Embed Size (px)

Citation preview

Life Can Be Uncertain.Retirement Doesn’t Have To Be.

MassMutual Transitions SelectSM

variable annuity

MassMutual EvolutionSM

variable annuity

Guide to Protection Benefits

Retirement Income

| insure | invest | retire |

What is a Deferred Variable Annuity?A deferred variable annuity is a contract between a contract owner and aninsurance company. It is a long-term investment designed to help peopleaccumulate and protect assets for retirement using the annuity’s invest-ment and insurance features. Deferred variable annuity contracts offer:

• Tax-deferred accumulation potential

• Professionally managed investment options and a fixed account

• Asset allocation strategies*

• Annuity income payments

• Living benefits**

• Death benefits

Deferred variable annuities are not appropriate for everyone. There arefees and charges associated with owning an annuity. Variable annuitiesdo not provide any additional tax advantage when used to fund a quali-fied plan. Investors should consider buying a variable annuity to fund aqualified plan for the annuity’s additional features, such as lifetimeincome payments and death benefit protection. Be sure to read theprospectus and talk with your financial professional prior to purchasingan annuity.

The optional features discussed in this brochure cannot be electedwithout purchasing a variable annuity contract. The benefits may not beappropriate for investors who do not foresee a need for additionalprincipal protection, lifetime income or death benefit protection andwhose primary focus is tax deferral. Please make sure the variableannuity contract is suitable for your investment goals before consid-ering electing these optional features.

**Asset allocation does not ensure a profit or protect against loss.**Earnings are taxable as income when distributed and if withdrawn before age 591/2, and may be subject to a 10% federal tax penalty.

Units may be worth more or less than their original cost when redeemed.

Not FDIC/NCUA Insured Not A Bank Deposit Not Bank GuaranteedMay Lose Value Not Insured By Any Federal Government Agency

Personalize Your Contract with Optional Protection BenefitsWhen planning for retirement, it’s important to select products and services thatmeet your needs today and in the future. In addition to a MassMutual variableannuity’s basic contract provisions, there are optional benefits that can be added tohelp personalize your contract. This brochure describes the most common optionalprotection benefits available with a MassMutual Evolution or MassMutualTransitions Select variable annuity. Additional features are described in the clientbrochures and product prospectuses.

Living Benefit for AccumulationGuaranteed Minimum Accumulation Benefit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . page 4Guaranteed Principal Protection or Double Principal Protection

Living Benefits for IncomeMassMutual Guaranteed Income Plus 5SM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . page 9Income Now through Immediate Withdrawals Income Later using a Guaranteed Minimum Benefit Base for Lifetime Income

MassMutual Lifetime Payment PlusSM. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . page 17Lifetime Income through the Guaranteed Flexibility of Withdrawals

Death Benefits

Annual Ratchet Death Benefit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .page 24Enhanced Protection for Beneficiaries

Contract Value Death Benefit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . page 25Death Benefit Protection Not a Primary Concern

Guarantees are based on the claims-paying ability of the issuing company. A withdrawal provision is available within each product at no additional cost. Please refer to the appropriate productprospectus for complete details. The protection benefits discussed in this brochure are only available through a MassMutual Evolution or MassMutualTransitions Select deferred variable annuity. They cannot be purchased separately and may not be available in all states.

1

Why MassMutual?When you purchase an annuity, you may depend on its guarantees for decades.That’s why it’s important to invest with a company that will be there to honor its commitments.

Founded in 1851, MassMutual is a mutually owned financial protection, accu-mulation and income management company with a long history of financialstrength and growth. Variable annuity guarantees are based on the claims-paying ability of the issuing company. A company’s claims-paying ability isbased on its financial strength, so when it comes time to choose a company,financial strength ratings are an important aspect to consider.

Our financial strength ratings are among the highest in any industry:

A.M. Best Company. . . . . . . . . . . . A++ (Superior – 1st category of 15)Fitch Ratings . . . . . . . . . . . . . . . . . AAA (Exceptionally Strong – 1st category of 24)Moody’s Investors Service, Inc . . . Aa1 (Excellent – 2nd category of 21)Standard & Poor’s Corp . . . . . . . . . AAA (Extremely Strong – 1st category of 20)

MassMutual Financial Group is a marketing name for Massachusetts Mutual Life Insurance Company(MassMutual) and its affiliated companies and sales representatives. Financial strength ratings are forMassachusetts Mutual Life Insurance Company as of November 1, 2008. Ratings are subject to change anddo not apply to the separate account or the variable investment choices offered through the contract.

2

livin

g b

en

efit fo

r ac

cu

mu

latio

n

3

Guaranteed MinimumAccumulation Benefit(GMAB) Optional Benefit

For investors who:• Don’t need income immediately• Want guaranteed principal protection, or

double principal protection• Have at least a 10-year investment horizon

Benefit Briefing• Guaranteed return of your first two years’

purchase payments (adjusted for withdrawals)after 10 years and the ability to lock in potentialinvestment gains, or

• Guaranteed return of 200% of your first two years’purchase payments (adjusted for withdrawals)after 20 years

Additional ChargeMassMutual Evolution: Current: 0.50%; Maximum: 1.00%(Charge deducted each day from the contract value in the

funds, after fund expenses are deducted.)

MassMutual Transitions Select:Current: 0.45%; Maximum: 1.00%(Charge deducted from each payment received during

the first contract year. After the first year, charge is

deducted from the assets of the separate account on the

contract’s anniversary.)

The GMAB guarantees your contract value at the endof a benefit period will be no less than the premiumpayments made during the first two contract years(adjusted for withdrawals), regardless of investmentperformance. Two benefit periods are offered: a 10-year benefit period with a reset option and a 20-yearbenefit period (26 years in New York).

10-Year GMAB with Reset OptionThis benefit period initially ends upon the 10th contractanniversary, although a reset can be requested. If areset is not requested and the contract value is lessthan the GMAB value at the end of the benefit period,MassMutual will credit the difference to your contract.

Resets “Lock in” Investment GainsA reset can be requested on the second contractanniversary and any anniversary thereafter, until theend of the benefit period. If the contract value isgreater than the GMAB value, the GMAB value will beincreased to the higher amount and a new 10-yearbenefit period will begin.

• Maximum age for issue: 89 (age 79 in New York)

• Maximum age for reset: 89 (age 79 in New York)

20-Year GMABThis benefit period ends upon the 20th contract anniversary (26th anniversary in New York). It guaran-tees that the contract value at the end of the period willbe no less than double the amount of the purchasepayments made during the first two years, adjustedfor withdrawals. The 20-year GMAB does not include areset option.

• Maximum age for issue: 79 (age 63 in New York)

liv

ing

be

ne

fit

– G

MA

B

4Guarantees are based on the claims-paying ability of the issuing company.

livin

g b

en

efit –

GM

AB

5

This hypothetical example is for illustrative purposes only and is meant to show how this feature works. It is not intended to predict or projectinvestment results.

