Embed Size (px)

Citation preview

8/8/2019 Ankita Sapm CIA II

http://slidepdf.com/reader/full/ankita-sapm-cia-ii 1/17

Security Analysis and

Portfolio Management

CIA-II

You are required to build a portfolio for the following three

clients who is ready to invest Rs. 30,00,000 with a varied risk

appetite.:-

High risk (Client 1)

Moderate risk (Client 2)

Low risk (Client 3)

BBM A Finance 1

ANKITA RANKA 08D1064

8/8/2019 Ankita Sapm CIA II

http://slidepdf.com/reader/full/ankita-sapm-cia-ii 2/17

Security Analysis and Portfolio Management CIA -II

2 ANKITA RANKA 08D1064 -----BBM A-----FINANCE 1

FINANCIAL INSTRUMENTS

Financial instruments are cash, evidence of an ownership interest in an entity, or a

contractual right to receive, or deliver, cash or another financial instrument.

Financial instruments can be categorized by form depending on whether they are cash

instruments or derivative instruments:

y Cash instruments are financial instruments whose value is determined directly by

markets. They can be divided into securities, which are readily transferable, and other

cash instruments such as loans and deposits, where both borrower and lender have to

agree on a transfer.

y Derivative instruments are financial instruments which derive their value from the

value and characteristics of one or more underlying assets. They can be divided into

exchange-traded derivatives and over-the-counter (OTC) derivatives.

Alternatively, financial instruments can be categorized by "asset class" depending on whether

they are equity based (reflecting ownership of the issuing entity) or debt based (reflecting a

loan the investor has made to the issuing entity). If it is debt, it can be further categorised into

short term (less than one year) or long term.

Foreign Exchange instruments and transactions are neither debt nor equity based and

belong in their own category.

8/8/2019 Ankita Sapm CIA II

http://slidepdf.com/reader/full/ankita-sapm-cia-ii 3/17

Security Analysis and Portfolio Management CIA -II

3 ANKITA RANKA 08D1064 -----BBM A-----FINANCE 1

EQUITY INSTRUMENTS

In business and finance, a share (also referred to as equity share) of stock means a share of

ownership in a corporation (company). In the plural, stocks is often used as a synonym for

shares especially in the United States, but it is less commonly used that way outside of North

America.

In the United Kingdom, South Africa, and Australia, stock can also refer to completely

different financial instruments such as government bonds or, less commonly, to all kinds of

marketable securities.

DEB T INSTRUMENTS

Debt instruments typically state a repayment schedule, establish a interest rate on outstanding

debt, and explicitly state the issuer's obligation to repay.

Standardize debt instruments make issuing, purchasing and transferring these obligations

easy. Such added liquidity makes the purchase and issuance of debt more attractive, since

purchases gain confidence that they may trade their debt easily in the market, and issuers may

be confident that can find a purchaser of their new debt.

Examples include bills, bonds, notes, CDs, GICs, commercial paper, and banker's

acceptances.

8/8/2019 Ankita Sapm CIA II

http://slidepdf.com/reader/full/ankita-sapm-cia-ii 4/17

Security Analysis and Portfolio Management CIA -II

4 ANKITA RANKA 08D1064 -----BBM A-----FINANCE 1

I NITIAL CAPITAL: - 30,00,000

I NSTRUMENTS FOR I NVESTMENT

EQUITY

BULLION

MUTUAL FUNDS

POST-OFFICE SAVING SCHEME

BONDS

FIXED DEPOSITS

NATIONAL SAVING CERTIFICATE

PORTFOLIO

HIGH RISK (CLIENT ± 1)

MODERATE RISK (CLIENT ± 2)

LOW RISK (CLIENT ± 3)

