Embed Size (px)

Citation preview

DOE/EIA-0383(97)Distribution Category UC-950

Annual Energy Outlook 1997

With Projections to 2015

December 1996

Energy Information AdministrationOffice of Integrated Analysis and Forecasting

U.S. Department of EnergyWashington, DC 20585

This report was prepared by the Energy Information Administration, the independent statisticaland analytical agency within the Department of Energy. The information contained hereinshould not be construed as advocating or reflecting any policy position of the Department ofEnergy or any other organization.

For Further Information . . .The Annual Energy Outlook 1997 (AEO97) was prepared by the Energy Information Administration(EIA), Office of Integrated Analysis and Forecasting, under the direction of Mary J. Hutzler([email protected], 202/586-2222). General questions may be addressed to Arthur T. Andersen([email protected], 202/586-1441), Director of the Energy Demand and Integration Division; ScottSitzer ([email protected], 202/586-2308), Director of the Energy Supply and Conversion Division; orAndy S. Kydes ([email protected], 202/586-2222), Senior Modeling Analyst. Detailed questions aboutthe forecasts and related model components may be addressed to the following analysts:

Overview, Emissions . . . . . . . . . . Susan H. Shaw ([email protected], 202/586-4838)Economic Activity . . . . . . . . . . . . Ronald Earley ([email protected], 202/586-1398)International Oil Markets . . . . . . G. Daniel Butler ([email protected], 202/586-9503)Residential Demand . . . . . . . . . . John Cymbalsky ([email protected], 202/586-4815)Commercial Demand . . . . . . . . . . Erin Boedecker ([email protected], 202/586-4791)Industrial Demand . . . . . . . . . . . T. Crawford Honeycutt ([email protected], 202-586-1420)Transportation Demand . . . . . . . David Chien ([email protected], 202/586-3994)Electricity Generation, Futures . . David Schoeberlein ([email protected], 202/586-2349)Electricity Prices, Deregulation . . Art Holland ([email protected], 202/586-2026)Nuclear Energy . . . . . . . . . . . . . . Laura Church ([email protected], 202/586-1494)Renewable Energy . . . . . . . . . . . Perry M. Lindstrom ([email protected], 202/586-0934)Oil and Gas Production . . . . . . . . Ted McCallister ([email protected], 202/586-4820)Natural Gas Markets . . . . . . . . . Phyllis Martin ([email protected], 202/586-9592)Natural Gas Regulations . . . . . . James Diemer ([email protected], 202/586-6126)Oil Refining and Markets . . . . . . Stacy MacIntyre ([email protected], 202/586-9795)Coal Supply and Prices . . . . . . . . Richard Newcombe ([email protected], 202/586-2415)

The AEO97 will be available on the EIA Home Page (http://www.eia.doe.gov/oiaf/aeo97/homepage.html) by January 1997, including text, forecast tables, and graphics. To download the tables or the entirepublication, go to the EIA FTP Site (ftp://ftp.eia.doe.gov/pub/forecasting/aeo97). Assumptions under-lying the projections and tables of regional and other detailed results will be available on the EIA HomePage by January 1997. AEO97, the assumptions, and the supplementary tables will be available onCD-ROM by February 1997. Forecast tables are available on diskette by contacting the Office ofScientific and Technical Information by telephone at 615/576-8401 or by mail at P.O. Box 62, Oak Ridge,TN 37831; they are also available through EIA’s Fax-on-Demand (see Appendix I).

Model documentation reports for the National Energy Modeling System (NEMS) are also available onCD-ROM. Quarterly projections of energy supply and demand for 1996 and 1997 are available in theShort-Term Energy Outlook (Fourth Quarter 1996). For ordering information and questions on otherenergy statistics available from EIA, please contact EIA’s National Energy Information Center.Addresses, telephone numbers, and hours are as follows:

National Energy Information Center, EI-231Energy Information AdministrationForrestal Building, Room 1F-048Washington, DC 20585

Telephone: 202/586-8800 E-mail: [email protected]: For people who are deaf World Wide Web Site: http://www.eia.doe.gov/

or hard of hearing: 202/586-1181 Gopher Site: gopher://gopher.eia.doe.gov/9 a.m. to 5 p.m., eastern time, M-F FTP Site: ftp://ftp.eia.doe.gov/

PrefaceThe Annual Energy Outlook 1997 (AEO97) presentsmidterm forecasts of energy supply, demand, andprices through 2015 prepared by the Energy Infor-mation Administration (EIA). These projections arebased on results of EIA’s National Energy ModelingSystem (NEMS).

This report begins with a summary of the referencecase, followed by a discussion of the legislativeassumptions and evolving legislative and regulatoryissues. “Issues in Focus” discusses emerging energyissues and other topics of particular interest. It isfollowed by the analysis of energy market trends.

The analysis in AEO97 focuses primarily on a refer-ence case and four other cases that assume higherand lower economic growth and higher and lowerworld oil prices than in the reference case. Forecasttables for these cases are provided in Appendixes Athrough C. Appendixes D and E present summariesof the reference case forecasts in units of oil equiva-lence and household energy expenditures. Twenty-three other cases explore the impacts of varying keyassumptions in NEMS—generally, technology pene-tration, with the major results shown in Appendix F.

Appendix G briefly describes NEMS and the majorAEO97 assumptions, with a summary table. Appen-dix H provides tables of energy conversion andmetric conversion factors. Appendix I presents

instructions for obtaining tables through the EIAFax-On-Demand system. AEO97 and the detailedassumptions will also be available on the EIA HomePage and on CD-ROM.

The AEO97 projections are based on Federal, State,and local laws and regulations in effect on October1, 1996. Pending legislation and sections of existinglegislation for which funds have not been appropri-ated are not reflected in the forecasts. The AEO97projections were prepared by using the most currentdata available as of July 31, 1996, when most 1995data but only partial 1996 data were available. His-torical data are presented for comparative purposes.Data documents referenced in the source notesshould be consulted for official values. The AEO97projections for 1996 and 1997 incorporate the short-term projections from EIA’s Short-Term EnergyOutlook (STEO), Fourth Quarter 1996, published inOctober 1996.

The AEO97 projections are used by Federal, State,and local governments, trade associations, and otherplanners and decisionmakers in the public and pri-vate sectors. They are published in accordance withSection 205c of the Department of Energy Organiza-tion Act of 1977 (Public Law 95-91), which requiresthe Administrator of EIA to prepare an annualreport that contains trends and projections of energyconsumption and supply.

The projections in AEO97 are not statements ofwhat will happen but of what might happen, giventhe assumptions and methodologies used. The pro-jections are business-as-usual trend forecasts,given known technology and demographic trendsand current laws and regulations, thus providinga policy-neutral reference case that can be used toanalyze policy initiatives. EIA does not propose,advocate, or speculate on future legislative andregulatory changes. All laws are assumed to re-main as currently enacted; however, the impacts ofemerging regulatory changes, when defined, arereflected.

Because energy markets are complex, models aresimplified representations of energy productionand consumption, regulations, and producer andconsumer behavior. The forecasts are highly de-pendent on the data, methodologies, model struc-tures, and assumptions used in their development.

Behavioral characteristics are indicative of real-world tendencies rather than representations ofspecific outcomes.

Energy market projections are subject to muchuncertainty. Many events which shape energymarkets are random and cannot be anticipated,including severe weather, political disruptions,strikes, and technological breakthroughs. In addi-tion, assumptions concerning future technology,demographics, and resources cannot be known withany degree of certainty. Many key uncertainties inthe AEO97 projections are addressed throughalternative cases.

