Embed Size (px)

Citation preview

ANALYSIS OF FACTORS AFFECTING THE AUDITOR

SWITCHING ON BANKING COMPANIES

LISTED IN INDONESIA STOCK EXCHANGE

PERIOD 2008 – 2014

SKRIPSI

By

Stefhany Natalia

008201200145

Presented to

The Faculty of Business, President University

In partial fulfillment of the requirements

for

Bachelor Degree in Business, Major in Accounting

PRESIDENT UNIVERSITY

Cikarang Baru - Bekasi

Indonesia

2016

i

ANALYSIS OF FACTORS AFFECTING THE AUDITOR

SWITCHING ON BANKING COMPANIES

LISTED IN INDONESIA STOCK EXCHANGE

PERIOD 2008 – 2014

SKRIPSI

By

Stefhany Natalia

008201200145

Presented to

The Faculty of Business, President University

In partial fulfillment of the requirements

for

Bachelor Degree in Business, Major in Accounting

PRESIDENT UNIVERSITY

Cikarang Baru - Bekasi

Indonesia

2016

ii

PANEL OF EXAMINERS

APPROVAL SHEET

Herewith, the Panel of Examiners declare that the skripsi entitled “Analysis Of Factors

Affecting The Auditor Switching On Banking Companies Listed In Indonesia Stock

Exchange Period 2008 – 2014” submitted by Stefhany Natalia majoring in Accounting,

Faculty of Business was assessed and proved to have passed the Oral Examination on Thursday,

January 21th, 2016

Chair, Panel of Examiner,

Misbahul Munir, Ak., MBA., CPMA., CA

Examiner I

Drs. Gatot Imam Nugroho, Ak., MBA., CA

Examiner II Co. Examiner II

Dr. Sumarno Zain, S.E., Ak., MBA Andi Ina Yustina, M.Sc

iii

SKRIPSI ADVISER

RECOMMENDATION LETTER

This skripsi entitled “Analysis Of Factors Affecting The Auditor Switching On Banking

Companies Listed In Indonesia Stock Exchange Period 2008 – 2014” prepared and

submitted by Stefhany Natalia in partial fulfillment of the requirements for Bachelor Degree in

Business - Major in Accounting, has been reviewed and found to have satisfied the

requirements for a thesis fit to be examined. We therefore recommend this thesis for Oral

Defense.

Cikarang, Indonesia, December 17th, 2016

Acknowledge

……………………………………..

Misbahul Munir, Ak., MBA.,

CPMA., CA

Head, Accounting Study Program

Skripsi Adviser,

……………………………………

Drs. Gatot Imam Nugroho, Ak.,

MBA., CA

iv

DECLARATION OF ORIGINALITY

This skripsi entitled “Analysis Of Factors Affecting The Auditor Switching On Banking

Companies Listed In Indonesia Stock Exchange Period 2008 – 2014” prepared and

submitted by Stefhany Natalia in partial fulfillment of the requirements for Bachelor Degree in

Business Major in Accounting has been reviewed and found to have satisfied the requirements

for a thesis fit to be examined. I therefore recommend this thesis for Oral Defense.

Cikarang, Indonesia, December 17th, 2016

Researcher,

Stefhany Natalia

008201200145

v

ANALYSIS OF FACTORS AFFECTING THE AUDITOR SWITCHING ON

BANKING COMPANIES LISTED IN INDONESIA STOCK EXCHANGE

PERIOD 2008 – 2014

ABSTRACT

Auditor switching is a process of public accountant firm replacement done by

the company. There are two types of auditor switching in Indonesia: voluntarily and

obligatory. Voluntarily auditor switching has brought a suspicion for stakeholder. This

research is proposed to discover the influence of auditor opinion, public accountant

firm size, management changes, and financial distress towards auditor switching in

banking companies since manufacturing companies research are many to find.

Population conducted in this research is banking companies that are

respectively listed in Indonesia Stock Exchange during 2008 – 2014. Sampling method

performed is purposive sampling where criteria are set as a benchmark of sample

compatibility which resulting in 28 banking companies. This research is exercising

secondary data and documentation technique. The data is analyzed by using descriptive

statistic and logistic regression as research method with α 0.05. Independent variables

in this research are Auditor Opinion, Public Accountant Firm Size, Management

Changes, and Financial Distress while the dependent variable is Auditor Switching.

The result of this research exhibits: auditor opinion, public accountant firm size,

management changes, and financial distress are simultaneously influencing auditor

switching. In hypothesis test, public accountant firm size hypothesis is supported with a

significant value 0.005 which is lower than α while the other variables are not. For

future researcher, the addition of some variables to attest might be proper. Moreover,

the computation of financial distress shall be attested by another method and model.

Keywords: Auditor Switching, Auditor Opinion, Public Accountant Firm Size,

Management Changes, and Financial Distress

vi

ACKNOWLEDGEMENT

Somebody once told me, “Love means giving no matter what it takes even when

you have nothing to get. Keep loving, sincerely, and whole-heartedly like it was the last

breath you can breathe.” These, are the people that hardly loving me with their best

way while whether I could repay or I even do not have a chance to. These, are the

people I am worth loving for. The one(s) who is always stand by me, giving their

shoulder for me to cry on, offering their ears to listen all my loves and grieves

obligingly, telling me impassioned words of wisdom and reminding me always that

when I can’t, He, My Jesus, is always can.

1. Papa and mama, I thank you for your understanding and support for all

things that I am doing, especially this skripsi. Thank you for waking up

every single morning and cooking me food, mam. Your ayam jahe will be

the one that I am looking for when I go to work, soon. Pap, thank you for

driving me over all places I need to go for job interview and this skripsi

thingy. No, you are not driver. You are my Superman and you will always

be.

2. Cayun and Adys, you girls are the best sister ever lived in the world and I

am grateful having you both. There is no even a person who wants to hear

my stories like you do, Cayun. Adys, thank you for being such a funny and

witty 8 years old sister and hearing my skripsi-tales. The one who always

hug me every single time I am coming home and kiss me all over my face. I

love you!

3. Mr. Misbahul Munir, MBA., Ak., CPMA as Dean of Faculty of Business

President University.

4. Mr. Gatot Imam Nugroho, AK., MBA., CA, my skripsi adviser. Thank you

sir for you time and patience encouraging me to have this skripsi finished.

5. Mr. Dr. Josep Ginting. You gave lots of food of thoughts and advices for this

skripsi. Thank you sir.

6. Mam Ina, the most friendly lecturer I have ever had and the one I came to

when I was in the middle of skripsi confusion. You are my journal helper. I

owe you a pan of pizza, mam!

7. Mr. Dr. Sumarno Zain, SE. Ak., MBA. Thank you sir for your kindness

helping me developing this skirpsi.

vii

8. My Jesus’ Bride. These girls are such a gift for me. Thank you for always

there supporting and encouraging your mom in doing this skripsi. I am proud

having you, girls.

9. Jesus’ Dizciple! I owe you lots of thank-you(s). A “father”, a best-friend(s),

a helper, the one who always I can cling to, a family who knows how hard I

am struggling. Thank you.

10. Epin, Hana, Monic, my Core Team forevermore.

11. God’s DNA Jababeka, even in the middle of this hectic skripsi-deadline you

guys are always here, head and heart.

12. Jesslin Putri, a roommate and a bestie. The craziest and finest girl I have

ever found in this universe.

13. Dian and Cecil, thank you for being a good sleepover-girl and study-mate

for these 8 semesters!

14. All accounting squads of President University, these 10 semesters

mesmerize me.

15. For all examiners, I will never pass Bachelor Degree without you.

I consciously realize that this skripsi is far from perfection and I would never

have it done with all those people I mentioned and do not able to mention one by one

above. I have a big hope that this research could become a useful matter for future

users.

Cikarang, Dec 16th 2015

Stefhany Natalia

viii

TABLE OF CONTENTS

PANEL OF EXAMINERS APPROVAL SHEET ................................................................. ii

RECOMMENDATION LETTER OF SKRIPSI ADVISER ............................................... iii

DECLARATION OF ORIGINALITY ................................................................................. iv

ABSTRACT ............................................................................................................................v

ACKNOWLEDGEMENT .................................................................................................... vi

TABLE OF CONTENTS .................................................................................................... viii

LIST OF TABLES ..................................................................................................................x

LIST OF FIGURES .............................................................................................................. xi

LIST OF APPENDICES ...................................................................................................... xii

CHAPTER 1 - INTRODUCTION ..........................................................................................1

1.1 Research Background ......................................................................................................1

1.2 Problem Statement ..........................................................................................................5

1.3 Research Objectives ........................................................................................................5

1.4 Research Benefits ............................................................................................................5

CHAPTER II – LITERATURE REVIEW.............................................................................7

2.1 Theoretical Review..........................................................................................................7

2.1.1 Agency Theory .........................................................................................................7

2.1.2 Auditor Switching ....................................................................................................8

2.1.3 Government Rule (Auditor Switching) ......................................................................9

2.1.4 Bank ....................................................................................................................... 10

2.1.5 Auditor Opinion ..................................................................................................... 11

2.1.6 Management Changes ............................................................................................. 13

2.1.7 Financial Distress ................................................................................................... 14

2.1.8 Hypothesis.............................................................................................................. 14

CHAPTER III – RESEARCH METHOD............................................................................ 19

3.1 Population and Sampling ............................................................................................... 19

3.2 Population and Sampling Design ................................................................................... 19

3.3 Research Variable and Operational Definitions Variable ................................................ 21

3.3.1 Dependent Variable ................................................................................................ 21

3.3.2 Independent Variable .............................................................................................. 22

3.4 Research Instrument ...................................................................................................... 24

3.5 Data Collection Procedures............................................................................................ 24

3.6 Data Analysis ................................................................................................................ 25

3.6.1 Descriptive Statistic ................................................................................................ 26

ix

3.6.2 Inferential Statistic Analysis ................................................................................... 28

3.6.3 Hypothesis Test ...................................................................................................... 29

CHAPTER IV – DATA ANALYSIS AND EVALUATION ................................................ 33

4.1 Research Object Description ..................................................................................... 33

4.2 Research Variable Description .................................................................................. 33

4.3 Descriptive Statistic .................................................................................................. 33

4.4 Preliminary Logistic Regression Test (Multicolinearity) ........................................... 36

4.4.1 Logistic Regression Model Test ............................................................................. 37

4.4.2 Overall Model Fit Test ........................................................................................... 38

4.4.3 Hypothesis Test ..................................................................................................... 40

4.4.4 Simultaneous Testing ............................................................................................. 41

4.4.5 Partially Testing .................................................................................................... 41

CHAPTER V – CONCLUSIONS AND RECOMMENDATIONS ..................................... 46

5.1 Conclusions ................................................................................................................... 46

5.2 Limitations .................................................................................................................... 48

5.3 Recommendations ......................................................................................................... 48

REFERENCES .......................................................................................................................

