Embed Size (px)

Citation preview

0

Analyst MeetingFY 2015

PTT Auditorium26 February 2016

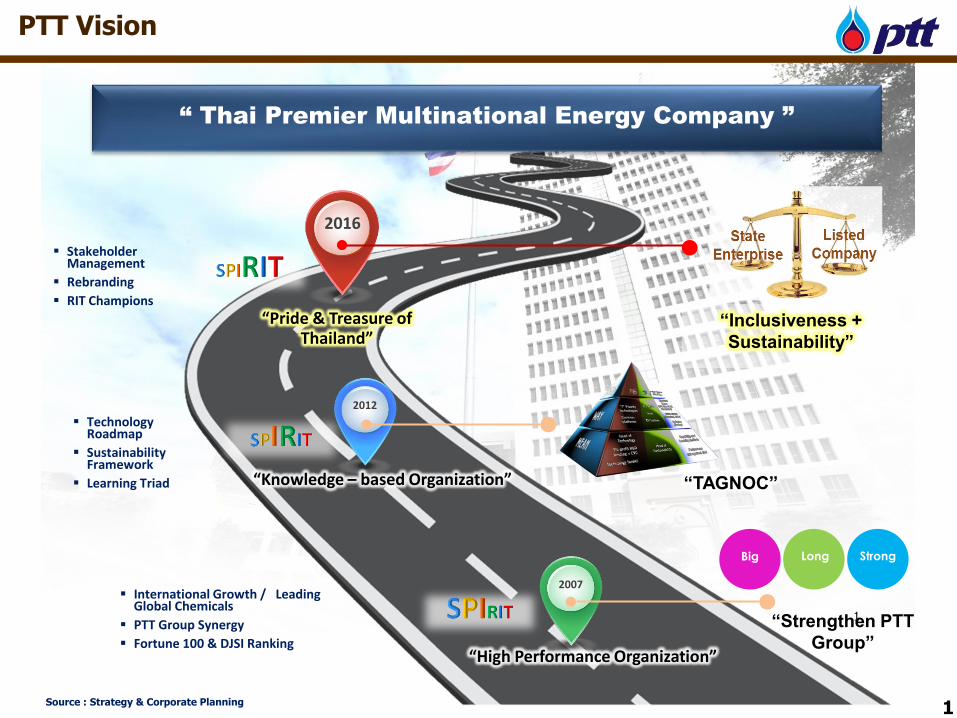

International Growth / Leading Global Chemicals

PTT Group Synergy

Fortune 100 & DJSI Ranking

“Strengthen PTT

Group”

Big Long Strong

2007

“High Performance Organization”

2012

“TAGNOC”“Knowledge – based Organization”

2016

Technology Roadmap

Sustainability Framework

Learning Triad

“Inclusiveness +

Sustainability”

Stakeholder Management

Rebranding

RIT Champions

“Pride & Treasure of Thailand”

“ Thai Premier Multinational Energy Company ”

1

Source : Strategy & Corporate Planning

PTT Vision

1

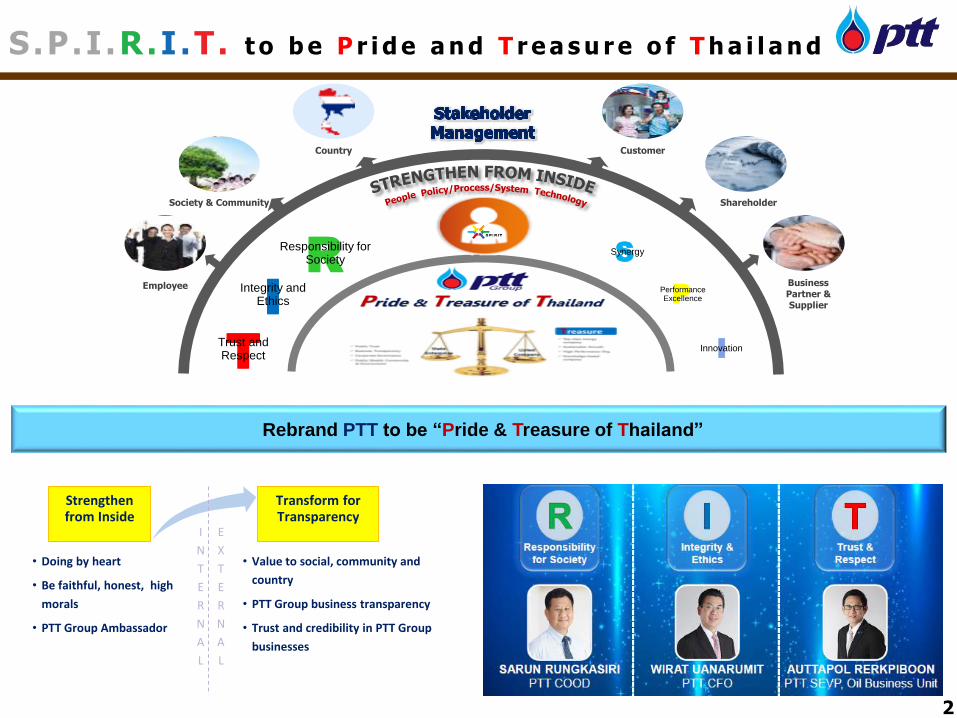

S.P.I .R.I .T . t o b e P r i d e a n d T r e a s u r e o f T h a i l a n d

2

Society & Community

CustomerCountry

Shareholder

Business Partner &Supplier

Employee

RResponsibility for

Society

IIntegrity and

Ethics

TTrust and Respect

SSynergy

PPerformanceExcellence

IInnovation

Rebrand PTT to be “Pride & Treasure of Thailand”

Strengthen from Inside

Transform for Transparency

• Doing by heart

• Be faithful, honest, high

morals

• PTT Group Ambassador

• Value to social, community and

country

• PTT Group business transparency

• Trust and credibility in PTT Group

businesses

I

N

T

E

R

N

A

L

E

X

T

E

R

N

A

L

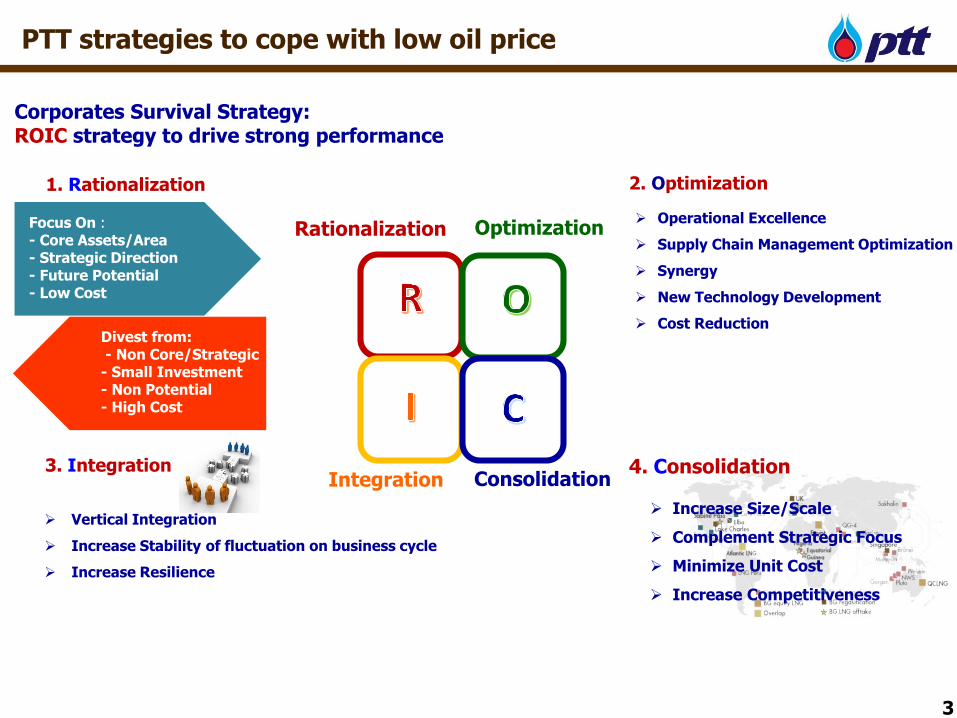

Corporates Survival Strategy:ROIC strategy to drive strong performance

Rationalization Optimization

Integration Consolidation

1. Rationalization

Focus On : - Core Assets/Area- Strategic Direction- Future Potential- Low Cost

Divest from: - Non Core/Strategic

- Small Investment- Non Potential- High Cost

2. Optimization

Operational Excellence

Supply Chain Management Optimization

Synergy

New Technology Development

Cost Reduction

3. Integration

Vertical Integration

Increase Stability of fluctuation on business cycle

Increase Resilience

4. Consolidation

Increase Size/Scale

Complement Strategic Focus

Minimize Unit Cost

Increase Competitiveness

3

PTT strategies to cope with low oil price

4

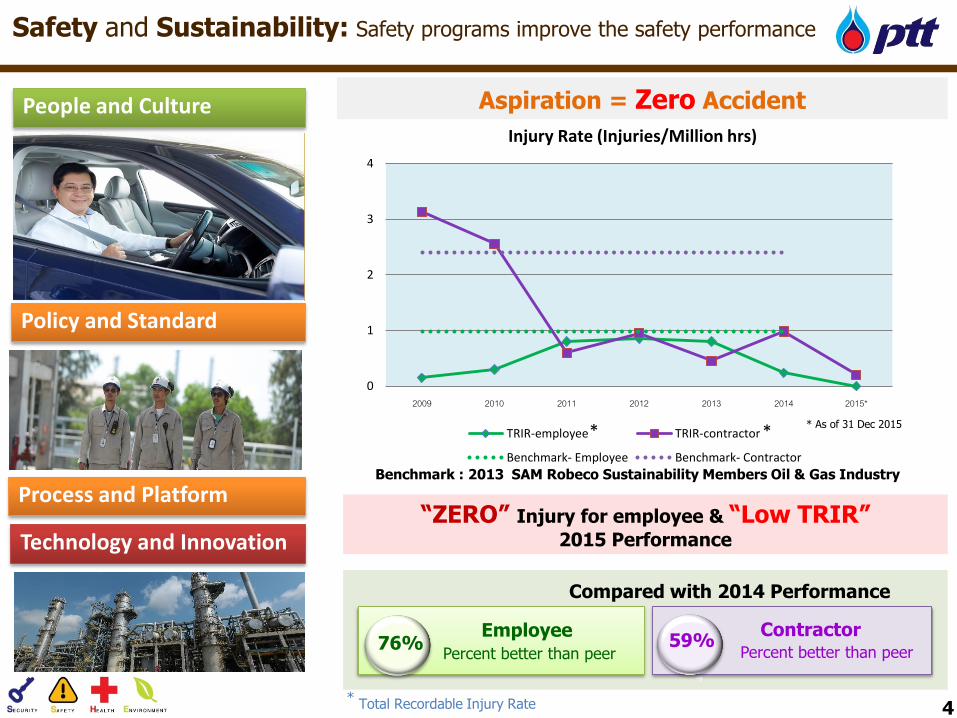

Safety and Sustainability: Safety programs improve the safety performance

Aspiration = Zero Accident

* Total Recordable Injury Rate

Benchmark : 2013 SAM Robeco Sustainability Members Oil & Gas Industry

Contractor76% 59%

EmployeePercent better than peer Percent better than peer

4

“ZERO” Injury for employee & “Low TRIR”2015 Performance

Compared with 2014 Performance

Policy and Standard

Process and Platform

Technology and Innovation

People and Culture

* ** As of 31 Dec 2015

0

1

2

3

4

2009 2010 2011 2012 2013 2014 2015*

Injury Rate (Injuries/Million hrs)

TRIR-employee TRIR-contractor

Benchmark- Employee Benchmark- Contractor

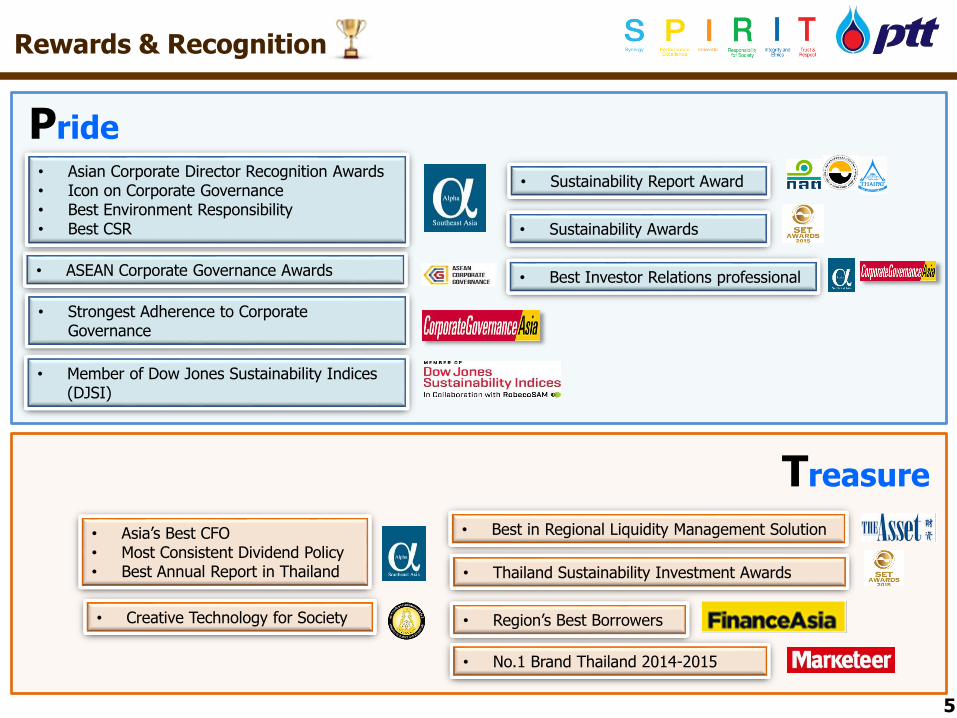

• Strongest Adherence to Corporate Governance

Rewards & Recognition

Pride

Treasure

• Member of Dow Jones Sustainability Indices (DJSI)

• Asia’s Best CFO• Most Consistent Dividend Policy• Best Annual Report in Thailand

• ASEAN Corporate Governance Awards

• Best in Regional Liquidity Management Solution

• Region’s Best Borrowers

• No.1 Brand Thailand 2014-2015

• Asian Corporate Director Recognition Awards • Icon on Corporate Governance• Best Environment Responsibility• Best CSR

• Thailand Sustainability Investment Awards

• Creative Technology for Society

• Sustainability Report Award

• Best Investor Relations professional

5

• Sustainability Awards

2015 Year in Review

Performance

2016 Outlook

2015 Year in Review Performance 2016 Outlook

Contents

6

0

20

40

60

80

100

120

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Dubai price$ / BBL

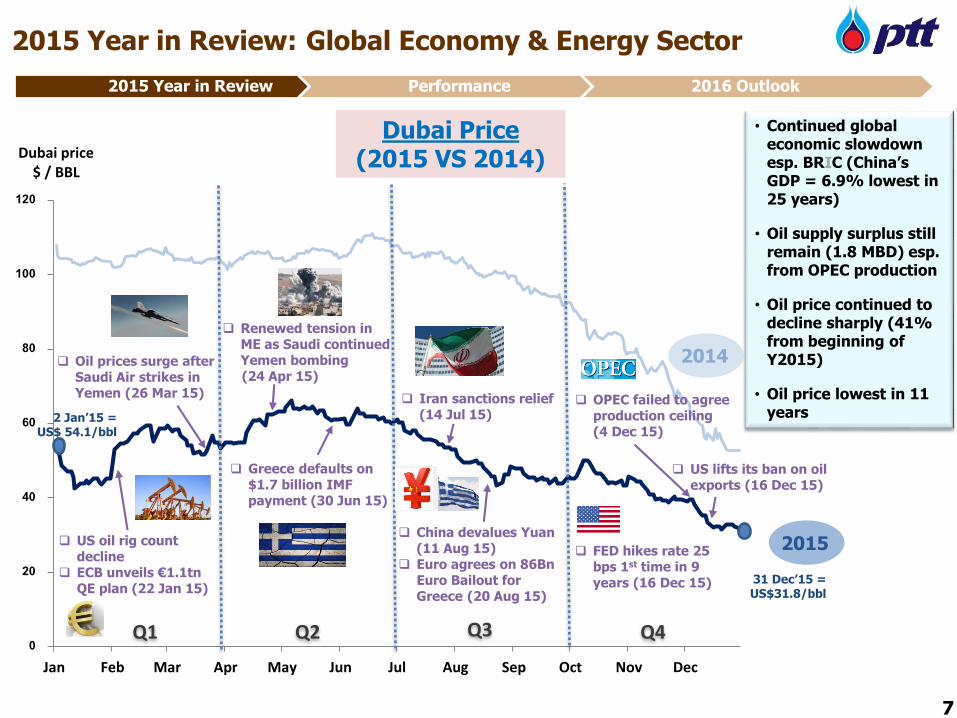

FED hikes rate 25 bps 1st time in 9 years (16 Dec 15)

OPEC failed to agree production ceiling (4 Dec 15)

Dubai Price(2015 VS 2014)

2015 Year in Review: Global Economy & Energy Sector

China devalues Yuan (11 Aug 15)

Euro agrees on 86Bn Euro Bailout for Greece (20 Aug 15)

Q3 Q4

• Continued global economic slowdown esp. BRIC (China’s GDP = 6.9% lowest in 25 years)

• Oil supply surplus still remain (1.8 MBD) esp. from OPEC production

• Oil price continued to decline sharply (41% from beginning of Y2015)

• Oil price lowest in 11 years

2014

2015

31 Dec’15 = US$31.8/bbl

2 Jan’15 = US$ 54.1/bbl

7

Q2Q1

US oil rig count decline

ECB unveils €1.1tn QE plan (22 Jan 15)

Iran sanctions relief (14 Jul 15)

Renewed tension in ME as Saudi continued Yemen bombing(24 Apr 15)

Oil prices surge after Saudi Air strikes in Yemen (26 Mar 15)

Greece defaults on $1.7 billion IMF payment (30 Jun 15)

2015 Year in Review Performance 2016 Outlook

US lifts its ban on oil exports (16 Dec 15)

7

Jan-15 Apr-15 Jul-15 Oct-15

Bomb at the Ratchaprasongintersection(17 Aug)

New constitution draft was rejected by council (6 Sep)

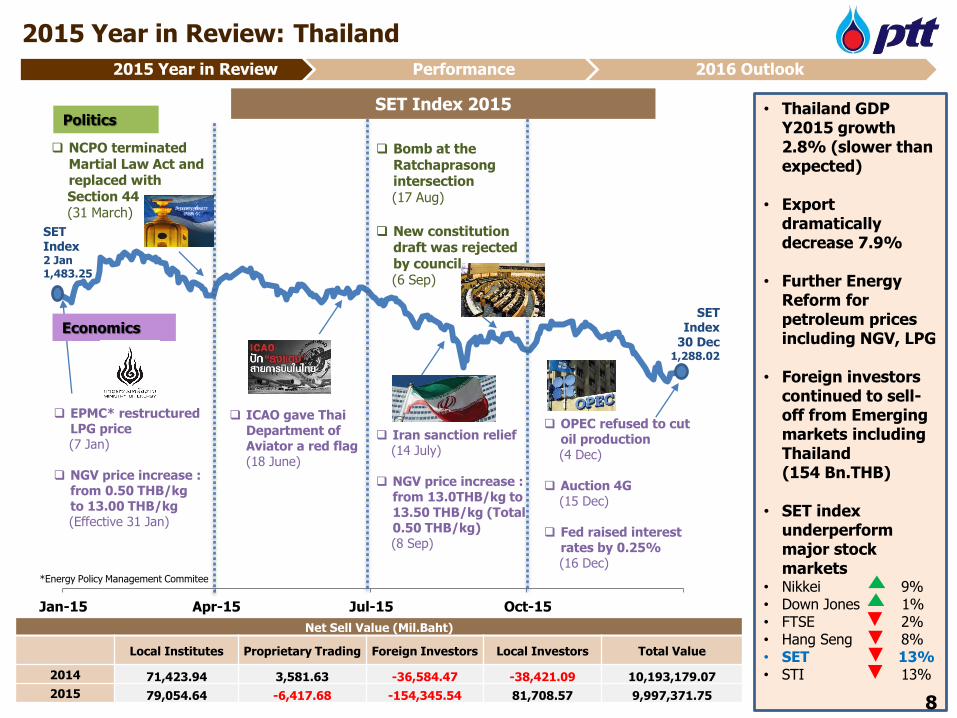

2015 Year in Review: Thailand

SET Index2 Jan

1,483.25

SET Index

30 Dec1,288.02

Politics

Economics

Iran sanction relief (14 July)

NGV price increase : from 13.0THB/kg to 13.50 THB/kg (Total 0.50 THB/kg) (8 Sep)

• Thailand GDP Y2015 growth 2.8% (slower than expected)

• Export dramatically decrease 7.9%

• Further Energy Reform for petroleum prices including NGV, LPG

• Foreign investors continued to sell-off from Emerging markets including Thailand(154 Bn.THB)

• SET index underperform major stock markets

• Nikkei 9%• Down Jones 1%• FTSE 2%• Hang Seng 8% • SET 13% • STI 13%

SET Index 2015

8

OPEC refused to cut oil production (4 Dec)

Auction 4G (15 Dec)

Fed raised interest rates by 0.25% (16 Dec)

NCPO terminated Martial Law Act and replaced with Section 44(31 March)

ICAO gave Thai Department of Aviator a red flag (18 June)

EPMC* restructured LPG price (7 Jan)

NGV price increase : from 0.50 THB/kg to 13.00 THB/kg (Effective 31 Jan)

Net Sell Value (Mil.Baht)

Local Institutes Proprietary Trading Foreign Investors Local Investors Total Value

