Embed Size (px)

DESCRIPTION

Book Review : ‘ Energy Derivatives: Pricing and Risk Management ’ by Clewlow and Strickland , 2000. Anatoliy Swishchuk Math & Comp Lab Dept of Math & Stat, U of C ‘Lunch at the Lab’ Talk November 7 th , 2006. About the Authors: Clewlow, Les. About the Authors: Strickland, Chris. - PowerPoint PPT Presentation

Citation preview

Book Review: ‘Energy Derivatives: Pricing and Risk Management’ by Clewlow and

Strickland, 2000

Anatoliy Swishchuk

Math & Comp Lab

Dept of Math & Stat, U of C

‘Lunch at the Lab’ Talk

November 7th, 2006

About the Authors: Clewlow, Les

About the Authors: Strickland, Chris

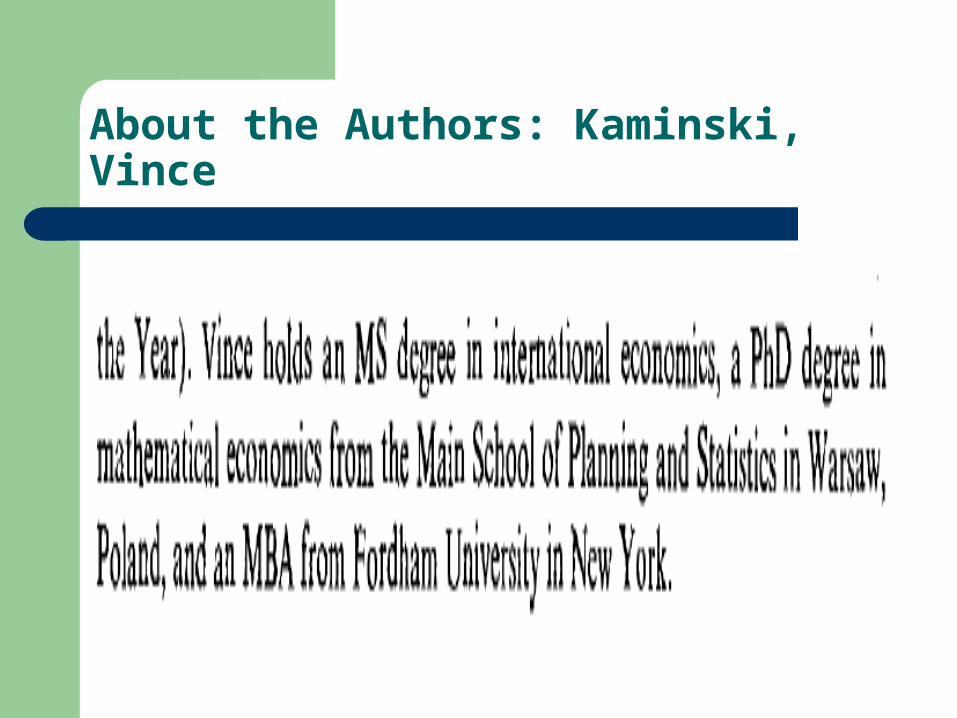

About the Authors: Kaminski, Vince

About the Authors: Kaminski, Vince

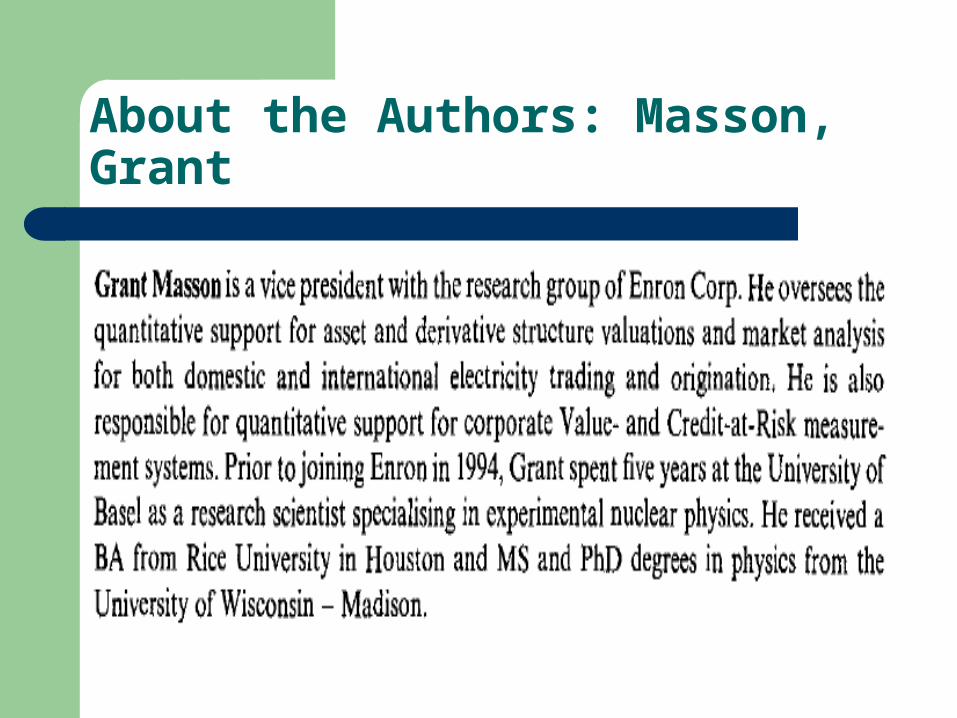

About the Authors: Masson, Grant

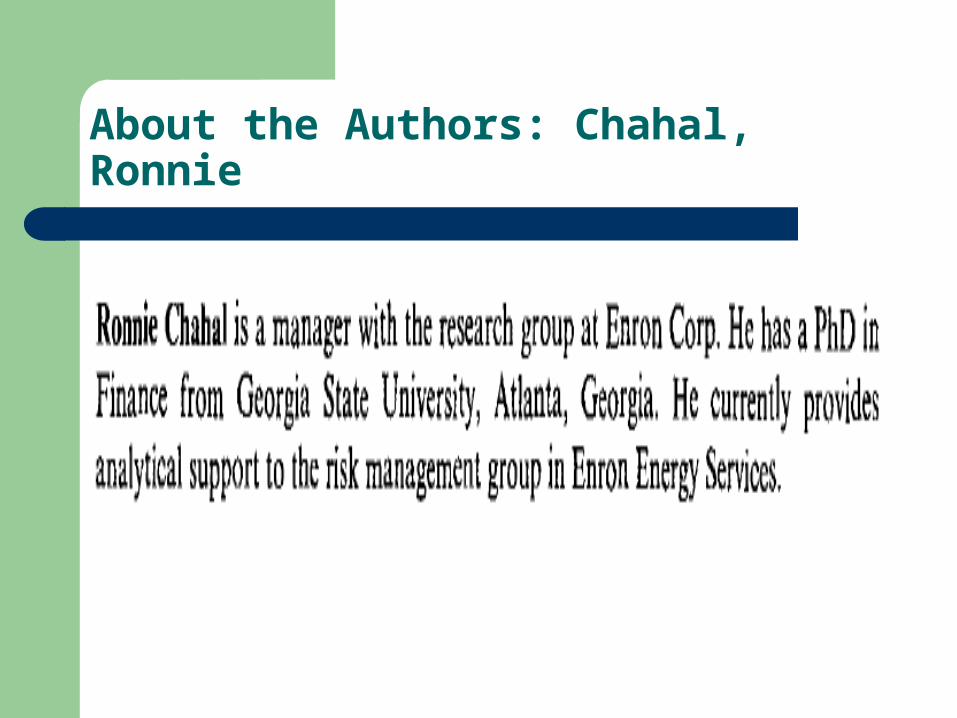

About the Authors: Chahal, Ronnie

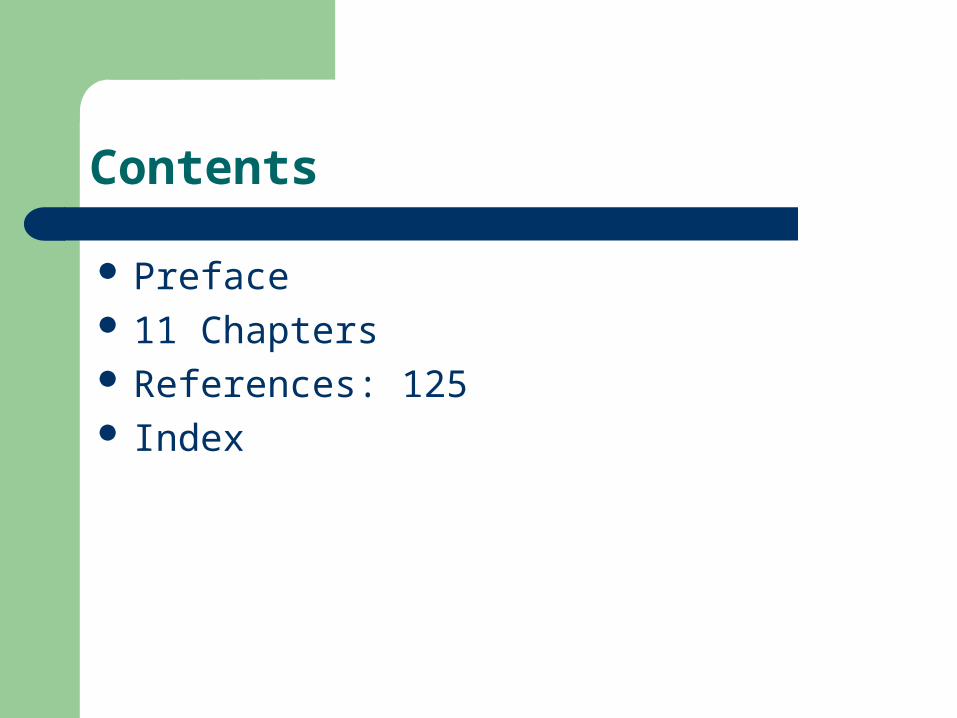

Contents

Preface 11 Chapters References: 125 Index

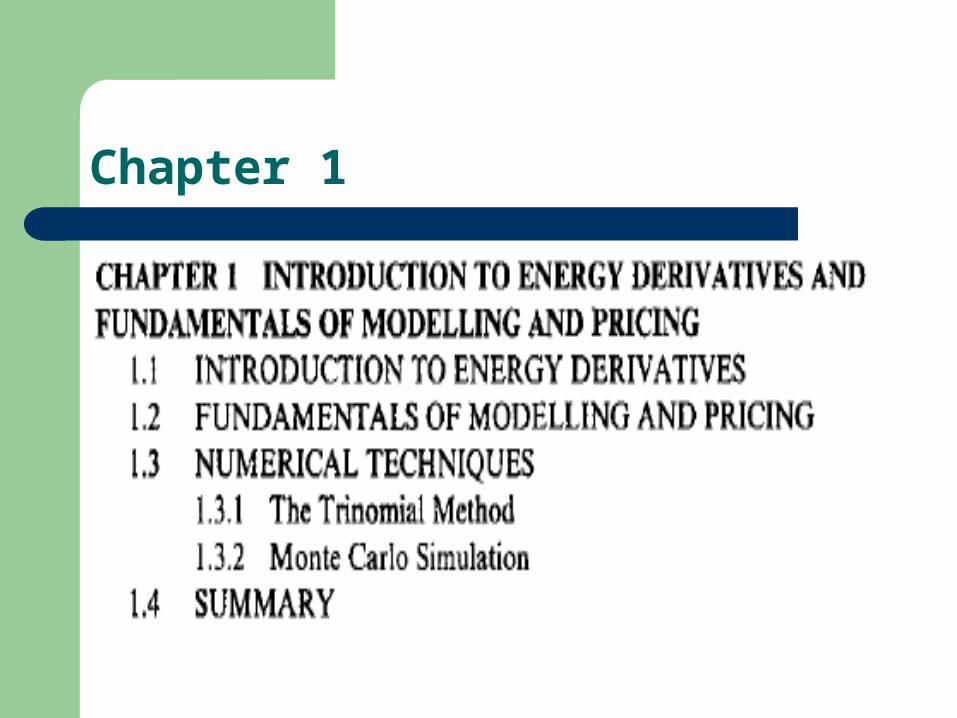

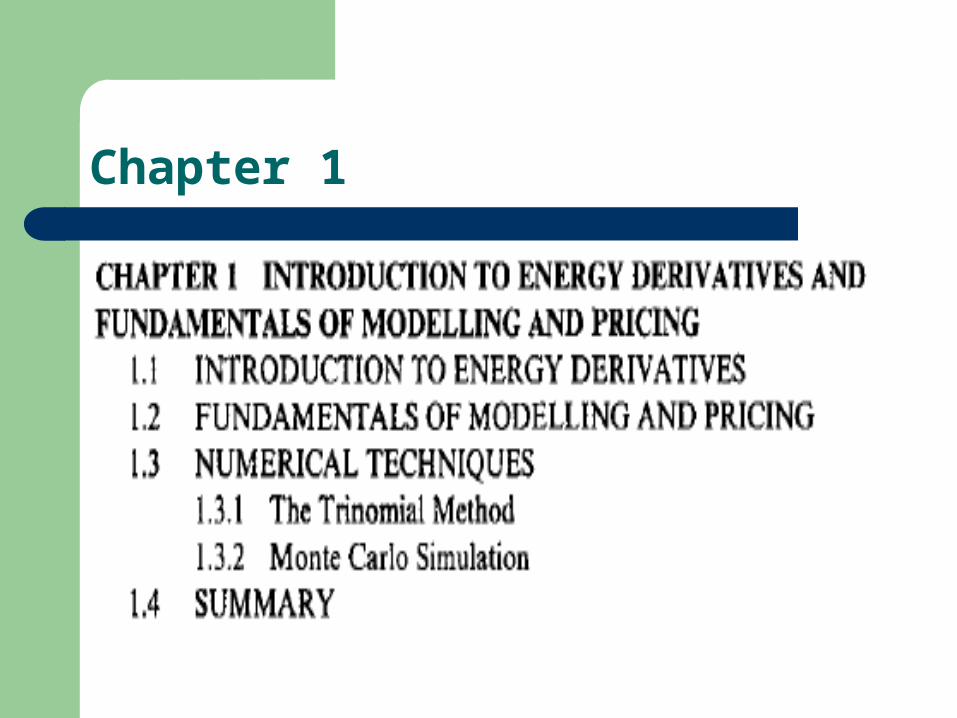

Chapter 1

Chapter 2

Chapter 3

Chapter 3 (cntd)