50 565554535251 57 6362 656461605958

waiting period

GMAB Value

10 Years After Last Reset

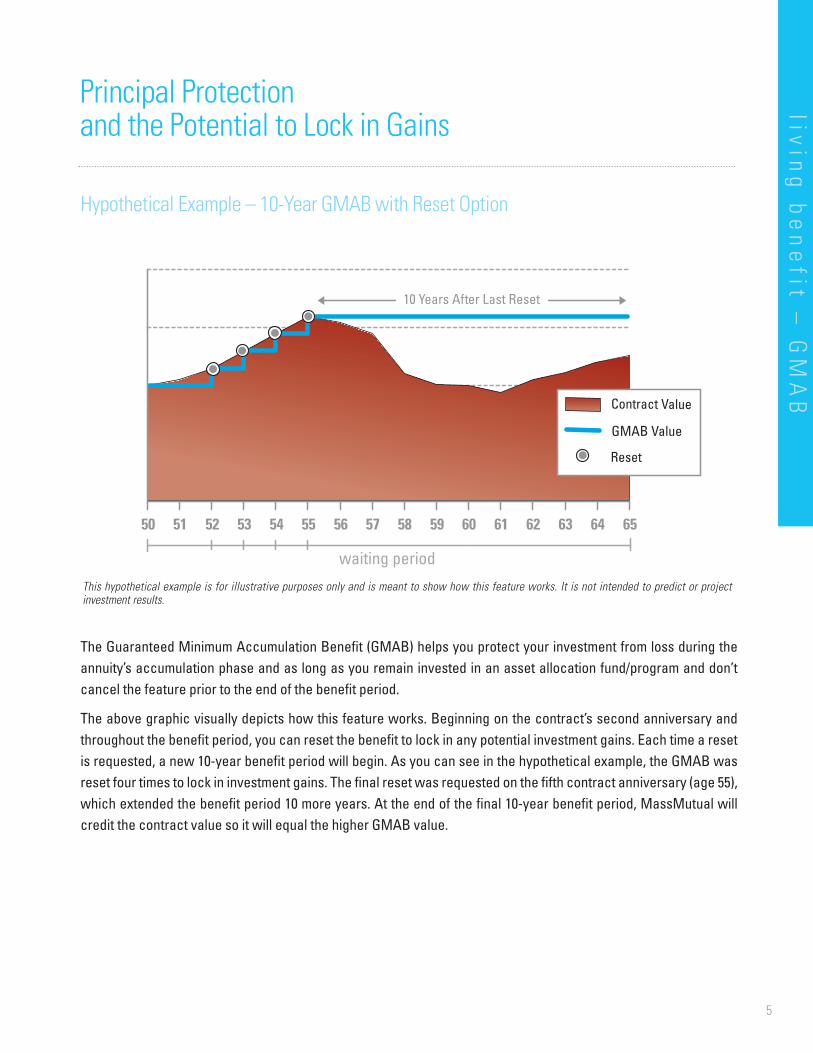

The Guaranteed Minimum Accumulation Benefit (GMAB) helps you protect your investment from loss during theannuity’s accumulation phase and as long as you remain invested in an asset allocation fund/program and don’tcancel the feature prior to the end of the benefit period.

The above graphic visually depicts how this feature works. Beginning on the contract’s second anniversary andthroughout the benefit period, you can reset the benefit to lock in any potential investment gains. Each time a resetis requested, a new 10-year benefit period will begin. As you can see in the hypothetical example, the GMAB wasreset four times to lock in investment gains. The final reset was requested on the fifth contract anniversary (age 55),which extended the benefit period 10 more years. At the end of the final 10-year benefit period, MassMutual willcredit the contract value so it will equal the higher GMAB value.

Hypothetical Example – 10-Year GMAB with Reset Option

Principal Protection and the Potential to Lock in Gains

liv

ing

be

ne

fit

–G

MA

B

6

Years 1 20

Initial Investment

GMAB Value: Double the Initial Investment

GMAB Value

Positive Annual Return

Contract Value (Positive Performance)

Negative Annual Return

Contract Value (Negative Performance)

�

�

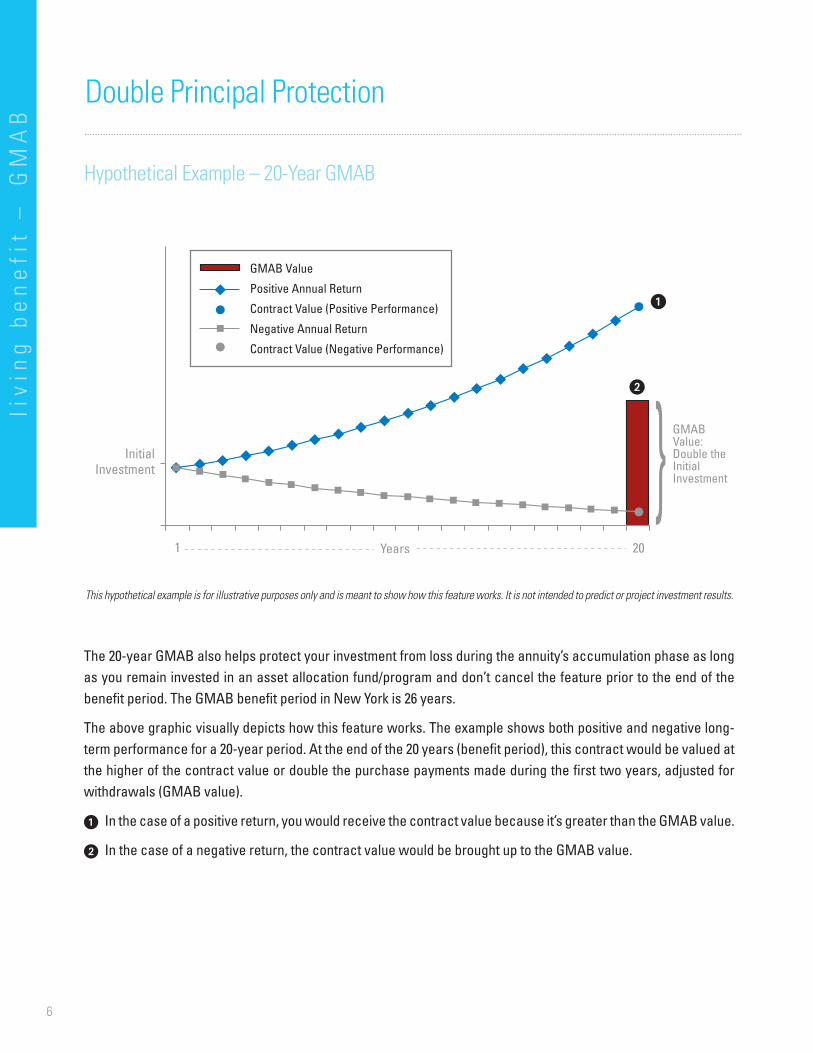

This hypothetical example is for illustrative purposes only and is meant to show how this feature works. It is not intended to predict or project investment results.

The 20-year GMAB also helps protect your investment from loss during the annuity’s accumulation phase as longas you remain invested in an asset allocation fund/program and don’t cancel the feature prior to the end of thebenefit period. The GMAB benefit period in New York is 26 years.

The above graphic visually depicts how this feature works. The example shows both positive and negative long-term performance for a 20-year period. At the end of the 20 years (benefit period), this contract would be valued atthe higher of the contract value or double the purchase payments made during the first two years, adjusted forwithdrawals (GMAB value).

� In the case of a positive return, you would receive the contract value because it’s greater than the GMAB value.

� In the case of a negative return, the contract value would be brought up to the GMAB value.

Hypothetical Example – 20-Year GMAB

Double Principal Protection

Benefit Details• This feature can only be elected at contract issue

and may be cancelled at any time. Once cancelled,it cannot be re-elected.

• Age calculation criteria:

• To receive the GMAB value, you cannot cancel thefeature or enter the income phase until the end ofthe benefit period and, you must invest in an MMLallocation fund or select investment choices withinthe parameters of the custom allocation choiceprogram until the end of the benefit period.

• The GMAB cannot be elected at the same time as another MassMutual living benefit.

• The GMAB does not guarantee the performance ofthe investment choices within the contract.

• Purchase payments made after the secondcontract year could increase the cost of the GMABwithout a corresponding increase in the benefit.

Key TermsBenefit Period – The amount of time you have to waitto get the GMAB value.

Guaranteed Minimum Accumulation Benefit (GMAB) –An optional feature that guarantees the contract valuewill be no less than a specified amount (GMAB value)at the end of a benefit period.

