Embed Size (px)

Citation preview

Status Paper on Acc&nting Reforms in Lou1 Bodies in India

and kole of Chartered Accountants

THE NSTITLITE OF CHARTERED ACCOUNTANTS OF INDIA (5otupbysnAelobParIimm~)

MEW DELHl

������������

����������� ���� ������������� �� �����

�������� ��������������������

������������������ ������������������������������ ������������� ������� �������������� �� �

��!� ����

��������

���� ����� ����� �� �� ��� ���� ���� ��� ������ �������� ������� �������������������� �������� ��������������������������������������������������������������� ���������������������� �� ������������������������������������������������������������ ���������������������� ��������������������������������������������������������������� ����������!������������������������������������������������������������ �������� ������������������������������� ���������������������������������������������

�������������������������������� ��������"���������#���������������������$�"#��%���� �������� ��� ������������ ���#����� ����&��������������������������������������������������� �������������������������

����������������������'����������������������������"������������������ ��� ���������������������������� ����������������� &��� ��� ����� �� ��������� ��� ������ ������(������ ��#�������� ��� ������ ��������"���������#������� ���� �����������������������������#����� ����

���� ������������������#����� ����&����������&� ��������� �������� � �������������������������������

)�&�*��� �"�������#��$��%� ��&��+,�*��� �����-../ ��������

1

Status paper on Accounting Reforms in Local Bodies in India...

Status paper on AccountingReforms in Local Bodies in India

and Role of CharteredAccountants

GENESIS OF ACCOUNTING REFORMS

• Mumbai and Chennai Municipal Corporations initiated theDouble Entry Accrual Based Accounting System in 1981-1991. Similar reforms were initiated in the State of Gujaratduring the period 1990-1995. These reforms initiatives weremade under the guidance and support of World Bank Projects.

• Recognising the need of transparency and accountability inthe Local Bodies, the 73rd and 74th ConstitutionalAmendments incorporated provisions with respect totransforming the Local Bodies and consequently theseconstitutional amendments paved the way for initiating theaccounting reforms in Urban Local Bodies and PanchayatiRaj Institutions in India.

• The financing of urban infrastructure in urban local bodiesremained major concern of the policy makers for considerabletime. The programme for development of urban infrastructurefinancing system through debt market in India by using theHousing Guarantee (HG) funds for contemplating the issuingof debt instruments to finance urban infrastructure projectswas not possible without reforming the accounting practices.The USAID through Financial Institutions Reform andExpansion programme (FIRE-D) provided the HG funds ofUS $ 125 million for a period of 30 years to develop an urbaninfrastructure finance system. HUDCO and IL&FS acted asthe financial intermediaries to channel funds along with a

Status paper on Accounting Reforms in Local Bodies in India...

2

matching amount of locally raised funds to municipalities orprivate sector entities to finance selected commercially viableurban infrastructure projects relating to water supply,sewerage, solid waste management and area development.The double entry accrual accounting was one of theprerequisite for financing these infrastructure projects.

• In January, 1999, the State of Tamil Nadu approved a measureto begin with pilot testing of Double Entry Accrual BasedAccounting System in two municipal corporations and 10municipalities. With the pilot project successfully in progress,the State inaugurated this new system in its remaining threemunicipal corporations and 92 municipalities on April 1, 2000.Tamil Nadu is the first state in India to initiate such extensiveaccounting reforms on a state-wide scale. The cities of Jaipurand Anand also initiated accounting reform process in 1999.In the year 2001, the State of Maharastra with the support ofWorld Bank – Technical Assistance (WB-TA) set on roll theprocess of accounting reforms in local bodies.

• In order to leverage this accounting reforms process, theInstitute of Chartered Accountants of India felt the need oflocal bodies and brought a publication ‘Technical Guide onAccounting and Financial Reporting by Urban Local Bodiesin India’ in 2000. This publication provides a broad frameworkfor reforming the accounting systems so as to provide theguidance for switching to double entry accrual system inthese bodies.

• The Eleventh Finance Commission in the year 2001recommended the introduction of Double Entry AccrualAccounting System.

• The Honourable Supreme Court of India recognising thedefects of single cash based accounting system in urbanlocal bodies delivered the judgement in case of Almitra Patelvs. Union of India in 2001 directing the Government to developguidelines for moving towards full cost based accrualaccounting system in urban local bodies.

3

Status paper on Accounting Reforms in Local Bodies in India...

PARADIGM SHIFT IN ACCOUNTING REFORMS

• Shifting trend of population indicates that in next 12 years theurban/semi-urban population of India would be around 50% ofthe total population. Keeping in view these trends in urbanpopulation; the planned improvement of urban infrastructureneeds to be developed. The pace of development should alsoneed to be aligned with the growth of urban population. TheGovernment of India and State Governments have initiatednumber of programmes for reforming urban sector. TheDouble Entry Accrual Accounting in Local Bodies is one ofthe important component of the urban reforms process.

• The Union Budget of 2002-2003 started a project by settingup Urban Reforms Incentive Fund (URIF). This fund hadprovision of 10% of total budget for introduction of DoubleEntry System of Accounting in Urban Local Bodies.

• The Task force of Comptroller & Auditor General made areport in 2002 recommended the accounting reforms in localbodies. The recommendations were: (i) uniform formats forfinancial statements and budget (ii) formats for determiningthe cost of important utilities and services like water supplyetc. and showing this information by way of disclosure to theaccounts (iii) significant accounting policies to be followed byULBs as per model accounting policies need to be disclosedin a separate schedule forming part of the accounts and(iv) initiate steps for smooth switch over to the double entryaccrual system of accounting.

• Municipal Corporation of Delhi is the first local body reduce inthe country to switch to the accrual-based, double-entryaccounting system in 2003. The ICAI-Accounting ResearchFoundation assisted the MCD in accounting, financial andmanagement reforms.

• The Model Municipal Law (MML) in 2003 vide Chapter XII(Appendix – I) incorporated the provisions relating to Accounts

Status paper on Accounting Reforms in Local Bodies in India...

4

and Audit requiring inter alia to prepare Income & ExpenditureAccount and Balance Sheet and also to prepare MunicipalAccounting Manuals. The salient feature of MML are: (i) StateGovernment to prepare municipal accounting manual (ii)capital and revenue heads to be separated in municipalaccounts (iii) separate accounting heads proposed for watersupply, roads etc. (iv) municipalities to prepare annual balancesheets (v) annual subsidy and environmental status reports(vi) provision for appointment of chartered accountants asauditors (vii) comprehensive debt initiation policy by stategovernment (vii) provision for appointment of a municipalaccounts committee and (viii) enabling access to capitalmarkets and financial institutions for capital investments.

o Status of State-wise Implementation of MML

• The MML has been implemented in the States/UTs of Bihar, Kerala, Nagaland, Sikkim, WestBengal and Andaman and Nicober Islands. Thedraft based on MML submitted to Governmentin the States of Rajasthan and Uttranchal.

• The review process of MML has begun in theStates/UTs of Andhra Pradesh, Chhattisgarh,Delhi, Goa, Gujarat, Haryana, Himachal Pradesh,Jammu and Kashmir, Karnataka, MadhyaPradesh, Maharashtra, Orissa, Punjab andTripura.

• The MML is under consideration in the Statesof Arunachal Pradesh, Chandigarh, Tamil Naduand Uttar Pradesh.

Source: Urban Finance, National Institute of UrbanAffairs, Vol. 10, No. 2, April–June, 2007.

5

Status paper on Accounting Reforms in Local Bodies in India...

FORMALISATION OF ACCOUNTING REFORMSPROCESS

• The Institute of Chartered Accountants of India (ICAI) in theyear 2005 constituted a Committee on Accounting Standardsfor Local Bodies (CASLB) to formulate the AccountingStandards for Bodies. The Committee has been establishedwith the primary responsibility to conceive and suggest areasin which Accounting Standards for Local Bodies (ASLBs)need to be developed, formulate ASLBs, integrate the ASLBsto the extent possible, with the International Public SectorAccounting Standards issued by the International Public SectorAccounting Standards Board, provide implementationguidance on ASLBs, review and revise the ASLBs, assistLocal Bodies in adoption of accrual system of accounting,and propagate the ASLBs among the stakeholders inpreparation and presentation of financial statements.

The Committee on Accounting Standards for Local Bodies(CASLB) has already published the ‘Preface to the AccountingStandards for Local Bodies’ in March 2007. The CASLB hastill now formulated two Accounting Standards for Local Bodiesnamely Accounting Standard for Local Bodies (ASLB) 3,‘Revenue from Exchange Transactions’ and AccountingStandard for Local Bodies (ASLB) 4, ‘Borrowing Costs’ andalso brought out the Booklet on ‘Accrual Accounting for LocalBodies: Elected Representatives & Stakeholders’ for thebenefits of Stakeholders and Representatives of the LocalBodies in particular and other Stakeholders in general. Allthe publications are available on the Institute’s website i.e.,www.icai.org. The status of the projects of the Committeefor the year 2009-2010 is at Appendix – II.

