified true copy of the certificate of commencement of business (in case of public

limited companies only).

Certified true copy of the memorandum and articles of association (in case of limited

companies).

Certified true copy of rules and regulations or By-Laws (in case of association etc.).

Certified true copy of the resolution of the Board of Directors/Managing

Committee/Governing Body regarding conduct of the account.

Features:

Account can be OPENED with Minimum Balance Rs.1000/- with no maximum limit.

Checking balance at any time during banking hours.

No profit is paid.

Statement of Account dispatched on request letter.

There is no restriction for withdrawals of amount and number of cheque.

2) Profit and loss sharing savings:

This type of account is for those persons who want to make small savings'. This type

of account is opened with a minimum deposit of Rs. 1000/- or the amount prescribed from

time to time. The profit is paid on these accounts on the minimum balance during a month for

the whole of that month. Zakat & other taxes are deducted as per rules of the government.

The requirements for this account is duly filled prescribed A/C opening FORM, Photo Copy

of National Identity Card (Resident Pakistani), two Passport size photographs with

Signatures/Thumb Impression (Resident Pakistani), Photo copy of Passport with Page

bearing Resident Visa of the Country where Pakistani Residing, two Passport size

photographs and signatures on A/C Opening Form for Non-Resident Pakistani with

Signatures/Thumb Impression etc.

Features:

Account can be OPENED with Minimum Balance Rs.1000/- or prescribed limit that

is announced time to time with no maximum limit.

Profit is payable at monthly subject to adjustment on deceleration of actual profit rate

declared every half year.

Profit is calculated on monthly products

Zakat will be deducted on valuation dates of account.

Profit is Paid/Credited in Account on half yearly basis in case of six monthly PLS

saving accounts.

Statement of Account dispatched on half yearly basis after posting of profit.

There is no restriction for withdrawals of amount and numbers of cheque.

3) PLS special notice deposit:

Special notice deposit is paid on daily product bases. Under this deposit scheme, a

deposit is received from the depositor under the condition that he will intimate the bank

before a certain period in case of withdrawals. There are two types of special notice deposit,

they are 7 days and 30 days notice deposits. The profit is paid on these deposits but it is

nearly equivalent to saving account rate that is paid on special notes.

4) PLS term deposit:

A type of term deposit, in which a receipt is issued for varying tenors

ranging of deposit. It is in the form of receipts and profit on these receipts is paid biannually.

These receipts are encashable after expiry of the period for which they were issued. Different

profit rates are applied to different type of term deposit. It has no maximum limit but not less

than 1 month. Account opening rate is 1000 and the zakat is deducted on the rules and

regulation.

Eligibility:

All Pakistani‟s Resident/Non-Resident individuals, Firms/Companies, Govt/Semi

Govt. Departments can purchase the TD.

Any Foreign National having valid Resident Pakistan VISA can purchase TD.

Requirements for Purchase of TD:

Duly filled prescribed FORM.

Photo Copy of National Identity Card (Resident Pakistani).

Two Passport size photographs with Signatures/Thumb Impression (Resident

Pakistani).

Photo copy of Passport with Page bearing Resident Visa of the Country where

Pakistani Residing

Two Passport size photographs and signatures on A/C Opening Form for Non-

Resident Pakistani with Signatures/Thumb Impression.

Photo Copy of Passport with Page bearing Resident Visa of Pakistan (Foreign

Nationals).

Features:

TD can be purchased with minimum of Rs.1000/- with no maximum limit.

Profit is payable at yearly rate declared every half year.

Profit is Paid/Credited in Account on half yearly basis.

The holder of term deposit receipt must keep the receipt under lock any loss of receipt

must inform the bank because without it the bank will not pay the amount.

5) PLS khas term deposit:

Pls khas term deposits are acceptable for a period ranging from one and half

year to five years in multiple of six months. In this regard the profit is declared from time to

time but will be paid only once at the time of encashment of receipt of maturity. Zakat will

be deducted only once at the time of maturity or before maturity.

Account opening in special cases

Blind person account:

A blind person can easily open an account in the bank like other persons but it is

preferred that he should open a joint account with a normal person. If he wants to open the

account individually, there should be an authorized person with him who checked the

signature and the amount filled by blind person. The banker can not fill the amount and

check the signature. The one thing that is provided extra by the blind person is two

photographs duly attested by an authorized person.

Non resident person account:

Non-resident persons are those who do not live in Pakistan permanently.

According to the tax authority the non-resident persons are those who live in Pakistan:

In case of foreigner not more than 180 days.

In case of Pakistani not more than 90 days etc.

In proceeding 4 years not more than 365 days.

All things will remain same, only one thing that is passport copy of the person will have to

provide to the bank. The logic behind this is that the bank insures the entry and the exit date

of the person in Pakistan. The person has to inform bank 15 days before entering in Pakistan

and the bank also send this information to State Bank of Pakistan. After getting this

information State Bank give instructions to bank about handling of not resident person‟s

account.

Zakat treatment on all accounts

Zakat will be deducted on all accounts except the followings:

Fiqah Gafreia account.

Non Muslim‟s account.

Trust account.

Government account.

Provident fund.

Defense account.

Non Pakistani‟s account.

SWIFT

Society for worldwide inter bank financial telecommunication.[SWIFT]

Only for banks

Telecommunication not transition

Head office in Belgium

Run by different country members

Lease lining by head office

Start in pak 1995-96

Awareness seminars start in 1997

Work through coding &decoding

Swift provide to members an id &password for connect

Charges from customers depend on message size

Min changes is 120

Changes for one LC is 1400

Code not more than three degits (ID and Passward code)

Authentic mode, people satisfied

Less chances of fraud

Work as E Mail

Version 2 relate to bank to bank information

Version 4 relate to bank to bank Document

Version 7 relate to bank to bank LC

In HBL use in domestic ---------- 70 branches

In overseas branches ---------- 21

Centralized system( send message to different countries at once)

REMITTANCES

DEMAND DRAFT:

Demand draft is a written order drawn by a branch of a bank upon the branch of same

or any other bank to pay certain sum of money to or to the order of specified person. It can be

issued to the customers as well as non customer against cash cheque and letter of instruction.

Demand draft is negotiable instruments that can be negotiating at any time before its

cancellation. Its Legal provisions are same as that of cheque.

Following parties are involved in demand draft:

Applicant

issuing branch

drawee branch

Beneficiary

A demand draft may be issued against the written request of the customer before issuing it

must be seen that the demand draft is in order.

The DD application must be scrutinized by the counter clerk in respect of following points.

There should be branch where payment is to be made.

Full name of payer should be mentioned.

Amount in words and figures must be same

The applicant on two places should sign application.

TELEGRAPHIC TRANSFER:

Telegraphic transfer means the transfer of funds from one branch to another

branch of the same bank or upon other bank under special arrangements just like a

telegram. Telegraphic transfer is not negotiable and the funds are not payable to bearer.

Minor cannot avail this facility. In telegraphic transfer the bankers use secret codes. One

code is with issuing person and the second is with an other person. When they combine

the codes it‟s become an amount that is called check. The payment is made after the

confirmation of the check.

Following parties are involved in TT

Applicant

Drawing branch

Drawee branch

Beneficiary

Following important things should be included in TT:

Full name of the beneficiary or account number should be mentioned in the

application form.

Instruction regarding mode of payment should be obtained.

A record in the remittance outward register should be maintained.

All the remittance must be controlled through number or codes.

PAY ORDER:

Pay order is an instrument through which payment can be made from one bank to

another bank. Pay order is meant for bank own payment but in practice they are also issued to

customers.

