Embed Size (px)

Citation preview

Angola’s Economy: Past, Present and Future

Ricardo Gazel, World BankSenior Economist and Acting Country Manager

Viking Club August 27, 2009

Angola’s Economy: Past, Present and Future

I. Recent Past: High Rates of Growth

II. Present: The Mother of all Crisis and the Impacts on Angola’s Economy

III. Future: Medium and Long Runs

I. Recent Past: High Rates of Growth

• 1.1 Economic Growth

• 1.2 Inflation

• 1.3 External Sector

• 1.4 Public Sector

• 1.5 Social Gains

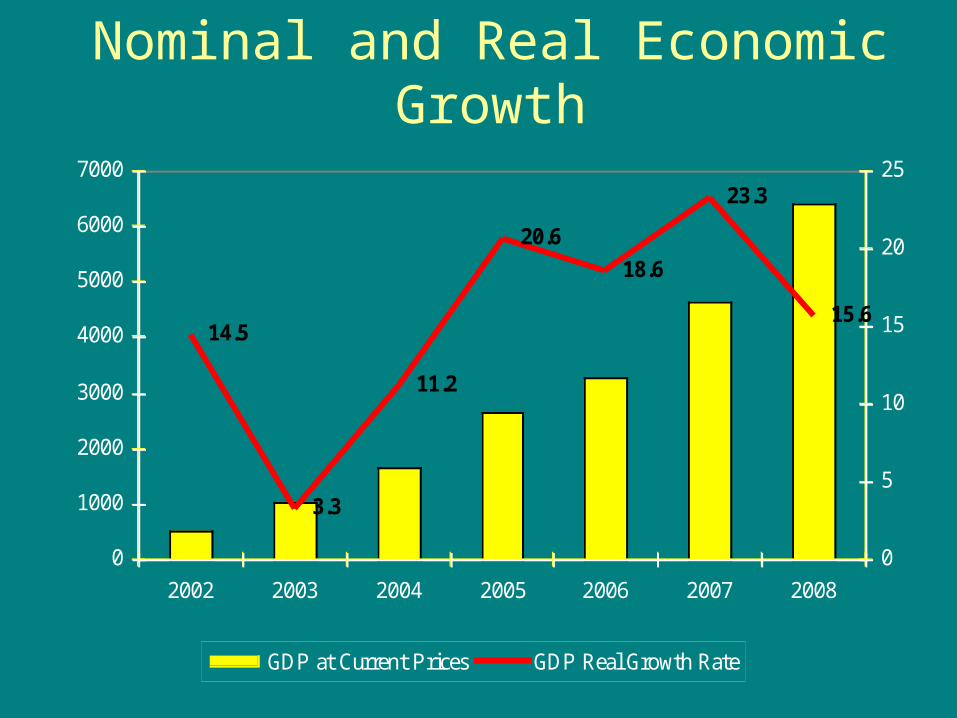

Nominal and Real Economic Growth

14.5

3.3

11.2

20.6

18.6

23.3

15.6

0

1000

2000

3000

4000

5000

6000

7000

2002 2003 2004 2005 2006 2007 2008

0

5

10

15

20

25

GDP at Current Prices GDP Real Growth Rate

I. Recent Past: High Rates of Growth

• 1.1 Economic Growth

• 1.2 Inflation

• 1.3 External Sector

• 1.4 Public Sector

• 1.5 Social Gains

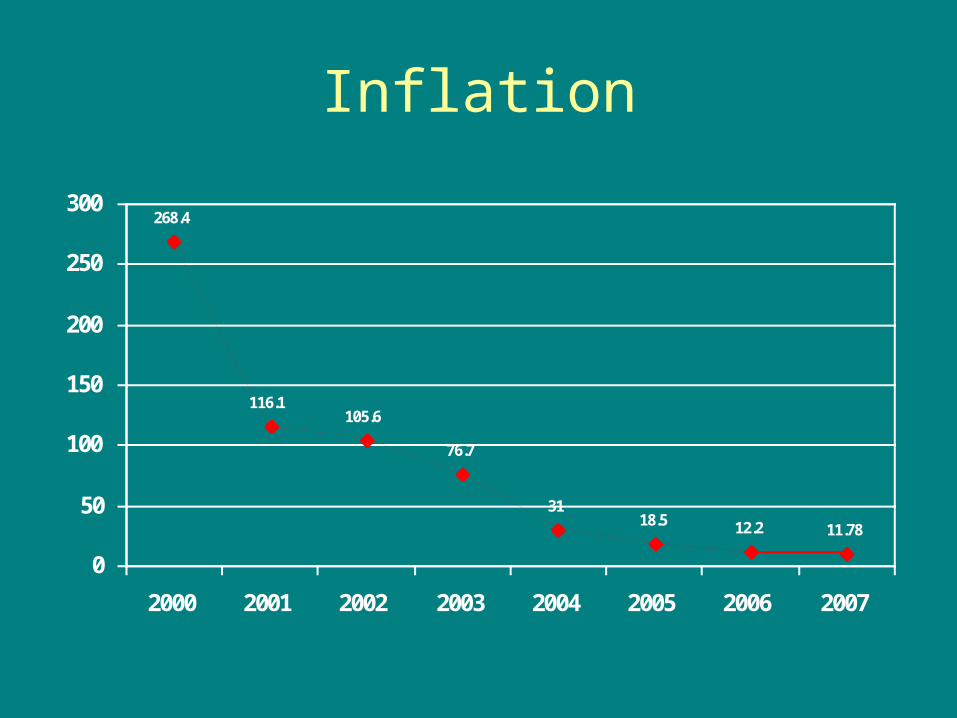

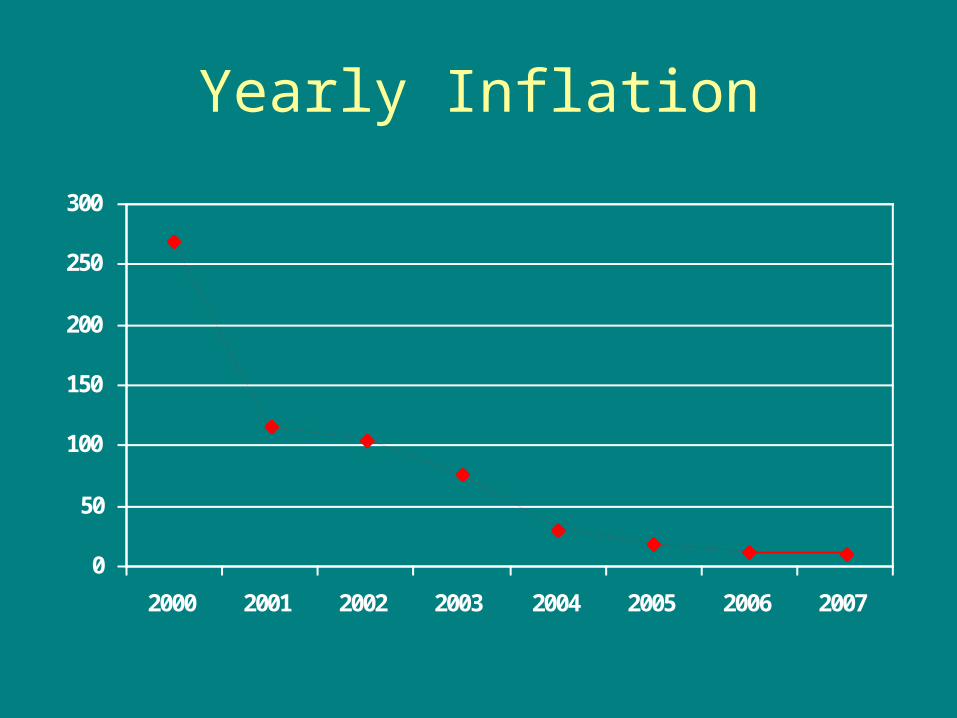

Inflation

268.4

116.1105.6

76.7

3118.5 12.2 11.78

0

50

100

150

200

250

300

2000 2001 2002 2003 2004 2005 2006 2007

I. Recent Past: High Rates of Growth

• 1.1 Economic Growth

• 1.2 Inflation

• 1.3 External Sector

• 1.4 Public Sector

• 1.5 Social Gains

Trade Balance – US$ billions

0

10

20

30

40

50

60

70

2002 2003 2004 2005 2006 2007 2008

Exports (FOB) Imports (FOB) Trade Balance

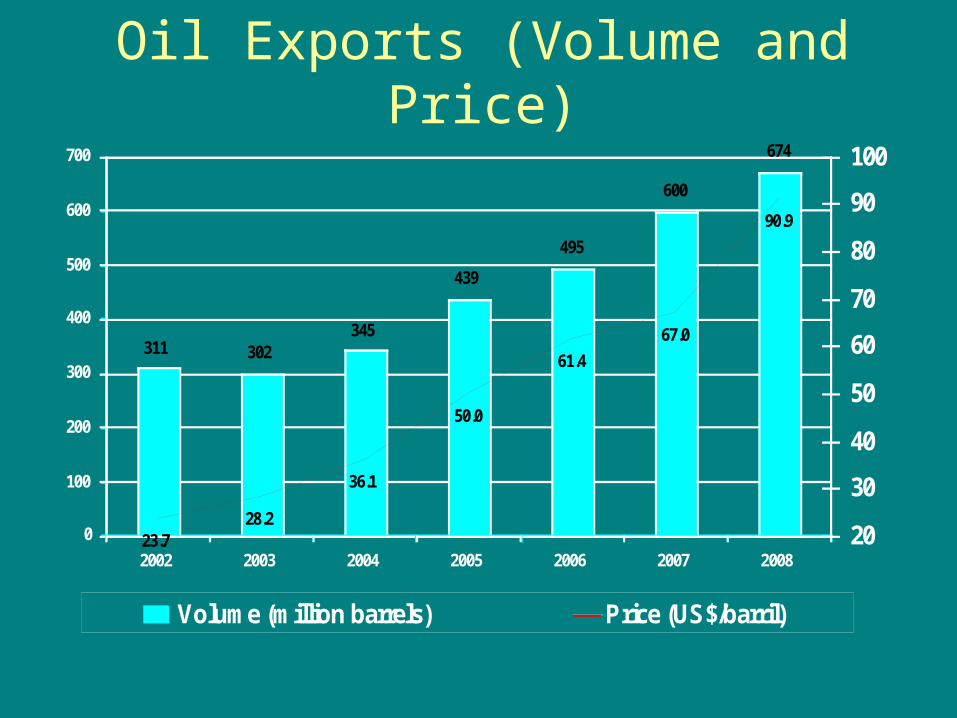

Oil Exports (Volume and Price)

311 302345

439

495

600

674

23.728.2

36.1

50.0

61.4

67.0

90.9

0

100

200

300

400

500

600

700

2002 2003 2004 2005 2006 2007 200820

30

40

50

60

70

80

90

100

Volume (million barrels) Price (US$/barril)