• The National Municipal Accounting Manual by the C&AG andthe Ministry of Urban Development, Government of India inthe year 2005 suggesting the modalities for implementingthe double entry accrual system. This manual was preparedby a firm of Chartered Accountants who were appointed for

Status paper on Accounting Reforms in Local Bodies in India...

6

the task. A pilot project for implementation of the draft manualin five Local Bodies was also successfully undertaken withthe aid of Chartered Accountants.

• The Ministry of Urban Development, Government of Indiahas constituted the Technical Committee on Budget andAccounting Standards for Urban Local Bodies on October03, 2006 with the main objective to recommend theAccounting Standards for Urban Local Bodies, formulated byCommittee on Accounting Standards for Local Bodies of theInstitute of Chartered Accountants of India, to the StateGovernments for notification.

• The Urban Local Government Disclosure Bill, 2006, aimed atthe need for bringing transparency and accountability infunctioning of Urban Bodies, has also a bearing on the reformprocess in general and double entry accrual system inparticular. This public disclosure law requires the municipalitiesto publish various information about its functioning on periodicbasis. Such information includes but is not limited to statutorilyaudited annual statements of performance covering operatingand financial parameters, and service levels for variousservices being rendered by the municipalities.

• The Jawaharlal Nehru National Urban Renewal Mission(JNNURM) is a reform linked incentive scheme for providingassistance to state governments and urban local bodies inselected 63 cities, comprising all cities with over one millionpopulation, state capitals and few other cities of religious andtourist importance for the purpose of reforming urbangovernance, facilitating urban infrastructure and providingbasic services to urban poor. This is the single largest initiativeof the Central Government in urban sector with an outlay ofRs. 50,000 crores and after adding the contribution of statesand municipalities the funding would be about Rs. 1,26,000crores over a period of seven years. This mission waslaunched by Government of India in December, 2005 withthe culmination of a process of neo-liberal urban reformsthat has been going on since late 1990s. Its predecessors

7

Status paper on Accounting Reforms in Local Bodies in India...

include Urban Reforms Incentive Fund (URIF) and ModelMunicipal Law (MML) both of which were formulated on thebasis of a set policy postulates developed by the WorldBank, the Asian Development Bank, the USAID and theUNDP. The Status of shifting to Double Entry AccountingSystem in the 63 cities and approved cost of UrbanInfrastructure Projects are given in Appendix – III.

o The Centre’s urban renewal mission is already goingplaces. It would now involve 28 more municipalities,with population over 5 lakh. When launched in 2005,the flagship scheme envisaged ‘coverage’ of 65 citieswith population of over 10 lakh, state capitals and touristand pilgrimage centres. The plan essentially is forinvestment support for stepped-up public transport,sewage disposal and water supply etc. For instance,what’s on the agenda is to provide funding-sharedequally between the Centre and the respective State formodern, low-floor buses in 118 towns and urban centreswith population over 2 lakh.

• The Guidelines on Tax free bonds by local bodies are alsolinked to adoption of modern, accrual-based double entrysystem of accounting in urban local bodies and audit of escrowaccount and the project account by a firm of CharteredAccountants appointed by the concerned State UrbanDevelopment Departments from the panel of CharteredAccountants approved by the C&AG.

• The Ministry of Urban Development, Government of Indiareleased the ‘National Municipal Accounts Training Manuals’for Elected Representatives and Staff of municipal bodies in2008 providing guidelines for understating the double entryaccrual system of accounting.

• Formulation of simplified Accounting system in PanchayatiRaj Institutions by C&AG in January 2007 which would workas start up and basic ingredient for smooth transitioning toaccrual accounting in the Panchayati Raj Institutions. Present

Status paper on Accounting Reforms in Local Bodies in India...

8

Status with regard to formulation of Chart of Accounts ofPanchayati Raj Institutions developed by C&AG is at Appendix– IV.

• The Ministry of Panchayati Raj, Government of India hasconstituted the Technical Committee on Budget andAccounting Standards for Panchayati Raj Institutions on May07, 2008 with the main objective to recommend theAccounting Standards for Panchayati Raj Institutions,formulated by Committee on Accounting standards for LocalBodies of the Institute of Chartered Accountants of India, tothe State Governments for notification. The TechnicalCommittee on Budget and Accounting Standards forPanchayati Raj Institutions has constituted a Sub-committeeconsisting of members representing Office of the Comptroller& Auditor General of India, Ministry of Panchayati Raj,Government of India, State Governments, Controller Generalof Accounts and National Informatics Centre for developingsimplified budget and accounting system and formats for PRIs.

• ‘National Municipal Assets Valuation Methodology Manual’has been brought out by the Ministry of Urban Development,Government of India in January 2009 suggesting detailedstep-by-step guidance to the municipalities for valuing theirfixed assets as envisaged in National Municipal AccountingManual.

ROLE OF CHARTERED ACCOUNTANTS IN LOCALBODIES

The Accounting Reforms are underway in the local bodies and inthis emerging area; the role of Chartered Accountants is as under:

Conversion of Accounts to Accrual Based DoubleEntry Accounting System

• Assessment of existing system and requirements includingreview of legislative framework with reference to existing

9

Status paper on Accounting Reforms in Local Bodies in India...

laws for smooth transitions into Double Entry AccrualAccounting System.

• Review of existing State Accounts Manual.

• Business process re-engineering with reference to AccrualSystem of Accounting.

• Categorisation, grouping and sub-grouping of assets andliabilities.

• Design of Chart of Accounts with Accounting Codes.

• Determination and valuation of fixed assets includinginfrastructure assets, current assets, investments, long-termliabilities, current liabilities and net worth as on openingbalance sheet date.

• Preparing formats of financial statements and voucher formatin the Accrual system.

• Design of Double Entry Accounting System on accrual basisfor Local Bodies.

• Preparation of opening balance sheet.

• Selection of appropriate accounting policies and drafting ofdisclosures of accounting policies.

• Implementation of Double Entry Accounting System on accrualbasis.

• Preparation of financial statements for the transition period.

• Training of finance and accounts personnel and training oftrainers.

Status paper on Accounting Reforms in Local Bodies in India...

10

Auditing and Assurance Services

• Assignment such as Internal Audit, Statutory Audit, andSpecial Audit of Local Bodies as provided in Model MunicipalLaw and Audit of Escrow Account and the Project Accountunder tax free municipal bonds guidelines (current status oftax free bonds approved for issue is at Appendix – V).

Management Consultancy Services

• Providing assistance as domain expert to the agenciesdesignated by the Government for computerization of recordsand computerization of Accounting System.

• Consultant in e-governance; implementation of IT basedManagement Information System and enterprises resourceplanning style system implementation.

• IT reforms including computerised accounting systemintroduction and implementation.

• Advising the Local Bodies in Statutory compliances,preparation of Detailed Project Feasibility Reports requiredto be submitted to the funding Agencies/programmes suchas World Bank, Asian Development Bank, USAID – FIRE –D, UNDP and JNNURM for enabling them to access capitalmarket and financial institutions for the capital investment.

• Consultant in drawing up reforms road-map, timelines andimplementation targets.

• Assisting in change management.

• Design and implementation of Budgetary Control System(Accrual Based Budget) in the line with the Accrual AccountingSystem and linkage among Budgetary System and FinancialManagement Information System and Decision-makingSystem.

11

Status paper on Accounting Reforms in Local Bodies in India...

• Revenue system assessment and financial analysis ofrevenue and expenditure exploring potential for raising debtcapital for projects, assessing financial viability of investmentplans, preparation of financial projections and revenuemobilisation plans of Local Bodies, undertaking detailedrevenue potential assessments, cost determination, controland reduction analysis, facilitating public private partnershipin new the projects and assist in bid process management,negotiations etc.

Status paper on Accounting Reforms in Local Bodies in India...

12

Appendix – I

Model Municipal LawChapter XII – Accounts & Audit

Maintenance of 88. The Chief Municipal Officer shall prepareaccounts. and maintain accounts of receipts and

expenditures of the Municipality in suchForm, and in such manner, as may beprescribed.

Preparation of 89. The State Government shall prepare andMunicipal maintain a Manual to be called theAccounting Manual. Municipal Accounting Manual containing

details of all financial matters andprocedures relating thereto in respect ofthe Municipality.

Financial statement. 90. (1) The Chief Municipal Officer shall,within four months of the close of a year,cause to be prepared a financialstatement containing an income andexpenditure account and a receipts andpayments account for the preceding yearin respect of the accounts of theMunicipality.

(2) The Form of the financial statement,and the manner in which the financialstatement shall be prepared, shall besuch as may be prescribed.

Balance sheet. 91. (1) The Chief Municipal Officer shall,within four months of the close of a year,cause to be prepared a balance sheet ofthe assets and the liabilities of theMunicipality for the preceding year.

13

Status paper on Accounting Reforms in Local Bodies in India...