APPENDIX .............................................................................................................................

x

LIST OF TABLES Table 3.2.1 - Sample selection sample based on criteria .................................... 20

Table 3.2.2 - List of sample .............................................................................. 21

Table 3.6.1.1 - Auditor Switching observed from Auditor Opinion ................... 27

Table 3.6.1.2 - Auditor Switching observed from PAF size ............................... 27

Table 3.6.1.3 - Auditor Switching observed from Management Changes........... 27

Table 3.6.1.4 - Auditor Switching observed from Financial Distress ................. 28

Table 4.3.1 - Data Descriptive Variable – Auditor Switcing .............................. 34

Table 4.3.2 - Data Descriptive Variable – Auditor Opinion ............................... 34

Table 4.3.3 - Data Descriptive Variable – Public Accountant Firm Size ............ 35

Table 4.3.4 - Data Descriptive Variable – Management Changes ...................... 35

Table 4.3.5 - Data Descriptive Variable – Financial Distress ............................. 36

Table 4.4 - Multicolinearity Testing Result ....................................................... 37

Table 4.4.1 – Hosmer and Lemeshow Test ........................................................ 38

Table 4.4.2 – Overall Model Fit Test ................................................................ 39

Table 4.4.3 – Nagelkerke R Square value on Logistic Regression Analysis ....... 40

Table 4.4.4 – Simultaneous Testing Result on Regression Analysis .................. 41

Table 4.4.5 – Partially Testing on Logistic Regression Analysis ....................... 42

xi

LIST OF FIGURES

Figure 2.1.8.4 – Research Model....................................................................... 18

xii

LIST OF APPENDICES

Appendix 1 - List of banking companies listed in IDX year 2008 ................................. A

Appendix 2 - List of banking companies listed in IDX year 2009 ..................................B

Appendix 3 - List of banking companies listed in IDX year 2010 ..................................C

Appendix 4 - List of banking companies listed in IDX year 2011 ................................. D

Appendix 5 - List of banking companies listed in IDX year 2012 .................................. E

Appendix 6 - List of banking companies listed in IDX year 2013 .................................. F

Appendix 7 - List of banking companies listed in IDX year 2014 ................................. G

Appendix 8 – Inadequate data bank list .......................................................................... I

Appendix 9 – Sample list of bank .................................................................................. J

Appendix 10 - List of public accountant firm used ..........................................................

Appendix 11 – Financial distress computation ................................................................

1

CHAPTER I

INTRODUCTION

I.1 Research Background

In this era, the level of Indonesian companies’ need toward public accountant

services is quite high. Generally, companies that need public accountant’ services

are the ones who need their service to audit financial statements and give opinion

for their specified purposes. Financial statements are prepared by public

accountants to help stakeholders understand the financial history of the company

and use that knowledge to predict the amount, timing and uncertainty of both future

cash flows and price appreciation of the company (Mautz & Angell, 2006).

Lybrand in Webster (1986) stated that a public accountant is one engaged

professionally in the practice of accountancy; the term accountancy being

understood to cover all forms of investigations of accounts for the determination of

financial conditions, detections of frauds or prevention thereof, or whatever

purpose data obtained from the accounts may be required. Public accountant holds

the engagement with their clients to examine and report on the financial statements

which is based on the arrangement. They undertake to perform their examination in

accordance with GAAS (Generally Accepted Auditing Standards) and to report to

the shareholders and directors as to whether or not, in their opinion, the financial

statement presented fairly (Hanson, 1967). Concerning to that fact, public

accountant can be regarded as an independent party which bridging personal

interests between principals and agents as the manager of enterprises. To perform

the best practice of their job, public accountant is required to produce audit opinion

with finest quality, which is useful not only for business purposes but also public

prominence (Wibowo & Hilda, 2009). Therefore, they are required to

2

independently perform their service without emphasizing on specific party’s

interest. In this phase, independence is highly needed to be owned by a public

accountant.

After the passage of Enron and Arthur Andersen case, Sarbanas-Oxley Act is

formed since the perception of independence has become a significant factor that

influencing auditor's opinion (Smith & Minter, 2005). The auditor should be

independence in two forms: appearance and fact (Irmawan et al., 2013). Once they

do not fulfill the criteria, they could not be categorized as independent (SPAP

(Standar Profesional Akuntan Publik) 2011). Independence is one of the main keys

to become a professional public accountant. The manner of independence builds

public accountants’ character to become insusceptible (SPAP (Standar Profesional

Akuntan Publik) 2011. Therefore, the opinion given by the auditor will be

accountable and credible since all the findings reported are authentic.

In this term, the independence of auditors will lead to the fairness of financial

statement presented by the auditor. To execute their best services, public accountant

has to have ability to produce certain qualities of audit opinion that is useful for

financial statement user which is investors, creditors, and the public (Wibowo &

Hilda, 2009).

Concerning to the discussion above, the issue of auditor’s independence is

becoming one of the most well-known issues among public accountant and the

public. The “auditor switching” phenomenon has been found to have implications

for the credibility of financial reporting and the cost to monitor management

activities (Huson et al. in Nazri et al., 2012). Since 1970s, accounting professionals

and industry experts have extensively studied the massive number of auditor

switching in developed countries. However, there are few studies have been

3

conducted in Indonesia to examine the significant reasons for auditor switching

(Nazri et al., 2012)

Based on the Indonesia Ministry of Finance’s act concerning to “Jasa Akuntan

Publik” (Public Accountant Services) in Article 2 as an amendment of the Ministry

of Finance’s act No. 432/KMK/06/2002, Indonesia is stated as one of some

countries that enforces the execution of mandatory auditor switching to maintain

auditor’s independence. This act thrashes out general audit services on financial

shall be conducted by a public accountant firm for the longest 5 (five) years

accounting period respectively and by a public accountant for the longest 3 (three)

year accounting period. It is enhanced with the issuance of Indonesia Minister of

Finance act No. 17/PMK.01/2008 with some modification of the period of service

provision of a public accountant firm which is 6 (six) years respectively (Article 3,

Paragraph 1).

Furthermore, public accountant and public accountant firm are permitted to give

general audit service for the same clients at least 1 (one) fiscal year after the last

moment they executed the service (Article 3, Paragraph 2 and 3). Before the

passage of SOX, companies did auditor switching to obtain a fresh opinion that will

be stated in their financial statement. In 2002, companies were doing auditor

switching in order to evade and anticipate bad news in going-concern issue. After

the demise of Andersen, a bunch of former Andersen’s clients that were more

visible in the capital markets switched auditor to mostly Big 4 firms and

experienced a more positive reaction as a result (Brazel & Bradford, 2011). In

consequence of this case, a bunch of ex-Andersen clients released more

conservative financial statements after they switched to a new public accountant

firm. The condition in 20th centuries is not much different from the passage before

SOX.

4

Concerning to the 20th centuries fact, there are a bunch of reasons of why

companies are doing auditor switching. Some of the researchers have done their

research about auditor switching and they used some related variables: audit fees,

management changes, public accountant firm’s size, client’s firm size, audit

opinion, financial distress, the image of a public accountant, distance between

public accounting firm and the client, client satisfaction, relationship, ROA, and

etc. After considering and reviewing some of former research, most of them are

using manufacturing companies as their research object. In this research, the writer

executes the research by using banking companies listed in Indonesian Stock

Exchange for the period 2008 - 2014 as research object.

As far as the researcher concerns, bank has unique values that other business

scopes do not have. All earnings earned by another business entity are saved in

bank. Moreover, banking companies have various products offered compared to

other non-financial companies. In addition, the main activities of the bank beside

channeling funds is also raising funds while other financial institutions geared more

towards channeling funds alone. Loan is the biggest product a bank is able to offer

to their customer while another business entities do not serve it.

Referring to the complexity of bank’s business process, in this research, the

writer will conduct the research on auditor switching by using management

changes, public accounting firm’s size, auditor’s opinion, and financial distress by

using banking companies as the object of research. Based on the discussion written

above, the most proper title of this research would be “Analysis Of Factors

Affecting The Auditor Switching On Banking Companies Listed In Indonesia

Stock Exchange Period 2008 – 2014”.

5

I.2 Problem Statement

The writer has intention to find out and discover the influence of the factors

affecting the execution of auditor switching by using auditor opinion, public

accounting firm’s size, management changes, and financial distress of banking

companies listed in Indonesia Stock Exchange for the period 2008 - 2014. Based on

some arguments mentioned above, here are some matters that will be evaluated in

this research:

1. How is the influence of auditor's opinion on auditor switching done by bank

listed in IDX for the period 2008 - 2014?