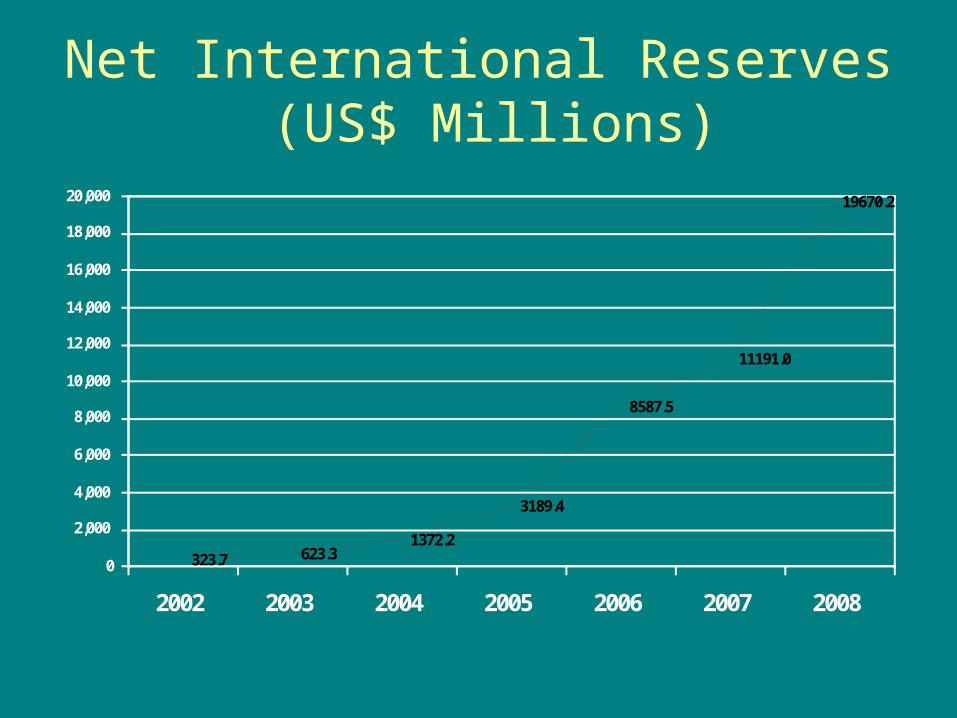

Net International Reserves (US$ Millions)

323.7 623.31372.2

3189.4

8587.5

11191.0

19670.2

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2002 2003 2004 2005 2006 2007 2008

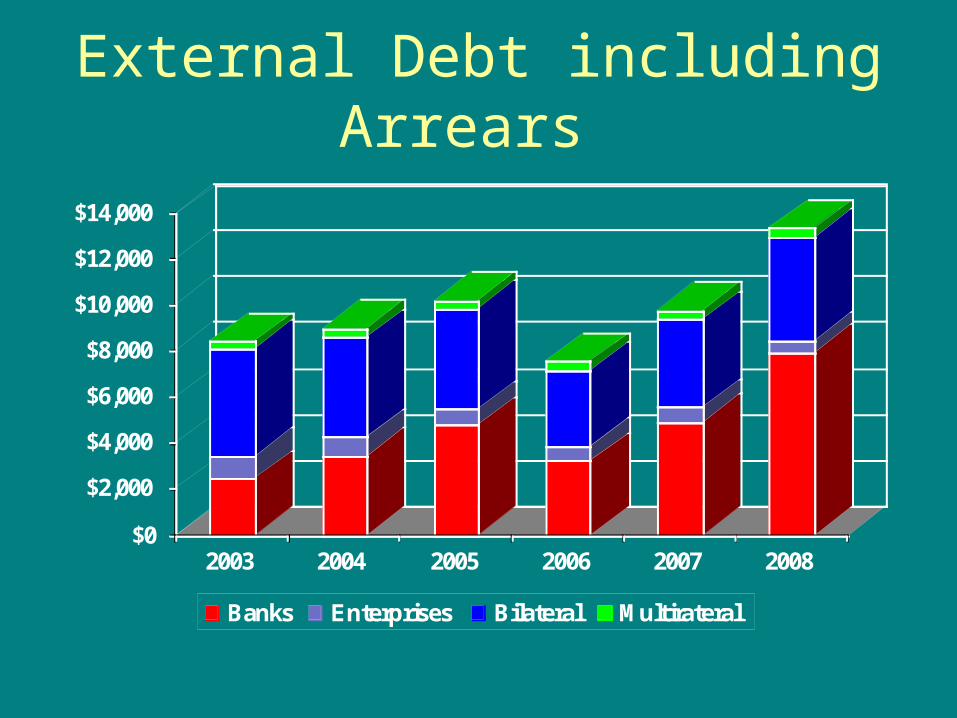

External Debt including Arrears

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2003 2004 2005 2006 2007 2008

Banks Enterprises Bilateral Multirateral

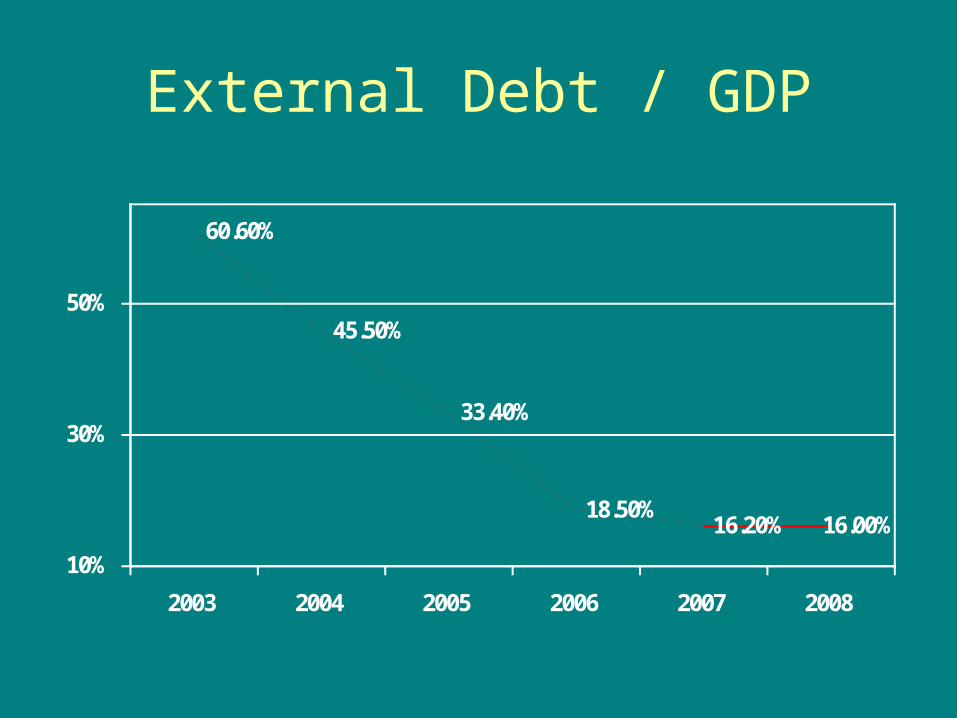

External Debt / GDP

60.60%

45.50%

33.40%

18.50%16.20% 16.00%

10%

30%

50%

2003 2004 2005 2006 2007 2008

I. Recent Past: High Rates of Growth

• 1.1 Economic Growth

• 1.2 Inflation

• 1.3 External Sector

• 1.4 Public Sector

• 1.5 Social Gains

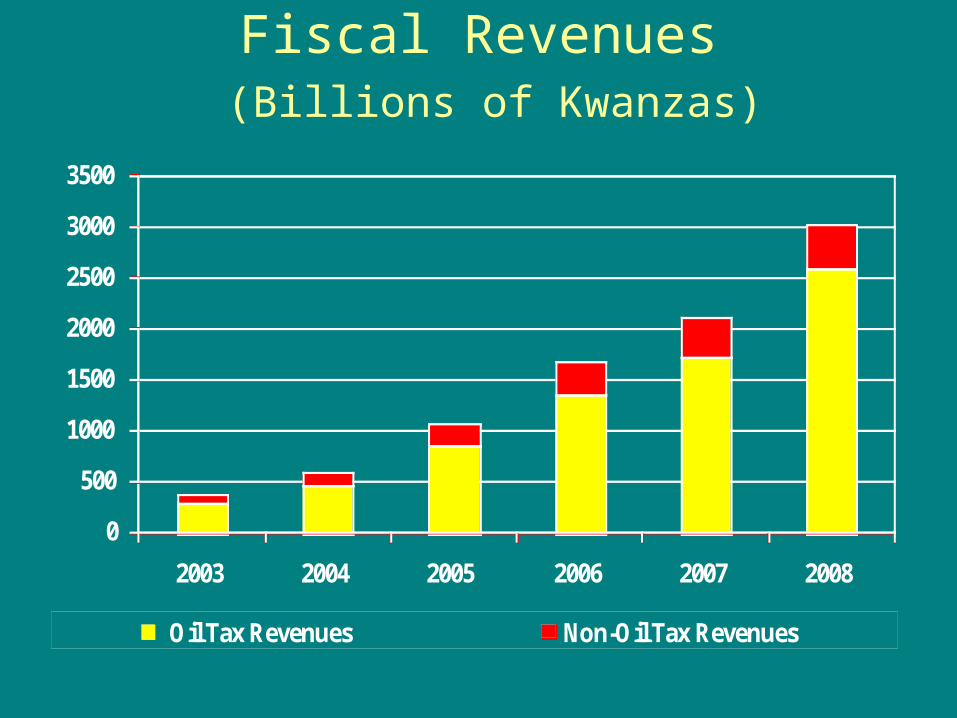

Fiscal Revenues (Billions of Kwanzas)

0

500

1000

1500

2000

2500

3000

3500

2003 2004 2005 2006 2007 2008

Oil Tax Revenues Non-Oil Tax Revenues

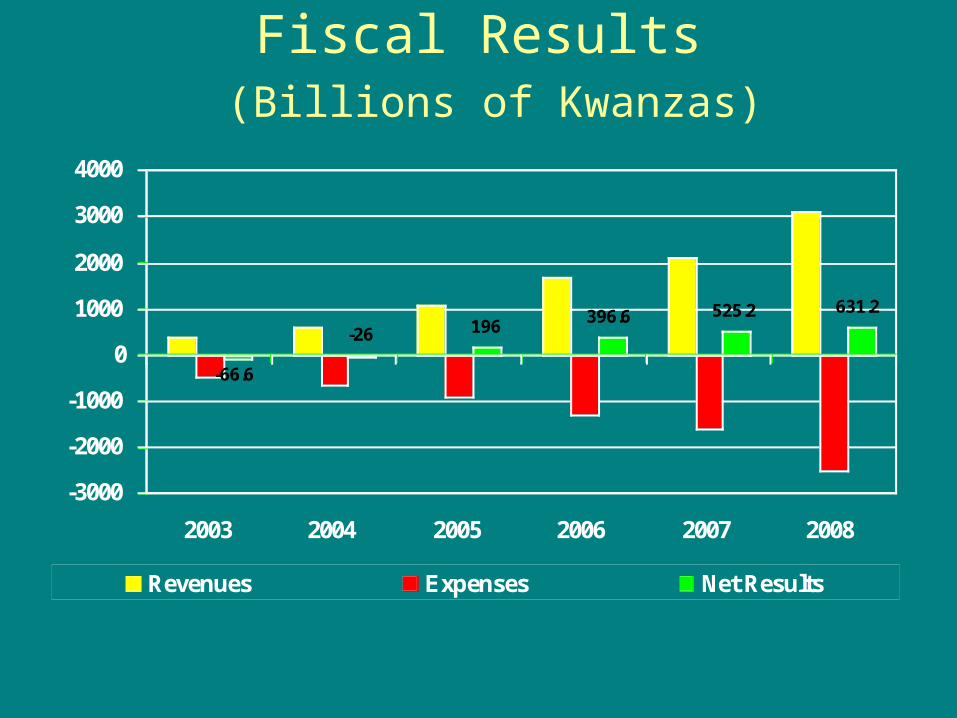

Fiscal Results (Billions of Kwanzas)

