Embed Size (px)

Citation preview

Corporate Profile

4 July 2012

2K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Introduction to Kim Loong Resources Berhad

(“KLR”) Group

• KLR’s holding company, Sharikat Kim Loong Sendirian Berhad, had its beginning back in 1967 with a 1,000 acre rubber plantation in Ulu Tiram, Johor

• KLR is listed on the Main Market of Bursa Malaysia Securities Berhad since year 2000 and currently with a RM771 million market capitalisation

• KLR is primarily involved in oil palm cultivation and related businesses which include the following:

• More than 15,000 Ha of oil palm plantations in Sabah, Sarawak and Johor (excluding potential additional 3,600 Ha of plantable NCR land to be secured and developed)

• 3 palm oil mills located in Johor and Sabah with a total processing capacity of 235MT of FFB per hour

3K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Group Structure (Active Companies Only)AS AT 30 JUNE 2012

KIM

LOONG

RESOURCES

BERHAD

100%

Okidville

Holdings

Sdn. Bhd.

100%

Kim Loong

Palm Oil

Sdn. Bhd.

100%

Kim Loong

Sabah Mills

Sdn. Bhd.

100%

Kim Loong

Technologies

Sdn. Bhd.

90%

Winsome

Yields

Sdn. Bhd.

70%

Desa Kim Loong

Palm Oil

Sdn. Bhd.

70%

Kim Loong –

KPD Plantations

Sdn. Bhd.

70%

Palm

Nutraceuticals

Sdn. Bhd.

51%

Desa

Okidville

Sdn. Bhd.

100%

Kim Loong

Palm Oil Mills

Sdn. Bhd.

68%

Winsome

Al-Yatama

Sdn. Bhd.

70%

Sungkit

Enterprise

Sdn. Bhd.

60%

Kim Loong

Evergrow

Sdn. Bhd.

100%

Kim Loong

Power

Sdn. Bhd.

100%

Kim Loong

Corporation

Sdn. Bhd.

60%

Winsome Pelita (Pantu)

Sdn. Bhd.

100%

Kim Loong

Technologies

(Sabah)

Sdn. Bhd.