8/8/2019 Ankita Sapm CIA II

http://slidepdf.com/reader/full/ankita-sapm-cia-ii 5/17

Secu it An l sis nd o tfolio n ement

CI A -II

5 AN A RAN A 08 1064 -----BB A----- NANC 1

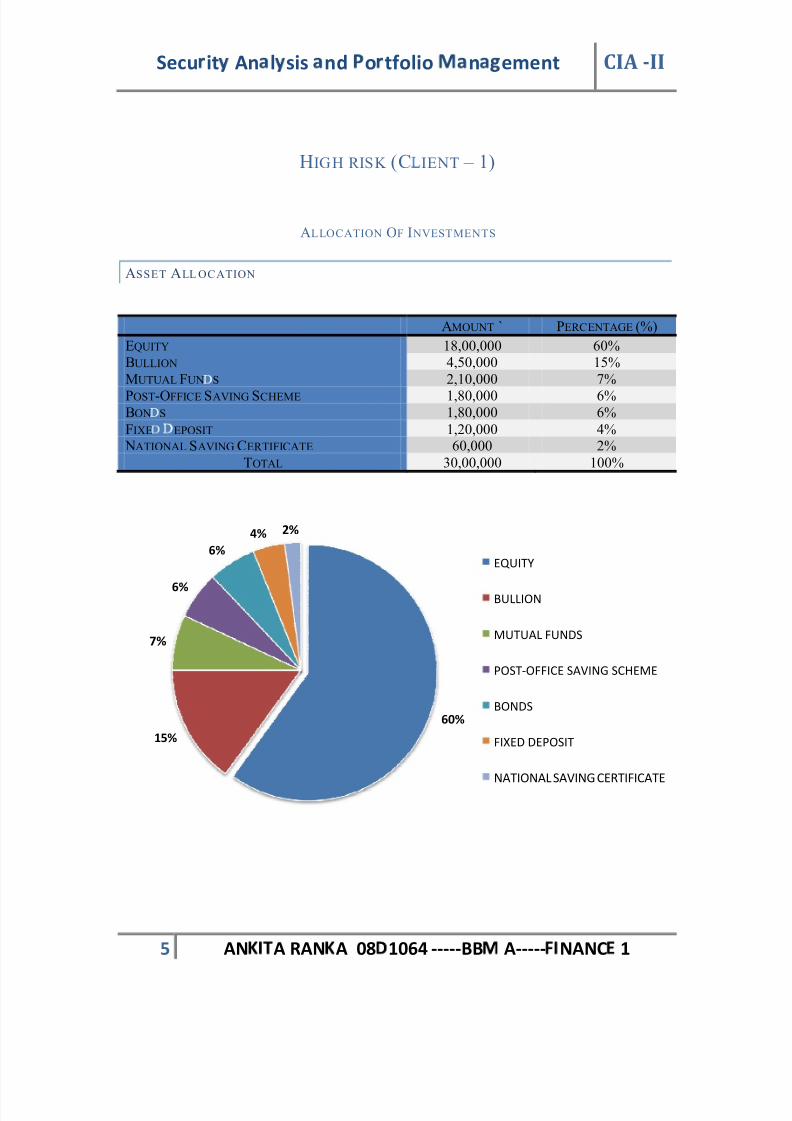

HIGH R ISK (C IENT ± 1)

ALLOCATION OF I NVESTMENTS

ASSET ALL OCATION

AMOUNT ` PERCENTAGE (%)

