Embed Size (px)

Citation preview

ANALYST BRIEFING 2013

YBhg. Dato’ Sri Zukri Samat3 April 2013

Strictly Private & Confidential

Managing Director’s Office 2

Managing Director’s Office 3

Financial Highlights & Notable Achievements

FY2012

Finance Division 4

INCOME STATEMENT

* Restated arising from change in accounting policy on the determination of collective assessment allowance under MFRS 139

Finance Division 5

KEY BALANCE SHEET ITEMS

* Restated arising from adoption of MFRS

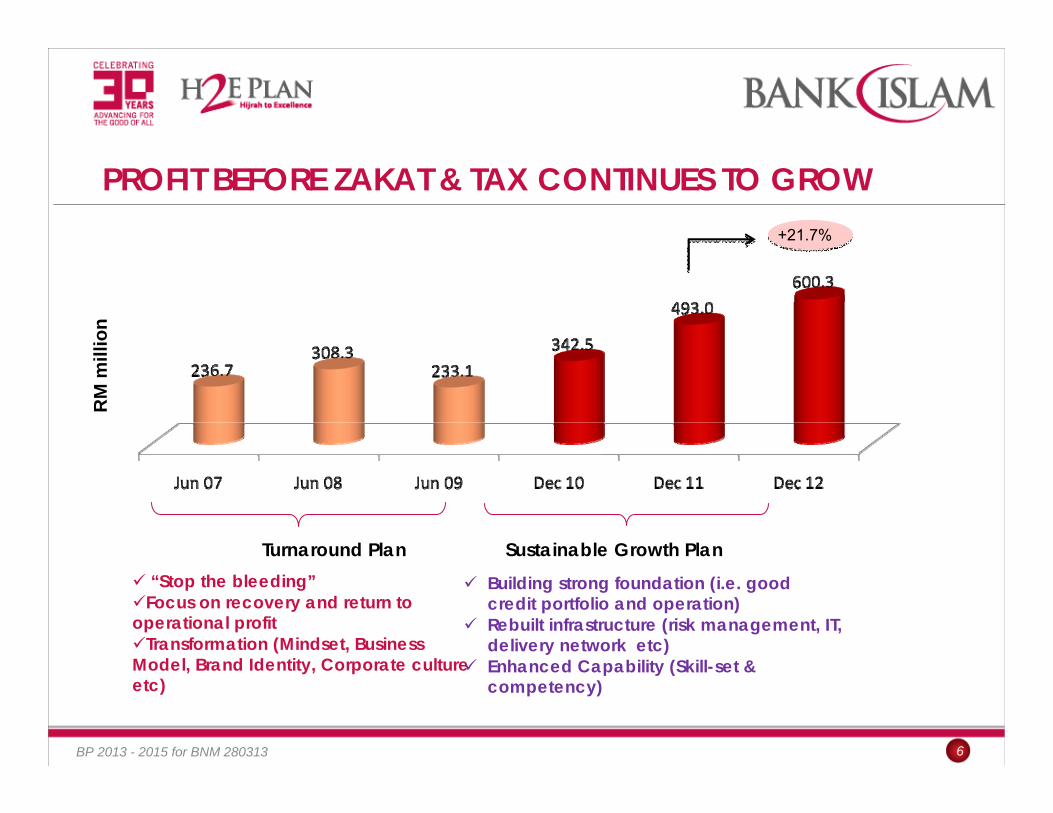

PROFIT BEFORE ZAKAT & TAX CONTINUES TO GROW

6

Turnaround Plan Sustainable Growth Plan“Stop the bleeding”

Focus on recovery and return to operational profit

Transformation (Mindset, Business Model, Brand Identity, Corporate culture etc)

Building strong foundation (i.e. good credit portfolio and operation)Rebuilt infrastructure (risk management, IT, delivery network etc)Enhanced Capability (Skill-set & competency)

RM

mill

ion

BP 2013 - 2015 for BNM 280313

+21.7%

TOTAL ASSETS : CAGR OF 12.1% OVER THE LAST 5 YEARS

7

Turnaround Plan Sustainable Growth PlanRecapitalisationBalance Sheet RestructuringRejuvenate Bank Islam brand

Robust Risk ManagementOptimising Balance Sheet Mix

RM

mill

ion

BP 2013 - 2015 for BNM 280313

+16.2%

TOTAL ASSETS: BENCHMARKED AGAINST OTHER ISLAMIC BANKS

Managing Director’s Office 8

Islamic Banking Assets (excluding DFIs) forms

20.0% of Banking System.Growth of 13.9% to

RM381.5b.