4K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

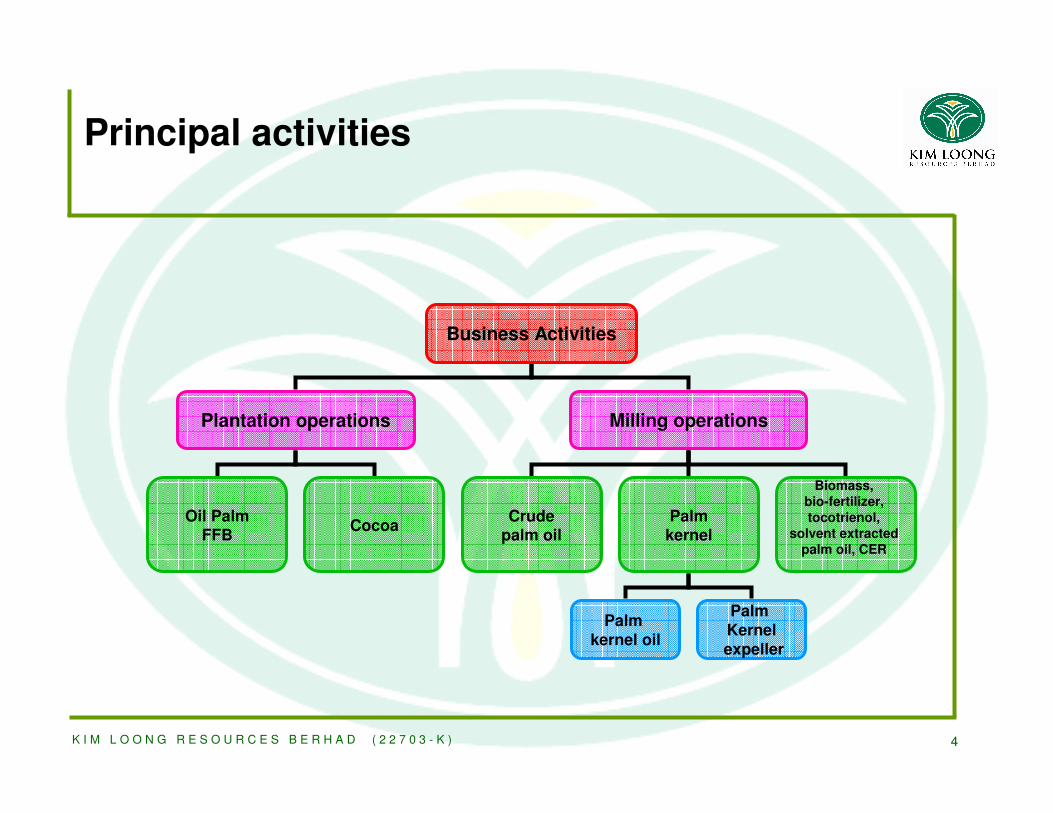

Principal activities

Business Activities

Plantation operations Milling operations

Oil PalmFFB

CocoaCrude

palm oilPalmkernel

Biomass,

bio-fertilizer,

tocotrienol,

solvent extracted

palm oil, CER

Palm kernel oil

Palm Kernelexpeller

5K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Recent Developments

Winsome Pelita (Pantu) Sdn. Bhd.

� Out of the total gross land area 10,471 Ha, the preliminary

estimated plantable area is approximately 6,500 Ha. To-date, we

have secured 2,210 Ha of which 1,780 Ha have already

been planted. The estimated plantable area is subject to Pelita

Holdings Sdn Bhd (“PHSB”), the Government agency which

monitors the implementation of the project, obtaining acceptance

from the NCR owners of those areas to participate.

� We plan to develop the remaining plantable land within the next 3

years.

6K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Financial Highlights

2011 2012 1Q2013*

Revenue (RM'000)563,408 768,332 157,762

EBITDA (RM'000) 111,649 189,848 34,977

Profit before tax (RM'000) 90,632 165,043 28,605

Weighted Average No. of Share ('000) 304,657 305,982 307,068

Shareholders' equity (RM'000) 445,143 507,355 526,835

Basic earnings per share (Sen)19.1 31.6 5.7

PE Ratio (times)12.5 7.9 N/A

Return on Capital Employed (Pre-tax) [N1]17.2% 26.7% 4.5%

Return on Total Equity (Pre-tax)18.4% 28.5% 4.8%

Return on Total Assets (Pre-tax)14.6% 23.0% 3.9%

Gearing 0.10 0.07 0.07

Financial year

FINANCIAL PERFORMANCE

* Based on unaudited 3 months results ended 30 April 2012.

N1 : Capital Employed includes Total Equity and Bank Borrowings.

7K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Financial Highlights (continued)

REVENUE

2011

RM'000

2012

RM'000

Plantation 126,282 197,299 33,011

Palm Oil Milling 561,757 766,907 156,382

Less : Inter-segment eliminations (124,631) (195,874) (31,631)

TOTAL GROUP 563,408 768,332 157,762

RESULTS

Plantation 66,228 134,591 14,878

Palm Oil Milling 27,053 35,952 9,667

93,281 170,543 24,545

Inter-segment eliminations 1,112 (4,535) 3,833

Unallocated cost ** (4,170) (3,808) (777)

Finance income 2,641 4,719 1,346

Finance cost (2,233) (1,876) (342)

Other investment income 1 - -

Profit before tax 90,632 165,043 28,605

1Q2013*

RM'000

Financial Year

ANALYSIS BY SEGMENTS

** Unallocated cost mainly consists of salaries and other office administration cost net of management fee and

commission income receivable.

* Based on unaudited 3 months results ended 30 April 2012.