2014 71,423.94 3,581.63 -36,584.47 -38,421.09 10,193,179.07

2015 79,054.64 -6,417.68 -154,345.54 81,708.57 9,997,371.75

*Energy Policy Management Commitee

2015 Year in Review Performance 2016 Outlook

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

9

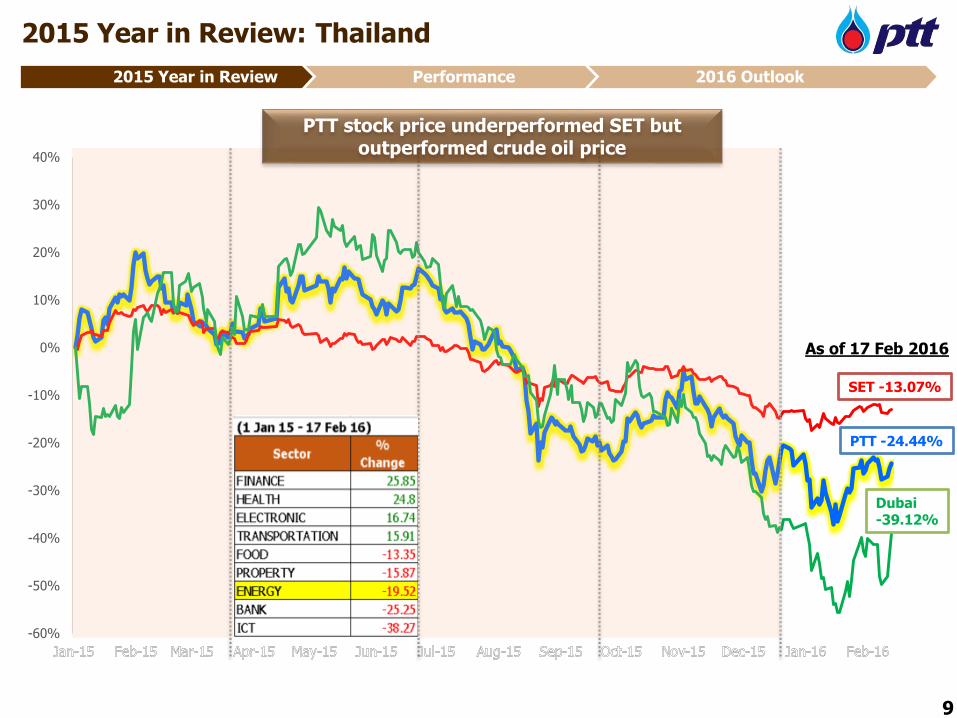

2015 Year in Review: Thailand

Dubai -39.12%

PTT -24.44%

SET -13.07%

As of 17 Feb 2016

2015 Year in Review Performance 2016 Outlook

9

PTT stock price underperformed SET but outperformed crude oil price

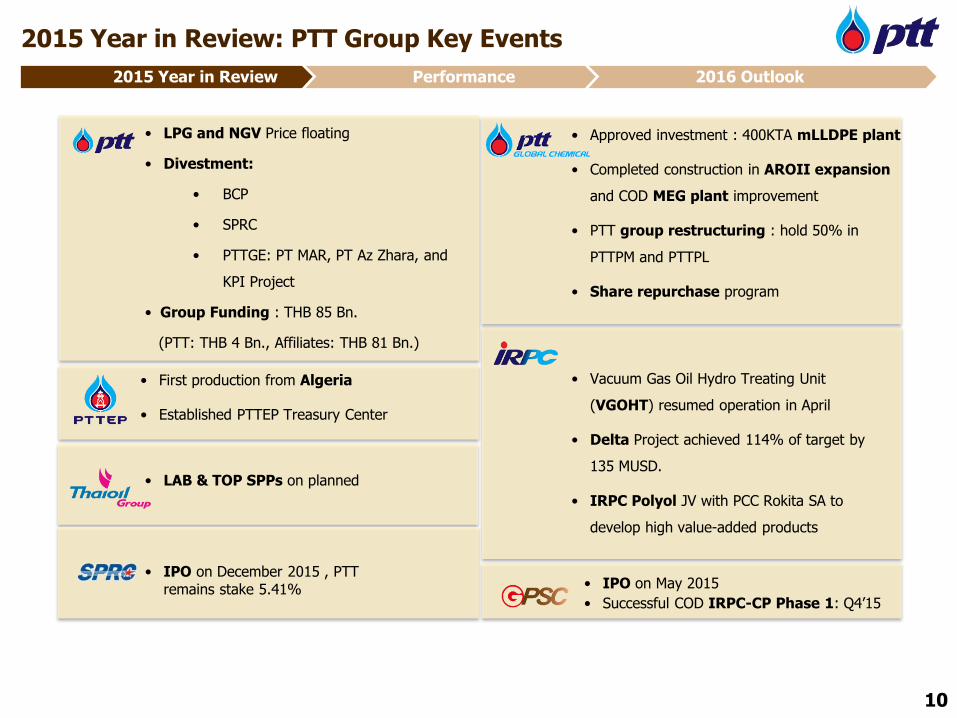

• First production from Algeria

• Established PTTEP Treasury Center

• IPO on May 2015

• Successful COD IRPC-CP Phase 1: Q4’15

2015 Year in Review: PTT Group Key Events

• LPG and NGV Price floating

• Divestment:

• BCP

• SPRC

• PTTGE: PT MAR, PT Az Zhara, and

KPI Project

• Group Funding : THB 85 Bn.

(PTT: THB 4 Bn., Affiliates: THB 81 Bn.)

• Vacuum Gas Oil Hydro Treating Unit

(VGOHT) resumed operation in April

• Delta Project achieved 114% of target by

135 MUSD.

• IRPC Polyol JV with PCC Rokita SA to

develop high value-added products

• LAB & TOP SPPs on planned

• IPO on December 2015 , PTT remains stake 5.41%

• Approved investment : 400KTA mLLDPE plant

• Completed construction in AROII expansion

and COD MEG plant improvement

• PTT group restructuring : hold 50% in

PTTPM and PTTPL

• Share repurchase program

10

2015 Year in Review Performance 2016 Outlook

0

5

10

15

20

25

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

LNG (JLC) ($/MMBTU) JKM Spot Avg. Pooled Gas ($/MMBTU)

31

32

33

34

35

36

37

Jan-14 Jul-14 Jan-15 Jul-15100

300

500

700

900

1100

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

HDPE-Naphtha Spread PX-Naphtha Spread

20

60

100

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

16.6

NG Prices ($/MMBTU)

* JLC = Japan LNG Cocktail : Landed LNG price in Japan

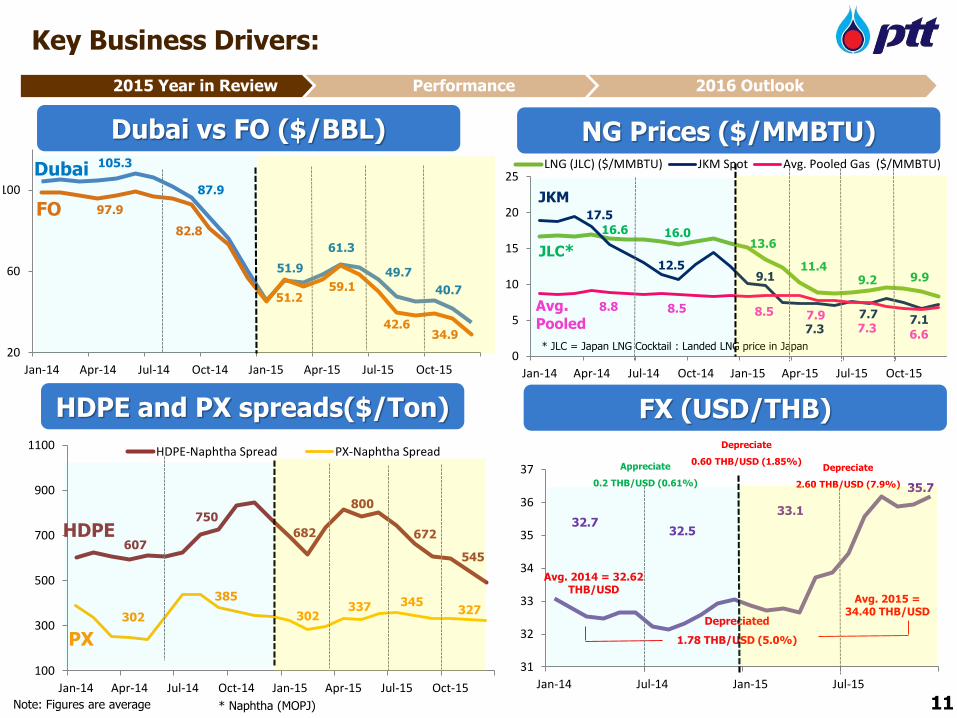

Key Business Drivers:

Note: Figures are average

607

Dubai vs FO ($/BBL)

HDPE and PX spreads($/Ton) FX (USD/THB)

Dubai

FO

HDPE

302

PX

87.9

82.8

750

385

16.0

JLC*

105.3

97.9

Avg. Pooled

8.58.8

51.9

51.2

682

302

13.6

8.5

17.5

12.5

JKM

9.1

32.733.1

11

Depreciated

1.78 THB/USD (5.0%)

Avg. 2014 = 32.62 THB/USD

Avg. 2015 = 34.40 THB/USD

Depreciate

2.60 THB/USD (7.9%)

7.37.7

9.249.7

42.6

672

345

11* Naphtha (MOPJ)

61.3

59.1

11.4

7.37.9

800

337

40.7

34.9

7.1

9.9

6.6

327

545

32.5

35.7

Appreciate

0.2 THB/USD (0.61%)

Depreciate

0.60 THB/USD (1.85%)

2015 Year in Review Performance 2016 Outlook

69%

110%

31%

340%

176%

66%

45,127

(54,698)

34,744

30,938

5,080

11,957

3,855

22,336

(26,083)

10,650

(4,045)

(1,247)

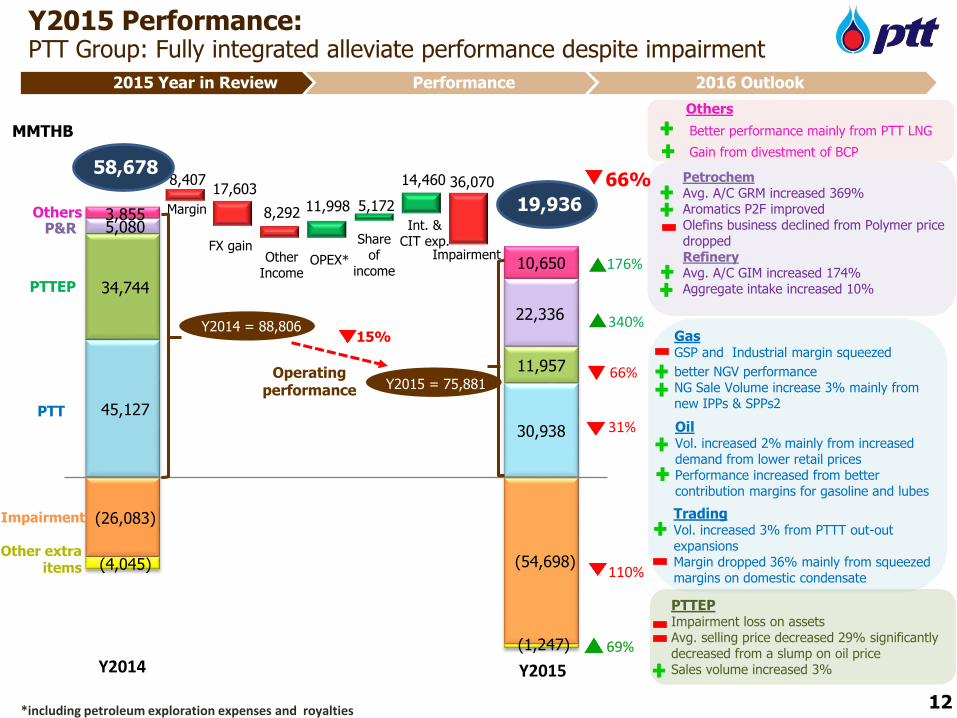

Y2015 Performance: PTT Group: Fully integrated alleviate performance despite impairment

12*including petroleum exploration expenses and royalties

OilVol. increased 2% mainly from increased demand from lower retail prices Performance increased from better contribution margins for gasoline and lubes

TradingVol. increased 3% from PTTT out-out expansionsMargin dropped 36% mainly from squeezed margins on domestic condensate

Better performance mainly from PTT LNG

Gain from divestment of BCP

Others

PTTEPImpairment loss on assets Avg. selling price decreased 29% significantly decreased from a slump on oil price Sales volume increased 3%

GasGSP and Industrial margin squeezed

better NGV performance NG Sale Volume increase 3% mainly from new IPPs & SPPs2

2015 Year in Review Performance 2016 Outlook

11,998 5,172

14,460 8,407 17,603

8,292

36,070 58,678

MMTHB

Margin

FX gainOPEX*

Share of

income

Int. & CIT exp.

Other Income

66%

19,936

Impairment

Y2014 Y2015

Y2015 = 75,881

Y2014 = 88,806

Operating performance

15%

PTTEP

PTT

OthersP&R

Impairment

Other extra items

PetrochemAvg. A/C GRM increased 369% Aromatics P2F improvedOlefins business declined from Polymer price dropped RefineryAvg. A/C GIM increased 174%Aggregate intake increased 10%

2015 Year in Review

Performance

2016 Outlook

13

2015 Year in Review Performance 2016 Outlook

Contents

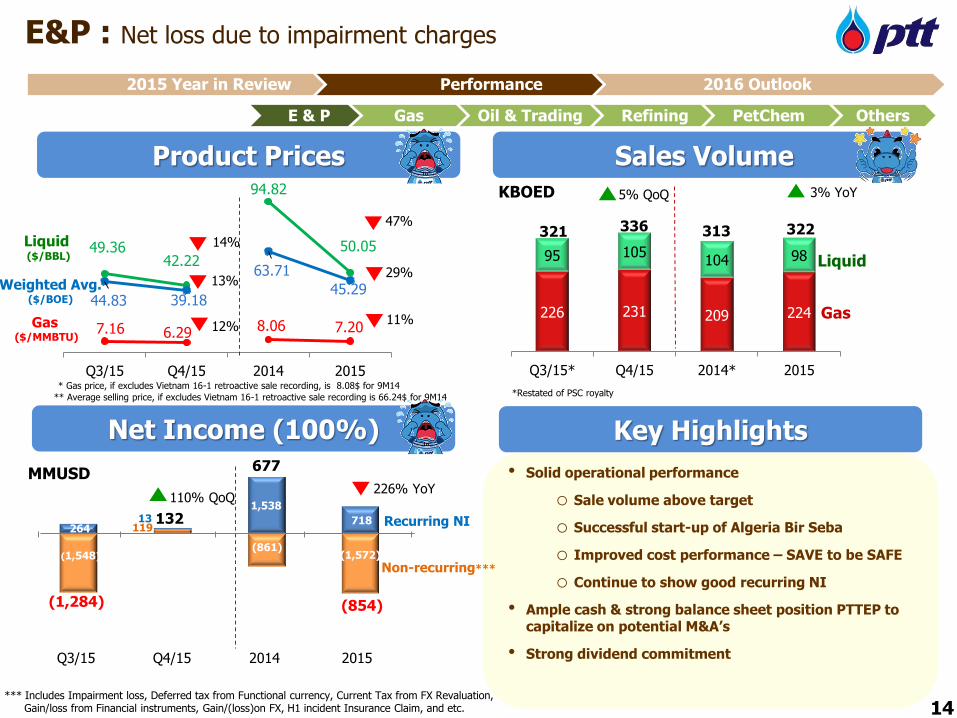

E&P : Net loss due to impairment charges

Product Prices

Net Income (100%)

Sales Volume

Key Highlights

7.16 6.29 8.06 7.20

49.3642.22

94.82

50.05

44.83 39.18

63.71

45.29

Q3/15 Q4/15 2014 2015

Liquid ($/BBL)

Gas($/MMBTU)

Weighted Avg.($/BOE)

MMUSD

226 231 209 224

95 105104 98

Q3/15* Q4/15 2014* 2015

336

Liquid

Gas

KBOED

321

14

* Gas price, if excludes Vietnam 16-1 retroactive sale recording, is 8.08$ for 9M14

** Average selling price, if excludes Vietnam 16-1 retroactive sale recording is 66.24$ for 9M14

313

Q4/15

14%

13%

3% YoY5% QoQ

2014

226% YoY110% QoQ

E & P Gas Oil & Trading Refining PetChem Others

12%

47%

29%

11%

322

2015

677

(854)(1,284)

132

*** Includes Impairment loss, Deferred tax from Functional currency, Current Tax from FX Revaluation, Gain/loss from Financial instruments, Gain/(loss)on FX, H1 incident Insurance Claim, and etc.

Q3/15

Non-recurring***

Recurring NI

*Restated of PSC royalty

• Solid operational performance

o Sale volume above target

o Successful start-up of Algeria Bir Seba

o Improved cost performance – SAVE to be SAFE

o Continue to show good recurring NI

• Ample cash & strong balance sheet position PTTEP to capitalize on potential M&A’s

• Strong dividend commitment

2015 Year in Review Performance 2016 Outlook

(1,548)(861)

(1,572)

718

1,53813

119264

15

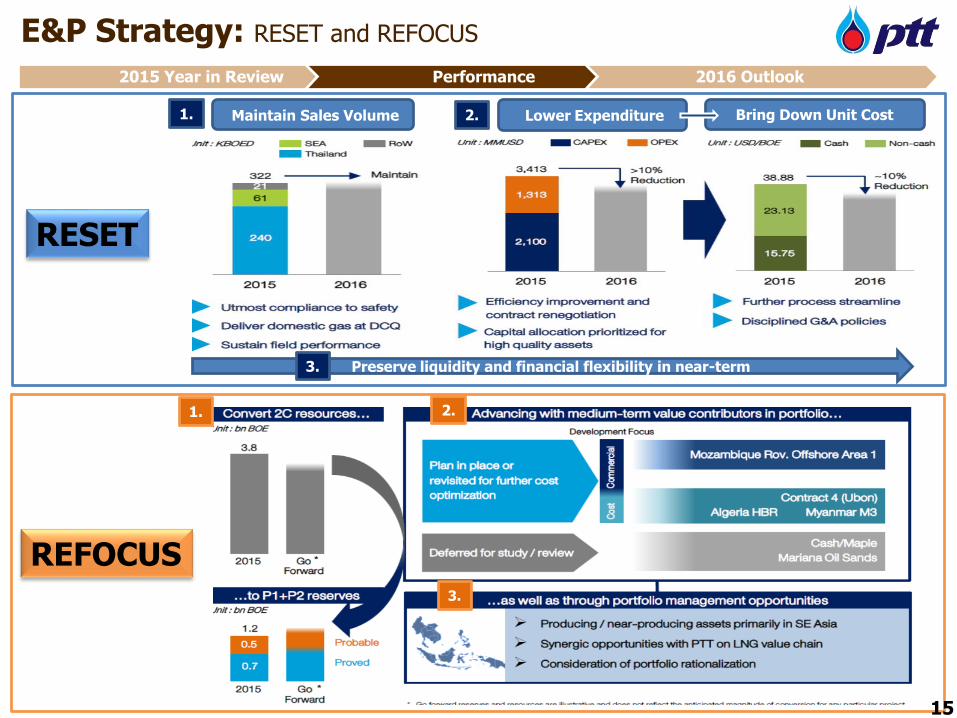

E&P Strategy: RESET and REFOCUS

2015 Year in Review Performance 2016 Outlook

RESET

REFOCUS

15

Maintain Sales Volume Lower Expenditure Bring Down Unit Cost

Preserve liquidity and financial flexibility in near-term

1. 2.

3.

1. 2.

3.

