Embed Size (px)

Citation preview

CONTENTS

Important Notes

Company Information

Financial Highlights

Changes in Share Capital and Shareholdings of Substantial Shareholders

Directors, Supervisors, Senior Management and Employees

Corporate Governance

Shareholders’General Meeting

Risk Management

Report of the Board of Directors

Report of the Board of Supervisors

Significant Events

References

Organizational Charts

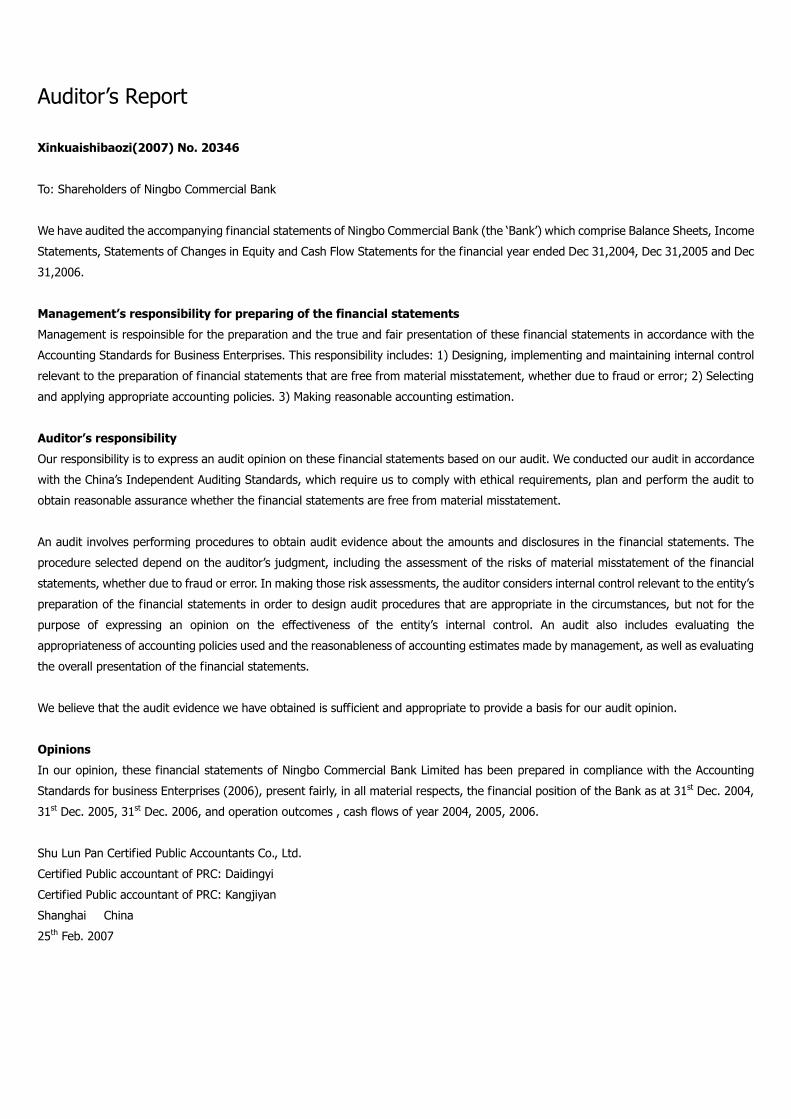

Independent Auditor’s Report

Financial Statements

Notes to Financial Statements

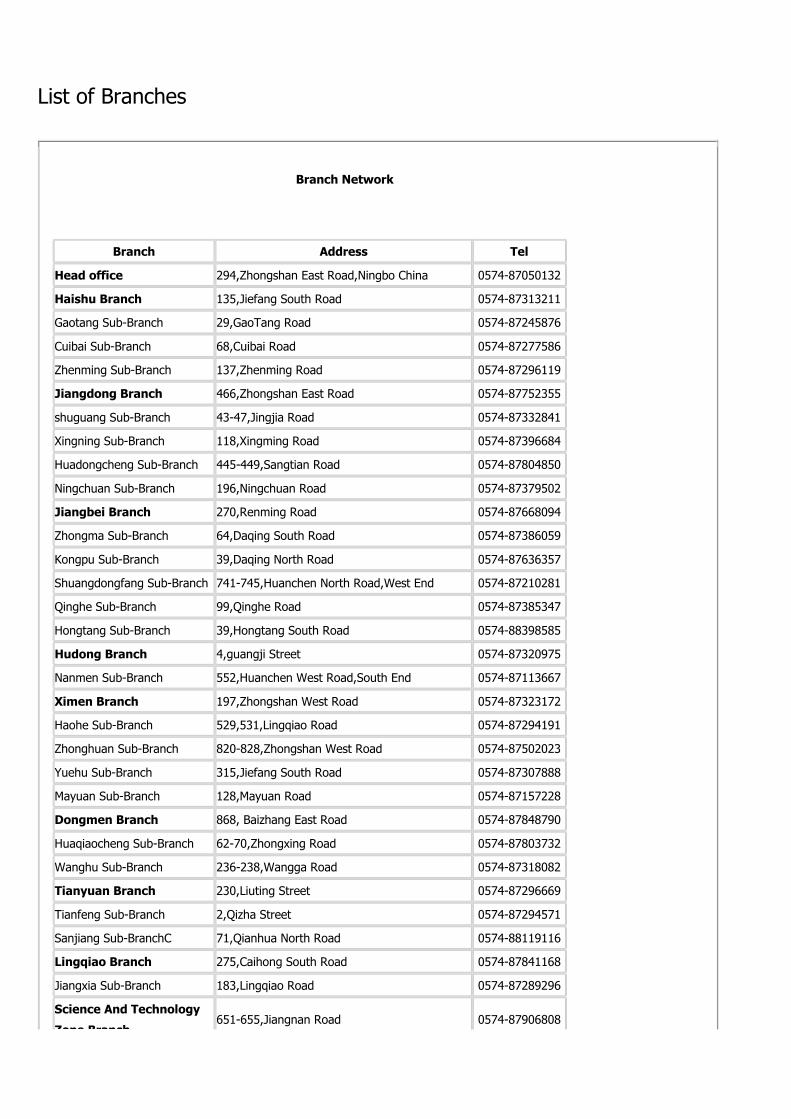

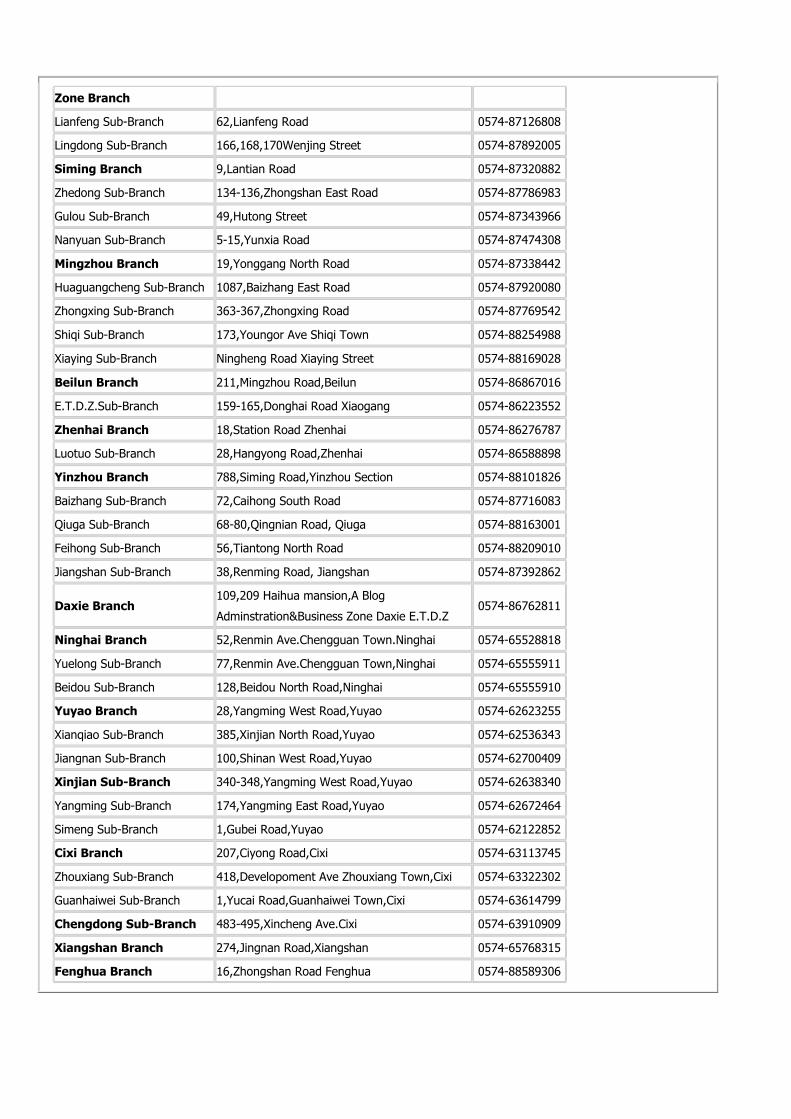

List of Branches

Important Notice

1 The Board of Directors of Ningbo Commercial Bank Co.,Ltd. warrants that there are no fraudulent

disclosures, misguiding statements or significant material omissions in this report and the Board is

responsible for the authenticity, accuracy and integrity of the report.

2 The financial statements for 2006 has been audited by Shu Lun Pan Certified Public Accountants Co.,

Ltd. in accordance with the independent auditing standards for the Chinese certified public accountants.

The company has formed the unqualified auditor’s opinion.

3 Mr. Luhuayu, Chairman of the directors, Ms. Yufengying, President of the Bank and Mr. Luoweikai,

CFO of the Bank undertake that the financial statements in this annual report are true and integrity.

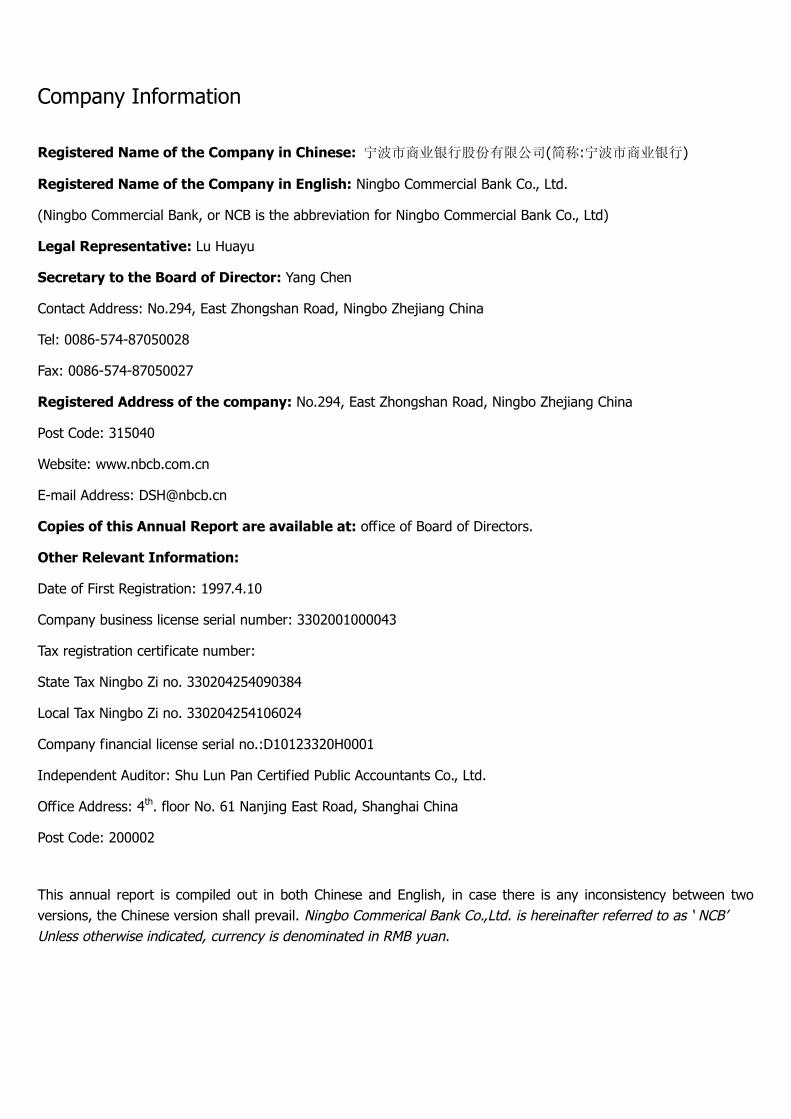

Company Information

Registered Name of the Company in Chinese: 宁波市商业银行股份有限公司(简称:宁波市商业银行)

Registered Name of the Company in English: Ningbo Commercial Bank Co., Ltd.

(Ningbo Commercial Bank, or NCB is the abbreviation for Ningbo Commercial Bank Co., Ltd)

Legal Representative: Lu Huayu

Secretary to the Board of Director: Yang Chen

Contact Address: No.294, East Zhongshan Road, Ningbo Zhejiang China

Tel: 0086-574-87050028

Fax: 0086-574-87050027

Registered Address of the company: No.294, East Zhongshan Road, Ningbo Zhejiang China

Post Code: 315040

Website: www.nbcb.com.cn

E-mail Address: [email protected]

Copies of this Annual Report are available at: office of Board of Directors.

Other Relevant Information:

Date of First Registration: 1997.4.10

Company business license serial number: 3302001000043

Tax registration certificate number:

State Tax Ningbo Zi no. 330204254090384

Local Tax Ningbo Zi no. 330204254106024

Company financial license serial no.:D10123320H0001

Independent Auditor: Shu Lun Pan Certified Public Accountants Co., Ltd.