EIA has endeavored to make these forecasts as ob-jective, reliable, and useful as possible, but theseprojections should serve as an adjunct to, not asubstitute for, the analytical process that should beused to examine policy initiatives.

ii Energy Information Administration/ Annual Energy Outlook 1997

ContentsPage

Administrator’s Message . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ix

Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Legislation and Regulations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Issues in Focus . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15Electricity Deregulation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Electricity Futures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Transportation Issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21Buildings Sector Issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25Effects of Oil and Gas Supply Technology on Natural Gas and Renewables Markets . . . . . . . . . . 26

Market Trends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31Key Assumptions in the Forecast . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

Trends in Economic Activity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32Economic Growth Cases . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33International Oil Markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

Energy Demand by End Use . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37Residential Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39Commercial Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40Industrial Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41Transportation Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43Energy Demand in Alternative Technology Cases . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

Electricity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48Sales . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48Generating Capacity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49Prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50Generation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51Nuclear Power . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52Alternative Cases . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53Electricity from Renewable Sources . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

Oil and Natural Gas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57Oil and Gas Prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57Oil and Gas Reserve Additions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58Natural Gas Production and Imports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59Natural Gas Consumption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60Natural Gas Prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61Oil and Gas Alternative Technology Cases . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62Oil Production and Consumption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64Petroleum Imports and Refining . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65Refined Petroleum Products . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

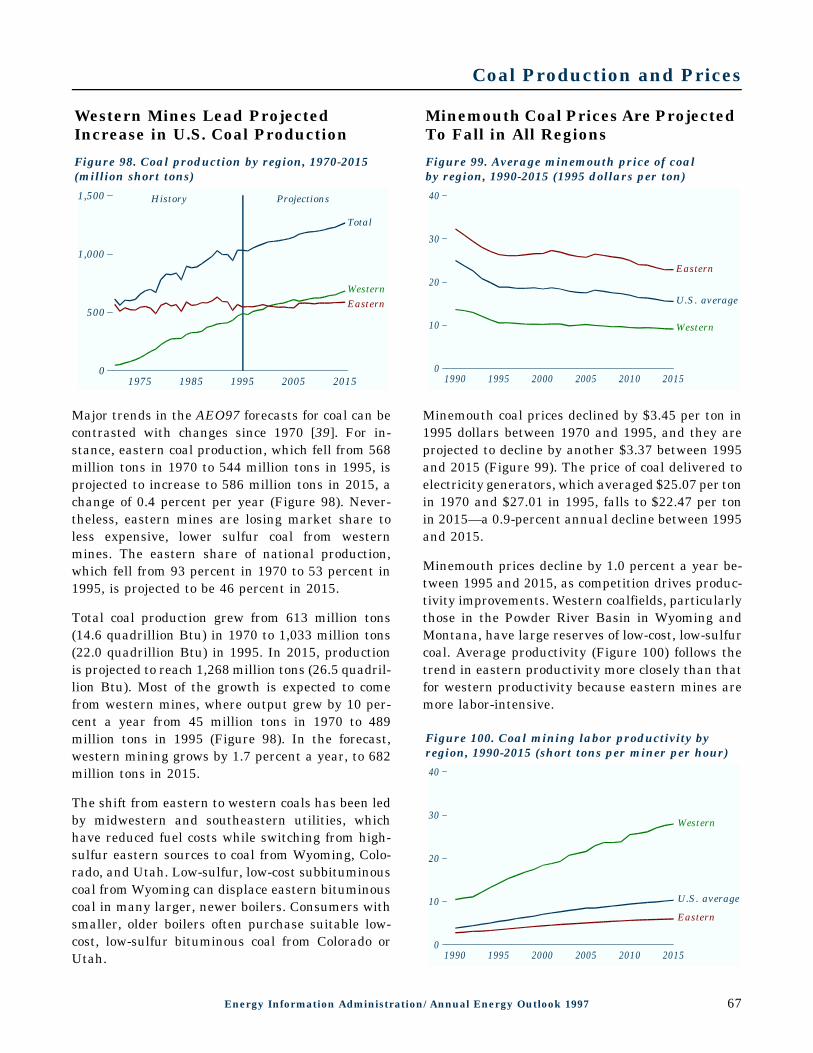

Coal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67Production and Prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67Coal Mining Labor Productivity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68Transportation Costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69Consumption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70Exports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71Clean Air Standards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

Emissions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72Carbon Emissions and Energy Use . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72Emissions from Electricity Generation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74

Energy Information Administration/ Annual Energy Outlook 1997 iii

Contents

PageForecast Comparisons . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

List of Acronyms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

Notes and Sources . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

AppendixesA. Reference Case Forecast . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96B. Economic Growth Case Comparisons . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 124C. Oil Price Case Comparisons . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152D. Crude Oil Equivalency Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 180E. Household Expenditures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 181F. Results from Side Cases . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 184G. Major Assumptions for the Forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 194H. Conversion Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 210I. EIA Fax-on-Demand . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 212

Index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 213

Tables

1. Summary of results for five cases . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62. NOx emissions standards under the Clean Air Act Amendments of 1990 . . . . . . . . . . . . . . . . . . . . 113. New car and light truck horsepower ratings and market shares, 1985, 1995, 2005, and 2015 . . . . . 434. Market shares of alternative-fuel light-duty vehicles by technology type, 2015 . . . . . . . . . . . . . . . . 445. Costs of producing electricity from new plants, 2000 and 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . 516. Economically recoverable oil and gas resources in 1990,

measured under different technology assumptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 577. Natural gas and crude oil drilling in three cases . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 588. Transmission and distribution revenues and margins, 1970, 1985, 1995, and 2015 . . . . . . . . . . . . 619. Components of residential and commercial natural gas end-use prices, 1985-2015 . . . . . . . . . . . . . 61

10. Representative average annual rates of technological progress in alternative technology cases . . . 6211. Petroleum consumption and net imports, 1995 and 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6512. Scrubber retrofits, allowance costs, and banked allowances, 2000-2015 . . . . . . . . . . . . . . . . . . . . . 7413. Forecasts of economic growth, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7614. Forecasts of world oil prices, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7615. Forecasts of average annual growth rates for energy consumption . . . . . . . . . . . . . . . . . . . . . . . . . 7716. Forecasts of average annual growth in residential and commercial energy demand . . . . . . . . . . . . 7717. Forecasts of average annual growth in industrial energy demand . . . . . . . . . . . . . . . . . . . . . . . . . 7718. Forecasts of average annual growth in transportation energy demand . . . . . . . . . . . . . . . . . . . . . . 7819. Comparison of electricity forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7920. Comparison of natural gas forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8021. Comparison of petroleum forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8222. Comparison of coal forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

Figures

1. Fuel price projections, 1995-2015: AEO96 and AEO97 compared . . . . . . . . . . . . . . . . . . . . . . . . . . 22. Energy production by fuel, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23. Net energy imports by fuel, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34. Energy consumption by fuel, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35. Electricity generation by fuel, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46. Energy use per capita and per dollar of gross domestic product, 1970-2015 . . . . . . . . . . . . . . . . . . 5

iv Energy Information Administration/ Annual Energy Outlook 1997

Contents

Figures (continued) Page

7. U.S. carbon emissions by sector and fuel, 1990-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58. Comparison of average natural gas transmission and distribution margins, 1970-2015 . . . . . . . . . 109. Nitrogen oxide emissions, 1994-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

10. Changes in oil consumption for transportation and other uses, 1980-2015 . . . . . . . . . . . . . . . . . . . 2211. Changes in carbon emissions, 1990-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2212. Trends in automobile fuel efficiency in the reference case, 1978-2015 . . . . . . . . . . . . . . . . . . . . . . 2213. Alternative-fuel vehicle shares of light-duty vehicle stock in two cases . . . . . . . . . . . . . . . . . . . . . . 2314. Trends in automobile fuel efficiency in the high efficiency case, 1978-2015 . . . . . . . . . . . . . . . . . . 2415. Changes from the reference case, assuming no increase in new car horsepower . . . . . . . . . . . . . . . 2416. Buildings sector energy prices, 1995 and 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2517. Buildings sector energy consumption in alternative price and efficiency cases . . . . . . . . . . . . . . . . 2618. Buildings sector carbon emissions in alternative price and efficiency cases . . . . . . . . . . . . . . . . . . 2619. Lower 48 natural gas wellhead prices in two alternative oil and gas technology cases,

1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2820. Lower 48 natural gas production in two alternative oil and gas technology cases, 1970-2015 . . . . . 2821. Lower 48 natural gas wellhead prices in alternative oil and gas technology cases, 1995-2015 . . . . 2822. Natural gas and coal use for electricity generation in two alternative oil and gas technology cases,