Chapter 4

Chapter 5

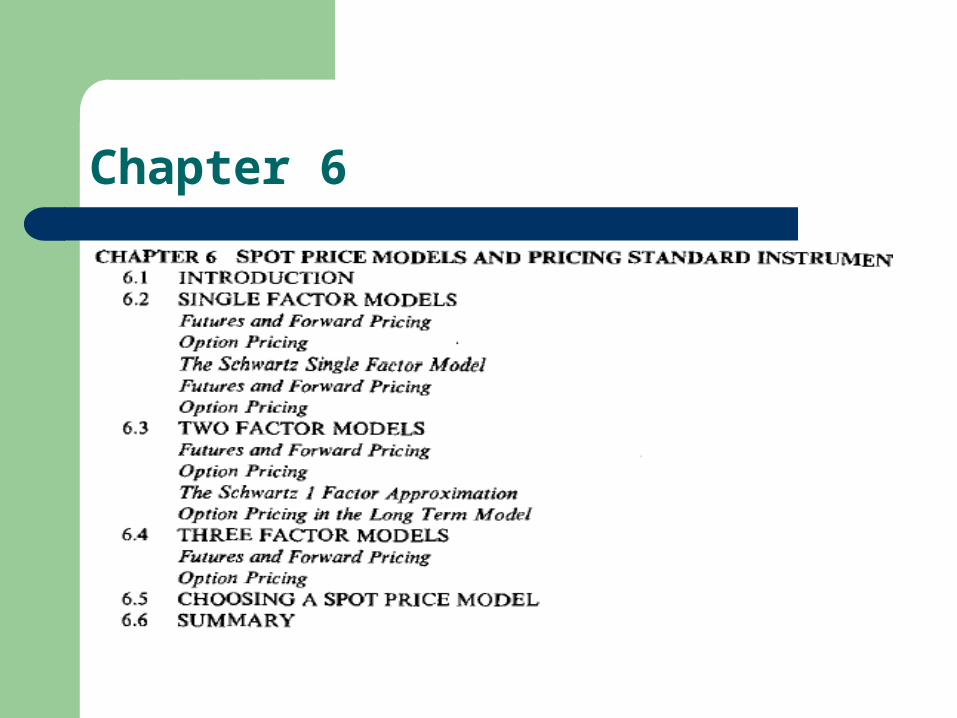

Chapter 6

Chapter 7

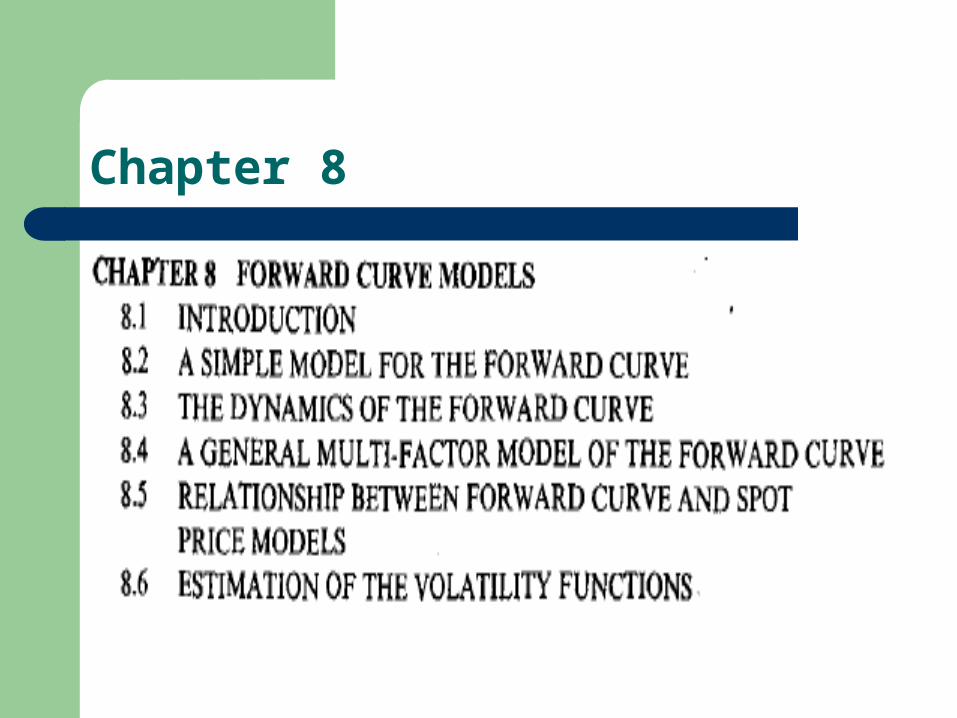

Chapter 8

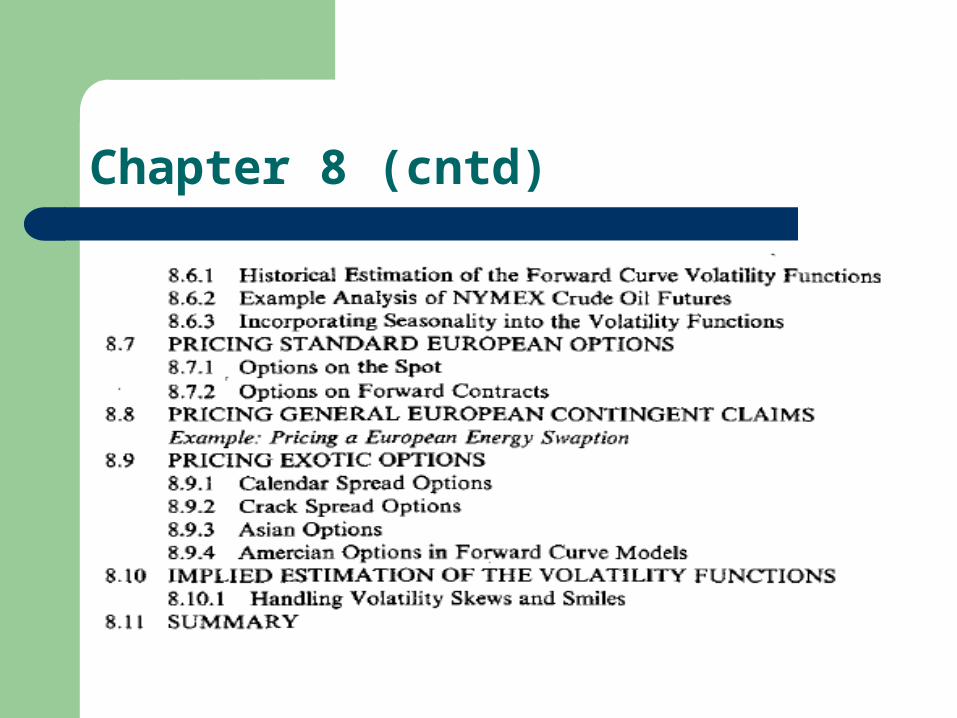

Chapter 8 (cntd)