Office Address: 4th. floor No. 61 Nanjing East Road, Shanghai China

Post Code: 200002

This annual report is compiled out in both Chinese and English, in case there is any inconsistency between two

versions, the Chinese version shall prevail. Ningbo Commerical Bank Co.,Ltd. is hereinafter referred to as ‘NCB’

Unless otherwise indicated, currency is denominated in RMB yuan.

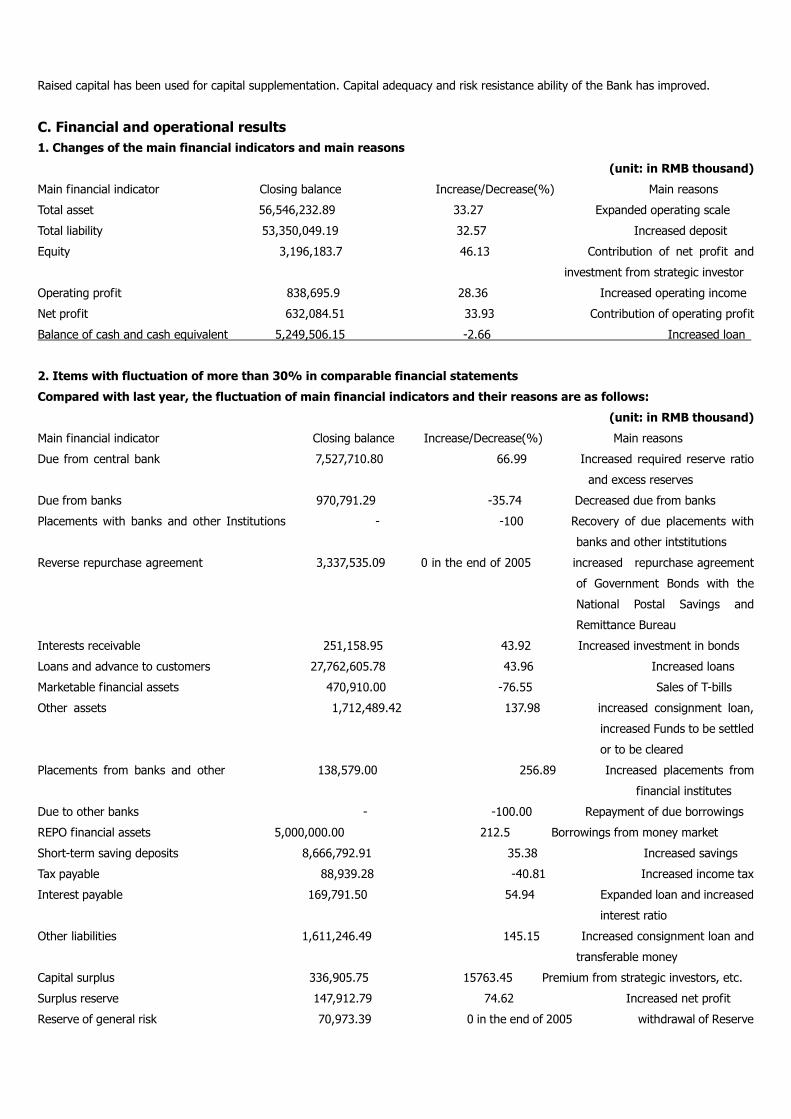

Financial Highlights

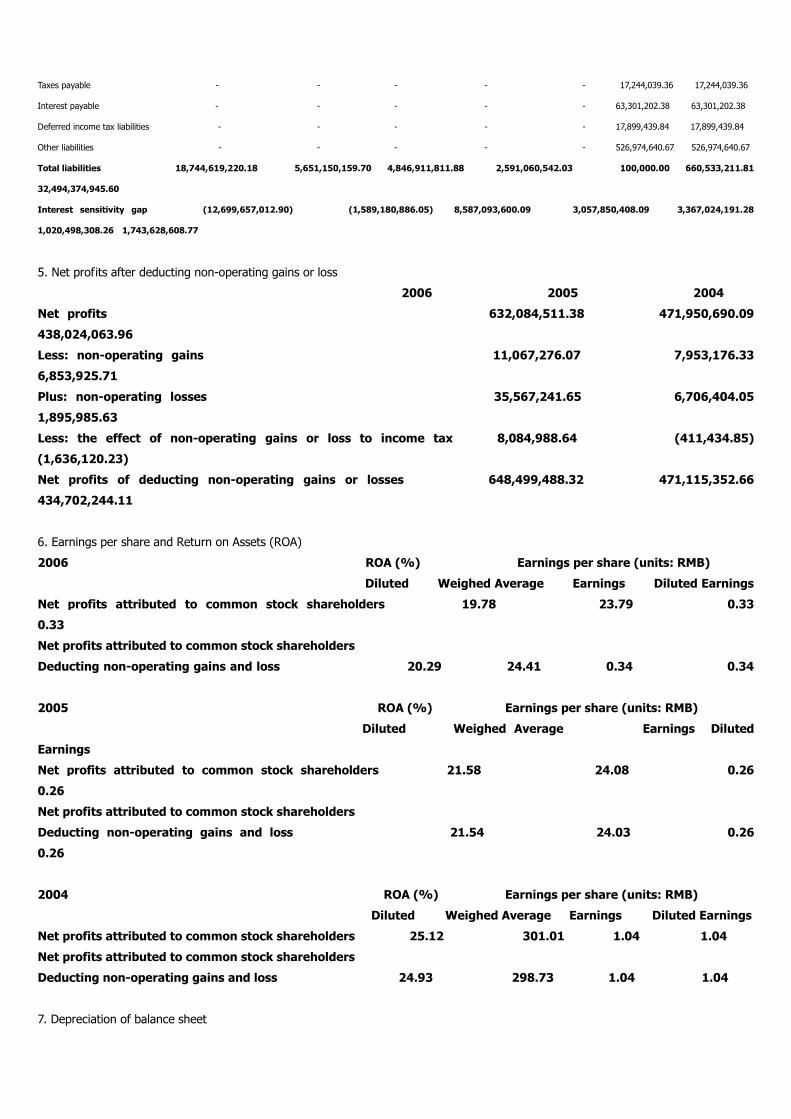

Key profits figures in reporting period (unit: in RMB thousand)

Profit before tax 814,196

Net profit 632,085

Operating profit 838,696

Investment income 8093

Net non-operating income -24500

Net cash flow from operating activities 141,410

Net increase in cash and cash equivalents -143,218

Three-year summary of selected financial figures (unit: in RMB thousand)

2006 2005 2004

Operating income 1,600,804 1.230,574 1,039,215

Net profit 632,085 471,951 438,024

Total assets 56,546,233 42,429,348 34,238,004

Equity 3,196,184 2,187,172 1,743,629

Diluted earnings per share (yuan) 0.33 0.26 1.04

Average earnings per share (yuan) 0.33 0.26 1.04

Net assets per share (yuan) 1.56 1.22 0.97

Net cash flow per share from operating activities 0.07 2.55 0.59

Diluted return on equity (%) 19.78 21.58 25.12

Average return on equity(%) 23.79 24.08 301.01

Adjusted net assets per share(yuan) 1.54 1.19 0.94

Three year supplemental financial data (unit: in RMB thousand)

2006 2005 2004

Total liabilities 53,350,049 40,242,176 32,494,375

Total deposit 46,191,396 37,521,242 29,755,055

Long-term deposit 3,702,605 2,469,591 2,472, 997

Placements from banks and

Other financial institutions _ 36,773 _

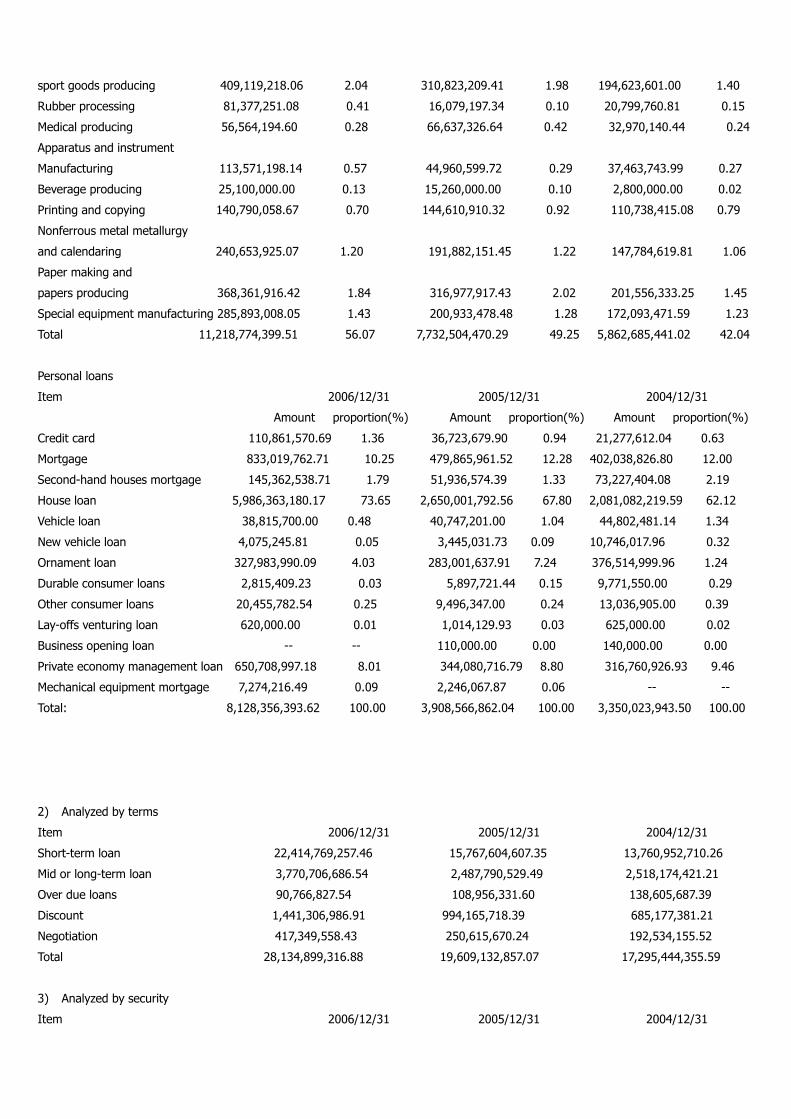

Total loans 28,134,899 19,609,133 17,295,444

Notes:

Total deposit comprises short-term deposit, short-term savings deposit, fiscal deposit, remittance payable, margin

deposit, outward remittance, short-term guaranteed deposit, long-term deposit, long-term savings deposit and

long-term security deposit;

Long-term deposit includes long-term deposit, long-term savings deposit and long-term security deposit;

Total loans include short-term loans, bill purchasing, refinancing, discounting, medium and long-term loans, overdue

loans and advances, less rediscounting and inter-bank discounting.

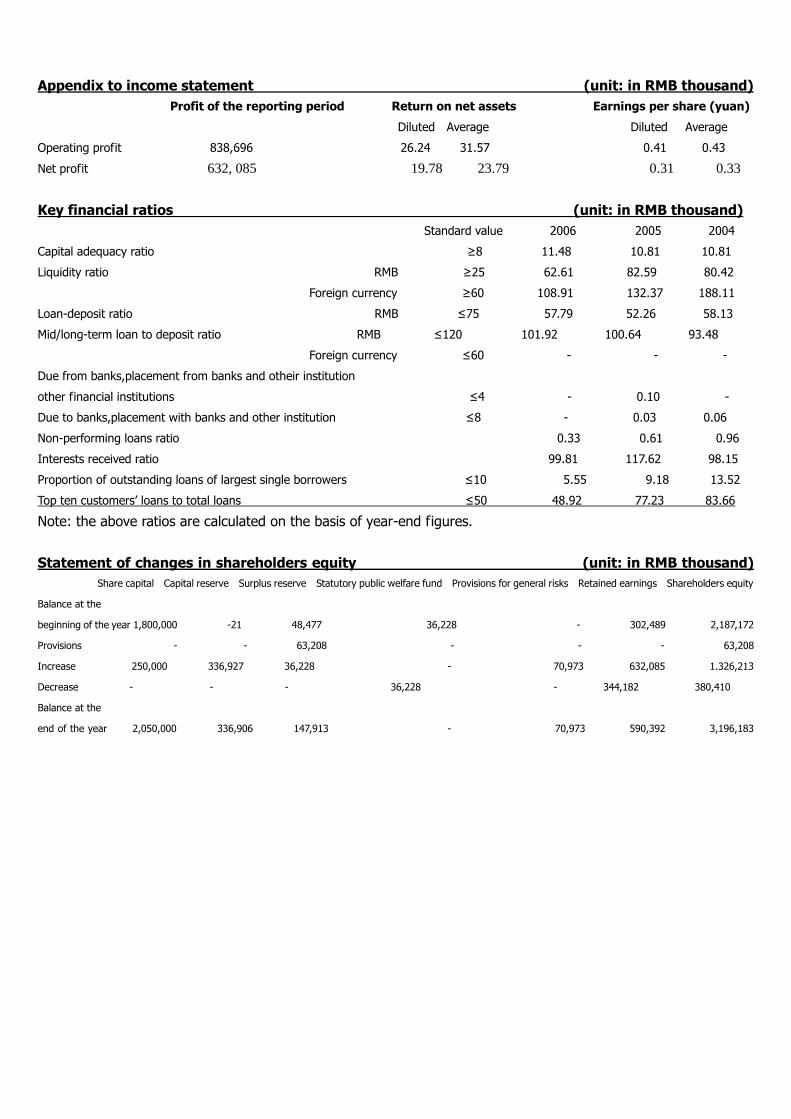

Appendix to income statement (unit: in RMB thousand)

Profit of the reporting period Return on net assets Earnings per share (yuan)

Diluted Average Diluted Average

Operating profit 838,696 26.24 31.57 0.41 0.43

Net profit 632, 085 19.78 23.79 0.31 0.33

Key financial ratios (unit: in RMB thousand)

Standard value 2006 2005 2004

Capital adequacy ratio ≥ 8 11.48 10.81 10.81

Liquidity ratio RMB ≥ 25 62.61 82.59 80.42

Foreign currency ≥ 60 108.91 132.37 188.11

Loan-deposit ratio RMB ≤ 75 57.79 52.26 58.13

Mid/long-term loan to deposit ratio RMB ≤ 120 101.92 100.64 93.48

Foreign currency ≤ 60 - - -

Due from banks,placement from banks and otheir institution

other financial institutions ≤ 4 - 0.10 -

Due to banks,placement with banks and other institution ≤ 8 - 0.03 0.06

Non-performing loans ratio 0.33 0.61 0.96

Interests received ratio 99.81 117.62 98.15

Proportion of outstanding loans of largest single borrowers ≤ 10 5.55 9.18 13.52

Top ten customers’loans to total loans ≤ 50 48.92 77.23 83.66

Note: the above ratios are calculated on the basis of year-end figures.