EQUITY 18,00,000 60%

BULLION 4,50,000 15%

MUTUAL FUN

S 2,10,000 7%

POST-OFFICE SAVING SCHEME 1,80,000 6%BON

S 1,80,000 6%

FIXE

EPOSIT 1,20,000 4% NATIONAL SAVING CER TIFICATE 60,000 2%

TOTAL 30,00,000 100%

60%

15%

7%

6%

6%

4% 2%

EQUITY

BULLION

MUTUAL FUNDS

POST-OFFICE SAVING SCHEME

BONDS

FIXED DEPOSIT

NATIONAL SAVING CERTIFICATE

8/8/2019 Ankita Sapm CIA II

http://slidepdf.com/reader/full/ankita-sapm-cia-ii 6/17

Secu it An l sis and Po tfolio Management CI A -II

6 AN A RAN A 08 1064 -----BBM A----- NANC 1

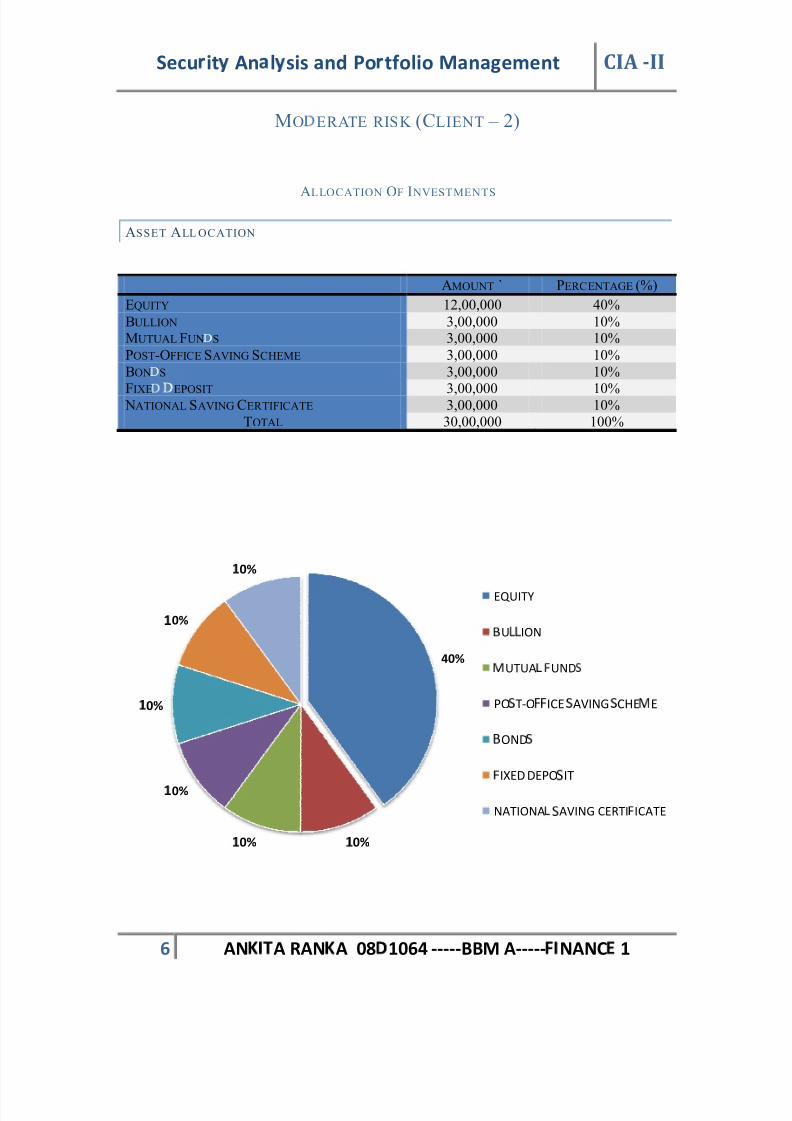

MO ER ATE R ISK (CLIENT ± 2)

ALLOCATION OF I NVESTMENTS

ASSET ALL OCATION

AMOUNT ` PERCENTAGE (%)