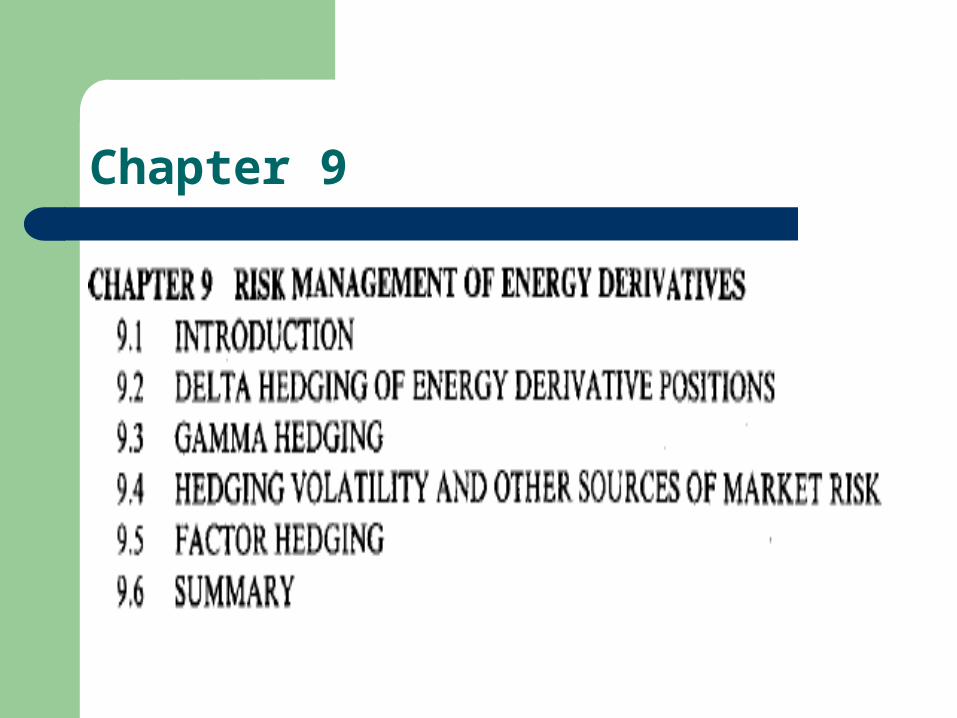

Chapter 9

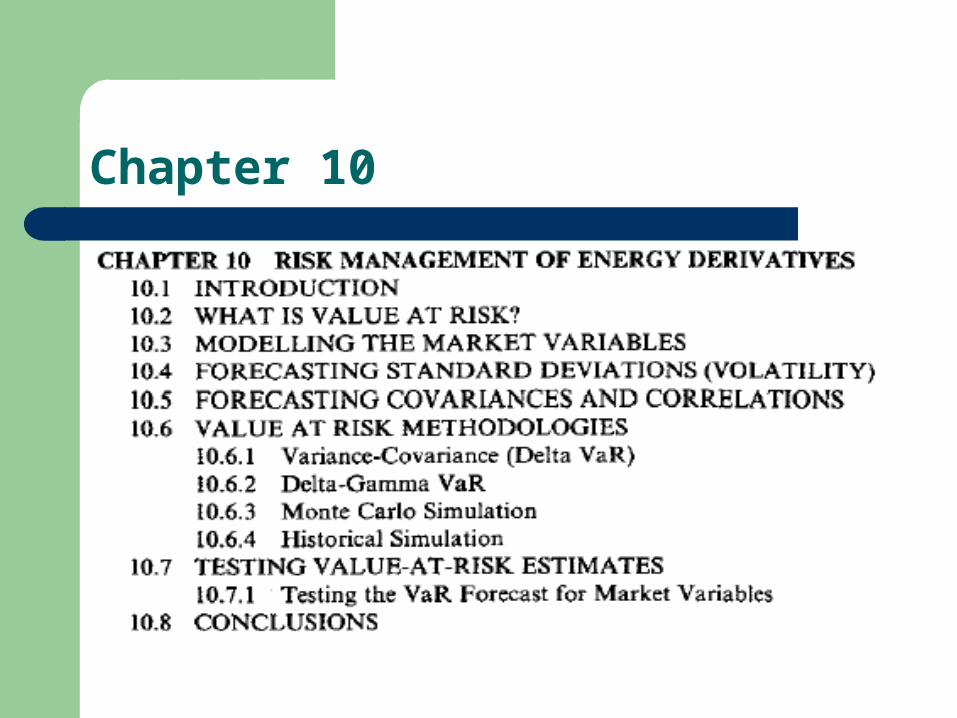

Chapter 10

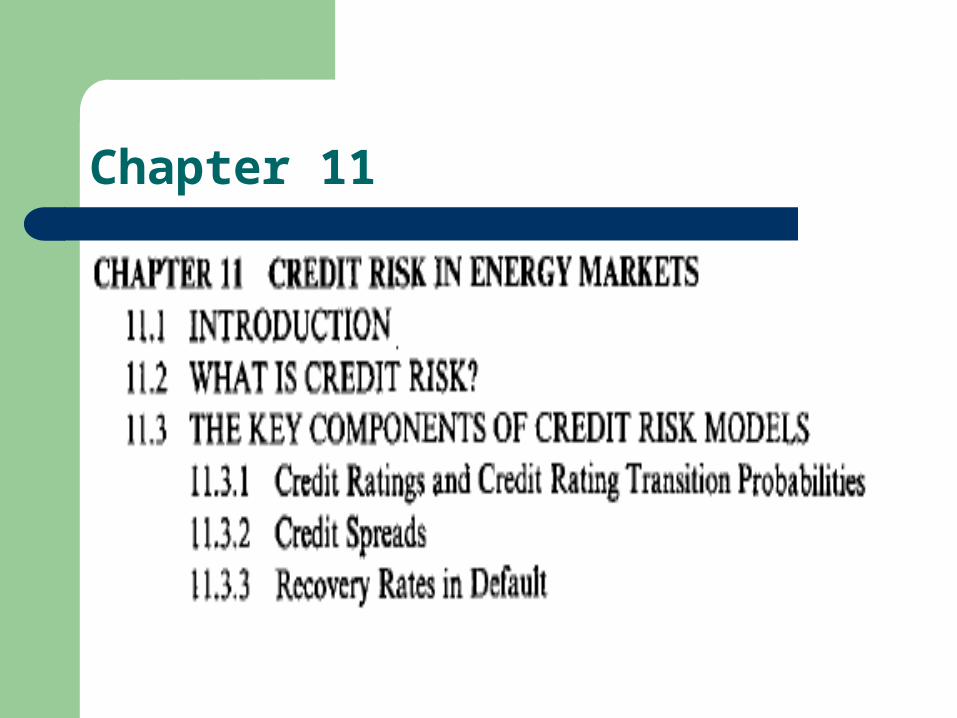

Chapter 11

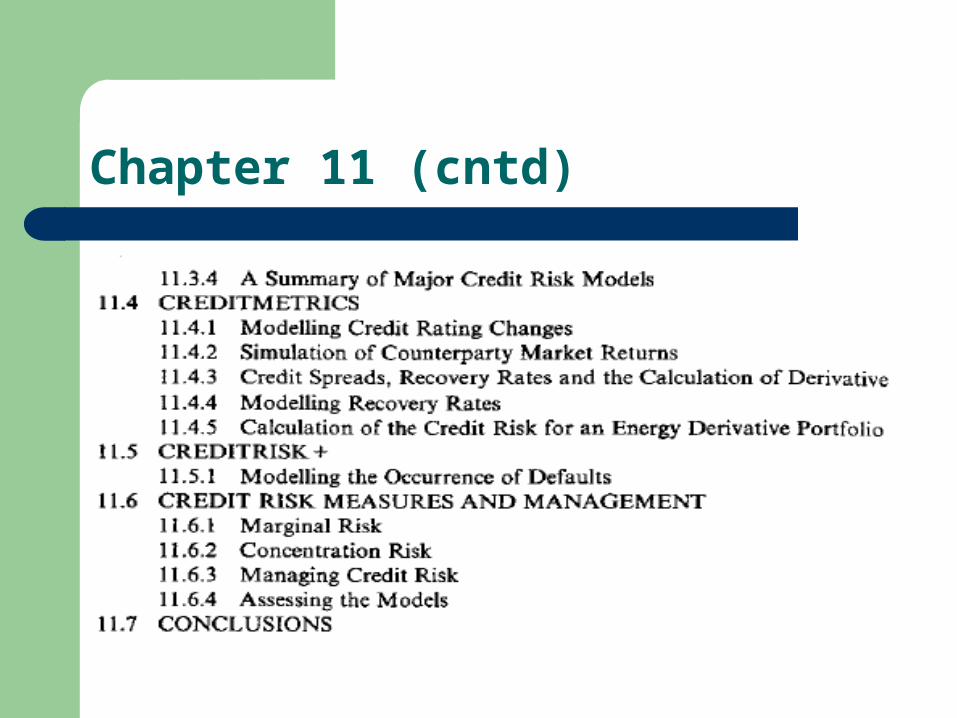

Chapter 11 (cntd)