22.3%RM81.3b

12.8%RM46.6b

9.8%RM35.6b

8.3%RM30.3b

7.8%RM28.3b

22.1%RM74.0b

12.9%RM43.1b

9.6%RM32.2b

8.8%RM29.4b

6.7%RM22.4b

@ Dec 11

^Based on best proxy per Islamic banking operations disclosure in the audited account of the conventional banking group

@ Sept 12

Market Share

24.4%RM92.9b

15.4%RM58.9b

9.8%RM37.5b

7.7%RM29.3b

7.8%RM29.6b

@ Dec 12^

24.4%RM92.9b

15.4%RM58.9b

9.8%RM37.5b

7.8%RM29.6b

7.7%RM29.3b

NET FINANCING GREW BY 37.8% IN FY2012

9

…still primarily a retail bank

“Putting the House in Order”Revamp Business Model

Risk based Target MarketFocus on Secured Financing

RM

mill

ion

Gross Financing by Business Unit

3,696.6 (62.7)641.3 1,110.0

BP 2013 - 2015 for BNM 280313

+37.8%

Managing Director’s Office 10

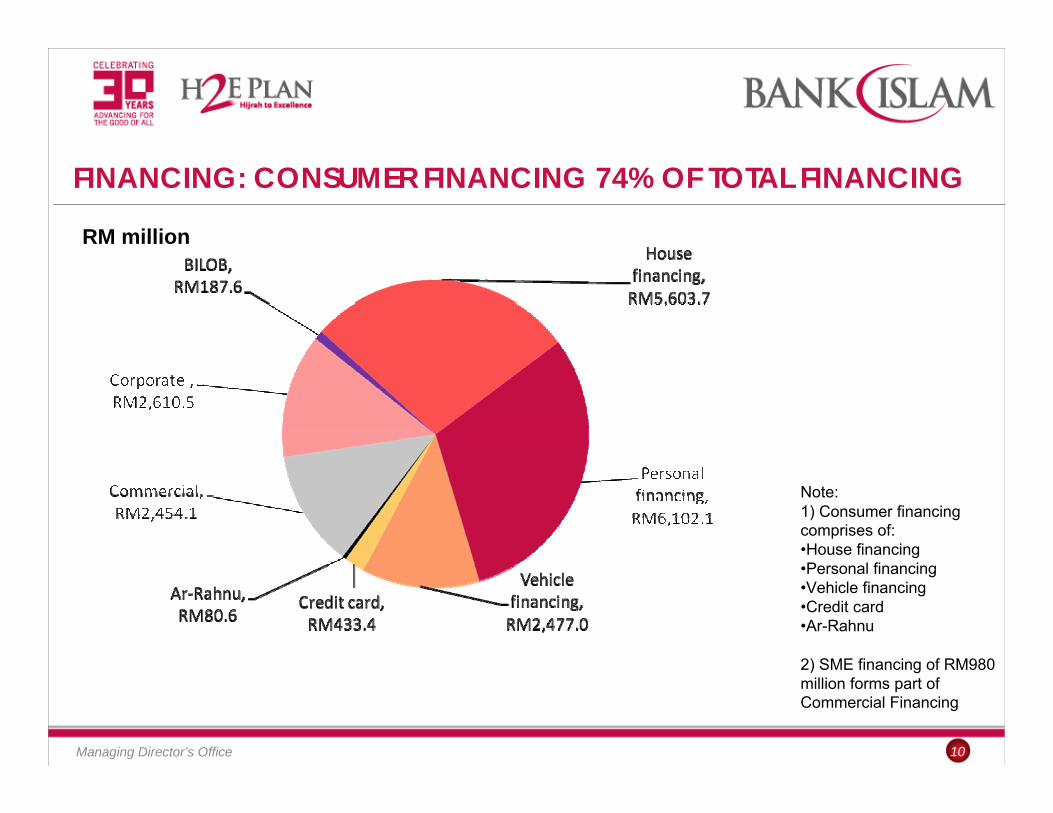

FINANCING: CONSUMER FINANCING 74% OF TOTAL FINANCING

RM million

Note:1) Consumer financing comprises of:•House financing•Personal financing•Vehicle financing•Credit card•Ar-Rahnu