Following parties are involved in pay order:

Applicant

issuing branch

Payee

MAIL TRANSFER:

Mail transfer is not negotiable and the procedure of it is same with the procedure of

DD.When a customer request the bank to transfer his money from this bank to any other

bank of the branch of same bank in the city, outside the city of outside the country the first

thing he has to do is to fill an application form. In which he states that I want to transfer the

money from this bank to that specific bank by mail. If the customer is the account holder of

this bank, the bank will debit his account and the concerned officer will fill forms to make

the mail transfer complete.

If the customer is not the account holder of the bank, then firstly he has to deposit the

money and then rest of the procedure will be adopted to transfer his money.

SBP ERF Scheme

SBP had introduced this scheme to promote country „s export and to earn foreign

exchange. This scheme is operated through authorized dealers under SBP control.

This scheme had been amended by time to time.

Features:

Concessions rate of markup as compare to commercial banks rate of markups.

Export refinance allow to exporters via authorized dealers.

In case of default, the SBP recover its principal loan amount, markup & penalty

through the bank to which exporter has submitted his refinance claim.

Refinance allows against value added products i.e. garments, print, dyed cloths, bed

sets.

Proceeds repatriated through banking channels.

Allow credit loan amount within 248 hrs.

Misutilization of SBP funds has been prohibited, if any violation occurs SBP imposed

penalty.

Risk:

If the exporter has been / will be defaulted the laps of funds of authorized dealers.

Cheating or misuse of funds, SBP may cause to impose not any penalty but also

termination of bank employee or change of management or authorized dealer‟s

reputation may destroy.

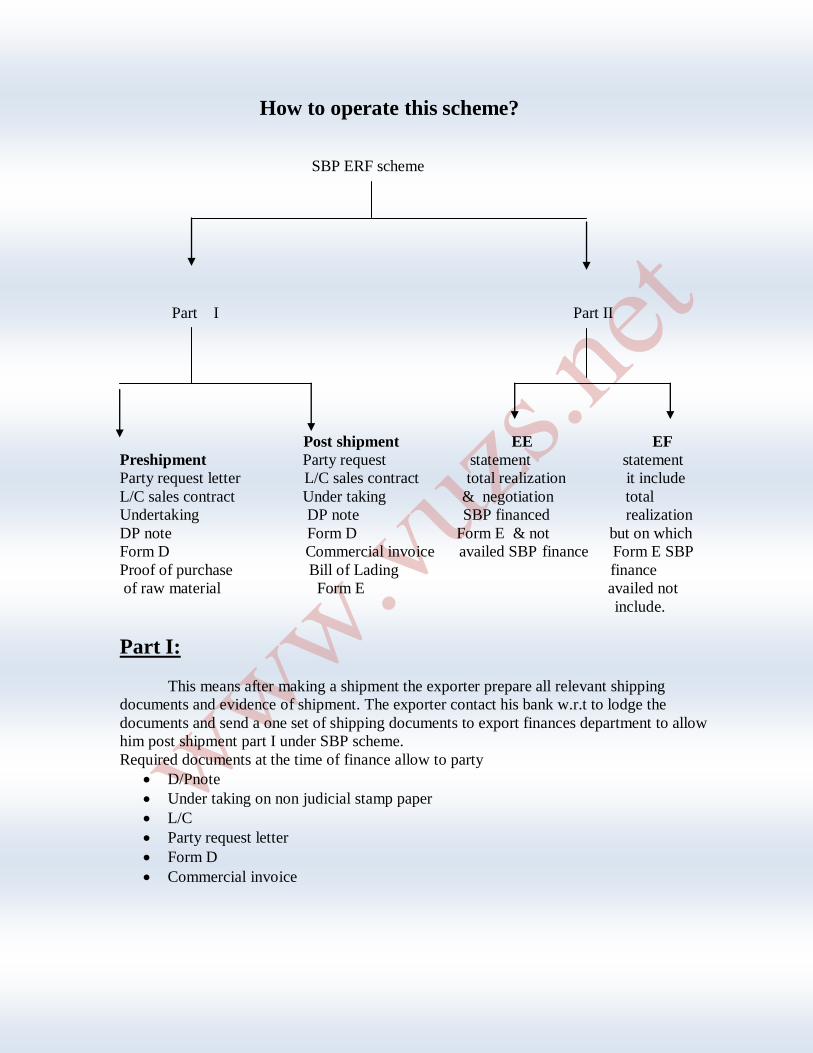

How to operate this scheme?

SBP ERF scheme

Part I Part II

Post shipment EE EF

Preshipment Party request statement statement

Party request letter L/C sales contract total realization it include

L/C sales contract Under taking & negotiation total

Undertaking DP note SBP financed realization

DP note Form D Form E & not but on which

Form D Commercial invoice availed SBP finance Form E SBP

Proof of purchase Bill of Lading finance

of raw material Form E availed not

include.

Part I:

This means after making a shipment the exporter prepare all relevant shipping

documents and evidence of shipment. The exporter contact his bank w.r.t to lodge the

documents and send a one set of shipping documents to export finances department to allow

him post shipment part I under SBP scheme.

Required documents at the time of finance allow to party

D/Pnote

Under taking on non judicial stamp paper

L/C

Party request letter

Form D

Commercial invoice

Penalties:

Non shipment 37 paisa/1000 per day

Short shipment

Delayed shipment

Late submission of documents to SBP

How to avoid from penalty of non shipment?

Provide proof of shipment against relevant sales contract or L/C on which finance

obtain

Substituted the old L/C or contract with new one after assurance that against new

L/C.

Restrictions/prohibitions

Evidence of shipment submit to SBP within 180 days or within time period fixed by

SBP

In case of substitution against new L/C or sales contract make sure that the exporter

has not availed pre or post shipment finance through any other bank.

How to calculate penalty?

Non shipment

180 days *1000000* 0.37/1000=66600

Short shipment

Finance amount 1000000

Shipment 800000

Short shipment amount =200000

180 days *200000*0.37/1000=13320

In case of post shipment only late repayment of finance penalty is involved.

Part II:

The authorized dealers provide this finance facility to exporters against their EE

statement. From the export earning during of one fiscal year the SBP sanction a limit of 50%

for the availment of the ERF part II. In the EE statement all foreign bills realized and

negotiated during a period of 01-07-04 to 30-06-05 are included in this statement.

Documents required at the time of sanction of finance

D/P note

Under taking on non judicial paper

Party request letter

Short fall in EE statement penalty:

Days*amount of finance*rate(0.37)/day/1000

Short fall in EF:

SBP calculate case to case basis daily product and match this with his EF performance, if

he avail excess Refinance from SBP and Business performance is short the SBP imposed a

short fall penalty.

Total short product*number of days*0.37/180

Demand Finance & Running Finance:

Demand finance :

This is common form of financing to commercial industrial concerns and is made

available either on pledge or hypothecation of goods, produce or merchandise. In demand

finance the party is finance up to certain limit either at once or as and when required.

The party due to facility of a paying mark prefers the financing up only on the amount it

actually utilizes.

Running Finance:

This form of financing was known as Overdraft when a bank customer requires

temporary accommodation, his banker allows withdrawals from his account and running

finance thus occurs. The accommodations generally allowed against collateral security. The

customer is in advantageous position in a running finance because he has to pay mark up

only on balance outstanding against him on daily products basis.

Pledge:

It is entitled to the exclusive possession of the property until the debt is charged.

Hypothecation:

When the property in the goods is charged as security of loan from the bank but the

ownership & possess

FAPC & FAFB:

FAPC (finance against packing credit):

It is a type of bank‟s own source finance provided to clients engaged in export

trade. As the term packing indicates that the credit line is granted to an exporter for the

purpose of packing merchandise for shipment to an importer abroad. An exporter should give

documentary proof to the bank consist of L/C in favor of exporter indicating the description

of the merchandise, the purchase price, date of delivery along with other terms.