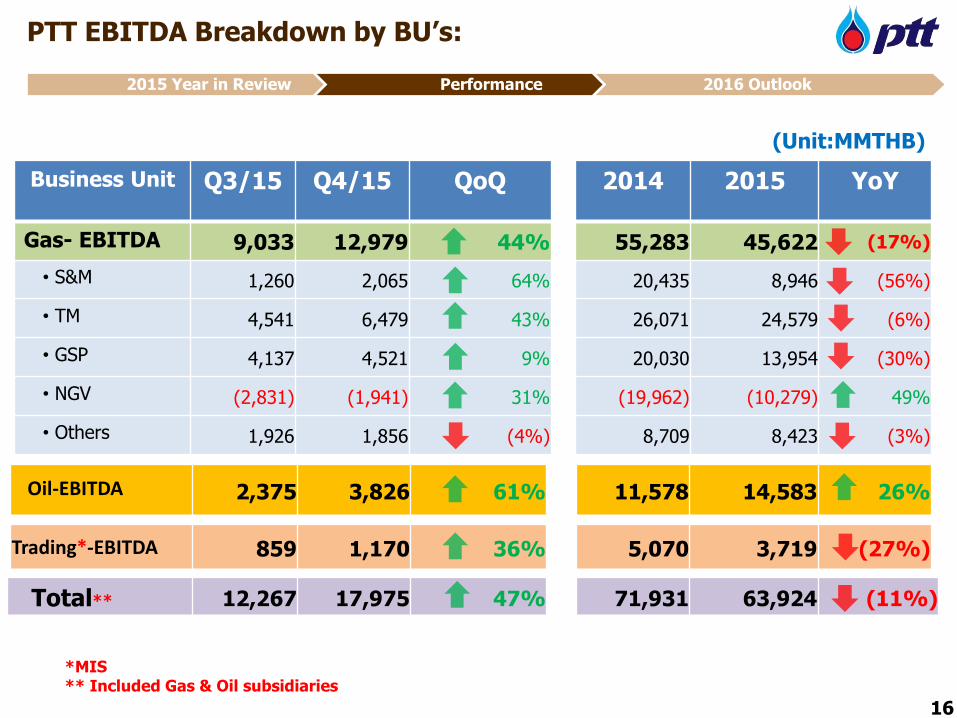

Business Unit Q3/15 Q4/15 QoQ 2014 2015 YoY

Gas- EBITDA 9,033 12,979 44% 55,283 45,622 (17%)

• S&M 1,260 2,065 64% 20,435 8,946 (56%)

• TM 4,541 6,479 43% 26,071 24,579 (6%)

• GSP 4,137 4,521 9% 20,030 13,954 (30%)

• NGV (2,831) (1,941) 31% (19,962) (10,279) 49%

• Others 1,926 1,856 (4%) 8,709 8,423 (3%)

(Unit:MMTHB)

2,375 3,826 61% 11,578 14,583 26%

859 1,170 36% 5,070 3,719 (27%)

*MIS** Included Gas & Oil subsidiaries

16

Oil-EBITDA

Trading*-EBITDA

Total** 12,267 17,975 47% 71,931 63,924 (11%)

PTT EBITDA Breakdown by BU’s:

2015 Year in Review Performance 2016 Outlook

8.6 9.2

8.6 8.5 8.5

7.9 7.3

6.6

610 607591

437

318377

265

217

-

100

200

300

400

500

600

700

5

7

9

11

13

15

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15

8.35

8.04

8.82

8.45

Q3/15 Q4/15 2014 2015

4% QoQ

1,105 1,075 1,206 1,151

1,067 971 852 995

765 721 699 740

949 1,008 959 961

636 632 655 656300 289 317 304

Q3/15 Q4/15 2014 2015

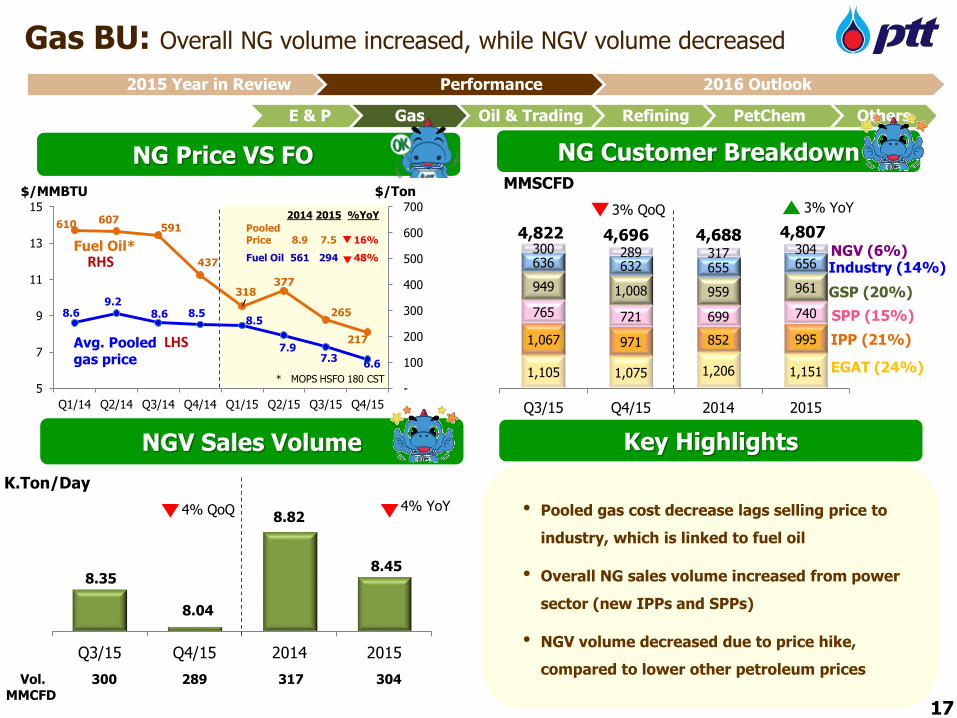

Gas BU: Overall NG volume increased, while NGV volume decreased

NG Price VS FO NG Customer Breakdown

$/MMBTU

EGAT (24%)

IPP (21%)

SPP (15%)

GSP (20%)

Industry (14%)NGV (6%)

MMSCFD

4,6884,822

3% YoY

NGV Sales Volume

Vol. MMCFD

300 289 317 304

• Pooled gas cost decrease lags selling price to

industry, which is linked to fuel oil

• Overall NG sales volume increased from power

sector (new IPPs and SPPs)

• NGV volume decreased due to price hike,

compared to lower other petroleum prices

Key Highlights

4,807

3% QoQ

ที่เพ่ิมข้ึนเป็นของ

K.Ton/Day

17

4% YoY

E & P Gas Oil & Trading Refining PetChem Others

4,696

2015 Year in Review Performance 2016 Outlook

$/Ton

Fuel Oil*

* MOPS HSFO 180 CST

Avg. Pooled gas price

LHS

RHS

2014 2015 %YoY

Pooled Price 8.9 7.5 16%

Fuel Oil 561 294 48%

2014 2015 %YoY

HDPE 1,545 1,238 -20%

LPG Ex-GSP 333 463 39%

Naphtha 786 438 -44%

Feed Cost 389 349 -10%Propane (12%)

858 876 832

577 444 505

405 399

1,375 1,234 1,576

1,266

1,188

1,375 1,234

1,153

333 333 333 333

443 497

470 440 389 394 391 382

380 359 352 310

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15

1,260 2,065

20,435 8,946 4,541 6,479

26,071

24,579

4,137 4,521

20,030

13,954

(2,831) (1,941) (19,962)(10,279)

1,926 1,855

8,709

8,422

Gas - EBITDA

MMTHB

Others

TM

GSP

12,9799,033

S&M

NGV

652 803

2,739 2,738

171 171

728 695

548 604

2,106 2,199

211 128

819 765

9 4

026

Q3/15 Q4/15 2014 2015

1,710

GSP Sales Volume

LPG (43%)

kTon

1,591

6,392

7% QoQ

0.5% YoY

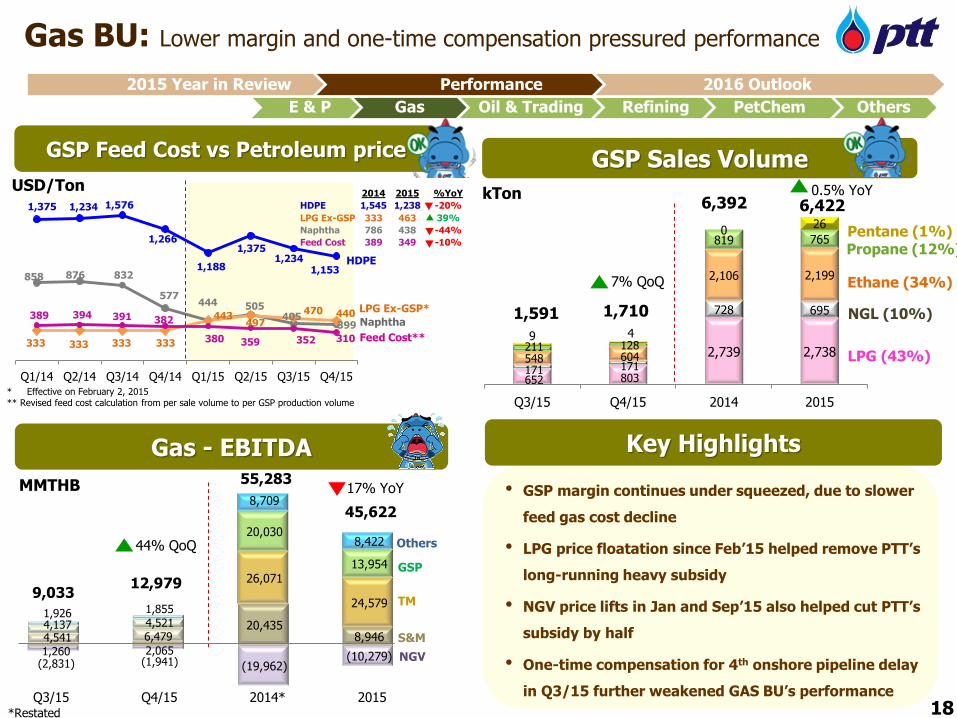

Gas BU: Lower margin and one-time compensation pressured performance

NGL (10%)

Ethane (34%)

Key Highlights

44% QoQ

GSP Feed Cost vs Petroleum price

Naphtha

USD/Ton

Feed Cost**

LPG Ex-GSP*

* Effective on February 2, 2015** Revised feed cost calculation from per sale volume to per GSP production volume

55,283

Pentane (1%)

17% YoY

E & P Gas Oil & Trading Refining PetChem Others

6,422

45,622

18

HDPE

*Restated

Q3/15 Q4/15 2014* 2015

• GSP margin continues under squeezed, due to slower

feed gas cost decline

• LPG price floatation since Feb’15 helped remove PTT’s

long-running heavy subsidy

• NGV price lifts in Jan and Sep’15 also helped cut PTT’s

subsidy by half

• One-time compensation for 4th onshore pipeline delay

in Q3/15 further weakened GAS BU’s performance

2015 Year in Review Performance 2016 Outlook

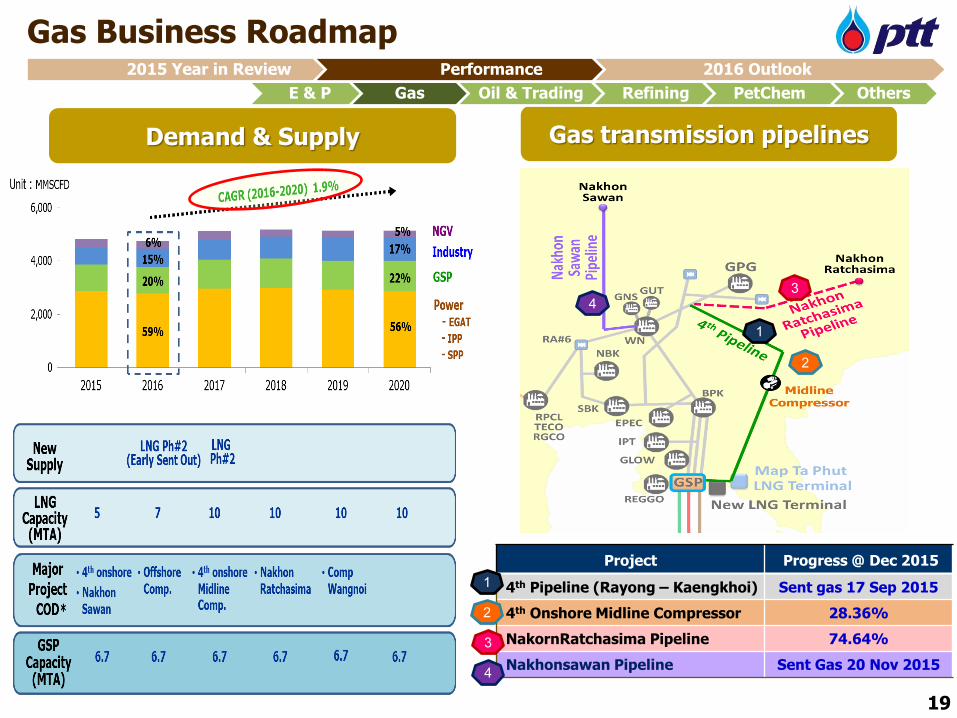

Gas Business Roadmap

Gas transmission pipelinesDemand & Supply

19

E & P Gas Oil & Trading Refining PetChem Others

2015 Year in Review Performance 2016 Outlook

34

1

2

Project Progress @ Dec 2015

4th Pipeline (Rayong – Kaengkhoi) Sent gas 17 Sep 2015

4th Onshore Midline Compressor 28.36%

NakornRatchasima Pipeline 74.64%

Nakhonsawan Pipeline Sent Gas 20 Nov 2015

3

4

1

2

0.0

0.2

0.4

0.6

Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-150

5

10

15

Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

Avg. Sales Vol. (K.Ton/day)Price (THB/Kg)

Industry Auto Household

-50

-40

-30

-20

-10

0

10

20

30

40

0

1,000

2,000

3,000

Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

Sales vol. Export Price (RHS)

-200

-150

-100

-50

0

50

0

500

1,000

Jul-14 Oct-14 Jan-15 Apr-15 Jul-15 Oct-15

Sales Vol. Export Price (RHS)

2015

20

Avg. Price

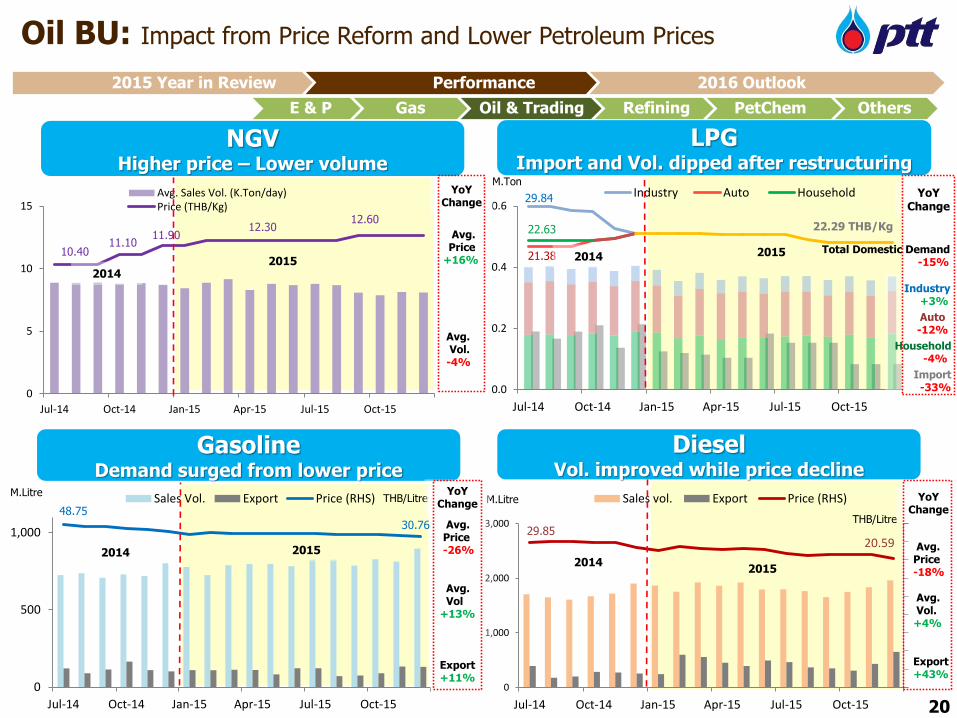

+16%

Avg.Vol.

-4%

E & P Gas Oil & Trading Refining PetChem Others

Oil BU: Impact from Price Reform and Lower Petroleum Prices

NGV Higher price – Lower volume

M.Ton

DieselVol. improved while price decline

GasolineDemand surged from lower price

M.Litre

THB/Litre48.75

30.7629.85

20.59

10.40

12.30

M.LitreTHB/Litre

29.84

21.38

22.6311.10

11.90

LPG Import and Vol. dipped after restructuring

Avg. Price-26%

Avg.Vol

+13%

Export +11%

Avg. Price -18%

Avg.Vol.

+4%

Export +43%

22.29 THB/Kg

Industry +3%

Auto-12%

Household -4%

Import -33%

Total Domestic Demand -15%

12.60

YoYChange

YoYChange

YoYChange

YoYChange

2015

20152015

2014

2014

2014

2014

2015 Year in Review Performance 2016 Outlook

6,157 6,511

25,268

Q3/15 Q4/15 2014 2015

24,657

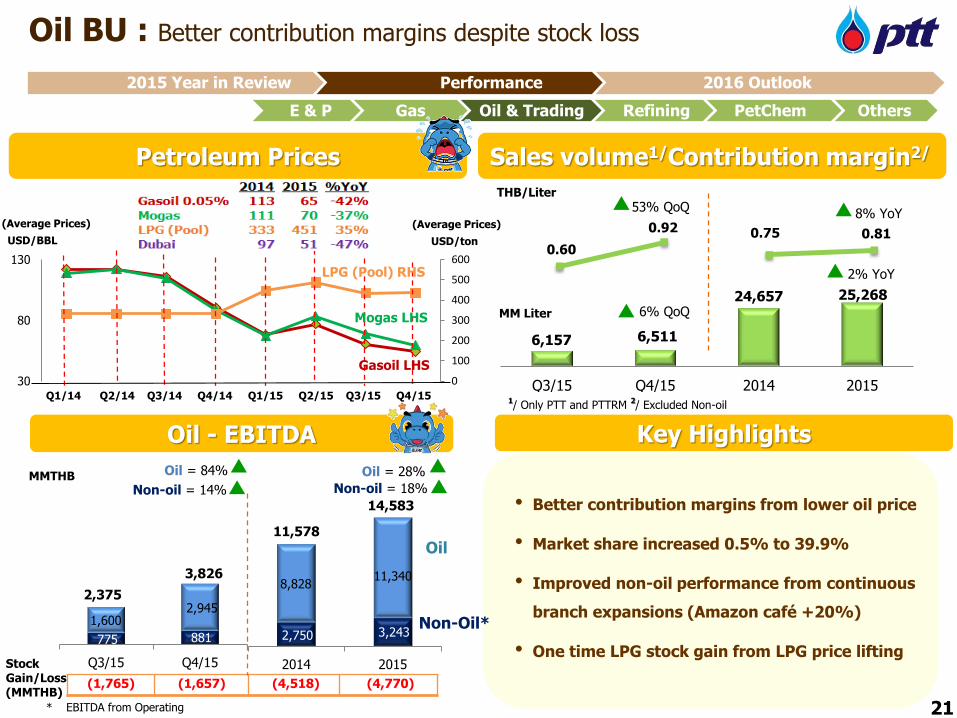

• Better contribution margins from lower oil price

• Market share increased 0.5% to 39.9%

• Improved non-oil performance from continuous

branch expansions (Amazon café +20%)

• One time LPG stock gain from LPG price lifting

0.60

0.92 0.75 0.81

2,750 3,243

8,828 11,340

2014 2015

11,578

14,583

Oil BU : Better contribution margins despite stock loss

MMTHB

THB/Liter

21

Oil

Non-Oil*

E & P Gas Oil & Trading Refining PetChem Others

* EBITDA from Operating

Sales volume1/Contribution margin2/

MM Liter

1/ Only PTT and PTTRM

2/ Excluded Non-oil

8% YoY

2% YoY

Oil = 28%

(1,765) (1,657) (4,518) (4,770)

Petroleum Prices

Stock Gain/Loss(MMTHB)

53% QoQ

6% QoQ

Oil - EBITDA

USD/BBL

(Average Prices)

Oil = 84%

0

100

200

300

400

500

600

30

80

130

Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15

2015 Year in Review Performance 2016 Outlook

Key Highlights

Non-oil = 18%Non-oil = 14%

USD/ton

(Average Prices)

Mogas LHS

Gasoil LHS

LPG (Pool) RHS

775 881

1,600 2,945

Q3/15 Q4/15

2,375

3,826

E & P Gas Oil & Trading Refining PetChem Others

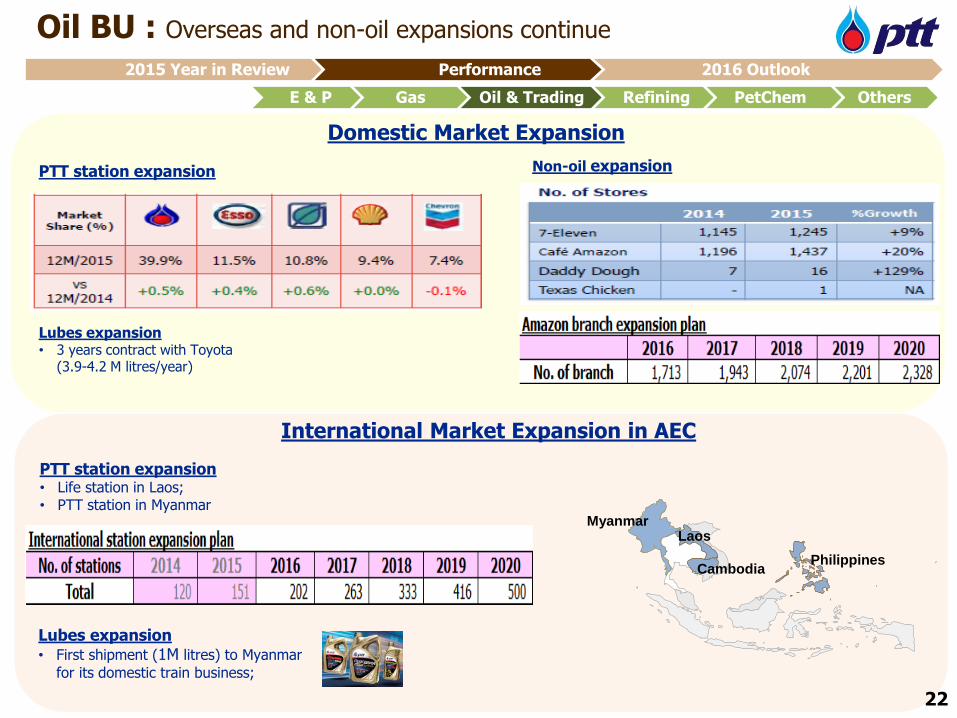

Oil BU : Overseas and non-oil expansions continue

22

Laos

CambodiaPhilippines

Myanmar

International Market Expansion in AEC

Domestic Market Expansion

Thailand

2015 Year in Review Performance 2016 Outlook

Lubes expansion• First shipment (1M litres) to Myanmar

for its domestic train business;

Lubes expansion• 3 years contract with Toyota

(3.9-4.2 M litres/year)

PTT station expansion• Life station in Laos;• PTT station in Myanmar

PTT station expansion Non-oil expansion

49.58 46.29

96.63

52.74

50% QoQ

0.06

0.09 0.10

0.07

Q3/15 Q4/15 2014 2015

30% YoY

* PTT only : FX Adjusted

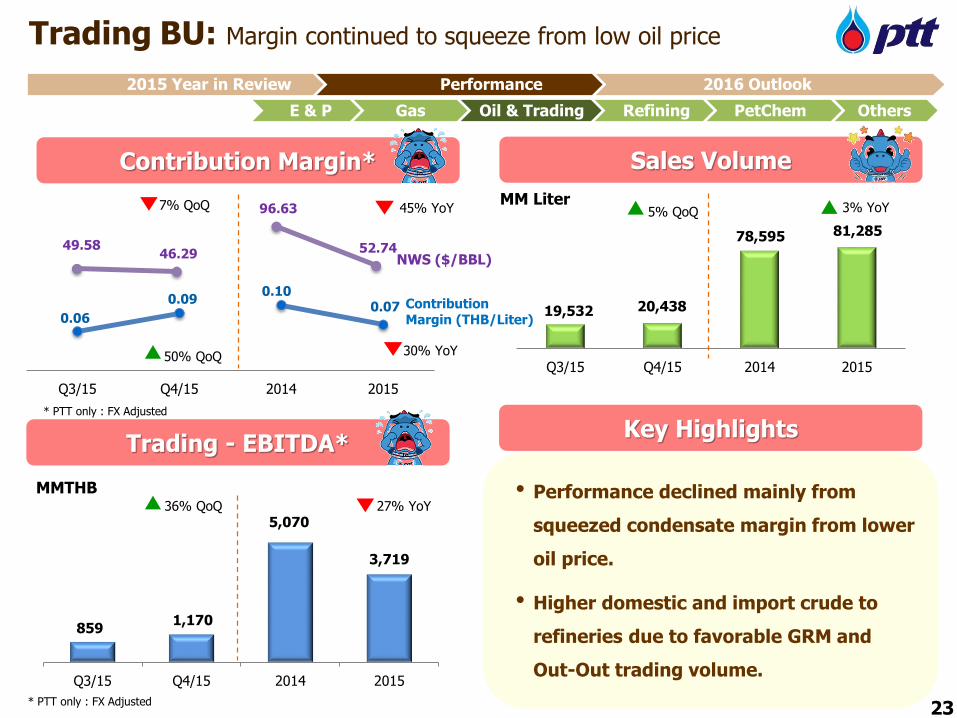

859 1,170

5,070

3,719

Q3/15 Q4/15 2014 2015

19,532 20,438

78,595 81,285

Q3/15 Q4/15 2014 2015

5% QoQ

Trading BU: Margin continued to squeeze from low oil price

Contribution Margin*

Trading - EBITDA*

Sales Volume

Key Highlights

MMTHB

MM Liter

23

* PTT only : FX Adjusted

27% YoY

E & P Gas Oil & Trading Refining PetChem Others

Contribution Margin (THB/Liter)

NWS ($/BBL)

45% YoY 3% YoY7% QoQ

36% QoQ• Performance declined mainly from

squeezed condensate margin from lower

oil price.