2) SME financing of RM980 million forms part of Commercial Financing

CONSUMER FINANCING DRIVEN BY PERSONAL & HOUSE FINANCING

11

27%

19%

13%

2%

62%

23%

17%

-4%100%

• Consumer banking (74% of total financing). • Personal financing and HFA contributes42% and 38% of consumer banking respectively.

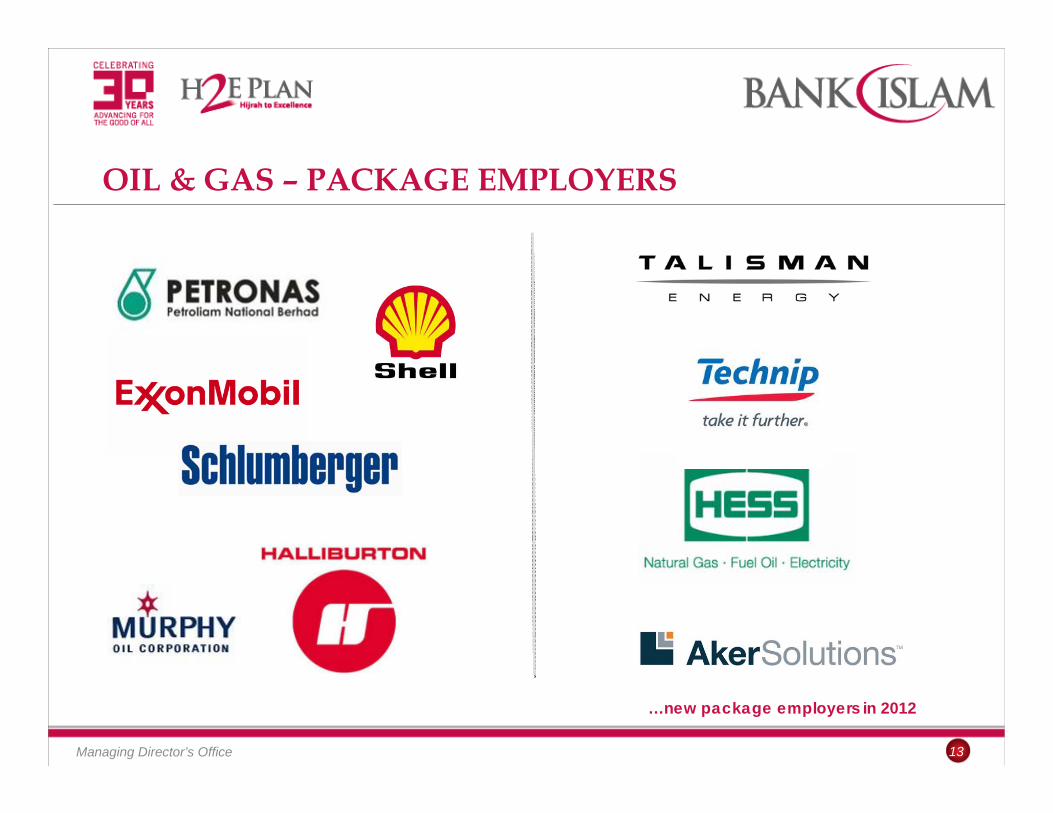

PACKAGE EMPLOYERS : GLCS & NON- GLCS

Managing Director’s Office 12

…about 51% of Consumer Banking

OIL & GAS – PACKAGE EMPLOYERS

Managing Director’s Office 13

…new package employers in 2012

KEY EXPOSURE TO ETP PROJECTS

Managing Director’s Office 14

Oil, Gas & Energy

Education

Palm Oil

Healthcare

Greater Kuala Lumpur

About RM350 million About RM5 billion

About RM4.5 billion

About RM500 million

NET FINANCING: BENCHMARKED AGAINST OTHER ISLAMIC BANKS

Managing Director’s Office 15

25.2%RM56.2b

14.1%RM31.4b

8.8%RM19.6b

8.7%RM19.5b

8.1%RM18.2b

25.4%RM49.9b

14.3%RM28.1b

7.8%RM15.3b

9.7%RM19.2b

7.2%RM14.2b

@ Dec 11@ Sept 12Market Share

26.7%RM62.2b

15.5%RM36.0b

8.6%RM19.9b

8.7%RM20.2b

8.4%RM19.5b

@ Dec12^

Islamic Banking Financing (excluding DFIs) forms

21.1% of Banking System.Growth of 16.2% to

RM232.8b.

^Based on best proxy per Islamic banking operations disclosure in the audited account of the conventional banking group

26.7%RM62.2b

15.5%RM36.0b 8.7%

RM20.2b 8.6%RM19.9b

8.4%RM19.5b

ASSET QUALITY CONTINUES TO IMPROVE

16

RM million Dec 10* Mar 11* June 11* Sept 11* Dec 11* Mar 12 June 12 Sept 12 Dec 12

Gross Impaired Financing 552 551 556 551 380 351 331 322 309Gross Financing 12,283 12,855 13,253 13,740 14,564 15,327 16,828 18,571 19,949

Individual Assessment 79 88 79 108 76 72 72 72 127Collective Assessment 347 342 349 338 328 341 345 348 313

Net Impaired Financing 126 121 128 105 (24) (62) (86) (98) (132)