EQUITY 12,00,000 40%

BULLION 3,00,000 10%MUTUAL FUN

¡

S 3,00,000 10%

POST-OFFICE SAVING SCHEME 3,00,000 10%

BON¡

S 3,00,000 10%

FIXE

¡

EPOSIT 3,00,000 10% NATIONAL SAVING CER TIFICATE 3,00,000 10%

TOTAL 30,00,000 100%

40%

¢ 0%¢ 0%

£ 0%

¢ 0%

£ 0%

¢ 0%

EQUITY

¤ U¥ ¥

ION

¦ UTUA ¥ § UND ̈

PO© T-O ICE © AVING © CHE E

OND©

IXED DEPO© IT

NATIONA ¥ ̈

AVING CERTI § ICATE

8/8/2019 Ankita Sapm CIA II

http://slidepdf.com/reader/full/ankita-sapm-cia-ii 7/17

Secu it Anal sis and Po tfolio Management CI A -II

7 AN A RAN A 08 1064 -----BBM A----- NANC 1

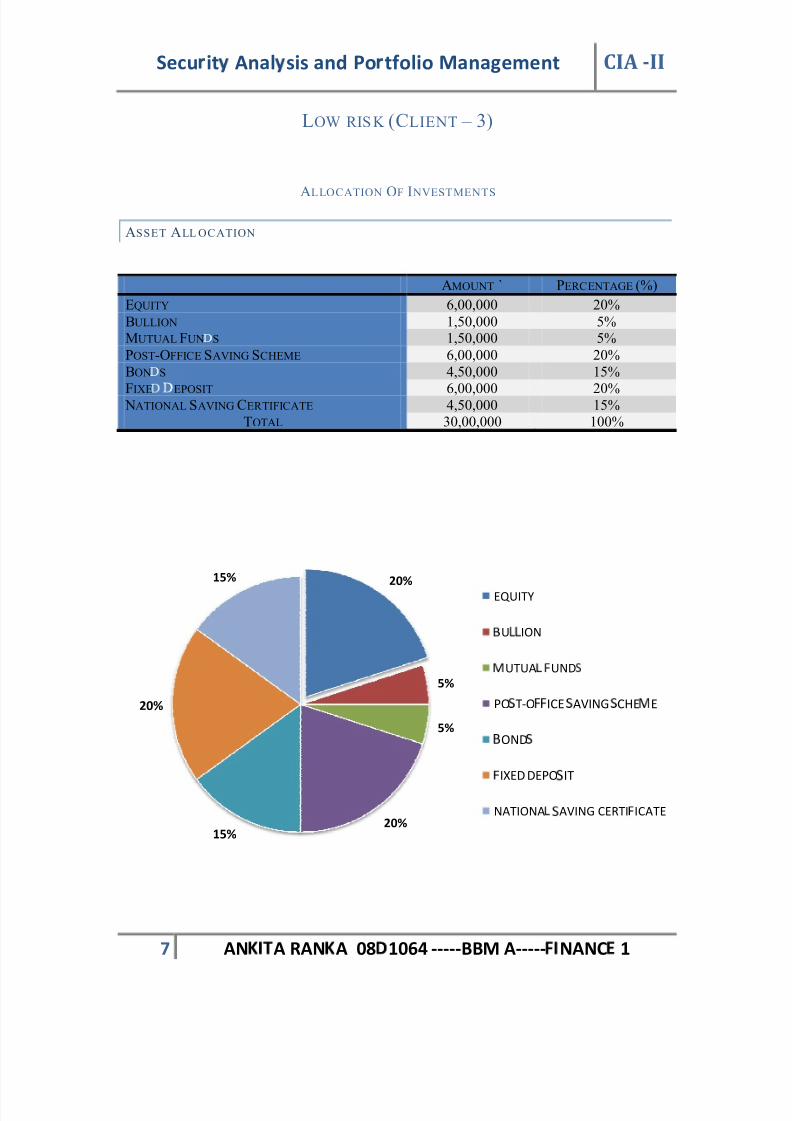

LOW R ISK (CLIENT ± 3)

ALLOCATION OF I NVESTMENTS

ASSET ALL OCATION

AMOUNT ` PERCENTAGE (%)