-66.6

-26 196 396.6 525.2 631.2

-3000

-2000

-1000

0

1000

2000

3000

4000

2003 2004 2005 2006 2007 2008

Revenues Expenses Net Results

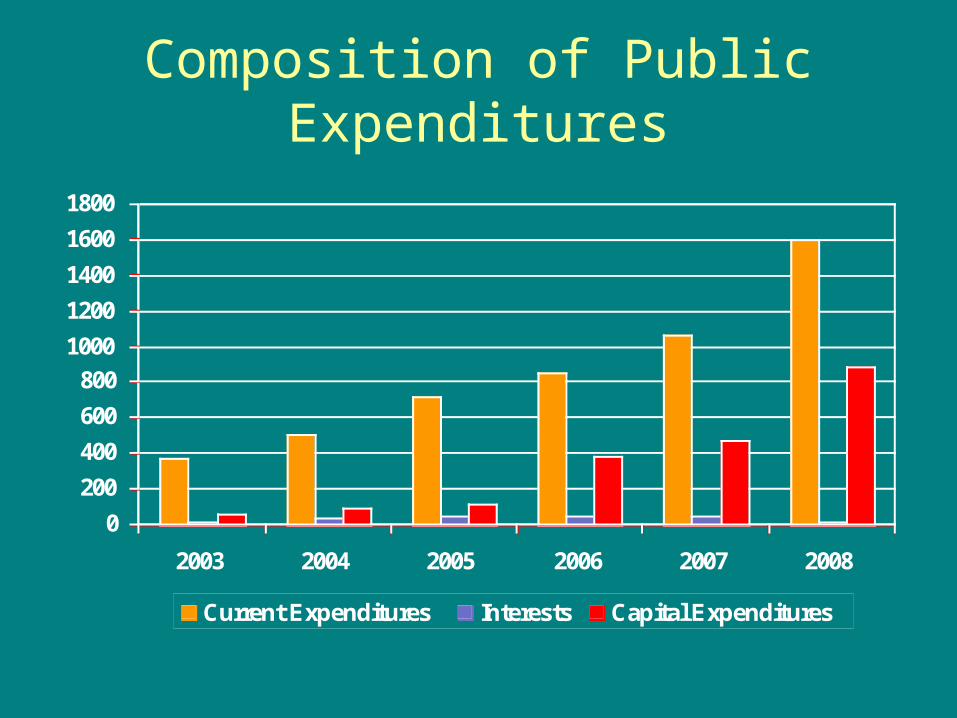

Composition of Public Expenditures

0

200

400

600

800

1000

1200

1400

1600

1800

2003 2004 2005 2006 2007 2008

Current Expenditures Interests Capital Expenditures

I. Recent Past: High Rates of Growth

• 1.1 Economic Growth

• 1.2 Inflation

• 1.3 External Sector

• 1.4 Public Sector

• 1.5 Social Gains

Social Gains in the Last Years

• Reduction of Poverty

• Improved Human Development Indicators

• Gains in the fight agains HIV/AIDS, malaria, etc.

Angola’s Economy: Past, Present and Future

I. Recent Past: High Rates of Growth

II. Present: The Mother of all Crisis and the Impacts on Angola’s Economy

III. Future: Medium and Long Runs

The Mother of all Crisis

• Financial Crisis:– Stock Markets Collapsed in many Advanced and

Developing Countries– Nacionalization of Fannie Mae and Freddie Mac – Bancrupcy of Banks and Insurance Companies– Liquidity Crisis– Others

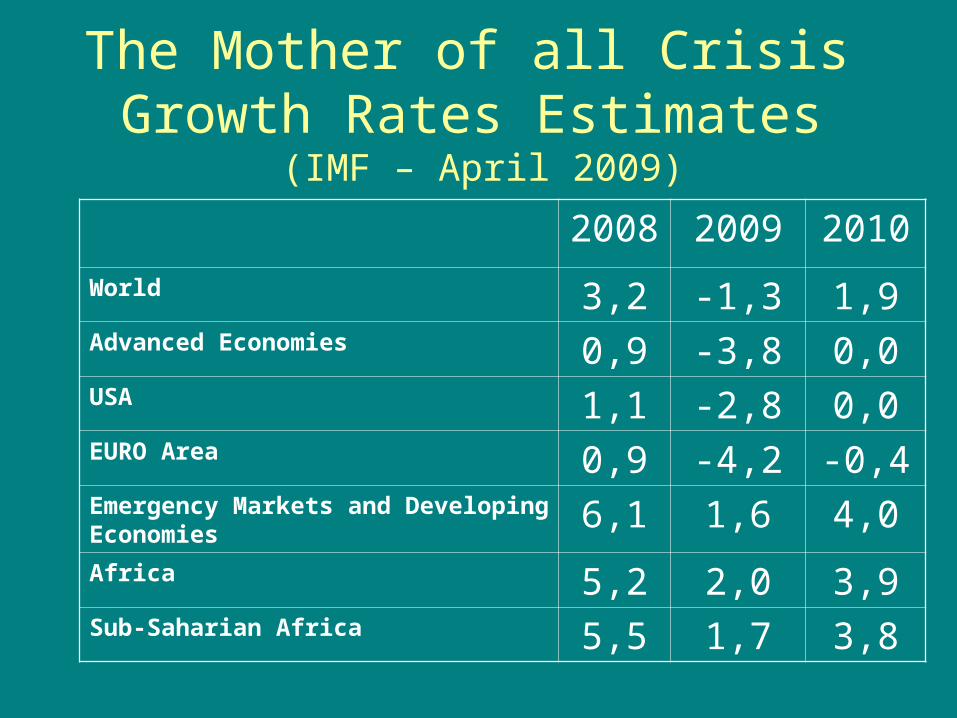

The Mother of all Crisis Growth Rates Estimates

(IMF – April 2009)

2008 2009 2010

World 3,2 -1,3 1,9Advanced Economies 0,9 -3,8 0,0USA 1,1 -2,8 0,0EURO Area 0,9 -4,2 -0,4Emergency Markets and Developing Economies

6,1 1,6 4,0

Africa 5,2 2,0 3,9Sub-Saharian Africa 5,5 1,7 3,8

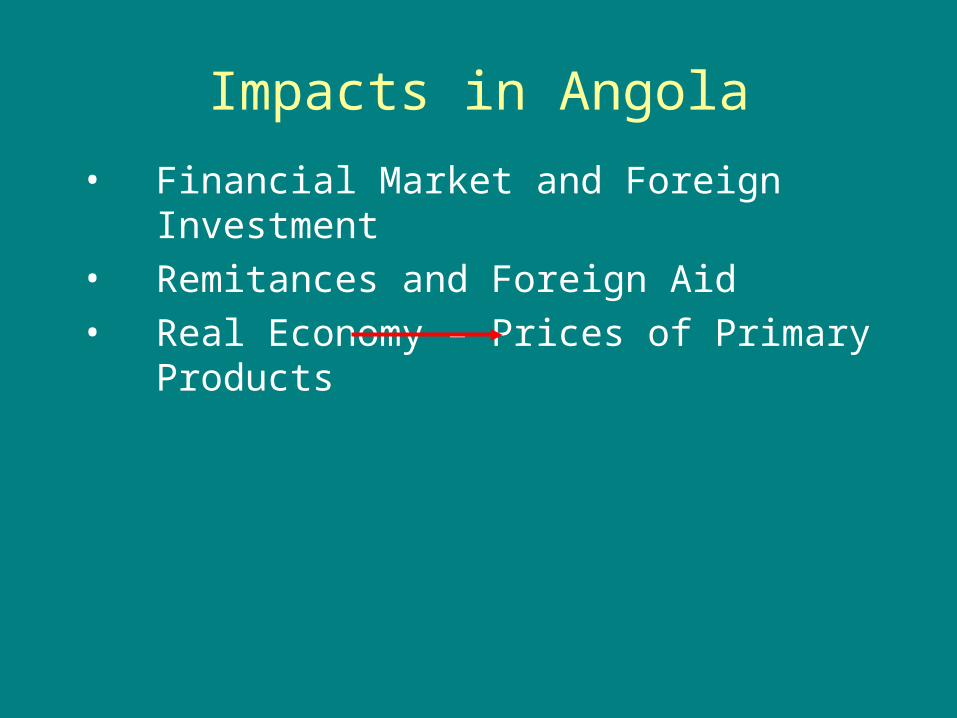

Impacts in Angola

• Financial Market and Foreign Investment• Remitances and Foreign Aid• Real Economy – Prices of Primary

Products

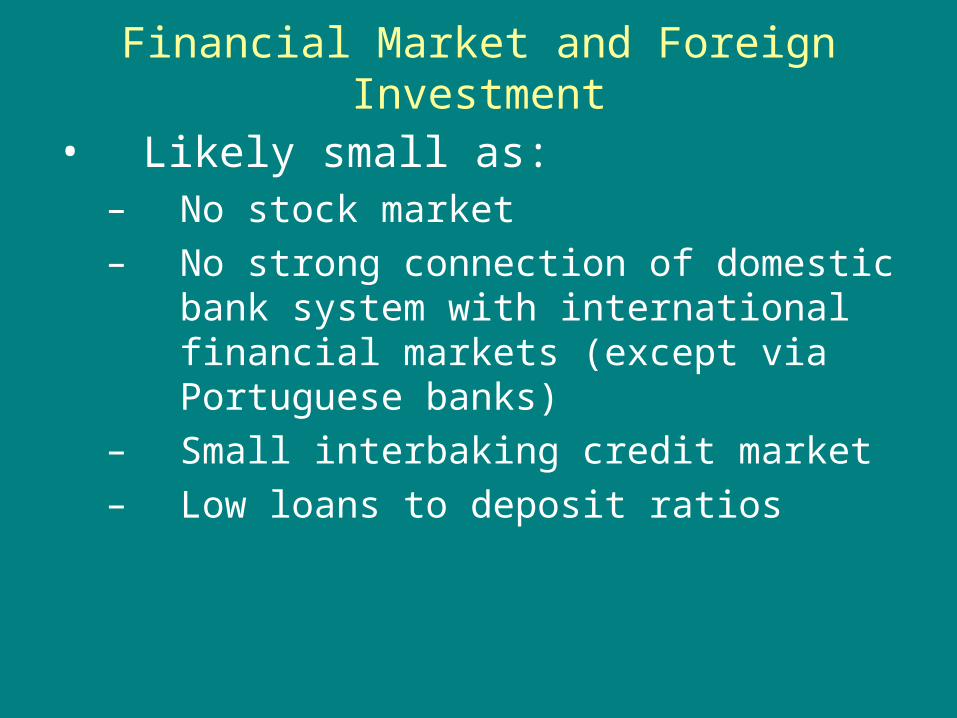

Financial Market and Foreign Investment

• Likely small as:– No stock market– No strong connection of domestic bank

system with international financial markets (except via Portuguese banks)