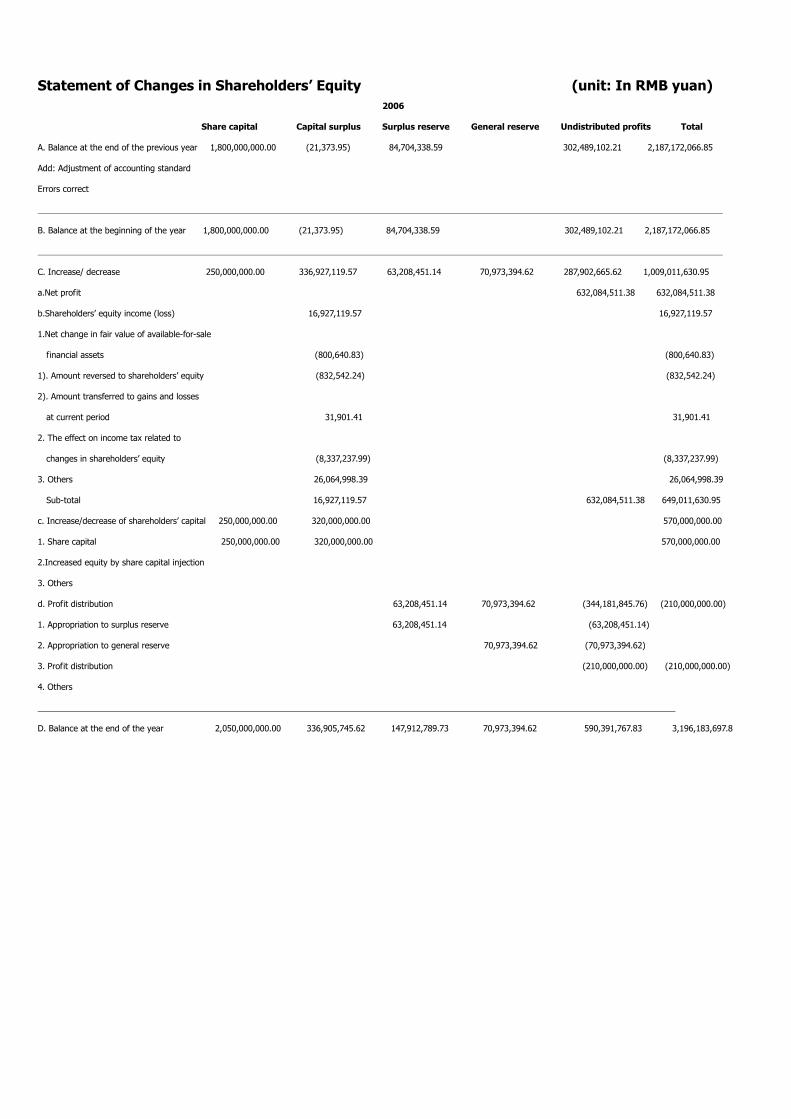

Statement of changes in shareholders equity (unit: in RMB thousand)

Share capital Capital reserve Surplus reserve Statutory public welfare fund Provisions for general risks Retained earnings Shareholders equity

Balance at the

beginning of the year 1,800,000 -21 48,477 36,228 - 302,489 2,187,172

Provisions - - 63,208 - - - 63,208

Increase 250,000 336,927 36,228 - 70,973 632,085 1.326,213

Decrease - - - 36,228 - 344,182 380,410

Balance at the

end of the year 2,050,000 336,906 147,913 - 70,973 590,392 3,196,183

Financial Highlight

Deposit (unit: in RMB thousand)

0

5000000

10000000

15000000

20000000

25000000

30000000

35000000

40000000

45000000

50000000

2001 2002 2003 2004 2005 2006

Deposit

9798762

Loan (unit: in RMB thousand)

0

5000000

10000000

15000000

20000000

25000000

30000000

2001 2002 2003 2004 2005 2006

Loan

6185380

Changes in Share Capital and Shareholdings of Substantial Shareholders

A. Changes of shareholders (unit: in thousands of shares)

Types Share capital Decrease during the year Iecrease during the year Share capital

(2005/12/31) (2006) (2006) (2006/12/31)

State-owned shares 270.000 _ _ 270,000

(Ningbo Financial Bureau)

Shares held by legal persons 1,156,593 37,777 _ 1,118,816

Shares held by natural persons 373,407 _ 37,777 411,184

Shares held by foreign investors _ _ 250,000 250,000

Total 1,800,000 37,777 287,777 2,050,000

B. Shareholders’information

As of 31 December 2006, the Bank has 3161 shareholders, of which 3 are state-owned shareholders, 116 are legal persons’shares, 1 is

foreign investor, 3040 are natural persons investors.

Top 10 Shareholders as at 31 December 2006 (unit: in thousands of shares)

No. Name End of the year Beginning of the year Increase/Decrease Proportion(%)

1 Ningbo Financial Bureau 27,000 27,000 _ 13.17

2 OCBC Group Singapore 25,000 0 25,000 12.20

3 Fubang (Holdings) Group Co Ltd. 17,900 17,900 _ 8.73

4 Ningbo Huamao Investment & Holding Co., Ltd 17,900 17,900 _ 8.73

5 Ningbo Shanshan Co., Ltd 17,900 17,900 _ 8.73

6 Ningbo Power Development Company 17,900 17,900 _ 8.73

7 Ningbo Youngor (Group) Co., Ltd 17,900 17,900 _ 8.73

8 Ningbo Yunsheng (Group) Co., Ltd 6084 6084 _ 2.97

9 Zhejiang Cuori Electical Appliances (Group)Co., Ltd 5400 5400 _ 2.63

10 Ningbo ETDZ Holdings Co., Ltd. 2,201 2,201 _ - 1.07

Total 155,185 130,185 25,000 75.70

Note: These shares are all ordinary shares.

C. Related party disclosures

1. Loans and credit facilities granted by the Bank to natural person in the Bank and their relatives

(unit: in RMB thousand)

Type of guarantee Approved Line of credit Remaining of approved Line of credit Balance of related loans

(I.E. VIP, Daiyitong, Bailingtong) (Including businesses under Line of

credit)

Secured by collaterals - - 24259

Secured by guarantee - - 3695

Total 3534 543.62 27854

Note: Natural person in the Bank comprises senior management, credit approval staffs, members of credit approval committee and their

closed relatives.

2. Loans and credit facilities granted by the Bank to the related parties of shareholders

who hold more than 5 percent shares

i. Ningbo Shanshan Co., Ltd and its related parties (G001) as at 2006/12/31 (unit: in RMB 10 thousand)

No. Name Line of credit balance Balance deducting guaranteed deposits

Remarks

1. Shanshan (Group) Co., Ltd 8,000 Loans 7,000 7,000

2. Ningbo Shanshan Technology Venturing Investment Co., Ltd - - -

3. Ningbo Shanshan Neo-Material Technology Co., Ltd 4580 Acceptances 1378.241 758.03255

500 Letter of credits 201.135 110.6005

4.Ningbo Shanshan Eco-protection Development Co., Ltd - - -

5.Ningbo Bellsen Maternity Articles Co.,Ltd - Loans 100 100

6. Ningbo Shanshan Garments Co., Ltd 7000 Loans1500 1500

7.China Ningbo International Corporation Co., Ltd - Letter of credits 54.951672 54.951672

8.Zhejiang Technology Imp.&Exp.(Ningbo) Co., Ltd - Loans 500 500

9.Ningbo Qineng Commercial Co., Ltd 500 - -

10..Ningbo Arts and Crafts I/E Co., Ltd USD300 - -

11.Ningbo ETDZ Huixing Trade Co., Ltd 1833.6 Loans 500 500

Acceptances 980 784

Bill purchasing 432.723906 432.723906

12.Ningbo Shanshan Ulica Solar Energy Science & Technology Co., Ltd - -

Total 12646.65 11740.308628

ii.Ningbo Youngor Group Co., Ltd and its relative parties (G002) (unit: in RMB 10 thousand)

No. Name Line of credit Balance Balance deducting guaranteed deposits

Remarks

1. Ningbo Youngor Group Co., Ltd - - -

2. China-base Ningbo Foreign Trade Co., Ltd 25000 Letter of credits 14002.047505 14002.047505

Discounts 1185.256925 1185.256925

3.Ningbo China-base I/E Co., Ltd - Letter of credits 1412.41448 1412.41448

4.Ningbo Free Trade Xinyue International Trade Co., Ltd - - -

5. Ningbo Youngor International Trade and

Transportation Co., Ltd. USD300 Discounts 342.56 342.56

6.Ningbo Qianyi I/E Co., Ltd - Letter of credits 26.59275 22.159774

Total - 16967 16964.438684

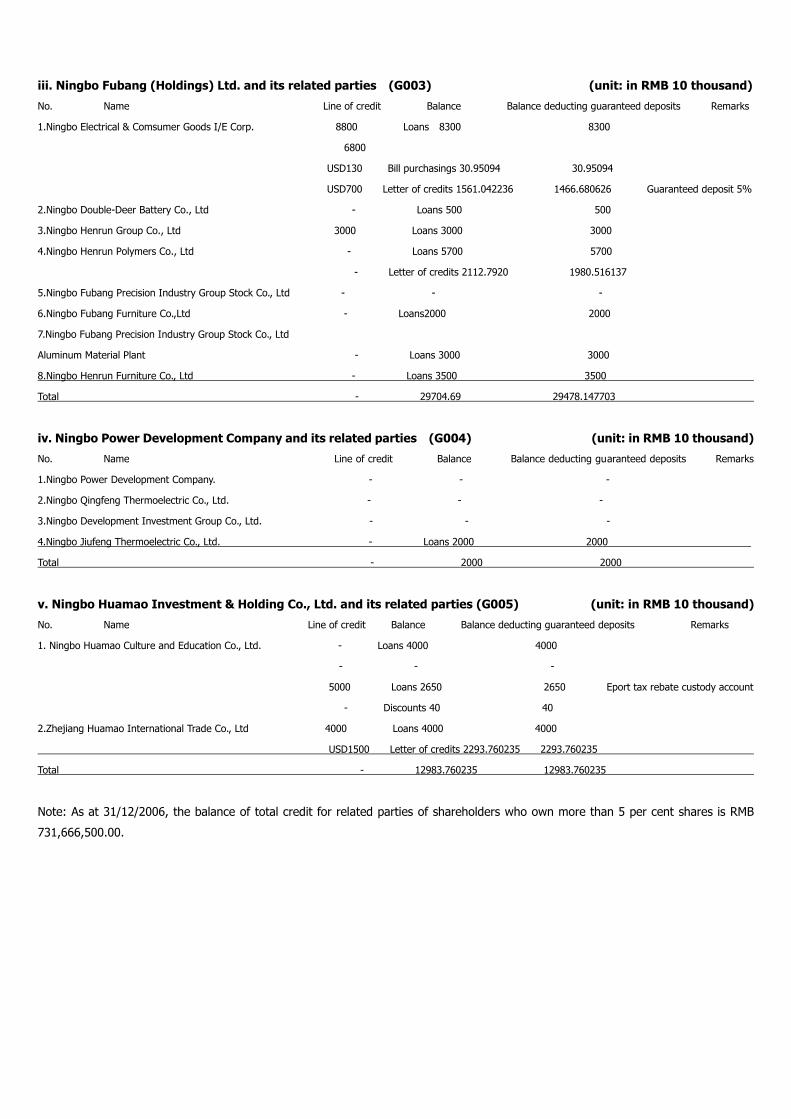

iii. Ningbo Fubang (Holdings) Ltd. and its related parties (G003) (unit: in RMB 10 thousand)

No. Name Line of credit Balance Balance deducting guaranteed deposits Remarks

1.Ningbo Electrical & Comsumer Goods I/E Corp. 8800 Loans 8300 8300

6800

USD130 Bill purchasings 30.95094 30.95094

USD700 Letter of credits 1561.042236 1466.680626 Guaranteed deposit 5%

2.Ningbo Double-Deer Battery Co., Ltd - Loans 500 500

3.Ningbo Henrun Group Co., Ltd 3000 Loans 3000 3000

4.Ningbo Henrun Polymers Co., Ltd - Loans 5700 5700

- Letter of credits 2112.7920 1980.516137

5.Ningbo Fubang Precision Industry Group Stock Co., Ltd - - -

6.Ningbo Fubang Furniture Co.,Ltd - Loans2000 2000

7.Ningbo Fubang Precision Industry Group Stock Co., Ltd

Aluminum Material Plant - Loans 3000 3000

8.Ningbo Henrun Furniture Co., Ltd - Loans 3500 3500

Total - 29704.69 29478.147703

iv. Ningbo Power Development Company and its related parties (G004) (unit: in RMB 10 thousand)

No. Name Line of credit Balance Balance deducting guaranteed deposits Remarks

1.Ningbo Power Development Company. - - -

2.Ningbo Qingfeng Thermoelectric Co., Ltd. - - -

3.Ningbo Development Investment Group Co., Ltd. - - -

4.Ningbo Jiufeng Thermoelectric Co., Ltd. - Loans 2000 2000

Total - 2000 2000

v. Ningbo Huamao Investment & Holding Co., Ltd. and its related parties (G005) (unit: in RMB 10 thousand)

No. Name Line of credit Balance Balance deducting guaranteed deposits Remarks

1. Ningbo Huamao Culture and Education Co., Ltd. - Loans 4000 4000

- - -

5000 Loans 2650 2650 Eport tax rebate custody account

- Discounts 40 40

2.Zhejiang Huamao International Trade Co., Ltd 4000 Loans 4000 4000

USD1500 Letter of credits 2293.760235 2293.760235

Total - 12983.760235 12983.760235

Note: As at 31/12/2006, the balance of total credit for related parties of shareholders who own more than 5 per cent shares is RMB

731,666,500.00.