GMAB Value – The total of all purchase paymentsmade during the first two contract years, adjusted forwithdrawals.

GMAB Value at Reset – The GMAB value is increased to the amount of the contract value, provided thecontract value is greater at the time of reset. The newvalue will be adjusted for any subsequent withdrawalsduring the balance of the benefit period.

livin

g b

en

efit –

GM

AB

7

Guaranteed Minimum Accumulation Benefit

Age = 6 months prior to and after the stated age. Ex: 79 yrs., 6 mo., 1 day � Age 80 � 80 yrs., 6 mo.

8

liv

ing

be

ne

fit

for

inc

om

e

livin

g b

en

efit –

GM

IB

9

MassMutual GuaranteedIncome Plus 5SM

Optional Benefit

For investors who want:

• Maximum lifetime income potential throughannuity payments, and

• Flexibility to receive income now throughwithdrawals

Benefit Briefing• Guaranteed lifetime income through

annuity payments

• Lifetime income guarantees starting at age 60 or in 10 years, whichever is later

• Immediate withdrawals up to 5% of the benefitbase annually to age 90

• Larger withdrawals and lifetime income payments if the market performs well

• If no current income needed, larger lifetimeincome through annuity payments, even ifmarkets perform poorly

• Death benefit protection prior to annuity payments beginning

Additional ChargeMassMutual Guaranteed Income Plus 5 Current: 0.65%; Maximum: 1.50%(Charges are assessed at quarter-end for the previousquarter and are based on the GMIB value.)

MassMutual Guaranteed Income Plus feature is aGuaranteed Minimum Income Benefit (GMIB). Thebenefit guarantees a minimum benefit base (GMIBvalue), regardless of investment performance. TheGMIB value equals your purchase payments (adjustedfor withdrawals) made during the first two contractyears, increased by a compound annual interest rateof 5%. If the GMIB value is greater than your contractvalue, it can be applied to an annuity payment optionon or after the tenth contract anniversary.

Income Now. Income Later.If needed, you can withdraw the interest credited toyour GMIB value in the current contract year, withoutimpacting the guarantee. Withdrawals will reduce yourGMIB value by one dollar for every dollar taken.Withdrawals in excess of the interest credited willreduce your GMIB value and the maximum GMIB valueproportionally and will negatively impact your benefit.Even if your contract value drops to zero, you can applyyour GMIB value to an annuity payment option.

Resets “Lock in” Potential Gains, OfferGreater Income PotentialIf your contract value grows, the amount you haveavailable to withdraw and your lifetime income willincrease automatically on your contract anniversary.A reset allows you to increase your GMIB value toequal your current contract anniversary value,provided it is greater. Your new GMIB value will begincompounding at the annual interest rate of the benefityou selected. Your GMIB value will automaticallyreset on or after your first contract anniversary up toage 80 (annuitant), unless you tell us otherwise. Eachtime you lock in investment gains through a reset, youwill start a new 10-year waiting period.

Guarantees are based on the claims-paying ability of the issuing company.

liv

ing

be

ne

fit

– G

MIB

10

Income Now – In a Down MarketEven if your contract value drops to zero

Guaranteed Income Plus 5 – Hypothetical Example1

waiting period

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

75747372717069686766656463626160

$6,375Guaranteed

for Life

Hypothetical Net Annual Returns (%)

-20.1 12.6 -15.0 -21.0 15.7 -15.6 3.8 11.7 22.3 1.1

$5,000$5,000

�

Contract Value

Withdrawals

Annuity Payment

GMIB Value

�

1 This hypothetical example is for illustrative purposes only and is meant to show how this feature works assuming hypotheti-cal rates of return. It is not intended to predict or project investment results. Assumptions: $100,000 investment. A net average annual investment return of –1.7% (gross 1.4%) over 10 years reflects a maximum 2.00% separate account charge,1.50% maximum (0.65% current) Guaranteed Income Plus 5 charge assessed quarterly at quarter end and 1.12% gross under-lying fund expenses. Fixed annuity payments assume a life with 10-year period certain, male age 71 and monthly payments.Payments shown reflect the sum of 12 monthly payments. The investment return and principal value of a variable annuity willfluctuate with market conditions. Accumulation Units, when redeemed, may be worth more or less than their original cost.

�Steady Income – The GMIB value and withdrawals do not decrease even though thecontract value declines significantly for an extended period of time.

�Guaranteed Lifetime Income – If the contract value drops to zero, withdrawals would nolonger be available. The GMIB value could be applied to an annuity payment option thatcould guarantee income for life. At age 71, annuity payments would provide more incomethan withdrawals.

livin

g b

en

efit –

GM

IB

11

Income Now – In a Down Market

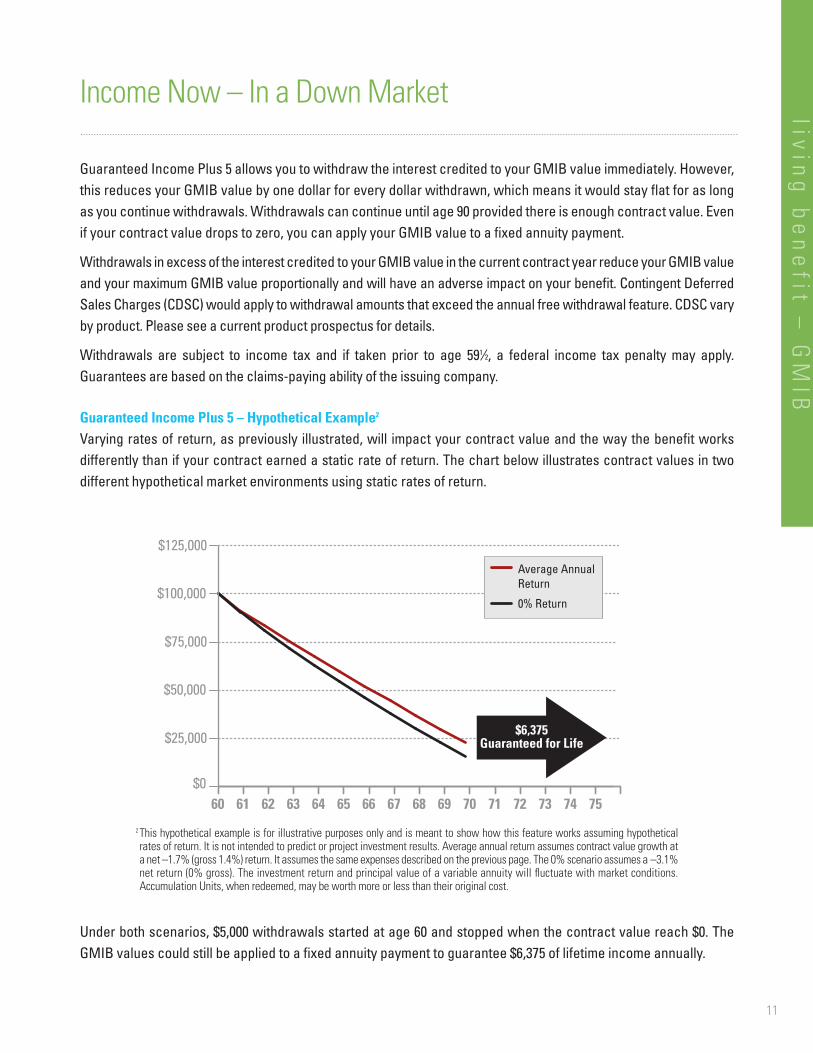

Guaranteed Income Plus 5 allows you to withdraw the interest credited to your GMIB value immediately. However,this reduces your GMIB value by one dollar for every dollar withdrawn, which means it would stay flat for as longas you continue withdrawals. Withdrawals can continue until age 90 provided there is enough contract value. Evenif your contract value drops to zero, you can apply your GMIB value to a fixed annuity payment.