1995, 2005, and 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2923. Electricity generation from renewables in two alternative oil and gas technology cases, 2015 . . . . 2924. Average annual real growth rates of economic factors, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . 3225. Sectoral composition of GDP growth, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3226. Average annual real growth rates of economic factors in three cases, 1995-2015 . . . . . . . . . . . . . . 3327. Change in annual GDP growth rate for the preceding 20 years, 1966-2015 . . . . . . . . . . . . . . . . . . 3328. World oil prices in three cases, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3429. OPEC oil production in three cases, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3430. OPEC and non-OPEC oil production in two cases, 1990-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3531. Persian Gulf share of worldwide oil exports, 1965-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3532. U.S. petroleum imports by source, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3633. Worldwide refining capacity by region, 1996 and 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3634. Primary and delivered energy consumption, excluding transportation use, 1970-2015 . . . . . . . . . . 3735. Energy use per capita and per dollar of gross domestic product, 1970-2015 . . . . . . . . . . . . . . . . . . 3736. Energy use by fuel, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3837. Energy use by sector, 1975-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3838. Residential total energy consumption by fuel, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3939. Residential total energy consumption by end use, 1987, 1995, and 2015 . . . . . . . . . . . . . . . . . . . . 3940. Commercial nonrenewable total energy consumption by fuel, 1970-2015 . . . . . . . . . . . . . . . . . . . . 4041. Commercial total energy consumption by end use, 1995 and 2015 . . . . . . . . . . . . . . . . . . . . . . . . . 4042. Efficiencies of commercial electric water heaters in the reference case, 1995-2015 . . . . . . . . . . . . . 4143. Industrial total energy consumption by fuel, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4144. Industrial primary energy consumption by industry category, 1995-2015 . . . . . . . . . . . . . . . . . . . . 4245. Manufacturing energy intensity by component, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4246. Transportation energy consumption by fuel, 1975, 1995, and 2015 . . . . . . . . . . . . . . . . . . . . . . . . . 4347. Transportation stock fuel efficiency by mode, 1980-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4348. Alternative-fuel vehicle sales by type of demand, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4449. Alternative-fuel light-duty vehicle sales by fuel type, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . 4450. Variation from reference case primary energy use by sector in two alternative technology cases . . 4551. Variation from reference case primary residential energy use in three alternative cases,

1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

Energy Information Administration/ Annual Energy Outlook 1997 v

Contents

Figures (continued) Page

52. Changes in fuel and capital costs for selected residential appliances in the high technology case,1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

53. Capital investment and energy cost savings for residential appliancesin the high technology case, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

54. Variation from reference case primary commercial energy use in three alternative cases,1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

55. Industrial energy intensity in two alternative technology cases, 1995-2015 . . . . . . . . . . . . . . . . . . 4756. Changes in key components of the transportation sector in two alternative cases, 2015 . . . . . . . . . 4757. Population, gross domestic product, and electricity sales growth, 1960-2015 . . . . . . . . . . . . . . . . . 4858. Annual electricity sales by sector, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4859. New generating capacity and retirements, 1990-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4960. Electricity generation and cogeneration capacity additions by fuel type, 1995-2015 . . . . . . . . . . . . 4961. Fuel prices to electricity suppliers and electricity price, 1990-2015 . . . . . . . . . . . . . . . . . . . . . . . . 5062. Electric utility generator revenue requirements, 1990-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5063. Electricity generation costs, 2000 and 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5164. Electricity generation by fuel, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5165. Nuclear power plant capacity factors, 1973-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5266. Operable nuclear capacity in three cases, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5267. Cumulative new generating capacity by type in two cases, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . 5368. Cumulative new generating capacity by type in three cases, 1995-2015 . . . . . . . . . . . . . . . . . . . . . 5369. Cumulative new electricity generating capacity by technology type in three cases, 1995-2015 . . . . 5470. Grid-connected electricity generation from selected renewable fuels, 1995-2015 . . . . . . . . . . . . . . . 5471. Wind-powered electricity generating capacity by region, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . 5572. Levelized costs of electricity from wind power, 1990-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5573. Solar thermal and photovoltaic electricity generation, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . 5674. Electricity generating capacity from renewable sources, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . 5675. Lower 48 crude oil wellhead prices, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5776. U.S. petroleum consumption in five cases, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5777. Lower 48 natural gas wellhead prices, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5778. Successful new lower 48 natural gas and oil wells in three cases, 1970-2015 . . . . . . . . . . . . . . . . . 5879. Lower 48 natural gas reserve additions in three cases, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . 5880. Lower 48 oil reserve additions in three cases, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5881. Natural gas production by source, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5982. Natural gas production, consumption, and imports, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . 5983. Natural gas consumption in five cases, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6084. Pipeline capacity expansion by Census division, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6085. Pipeline capacity utilization by Census division, 1995 and 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . 6086. Natural gas end-use prices by sector, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6187. Wellhead share of natural gas end-use prices by sector, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . 6188. Lower 48 natural gas production and wellhead prices in the low economic growth case,

1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6289. Lower 48 natural gas wellhead prices in three cases, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . 6290. Lower 48 natural gas production in alternative technology cases, 1995-2015 . . . . . . . . . . . . . . . . . 6391. Lower 48 oil production in alternative technology cases, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . 6392. Crude oil production by source, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6493. Petroleum production, consumption, and imports, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6494. Share of U.S. petroleum consumption supplied by net imports, 1970-2015 . . . . . . . . . . . . . . . . . . . 6595. Domestic refining capacity, 1975-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6596. Change in petroleum products supplied in five cases, 1995 to 2015 . . . . . . . . . . . . . . . . . . . . . . . . 66

vi Energy Information Administration/ Annual Energy Outlook 1997

Contents

Figures (continued) Page

97. Components of refined product costs, 1995 and 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6698. Coal production by region, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6799. Average minemouth price of coal by region, 1990-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

100. Coal mining labor productivity by region, 1990-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67101. Labor cost component of minemouth coal prices, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68102. Average minemouth coal prices in three cases, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68103. Percent change in coal transportation costs in three cases, 1995-2015 . . . . . . . . . . . . . . . . . . . . . 69104. Variation from reference case projection of coal demand in 2015 in two alternative cases . . . . . . . 69105. Electricity and other coal consumption, 1970-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70106. Non-electricity coal consumption by sector, 1995, 2000, and 2015 . . . . . . . . . . . . . . . . . . . . . . . . . 70107. U.S. coal exports by destination, 1995, 2000, and 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71108. Coal distribution by sulfur content, 1995, 2000, and 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71109. Carbon emissions by sector, 1990-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72110. Carbon emissions per capita, 1990-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72111. Carbon emissions by fuel, 1990-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73112. Carbon emissions from electricity generation by fuel, 1990-2015 . . . . . . . . . . . . . . . . . . . . . . . . . 73113. Sulfur dioxide emissions from electricity generation, 1990-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . 74114. Nitrogen oxide emissions from electricity generation, 1995-2015 . . . . . . . . . . . . . . . . . . . . . . . . . 74

Energy Information Administration/ Annual Energy Outlook 1997 vii

Administrator’s MessageOnce again, in the Annual Energy Outlook 1997(AEO97), the Energy Information Administration(EIA) presents baseline projections of energy mar-kets for the use of our customers. These projectionsextend to the year 2015 and, in addition to thereference case, include a number of side analysesthat address some of the key uncertainties thatinfluence energy supply, demand, and prices.

Use of the Projections

The projections in AEO97 are generated from EIA’sNational Energy Modeling System (NEMS), whichexamines the total energy system, including allenergy-producing and consuming sectors and themost significant macroeconomic indicators thataffect or are affected by the energy system. Thisallows us to look at the complex interactions withinenergy markets—as examples, the impact of increas-ing energy demand on domestic and internationalsupplies and prices, or the economic tradeoffsbetween conventional fossil fuels and renewableenergy sources.

As important as the projections in AEO97 are to themany users of the report as forecasts of energy, evenmore important is its use as a baseline for policyanalysis. Here again, the total look at energy mar-kets is valuable, as NEMS is used to anticipate theimpacts of new or proposed policies. The directimpacts of policies are often obvious, but the magni-tude of those impacts and the indirect impacts arefrequently less obvious without the total view of theenergy system. For example, an initiative to stimu-late production of domestic oil and natural gaswould have the positive impact of lowering consumerprices for the fuels and reducing oil imports. How-ever, secondary effects would include reducing theincentive for more efficient energy-using equipmentand slowing the penetration of renewable sources ofenergy—ultimately increasing consumption and po-tentially harmful emissions. This total look enablesus to identify and quantify the most significant out-comes of policy initiatives.

The AEO97 projections extend to 2015. This 20-yearperiod is a time interval during which EIA believesthat the most important characteristics of energyconsumption and production are sufficiently wellunderstood for credible projections to be developed

in considerable detail. The longer view is significantfor several reasons. First, the impacts of energypolicies or new technologies often take a number ofyears to develop fully because of the gradual turn-over of the vast stock of energy-using and producingequipment and the gradual adaption to changingenergy prices. Second, the longer term projections,examined in conjunction with long historical trends,help us put short-term phenomena in perspective.Severe weather conditions, international politicalevents, and disruptions in domestic supplies all havehad significant, but short-term, impacts on the priceand availability of energy in the past several years.But such short-term events typically have little im-pact on the longer term trends presented in AEO97.Finally, by projecting energy markets for twodecades, the report can alert readers to futureissues, such as the likely retirement of a significantnumber of the Nation’s nuclear generating plantsand the need to replace them with new plants usingnatural gas, coal, or renewable fuels.