Gross Impaired Financing Ratio 4.50% 4.29% 4.19% 4.01% 2.61% 2.29% 1.97% 1.74% 1.55%Net Impaired Financing Ratio 1.06% 0.98% 0.99% 0.79% -0.17% -0.42% -0.53% -0.54% -0.67%

* Restated arising from change in accounting policy on the determination of collective assessment allowance under MFRS 139

BP 2013 - 2015 for BNM 280313

Impaired financing

STRONG CUSTOMER DEPOSITS GROWTH OF 15.1% IN FY2012

17

Growth+ 15.1%

of which Al-Awfar

7032.5%

of which Al-Awfar

1120.4%

of which Al-Awfar1,1213.6%

of which Al-Awfar

1090.4%

BP 2013 - 2015 for BNM 280313

RM

mill

ion

CASA DEPOSITS RATIO REMAINS STABLE

18

RM million Dec 2011 Dec 2012Islamic Banking Industry as at

Dec 2012

Banking System as at Dec 2012

Total CASA 12.3 13.4 82.6 363.1

% of Total Deposits 43.4% 41.2% 26.9% 25.7%

Non CASA RM16,022m

CASA RM12,283m

Demand RM8,420m

Savings Mudharabah RM1,264m

CASA – RM13,426.1mNon CASA – RM19,157.1m

Demand RM8,968.6m

Savings Mudharabah RM1,942.2m

Savings Non-Mudharabah RM2,515.3m

…continues to focus on cheaper funds

BP 2013 - 2015 for BNM 280313

CASA GREW DESPITE INTENSE COMPETITION

19

RM’m

illio

n

… stiff competition ahead

BP 2013 - 2015 for BNM 280313

TOTAL CASA: BENCHMARKED AGAINST OTHER ISLAMIC BANKS

Managing Director’s Office 20

27.7%RM21.4b

15.8%RM12.2b

10.8%RM8.3b

9.4%RM7.2b

6.5%RM5.0b

24.8%RM16.6b

18.4%RM12.3b

10.4%RM6.9b

10.0%RM6.7b

5.6%RM3.7b

@ Dec 11@ Sept 12

Market Share

28.6%RM23.6b

16.3%RM13.4b

12.2%RM10.0b

8.7%RM7.2b

6.5%RM5.3b

@ Dec 12^

^Based on best proxy per Islamic banking operations disclosure in the audited account of the conventional banking group

28.6%RM23.6b

16.3%RM13.4b 12.2%

RM10.0b 8.7%RM7.2b 6.5%

RM5.3b

Islamic Banking CASA (excluding DFIs) forms

22.4% of Banking System.Growth of 15.4% to

RM77.0b.