Withdrawals in excess of the interest credited to your GMIB value in the current contract year reduce your GMIB valueand your maximum GMIB value proportionally and will have an adverse impact on your benefit. Contingent DeferredSales Charges (CDSC) would apply to withdrawal amounts that exceed the annual free withdrawal feature. CDSC varyby product. Please see a current product prospectus for details.

Withdrawals are subject to income tax and if taken prior to age 591⁄2, a federal income tax penalty may apply.Guarantees are based on the claims-paying ability of the issuing company.

Guaranteed Income Plus 5 – Hypothetical Example2

Varying rates of return, as previously illustrated, will impact your contract value and the way the benefit worksdifferently than if your contract earned a static rate of return. The chart below illustrates contract values in twodifferent hypothetical market environments using static rates of return.

Under both scenarios, $5,000 withdrawals started at age 60 and stopped when the contract value reach $0. TheGMIB values could still be applied to a fixed annuity payment to guarantee $6,375 of lifetime income annually.

2 This hypothetical example is for illustrative purposes only and is meant to show how this feature works assuming hypotheticalrates of return. It is not intended to predict or project investment results. Average annual return assumes contract value growth ata net –1.7% (gross 1.4%) return. It assumes the same expenses described on the previous page. The 0% scenario assumes a –3.1%net return (0% gross). The investment return and principal value of a variable annuity will fluctuate with market conditions.Accumulation Units, when redeemed, may be worth more or less than their original cost.

$0

$25,000

$50,000

$75,000

$100,000

$125,000

75747372717069686766656463626160

Average Annual Return

0% Return

$6,375Guaranteed for Life

liv

ing

be

ne

fit

– G

MIB

12

Income Later – In an Up MarketResets offer Rising Income Potential

Guaranteed Income Plus 5 – Hypothetical Example3

waiting period

$0

$50,000

$100,000

$150,000

$200,000

$250,000

8079787776757473727170696867666564636261605958575655

$16,742Guaranteed

for Life

$5,829$6,463

$8,574$9,842 $11,738

$11,738

Hypothetical Net Annual Returns (%)

10.2 12.6 13.1 3.2 4.2 -3.1 -13.0 -5.1 6.5 12.0 9.2 -1.1 18.5 14.8 12.3 -6.6 11.4 15.8 16.6

$5,000

Annual Withdrawals Available

$129,720

$234,761

�

�

�

�

Contract Value

Withdrawals

Annuity Payments

GMIB Value

Reset

$6,786

�

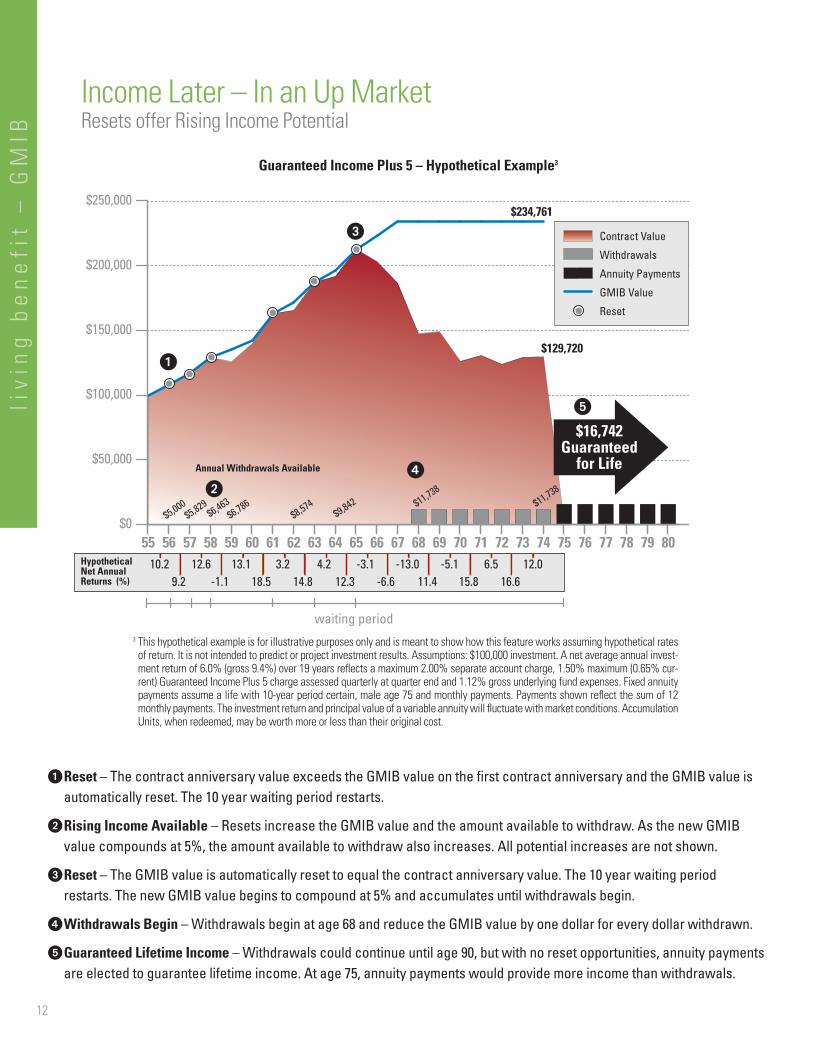

�Reset – The contract anniversary value exceeds the GMIB value on the first contract anniversary and the GMIB value isautomatically reset. The 10 year waiting period restarts.

�Rising Income Available – Resets increase the GMIB value and the amount available to withdraw. As the new GMIBvalue compounds at 5%, the amount available to withdraw also increases. All potential increases are not shown.

�Reset – The GMIB value is automatically reset to equal the contract anniversary value. The 10 year waiting periodrestarts. The new GMIB value begins to compound at 5% and accumulates until withdrawals begin.

�Withdrawals Begin – Withdrawals begin at age 68 and reduce the GMIB value by one dollar for every dollar withdrawn.

�Guaranteed Lifetime Income – Withdrawals could continue until age 90, but with no reset opportunities, annuity paymentsare elected to guarantee lifetime income. At age 75, annuity payments would provide more income than withdrawals.

3 This hypothetical example is for illustrative purposes only and is meant to show how this feature works assuming hypothetical ratesof return. It is not intended to predict or project investment results. Assumptions: $100,000 investment. A net average annual invest-ment return of 6.0% (gross 9.4%) over 19 years reflects a maximum 2.00% separate account charge, 1.50% maximum (0.65% cur-rent) Guaranteed Income Plus 5 charge assessed quarterly at quarter end and 1.12% gross underlying fund expenses. Fixed annuitypayments assume a life with 10-year period certain, male age 75 and monthly payments. Payments shown reflect the sum of 12monthly payments. The investment return and principal value of a variable annuity will fluctuate with market conditions. AccumulationUnits, when redeemed, may be worth more or less than their original cost.