Limitations of the Projections

Recognizing the value of the AEO97 projections, wemust also be aware of and alert our readers to thelimitations of the projections. First, although we usethe term “forecast” interchangeably with “projec-tions,” we fully recognize that we cannot predict thefuture. There are too many underlying forces ofenergy markets that cannot be known with certain-ty. Also, in its role as a policy-neutral data andanalysis organization, EIA does not speculate onchanges in energy policy. For this analysis, weassume that all current policies and regulations willbe stable over the projection period. However, policywill be modified over a 20-year period, and thatalone is a significant reason for energy markets todevelop differently than the forecasts indicate. Theassumption of stable regulation leads to assumptionsas sweeping as assuming that the current regulatoryenvironment for the electricity industry will contin-ue and as simple, but still important, as assumingthat Federal gasoline taxes will remain unchanged.

In addition, the projections do not reflect short-termvolatility. Prices on the futures markets can shiftdramatically over several weeks or even days as aresult of short-term conditions. Although monthlyand annual averages serve to dampen the extent of

Energy Information Administration/ Annual Energy Outlook 1997 ix

Administrator’s Message

price movements or other short-term events, ex-treme conditions can cause actual markets to differfrom projections. To consider these possibilities, wepresent ranges for key energy variables, such asworld oil prices. While prices can move outside theseranges, it would most likely be for a short period oftime.

Users of this report also must be alerted to the factthat the projections employ many of the perspectivesand conventions of economics. The prices projectedin AEO97 are controlled for general levels of infla-tion. Thus, a level track of prices does not indicatethat prices would be unchanged but that they wouldincrease at the general level of inflation. Forexample, the average crude oil price is projected torise from about $17 a barrel in 1995 to $21 a barrelin 2015 in inflation-adjusted dollars, or 1995 realdollars. Accounting for likely inflation, the price in2015 would be about $39 per barrel.

Technology is another key dynamic in energy mar-kets. Over recent years, major improvements inenergy technologies have dramatically improved theefficiency of energy consumption and production. Atthe same time, new end uses of energy have devel-oped, and other uses, such as air-conditioning, havecontinued to penetrate. Because of the time it takesnew technologies to penetrate markets, it is fareasier to assess such penetration in the early yearsof the forecast period than in the more distant years.We project substantial improvements in technologythrough the forecast horizon, but the magnitude ofsuch improvements is particularly difficult to assessin the later years. Also, we do not project any break-through or substantially new technologies. Becauseof these uncertainties and because technology is soimportant in the use and production of energy,AEO97 presents a number of alternative cases thatexplore the impacts of slower or more rapid rates ofimprovement in technology or productivity thanthose assumed in the reference case.

As difficult as it is to project developments in energyin the United States, where the economy is relative-ly stable and valid data are readily available, it iseven more difficult to assess international trends,which increasingly have impacts on the UnitedStates. It has long been recognized that events inthe energy-exporting nations have profound effectson international energy supply and prices. Butincreasingly, attention is being focused on economicgrowth and related energy use in countries withoutthe developed infrastructure of the nations in theOrganization for Economic Cooperation and Develop-ment. In addition, although we assume sometechnological improvements in the internationalproduction of oil, our ability to assess technologicaldevelopments worldwide and their impacts ondomestic technology development is limited. Forfurther discussions of international energy develop-ments, readers are referred to the InternationalEnergy Outlook 1997, scheduled for publication inApril 1997.

Early Availability of AEO97

Early availability of the AEO results is a frequentrequest to EIA, and we are making an effort toaccelerate the release of all our data and analysispublications. As a result, AEO97 is being publisheda month earlier, in December 1996, still using thesame dates for historical data inputs and assump-tions about legislation and regulations. In addition,with continued growth in the use of EIA’s Internetsite, we have made the reference case results and asummary discussion available on our Home Page inNovember, at the time this report was released forprinting. We intend to continue this service to ourcustomers in the future.

Jay E. HakesAdministratorEnergy Information Administration

x Energy Information Administration/ Annual Energy Outlook 1997

Overview

Overview

Prices

The Annual Energy Outlook 1997 (AEO97) projectslower prices for all energy fuels than were projectedin AEO96 (Figure 1). Average world crude oil pricesin AEO97 are projected to be about $21 a barrel (in1995 dollars) in 2015, $5 lower than the AEO96price of $26 a barrel. The lower prices reflect expec-tations that oil production from the Organization ofPetroleum Exporting Countries (OPEC) will expandand that technology advances will sustain non-OPEC production. It is assumed that Iraqi oil pro-duction will not resume until 1998 and then willincrease gradually to full capacity in 2000.

1995 2000 2005 2010 20150

5

10

15

20

AEO97

AEO96

1995 2000 2005 2010 20150

1

2

3

AEO97

AEO96

1995 2000 2005 2010 20150

2

4

6

8 AEO96

AEO97

1995 2000 2005 2010 20150

10

20

30 AEO96

AEO97

Electricity(cents per kilowatthour)

Natural gas wellhead(dollars per thousand cubic feet)

Crude oil(dollars per barrel)

Coal minemouth(dollars per ton)

Figure 1. Fuel price projections, 1995-2015:AEO96 and AEO97 compared (1995 dollars)

The AEO97 average wellhead price of natural gas in2015 is $2.13 per thousand cubic feet, comparedwith $2.63 in AEO96, primarily as the result of a re-evaluation of the impacts of technological progresson oil and natural gas discovery. In AEO96, techno-logical progress was assumed to slow the decline infinding rates—reserves discovered per new well. InAEO97, technological progress arrests and even re-verses declining finding rates in some regions. As aresult, natural gas production is increased, with lessdrilling activity and at lower cost, particularly inoffshore regions, where technological progress has agreater impact on the development of relativelyimmature fields. In addition, competition within theindustry and projections of lower interest ratesreduce the costs of transmission and distribution,offsetting the projected increase in wellhead prices,so that the average delivered price of natural gasdeclines between 1995 and 2015 at an averageannual rate of 0.2 percent.

Coal minemouth prices are projected to decline inthe forecast as a result of increasing productivity, a

shift to western production, and competitive pres-sures on labor costs. In AEO97, the average mine-mouth price of coal is projected to be $15.46 per tonin 2015, compared with $17.75 in AEO96. Lowercoal transportation rates—leading to higher produc-tion from western mines, where production costs arelower than in the East—are the primary reason forthe lower minemouth prices.

Average electricity prices also decline through 2015and are lower than in AEO96. The average price in2015 is projected to be 6.3 cents per kilowatthour,compared with 7.1 cents in AEO96, as a result oflower projected fossil fuel prices and anticipatedindustry restructuring. Increased competition in theelectricity industry is assumed to lead to loweroperating and maintenance costs, lower general andadministrative costs, early retirement of inefficientunits, and other cost reductions. AEO97 reflects theevolving trend of competition within electricity mar-kets but does not include the full impacts of restruc-turing and deregulation. Although the projectionsinclude the recent actions taken by the FederalEnergy Regulatory Commission on open access,specific actions to be taken by State public utilitycommissions and their timing are not yet known andhave not been incorporated. Electricity industry re-structuring is discussed further on pages 16-19.

Production and Imports

As a result of lower projected oil prices, crude oilproduction in the United States is lower in theAEO97 forecast, declining to 5.2 million barrels aday in 2015 (Figure 2), compared with 5.8 millionbarrels a day in AEO96. On average, U.S. oil pro-duction declines by 1.1 percent a year between 1995and 2015, consistent with long-term historical

1975 1985 1995 2005 20150

10

20

30

Coal

Natural gas

Nonhydrorenewablesand other

Nuclear

Petroleum

Hydro

History Projections

Figure 2. Energy production by fuel, 1970-2015(quadrillion Btu)

2 Energy Information Administration/ Annual Energy Outlook 1997

Overview

trends. Advances in oil discovery technologies areexpected to be insufficient to offset declining re-sources.

Declining production and rising consumption lead togrowing reliance on petroleum imports through 2015(Figure 3). The share of petroleum consumption metby net imports rises from 44 percent in 1995 (meas-ured in barrels per day) to 61 percent in 2015.