(2) The Form of the balance sheet, andthe manner in which the balance sheetshall be prepared, shall be such as maybe prescribed.

Submission of 92. The financial statement prepared underfinancial statement section 90 and the balance sheet of theand balance assets and the liabilities prepared undersheet to Auditor. section 91 shall be placed by the Chief

Municipal Officer before the EmpoweredStanding Committee which, afterexamination of the same, shall adopt andremit them to the Auditor as may beappointed in this behalf by the StateGovernment.

Power of Auditor. 93. (1) The municipal accounts as containedin the financial statement, including theaccounts of special funds, if any, andthe balance sheet shall be examined andaudited by an Auditor appointed by theState Government from the panel ofprofessional chartered accountantsprepared in that behalf by the StateGovernment.

(2) The Chief Municipal Officer shallsubmit such further accounts to theAuditor as may be required by him.

(3) The Auditor so appointed may –

(a) require, by a notice, in writing, theproduction before him, or before anyofficer subordinate to him, of anydocument which he considersnecessary for the proper conduct ofthe audit,

(b) require, by a notice, in writing, anyperson accountable for, or having the

Status paper on Accounting Reforms in Local Bodies in India...

14

custody or control of, any document,cash or article, to appear in personbefore him or before any officersubordinate to him,

(c) require any person so appearingbefore him, or before any officersubordinate to him, to make or signa declaration with respect to suchdocument, cash or article or toanswer any question or prepare andsubmit any statement, and

(d) cause physical verification of anystock of articles in course ofexamination of accounts.

(4) The Auditor, or the officer subordinateto him, may report any item of accountscontrary to the provisions of this Act tothe Empowered Standing Committee.

(5) The Empowered Standing Committeeshall consider the report of the Auditoras early as possible and shall, ifnecessary, take prompt action thereon,and shall also, if necessary, surchargethe amount of any illegal payment on theperson making or authorizing it, andcharge against any person responsibletherefor the amount of any deficiency orloss incurred by the negligence ormisconduct of such person or any amountwhich ought to have been, but is not,brought into account by such person, andshall, in every such case, certify theamount due from such person :Providedthat any person aggrieved by an order ofpayment of certified sums may appealto the State Government whose decisionon such appeal shall be final.

15

Status paper on Accounting Reforms in Local Bodies in India...

(6) Any person who wilfully neglects, orrefuses to comply with, the requisitionmade by an Auditor, or the officersubordinate to him, shall, on convictionby a court, be punishable with fine whichmay extend to* rupees in respect of eachitem included in the requisition.

Audit report. 94. (1) As soon as practicable after thecompletion of audit of the accounts ofthe Municipality, but not later than thethirtieth day of September each year, theAuditor shall prepare a report of theaccounts audited and examined and shallsend such report to the Chief MunicipalOfficer.

(2) The Auditor shall include in suchreport a statement showing –

(a) every payment which appears to theAuditor to be contrary to law,

(b) the account of any deficiency or loss,which appears to have been causedby gross negligence or misconductof any person,

(c) the account of any sum receivedwhich ought to have been, but hasnot been, brought into account by anyperson, and

(d) any other material impropriety orirregularity in the accounts.

Placing of audited 95. (1) The Chief Municipal Officer shall placeaccounts before the audited financial statement, theMunicipality. balance sheet and the report of the

Auditor and his comments thereon before

* Each State Government may specify an amount in this regard.

Status paper on Accounting Reforms in Local Bodies in India...

16

the Empowered Standing Committeewhich, after the examination thereof, shallplace them before the Municipality withits comments, if any.

(2) The Chief Municipal Officer shallremedy any defect that has been pointedout by the Auditor in his report.

Submission of 96. (1) The Chief Municipal Officer shall, afteraudited accounts. adoption of the financial statement and

the balance sheet and the report of theAuditor by the Municipality, forward thesame to the State Government togetherwith a report of the action taken thereonby the Municipality and shall also sendcopies thereof to the Auditor.

(2) If there is any difference of opinionbetween the Auditor and the Municipalityor if the Municipality does not remedythe defects or the irregularities mentionedin the report of the Auditor within areasonable period, the Auditor shall referthe matter to the State Governmentwhose decision thereon shall be final andbinding.

Power of State 97. If any order made by the StateGovernment to Government under this chapter is notenforce order complied with, it shall be lawful for theupon audit report. State Government to take such steps as

it thinks fit to secure the compliance ofthe order and to direct that all expensestherefor shall be defrayed from theMunicipal Fund.

Special audit. 98. In addition to the audit of annual accounts,the State Government or the Municipality

17

Status paper on Accounting Reforms in Local Bodies in India...

may, if it thinks fit, appoint an Auditor toconduct special audit pertaining to aspecified item or series of items requiringthorough examination, and the procedurerelating to audit shall apply mutatismutandis to such special audit.

Internal audit. 99. The State Government or the Municipalitymay provide for internal audit of the dayto day accounts of the Municipality in themanner prescribed.

Municipal Accounts 100. (1) The Municipality shall, at its firstCommittee. meeting in each year or as soon as may

be at any meeting subsequent thereto,constitute a Municipal AccountsCommittee.

(2) The Municipal Accounts Committeeshall consist of -

(a) such number of members, not beingless than ..*.. and not more than ..*..,as the Municipality may determine,to be elected by the Councillors, notbeing the members of theEmpowered Standing Committee,from amongst themselves, and

(b) such number of persons, not beingCouncillors, or officers or otheremployees of the Municipality andnot exceeding two in number, havingknowledge and experience in financialmatters, as may be nominated bythe Municipality.

* Each State Government may specify the numbers of members havingregard to the members of Councillors.

Status paper on Accounting Reforms in Local Bodies in India...

18

(3) The members of the MunicipalAccounts Committee shall elect fromamongst themselves one member to beits Chairperson.

(4) Subject to the other provisions of thisAct, the members of the MunicipalAccounts Committee shall hold office untila new Municipal Accounts Committee isconstituted.

(5) The manner of submission ofresignation by the Chairperson or anyother member, and the manner of fillingup of a casual vacancy in the office of amember, of the Municipal AccountsCommittee shall be such as may beprescribed.

(6) Subject to the provisions of this Actand the rules and the regulations madethereunder, it shall be the duty of theMunicipal Accounts Committee -

(a) to examine the accounts of theMunicipality showing the appropriationof sums granted by the Municipalityfor its expenditure and the annualfinancial accounts of the Municipality,

(b) to examine and scrutinize the reporton the accounts of the Municipalityby the Auditor appointed undersection 92 and to satisfy itself thatthe moneys shown in the accountsas having been disbursed wereavailable for, and applicable to, theservices or purposes to which theywere applied or charged and that the

19

Status paper on Accounting Reforms in Local Bodies in India...

expenditure was incurred inaccordance with the authoritygoverning such expenditure,

(c) to submit report to the Municipalityevery year and from time to time onsuch examination and scrutiny,

(d) to consider the report of the Auditorappointed under section 98 in caseswhere the State Government or theMunicipality requires him to conducta special audit of any receipt orexpenditure of the Municipality or toexamine the accounts of stores andstocks of the Municipality or to checkthe inventory of the properties of theMunicipality including its landholdings and buildings, and

(e) to discharge such other functions asmay be prescribed.

(7) The Municipal Accounts Committeemay call for any book or document if, inits opinion, such book or document isnecessary for its work and may send forsuch officers of the Municipality as it mayconsider necessary for explaining anymatter in connection with its work.

(8) The manner of transaction of businessof the Municipal Accounts Committeeshall be such as may be determined byregulations :

Provided that the persons nominatedunder clause (b) of sub-section (2)shall not have the right to vote at themeeting of the Municipal AccountsCommittee.

Sta

tus

pape

r on

Acc

ount

ing

Ref

orm

s in

Loc

al B

odie

s in

Ind

ia...