livin

g b

en

efit –

GM

IB

13

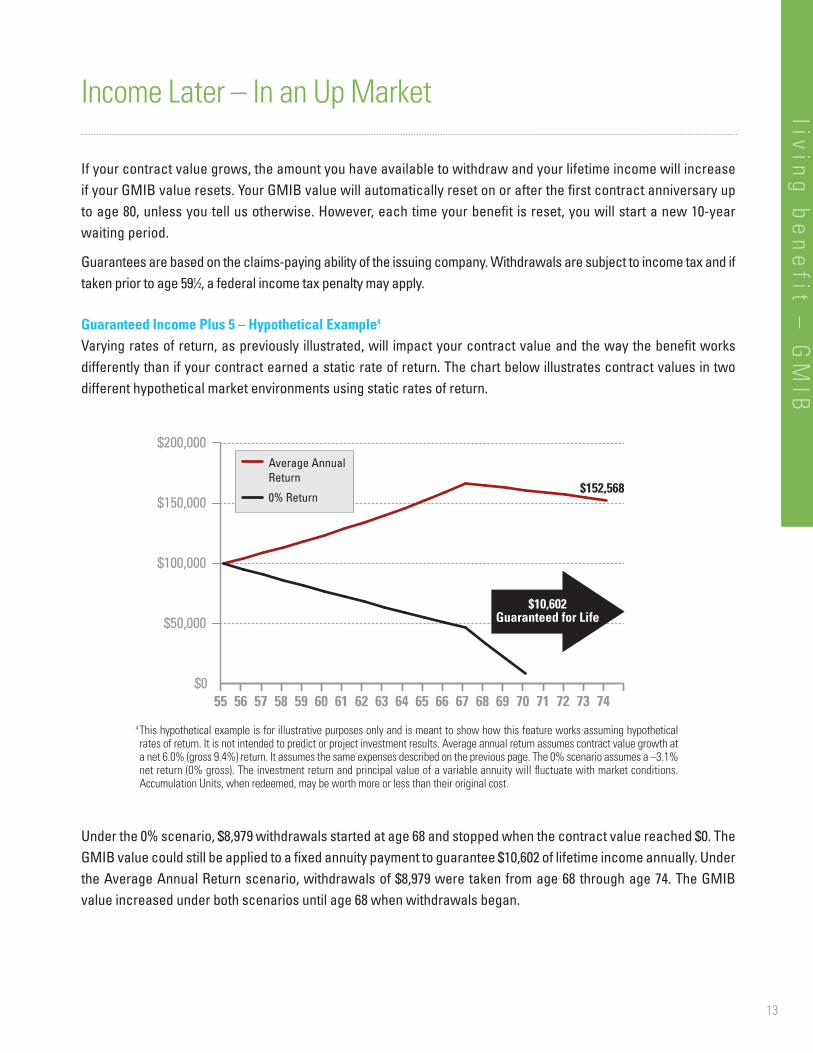

Income Later – In an Up Market

If your contract value grows, the amount you have available to withdraw and your lifetime income will increaseif your GMIB value resets. Your GMIB value will automatically reset on or after the first contract anniversary upto age 80, unless you tell us otherwise. However, each time your benefit is reset, you will start a new 10-yearwaiting period.

Guarantees are based on the claims-paying ability of the issuing company. Withdrawals are subject to income tax and iftaken prior to age 591⁄2, a federal income tax penalty may apply.

Guaranteed Income Plus 5 – Hypothetical Example4

Varying rates of return, as previously illustrated, will impact your contract value and the way the benefit worksdifferently than if your contract earned a static rate of return. The chart below illustrates contract values in twodifferent hypothetical market environments using static rates of return.

4 This hypothetical example is for illustrative purposes only and is meant to show how this feature works assuming hypotheticalrates of return. It is not intended to predict or project investment results. Average annual return assumes contract value growth ata net 6.0% (gross 9.4%) return. It assumes the same expenses described on the previous page. The 0% scenario assumes a –3.1%net return (0% gross). The investment return and principal value of a variable annuity will fluctuate with market conditions.Accumulation Units, when redeemed, may be worth more or less than their original cost.

$0

$50,000

$100,000

$150,000

$200,000

7473727170696867666564636261605958575655

Average Annual Return

0% Return

$10,602Guaranteed for Life

$152,568

Under the 0% scenario, $8,979 withdrawals started at age 68 and stopped when the contract value reached $0. TheGMIB value could still be applied to a fixed annuity payment to guarantee $10,602 of lifetime income annually. Underthe Average Annual Return scenario, withdrawals of $8,979 were taken from age 68 through age 74. The GMIBvalue increased under both scenarios until age 68 when withdrawals began.

liv

ing

be

ne

fit

– G

MIB

14

Do You Want Guaranteed Lifetime Income?

Guaranteed Income Plus 5 allows you to defer income or choose when and how you want to take it. You can choose towithdraw the interest on your GMIB value for as long as you have contract value up to age 90. However, at age 90 you willhave to make a decision to:

� Receive Guaranteed Lifetime Income – You could choose to apply your GMIB value to a fixed annuity paymentoption and receive guaranteed income for life; or

� Discontinue the Benefit – If you choose to do nothing, the benefit and its charge will terminate. However, ifyour contract value has declined significantly you will have some additional protection.

60% GMIB value feature: If your contract value is less than 60% of your GMIB value, your contract value willincrease to an amount equal to 60% of your GMIB value.

Your decision will most likely depend on your investment experience. If your contract value has appreciated signif-icantly, then you may want to discontinue the benefit and continue withdrawals without any guarantees. Or, youcould choose to apply your contract value to an annuity payment option. This could be done up to age 100. The chartbelow illustrates your choices using a hypothetical example of a protracted market decline.

This hypothetical example is for illustrative purposes only and is meant to show how this feature works assuming a static rate of return.It is not intended to predict or project investment results. Assumptions: $100,000 investment. A net average annual investment returnof 4.6% (gross 8.0%) over 20 years reflects a maximum 2.00% separate account charge, 1.50% maximum (0.65% current) GuaranteedIncome Plus 5 charge assessed quarterly at quarter end and 1.12% gross underlying fund expenses. At age 90 a withdrawal is assumedalthough not graphically depicted as it pertains to the 60% GMIB value feature illustration. Fixed annuity payments assume a life with10-year period certain, male age 90 and monthly payments. Payments shown reflect the sum of 12 monthly payments. The 0% lineincludes the same charges but assumes a net average annual investment return of –3.12% (gross 0.0%). The investment return andprincipal value of a variable annuity will fluctuate with market conditions. Accumulation Units, when redeemed, may be worth moreor less than their original cost.

waiting period

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

9594939291908988878685848382818079787776757473727170

$9,804Guaranteed for Life

$5,000$5,000

�

�

Contract Value

Annuity Payments

Withdrawals

GMIB Value

0% Contract Value

Withdrawals

Two Choices at Age 90: � or �

livin

g b

en

efit –

GM

IB

15

Benefit Details• This feature can only be elected at contract issue

and may be cancelled at any time. Once cancelled,it cannot be re-elected.

• Maximum issue age is 80 (annuitant).

• Age calculation criteria:

• You must invest in an MML allocation fund or selectinvestment choices within the parameters of a customallocation choice program offered by MassMutual.

• To apply the GMIB value to an annuity paymentoption, the annuitant must be between the ages of60 and 90 and at least 10 years must have passedfrom the purchase date or the date of the last reset.

• Subsequent payments after year two will notincrease the GMIB value. They will only increasethe GMIB value and the applicable cost if theGMIB value is reset.

• This benefit cannot be elected at the same time asanother MassMutual living benefit.

• You may elect a life or life with period certain fixedannuity payment option. A period certain can’t begreater than 20 years if the annuitant is age 80 orunder or 10 years if the annuitant is over age 81.Annuity payment options vary in NY.

• Withdrawals will reduce the contract value andthe contract death benefit.

• A free withdrawal provision is available withineach product. You should weigh the additional costof MassMutual Guaranteed Income Plus againstthe benefits provided by the feature.

Compound Annual Interest Rate: 5%Maximum GMIB Value: 200% of first two years’purchase payments or most recent reset, adjusted forwithdrawals.

Key TermsBenefit Period – A 10-year period during which youmust wait before applying your GMIB value to anannuity payment option.

GMIB Value – Your first two contract years’ purchasepayments (adjusted for withdrawals), increased by a5% compound annual interest rate.