Chapter 1

Ch. 1 (1.1. Intro to Energy Derivatives)

A Derivative Security: security whose payoff depends on the value of other more basic variables

Deregulation of energy markets: the need for risk management

Energy derivatives-one of the fastest growing of all derivatives markets

The simplest types of derivatives: forward and futures contracts

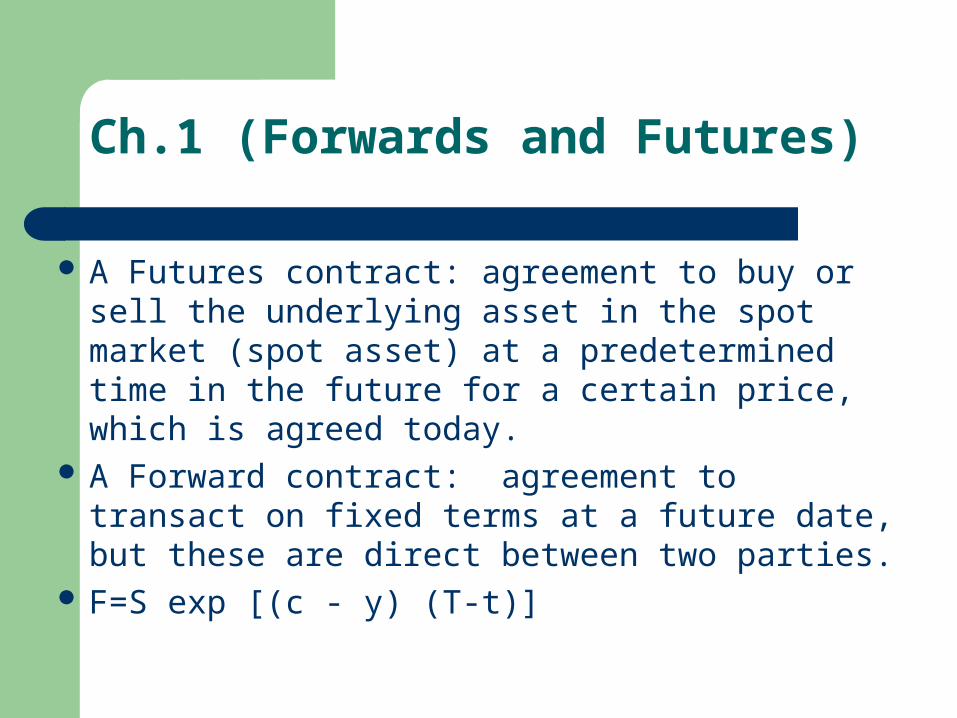

Ch.1 (Forwards and Futures)

A Futures contract: agreement to buy or sell the underlying asset in the spot market (spot asset) at a predetermined time in the future for a certain price, which is agreed today.

A Forward contract: agreement to transact on fixed terms at a future date, but these are direct between two parties.

F=S exp [(c - y) (T-t)]

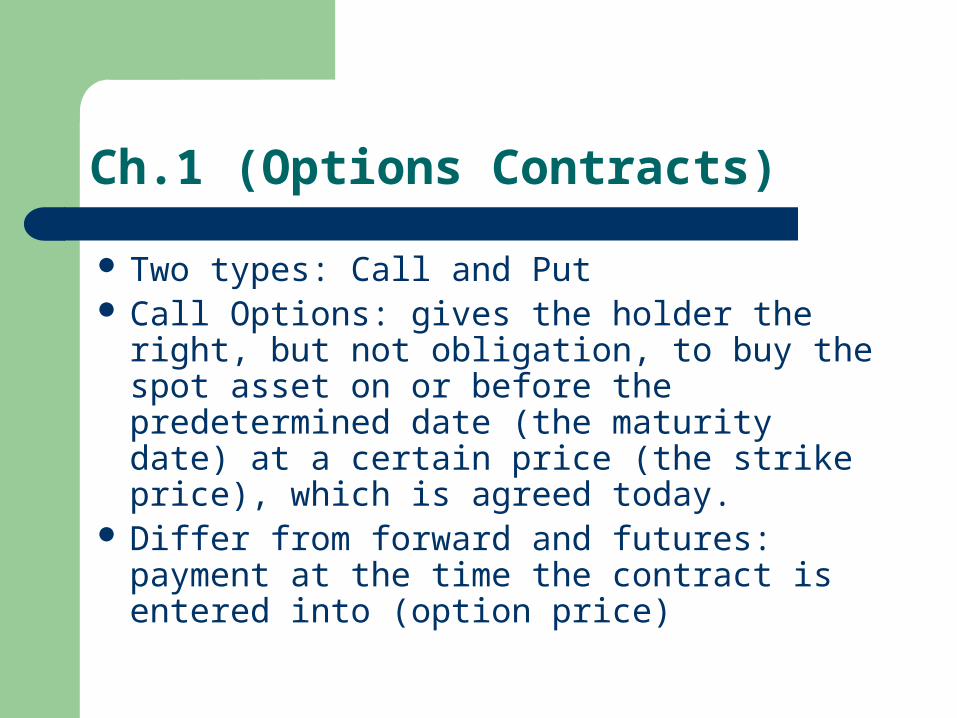

Ch.1 (Options Contracts)

Two types: Call and Put Call Options: gives the holder the right, but

not obligation, to buy the spot asset on or before the predetermined date (the maturity date) at a certain price (the strike price), which is agreed today.

Differ from forward and futures: payment at the time the contract is entered into (option price)

Ch.1 (Options Contracts II)

Ch. 1(1.2. Fundamentals of Modelling and Pricing)

F. Black, M. Scholes, R. Merton (1973)-BSM approach

SDE (GBM)

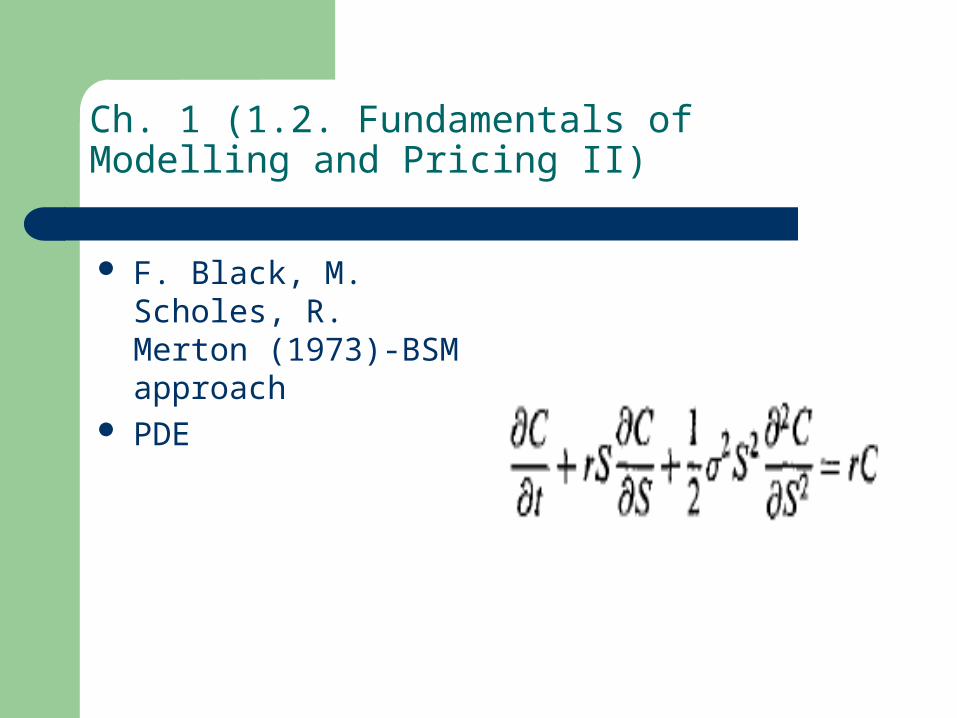

Ch. 1 (1.2. Fundamentals of Modelling and Pricing II)