FAFB(finance against foreign bills):

It is a post shipment finance facility which is provided by the banks to its clients

after providing the evidence of shipment, he contacts his bank to request him to lodge the

documents. He then provide the request letter with sale contract to grant him finance & this

department grant him finance (90% value of commercial invoice).

Imports and exports department:

Exports:

Introduction and registration:

Imports and exports act 1950 have empowered the federal Govt to control the import

and export in Pakistan. Pakistan is developing country and like other developing countries its

imports exceeds than exports. To control this situation the registration of import and export

has been made obligatory under the registration order 1993. The authority of registration has

been given to export promotion bureau. No importer and exporter who has no granted

registration shall indent, import and export of any good into or out of Pakistan. The

requirements for getting registration are as under:

Application form.

Photocopy of I.D card.

Copy of memorandum and article of association (in case of limited company).

Ownership deed of office.

Fee payment.

Certificate of incorporation.

Applicant should regular taxpayer.

The major exports from Pakistan are surgical goods, sports goods hand noted goods, leather

goods, textile goods, etc.

Export procedure:

All the exports work under the imports and exports act that is changed by the state in

every year. When the importer send the L.C to bank in respect to import or when the L.C

comes to the advising bank from the issuing bank then the concerned officer allot the number

to the L.C and get registered. The concerned officer write down the name of issuing bank and

the party name in a register and intimate the party about L.C. the exporter after receiving the

L.C from bank will prepare the documents as per the L.C usually the following documents

have to be prepared by the exporter:

Bill of lading

Covering letter

E- Form

Bill of exchange

Packing list

Commercial invoice

Quota documents in case of quota country

Certificate of origin

Special custom invoice

The export form (E-FORM):

E-FORM means “export form” which is the first and foremost requirement for the

exports from Pakistan. It is control instrument by Govt of Pakistan by which it monitors the

receipts from exports and checks the goods that are transferred without foreign exchange. all

banks which are engaged with the foreign exchange are required to print and maintained the

E form that is checked by the state bank of Pakistan. For export an e form is issued by the

bank on the request letter of a company. Two separate registers are maintained by the bank

one for his use and the other one are for the requirement of the SBP. On issuance of E forms

the banker lists it in the register and makes sign from the exporters. Banks record the name of

party, amount, the goods description, port of destination, importer name port of loading etc.

The functional utility of E-FORM:

The export form has four copies. The exporters and banks use it. Without it the

exporter can not make export. These copies are used as:

Original copy is for SBP that is checked by the higher authority.

Duplicate copy is for the bank use that is upraised by the custom authorities.

Triplicate for the use to report of SBP at the time of payment received.

Quartiplacte is for the company used.

Usage of E- FORM:

E- FORM is an important document for export. It has its own importance such as this

form is used as a checker means it monitor that what things are going abroad and in return

what things we are getting. So it creates a check and balance on the foreign exchange. It

shows the total quantity and quality of the goods that is sending to another country. An E –

Form shoe the party worth that is very helpful for the party and the bank. Bank can create a

party limit for the credit on the behalf of it and a party can arrange a loan for its future

requirements from the bank. It shows the terms of payment by the importer and the delivery

terms by the both parties that is helpful in case of any discrepancy during the contact.

Short shipment notice:

A shipment may be cancelled by the importer or exporter due to many reasons.

The cancellation of the export letter is called short shipment notice. In this situation the

company has to inform the bank. Company has to give a written letter to the bank that he is

not the export so please cancelled their e form. On the other hand bank at the time of

receiving the letter will stop the e form and cancelled the all documents.

IMPORTS

Imports regulation:

Import is being regulated by the ministry of commerce and the government of

Pakistan under the import and export act:

Categories of imports:

Imports are classified into the following categories:

Commercial sector imports

Industrial sector imports

Public sector imports

Registration of importers:

A person who wants to approach the bank for importing goods from abroad, he

should have to get himself registered with the export promotion bureau under registration

of imports and exports act. He must fulfill the following conditions before getting himself

registered:

NIC NUMBER

NATIONAL TAX NUMBER

MEMBER OF REGISTERED ASSOSITATION

Documentary letter of credit:

A documentary letter of credit is an instrument or document issued by the bank on

the behalf of a customer, authorizing a beneficiary to draw a draft and drafts or

sometimes the requirement of a draft, which will be honored, on presentation by the bank

if drawn accordance with the te3rm and condition specified in the letter of credit.

It is the written undertaking by the bank (issuing bank) pay to the seller (beneficiary)

at the request or as per the instruction given by the opener (applicant) pay at sight or at

the future date, a stated sum of money against the required documents. The documents

include the commercial invoice, certificate of origin, insurance policy or certificate and

the documents of transport relating to the mode sending goods. L/C is therefore is an

arrangement of security for the parties. The conditional guarantee is related to the

documents only and not on the underlying

goods or services.

Establishment of letter of credit:

Procedure:

The person applying for the letter of credit must be registered with the EPB. The opening

bank verifies this registration or otherwise exemption. This is mentioned in the “I” form. The

importer also shows the valid certificate of an organization membership. A category pass

book is issued by the EPB for registered importer specifying his category. This book is

centralized by the centralized banks in the city. It is not necessary for the bank to hold the

original copy of the pass book of all the importers. But some times the importer gets L.C

from more than one bank so the bank have to hold the photo copy of this pass book. The

applicant can get the application from any branch of the Habib Bank Limited. However only

some branches are authorized to open L.C. That branches how are not authorized have to

contact with the authorized branches to open an L.C. The authorized branches in such case

require the certificate from the applicant branch that the required formalities are fulfilled and

the approval was obtained with required margin.

For establishment of letter of credit, the importer requests the opening bank with the

following documents:

1) Application and agreement form IB-8:

Credit application form is an agreement between the bank and the customer on the

basis of which the letter of credit is opened. This form contains the undertaking of the

importer that get the documents from the bank at the mark up price. It contains the

following information:

Name and address of importer.

Name and address of exporter.

Amount in foreign currency.

Terms of credit.

Description of goods.

Origin of goods.

Port of loading and discharge.

Last date of shipment.

Foreign bank charges.

Terms of shipment. (Partial shipment or transshipment)

Insurance cover note, policy no, and name of insurance company.

Forward booking.

Mode of transmission.

Import registration no.

Any other documents required.

Detailed documents.

2) Performa invoice/ purchase order:

A Performa invoice is quotation of seller containing the description and the

specification of the goods, price, and terms of the sale. Some times the exporter has their

agent in the country. The agent must be registered from the EPB.

3)Insurance cover note:

All the goods imported under the documentary credit must always be insured. In

accordance with our country import policy, insured must be issued by a Pakistani

insurance company or the foreign company operating in Pakistan and such company must

be approved by the bank. Insurance covered based on the following:

It is issued in the name of issuing bank A/C importer.

The rider should cover against war.

The port of shipment and the port of destination.

Amount of premium prepaid.

Shipment period.

The description of goods should be the same as per the form.

4) Appendix B:

This Performa replaces the import license and is submitted along with L.C

application form duly filled in triplicate. It is conditional undertaking that the imports goods

are not banned, not smuggled. It is also an undertaking that if the bank is unable to arrange

the said currency the importer have to purchase it from other banks or from any other place.

It includes the details and description of goods, codes, class, type, source of import, country

of import, Performa invoice no etc.

5) “I” FORM:

This form is used at the time of retirement of documents against L.C established

earlier for reporting to the transaction to SBP through the bill of entry deptt. It has four

copies that is used as follows:

Original is for the use of SBP.

Duplicate for the authorized dealer to be used for processing exchange control.

Triplicate for the authorized dealer record.

Quartiplacte is for the submission in SBP in the case of import where the

documents are not retired.