1975 1985 1995 2005 2015

0

10

20

30

0

-10

Coal

Natural gas

Petroleum

History Projections

Figure 3. Net energy imports by fuel, 1970-2015(quadrillion Btu)

Natural gas production is projected to increase at anaverage annual rate of 1.7 percent between 1995and 2015 to meet most of the growing demand forgas. In 2015, production is estimated to reach 26.1trillion cubic feet, compared to 18.5 trillion cubic feetin 1995. Net imports of natural gas, primarily fromCanada, also increase by 1.6 trillion cubic feet by2015 due to assumed growth and higher utilizationof pipeline capacity coupled with abundant suppliesof Canadian gas available at competitive prices.

Coal production increases by 1.0 percent a yearthrough 2015, from 1,033 million tons in 1995 to1,268 million in 2015. Most of the increase resultsfrom increasing domestic consumption. In addition,export demand is projected to rise through 2015.Exports of steam coal will primarily serve expandingmarkets for electricity generation in Europe andAsia, and some growth in metallurgical coal exportsto Asia is also projected in response to increasingdemand for steel.

With lower prices projected for all fuels, renewableenergy production, including hydropower, is 0.8quadrillion British thermal units (Btu) lower in theAEO97 forecast in 2015 than it was in AEO96. Low-er prices, particularly for natural gas, delay the pen-etration of some renewable technologies. Renewable

energy production, including hydropower, is project-ed to reach 7.7 quadrillion Btu in 2015, up from 6.3quadrillion Btu in 1995. More than half the in-crease, 0.8 quadrillion Btu, is biomass used byindustry and electricity generators, and most of therest is geothermal, municipal solid waste, and wind.

Consumption

The lower energy prices in AEO97 than in AEO96result in higher total consumption in 2015—111quadrillion Btu, compared with 108 quadrillion Btuin AEO96. Both industrial and transportation de-mand are higher, with stronger economic growthand higher projected travel.

Residential demand is the same in AEO97 as inAEO96. The lower prices are offset by more mobileand multifamily homes, improvements in shell andequipment efficiencies, and more conversions fromoil and conventional resistance heating to higherefficiency heating. Commercial demand is onlyslightly higher than in AEO96, because the lowerprices are mostly offset by improvements in lightingand in building shells for new construction, and bya 4 percent lower estimate of floorspace in 2015.

Natural gas consumption increases by an average of1.7 percent a year (Figure 4), mainly because ofgrowth in gas-fired electricity generation. Gas con-sumption by electric generators, excluding cogenera-tors, is projected to increase from 3.5 trillion cubicfeet in 1995 to 8.5 trillion cubic feet in 2015. Gasconsumption in the industrial sector, which includescogenerators, increases by 1.3 trillion cubic feet.Combined, by 2015 the residential and commercialsectors contribute 1.2 trillion cubic feet to theincreased use of gas.

1975 1985 1995 2005 20150

10

20

30

40

50

Coal

Natural gas

Nonhydrorenewablesand other

Nuclear

Petroleum

History Projections

Hydro

Figure 4. Energy consumption by fuel, 1970-2015(quadrillion Btu)

Energy Information Administration/ Annual Energy Outlook 1997 3

Overview

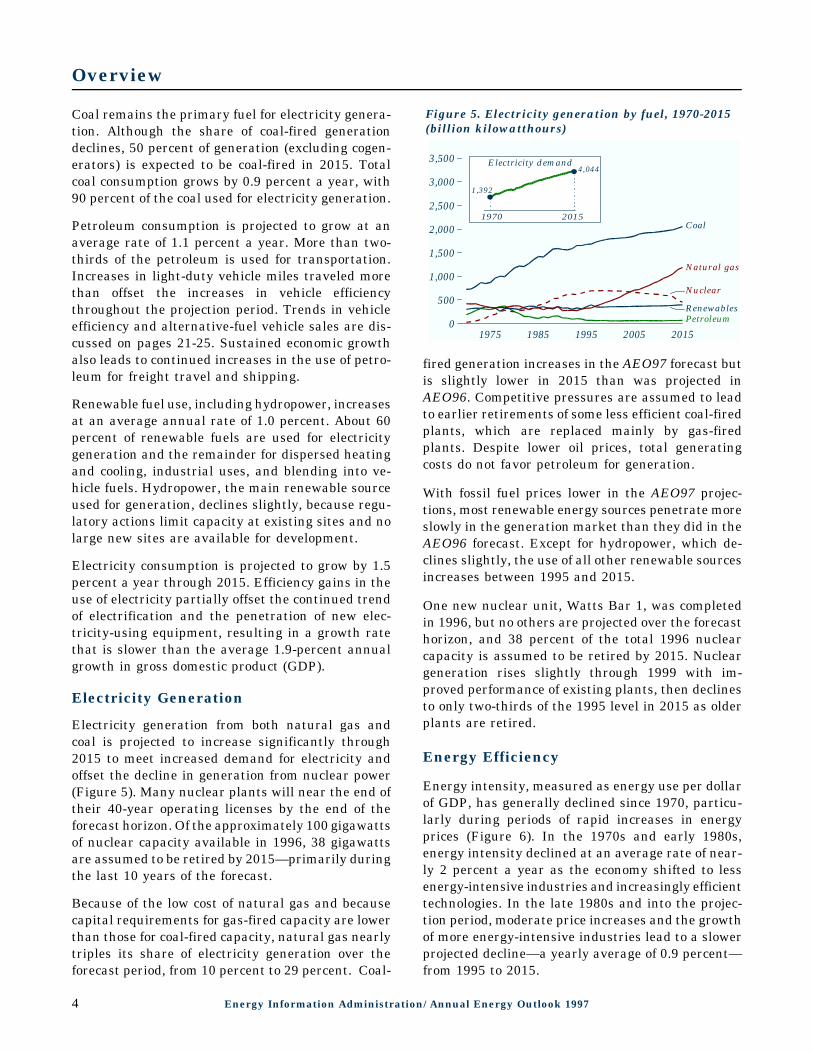

Coal remains the primary fuel for electricity genera-tion. Although the share of coal-fired generationdeclines, 50 percent of generation (excluding cogen-erators) is expected to be coal-fired in 2015. Totalcoal consumption grows by 0.9 percent a year, with90 percent of the coal used for electricity generation.

Petroleum consumption is projected to grow at anaverage rate of 1.1 percent a year. More than two-thirds of the petroleum is used for transportation.Increases in light-duty vehicle miles traveled morethan offset the increases in vehicle efficiencythroughout the projection period. Trends in vehicleefficiency and alternative-fuel vehicle sales are dis-cussed on pages 21-25. Sustained economic growthalso leads to continued increases in the use of petro-leum for freight travel and shipping.

Renewable fuel use, including hydropower, increasesat an average annual rate of 1.0 percent. About 60percent of renewable fuels are used for electricitygeneration and the remainder for dispersed heatingand cooling, industrial uses, and blending into ve-hicle fuels. Hydropower, the main renewable sourceused for generation, declines slightly, because regu-latory actions limit capacity at existing sites and nolarge new sites are available for development.

Electricity consumption is projected to grow by 1.5percent a year through 2015. Efficiency gains in theuse of electricity partially offset the continued trendof electrification and the penetration of new elec-tricity-using equipment, resulting in a growth ratethat is slower than the average 1.9-percent annualgrowth in gross domestic product (GDP).

Electricity Generation

Electricity generation from both natural gas andcoal is projected to increase significantly through2015 to meet increased demand for electricity andoffset the decline in generation from nuclear power(Figure 5). Many nuclear plants will near the end oftheir 40-year operating licenses by the end of theforecast horizon. Of the approximately 100 gigawattsof nuclear capacity available in 1996, 38 gigawattsare assumed to be retired by 2015—primarily duringthe last 10 years of the forecast.

Because of the low cost of natural gas and becausecapital requirements for gas-fired capacity are lowerthan those for coal-fired capacity, natural gas nearlytriples its share of electricity generation over theforecast period, from 10 percent to 29 percent. Coal-

1975 1985 1995 2005 20150

500

1,000

1,500

2,000

2,500

3,000

3,500

Coal

Natural gas

Renewables

Nuclear

Petroleum

1970 2015

Electricity demand

1,392

4,044

Figure 5. Electricity generation by fuel, 1970-2015(billion kilowatthours)

fired generation increases in the AEO97 forecast butis slightly lower in 2015 than was projected inAEO96. Competitive pressures are assumed to leadto earlier retirements of some less efficient coal-firedplants, which are replaced mainly by gas-firedplants. Despite lower oil prices, total generatingcosts do not favor petroleum for generation.