8K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Financial Highlights

2011 2012

Net profit attributable to equity holders

of the Company (RM'000)

58,256 96,572 17,390

Net dividend declared (RM'000) 36,637 49,031** -

Gross Dividend Per Share (sen) 12.0 16.0 -

Gross Dividend Yield (%) 5.0% 6.4% -

Dividend Pay-out (%) 62.9% 50.8% -

Market Price at period end (RM) 2.38 2.50 2.61

NTA per share (RM) 1.46 1.66 1.71

1Q2013*

Financial Year

DIVIDEND PAYMENT RECORD

** An interim dividend of 6 sen single tier tax exempt paid on 18 November 2011 for the financial year ended 31 January 2012

and a final dividend of 10 sen single tier tax exempt proposed for the financial year ended 31 January 2012 payable on 29

August 2012.

.

* Based on unaudited 3 months results ended 30 April 2012.

9K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Oil palm estates (7,220 Ha)

Keningau

Oil palm estate(1,997 Ha),

Telupid

Oil palm estate(2,731 Ha),

Sandakan

Oil palm estate

(1,093 Ha) Kota

Tinggi, Johor

Plantation Operations :

PENINSULAR

MALAYSIA

SARAWAK

SABAH

Sandakan

Pasir Gudang

LOCATION OF OPERATIONS

Oil palm estates (6,500 Ha)

Sg.Tenggang/Kranggas

10K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Palm oil mill (90MT

FFB/hr), Sook, Keningau

Palm oil mill (100MT

FFB/Hr), Kota

Tinggi, Johor

Palm Oil Milling:

PENINSULAR

MALAYSIA

SARAWAK

SABAH

Sandakan

Pasir Gudang

MILLING LOCATION

Palm oil mill (45MT

FFB/hr), Telupid

11K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

StatisticsPRODUCTION, AREA AND AGE OF PALMS

PRODUCTION FINANCIAL YEAR

2012

(MT)

1Q2013

(MT)

%

FFB 313,035 51,869 16.6

CPO 210,784 37,807 17.9

PK 50,356 9,033 17.9

12K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

FFB PRODUCTION

PRODUCTION, AREA AND AGE OF PALMS (CONTINUED)

Statistics (continued)

248,268

272,334262,687

227,325

313,035

51,869

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2008 2009 2010 2011 2012 1Q2013

FINANCIAL YEAR

MT

FFB (MT)

13K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

FFB YIELD PER HECTARE

PRODUCTION, AREA AND AGE OF PALMS (CONTINUED)

22.18

24.33

21.71

17.39

19.0320.18

19.218.03

23.79

19.69

0

5

10

15

20

25

30

2008 2009 2010 2011 2012

FINANCIAL YEAR

MT

/Ha

KLR Group

Malaysia

Statistics (continued)

Notes: ▲The Group’s FFB yield for FY 2012 increased by 38% compared to FY 2011 mainly due to recovery in production in our estates in Keningau.

14K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

OIL YIELD PER HECTARE

PRODUCTION, AREA AND AGE OF PALMS (CONTINUED)

0

1

2

3

4

5

6

7

FINANCIAL YEAR

MT

/Ha

KLR - Sabah estate 5.34 5.70 5.39 4.47 6.24

Sabah state 4.89 4.85 4.52 4.30 4.63

2008 2009 2010 2011 2012

Statistics (continued)

Note :

The statistics for Sabah state are extracted from MPOB web-site based on calendar year 2007 to 2011 whilst the figures from KLR are based on its financial year (Feb – Jan).

15K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Statistics (continued)

CPO OER COMPARISON

18.8919.6919.65 19.88

23.11 23.14

21.27 20.74

0

5

10

15

20

25

2011 2012

FINANCIAL YEAR

%

KLR - Johor

Johor State

KLR - Sabah

Sabah State

PRODUCTION, AREA AND AGE OF PALMS (CONTINUED)

Note :

The statistics for Johor and Sabah state are extracted from MPOB web-site based on calendar year

2010 and 2011 whilst the figures from KLR are based on its financial year (Feb – Jan).