• Higher domestic and import crude to

refineries due to favorable GRM and

Out-Out trading volume.

2015 Year in Review Performance 2016 Outlook

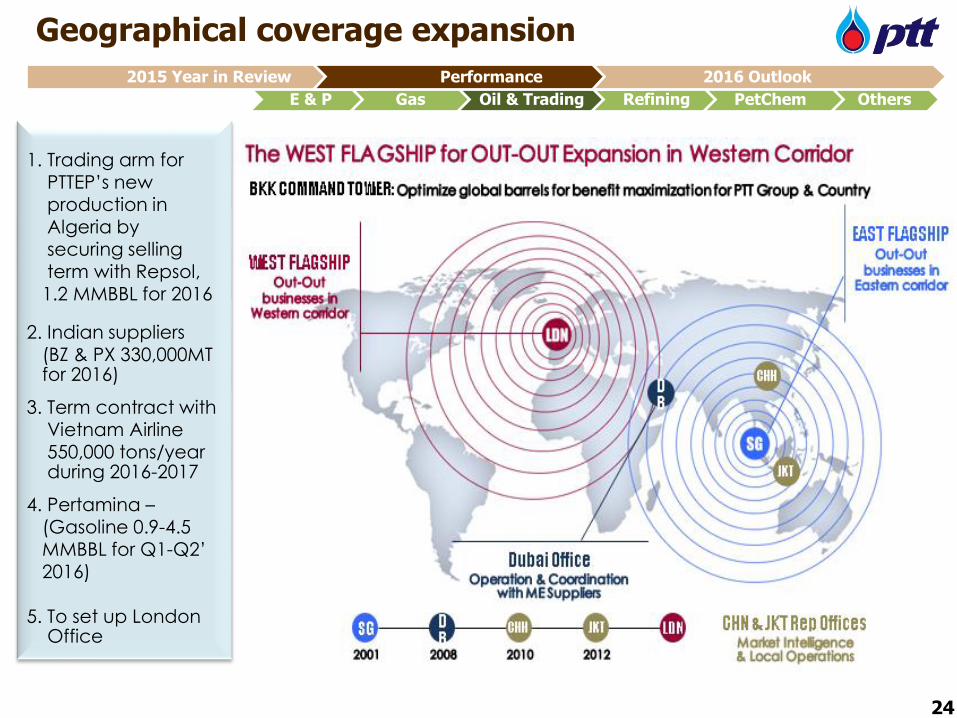

Geographical coverage expansion

24

E & P Gas Oil & Trading Refining PetChem Others

2015 Year in Review Performance 2016 Outlook

1. Trading arm for PTTEP’s new production in Algeria by securing selling term with Repsol, 1.2 MMBBL for 2016

2. Indian suppliers

(BZ & PX 330,000MT for 2016)

3. Term contract with Vietnam Airline 550,000 tons/year during 2016-2017

4. Pertamina –(Gasoline 0.9-4.5 MMBBL for Q1-Q2’ 2016)

5. To set up London Office

Stock gain/lossnet NRV

7,997 13,474

28,792

45,428

(10,013) (7,304)

(43,822)

(13,556)

Q3/15 Q4/15 2014 2015

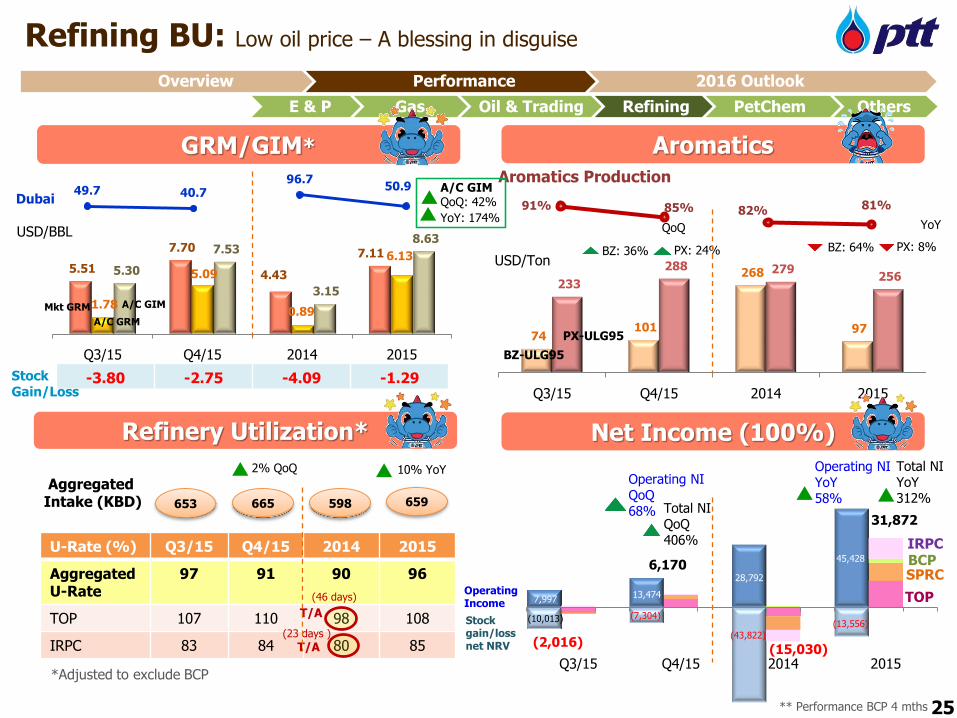

91% 85% 82% 81%

** Performance BCP 4 mths

74 101

268

97

233

288 279 256

Q3/15 Q4/15 2014 2015

49.7 40.796.7

50.9

5.51

7.70

4.43

7.11

1.78

5.09

0.89

6.13

5.30

7.53

3.15

8.63

Q3/15 Q4/15 2014 2015

GRM/GIM*

Refinery Utilization*

USD/BBL

A/C GRM

A/C GIMMkt GRM

Dubai

Net Income (100%)

U-Rate (%) Q3/15 Q4/15 2014 2015

Aggregated U-Rate

97 91 90 96

TOP 107 110 98 108

IRPC 83 84 80 85

Aggregated Intake (KBD) 665653

2% QoQ

598

AromaticsAromatics Production

BZ-ULG95

PX-ULG95

Refining BU: Low oil price – A blessing in disguise

25

BZ: 36%

QoQ

PX: 24%

-3.80 -2.75 -4.09 -1.29StockGain/Loss

T/A(23 days )

BZ: 64%

YoY

PX: 8%

E & P Gas Oil & Trading Refining PetChem Others

USD/Ton

659

10% YoY Total NIYoY312%

T/A

(46 days)

*Adjusted to exclude BCP

IRPC

TOP

SPRCBCP6,170

(2,016)

31,872Total NIQoQ406%

OperatingIncome

Operating NIYoY58%

Operating NIQoQ68%

A/C GIMQoQ: 42%

YoY: 174%

(15,030)

Overview Performance 2016 Outlook

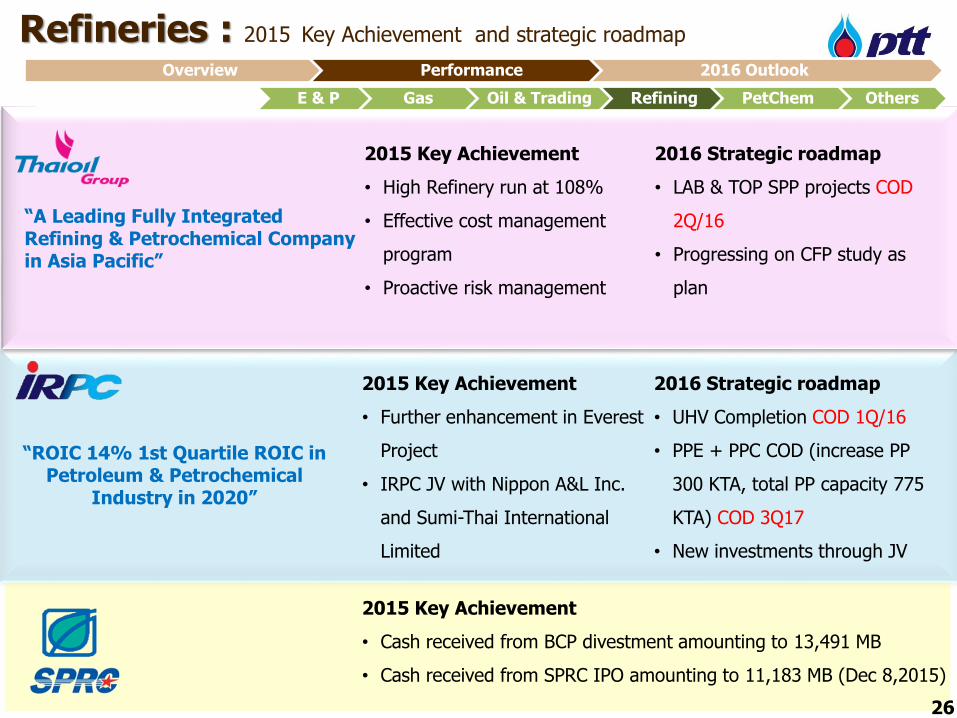

Refineries : 2015 Key Achievement and strategic roadmap

E & P Gas Oil & Trading Refining PetChem Others

Overview Performance 2016 Outlook

“ROIC 14% 1st Quartile ROIC in Petroleum & Petrochemical

Industry in 2020”

2015 Key Achievement

• Cash received from BCP divestment amounting to 13,491 MB

• Cash received from SPRC IPO amounting to 11,183 MB (Dec 8,2015)

2015 Key Achievement

• High Refinery run at 108%

• Effective cost management

program

• Proactive risk management

2016 Strategic roadmap

• LAB & TOP SPP projects COD

2Q/16

• Progressing on CFP study as

plan

2015 Key Achievement

• Further enhancement in Everest

Project

• IRPC JV with Nippon A&L Inc.

and Sumi-Thai International

Limited

2016 Strategic roadmap

• UHV Completion COD 1Q/16

• PPE + PPC COD (increase PP

300 KTA, total PP capacity 775

KTA) COD 3Q17

• New investments through JV

“A Leading Fully Integrated Refining & Petrochemical Company in Asia Pacific”

26

27

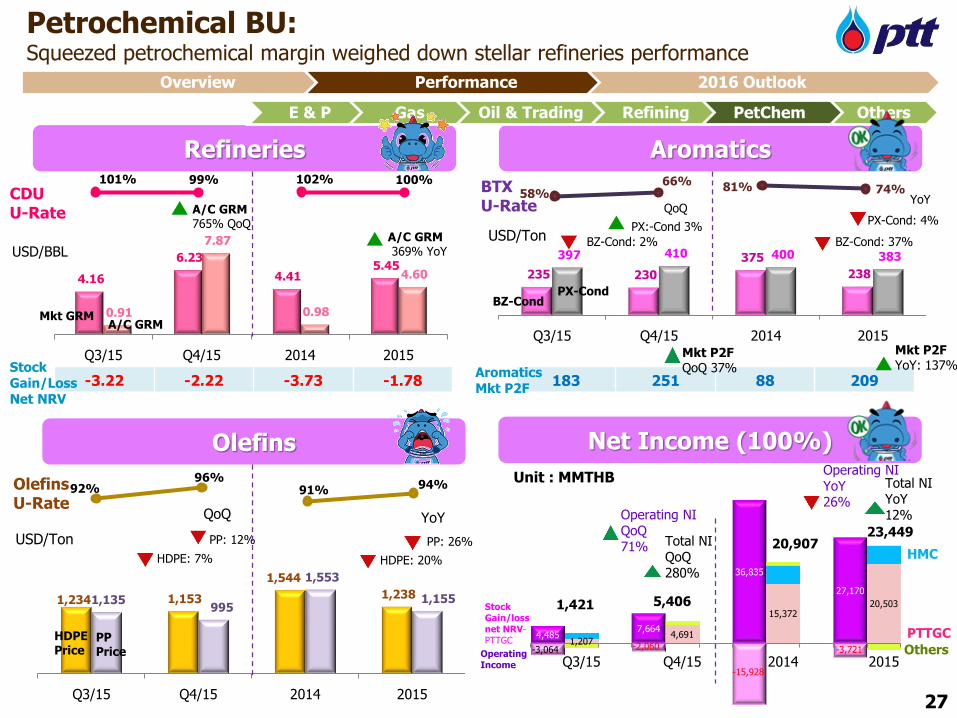

4.16

6.23

4.41 5.45

0.91

7.87

0.98

4.60

Q3/15 Q4/15 2014 2015

101% 99% 102% 100%58%

66% 81% 74%

1,234 1,153

1,544

1,238 1,135 995

1,553

1,155

Q3/15 Q4/15 2014 2015

235 230

375

238

397 410 400 383

Q3/15 Q4/15 2014 2015

Net Income (100%)

Aromatics

Unit : MMTHB

4,4851,207

7,6644,691

36,835

15,372

27,170

20,503

-3,064 -2,060

-15,928

-3,721

Q3/15 Q4/15 2014 2015

PTTGC

HMC

Others

5,406

Olefins U-Rate

92%96%

91% 94%

Olefins

USD/Ton

BTXU-Rate

Refineries

CDU U-Rate

A/C GRMMkt GRM

BZ-CondPX-Cond

-3.22 -2.22 -3.73 -1.78StockGain/LossNet NRV

Petrochemical BU: Squeezed petrochemical margin weighed down stellar refineries performance

1,421

HDPEPrice

PPPrice

HDPE: 7%

QoQ

PP: 12%

BZ-Cond: 2%

QoQ

PX:-Cond 3%

BZ-Cond: 37%

YoY

PX-Cond: 4%

HDPE: 20%

YoY

PP: 26%

E & P Gas Oil & Trading Refining PetChem Others

183 251 88 209

USD/TonUSD/BBL

Mkt P2FQoQ 37%Aromatics

Mkt P2F

A/C GRM 765% QoQ

Mkt P2FYoY: 137%

20,90723,449

Total NIYoY12%

Total NIQoQ280%

Operating Income

Stock Gain/loss net NRV-PTTGC

Operating NI YoY26%

Operating NI QoQ71%

A/C GRM 369% YoY

Overview Performance 2016 Outlook

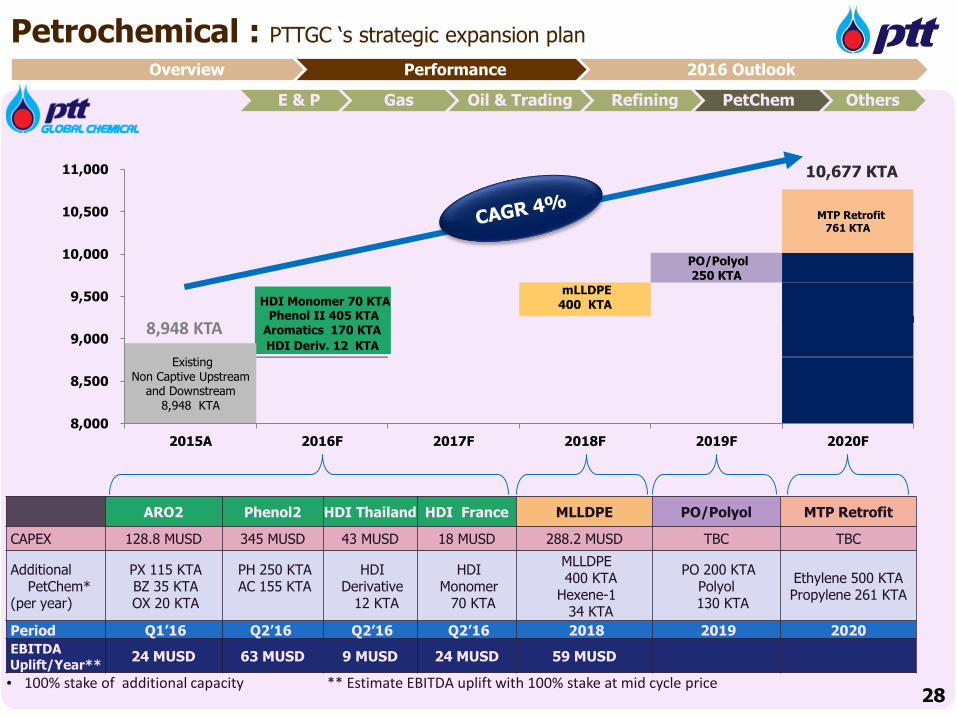

ARO2 Phenol2 HDI Thailand HDI France MLLDPE PO/Polyol MTP Retrofit

CAPEX 128.8 MUSD 345 MUSD 43 MUSD 18 MUSD 288.2 MUSD TBC TBC

Additional PetChem*

(per year)

PX 115 KTA BZ 35 KTAOX 20 KTA

PH 250 KTAAC 155 KTA

HDI Derivative

12 KTA

HDI Monomer

70 KTA

MLLDPE 400 KTA

Hexene-1 34 KTA

PO 200 KTAPolyol 130 KTA

Ethylene 500 KTAPropylene 261 KTA

Period Q1’16 Q2’16 Q2’16 Q2’16 2018 2019 2020

EBITDA Uplift/Year**

24 MUSD 63 MUSD 9 MUSD 24 MUSD 59 MUSD

• 100% stake of additional capacity ** Estimate EBITDA uplift with 100% stake at mid cycle price

Petrochemical : PTTGC ‘s strategic expansion plan

E & P Gas Oil & Trading Refining PetChem Others

Overview Performance 2016 Outlook

Existing Non Captive Upstream

and Downstream8,948 KTA

HDI Deriv. 12 KTA

Phenol II 405 KTAAromatics 170 KTA

HDI Monomer 70 KTAmLLDPE

400 KTA

PO/Polyol 250 KTA

MTP Retrofit761 KTA

8,000

8,500

9,000

9,500

10,000

10,500

11,000

2015A 2016F 2017F 2018F 2019F 2020F

8,948 KTA

10,677 KTA

28

(5)

(149)(149)

24 9

(154)

49

(125)

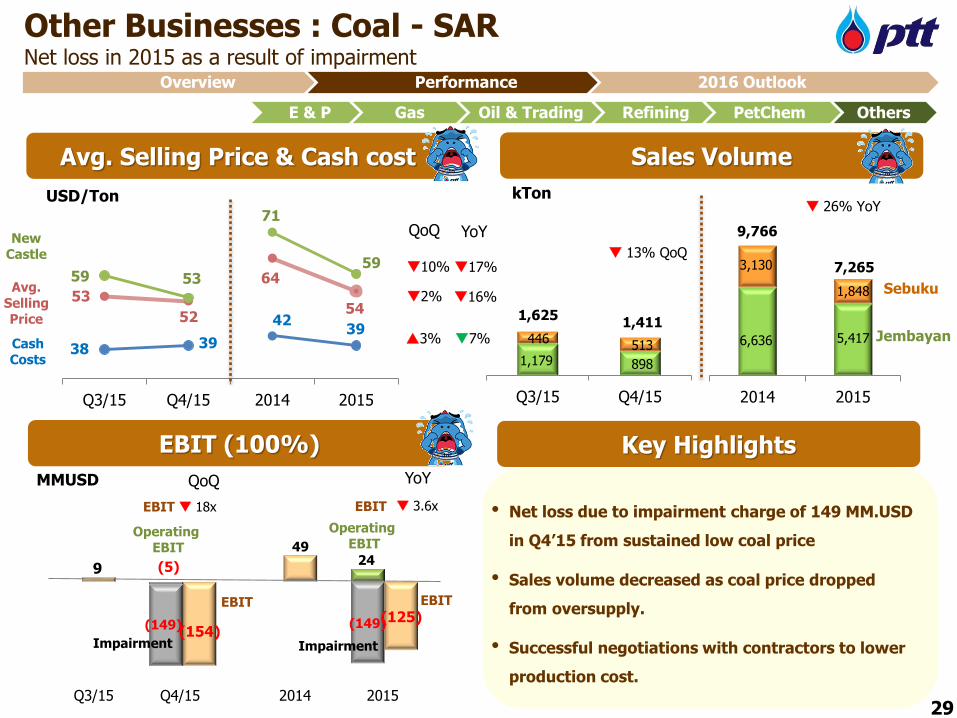

Other Businesses : Coal - SAR Net loss in 2015 as a result of impairment

EBIT (100%)

Sales Volume

Key Highlights

MMUSD

USD/Ton

6,636 5,417

3,130

1,848

9,766

7,265

2014 2015

kTon

Jembayan

SebukuAvg. Selling Price

Cash Costs

13% QoQ

Avg. Selling Price & Cash cost

New Castle

2%

26% YoY

3.6x

Q3/15 Q4/15 2014 2015

Impairment

10%

3%

16%

17%

7%

•

29

EBIT 18x

QoQ YoY

YoYQoQ

E & P Gas Oil & Trading Refining PetChem Others

53

52

64

54

38 39

4239

59 53

71

59

Q3/15 Q4/15 2014 2015

Impairment

EBIT • Net loss due to impairment charge of 149 MM.USD

in Q4’15 from sustained low coal price

• Sales volume decreased as coal price dropped

from oversupply.