With fossil fuel prices lower in the AEO97 projec-tions, most renewable energy sources penetrate moreslowly in the generation market than they did in theAEO96 forecast. Except for hydropower, which de-clines slightly, the use of all other renewable sourcesincreases between 1995 and 2015.

One new nuclear unit, Watts Bar 1, was completedin 1996, but no others are projected over the forecasthorizon, and 38 percent of the total 1996 nuclearcapacity is assumed to be retired by 2015. Nucleargeneration rises slightly through 1999 with im-proved performance of existing plants, then declinesto only two-thirds of the 1995 level in 2015 as olderplants are retired.

Energy Efficiency

Energy intensity, measured as energy use per dollarof GDP, has generally declined since 1970, particu-larly during periods of rapid increases in energyprices (Figure 6). In the 1970s and early 1980s,energy intensity declined at an average rate of near-ly 2 percent a year as the economy shifted to lessenergy-intensive industries and increasingly efficienttechnologies. In the late 1980s and into the projec-tion period, moderate price increases and the growthof more energy-intensive industries lead to a slowerprojected decline—a yearly average of 0.9 percent—from 1995 to 2015.

4 Energy Information Administration/ Annual Energy Outlook 1997

Overview

1975 1985 1995 2005 20150.0

0.2

0.4

0.6

0.8

1.0

1.2Energyuse percapita

Energyuse perdollarof GDP

History Projections

Figure 6. Energy use per capita and per dollar ofgross domestic product, 1970-2015 (index, 1970 = 1)

Energy use per person, which also declined from1970 through the mid-1980s, rose in the mid-1980sas energy prices dropped. Per capita energy use isexpected to remain nearly stable through 2015 andbelow the high in the early 1970s, as efficiency gainsoffset higher demand for energy services.

AEO97 incorporates the efficiency standards for newenergy-using equipment in buildings and for motorsmandated through 1994 by the National ApplianceEnergy Conservation Act of 1987 and the EnergyPolicy Act of 1992. Additional improvements in theefficiency of energy-using technologies beyond thestandards are likely. Several alternative cases inAEO97 examine the impact of the penetration ofmore energy-efficient technologies in the end-usesectors beyond that projected in the reference case.

Carbon Emissions

Carbon emissions from energy use are projected toincrease by 1.2 percent a year through 2015, reach-ing 1,799 million metric tons (Figure 7), comparedwith the AEO96 projection of 1,735 million metrictons. The higher emissions projections are the resultof higher total energy consumption and lower pene-tration of renewable energy sources.

Higher projected economic growth in AEO97 andlower use of renewables contribute to higher carbonemissions in the industrial sector. Emissions arealso higher in the transportation sector, as strongereconomic growth and lower fuel prices boost person-al and freight travel and fuel consumption. Emis-sions in the residential and commercial sectors areonly slightly higher.

19901990 20002000 20102010 2015201500

500

1,000

1,500

2,000 IndustrialCommercial

Residential

Transportation

Natural gas

Coal

Petroleum

1990 2000 2010 2015

}}}

Figure 7. U.S. carbon emissions by sector and fuel,1990-2015 (million metric tons)

Over the forecast horizon, 40 percent of the increasein emissions results from the transportation sector,where increases in travel are projected for all modes.The industrial sector accounts for 28 percent of theincrease. The sectoral values in Figure 7 includeemissions from the generation of electricity used ineach sector. Although part of the growth in emis-sions from electricity generation results from thereplacement of nuclear power by fossil-fired genera-tion, the increased use of natural gas relative to coalmoderates the growth in emissions.

The Climate Change Action Plan (CCAP) was devel-oped to stabilize greenhouse gas emissions in 2000at 1990 levels. In 1990, carbon emissions from ener-gy use were estimated to be about 1,340 millionmetric tons. AEO97 analyzes the impacts of CCAPprovisions, including Climate Challenge and ClimateWise, which foster voluntary reductions in emissionsby electric utilities and industry. The first report onvoluntary programs, Voluntary Reporting of Green-house Gases 1995, was released in July 1996 [1].That report documents the Climate Wise and Cli-mate Challenge commitments.

Emissions grew more rapidly than expected in theearly 1990s, partly due to lower than expectedgrowth in energy prices, which is projected tocontinue through 2015. That trend, combined withfunding reductions for some CCAP programs, leadsto higher projected emissions than were estimated atthe time CCAP was formulated. The impacts ofadditional efforts that may be undertaken to curtailemissions are not analyzed in these projections.Further discussion of carbon emissions, as well asother emissions, begins on page 72.

Energy Information Administration/ Annual Energy Outlook 1997 5

Overview

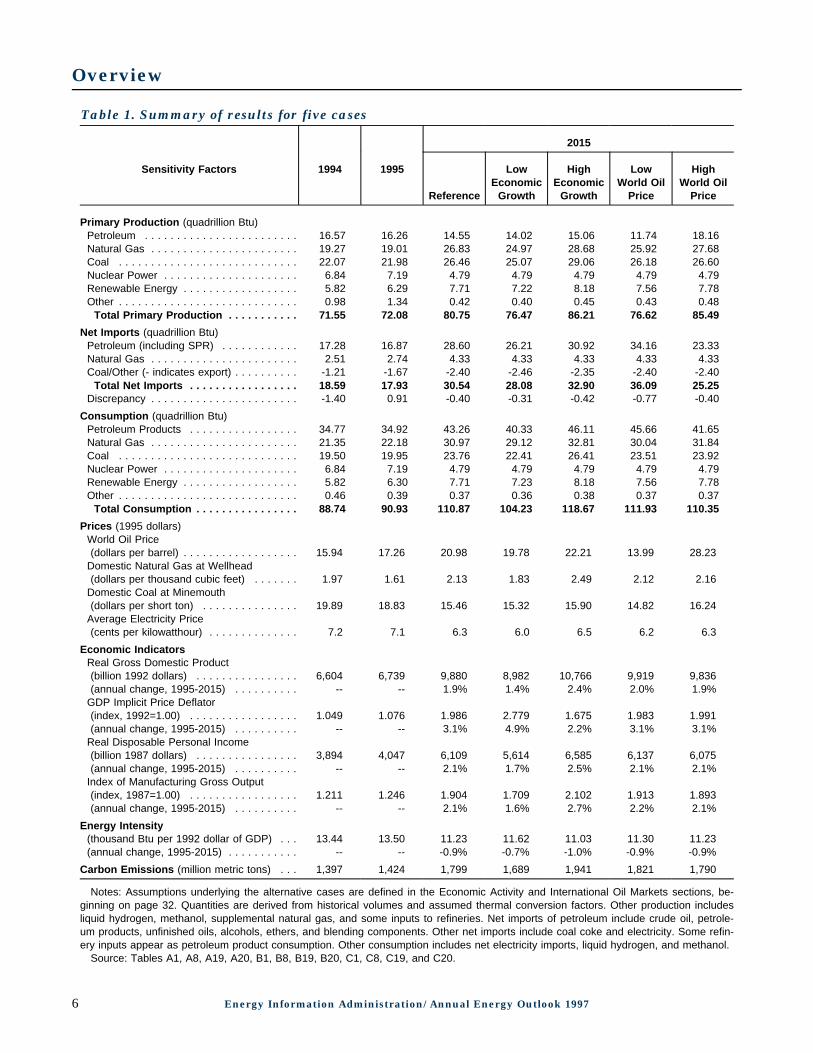

Table 1. Summary of results for five cases

Sensitivity Factors 1994 1995

2015

Reference

LowEconomic

Growth

HighEconomic

Growth

LowWorld Oil

Price

HighWorld Oil

Price

Primary Production (quadrillion Btu)Petroleum . . . . . . . . . . . . . . . . . . . . . . . . 16.57 16.26 14.55 14.02 15.06 11.74 18.16Natural Gas . . . . . . . . . . . . . . . . . . . . . . . 19.27 19.01 26.83 24.97 28.68 25.92 27.68Coal . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22.07 21.98 26.46 25.07 29.06 26.18 26.60Nuclear Power . . . . . . . . . . . . . . . . . . . . . 6.84 7.19 4.79 4.79 4.79 4.79 4.79Renewable Energy . . . . . . . . . . . . . . . . . . 5.82 6.29 7.71 7.22 8.18 7.56 7.78Other . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.98 1.34 0.42 0.40 0.45 0.43 0.48

Total Primary Production . . . . . . . . . . . 71.55 72.08 80.75 76.47 86.21 76.62 85.49