EQUITY 6,00,000 20%

BULLION 1,50,000 5%MUTUAL FUN

S 1,50,000 5%

POST-OFFICE SAVING SCHEME 6,00,000 20%

BON

S 4,50,000 15%

FIXE

EPOSIT 6,00,000 20% NATIONAL SAVING CER TIFICATE 4,50,000 15%

TOTAL 30,00,000 100%

20%

5%

5%

20%15%

20%

15%

EQUITY

U

ION

UTUA UND

PO T-O ICE AVING CHE ! E

" OND

IXED DEPO IT

NATIONA

AVING CERTI ICATE

8/8/2019 Ankita Sapm CIA II

http://slidepdf.com/reader/full/ankita-sapm-cia-ii 8/17

Security Analysis and Portfolio Management CIA -II

8 ANKITA RANKA 08D1064 -----BBM A-----FINANCE 1

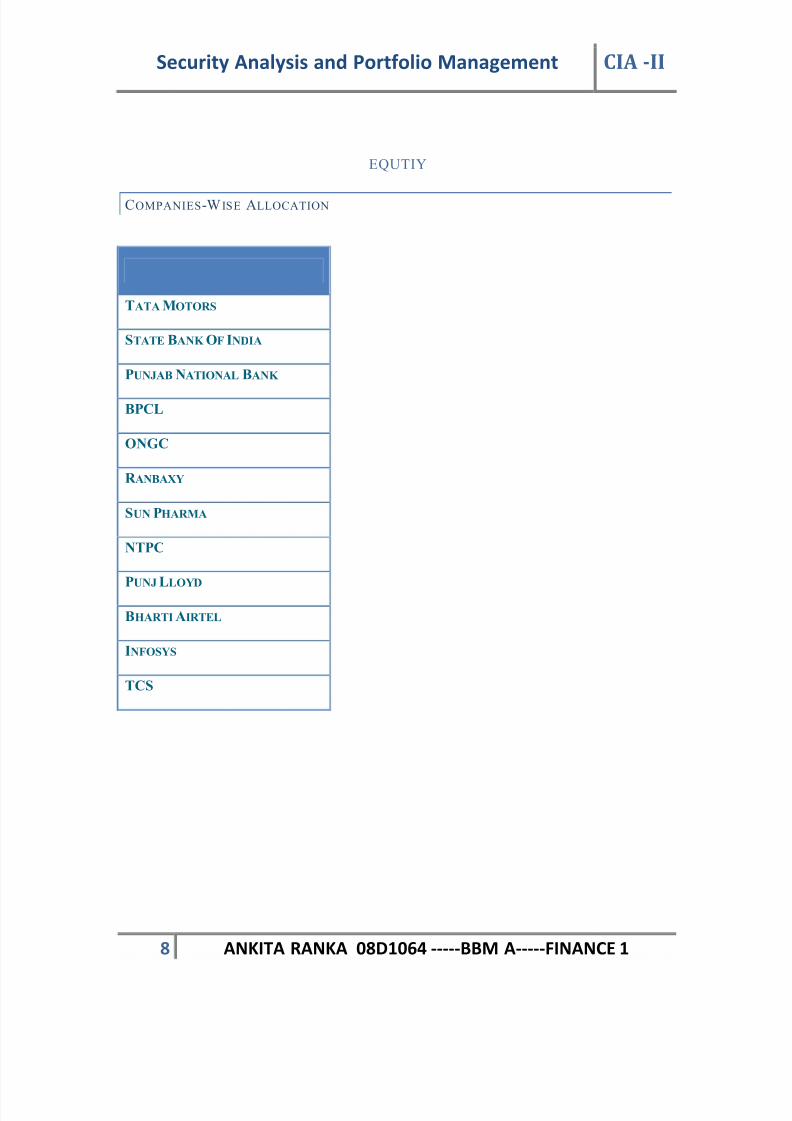

EQUTIY

COMPANIES-W ISE ALLOCATION

TATA MOTORS

STATE BANK OF INDIA

PUNJAB NATIONAL BANK

BPCL

ONGC

R ANBAXY

SUN PHARMA

NTPC

PUNJ

LLOYD

BHARTI AIRTEL

INFOSYS

TCS

8/8/2019 Ankita Sapm CIA II

http://slidepdf.com/reader/full/ankita-sapm-cia-ii 9/17

Security Analysis and Portfolio Management CIA -II

9 ANKITA RANKA 08D1064 -----BBM A-----FINANCE 1

R EASONS FOR INVESTMENT IN EQUITY

The Company you invested in will pay dividends based on their profits for the year.

The main one is that the investor has proportional share of the dividends generated by

the company in which he bought his stock.

A company may decide to offer additional stock to its shareholders giving them a

preferential right to subscribe for the shares. The price of a Rights Issue is generally

below the market value of a share.

A Company may allot shares free of charge to its shareholders. Bonus Issues are

provided when a company has large reserves and wishes to capitalize a part of these

reserves. When a Bonus Issue is announced the price of the share usually increases.

Other Benefits in the long-term, shares usually provide a higher return to investors

in comparison to maintaining the investment in a fixed deposit at a bank.

Investments made to get huge rate of return is only possible with the help of equity.

The return is uncertain but it is very efficient.

8/8/2019 Ankita Sapm CIA II

http://slidepdf.com/reader/full/ankita-sapm-cia-ii 10/17

Security Analysis and Portfolio Management CIA -II

10 ANKITA RANKA 08D1064 -----BBM A-----FINANCE 1

R EASONS FOR INVESTMENT IN GOLD ETF

Gold exchange-traded funds (ETF) may be new for India, but are gaining in

popularity as investors become aware of the benefits of investing in gold in a non-

material form as opposed to holding it as jewellery.