Approval for establishment of letter of credit:

After scrutiny of the documents, IB-8 along with attached documents is put

before the corporate head for approval. If the amount of application exceeds the power of

the corporate head the branch concerned prepared the memorandum for the corporate

banking head for obtaining his approval.

In case party enjoying regular limit, the L.C is established without adopting the procedure

mentioned above. However the amount of L.C should not exceed the regular limit.

Types of letter of credit:

1) Revocable credit:

The letter of credit that can be cancel with the consent of importer, without

giving any prior information to the exporter.

2) Irrevocable letter of credit:

The letter of credit that can be cancelled by the mutual consent of the both

parties. Only one party cannot cancel it.

3) Irrevocable confirmed letter of credit:

When an issuing bank authorizes and or request to an other bank to confirm

his irrevocable credit and adds its confirmation. Such confirmation constitutes a definite

undertaking of such bank in addition to that of the issuing bank. There are following

other letter of credits:

1. Revolving Credit

2. Transferable Credit

3. Back to Back Credit

4. Green Clause Credit

5. Red Clause Credit

6. Clean Documentary Credit

7. Transit Credit

8. Stand by Credit

9. Sight Credit

Parties to a credit:

The applicant:

The applicant of the letter of credit is called the importer or buyer. The buyer requests

to the bank to open a documentary letter of credit in favor of the seller.

Opening bank (issuing bank or importer bank):

At the request of the importer an issuing bank issues a credit under the instructions in

the favor of the seller.

Advising bank:

An advising bank is a bank in the seller‟s country. The issuing bank forwards the

advice of the credit by mail or by any mode to the correspondent bank in the exporter country

as instructions of the opener.

Beneficiary (exporter):

The person or body receiving the letter of credit from the importer that is opened in

favor of him.

Confirming bank:

The bank that on the requests of the issuing bank adds confirmation to a credit. It is

definite undertaking of the confirming bank, in addition to the issuing bank.

Negotiating bank:

It May or may not be the advising bank. An authorized bank that gives the value to

the draft for processing and payment.

Reimbursing bank:

Reimbursing bank is the bank, which on the behalf of the opening bank, honors the

Reimbursing claim lodged by the negotiating bank.

Modes of payment:

Sight letter of credit:

The seller submit all the documents with draft in the importer country

Complying with the all terms and conditions. The payments are made on the presence of

the documents.

Usance letter of credit:

Under these circumstances it is agreed that the payment will be made after a

specified period. So the payment is made after or on the expiry of that date.

Risks for importer and exporter:

Importer’s risks:

He does not know the seller.

He does not know that goods will be delivered in time.

He does not know how to check the goods.

Exporter’s risks:

He does not know the buyer.

He does not know the credit worthiness of the buyer.

He does not wait for payment.

He does not wait for exchange control.

Buyers and sellers obligations:

The seller’s obligations:

Provision of goods as per contract.

License authorization and formalities.

Contract of carriage and insurance.

Delivery at time.

Transfer of risk.

Division of cost.

Notice to buyer.

Proof of delivery.

Good checking marking and packing.

Other obligations.

Buyer’s obligations:

Payment of price.

License authorization and formalities.

Contract of carriage and insurance.

Taking Delivery at time.

Transfer of risk.

Division of cost.

Notice to seller.

Proof of delivery.

Inspection of goods.

Possible problems in international trade:

Non-payment.

Delay in delivery.

Financing, how and against what.

Currency restrictions.

Regulatory restrictions.

Documentation and mode of settlement.

ICC rules and INCO terms.

HUMAN RESOURCE DEPARTMENT

FFUUNNCCTTIIOONNAALL RREESSPPOONNSSIIBBIILLIITTIIEESS::

RRiigghhtt NNooww tthhee rreessppoonnssiibbiilliittiieess aassssiiggnneedd ttoo HHRR ddeeppaarrttmmeenntt aatt CCoorrppoorraattee CCeenntteerr ccaann

bbee ccaatteeggoorriizzeedd uunnddeerr tthhrreeee hheeaaddss::

SSttaaffff mmaatttteerrss // BBaassiicc HHRR FFuunnccttiioonnss

EExxppeennsseess ccoonnttrrooll

SSeeccuurriittyy mmaatttteerrss

NNooww II‟‟llll ddiissccuussss tthheessee oonnee bbyy oonnee::

BBaacckkggrroouunndd::

The banking council of Pakistan was responsible for the recruitment, selection and

allocation of human resources. After the dissolution of the Pakistan Banking Council, the

Banking & Financial Services Commission of Pakistan is responsible for these activities.

Procedure:

Staff requirements are met according to the changing needs of macro environment

scenario and particularly the arising needs of the bank itself. A need analysis is conducted.

After assessing the human resources requirements and screening of the applications, most

probably, the suspects are invited for a written test.

Short listed candidates are called for an interview for personality and social appraisal.

Interviews are a mix of direct and indirect interviewing techniques and information required.

The selected candidates are sent for training of six months training from MDI‟s.

The training is through the lectures regarding banking procedural guidelines and other

behavioral aspects. After the completion of training employees are allocated to different

offices. The effective management of people in an organization requires an understanding of

motivation, job design, reward systems, and group influence.

RReeccrruuiittiinngg

RReetteennttiioonn

SSuucccceessssiioonn ppllaannnniinngg

RRiisskk MMaannaaggeemmeenntt

DDiivveerrssiittyy iinn oouurr wwoorrkkffoorrccee

MMaannaaggeemmeenntt iinnffoorrmmaattiioonn

PPrrooggrreessssiivvee ccoommppeennssaattiioonn aanndd bbeenneeffiittss ddeessiiggnn aanndd iimmpplleemmeennttaattiioonn

EEmmppllooyyeeee ccoommmmuunniiccaattiioonnss aanndd rreellaattiioonnss

TTrraaiinniinngg nneeeeddss aannaallyyssiiss,, pprrooggrraamm ddeessiiggnn aanndd iimmpplleemmeennttaattiioonn

PPeerrffoorrmmaannccee eevvaalluuaattiioonn

Work-life initiatives

CREDIT & ADMINISTRATION DEPARTMENT

TThhee rreessppoonnssiibbiilliittyy ooff pprroovviiddiinngg aaddmmiinniissttrraattiivvee ssuuppppoorrtt ffoorr tthhee lleennddiinngg aaccttiivviittiieess ooff tthhee

BBaannkk,, aanndd ddaayy--ttoo--ddaayy mmoonniittoorriinngg ooff ccrreeddiitt--eexxppoossuurree,, iiss vveesstteedd iinn tthhee CCrreeddiitt AAddmmiinniissttrraattiioonn

DDeeppaarrttmmeenntt ((CCAADD))..

FFUUNNCCTTIIOONNAALL RREESSPPOONNSSIIBBIILLIITTIIEESS::

TThhee mmaaiinn rreessppoonnssiibbiilliittiieess uunnddeerr tthhiiss ddeeppaarrttmmeenntt aarree::

IImmpplleemmeennttaattiioonn ooff ccrreeddiitt ffaacciilliittyy aanndd tthheeiirr mmaaiinntteennaannccee aaccccoorrddiinngg ttoo tteerrmmss ooff ccrreeddiitt

aapppprroovveedd..

EEnnssuurree tthhaatt ssttaannddaarrdd llooaann ddooccuummeennttaattiioonn ffoorr eeaacchh ccrreeddiitt ffaacciilliittyy iiss mmaaiinnttaaiinneedd aanndd tthhee

ccoorrrreeccttnneessss && ccoommpplleetteenneessss ooff ssuucchh ddooccuummeennttaattiioonn aanndd aallssoo rreessppoonnssiibbllee ffoorr ccuussttooddyy

ooff aallll ccrreeddiitt ffiilleess..