2. How is the influence of public accountant firm’s size on auditor switching

done by bank listed in IDX for the period 2008 - 2014?

3. How is the influence of management changes on auditor switching done by

bank listed in IDX for the period 2008 - 2014?

4. How is the influence of financial distress on auditor switching done by bank

listed in IDX for the period 2008 - 2014?

I.3 Research Objectives

The objective of this research is generally to identify the influence of auditor’s

opinion, public accountant’s firm size, management changes, and financial distress

on auditor switching done by the bank listed in Indonesia Stock Exchange for the

period 2008 - 2014. Moreover, it is proposed to prove the hypothesis presumed by

the writers.

I.4 Research Benefits

This research is made to identify the influence of auditor’s opinion, public

accountant’s firm size, management changes, and financial distress on auditor

6

switching done by the public companies listed in Indonesia Stock Exchange for the

period 2008 - 2014.

1. For business and corporate practitioner literature, it helps them as a

reference in auditor switching determination by measuring the cost and

benefit using auditor opinion, public accountant’s firm size, management

changes, and financial distress in banking companies.

2. For students, this research is intended to give a deeper knowledge regarding

the influence of auditors opinion, public accountant’s firm size,

management changes, and financial distress on auditor switching done by

public banking companies and as a reference to make next research.

3. For stakeholders, the information provided in this research is intended to

help them in analyzing the effect of auditors opinion, public accountant’s

firm size, management changes, and financial distress on auditor switching

done by banking companies listed in Indonesia Stock Exchange for period

2008 – 2014.

7

CHAPTER II

LITERATURE REVIEW

II.1 Theoretical Review

This chapter is made to expand all theories that relate to this research. The

theories are derived from journal articles and books. This is intended to enlighten and

makes the research clearer.

II.1.1 Agency Theory

Agency theory has attracted a big space of financial accounting researcher since

this theory has caused the agency conflict between principal and agent. The agency

conflict is issued by personal conflict between principal and agent since their

purposes are not in tune. The manager who takes a role as an agent carries out a

moral responsibility to optimize the benefit of the principal. However, on different

sides manager also has the aim to maximize his welfare and interests. Therefore,

there is a concern possibility that agents do not always act on the principal’s best

interest (Jensen and Meckling, 1976). As a party who immediately manage and

handling the company, agent has internal information about the company's prospects

in the future more than the principal has. Thus, the agent has a necessity to give

signs or signals about company's condition to the principal. The financial report is

one form of signs or signals that can be given by the manager as the disclosure of

accounting information that describes the company's performance.

Jensen and Meckling (1976) described that problems may arise when

information received by interested parties are not the same as the actual condition of

the company. This situation is known as an information asymmetry (asymmetric

information) or information that is not symmetrical. Information asymmetry occurs

8

because the agent is superior in knowing and understanding the information

compared to another parties (principal and stakeholders). Principal wants a rapid

and high return as much as possible on investment while the agent has a goal to

open the door of opportunities then they could receive a profuse amount of bonuses

and incentives.

Agency theory also states that every human being will take action in accordance

with their interests. Putting personal interest on top will also give rise to agency

costs. Therefore, the auditor, which is an independent party that adhered to the

auditing standards established by the official institutions and which comply with the

code of professional conduct acts to reduce and prevent the agency costs. The

agency cost that will arise are various depend on the variables existed. Dopuch and

Simunic (1982) in Nasser and Wahid (2006) suggested that in the economy

knowledge the election of trusted and reputable public accountant firm is used as a

signal of management honesty. In addition, Watts and Zimmerman (1986) in Nasser

and Wahid (2006) states that the wider the complexity of company's operations, a

trustworthy public accountant firm with high level of independence is required to be

hired due to reducing the agency cost.

II.1.2 Auditor Switching

Auditor switching is a displacement of auditor (public accountant firm)

conducted by the client. The theoretical evidence was based on agency theory and

economic information. In both cases, demand for audit services arose mainly from

the existence of information asymmetry. In agency theory, an independent audit

function is to reduce agency costs arising from the self-interested behavior by the

agent. In the information economy, the election of trustworthy auditor is used as a

signal of management honesty (Dopuch and Simunic in Nasser et al., 2006).

9

Two approaches that can be used to explain why company does auditor

switching are the auditor-initiated and client-initiated (Nazri, 2012). Auditor

switching could be done mandatory and voluntarily. Mandatory auditor switching

could be distinguished on the basis of which party is the focus of attention from the

issue. If the change of auditor occurs voluntarily, then the main concern is on the

client side. Conversely, if the change occurs on a mandatory basis, the main concern

shifted to the auditor.

II.1.3 Government Rule (Auditor Switching)

In order to maintain independency of auditor, the government of Indonesia has

set the rule of mandatory auditor switching which is stated on Minister of Finance

act. Based on Minister of Finance act no. 359/KMK.06/2003 article 2 concerning to

Public Accountant Services (as the amendment of act no. 423/KMK.06/2002 article

6 paragraph 4), it mentioned:

“Pemberian jasa audit umum atas laporan keuangan dari suatu entitas dapat

dilakukan oleh KAP paling lama untuk 5 (lima) tahun buku berturut-turut dan oleh

seorang Akuntan Publik paling lama untuk 3 (tiga) tahun buku berturut-turut.”

(The execution of general audit service on financial statement from one entity can

be done by public accountant firm for the longest 5 (five) year book respectively

and by a public accountant for the longest 3 (three) year book respectively.)

In 2003, the 2002’s act has been amendment. The act about auditor switching

and public accountant firm switching which is stated that general audit on financial

statement still can be done by public accountant firm for maximum has reach 5

(five) year book or 3 (three) year book respectively was until 2003. In 2008,

Minister of Finance reissued the act concerning public accountant service. These are

the changes that have been done:

10

1. The execution of general audit on financial statement from an entity can be

done by public accountant firm for the longest 6 (six) year book

respectively, and by public accountant for the longest 3 (three) year book

respectively (Article 3 paragraph 1).

2. Public accountant and public accountant firm can reinstate the assignation

after 1 (one) year book not giving the service to the same client (Article 3

paragraph 2 and 3).

This act is summarized in Indonesia Minister of Finance’s act no

17/PMK.01/2008 about “Jasa Akuntan Publik” (Public Accountant Service) is a

base used in the research because the period that is used was 2008 – 2012.

II.1.4 Bank

Based on Undang-Undang Republik Indonesia no. 10 year 1998, Bank is an

enterprise that collects public funds in form of saving and channeling them to the

public in form of credit and or another forms due to the elevation of standard living

of people. Like in most cases, banking companies are also issuing financial

statement. In PSAK 31 issued by IAI (Ikatan Akuntan Indonesia), the content of

bank financial statements are:

1. Statement of Financial Position (Balance Sheet)

It contains list of assets, liabilities, and equity of the bank provided with the

amount of each explanation.

2. Statement of Income (Income Statement)

It serves in detail the income and expenses information and the source of

them: operational or non-operational sources.

11

3. Cash Flow statement

It defines the flow of banking companies’ cash following those categorized:

operating, investing, and financing.

4. Statement of Changes in Equity

It presents the increasing and decreasing of bank equity in certain period

completed with the amount.

5. Notes to Financial Statement

This part is the elaboration of all those statements and it defines all

information needed to be disclosed within certain period of financial

statement.

Those explanations served the need of information that is required to be

provided in this research: auditor opinion, organization structure, name of CEO,

name of Public Accountant firm, and company’s financial information.

II.1.5 Auditor Opinion

Based on William C. Boynton in Modern Auditing 8th Edition (Assurance

Services & The Integrity of Financial Reporting), there are four types of audit

opinions:

1. Unqualified

Often called a clean opinion, an unqualified opinion is an audit report that is

issued when an auditor determines that each of the financial records is free

of any misrepresentations. In addition, an unqualified opinion indicates that

the financial records have been maintained in accordance with the standards

known as Generally Accepted Accounting Principles (GAAP). This is the

best type of report a business can receive.

12

2. Unqualified with explanatory paragraph

This kind of opinion will be issued while there is a lack of consistent

application of GAAP and substantial doubt about going concern. Moreover,

auditor agreement concerning to the departure from a promulgated

accounting principle also recognized as the cause of this opinion issuance.

3. Qualified

In situations when a company’s financial records have not been maintained

in accordance with GAAP but no misrepresentations are identified, an

auditor will issue a qualified opinion. The writing of a qualified opinion is

extremely similar to that of an unqualified opinion. A qualified opinion,

however, will include an additional paragraph that highlights the reason why

the audit report is not unqualified.

4. Disclaimer

On some occasions, an auditor is unable to complete an accurate audit report

since there is a scope limitations in data provided. This may occur for a

variety of reasons, such as an absence of appropriate financial records. When

this happens, the auditor issues a disclaimer of opinion, stating that an

opinion of the firm’s financial status could not be determined.

5. Adverse

The worst type of financial report that can be issued to a business is an

adverse opinion. This indicates that the firm’s financial records do not

conform to GAAP. In addition, the financial records provided by the

company have been grossly misrepresented. Although this may occur by

error, it is often an indication of fraud. When this type of report is issued, a

company must correct its financial statement and have it re-audited, as

investors, lenders, and other requesting parties will generally not accept it.

13

A significant issue in relation to auditor change is the qualification of the audit

opinion, especially where one of management’s goals in an audit is to receive an

unqualified audit opinion from the auditors (Hendrickson and Espahbodi, 1991).

Managers might seek a new auditor when they perceive that their reputation is being

tarnished. The receipt of an audit opinion other than unqualified is widely

recognized as being one of the factors that might damage a manager’s reputation

(William, 1988).