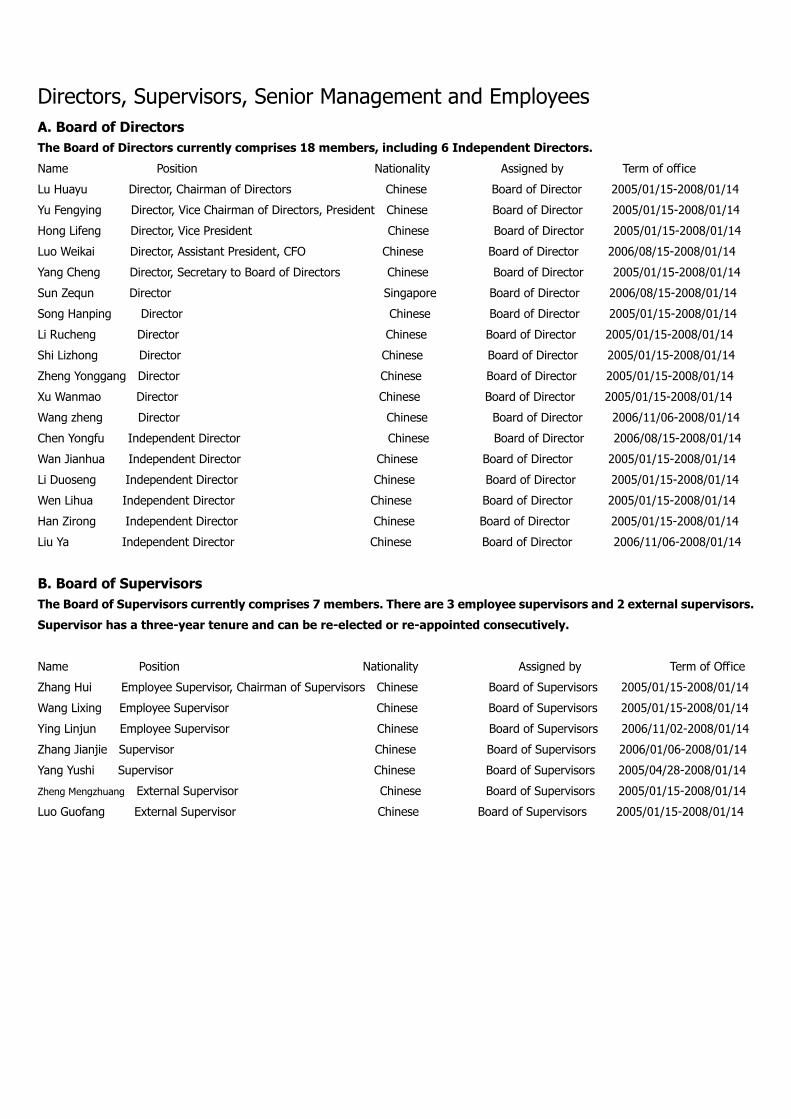

Directors, Supervisors, Senior Management and Employees

A. Board of Directors

The Board of Directors currently comprises 18 members, including 6 Independent Directors.

Name Position Nationality Assigned by Term of office

Lu Huayu Director, Chairman of Directors Chinese Board of Director 2005/01/15-2008/01/14

Yu Fengying Director, Vice Chairman of Directors, President Chinese Board of Director 2005/01/15-2008/01/14

Hong Lifeng Director, Vice President Chinese Board of Director 2005/01/15-2008/01/14

Luo Weikai Director, Assistant President, CFO Chinese Board of Director 2006/08/15-2008/01/14

Yang Cheng Director, Secretary to Board of Directors Chinese Board of Director 2005/01/15-2008/01/14

Sun Zequn Director Singapore Board of Director 2006/08/15-2008/01/14

Song Hanping Director Chinese Board of Director 2005/01/15-2008/01/14

Li Rucheng Director Chinese Board of Director 2005/01/15-2008/01/14

Shi Lizhong Director Chinese Board of Director 2005/01/15-2008/01/14

Zheng Yonggang Director Chinese Board of Director 2005/01/15-2008/01/14

Xu Wanmao Director Chinese Board of Director 2005/01/15-2008/01/14

Wang zheng Director Chinese Board of Director 2006/11/06-2008/01/14

Chen Yongfu Independent Director Chinese Board of Director 2006/08/15-2008/01/14

Wan Jianhua Independent Director Chinese Board of Director 2005/01/15-2008/01/14

Li Duoseng Independent Director Chinese Board of Director 2005/01/15-2008/01/14

Wen Lihua Independent Director Chinese Board of Director 2005/01/15-2008/01/14

Han Zirong Independent Director Chinese Board of Director 2005/01/15-2008/01/14

Liu Ya Independent Director Chinese Board of Director 2006/11/06-2008/01/14

B. Board of Supervisors

The Board of Supervisors currently comprises 7 members. There are 3 employee supervisors and 2 external supervisors.

Supervisor has a three-year tenure and can be re-elected or re-appointed consecutively.

Name Position Nationality Assigned by Term of Office

Zhang Hui Employee Supervisor, Chairman of Supervisors Chinese Board of Supervisors 2005/01/15-2008/01/14

Wang Lixing Employee Supervisor Chinese Board of Supervisors 2005/01/15-2008/01/14

Ying Linjun Employee Supervisor Chinese Board of Supervisors 2006/11/02-2008/01/14

Zhang Jianjie Supervisor Chinese Board of Supervisors 2006/01/06-2008/01/14

Yang Yushi Supervisor Chinese Board of Supervisors 2005/04/28-2008/01/14

Zheng Mengzhuang External Supervisor Chinese Board of Supervisors 2005/01/15-2008/01/14

Luo Guofang External Supervisor Chinese Board of Supervisors 2005/01/15-2008/01/14

C. Senior Management

Senior management comprises of the Chairman of Board of Directors, the President, the Chairman of Board of

Supervisors, the Vice President, the Assistant Presidents, the CFO, and the Secretary to Board of Directors.

Name Position Name Position

Lu Huayu Chairman of Directors Luo Weikai Assistant President, CFO

Yu Fengying President Yang Chen Secretary of Directors

Zhang Hui Chairman of Supervisors Ren Zhishui Assistant President,

Hong Lifeng Vice President Chen Xuefeng Assistant President,

D. Brief working experience and other positions of Directors, Supervisors and Senior Management

1. Directors

Mr. Lu Huayu, has served as Chairman of the Board of Directors since January 2005. He also served as our President from November

2000 to January 2005. From July 1988 to November 2000, Mr. Lu held various positions in Ningbo Financial Bureau, including vice

president, chief of the Budgeting Department II and General Office, vice chief of Budgeting Department. During this period he was also

the vice director of the State–owned Assets Bureau. Mr. Lu was awarded a master’s degree and is a senior accountant. Age 43.

Ms Yu Fengying, has served as President of the Bank since January 2005. Ms Yu also served as vice president of the Bank. From

September 1980, she was the director of Yinxian Finance and Taxation Bureau, the vice president, president of Bank of China, Yingzhou

sub-branch, the vice director of Ningbo Urban Credit Cooperative. Ms Yu holds a bachelor’s degree and is a senior economist. Age 49.

Mr. Hong Lifeng, has served as the vice-president of NCB since January 2003. From July 1986, he was the section chief of International

Settlement Department of Bank of China Ningbo Branch, the senior manager of Mainland Branch Transactions Department of Bank of

China (Hong Kong) Ltd., the director, senior manager and manager of China Service Department and Industrial and Commercial

Department in Hua Chiao Commercial Bank Ltd.. Mr. Hong also acted as the vice-director of Credit Card Department and Loan

Department of Bank of China Ningbo Branch and the vice-president of Bank of China Beilun Sub-branch. Mr. Hong holds a bachelor’s

degree and is a senior economist. Age 43.

Mr. Luo Weikai, has served as the assistant president of NCB since March 2005. From August 1984, he was the vice-president of

Tianyuan Br. of NCB and also held the positions of general manager of Accounting Department, Business Department and E-banking

Department of NCB. He also held the positions as assistant section chief and the department director of China Industry and Commercial

Bank Ningbo Branch. Mr. Luo holds a master’s degree and is an economist. Age 42.

Mr. Yang Chen, has served as the secretary of directors of NCB since January 2005. From August 1982, Mr. Yang acted as the director

of the general office of NCB, the senior staff of Ningbo Municipal Government Office,

chief staff in Ningbo Foreign Investment Office, chief staff of Wenzhou Municipal Government Office, the vice-director of the Secretary

Department of Wenzhou Longwan District Government Office and a senior staff of Wenzhou Municipal Government Office, Mr. Yang holds

a bachelor’s degree and is a senior economist. Age 46.

Mr Soon Tit Koon, has served as Executive Vice President and CFO, the chairman of security director board of the OCBC Bank and the

director of the OCBC Bank Malaysia currently. Mr. Soon was formerly the CFO of Wilmar Holdings, was with CITI Investment Bank,

Singapore for 17 years and was an engineer for the oil excavation and equipment maintenance of Dowell Schelumberger Incorporated.

Mr. Soon holds a MBA degree. Age 56.

Mr. Song Hanping, has served as the president and CEO of Ningbo Fubang Holding Group Co., Ltd. since April 2002. From 1984, Mr.

Song was the chairman and general manager of Ningbo Light Industry Group Co. Ltd., vice general manager of Ningbo No. 2 Light

Industry Group Co. Ltd., general manager of Ningbo Henrun Group Co. Ltd, general manager of Ningbo Yujiang Industrial Co. Ltd. and

Ningbo Yujiang Plastic Co. Ltd. and the vice-general manager of Ningbo Bomei Zipper Co. Ltd.. Mr. Song holds a master’s degree and is a

senior economist. Age 44.

Mr. Li Rucheng, has served as the chairman and president of Ningbo Youngor Group Co., Ltd., and the director of CITIC Securities Co.,

Ltd since 7 July 2003. From 1981, Mr. Li was the chairman and general manager of Ningbo Youngor Garment Co., Ltd. and the director of

Ningbo Qingchun Garment Factory. Mr. Li has a college diploma and is a senior economist. Age 56

Mr. Shi Lizhong, has served as the general manager of Ningbo Development and Investment Group Co., Ltd. (the general manager of

Ningbo Power Develop Company) since March 2004. From December1970, Mr. Shi was the general manager, the vice general manager of

Ningbo Power Develop Company, the section chief of Planning section in Bureau of Ningbo Electric Power. Mr. Shi holds a bachelor’s

degree and is a senior engineer. Age 52.

Mr Zheng Yonggang, has served as the president and chairman of Ningbo Shanshan Group Co., Ltd since 1996. From 1989, Mr Zheng

was the director of Ningbo Yonggang Garment Factory (current: Ningbo Shanshan Group Co. Ltd.). Mr. Zheng holds a MBA degree and is

a senior economist. Age 49.

Mr. Xu Wanmao, has served as the president of directors and the Party Committee’s secretary of Huamao Group since 2000. From 1968,

Mr Xu was the CEO and the chairman of the board of directors of Huamao Group Co., Ltd., the president and the Party Committee’s

secretary of Ningbo Huamao Group Co., Ltd., the director of Ningbo Education and Technology Appliance Factory, the director, the Party

Committee’s secretary and vice director of Ningbo Yunzhou County Craftwork factory. Mr. Xu has acquired college diploma and is a senior

economist. Age 62.

Mr Wang zheng, has served as vice general manger, commissary of the Party Committee and the director of Ningbo Development and

Investment Group Ltd since March 2004.From 1982. Mr. Wang was CFO, commissary of the Party Committee and director of Ningbo

Development and Investment Group Ltd., the senior section staff and vice section chief of Ningbo Financial Bureau, the department chief

of the First Branch of Ningbo Regional Taxation Bureau and a department chief of Ningbo Financial Bureau. Mr. Wang holds a MBA degree

and is a senior accountant. Age 42.