16K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

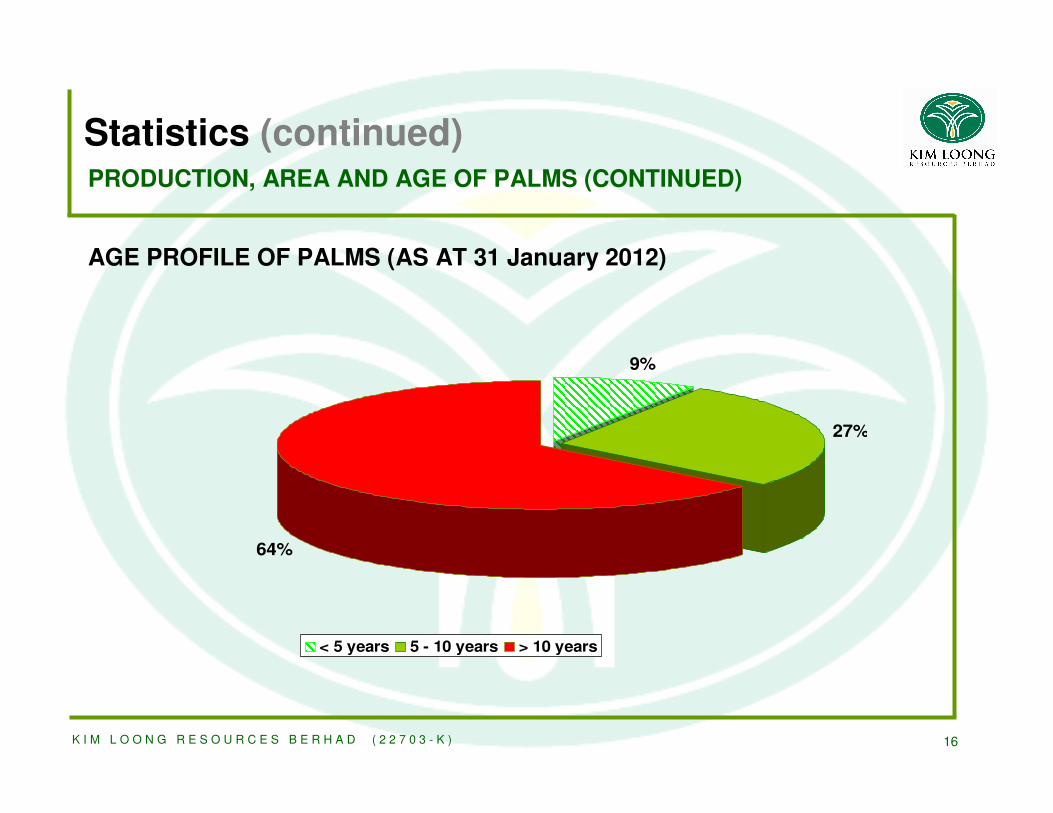

9%

27%

64%

< 5 years 5 - 10 years > 10 years

Statistics (continued)PRODUCTION, AREA AND AGE OF PALMS (CONTINUED)

AGE PROFILE OF PALMS (AS AT 31 January 2012)

17K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Achievements

» The FIRST Palm-pressed Fibre Oil Extraction (“PFOE”) plant in the World.

The Group has successfully commissioned the first PFOE plant in Kota Tinggi, Johor in September 2007

and operated profitably ever since. The second PFOE plant in Keningau, Sabah was commissioned in

September 2010 and is also running smoothly.

» The FIRST registered methane emission reduction CDM Project from palm oil

mill effluent in the World.

The Group has successfully registered its first biogas project in Kota Tinggi, Johor with the Clean

Development Mechanism (“CDM”) Executive Board of United Nations Framework Convention on Climate

Change (“UNFCCC”) on 8 April 2007. The plant was fully commissioned in August 2008 and is awaiting

certification of CER generated.