While a company receives opinions other than unqualified, it also perceived to

have a negative effect on companies’ share price (Chow and Rice, 1982), and can

affect a company’s ability to source new financing (Schwartz and Menon, 1985).

Concerning to that argument, in this research the researcher will divide the opinion

classification into two parts: Unqualified and other than unqualified.

II.1.6 Management Changes

Changes in management are perceived to have a significant impact on auditor

change. Mostly, new management may be dissatisfied with the quality (and cost) of

the previous auditor and demand auditor change. In addition, new management

tends to look for new auditors who agree with new reporting methods which show

more favorable financial results. As a result, new management may change to a new

auditor with whom they had some previous association (Nazri et al., 2012). Agency

theory views the relationship between auditor and client to be a nexus of contracts

and a change in the principal-agent contract, as a result of the appointment of a new

manager (agent), may precipitate a change in auditor (Williams, 1988). An

incumbent auditor may be dismissed as he or she is viewed as being closely

associated with the former management. The new management could also request

14

an auditor change because they would like to bring in an auditor with whom they

are familiar.

Based on previous studies, changes in management consist of changes in the

management team such as the change of the chairman of board of directors,

financial controller, managing director and the chairman of audit committee. Based

on the previous research of Beattie and Fearnley (1998), they provide further

evidence in relation to management change with a report that indicates 35 percent of

auditor change companies cited top management changes as a reason for the change.

II.1.7 Financial Distress

Financial distress refers to a period when a borrower (either individual or

institutional) is unable to meet a payment obligation to lenders and other creditors.

This distress may be due to borrower specific factors like reputation, leverage,

volatility of earnings, collateral or may be due to market specific factors like the

economic condition and level of interest rates (Zaki et al., 2011). In a simple way,

financial distress is the condition while a company faces financial difficulties.

Financial distress significantly influences the decision of auditor switching

(Schwartz dan Menon, 1985). While companies do not meet ability to finance their

businesses, their going concern is value is threatened. Schwartz and Soo (1995) in

Kadek (2010) stated that a liquidated company tends to do change public accountant

firm frequently rather than a favorable company.

II.1.8 Hypothesis

II.1.8.1 The influence of Auditor Opinion on Auditor Switching

Prior research on the relationship between audit reports and auditor

change has focused on the effect of the auditors’ reports on the decision to

15

switch auditors. Roberts et al. (1990), Chow and Rice (1982) and Johnson

and Lys (1990) report that unfavorable audit reports may increase the

likelihood of an auditor change. Chow and Rice’s (1982) finding, however,

indicates that firms that change auditor after receiving a qualified opinion do

not tend to move to auditors that issue relatively fewer qualified opinions.

A Singapore study conducted by Woo and Koh (2001) found

unfavorable opinions may actually trigger auditor change which could be

traced to causes where the qualification arose due to some matter of

fundamental importance. A study conducted by Krishnan et al. (1996) also

found evidence that audit opinion influences auditor change. This study

therefore posits the following relationship between opinion other than

unqualified and auditor change:

H1: If the changes of auditor opinion influences auditor switching,

auditor opinion is positively affecting auditor switching.

II.1.8.2 The influence of Public Accountant Firm size on Auditor Switching

After the demise of Arthur Andersen, however, many former Andersen

clients that were more visible in the capital markets switched auditors sooner

mostly to Big 4 firms and experienced a more positive market reaction as a

result (Brazel and Bradford, 2011). Attestation by credible auditors may

serve the honesty signal of management since they entrust their reputation

while Non Big 4 public accountant firms are mostly not (Nasser and Wahid,

2006). Moreover, Big 4 public accountant firm is known as a reliable team

to entrust their reputation in public. In consequence of that, they have

smaller intention to execute indiscriminate audit service. In the light of the

discussion, the following hypothesis is suggested:

16

H2: If most of Big 4 clients do not move Non Big 4, public accountant

firm size is negatively influencing auditor switching.

II.1.8.3 The influence of Management Changes on Auditor Switching

As a result of change in management, new management could demand

the replacement of the incumbent auditor with a new one with whom it has

had favorable dealings in the past (Hudaib and Cooke, 2005;Williams,

1988). Empirically, Woo and Koh (2001) did not find an association

between management change and higher quality auditor selection while

Schwartz and Menon (1985) found evidence that a change in managing

director leads to switching because new management attempts to

disassociate itself from previous relationships and prefers to deal with

familiar parties. Beattie and Fearnley (1998) provide further evidence in

relation to management change. They report that 35 percent of auditor

change companies cited top management changes as a reason for the change.

In addition, Hudaib and Cooke (2005) found evidence of a positive

association between management change and the propensity to change

auditor. In Singapore, Woo and Koh (2001) indicate that management

changes are one of the main reasons for a company to change auditor. Woo

and Koh (2001) also found that director change is associated with a higher

probability of auditor change while Chow and Rice (1982), Schwartz and

Menon (1985), and Williams (1988) reported any such association.

The signaling hypothesis argues that the choice of auditor is a means by

which managers may impart to the market additional information about the

company, as well as their own behavior. This suggests that a new manager

may signal to stakeholders that companies’ management is being well

17

monitored by choosing a higher quality auditor as a replacement. However,

there is also the possibility that the new manager may bring in a lower

quality auditor, with whom he is more familiar. Given that this action might

trigger stakeholders to question the auditor’s quality and consequently the

manager’s motive, the new manager may be reluctant to choose this option.

In the light of the discussion, the following hypothesis is suggested:

H3: If management changes affect auditor switching, management

changes (CEO) is positively associated with auditor change.

II.1.8.4 The influence of Financial Distress on Auditor Switching

Schwartz and Menon, 1985 and Hudaib and Cooke, 2005 stated in their

research that a company which faces high level of financial distress tends to

change their public accountant firm compared to another healthful

companies. Auditor switching is also possible to be done while a company

does not meet ability to settle fee audit since they experience decreasing in

financial abilities. In consequence of that, company will attempt to change

their public accountant firm.

Concerning to the discussion above, the researcher concludes:

H4: Financial distress is significantly affecting auditor switching

18

Table 2.1.8.4 Research Model

Independent Variables Dependent Variables

Auditor Opinion

Public

Accountant Firm

size

Management

Changes

Financial Distress

Auditor

Switching

19

CHAPTER III

RESEARCH METHOD

III.1 Population and Sampling

Secondary data in this research is provided by Indonesia Stock Exchange website

(www.idx.co.id) and other related sources. Type of secondary data which is accessed by

the researcher is audited financial statement of banking companies listed in Indonesia

Stock Exchange. There are 28 banking companies with 7 period of year (2008-2014)

chosen as the sample of this research. The data is processed by using the Statistical

Package for Social Science (SPSS) 16.0 for Windows.

III.2 Population and Sampling Design

Population is a generalization area consisting of the object or subject that has

certain qualities and characteristics which determined by the investigators to be

studied as a tool of conclusion drawing. The population of this research is banking

companies listed in Indonesia Stock Exchange for the period 2008 – 2014. Sample

is part of the number and characteristic possessed by the population. Sampling

technique of this research is purposive sampling method (judgment sampling). This

sampling method aims are based on particular considerations by selecting the

sample that is conform to certain criteria set by the researcher. The required criteria

used for this research are as follows:

1. Banking companies that are respectively listed in Indonesia Stock Exchange

(IDX) during 2008 – 2014.

2. Banking companies that provide complete and sufficient data of the

information of the execution of auditor switching during the research period

2008 - 2014.

20

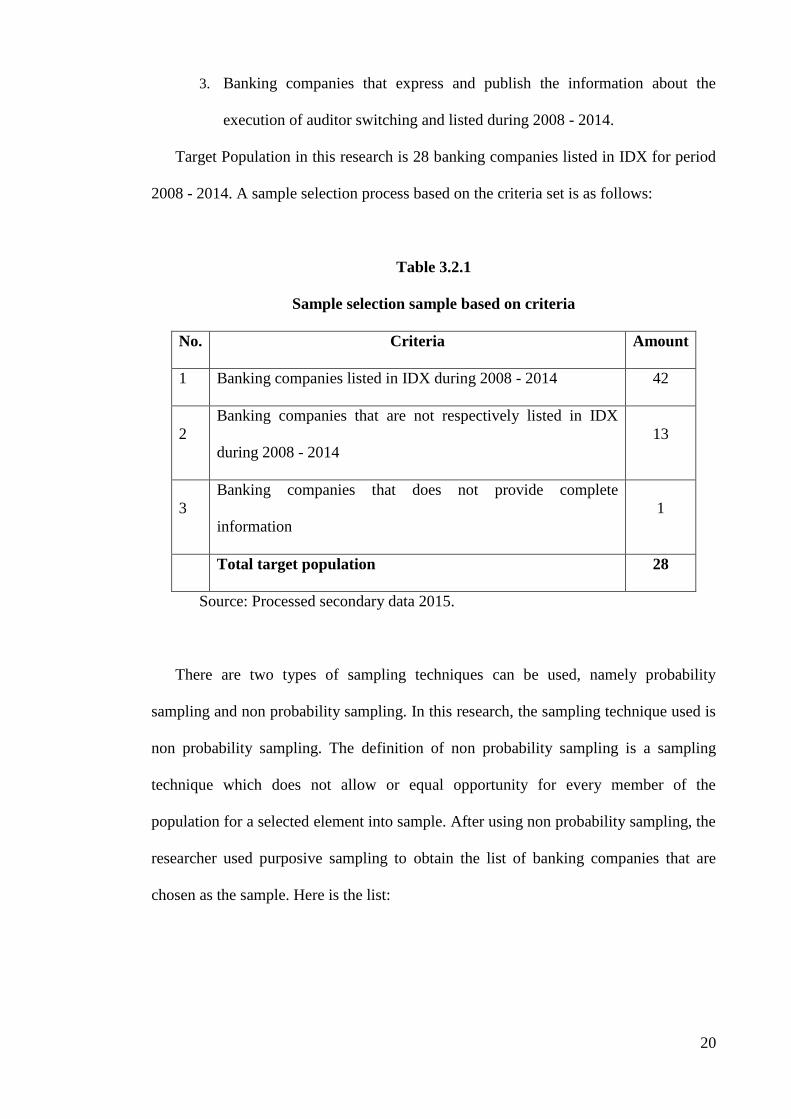

3. Banking companies that express and publish the information about the

execution of auditor switching and listed during 2008 - 2014.