F. Black, M. Scholes, R. Merton (1973)-BSM approach

PDE

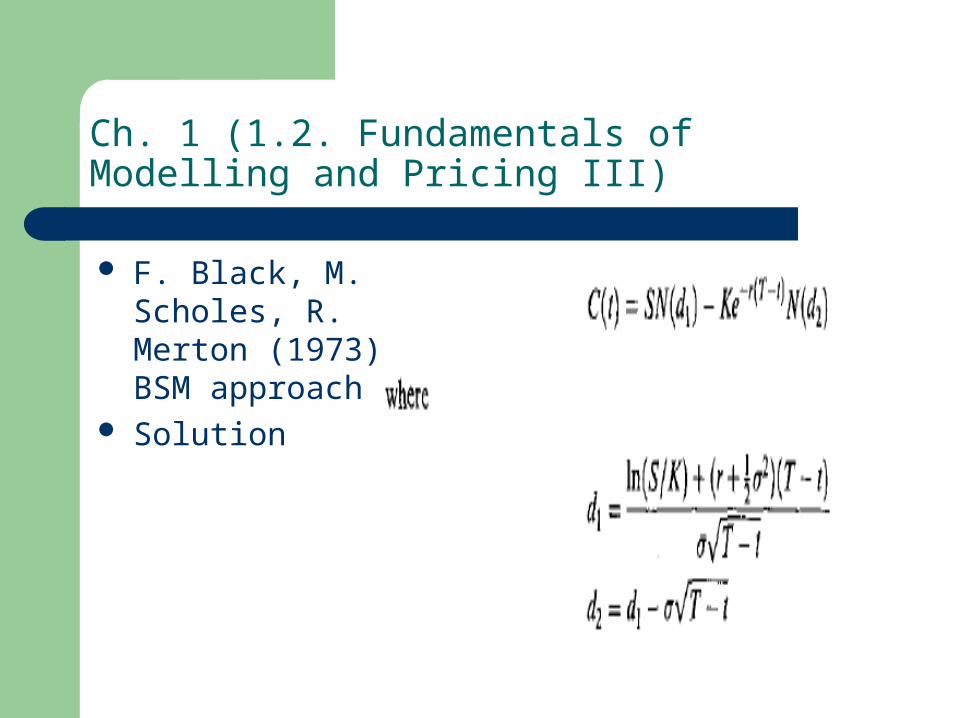

Ch. 1 (1.2. Fundamentals of Modelling and Pricing III)

F. Black, M. Scholes, R. Merton (1973)-BSM approach

Solution

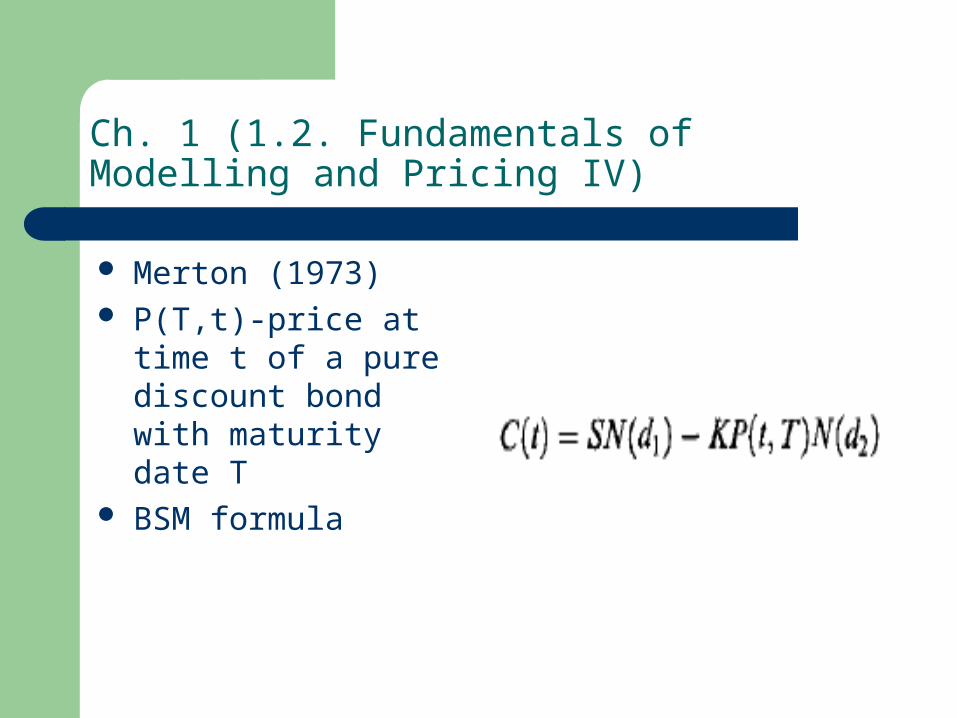

Ch. 1 (1.2. Fundamentals of Modelling and Pricing IV)

Merton (1973) P(T,t)-price at time t of

a pure discount bond with maturity date T

BSM formula

Ch. 1 (1.3. Numerical Techniques)

Trinomial Tree Method (this book) Monte Carlo Simulation (this book) Finite difference schemes (another one) Numerical integration (-//-) Finite element methods (-//-)

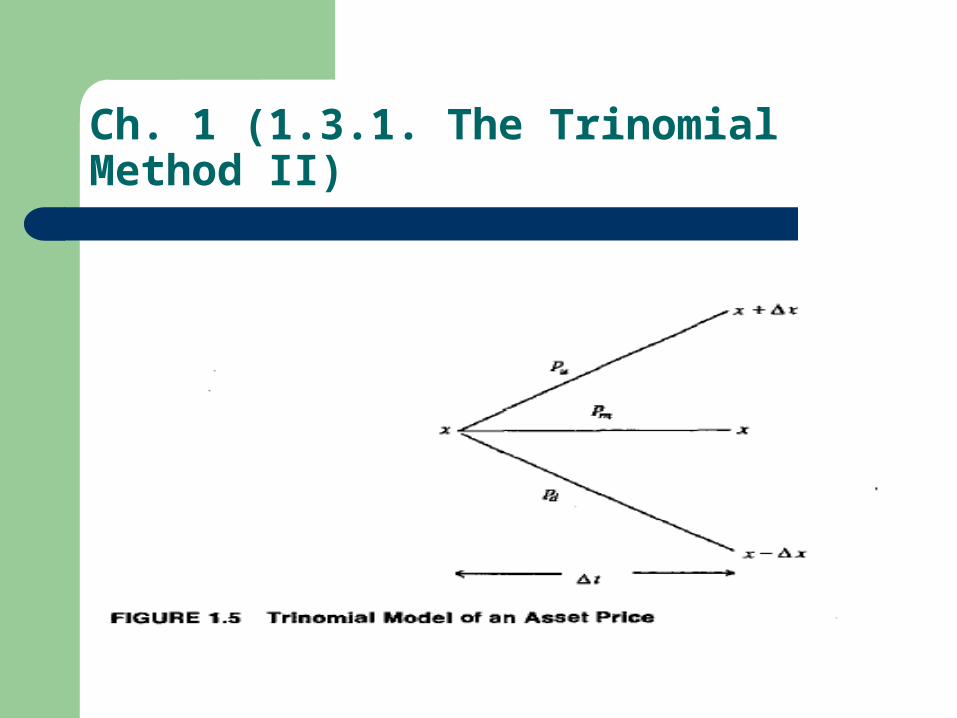

Ch. 1 (1.3.1. The Trinomial Method)