MMaaiinnttaaiinn tthhee ssaaffee ccuussttooddyy ooff aallll ccoollllaatteerraall aass ppeerr bbaannkk‟‟ss ssttaannddaarrdd ooppeerraattiinngg

pprroocceedduurreess;; uunnddeerrttaakkee ppeerriiooddiicc eevvaalluuaattiioonn aanndd iinnssppeeccttiioonn ooff hhyyppootthheeccaatteedd// pplleeddggeedd

iinnvveennttoorriieess iinn aaccccoorrddaannccee wwiitthh tthhee tteerrmmss ooff ccrreeddiitt..

EEnnssuurree ccoommpplliiaannccee wwiitthh

oo IInnssttiittuuttiioonnaall ccrreeddiitt ppoolliicciieess && pprroocceedduurreess

oo LLooccaall rreegguullaattoorryy rreeqquuiirreemmeennttss..

PPrreeppaarree vvaarriioouuss ppoorrttffoolliioo ccoommppoossiittiioonn rreeppoorrttss aanndd ootthheerr ddooccuummeennttaattiioonn ffoorr

ssuubbmmiissssiioonn ttoo GGRRMM‟‟ss && RRMM‟‟ss..

CCRREEDDIITT FFAACCIILLIITTYY IIMMPPLLEEMMEENNTTAATTIIOONN PPRROOCCEEDDUURREE::

UUppoonn aapppprroovvaall ooff ccrreeddiitt pprrooppoossaall,, tthhee ccrreeddiitt pprrooppoossaall aanndd aapppprroovvaall aarree hhaannddeedd oovveerr ttoo

CCAADD.. NNooww CCAADD ddeetteerrmmiinneess tthhee nnaattuurree ooff ddooccuummeennttaattiioonn rreeqquuiirreedd aanndd oonn rreecceeiipptt ooff ssaammee

eennssuurreess tthhaatt aallll lleeggaall ddooccuummeennttss aarree oobbttaaiinneedd aanndd aarree lleeggaallllyy eennffoorrcceeaabbllee.. AAfftteerr aallll tthheessee

aaccttiivviittiieess iitt ccaann rreelleeaassee tthhee ffaacciilliittyy ffoorr uuttiilliizzaattiioonn..

MARKETING DEPARTMENT

The marketing department in HABIB BANK LIMITED is very strong. It is the main

source of gaining and maintains the customers that can give a large profit to the bank. There

are five relationship managers in Habib bank and every person is responsible for the credit of

his party.

CUSTOMER DEALING:

HBL corporate center only deal with the following categories of business:

The organization that have minimum 250 million sales in a year.

The organization that have availed 80 million finance

Agri based industry.

HBL do not deal with the agriculture sector.

PROCEDURE FOR CREDIT APPROVAL:

It is the responsibility of the relationship manager to provide or fulfill the

requirement of the customer by checking his financial and position. The procedure of

credit approval starts with the credit proposal. First of all the customer request to the bank

for credit and on the behalf of him the RM check the memorandum. The

Memorandum includes:

The company information.

Purpose of credit.

Assessment of management.

Risks.

Financial analysis.

Third party or other bank information.

Conclusion and recommendations.

Then the RM sends it to the authorities who accept or reject the proposal. If they accept the

proposal they announced a credit range for the party. At the end RM sends the proposal to

CAD deptt custody and check.

EXCESS FACILITY CREDIT BY RM:

Relationship manager is authorized to provide the excess facility to the customer

than the credit line. It may be up to

10 percent of excess amount

OR

12.5 million Whichever is less?

It is not more than 15 days if the customer wants to increase this facility he has to contact

with the head office.

TYPES OF CREDIT FACILITY:

1) fund based:

It is first type of credit facility. In this facility the bank actually provides fund to

customers.

2) non fund base:

Second type of credit facility that does not provides fun but only give the guarantee.

If the customer is unable to make the payment at maturity date then bank will be

responsible to make the payment.

Work done by me in HBL

ACCONTS OPENING DEPARTMENT:

In this account department I gain the particle knowledge about opening. This

department deals with opening account and saving account for its customer and all matters

regarding there off. The customer opening account/saving accounts can be categorized as

following:

1) individual

2) firm

3) company

4) trust

5) staff

6) others

OPENING AN ACOOUNT:

In order to open an account first of all the customer has to fill a form prescribed by

the bank. The person is required to bring some reference or introduction for opening the

account. Introducer may be a person who has an account with HBL.

Some important information regarding introducer e.g. the name and account number

of the introducer is written on the space provided on the specimen signature cards. Then in

order to find out whether he is a true introducer or not a letter is sent to him thanking him for

this introduction, so that any thing wrong may come into notice.

There are different requirement for different types of accounts and account holders.

An important thing is that the customer should have a corporate customer. The corporate

customer limit is 40 million and this branch always deals the corporate customer.

General rules for opening an account:

One person can open only one account in the same branch with the same category.

In the event of death of an account holder the credit balance will be transfer to the

heirs of the diseased individual account.

Services charges will be deducted periodically as prescribed from time to time on the

accounts that are under the limit of specific account.

Services charges are not applicable on that accounts that are prescribed as exempted.

A distinctive number will be allotted to the each account.

The bank can close those accounts that are under the minimum limit of the bank.

Any sum to be deposited in the account should be accompanied by paying in slip

showing the party account number and the name.

Account holder can only withdraw the sum of money by his own account by cheque.

Cheque should be signed by the account holder by the specimen given by the bank.

Post dated and defective cheque is not accepted.

If statement of account spoiled a new will be issued on cost.

Any change in the address should immediately communicate to the bank.

The account holder wishing to close the account must surrender the cheque book.

Account may be transfer from one branch to another same branch without any

charges etc.

DEPOSIT DEPARTMENT

“Deposit are the blood of a Bank”

I worked in this deptt for one week and learned that the acceptance of deposit is the

real source of income of a bank. Deposit Department is the backbone of commercial banking.

Deposit is often used to describe the money which customers of all kinds leave with the

bank. Deposit account can be defined as an account, which is opened to earn interest.

The term deposit is highly misleading. It is not something deposited for safe deposit box.

Bank deposit is not like that; when one brings currency to the bank for deposit the bank does

not put the currency in the vault. It may put small fraction of the currency in the vault as

Reserve but it will lend most of deposits to someone else.

The entire banking system is based upon borrowing. Like all banks, deposit department has

acknowledged its worth as the most important. Almost all the operations generated from the

deposit department and with due course of time reflect back to the deposit department. In

order to attract funds bank has introduced various types of deposit schemes that may suit the

need and tastes of a large number of depositors.

TYPES OF DEPOSIT FACILITY:

Deposits are broadly classified into the following three categories:

i) Demand deposits

ii) Saving deposits

iii) Time deposits

The procedure undertaken upon receiving deposits from the customer is as follows:

1) Examining the deposit slip to ensure that the name and the account numbers are clearly

indicated.

2) Counting the cash/cheque and agree the total with the amount on the deposit slip.

3) After that the pay-in-slip is validated for cash transaction/ transfer/ clearing transfer as

appropriate before the counterfoil a handed over the customer.

4) Cheque assigned by the director, partners, employees of a company, drawn in favor of

themselves and credited in their account in the bank are to be scrutinized

WITHDRAWALS:

An amount can be withdrawn by the cheque. The withdrawals can be made only at

branch where the account is maintained. All cash withdrawals will be made under account

holder‟s full signature. One or two bank officers have to verify the signature.

In current account the bank does not offer any interest. We can deposit and withdraw

any amount during the banking hours.