ETFs are instruments that trade like shares and are backed by physical holdings of the

commodity.

India is the world's top consumer of gold, accounting for 20 percent of global

demand. Indians traditionally invest in gold jewellery.

India has eight gold ETFs currently listed with a total collection of more than 11

tonnes, nearly double compared to last year.

Gold ETFs are a "must have", according to mutual funds, who typically advise clients

to allocate 10 percent of their portfolios to gold.

More financial firms are expected to launch gold ETFs in their bid to offer a full

basket of investment products to clients.

India's gold ETF collection is small compared to its approximately 700 tonnes of

annual gold consumption, but is seen growing by at least 50 percent year-on-year.

Indians' religious sentiment for gold is visible in ETF purchases as well, as volumes

tend to rise on days that are considered auspicious for buying the metal, officials

managing the ETFs say.

Gold is considered to be a safe and stable investment compared to other asset classes.

Its return potential is less when compared to an equity investment, so is the risk.

8/8/2019 Ankita Sapm CIA II

http://slidepdf.com/reader/full/ankita-sapm-cia-ii 11/17

Security Analysis and Portfolio Management CIA -II

11 ANKITA RANKA 08D1064 -----BBM A-----FINANCE 1

R EASONS TO INVEST IN MUTUAL FUNDS

Professional Management - The primary advantage of funds is the professional

management of your money. Investors purchase funds because they do not have the

time or the expertise to manage their own portfolios. A mutual fund is a relatively

inexpensive way for a small investor to get a full-time manager to make and monitor

investments.

Diversification - By owning shares in a mutual fund instead of owning individual

stocks or bonds, your risk is spread out. The idea behind diversification is to invest in

a large number of assets so that a loss in any particular investment is minimized by

gains in others.

Economies of Scale - Because a mutual fund buys and sells large amounts of

securities at a time, its transaction costs are lower than what an individual would pay

for securities transactions.

Liquidity - Just like an individual stock, a mutual fund allows you to request that

your shares be converted into cash at any time.

Simplicity - Buying a mutual fund is easy. Pretty well any bank has its own line of

mutual funds, and the minimum investment is small.

Flexibility: The investments pertaining to the Mutual Fund offers the public a lot

of flexibility by means of dividend reinvestment, systematic investment plans and

systematic withdrawal plans.

Affordability: The Mutual funds are available in units. Hence they are highly

affordable and due to the very large principal sum, even the small investors are

benefited by the investment scheme.

The fees pertaining to the custodial, brokerage, and others is very low.

8/8/2019 Ankita Sapm CIA II

http://slidepdf.com/reader/full/ankita-sapm-cia-ii 12/17

Security Analysis and Portfolio Management CIA -II

12 ANKITA RANKA 08D1064 -----BBM A-----FINANCE 1

R EASONS FOR INVESTMENT IN POST-OFFICE (MIS)

Safe & sure way to get a regular monthly income.

The regular income can be used to meet various expenses incurred in maintaining the

portfolio.

It is healthy have some amount of liquid assets which may be helpful to meet the

uncertainty.

Premature closure of the account is permitted any time after the expiry of a period of

one year of opening the account.

Deduction of an amount equal to 5 per cent of the deposit is to be made when the

account is prematurely closed.

Investors can withdraw money before three years, but a discount of 5%. Closing of

account after three years will not have any deductions.

Monthly interest can be automatically credited to savings account provided both the

accounts standing at the same post office.

The interest income accruing from a post-office MIS is exempt from tax under

Section 80L of the Income Tax Act, 1961. Moreover, no TDS is deductible on the

interest income.

The balance is exempt from Wealth Tax.

8/8/2019 Ankita Sapm CIA II

http://slidepdf.com/reader/full/ankita-sapm-cia-ii 13/17

Security Analysis and Portfolio Management CIA -II

13 ANKITA RANKA 08D1064 -----BBM A-----FINANCE 1

R EASONS FOR INVESTMENT IN K ISAN VIKAS PATRA

It is a safe investment with guaranteed returns

There is absolutely no risk involves, thus it acts as an anchor to an investment

portfolio.