Mr Chen Yongfu, served as the vice president and vice secretary of the Party Committee of the People’s Bank, Shanghai branch from

November 1998 to October 2005. From 1970, Mr. Chen was the vice director of the office of the People’s Bank, vice director and section

chief of Bank of Communications, Department chief, vice Department chief, section chief and vice section chief of China Agricultural Bank,

Jiangsu Branch, senior staff of the People’s Bank, Jiangsu Branch, the faculty of Jiangsu Jiangdu County Party School and a senior staff of

Jiangsu Jiangdu County P.D.. Mr. Chen holds a bachelor’s degree and is a senior economist. Age 62.

Mr. Wan Jianhua, is now the president of China Unionpay Co., Ltd. Mr Wan is now the professor of Fudan University, Graduates

Institution of the People’s Bank and Amoy Uni, the supervisor of Graduates Institution of the People’s Bank, director of China Finance

Association. From 1985, Mr. Wan was the general manager and the vice-chairman of Hong Kong Jiang Nan Finance Ltd., the chairman of

Great Wall Securities Co., Ltd., the standing vice president and vice president of China Merchant’s Bank and chairman of Guotong

Securities Co., Ltd., the section chief and vice section chief of Asset Management Section in People’s Bank of China. Mr Wan acquired a

bachelor’s degree of economics from Amoy University, a master’s degree of money banking from the Graduates Institution of the People’s

Bank, the diploma of PHD and the candidate qualification of PHD in National University of Australia, and the DBA degree from the South

California Career University of the U.S. Mr. Wan is also a senior economist. Age 43.

Mr. Li Duosen, is now a member of Hong Kong Securities Institute, the independent non-executive director of United Metals holdings

Limited(Listed Company) and the director of Hua Chiao Commercial Bank, Hongkong. Mr. Li was retired on 1 December 2001. He took

various positions in Hua Chiao Commercial Bank from 1963: the director and the deputy general manager, chief of Loan Lending Centre,

Credit Loan Department, Research Department, Management Department of Branch, Banking Department and Business Develop

Department. Meanwhile, from 1985, Mr Li also holds positions as the director of Hong Kong Caizhi Development Co., Ltd., the chairman

and the director of Hong Kong Anlian Trading Co., Ltd., the chairman and the director of Hong Kong Kiu Sheung (Agent) Co., Ltd., the

chairman and the director of Hong Kong Chiao Yue Finance Co., Ltd., the standing director and director of Beijing Yanshan Hotel. Mr. Li

holds a bachelor’s degree. Age 67.

Mr. Wen Lihua, has served as the vice-director of Economy Construction Qualification Committee, the vice-chief of Preparation Office of

China Museum Construction, Ministry of Finance, the director of Culture and History Research Center in Zhejiang University. Mr Wen is

also a professor of Zhejiang University and a part-time professor of Zhejiang University of Finance and Economics, Zhejiang University of

Science and Technology and Zhejiang Province Party Committee School. From September 1967, he was the director of Zhejiang

State-owned Assets Office, director of Zhejiang Local Taxation Bureau and director Zhejiang Financial Bureau, the vice general secretary

of Zhejiang Province Government, the vice director of General Office of Zhejiang Province , the Head of Fenghua County and Yinxian

County. Mr. Wen holds a bachelor’s degree. Age 43.

Mr. Han Zirong, has served as the chief partner of Shenzhen Rongxin Chartered Public Accountant Office. Mr. Han was engaged in

national audit and social audit for years. He was also in charge of overall loan management in ICBC Changchun. Mr. Han has worked in

Loan Management Department of China Industrial and Commercial Bank Changchun Branch for seven years. Mr Han holds a bachelor’s

degree and a CPA certificate. Age 44.

Mr Liu Ya, has served as the vice principal of University of International Business and Economy. Mr Liu is now also the director of the

China Financial Association, the expert getting special allowance from the government, the president of Beijing Jinghua Zhiye Education

and Technology Co.,Ltd. Since December 1984, Mr. Liu was the vice principal and the Party committee member of University of

International Business and Economy, professor and vice principal of China Financial Institution, vice director of Department Of

International Finance, assistant director of International Economics, director of International Finance Research Center, supervisor of

masters in International Finance and the vice professor of international finance in the Economic Department Of University of Liaoning. Mr

Liu holds a PHD degree specialized in International finance and is a professor of finance, supervisor of PHD. Age 48.

2. Supervisors

Mr. Zhang Hui, has served as the chairman of supervisors of NCB since January 2005. He also served as Vice-president of NCB from

December 2000 to January 2005. From April 1978, He held positions as: President of Beilun Branch of NCB, General Manager of Ningbo

Yongxin City Credit Union, secretary of Ningbo Economic Study Centre and Economic Researching Office of Ningbo Government, senior

staff of Ningbo Economic Researching Office. Mr. Zhang holds a bachelor’s degree and is a senior economist. Age 43.

Mr. Wang Lixing, has served as the position as general manager of Settlement Administration Department in NCB since November 2004.

Mr. Wang held various positions in his banking career from November1979: president of NCB’s Yinzhou Br. and Mingzhou Br., director of

Xinye business office of Ningbo City Credit Union, manager of international settlement Department, director of audit section, accounting

section as well as credit section of branch, director of business office of Yinzhou branch of Agricultural Bank of China. Mr. Wang holds a

bachelor’s degree and is a senior economist. Age 48.

Mr. Ying Linjun, has served as the chief of the auditing department of NCB since July 2002. From July 1994, He was vice manager of

business department, chief of accounting department and the vice manager of the operating department of Zhedong Branch, NCB, the

accountant of the financial department of Ningbo Shuangyuan Group Co., Ltd. Mr Ying holds a bachelor’s degree and is an economist. Age

34.

Mr. Zhang Jianjie, has served as the president, the general manager of Zhejiang Cuori Wiring Group Co., Ltd since 1996. Mr. Zhang was

the director of Ningbo Hengfa Wiring Co.,Ltd. and used to work in Cixi Yuncheng Agricultural Machine Factory and Cixi Wireless Yuncheng

NO.7 Factory. Mr. Zhang holds a college diploma. Age 39.

Mr. Yang Yushi, has served as the CFO of Ningbo Yunsheng Group. Ltd.. Mr Yang was the director of Fenghua Audit Office from April

1994 to October 1999, the vice director of Fenghua Juice factory from April 1986 to April 1994 and used to work in Zhejiang Shipping

Factory from December1976 to April 1986. Mr. Yang has acquired college diploma and is a senior accountant. Age 48.

Mr. Zhen Mengzhuang, has served as vice-president of Ningbo University, member of Standing Committee of Ningbo People’s Congress,

council of China International Law Research Institution, arbitrator of China International Economic and Trading Arbitration Committee and

the chief consultant of Zhejiang Zhongxin Lawyer Office. From 1987, Mr. Zhen was professor, vice-professor, vice-president, assistant

president, chairman of Law Institution and director of Law and Regulations Departmentof Ningbo University. Mr Zhen was graduated from

the Law Institution of Macgill University Canada. Mr. Zhen holds a master’s degree and is a lawyer. Age 43.

Mr. Luo Guofang, has served as the chairman of Ningbo Kexin Certified Public Accountants Co., Ltd. From August 1986, Mr. Luo was

CPA of several outstanding companies, the president of Ningbo Kexin Certified Public Accountants Co., Ltd., vice director of Ningbo

Mingzhou Accountants Co., Ltd, and a teacher in Ningbo Tax and Financial School. Mr. Luo holds a bachelor’s degree, and is a CPA and

China Certified Public Tax Accountant. Age 49.

3. Other Senior Managers

Lu Huayu 43 Director, Chairman of Directors Please refer to the part of “Directors” .

Yu Fengying 49 Director, Vice-Chairman of Directors, President Please refer to the part of “Directors” .

Zhang Hui 47 Chairman of Supervisors Please refer to the part of “Supervisors”.

Hong Lifeng 43 Director, Vice President Please refer to the part of “Directors” .

Luo Weikai 42 Director, Assistant President, CFO Please refer to the part of “Directors” .

Yang Chen 46 Director, Secretary of Directors Please refer to the part of “Directors” .

Mr. Ren Zhishui, has served as assistant president of NCB since May 2005. From October 1981, Mr. Ren was general manager of

International Settlement Department of NCB, the assistant general manager of Ningbo International Trust and Investment Co., Ltd.,

general manager of Hongkang Yongxin Investment Co.,Ltd., general manager of Ningbo Bonded Zone Xinya Trading Co., Ltd., deputy

manager and manager of International Department in Ningbo International Trust and Investment Co., Ltd., vice-manager of Corporate

Securities Department, the vice-manager of Credit Card Department of Bank of China Ningbo branch and the chief of Deposit and

Remittance Department, Mr. Ren holds bachelor’s degree and is an economist. Age 43.

Mr. Chen Xuefeng, has served as the assistant president of NCB since Dec 2005. From August 1985, he was the president of Cixi Branch,

NCB, director and general manager of Ningbo Anxin investment Co., vice president and budgeting manager of Cixi Financial Bureau, vice

president of Cixi Henghe Financial and Tax Office, secretary of Cixi Government Office, secretary and vice-director of administration office

of Cixi Financial Bureau, special management staff of Cixi Xiaolin Financial and Tax Office. Mr. Chen holds a master’s degree.Age 40.

E. Composition of employees

By the end of 2006, the Bank has a total staff of 1393. Classified according to age: 36.6% of the employees are under 30, 46.4% are aged

31-40, 16.4% are aged 41-50, 0.57% are aged 51-60. According to education background, 50.3% have bachelor’s degrees or higher,

32.7% of the employees hold a college diploma, 15.8% hold a technical secondary school diploma. According to their professional title,

20.3% acquired intermediate or senior titles, and 41.3% have elementary titles. The Bank has 149 intermediate or senior managers and

388 counter clerks.

Corporate Governance

In 2006, the Bank continued its efforts to improve its corporate governance framework as a joint-stock company, which is in compliance

with the PRC Company Law, the Guidelines for PRC Joint-stock Commercial Banking Corporate Governance and the relevant regulations

promulgated by regulatory authorities. The Bank further revised NCB Articles of Association, Rules for NCB Group Customer and its

Related Parties Credit Risk Management, Rules for Related Parties of Shareholders Credit Risk Management and other relevant rules and

regulations, which enhance and specialize NCB’s management system through the set of processes, policies and institutions.

Shareholders and shareholder’s meeting

The Bank established rules of procedure for Shareholder’s Meeting, and held Shareholder’s Meeting to ensure that all shareholders

especially minority shareholders are recognized and treated equally, can exercise their rights in the Bank. The Bank has set up an

effective channel to communicate with shareholders, reviewe shareholders’opinions and suggestions, which ensure all shareholders are

properly informed and are able to participate in and exercise their voting rights on major issues of the Bank.

Shareholders and the company

Shareholdings of the Bank are decentralized, which means none of the shareholders has genuine control rights over the Bank. The top

five shareholders in the Bank do not have the rights to override the Shareholder’s Meeting intervening the Bank’s business activities and

decision-making directly or indirectly. In respect of employees, assets, financing, institutions, and businesses, the top five shareholders

are independent to the Bank. The Board of Directors, the Board of Supervisors, and internal organizations are able to operate

independently.

Directors and the Board of Directors

According to the Directors’electing procedure to the Articles of Association of the Bank, in 2006, the Board of Directors consists of 18

directors, includes 6 independent directors who bring broad vision and experiences and provide a reasonable specialist structure to the

Board of Directors. The personnel composition is fully in compliance with the laws and relevant regulations with which can not only

effectively represent different parts of investor entities and maintain the benefits for the Bank and Shareholders, but also ensure the

quality and standard of strategies that Board of Directors make as well as the core functions that the Board of Directors have within the

corporate governance. In compliance with relative regulations promulgated, the Board of Directors has set up the Strategic Development

Committee, Audit Committee, Related Party Transaction Control Committee, Risk Management Committee, Nominating Committee and

Remuneration Committee. Other than Strategic Development Committee and Remuneration Committee, the Chairmanship of the other

four committees is assumed by independent directors.

The attendance of the board meetings of the Independent Directors: In 2006, the Board of Directors held 10 meetings, 3 independent

directors attended 10 out of a total of 10 meetings, Mr. Wan Jianhua appointed authorized person attending 2 out of 10 meetings, Mr.

Weng Lihua and Mr. Chen Yongfu entrusted authorized person to attend 1 out of 10 meetings on his behalf.

The attendance of the board meetings of other Directors: In reporting period, Mr. Xu Wanmao and Mr. Zheng Yonggang appointed

authorized person attending 1 out of 10 meetings respectively, other Directors attended all the meetings.

Supervisors and the Board of Supervisors

In 2006, the Board of Supervisors is comprised of 7 supervisors, including 3 employee supervisors and 2 external supervisors, the

personnel structure is in compliance with laws and relative regulation promulgated. The Board of Supervisors has set up the Auditing

Committee and Nomination Committee. Supervisors are able to perform their responsibilities conscientiously for the shareholders. The

Board of Supervisors is responsible for overseeing the Bank’s financial activities and the legality and compliance of the Board of Directors

and Senior Management in performing their roles.

The attendance of the supervisors’meetings of the External Supervisors: in 2006, the Board of supervisors held four meetings, Mr.

Luoguofang attended 4 out of a total 4 meetings, Mr. Zheng Mengzhuang entrusted authorized person to attend 1 out of a total 4

meetings.

The attendance of the supervisors’meetings of other supervisors: in 2006, all other supervisors attended the meetings.