• Successful negotiations with contractors to lower

production cost.

Overview Performance 2016 Outlook

1,179 898

446 513

1,625 1,411

Q3/15 Q4/15

Operating EBIT

Operating EBIT

EBITEBIT

1,038 1,076

5,422 5,582

1,117 1,288

4,981 4,893

Q3/15 Q4/15 2014 2015

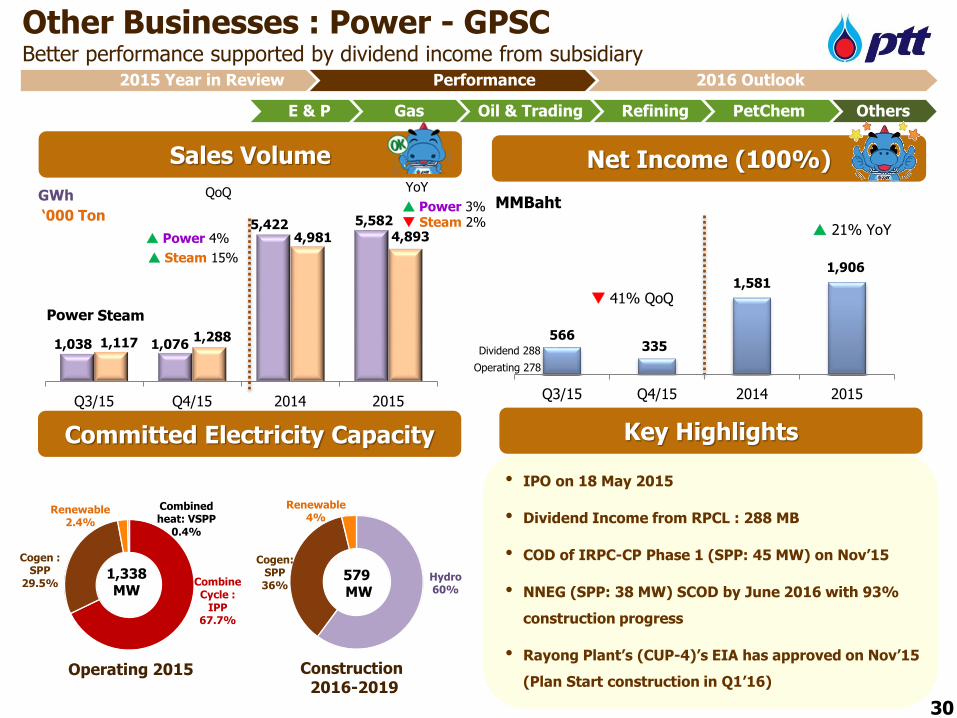

Net Income (100%)Sales Volume

Key Highlights

MMBahtGWh

Other Businesses : Power - GPSCBetter performance supported by dividend income from subsidiary

‘000 Ton

E & P Gas Oil & Trading Refining PetChem Others

Committed Electricity Capacity

Power Steam

30

QoQ YoY

Power 3%

Steam 15%

Steam 2%

Power 4%

566335

1,5811,906

Q3/15 Q4/15 2014 2015

21% YoY

41% QoQ

Operating 278

Dividend 288

Combine Cycle :

IPP67.7%

Cogen : SPP

29.5%

Renewable2.4%

Combined heat: VSPP

0.4%

Hydro60%

Cogen: SPP36%

Renewable4%

• IPO on 18 May 2015

• Dividend Income from RPCL : 288 MB

• COD of IRPC-CP Phase 1 (SPP: 45 MW) on Nov’15

• NNEG (SPP: 38 MW) SCOD by June 2016 with 93%

construction progress

• Rayong Plant’s (CUP-4)’s EIA has approved on Nov’15

(Plan Start construction in Q1’16)

2015 Year in Review Performance 2016 Outlook

Construction 2016-2019

Operating 2015

1,338 MW

579MW

99%

GA, 1%

Shareholding

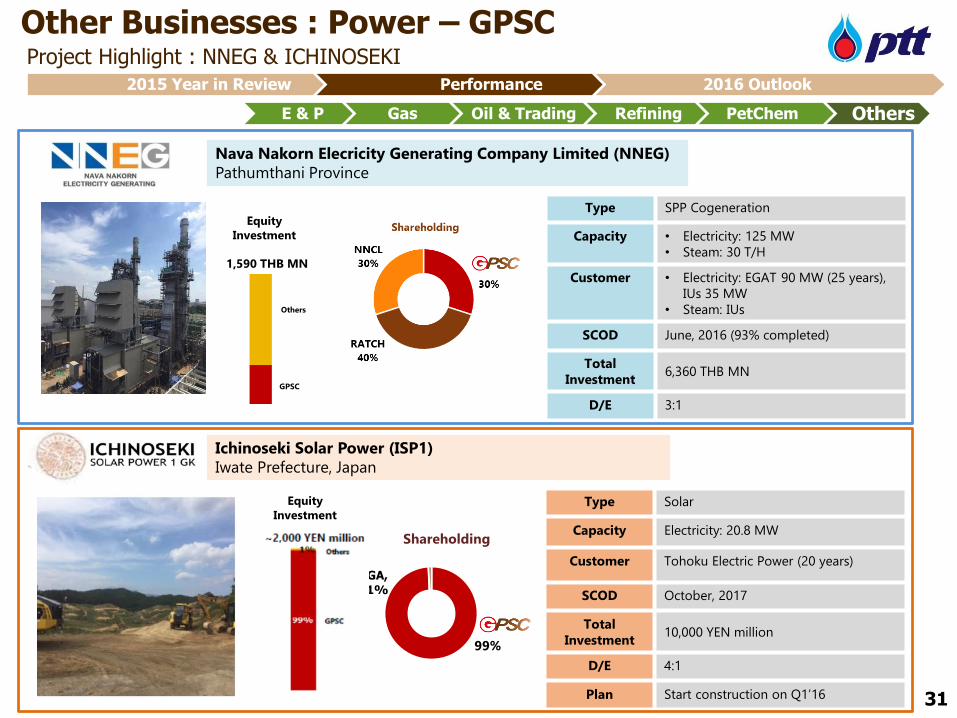

Other Businesses : Power – GPSC Project Highlight : NNEG & ICHINOSEKI

E & P Gas Oil & Trading Refining PetChem Others

31

Ichinoseki Solar Power (ISP1)

Iwate Prefecture, Japan

Type Solar

Capacity Electricity: 20.8 MW

Customer Tohoku Electric Power (20 years)

SCOD October, 2017

Total

Investment10,000 YEN million

D/E 4:1

Plan Start construction on Q1’16

Equity

Investment

2015 Year in Review Performance 2016 Outlook

Nava Nakorn Elecricity Generating Company Limited (NNEG)

Pathumthani Province

Equity

Investment

1,590 THB MN

GPSC

Others

Type SPP Cogeneration

Capacity • Electricity: 125 MW

• Steam: 30 T/H

Customer • Electricity: EGAT 90 MW (25 years),

IUs 35 MW

• Steam: IUs

SCOD June, 2016 (93% completed)

Total

Investment6,360 THB MN

D/E 3:1

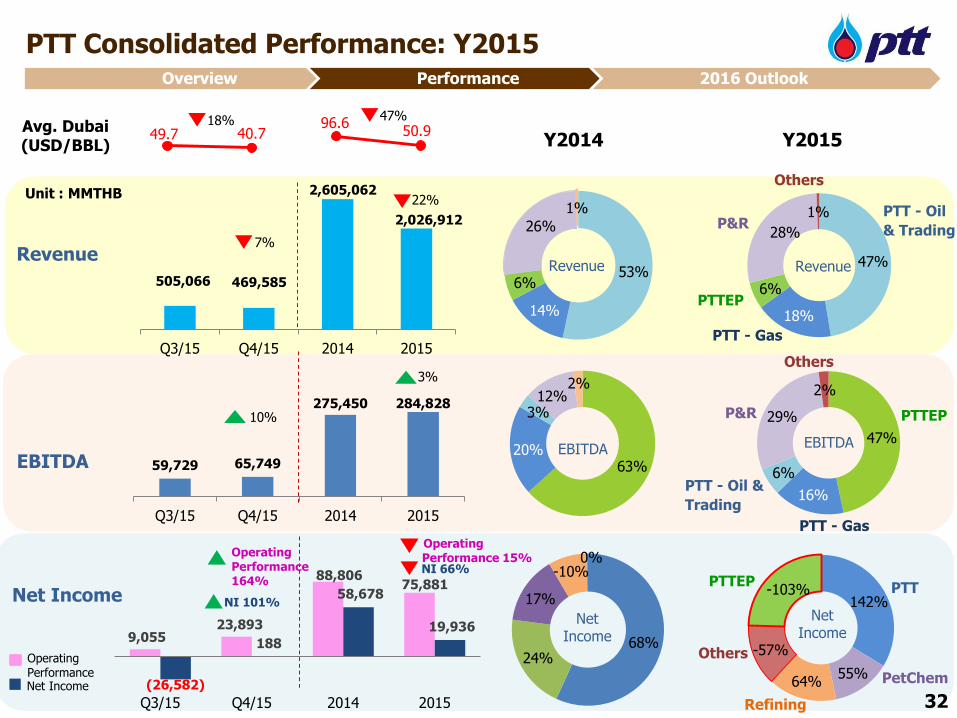

9,055 23,893

88,806 75,881

(26,582)

188

58,678

19,936

Q3/15 Q4/15 2014 2015

47%

18%

6%

28%

1% PTT - Oil

& Trading

PTT - Gas

Others

PTTEP

49.7 40.796.6

50.9

PTT Consolidated Performance: Y2015

Avg. Dubai (USD/BBL) Y2015Y2014

68%24%

17%

-10%0%

47%

16%

6%

29%

2%

PTT - Oil &

Trading

PTT - Gas

Others

PTTEP

505,066 469,585

2,605,062

2,026,912

Q3/15 Q4/15 2014 2015

142%

55%64%

-57%

-103% PTT

PetChem

Others

PTTEP

Refining

Net Income

Unit : MMTHB

EBITDA

Net Income

RevenueRevenue

EBITDA

53%

14%

6%

26%

1%

63%20%

3%12%

2%

Revenue

EBITDA

Net Income

59,729 65,749

275,450 284,828

Q3/15 Q4/15 2014 2015

32

P&R

P&R

22%

7%

10%

3%

NI 101%

18% 47%

NI 66%

Operating PerformanceNet Income

Overview Performance 2016 Outlook

Operating Performance 164%

Operating Performance 15%

33

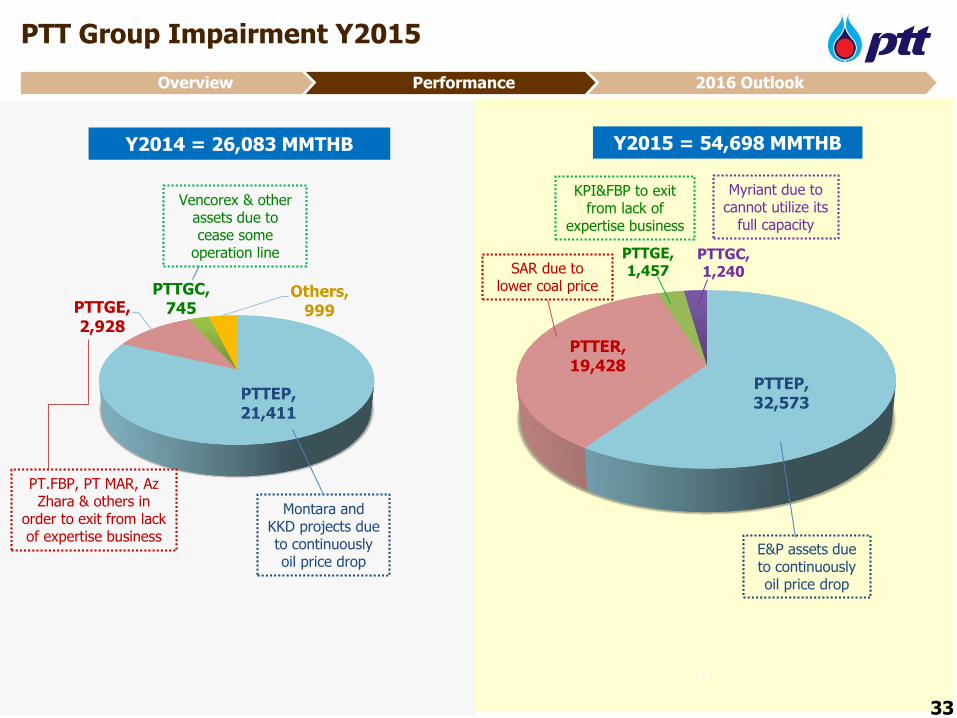

PTT Group Impairment Y2015

Overview Performance 2016 Outlook

33

Y2015 = 54,698 MMTHBY2014 = 26,083 MMTHB

PTTEP, 21,411

PTTGE, 2,928

PTTGC, 745

Others, 999

PTTEP, 32,573

PTTER, 19,428

PTTGE, 1,457

PTTGC, 1,240

Montara and KKD projects due to continuously oil price drop

Vencorex & other assets due to cease some

operation line

PT.FBP, PT MAR, AzZhara & others in

order to exit from lack of expertise business

E&P assets due to continuously oil price drop

KPI&FBP to exit from lack of

expertise business

Myriant due to cannot utilize its

full capacity

SAR due to lower coal price

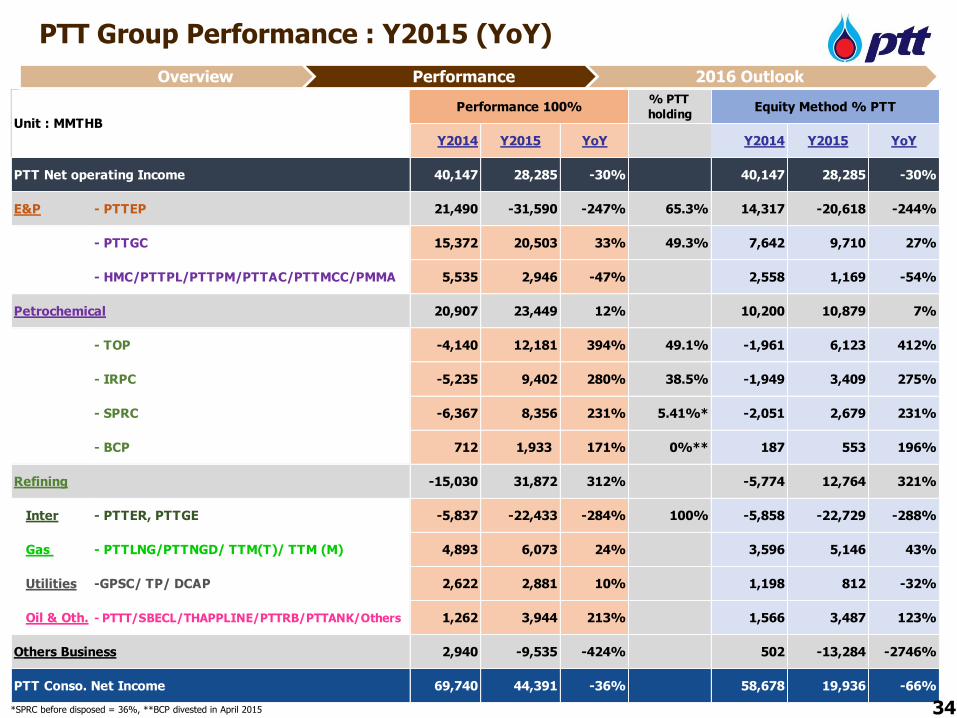

PTT Group Performance : Y2015 (YoY)

% PTT

holding

Y2014 Y2015 YoY Y2014 Y2015 YoY

PTT Net operating Income 40,147 28,285 -30% 40,147 28,285 -30%

E&P - PTTEP 21,490 -31,590 -247% 65.3% 14,317 -20,618 -244%

- PTTGC 15,372 20,503 33% 49.3% 7,642 9,710 27%

- HMC/PTTPL/PTTPM/PTTAC/PTTMCC/PMMA 5,535 2,946 -47% 2,558 1,169 -54%

Petrochemical 20,907 23,449 12% 10,200 10,879 7%

- TOP -4,140 12,181 394% 49.1% -1,961 6,123 412%

- IRPC -5,235 9,402 280% 38.5% -1,949 3,409 275%

- SPRC -6,367 8,356 231% 5.41%* -2,051 2,679 231%

- BCP 712 1,933 171% 0%** 187 553 196%

Refining -15,030 31,872 312% -5,774 12,764 321%

Inter - PTTER, PTTGE -5,837 -22,433 -284% 100% -5,858 -22,729 -288%

Gas - PTTLNG/PTTNGD/ TTM(T)/ TTM (M) 4,893 6,073 24% 3,596 5,146 43%

Utilities -GPSC/ TP/ DCAP 2,622 2,881 10% 1,198 812 -32%

Oil & Oth. - PTTT/SBECL/THAPPLINE/PTTRB/PTTANK/Others 1,262 3,944 213% 1,566 3,487 123%

Others Business 2,940 -9,535 -424% 502 -13,284 -2746%

PTT Conso. Net Income 69,740 44,391 -36% 58,678 19,936 -66%

Equity Method % PTTPerformance 100%

Unit : MMTHB

34

Overview Performance 2016 Outlook

*SPRC before disposed = 36%, **BCP divested in April 2015

0.390.29

1.50

1.10

0.00

0.50

1.00

1.50

2.00

(0.1)

0.1

0.3

0.5

0.7

0.9

2014 2015

Other Liabilities

PP&E

Others Non-

currentAssets

OtherCurrentAssets

L/TLiabilities(incl. due within 1 yr)

TotalEquity

MMTHB

Cash & S/T Invest

31 Dec 13 30 Sep 14

1,805,041 1,818,746

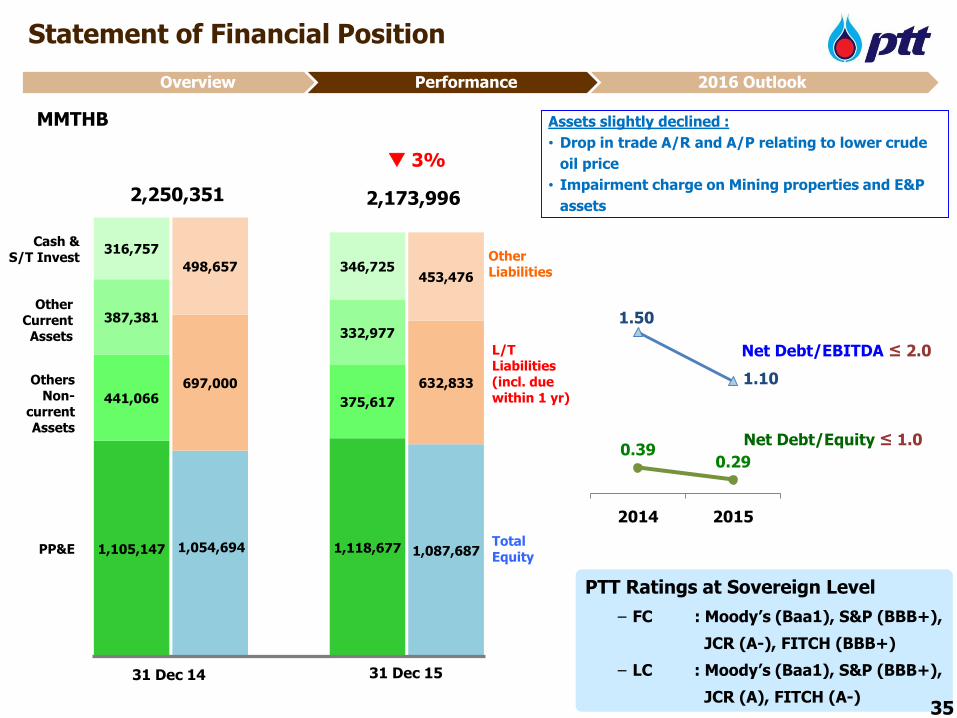

Statement of Financial Position

PTT Ratings at Sovereign Level

− FC : Moody’s (Baa1), S&P (BBB+),

JCR (A-), FITCH (BBB+)

− LC : Moody’s (Baa1), S&P (BBB+),

JCR (A), FITCH (A-)

Net Debt/EBITDA ≤ 2.0

Net Debt/Equity ≤ 1.0

1,105,147 1,118,677

441,066 375,617

387,381332,977

316,757

346,725

1,054,694 1,087,687

697,000 632,833

498,657453,476

1 2 3 4 5

3%

2,173,9962,250,351

31 Dec 1531 Dec 14

Assets slightly declined :

• Drop in trade A/R and A/P relating to lower crude

oil price

• Impairment charge on Mining properties and E&P

assets

35

Overview Performance 2016 Outlook

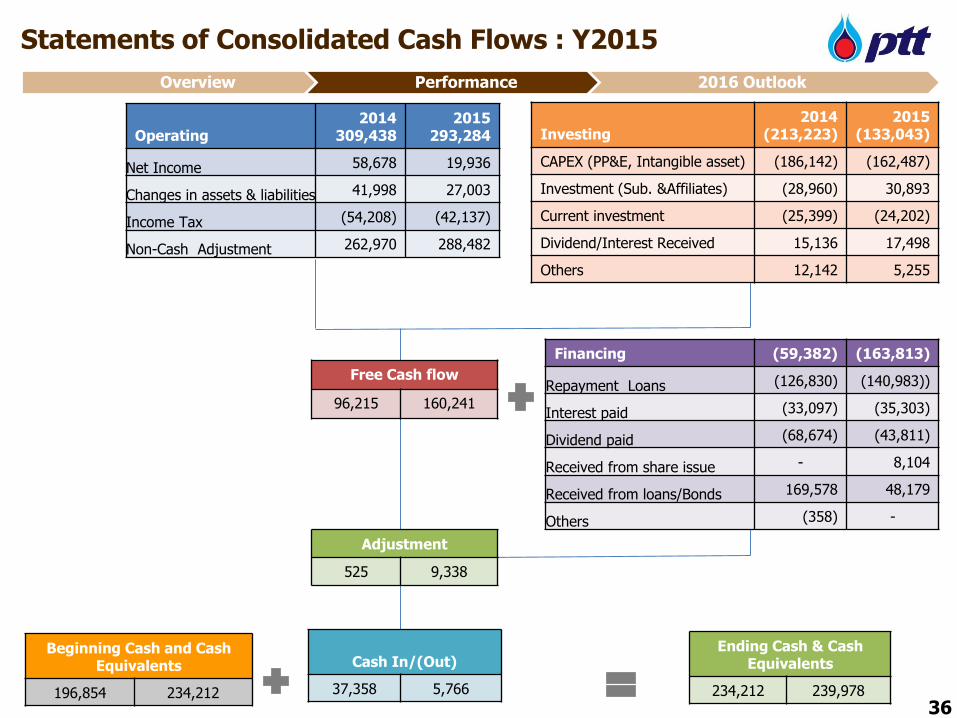

Free Cash flow

96,215 160,241

Investing2014

(213,223)2015

(133,043)