GMIB Value at Reset – If your contract value exceedsyour GMIB value on or after your first contract anniver-sary, your GMIB value will automatically increase toequal your contract value, unless you tell us otherwise.A reset locks in potential gains and begins a new10-year benefit waiting period. If you choose to opt outof the automatic resets, you would have to choose toopt back in to start receiving automatic resets again.

MassMutual Guaranteed Income Plus 5

Age = 6 months prior to and after the stated age. Ex: 79 yrs., 6 mo., 1 day � Age 80 � 80 yrs., 6 mo.

liv

ing

be

ne

fit

for

inc

om

e

16

17

livin

g b

en

efit –

GM

WB

MassMutual LifetimePayment PlusSM

Optional Benefit

For investors who want:• Lifetime income, and

• Full access to contract value during life and forbeneficiaries at death

Benefit Briefing• Guaranteed lifetime income through

withdrawals

• Lifetime income guarantees starting at age 60*

• Immediate withdrawals up to 5% of the benefitbase annually

• Larger withdrawals and lifetime withdrawals ifthe market performs well

• If no withdrawals are taken, larger withdrawalsand lifetime withdrawals, even if marketsperform poorly

• Death benefit protection during entire lifetime

* In the case of joint lives, all age restrictions noted arebased on the age of the youngest person.

Additional chargeSingle Life Charge: Current: 0.60%; Maximum 1.50%

Joint/Spousal LifeCharge: Current: 0.85%; Maximum 1.50% (Charges are assessed at quarter-end for the previousquarter on the benefit base.)

All taxable withdrawals are subject to income tax and iftaken prior to age 591⁄2, a federal tax penalty may apply.

This feature is a Guaranteed Minimum WithdrawalBenefit (GMWB). It guarantees a minimum amount ofincome that can be withdrawn for life, regardless ofinvestment performance. It also allows for increasesin withdrawal amounts if your contract experiencespositive investment performance.

Guaranteed Lifetime IncomeBeginning at age 60, you can take 5% of your contract’sbenefit base annually (Guaranteed Lifetime Withdrawals).The base equals your purchase payments, but mayincrease over time due to credits or positive invest-ment performance that is reflected in Annual Ratchets.

Income Guaranteed Not to DecreaseYour Guaranteed Lifetime Withdrawal Amount willnever be less than your initial amount, unless youbegin withdrawals prior to age 60 or you withdraw anamount in excess of 5% of your benefit base.

Withdrawals taken prior to age 60 that equal 5% of yourbenefit base annually are referred to as GuaranteedWithdrawal Amounts. They will reduce your benefitbase by one dollar for every dollar withdrawn and couldreduce your Guaranteed Lifetime Withdrawal amounts.

Automatic Rising Income PotentialThe amount of income available for withdrawal willautomatically increase each year if there is an increasein your contract value on your contract’s anniversarydate, prior to age 91.

Rewards for WaitingYour benefit base will be credited each year you do nottake a withdrawal during the first 10 contract years.The credit will equal 6% of your initial benefit base andmay increase or decrease with changes in your benefitbase amount.

You can receive an enhanced credit to your benefit baseequal to 200% of your first year’s purchase payments ifyou do not withdraw from your contract during the first10 contract years or age 70, whichever is later.

18

liv

ing

be

ne

fit

– G

MW

B Guaranteed Lifetime Income Even if Your Contract Value Drops to Zero

Lifetime Payment Plus – Hypothetical Example5

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

75747372717069686766656463626160Hypothetical Net Annual Returns (%)

-16.6 9.7 -23.5 -18.2 8.8 -14.1 5.0 8.5 16.5 -17.5

$5,000$5,000

�

� Guaranteed Lifetime Withdrawals

Contract Value

Guaranteed Lifetime Withdrawal Amount

Benefit Base

5 This hypothetical example is for illustrative purposes only and is meant to show how this feature works assuming hypotheti-cal rates of return. It is not intended to predict or project investment results. Assumptions: $100,000 investment. A net aver-age annual investment return of –5.2% (gross –2.1%) over 10 years reflects a maximum 2.00% separate account charge,1.50% maximum (0.60% current / single life) Lifetime Payment Plus charge assessed quarterly at quarter end and 1.12% grossunderlying fund expenses. The investment return and principal value of a variable annuity will fluctuate with market condi-tions. Accumulation Units, when redeemed, may be worth more or less than their original cost.

�Steady Income – Your benefit base and withdrawals do not decrease even though thecontract value declines significantly for an extended period of time.

�Guaranteed Lifetime Income – Withdrawals are guaranteed for life, even if the contractvalue drops to zero.

At age 60, you may begin Guaranteed Lifetime Withdrawals equal to 5% of your benefit base. Thisis your minimum Guaranteed Lifetime Withdrawal Amount. It will never decrease, unless you with-draw more than 5% of your benefit base. In this example, you would be guaranteed to receivewithdrawals annually for as long as you live, even though your contract value drops to zero.

19

livin

g b

en

efit –

GM

WB

Contracts below the minimum contract value after a withdrawal enter the settlement phase. The settlement phaseallows you to receive guaranteed payments for life. However, other contract rights, including death benefits andthe right to make additional purchase payments, will terminate. The charge for this benefit will also terminate.

Guarantees are based on the claims-paying ability of the issuing company.

Withdrawals are subject to income tax and, if taken prior to age 591/2, a federal income tax penalty may apply.

Lifetime Payment Plus – Hypothetical Example6

Varying rates of return, as previously illustrated, will impact your contract value and the way the benefit works dif-ferently than if your contract earned a static rate of return. The chart below illustrates contract values in two dif-ferent hypothetical market environments using static rates of return.

6 This hypothetical example is for illustrative purposes only and is meant to show how this feature works assuming hypotheti-cal rates of return. It is not intended to predict or project investment results. Average annual return assumes contract valuegrowth at a net –5.2% (gross –2.1%) return. It assumes the same expenses described on the previous page. The 0% scenarioassumes a –3.1% net return (0% gross). The investment return and principal value of a variable annuity will fluctuate withmarket conditions. Accumulation Units, when redeemed, may be worth more or less than their original cost.

In this example, you would be guaranteed to receive withdrawals annually for as long as youlive, even though your contract value drops to zero.

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

75747372717069686766656463626160

Average Annual Return

0% Return

Guaranteed LifetimeWithdrawals

20

liv

ing

be

ne

fit

– G

MW

B Automatic Rising Income PotentialCredits and Annual Ratchets

Lifetime Payment Plus – Hypothetical Example7

$0

$30,000

$60,000

$90,000

$120,000

$150,000

$180,000

$210,000

$240,000

75747372717069686766656463626160

$10,000$10,000

�

�

�

�

�

�

Guaranteed Lifetime Withdrawals

Enhanced Credit

Hypothetical Net Annual Returns (%)

4.7 -0.9 19.7 15.7 -5.1 17.5 4.5 16.2 3.7 2.1 20.9 -7.9 -1.2 0.4 8.8

Contract Value

Guaranteed Lifetime Withdrawal Amount

Benefit Base

Annual Ratchets

$6,200$7,210

$8,717

Annual Withdrawals Available

$5,600

7 This hypothetical example is for illustrative purposes only and is meant to show how this feature works assuming hypotheticalrates of return. It is not intended to predict or project investment results. Assumptions: $100,000 investment. A net averageannual investment return of 6.2% (gross 9.6%) over 15 years reflects a maximum 2.00% separate account charge, 1.50% max-imum (0.60% current / single life) Lifetime Payment Plus charge assessed quarterly at quarter end and 1.12% gross underlying fund expenses. The investment return and principal value of a variable annuity will fluctuate with market condi-tions. Accumulation Units, when redeemed, may be worth more or less than their original cost.

�6% Credit – a simple interest credit is added to the benefit base each year there are nowithdrawals.