20

20

Appendix – II

Committee on Accounting Standards for Local Bodies

The status of the various projects as on October 31, 2009:

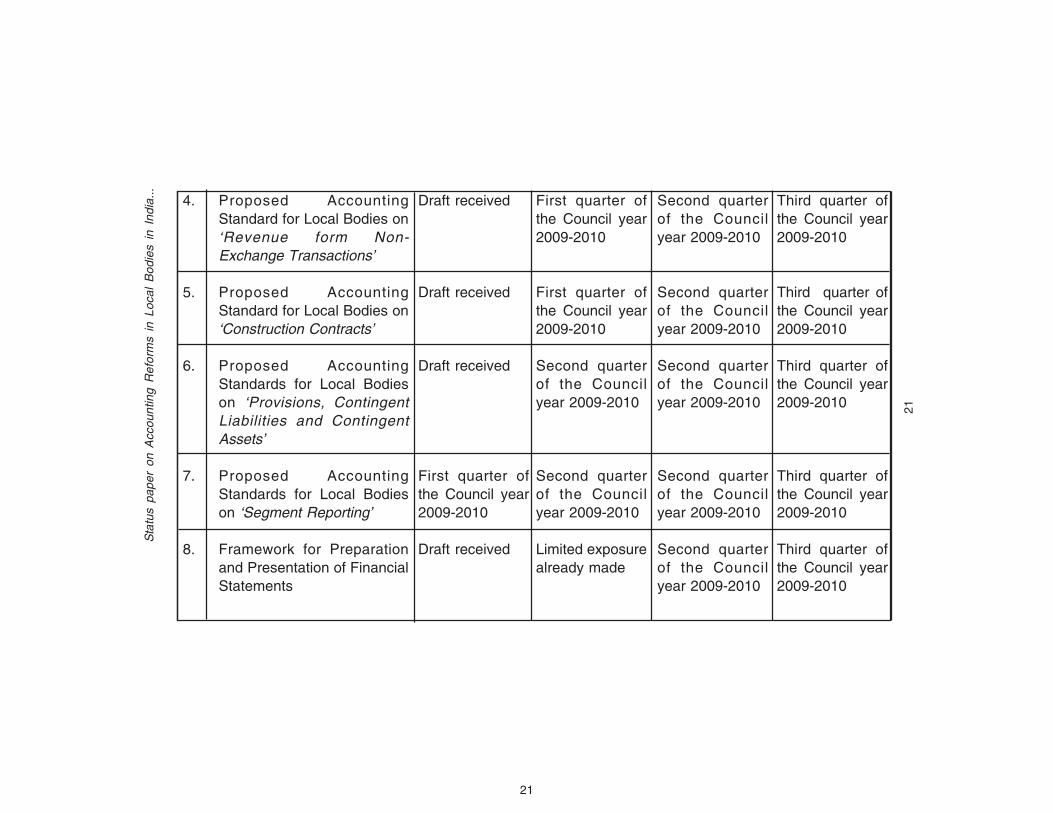

S. ProjectNo.

1. Proposed AccountingStandard for Local Bodies(ASLB) 1, ‘Presentation ofFinancial Statements’

2. Proposed AccountingStandard for Local Bodies(ASLB) 5, ‘Property, Plantand Equipment’

3. Proposed AccountingStandard for Local Bodies‘(ASLB) 6, Events After theReporting Date’

PreliminaryDraft by

Draft received

Draft received

Draft received

LimitedExposureDraft by

First quarter ofthe Council year2009-2010

Limited exposurealready made

Limited exposurealready made

PublicExposureDraft by

Second quarterof the Councilyear 2009-2010

Public Exposurealready made

Public Exposurealready made

CouncilApproval by

Third quarter ofthe Council year2009-2010

Third quarter ofthe Council year2009-2010

Third quarter ofthe Council year2009-2010

21

Sta

tus

pape

r on

Acc

ount

ing

Ref

orm

s in

Loc

al B

odie

s in

Ind

ia...

21

4. Proposed AccountingStandard for Local Bodies on‘Revenue form Non-Exchange Transactions’

5. Proposed AccountingStandard for Local Bodies on‘Construction Contracts’

6. Proposed AccountingStandards for Local Bodieson ‘Provisions, ContingentLiabilities and ContingentAssets’

7. Proposed AccountingStandards for Local Bodieson ‘Segment Reporting’

8. Framework for Preparationand Presentation of FinancialStatements

Draft received

Draft received

Draft received

First quarter ofthe Council year2009-2010

Draft received

First quarter ofthe Council year2009-2010

First quarter ofthe Council year2009-2010

Second quarterof the Councilyear 2009-2010

Second quarterof the Councilyear 2009-2010

Limited exposurealready made

Second quarterof the Councilyear 2009-2010

Second quarterof the Councilyear 2009-2010

Second quarterof the Councilyear 2009-2010

Second quarterof the Councilyear 2009-2010

Second quarterof the Councilyear 2009-2010

Third quarter ofthe Council year2009-2010

Third quarter ofthe Council year2009-2010

Third quarter ofthe Council year2009-2010

Third quarter ofthe Council year2009-2010

Third quarter ofthe Council year2009-2010

Sta

tus

pape

r on

Acc

ount

ing

Ref

orm

s in

Loc

al B

odie

s in

Ind

ia...

22

22

9. Proposed AccountingStandards for Local Bodies on‘Cash Flow Statement’

10. Proposed AccountingStandards for Local Bodies on‘Accounting Policies, Changesin Accounting Estimates andErrors’

11. Translation of the Booklet on‘Accrual Accounting for LocalBodies: ElectedRepresentatives &Stakeholders’ into other fourregional languages

12. Awareness Workshops on‘Accrual Accounting in LocalBodies’

13. Implementation Guidance /FAQs on AccountingStandards for Local Bodies

Second quarterof the Councilyear 2010-2011

Second quarterof the Councilyear 2010-2011

First quarter ofthe Council year2010-2011

First quarter ofthe Council year2010-2011

Third quarter ofthe Council year2009-2010

Third quarter ofthe Council year2009-2010

Second quarterof the Councilyear 2009-2010

Second quarterof the Councilyear 2009-2010

The Booklet is likely to be published in the First & Second Quarter of theCouncil year 2009-2010.The Hindi version of the booklet has beenpublished recently and Kannada, Tamil & Punjabi versions are underprocess.

One Awareness Workshop each in the Eastern, Southern and Centralregions.

This Implementation Guidance / FAQs on Accounting Standards for LocalBodies is to be developed in the Council year 2010-2011.

23

Status paper on Accounting Reforms in Local Bodies in India...

Appendix – III

Status of JNNURM Reforms relating toshifting to Accrual Based Double Entry

Accounting and Approved Cost of UrbanInfrastructure Projects

(Source www.jnnurm.nic.in)

S. Name of City State Status of Shifting Approved to Accrual Based Cost of

No. Accounting System Urban Infra-structure

Target Status ProjectsDate as on (In Lakhs)

30-08-09

01 Hydrabad AP 2008-2009 Achieved 173,942.51

02 Vijayawada AP 2007-2008 Achieved 47,712.00

03 Vishakhapatnam AP 2007-2008 Achieved 115,923.00

04 Itanagar ArunachalPradesh 2008-2009

05 Guwahati Assam 2008-2009 3,516.71

06 Patna Bihar 2007-2008 3,695.40

07 Bodhgaya Bihar 2009-2010

08 Chandigarh ChandigarhUT 2008-2009 5,698.60

09 Raipur Chattsgarh 2007-2008 30,364.00

10 Ahamedabad Gujrat 2007-2008 Achieved 129,156.52

11 Rajkot Gujrat 2007-2008 Achieved 27,971.00

12 Surat Gujrat 2007-2008 Achieved 60,329.37

13 Vadodara Gujrat 2007-2008 32,313.03

Status paper on Accounting Reforms in Local Bodies in India...

24

14 Fridabad Haryana 2009-2010 21,097.70

15 Delhi Delhi

16 Shimla HP 2007-2008 Achieved 2,613.06

17 Srinagar J&K 2008-2009 28,129.00

18 Jammu J&K 2008-2009 12,923.00

19 Bangalore Karnatka 2007-2008 Achieved 153,695.28

20 Mysore Karnatka 2007-2008 Achieved 27,979.74

21 Chochin Kerala 2007-2008 Achieved 37,748.00

22 Thiruvanthapuram Kerala 2007-2008 Achieved 30,257.00

23 Bhopal MP 2008-2009 Achieved 30,956.00

24 Indore MP Achieved 57,285.99

25 Jabalpur MP 2007-2008 15,602.00

26 Greater Mumbai Maharashtra 2007-2008 Achieved 353,753.75

27 Nagpur Maharashtra 2005-2006 Achieved 81,144.49

28 Nanded Maharashtra 2008-2009 68,704.45

29 Nashik Maharashtra 2008-2009 56,928.23

30 Pune Maharashtra 2007-2008 192,355.18

31 Bhubaneshwar Orrisa 2006-2007 Achieved 50,492.66

32 Puri Orrisa 2007-2008

33 Amritsar Punjab 2007-2008 32,883.00

34 Agartala Tripura 2008-2009

35 Dehradun Uttrakhand 2008-2009 7,002.70

36 Nainital Uttrakhand 2009-2010 547.00

37 Imphal Manipur 2008-2009 2,580.71

38 Jaipur Rajasthan Achieved 42,980.37

39 Chennai Tamilnadu 2005-2006 Achieved 105,468.02

40 Coimbatore Tamilnadu Achieved 58,738.18

41 Mudurai Tamilnadu Achieved 63,710.17

42 Agra UP 2008-2009 5,245.99

25

Status paper on Accounting Reforms in Local Bodies in India...