The decision-making system

The Shareholders’ Meeting is the highest authority within the Bank, implementing decision-making, management and supervision

through the Board of Directors and the Board of Supervisors. The president is appointed by the Board of Directors and responsible for the

Bank’s day-to-day business. The Bank implement first tier legal person management system, all branches and subsidiaries do not have

legal personalities. The branches operate their businesses with the authorization of the head office; the head office is responsible for the

civil liabilities.

Information disclosure and transparency

The Bank formulated the information disclosure policy and appointed the secretary of the Board of Directors disclosing information,

reception of visits and giving consultation. The Bank discloses information in compliance with laws, regulations, the Article of Association

and the Bank’s information disclosure policy. Information disclosure is truthful, accurate, complete, and timely which ensure that all

investors are able to receive information fairly.

Shareholder’s Meeting

In January 6, 2006, the Bank held extraordinary Shareholder’s Meeting for the first time, approved introducing strategic foreign investor

into the Bank, amendments to the Article of Association and the changing of directors and supervisors. There are 10 shareholders and the

representative of shareholders who hold 1,639,840,000 shares of the Bank attended the meeting, their shares consist 91.1% of the total

share capitals to the Bank.

The Bank held 2005 Annual Shareholder’s Meeting in April 22, 2006. The meeting approved Report of Board of Director, Report of Board

of Supervisors, 2005 annual financial report, annual budgets, profit distribution plan for the year 2005, strategic development plans for

2006-2008, appointment of external auditors. There are 12 shareholders and representative of shareholders who hold 1,651,662,700

shares attended the meeting. Their shares constitute 91.76% of a total share capital to the Bank.

Amendment of the Articles of Association and the appointment of Mr. Sun Zequn, Mr. Lou Weikai as directors, Mr. Chen Yongfu as

independent director of the Bank were approved at the extraordinary meeting held on August 15, 2006. There are 12 shareholders and

representative of shareholders who hold 1,830,828,416 shares attended the meeting, their shares constitute 89.31% of a total share

capital to the Bank.

In November 6, 2006, the Bank held extraordinary meeting for the third time. The meeting approved the Initial Public Offering and Listing

of A shares scheme, revision of the Articles of Association, rules of procedures for Board of Directors of the Bank, rules of procedures for

Board of Supervisors of the Bank and connected transaction management, all of which are adopted disclosed ballot method. The meeting

approved the resignation of Mr. Zhou Haiming as director of shareholders, appointed Mr. Wang Zeng as director and Mr. Liu Ya as

independent director of the Bank. There are 14 shareholders and representative of shareholders who hold 1,890,246,000 shares attended

the meeting, their shares constitute 92.37% of a total share capital to the Bank.

Risk Management

A. Main regulatory indicators

By the end of 2006, the Bank’s CAR level is 11.48%, Core CAR level is 9.71% which is less than the regulatory guideline 8% and 4% level

respectively.

Risk concentration

Loan concentration by single borrower: the largest single borrower is Ningbo Inner City Reconstruction Office with RMB200 million

of outstanding loans which consists 5.55% of net regulatory capital (RMB3606.79 million by the end of 2006) from the Bank and the level

is 4.45 percent lower than regulatory guideline at 10%.

Line of credit concentration by largest single group borrower: the largest single group borrower and its related parties has a total

of RMB328.06 million in Line of credits which is 9.1% of net regulatory capital payable to the Bank and the level is 5.9 percent lower than

regulatory guideline at 15%.

Related parties Line of credit: All related parties have loans outstanding RMB981.77 million by the end of 2006. The proportion of

outstanding loans of all related parties is 27.22% of net regulatory capitals to the Bank, which is 22.78 percentage points lower than

regulatory guideline at 50% level.

Loan concentration by non-local borrowers: Outstanding Loans of Non-local Borrower is RMB740.24 million, which is 2.63% of

the total loan (RMB28134.90 million) payable to the Bank. The figure is 7.37 percentage points lower than regulatory guideline at 10%

level.

Top 10 customers’ loan ratio: Total outstanding loans to the top ten customers are RMB1764.29 million to the Bank by the end of

2006. Total outstanding loans payable to net regulatory capital ratio is 48.92% which is 1.08% lower than regulatory criteria and down

28.31 percentage points from last year. Total outstanding loans to the top ten customers to total loans ratio is 6.27%, down 3.17

percentage points than that of last year.

List of largest ten single borrowers

(units: in RMB thousand /in USD thousand)

Rank Name RMB Foreign currency Balance Proportion to net Prop. to regulatory capital

1 Ningbo Inner City Reconstruction Office 200000 - 200000 5.55 0.71

2 Ninghai ETDZ Xinxin Industrial Park Co., Ltd 200000 - 200000 5.55 0.71

3 Ningbo Communication Real Estate Co., Ltd 194930 - 194930 5.4 0.69

4 Ningbo Zhenhai Zone Urban Construction 180000 - 180000 4.99 0.64

Investment Development Co., Ltd

5 Ningbo Jiangbei Zone Investment 179000 - 179000 4.96 0.64

Venture Development Co., Ltd

6 Ningbo Airtac Automatic Industry Co., Ltd 174020 - 174020 4.82 0.62

7 Ningbo Yuanwang Huaxia Real Estate 170000 - 170000 4.71 0.6

Development Co., Ltd

8 Konced Group Co.,Ltd 158550 - 158550 4.4 0.56

9 Ningbo Zhenhai Investment Co., Ltd 156500 - 156500 4.34 0.56

10 Ningbo LG Yongxin Latex Co., Ltd 151290 - 151290 4.19 0.54

Total 1764290 - 1764290 48.92 6.27

Liquidity ratio: Liquidity ratio is 63.46%, decreased 19.79 percent points than that of last year and 38.46 percentage points over

regulatory standards, which is 25% level.

Mid-long term loan ratio: Mid-long term loan to mid-long term deposit ratio is 101.78%, which is 18.22 percentage points lower than

regulatory standards at 120%.

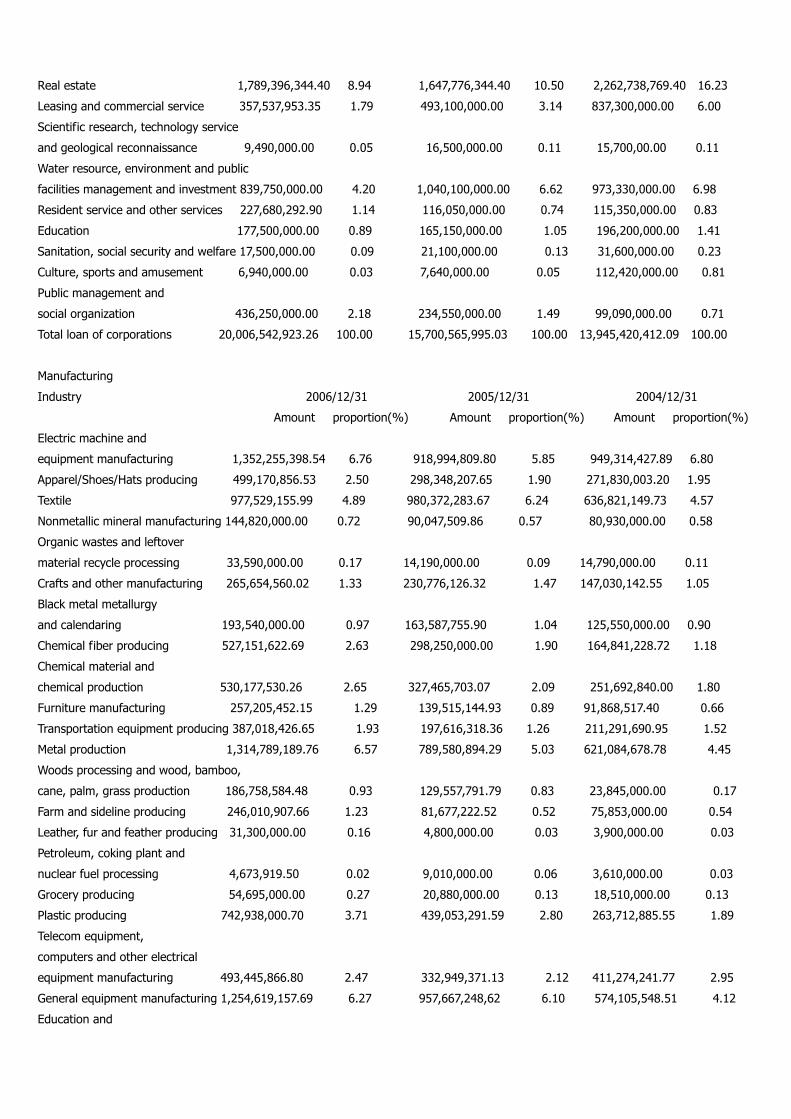

B. Loan concentration by top five industries (units: in RMB thousand )

Rank Industry Balance Proportion

1 Manufacturing 11220287 39.88

2 Individual person 8128356 28.89

3 Wholesale and retail 3333513 11.85

4 Real estate 1789396 6.36

5 Irrigation works, environmental and public facilities management 839750 2.98

Total 25311302 89.96

C. Loan classification

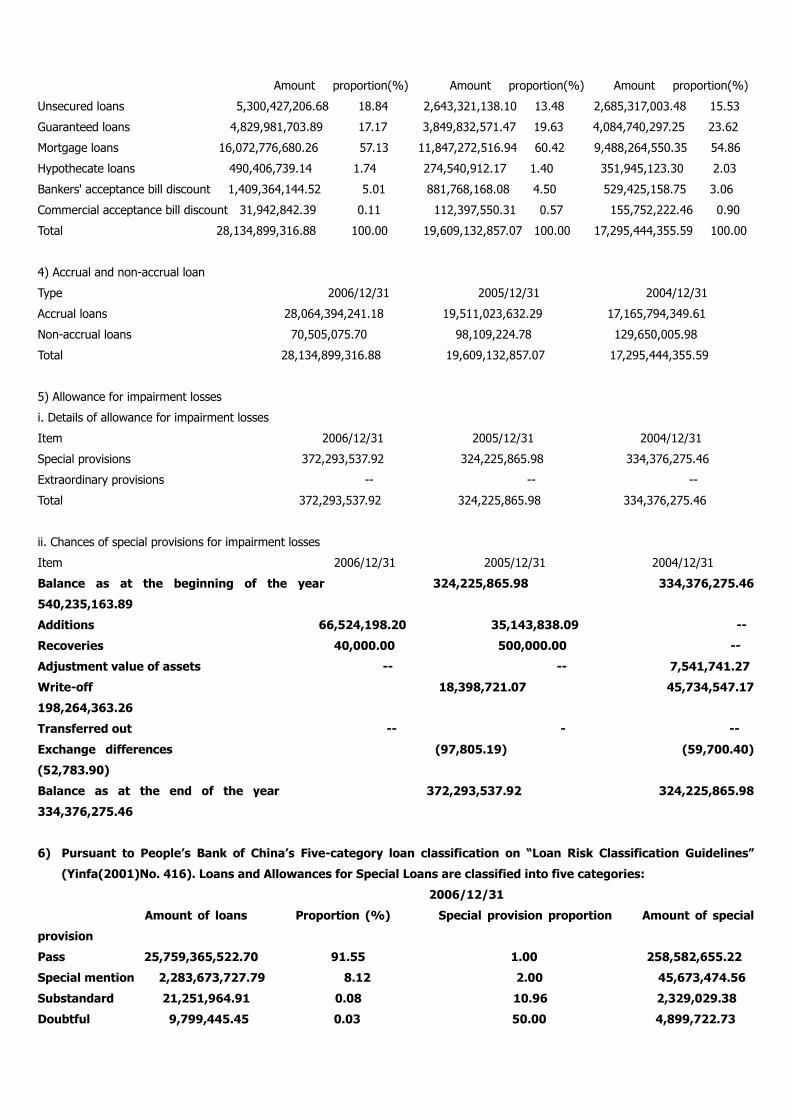

The Bank started to apply a Ten-category Loan Classification Principle to measure and manage the quality of credit assets from December

2005, which is based on the Five-category Loan Classification Principle. The method further decomposes ‘pass’loan into three categories,

which are pass +, pass and pass-, subdivided ‘special-mention’loan and into special-mention +, special-mention, special-mention – three

categories, classified two levels in ‘substandard’loan, substandard + and substandard.

By the end of 2006, loan outstanding of substandard loan is RMB21.25 million with 8 basis points to the total loan that is 9 basis points

lower than that of at the beginning of the year. Loan outstanding of doubtful loan is RMB9.8 million, representing a decrease of 1 basis

point to 0.03% from that at the beginning of the year. Loss loan dropped 18 basis points to 0.22% with RMB60.81 million loan

outstanding. Total non-performing loans outstanding amount is RMB91.86, which improved 28 basis points to 0.33%.

D. Changes of special provision for loan losses (units: in RMB thousand)

Items 2006 2005 2004

Balance at the beginning of the year 324,226 334,376 540,235

Provision for the year 66,524 35,144 -

Withdraw for the year 40 500 -

Draw back of appreciation of assets value - - 7,542

Write-off 18,399 45,735 198,264

Transfer out - - -

Converting differences -98 -60 -53

Balance as at the end of year 372,294 324,226 334,376

E. Repossessed assets

Repossessed assets are accounted as ‘Assets held for sale’ and reported in ‘Other assets’. As of 31 December 2006, the Bank has

repossessed assets of RMB108.41 million, including RMB104.55 real estate, which consists 96.43% of the total, repossessed assets, and

the remaining is other repossessed assets with RMB3.86 million.