Income is assured at the prescribed rate of interest. As mentioned, this is a risk-free

investment channel as the KVP comes with the backing of the Government of India.

Depending on whether the finance company or the bank from where you are raising

the loan accepts it or not. Some banks accept it for raising house loans. It is the only fixed income instrument which guarantees to double your investment

over a few years. So those who are conservative but still aim to create wealth over a

period of time may think of KVP.

KVP accumulates money at a fixed rate, and your money doubles in 7 years and 3

months. But KVP is not meant for regular income. It is for those looking for a safe

avenue of investment without the pressing need for a regular source of income.

Most of the other post office savings instruments are not liquid but this is not true in

case of KVP. Encashment of the KVP before maturity is possible from two and a half

years. However, one may forgo some interest income.

8/8/2019 Ankita Sapm CIA II

http://slidepdf.com/reader/full/ankita-sapm-cia-ii 14/17

Security Analysis and Portfolio Management CIA -II

14 ANKITA RANKA 08D1064 -----BBM A-----FINANCE 1

R EASONS FOR INVESTMENT IN FIX ED DEPOSITS

A good investment strategy requires choosing the right mix of safe and risky

investments. Among safe investments, fixed deposits FDs are the most popular

today. It is the most conservative and simplest form of investment one can opt for. It is

also one of the oldest and most trusted investments.

It will provide for the reduction of the risk factor in the portfolio by facilitating

steady, safe and assured returns with no risk.

The fixed deposits of reputed banks and financial institutions regulated by R BI

(Reserve Bank of India) the banking regulator in India is very secure and

considered as one of the safest investment methods.

With the directives of the income tax department stating that investment in fixed

deposits up to a maximum of ` 100,000 for 5 years are eligible for tax deductions

under section 80 C of income tax act, fixed deposits have again become

popular. Fixed deposits save tax and give high returns on invested money.

Loans up to 75%- 90% of the deposit amount from banks against fixed deposit

receipts. The interest charged will be 2 more than the rate of interest earned by the

deposit.

With fluctuation in market conditions and the immense effect of the global

scenario on Indian investment avenues, FDs act as a buffer for such factors which

threaten the stability and profitability of a portfolio.

8/8/2019 Ankita Sapm CIA II

http://slidepdf.com/reader/full/ankita-sapm-cia-ii 15/17

Security Analysis and Portfolio Management CIA -II

15 ANKITA RANKA 08D1064 -----BBM A-----FINANCE 1

R EASONS FOR INVESTMENT IN NS C

Compared with NSC, there is no ignoring the instrument's respectable returns,

which are not only assured, but also tax-exempt (under 80C) and government

guaranteed.

NSCs do not have a limit of how much one can invest. What's more, interest up to

Rs 1 lakh is tax-free. You read that correctly. NSCs offer you the possibility of

earning up to Rs 1 lakh fully tax-free.

Tax benefits are available on amounts invested in NSC under section 88, and

exemption can be claimed under section 80L for interest accrued on the NSC.

Interest accrued for any year can be treated as fresh investment in NSC for that

year and tax benefits can be claimed under section 88.

NSCs can be transferred from one person to another through the post office on the

payment of a prescribed fee.

The scheme has the backing of the Government of India so there are no risks

associated with your investment.

It is an investment with zero risk and assured returns.