Target Population in this research is 28 banking companies listed in IDX for period

2008 - 2014. A sample selection process based on the criteria set is as follows:

Table 3.2.1

Sample selection sample based on criteria

No. Criteria Amount

1 Banking companies listed in IDX during 2008 - 2014 42

2

Banking companies that are not respectively listed in IDX

during 2008 - 2014

13

3

Banking companies that does not provide complete

information

1

Total target population 28

Source: Processed secondary data 2015.

There are two types of sampling techniques can be used, namely probability

sampling and non probability sampling. In this research, the sampling technique used is

non probability sampling. The definition of non probability sampling is a sampling

technique which does not allow or equal opportunity for every member of the

population for a selected element into sample. After using non probability sampling, the

researcher used purposive sampling to obtain the list of banking companies that are

chosen as the sample. Here is the list:

21

Table 3.2.2

List of Sample

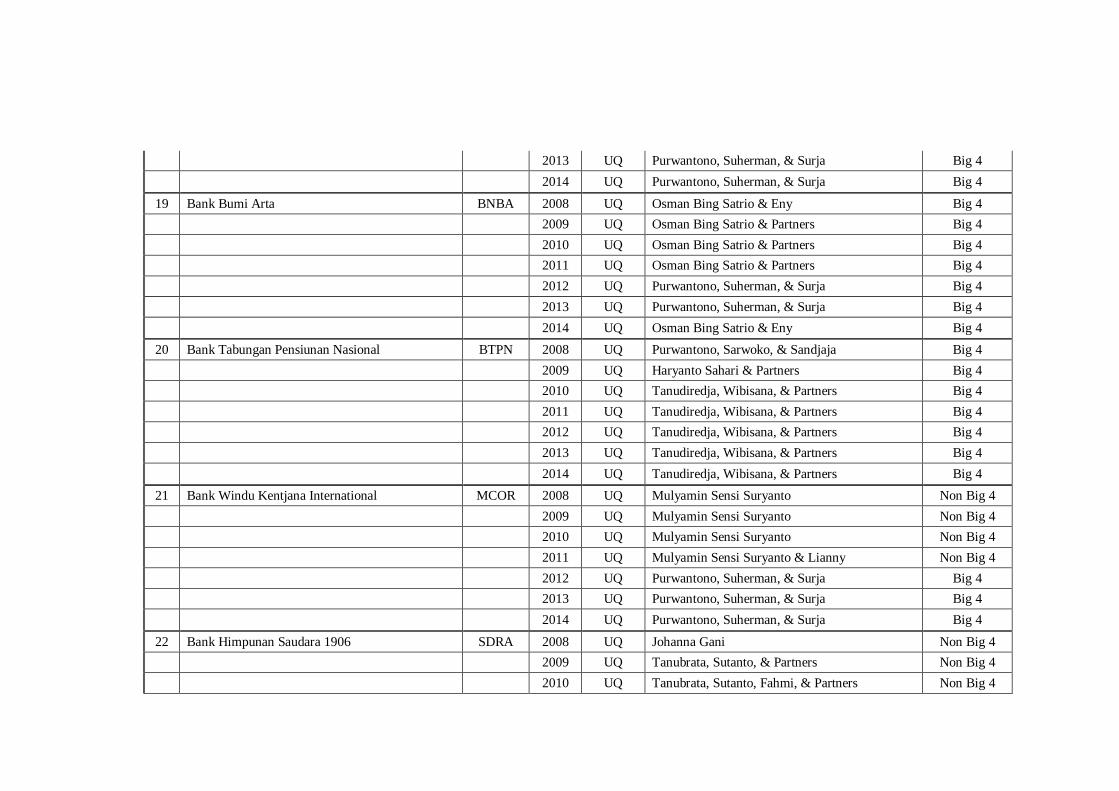

No. Bank Name Code

1 PT Bank ICB Bumiputera Tbk (formerly PT Bank Bumiputera Indonesia

Tbk) BABP

2 PT Bank Danamon Indonesia Tbk BDMN

3 PT Bank Century Tbk (formerly PT Bank CIC Internasional Tbk) BCIC

4 PT Bank Eksekutif Internasional Tbk BEKS

5 PT Bank Internasioanal Indonesia Tbk BNII

6 PT Bank Artha Graha International Tbk (formerly PT Bank Inter-Pacific

Tbk) INPC

7 PT Bank Kesawan Tbk BKSW

8 PT Bank Mandiri (Persero) Tbk BMRI

9 PT Bank Mayapada Internasional Tbk MAYA

10 PT Bank Mega Tbk MEGA

11 PT Bank Negara Indonesia (Persero) Tbk BBNI

12 PT Bank Nusantara Parahyangan Tbk BBNP

13 PT Bank Swadesi Tbk BSWD

14 PT Bank Victoria Internasional Tbk BVIC

15 PT Bank Agroniaga Tbk AGRO

16 PT Bank Ekonomi Raharja Tbk BAEK

17 PT Bank Central Asia Tbk BBCA

18 PT Bank Jabar Banten BJBR

19 PT Bank Bumi Arta Tbk BNBA

20 PT Bank Tabungan Pensiunan Nasional BTPN

21 PT Bank Windu Kentjana International Tbk (formerly PT Bank Multicor

Tbk) MCOR

22 PT Bank Himpunan Saudara 1906 Tbk SDRA

23 PT Bank Bukopin BBKP

24 PT Bank Rakyat Indonesia BBRI

25 PT Bank Niaga BNGA

26 PT Bank OCBC NISP Tbk (formerly PT Bank NISP Tbk) NISP

27 PT Bank Pan Indonesia Tbk PNBN

28 PT Bank Permata BNLI

III.3 Research Variable and Operational Definitions Variable

III.3.1 Dependent Variable

In this research, the dependent variable that will be used is auditor

switching. Auditor switching is the replacement of auditor or public accountant

firm done by the client due to several specified reasons, whether it is caused by

22

the client or the auditor. In this research, the research is trying to understand the

dependent variable, explain its variability, and predict it. Furthermore, the

auditor switching that will become the object of research is voluntary auditor

switching.

Dependent variable in this research is dummy since the score will be 1 or

0. The 1 here means this company is doing auditor switching voluntarily and the

0 means the opposite.

III.3.2 Independent Variables

Independent variable is a free variable. This variable affects the

movement of dependent variable which is auditor switching. In this research, the

writer uses auditor opinion, public accountant firm size, management changes,

and financial distress as the independent variables.

1. Auditor’s Opinion

This variable uses dummy variable. If the client receives the opinion

except Unqualified, the score will be 1. If it received Unqualified, the score

will be 0. There are 5 opinions that should be given by the auditor.

2. Public Accountant Firm size

This variable uses dummy variable. If the company tested is audited by

Big 4 audit firms, it will be scored 1. If it is audited by non Big 4, it will be

scored 0 (Nasser and Wahid, 2006).

Here is the list of Big 4 public accountant firm (based on alphabets):

1. Deloitte Touche Tohmatsu

It is affiliated with Hans Tuanakotta Mustofa & Halim; Osman Ramli

Satrio & Partners; Osman Bing Satrio and Partners.

23

2. Ernest & Young (EY)

It is affiliated with Prasetio, Sarwoko, & Sandjaja; Purwantono, Sarwoko

& Sandjaja.

3. Klynveld Peat Marwick Goerdeler (KPMG)

In Indonesia, this public accountant firm is affiliated with Siddharta and

Widjaja.

4. Pricewaterhouse Coopers (PwC)

This public accountant firm in Indonesia is affiliated with Tanudiredja,

Rintis, Wibisana, and Partners.

3. Management Changes

In this research, company will be valued doing management changes

when the CEO is changed. This variable is dummy variable. If the CEO is

changed it will be scored 1 and if it is not it will be scored 0.

4. Financial Distress

Financial distress refers to a period when a borrower (either individual or

institutional) is unable to meet a payment obligation to lenders and other

creditors. This distress may be due to borrower specific factors like

reputation, leverage, volatility of earnings, collateral or may be due to

market specific factors like the economic condition and level of interest

rates. In the previous research, Zaki et al. (2012) assessed probabilities of

financial distress of banks in UAE by using time-discrete hazard model with

Logit and Probit. In this research, the analytical method that will be used is

Z-Score Altman. This model for go public banking companies has been

determined by this model:

24

𝒁𝑺𝒄𝒐𝒓𝒆 = 𝟏,𝟐𝑿𝟏 + 𝟏,𝟒𝑿𝟐 + 𝟑,𝟑𝑿𝟑 + 𝟎,𝟔𝑿𝟒 + 𝟏,𝟎𝑿𝟓

Explanation:

Z = Index overall

X1 = Working Capital to Total Assets

X2 = Retained Earning to Total Assets

X3 = EBIT (Earning Before Interest Taxes) to Total Assets

X4 = Market Value of Equity to Book Value of Total Liabilities

X5 = Sales to Total Assets

Z-Score value will explain the condition of banking companies divided

into several levels:

1. Z-Score > 2,99 is categorized as healthful companies. There is no

financial difficulties occurred.