– Small interbaking credit market– Low loans to deposit ratios

Impacts in Angola

• Financial Market and Foreign Investment• Remitances and Foreign Aid• Real Economy – Prices of Primary

Products

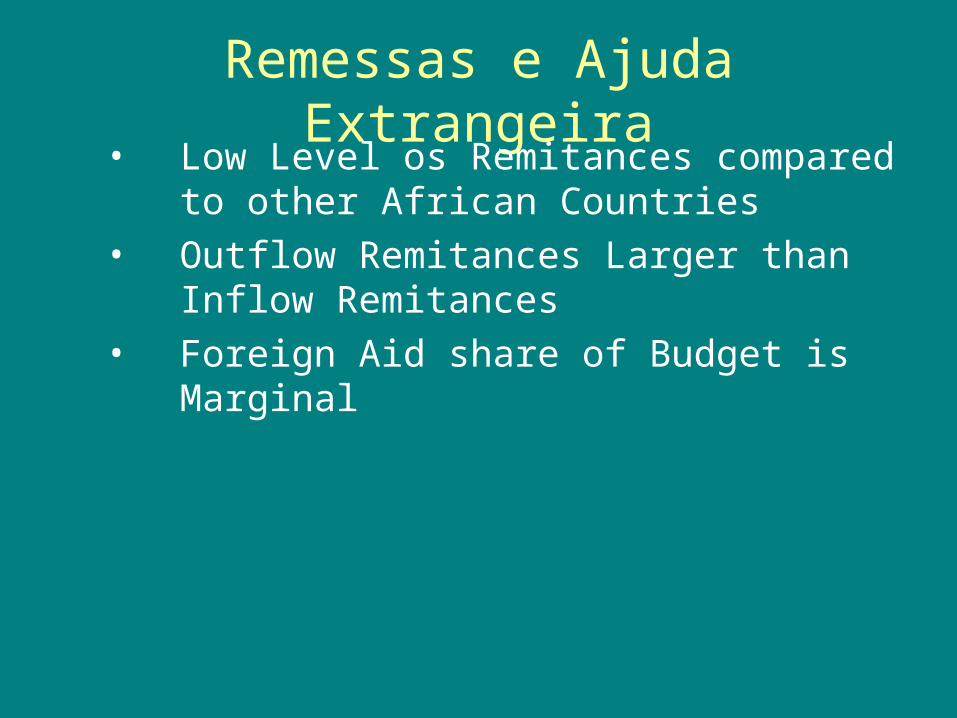

Remessas e Ajuda Extrangeira• Low Level os Remitances compared to

other African Countries• Outflow Remitances Larger than Inflow

Remitances• Foreign Aid share of Budget is Marginal

Impacts in Angola

• Financial Market and Foreign Investment• Remitances and Foreign Aid• Real Economy – Prices of Primary

Products

Real Economy

Economic Growth

Inflation

External Sector

Public Sector

Risks

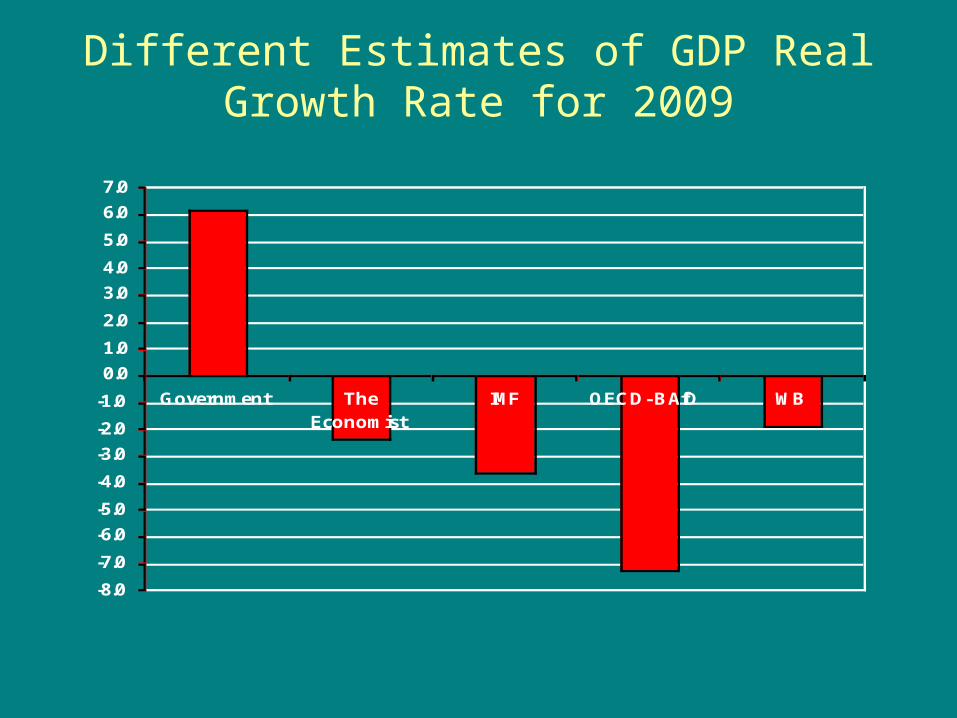

Different Estimates of GDP Real Growth Rate for 2009

-8.0

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Government TheEconomist

IMF OECD- BAfD WB

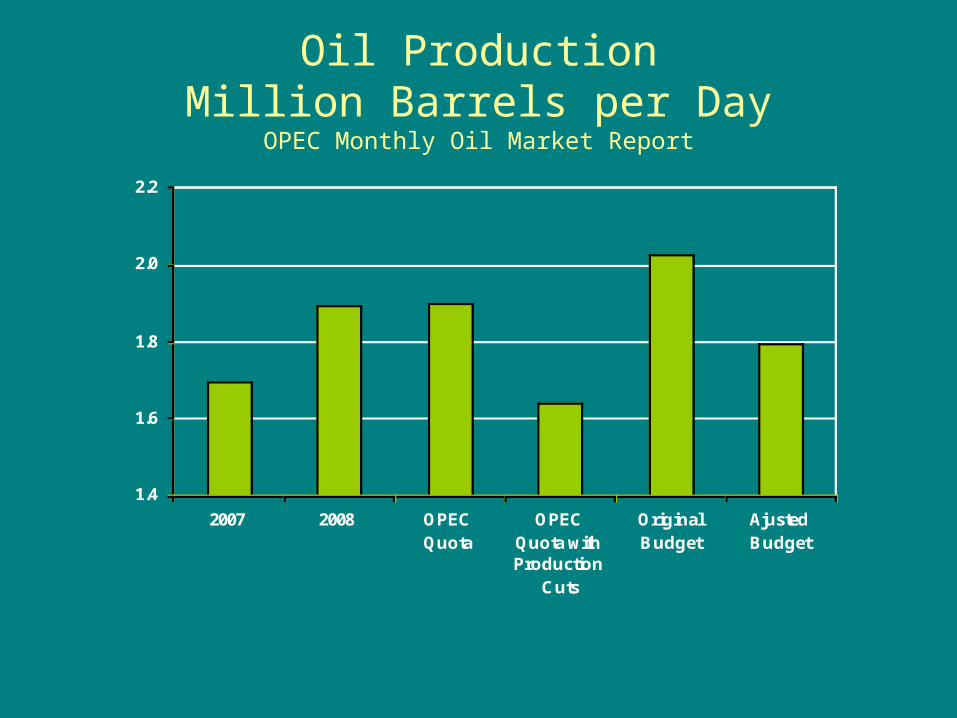

Oil ProductionMillion Barrels per Day

OPEC Monthly Oil Market Report

1.4

1.6

1.8

2.0

2.2

2007 2008 OPECQuota

OPECQuota withProduction

Cuts

OriginalBudget

AjustedBudget

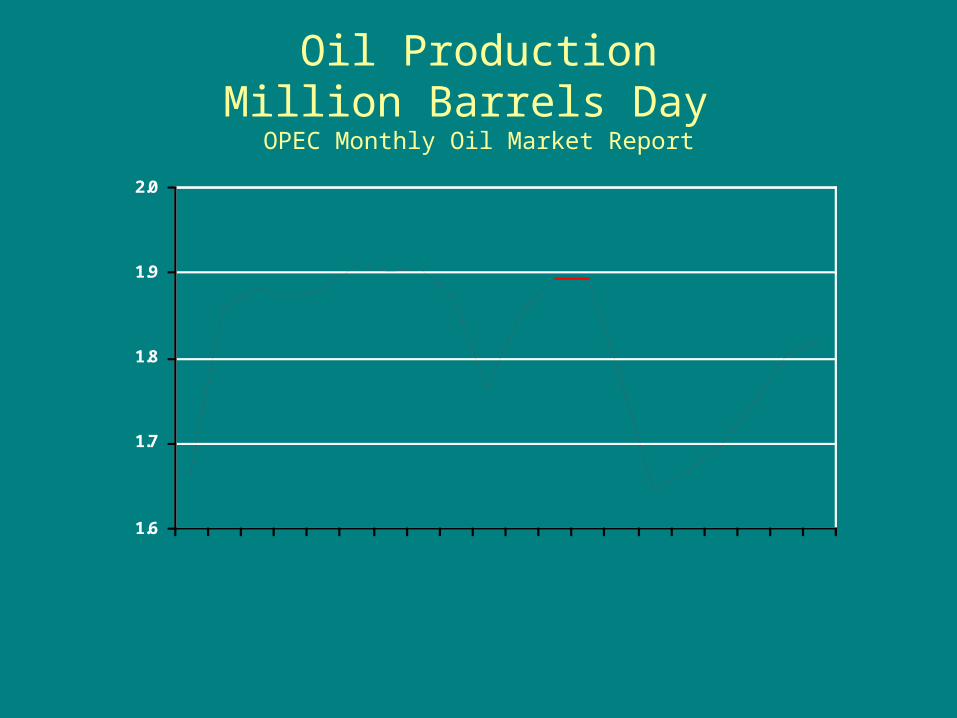

Oil ProductionMillion Barrels Day OPEC Monthly Oil Market Report

1.6

1.7

1.8

1.9

2.0

200708-Jan08-Feb08-Mar08-Apr08-May08-Jun08-Jul08-Aug08-Sep08-Oct08-Nov08-Dec09-Jan09-Feb09-Mar09-Apr09-May09-Jun09-Jul