8/8/2019 Ankita Sapm CIA II

http://slidepdf.com/reader/full/ankita-sapm-cia-ii 16/17

Security Analysis and Portfolio Management CIA -II

16 ANKITA RANKA 08D1064 -----BBM A-----FINANCE 1

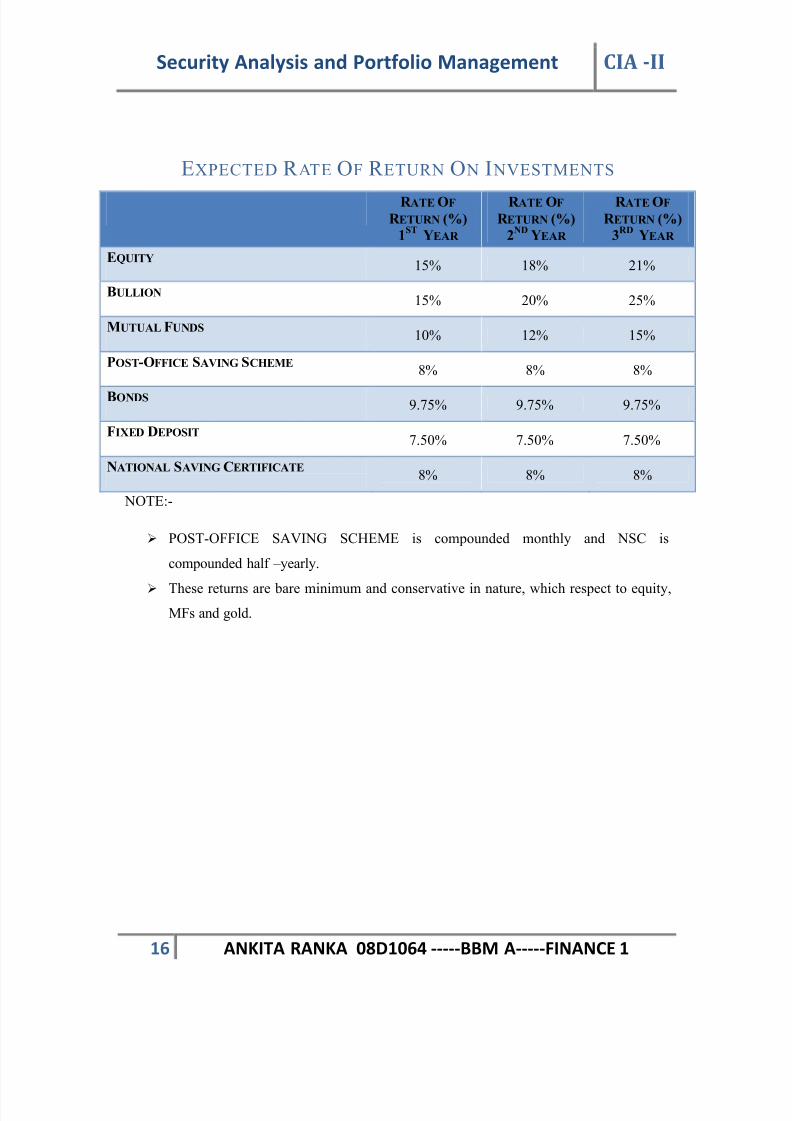

EXPECTED R ATE OF R ETURN O N I NVESTMENTS

R ATE OF

R ETURN (%)

1ST

YEAR

R ATE OF

R ETURN (%)

2ND

YEAR

R ATE OF

R ETURN (%)

3R D

YEAR

EQUITY 15% 18% 21%

BULLION 15% 20% 25%

MUTUAL FUNDS 10% 12% 15%

POST-OFFICE SAVING SCHEME 8% 8% 8%

BONDS 9.75% 9.75% 9.75%

FIXED DEPOSIT7.50% 7.50% 7.50%

NATIONAL SAVING CERTIFICATE 8% 8% 8%

NOTE:-

POST-OFFICE SAVING SCHEME is compounded monthly and NSC is

compounded half ±yearly.

These returns are bare minimum and conservative in nature, which respect to equity,

MFs and gold.

8/8/2019 Ankita Sapm CIA II

http://slidepdf.com/reader/full/ankita-sapm-cia-ii 17/17

Security Analysis and Portfolio Management CIA -II

17 ANKITA RANKA 08D1064 -----BBM A-----FINANCE 1

PORTFOLIO-OVERVIEW

The investment is widely classified into various financial instruments with the initial capital

30,00,000.00 with a varied risk appetite.

High risk (Client ± 1)

Moderate risk (Client ± 2)

Low risk (Client ± 3)

The diversification in the investment is done widely in 7 instruments which will give stability

to the short-term and long-term return for the portfolio. These instruments have a strong

presence in the market with good governance by their respective regulatory bodies.

Investments have been well spread in all avenues, having a heavy inclination towards equity

due to their good returns. Besides equity, the funds are also widely diversified in various

instruments when brings a degree of flexibility in our portfolio along with a good risk

management system.

Portfolio¶s is well designed in tandem with the micro and macro environment of the

economy, also keeping in mind the future uncertainties and inclinations of the economy.