2. 1,81 < Z-Score < 2,99 is categorized as grey area which can be

considered experiencing financial difficulties but the probability of

safe or insolvent are depend on the decision of companies

management as the decision maker.

3. Z-Score < 1,81 is categorized as black are where company is

experiencing financial difficulties and has high risk to go into

liquidation.

Financial distress in this research can be seen by evaluating Z-Score Altman

value.

III.4 Research Instrument

In quantitative research, data testing to prove or disprove the hypothesis is

conducted by using the statistical tool called SPSS. SPSS stands for Statistical Product

25

and Service Solutions or nowadays being known as PASW or Predictive Analytics

Software. SPSS is an application program that has a high statistical analysis capabilities

as well as the data management system in a graphical environment using descriptive

menus and dialog boxes. It is therefore suitable to process all the data by using

computer software called SPSS (Statistical Package for the Social Sciences) version

16.0 for Windows.

III.5 Data Collection Procedures

Data collection being used in this research is through documentation method and

literature review. Documentation method is done through studying archives and

journals which relevant with the research conducted. The secondary data is a source of a

research which is obtained from the existing resources. The data already exist and do

not have to be collected individually by the researcher. This research use the financial

data that obtained from the published financial reports of company listed in Indonesia

Stock Exchange (IDX). The financial data that being used in this research are the

financial statements of companies listed in Indonesia Stock Exchange (IDX) from 2008

until 2014. The data are being downloaded by accessing the website of IDX itself. The

website we can find in internet the key word is Indonesia Stock Exchange

(www.idx.co.id). Later this data will be categorized based on the criteria of the samples

needed.

III.6 Data Analysis

In this research, the writer would like to use quantitative analysis. It quantifies

and transfers information become measurable and readable. Analysis tool that will be

performed in this research is logistic regression since dependent variable is naturally

dichotomy (execute auditor switching and do not execute auditor switching). The

26

execution of regression method does not need normality assumption for independent

variables. Multivariate normal distribution is unable to be performed since independent

variables are the fusion of matrix and non-matrix variable. Therefore, it is able to be

analyzed by using logistic regression since normality assumption at independent

variables is unnecessary to be performed. The purpose of this method is to get the whole

picture about the relation between the independent variables and dependent variables

for the company performance of a company in knowledge intensive industry category

for a bank in Indonesia Stock Exchange (IDX) from 2008 until 2014. The steps in doing

logistic regression are explained below:

III.6.1 Descriptive Statistic

Descriptive statistic is used to provide and define a description of the

data seen from the average (mean), standard deviation, and maximum-minimum.

The mean used to estimate the average size of population estimated from the

sample. The standard deviation is used to assess the average dispersion of the

sample. The maximum-minimum is used to view the minimum value and

maximum of the population. It needs to be done to see the entire picture of the

samples collected and qualified as research sample. This will be applied on all

independent variables:

In this research, the auditor opinion will be categorized into two types:

Unqualified and other than unqualified (qualified, disclaimer, and adverse). Here

is the table:

27

Table 3.6.1.1

Auditor Switching observed from Auditor Opinion

Variable Change PAF Does not

change PAF Total

4-4 4-N N-4 N-N ∑

Opinion

UQ

Other

than UQ

TOTAL

For this part, the size of public accountant firm (PAF) is divided into two

categories: Big 4 and Non Big 4. Here is the table:

Table 3.6.1.2

Auditor Switching observed from PAF size

Variable Change PAF Does not change

PAF Total

4-4 4-N N-4 N-N ∑

PAF size (latest

used)

Big 4

Non Big

4

TOTAL

The management changes that will be observed in this research is whether the

company change the CEO. The consideration will be parted into two which are yes and

no. Here is the table:

Table 3.6.1.3

Auditor Switching observed from Management Changes

Variable Change PAF Does not change

PAF Total

4-4 4-N N-4 N-N ∑

Management

Changes

Yes

No

TOTAL

28

Descriptive from financial distress variable can be measured with Z-Score

Altman which is divided into three categories: safe from liquidation, grey area which is

company who stands on the verge of liquidation, and black area which is company who

was experiencing financial difficulties and would experience liquidation.

Table 3.6.1.4

Auditor Switching observed from Financial Distress

Variable

Change PAF Does

not

change

PAF

Total 4-4 4-N N-4 N-N ∑

Financial Distress

Safe

Gray Area

FD

TOTAL

III.6.2 Inferential Statistic Analysis

Inferential statistic analysis that is used to test the hypothesis in this

research is multivariate with logistic regression. Logistic regression measures

the power of relationship between independent and dependent variables. The

dependent variable is assumed random which means has probabilistic

distribution. Logistic regression ignores heteroscedasticity which explains that

dependent variable does not need homoscedasticity for each independent

variable. The purpose of normality and heteroscedasticity test is to ensure that

analysis regression model used in this research is valid.

This test does not need to perform normality and heterdoscedasticity test

since before hypothesis test is executed the first step that has to be done is test

the validity of regression model and valuing fit model. Those methods are the

substitution of classic assumption test.

29

III.6.3 Hypothesis Test

The parameter estimation is using Maximum Likehood Estimation (MLE).

Ho = b1 = b2 = b3 = …= bi = 0

Ho ≠ b1 ≠ b2 ≠ b3 ≠ … ≠ bi ≠ 0

The 0 hypothesis states that independent variable (X) does not have influence on

responded variable (in population). The test over hypothesis is done by using a =

5%. The decision making rules is:

1. If probability score (sig.) < a = 5%, the alternative hypothesis is

supported.

2. If probability score (sig.) > a = 5%, the alternative hypothesis is not

supported.

III.6.3.1 Valuing Overall Model Fit

The first step of this model is to valuing overall model fit upon the data

by giving some statistic tests. The hypothesis to value this model fit is:

H0 : Hypothesized model that is fit with the data

HA : Hypothesized model that is unfit with the data

From this hypothesis, it is clear that the model fits the data. The statistics

used in this research is based on the likelihood function. Likelihood L of the

model is the probability that the hypothesized model depicts the input data.

To test null hypothesis and alternative hypothesis, L has to be transformed

into -2LogL. Decreasing of likelihood (-2LL) shows better regression model.

In other words, the hypothesized model fits the data.

30

III.6.3.2 Coefficient of Determination (Nagelkerke R Square)

Cox and Snell's R Square is a measure that seeks to imitate the size of R2

at multiple regression based on likelihood estimation techniques with a

maximum value of less than 1 (one) so it is difficult to interpret.

Nagelkerke's R-square is a modification of the coefficient Cox and Snell to

ensure that its value varies from 0 (zero) to 1 (one). This is done by dividing

the value of Cox and Snell's R2 to the maximum value. Nagelkerke's value

R2 can be interpreted as the value of R2 in the multiple regressions. A small

value means the ability of variables independent in explaining variations in

the dependent variable is very limited. A value which is close to one mean of

independent variables provides almost all the information needed to predict

the variation of the dependent variable.

III.6.3.3 Regression Model Test

The fairness of regression model was valued with Hosmer and

Lemeshow's Goodness of Fit Test. Hosmer and Lemeshow's Goodness of Fit

Test. It is used to test the null hypothesis that the empirical data is fit with

the model (there was no difference between the models with the data so that

the model can be said to be fit). If the value of statistical Hosmer and

Lemeshow's Goodness of Fit Test is equal to or less than 0.05, the null

hypothesis is rejected, which means there are significant differences between

the models with observations that the value of Goodness fit model is not

good because the model cannot predict the value of his observations. If the

statistical value of Hosmer and Lemeshow's Goodness of Fit Test is greater

than 0.05, the null hypothesis cannot be rejected and means that the model is

31

able to predict the value of observation or can be said to be acceptable as a

model fits the data observations.

The appropriateness of this regression model is using Hosemer and

Lemeshow’s Goodness of Fit Test. Hosmer and Lemeshow’s Goodness of

Fit Test attest null hypothesis that empirical data is suitable with the model

(there is no significant differences between model and data, therefore model

can be counted as suitable). If Hosmer and Lemeshow’s statistic value is

equal or less than 0.05, null hypothesis is rejected which also means there is

a significant differences between model and observation value. In result,

Goodness Fit model is categorized as bad since it is not able to predict the

value of observation. If the statistic value is higher than 0.05, null hypothesis

is accepted which means model is able to predict the value of observation or

simply said it can be accepted since it fits observation data.

III.6.3.4 Multicolinearity Test

A good regression model is the one that does not have a strong

phenomenon correlation between their independent variables. This test is

using matrix correlation between independent variables to see how big the

correlation between them. If independent variables are simultaneously

correlated, these variables are orthogonal. The orthogonal variable means

independent variable equal zero.

III.6.3.5 Matrix Classification

Matrix classification shows prediction power of regression model to

predict the possibility of auditor switching done by public accountant firm.

32

III.6.3.6 Logistic Regression Model

The analysis in this research is using the statistical parameters with

logistic regression model. The model of logistic regression in this research

is:

SWITCHt = bo + b1OPINI + b2PAF + b3MG + b4FD + e............

Explanation:

SWITCH : auditor switching

bo : constant

b1-b4 : regression coefficient

OPINI : auditor opinion

PAF : public accountant firm size

MG : management changes

FD : financial distress

e : error

33

CHAPTER IV

DATA ANALYSIS AND EVALUATION

IV.1 Research Object Description

In this research, the data used is secondary data from audited financial

statements of banking companies listed in Indonesia Stock Exchange for period

2008 – 2014. There are 42 bank listed in Indonesia Stock Exchange within

period 2008 – 2014 and 14 bank are excluded from total sample since they do

not match the criteria. In conclusion, there are 28 banking companies left within

7 periods which is from 2008 – 2014 which resulted in 196 data from 28 bank

times 7 periods. The sampling method of this data is purposive sampling which

have criteria for sample determination.