Net Imports (quadrillion Btu)Petroleum (including SPR) . . . . . . . . . . . . 17.28 16.87 28.60 26.21 30.92 34.16 23.33Natural Gas . . . . . . . . . . . . . . . . . . . . . . . 2.51 2.74 4.33 4.33 4.33 4.33 4.33Coal/Other (- indicates export) . . . . . . . . . . -1.21 -1.67 -2.40 -2.46 -2.35 -2.40 -2.40

Total Net Imports . . . . . . . . . . . . . . . . . 18.59 17.93 30.54 28.08 32.90 36.09 25.25Discrepancy . . . . . . . . . . . . . . . . . . . . . . . -1.40 0.91 -0.40 -0.31 -0.42 -0.77 -0.40

Consumption (quadrillion Btu)Petroleum Products . . . . . . . . . . . . . . . . . 34.77 34.92 43.26 40.33 46.11 45.66 41.65Natural Gas . . . . . . . . . . . . . . . . . . . . . . . 21.35 22.18 30.97 29.12 32.81 30.04 31.84Coal . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19.50 19.95 23.76 22.41 26.41 23.51 23.92Nuclear Power . . . . . . . . . . . . . . . . . . . . . 6.84 7.19 4.79 4.79 4.79 4.79 4.79Renewable Energy . . . . . . . . . . . . . . . . . . 5.82 6.30 7.71 7.23 8.18 7.56 7.78Other . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.46 0.39 0.37 0.36 0.38 0.37 0.37

Total Consumption . . . . . . . . . . . . . . . . 88.74 90.93 110.87 104.23 118.67 111.93 110.35

Prices (1995 dollars)World Oil Price(dollars per barrel) . . . . . . . . . . . . . . . . . . 15.94 17.26 20.98 19.78 22.21 13.99 28.23

Domestic Natural Gas at Wellhead(dollars per thousand cubic feet) . . . . . . . 1.97 1.61 2.13 1.83 2.49 2.12 2.16

Domestic Coal at Minemouth(dollars per short ton) . . . . . . . . . . . . . . . 19.89 18.83 15.46 15.32 15.90 14.82 16.24

Average Electricity Price(cents per kilowatthour) . . . . . . . . . . . . . . 7.2 7.1 6.3 6.0 6.5 6.2 6.3

Economic IndicatorsReal Gross Domestic Product(billion 1992 dollars) . . . . . . . . . . . . . . . . 6,604 6,739 9,880 8,982 10,766 9,919 9,836(annual change, 1995-2015) . . . . . . . . . . -- -- 1.9% 1.4% 2.4% 2.0% 1.9%

GDP Implicit Price Deflator(index, 1992=1.00) . . . . . . . . . . . . . . . . . 1.049 1.076 1.986 2.779 1.675 1.983 1.991(annual change, 1995-2015) . . . . . . . . . . -- -- 3.1% 4.9% 2.2% 3.1% 3.1%

Real Disposable Personal Income(billion 1987 dollars) . . . . . . . . . . . . . . . . 3,894 4,047 6,109 5,614 6,585 6,137 6,075(annual change, 1995-2015) . . . . . . . . . . -- -- 2.1% 1.7% 2.5% 2.1% 2.1%

Index of Manufacturing Gross Output(index, 1987=1.00) . . . . . . . . . . . . . . . . . 1.211 1.246 1.904 1.709 2.102 1.913 1.893(annual change, 1995-2015) . . . . . . . . . . -- -- 2.1% 1.6% 2.7% 2.2% 2.1%

Energy Intensity(thousand Btu per 1992 dollar of GDP) . . . 13.44 13.50 11.23 11.62 11.03 11.30 11.23(annual change, 1995-2015) . . . . . . . . . . . -- -- -0.9% -0.7% -1.0% -0.9% -0.9%

Carbon Emissions (million metric tons) . . . 1,397 1,424 1,799 1,689 1,941 1,821 1,790

Notes: Assumptions underlying the alternative cases are defined in the Economic Activity and International Oil Markets sections, be-ginning on page 32. Quantities are derived from historical volumes and assumed thermal conversion factors. Other production includesliquid hydrogen, methanol, supplemental natural gas, and some inputs to refineries. Net imports of petroleum include crude oil, petrole-um products, unfinished oils, alcohols, ethers, and blending components. Other net imports include coal coke and electricity. Some refin-ery inputs appear as petroleum product consumption. Other consumption includes net electricity imports, liquid hydrogen, and methanol.

Source: Tables A1, A8, A19, A20, B1, B8, B19, B20, C1, C8, C19, and C20.

6 Energy Information Administration/ Annual Energy Outlook 1997

Legislation andRegulations

Legislation and Regulations

Because EIA analyses are required to remain policy-neutral, the AEO97 projections assume that Federal,State, and local laws and regulations in effect onOctober 1, 1996, remain unchanged through 2015.The impacts of pending or proposed legislation andsections of existing legislation for which funds havenot been appropriated are not reflected in the projec-tions.

Federal legislation incorporated in the projectionsincludes the Omnibus Budget Reconciliation Act of1993, which adds 4.3 cents per gallon [2] to theFederal tax on highway fuels; the Clean Air ActAmendments of 1990 (CAAA90); and the EnergyPolicy Act of 1992 (EPACT). The provisions ofEPACT are focused primarily on reducing energy de-mand, requiring minimum building efficiency stand-ards for Federal buildings and other new buildingsthat receive federally backed mortgages. Efficiencystandards for electric motors, lights, and otherequipment are required, and owners of fleets ofautomobiles and trucks are required to phase invehicles that do not rely on petroleum products.

CAAA90 requires a phased reduction in vehicleemissions of regulated pollutants, to be met pri-marily through the use of reformulated gasoline. Inaddition, under CAAA90, annual emissions of sulfurdioxide by electricity generators are, in general,capped at 8.9 million short tons a year in 2000 andthereafter, although banking of allowances fromearlier years is permitted. CAAA90 also calls for theU.S. Environmental Protection Agency (EPA) toissue standards for the reduction of nitrogen oxide(NOx) emissions, leading to regulations that imposelimits on electricity generators for NOx emissions.The impacts of CAAA90 on electricity generators arediscussed on page 74. NOx emissions regulations arediscussed below.

Climate Change Action Plan

The AEO97 projections include analysis of provisionsof the Climate Change Action Plan (CCAP), 44 ac-tions developed by the Clinton Administration toachieve the stabilization of greenhouse gas emis-sions (carbon dioxide, methane, nitrous oxide, andothers) in the United States at 1990 levels by 2000.Energy combustion is the primary source of anthro-pogenic (human-caused) carbon emissions. AEO97estimates of emissions from fuel combustion do not

include emissions from activities other than fuelcombustion, such as landfills and agriculture, nor dothey take into account sinks that absorb carbon,such as forests. Of the 44 CCAP actions, 13 are notrelated to energy fuels and are not incorporated inthe analysis. The projections do not include addi-tional steps that might be taken in response to therecent call by Timothy Wirth, Under Secretary ofState for Global Affairs, for binding internationalagreements.

Climate Wise and Climate Challenge are two pro-grams cosponsored by EPA and the U.S. Departmentof Energy to foster voluntary reductions in emissionson the part of industry and electricity generators.These programs are new and are only beginning tohave effects, as reported in the EIA publicationVoluntary Reporting of Greenhouse Gases 1995 [3].AEO97 includes analysis of the impacts of bothprograms (see Appendix G).

Recent Actions

Legislation lifting a ban on exports of Alaskan crudeoil was signed on November 28, 1995. With the ex-ception of limited trade agreements, export of NorthSlope crude oil had been banned since 1973. Al-though this legislation passed late in 1995, theimpacts were included in AEO96. With the exportban removed, it is expected that Alaskan crude oilwill be exported to the Pacific Rim—primarily toJapan. It is projected that 100,000 barrels per daywill be shipped in 1997, declining to 70,000 barrelsin 1999. Exports of less than 50,000 barrels per dayare expected to continue through the remainder ofthe forecast.

The Outer Continental Shelf Deep Water RoyaltyRelief Act was also enacted on November 28, 1995.This legislation gives the Secretary of the Interiorauthority to suspend royalty requirements on newoil and gas production from qualifying existingleases—generally, production in most deep areas ofthe Gulf of Mexico that would not be economicalwithout royalty relief. It also requires that royaltypayments be waived on new leases sold in the next5 years for production in most of the deep Gulf.Although a representation of this legislation isincluded for the first time in the analytical frame-work underlying AEO97, the projected impacts oncrude oil and natural gas production are small.