Others Sectors

• Sector Positive Negative• Agriculture and Fishing High • Extractive Industries Low

– Oil and Gas Low – Diamants e other extractives High

• Manufacturing Low• Construction Low • Services Medium

Real Economy

Economic Growth

Inflation

External Sector

Public Sector

Risks

Yearly Inflation

0

50

100

150

200

250

300

2000 2001 2002 2003 2004 2005 2006 2007

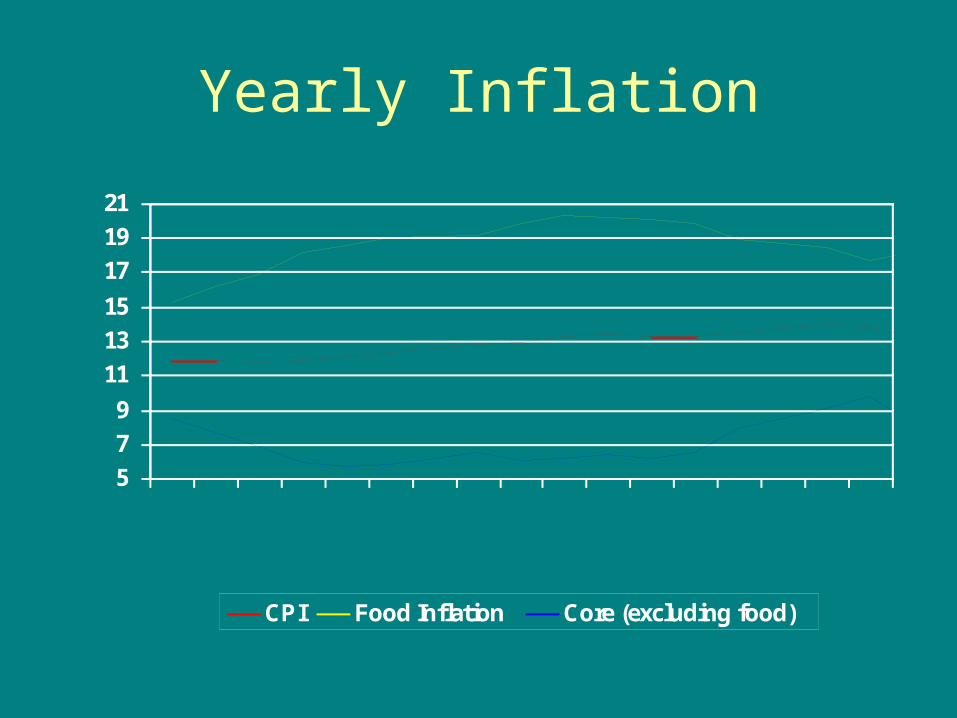

Yearly Inflation

5

7

9

11

13

15

17

19

21

Jan-08Feb-08Mar-08Apr-08May-08Jun-08Jul-08Aug-08Sep-08Oct-08Nov-08Dec-08Jan-09Feb-09Mar-09Apr-09May-09

CPI Food Inflation Core (excluding food)

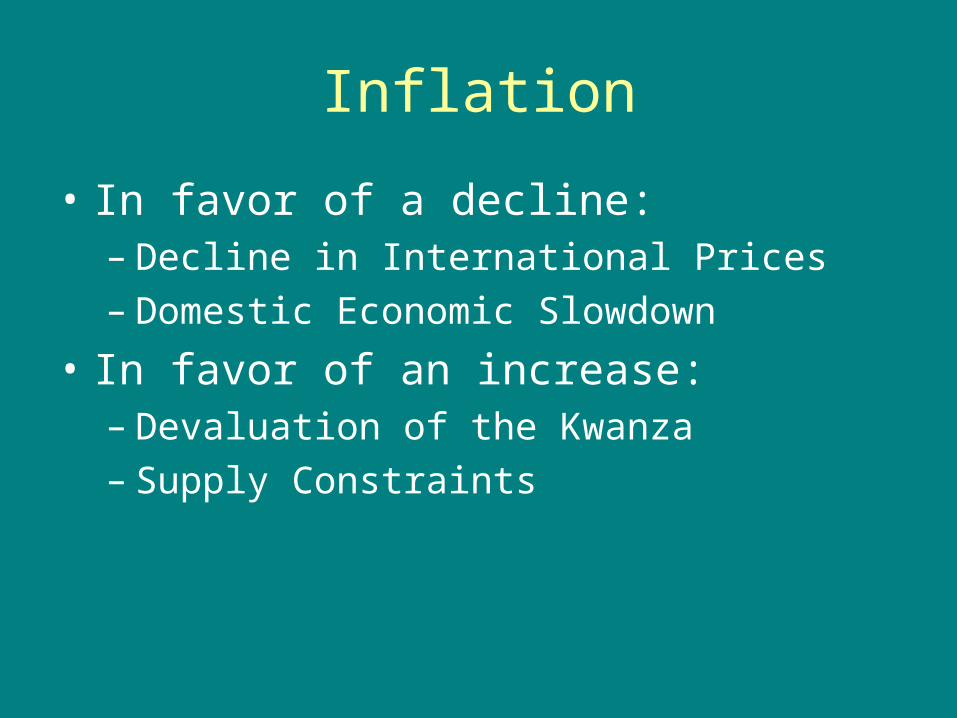

Inflation

• In favor of a decline:– Decline in International Prices– Domestic Economic Slowdown

• In favor of an increase:– Devaluation of the Kwanza– Supply Constraints

Real Economy

Economic Growth

Inflation

External Sector

Public Sector

Risks

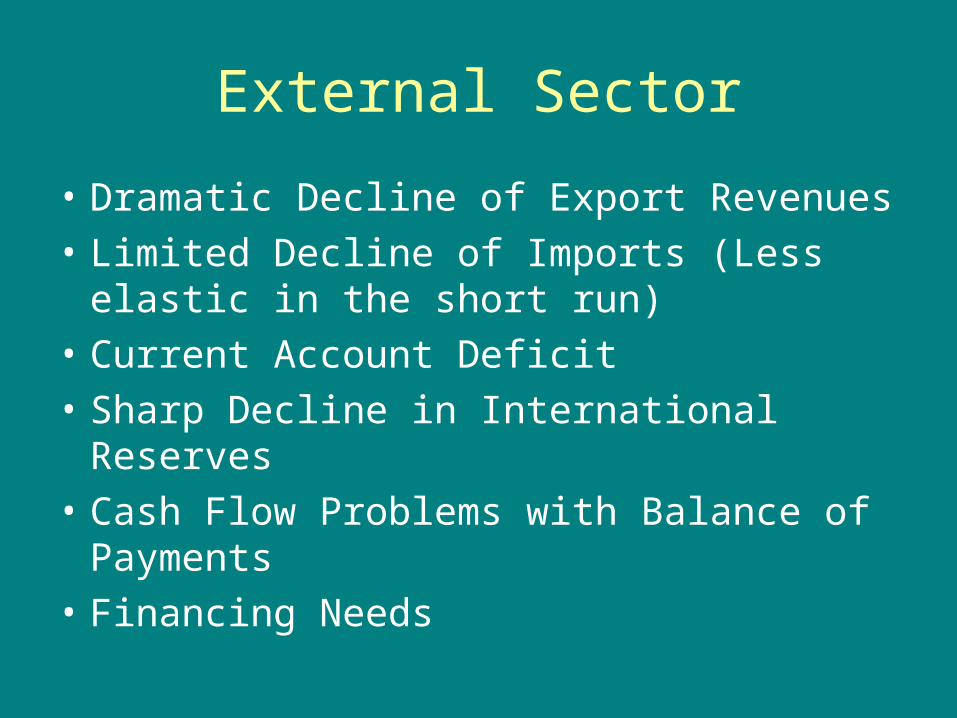

External Sector

• Dramatic Decline of Export Revenues

• Limited Decline of Imports (Less elastic in the short run)

• Current Account Deficit

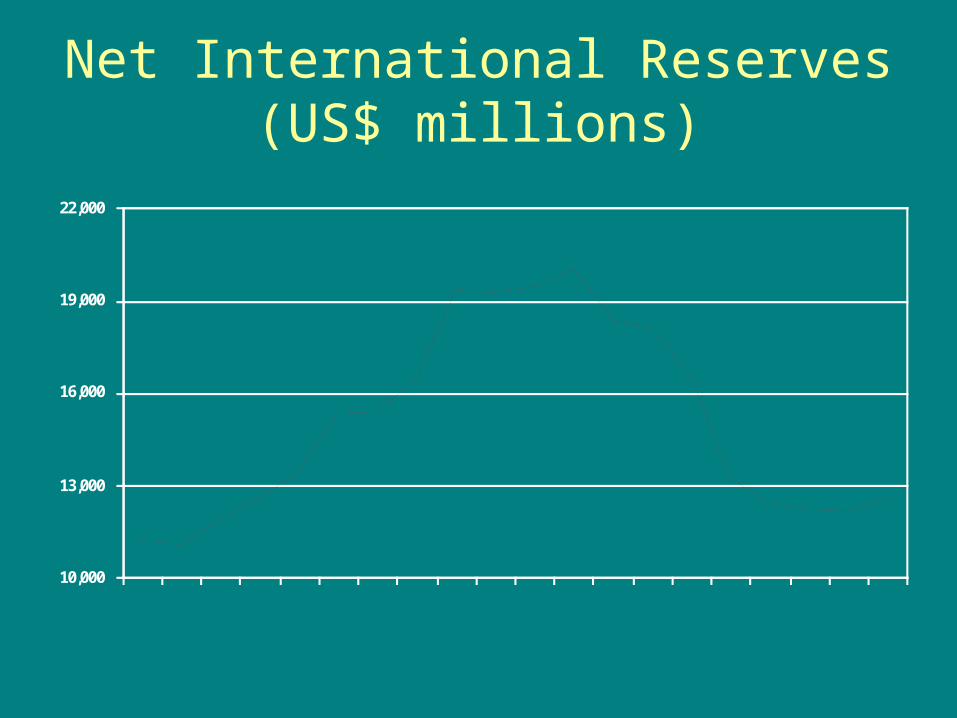

• Sharp Decline in International Reserves

• Cash Flow Problems with Balance of Payments

• Financing Needs

OPEC Reference Basket Daily Price - 2007, 2008, 2009US$

30

50

70

90

110

130

150

2-Jan 2-Feb 2-Mar 2-Apr 2-May 2-Jun 2-Jul2-Aug 2-Sep 2-Oct 2-Nov 2-Dec

2008

2009

2007

Net International Reserves (US$ millions)