ISSUANCE OF CHEQUE BOOK:

The account holder requests for a new cheque book by presenting the requisition slip

along with the authority letter to the concerned officer. His signature was verified before

giving him the new cheque book. One or two bank officers have to verify the signature

REMITTANCES DEPARTMENT:

I work in this department for one week; this department deals in transfer of money

from one place to another or country by:

1) Demand draft

2) Mail transfer

3) Telegraphic transfer

In this department internees are advised to observe the working of transfer of money from

one place to another place or country by the above mode of transferring money. During my

stay in this department I observed that how demands draft be issued.

The procedure is as follows:

First a bank receives a request from the customer to issue a bank draft. The written

request is either in a banks standard from or separate paper signed by the applicant with cash

or cheque covering the amount of the draft and other charges of the bank.

While issuing a bank draft it is necessary that they should be free from alternations.

All the details must be written clearly in ink. After issuing a demand draft it is handed over to

the applicant and it advice containing the particulars of the draft is sent to drawer branch with

it is necessary information and payment of the draft is made on its presentation or according

to the terms and condition of the mode of transfer.

Financial Analysis of the client

Group Overview :

Rafiq Group is consisting of:

1. Muhammad Anwar & Brothers Cotton Fiber Recovery Plant.

2. Qutub Textile Mills (Pvt) Limited

3. Rafiq Spinning Mills (Pvt) Limited

1. MUHAMMAD ANWAR & BROTHERS COTTON FIBRE RECOVERY

PLANT:

The group started textile waste business 20 years ago and established cotton fiber

recovery plant in Faisalabad. It is the parent company of the group. Annual production

capacity of the plant is approx. 150,000 tons. The raw material is procured mainly from open

market and a very negligible quantity is obtained from their two sister concerns

2. QUTUB TEXTILE MILLS (PVT) LIMITED:

Qutub Textile Mills (Pvt) Limited is situated in Sheikhupura. The unit was

established five years ago with 1600 rotors. Rafiq Spinning Mills( Pvt) Ltd is utilizing the

production facilities of “ QTM” under lease arrangements.

.

3. RAFIQ SPINNING MILLS (PVT) LIMITED:

After successful operation of the above two projects, the group established

another unit on 11.11.1997 in the name of Rafiq Spinning Mills (Pvt) Limited, consisting of

3,000 open ended rotors. It started its commercial production in April 1998 and is showing

profits continuously. The Company has undertaken expansion of the unit by installing 16,980

spindles. The company through their own sources has imported the machinery. Having a

successful experience, now the company is once again going into expansion by setting up

15,480 spindles.

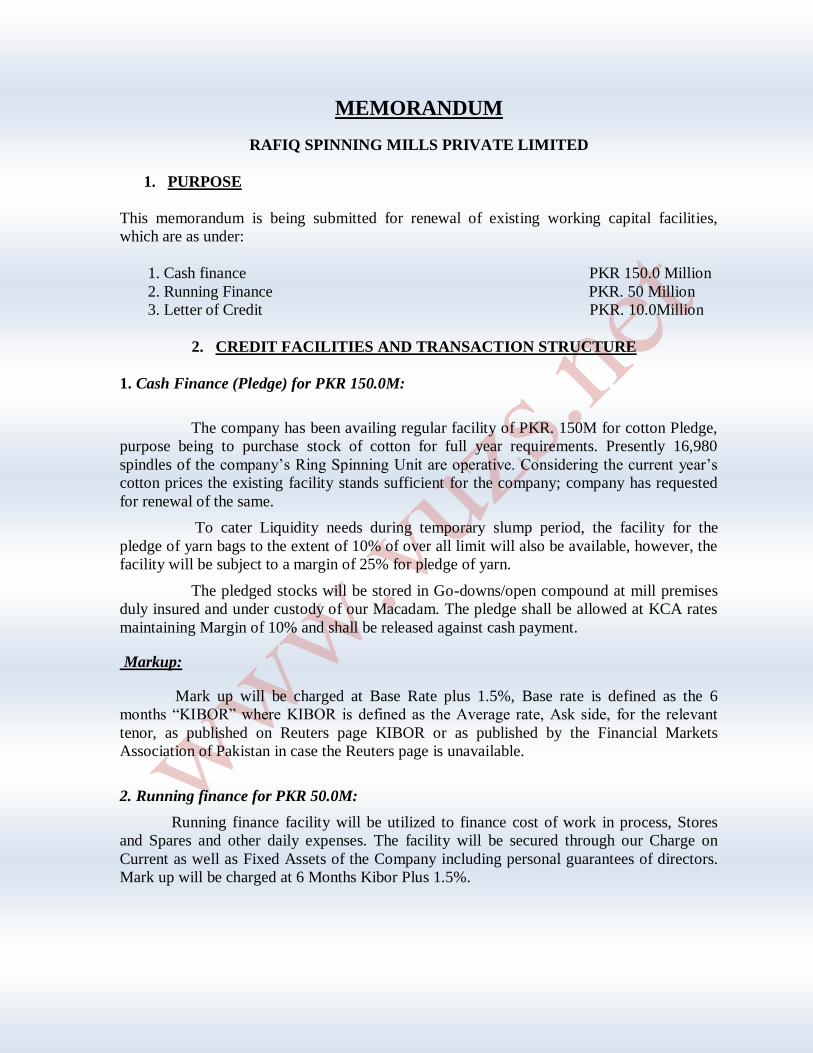

MEMORANDUM

RAFIQ SPINNING MILLS PRIVATE LIMITED

1. PURPOSE

This memorandum is being submitted for renewal of existing working capital facilities,

which are as under:

1. Cash finance PKR 150.0 Million

2. Running Finance PKR. 50 Million

3. Letter of Credit PKR. 10.0Million

2. CREDIT FACILITIES AND TRANSACTION STRUCTURE

1. Cash Finance (Pledge) for PKR 150.0M:

The company has been availing regular facility of PKR. 150M for cotton Pledge,

purpose being to purchase stock of cotton for full year requirements. Presently 16,980

spindles of the company‟s Ring Spinning Unit are operative. Considering the current year‟s

cotton prices the existing facility stands sufficient for the company; company has requested

for renewal of the same.

To cater Liquidity needs during temporary slump period, the facility for the

pledge of yarn bags to the extent of 10% of over all limit will also be available, however, the

facility will be subject to a margin of 25% for pledge of yarn.

The pledged stocks will be stored in Go-downs/open compound at mill premises

duly insured and under custody of our Macadam. The pledge shall be allowed at KCA rates

maintaining Margin of 10% and shall be released against cash payment.

Markup:

Mark up will be charged at Base Rate plus 1.5%, Base rate is defined as the 6

months “KIBOR” where KIBOR is defined as the Average rate, Ask side, for the relevant

tenor, as published on Reuters page KIBOR or as published by the Financial Markets

Association of Pakistan in case the Reuters page is unavailable.

2. Running finance for PKR 50.0M:

Running finance facility will be utilized to finance cost of work in process, Stores

and Spares and other daily expenses. The facility will be secured through our Charge on

Current as well as Fixed Assets of the Company including personal guarantees of directors.

Mark up will be charged at 6 Months Kibor Plus 1.5%.

3. Inland Foreign Letter of Credit for PKR 10.0M:

To meet stores, spares and imported cotton requirements, the company intends to

avail L/C facility of PKR 10.0M. The facility shall be secured against our lien on import

shipping documents in addition to our Charge on Fixed Assets of the Company.

LLCC CCoommmmiissssiioonn::

LLCC ccoommmmiissssiioonn oonn tthhee pprrooppoosseedd ffaacciilliittyy wwiillll bbee aass ppeerr llaatteesstt sscchheedduullee ooff cchhaarrggeess..

3. WAYS OUT ANALYSIS:

PRIMARY SOURCE:

Through sales proceed i.e. internal cash flows of the company. During FY 05,

company generated gross operating funds of PKR.28.962M.