8 Energy Information Administration/ Annual Energy Outlook 1997

Legislation and Regulations

Within the past year, Congressional action was initi-ated to allow leasing of the 1.5-million-acre coastalplain of the Arctic National Wildlife Refuge for oiland gas drilling and to suspend the 4.3-cents-per-gallon tax on highway fuels added in 1993. Neithereffort has resulted in signed legislation. Therefore,these changes are not included in the projections.

Recent actions by the Federal Energy RegulatoryCommission (FERC) foster alternative ratemakingby the natural gas industry and efficient capacityrelease, leading to a more efficient market. FERCalso issued Orders 888 and 889, providing openaccess to interstate transmission lines in electricitymarkets, a major step toward restructuring of theelectricity industry. The impacts of these actions onthe natural gas and electricity industries are dis-cussed below.

Natural Gas Regulatory Actions

The natural gas industry has witnessed major regu-latory and legislative changes during the pastseveral years [4]. Some of the regulatory changeshave allowed market forces to govern rate and serv-ice levels in areas of the industry where traditionalregulatory oversight was previously in effect. Recentregulatory actions have continued to expose moreaspects of the industry to market forces and haveincreased the options for interstate pipeline compa-nies and shippers.

An alternative rate policy paper issued by FERC onJanuary 31, 1996, provided interstate pipeline com-panies with the criteria for approval of applicationsfor rates other than the traditional cost-of-servicerates for transportation service. Options for alter-native rates include market-based rates (customer-driven, based on rates for competing services),negotiated rates (negotiated individually with eachcustomer), and incentive rates (determined by theachievement of target goals, such as improved effi-ciency or improved customer satisfaction relative tosome specific index).

Issuance of the policy statement indicates FERC’srecognition that additional rate design flexibilitymay be needed in the restructured environment. Forinstance, pipeline companies may need rate designflexibility to market, and recover the costs associ-ated with, excess capacity (capacity over and abovethat which is subscribed to by customers). FERC

will evaluate requests for alternative rates on acase-by-case basis.

In addition to its policy statement on alternativeratemaking methods, FERC has established a formalregulatory proceeding in which it will consider aproposal to allow pipeline companies to negotiateservice terms and conditions. Negotiating terms andconditions may allow pipeline companies to tailorservices to meet their customers’ specific needs.

FERC is also providing pipeline companies withflexibility in their access to markets. In an Orderissued on January 31, 1996 [5], FERC clarified thatOrder 636 does not prohibit interstate pipeline com-panies from obtaining capacity on other pipelines[6]. FERC cites at least two benefits of pipelinecompanies holding capacity on other pipelines. First,it would allow the pipeline companies to provideshippers access to new supply and market areas.Second, it would reduce the administrative burdenof shippers having to deal with several pipelinecompanies to secure the flow paths they desire.

On July 31, 1996, FERC issued a Notice of ProposedRulemaking (NOPR) that eliminates the require-ment for competitive bidding and price constraintson released capacity (unused firm capacity that ismade available for resale on the secondary, orcapacity release, market) in some instances. Thenotice also requires pipeline companies to havecomparable procedures for procuring released ca-pacity, interruptible, and short-term service (servicenot held under long-term contract and generally forless than 30 days). In the notice, FERC proposes todiscontinue the current bidding requirements in aneffort to end the uncertainty and delay that someshippers have experienced before they may use thereleased capacity. FERC is also proposing to removethe price cap for released, interruptible, and short-term firm capacity when releasing shippers andpipeline companies can demonstrate that they areunable to exercise market power.

In addition to making these services more compar-able, the removal of the price cap will enable releas-ing shippers and pipeline companies to sell thecapacity at market prices. Shippers releasing capac-ity may also be able to recover more of their firmcapacity costs, making this secondary (resale) mar-ket more attractive.

Energy Information Administration/ Annual Energy Outlook 1997 9

Legislation and Regulations

At the State level, unbundling is also making con-siderable inroads. Unbundled sales and delivery ser-vices for large industrial and electricity generatorcustomers are now commonplace, and State regula-tors are experimenting with various methods toextend choice to small customers. Some regulatorsare making provisions to allow third-party market-ers to aggregate the gas needs of smaller residentialand commercial customers so that these customerscan exercise choice in gas markets. A number ofStates have announced pilot projects in which par-ticipating residential customers may choose theirgas suppliers. All of these changes are driven by thedesire of regulators to give customers access to gasservices that meet individual needs in the best wayand at the least cost.

An unintended impact on consumer prices some-times occurs as the result of taxes during the re-structuring of public utility industries. When finalconsumers purchase gas and transportation servicesfrom parties other than the locally franchised pro-vider, they may avoid paying some or all of theState and local taxes that would have been collectedon a sale had it been made by the traditional pro-vider. This sometimes makes it less expensive topurchase services from third-party, out-of-Statevendors, even when the vendor’s prices before taxesare higher than the traditional provider’s. Manyjurisdictions are now trying to remedy both the com-petitive and the revenue impacts of these taxes byreplacing franchise and public utility sales taxeswith energy importation or consumption taxes.

All of these changes tend to reduce the price of gasto end-use consumers, and projected transmissionand distribution margins (costs the customers payfor transmission and distribution services) decline atan even greater rate than was projected in AEO96(Figure 8). Other factors that have contributed tothe decline in the projected average margin arechanges in the mix of end uses and changes in capi-tal costs. While changes in the mix of end uses aresimilar in both AEO96 and AEO97, a significant re-duction in the cost of capital as a result of projectedlower interest rates is reflected in AEO97. This re-duction contributes to a decline in transmission anddistribution margins over the forecast period, withprojected margins in 2015 almost 20 percent lowerthan those projected in AEO96.

1975 1985 1995 2005 2015 10

1

2

3

4

5

6

Residential

Commercial

WeightedaverageIndustrial

History Projections

Electricitygenerators

Figure 8. Comparison of average natural gastransmission and distribution margins, 1970-2015(1995 dollars)

The greatest decline in margins is seen in the resi-dential and commercial sectors, which consist pre-dominantly of core customers who depend on firmtransportation service. Declines in margins in bothof these sectors are about 30 percent between 1995and 2015. Margins in these two sectors include sig-nificant distribution costs, which are heavily influ-enced by interest rates, inasmuch as approximately40 percent of the distribution costs is assumed to berelated to the cost of capital. Industrial customersand electricity generators generally incur smalldistribution costs because they place a low burdenon the system relative to the large volumes theypurchase, or because they obtain their natural gasdirectly from the pipelines, bypassing the distri-bution segment of the market. Thus, they do not seethe declines that are seen in the other sectors.

Nitrogen Oxide Emissions Regulations

Title IV of CAAA90 requires that EPA establish NOxemission standards for certain coal-fired powerplants. NOx emissions from these power plants con-tribute to acid deposition in lakes and streams,concentrations of ground level ozone, and smog. Thegoal of the program is to reduce NOx emissions byapproximately 2 million tons from what they wouldhave been without the program.

As specified in CAAA90, the EPA has developed atwo-phase program, with the first set of standardstaking force in 1996 and the second set to be imple-mented in 2000 [7] (Table 2). Dry-bottom wall-firedand tangential-fired boilers, the most common boilertypes, referred to as Group 1 boilers, are required tomake significant reductions beginning in 1996 and

10 Energy Information Administration/ Annual Energy Outlook 1997

Legislation and Regulations

further reductions in 2000. Relative to their un-controlled emission rates, which range roughlybetween 0.6 and 1.0 pounds per million Btu, theyare required to make reductions of between 25 and50 percent to meet the Phase I limits.

The remaining boilers, Group 2 boilers, are not

Table 2. NOx emissions standards under theClean Air Act Amendments of 1990(pounds per million Btu)

Boiler typeNumber of

boilersPhase I

limitPhase II

limit

Group 1 boilersDry-bottom wall-fired 284 0.50 0.45Tangential-fired 296 0.45 0.38

Group 2 boilersCell burners 35 NA 0.68Cyclones 88 NA 0.94Wet-bottom wall-fired 38 NA 0.86Vertically fired 29 NA 0.80Fluidized-bed 5 NA 0.29

NA = not applicable.

required to make reductions until 2000. With theexception of fluidized-bed boilers, these boiler typesare not as amenable to control as Group 1 boilers,and as a result their standards are higher. However,the required reductions are still significant, rangingbetween 40 and 50 percent below their uncontrolledlevels.