IV.2 Research Variable Description

This part is used to depict the total of sample of banking companies that

executed auditor switching during 2008 – 2014 based on independent variables

of the research: auditor opinion, public accountant firm size, management

changes, and financial distress towards auditor switching from Big 4 to Big 4,

Big 4 to Non Big 4, Non Big 4 to Big 4, and Non Big 4 to Non Big 4.

Consequently, there are 4 independent variables and 1 independent variable that

will be examined here.

IV.3 Descriptive Statistic

There are two types of descriptive statistic valuation used in this

research: Frequencies and Descriptives. Frequencies is used for dummy data

valuation and Descriptives is used for financial ratios valuation. Therefore, the

34

descriptive statistic data below is presented as the result of financial distress

variable only.

Table 4.3.1 Data Descriptive Variable

Audit Switching

Frequency Percent Valid Percent

Cumulative

Percent

Valid Non Audit Switching 148 75.5 75.5 75.5

Audit Switching 48 24.5 24.5 100.0

Total 196 100.0 100.0

This result gives an explanation that based on the analysis result of auditor

switching, most respondents did not execute auditor switching. There are 48 data of

banking companies or 24.5% from the total sample perform which performed auditor

switching and 148 data of banking companies or 75.5% of the total sample which did

not.

Table 4.3.2 Data Descriptive Variable

Auditor's Opinion

Frequency Percent Valid Percent

Cumulative

Percent

Valid Unqualified 189 96.4 96.4 96.4

Qualified 7 3.6 3.6 100.0

Total 196 100.0 100.0

35

Based on descriptive analysis result above, most of banking companies

presented as the sample obtained unqualified opinion. It reaches 189 data of banking

companies or 96.4% from the total sample while the one that obtained qualified opinion

(other than unqualified) are 7 data of banking companies or 3.6% which is only one

bank.

Table 4.3.3 Data Descriptive Variable

Public Accountant Firm Size

Frequency Percent Valid Percent

Cumulative

Percent

Valid Non Big Four 59 30.1 30.1 30.1

Big four 137 69.9 69.9 100.0

Total 196 100.0 100.0

The majority of banking companies in this research used Big 4 public

accountant firm. There are 137 data of banking companies or 69.9% from the total

sample that used the service of Big 4. On contrary, the Non Big 4 customers are 59 data

of banking companies or 30.1% in type of percentage.

Table 4.3.4 Data Descriptive Variable

Management Changes

Frequency Percent Valid Percent

Cumulative

Percent

Valid CEO not changes 137 69.9 69.9 69.9

CEO changes 59 30.1 30.1 100.0

Total 196 100.0 100.0

36

From 196 data of companies chosen as the sample of research, it is discovered

that 59 data of banking companies performed management changes while 137 of them

did not. In conclusion, most of banking companies that respectively listed in Indonesia

Stock Exchange during 2008 – 2014 research periods did not performing management

changes. In percentage, 30.1% of them did change their management and 69.9% of

them did not do so.

Table 4.3.5 Data Descriptive Variable

Financial Distress

Descriptive Statistics

N Minimum Maximum Mean Std. Deviation

Audit Switching 196 .00 1.00 .2449 .43113

Zscore 196 -.74 38.10 1.4049 4.55326

Valid N (listwise) 196

Based on the result presented above, the table shows that financial distress

variable has -0.74 for minimum value and 38.10 for maximum value. The average point

of this variable is 1.4049 and 4.55326 is shown as standard deviation.

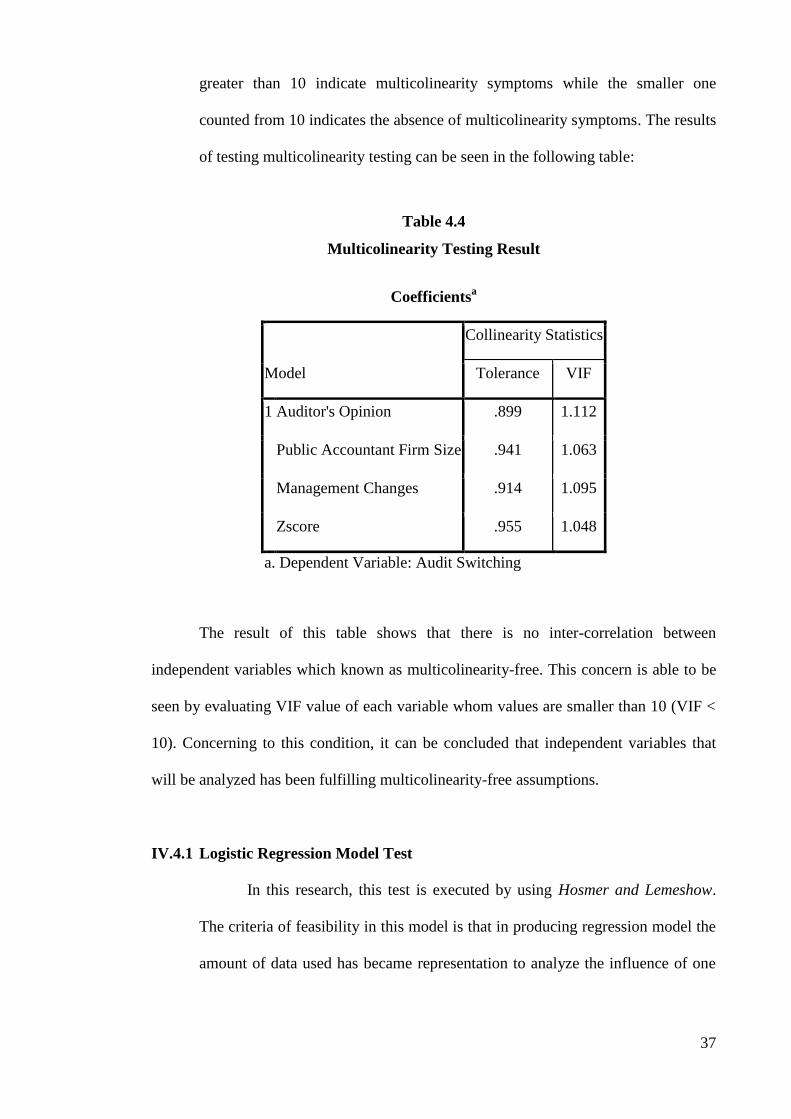

IV.4 Preliminary Logistic Regression Test (Multicolinearity)

Multicolinearity is shown as a cause-and-effect relationship between two

or more independent variables within one analysis model. In this research,

multicolinearity test is performed toward 4 independent variables: auditor’s

opinion, public accountant firm size, management changes, and financial

distress towards auditor switching. To discover the existence of multicolinearity,

the researcher uses Variance Inflation Factor (VIF). The VIF values which

37

greater than 10 indicate multicolinearity symptoms while the smaller one

counted from 10 indicates the absence of multicolinearity symptoms. The results

of testing multicolinearity testing can be seen in the following table:

Table 4.4

Multicolinearity Testing Result

Coefficientsa

Model

Collinearity Statistics

Tolerance VIF

1 Auditor's Opinion .899 1.112

Public Accountant Firm Size .941 1.063

Management Changes .914 1.095

Zscore .955 1.048

a. Dependent Variable: Audit Switching

The result of this table shows that there is no inter-correlation between

independent variables which known as multicolinearity-free. This concern is able to be

seen by evaluating VIF value of each variable whom values are smaller than 10 (VIF <

10). Concerning to this condition, it can be concluded that independent variables that

will be analyzed has been fulfilling multicolinearity-free assumptions.

IV.4.1 Logistic Regression Model Test

In this research, this test is executed by using Hosmer and Lemeshow.

The criteria of feasibility in this model is that in producing regression model the

amount of data used has became representation to analyze the influence of one

38

variable. The result of this attempt of Hosmer and Lemeshow is presented below

in this table:

Table 4.4.1

Hosmer and Lemeshow Test

Hosmer and Lemeshow Test

Step Chi-square df Sig.

1 3.409 8 .906

This table provides the analysis of Hosmer and Lemeshow test and

presents the evidence of regression model feasibility which has met the criteria.

The significant value is much greater than alpha 5% (0.906 > 0.05) which

caused the acceptance of null hypothesis. It has a meaning that the data analyzed

in logistic model has been fulfilling feasibility criteria. Therefore, the model is

accepted and hypothesis test shall be run.