TOTAL DEPOSITS: BENCHMARKED AGAINST OTHER ISLAMIC BANKS

Managing Director’s Office 21

20.7%RM59.1b

10.8%RM31.0b

10.7%RM30.7b

8.5%RM24.4b

7.2%RM20.7b

22.1%RM58.7b

10.6%RM28.3b

11.0%RM29.2b

7.5%RM20.0b

6.4%RM17.0b

@ Dec 11@ Sept 12

Market Share

23.3%RM71.3b

10.6%RM32.6b

12.7%RM38.9b

7.7%RM23.7b

7.1%RM21.7b

@ Dec12^

^Based on best proxy per Islamic banking operations disclosure in the audited account of the conventional banking group

23.3%RM71.3b

12.7%RM38.9b

10.6%RM32.6b 7.7%

RM23.7b7.1%

RM21.7b

Islamic Banking Deposits (excluding DFIs) forms

21.8% of Banking System.Growth of 15.1% to RM306.5b.

INCREASING TREND FOR AVERAGE YIELD ON TOTAL ASSETS

Managing Director’s Office 22

AVERAGE COST OF DEPOSITS INCREASED TOO

Managing Director’s Office 23

NET INCOME SPREAD (NIM) IMPROVED FROM 3.17% TO 3.25% YOY

Managing Director’s Office 24

…drop in net income spread in Q4 was mainly due to the Bank’s strategy to drive deposits and defend its market position.

…however continued financing growth has mitigated NIM erosion YoY.

KEY FINANCIAL RATIOS

25

AuditedFY

June 07

AuditedFY

June 08

Audited FY

June 09

ActualFYE Dec 2010**

Audited FYDec 11 **

Actual Dec 12

IslamicBanking System

Banking System

PROFITABILITY

Return on equity (%) – based on PBT 23.3% 26.5% 16.5% 14.4% 18.5% 20.4% ^ 19.6% * 17.5% *

Return on assets (%) – based on PBT 1.4% 1.5% 0.9% 1.2% 1.6% 1.7% ^ 1.4% * 1.6% *

Cost Income Ratio (%) 68.2% 60.8% 56.7% 55.4% 53.8% 51.4% 46.1% * 46.6% *

Non-Fund Based Income Ratio (%) 9.0% 7.8% 10.3% 10.8% 13.8% 13.5% 11.0% * 19.6% *

ASSET QUALITY

Gross Non-Performing/Impaired Financing Ratio (%) 24.7% 21.2% 16.4% 4.5% 2.6% 1.6% 1.6% # 2.0 % #

Net Non-Performing/Impaired Financing Ratio - Less IA & CA (%) 11.4% 7.8% 6.7% 1.1% -0.2% -0.7% -0.3% # -0.02% #

Financing Loss Coverage Ratio (%) 67.7% 75.8% 80.8% 77.2% 106.2% 142.6% 119.3% # 100.9% #

EFFICIENCY

Financing to Deposits (%) 57.6% 52.0% 43.5% 45.7% 51.5% 61.2% 77.2% # 78.7% #

CAPITALISATION

RWCR (%) – before proposed dividend 12.0% 12.9% 13.6% 16.8% 16.9% 14.1% 14.3% *

# 15.2% *#

^ Annualised * Bank Negara Malaysia Annual Report 2012 # Bank Negara Malaysia Monthly Statistical Bulletin @ Dec 2012 ** Restated arising from adoption of MFRS