Alternative to binomial model by Cox, Ross, Rubinstein (1979): continuous-time limit is the GBM

Provide a better approximation to a continuous price process

Easier to work with (more regular grid and more flexible)

Ch. 1 (1.3.1. The Trinomial Method II)

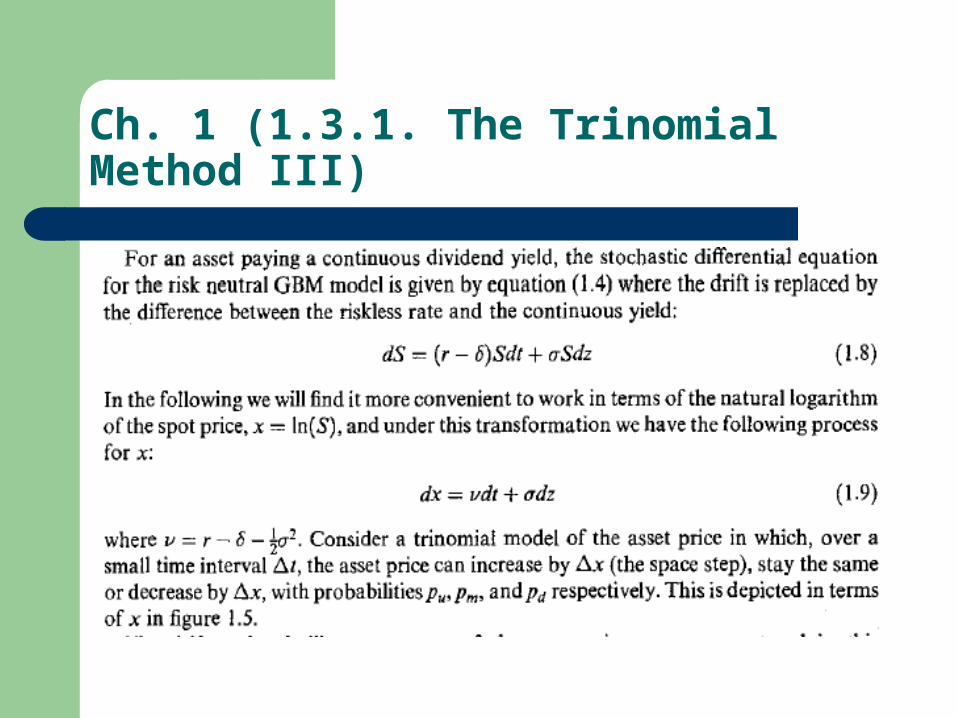

Ch. 1 (1.3.1. The Trinomial Method III)

Ch. 1 (1.3.1. The Trinomial Method IV)

Ch. 1 (1.3.1. The Trinomial Method V)

Ch. 1 (1.3.1. The Trinomial Method VI)

Ch. 1 (1.3.1. The Trinomial Method VII)

Ch. 1 (1.3.1. The Trinomial Method VIII) (The value of option)

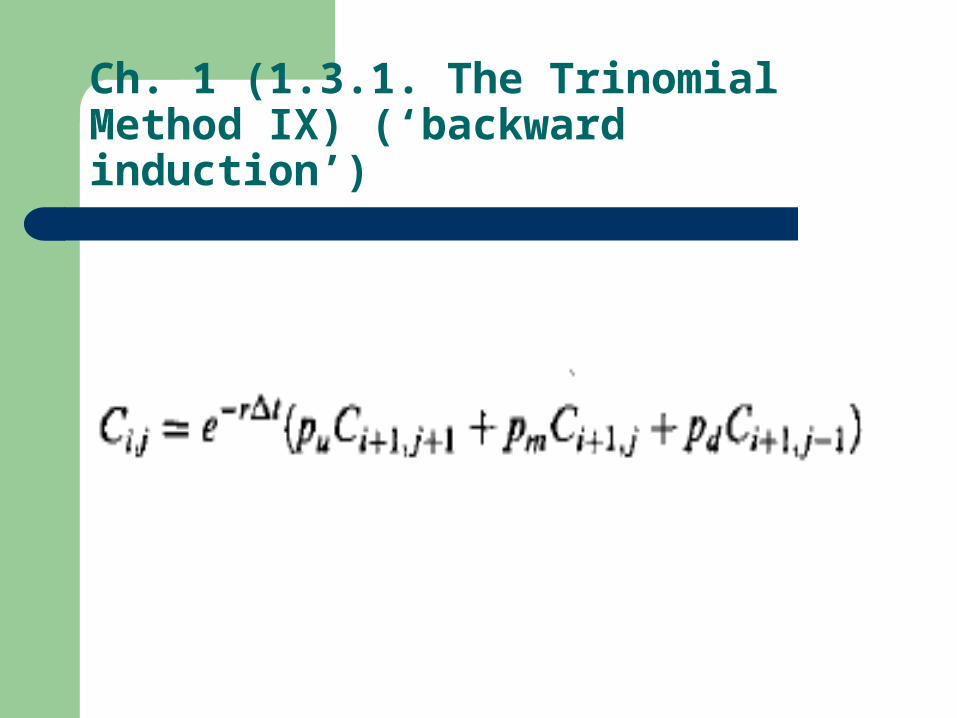

Ch. 1 (1.3.1. The Trinomial Method IX) (‘backward induction’)

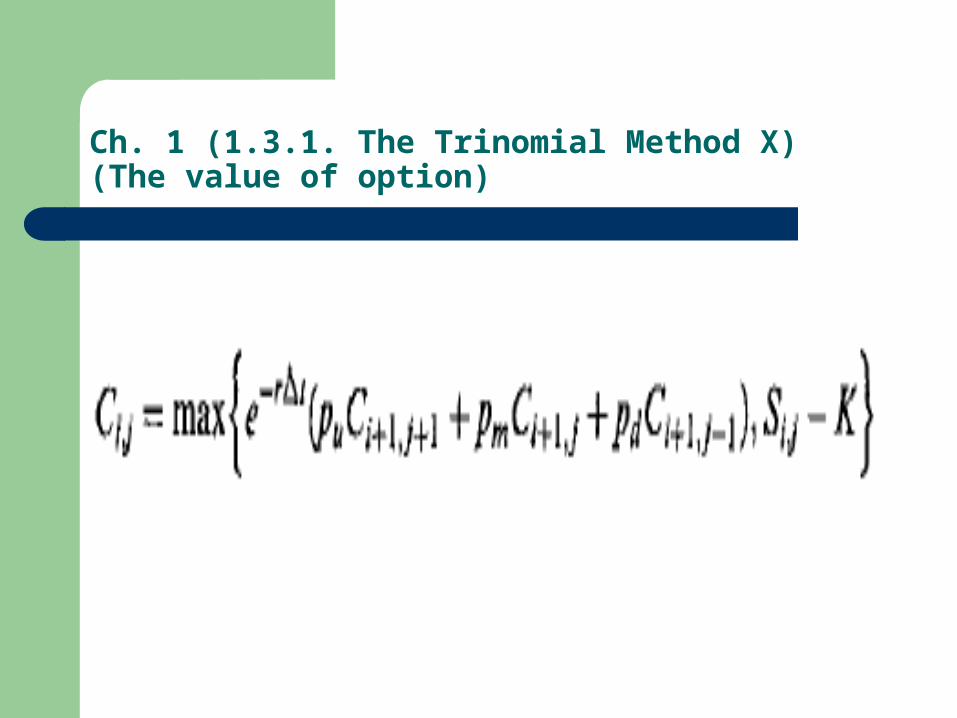

Ch. 1 (1.3.1. The Trinomial Method X) (The value of option)