» Second biogas plant in Keningau was commissioned in October 2009.

18K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Achievements (continued)

KENINGAU MILL WAS

AWARDED BY MPOB AS

THE HIGHEST OER MILL

IN MALAYSIA IN YEAR

2007 & 2005.

19K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Achievements (continued)

KIM LOONG RESOURCES

BERHAD RECEIVED THE

SHAREHOLDER VALUE AWARD

2010 (AGRICULTURE &

FISHERIES SECTOR) FROM

KPMG MALAYSIA .

20K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Competitive Strengths

1. High FFB production yield will lead to strong cash flows and

financial position :

» A large proportion of palm trees in our estates is at its prime age which

offer strong FFB production yield.

21K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

300,000 315,000

020,00040,00060,00080,000

100,000120,000140,000160,000180,000200,000220,000240,000260,000280,000300,000320,000340,000360,000380,000400,000

2013 2014

FINANCIAL YEAR

MT

(F

FB

) Projection

Estimate

Note : Projection of production is based on existing land bank.

FFB PRODUCTION PROJECTION

Competitive Strengths (continued)

22K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Competitive Strengths (continued)

2. High OER to ensure our mill remain competitive :

» Higher OER from mills will generate higher processing margin for mills and able to offer competitive FFB price to attract external crops. This will also improve efficiency in terms of oil yield per Ha.

Kota Tinggi mill Keningau mill Telupid mill

23K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

The Company has achieved complete integration of milling operations

resulting in improved efficiency and at the same time generating

additional income from wastes. We have positively contributed towards

reducing the pollution impact of our palm oil mills on the environment

and improved sustainability of palm oil production.

Some of our projects in improving efficiency and conversion of wastes

through new innovation and technology are as follow:

- PFOE plant in our Kota Tinggi mill & Keningau mill

� The plant will extract residual oil from pressed fibre and increase OER by

about 0.5%.

� Profit after tax based on average selling price of RM3,090/MT in FY2012

is RM2.3 million in Kota Tinggi mill.

Competitive Strengths (continued)

3. Improved efficiency and additional income from wastes in Mill

24K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

(Cont’d)

- Biogas CDM project at Kota Tinggi mill, Keningau mill & Telupid mill

� This project will reduce greenhouse gas emissions from palm oil mill effluent by capturing the methane gas emissions to generate power/ steam, thereby reducing environmental impact of milling operations.

� Expected CER sale will generate tax free profit of RM2 million per year when in full operation.

- Full conversion of biomass into fuel for milling operations.

� Sale of surplus shell to replace usage of fossil fuel. The revenue for FY2012 from the sale of shell to third parties is RM1.9 million from Kota Tinggi mill.

- Bio-fertiliser plant at Kota Tinggi mill

� Convert part of the oil palm biomass and decanter solids into bio-fertilizers for local and international markets. However, contribution from this plant is much reduced in FY2012 owing to lack of raw materials.

Competitive Strengths (continued)

3. Improved efficiency and additional income from wastes in Mill

25K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Competitive Strengths (continued)

� Latest planting material and technology shall be used to improve yield potential from plantation operations.

� Recycling mill wastes to improve soil in plantations.

� To improve productivity and reduce reliance on foreign labour through mechanisation on certain activities and areas suitable for mechanisation.

4. Commitment to improve efficiency in Plantation

26K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Competitive Strengths (continued)

5. Management Capability

» Top management has over 40 years’ experience in oil palm industry.

» Capable managers and supporting staffs in all business entities.

» Ability to identify commercially viable projects for expansion or

diversification backed by strong in-house research capability

27K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

BUSINESS

OUTLOOK

AND

STRATEGIES

28K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Near Term Prospect

Plantation

» The FFB production for plantation operations in FY2012 is 38% higher than the quantity achieved in FY2011 which was mainly from our estates in Keningauregion which had recovered from the exceptional low yield last year. FFB price was also 16% higher in FY2012 compared to in FY2011.