CAPEX (PP&E, Intangible asset) (186,142) (162,487)

Investment (Sub. &Affiliates) (28,960) 30,893

Current investment (25,399) (24,202)

Dividend/Interest Received 15,136 17,498

Others 12,142 5,255

Operating2014

309,4382015

293,284

Net Income 58,678 19,936

Changes in assets & liabilities 41,998 27,003

Income Tax (54,208) (42,137)

Non-Cash Adjustment 262,970 288,482

Ending Cash & Cash Equivalents

234,212 239,978

Beginning Cash and Cash Equivalents

196,854 234,212

Cash In/(Out)

37,358 5,766

Adjustment

525 9,338

Financing (59,382) (163,813)

Repayment Loans (126,830) (140,983))

Interest paid (33,097) (35,303)

Dividend paid (68,674) (43,811)

Received from share issue - 8,104

Received from loans/Bonds 169,578 48,179

Others (358) -

Statements of Consolidated Cash Flows : Y2015

36

Overview Performance 2016 Outlook

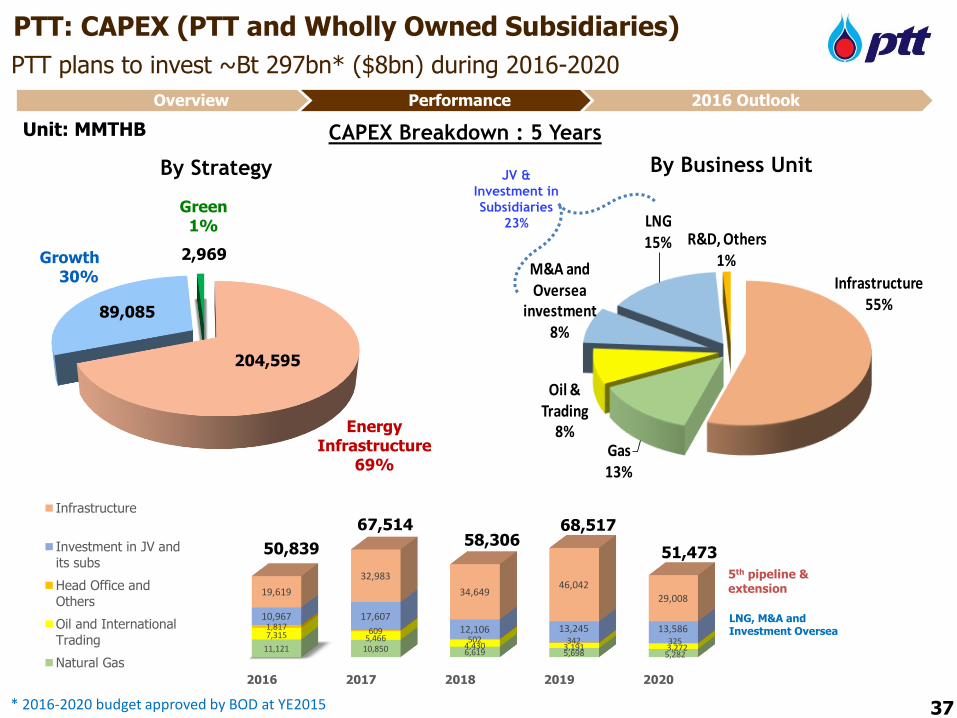

2016 2017 2018 2019 2020

11,121 10,850 6,619 5,698 5,282

7,315 5,4664,430 3,191 3,272

1,817 609502 342 325

10,967 17,60712,106 13,245 13,586

19,619

32,983

34,64946,042

29,008

Infrastructure

Investment in JV andits subs

Head Office andOthers

Oil and InternationalTrading

Natural Gas

204,595

89,085

2,969

Infrastructure55%

Gas13%

Oil & Trading

8%

M&A and Oversea

investment8%

LNG15% R&D, Others

1%

PTT: CAPEX (PTT and Wholly Owned Subsidiaries)

PTT plans to invest ~Bt 297bn* ($8bn) during 2016-2020

CAPEX Breakdown : 5 Years

By Business UnitJV &

Investment in

Subsidiaries

23%

37

67,514 68,517

51,47350,83958,306

* 2016-2020 budget approved by BOD at YE2015

5th pipeline & extension

LNG, M&A and Investment Oversea

Energy Infrastructure

69%

Green1%

Growth30%

Unit: MMTHB

By Strategy

Overview Performance 2016 Outlook

2015 Year in Review

Performance

2016 Outlook

2015 Year in Review Performance 2016 Outlook

38

Contents

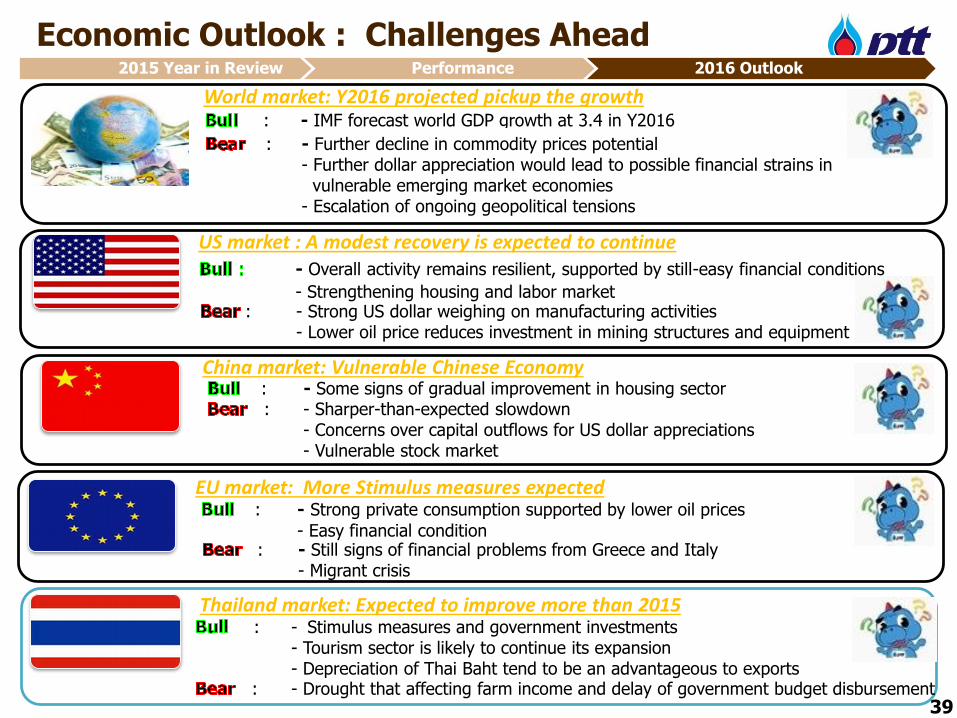

: - Some signs of gradual improvement in housing sector

: - IMF forecast world GDP growth at 3.4 in Y2016

: - Further decline in commodity prices potential- Further dollar appreciation would lead to possible financial strains in

vulnerable emerging market economies- Escalation of ongoing geopolitical tensions

Economic Outlook : Challenges Ahead

US market : A modest recovery is expected to continue

EU market: More Stimulus measures expected : - Strong private consumption supported by lower oil prices

- Easy financial condition: - Still signs of financial problems from Greece and Italy

- Migrant crisis

Thailand market: Expected to improve more than 2015: - Stimulus measures and government investments

- Tourism sector is likely to continue its expansion- Depreciation of Thai Baht tend to be an advantageous to exports

: - Drought that affecting farm income and delay of government budget disbursement

World market: Y2016 projected pickup the growth

: - Sharper-than-expected slowdown- Concerns over capital outflows for US dollar appreciations- Vulnerable stock market

China market: Vulnerable Chinese Economy

- Overall activity remains resilient, supported by still-easy financial conditions

- Strengthening housing and labor market : - Strong US dollar weighing on manufacturing activities

- Lower oil price reduces investment in mining structures and equipment

39

2015 Year in Review Performance 2016 Outlook

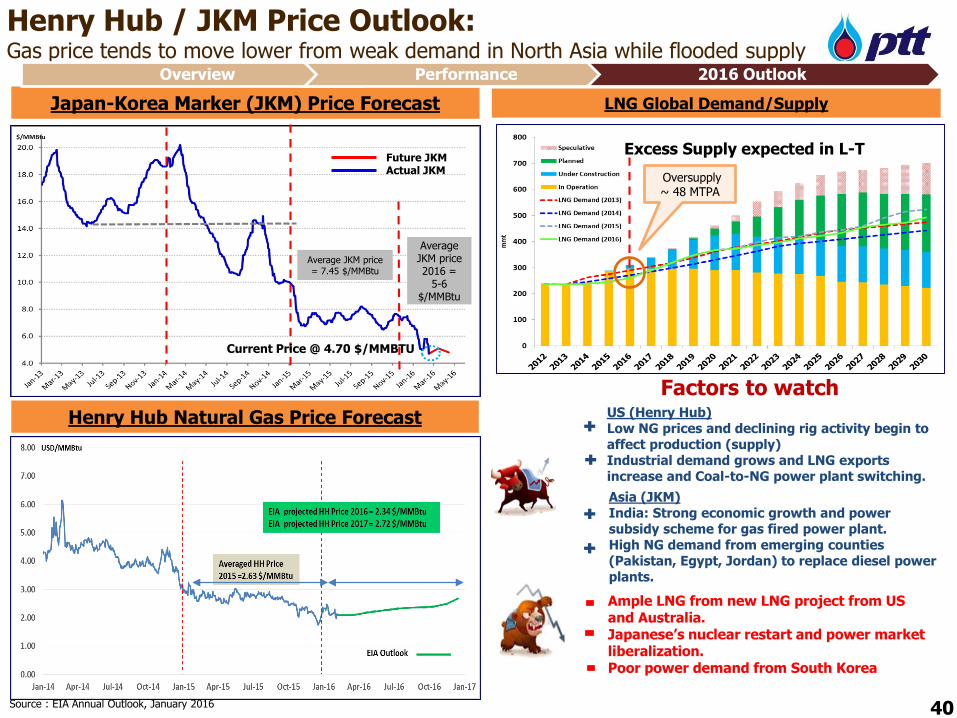

US (Henry Hub)Low NG prices and declining rig activity begin to affect production (supply)Industrial demand grows and LNG exports increase and Coal-to-NG power plant switching.

Factors to watch

Source : EIA Annual Outlook, January 2016

Henry Hub Natural Gas Price Forecast

Henry Hub / JKM Price Outlook: Gas price tends to move lower from weak demand in North Asia while flooded supply

LNG Global Demand/Supply

Ample LNG from new LNG project from US and Australia. Japanese’s nuclear restart and power market liberalization.Poor power demand from South Korea

Japan-Korea Marker (JKM) Price Forecast

Excess Supply expected in L-T

Average JKM price= 7.45 $/MMBtu

Asia (JKM)India: Strong economic growth and power subsidy scheme for gas fired power plant.High NG demand from emerging counties (Pakistan, Egypt, Jordan) to replace diesel power plants.

40

Current Price @ 4.70 $/MMBTU

Future JKM Actual JKM

Oversupply ~ 48 MTPA

Average JKM price2016 =

5-6 $/MMBtu

Overview Performance 2016 Outlook

92.80

94.50

95.70

93.70

96.30 96.35

0.90

1.80

0.65

-0.50

0.50

1.50

2.50

3.50

4.50

90.00

91.00

92.00

93.00

94.00

95.00

96.00

97.00

98.00

2014 2015 2016

World oil Demand(LHS) World Oil Supply(LHS) Stockbuild*(RHS)

26.8

28.529.0 30.031.131.533.034.9 36.1 38.8

39.5 41.0

20

30

40

50

60

70

80

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Oct-16WTI Brent Dubai Dubai Forecast (PTT Group PRISM)

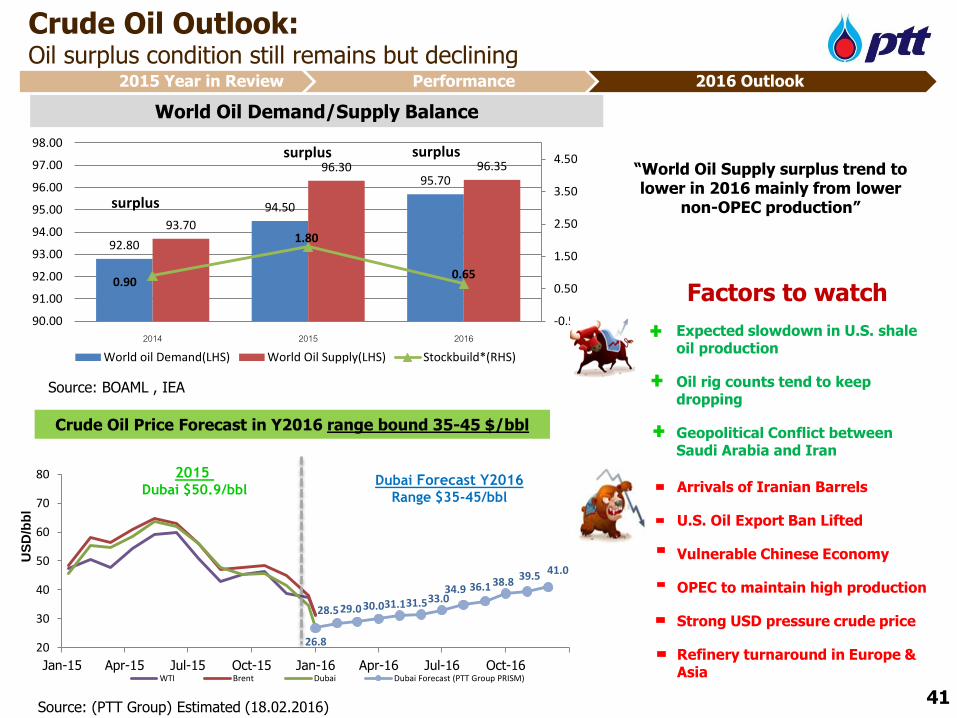

2015 Dubai $50.9/bbl

Dubai Forecast Y2016Range $35-45/bbl

Expected slowdown in U.S. shale oil production

Oil rig counts tend to keep dropping

Geopolitical Conflict between Saudi Arabia and Iran

“World Oil Supply surplus trend to lower in 2016 mainly from lower

non-OPEC production”

Source: (PTT Group) Estimated (18.02.2016)

Crude Oil Outlook: Oil surplus condition still remains but declining

Arrivals of Iranian Barrels

U.S. Oil Export Ban Lifted

Vulnerable Chinese Economy

OPEC to maintain high production

Strong USD pressure crude price

Refinery turnaround in Europe & Asia

Crude Oil Price Forecast in Y2016 range bound 35-45 $/bbl

Factors to watch

World Oil Demand/Supply Balance

Source: BOAML , IEA

surplus

surplus surplus

US

D/b

bl

41

2015 Year in Review Performance 2016 Outlook

Source: FACTS, DB, KBC, Reuters , IEA, Reuters, Thaioil and PRISM Estimated ( Feb 2016)

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Oct-16

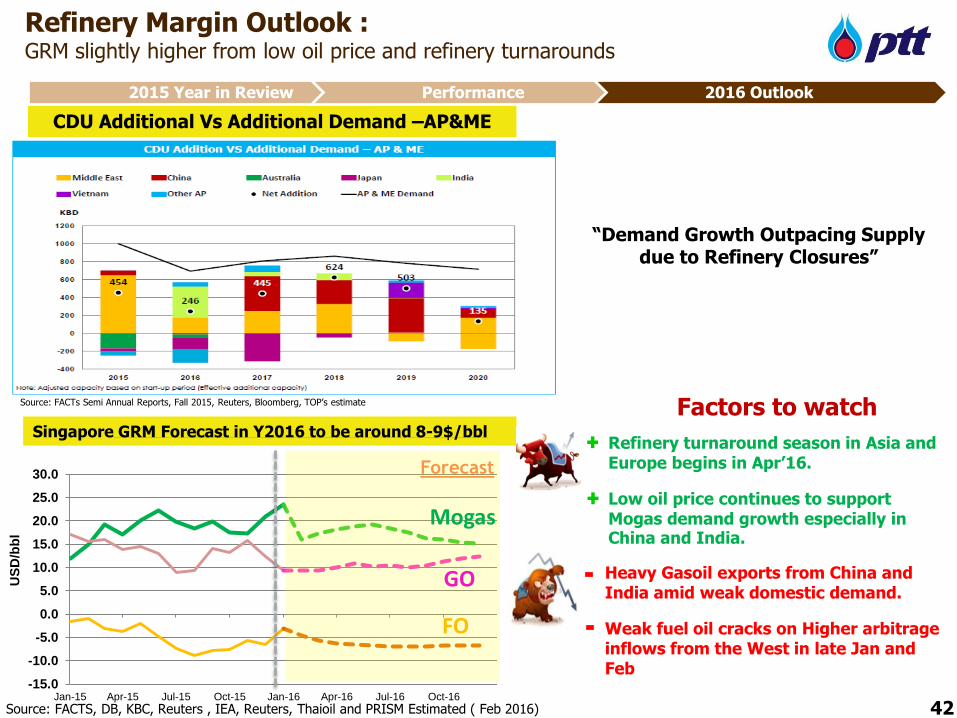

Refinery turnaround season in Asia and Europe begins in Apr’16.

Low oil price continues to support Mogas demand growth especially in China and India.

Forecast

GO

Mogas

FO

Heavy Gasoil exports from China and India amid weak domestic demand.

Weak fuel oil cracks on Higher arbitrage inflows from the West in late Jan and Feb

Singapore GRM Forecast in Y2016 to be around 8-9$/bbl

Factors to watch

“Demand Growth Outpacing Supply due to Refinery Closures”

Refinery Margin Outlook : GRM slightly higher from low oil price and refinery turnarounds

CDU Additional Vs Additional Demand –AP&ME

Source: FACTs Semi Annual Reports, Fall 2015, Reuters, Bloomberg, TOP’s estimate

US

D/b

bl

42

2015 Year in Review Performance 2016 Outlook

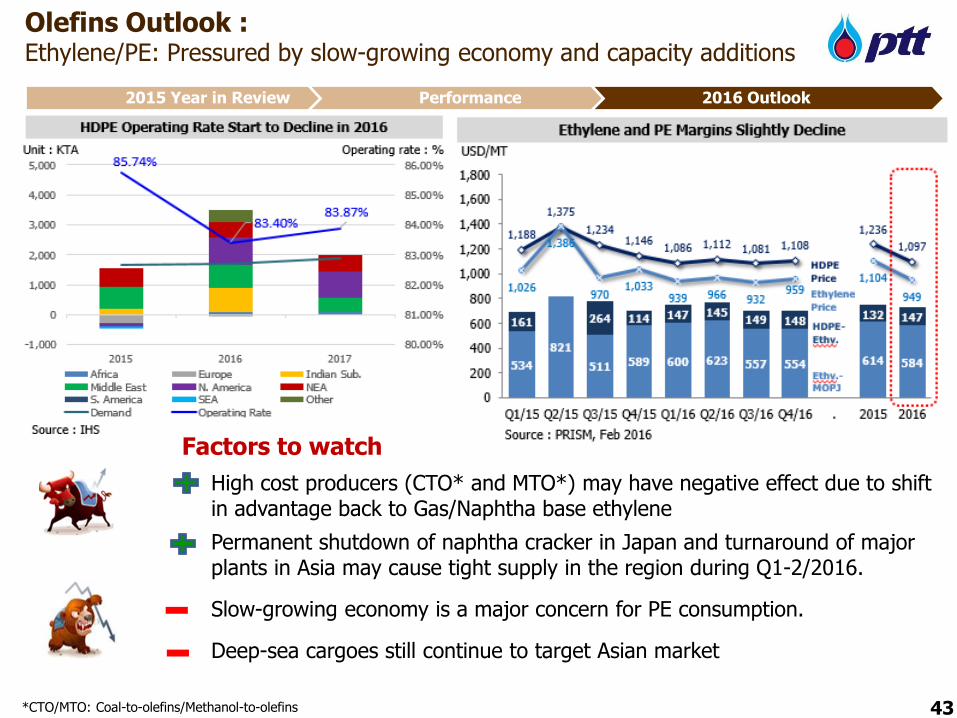

Olefins Outlook :Ethylene/PE: Pressured by slow-growing economy and capacity additions

43

High cost producers (CTO* and MTO*) may have negative effect due to shift in advantage back to Gas/Naphtha base ethylene

Permanent shutdown of naphtha cracker in Japan and turnaround of major plants in Asia may cause tight supply in the region during Q1-2/2016.

Slow-growing economy is a major concern for PE consumption.