SECONDARY SOURCE:

JPP first charge on all current assets of worth PKR.178M, our share stands at 70.00M,

which is to be enforced in case needed. Market value of current assets is 352.741M.

JPP first charge on all fixed assets of worth PKR 188 M, our share stands at 120M,

which is to be enforced in case needed.

4. BUSINESS UPDATE / COMPANY STRATEGY:

The group is in cotton waste/spinning sector for last twenty years. Yarn produced by

company is utilized as raw material in towel industry. Buyers of company are located in all

major cities; however, most of the buyers are residing in Karachi. Company is pursuing the

policy of large number of buyers. Days receivables have been nominal over the years since

selling terms of the company are on cash basis, this truly indicates quality and penetration of

company‟s products in the market. Major buyers of company are as under:

MAJOR BUYERS:

J. SONS TEXTILE KARACHI

J.K.SONS (PVT) LTD FAISALABAD

HIRA TEXTILE MILLS LTD LAHORE

JANNAT APPAREL (PVT) LTD FAISALABAD

SHARIFSONS FAISALABAD

AMTEX FAISALABAD

BABAR HOISERY KNITTING FAISALABAD

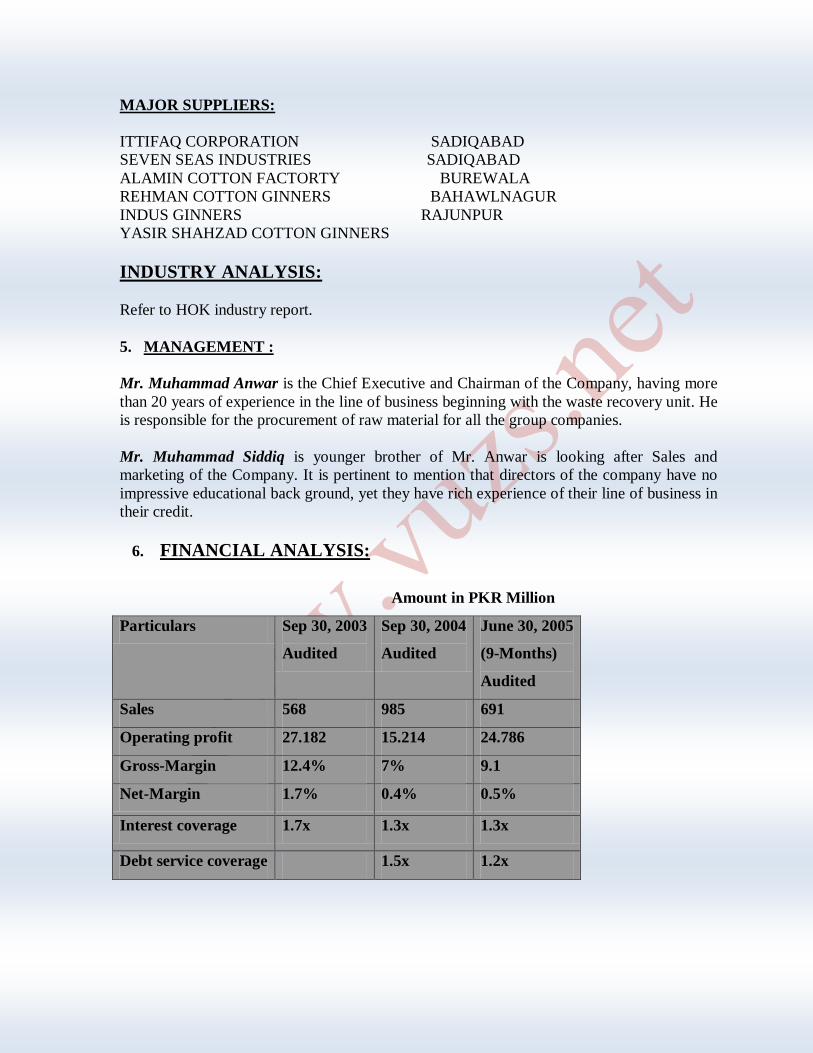

MAJOR SUPPLIERS:

ITTIFAQ CORPORATION SADIQABAD

SEVEN SEAS INDUSTRIES SADIQABAD

ALAMIN COTTON FACTORTY BUREWALA

REHMAN COTTON GINNERS BAHAWLNAGUR

INDUS GINNERS RAJUNPUR

YASIR SHAHZAD COTTON GINNERS

INDUSTRY ANALYSIS:

Refer to HOK industry report.

5. MANAGEMENT :

Mr. Muhammad Anwar is the Chief Executive and Chairman of the Company, having more

than 20 years of experience in the line of business beginning with the waste recovery unit. He

is responsible for the procurement of raw material for all the group companies.

Mr. Muhammad Siddiq is younger brother of Mr. Anwar is looking after Sales and

marketing of the Company. It is pertinent to mention that directors of the company have no

impressive educational back ground, yet they have rich experience of their line of business in

their credit.

6. FINANCIAL ANALYSIS:

Amount in PKR Million

Particulars Sep 30, 2003

Audited

Sep 30, 2004

Audited

June 30, 2005

(9-Months)

Audited

Sales 568 985 691

Operating profit 27.182 15.214 24.786

Gross-Margin 12.4% 7% 9.1

Net-Margin 1.7% 0.4% 0.5%

Interest coverage 1.7x 1.3x 1.3x

Debt service coverage 1.5x 1.2x

INCOME STATEMENT:

Sales:

Sales of the company have been improving over the years and increased to PKR 985M

IN FY-04 from 568M in year 03 owing to increased & focused marketing efforts,

establishment of new local markets backed by enhanced production. While For the nine

months audited financials of year 05 sales stand at 737.774 M. Yarn.16 single, 20 single, 24

single, 40 single are the different qualities of yarn being produced by the company with

prices ranging from 3200 per bag to 5600 per bag.

Gross profit Margin:

Gross profit margin increased from 7% to 9.1% in year 2005 due to decrease in cost of

goods sold while cost of goods sold decreased mainly due to substantial drop in prices of

cotton in year 2005 in addition to this, Lower power & fuel consumption cost is one of the

reasons supporting cost efficiency and effectiveness, consequently leading to higher gross

profit margin in year 2005.

Operating profit:

Operating profit increased from 15.214M (1.5%) in year 04 to 24.786M (3.4%) in year

05 mainly due to carry forward impact of lower COGS happened due to lower cotton prices

during the year under review.

Net margin:

The profitability shown in the financials is tax tailored, actually their net margins fall

between 5 to 6 %. There is no significant improvement in net margin, in terms of percentage

because of high financials cost during the year, as the same has improved to 0.5% from

previous 0.4%.

Debt Service Coverage Ratio:

Debt service coverage ratio stands at 1.5x & 1.2x in year 04 and 05, the main reason

for relatively lower Debt to service coverage is lower profitability shown in books which are

more often tax-tailored.