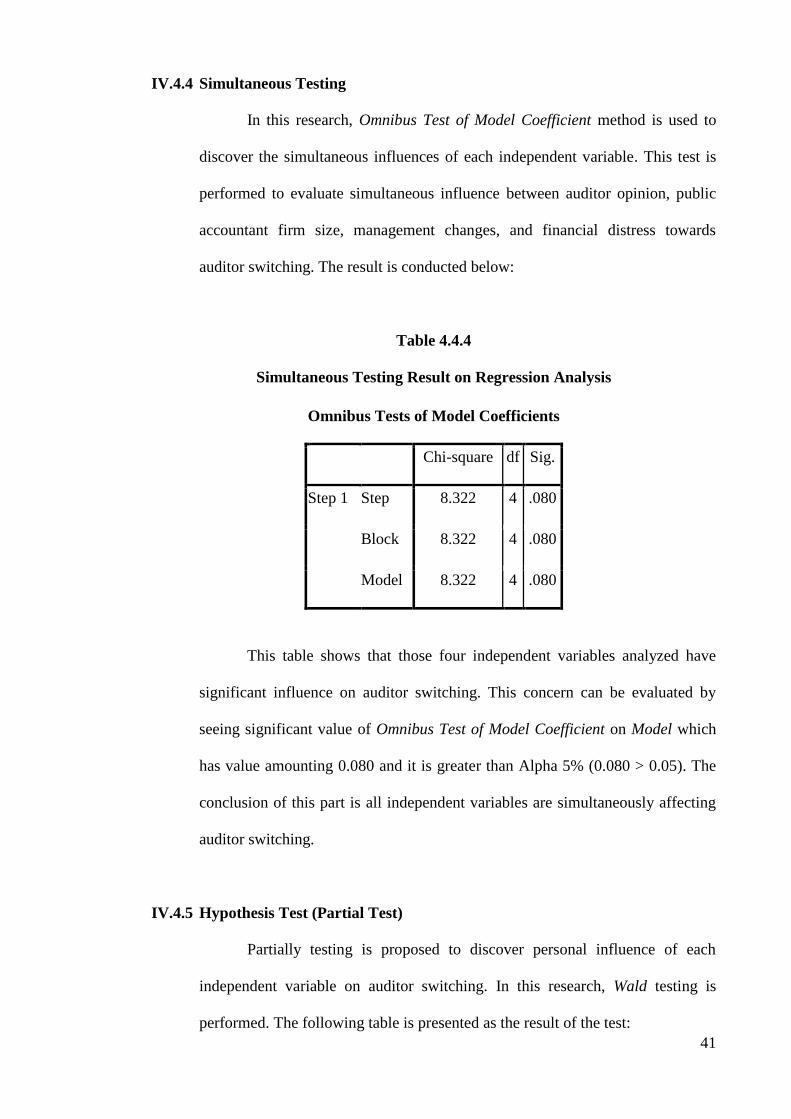

IV.4.2 Overall Model Fit Test

This test is performed to see if the model fit the data both before and

after independent variable addition into the model. Assessment of the overall

regression model using the -2 log likelihood (LL) value where if figure -2 log

likelihood experiences shortfall on the second block compared to the first block

then it can be inferred that regression model is good. The evaluation of the

overall model is done by comparing the initial -2 log likelihood (-2LL) (block

number = 0), where the models only insert constants with values -2 log

likelihood (-2LL) at the end (block number = 1), where a model incorporating

constants and independent variables.

39

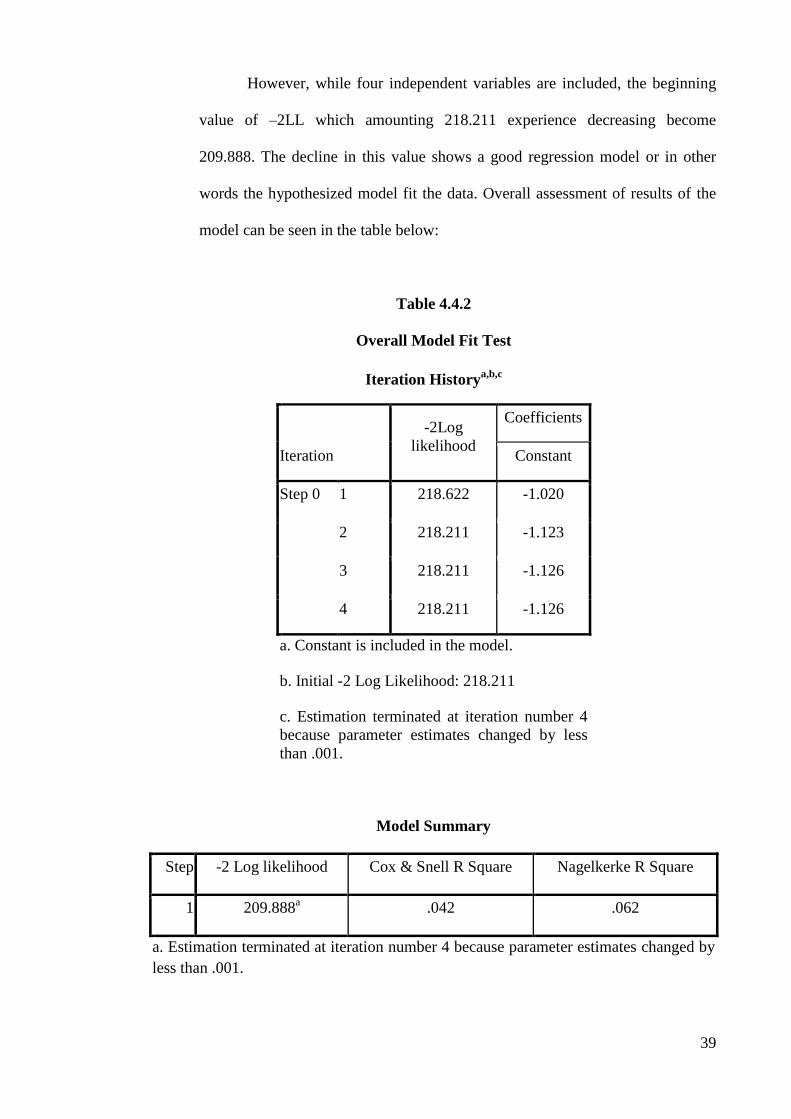

However, while four independent variables are included, the beginning

value of –2LL which amounting 218.211 experience decreasing become

209.888. The decline in this value shows a good regression model or in other

words the hypothesized model fit the data. Overall assessment of results of the

model can be seen in the table below:

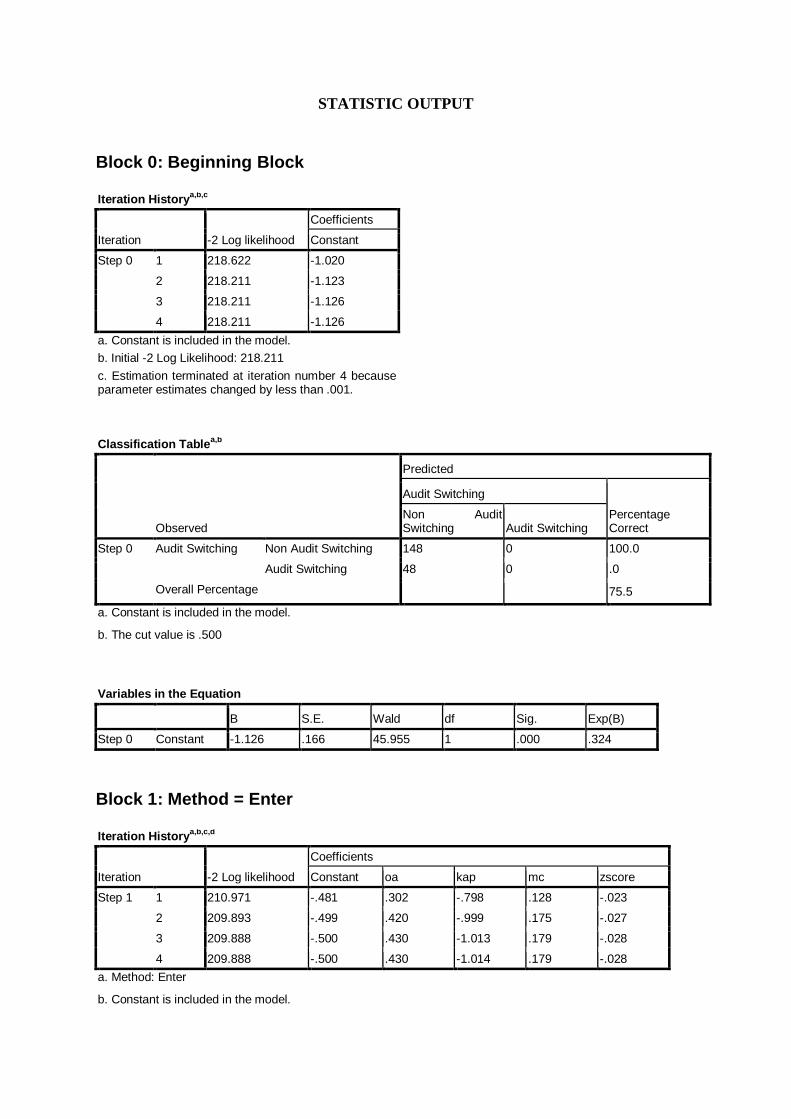

Table 4.4.2

Overall Model Fit Test

Iteration Historya,b,c

Iteration

-2Log

likelihood

Coefficients

Constant

Step 0 1 218.622 -1.020

2 218.211 -1.123

3 218.211 -1.126

4 218.211 -1.126

a. Constant is included in the model.

b. Initial -2 Log Likelihood: 218.211

c. Estimation terminated at iteration number 4

because parameter estimates changed by less

than .001.

Model Summary

Step -2 Log likelihood Cox & Snell R Square Nagelkerke R Square

1 209.888a .042 .062

a. Estimation terminated at iteration number 4 because parameter estimates changed by

less than .001.

40

IV.4.3 Hypothesis Test

(Coefficient of Determination Nagelkerke R Square)

This paragraph describes the research data outcome to attest every

hypothesis of research that has been made. By performing Nagelkerke R Square,

the ability to look over the magnitude of all independent variables in affecting

and describing the diversity of dependent variable timeliness of reporting can be

observed. It can be seen by evaluating the value of Nagelkerke R Square

logistics analysis results. Hereby presented Nagelkerke R Square value in the

logistic regression models formed:

Table 4.4.3

Nagelkerke R Square value on Logistic Regression Analysis

Model Summary

Step -2 Log likelihood Cox & Snell R Square Nagelkerke R Square

1 209.888a .042 .062

a. Estimation terminated at iteration number 4 because parameter estimates changed by

less than .001.