Deep-sea cargoes still continue to target Asian market

Factors to watch

*CTO/MTO: Coal-to-olefins/Methanol-to-olefins

2015 Year in Review Performance 2016 Outlook

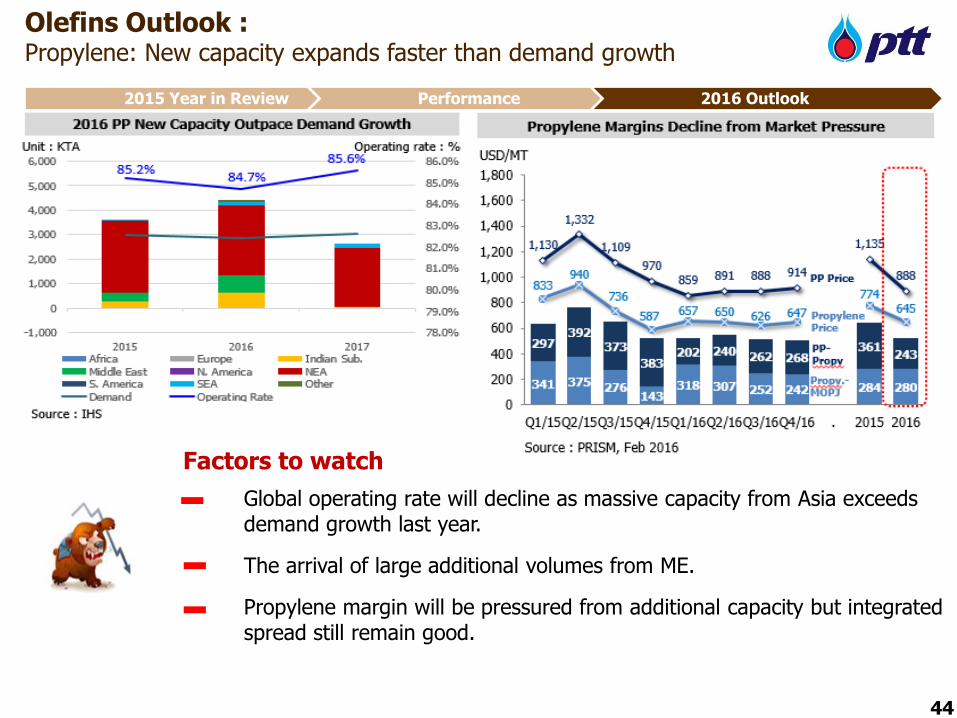

Olefins Outlook :Propylene: New capacity expands faster than demand growth

44

Global operating rate will decline as massive capacity from Asia exceeds demand growth last year.

The arrival of large additional volumes from ME.

Propylene margin will be pressured from additional capacity but integrated spread still remain good.

Factors to watch

2015 Year in Review Performance 2016 Outlook

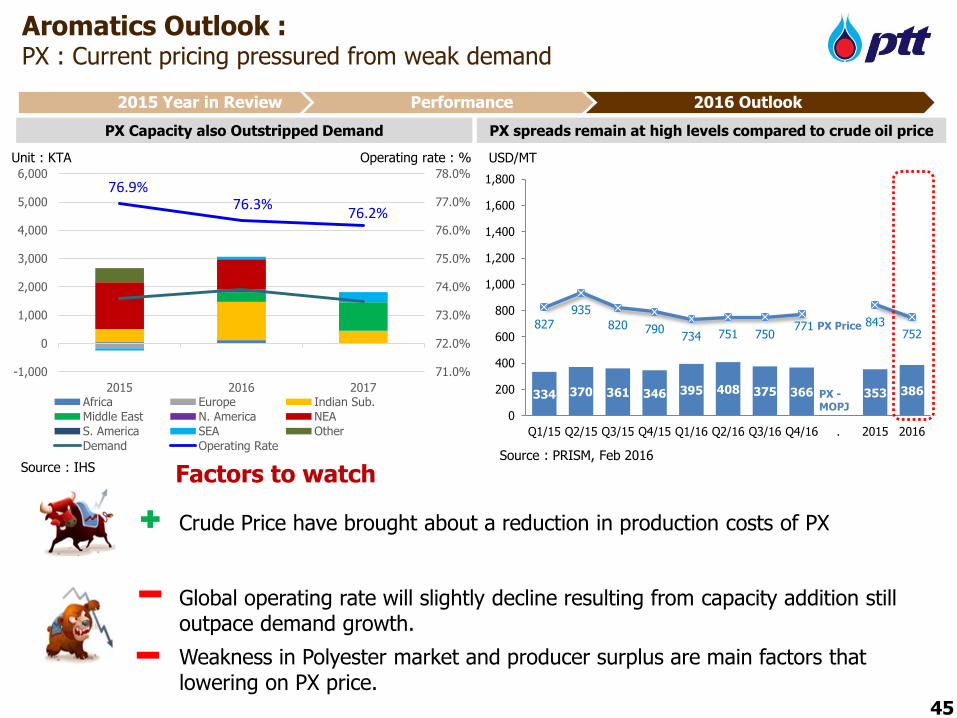

Aromatics Outlook :PX : Current pricing pressured from weak demand

PX Capacity also Outstripped Demand

Crude Price have brought about a reduction in production costs of PX

Global operating rate will slightly decline resulting from capacity addition still outpace demand growth.

Weakness in Polyester market and producer surplus are main factors that lowering on PX price.

PX spreads remain at high levels compared to crude oil price

334 370 361 346 395 408 375 366 353 386

827935

820 790734 751 750

771 843752

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16 Q3/16 Q4/16 . 2015 2016

USD/MT

PX -MOPJ

PX Price

Source : PRISM, Feb 2016Source : IHS

76.9%76.3%

76.2%

71.0%

72.0%

73.0%

74.0%

75.0%

76.0%

77.0%

78.0%

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

2015 2016 2017Africa Europe Indian Sub.

Middle East N. America NEA

S. America SEA Other

Demand Operating Rate

Unit : KTA Operating rate : %

Factors to watch

45

2015 Year in Review Performance 2016 Outlook

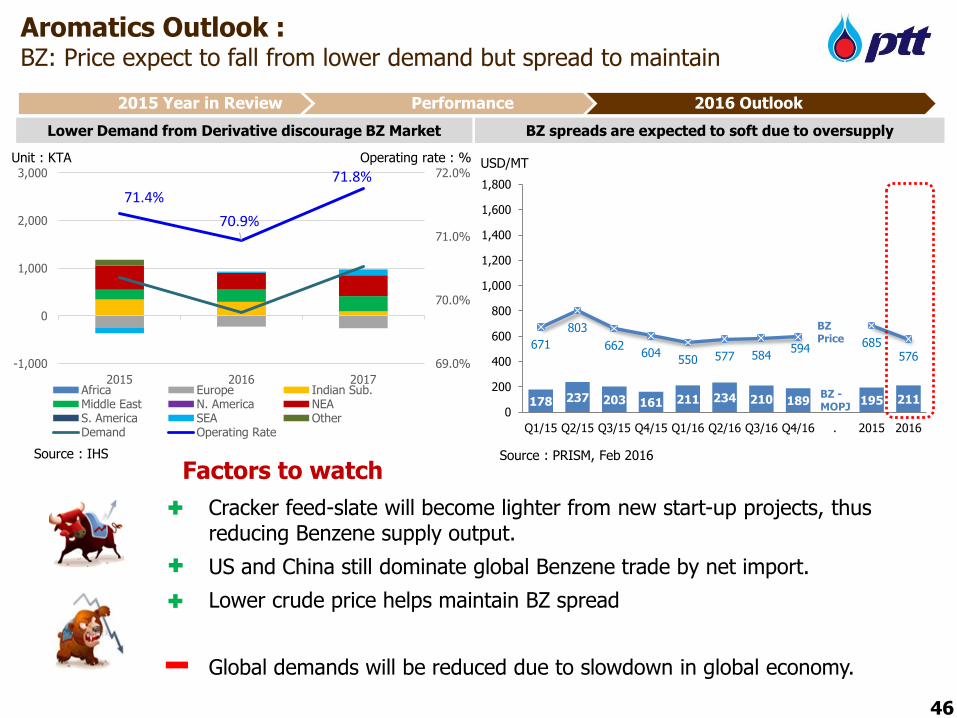

Aromatics Outlook :BZ: Price expect to fall from lower demand but spread to maintain

Lower Demand from Derivative discourage BZ Market

Cracker feed-slate will become lighter from new start-up projects, thus reducing Benzene supply output.

US and China still dominate global Benzene trade by net import.

Lower crude price helps maintain BZ spread

Global demands will be reduced due to slowdown in global economy.

BZ spreads are expected to soft due to oversupply

178 237 203 161 211 234 210 189 195 211

671

803

662604

550 577 584594 685

576

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Q1/15 Q2/15 Q3/15 Q4/15 Q1/16 Q2/16 Q3/16 Q4/16 . 2015 2016

USD/MT

BZ -MOPJ

BZ Price

Source : IHS

71.4%

70.9%

71.8%

69.0%

70.0%

71.0%

72.0%

-1,000

0

1,000

2,000

3,000

2015 2016 2017Africa Europe Indian Sub.Middle East N. America NEAS. America SEA OtherDemand Operating Rate

Unit : KTA Operating rate : %

Source : PRISM, Feb 2016

Factors to watch

46

2015 Year in Review Performance 2016 Outlook

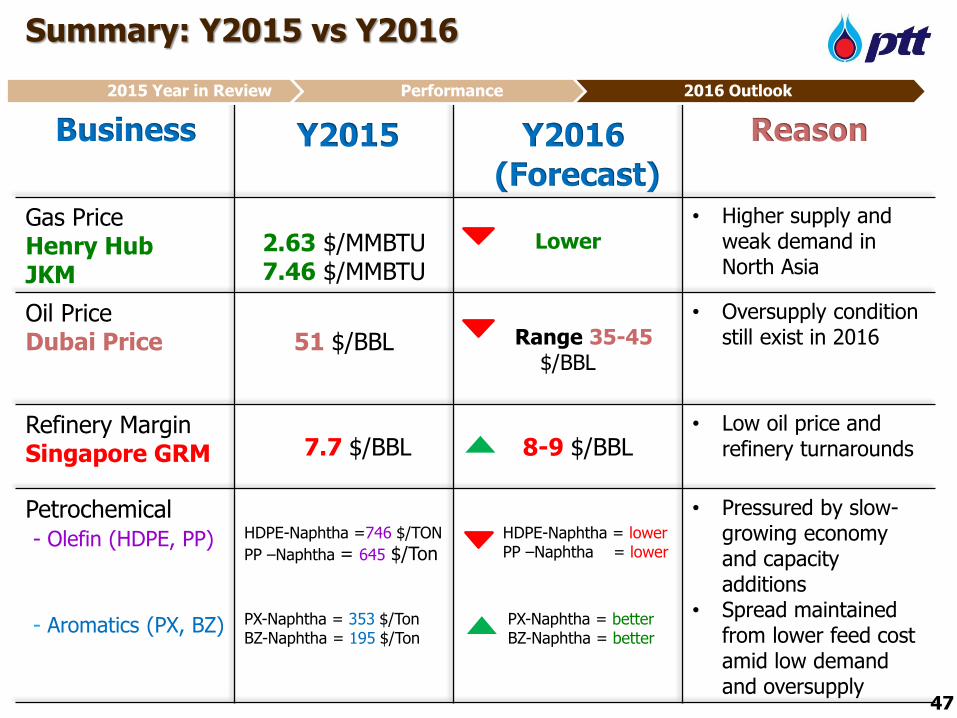

Summary: Y2015 vs Y2016

Business Y2015 Y2016

(Forecast)

Reason

Gas PriceHenry HubJKM

2.63 $/MMBTU7.46 $/MMBTU

Lower• Higher supply and

weak demand in North Asia

Oil PriceDubai Price 51 $/BBL Range 35-45

$/BBL

• Oversupply condition still exist in 2016

Refinery MarginSingapore GRM 7.7 $/BBL 8-9 $/BBL

• Low oil price and refinery turnarounds

Petrochemical - Olefin (HDPE, PP)

- Aromatics (PX, BZ)

HDPE-Naphtha =746 $/TON

PP –Naphtha = 645 $/Ton

PX-Naphtha = 353 $/TonBZ-Naphtha = 195 $/Ton

HDPE-Naphtha = lowerPP –Naphtha = lower

PX-Naphtha = betterBZ-Naphtha = better

• Pressured by slow-growing economy and capacity additions

• Spread maintained from lower feed cost amid low demand and oversupply

47

2015 Year in Review Performance 2016 Outlook

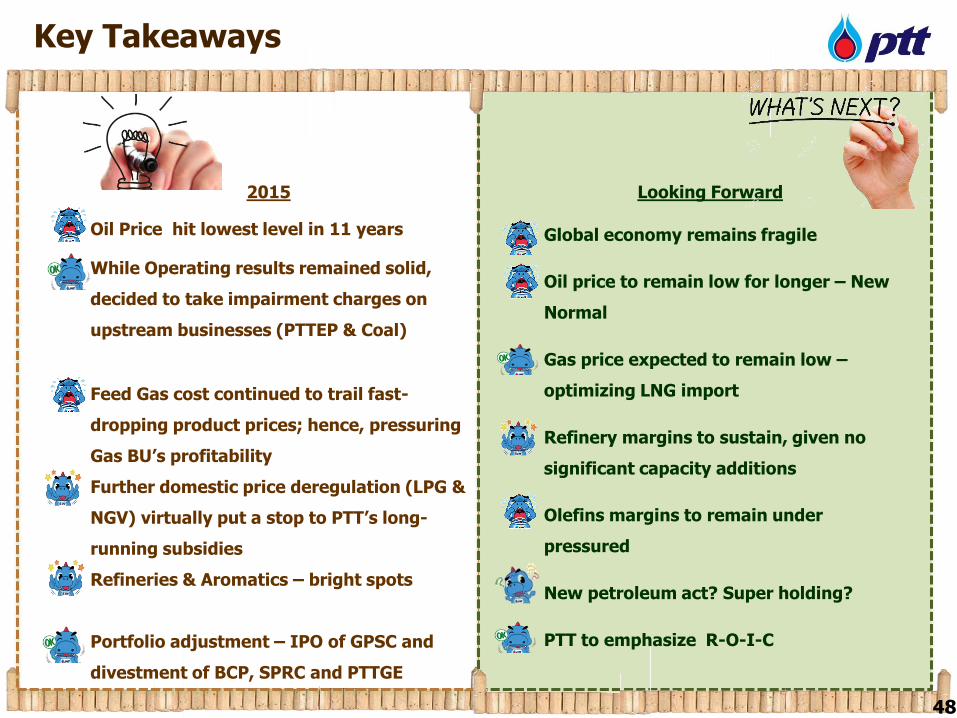

2015

• Oil Price hit lowest level in 11 years

• While Operating results remained solid,

decided to take impairment charges on

upstream businesses (PTTEP & Coal)

• Feed Gas cost continued to trail fast-

dropping product prices; hence, pressuring

Gas BU’s profitability

• Further domestic price deregulation (LPG &

NGV) virtually put a stop to PTT’s long-

running subsidies

• Refineries & Aromatics – bright spots

• Portfolio adjustment – IPO of GPSC and

divestment of BCP, SPRC and PTTGE

Looking Forward

• Global economy remains fragile

• Oil price to remain low for longer – New

Normal

• Gas price expected to remain low –

optimizing LNG import

• Refinery margins to sustain, given no

significant capacity additions

• Olefins margins to remain under

pressured

• New petroleum act? Super holding?

• PTT to emphasize R-O-I-C

Key Takeaways

48

Thank youPTT Public Company Limited – Investor Relations Department

Tel. +66 2 537-3518, Fax. +66 2 537-3948, E-mail: [email protected] Website: http://www.pttplc.com

Disclaimer

The information contained in our presentation is intended solely for your personal reference only. In addition, such information contains projections and forward-looking

statements that reflect our current views with respect to future events and financial performance. These views are based on assumptions subject to various risks and

uncertainties. No assurance is given that future events will occur, that projections will be achieved, or that our assumptions are correct. Actual results may differ

materially from those projected.

Petroleum Reserves and Resources Information

In this presentation, the Company discloses petroleum reserves and resources that are not included in the Securities Exchange and Commission of Thailand (SEC) Annual

Registration Statement Form 56-1 under “Supplemental Information on Petroleum Exploration and Production Activities”. The reserves and resources data contained in

this presentation reflects the Company’s best estimates of its reserves and resources. While the Company periodically obtains an independent audit of a portion of its

proved reserves, no independent qualified reserves evaluator or auditor was involved in the preparation of reserves and resources data disclosed in this presentation.

Unless stated otherwise, reserves and resources are stated at the Company’s gross basis. This presentation may contain the terms “proved reserves”, “probable reserves”,

and/or “contingent resources”. Unless stated otherwise, the Company adopts similar description as defined by the Society of Petroleum Engineers.

Proved Reserves - Proved reserves are defined as those quantities of petroleum which, by analysis of geological and engineering data, can be estimated with reasonable

certainty to be commercially recoverable, from a given date forward, from known reservoirs and under current economic conditions, operating methods, and government

regulations.

Probable Reserves - Probable reserves are defined as those unproved reserves which analysis of geological and engineering data suggests are more likely than not to be

recoverable.

Contingent Resources – Contingent resources are defined as those quantities of petroleum which are estimated, on a given date, to be potentially recoverable from

known accumulations, but which are not currently considered to be commercially recoverable. The reasons for non commerciality could be economic including market

availability, political, environmental, or technological.

49

49

50

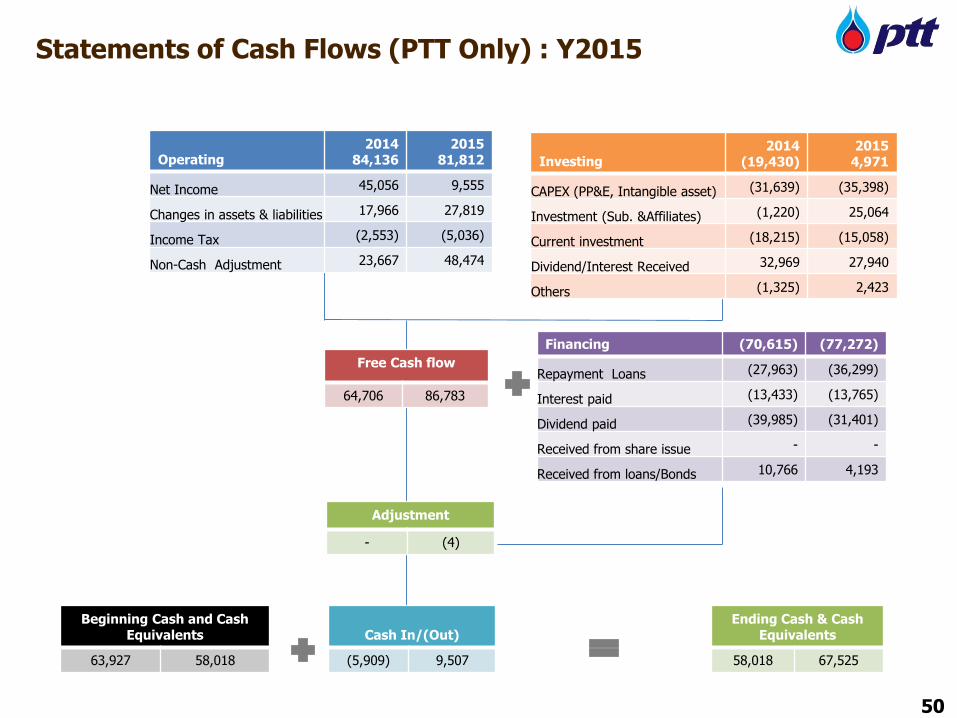

Free Cash flow

64,706 86,783

Financing (70,615) (77,272)

Repayment Loans (27,963) (36,299)

Interest paid (13,433) (13,765)

Dividend paid (39,985) (31,401)

Received from share issue - -

Received from loans/Bonds 10,766 4,193

Investing2014

(19,430)2015

4,971

CAPEX (PP&E, Intangible asset) (31,639) (35,398)

Investment (Sub. &Affiliates) (1,220) 25,064

Current investment (18,215) (15,058)

Dividend/Interest Received 32,969 27,940

Others (1,325) 2,423

Operating2014

84,1362015

81,812

Net Income 45,056 9,555

Changes in assets & liabilities 17,966 27,819

Income Tax (2,553) (5,036)

Non-Cash Adjustment 23,667 48,474

Ending Cash & Cash Equivalents

58,018 67,525

Beginning Cash and Cash Equivalents

63,927 58,018

Cash In/(Out)

(5,909) 9,507

Adjustment

- (4)

Statements of Cash Flows (PTT Only) : Y2015

50

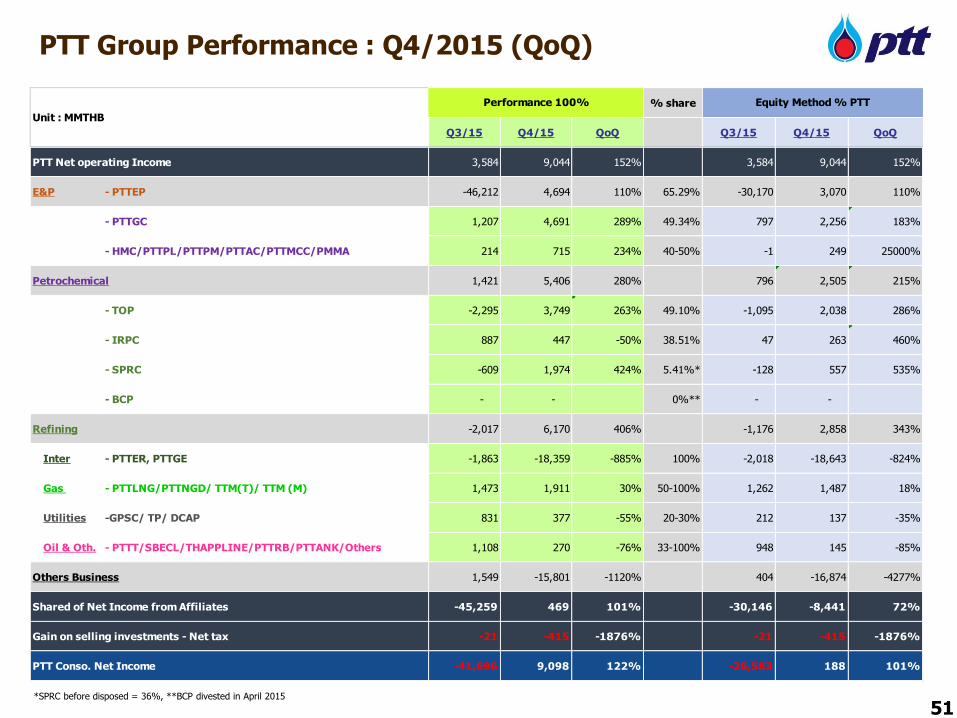

PTT Group Performance : Q4/2015 (QoQ)