43 Kanpur UP 2008-2009 51,806.90

44 Allahbad UP 2007-2008 Achieved 8,969.00

45 Varanasi UP 2008-2009 15,969.73

46 Mathura UP 2007-2008 991.60

47 Meeerut UP 2007-2008 2,259.40

48 Kolkotta WB 2006-2007 Achieved 118,539.36

49 Asansol WB 2008-2009 Achieved 21,298.23

50 Aizwal Mizoram 1,681.80

51 Ajmer-Pushker Rajasthan 35,515.00

52 Dhanbad Jharkhand 2009-10

53 Gangtok Sikkim 2,392.01

54 Haridwar UP

55 Jamshedpur Jharkhand

56 Kohima Nagaland 2,525.60

57 Lucknow UP 2008-2009 66,776.37

58 Ludhiana Punjab

59 Panaji Goa 2009-2010

60 Puducherry Pondichery 2009-2010 20,340.00

61 Ranchi Jharkhand 2009-2010

62 Shillong Meghalya

63 Ujjan MP Achieved

TOTAL APPROVED COST 25,20,508.81

Status paper on Accounting Reforms in Local Bodies in India...

26

Appendix – IV

Chart of Accounts for PRIs: Present Status

PART IPANCHAYAT FUND

Revenue Section

RECEIPTS

Tax Receipts

MAJOR HEAD MINOR HEAD OBJECT HEAD

0028 Taxes on 101 Profession TaxProfessions, 102 Trade TaxTrades,Callings andEmployment

0029 Land Revenue 101 Land Revenue102 Land Tax103 Taxes on Plantations

0030 Duty on transfer 101 Duty on transfer byof immovable saleproperty 102 Duty on transfer by gift

103 Duty on transfer bymortgage

104 Duty on transfer bylease

0035 Taxes on 101 Taxes on ResidentialBuildings/ Buildings/PropertyProperty 102 Taxes on Non-

residential Buildings/Property

27

Status paper on Accounting Reforms in Local Bodies in India...

MAJOR HEAD MINOR HEAD OBJECT HEAD

* In states where there is no public works department at the PRI level, thesereceipts can be booked under 0515 Ponchayat Raj.

0041 Taxes on 101 Taxes on bi-cycles,Vehicles carts and other

vehicles

0042 Taxes on Goodsand Passengers 101 Tolls on Roads

102 Taxes on entry ofgoods into local area

103 Taxes on Passengers/Pilgrims

0045 Taxes and 101 Entertainment TaxDuties on 102 Advertisement TaxCommodities 103 Receipts under otherand Services Acts

104 Forest DevelopmentTax

Non-Tax ReceiptsMAJOR HEAD MINOR HEAD OBJECT HEAD

0049 Interest 101 Interest realised onReceipts investment of cash

balances102 Interest on bank

accounts103 Interest on loans and

advances 0059 Public Works* 101 Rent from non-

residential buildings102 Premium realised

from non-residentialbuildings

103 Licence fees fromresidential buildings

0071 Contributions 101 Leave Salary andand Recoveries PensionSubscriptiontowards Pension and Contributions

Status paper on Accounting Reforms in Local Bodies in India...

28

MAJOR HEAD MINOR HEAD OBJECT HEAD

and Other Re-tirementBenefit

0202 Education, 101 Pre-primary, Primary 41 FeesSports, Arts and Secondaryand Culture Education 42 Fines

102 Sports and YouthServices

103 Public Libraries

0210 Medical andPublic Health 101 Receipts from Patients 51 Accommod-

ation52 Supply of

Medicines53 Cost of Tests54 Supply of

Blood102 Sale of Serum/Vaccine103 Fees and Fines

0211 Family Welfare 101 Sale of Contraceptives

0215 Water Supply 101 Water Supply 41 Feesand 42 FinesSanitation 43 Service fees

102 Sewerage andSanitation 41 Fees

42 Fines43 Service fees

0216 Rural Housing 112 Schemes XYZ

0401 Crop 101 Sale of SeedsHusbandry 102 Receipts from

Agricultural Farm103 Sale of Manures

and Fertilizers104 Receipts from

Commercial Crops

29

Status paper on Accounting Reforms in Local Bodies in India...

0403 Animal 101 Receipts from CattleHusbandry & Buffalo Development 45 Sale of Milk

102 Receipts from Poultry 46 Sale ofDevelopment Animals

103 Receipts from PiggeryDevelopment

104 Receipts from Fodder& Feed Development

0405 Fisheries 101 Licence fees, Finesetc

102 Sale of Fish, Fishseeds etc

103 Service fees

0406 Forestry and 101 Sale of timber andWild Life other forest produce

102 Receipts from forestplantations

103 Receipts fromfirewood plantations

104 Sale of grazing rights

0515 Panchayat Raj 101 Licence fees102 Fees for use of quarry103 Rent for use of land

vested in ZillaParishad/PanchayatSamiti/VillagePanchayat

104 Receipts fromCommunityDevelopment Projects

105 Other Rates andFees*

106 Other Registrationcharges

107 Other Service Fees108 Other Fines

MAJOR HEAD MINOR HEAD OBJECT HEAD

* When rates are in the nature of tax, this is to be accounted for under theappropriate tax receipts heads.

Status paper on Accounting Reforms in Local Bodies in India...

30

MAJOR HEAD MINOR HEAD OBJECT HEAD

MAJOR HEAD MINOR HEAD OBJECT HEAD

0702 Minor Irrigation 101 Lift Irrigationcharges

102 Receipts fromtube-wells

0801 Power 101 Rural Electrification

Grants-in-Aid & Contribution

1601 Grants-in-aid/ 101 Scheme XYZAssistance 102 Scheme ABCfrom CentralGovernment

1602 Grants-in-aid/ 101 Scheme MNOAssistance 102 Scheme JKLfrom StateGovernment

1604 Compensation 101 Miscellaneous 61 Share of Co-and Compensation mpensationAssignments and Assignments andfrom State AssignmentGovernemnt from Stateand other PRIs Government

62 Share of Co-mpensationandAssignmentsfrom ZillaParishad

63 Share of Co-mpensationandAssignmentfromPanchayatSamiti

1608 Contributions/Donations fromprivate agencies

31

Status paper on Accounting Reforms in Local Bodies in India...

EXPENDITURE

MAJOR HEAD MINOR HEAD OBJECT HEAD

2049 Interest 102 Interest on loan fromPayment Zilla Parishad

103 Interest on loans fromPanchayat Samiti

104 Interest on loansfrom other organization/Financial Institution

105 Interest on loans fromCentralGovernment

55 Details of theloan

56 Details of theloan

106 Interest on loans fromState Government 55 Details of the

loan56 Details of the

loan107 Interest on Savings

Funds

2059 Public Worksð 102 Office Buildings 65 Work chargedestablishmentexpenditure

66 Othermaintenanceexpenditure

103 Other Buildings

2071 Pension and 102 Pensionary chargesother retirement 103 Contribution tobenefits Pension and Gratuity

104 Contribution toProvident Fund

2203 Technical 102 Technical Schools,Education Craft Centres etc.

103 Scholarship

ð This head may not be operated in states where constructions andmaintenance expenditure is booked under the respective functional heads.

Status paper on Accounting Reforms in Local Bodies in India...

32

2204 Sports and 102 Physical Education 71 Assistance toYouth Services Primary

Schools72 Assistance to

SecondarySchools

73 Assistance toNon-Govt.Schools

103 Youth Camps104 Youth Hostels105 N.C.C.106 Sports and Games

2205 Art and Culture 102 Fine arts education103 Promotion of Arts

and Culture104 Public Libraries

2206 Pre-PrimaryEducation 102 Mid-day meal

103 Scholarshipsand Incentives

104 Extra-curricularActivities

105 Teachers’ training106 Supply of books

and study materialsto students

107 Other assistanceto students

120 Assistance toVoluntaryOrganisations

2207 Primary 102 Mid-day mealEducation 103 Scholarships and

Incentives104 Extra-curricular

Activities

MAJOR HEAD MINOR HEAD OBJECT HEAD

33

Status paper on Accounting Reforms in Local Bodies in India...

105 Teachers’ training106 Supply of books

and study materialsto students

107 Other assistance tostudents

120 Assistance toVoluntaryOrganisations

2208 Secondary 103 Scholarships andEducation Incentives

104 Extra-curricular Activities105 Teachers’ training106 Supply of books and

study materials tostudents

107 Other assistance tostudents

120 Assistance toVoluntaryOrganisations

2209 Adult Education 102 Rural FunctionalLiteracy Programme

112 Scheme XYZ

2210 Medical and 102 District HospitalPublic 103 Community Health

Centre104 Primary Health Centre105 Health Sub Centre106 Medical Relief Camps112 National Anti-Malarial

Programme113 Trachoma & Blindness

Control Programme114 National Aids Control

Programme115 Scheme XYZ

MAJOR HEAD MINOR HEAD OBJECT HEAD

Status paper on Accounting Reforms in Local Bodies in India...