10,000

13,000

16,000

19,000

22,000

200708-Jan08-Feb08-Mar08-Apr08-May08-Jun08-Jul08-Aug08-Sep08-Oct08-Nov08-Dec09-Jan09-Feb09-Mar09-Apr09-May09-Jun09-Jul

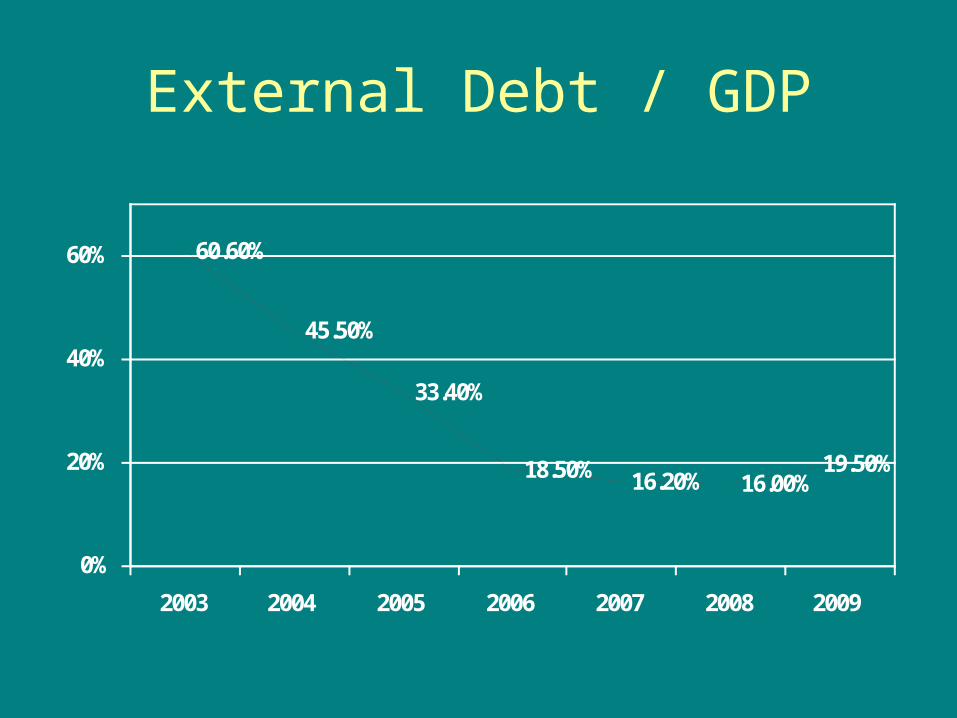

External Debt / GDP

60.60%

45.50%

33.40%

18.50% 16.20% 16.00%19.50%

0%

20%

40%

60%

2003 2004 2005 2006 2007 2008 2009

Real Economy

Economic Growth

Inflation

External Sector

Public Sector

Risks

Public Sector

• Lower Revenues

• Drastic Cuts in Spending

• How to Finance the Deficit?– High Cost, low demand for government bonds

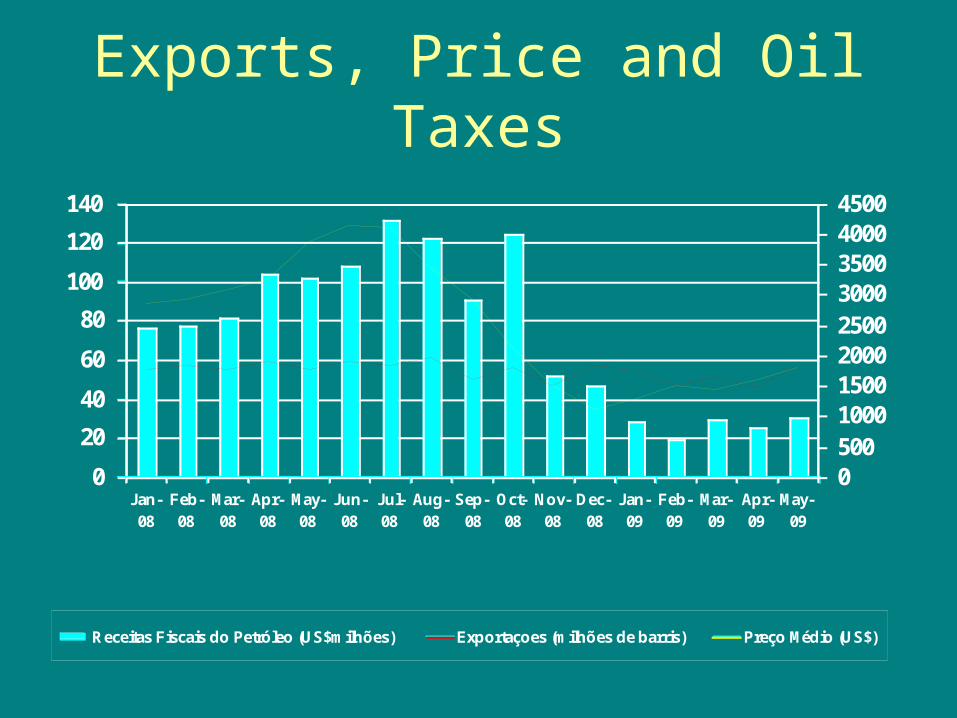

Exports, Price and Oil Taxes

0

20

40

60

80

100

120

140

Jan-08

Feb-08

Mar-08

Apr-08

May-08

Jun-08

Jul-08

Aug-08

Sep-08

Oct-08

Nov-08

Dec-08

Jan-09

Feb-09

Mar-09

Apr-09

May-09

050010001500200025003000350040004500

Receitas Fiscais do Petróleo (US$milhões) Exportaçoes (milhões de barris) Preço Médio (US$)

Real Economy

Economic Growth

Inflation

External Sector

Public Sector

Risks

Risks

• Global Recession • Fiscal and Monetary Policies

– Fiscal Policy:• Budget Adjustments• Payment Delays to Suppliers• Financing the Fiscal Deficit (High Cost)

– Monetary and Exchange Rate Policies:• Required Reserves• Exchange Rate policy

• Social Impacts

Social Impacts

• Increase in Poverty• Worsening of Human Development

Indicators• Potential increase in hunger• Infant Mortality• Political and Social Stress

Angola’s Economy: Past, Present and Future

I. Recent Past: High Rates of Growth

II. Present: The Mother of all Crisis and the Impacts on Angola’s Economy

III. Future: Medium and Long Runs

Prespectives for the Futuro:Medium Run

• At the Global Level:• Bad News: Recession in 2009 and increased

unemployment. Price of OIL?• Good News: Some indicators show

improvements and that the crisis may have hit bottom, but recovery will be slow

• In Angola:• Prepare for the Future• Diversification • Reforms

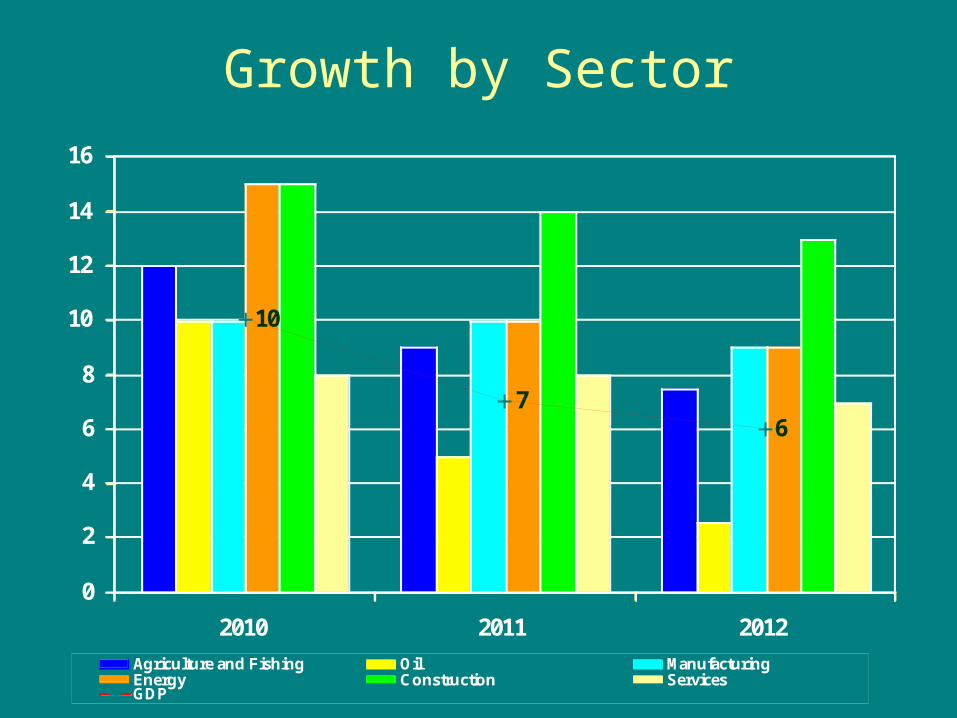

Growth by Sector

10

76

0

2

4

6

8

10

12

14

16

2010 2011 2012

Agriculture and Fishing Oil ManufacturingEnergy Construction ServicesGDP

Diversification

• Why?

• Where is Angola?

• How to Diversify?

• Challenges: How to surpass them

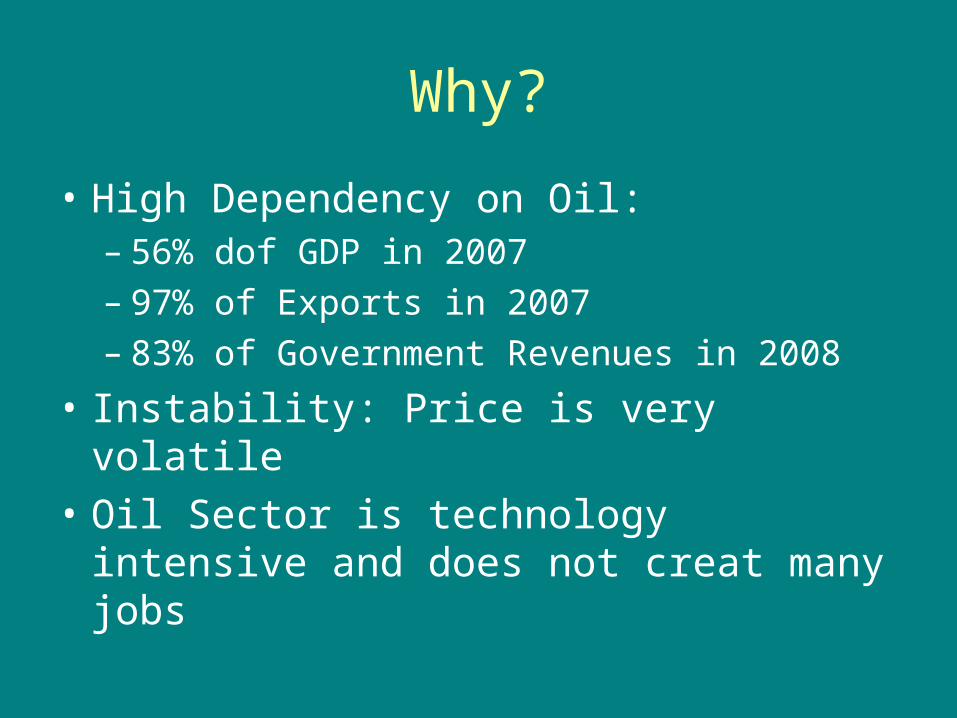

Why?