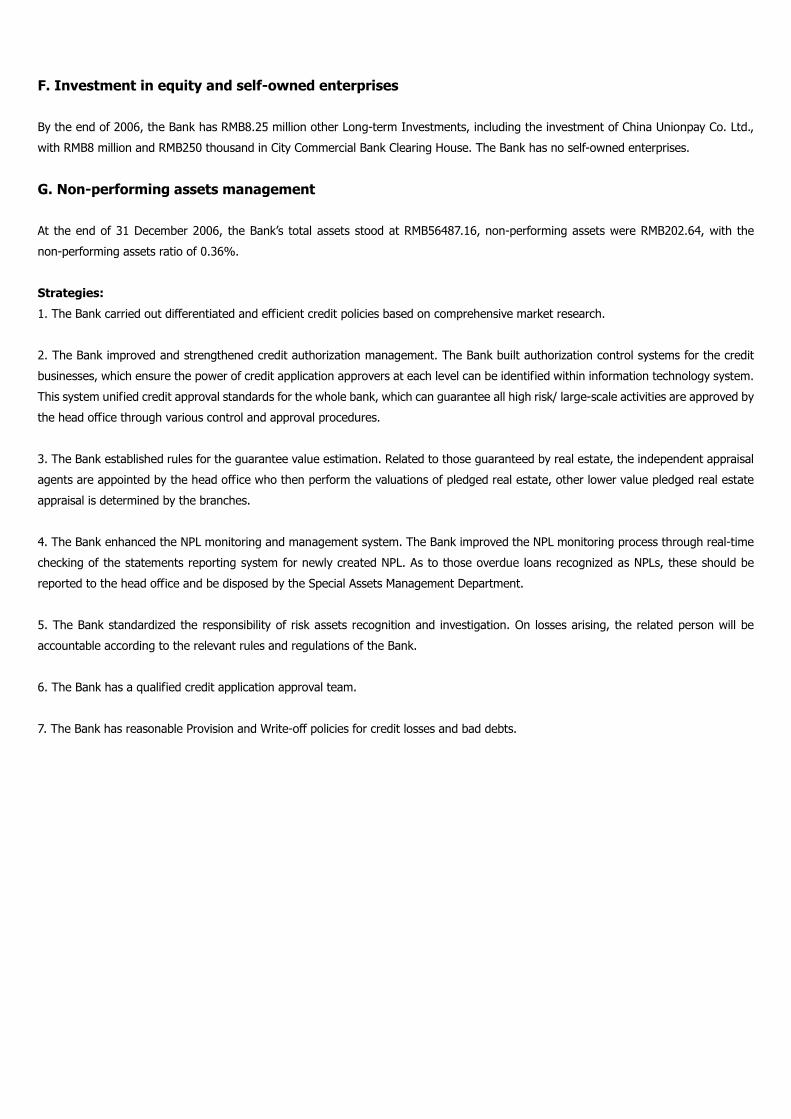

F. Investment in equity and self-owned enterprises

By the end of 2006, the Bank has RMB8.25 million other Long-term Investments, including the investment of China Unionpay Co. Ltd.,

with RMB8 million and RMB250 thousand in City Commercial Bank Clearing House. The Bank has no self-owned enterprises.

G. Non-performing assets management

At the end of 31 December 2006, the Bank’s total assets stood at RMB56487.16, non-performing assets were RMB202.64, with the

non-performing assets ratio of 0.36%.

Strategies:

1. The Bank carried out differentiated and efficient credit policies based on comprehensive market research.

2. The Bank improved and strengthened credit authorization management. The Bank built authorization control systems for the credit

businesses, which ensure the power of credit application approvers at each level can be identified within information technology system.

This system unified credit approval standards for the whole bank, which can guarantee all high risk/ large-scale activities are approved by

the head office through various control and approval procedures.

3. The Bank established rules for the guarantee value estimation. Related to those guaranteed by real estate, the independent appraisal

agents are appointed by the head office who then perform the valuations of pledged real estate, other lower value pledged real estate

appraisal is determined by the branches.

4. The Bank enhanced the NPL monitoring and management system. The Bank improved the NPL monitoring process through real-time

checking of the statements reporting system for newly created NPL. As to those overdue loans recognized as NPLs, these should be

reported to the head office and be disposed by the Special Assets Management Department.

5. The Bank standardized the responsibility of risk assets recognition and investigation. On losses arising, the related person will be

accountable according to the relevant rules and regulations of the Bank.

6. The Bank has a qualified credit application approval team.

7. The Bank has reasonable Provision and Write-off policies for credit losses and bad debts.

H. Main off-balance items and risk management statement

Off-balance sheet (unit: in thousands of RMB)

Items

Balance as at the end

of the year Bails

Assessment

value of

collaterals Unsecured loans

Increase during

the year

Revalua

tion

Advances at

the end of

year

Advances

increase during

the year

RMB 9178823.92 5101434.40 2189349.84 1888039.67 21366299.06 - 904.00 1845820.78

Foreign

currency

1316241.61

224360.95 86620.66 1005260.00 8910976.03 - - 966.44

1.Guarantee

Total 10495065.53 5325795.35 2275970.51 2893299.67 30277275.09 - 904.00 1846787.21

RMB 8856094.46 4938199.33 2174338.20 1743556.93 21103635 - 904.00 1845820.78

Foreign

currency - - - - - - - -

2.Bank acceptances

Total 8856094.46 4938199.33 2174338.20 1743556.93 21103635.35 - 904.00 1845820.78

RMB - - - - - - - -

Foreign

currency 1274724.74 193118.45 86620.66 994985.63 8847049.25 - - 966.44

3.L/C issuing

Total 1274724.74 193118.45 86620.66 994985.63 8847049.25 - - 966.44

RMB 322729.46 163235.07 15011.64 144482.75 262663.71 - - -

Foreign

currency 41517 31242.50 - 10274.37 63926.78 - - -

4.Letter of guarantee

Total 364246.33 194477.57 15011.64 154757.11 326590.49 - - -

RMB - - - - - - - -

Foreign

currency - - - - - - - -5.Guarantee for bond

issuance

Total - - - - - - - -

RMB - - - - - - - -

foreign

currency - - - - - - - -6.Guarantee for convertible

bond Total - - - - - - - -

RMB - - - - - - - -

Foreign

currency - - - - - - - -7.Other guaranty businesses

Total - - - - - - - -

RMB - - - - 111850.00 - - -

Foreign

currency - - - - - - - -8.Commitment

Total - - - - 111850.00 - - -

RMB - - - - 118500.00 - - -

Foreign

currency - - - - - - - -

9.Loan commitment

Total - - - - 11850.00 - - -

RMB - - - - - - - -

Foreign

currency

- - - - - - - -

10.Revolving Line of credit

Total - - - - - - - -

RMB - - - - - - - -

Foreign

currency

- - - - - - - -

11.Other commitment

Total - - - - - - - -

RMB - - - - - - - -12.Financial derivatives

Foreign

currency

- - - - - - - -

13.Options Foreign

currency

- - - - - - - -

14.Swaps Foreign

currency

- - - - - - - -

RMB - - - - - - - -15.Forward for foreign

exchange Foreign

currency

- - - - - - - -

I. Main risks and strategies

As a special financial institution, there are many risks affecting the Bank to certain degrees, such as credit risk, market risk, operational

risk, liquidity risk, reputation/brand risk and other miscellaneous risks which are risks beyond management’s ability to control, regulate

(through policies or legally), and so on.

With sufficient reference to the successful practices of international leading banks, the Bank implemented steady progress in its risk

management system, further improved its risk management ability with a view to promoting complete, centralization, professionalism,

matrix reporting in its risk management reform. Meanwhile, the Bank established rigorous risk monitoring system through combining

internal control and external auditing mechanism. The Bank appointed Ernst and Young, Shu Lun Pan Certified Public Accountants Co.,

Ltd. as independent auditors, was inspected and audited by external regulatory authorities, such as Auditing Bureau, CBRC and PBC

Ningbo.

Credit risk management

1. The Bank further improved and revised policies and guidelines, meanwhile, actively adjusted the credit structure.

In 2006, the Bank enhanced market analysis and prediction, researching changes of different industries of its credit business, realizing

pre-warning controls for credit risk. According to the risk management scheme for the year 2006, which was carried out at the general

meeting of Board of Directors at the beginning of the year, the Bank established ‘the Lending Guidelines of NBCB 2006’, which set up

differentiated guidelines for corporate customers and retail customers.

2. The Bank implemented the internal credit rating of customers, established the credit of entry and exit mechanisms.

The Bank set up an overall customer internal credit rating system through quantitative analysis combined with qualitative analysis, static

and dynamic analysis. Through implementing internal credit rating, the Bank set up its credit entry and exit mechanisms, which is

complied within our risk control requirements, further improved the mix of our loan portfolio with the reduction of NPL arising.

3. The Bank improved its authorization management.The Bank adjusted authorization letters on a timely basis according to the change of

personnel or the previous authorization letters are invalid, meanwhile, we rigorously standardized our re-authorization, temporary

authorization, and specialized authorization management processes. All intercity credit businesses should be authorized by the head

office and operated at tier one branches, other than Bank Acceptance Discount, Commercial Acceptance Bill Discount which is approved

by the head office, Acceptance of 100% security deposits for the Bank Acceptance. Bank Acceptances are operated in tier one branches

and are prohibited to be performed by tier two branches.

4. The Bank strengthened and standardizedits post-credit analysis and inspection control.

5. The Bank implemented a personal lending quantitative credit rating system, which further improved and specialized its credit risk

management.

6. The Bank employed ten-category classification for its credit business, further broke down five-category classification into ten

categories, which are Pass+, Pass, Pass-, Special-mention+, Special-mention, Special –mention-, substandard+, substandard-, doubtful

and loss. We disclosed changes of our asset quality by auditing loan classifications and analyzing asset quality on a seasonal basis; based

on associated data, the Bank implemented five-category classification for the total loan portfolio.

7. The value evaluation management for collaterals and pledged goods was improved and standardized which reduced credit risk for the

Bank. The confirmation of estimated real estate value over equivalent to RMB 2 million should be performed internally by the Risk

Management Department in the head office or by other assets appraisal companies who are appointed by the Risk Management

Department.

Market risk management

1. A series of market risk management policies and rules were set up by the Bank, which ensure market risk management can be

pursuant with the proper documentary rules.

2. The Bank set trading limitation and controls for each trader and created an authorization systemin line with the treasury business. The

Bank manages market risk through setting up investing, trading and stop-loss limits for securities; daily, overnight exposure position limits

and stop-loss limits for foreign exchange. Pursuant to tiered authorization requirements, the Bank implemented tiered authorization

management from the Board of Directors, president, general manager of Treasury Operating Department to the traders.

3. The Bank implemented middle office risk management monitoring to the treasury business.

4. A product innovation committee was set up, which is responsible for the bank’s new products development and management.

Liquidity risk management

1. The Bank set up a series of rules and policies for liquidity risk management, which ensured liquidity risk management, is in accordance

with the correct documentary rules.

2. The Bank set up Asset and Liability Management Committee, which is responsible for the establishment of targets and policies for asset

and liability management, asset and liability operation monitoring and decision-making for significant events concerned with asset and

liability management for the whole bank.

3. The Bank control and monitor regulatory indicators through managing risk level indicators, risk migration indicators and risk offset

indicators.

Operational risk management

1. The Bank established guidance on banking crime resolution 2006, and carried out specific measures and approaches for the Bank to

enhance its competence in fighting banking irregularities. The Bank conducted self-inspection and on-the-spot specific inspection through

a vertical management model, in the corporate line, retail customer line and operational line within the whole bank, which ensured no

material criminal cases occurred in the year 2006.

2. The Bank tried to prevent commercial bribes to enhance curbing rule-breaking irregularities on commercial bribe. The Bank inspected

case by case and put forward specific measures on different divisions to fight against banking violations, such as capital construction,

material purchasing, credit business, special assets management, IT department and sales staffs in branch level.

3. The Bank efficiently and effectively prevented operational risk on account distribution through centralizing account distribution to the

head office in bank acceptance, trade finance in international banking, credit business in personal banking and all other credit business

except discount.

4. The Bank improved operational risk on bank acceptance by setting up rules of operational flow for the Bank acceptance transactions,

which clearly formulated provisions of sales, acceptance and transfer for bank acceptance.

5. Security management for personal E-Banking was improved. The Bank applied dynamic password instead of formerly transaction

password for the personal E-Banking business, which ensured the E-Banking transactions were executed with increased safety .

6. A fingerprint verification system substituted previous operational card in the Bank’s core accounting system AS400 to prevent potential

operational risk in checking and authorization.

7. After June 2006, the head office inspected and audited the branches in respect of corporate banking, personal banking and

administration and carried out internal control assessments for internal monitoring and control of each branches.

8.In order to reduce the information updating risk in IT system, the Bank use Concurrent Version System and two-people updating

principle to control the risk. In respect to mitigating the incomplete test risk, the Bank formulated a program for updating and restoring,

which can return to the correct program version prior to a failure in testing of newly compiled software in time.

Legal and compliance risk management

1. The Bank conducted legal examinations on standard form contract amendments, non-standard form contracts, other non-standard

form contracts that over RMB1 million, business agreements and new products’legal risk prevention, providing assurance to the legality,

compliance and validity of the credit business.

2. The Bank further mitigated legal risks through examining different standard form contracts, formulating specific contract for the new

products.

3. The Bank revised and amended the Article of Association cooperated with an external legal agent, reelected directors and supervisors

of the Board of Directors and the Board of Supervisions which provide effective corporate governance in the Bank.