% share

Q3/15 Q4/15 QoQ Q3/15 Q4/15 QoQ

PTT Net operating Income 3,584 9,044 152% 3,584 9,044 152%

E&P - PTTEP -46,212 4,694 110% 65.29% -30,170 3,070 110%

- PTTGC 1,207 4,691 289% 49.34% 797 2,256 183%

- HMC/PTTPL/PTTPM/PTTAC/PTTMCC/PMMA 214 715 234% 40-50% -1 249 25000%

Petrochemical 1,421 5,406 280% 796 2,505 215%

- TOP -2,295 3,749 263% 49.10% -1,095 2,038 286%

- IRPC 887 447 -50% 38.51% 47 263 460%

- SPRC -609 1,974 424% 5.41%* -128 557 535%

- BCP - - 0%** - -

Refining -2,017 6,170 406% -1,176 2,858 343%

Inter - PTTER, PTTGE -1,863 -18,359 -885% 100% -2,018 -18,643 -824%

Gas - PTTLNG/PTTNGD/ TTM(T)/ TTM (M) 1,473 1,911 30% 50-100% 1,262 1,487 18%

Utilities -GPSC/ TP/ DCAP 831 377 -55% 20-30% 212 137 -35%

Oil & Oth. - PTTT/SBECL/THAPPLINE/PTTRB/PTTANK/Others 1,108 270 -76% 33-100% 948 145 -85%

Others Business 1,549 -15,801 -1120% 404 -16,874 -4277%

Shared of Net Income from Affiliates -45,259 469 101% -30,146 -8,441 72%

Gain on selling investments - Net tax -21 -415 -1876% -21 -415 -1876%

PTT Conso. Net Income -41,696 9,098 122% -26,583 188 101%

Equity Method % PTTPerformance 100%

Unit : MMTHB

51*SPRC before disposed = 36%, **BCP divested in April 2015

52

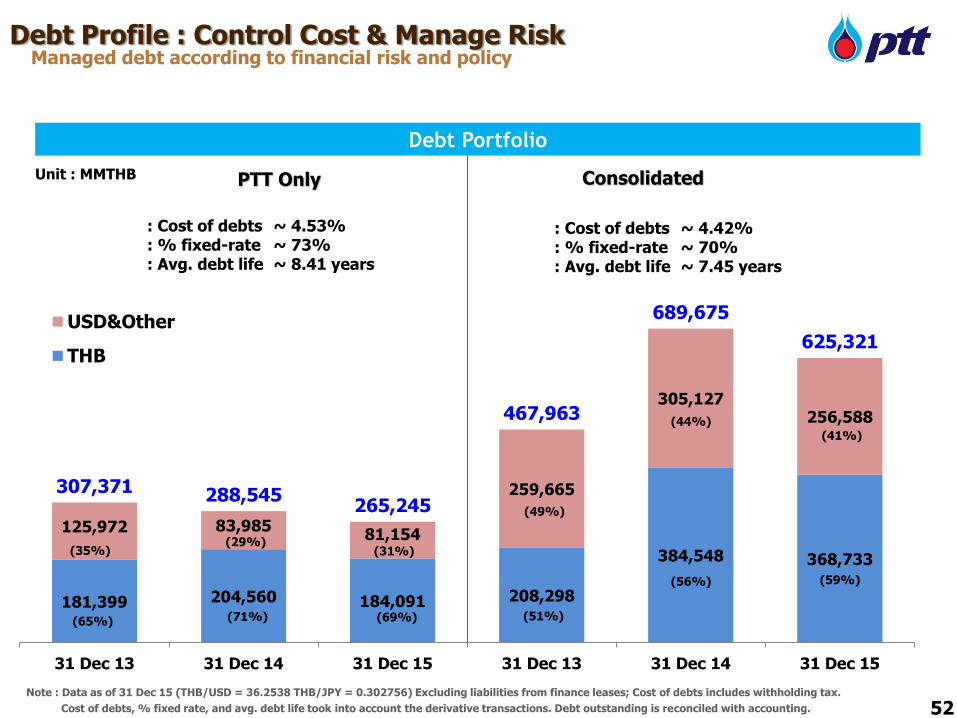

Debt Profile : Control Cost & Manage Risk

Debt Portfolio

Managed debt according to financial risk and policy

ConsolidatedPTT OnlyUnit : MMTHB

: Cost of debts ~ 4.53%: % fixed-rate ~ 73%: Avg. debt life ~ 8.41 years

: Cost of debts ~ 4.42%: % fixed-rate ~ 70%: Avg. debt life ~ 7.45 years

181,399 204,560 184,091 208,298

384,548 368,733

125,972 83,98581,154

259,665

305,127256,588

307,371 288,545265,245

467,963

689,675

625,321

31 Dec 13 31 Dec 14 31 Dec 15 31 Dec 13 31 Dec 14 31 Dec 15

USD&Other

THB

(35%)

(65%)

(29%)

(71%)

(31%)

(69%)

(49%)

(51%)

(44%)

(56%)

(41%)

(59%)

Note : Data as of 31 Dec 15 (THB/USD = 36.2538 THB/JPY = 0.302756) Excluding liabilities from finance leases; Cost of debts includes withholding tax.

52Cost of debts, % fixed rate, and avg. debt life took into account the derivative transactions. Debt outstanding is reconciled with accounting.

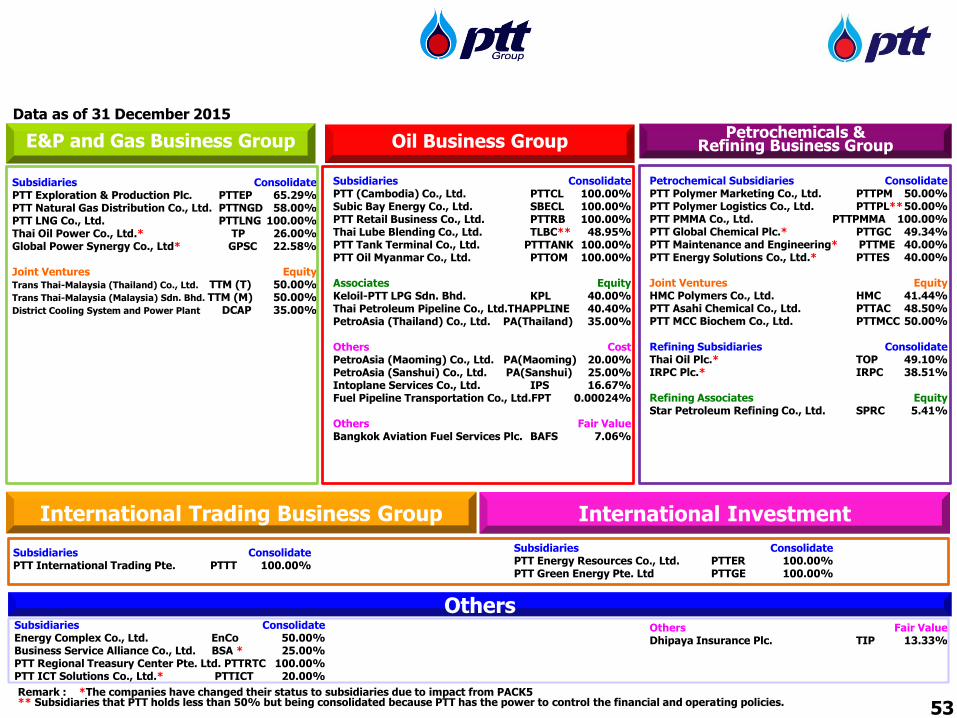

Subsidiaries ConsolidatePTT (Cambodia) Co., Ltd. PTTCL 100.00%Subic Bay Energy Co., Ltd. SBECL 100.00%PTT Retail Business Co., Ltd. PTTRB 100.00%Thai Lube Blending Co., Ltd. TLBC** 48.95%PTT Tank Terminal Co., Ltd. PTTTANK 100.00%PTT Oil Myanmar Co., Ltd. PTTOM 100.00%

Associates EquityKeloil-PTT LPG Sdn. Bhd. KPL 40.00%Thai Petroleum Pipeline Co., Ltd.THAPPLINE 40.40%PetroAsia (Thailand) Co., Ltd. PA(Thailand) 35.00%

Others CostPetroAsia (Maoming) Co., Ltd. PA(Maoming) 20.00%PetroAsia (Sanshui) Co., Ltd. PA(Sanshui) 25.00%Intoplane Services Co., Ltd. IPS 16.67%Fuel Pipeline Transportation Co., Ltd.FPT 0.00024%

Others Fair ValueBangkok Aviation Fuel Services Plc. BAFS 7.06%

Others

Subsidiaries ConsolidatePTT Exploration & Production Plc. PTTEP 65.29%PTT Natural Gas Distribution Co., Ltd. PTTNGD 58.00%PTT LNG Co., Ltd. PTTLNG 100.00%Thai Oil Power Co., Ltd.* TP 26.00%Global Power Synergy Co., Ltd* GPSC 22.58%

Joint Ventures EquityTrans Thai-Malaysia (Thailand) Co., Ltd. TTM (T) 50.00%Trans Thai-Malaysia (Malaysia) Sdn. Bhd. TTM (M) 50.00%District Cooling System and Power Plant DCAP 35.00%

Petrochemical Subsidiaries ConsolidatePTT Polymer Marketing Co., Ltd. PTTPM 50.00%PTT Polymer Logistics Co., Ltd. PTTPL**50.00%PTT PMMA Co., Ltd. PTTPMMA 100.00%PTT Global Chemical Plc.* PTTGC 49.34%PTT Maintenance and Engineering* PTTME 40.00%PTT Energy Solutions Co., Ltd.* PTTES 40.00%

Joint Ventures EquityHMC Polymers Co., Ltd. HMC 41.44%PTT Asahi Chemical Co., Ltd. PTTAC 48.50%PTT MCC Biochem Co., Ltd. PTTMCC 50.00%

Refining Subsidiaries ConsolidateThai Oil Plc.* TOP 49.10%IRPC Plc.* IRPC 38.51%

Refining Associates EquityStar Petroleum Refining Co., Ltd. SPRC 5.41%

Others Fair ValueDhipaya Insurance Plc. TIP 13.33%

Subsidiaries ConsolidateEnergy Complex Co., Ltd. EnCo 50.00%Business Service Alliance Co., Ltd. BSA * 25.00%PTT Regional Treasury Center Pte. Ltd. PTTRTC 100.00%PTT ICT Solutions Co., Ltd.* PTTICT 20.00%

International Trading Business Group

Subsidiaries ConsolidatePTT International Trading Pte. PTTT 100.00%

Remark : *The companies have changed their status to subsidiaries due to impact from PACK5** Subsidiaries that PTT holds less than 50% but being consolidated because PTT has the power to control the financial and operating policies.

Petrochemicals & Refining Business GroupE&P and Gas Business Group Oil Business Group

Data as of 31 December 2015

International Investment

Subsidiaries ConsolidatePTT Energy Resources Co., Ltd. PTTER 100.00%PTT Green Energy Pte. Ltd PTTGE 100.00%

53

53

54

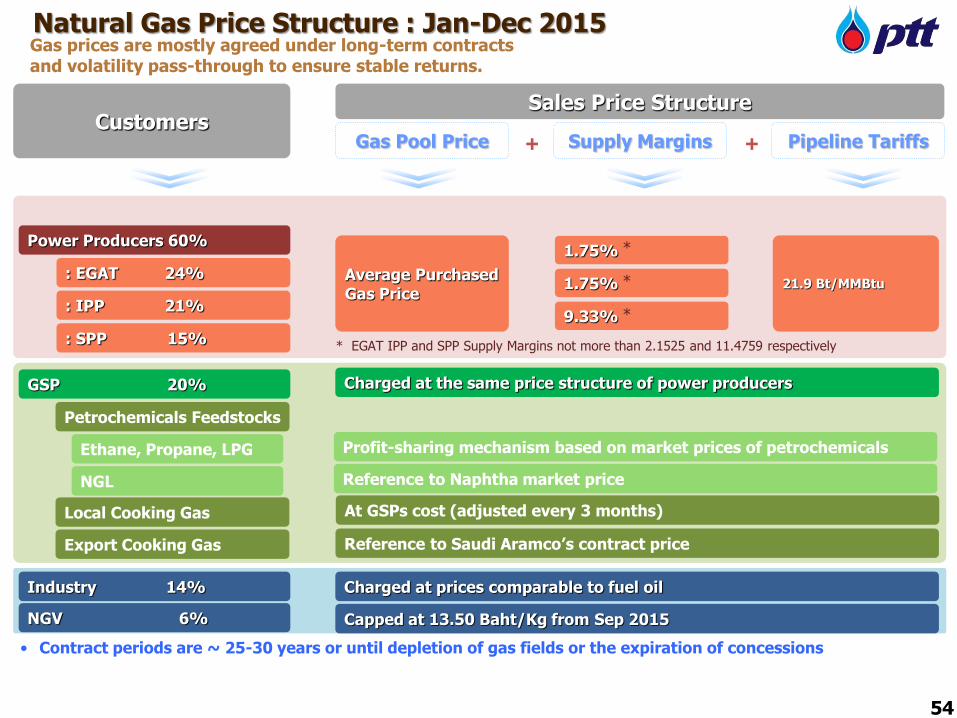

Natural Gas Price Structure : Jan-Dec 2015

CustomersSales Price Structure

Gas Pool Price Supply Margins Pipeline Tariffs+ +

Average Purchased Gas Price

1.75%

1.75%

9.33%

21.9 Bt/MMBtu

Charged at the same price structure of power producers

Reference to Saudi Aramco’s contract price

Charged at prices comparable to fuel oil

Gas prices are mostly agreed under long-term contracts and volatility pass-through to ensure stable returns.

Capped at 13.50 Baht/Kg from Sep 2015

Profit-sharing mechanism based on market prices of petrochemicals

Reference to Naphtha market price

At GSPs cost (adjusted every 3 months)

• Contract periods are ~ 25-30 years or until depletion of gas fields or the expiration of concessions

54

*

* EGAT IPP and SPP Supply Margins not more than 2.1525 and 11.4759 respectively

*

*

Power Producers 60%

: EGAT 24%

: IPP 21%

: SPP 15%

GSP 20%

Petrochemicals Feedstocks

Industry 14%

NGV 6%

Ethane, Propane, LPG

NGL

Local Cooking Gas

Export Cooking Gas

55Source : PTT

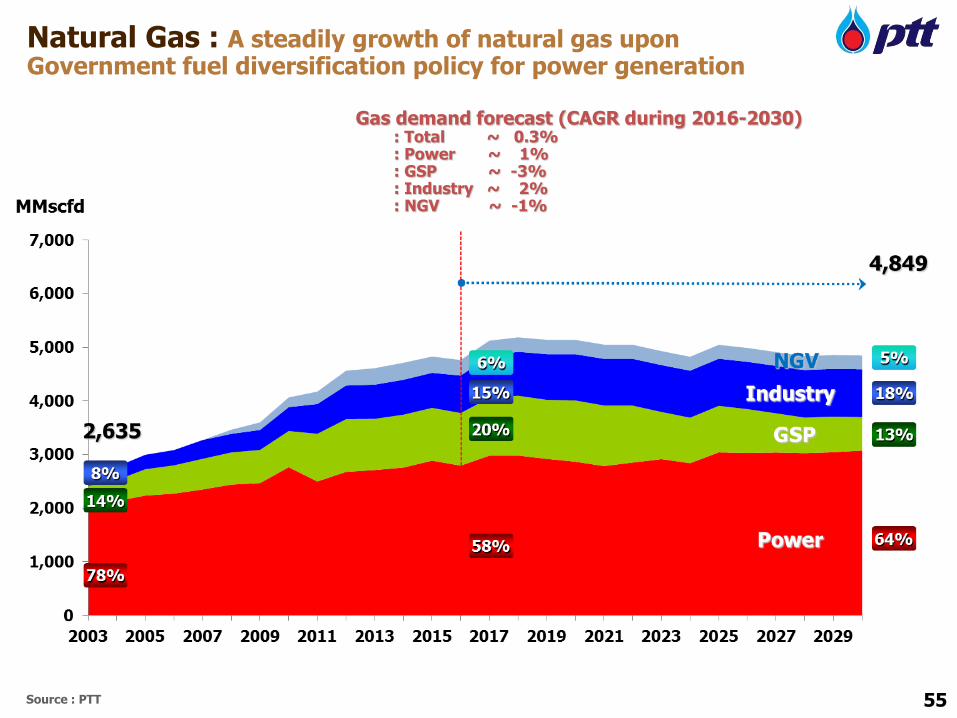

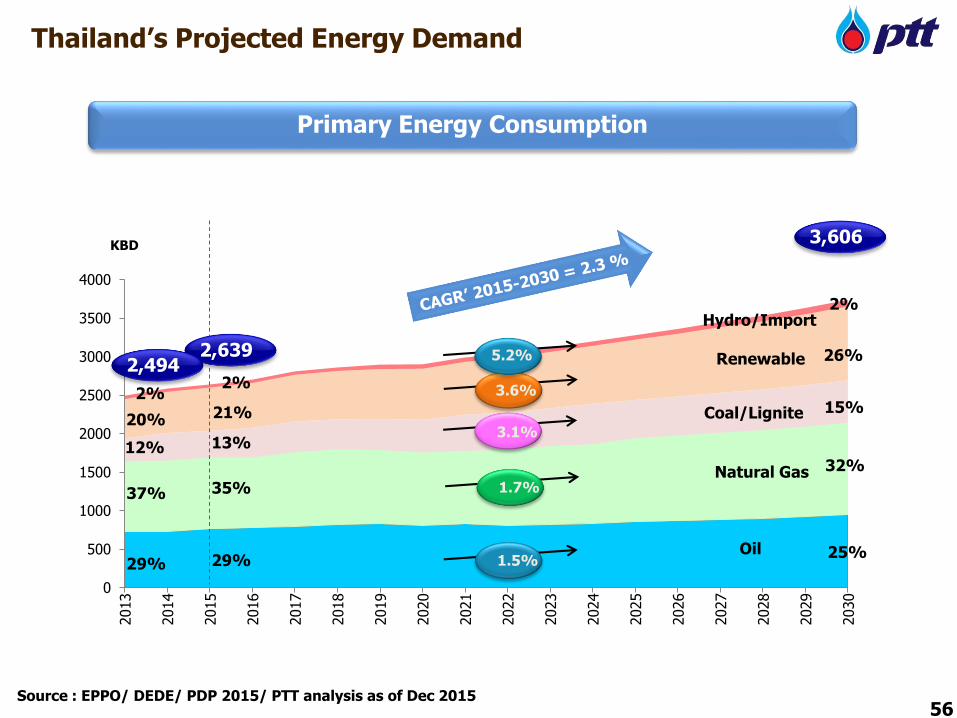

Gas demand forecast (CAGR during 2016-2030): Total ~ 0.3%: Power ~ 1%: GSP ~ -3%: Industry ~ 2%: NGV ~ -1%

Natural Gas : A steadily growth of natural gas upon Government fuel diversification policy for power generation

Thailand’s Projected Energy Demand

56

Primary Energy Consumption

Source : EPPO/ DEDE/ PDP 2015/ PTT analysis as of Dec 2015

0

500

1000

1500

2000

2500

3000

3500

4000

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

Oil

Natural Gas

Coal/Lignite

Hydro/Import

KBD

Renewable2,639

25%

32%

15%

2%

26%

3,606

2,494

29%

35%

13%

21%

2%

29%

37%

12%

20%

2%

1.5%

1.7%

3.1%

3.6%

5.2%

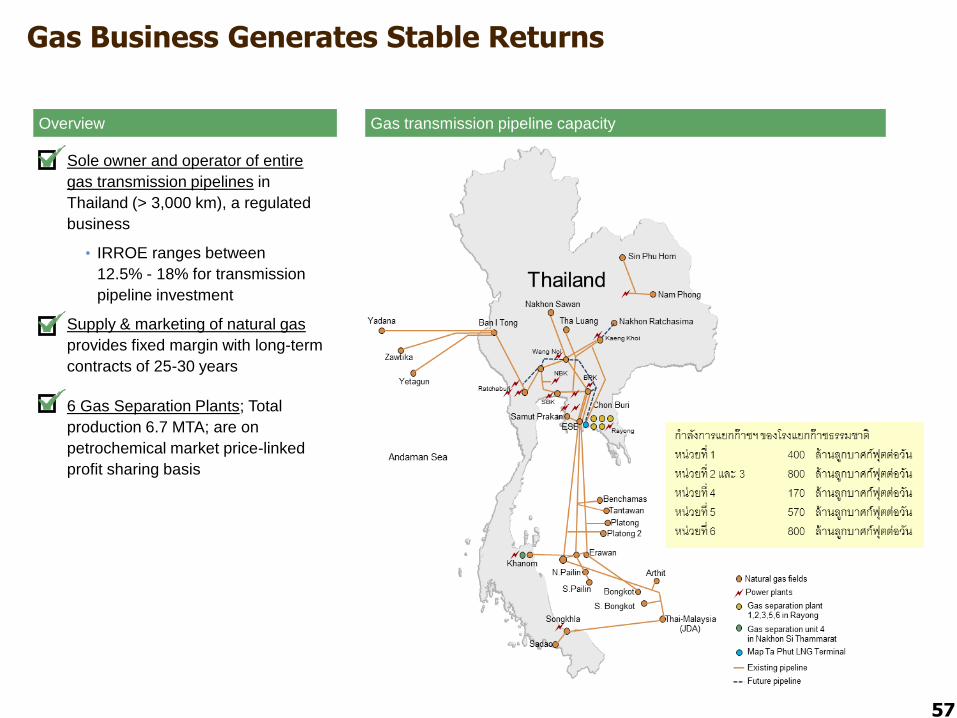

Gas Business Generates Stable Returns

Sole owner and operator of entire

gas transmission pipelines in

Thailand (> 3,000 km), a regulated

business

• IRROE ranges between

12.5% - 18% for transmission

pipeline investment

Supply & marketing of natural gas

provides fixed margin with long-term

contracts of 25-30 years

6 Gas Separation Plants; Total

production 6.7 MTA; are on

petrochemical market price-linked

profit sharing basis

Overview Gas transmission pipeline capacity

57