• High Dependency on Oil:– 56% dof GDP in 2007– 97% of Exports in 2007– 83% of Government Revenues in 2008

• Instability: Price is very volatile

• Oil Sector is technology intensive and does not creat many jobs

Diversification

• Why?

• Where is Angola?

• How to Diversify?

• Challenges: How to surpass them

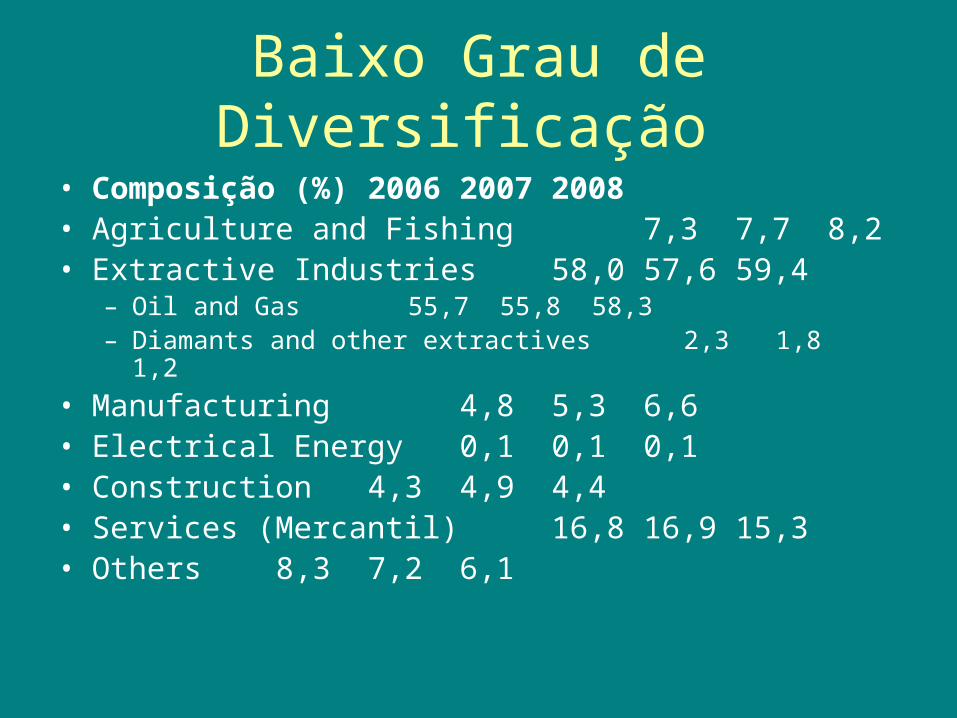

Baixo Grau de Diversificação

• Composição (%) 2006 2007 2008• Agriculture and Fishing 7,3 7,7 8,2• Extractive Industries 58,0 57,6 59,4

– Oil and Gas 55,7 55,8 58,3– Diamants and other extractives 2,3 1,8 1,2

• Manufacturing 4,8 5,3 6,6• Electrical Energy 0,1 0,1 0,1• Construction 4,3 4,9 4,4• Services (Mercantil) 16,8 16,9 15,3• Others 8,3 7,2 6,1

Diversification

• Why?

• Where is Angola?

• How to Diversify?

• Challenges: How to surpass them

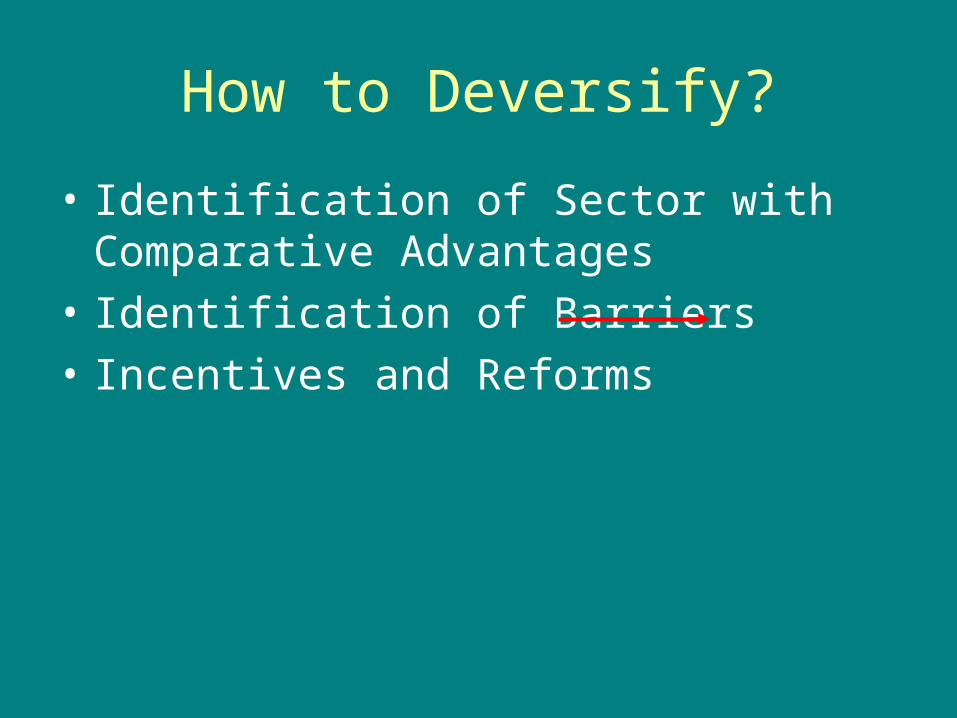

How to Deversify?

• Identification of Sector with Comparative Advantages

• Identification of Barriers

• Incentives and Reforms

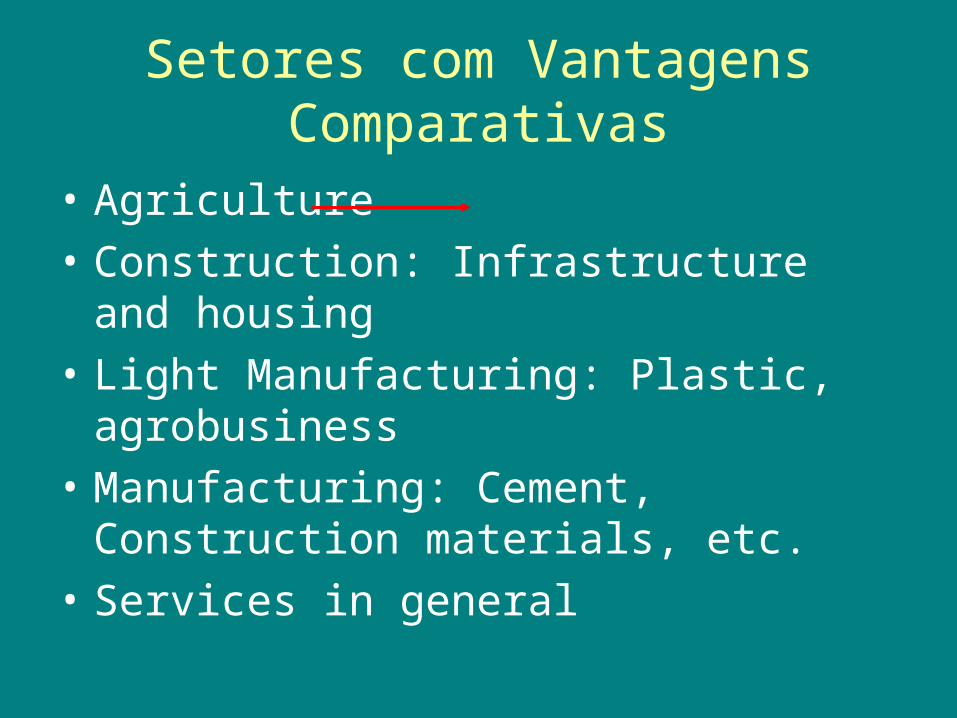

Setores com Vantagens Comparativas

• Agriculture

• Construction: Infrastructure and housing

• Light Manufacturing: Plastic, agrobusiness

• Manufacturing: Cement, Construction materials, etc.

• Services in general

Diversification is a Process

• Exemple: Agriculture– Steps:

• Deminization• Recuperation and construction of infrastructure

– Roads and bridges

– Water and electricity

– Others

• Realocation of Displaced rural population during the war• Distribution and preparation of land• Seed distribution• Logistic Support: Extention, Credit, distribution of production,

etc.

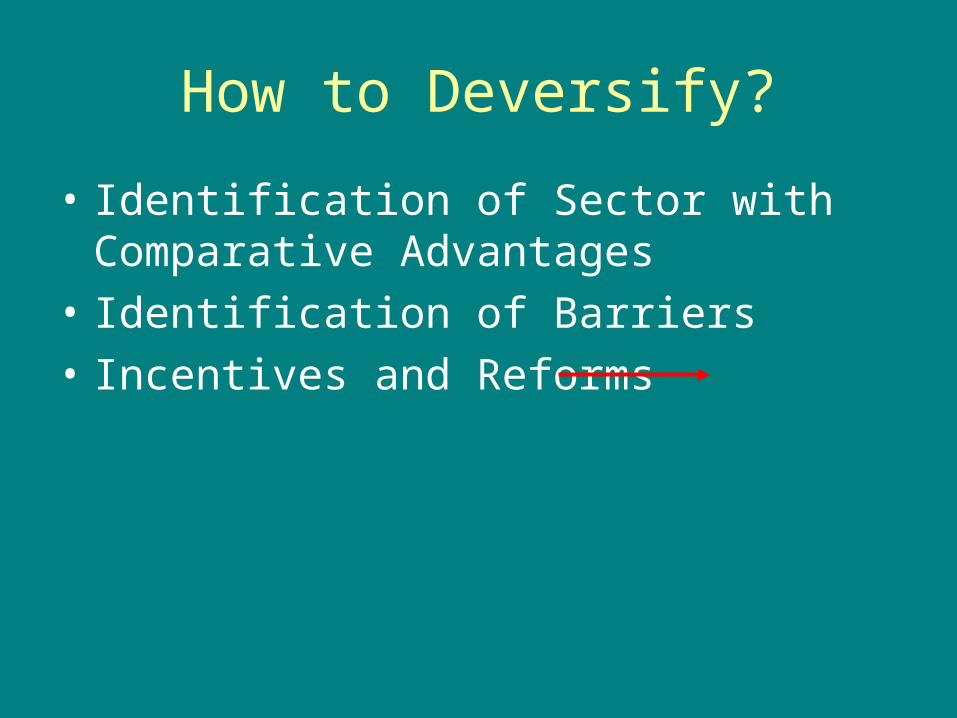

How to Deversify?