4. Legal and Compliance risk management provide compliance support to product innovation and process reengineering.

J. Strategies to improve internal control

1. An Internal control system was comprehensively integrated and improved. Pursuant to ‘Commercial Bank Internal Control Guidance’

and ‘Commercial Bank Internal Control Assessment (for trial implementation)’ issued by CBRC, the Bank further formed, revised and

improved infrastructure of the internal control system. By further playing the roll of early risk warning, improving and building an internal

reporting system, the Bank provides assurance as to standardize operations from systems building, preventing initiating of risk. In 2006,

the Bank formulated and revised 192 different material rules and policies.

2. The Operational risk management structure was improved; the rebuilt operational risk prevention processes were implemented and

self-analysis, assessment mechanism of the operational risk was improved which accompanied with the introduction of separating and

controlling front, middle and back offices.

3. The Bank implemented an internal control assessment system within different levels of the branches. An Audit department regularly

assessed internal controls of corporate banking, personal banking and administration management in the different branches. According to

the results of the assessment ratings, the internal control of assessed branches, The results would influence the synthesis business

administration assessment for the branches and is one of the qualification requirements for director and vice director of branches.

4. The Bank adopted vertical inspection for specific governance of internal control in four lines, which are personal banking, corporate

banking, clearing and IT. Audit department in the head office regularly evaluate the result of inspection in respect of branches and

different departments.

Report of the Board of Directors

A. Management discussion and analysis

1. Scope of principal activities and operating conditions

The scope of our principal operating business are various banking businesses approved by the China Banking Regulatory Commission

(CBRC), including: absorption of deposits; release of short-term, medium–term and long-term loans; domestic settlements; discounting;

issuance of financial bonds; issuance, payment, subscription of government bonds on behalf of the state; trade of government bonds;

inter-bank lending/borrowing; bank guarantee; payment/collection agent and insurance agent; safe deposit box; consignment loan of

local fiscal revolving fund; foreign currency deposits, loans, and remittance; international settlement; purchase and sale of foreign

currency; inter-bank foreign currency lending/borrowing; acceptance and discount of foreign-currency paper; foreign currency guarantee;

and all other business under the approval of CBRC.

During the reporting period, the Bank has completed all tasks of the current year by introducing an overseas strategic investor, optimizing

operations and management workflows, actively promoting product services and derivatives, changing the operational concept and

marketing patterns. By the end of the reporting period, the total assets of the Bank reached RMB56.546 billion with a 33.27% increase

from the year-beginning base; deposit amounts increased by 23.10% to RMB46.191 billion; loan amount totaled RMB28.135 billion, with

a increment of 43.48%; net profit reached RMB632 million; ROE reached 23.79%; ROA approached 1.3%; CAR is 11.48%; the core

capital adequacy ratio reached 9.71%; NPL ratio dropped by 0.28% to 0.33% from the beginning of the year; the provision ration soared

to 405.28% with a 145.26% improvement.

During the reporting period, the Bank endeavored to adjust the capital and customer structure. Meanwhile, the personal banking business

was also greatly enhanced. These efforts promoted the business development and improvements reliably and rapidly.

During the reporting period, corporate deposits increased by RMB6.248 billion to RMB36.933 billion; corporate loans amounted

RMB20.007 billion with a growth of RMB4.306 billion; the new effective clients totaled 486 in the whole year.

Saving deposits increased by 35.43% to RMB9.258 billion; saving deposits recorded 20.04% of the total deposit amount, raised by 1.82%;

personal loan balance increased by 107.93% to RMB8.128 billion; personal loan represents 28.89% of the total loan amount, a growth of

8.96%.

Newly issued HuiTong deposit cards reached 531.5 thousand and outstanding card amount totaled 928.8 thousand. Our credit card

increased by 75 thousand and its total issuance is 102.5 thousand.

We realized USD4.73 billion in International Banking, recording a growth of 39%. E-banking volume accumulated RMB78.971 billion, or

RMB6.581 billion on a monthly average.

At the same time, the Bank actively developed its treasury business. In Oct. 2006, we were approved to operate financial derivatives,

becoming the forth city commercial bank actively participating in this business area. Our first HuiTong RMB/foreign currency (FC) product

has been launched. In 2006, we issued certificate T-bonds with an amount of RMB780 million, which constitutes one-thirds of the total

amount of certificate T-bonds issued in Ningbo. We realized earnings of RMB409 million in dealing T-bills. By steadily developing the

trading business, which earned RMB25.28 million.

i. Increment of major operating income, operating profit, net profit, cash equivalents during the reporting period.

(unit: in RMB thousand)

Items Closing balance Balance of the prior year Increase/Decrease%

Operating income 1,600,803.72 1,230,573.95 30.09

Operating profit 838,695.90 653,380.64 28.36

Net profit 632,084.51 471,950.69 33.93

Balance of cash and cash equivalent 5,249,506.15 5,392,724.11 -2.66

ii. Comparisons of the total assets and equity between the starting balance and closing balance.

(unit: in RMB thousand)

Items Closing balance Starting balance Increase/Decrease %

Total assets 56,546,232.89 42,429,347.76 33.27

Equity 3,196,183.70 2,187,172.07 46.13

iii. Our organizations

The Bank has 68 branches and outlets and 38 remote-ATMs at present.

iv. Principal products and market share

At the end of the reporting period, the total deposits are RMB46.191 billion, constituting 9.81% of the market. The total loan recorded

RMB28.135 billion, occupying 7.21% of the market. The accumulated credit card issuance is 102.5 thousand, ranking it number 1

amongst other lenders in Ningbo city.

2. Major holding companies

(unit: in RMB thousand)

Name Investment tenor Proportions of total shares(%) Shares at the end of the year

China UnionPay Co., Ltd. 0.48 8,000.00

City Commercial Bank Fund Clearing House 0.83 250.00

3. Major clients

During the reporting period, the Bank’s top-10 borrowers are as following:

(unit: in RMB thousand)

Name of clients Industry Loan balance Ratio

Ningbo Inner City Reconstruction Office Irrigational, environmental

and public facilities management 200,000.00 0.71

Ninghai ETDZ Xinxin Industrial Park Co., Ltd Public management and social

organization 200,000.00 0.71

Ningbo Communication Real Estate Co., Ltd. Real estates 194,930.00 0.69

Ningbo Zhenhai Zone Urban Construction

Investment Development Co., Ltd. Real estates 180,000.00 0.64

Ningbo Jiangbei investment

Venture Development Co., Ltd. Public management and social

organization 179,000.00 0.64

Ningbo Airtac Automation Industry Co., Ltd. Manufacturing 174,022.70 0.62

Ningbo Yuanwang Huaxia Real estate Co., Ltd Real estate 170,000.00 0.60

.

Konced Group Co.,Ltd. Manufacturing 158550.00 0.56

Ningbo Zhenhai Investment Co., Ltd. Irrigational, environmental

. and public facilities management 156,500.00 0.56

Ningbo LG Yongxing Latex Co., Ltd. Manufacturing 151,290.14 0.54

Total 1,764,292.84 6.27

By the end of the reporting period, the net capital of the Bank reached RMB3.607 billion. The largest borrower is Ningbo Inner city

Reconstruction Office, its loan balance is RMB0.2 billion, constituting 5.55% of the total net capital. This complies with the requirement

set by the supervisory authority that the loan balance of a single borrower must not exceed 10% of the net capital of a bank.

4. Five-Category classification of loans and loss provision of loans

(unit: in RMB thousand)

Item Amount Proportion to total loans(%)

Pass 25,759,365.52 91.55

Special-mentioned 2,283,673.73 8.12

Substandard 21,251.96 0.08

Doubtful 9,799.45 0.03

Loss 60,808.66 0.22

Total loans 28,134,899.32 100.00

Note: loan amount includes inter-bank discount and credit card loan balance;

By the end of the reporting period, the balance of loss provision is RMB0.372 billion,complying with supervisory requirements/guidance

on loss provisioning.

5. Challenges in operations and solutions

During the reporting period, the challenges we are facing include: governmental macroeconomic adjustments and diversity of corporate

financing channels; resulting in a decline in corporations’need for loans; With further development of financial market(s), complex

operating environments of banks and capital constraints, the development of the Bank is limited by the influence of such factors. In order

to mitigate or deal with the challenges outlined above, the Bank adopted the following measures (actions):

1. Completing assessment systems, optimizing workflows of management. We synthetically assess the operational targets, improve

internal controls, emphasis on team-working, and focus on the overall development and improvement of activities executed by our

sub-branches. The establishment and effective implementation of this assessment system greatly promoted overall development of

business and significantly enhanced the development of the Bank’s business. Further effort was introduced to optimize workflow of

management and to strengthen marketing and business expansion, achieved by improving management practices and creating new

marketing activities. A brand new management system of personal business; with a professional team dealing was introduced. In line

with market competency and business development. The Bank reviews and introduces optimized processes for over the counter services,

improving allocation of clerks and increasing efficiency.

2. Actively expanding all business to realize steady growth of every business. According to the annual scheme of risk management set by

the board, we outlined the credit policies for 2006. The continuous and steady development of corporate business, the greatly enhanced

expanding abilities and marketing abilities of the overall business, reflect that these policies have been well implemented through out the

whole year. Personal business witnessed a sound start, experienced break-through development, initially carving out a path for our

personal business and accumulated experiences for future development.The treasury business has just started up and financial derivative

business is approved to operate. Subscription of T-bills, investment and trading business has recorded a steady expanding.

3. Actively probing new risk management mechanisms, completing and implementing risk management measures, enhancing

construction of internal control regulations and promoting standards in risk management and internal-controls of the Bank. the Bank has

enhanced asset liability management, gradually established asset liability management system with risk prevention/mitigation at its core,

and with risk supervision, risk assessment, risk prevention and risk control as its main procedures. the Bank implemented quantitative

evaluation for credit; internal credit-rating of clients, ten-catogory risk classification, and individual borrowers. We enhanced

post-examination of credit loan clients. The in-out mechanism of credit loan has also been built up. At the same time, we actively

promoted banking crime resolution and commercial bribe. The Bank further utilized risk assessment effect and complete, accurate

internal-reporting mechanisms to ensure operational consistency and to prevent against risks from the source.

4. Promoting strategic co-operation with OCBC Singapore. We constructed ‘Five-year A Hundred Persons Fostering Plan’and Technology

Assistance Commission with OCBC. The plan now is entering into the implementing phase. Four groups of our personnel will be sent to

OCBC to learn about and investigate the retail business, treasury business, financial business, corporate banking business and risk

management. OCBC will also dispatch staff to assist the preparation, application and product development of our financial derivative

business.

5. Improving exchange of employees and strengthening man-power reservation. In line with human-resource demand of our business

development, we actively improved human-resource planning, allocation and hiring. In order to resolve personnel gaps in sub-branches,

we have accepted 224 college graduates in 2006. the Bank expanded the channel of personnel introducing and enrolled senior talents

specialized in wealth management, cash management, trasury management products from overseas. We have also run all kinds of

specific fundamental training to promote the quality of our employees.

6. Promoting development of technology system to support the business development and risk management. Based on perfecting the

AS/400 core system, we actively developed other business systems, including completion of 1104 statements supervisory system,

utilization of small-amount-payment system, completion of the first phase of Customer Service Center, initiation of data-base construction,

basic completion of audit sheets system, implementation of corporate-class CIF(customer information foundation) system construction,

preliminary construction of CIF system and introducing and development of money management system. The completion and

construction of these systems provided business development and risk management ability with powerful technical assurance.

7. Praperation an IPO program and implementing tran-regional operations. In order to speed up our business development, raise

operation/management standards and core competency, and to build up capital-supplementary mechanism, the Bank launched an IPO

application program in Aug. 2006. Under our efforts, IPO application materials were officially accepted by CSRC (China Security

Regulatory Commission) IN Nov. 2006. Meanwhile, in order to promote comprehensive competency and expand business development

scope, the Bank applied to set up a Shanghai Branch, and the supervisory authority approved our application in Jan. 2007.

8. Further strengthening the construction of the Board of Directors, promoting operating efficiency and decision-making ability, perfecting

corporate governance mechanism and standardizing corporate governance activities. Based on the completion of special commissions of

the Board, these commissions better performed their effects, the Board of Directors continuously promoted its operating quality and

efficiency to ensure all businesses run healthily. We formulated and implemented the Bank’s ‘Three-year Development Plan’, constructed

IPO scheme according to requirements imposed on IPO program, we further enhanced the construction of corporate governance

mechanism, modified the Bank’s article of association and the discussion rules of the Board of Shareholders and the Board of Directors.

We formulated methods of introducing independent directors to the board the implementation method of the trading rules of related

parties, the method of investor relationship management, the method of information release management, the detailed working rules of

the board secretaries, and the detailed working rules of the presidents. According to the requirements placed on corporate governance,

the Bank adjusted and supplemented members in the Board of Directors and the Special Commissions, and optimized the structure of

corporate governance. The assessment mechanism for directors and mutual-assessment mechanism for independent directors, the

appraisal mechanism for senior management and senior managers have been established. We also further perfected and implemented

communication-feedback mechanism, implemented reporting mechanism of highlighted affairs among directors, so that the directors’

right of being informed is ensured.

B. Statement of capital raising

Under its replied document (Yinjianfu[2006]No.115), CBRC has approved OCBC to make investment to the Bank in a manner of increasing

capital and expanding shares outstanding. OCBC purchased 250 million shares of our stock for RMB570 million at RMB2.28 per share. The