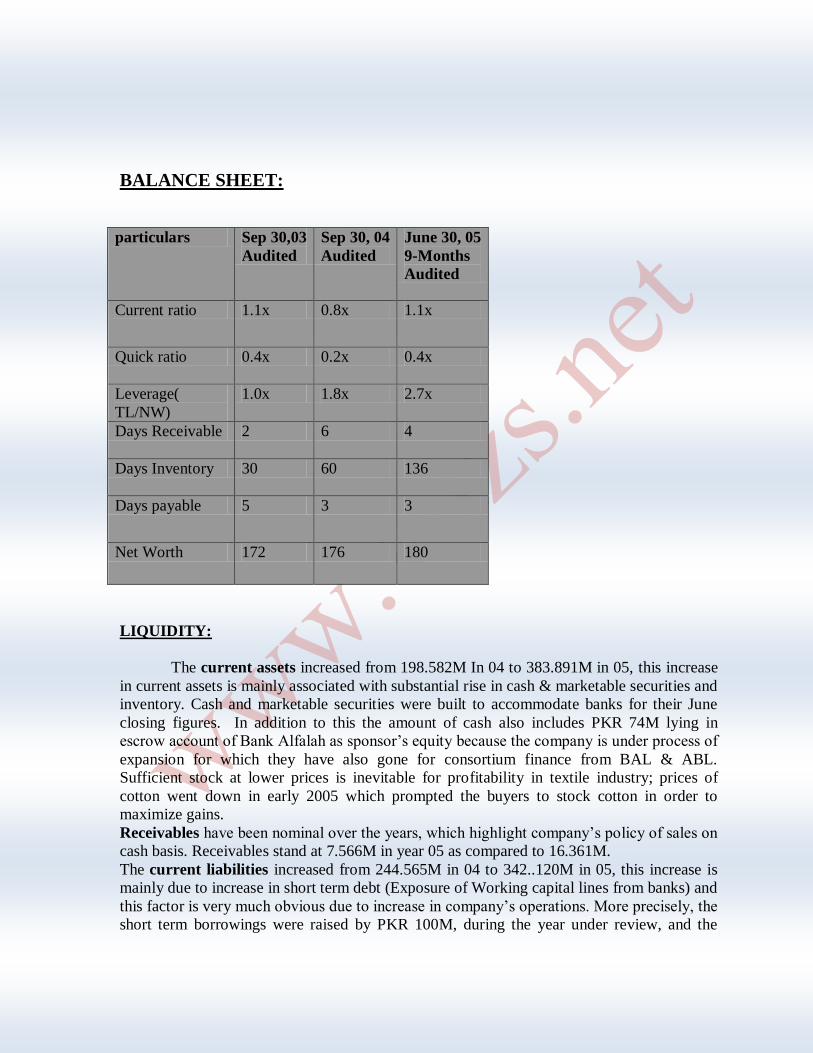

BALANCE SHEET:

particulars Sep 30,03

Audited

Sep 30, 04

Audited

June 30, 05

9-Months

Audited

Current ratio 1.1x 0.8x 1.1x

Quick ratio 0.4x 0.2x 0.4x

Leverage(

TL/NW)

1.0x 1.8x 2.7x

Days Receivable 2 6 4

Days Inventory 30 60 136

Days payable 5 3 3

Net Worth 172 176 180

LIQUIDITY:

The current assets increased from 198.582M In 04 to 383.891M in 05, this increase

in current assets is mainly associated with substantial rise in cash & marketable securities and

inventory. Cash and marketable securities were built to accommodate banks for their June

closing figures. In addition to this the amount of cash also includes PKR 74M lying in

escrow account of Bank Alfalah as sponsor‟s equity because the company is under process of

expansion for which they have also gone for consortium finance from BAL & ABL.

Sufficient stock at lower prices is inevitable for profitability in textile industry; prices of

cotton went down in early 2005 which prompted the buyers to stock cotton in order to

maximize gains.

Receivables have been nominal over the years, which highlight company‟s policy of sales on

cash basis. Receivables stand at 7.566M in year 05 as compared to 16.361M.

The current liabilities increased from 244.565M in 04 to 342..120M in 05, this increase is

mainly due to increase in short term debt (Exposure of Working capital lines from banks) and

this factor is very much obvious due to increase in company‟s operations. More precisely, the

short term borrowings were raised by PKR 100M, during the year under review, and the

same has been invested in inventory which increased by PKR 100m fully complying the

matching principle requirement.

LONG TERM LIABILITIES:

Total Long term liabilities increased from 62 .513M in 04 to 139.797M in 2005,

mainly due to increase in Director‟s Loan as the company is under process of expansion (new

Ring spinning unit) and has made investment of its share through directors loan as authorised

capital of the company has been matured. In addition to this company has also gone for

syndication with BANK ALFALAH Ltd and ALLIED BANK LTD and cash invested by

the sponsors through directors loan is lying in escrow accounts parked in these banks.

LEVERAGE:

The company has been low leveraged over the years with leverage standing at 1.8 x

& 2..7x in year 04 & 05 respectively, Total Net Worth increased during the period 03-05

from 172M TO 180M due to increase in retained earnings over the period. Paid-up-capital

stays same at 150M during the period 03-05.

CASH FLOW:

During the year 2005, gross operating funds generated were PKR 28.962M. The

company generated net operating cash deficit of PKR 73.917M during the year. The

operating needs increased by 93.683M owing to growth in sales, on the other side operating

sources were reduced by 9.196 M because of company‟s policy of replacing costly market

credit thus rendering increase in working capital requirements by 102..879 M. the inventory

requirements increased by 99.771M which were financed thru increase in short t term

borrowings by PKR. 99.548M and remaining through gross operating funds generated.

CAPEX of PKR 12 .383 was made during the year, which was financed thru gross operating

funds generated of PKR 28.962M.

PPrroojjeeccttiioonnss

The company has projected its total sales to be around 1034M by 30th

June

2006.These projections are supported by the fact that their sales by the end of 31stDec

2005(from July01, 2005 to Dec31, 2005) were 503.479M. This year company has also routed

export business of 12M to Korea. Net fixed assets are projected to grow around 614M since

company is intending to undertake the expansion project (New Ring Spinning) in the year

under projection. On the source side the long term liabilities are projected to be around

434M, the company wants to finance the proposed project thru Directors loan (222M),in

addition to this the company has also gone for the syndication( Long term senior Debt of

PKR 210M) with BAL & ABL.

Gross operating funds generated are projected to be around 33.747 M. Total Non-Operating

needs in year 06 will be 366 M due to increase in proposed CAPEX, on the other hand the

Non-operating source side will increase by 289M to finance Non-operating need.

7. CRITICAL SUCCESS AND RISK FACTORS

Critical Success Factors :

1- Lower Costs (economies of large scale).

2- Access to required Working Capital Lines.

3- Long experience of spinning.

4- Efficiency of Operations.

5- High Capacity Utilization.

Critical Risk Factors:

1- Recession in the Global Textile Industry.

2- GOP Policies.

3- Deterioration in Law & Order in the country.

4- Margins depend to an extent on size & quality of Cotton Crops.

5- Foreign Competition in wake of WTO.

MMiittiiggaattiinngg FFaaccttoorrss

Mitigating factors to these risks include;

1. New spinning unit will enable the company to enjoy economies of large scale

production, reduce costs, improve quality of their products and enhance their

productive efficiency.

2. GOP policies are comparatively stable and a separate ministry for textile has

been established with a leading Textile figure being in chair.

3. The company has always emphasized on sheer commitment for quality

improvement to capture the market.

4. Regarding risks associated with size / quality of cotton crop, they have

sufficient liquidity (due to availability of required credit lines) which allows

procuring cotton at the right time and competitive prices.

5. Experienced technical and operational staff to ensure smooth operation of the

Unit.

6. The company enjoys the edge of comparatively cheap raw material and labor

force while maintaining strict quality measures at par with international

standards. New spinning unit will enable the company to enjoy economies of

large-scale production.

8. THIRD PARTY INFORMATION:

The sponsors enjoy excellent relationship with banks and are highly regarded for

their reputation of meeting their financial obligations on ti

9.ACCOUNT RELATIONSHIP STRATEGY:

Rafiq is one of our valued clients with clean history of relationship spanning well

over four years. Keeping in view sufficient equity injection, comfortable level of leverage,

momentum of growth in sales and a team of professionals to look after the technical,

operational & marketing aspects of the business we should enhance our relationship with the

customer while opting the “Growth strategy”.

10. CONCLUSION / RECOMMENDATIONS :