…healthy capitalisation

…financing-to deposit ratio inching closer to optimum level

…cost income ratio continue to trend downwards

…commendable post 2006 asset quality

BP 2013 - 2015 for BNM 280313

FRANCHISE DEVELOPMENT – BRANCH NETWORK

Managing Director’s Office 26

Perlis - 1

Kedah - 10

Kelantan - 11Pulau Pinang - 5

Perak - 9

Pahang - 9

Terengganu - 5

Selangor – 25Kuala Lumpur - 17

NegeriSembilan -5

Melaka - 4

Johor - 14

Sarawak - 6

Sabah - 5

Labuan- 1

Region Total

Central 42

Northern 25

Eastern 25

Southern 23

East Malaysia 12

Total 127…127 branches as at end of 2012… 6 new branches in 2013 (Sungai Buloh, Bukit Indah (JB), Bandar Baru Tunjung (Kelantan) Sungai Petani (Kedah), Tabung Haji Convention Centre Sepang, & Senawang (N. Sembilan)

Managing Director’s Office 27

New Corporate Plan for 2013-2015

CORPORATE MASTER PLAN/ BLUEPRINT

BP 2013 - 2015 for BNM 280313

OCT 2006 – JUNE 2009 JULY 2009 – DEC 2012

…in our pursuit to be a “Global Leader in Islamic Banking”