�Credits Increase Income Available – Credits to the benefit base increase the GuaranteedLifetime Withdrawal Amounts available during the first five years when there’s negative orslow growth.

�Annual Ratchet – Each year the contract anniversary value exceeds the benefit base, thebenefit base automatically ratchets up to equal the contract anniversary value.

�Credit Increases – After an annual ratchet, credits increase because they’re now equal to6% of the new benefit base.

21

livin

g b

en

efit –

GM

WB

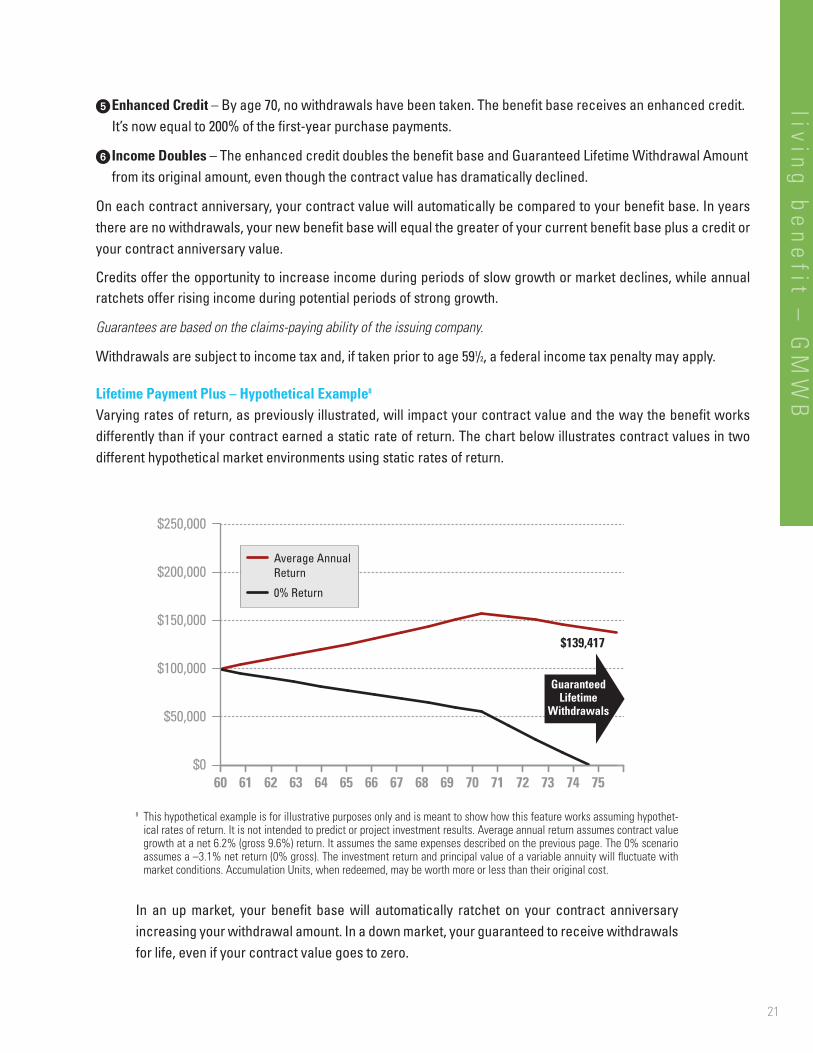

�Enhanced Credit – By age 70, no withdrawals have been taken. The benefit base receives an enhanced credit.It’s now equal to 200% of the first-year purchase payments.

� Income Doubles – The enhanced credit doubles the benefit base and Guaranteed Lifetime Withdrawal Amountfrom its original amount, even though the contract value has dramatically declined.

On each contract anniversary, your contract value will automatically be compared to your benefit base. In yearsthere are no withdrawals, your new benefit base will equal the greater of your current benefit base plus a credit oryour contract anniversary value.

Credits offer the opportunity to increase income during periods of slow growth or market declines, while annualratchets offer rising income during potential periods of strong growth.

Guarantees are based on the claims-paying ability of the issuing company.

Withdrawals are subject to income tax and, if taken prior to age 591/2, a federal income tax penalty may apply.

Lifetime Payment Plus – Hypothetical Example8

Varying rates of return, as previously illustrated, will impact your contract value and the way the benefit worksdifferently than if your contract earned a static rate of return. The chart below illustrates contract values in twodifferent hypothetical market environments using static rates of return.

8 This hypothetical example is for illustrative purposes only and is meant to show how this feature works assuming hypothet-ical rates of return. It is not intended to predict or project investment results. Average annual return assumes contract valuegrowth at a net 6.2% (gross 9.6%) return. It assumes the same expenses described on the previous page. The 0% scenarioassumes a –3.1% net return (0% gross). The investment return and principal value of a variable annuity will fluctuate withmarket conditions. Accumulation Units, when redeemed, may be worth more or less than their original cost.

In an up market, your benefit base will automatically ratchet on your contract anniversaryincreasing your withdrawal amount. In a down market, your guaranteed to receive withdrawalsfor life, even if your contract value goes to zero.

$0

$50,000

$100,000

$150,000

$200,000

$250,000

75747372717069686766656463626160

Average Annual Return

0% Return

$139,417

Guaranteed Lifetime

Withdrawals

22

Benefit Details• This benefit may only be elected at contract issue

and can be cancelled at any time. Once cancelled, it cannot be re-elected.

• Maximum election age is 80, based on theyoungest covered person.

• Age calculation criteria:

• This benefit and other living benefits cannot beelected at the same time.

• You must invest in an MML allocation fund(excluding the Aggressive Allocation Fund) orselect investment choices within the parametersof the custom allocation program offered byMassMutual, where there must be a 20%allocation to fixed income.

• Guaranteed lifetime withdrawals will be paid overthe life of the covered person named by you. Onecovered person for single life and two for joint life.

• Withdrawals for required minimum distributionsusing an automatic distribution program will notreduce the benefit base.

• Withdrawals reduce the contract value and thecontract’s death benefit.

• The maximum benefit base is $5 million.

Important Considerations• Withdrawals prior to age 60, or that exceed 5% of

the benefit base on an annual basis will reduceyour benefit base and negatively impact the valueof this feature.

• The longer you wait to take withdrawals, the morethe value of this benefit may be limited, your lifeexpectancy will be shorter.

• Each product offers a free withdrawal provisionthat allows you to withdraw a percentage of yourcontract value each year without incurring acontingent deferred sales charge. You mustweigh the additional cost of MassMutual LifetimePayment Plus against the benefit provided by thisoptional benefit.

Key TermsBenefit Base – Is equal to the contract value, adjustedfor withdrawals, additions or Annual Ratchets.

Covered Person – The person named on the contractwhose life is used to determine the duration of theGuaranteed Lifetime Withdrawal Amount.

Credit Period – A specified period of time after whichan additional credit will be applied to the GMWBBenefit Base.

Guaranteed Lifetime Withdrawal Amount – Beginningat age 60, the annual amount up to 5%, that is guaran-teed to be available for withdrawals each contractyear for life.

Guaranteed Withdrawal Amount – Prior to theGuaranteed Lifetime Withdrawal Date, the annualamount, up to 5%, that is guaranteed to be availablefor withdrawals each year while the rider is in effect.

MassMutual Lifetime Payment Plus

liv

ing

be

ne

fit

– G

MW

B

Age = 6 months prior to and after the stated age. Ex: 79 yrs., 6 mo., 1 day � Age 80 � 80 yrs., 6 mo.

23

de

ath

be

ne

fits

Death BenefitsRetirement income is important, but wealth transfer is stilla major consideration for many people. Both MassMutualEvolution and MassMutual Transitions Select variableannuity contracts come with a basic death benefit andthe ability to elect an optional death benefit. Only onedeath benefit may be elected at a time.