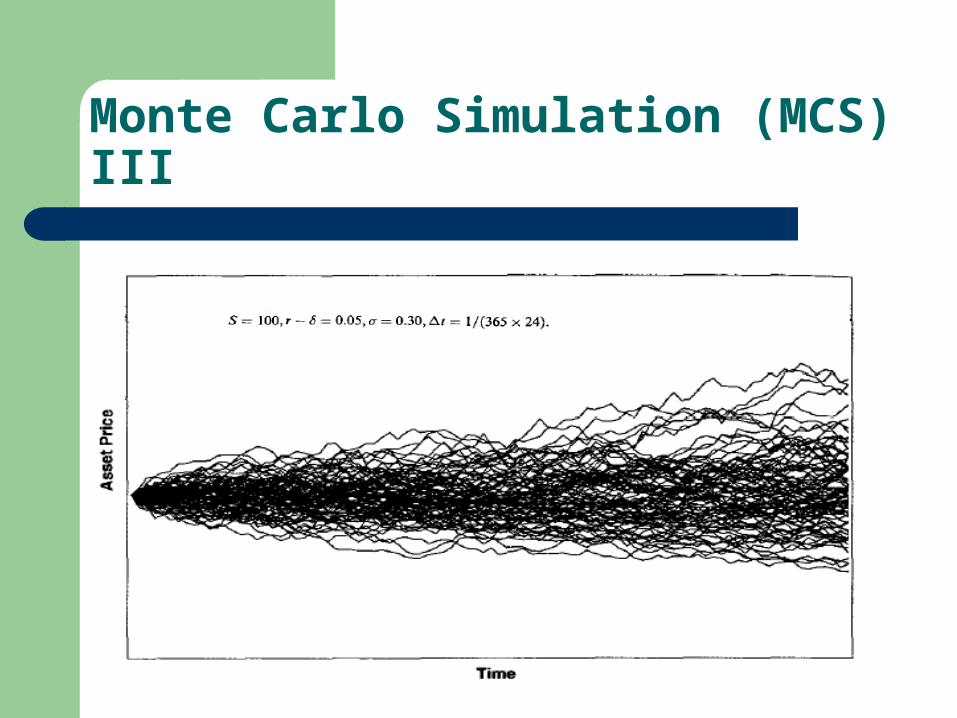

Monte Carlo Simulation (MCS)

MCS: estimation of the expectation of the discounted payoff of an option by computing the average of a large number of discounted payoff computed via simulation

Felim Boyle (UW, 1977)-first applied MCS to the pricing of financial instruments

Monte Carlo Simulation (MCS) II

Monte Carlo Simulation (MCS) III

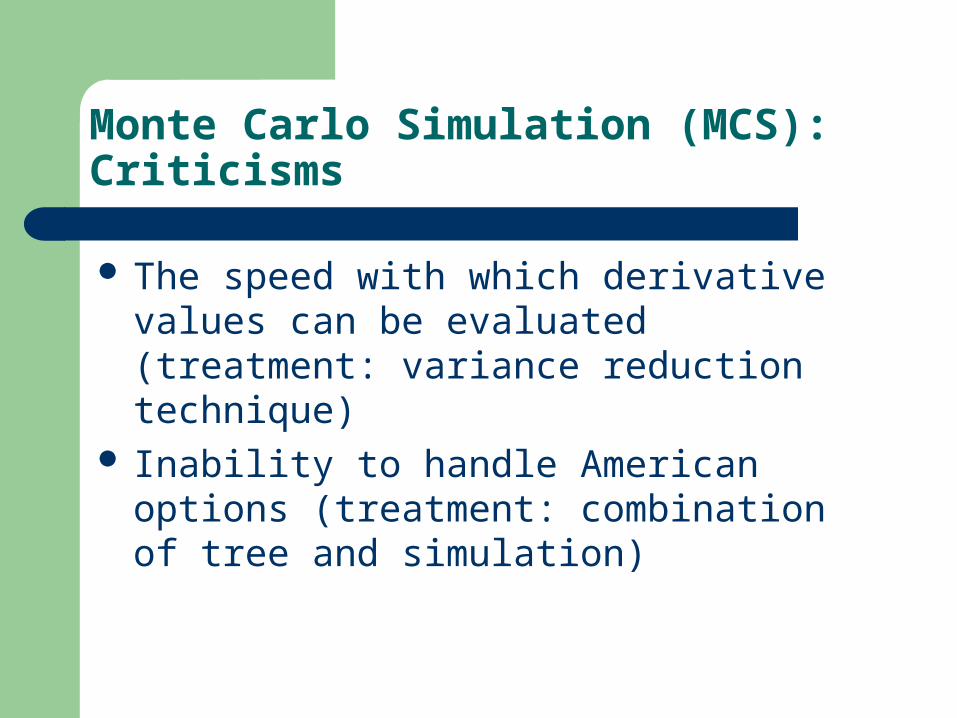

Monte Carlo Simulation (MCS): Criticisms

The speed with which derivative values can be evaluated (treatment: variance reduction technique)

Inability to handle American options (treatment: combination of tree and simulation)

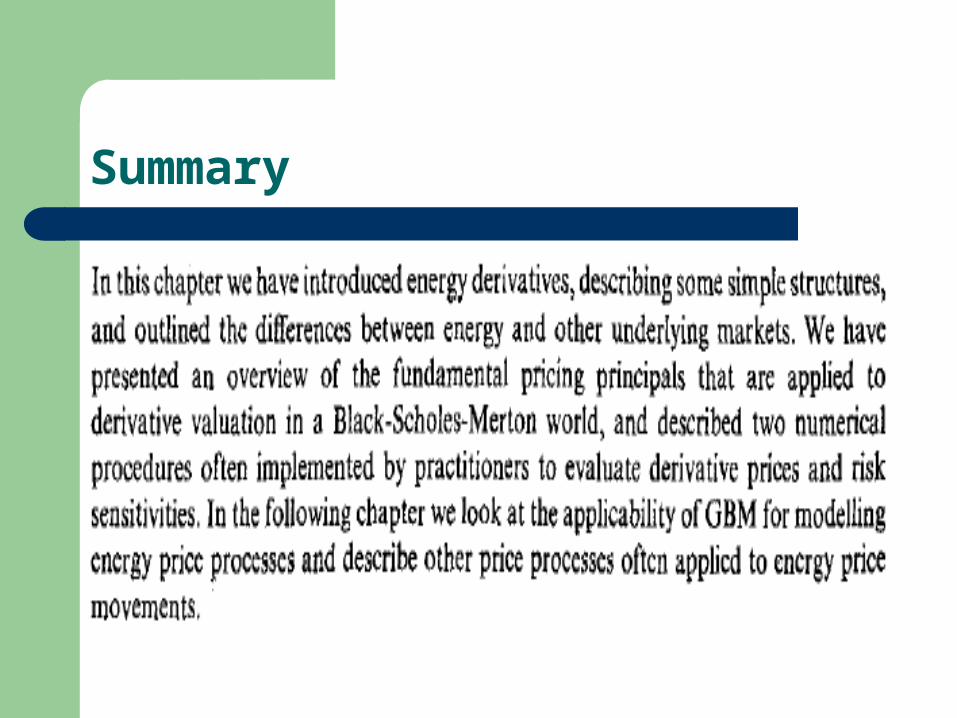

Summary

The End

Thank You for Your Attention!

Next Talk: Chapter 2: Understanding and Analysing Spot Prices

Speaker: Ouyang, Yuyuan (Lance) November 17, 2006, 12:00pm, MS 543

Distribution list of Chapters:

Ch 1,3,6-Anatoliy Ch 2,7-Lance Ch 4,8-Matt Ch 5,9-Matthew Ch 10-Xu Ch 11-Greg