• Identification of Sector with Comparative Advantages

• Identification of Barriers

• Incentives and Reforms

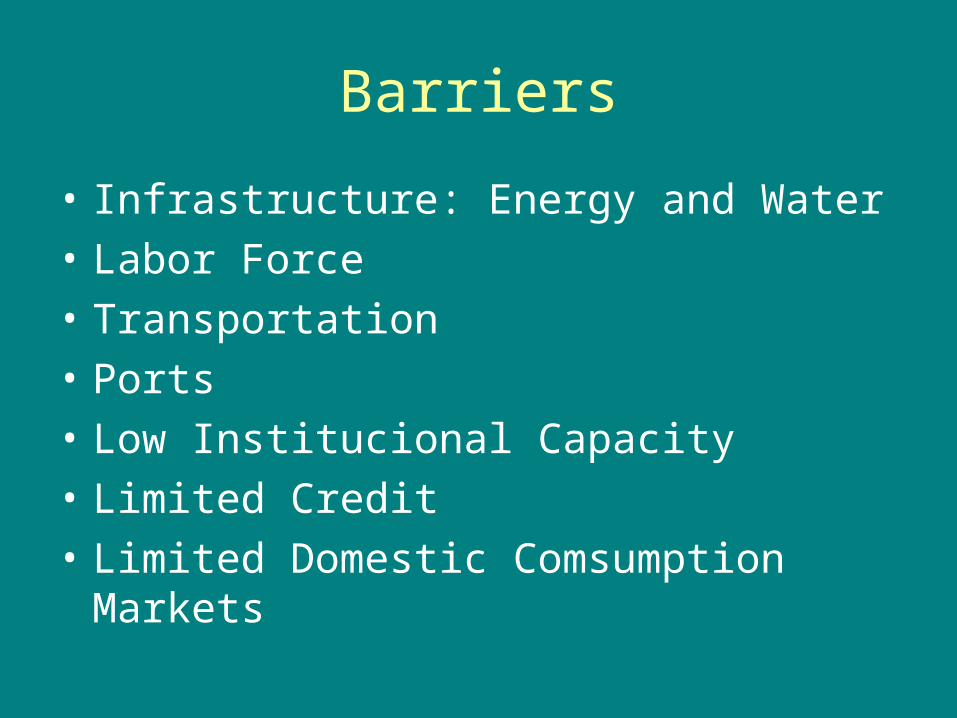

Barriers

• Infrastructure: Energy and Water

• Labor Force

• Transportation

• Ports

• Low Institucional Capacity

• Limited Credit

• Limited Domestic Comsumption Markets

How to Deversify?

• Identification of Sector with Comparative Advantages

• Identification of Barriers

• Incentives and Reforms

Incentives

– Fiscal– Credit– Joinventures– PPPs

Reforms

– Fiscal– Labor– Regulations– Public Sector: More Efficiency

Diversification

• Why?

• Where is Angola?

• How to Diversify?

• Challenges: How to surpass them

Challenges

• Short Run– Maintain Macro Stability in a scenario of

global crisis

• Medium and Long Run– Increase Competitiveness:

• Lower Cost of Production (transportation, credit)• Increase Factor Productivity

Angola’s Economy: Past, Present and Future

I. Recent Past: High Rates of Growth

II. Present: The Mother of all Crisis and the Impacts on Angola’s Economy

III. Future: Medium and Long Runs

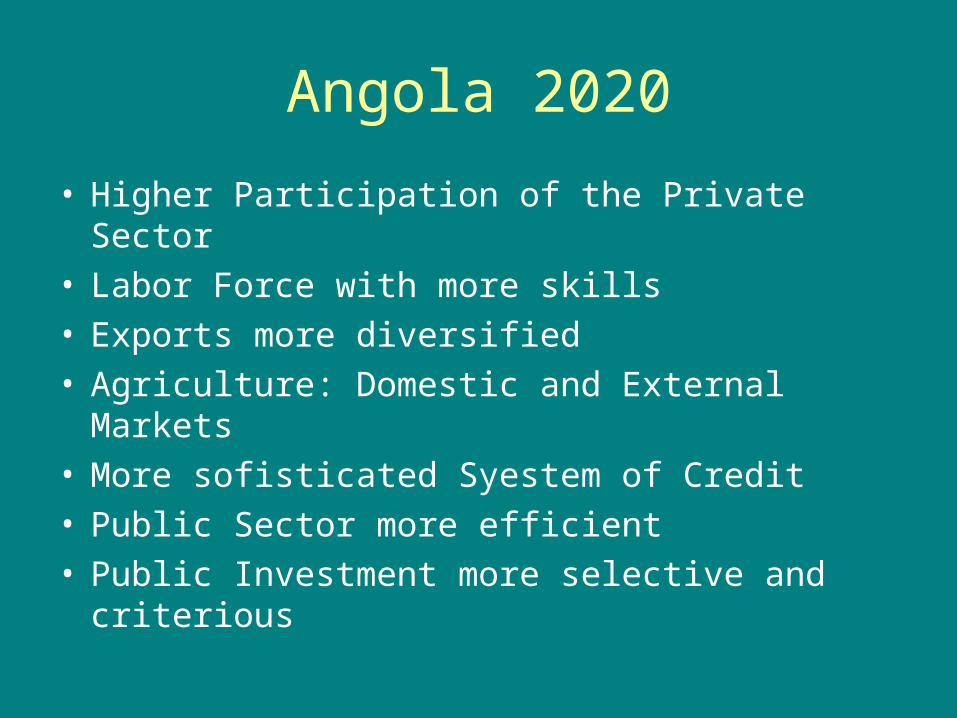

Angola 2020

• Higher Participation of the Private Sector• Labor Force with more skills• Exports more diversified• Agriculture: Domestic and External Markets• More sofisticated Syestem of Credit• Public Sector more efficient• Public Investment more selective and criterious

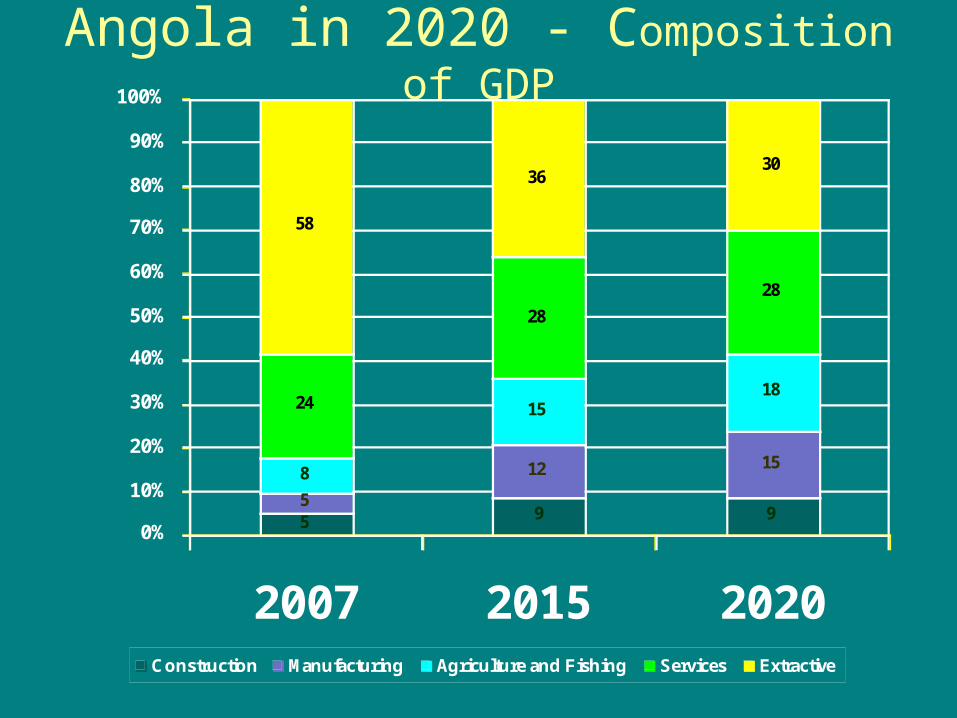

Angola in 2020 - Composition of GDP

5 9 95

12 158

1518

24

28

28

58

3630

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2015 2020Construction Manufacturing Agriculture and Fishing Services Extractive

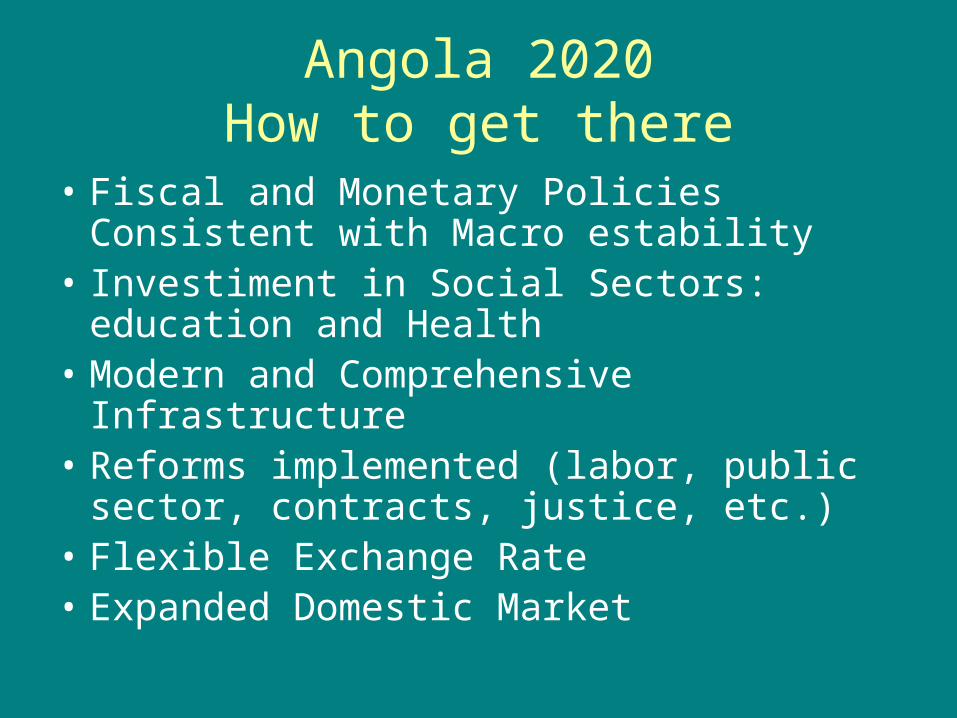

Angola 2020How to get there

• Fiscal and Monetary Policies Consistent with Macro estability

• Investiment in Social Sectors: education and Health

• Modern and Comprehensive Infrastructure• Reforms implemented (labor, public

sector, contracts, justice, etc.)• Flexible Exchange Rate• Expanded Domestic Market