JAN 2013 – DEC 2015

28

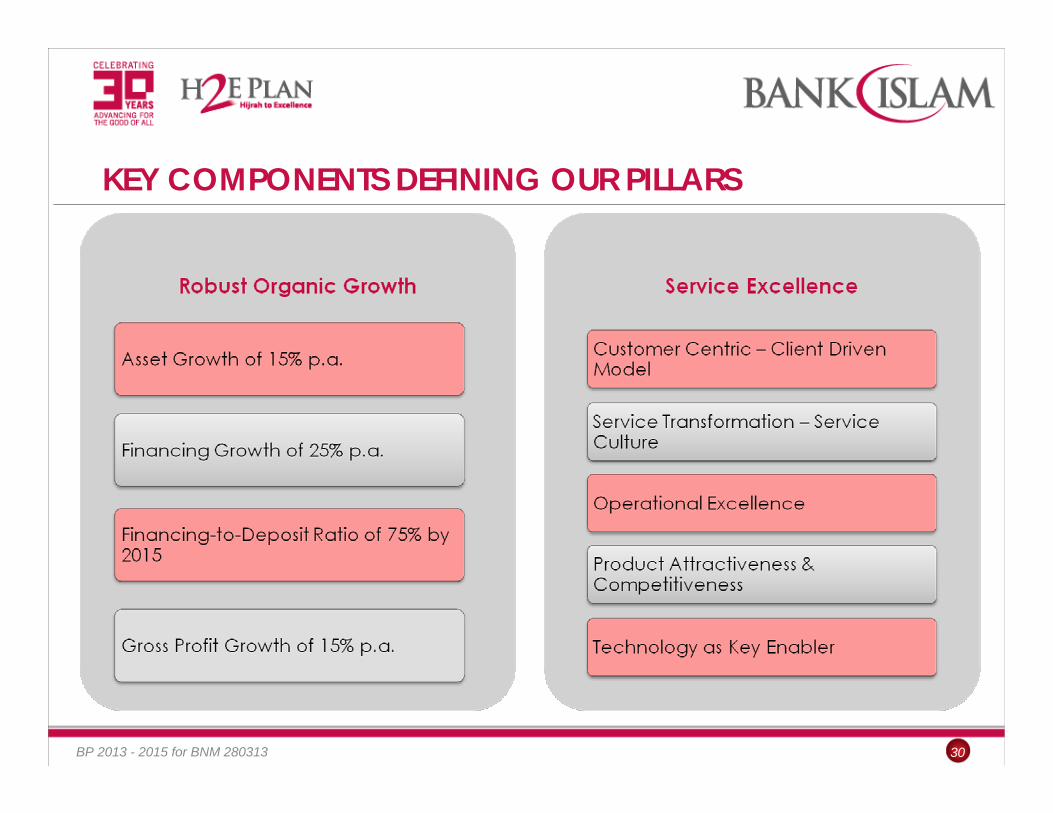

SIX PILLARS OF H2E PLAN

BP 2013 - 2015 for BNM 280313

Robust Organic Growth

Service Excellence

Shariah-led Innovation

Resource Optimisation

Employer of Choice

Regionalisation

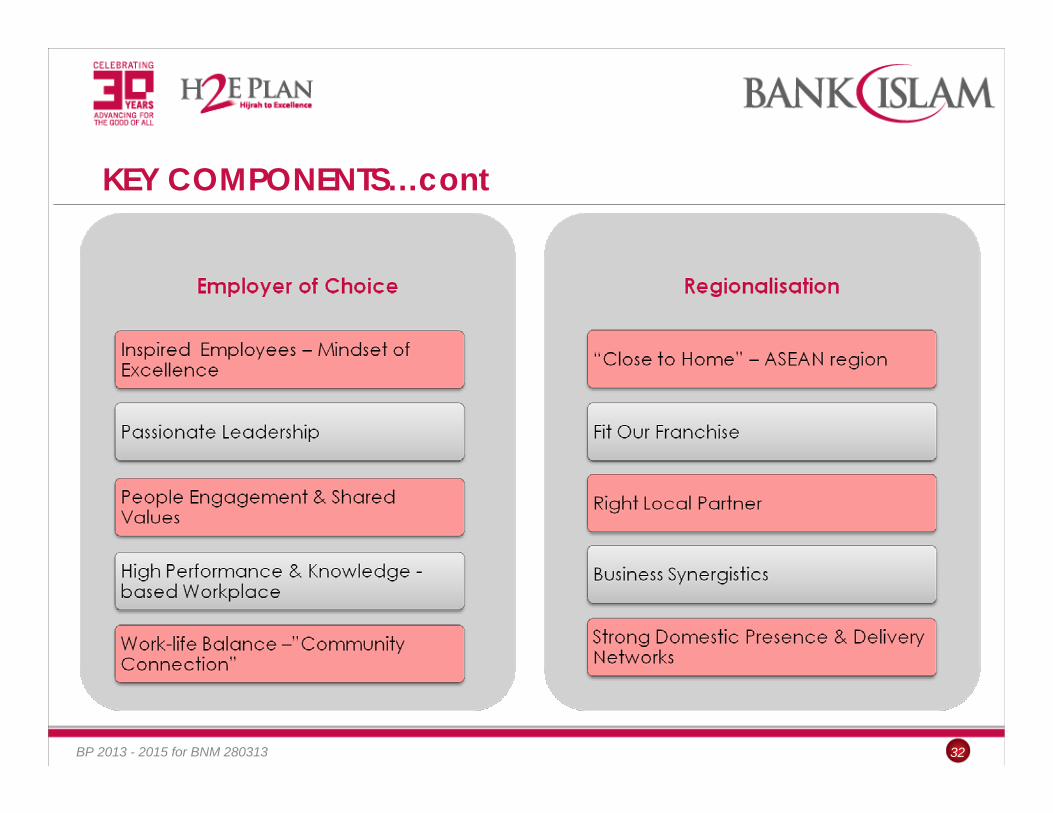

29

KEY COMPONENTS DEFINING OUR PILLARS

BP 2013 - 2015 for BNM 280313 30

KEY COMPONENTS…cont

BP 2013 - 2015 for BNM 280313 31

KEY COMPONENTS…cont

BP 2013 - 2015 for BNM 280313 32

Managing Director’s Office 33

Outlook

ISLAMIC BANKING: MOVING FORWARD

BP 2013 - 2015 for BNM 280313 34

Opportunities Challenges

www.bankislam.com.my

Managing Director’s Office 35

& Thank You

شكرا جزيال شكرا جزيال

Disclaimer: This presentation material has been prepared by Bank Islam Malaysia Berhad (the Bank”) for information purposes only and does not purport to contain all the information that may be required to evaluate the Bank or its financial position. No

representation or warranty, express r implied, is given by or on behalf of the Bank as to the accuracy of the information or opinions contained in this presentation. The presentation does not constitute or form part of an offer, solicitation or invitation of any offer, to buy or subscribe for any securities , nor should it or any part of it form the basis of, or be relied in any connection with, any contract, investment decision or commitment whatsoever. The Bank does not accept any liability whatsoever for any loss howsoever arising

from any use of this presentation or their contents or otherwise arising in connection therewith.