The Basic Death Benefit provides standard protectionfor your beneficiaries at no additional cost. If deathoccurs during a contract’s accumulation phase, bene-ficiaries will receive the greater of:

• The contract value, or

• Total purchase payments adjusted for withdrawalsand any applicable charges.

The basic death benefit is automatically provided toindividuals younger than age 76 at the time of contractissue, unless an optional death benefit is elected.

Withdrawals will reduce the death benefit proportionally,except with contracts that have the MassMutual LifetimePayment Plus feature added.

The total purchase payments on contracts issued withLifetime Payment Plus are reduced dollar-for-dollar forwithdrawals taken up to the Guaranteed WithdrawalAmount (GWA) or Guaranteed Lifetime WithdrawalAmount (GLWA). Withdrawals in excess of the GWAor GLWA reduce the total purchase payments andcontract value.

For MassMutual Evolution contract owners age 76or older at issue, the contract value is the basicdeath benefit.

MassMutual Transitions Select contract owners age76 or older at issue are not eligible for the basic deathbenefit. They can elect the Annual Ratchet DeathBenefit or the Contract Value Death Benefit.

Annual Ratchet Death Benefit Optional BenefitProvides additional investment protection for yourbeneficiaries in the event of a market downturn. You willhave the ability to lock in potential gains and transferthem to your beneficiary upon death. The death benefitwill be the greatest of:

• The contract value, or

• Total purchase payments adjusted for withdrawalsand any applicable charges, or

• The highest contract anniversary value prior toage 80, adjusted for withdrawals.

Withdrawals reduce the death benefit proportionally,except with contracts that have the MassMutualLifetime Payment Plus feature added.

The total purchase payments on contracts issued withLifetime Payment Plus are reduced dollar-for-dollar forwithdrawals taken up to the Guaranteed WithdrawalAmount (GWA) or Guaranteed Lifetime WithdrawalAmount (GLWA). Withdrawals in excess of the GWAor LWA reduce the total purchase payments andcontract value.

The Annual Ratchet Death Benefit feature is availablefor an additional cost.

Additional ChargeCurrent: 0.40%; Maximum 0.90%(Charge is deducted each business day from the assets ofthe separate account. Charge is equal on an annual basis tothe daily value of the assets invested in each fund, after fundexpenses are deducted.)

24

de

ath

be

ne

fits

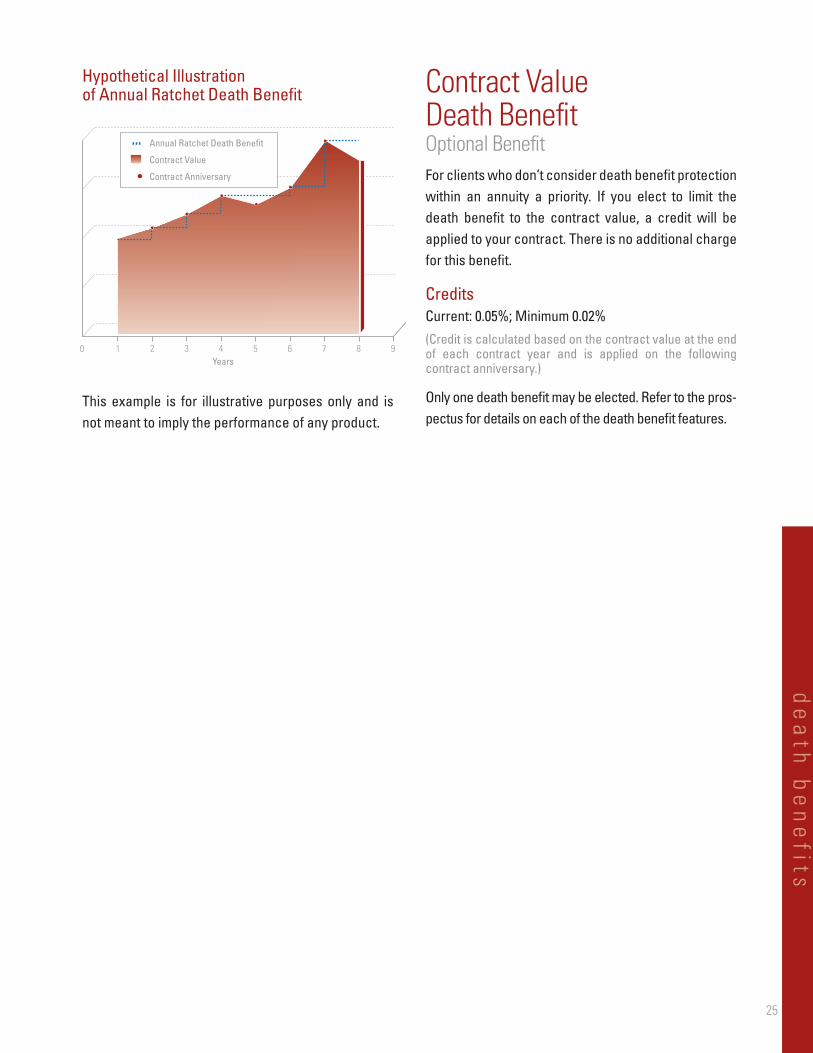

Hypothetical Illustration of Annual Ratchet Death Benefit

This example is for illustrative purposes only and isnot meant to imply the performance of any product.

Contract Value Death BenefitOptional BenefitFor clients who don’t consider death benefit protectionwithin an annuity a priority. If you elect to limit thedeath benefit to the contract value, a credit will beapplied to your contract. There is no additional chargefor this benefit.

CreditsCurrent: 0.05%; Minimum 0.02%(Credit is calculated based on the contract value at the endof each contract year and is applied on the followingcontract anniversary.)

Only one death benefit may be elected. Refer to the pros-pectus for details on each of the death benefit features.

Annual Ratchet Death Benefit

Contract Value

Contract Anniversary

de

ath

be

ne

fits

25

Massachusetts Mutual Life Insurance Companyand affiliates, Springfield, MA 01111-0001

www.massmutual.com

© 2008 Massachusetts Mutual Life Insurance Company. All rights reserved.

MassMutual Financial Group is a marketing name for Massachusetts Mutual Life Insurance Company (MassMutual)and its affiliated companies and sales representatives.

AN7600 1108RI01665 1110

MassMutual Evolution and MassMutual Transitions Select variable annuities are soldby prospectus. Before purchasing a variable annuity contract, investors should carefullyconsider the investment objectives, risks, charges and expenses of the variable annuitycontract and its underlying investment choices. For this and other information, obtainthe applicable product prospectus and the underlying investment choices prospectusfrom your registered representative. The prospectuses should be carefully consideredbefore investing or sending money.

The information provided in this brochure is not written or intended as tax or legal advice and maynot be relied on for purposes of avoiding any Federal tax penalties. MassMutual, its employees andrepresentatives are not authorized to give tax or legal advice. Individuals are encouraged to seek advicefrom their own tax or legal counsel.

Depending on the state in which you live, some benefits described within this brochure may not beavailable within the product you select. Please consult with your financial professional.

MassMutual Evolution (policy form number is TMLS, TMLS (NC) in North Carolina) is a deferredvariable annuity issued by Massachusetts Mutual Life Insurance Company, 1295 State Street,Springfield, MA 01111-0001.

MassMutual Transitions Select (policy form number is TMLS, TMLS (NC) in North Carolina) is adeferred variable annuity issued by Massachusetts Mutual Life Insurance Company, 1295 State Street,Springfield, MA 01111-0001.

Principal UnderwriterMML Distributors, LLC1295 State StreetSpringfield, MA 01111-0001

Wholly owned subsidiary ofMassachusetts Mutual Life Insurance Company1295 State StreetSpringfield, MA 01111-0001