34

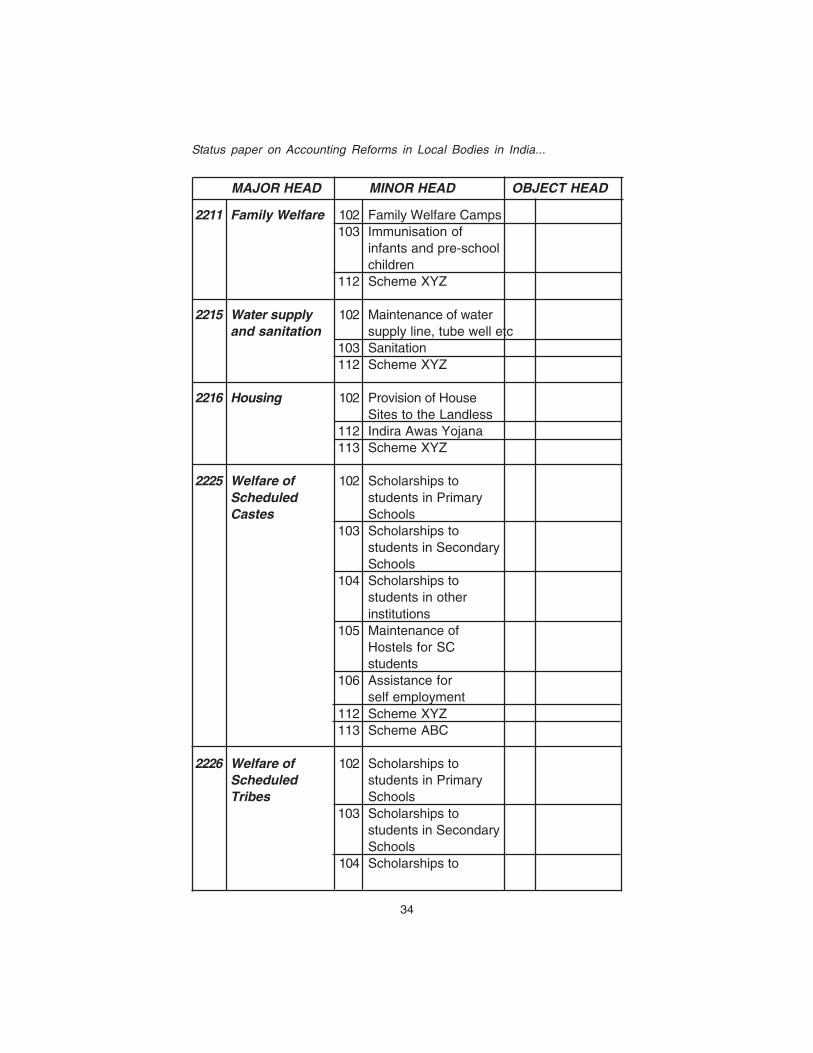

MAJOR HEAD MINOR HEAD OBJECT HEAD

2211 Family Welfare 102 Family Welfare Camps103 Immunisation of

infants and pre-schoolchildren

112 Scheme XYZ

2215 Water supply 102 Maintenance of waterand sanitation supply line, tube well etc

103 Sanitation112 Scheme XYZ

2216 Housing 102 Provision of HouseSites to the Landless

112 Indira Awas Yojana113 Scheme XYZ

2225 Welfare of 102 Scholarships toScheduled students in PrimaryCastes Schools

103 Scholarships tostudents in SecondarySchools

104 Scholarships tostudents in otherinstitutions

105 Maintenance ofHostels for SCstudents

106 Assistance forself employment

112 Scheme XYZ113 Scheme ABC

2226 Welfare of 102 Scholarships toScheduled students in PrimaryTribes Schools

103 Scholarships tostudents in SecondarySchools

104 Scholarships to

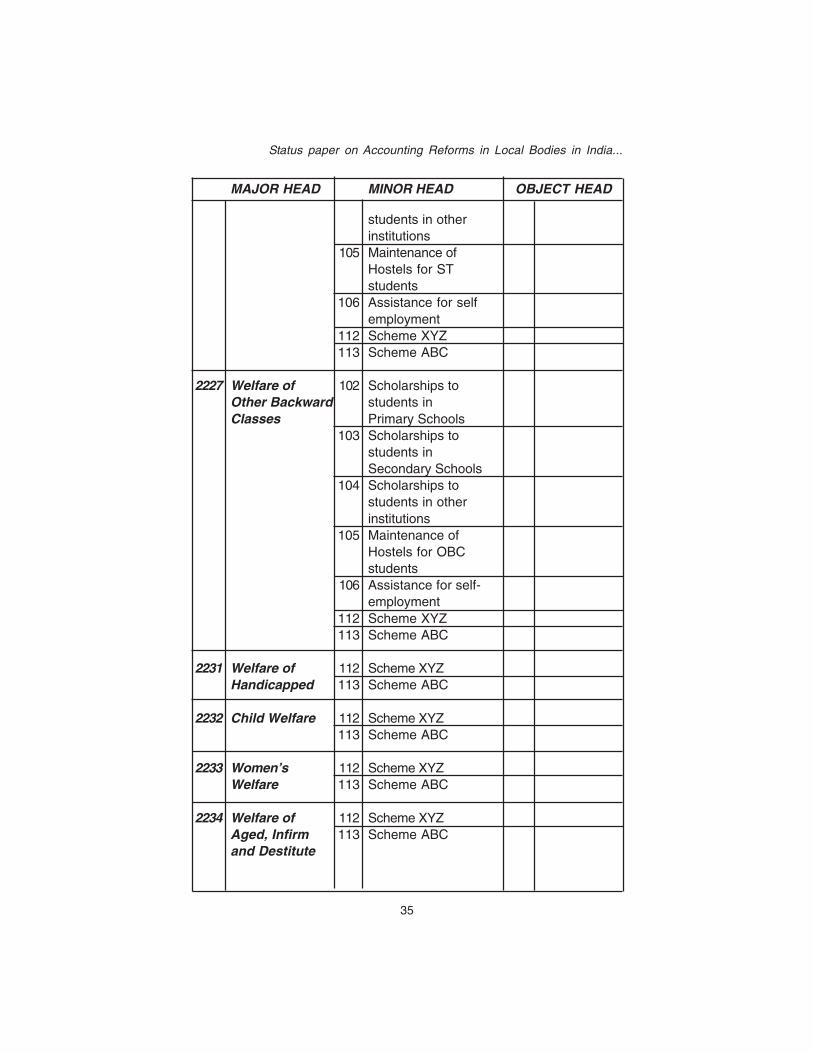

35

Status paper on Accounting Reforms in Local Bodies in India...

students in otherinstitutions

105 Maintenance ofHostels for STstudents

106 Assistance for selfemployment

112 Scheme XYZ113 Scheme ABC

2227 Welfare of 102 Scholarships toOther Backward students inClasses Primary Schools

103 Scholarships tostudents inSecondary Schools

104 Scholarships tostudents in otherinstitutions

105 Maintenance ofHostels for OBCstudents

106 Assistance for self-employment

112 Scheme XYZ113 Scheme ABC

2231 Welfare of 112 Scheme XYZHandicapped 113 Scheme ABC

2232 Child Welfare 112 Scheme XYZ113 Scheme ABC

2233 Women’s 112 Scheme XYZWelfare 113 Scheme ABC

2234 Welfare of 112 Scheme XYZAged, Infirm 113 Scheme ABCand Destitute

MAJOR HEAD MINOR HEAD OBJECT HEAD

Status paper on Accounting Reforms in Local Bodies in India...

36

2235 Social SecurityPensions 112 Scheme XYZ

113 Scheme ABC

2236 Nutrition 102 Distribution ofnutritious food tochildren

103 Distribution of nutritiousfood to expectant /lactating mothers

2401 Crop 102 Extension andHusbandry Farmers’ Training

103 Crop insurance104 Scheme for Small/

Marginal farmers andagricultural labourers

105 Horticulture andvegetable crops

106 Assistance tofarming cooperation

2402 Soil and Water 102 Reclamation ofConservation Ravines

103 Water conservation

2403 Animal 102 Prevention and ControlHusbandry of animal diseases

103 Cattle and BuffaloDevelopment

104 Other DomesticAnimals

105 Poultry Development106 Fodder and feed

development107 Insurance of livestock

and poultry

2405 Fisheries 112 Scheme XYZ113 Scheme ABC

MAJOR HEAD MINOR HEAD OBJECT HEAD

37

Status paper on Accounting Reforms in Local Bodies in India...

MAJOR HEAD MINOR HEAD OBJECT HEAD

2406 Forestry and 102 Rural ForestryWild Life

2408 Food, Storage 102 Public Distributionand Ware Systemhousing 103 Fair Price Shops

104 Co-operative Societies

2501 Special 112 Swarnajayanti GramProgrammes Samridhi Yojanafor Rural 113 TRYSEMDevelopment 114 Drought prone

Areas DevelopmentProgramme

115 Desert DevelopmentProgramme

116 Self-employmentProgramme

117 Scheme XYZ

2505 Rural 112 NREG Scheme XX Water con-Employment servation,

droughtproofing, floodcontrol works

YY AfforestationZZ Minor

Irrigation❒

2515 Panchayat Raj 102 Allowances andhonorarium ofChairman/ViceChairman/Councillors/Members

103 Panchayat 17 ProfessionalEstablishment Services

(Fees forpreparation ofAnnualAccounts)

❒ This is only on illustrative list of works. State may operate as per localrequirements.