» The Group’s FFB production for FY2013 is expected to be slightly lower than FY2012 due to replanting of 900 Ha of oil palm in FY2012 and FY2013 and industry wide decline in yield owing to palm exhaustion caused by high FFB yield in FY2012.

» Our main focus in the near term is to secure and plant up the NCR land within our project area in Sarawak. We expect the FFB production for the Group to grow from FY2014 onwards. The growth is contributed from our young palm from Johorand new planting in Sarawak and replanting in Sabah.

» Profit is expected to remain good in FY2013 due to the steady CPO price.

29K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Near Term Prospect (continued)

Mill

» We expect the profits from our milling operations to remain good in FY2013.

» Increasing crops from newly matured plantations near our existing mills will improve capacity utilisation.

» Estimated increase sales of excess palm kernel shells to third parties to a total of over RM4.0 million from all three mills in FY2013.

» Both solvent extraction plants in our Kota Tinggi and Keningau mills are running satisfactorily, generating substantial revenue for the Group.

» The PFOE plant at Keningau can increase the OER by approximately 0.5% which is equivalent to about RM5.0 million increase in annual revenue for milling operations based on the estimated CPO price of RM3,200/MT.

30K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Development of Downstream Projects

(a) Implementation of biogas CDM project

� After successful installation of the biogas plant in Kota Tinggi and Keningau, we are currently installing the 3rd biogas plant at our Telupid mill.

� To minimise disruption to supply of power even during low crops period/mill shut down for maintenance to our downstream project such as kernel crushing, solvent extraction, bio-fertiliser as well as staff and labour quarters, we are implementing a gas engine system to all our 3 mills to efficiently convert biogas generated from palm oil mill effluent (“POME”) into power.

31K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Development of Downstream Projects

(continued)

(b) Kernel Oil Solvent Extraction Plant at Kota Tinggi

� The plant has been successfully commissioned in February 2012 and

started commercial operations.

� The plant will increase the PKO extraction rate by approximately

2%.

� At current high price of PKO, the estimated additional revenue is RM2

million.

32K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

KLR Group’s Future Plan

KLR’s future plan include the following:

� To source for additional plantation land in Johor, Kelantan,

Sabah and Sarawak.

� Future sales of de-oiled fibre and empty fruit bunches as raw

materials for other downstream products.

� To generate power from biogas for sale to TNB national and

Sabah Electricity Sdn. Bhd. grid.

33K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

THANK YOU

(22703-K)

(Incorporated in Malaysia under the Companies Act, 1965)

Contact person : Mr Gooi Seong Lim (Executive Chairman)

Tel : 607-2248316

Email : [email protected]

34K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Corporate Fact Sheet

Corporate Address Lot 18.01, 18th Floor, Public Bank Tower

19, Jalan Wong Ah Fook,

80000 Johor Bahru, Johor, Malaysia

Directors Gooi Seong Lim Executive Chairman

Gooi Seong Heen Managing Director

Gooi Seong Chneh Executive Director

Gooi Seong Gum Executive Director

Gan Kim Guan Senior Independent Director

Chew Poh Soon Independent Director

Chan Weng Hoong Independent Director

Cheang Kwan Chow Independent Director

35K I M L O O N G R E S O U R C E S B E R H A D ( 2 2 7 0 3 - K )

Corporate Fact Sheet (continued)

Stock Exchange Listing Main Market of Bursa Malaysia Securities Berhad

Listed on 27 November 2000

Issued shares 308.4 million shares of RM1.00 par value

Market Cap RM771 million (based on share price of RM2.50 on 30 June 2012)

Major Shareholders Sharikat Kim Loong Sendirian Berhad 63.64%

(as at 7 June 12) Teo Chuan Keng Sdn Bhd 1.94%

Krishnan Chellam 1.73%

Timbas Helmi Bin Oesman Joesoef Helmi 1.20%

ECM Libra Foundation 0.94%

Financial year end 31 January