Status paper on Accounting Reforms in Local Bodies in India...

38

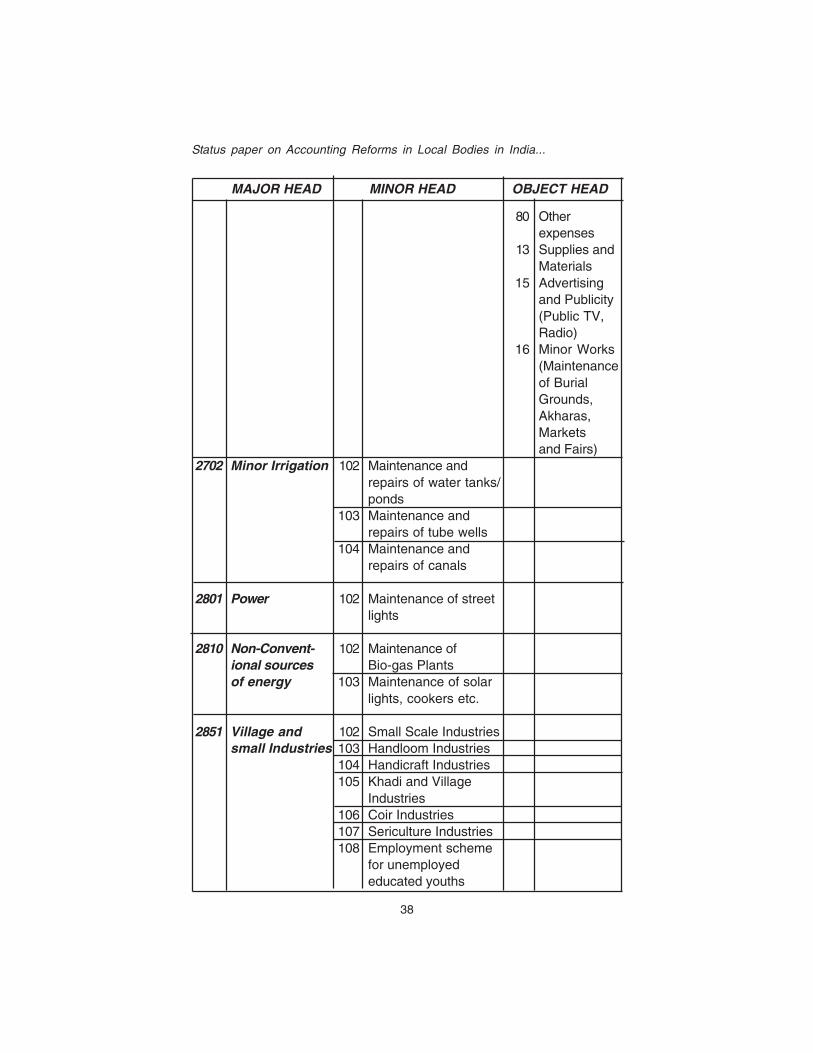

MAJOR HEAD MINOR HEAD OBJECT HEAD

80 Otherexpenses

13 Supplies andMaterials

15 Advertisingand Publicity(Public TV,Radio)

16 Minor Works(Maintenanceof BurialGrounds,Akharas,Marketsand Fairs)

2702 Minor Irrigation 102 Maintenance andrepairs of water tanks/ponds

103 Maintenance andrepairs of tube wells

104 Maintenance andrepairs of canals

2801 Power 102 Maintenance of streetlights

2810 Non-Convent- 102 Maintenance ofional sources Bio-gas Plantsof energy 103 Maintenance of solar

lights, cookers etc.

2851 Village and 102 Small Scale Industriessmall Industries 103 Handloom Industries

104 Handicraft Industries105 Khadi and Village

Industries106 Coir Industries107 Sericulture Industries108 Employment scheme

for unemployededucated youths

39

Status paper on Accounting Reforms in Local Bodies in India...

MAJOR HEAD MINOR HEAD OBJECT HEAD

MAJOR HEAD MINOR HEAD OBJECT HEAD

109 Food ProcessingIndustries

3054 Roads and 102 Maintenance andBridges Repairs

Capital SectionRECEIPTS

4000 Capital Receipts

EXPENDITURE

4059 Capital Outlay 102 Construction ofon Public Office BuildingsWorksð 103 Construction of

Other Buildings104 Acquisition of Land

4202 Capital Outlay 102 Construction ofon Education, Primary Schools,Sports, Art and Pathshalas etcCulture 103 Construction of Youth

Hostels104 Construction of Sports

Stadium105 Construction of Block/

Village Library

4210 Capital Outlay 102 District Hospitalon Medical and 103 Community HealthPublic Health Centre

104 Primary Health Centre105 Health Sub Centre106 Medical Relief Camps112 National Anti-Malaria

Programme

MAJOR HEAD MINOR HEAD OBJECT HEAD

ð This head may not be operated in states where construction andmaintenance expenditure is booked under the respective functional heads.

Status paper on Accounting Reforms in Local Bodies in India...

40

MAJOR HEAD MINOR HEAD OBJECT HEAD

113 Trachoma & BlindnessControl Programme

114 National Aids ControlProgramme

115 Scheme XYZ

4211 Capital Outlay 102 Construction ofon Family Maternity andWelfare Child Welfare Centres

4215 Capital Outlay 102 Laying of wateron Water Supply supply schemeand Sanitation 103 Drilling of tube wells /

wells

4225 Capital Outlay 112 Scheme XYZon Welfare of 113 Scheme ABCScheduledCastes

4226 Capital Outlay 112 Scheme XYZon Schedule 113 Scheme ABCTribes

4227 Capital Outlay 112 Scheme XYZon Welfare of 113 Scheme ABCOther BackwardClasses

4231 Capital Outlay 102 Construction ofon Welfare of Training Centres forHandicapped Welfare of

Handicapped

4232 Capital Outlay 102 Construction ofon Child Anganwadi CentresWelfare and storage shed

4233 Capital Outlay 102 Construction ofon Women’s Training Centres forWelfare Welfare of Women

41

Status paper on Accounting Reforms in Local Bodies in India...

MAJOR HEAD MINOR HEAD OBJECT HEAD

4234 Capital Outlay 102 Construction ofon Welfare of Rehabilitation CentresAged, Infirm for Welfare of theand Destitute Aged, Infirm and

Destitute

4405 Capital Outlay 102 Construction of Fishon Fisheries Ponds

4406 Capital Outlay 102 Development ofon Forestry and plantations and wasteWild Life land development

103 Development ofGrazing Lands

104 Development ofFirewood Plantations

4408 Capital Outlay 102 Development ofon Food Rural GodownsStorage and 103 Construction ofWarehousing Rural Godowns

104 Development ofMandies, Warehouses

4515 Capital Outlay 102 Panchayat officeon Panchayat buildingsRaj

4702 Capital Outlay 102 Capital Outlay onon Minor CanalsIrrigation 103 Capital Outlay on

Tube Wells104 Capital Outlay on

Tanks105 Machinery and

Equipment

4801 Capital Outlay 102 Installation of Streeton Power LightsProjects

4810 Capital Outlay 102 Construction ofon Non- Bio-Gas Plants

Status paper on Accounting Reforms in Local Bodies in India...

42

MAJOR HEAD MINOR HEAD OBJECT HEAD

Conventional 103 Construction ofSources of Solar Energy ProjectsEnergy

5054 Capital Outlay 102 Construction of Villageon Roads and /District RoadsBridges 103 Acquisition of land for

construction of Roadsand Bridges

112 PMGSY

Borrowing Section❒❒❒❒❒

RECEIPTS

6003 Loans from 101 Loans from ZillaNon-Govern- Parishadment sources 102 Loans from Panchayat

Samiti103 Loans from other

organizations/Financial Institutions

6004 Loans from 101 Loans from Central 01 Details of theGovernment Govt loansources 02 Details of the

loan102 Loans from State Govt 01 Details of the

loan02 Details of the

loan

MAJOR HEAD MINOR HEAD OBJECT HEAD

❒This represents borrowings by PRls.

43

Status paper on Accounting Reforms in Local Bodies in India...

MAJOR HEAD MINOR HEAD OBJECT HEAD

✼ This represents lending by PRIs.

EXPENDITURE

6003 Loans from Non- 101 Repayment of LoansGovernment from Zilla Parishadsources 102 Repayment of Loans

from Panchayat Samiti103 Repayment of

Loans from otherorganizations/FinancialInstitutions

6004 Loans from 101 Repayment of Loans 01 Details of theGovernment from Central Govt loansources 02 Details of the

loan102 Repayment of Loans 01 Details of the

from State Govt loan02 Details of the

loan

Lending Section*

EXPENDITURE

6202 Loans for 101 Payment of loans forEducation, education purposeSports, Art andCulture

6401 Loans for Crop 101 Payment of loansHusbandry to cultivators

7610 Loans to 101 Payment of loans to 01 House Build-Panchayat employees ing AdvanceEmployees etc 02 Motor Convey-

ance Advance03 Bi-cycle

Advance

MAJOR HEAD MINOR HEAD OBJECT HEAD

Status paper on Accounting Reforms in Local Bodies in India...

44

MAJOR HEAD MINOR HEAD OBJECT HEAD

RECEIPTS

6202 Loans for 101 Payment of loansEducation, for education purposeSports, Artand Culture

6401 Loans for Crop 101 Payment of loansHusbandry to cultivators

7610 Loans to 101 Payment of loans 01 HousePanchayat to employees BuildingEmployees etc Advance

02 MotorConveyanceAdvance

03 Bi-cycleAdvance

45

Status paper on Accounting Reforms in Local Bodies in India...

MAJOR HEAD MINOR HEAD OBJECT HEAD

PART IIEXTRAORDINARY FUND

Savings Fund Section

RECEIPTS

8009 Provident Funds 101 General Providentand Small FundSavings 102 Panchayat Employees

Provident Fund

8011 Insurance and 101 Employees GroupPension Funds Insurance Scheme

102 Panchayat EmployeesPension Fund

EXPENDITURE

8009 Provident Funds 101 General Providentand Small FundSavings 102 Panchayat Employees

PF

8011 Insurance and 101 Employees GroupPension Funds Insurance Scheme

MAJOR HEAD MINOR HEAD OBJECT HEAD

Status paper on Accounting Reforms in Local Bodies in India...

46

MAJOR HEAD MINOR HEAD OBJECT HEAD

Deposit and Advance Section

RECEIPTS

8443 Deposits 101 PRI Deposits 01 SecurityDeposit

102 Public Works Deposits 01 Deposits byContractors

02 Deposits ofearnestmoney bysuccessfultenderers

8550 PRI Advances 101 Advances to PRIfunctionaries for worksand supplies

102 Advances toagencies for worksand supplies

EXPENDITURE

8443 Deposits 101 PRI Deposits 01 SecurityDeposit

102 Public Works Deposits 01 Deposits byContractors

02 Deposits ofearnestmoney bysuccessfultenderers

8550 PRI Advances 101 Advances to PRIfunctionaries for worksand supplies

102 Advances toagencies for worksand supplies

MAJOR HEAD MINOR HEAD OBJECT HEAD

47

Status paper on Accounting Reforms in Local Bodies in India...

Suspense and Remittance Section

RECEIPTS

MAJOR HEAD MINOR HEAD OBJECT HEAD

8650 Material 101 CementSuspense 102 BitumenAccount 103 Rods

104 Stone chips105 Pipes106 Bricks800 Other materials

8658 Other Suspense 101 Tax deducted atAccounts source suspense 01 Income Tax

02 Sales Tax03 Profession

Tax102 Housing Loan

Suspense103 Insurance Premium

Suspense120 Unclassified

transaction

8673 Cash Balance 102 Purchase of bond/Investment debentureAccount 103 Purchase of FDC

800 Other forms of cashbalance investment

8782 Cash 101 Remittances betweenRemittances Zilla Parishad andbetween PRIs Panchayat Samiti

102 Remittances betweenZilla Parishad andVillage Panchayat

103 Remittances betweenPanchayat Samiti &Village Panchayat

Status paper on Accounting Reforms in Local Bodies in India...

48

EXPENDITURE

MAJOR HEAD MINOR HEAD OBJECT HEAD

8650 Material 101 CementSuspense 102 BitumenAccount 103 Rods

104 Stone chips105 Pipes106 Bricks800 Other materials

8658 Other 101 Tax deducted at 01 Income TaxSuspense source suspense 02 Sales TaxAccounts 03 Profession

Tax102 Housing Loan

Suspense103 Insurance Premium

Suspense120 Unclassified

transaction

8673 Cash Balance 101 Purchase of bond/Investment debentureAccount 102 Purchase of FDC

800 Other forms of cashbalance investment

8782 Cash 101 Remittances betweenRemittances Zilla Parishad andbetween PRIs Panchayat Samiti

102 Remittances betweenZilla Parishad andVillage Panchayat

103 Remittances betweenPanchayat Samiti &Village Panchayat

49

Status paper on Accounting Reforms in Local Bodies in India...

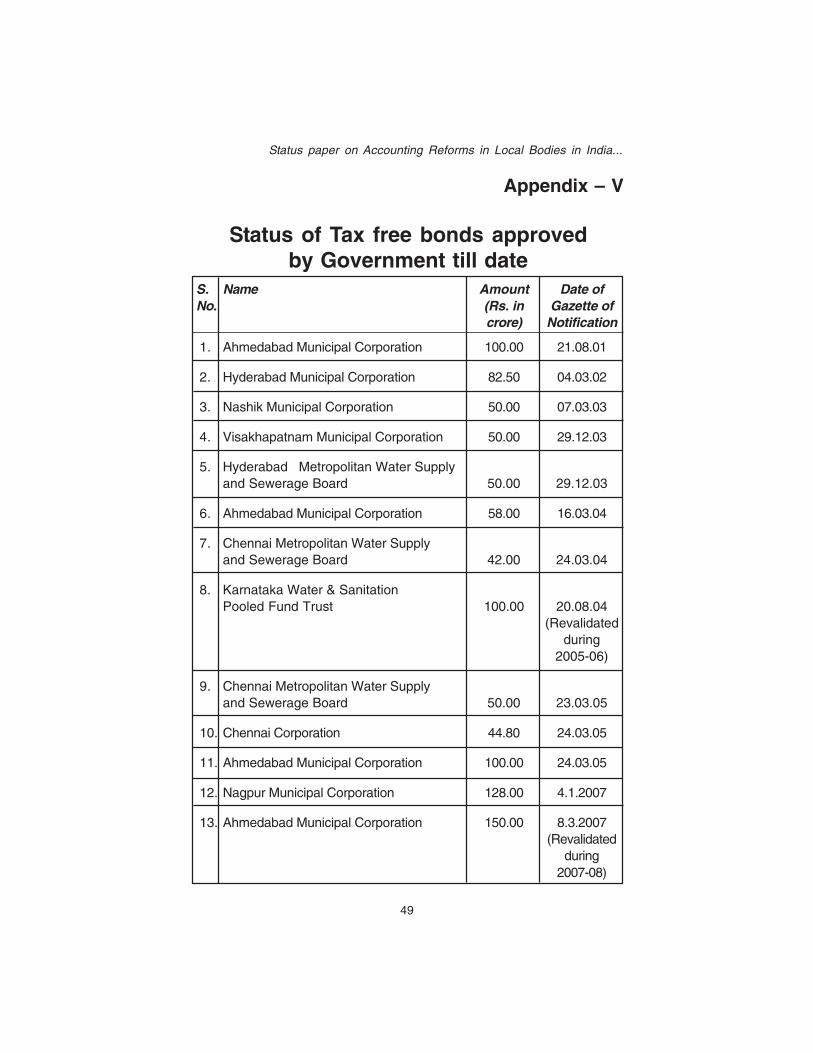

Appendix – V

Status of Tax free bonds approvedby Government till date

S. Name Amount Date ofNo. (Rs. in Gazette of

crore) Notification

1. Ahmedabad Municipal Corporation 100.00 21.08.01

2. Hyderabad Municipal Corporation 82.50 04.03.02

3. Nashik Municipal Corporation 50.00 07.03.03

4. Visakhapatnam Municipal Corporation 50.00 29.12.03

5. Hyderabad Metropolitan Water Supplyand Sewerage Board 50.00 29.12.03

6. Ahmedabad Municipal Corporation 58.00 16.03.04

7. Chennai Metropolitan Water Supplyand Sewerage Board 42.00 24.03.04

8. Karnataka Water & SanitationPooled Fund Trust 100.00 20.08.04

(Revalidatedduring

2005-06)

9. Chennai Metropolitan Water Supplyand Sewerage Board 50.00 23.03.05

10. Chennai Corporation 44.80 24.03.05

11. Ahmedabad Municipal Corporation 100.00 24.03.05

12. Nagpur Municipal Corporation 128.00 4.1.2007

13. Ahmedabad Municipal Corporation 150.00 8.3.2007(Revalidated

during2007-08)

![C L GOLCHHA & ASSOCIATES [ CHARTERED ACCOUNTANTS ] Firm Profile Presentation CHARTERED ACCOUNTANTS C L GOLCHHA & ASSOCIATES](https://img.pdfslide.net/doc/110x75/5697c0301a28abf838cdac32/c-l-golchha-associates-chartered-accountants-firm-profile-presentation.jpg)